FISHERIAN MODELS OF FINANCIAL CRISES IN MACROEONOMICS. Enrique G. Mendoza University of Pennsylvania & NBER

|

|

|

- Anabel Walsh

- 5 years ago

- Views:

Transcription

1 FISHERIAN MODELS OF FINANCIAL CRISES IN MACROEONOMICS Enrique G. Mendoza University of Pennsylvania & NBER

2 A writer s perspective debt happens as a result of actions occurring over time. Therefore, any debt involves a plot line: how you got into debt, what you did, said and thought while you were there, and then depending on whether the ending is to be happy or sad how you got out of debt, or else how you go further and further into it until you became overwhelmed by it, and sank from view. (Margaret Atwood, Debtor s Prism, WSJ, 09/20/2008)

3 Financial crises, Black swans and nonlinearities (R. Merton, Observations on the Science of Finance in the Practice of Finance, Muh Award Lecture, 03/05/2009) Things are not conceptually out of control, this is not some mystery black swan we don t understand and we need to rewrite all the paradigms because all the modeling is wrong. If people are acting using a linear model, what looks like a ten-sigma event can actually be a two-sigma event... Most of the models in credit, in trading desks, in macro models do quite well locally, the problem is when you stop being locally nonlinearities are really quite large, If you want to see what happened in AIG they wrote a whole lot of credit default swaps the assets underlying them went down not one shock, not two shocks, not three shocks, but over and over. Each time the same size shock is going to create something even larger

4 Layout of the lecture 1. Stylized facts: Sudden Stops in EMs, credit booms/busts 2. Limitations of the literature & lessons from debt-deflation theory 3. General features of debt deflation (DD) models 4. Simple example of amplification & asymmetry w. DD mechanism 5. Quantitative DSGE models a) New Mercantilism in emerging markets (surge in reserves) b) International asset trading & portfolio choice c) Business cycles w. endogenous Sudden Stops 6. Conclusions & policy implications a) Similarities with LTCM, 2008 global crisis, Euro crisis b) Creative policies: price guarantees, macro prudential policy c) Importance of financial development d) Contagion

5 1. STYLIZED FACTS

6 Sudden Stop facts 1. Large, abrupt reversals in capital flows 2. Preceded (followed) by expansions (contractions) in domestic production, absorption, asset prices, credit & leverage 3. Capital, labor account for small fraction of output drop, compared to imported inputs, capacity utilization, and TFP (Mendoza (06), Meza (08), Calvo et al. (06)) 4. Infrequent events nested within regular business cycles

7 Documenting the empirical evidence 1. Cross-country event analysis of Sudden Stops: a) Classification of systemic Sudden Stop events from Calvo et al. (06) b) Capital flows criterion: fall in capital flows exceeding 2sd s c) Spread criterion: spike in aggregate EMBI spread exceeding 2sd s d) 33 SS events in sample of emerging economies (not excluding mild output collapse cases) e) Event windows based on medians of HP detrended data Event analysis of credit booms in macro and micro data

8 Sudden Stops: Cross- Country Event Analysis

9 Current account reversals in SS events (Sudden Stop events from Calvo et al. (2006), , deviations from HP trends) 3.00% Current Account GDP ratio 2.00% 1.00% 0.00% 1.00% 2.00% 3.00% t 2 t 1 t t+1 t+2

10 U.S. Current account as a share of GDP (deviation from mean)

11 Output and Consumption in Sudden Stop events (Sudden Stop events from Calvo et al. (2006), , deviations from HP trends) Gross Domestic Product Private Consumption 6.00% 6.00% 4.00% 4.00% 2.00% 2.00% 0.00% 0.00% 2.00% 2.00% 4.00% 4.00% 6.00% t 2 t 1 t t+1 t % t 2 t 1 t t+1 t+2

12 Investment and Tobin s Q in Sudden Stop Events (Sudden Stop events from Calvo et al. (2006), , deviations from HP trends) Investment Tobin Q 20.00% % 10.00% % 0.00% % % 15.00% % t 2 t 1 t t+1 t t 2 t 1 t t+1 t+2

13 Leverage ratios in Sudden Stop events (listed corporations in Indonesia, Korea, Malaysia & Thailand) debt to market value of equity (right axis) debt to book value of equity (left axis) debt to sales (left axis) Note: Cross-country arithmetic average of median leverage ratios across all publicly listed corporations in each country. Data from Worldscope database.

14 Credit Boom Events in Macro & Micro Data (Mendoza & Terrones 2009, 2012)

15 Methodology: Thresholds Method Country i is in a credit boom if: Credit booms observed with 2.8% frequency (70 episodes in sample of 61 ICs and EMs), with strong macro/micro linkages

16 Credit booms: seven year event windows (Cross-country means and medians of cyclical component of credit) 35 Industrial Countries 35 Emerging Economies Median 0-5 Median Mean Mean

17 Credit boom episodes (relative to std. deviation of credit in each country) INDUSTRIAL COUNTRIES 3.50 BEL_1979 GRC_2007 USA_2007 JPN_1990 AUS_1973 AUS_1988 IRL_2007 BEL_1989 IRL_1979 ESP_2007 JPN_1972 AUT_1979 BEL_2007 CHE_2007 SWE_2007 NOR_1987 USA_1988 AUT_1972 DEU_2000 ITA_1992 GRC_1972 DEU_1972 ITA_1973 FRA_1990 NOR_2007 CHE_1989 DNK_1987 PRT_2000 GBR_1989 SWE_1989 NZL_1974 NLD_1979 FIN_1990 GBR_1973 PRT_1973 Median

18 Credit boom episodes (relative to std. deviation of credit in each country) EMERGING MARKET ECO NO MIES 1/ RUS_2007 PAK_1986 IND_1989 POL_2008 URY_1980 PER_1987 THA_1978 BRA_1989 CHL_1980 NGA_1982 EST_2007 TUR_1997 KOR_1998 TUR_1976 SVN_2007 ECU_1997 ROM_1998 HKG_1997 CRI_1979 PHL_1997 URY_2002 NGA_2008 IDN_1997 SGP_1983 EGY_1981 HKG_2010 COL_1998 PHL_1983 CIV_1977 THA_1997 ZAF_2007 VEN_2007 MYS_1997 ISR_1978 MEX_1994 Median 1/ Ongoing credit booms are shown in green.

19 CBs are synchronized around big events IND EMEs Global Financial Crisis 10 Sudden Stops 8 Petro-dollar Recycling and Debt Crises ERM and Nordic Crises 6 Bretton Woods Collapse 4 2 0

20 Macro credit cycles Seven-year event windows centered at CB peaks Clear credit cycle pattern 1. y, NTy, c, i, stock & housing prices, and REER rise above trend in build up phase, drop below trend in the downswing 2. Current account falls first and then rises. 3. Minor changes in inflation Higher correlations with credit during CBs ⅓-½ of CBs are associated with booms in y, NTy, c, i Industrial countries show smaller fluctuations but normalized fluctuations are similar

21 6 Output credit cycles (Cross-country means and medians of cyclical component of GDP) Industrial Countries Output (Y) 6 Emerging Economies Output (Y) Mean Mean 1 Median 0 0 Median

22 Credit cycles in NT output & REER (Cross-country means and medians of cyclical components) Industrial Countries Emerging Economies 8 6 Non-tradables Output (YN) 8 6 Non-tradables Output (YN) Mean Median Mean Median Real Exchange Rate (RER) 8 6 Real Exchange Rate (RER) Median 4 2 Mean Median Mean

23 Credit cycles in the current account (Cross-country means and medians of cyclical component of CAY)

24 Credit cycles in asset prices (Cross-country means and medians of cyclical component) Industrial Countries Emerging Markets Real stock prices Real stock prices Median Mean Median Mean Real house prices Real house prices 10 Mean 10 5 Median 5 Mean Median

25 Credit booms and potential triggers (frequency analysis) All countries Industrial countries Emerging countries Surge in Large TFP Large financial capital inflows gains sector changes

26 Credit booms and financial crises (frequency analysis) All countries Industial countries Emerging countries Banking Currency Sudden Crisis Crisis Stop

27 Micro credit cycles (firm-level medians averaged across countries)

28 EM corporations: Tradables v. Nontradables

29 Bank-level indicators

30 2. LIMITATIONS OF THE LITERATURE & LESSONS FROM DD THEORY

31 Limitations of the literature 1. Sudden Stops as exogenous surprises (large, unexpected shocks) Calvo (98), Gertler et al. (07), Christiano et al. (04), Caballero & Krishnamurty (01), Cook & Devereux (06), Agents do not take financial frictions, possibility of SSs into account 2. Financial frictions examined as perturbations to deterministic equilibria in which constraints always bind Cannot generate SSs nested within common cycles (amplification and asymmetry in response to standard shocks) Abstracting from nonlinear effects caused by occasionally binding constraints (Fisher s debt deflation channel) 3. Quantitative relevance of credit frictions Amplification effects may be too small (Kocherlakota (00)) Credit frictions could make output expand (Chari et al. (05)) Can credit frictions yield infrequent SSs nested within normal cycles?

32 Kocherlakota s critique

lead to output expansion because of wealth effect on labor supply Correct result of a grossly counterfactual theory! Endogenous credit constraints lead to output expansion because mg.")

33 Chari et al. s (05) controversy Subtle constraints with little empirical evidence: One of 72,700 Google hits on margin loans in Oct Exogenous credit constraints (akin to sudden rise in gov. purchases) lead to output expansion because of wealth effect on labor supply Correct result of a grossly counterfactual theory! Endogenous credit constraints lead to output expansion because mg. benefit of investment rises (extra capital relaxes constraints) Incorrect result (assumes extra investment absorbs less resources than those gained by enhanced borrowing ability)

34 Lessons from Debt-Deflation Theory 1. SS are endogenous response to typical shocks when leverage ratios are high ( liabilities / value of collateral assets or income ) High leverage is endogenous outcome preceded by booms Prec. saving rules out largest crashes, lowers long-run prob. of SS (negligible effects on long-run cyclical moments) 2. Collateral constraints cause larger recessions in SS events Collateral constraint deflates Tobin s Q causing investment collapse Reduced access to working capital causes immediate output drop Relative price deflation lowers factor demands 3. Large amplification and asymmetry Sudden Stops nested within regular cycles Standard SOE-DSGE results if credit constraints do not bind 4. Consistent with stylized facts (except size of asset price drop)

35 3. GENERAL FEATURES OF DEBT-DEFLATION MODELS

36 Common elements of the models Small open economy DSGE framework: Incomplete financial markets: non-state-contingent bonds Model-based stationary distribution of NFA (by using Uzawa-Epstein or Bewley-Aiyagari-Hugget preferences) Imperfect credit markets reflected in collateral constraints: Nonlinear feedback between Systemic credit externalities because of price effects on credit Wide class of credit constraints (Kiyotaki & Moore (97), Aiyagari & Gertler (99), Kocherlakota (00), liquidity constraints, etc.)

37 Recursive competitive equilibrium Collateral constraints can affect households, firms, gov. in the decentralized equilibrium (each max. own payoff) If decentralized eq. can be represented as quasi-social planer s problem (neglible pecuniary credit externality), we can represent the equilibrium as Alternatively, use methods to split individual from aggregate decisions & states, or solve with foc s, or use heterogeneous agents

38 Endogenous financing premia 1. Higher effective real interest rate ( ) 2. Higher excess asset returns, lower prices: - Direct effect: requires limited ability to leverage! - Indirect effect: 3. Higher marginal fin. cost of inputs paid with working capital

39 4. AMPLIFICATION & ASYMMETRY IN DEBT-DEFLATION MODELS: A SIMPLE DETERMINISTIC EXAMPLE

40 Liability dollarization example Perfect-foresight, two-sector DGE model: With perfect credit markets, or if constraint does not bind: perfectlysmooth case of Permanent Income Theory Wealth-neutral shocks to y 0T do not alter equilibrium When the constraint binds: amplification & asymmetry in c, p n, ca ca reversal produced by DD channel, not by assumption and more than a one-shot balance sheet effect (as in Calvo (98))

41 Equilibrium with nonbinding credit friction

42 Amplification with the Debt-Deflation mechanism

43 Calibration for quantitative application Functional forms: Parameter values:

44 Sudden Stop effects of the Debt-Deflation mechanism

45 Limitations of this experiment It only tells us that very bad things can happen if you were borrowing a lot and suddenly, unexpectedly credit stops It doesn t tell us: How knowing this may happen affects borrowers behavior before the credit crunch? What magnitudes of shocks can trigger the credit constraint? What is the probability of observing credit crises? Is this a useful approach to model Sudden Stops (i.e. can it explain the stylized facts?) but it does illustrate the potential for large amplification and asymmetry in macro responses to shocks!

46 5. QUANTITATIVE DSGE MODELS

47 Model 1: Assessment of the New Mercantilism (Durdu, Mendoza & Terrones, Precautionary Demand for Foreign Assets in Sudden Stop Economies, JDE) Is the surge in reserves in EMs self-insurance against SS events? Compared with higher volatility and financial globalization DD model with endogenous Sudden Stop risk via liability dollarization and imported intermediate goods Quantifying amount of optimal reserves as self insurance Endogenous mapping between savings and prob. of sudden stop Key findings: 1. Endogenous SSs in response to typical shocks at high leverage 2. Sudden Stop risk causes large increase in NFA 3. Self insurance reduces sharply long-run prob. of Sudden Stops 4. Slow adjustment with ca surpluses, undervalued rer s 5. Results robust to specification of preferences

48 Surge in reserves in Sudden Stop Countries (difference of averages for SS year to 2005 minus 1985 to SS year) Country Year of Sudden Stop Change in reserves Hong Kong Korea Malaysia Thailand Uruguay Indonesia Philippines Russia Turkey Peru Pakistan Argentina II Argentina I Chile Brazil Colombia Mexico Ecuador Median 7.66 Median Asian Countries 13.17

49 DSGE model Preferences Households budget constraint

50 Credit constraint w. liability dollarization Nontradables produced with imported inputs Shocks to tradables endowment and nontradables TFP

, 7.")

51 Endogenous Sudden Stops Business cycles lead to binding borrowing constraint Countercyclical current account Long-run business cycle moments unchanged Fisherian DD amplifies effects of shocks causing Sudden Stops: Extra incentive for precautionary savings Excessive SSs ruled out from stochastic steady state Long-run probabilities of Sudden Stops: 3.9% (BAH), 7.9% (UE)

52 Why two preferences? Subjective discounting affects self insurance incentives CRRA utility imposes Aiyagari s Natural Debt Limit Since u (.) as c 0, BAH setup: Equilibrium requires r BAH > r otherwise b E[b] is inelastic at f for low r, and infinitely elastic as r r BAH Skewed wealth distributions UE setup: RTP rises w. past consumption Well-defined equilibrium requires r UE g Symmetric wealth distributions

53 Elasticity of savings under BAH & UE preferences Mean foreign assets: BAH preferences Mean foreign assets: UE preferences

54 Recursive problem

55 Calibration

56 Stochastic process of exogenous shocks VAR of tradables endowment, nontradables TFP Tradables endowment = tradables GDP Nontradables TFP first proxied with nontradables GDP SMM for NT TFP to match nontradables variability, autocorrelation and correlation with tradables GDP Unconditional moments of the Markov chain: Moments in the data:

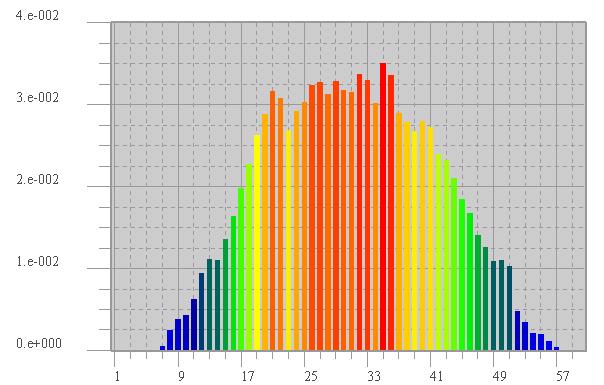

57 Long-run distribution of net foreign assets

58 Stochastic steady states UE Econ w/ perfect Econ w/ binding credit markets credit constraints BAH Econ w/ perfect Econ w/ binding credit markets credit constraints Foreign assets/output ratio Mean Coefficient of variation Correlation with GDP First Order Autocorrelation Coefficients of variation (in percent) Consumption of tradables Consumption of nontradables Consumption Price of nontradables Current Account-GDP ratio Tradables GDP GDP in units of tradables Nontradables GDP Intermediate input Correlation with GDP in units of tradables Consumption of tradables Price of nontradables Current Account-GDP ratio Nontradables GDP

59 Impact amplification effects in Sudden Stop region (excess responses to 1 s.d. shocks) BAH long run prob. border UE long run prob. border long-run Sudden Stop region Foreign assets as a percent of long-run GDP Price of Nontradables: UE setup Price of Nontradables: BAH setup Current account-gdp ratio: UE setup Current account-gdp ratio: BAH setup

60 Sudden Stop dynamics at a 49% debt ratio (excess responses to 1 s.d. shocks) Current Account-Output Ratio 4 2 Price of Nontradables CES Consumption Bewley-Aiyagari-Hugget Preferences Total Output in Units of Tradables Uzawa-Epstein Preferences

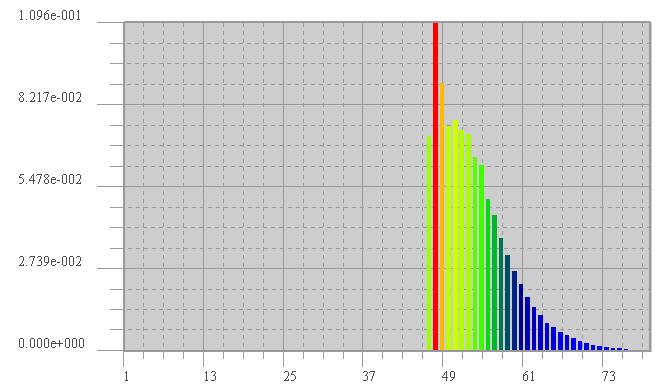

61 Transitional distributions in Sudden Stop economies (foreign assets in percent of mean GDP) 1.00 UE setup 1.00 BAH setup years 5 years 10 years 15 years Long-run distribution

62 The magic of precautionary savings Mean foreign assets and probability of a Sudden Stop at a -48.7% debt ratio BAH setup UE setup Prob. of Mean Prob. of Mean Sudden Stop foreign assets Sudden Stop foreign assets Economy with credit constraints year % -48.7% 100.0% -48.7% year % -48.2% 21.0% -48.2% year % -41.7% 3.4% -42.9% long run 0.9% -24.3% 1.1% -37.8% Frictionless economy long run 0.0% -44.7% 0.0% -42.4% Change in mean foreign assets 20.4% 4.6%

63 Model 2: Global asset trading (Mendoza & Smith, JIE 2006) Two-agent equilibrium asset pricing model Margin constraint: Endogenous supply-side but independent of financial frictions GHH utility u(c-g(l)): MRS(c,L) independent of c Competitive firms, no capital accumulation: e ta F(L t,k) Foreign securities firms with trading costs: Foreign traders demand: SS are endogenous response to 1sd. TFP shocks: Requires high enough leverage liquid asset market ca, c close to actual SS, large fall in q needs high elasticity (1/a ) Long-run prob. of binding margin constraint = 2.5% (with 1/a = 0.5) Trading costs in percent of returns in line with empirical evidence

64 Households and foreign traders Households preferences and budget constraint (need also short selling constraint on equity): Value of foreign traders firms per unit of capital:

65 Long-run distributions of equity & bonds

66 Sudden Stop effects at high and low leverage ratios (differences in forecast functions in response to 1sd, negative TFP shock) High leverage state: α=0.806, b=-1.481, b/qα=-10.9% Low leverage state: α=0.806, b=-1.01, b/qα=-7.4%

67 Sudden Stop effects: low foreign demand elasticity (½) Figure 2. Sudden Stop Dynamics in Mendoza-Smith Model with Foreign Demand Elasticity of 1/2 (percent deviations relative to economy with perfect credit markets) consumption current account-gdp ratio equity price Note: Forecast functions conditional on a negative, one-standard-deviation productivity shock and a leverage ratio of 12.2% at date 1 (see Mendoza and Smith (2005) for details).

68 Model 3: Sudden Stops, Financial Crises (Mendoza, AER 10) Equilibrium business cycle model with: Endogenous collateral constraint on debt and working capital Imported intermediate goods Shocks to [R, p v, TFP] taken from data Representative firm-household problem: subject to

69 Main findings Long-run business cycle moments unaffected by credit constraints Sudden Stops nested with normal cycle Prec. savings reduces prob. of SS events ( calibrated to match actual frequency of SS events) Constraints bind in high leverage states, reached with positive prob., and in these states typical shocks cause Sudden Stops Model matches output, consumption, investment and net exports Expansions precede SS events, slow recovery in the aftermath Collapse is asset prices is smaller than in data Large amplification & asymmetry Larger than Kocherlakota s (00) due to strong debt-deflation feedback WK crucial for initial drops in output & factor demands Along with imported inputs generates downward bias in Solow residual Exogenous credit constraint yields smaller effects

70 Calibration

71 Stochastic steady states net foreign assets capital

72 Universe of consumption impact effects (percent deviations from mean in response to 1sd shocks to TFP, R and p v ) Perfect credit markets Economy with collateral constraint

73 Amplification & Asymmetry Features of SS events (mean excess responses relative to frictionless economy in percent of frictionless averages)

74 Sudden Stop events in the data and in the model

75

76 6. CONCLUSIONS & POLICY LESSONS

77 Conclusions & policy lessons Endogenous Sudden Stops nested with normal cycles & caused by normal shocks in highly-leveraged economies Similar features in LTCM, 2008 global financial crisis, Euro crisis Constraints cause output collapse, large amplification & asymmetry Amplification driven by Fisher s debt deflation Eliminating Sudden Stops requires addressing contractual frictions (i.e. financial development) Ad-hoc capital requirements poor safeguard against aggregate risk but policy can be considered taking those frictions as given: Neo-Mercantilism: war chest of reserves to fight Sudden Stops Stabilize asset prices/liquidity to maintain market access (Calvo (02), Lerrick & Meltzer (02), bankruptcy court, indexed bonds) but with moral hazard tradeoffs (Durdu & Mendoza JIE (06)) Macro-prudential policies (Korinek (09), Bianchi (10), Mendoza & Bianchi (10)) but require precise knowledge of credit dynamics Contagion: shocks can trigger SSs in waves despite fundamentals (Mendoza & Quadrini JME (10))

University of Pennsylvania & NBER. This paper reflects only the authors views, and not those of the IMF

An Anatomy of Credit Booms and their Demise Enrique G. Mendoza University of Pennsylvania & NBER Marco E. Terrones IMF This paper reflects only the authors views, and not those of the IMF Motivation and

An Anatomy of Credit Booms and their Demise Enrique G. Mendoza University of Pennsylvania & NBER Marco E. Terrones IMF This paper reflects only the authors views, and not those of the IMF Motivation and

Precautionary Demand for Foreign Assets in Sudden Stop Economies: An Assessment of the New Mercantilism

Precautionary Demand for Foreign Assets in Sudden Stop Economies: An Assessment of the New Mercantilism Ceyhun Bora Durdu Enrique G. Mendoza Marco E. Terrones Board of Governors of the University of Maryland

Precautionary Demand for Foreign Assets in Sudden Stop Economies: An Assessment of the New Mercantilism Ceyhun Bora Durdu Enrique G. Mendoza Marco E. Terrones Board of Governors of the University of Maryland

2. Preceded (followed) by expansions (contractions) in domestic. 3. Capital, labor account for small fraction of output drop,

by expansions (contractions) in domestic. 3. Capital, labor account for small fraction of output drop,") Mendoza (AER) Sudden Stop facts 1. Large, abrupt reversals in capital flows 2. Preceded (followed) by expansions (contractions) in domestic production, absorption, asset prices, credit & leverage 3. Capital,

Mendoza (AER) Sudden Stop facts 1. Large, abrupt reversals in capital flows 2. Preceded (followed) by expansions (contractions) in domestic production, absorption, asset prices, credit & leverage 3. Capital,

Overborrowing, Financial Crises and Macro-prudential Policy

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin Enrique G. Mendoza University of Maryland & NBER The case for macro-prudential policies Credit booms are

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin Enrique G. Mendoza University of Maryland & NBER The case for macro-prudential policies Credit booms are

Global Liquidity, House Prices, and the Macroeconomy: Evidence from Advanced and Emerging Economies

Global Liquidity, House Prices, and the Macroeconomy: Evidence from Advanced and Emerging Economies By Ambrogio Cesa-Bianchi, Luis Felipe Cespedes, Alessandro Rebucci Bank of Canada and European Central

Global Liquidity, House Prices, and the Macroeconomy: Evidence from Advanced and Emerging Economies By Ambrogio Cesa-Bianchi, Luis Felipe Cespedes, Alessandro Rebucci Bank of Canada and European Central

2016 External Sector Report

216 External Sector Report Global Imbalances and Policy Challenges September, 216 o Evolution of Global Current Accounts and Exchange Rates Widening and reconfiguration of imbalances in 215 Drivers: Asymmetric

216 External Sector Report Global Imbalances and Policy Challenges September, 216 o Evolution of Global Current Accounts and Exchange Rates Widening and reconfiguration of imbalances in 215 Drivers: Asymmetric

Overview of Presentation

Overview of Presentation Fiscal Outlook and Challenges How to Address Fiscal Challenges? 2 Fiscal Outlook and Challenges 3 While the fiscal drag is waning in AE, EMEs would need to start rebuilding buffers

Overview of Presentation Fiscal Outlook and Challenges How to Address Fiscal Challenges? 2 Fiscal Outlook and Challenges 3 While the fiscal drag is waning in AE, EMEs would need to start rebuilding buffers

Overborrowing, Financial Crises and Macro-prudential Policy. Macro Financial Modelling Meeting, Chicago May 2-3, 2013

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin & NBER Enrique G. Mendoza Universtiy of Pennsylvania & NBER Macro Financial Modelling Meeting, Chicago

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin & NBER Enrique G. Mendoza Universtiy of Pennsylvania & NBER Macro Financial Modelling Meeting, Chicago

Fiscal Policy and Macro-systemic Risks

Fiscal Policy and Macro-systemic Risks Vitor Gaspar Director, Fiscal Affairs Department International Monetary Fund Integrated Macro-Financial Modeling for Robust Policy Design MACFINROBODS Paris, June

Fiscal Policy and Macro-systemic Risks Vitor Gaspar Director, Fiscal Affairs Department International Monetary Fund Integrated Macro-Financial Modeling for Robust Policy Design MACFINROBODS Paris, June

The Challenge of Public Pension Reform in Advanced and Emerging Economies

The Challenge of Public Pension Reform in Advanced and Emerging Economies Mauricio Soto Fiscal Affairs Department International Monetary Fund January 212 The views expressed herein are those of the author

The Challenge of Public Pension Reform in Advanced and Emerging Economies Mauricio Soto Fiscal Affairs Department International Monetary Fund January 212 The views expressed herein are those of the author

Credit Supply, Household Debt, and Business Cycles

Credit Supply, Household Debt, and Business Cycles Amir Sufi University of Chicago Booth School of Business; NBER; co-director of IGM February 2017 Big Picture Questions What is the source of macroeconomic

Credit Supply, Household Debt, and Business Cycles Amir Sufi University of Chicago Booth School of Business; NBER; co-director of IGM February 2017 Big Picture Questions What is the source of macroeconomic

OECD Science, Technology and Industry Scoreboard 2013

OECD Science, Technology and Industry Scoreboard 213 CANADA HIGHLIGHTS Canada experienced a decline in business spending on R&D between 21 and 211, despite generous public support, mainly through tax incentives

OECD Science, Technology and Industry Scoreboard 213 CANADA HIGHLIGHTS Canada experienced a decline in business spending on R&D between 21 and 211, despite generous public support, mainly through tax incentives

The Global Economic Outlook: Stronger growth ahead, but more risks Paris, 19th November h00 Paris time

The Global Economic Outlook: Stronger growth ahead, but more risks Paris, 19th November 2013 11h00 Paris time Pier Carlo Padoan Deputy Secretary-General and Chief Economist OECD Economic Outlook: key messages

The Global Economic Outlook: Stronger growth ahead, but more risks Paris, 19th November 2013 11h00 Paris time Pier Carlo Padoan Deputy Secretary-General and Chief Economist OECD Economic Outlook: key messages

SERVICES TRADE, REGULATION AND GVCS

UNITED NATIONS CONFERENCE ON TRADE AND DEVELOPMENT MULTI-YEAR EXPERT MEETING ON TRADE, SERVICES AND DEVELOPMENT Geneva, 11 13 May 2015 SERVICES TRADE, REGULATION AND GVCS SESSION 2 Ms. Dorothée Rouzet

UNITED NATIONS CONFERENCE ON TRADE AND DEVELOPMENT MULTI-YEAR EXPERT MEETING ON TRADE, SERVICES AND DEVELOPMENT Geneva, 11 13 May 2015 SERVICES TRADE, REGULATION AND GVCS SESSION 2 Ms. Dorothée Rouzet

The Challenge of Public Pension Reform

The Challenge of Public Pension Reform Baoping Shang Fiscal Affairs Department International Monetary Fund May 4, 212 This presentation represents the views of the author and should not be attributed to

The Challenge of Public Pension Reform Baoping Shang Fiscal Affairs Department International Monetary Fund May 4, 212 This presentation represents the views of the author and should not be attributed to

Fiscal Policy and Economic Growth

Fiscal Policy and Economic Growth Vitor Gaspar Director, Fiscal Affairs Department International Monetary Fund Peterson Institute for International Economics June 3, 15 Background The study draws on an

Fiscal Policy and Economic Growth Vitor Gaspar Director, Fiscal Affairs Department International Monetary Fund Peterson Institute for International Economics June 3, 15 Background The study draws on an

Economic Growth: Lecture 1 (first half), Stylized Facts of Economic Growth and Development

, Stylized Facts of Economic Growth and Development") 14.452 Economic Growth: Lecture 1 (first half), Stylized Facts of Economic Growth and Development Daron Acemoglu MIT October 24, 2012. Daron Acemoglu (MIT) Economic Growth Lecture 1 October 24, 2012. 1

14.452 Economic Growth: Lecture 1 (first half), Stylized Facts of Economic Growth and Development Daron Acemoglu MIT October 24, 2012. Daron Acemoglu (MIT) Economic Growth Lecture 1 October 24, 2012. 1

Deflation, Credit Collapse and Great Depressions. Enrique G. Mendoza

Deflation, Credit Collapse and Great Depressions Enrique G. Mendoza Main points In economies where agents are highly leveraged, deflation amplifies the real effects of credit crunches Credit frictions

Deflation, Credit Collapse and Great Depressions Enrique G. Mendoza Main points In economies where agents are highly leveraged, deflation amplifies the real effects of credit crunches Credit frictions

Corporate Standards and Disclosure Around the World: What works?

Corporate Standards and Disclosure Around the World: What works? Professor Florencio Lopez-de-Silanes Yale University International Institute for Corporate Governance September 20, 2002. Why do some countries

Corporate Standards and Disclosure Around the World: What works? Professor Florencio Lopez-de-Silanes Yale University International Institute for Corporate Governance September 20, 2002. Why do some countries

Devaluation Risk and the Business Cycle Implications of Exchange Rate Management

Devaluation Risk and the Business Cycle Implications of Exchange Rate Management Enrique G. Mendoza University of Pennsylvania & NBER Based on JME, vol. 53, 2000, joint with Martin Uribe from Columbia

Devaluation Risk and the Business Cycle Implications of Exchange Rate Management Enrique G. Mendoza University of Pennsylvania & NBER Based on JME, vol. 53, 2000, joint with Martin Uribe from Columbia

Introduction: Basic Facts and Neoclassical Growth Model

Introduction: Basic Facts and Neoclassical Growth Model Diego Restuccia University of Toronto and NBER University of Oslo August 14-18, 2017 Restuccia Macro Growth and Development University of Oslo 1

Introduction: Basic Facts and Neoclassical Growth Model Diego Restuccia University of Toronto and NBER University of Oslo August 14-18, 2017 Restuccia Macro Growth and Development University of Oslo 1

Understanding the Downward Trend in Labor Income Shares

Understanding the Downward Trend in Labor Income Shares Mai Dao, Mitali Das (team lead), Zsoka Koczan and Weicheng Lian, 1 with contributions from Jihad Dagher and support from Ben Hilgenstock and Hao

Understanding the Downward Trend in Labor Income Shares Mai Dao, Mitali Das (team lead), Zsoka Koczan and Weicheng Lian, 1 with contributions from Jihad Dagher and support from Ben Hilgenstock and Hao

ECON 385. Intermediate Macroeconomic Theory II. Solow Model With Technological Progress and Data. Instructor: Dmytro Hryshko

ECON 385. Intermediate Macroeconomic Theory II. Solow Model With Technological Progress and Data Instructor: Dmytro Hryshko 1 / 35 Examples of technological progress 1970: 50,000 computers in the world;

ECON 385. Intermediate Macroeconomic Theory II. Solow Model With Technological Progress and Data Instructor: Dmytro Hryshko 1 / 35 Examples of technological progress 1970: 50,000 computers in the world;

The Perils of Financial Globalization without Financial Development (International Macroeconomics with Heterogeneous Agents and Incomplete Markets)

") The Perils of Financial Globalization without Financial Development (International Macroeconomics with Heterogeneous Agents and Incomplete Markets) Enrique G. Mendoza University of Pennsylvania & NBER

The Perils of Financial Globalization without Financial Development (International Macroeconomics with Heterogeneous Agents and Incomplete Markets) Enrique G. Mendoza University of Pennsylvania & NBER

Chapter 6. Macroeconomic Data. Zekarias M. Hussein and Angel H. Aguiar Uses of Macroeconomic Data

Chapter 6 Macroeconomic Data Zekarias M. Hussein and Angel H. Aguiar This chapter provides an overview of the macroeconomic features of the 8 Data Base. We will first present how the macroeconomic data

Chapter 6 Macroeconomic Data Zekarias M. Hussein and Angel H. Aguiar This chapter provides an overview of the macroeconomic features of the 8 Data Base. We will first present how the macroeconomic data

Chapter 6 Macroeconomic Data

Chapter 6 Macroeconomic Data Angel H. Aguiar and Betina V. Dimaranan 6.1 Uses of Macroeconomic Data During the Data Base construction process, macroeconomic data are used in various stages. The primary

Chapter 6 Macroeconomic Data Angel H. Aguiar and Betina V. Dimaranan 6.1 Uses of Macroeconomic Data During the Data Base construction process, macroeconomic data are used in various stages. The primary

Online Appendix for Explaining Educational Attainment across Countries and over Time

Online Appendix for Explaining Educational Attainment across Countries and over Time Diego Restuccia University of Toronto Guillaume Vandenbroucke University of Southern California March 2014 Contents

Online Appendix for Explaining Educational Attainment across Countries and over Time Diego Restuccia University of Toronto Guillaume Vandenbroucke University of Southern California March 2014 Contents

THE PAST, PRESENT, AND FUTURE

THE PAST, PRESENT, AND FUTURE OF ECONOMIC CONVERGENCE Dani Rodrik October 2013 Global income disparities $35,000 $30,000 Per capita income levels in different country groups (2012, in 2005 PPP$) $31,625

THE PAST, PRESENT, AND FUTURE OF ECONOMIC CONVERGENCE Dani Rodrik October 2013 Global income disparities $35,000 $30,000 Per capita income levels in different country groups (2012, in 2005 PPP$) $31,625

1 Business-Cycle Facts Around the World 1

Contents Preface xvii 1 Business-Cycle Facts Around the World 1 1.1 Measuring Business Cycles 1 1.2 Business-Cycle Facts Around the World 4 1.3 Business Cycles in Poor, Emerging, and Rich Countries 7 1.4

Contents Preface xvii 1 Business-Cycle Facts Around the World 1 1.1 Measuring Business Cycles 1 1.2 Business-Cycle Facts Around the World 4 1.3 Business Cycles in Poor, Emerging, and Rich Countries 7 1.4

Household Debt and Business Cycles Worldwide

Household Debt and Business Cycles Worldwide Atif Mian, Amir Sufi, and Emil Verner Princeton University, University of Chicago, and Princeton University IMF Jacques Polak Annual Research Conference November

Household Debt and Business Cycles Worldwide Atif Mian, Amir Sufi, and Emil Verner Princeton University, University of Chicago, and Princeton University IMF Jacques Polak Annual Research Conference November

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Optimal Holdings of International Reserves: Self-Insurance Against Sudden Stops

Optimal Holdings of International Reserves: Self-Insurance Against Sudden Stops Guillermo Calvo, Alejandro Izquierdo and Rudy Loo-Kung October 30, 2012 XXX Research Meeting Central Reserve Bank of Peru

Optimal Holdings of International Reserves: Self-Insurance Against Sudden Stops Guillermo Calvo, Alejandro Izquierdo and Rudy Loo-Kung October 30, 2012 XXX Research Meeting Central Reserve Bank of Peru

Comments by: Sebnem Kalemli-Ozcan Associate Professor of Economics University of Houston and NBER. August 2007

Capital Flows and Asset Prices by Kosuke Aoki, Gianluca Benigno, and Nobuhiro Kiyotaki Comments by: Sebnem Kalemli-Ozcan Associate Professor of Economics University of Houston and NBER August 2007 This

Capital Flows and Asset Prices by Kosuke Aoki, Gianluca Benigno, and Nobuhiro Kiyotaki Comments by: Sebnem Kalemli-Ozcan Associate Professor of Economics University of Houston and NBER August 2007 This

Fiscal Policy and Income Inequality. March 13, 2014

Fiscal Policy and Income Inequality March 13, 2014 Inequality has been increasing in most economies 0.55 Disposable Income Inequality: 1980 2010 0.5 0.45 Gini coefficient 0.4 0.35 0.3 0.25 0.2 1980 1985

Fiscal Policy and Income Inequality March 13, 2014 Inequality has been increasing in most economies 0.55 Disposable Income Inequality: 1980 2010 0.5 0.45 Gini coefficient 0.4 0.35 0.3 0.25 0.2 1980 1985

Financial Integration, Financial Deepness and Global Imbalances

Financial Integration, Financial Deepness and Global Imbalances Enrique G. Mendoza University of Maryland, IMF & NBER Vincenzo Quadrini University of Southern California, CEPR & NBER José-Víctor Ríos-Rull

Financial Integration, Financial Deepness and Global Imbalances Enrique G. Mendoza University of Maryland, IMF & NBER Vincenzo Quadrini University of Southern California, CEPR & NBER José-Víctor Ríos-Rull

Emerging & Frontier Market Outlook

Emerging & Frontier Market Outlook Recovery, Rebalancing and Risk in an Uneven Global Environment DAVID STAPLES, MANAGING DIRECTOR, EMEA CORPORATE FINANCE MATT ROBINSON, ASSOCIATE MANAGING DIRECTOR, AFRICA

Emerging & Frontier Market Outlook Recovery, Rebalancing and Risk in an Uneven Global Environment DAVID STAPLES, MANAGING DIRECTOR, EMEA CORPORATE FINANCE MATT ROBINSON, ASSOCIATE MANAGING DIRECTOR, AFRICA

A note on tax base, public debt, and investors beliefs. May Abstract

A note on tax base, public debt, and investors beliefs May 2011 Abstract This paper provides a new evidence and theoretical support for the role of market expectation in the public debt markets. Dispersion

A note on tax base, public debt, and investors beliefs May 2011 Abstract This paper provides a new evidence and theoretical support for the role of market expectation in the public debt markets. Dispersion

Determinantes de los flujos de capitales. a las economías emergentes

Determinantes de los flujos de capitales a las economías emergentes XCV Reunión de Gobernadores de Bancos Centrales del CEMLA Jose Juan Ruiz Aide memoir CEMLA Seminar Based on Capital Flows in South America.

Determinantes de los flujos de capitales a las economías emergentes XCV Reunión de Gobernadores de Bancos Centrales del CEMLA Jose Juan Ruiz Aide memoir CEMLA Seminar Based on Capital Flows in South America.

From Here to Eternity: The Outlook for Fiscal Adjustment in Advanced Economies. Carlo Cottarelli Director, Fiscal Affairs Department

From Here to Eternity: The Outlook for Fiscal Adjustment in Advanced Economies Carlo Cottarelli Director, Fiscal Affairs Department Peterson Institute May 2, 213 1 Main Questions How bad is the fiscal

From Here to Eternity: The Outlook for Fiscal Adjustment in Advanced Economies Carlo Cottarelli Director, Fiscal Affairs Department Peterson Institute May 2, 213 1 Main Questions How bad is the fiscal

The Public Debt Crisis of the United States

The Public Debt Crisis of the United States Enrique G. Mendoza University of Pennsylvania, NBER & PIER Seminario sobre Sostenibilidad de la Deuda Pública: AIReF September 5, 2017 Madrid, Spain What debt

The Public Debt Crisis of the United States Enrique G. Mendoza University of Pennsylvania, NBER & PIER Seminario sobre Sostenibilidad de la Deuda Pública: AIReF September 5, 2017 Madrid, Spain What debt

The Term Structure of Growth-at-Risk

The Term Structure of Growth-at-Risk Tobias Adrian (IMF), Federico Grinberg (IMF), Nellie Liang (Brookings), and Sherheryar Malik (IMF) BIS Research meeting on Pushing the Frontier of Central Bank s Macro

The Term Structure of Growth-at-Risk Tobias Adrian (IMF), Federico Grinberg (IMF), Nellie Liang (Brookings), and Sherheryar Malik (IMF) BIS Research meeting on Pushing the Frontier of Central Bank s Macro

Managing Public Wealth

Managing Public Wealth Jason Harris IMF Fiscal Monitor October 218 November 218 Managing Public Wealth Overview I. The Public Sector Balance Sheet II. Why Does it Matter? III. Policy Implications Risk

Managing Public Wealth Jason Harris IMF Fiscal Monitor October 218 November 218 Managing Public Wealth Overview I. The Public Sector Balance Sheet II. Why Does it Matter? III. Policy Implications Risk

A Virtuous Cycle in Local Currency Bond Markets?

A Virtuous Cycle in Local Currency Bond Markets? John D. Burger The Sellinger School, Loyola College in Maryland Katholieke Universiteit Leuven Francis E. Warnock Darden Business School, NBER, IIIS at

A Virtuous Cycle in Local Currency Bond Markets? John D. Burger The Sellinger School, Loyola College in Maryland Katholieke Universiteit Leuven Francis E. Warnock Darden Business School, NBER, IIIS at

Financial Crises and Asset Prices. Tyler Muir June 2017, MFM

Financial Crises and Asset Prices Tyler Muir June 2017, MFM Outline Financial crises, intermediation: What can we learn about asset pricing? Muir 2017, QJE Adrian Etula Muir 2014, JF Haddad Muir 2017 What

Financial Crises and Asset Prices Tyler Muir June 2017, MFM Outline Financial crises, intermediation: What can we learn about asset pricing? Muir 2017, QJE Adrian Etula Muir 2014, JF Haddad Muir 2017 What

ORIGINAL SIN AND DARK MATTER (STILL) MATTER: ASSET COMPOSITION AND SOLVENCY. Ricardo Hausmann Harvard University & Santa Fe Institute

MATTER: ASSET COMPOSITION AND SOLVENCY. Ricardo Hausmann Harvard University & Santa Fe Institute") ORIGINAL SIN AND DARK MATTER (STILL) MATTER: ASSET COMPOSITION AND SOLVENCY Ricardo Hausmann Harvard University & Santa Fe Institute Why do we care about deficits? Because deficits determine the evolution

ORIGINAL SIN AND DARK MATTER (STILL) MATTER: ASSET COMPOSITION AND SOLVENCY Ricardo Hausmann Harvard University & Santa Fe Institute Why do we care about deficits? Because deficits determine the evolution

OECD ECONOMIC SURVEY OF BRAZIL 2018

OECD ECONOMIC SURVEY OF BRAZIL 2018 Towards a more prosperous and inclusive Brazil Brasília, 28 February 2018 http://www.oecd.org/eco/surveys/economic-survey-brazil.htm @OECDeconomy @OECD The economy is

OECD ECONOMIC SURVEY OF BRAZIL 2018 Towards a more prosperous and inclusive Brazil Brasília, 28 February 2018 http://www.oecd.org/eco/surveys/economic-survey-brazil.htm @OECDeconomy @OECD The economy is

Productivity and income differences in the 20 th century

Productivity and income differences in the 20 th century Robert Inklaar and Daniel Gallardo Albarrán (University of Groningen) World KLEMS Conference, June 4 5 2018 Development accounting What can account

Productivity and income differences in the 20 th century Robert Inklaar and Daniel Gallardo Albarrán (University of Groningen) World KLEMS Conference, June 4 5 2018 Development accounting What can account

Sudden Stops and Output Drops

Federal Reserve Bank of Minneapolis Research Department Staff Report 353 January 2005 Sudden Stops and Output Drops V. V. Chari University of Minnesota and Federal Reserve Bank of Minneapolis Patrick J.

Federal Reserve Bank of Minneapolis Research Department Staff Report 353 January 2005 Sudden Stops and Output Drops V. V. Chari University of Minnesota and Federal Reserve Bank of Minneapolis Patrick J.

Precautionary Demand for Foreign Assets in Sudden Stop Economies: An Assessment of the New Merchantilism

WP/07/146 Precautionary Demand for Foreign Assets in Sudden Stop Economies: An Assessment of the New Merchantilism Ceyhun Bora Durda, Enrique G. Mendoza, and Marco E. Terrones 2007 International Monetary

WP/07/146 Precautionary Demand for Foreign Assets in Sudden Stop Economies: An Assessment of the New Merchantilism Ceyhun Bora Durda, Enrique G. Mendoza, and Marco E. Terrones 2007 International Monetary

Upgrading business investment

218 OECD ECONOMIC SURVEY OF TURKEY Upgrading business investment Paris, 13 July 218 http://www.oecd.org/eco/surveys/economic-survey-turkey.htm @OECDeconomy @OECD Growth remains strong despite headwinds

218 OECD ECONOMIC SURVEY OF TURKEY Upgrading business investment Paris, 13 July 218 http://www.oecd.org/eco/surveys/economic-survey-turkey.htm @OECDeconomy @OECD Growth remains strong despite headwinds

Efficient Bailouts? Javier Bianchi. Wisconsin & NYU

Efficient Bailouts? Javier Bianchi Wisconsin & NYU Motivation Large interventions in credit markets during financial crises Fierce debate about desirability of bailouts Supporters: salvation from a deeper

Efficient Bailouts? Javier Bianchi Wisconsin & NYU Motivation Large interventions in credit markets during financial crises Fierce debate about desirability of bailouts Supporters: salvation from a deeper

WORLD ECONOMIC OUTLOOK October 2017

WORLD ECONOMIC OUTLOOK October 2017 Andreas Bauer Sr Resident Representative @imf_delhi World Economic Outlook The big picture Global activity picked up further in 2017H1 the outlook is now for higher

WORLD ECONOMIC OUTLOOK October 2017 Andreas Bauer Sr Resident Representative @imf_delhi World Economic Outlook The big picture Global activity picked up further in 2017H1 the outlook is now for higher

Quantitative Implications of Indexed Bonds in Small Open Economies

Quantitative Implications of Indexed Bonds in Small Open Economies Ceyhun Bora Durdu Congressional Budget Office May 2007 Abstract Some studies have proposed setting up a benchmark market for indexed bonds

Quantitative Implications of Indexed Bonds in Small Open Economies Ceyhun Bora Durdu Congressional Budget Office May 2007 Abstract Some studies have proposed setting up a benchmark market for indexed bonds

Global Liquidity, House Prices, and the Macroeconomy: Evidence from Advanced and Emerging Economies

Global Liquidity, House Prices, and the Macroeconomy: Evidence from Advanced and Emerging Economies Ambrogio Cesa-Bianchi 1 Luis F. Cespedes 2 Alessandro Rebucci 3 1 Bank of England & Centre for Macroeconomics

Global Liquidity, House Prices, and the Macroeconomy: Evidence from Advanced and Emerging Economies Ambrogio Cesa-Bianchi 1 Luis F. Cespedes 2 Alessandro Rebucci 3 1 Bank of England & Centre for Macroeconomics

Policy Forum: How to address Inequality and Poverty in South Africa 7 June 2011, Reserve Bank, Pretoria

Policy Forum: How to address Inequality and Poverty in South Africa 7 June 2011, Reserve Bank, Pretoria Growing Unequal? International trends in inequality and poverty Michael Förster OECD, Social Policy

Policy Forum: How to address Inequality and Poverty in South Africa 7 June 2011, Reserve Bank, Pretoria Growing Unequal? International trends in inequality and poverty Michael Förster OECD, Social Policy

Country Risk, Exchange Rates and Economic Fluctuations in Emerging Economies

Country Risk, Exchange Rates and Economic Fluctuations in Emerging Economies Luis Felipe Céspedes Roberto Chang Central Bank of Chile Rutgers University & NBER September 2009 Luis Felipe Céspedes Roberto

Country Risk, Exchange Rates and Economic Fluctuations in Emerging Economies Luis Felipe Céspedes Roberto Chang Central Bank of Chile Rutgers University & NBER September 2009 Luis Felipe Céspedes Roberto

Booms and Banking Crises

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

Booms and Banking Crises F. Boissay, F. Collard and F. Smets Macro Financial Modeling Conference Boston, 12 October 2013 MFM October 2013 Conference 1 / Disclaimer The views expressed in this presentation

The Risky Steady State and the Interest Rate Lower Bound

The Risky Steady State and the Interest Rate Lower Bound Timothy Hills Taisuke Nakata Sebastian Schmidt New York University Federal Reserve Board European Central Bank 1 September 2016 1 The views expressed

The Risky Steady State and the Interest Rate Lower Bound Timothy Hills Taisuke Nakata Sebastian Schmidt New York University Federal Reserve Board European Central Bank 1 September 2016 1 The views expressed

ROUNDTABLE COMMENTS ON MONETARY AND REGULATORY POLICY IN AN ERA OF GLOBAL MARKETS

ROUNDTABLE COMMENTS ON MONETARY AND REGULATORY POLICY IN AN ERA OF GLOBAL MARKETS Liliana Rojas-Suarez Institute for International Economics D uring the conference we have heard a lot of stress placed

ROUNDTABLE COMMENTS ON MONETARY AND REGULATORY POLICY IN AN ERA OF GLOBAL MARKETS Liliana Rojas-Suarez Institute for International Economics D uring the conference we have heard a lot of stress placed

Entrepreneurship at a Glance 2018 Highlights

Entrepreneurship at a Glance 218 Highlights OECD Entrepreneurship at a Glance Highlights 218 SDD 1 October 218 List of figures ENTREPRENEURSHIP AND BUSINESS STATISTICS DATABASES 218 UPDATE 2 1. New enterprise

Entrepreneurship at a Glance 218 Highlights OECD Entrepreneurship at a Glance Highlights 218 SDD 1 October 218 List of figures ENTREPRENEURSHIP AND BUSINESS STATISTICS DATABASES 218 UPDATE 2 1. New enterprise

Can employment be increased only at the cost of more inequality?

Can employment be increased only at the cost of more inequality? Engines for More and Better Jobs in Europe ZEW Conference, Mannheim April 2013 Torben M Andersen Aarhus University Policy questions How

Can employment be increased only at the cost of more inequality? Engines for More and Better Jobs in Europe ZEW Conference, Mannheim April 2013 Torben M Andersen Aarhus University Policy questions How

THE BENEFITS OF EXPANDING THE ROLE OF WOMEN AND YOUTH IN ECONOMIC ACTIVITIES

G7 International Forum for Empowering Women and Youth in the Agriculture and Food Systems THE BENEFITS OF EXPANDING THE ROLE OF WOMEN AND YOUTH IN ECONOMIC ACTIVITIES Randall S. Jones Head, Japan/Korea

G7 International Forum for Empowering Women and Youth in the Agriculture and Food Systems THE BENEFITS OF EXPANDING THE ROLE OF WOMEN AND YOUTH IN ECONOMIC ACTIVITIES Randall S. Jones Head, Japan/Korea

Commodity Price Beliefs, Financial Frictions and Business Cycles

Commodity Price Beliefs, Financial Frictions and Business Cycles Jesús Bejarano Franz Hamann Enrique G. Mendoza 1 Diego Rodríguez Preliminary Work Closing Conference - BIS CCA Research Network on The commodity

Commodity Price Beliefs, Financial Frictions and Business Cycles Jesús Bejarano Franz Hamann Enrique G. Mendoza 1 Diego Rodríguez Preliminary Work Closing Conference - BIS CCA Research Network on The commodity

THE SEVERITY OF AND POLICY RESPONSES TO SYSTEMIC CRISES. Lorenzo Giorgianni July, 2011

THE SEVERITY OF AND POLICY RESPONSES TO SYSTEMIC CRISES Lorenzo Giorgianni July, 211 OUTLINE Increasing linkages Anatomy of systemic crises Policy Responses to Past Systemic Crises Key Lessons Based on

THE SEVERITY OF AND POLICY RESPONSES TO SYSTEMIC CRISES Lorenzo Giorgianni July, 211 OUTLINE Increasing linkages Anatomy of systemic crises Policy Responses to Past Systemic Crises Key Lessons Based on

A Macroeconomic Framework for Quantifying Systemic Risk. June 2012

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy University of Chicago & NBER Northwestern University & NBER June 212 Systemic Risk Systemic risk: risk (probability)

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He Arvind Krishnamurthy University of Chicago & NBER Northwestern University & NBER June 212 Systemic Risk Systemic risk: risk (probability)

Is Full Employment Sustainable?

Is Full Employment Sustainable? Antonio Fatas INSEAD Very preliminary. This version: March 11, 2019 Introduction The US economy started its current expansion phase in June 2009. This means that, as of

Is Full Employment Sustainable? Antonio Fatas INSEAD Very preliminary. This version: March 11, 2019 Introduction The US economy started its current expansion phase in June 2009. This means that, as of

What is the economic outlook for OECD countries?

The outlook What is the economic outlook for OECD countries? Paul van den Noord Counselor to the Chief Economist The outlook Real GDP growth, in per cent.....9. -..9 Japan. -... Total OECD.... Brazil....

The outlook What is the economic outlook for OECD countries? Paul van den Noord Counselor to the Chief Economist The outlook Real GDP growth, in per cent.....9. -..9 Japan. -... Total OECD.... Brazil....

International Debt Deleveraging

International Debt Deleveraging Luca Fornaro London School of Economics ECB-Bank of Canada joint workshop on Exchange Rates Frankfurt, June 213 1 Motivating facts: Household debt/gdp Household debt/gdp

International Debt Deleveraging Luca Fornaro London School of Economics ECB-Bank of Canada joint workshop on Exchange Rates Frankfurt, June 213 1 Motivating facts: Household debt/gdp Household debt/gdp

Sudden Stops and Output Drops

NEW PERSPECTIVES ON REPUTATION AND DEBT Sudden Stops and Output Drops By V. V. CHARI, PATRICK J. KEHOE, AND ELLEN R. MCGRATTAN* Discussants: Andrew Atkeson, University of California; Olivier Jeanne, International

NEW PERSPECTIVES ON REPUTATION AND DEBT Sudden Stops and Output Drops By V. V. CHARI, PATRICK J. KEHOE, AND ELLEN R. MCGRATTAN* Discussants: Andrew Atkeson, University of California; Olivier Jeanne, International

OECD INTERIM ECONOMIC OUTLOOK. Will Soft Foundations and Financial Vulnerabilities Derail the Modest Recovery? Catherine L. Mann OECD Chief Economist

OECD INTERIM ECONOMIC OUTLOOK Will Soft Foundations and Financial Vulnerabilities Derail the Modest Recovery? Presentation to LUISS 10 April 2017 Catherine L. Mann OECD Chief Economist Key messages Global

OECD INTERIM ECONOMIC OUTLOOK Will Soft Foundations and Financial Vulnerabilities Derail the Modest Recovery? Presentation to LUISS 10 April 2017 Catherine L. Mann OECD Chief Economist Key messages Global

Optimal Time-Consistent Macroprudential Policy

Optimal Time-Consistent Macroprudential Policy Javier Bianchi Minneapolis Fed & NBER Enrique G. Mendoza Univ. of Pennsylvania, NBER & PIER Why study macroprudential policy? MPP has gained relevance as

Optimal Time-Consistent Macroprudential Policy Javier Bianchi Minneapolis Fed & NBER Enrique G. Mendoza Univ. of Pennsylvania, NBER & PIER Why study macroprudential policy? MPP has gained relevance as

Banks and Liquidity Crises in Emerging Market Economies

Banks and Liquidity Crises in Emerging Market Economies Tarishi Matsuoka Tokyo Metropolitan University May, 2015 Tarishi Matsuoka (TMU) Banking Crises in Emerging Market Economies May, 2015 1 / 47 Introduction

Banks and Liquidity Crises in Emerging Market Economies Tarishi Matsuoka Tokyo Metropolitan University May, 2015 Tarishi Matsuoka (TMU) Banking Crises in Emerging Market Economies May, 2015 1 / 47 Introduction

Taxing Firms Facing Financial Frictions

Taxing Firms Facing Financial Frictions Daniel Wills 1 Gustavo Camilo 2 1 Universidad de los Andes 2 Cornerstone November 11, 2017 NTA 2017 Conference Corporate income is often taxed at different sources

Taxing Firms Facing Financial Frictions Daniel Wills 1 Gustavo Camilo 2 1 Universidad de los Andes 2 Cornerstone November 11, 2017 NTA 2017 Conference Corporate income is often taxed at different sources

MINIMUM WAGES ACROSS OECD COUNTRIES: BACK TO THE FUTURE?

Paris, 20 October 2017 MINIMUM WAGES ACROSS OECD COUNTRIES: BACK TO THE FUTURE? Andrea Garnero Economist Employment, Labour and Social Affairs OECD A widespread (but heterogenous) wage setting institution

Paris, 20 October 2017 MINIMUM WAGES ACROSS OECD COUNTRIES: BACK TO THE FUTURE? Andrea Garnero Economist Employment, Labour and Social Affairs OECD A widespread (but heterogenous) wage setting institution

Sudden Stops in a Business Cycle Model with Credit Constraints: A Fisherian Deflation of Tobin s Q *

Draft: September 8, 2005 preliminary draft Sudden Stops in a Business Cycle Model with Credit Constraints: A Fisherian Deflation of Tobin s Q * By Enrique G. Mendoza University of Maryland, International

Draft: September 8, 2005 preliminary draft Sudden Stops in a Business Cycle Model with Credit Constraints: A Fisherian Deflation of Tobin s Q * By Enrique G. Mendoza University of Maryland, International

Quantitative Significance of Collateral Constraints as an Amplification Mechanism

RIETI Discussion Paper Series 09-E-05 Quantitative Significance of Collateral Constraints as an Amplification Mechanism INABA Masaru The Canon Institute for Global Studies KOBAYASHI Keiichiro RIETI The

RIETI Discussion Paper Series 09-E-05 Quantitative Significance of Collateral Constraints as an Amplification Mechanism INABA Masaru The Canon Institute for Global Studies KOBAYASHI Keiichiro RIETI The

CAN FDI CONTRIBUTE TO INCLUSIVE GROWTH: ROLE OF INVESTMENT FACILITATION

CAN FDI CONTRIBUTE TO INCLUSIVE GROWTH: ROLE OF INVESTMENT FACILITATION Iza Lejarraga Head of Unit, Investment Policy Linkages OECD Investment Division FIFD Workshop on Investment Facilitation for Development

CAN FDI CONTRIBUTE TO INCLUSIVE GROWTH: ROLE OF INVESTMENT FACILITATION Iza Lejarraga Head of Unit, Investment Policy Linkages OECD Investment Division FIFD Workshop on Investment Facilitation for Development

Exchange Rate Adjustment in Financial Crises

Exchange Rate Adjustment in Financial Crises Michael B. Devereux 1 Changhua Yu 2 1 University of British Columbia 2 Peking University Swiss National Bank June 2016 Motivation: Two-fold Crises in Emerging

Exchange Rate Adjustment in Financial Crises Michael B. Devereux 1 Changhua Yu 2 1 University of British Columbia 2 Peking University Swiss National Bank June 2016 Motivation: Two-fold Crises in Emerging

Financial Inclusion, Education & the Arab World

Financial Inclusion, Education & the Arab World Nadine Chehade nchehade@worldbank.org October 2016 Framing the discussions Why is financial inclusion important? Where does / will the Arab world stand?

Financial Inclusion, Education & the Arab World Nadine Chehade nchehade@worldbank.org October 2016 Framing the discussions Why is financial inclusion important? Where does / will the Arab world stand?

Corrigendum. Page 41, Table 1.A1.1. Details of pension reforms, September 2013-September 2015 : Columns on Portugal should read as follows:

Pensions at a Glance: OECD and G Indicators DOI: http://dx.doi.org/.787/pension_glance-5-en ISBN 9789644636 (print) ISBN 97896444443 (PDF) OECD 5 Corrigendum Page 4, Table.A.. Details of pension reforms,

Pensions at a Glance: OECD and G Indicators DOI: http://dx.doi.org/.787/pension_glance-5-en ISBN 9789644636 (print) ISBN 97896444443 (PDF) OECD 5 Corrigendum Page 4, Table.A.. Details of pension reforms,

Trade in Value Added. Fabienne Fortanier. International trade past, present, future Alpbach Economic Symposium

Trade in Value Added International trade past, present, future Alpbach Economic Symposium Fabienne Fortanier Head of Trade Statistics Statistics Directorate, OECD 1 Increasing international fragmentation

Trade in Value Added International trade past, present, future Alpbach Economic Symposium Fabienne Fortanier Head of Trade Statistics Statistics Directorate, OECD 1 Increasing international fragmentation

Nero Meeting: Alain de Serres OECD Economics Department. 21 June 2013

Nero Meeting: The structural reform agenda to boost longterm growth and its side-effects on nearterm activity and other objectives Alain de Serres OECD Economics Department 21 June 2013 Benchmarking exercise

Nero Meeting: The structural reform agenda to boost longterm growth and its side-effects on nearterm activity and other objectives Alain de Serres OECD Economics Department 21 June 2013 Benchmarking exercise

Are Indexed Bonds a Remedy for Sudden Stops?

Are Indexed Bonds a Remedy for Sudden Stops? Ceyhun Bora Durdu University of Maryland December 2005 Abstract Recent policy proposals call for setting up a benchmark indexed bond market to prevent Sudden

Are Indexed Bonds a Remedy for Sudden Stops? Ceyhun Bora Durdu University of Maryland December 2005 Abstract Recent policy proposals call for setting up a benchmark indexed bond market to prevent Sudden

G20 Finance and Central Bank Deputies Meeting February February, Structural Reform in a Crisis Environment.

G20 Finance and Central Bank Deputies Meeting February 24-25 February, 2012 Structural Reform in a Crisis Environment Note by the OECD Structural reform is an essential ingredient to achieve sustainable

G20 Finance and Central Bank Deputies Meeting February 24-25 February, 2012 Structural Reform in a Crisis Environment Note by the OECD Structural reform is an essential ingredient to achieve sustainable

How to deal with potential secular stagnation

How to deal with potential secular stagnation Catherine L. Mann OECD Chief Economist Banque de France Paris 16 January 2017 www.oecd.org/economy/economicoutlook.htm ECOSCOPE blog: oecdecoscope.wordpress.com/

How to deal with potential secular stagnation Catherine L. Mann OECD Chief Economist Banque de France Paris 16 January 2017 www.oecd.org/economy/economicoutlook.htm ECOSCOPE blog: oecdecoscope.wordpress.com/

Sudden Stops in a Business Cycle Model with Credit Constraints: A Fisherian Deflation of Tobin s Q * Enrique G. Mendoza University of Maryland & NBER

Draft: April 18, 2005 preliminary draft Sudden Stops in a Business Cycle Model with Credit Constraints: A Fisherian Deflation of Tobin s Q * By Enrique G. Mendoza University of Maryland & NBER Sudden Stops

Draft: April 18, 2005 preliminary draft Sudden Stops in a Business Cycle Model with Credit Constraints: A Fisherian Deflation of Tobin s Q * By Enrique G. Mendoza University of Maryland & NBER Sudden Stops

The Macroeconomic Effects of Protectionism

The Macroeconomic Effects of Protectionism Fabio Ghironi University of Washington, CEPR, and NBER Global Business Forum November 26, 28 Modeling the Macroeconomic Effects of Protectionism IMF, Fed: Multi-country,

The Macroeconomic Effects of Protectionism Fabio Ghironi University of Washington, CEPR, and NBER Global Business Forum November 26, 28 Modeling the Macroeconomic Effects of Protectionism IMF, Fed: Multi-country,

Global Pricing of Risk and Stabilization Policies

Global Pricing of Risk and Stabilization Policies Tobias Adrian Daniel Stackman Erik Vogt Federal Reserve Bank of New York The views expressed here are the authors and are not necessarily representative

Global Pricing of Risk and Stabilization Policies Tobias Adrian Daniel Stackman Erik Vogt Federal Reserve Bank of New York The views expressed here are the authors and are not necessarily representative

RESILIENCE IN A TIME OF HIGH DEBT

RESILIENCE IN A TIME OF HIGH DEBT PRE-RELEASE OF THE SPECIAL CHAPTER OF THE OECD ECONOMIC OUTLOOK (To Be Released on 28th November at 11.00am CET) Paris, 23th November 2017 www.oecd.org/economy/economicoutlook.htm

RESILIENCE IN A TIME OF HIGH DEBT PRE-RELEASE OF THE SPECIAL CHAPTER OF THE OECD ECONOMIC OUTLOOK (To Be Released on 28th November at 11.00am CET) Paris, 23th November 2017 www.oecd.org/economy/economicoutlook.htm

WHAT DO HOUSEHOLD SURVEYS SUGGEST ABOUT THE TOP 1% INCOMES AND INEQUALITY IN OECD COUNTRIES? Nicolas Ruiz (OECD)

") WHAT DO HOUSEHOLD SURVEYS SUGGEST ABOUT THE TOP 1% INCOMES AND INEQUALITY IN OECD COUNTRIES? Nicolas Ruiz (OECD) Motivation: the Inclusive growth puzzle the top percentile managed to capture a very large

WHAT DO HOUSEHOLD SURVEYS SUGGEST ABOUT THE TOP 1% INCOMES AND INEQUALITY IN OECD COUNTRIES? Nicolas Ruiz (OECD) Motivation: the Inclusive growth puzzle the top percentile managed to capture a very large

2018 OECD ECONOMIC SURVEY OF CHILE

2018 OECD ECONOMIC SURVEY OF CHILE Boosting productivity and quality jobs Santiago, 26 February 2018 http://www.oecd.org/eco/surveys/economic-survey-chile.htm @OECDeconomy @OECD Convergence has been impressive

2018 OECD ECONOMIC SURVEY OF CHILE Boosting productivity and quality jobs Santiago, 26 February 2018 http://www.oecd.org/eco/surveys/economic-survey-chile.htm @OECDeconomy @OECD Convergence has been impressive

Foreign Capital and Economic Growth

Foreign Capital and Economic Growth Arvind Subramanian (Eswar Prasad and Raghuram Rajan) Western Hemisphere Department Workshop November 17, 2006 *This presentation reflects the views of the authors only

Foreign Capital and Economic Growth Arvind Subramanian (Eswar Prasad and Raghuram Rajan) Western Hemisphere Department Workshop November 17, 2006 *This presentation reflects the views of the authors only

38th meeting of the EU-Turkey Joint Consultative Committee (JCC)

") tepav The Economic Policy Research Foundation of Turkey 38th meeting of the EU-Turkey Joint Consultative Committee (JCC) SMEs-Trade development and investment environment opportunities between the EU and

tepav The Economic Policy Research Foundation of Turkey 38th meeting of the EU-Turkey Joint Consultative Committee (JCC) SMEs-Trade development and investment environment opportunities between the EU and

Introduction: macroeconomic implications of capital flows in a global economy

Journal of Economic Theory 119 (2004) 1 5 www.elsevier.com/locate/jet Editorial Introduction: macroeconomic implications of capital flows in a global economy Abstract The papers in this volume address

Journal of Economic Theory 119 (2004) 1 5 www.elsevier.com/locate/jet Editorial Introduction: macroeconomic implications of capital flows in a global economy Abstract The papers in this volume address

Building Blocks for the FTAAP: Investment and Services

Building Blocks for the FTAAP: Investment and Services Robert Scollay New Zealand APEC Study Centre, University of Auckland Presented at CNCPEC Symposium on FTAAP: Asia-Pacific Economic Integration by

Building Blocks for the FTAAP: Investment and Services Robert Scollay New Zealand APEC Study Centre, University of Auckland Presented at CNCPEC Symposium on FTAAP: Asia-Pacific Economic Integration by

NAVIGATING an INTERCONNECTED WORLD. Sean Hagan, Tamim Bayoumi, and Steven Phillips

NAVIGATING an INTERCONNECTED WORLD Sean Hagan, Tamim Bayoumi, and Steven Phillips I NTEGRATED S URVEILLANCE D ECISION Why an Integrated Surveillance Decision? Highly interconnected world: need to monitor

NAVIGATING an INTERCONNECTED WORLD Sean Hagan, Tamim Bayoumi, and Steven Phillips I NTEGRATED S URVEILLANCE D ECISION Why an Integrated Surveillance Decision? Highly interconnected world: need to monitor

EFFECTS OF NEW US AUTO TARIFFS ON GERMAN EXPORTS, AND ON INDUSTRY VALUE ADDED AROUND THE WORLD

1 ifo Institute ifo Center for International Economics Gabriel Felbermayr & Marina Steininger Feb 15, 2019 EFFECTS OF NEW US AUTO TARIFFS ON GERMAN EXPORTS, AND ON INDUSTRY VALUE ADDED AROUND THE WORLD

1 ifo Institute ifo Center for International Economics Gabriel Felbermayr & Marina Steininger Feb 15, 2019 EFFECTS OF NEW US AUTO TARIFFS ON GERMAN EXPORTS, AND ON INDUSTRY VALUE ADDED AROUND THE WORLD

Fiscal Implications of Population Ageing Asian Countries

Disclaimer: The findings, interpretations, and conclusions expressed in this material represent the views of the author(s) and are not necessarily those of the ASEAN+3 Macroeconomic Research Office (AMRO)

Disclaimer: The findings, interpretations, and conclusions expressed in this material represent the views of the author(s) and are not necessarily those of the ASEAN+3 Macroeconomic Research Office (AMRO)

Productivity, Reallocation, and Equity: Challenges of disruptive technology and trade

Productivity, Reallocation, and Equity: Challenges of disruptive technology and trade Catherine L. Mann OECD Chief Economist Peterson Institute for International Economics October 2017 www.oecd.org/economy

Productivity, Reallocation, and Equity: Challenges of disruptive technology and trade Catherine L. Mann OECD Chief Economist Peterson Institute for International Economics October 2017 www.oecd.org/economy

Monetary and Macro-Prudential Policies: An Integrated Analysis

Monetary and Macro-Prudential Policies: An Integrated Analysis Gianluca Benigno London School of Economics Huigang Chen MarketShare Partners Christopher Otrok University of Missouri-Columbia and Federal

Monetary and Macro-Prudential Policies: An Integrated Analysis Gianluca Benigno London School of Economics Huigang Chen MarketShare Partners Christopher Otrok University of Missouri-Columbia and Federal