WELCOME TO WPA Insurance Panel. January 20, 2014

|

|

|

- Melina Wade

- 5 years ago

- Views:

Transcription

1 WELCOME TO WPA Insurance Panel January 20, 2014

employing a staff of 20.")

2 MICHAEL OSKOUIAN, CRM, CIC, LUTCF BIO Michael is a Vice President within the Willis North America Practice and is located in Seattle. He specializes in identifying risks and providing valuable solutions within the areas of Property and Casualty. As a Certified Risk Manager and an Entrepreneur he understands the business risks owners face every day and has the solutions to mitigate those risks. Prior to joining Willis, Michael owned an insurance agency in Seattle for eighteen years (18) employing a staff of 20. Michael Oskouian, CRM, CIC, LUTCF (425) Cell (206) Direct (206) Office th Ave S Suite 200 Seattle, WA michael.oskouian@willis.com

3 Willis is a Risk Advisor: 100% Transparent Client Broker Insurer Client Advisor Broker Insurer

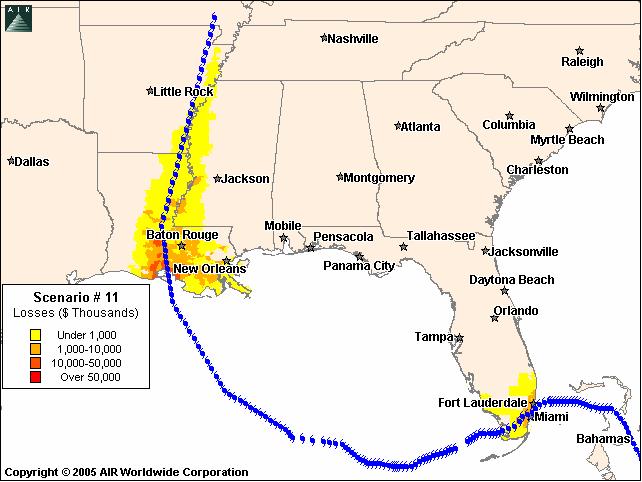

4 ANALYTIC/MODELING TOOLS bigger

5 ANALYTIC/MODELING TOOLS

6 ANALYTIC/MODELING TOOLS

7 ANALYTIC/MODELING TOOLS

8 WHAT UNDERWRITERS REQUIRE IN A SUBMISSION Description of Operations Program Specifications Value Summaries Loss History Policy Form Engineering

9 Casualty Expertise Portals Casualty Communities linking Experts and Evolution Employee Health and Safety Product Liability Casualty General and Auto Liability Catastrophic & Excess Risks Collateral and Risk Finance

10 Casualty Expert Teams Building Communities of the Best Brokers to build Best Practices and Coverage Specifications We have assembled 6 Expert Working Groups: Workers Comp Auto Liability General Liability Product Liability Umbrella and Excess Liability Collateral and Risk Finance Teams are comprised of National, Regional and Local Experts with technical expertise in an industry, risk, state or coverage.

11 National Casualty Practice Unlocking the Power of Connection Casualty Expert Team Members are easy to spot by the Blue Ribbon Banner highlighting their Avatar!

12 Great Advocates Deliver Value Cost Reduction in Casualty Costs can deliver more Cash, Capital and/or Earnings Casualty Savings drop to the Bottom Line I have yet to meet a CFO or Treasurer or Risk Manager that feels their Capital is best deployed in their Risk Management Program. I have met CFOs and Treasurers that have perceived economic value in new structures, additional limits or better coverage Communicate value in a common economic value

13 Building the Best Team Willis Service Plan Best Practices Time Table Client Name Client Name ABC Company Renewal Date 8/1/2014 Today's Date 1/6/2014 Client Coverage Lines / Industry Workers Compensation Automobile Liability General Liability Property Construction Healthcare Executive Risks Environmental / Pollution Surety Surplus Lines Guaranteed Cost Premium Financing Loss Data Team Role Assignment Client Client Advocate Client Manager Senior Client Manager Assistant Client Manager Placement Specialists / Marketing Industry Marketing Specialists Risk Consultant (Claims Specialists) Loss Control Specialists Is WC a part of this placement? Is AL a part of this placement? Is GL a part of this placement? Is Property a part of this placement? Is Construction a part of this placement? Is Healthcare a part of this placement? Is Executive Risks a part of this placement? Is Environmental / Pollution a part of this placement? Is Surety a part of this placement? Does this placement involve SL? Is this placement a guaranteed cost? Is Premium Financing an interest? Does client have credible loss data? ABC Company Pam Mike Karen Mary Steve Rob Lori Jim Yes Yes Yes Yes No No No No No No No No Yes

14 Consistently delivering a Great Casualty Program Best Practices Casualty Service Plan ABC Company Willis Service Plan (WSP) Best Practices Timetable Action Task Target Date 1. Client Advocacy Report [Annual Review / Stewardship Report] 11/4/ Client Service Evaluation [Client Survey] 12/4/ Delivery of the Client Engagement Guide 2/2/ Conduct Analytics Meetings with Incumbent Market [Actuarial / Credit / Underwriting] 2/2/ Needs Analysis / Risk Assessment / Identification Review 3/14/ Prepare for Renewal Strategy Meeting T 3/14/ Conduct Team Renewal Strategy Meeting I 3/24/ Conduct Client Renewal Strategy Meeting M 4/3/ Prepare Submission - Gather and Review Underwriting Data - E Losses, Exposures, Coverage Specs & Financials 5/3/ Send Submission to Client and Market(s) L 5/3/ Meet with Market(s) to Provide Quotes I 5/18/ Analyze Quotation Proposals N 6/2/ Prepare Renewal Proposal E 6/12/ Present Renewal Proposal to Client 6/22/ Bind Renewals 7/2/ Invoicing 7/12/ Policy Administration - Certs / ID Cards / Posting Notices / UM UIM Forms 7/17/ Renewal Incepts 8/1/ Receive and Review Renewal Policies 8/31/ Deliver Policies to Client 9/15/ Obtain Client Feedback Note: Blue italic if Action Task should have been completed by today's date. 9/15/

15 Consistently delivering a Great Casualty Program Delivering the Value > Present Client Advocacy Report - review and meet with Client - obtain BOR's if necessary 11/04/13 Overdue task Pam > Document discussions with Client 11/04/13 Overdue task Pam Days Prior - Client Service Evaluation [Client Survey] > Client Service Evaluation [Client Survey] 12/04/13 Overdue task Pam > Formal evaluation of the overall quality and delivery of broking and risk management services using the electronic client survey and open discussions 12/04/13 Overdue task Pam > Discussion about areas or activities currently not covered by the insurance program 12/04/13 Overdue task Pam > Advise Client about Survey 12/04/13 Overdue task Pam > Provide and review Client Survey results with the client team 12/04/13 Overdue task Pam > Prepare and send "Thank You" letter to Client 12/04/13 Overdue task Pam > Schedule and conduct Client Survey meeting to review the results 12/04/13 Overdue task Pam > Document discussions with Client 12/04/13 Overdue task Pam > Conduct Broker Claim Review - (Strategic Outcomes Practice delivers Claim, Risk Control, Safety and Data Analytic consulting services) 12/04/13 Overdue task Mike / Lori - Evaluate claim reserves - Reserve to present known outcome 12/04/13 Overdue task Mike / Lori - Audit claim activity 12/04/13 Overdue task Mike / Lori - Resolution of pending claims 12/04/13 Overdue task Mike / Lori - Identify subrogation potential 12/04/13 Overdue task Mike / Lori - Adherence to action plan for claim resolution / closure 12/04/13 Overdue task Mike / Lori - Evaluate claims servicing account instructions 12/04/13 Overdue task Mike / Lori - Identify adjuster service issues 12/04/13 Overdue task Mike / Lori - Evaluate Managed Care and Bill Re-pricing activity 12/04/13 Overdue task Mike / Lori > Document claim review discussions with Client, Carrier and Client Team 12/04/13 Overdue task Mike / Lori > Workers' Compensation Experience Modification review 12/04/13 Overdue task Mike / Lori Days Prior - Delivery of the Client Engagement Guide (CEG) > Create Master Marketing File (required for documentation) 02/02/14 Pam > Prepare Placing File Checklist (PFC) to document compliance requirements and place copy in file (and WPC) 02/02/14 Pam > Prepare Client Relationship Information Pack (Client Engagement Guide) 02/02/14 Pam > Present and discuss the following key documents which define the way we work together to the Client: 02/02/14 Pam

16 Willis Global Captive Practice The Willis Captive Practice provides unparalleled expertise in designing, forming, managing and providing strategic guidance to captives of all types in all major captive domiciles. Willis manages more than 375 captives in 28 domiciles worldwide, our clients gross premiums exceed $4 billion, with total captive insurance company assets of nearly $40 billion. Our operating platform has three main structures: Captive Consulting Captive Management Group Captives The Practice has over 150 dedicated employees, including CPAs, risk finance specialists, captive management experts and strategic planning consultants.

, Ltd.")

, Ltd.")

17 The Americas Les Boughner Executive VP & MD of the Willis Captive Management Practice Group Captives Randy Boomgarden Alembic Craig Ream Construction Solutions Consulting/Sales Sean Rider New York Richard W. Wright New Jersey Anne Marie Towle - Chicago Kathleen Waslov Employee Benefits Bruce Whitmore - Healthcare Willis Management (Bermuda), Ltd. Oliver Heyliger Willis Management (Cayman), Ltd. Barbados Stephen Gray Willis Management (Vermont), Ltd. New York, South Carolina, Tennessee David Guerino Willis Management (Hawaii) Arizona, Nevada, Utah Jason Palmer

18 Willis Captive Practice Captive Consulting New Captive Feasibility Strategic Consulting for Mature Captives Captive Management Liaison with Actuaries, Regulators, Auditors Ongoing servicing Preparation of captive financials Ongoing filing maintenance Shareholder Board of Directors meeting Group Captives

19 Willis Captive Consulting Practice Strategic Consulting for Mature Captives Our various efforts classed as strategic consulting for mature captives aim at assessing and maximizing how an organization achieves value from an existing captive vehicle. As organizations change and regulatory, domicile, tax, and risk tolerance regimes morph over time, the efficacy of captives and their utilization opportunities also change. Our services are focused on helping captive owners determine the optimal use, structure, and/or winding down of a captive. Periodic brainstorming with key members of the captive owner s management group and other service partners to consider risk retention levels and alternatives, additional lines of coverage, what-if scenarios, domicile issues, etc. Interpretation and analysis of actuarial, financial, and other captive data; Attendance and participation at captive board meetings; Keeping the captive s leadership current with captive industry, domicile, tax and accounting changes and assessing the impact of these changes; Providing an independent voice in vendor assessment and assisting in RFP processes as needed; Evaluating risk areas where the captive s participation would enhance protection and reduce cost-ofrisk; Evaluation of the ongoing efficacy of a captive, and management of the outcomes of that analysis.

20 Lines of Business TRADITIONAL EXPANDED EMERGING Workers Compensation Auto Liability General Liability Professional and Products Liability Director and Officer Liability Employment Practices Liability Environmental Liability Product or Service Extended Warranty Property and Business Interruption EE Benefits Terrorism (TRIA) Shipping Coverage Title and Private Mortgage Insurance Equipment Maintenance Construction Exposures Trade Credit Risk Cyber-Risk Managed Care Errors and Omissions Self-Insured Medical Stop-Loss (non- ERISA) Reputation/Brand/Loss of Income Risks Intellectual Property (patent, trademark, copyright) Product Recall Coverage Medicare Fraud and Abuse Insurance Lease Residual Value Risk Punitive Damages Coverage

21 Types of Captive Utilization Retained Risk Finance Risk Transfer Rate Arbitrage Access to Capacity Entrepreneurial Utilizations Infrastructure for providing transparency, validation, and rationalization of retained risk positions Enhancing risk management efforts Accelerating tax treatment of deductible liabilities Reinsurance market cost of risk transfer is less than commercial retail cost of risk transfer Better use of capital to retain risk than transfer it Managing total cost of risk Federal programs (TRIA) Reinsurance capacity, which may not be otherwise accessible in commercial retail market (trade credit risk, +10 yr pollutions risks) Franchisee programs Consumer facing insurance programs (warranty, service contract, point of sale insurances, etc) Affiliate business (vendors, VAPs, distributors, etc) Agency captives 3 rd party business

22 831b / Microcaptives Underwriting income for the captive is tax free. Can be utilized as a wealth transfer and estate planning vehicle for private companies. Willis will only become involved with Microcaptives when there is a sustainable business plan.

23 831b / Microcaptives Under the provisions of the United States Tax Code 831(b), a tax election may be available to U.S. Property and Casualty ("P&C") Insurers (Small Insurance Companies) with written premiums less than $1.2 million dollars. If properly structured, the insurance company is taxed on net investment income only and not on underwriting income. Non-taxed underwriting income, if any will accrue to the captive s surplus and dividends and may be eligible for the dividends received deduction when distributed to the corporate shareholder(s) or parent, and dividends distributed to an individual owner are taxed at the capital gains rate

24 The aim is to put our clients in a superior information position

25 Resilience example: ERM Maturity Model Framework Element Immature Basic Mature Advanced World-Class Risk Identification No formal process for identification of risks Annual risk identification exercise for key projects and sites Key corporate risks identified with limited interaction among groups Business risks frequently identified with assessment of likelihood, impact and mitigating actions; cross-group work All major risks regularly identified. Robust process also surfaces new and emerging risks Risk Assessment and Prioritization No formal process for assessment of risks Limited analysis to assess and provide insight. Major business risks discussed at Business Unit level Prioritization of key risks across the group with detailed quantification of selected risks Prioritization based on aggregation of all business risks across the group; risk tolerance known and included in assessment Prioritization of aggregated risks across group with classification by key underlying risk drivers and company-killer scenarios Risk Mitigation and Financing Options Little or no systematic development and comparison of options; external risk reporting requirements sometimes not met Methodologies for risk categories identified and used inconsistently; compliance mentality Options compared within business units using consistent methods but done within functions primarily Company-wide comparison of options, but within functions (finance, operations, insurance, construction, etc) Options compared across company and across functions in single language of risk and decisions made accordingly Risk Strategy and Action Plans No action plan for risk management and finance exists One or more action plans exists within one or more functions and one or more business units Functions each have an independent action plan with limited or no communication with other functions; business units may have action plans Action plans completed annually within functions and business units in consistent manner Board has owners of key black swan scenarios and is continuously engaged in assessing action plans, all of which are in single risk language Risk Implementation Little or no followthrough on option recommendations; poor results in key risk management metrics Some key risks are managed resulting in fewer surprises; but little or no preparation for major risk response Functions implement their action plans well and business units track progress of these functional plans Top management tracks business unit and function progress and oversees implementation Board receives updates on actions regularly, participates in simulation exercises and guides management

26 IMPLEMENTATION RISK STRATEGY How Willis GSCG Thinks About Risk Client Risk Landscape Risk Insight Steps Solution Choices 6. Retain - Balance Sheet - Captive Transfer Understand Define Risk Identify Model Loss Calculate - To Insurers Client and Tolerance Priority Frequency CCoR SM - To Capital Industry Exposures and Severity Markets Dynamics and Risks 8. Mitigate Data gathering, preparation and provision 9. Avoid Risk financing options Risk management options

Identifies technically optimal risk financing program structure for a given risk and quantifies volatility of retained risk $")

")

27 Earthquake Loss OEP Curve Proprietary Tools and Processes FIA SM (Financial Impact Analysis) Measures an organizations risk tolerance based on pre-determined ranges of variability in key financial metrics 5 CCoR SM (Comprehensive Cost of Risk) Identifies technically optimal risk financing program structure for a given risk and quantifies volatility of retained risk $ Millions 4 $0.20 $0.40 $1.00 $0.50 $ $ $2.20 $4.00 $ $2.00 $ $ No Insurance Large Deductible Small Deductible Guaranteed Cost Expected Retained Losses Exp Premium Cost of Volatility Program Value PRISM SM (Privacy Risk Insurance Strategy Model) Quantifies privacy risk data and identifies optimal insurance program structure WISDOM SM (Willis Integrated Solutions Directors & Officers Model) Quantifies D&O risk, identifies optimal insurance structure Natural Catastrophe Analysis Modeling and managing natural catastrophe (nat. cat) risk ) Modelled Loss ($mn) 8 ($mn 7 7 ss o L 66 ed l el 5 d o M 4 Earthquake Loss OEP Curve 3 2 Policy Programme Activation Exhaustion ,000 Return Period (yrs)

28 FIA Financial Impact Analysis Establish the surprise negative deviations in key financial metrics that a company is able to sustain in a given year Model the company's financials to demonstrate the impact of increasing levels of retained downside risks on these metrics Incorporate the output into a risk financing strategy that achieves lowest cost of risk within the acceptable range of tolerance

29 CCoR SM Comprehensive Cost of Risk Antithesis of benchmarking Establishes the optimal premium / limit / retention configuration for a given risk Identifies what should be retained rather than what could be retained Achieves most efficient use of risk financing capital 5 $ Millions 4 3 $0.20 $0.40 $1.00 $0.50 $0.10 $ $2.20 $4.00 $ $ $1.00 -$0.30 No Insurance Large Deductible Small Deductible Guaranteed Cost Expected Retained Losses Exp Premium Cost of Volatility Program Value

30 CCoR SM 100% 90% Probability (%) 80% 70% 60% 50% 40% After risk financing (Including Prem) Before risk financing Risk Volatility 30% 20% 10% Risk Volatility 0% Impact ($MM) 12.7 Expected Loss

Accesses a proprietary database of thousands of privacy risks Adjusts industry data")

Actual Total Records Affected Selected Severity Distribution Utilizes CCoRSM to determine the optimal privacy insurance program structure UNINSURED LOSS PROBABILITY DISTRIBUTIONS Value of")

31 PRISM SM Privacy Risk Insurance Strategy Model Analytic model used to quantify privacy risk 0.25 Probability Distribution of Total Records Affected (Actual Total Records Affected vs Selected Distribution) Accesses a proprietary database of thousands of privacy risks Adjusts industry data relative to client-specific risks and controls Cumulative Probability 100% 90% 80% 70% 60% 50% 40% 30% 20% Applies Monte Carlo simulation to generate several thousand hypothetical loss years Historical Breach Frequency Projected Breach Frequency 10% 0% ,000 10, ,000 1,000,000 10,000, ,000,000 Total Records Affected (Logarithmic Scale) Actual Total Records Affected Selected Severity Distribution Utilizes CCoRSM to determine the optimal privacy insurance program structure UNINSURED LOSS PROBABILITY DISTRIBUTIONS Value of Various Privacy Breach Insurance Structures (Safety Level = 99.9% ) 100.0% 95.0% 3,000, % 2,500, , ,596 33, ,000 2,000,000 1,400,000 1,744, ,000 1,500,000 1,245,083 1,000, , ,090 1,260,518 CUMULATIVE PROBABILITY (CONFIDENCE LEVE 85.0% 80.0% 75.0% 70.0% 65.0% 60.0% 389, , , % 0 617, , , ,116 No Insurance 25M/25M xs 2M 50M/35M xs 2M 100M/50M xs 5M 175M/175M xs 10M Expected Retained Losses Cost of Volatility Premium Value "Break-Even" Premium 50.0% $100 $1,000 $10,000 $100,000 $1,000,000 $10,000,000 $100,000,000 AGGREGATE ANNUAL LOSSES Notification, Regulatory Fines All Other Insurable Costs Total Discovery, Response

32 WISDOM SM Willis Integrated Solutions Directors & Officers Model Analytic tool used to quantify D&O risks for public companies Generates a frequency distribution based on industry, market cap, and a robust proprietary database of historic D&O losses Generates a severity distribution using the proprietary database of historic D&O losses Combines frequency and severity distributions, simulating thousands of hypothetical loss years using Monte Carlo Simulation Utilizes CCoR SM to determine the optimal D&O insurance program structure

Modelled Loss ($mn) 8 ($mn 7 7 ss o L 6 ed l el 5 d o M")

33 Natural Catastrophe Analysis Strategic CAT review High level review and mapping of a client s natural hazard exposures on a regional or global basis. CAT Modeling Use of natural catastrophe models to quantify a client s portfolio losses at an aggregate level and compare against their current retention levels and CAT limits in their insurance program ) Modelled Loss ($mn) 8 ($mn 7 7 ss o L 6 ed l el 5 d o M 4-3 Earthquake Loss OEP Curve 2 Policy Programme Activation Exhaustion ,000 Return Period (yrs) CAT Risk Engineering On-site risk engineering surveys for individual facilities that are identified as having high levels of localized property damage and business interruption exposures. Provision of cost-effective improvement measures to reduce the exposure.

34 LossPIQ SM Overview Prospective Identification & Quantification Quantifies low frequency / high severity risks where loss data is scare or non-existent Identifies most plausible future loss scenarios Willis develops a loss model for each risk and populates it with risk impact types and cost drivers Expert client team disassembles each major scenario into 3 sub-scenarios and then by consensus assigns impact and likelihood parameters Model aggregates data and generates an overall loss distributions curve of the risk Synthesize most plausible future scenarios Transition qualitative into quantitative measurement Integrate with historical and public domain data, run simulations

35 LossPIQ SM Risk Register XYZ BANK DENIAL OF ACCESS COSTS Notification Recovery Site Invocation Alternative Accommodations # of Locations % of Events # Days # Days % of Events # of Alt # Years % of Events Scenario Subscenario Description/Comments Likelihood Low High This Would Occur Low High This Would Occur Sites Rental This Would Occur DOA - Natural Event Anticipated UK Southern Severe Snow DOA - Natural Event Mid Range London Flood DOA - Natural Event Worst Case Pandemic Affecting >30% DOA - Man Made Event Anticipated Building evacuation DOA - Man Made Event Mid Range Terrorist non-cbnr attack DOA - Man Made Event Worst Case Terrorist CBNR attack Information Security Breach Anticipated Unauthorized access Information Security Breach Mid Range Data leakage Information Security Breach Worst Case Malicious cyber attack Infrastructure Failure Anticipated Power/cooling outage Infrastructure Failure Mid Range Data corruption Infrastructure Failure Worst Case Multiple data center losses Inadequate Planning Anticipated Included in other scenarios Inadequate Planning Mid Range Included in other scenarios Inadequate Planning Worst Case Included in other scenarios Third Party/Vendor Error Anticipated Virus Third Party/Vendor Error Mid Range Connectivity/network outage Third Party/Vendor Error Worst Case SBSA domain security outage Regulatory Censure Anticipated Greater regulatory oversight/fines Regulatory Censure Mid Range Conditions on license/fines>$10m Regulatory Censure Worst Case Loss or suspension of license/removal of senior mgt DOA - Political/Social Unrest Anticipated Industrial action DOA - Political/Social Unrest Mid Range Large scale civil unrest DOA - Political/Social Unrest Worst Case Civil war in South Africa Anticipated Mid Range Worst Case

36 LossPIQ SM Output XYZ BANK PERCENTILE EXPECTED LOSS- $M 50.0% $ % $ % $ % $ % $ % $ % $ % $ % $ % $ % $ % $ % $ % $ % $ % $ % $ % $ % $ % $ % $ % $ % $ AVERAGE: $4.60 STDEV: $23.48

37 RAPID SM Risk Assessment Probability & Impact Diagnostic FEATURES Consensus driven process to identify, assess, and communicate enterprise risk Can be used across an enterprise or on a surgical basis Comprehensive, accelerated, and cost effective Fully articulates and prioritizes the major risks to achieving business objectives Surfaces emerging and unforeseen risks Generates high impact, real time graphics Built-in module for Improvement Planning

38 Risk Optimizer Combines CCoR SM and FIA CCoR SM establishes optimal structure by line of coverage FIA establishes corporate risk tolerance level Probability of collective retentions breaching tolerance is determined Individual retentions are adjusted to accommodate overall tolerance and risk appetite Analytics are periodically recalculated to accommodate changes in both risks and financials Program structure is adjusted as necessary to maintain the lowest cost within the risk tolerance level

13612 (12612) 13412 (12412) 13411 Current 33412 33411 (32411) 36.0 36.5 37.0 37.5 38.0 38.5 39.0 39.5 40.")

39 Risk Optimizer Risk Optimizer (Expected Cost vs Probability of Exceeding $50M Risk Tolerance, Excluding No Insurance) 1.90% Prob. of Exceeding $50M Above Expected Cost 1.85% 1.80% 1.75% 1.70% 1.65% 1.60% (12622) (12612) (12412) Current (32411) Millions Expected Cost (Premium + Discounted Expected Retained Losses)

40 We are honored to be part of Western Pallet Association. THANK YOU

Captives/RRGs 101-the Basics of Alternative Risk Transfer

Captives/RRGs 101-the Basics of Alternative Risk Transfer Sean Rider- Willis Captive Consulting Practice Jules Rousseau-Arent Fox LLP David Provost-State of Vermont Monday, March 14th - 1:30pm 3:00pm Presentation

Captives/RRGs 101-the Basics of Alternative Risk Transfer Sean Rider- Willis Captive Consulting Practice Jules Rousseau-Arent Fox LLP David Provost-State of Vermont Monday, March 14th - 1:30pm 3:00pm Presentation

Captive 101-Back to the Basics

Captive 101-Back to the Basics Sean Rider, Willis Global Captive Practice Scott Spencer, Stevens & Lee Moderator: Anne Marie Towle, Willis Global Captive Practice Presentation Topics Captive Primer Feasibility

Captive 101-Back to the Basics Sean Rider, Willis Global Captive Practice Scott Spencer, Stevens & Lee Moderator: Anne Marie Towle, Willis Global Captive Practice Presentation Topics Captive Primer Feasibility

Risk & Analytics. Trends within Insurance Companies Risk Management. Marc Paasch June Willis Towers Watson. All rights reserved.

Risk & Analytics Trends within Insurance Companies Risk Management Marc Paasch June 2017 2017 Willis Towers Watson. All rights reserved. Key drivers & benefits Outcomes from an analytical approach to own

Risk & Analytics Trends within Insurance Companies Risk Management Marc Paasch June 2017 2017 Willis Towers Watson. All rights reserved. Key drivers & benefits Outcomes from an analytical approach to own

Aon Risk Solutions. Real Estate Practice. Fact-based Solutions for Real Estate Risk Management. Risk. Reinsurance. Human Resources.

Aon Risk Solutions Real Estate Practice Fact-based Solutions for Real Estate Risk Management Risk. Reinsurance. Human Resources. Do these problems sound familiar? My insurance broker doesn t understand

Aon Risk Solutions Real Estate Practice Fact-based Solutions for Real Estate Risk Management Risk. Reinsurance. Human Resources. Do these problems sound familiar? My insurance broker doesn t understand

THIS SESSION WILL USE POLLING!

THIS SESSION WILL USE POLLING! (To access in an internet browser, go to vcia.cnf.io) Click on the Polling Icon on the VCIA app Click on your session Respond to the Polls HOW TO USE SOCIAL Q&A! (To access

THIS SESSION WILL USE POLLING! (To access in an internet browser, go to vcia.cnf.io) Click on the Polling Icon on the VCIA app Click on your session Respond to the Polls HOW TO USE SOCIAL Q&A! (To access

WELCOME TO THE WORLD OF CAPTIVES

WELCOME TO THE WORLD OF CAPTIVES Mike Meehan, CIC, CRM Consultant Milliman, Inc. Anne Marie Towle, CPA EVP, Captive Practice Leader JLT Insurance Management November 27, 2018 Learning Objectives Objective

WELCOME TO THE WORLD OF CAPTIVES Mike Meehan, CIC, CRM Consultant Milliman, Inc. Anne Marie Towle, CPA EVP, Captive Practice Leader JLT Insurance Management November 27, 2018 Learning Objectives Objective

Section 831(b) Captive Nuances and Best Practices, Tax Risk Distribution/Sharing and. Accounting Risk Transfer Rules

Captive Nuances and Best Practices, Tax Risk Distribution/Sharing and. Accounting Risk Transfer Rules") ACI s 2 nd Advanced Forum on Captive Insurance Section 831(b) Captive Nuances and Best Practices, Tax Risk Distribution/Sharing and April 24-25, 2014 Accounting Risk Transfer Rules Anne Marie Towle Senior

ACI s 2 nd Advanced Forum on Captive Insurance Section 831(b) Captive Nuances and Best Practices, Tax Risk Distribution/Sharing and April 24-25, 2014 Accounting Risk Transfer Rules Anne Marie Towle Senior

Wednesday, March 5, 2014 Houston, TX. 1:30 2:45 p.m. IMPROVING RISK MANAGEMENT AND INSURANCE PLACEMENTS USING ANALYTICS

Wednesday, March 5, 2014 Houston, TX 1:30 2:45 p.m. IMPROVING RISK MANAGEMENT AND INSURANCE PLACEMENTS USING ANALYTICS Presented by Joe Beesack Senior Vice President, Alternative Risk Solutions Practice

Wednesday, March 5, 2014 Houston, TX 1:30 2:45 p.m. IMPROVING RISK MANAGEMENT AND INSURANCE PLACEMENTS USING ANALYTICS Presented by Joe Beesack Senior Vice President, Alternative Risk Solutions Practice

UTILIZATION OF CAPTIVES TODAY

UTILIZATION OF CAPTIVES TODAY November 20, 2015 Prepared by: Julie Patel Vice President Marsh Captive Solutions Utilization of Captives Today Objectives of Discussion 1. Captive Basics 2. The Process of

UTILIZATION OF CAPTIVES TODAY November 20, 2015 Prepared by: Julie Patel Vice President Marsh Captive Solutions Utilization of Captives Today Objectives of Discussion 1. Captive Basics 2. The Process of

THE SMART WAY TO ANALYSE YOUR RISKS. DAVID STEBBING Partner, Willis Risk & Analytics

THE SMART WAY TO ANALYSE YOUR RISKS DAVID STEBBING Partner, Willis Risk & Analytics Increasing risks and challenges Commodity market volatility Short-term cashflow planning Profitability of longterm investments

THE SMART WAY TO ANALYSE YOUR RISKS DAVID STEBBING Partner, Willis Risk & Analytics Increasing risks and challenges Commodity market volatility Short-term cashflow planning Profitability of longterm investments

OWN RISK AND SOLVENCY ASSESSMENT. ERM Seminar Compliance All Dealing from the same deck now

OWN RISK AND SOLVENCY ASSESSMENT ERM Seminar - 2014 Compliance All Dealing from the same deck now Own and Solvency Assessment! Originated in the UK about 10 years ago Now a global insurance regulatory

OWN RISK AND SOLVENCY ASSESSMENT ERM Seminar - 2014 Compliance All Dealing from the same deck now Own and Solvency Assessment! Originated in the UK about 10 years ago Now a global insurance regulatory

BLUEPRINT GLIMMERS OF SUN FOR CONSTRUCTION WHILE CLOUDS GATHER FOR INSURANCE CARRIERS CONSTRUCTION PRACTICE THE CONSTRUCTION INDUSTRY

CONSTRUCTION PRACTICE BLUEPRINT March 2012 www.willis.com GLIMMERS OF SUN FOR CONSTRUCTION WHILE CLOUDS GATHER FOR INSURANCE CARRIERS The construction industry and the insurance industry have in common

CONSTRUCTION PRACTICE BLUEPRINT March 2012 www.willis.com GLIMMERS OF SUN FOR CONSTRUCTION WHILE CLOUDS GATHER FOR INSURANCE CARRIERS The construction industry and the insurance industry have in common

Sections of the ORSA Report

Lessons Learned From Orsa Reviews Impact on Risk Focused Examination NAIC Insurance Summit INS Companies Joe Fritsch, Director INS Companies Don Carbone, Exam Manager INS Companies Sections of the ORSA

Lessons Learned From Orsa Reviews Impact on Risk Focused Examination NAIC Insurance Summit INS Companies Joe Fritsch, Director INS Companies Don Carbone, Exam Manager INS Companies Sections of the ORSA

The Purpose of a Captive Captives vs. Traditional Insurance Structuring a Captive Determining the Feasibility and Goals of a Captive Domicile

The Purpose of a Captive Captives vs. Traditional Insurance Structuring a Captive Determining the Feasibility and Goals of a Captive Domicile Selection Partner Selection Operating a Captive Captive Advantages

The Purpose of a Captive Captives vs. Traditional Insurance Structuring a Captive Determining the Feasibility and Goals of a Captive Domicile Selection Partner Selection Operating a Captive Captive Advantages

S L tr lo a y t d egy s Cyber -Attack

Lloyd s Cyber-Attack Strategy 02 Introduction The focus of this paper is on insurance losses arising from malicious electronic acts, referred to throughout as cyber-attack. The malicious act is the proximate

Lloyd s Cyber-Attack Strategy 02 Introduction The focus of this paper is on insurance losses arising from malicious electronic acts, referred to throughout as cyber-attack. The malicious act is the proximate

SOCIETY OF ACTUARIES Enterprise Risk Management General Insurance Extension Exam ERM-GI

SOCIETY OF ACTUARIES Exam ERM-GI Date: Tuesday, November 1, 2016 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 80 points. This exam consists

SOCIETY OF ACTUARIES Exam ERM-GI Date: Tuesday, November 1, 2016 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 80 points. This exam consists

Catastrophe Reinsurance Pricing

Catastrophe Reinsurance Pricing Science, Art or Both? By Joseph Qiu, Ming Li, Qin Wang and Bo Wang Insurers using catastrophe reinsurance, a critical financial management tool with complex pricing, can

Catastrophe Reinsurance Pricing Science, Art or Both? By Joseph Qiu, Ming Li, Qin Wang and Bo Wang Insurers using catastrophe reinsurance, a critical financial management tool with complex pricing, can

NAIC CIPR Spring Event on Pandemics

NAIC CIPR Spring Event on Pandemics Phoenix, Arizona March 27, 2015 David Rains Pandemic Solutions Key Considerations Multiple pandemic hedging options may be available. The optimal strategy will depend

NAIC CIPR Spring Event on Pandemics Phoenix, Arizona March 27, 2015 David Rains Pandemic Solutions Key Considerations Multiple pandemic hedging options may be available. The optimal strategy will depend

Modeling Extreme Event Risk

Modeling Extreme Event Risk Both natural catastrophes earthquakes, hurricanes, tornadoes, and floods and man-made disasters, including terrorism and extreme casualty events, can jeopardize the financial

Modeling Extreme Event Risk Both natural catastrophes earthquakes, hurricanes, tornadoes, and floods and man-made disasters, including terrorism and extreme casualty events, can jeopardize the financial

Risks. Insurance. Credit Inflation Liquidity Operational Strategic. Market. Risk Controlling Achieving Mastery over Unwanted Surprises

CONTROLLING INSURER TOP RISKS Risk Controlling Achieving Mastery over Unwanted Surprises Risks Insurance Underwriting - Nat Cat Underwriting Property Underwriting - Casualty Reserve Market Equity Interest

CONTROLLING INSURER TOP RISKS Risk Controlling Achieving Mastery over Unwanted Surprises Risks Insurance Underwriting - Nat Cat Underwriting Property Underwriting - Casualty Reserve Market Equity Interest

Insurance Program Benchmarking Methodology July 2015 Global Headquarters 1430 Broadway, 8th Floor New York, NY

Insurance Program Benchmarking Methodology July 2015 Table of Contents Table of Contents Overview 4 Why Insurance Program Benchmarking? 4 Advisen Patent US8762178 B2 4 What Insurance Program Data is included?

Insurance Program Benchmarking Methodology July 2015 Table of Contents Table of Contents Overview 4 Why Insurance Program Benchmarking? 4 Advisen Patent US8762178 B2 4 What Insurance Program Data is included?

Client Risk Solutions Going beyond insurance. Risk solutions for Construction. Start

Client Risk Solutions Going beyond insurance Risk solutions for Construction Start Partnering to Reduce Risk AIG s Client Risk Solutions (CRS) team builds long-term relationships with organizations to

Client Risk Solutions Going beyond insurance Risk solutions for Construction Start Partnering to Reduce Risk AIG s Client Risk Solutions (CRS) team builds long-term relationships with organizations to

CyberMatics SM FAQs. General Questions

CyberMatics SM FAQs General Questions What is CyberMatics? Like telematics for auto insurance, CyberMatics is a technology-driven process to help clients understand their current cyber risk as seen by

CyberMatics SM FAQs General Questions What is CyberMatics? Like telematics for auto insurance, CyberMatics is a technology-driven process to help clients understand their current cyber risk as seen by

Examination Best Practices and Hawaii Domicile Update. Honolulu, Hawaii October 22, 2014

Examination Best Practices and Hawaii Domicile Update Honolulu, Hawaii October 22, 2014 1 Welcome and Introductions Aloha 2 The Panel Robert Panah, CPA, CFE, CISA, Managing Director, Noble Consulting Services,

Examination Best Practices and Hawaii Domicile Update Honolulu, Hawaii October 22, 2014 1 Welcome and Introductions Aloha 2 The Panel Robert Panah, CPA, CFE, CISA, Managing Director, Noble Consulting Services,

The Reinsurance Placement Cycle

Session 507 Tuesday, June 10, 2014 1:45pm 3:15pm IASA 86 TH ANNUAL EDUCATIONAL CONFERENCE & BUSINESS SHOW Overview This will be an interactive session describing the placement of a reinsurance program

Session 507 Tuesday, June 10, 2014 1:45pm 3:15pm IASA 86 TH ANNUAL EDUCATIONAL CONFERENCE & BUSINESS SHOW Overview This will be an interactive session describing the placement of a reinsurance program

Lindsay Grimes Marsh USA Inc.

Lindsay Grimes Vice President Marsh USA Inc. 3560 Lenox Road NE Suite 2400 Atlanta, GA 30326 Lindsay.Grimes@marsh.com Date Client Name Title Address Subject: NFIP Engagement Letter Client Name, We are

Lindsay Grimes Vice President Marsh USA Inc. 3560 Lenox Road NE Suite 2400 Atlanta, GA 30326 Lindsay.Grimes@marsh.com Date Client Name Title Address Subject: NFIP Engagement Letter Client Name, We are

Practical Considerations for Building a D&O Pricing Model. Presented at Advisen s 2015 Executive Risk Insights Conference

Practical Considerations for Building a D&O Pricing Model Presented at Advisen s 2015 Executive Risk Insights Conference Purpose The intent of this paper is to provide some practical considerations when

Practical Considerations for Building a D&O Pricing Model Presented at Advisen s 2015 Executive Risk Insights Conference Purpose The intent of this paper is to provide some practical considerations when

Insurance Contracts for 831(b) Enterprise Risk Captives Policies and Pooling Agreements

Enterprise Risk Captives Policies and Pooling Agreements") Insurance Contracts for 831(b) Enterprise Risk Captives Policies and Pooling Agreements Jeffrey K. Simpson John R. Capasso Brian Johnson Gordon, Fournaris & Mammarella, P.A. Captive Planning Associates,

Insurance Contracts for 831(b) Enterprise Risk Captives Policies and Pooling Agreements Jeffrey K. Simpson John R. Capasso Brian Johnson Gordon, Fournaris & Mammarella, P.A. Captive Planning Associates,

RISK MANAGEMENT DUE DILIGENCE FOR MERGERS & ACQUISITIONS

DUE DILIGENCE due dil i gence noun Research and analysis of a company or organization done in preparation for a business transaction, particularly for mergers and acquisitions. RISK MANAGEMENT DUE DILIGENCE

DUE DILIGENCE due dil i gence noun Research and analysis of a company or organization done in preparation for a business transaction, particularly for mergers and acquisitions. RISK MANAGEMENT DUE DILIGENCE

Captive Insurance. A Risk Management Solution for Businesses

Captive Insurance A Risk Management Solution for Businesses The Concept Captive insurance is a tool to manage the insurance risks of operating a business, while providing the owners of the business substantial

Captive Insurance A Risk Management Solution for Businesses The Concept Captive insurance is a tool to manage the insurance risks of operating a business, while providing the owners of the business substantial

GALLAGHER REAL ESTATE & HOSPITALITY PRACTICE. Real Insurance Solutions for Real Estate and Hospitality

GALLAGHER REAL ESTATE & HOSPITALITY PRACTICE Real Insurance Solutions for Real Estate and Hospitality Real Estate & Hospitality Risk Management Services We Understand Your Business Understanding the specific

GALLAGHER REAL ESTATE & HOSPITALITY PRACTICE Real Insurance Solutions for Real Estate and Hospitality Real Estate & Hospitality Risk Management Services We Understand Your Business Understanding the specific

Guideline. Earthquake Exposure Sound Practices. I. Purpose and Scope. No: B-9 Date: February 2013

Guideline Subject: No: B-9 Date: February 2013 I. Purpose and Scope Catastrophic losses from exposure to earthquakes may pose a significant threat to the financial wellbeing of many Property & Casualty

Guideline Subject: No: B-9 Date: February 2013 I. Purpose and Scope Catastrophic losses from exposure to earthquakes may pose a significant threat to the financial wellbeing of many Property & Casualty

MANAGE RISK WORLDWIDE

MANAGE RISK WORLDWIDE Zurich International Programs Corporate customers At Zurich, we re proud of our ability to help protect businesses that operate internationally. For nearly 40 years, we have built

MANAGE RISK WORLDWIDE Zurich International Programs Corporate customers At Zurich, we re proud of our ability to help protect businesses that operate internationally. For nearly 40 years, we have built

An Actuarial Evaluation of the Insurance Limits Buying Decision

An Actuarial Evaluation of the Insurance Limits Buying Decision Joe Wieligman Client Executive VP Hylant Travis J. Grulkowski Principal & Consulting Actuary Milliman, Inc. WWW.CHICAGOLANDRISKFORUM.ORG

An Actuarial Evaluation of the Insurance Limits Buying Decision Joe Wieligman Client Executive VP Hylant Travis J. Grulkowski Principal & Consulting Actuary Milliman, Inc. WWW.CHICAGOLANDRISKFORUM.ORG

Catastrophe Risk Engineering Solutions

Catastrophe Risk Engineering Solutions Catastrophes, whether natural or man-made, can damage structures, disrupt process flows and supply chains, devastate a workforce, and financially cripple a company

Catastrophe Risk Engineering Solutions Catastrophes, whether natural or man-made, can damage structures, disrupt process flows and supply chains, devastate a workforce, and financially cripple a company

The Role of ERM in Reinsurance Decisions

The Role of ERM in Reinsurance Decisions Abbe S. Bensimon, FCAS, MAAA ERM Symposium Chicago, March 29, 2007 1 Agenda A Different Framework for Reinsurance Decision-Making An ERM Approach for Reinsurance

The Role of ERM in Reinsurance Decisions Abbe S. Bensimon, FCAS, MAAA ERM Symposium Chicago, March 29, 2007 1 Agenda A Different Framework for Reinsurance Decision-Making An ERM Approach for Reinsurance

JLT MERGERS & ACQUISITIONS GROUP. Fund Liability, Transactional Risks, Due Diligence, Operational Risk Solutions

JLT MERGERS & ACQUISITIONS GROUP Fund Liability, Transactional Risks, Due Diligence, Operational Risk Solutions 2 WHO IS JLT? JLT Group is one of the world s five largest global brokers, a leading provider

JLT MERGERS & ACQUISITIONS GROUP Fund Liability, Transactional Risks, Due Diligence, Operational Risk Solutions 2 WHO IS JLT? JLT Group is one of the world s five largest global brokers, a leading provider

ERM and ORSA Assuring a Necessary Level of Risk Control

ERM and ORSA Assuring a Necessary Level of Risk Control Dave Ingram, MAAA, FSA, CERA, FRM, PRM Chair of IAA Enterprise & Financial Risk Committee Executive Vice President, Willis Re September, 2012 1 DISCLAIMER

ERM and ORSA Assuring a Necessary Level of Risk Control Dave Ingram, MAAA, FSA, CERA, FRM, PRM Chair of IAA Enterprise & Financial Risk Committee Executive Vice President, Willis Re September, 2012 1 DISCLAIMER

Insurance Solutions for the Energy Industry

Insurance Solutions for the Energy Industry Chubb offers a full spectrum of insurance products designed to meet the needs of the energy industry. As the world s population continues to increase, so too

Insurance Solutions for the Energy Industry Chubb offers a full spectrum of insurance products designed to meet the needs of the energy industry. As the world s population continues to increase, so too

Results of Lockton s 2018 risk management survey

Results of Lockton s 2018 risk management survey Risk managers spending more time on emerging risks, claim issues, and contract reviews Ryan Brown SVP, Client Advocate 314.812.3241 rbrown@lockton.com According

Results of Lockton s 2018 risk management survey Risk managers spending more time on emerging risks, claim issues, and contract reviews Ryan Brown SVP, Client Advocate 314.812.3241 rbrown@lockton.com According

Insurance and Financial Services

Insurance and Financial Services 2016 1 Risk Transfer gives you the tools to grow and the resources to mitigate your costs. 2016 2 Your Team of Industry Experts Risk Transfer Insurance Agency is a full

Insurance and Financial Services 2016 1 Risk Transfer gives you the tools to grow and the resources to mitigate your costs. 2016 2 Your Team of Industry Experts Risk Transfer Insurance Agency is a full

Catastrophe Risk Modelling. Foundational Considerations Regarding Catastrophe Analytics

Catastrophe Risk Modelling Foundational Considerations Regarding Catastrophe Analytics What are Catastrophe Models? Computer Programs Tools that Quantify and Price Risk Mathematically Represent the Characteristics

Catastrophe Risk Modelling Foundational Considerations Regarding Catastrophe Analytics What are Catastrophe Models? Computer Programs Tools that Quantify and Price Risk Mathematically Represent the Characteristics

Client Risk Solutions Going beyond insurance. Risk solutions for Financial Institutions. Start

Client Risk Solutions Going beyond insurance Risk solutions for Financial Institutions Start Partnering to Reduce Risk Financial Institutions compete vigorously to maintain profitability and deliver superior

Client Risk Solutions Going beyond insurance Risk solutions for Financial Institutions Start Partnering to Reduce Risk Financial Institutions compete vigorously to maintain profitability and deliver superior

Retailer Risk: The Tipping Point IND019

Speakers: Retailer Risk: The Tipping Point IND019 Carol L. Murphy, Managing Director, Aon Risk Solutions Maggie Biggs, Director, Risk & Insurance, PetSmart Lé Andra Holly, Senior Manager, Risk Management,

Speakers: Retailer Risk: The Tipping Point IND019 Carol L. Murphy, Managing Director, Aon Risk Solutions Maggie Biggs, Director, Risk & Insurance, PetSmart Lé Andra Holly, Senior Manager, Risk Management,

The Hartford Financial Services Group

May 23, 2006 Investor Day The Hartford Financial Services Group Enterprise Risk Management David Johnson Executive Vice President Chief Financial Officer The Hartford Financial Services Group, Inc. Safe

May 23, 2006 Investor Day The Hartford Financial Services Group Enterprise Risk Management David Johnson Executive Vice President Chief Financial Officer The Hartford Financial Services Group, Inc. Safe

NAIC ORSA: A Practical Guide to the DOI s First Year Reviews

ZZ NAIC ORSA: A Practical Guide to the DOI s First Year Reviews Eli Russo Sherry Flippo NAIC 2 Attention APIR, PIR, or SPIR Designees This presentation is pre-qualified for NAIC Designation Renewal Credits

ZZ NAIC ORSA: A Practical Guide to the DOI s First Year Reviews Eli Russo Sherry Flippo NAIC 2 Attention APIR, PIR, or SPIR Designees This presentation is pre-qualified for NAIC Designation Renewal Credits

CAPTIVES December 1, 2015

CAPTIVES 101 - December 1, 2015 Peter Jones Captive Management Initiatives, Ltd. Managing Director Sean Rider Willis North America, Inc. Managing Director Julie Robertson Honigman Miller Schwartz and Cohn

CAPTIVES 101 - December 1, 2015 Peter Jones Captive Management Initiatives, Ltd. Managing Director Sean Rider Willis North America, Inc. Managing Director Julie Robertson Honigman Miller Schwartz and Cohn

GUIDELINE ON ENTERPRISE RISK MANAGEMENT

GUIDELINE ON ENTERPRISE RISK MANAGEMENT Insurance Authority Table of Contents Page 1. Introduction 1 2. Application 2 3. Overview of Enterprise Risk Management (ERM) Framework and 4 General Requirements

GUIDELINE ON ENTERPRISE RISK MANAGEMENT Insurance Authority Table of Contents Page 1. Introduction 1 2. Application 2 3. Overview of Enterprise Risk Management (ERM) Framework and 4 General Requirements

Tokio Marine Group s Growth Strategies

Tokio Marine Group s Growth Strategies Overview of the Management Strategies 25 Group CFO on Tokio Marine Group s Capital Strategy 27 Group CRO on Tokio Marine Group s Risk Management 29 Group Synergies

Tokio Marine Group s Growth Strategies Overview of the Management Strategies 25 Group CFO on Tokio Marine Group s Capital Strategy 27 Group CRO on Tokio Marine Group s Risk Management 29 Group Synergies

2017 MARKET REVIEW AND FORECAST

2017 MARKET REVIEW AND FORECAST SAFEGUARDING YOUR SUCCESS Executive Summary If 2016 taught us anything, the lesson would be not to rely on data for which there is no method of accounting. Put another way:

2017 MARKET REVIEW AND FORECAST SAFEGUARDING YOUR SUCCESS Executive Summary If 2016 taught us anything, the lesson would be not to rely on data for which there is no method of accounting. Put another way:

Statement of Guidance for Licensees seeking approval to use an Internal Capital Model ( ICM ) to calculate the Prescribed Capital Requirement ( PCR )

to calculate the Prescribed Capital Requirement ( PCR )") MAY 2016 Statement of Guidance for Licensees seeking approval to use an Internal Capital Model ( ICM ) to calculate the Prescribed Capital Requirement ( PCR ) 1 Table of Contents 1 STATEMENT OF OBJECTIVES...

MAY 2016 Statement of Guidance for Licensees seeking approval to use an Internal Capital Model ( ICM ) to calculate the Prescribed Capital Requirement ( PCR ) 1 Table of Contents 1 STATEMENT OF OBJECTIVES...

Client Risk Solutions Going beyond insurance. Risk solutions for Retail. Start

Client Risk Solutions Going beyond insurance Risk solutions for Retail Start Partnering to Reduce Risk Retail companies compete vigorously to deliver superior service to customers with diverse and everchanging

Client Risk Solutions Going beyond insurance Risk solutions for Retail Start Partnering to Reduce Risk Retail companies compete vigorously to deliver superior service to customers with diverse and everchanging

ENTERPRISE RISK MANAGEMENT (ERM) The Conceptual Framework

The Conceptual Framework") ENTERPRISE RISK MANAGEMENT (ERM) The Conceptual Framework ENTERPRISE RISK MANAGEMENT (ERM) ERM Definition The Conceptual Frameworks: CAS and COSO Risk Categories Implementing ERM Why ERM? ERM Maturity

ENTERPRISE RISK MANAGEMENT (ERM) The Conceptual Framework ENTERPRISE RISK MANAGEMENT (ERM) ERM Definition The Conceptual Frameworks: CAS and COSO Risk Categories Implementing ERM Why ERM? ERM Maturity

The Role of the Captive Manager

The Role of the Captive Manager Linda Danna Senior Vice President Marsh Management Services, Inc. Charleston, SC Conception What is a Captive? An insurance vehicle formed by an organization, not otherwise

The Role of the Captive Manager Linda Danna Senior Vice President Marsh Management Services, Inc. Charleston, SC Conception What is a Captive? An insurance vehicle formed by an organization, not otherwise

Sandell Re Ltd. Financial Condition Report For the twelve month (12) period ending 31st December 2016

period ending 31st December 2016") Sandell Re Ltd Financial Condition Report For the twelve month (12) period ending 31st December 2016 Sandell Re Ltd. (the Company ) was incorporated in Bermuda on 18th December 2014, and was licensed as

Sandell Re Ltd Financial Condition Report For the twelve month (12) period ending 31st December 2016 Sandell Re Ltd. (the Company ) was incorporated in Bermuda on 18th December 2014, and was licensed as

Tuesday, March 17, 2015 Houston, TX. 3:45 5:00 p.m. CAPTIVATING RISK: ART MARKET AND CAPTIVE SOLUTIONS

Tuesday, March 17, 2015 Houston, TX 3:45 5:00 p.m. : ART MARKET AND CAPTIVE SOLUTIONS Presented by Michael O Neill, CPCU, ARM President and CEO American Contractors Insurance Group Many companies look

Tuesday, March 17, 2015 Houston, TX 3:45 5:00 p.m. : ART MARKET AND CAPTIVE SOLUTIONS Presented by Michael O Neill, CPCU, ARM President and CEO American Contractors Insurance Group Many companies look

Advances in Catastrophe Modeling Primary Insurance Perspective

Advances in Catastrophe Modeling Primary Insurance Perspective Jon Ward May 2015 The Underwriter must be Empowered The foundational element of our industry is underwriting A model will never replace the

Advances in Catastrophe Modeling Primary Insurance Perspective Jon Ward May 2015 The Underwriter must be Empowered The foundational element of our industry is underwriting A model will never replace the

C5: THE EVOLVING USE OF ENTERPRISE RISK CAPTIVES (ERCs) SIIA NATIONAL CONFERENCE

SIIA NATIONAL CONFERENCE") C5: THE EVOLVING USE OF ENTERPRISE RISK CAPTIVES (ERCs) SIIA NATIONAL CONFERENCE Jeffrey K. Simpson Attorney Gordon, Fournaris & Mammarella, PA 1925 Lovering Avenue Wilmington, DE 19806 302-652-2900 JSimpson@Gfmlaw.com

C5: THE EVOLVING USE OF ENTERPRISE RISK CAPTIVES (ERCs) SIIA NATIONAL CONFERENCE Jeffrey K. Simpson Attorney Gordon, Fournaris & Mammarella, PA 1925 Lovering Avenue Wilmington, DE 19806 302-652-2900 JSimpson@Gfmlaw.com

Preparing for a Successful Reinsurance Meeting

Preparing for a Successful Reinsurance Meeting Tuesday, September 24, 2013, 1:00 p.m. David Thomas Managing Director Guy Carpenter & Company, LLC Philadelphia, Pa. David Thomas is a managing director in

Preparing for a Successful Reinsurance Meeting Tuesday, September 24, 2013, 1:00 p.m. David Thomas Managing Director Guy Carpenter & Company, LLC Philadelphia, Pa. David Thomas is a managing director in

The role of an actuary in a Policy Administration System implementation

The role of an actuary in a Policy Administration System implementation Abstract Benefits of a New Policy Administration System (PAS) Insurance is a service and knowledgebased business, which means that

The role of an actuary in a Policy Administration System implementation Abstract Benefits of a New Policy Administration System (PAS) Insurance is a service and knowledgebased business, which means that

Alternative Regulatory Structures for Pools What If Being A JPA Isn t Enough?

Alternative Regulatory Structures for Pools What If Being A JPA Isn t Enough? Patrick Theriault, Managing Director, SRS Shawn Bubb, Director of Insurance Services, MSGIA Joel Kress, Underwriting Manager,

Alternative Regulatory Structures for Pools What If Being A JPA Isn t Enough? Patrick Theriault, Managing Director, SRS Shawn Bubb, Director of Insurance Services, MSGIA Joel Kress, Underwriting Manager,

LLOYD S MINIMUM STANDARDS

LLOYD S MINIMUM STANDARDS Ms1.5 - EXPOSURE MANAGEMENT October 2015 1 Ms1.5 - EXPOSURE MANAGEMENT UNDERWRITING MANAGEMENT PRINCIPLES, MINIMUM STANDARDS AND REQUIREMENTS These are statements of business

LLOYD S MINIMUM STANDARDS Ms1.5 - EXPOSURE MANAGEMENT October 2015 1 Ms1.5 - EXPOSURE MANAGEMENT UNDERWRITING MANAGEMENT PRINCIPLES, MINIMUM STANDARDS AND REQUIREMENTS These are statements of business

Building Actuarial Cost Models from Health Care Claims Data for Strategic Decision-Making. Introduction. William Bednar, FSA, FCA, MAAA

Building Actuarial Cost Models from Health Care Claims Data for Strategic Decision-Making William Bednar, FSA, FCA, MAAA Introduction Health care spending across the country generates billions of claim

Building Actuarial Cost Models from Health Care Claims Data for Strategic Decision-Making William Bednar, FSA, FCA, MAAA Introduction Health care spending across the country generates billions of claim

Exam ERM-GI. Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES. Recognized by the Canadian Institute of Actuaries.

Enterprise Risk Management General Insurance Extension Exam ERM-GI Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total

Enterprise Risk Management General Insurance Extension Exam ERM-GI Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total

Managing Risk For Financially Successful Families

Managing Risk For Financially Successful Families Guide To Finding The Right Insurance Partners Personal Risk Services Contents Executive Summary 03 What to Look for in a Family Insurance Team 03 Who will

Managing Risk For Financially Successful Families Guide To Finding The Right Insurance Partners Personal Risk Services Contents Executive Summary 03 What to Look for in a Family Insurance Team 03 Who will

Aon Insurance Managers Bermuda

Aon Risk Solutions Issue 1 2018 Aon Insurance Managers Bermuda A Message from Anup Seth Welcome to the inaugural edition of the Aon Insurance Managers In this Issue (Bermuda) newsletter. As we continue

Aon Risk Solutions Issue 1 2018 Aon Insurance Managers Bermuda A Message from Anup Seth Welcome to the inaugural edition of the Aon Insurance Managers In this Issue (Bermuda) newsletter. As we continue

An Overview of Cyber Insurance at AIG

An Overview of Cyber Insurance at AIG Michael Lee, MBA Cyber Business Development Manager AIG 2018 Brittney Mishler, ARM Cyber Casualty Underwriting Specialist AIG Cyber Insurance It s a peril, not a product

An Overview of Cyber Insurance at AIG Michael Lee, MBA Cyber Business Development Manager AIG 2018 Brittney Mishler, ARM Cyber Casualty Underwriting Specialist AIG Cyber Insurance It s a peril, not a product

Client Risk Solutions Going beyond insurance. Risk solutions for Energy. Oil, Gas and Petrochemical. Start

Client Risk Solutions Going beyond insurance Risk solutions for Energy Oil, Gas and Petrochemical Start Partnering to Reduce Risk AIG s Client Risk Solutions (CRS) partners with organizations to build

Client Risk Solutions Going beyond insurance Risk solutions for Energy Oil, Gas and Petrochemical Start Partnering to Reduce Risk AIG s Client Risk Solutions (CRS) partners with organizations to build

May 2015 DISCUSSION DRAFT For Illustrative Purposes Only Content NOT Reviewed or Approved by the Actuarial Standards Board DISCUSSION DRAFT

DISCUSSION DRAFT Capital Adequacy Assessment for Insurers Developed by the Enterprise Risk Management Committee of the Actuarial Standards Board TABLE OF CONTENTS Transmittal Memorandum iv STANDARD OF

DISCUSSION DRAFT Capital Adequacy Assessment for Insurers Developed by the Enterprise Risk Management Committee of the Actuarial Standards Board TABLE OF CONTENTS Transmittal Memorandum iv STANDARD OF

Energize Your Enterprise Risk Management

Energize Your Enterprise Risk Management Presented By Mark Caiazzo, CISA, CISM, CRISC Tammy Michaud, CPA May 15, 2017 Reviewed: Agenda Enterprise Risk Management Defined Benefits of ERM Key Components

Energize Your Enterprise Risk Management Presented By Mark Caiazzo, CISA, CISM, CRISC Tammy Michaud, CPA May 15, 2017 Reviewed: Agenda Enterprise Risk Management Defined Benefits of ERM Key Components

NAIC OWN RISK AND SOLVENCY ASSESSMENT (ORSA) GUIDANCE MANUAL

GUIDANCE MANUAL") NAIC OWN RISK AND SOLVENCY ASSESSMENT (ORSA) GUIDANCE MANUAL Created by the NAIC Group Solvency Issues Working Group Of the Solvency Modernization Initiatives (EX) Task Force 2011 National Association

NAIC OWN RISK AND SOLVENCY ASSESSMENT (ORSA) GUIDANCE MANUAL Created by the NAIC Group Solvency Issues Working Group Of the Solvency Modernization Initiatives (EX) Task Force 2011 National Association

Fundamentals of Catastrophe Modeling. CAS Ratemaking & Product Management Seminar Catastrophe Modeling Workshop March 15, 2010

Fundamentals of Catastrophe Modeling CAS Ratemaking & Product Management Seminar Catastrophe Modeling Workshop March 15, 2010 1 ANTITRUST NOTICE The Casualty Actuarial Society is committed to adhering

Fundamentals of Catastrophe Modeling CAS Ratemaking & Product Management Seminar Catastrophe Modeling Workshop March 15, 2010 1 ANTITRUST NOTICE The Casualty Actuarial Society is committed to adhering

ROI CASE STUDY SPSS INFINITY PROPERTY & CASUALTY

ROI CASE STUDY SPSS INFINITY PROPERTY & CASUALTY THE BOTTOM LINE Infinity Property & Casualty Corporation (IPACC) deployed SPSS to reduce its payments on fraudulent claims and improve its ability to collect

ROI CASE STUDY SPSS INFINITY PROPERTY & CASUALTY THE BOTTOM LINE Infinity Property & Casualty Corporation (IPACC) deployed SPSS to reduce its payments on fraudulent claims and improve its ability to collect

Aon Hewitt Solutions. Curtiss Wright. June 2, 2014 Meeting. Risk. Reinsurance. Human Resources.

Aon Hewitt Solutions Curtiss Wright June 2, 2014 Meeting Risk. Reinsurance. Human Resources. Aon overview Aon was founded in 1979 although our history, through mergers and acquisitions, dates back to the

Aon Hewitt Solutions Curtiss Wright June 2, 2014 Meeting Risk. Reinsurance. Human Resources. Aon overview Aon was founded in 1979 although our history, through mergers and acquisitions, dates back to the

A pioneer in ILS solutions

A pioneer in ILS solutions Insurance Linked Securities from We combine superior insurance and investment expertise About us Secquaero Advisors Ltd (Secquaero) is a specialist advisory firm in the areas

A pioneer in ILS solutions Insurance Linked Securities from We combine superior insurance and investment expertise About us Secquaero Advisors Ltd (Secquaero) is a specialist advisory firm in the areas

Client Risk Solutions Going beyond insurance. Overview

Client Risk Solutions Going beyond insurance Overview For nearly a century AIG has handled millions of business insurance claims throughout the world, giving us a vast storehouse of data and insights across

Client Risk Solutions Going beyond insurance Overview For nearly a century AIG has handled millions of business insurance claims throughout the world, giving us a vast storehouse of data and insights across

Meeting the challenges of the changing actuarial role. Actuarial Transformation in property-casualty insurers

Meeting the challenges of the changing actuarial role Actuarial Transformation in property-casualty insurers 1 As companies seek to drive profitable growth, both short term and long term, increasing the

Meeting the challenges of the changing actuarial role Actuarial Transformation in property-casualty insurers 1 As companies seek to drive profitable growth, both short term and long term, increasing the

Cover title 26/29 Risk appetite gains momentum 45 light white in a changing world

Cover title 26/29 Risk appetite gains momentum 45 light white in a changing world Cover subtitle 12/15 65 medium black 2017/2018 Global Reinsurance and Risk Appetite Survey Report How is risk appetite

Cover title 26/29 Risk appetite gains momentum 45 light white in a changing world Cover subtitle 12/15 65 medium black 2017/2018 Global Reinsurance and Risk Appetite Survey Report How is risk appetite

The Internet of Everything: Building Cyber Resilience in a Connected World

The Internet of Everything: Building Cyber Resilience in a Connected World The Internet of Things (IoT) is everywhere, ushering in a technological revolution at lightning speed. According to an Oliver

The Internet of Everything: Building Cyber Resilience in a Connected World The Internet of Things (IoT) is everywhere, ushering in a technological revolution at lightning speed. According to an Oliver

Everything You Need to Know about the PCS Catastrophe Loss Index

Everything You Need to Know about the Since 1949, the property/casualty insurance industry has relied on catastrophe loss estimates from PCS and its predecessor organizations to set catastrophe reserves

Everything You Need to Know about the Since 1949, the property/casualty insurance industry has relied on catastrophe loss estimates from PCS and its predecessor organizations to set catastrophe reserves

Guidance Note. Securitization. March Ce document est aussi disponible en français. Revised in October 2018

Guidance Note Securitization March 2018 Revised in October 2018 Ce document est aussi disponible en français. Applicability The Guidance Note: Securitization (Guidance Note) is for use by all credit unions

Guidance Note Securitization March 2018 Revised in October 2018 Ce document est aussi disponible en français. Applicability The Guidance Note: Securitization (Guidance Note) is for use by all credit unions

Non-physical Damage Business Interruption (NDBI) Innovative Earnings Protection

Innovative Earnings Protection") Non-physical Damage Business Interruption (NDBI) Innovative Earnings Protection Agenda Introductions It s a Dangerous World A Framework for Evaluating Corporate Risks Limitations of Traditional Insurance

Non-physical Damage Business Interruption (NDBI) Innovative Earnings Protection Agenda Introductions It s a Dangerous World A Framework for Evaluating Corporate Risks Limitations of Traditional Insurance

ALLIANZ MULTINATIONAL YOUR WORLD IS OUR BUSINESS

ALLIANZ MULTINATIONAL YOUR WORLD IS OUR BUSINESS ALLIANZ MULTINATIONAL YOUR WORLD IS OUR BUSINESS ABOUT ALLIANZ MULTINATIONAL In a world where business and trade opportunities are constantly evolving,

ALLIANZ MULTINATIONAL YOUR WORLD IS OUR BUSINESS ALLIANZ MULTINATIONAL YOUR WORLD IS OUR BUSINESS ABOUT ALLIANZ MULTINATIONAL In a world where business and trade opportunities are constantly evolving,

BERMUDA INSURANCE (GROUP SUPERVISION) RULES 2011 BR 76 / 2011

RULES 2011 BR 76 / 2011") QUO FA T A F U E R N T BERMUDA INSURANCE (GROUP SUPERVISION) RULES 2011 BR 76 / 2011 TABLE OF CONTENTS 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 Citation and commencement PART 1 GROUP RESPONSIBILITIES

QUO FA T A F U E R N T BERMUDA INSURANCE (GROUP SUPERVISION) RULES 2011 BR 76 / 2011 TABLE OF CONTENTS 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 Citation and commencement PART 1 GROUP RESPONSIBILITIES

Solvency II Standard Formula: Consideration of non-life reinsurance

Solvency II Standard Formula: Consideration of non-life reinsurance Under Solvency II, insurers have a choice of which methods they use to assess risk and capital. While some insurers will opt for the

Solvency II Standard Formula: Consideration of non-life reinsurance Under Solvency II, insurers have a choice of which methods they use to assess risk and capital. While some insurers will opt for the

DISCUSSION ITEM UPDATE ON RISK SERVICES AND FIAT LUX CAPTIVE INSURANCE COMPANY EXECUTIVE SUMMARY

C5 Office of the President TO MEMBERS OF THE COMPLIANCE AND AUDIT : For Meeting of DISCUSSION ITEM UPDATE ON RISK SERVICES AND FIAT LUX CAPTIVE INSURANCE COMPANY EXECUTIVE SUMMARY The Office of Risk Services,

C5 Office of the President TO MEMBERS OF THE COMPLIANCE AND AUDIT : For Meeting of DISCUSSION ITEM UPDATE ON RISK SERVICES AND FIAT LUX CAPTIVE INSURANCE COMPANY EXECUTIVE SUMMARY The Office of Risk Services,

Streamline and integrate your claims processing

Increase flexibility Reduce costs Expedite claims Streamline and integrate your claims processing DXC Insurance RISKMASTERTM For corporate claims and self-insured organizations DXC Insurance RISKMASTER

Increase flexibility Reduce costs Expedite claims Streamline and integrate your claims processing DXC Insurance RISKMASTERTM For corporate claims and self-insured organizations DXC Insurance RISKMASTER

Domestic Casualty & Property State of the Market

Domestic Casualty & Property State of the Market Lance J. Ewing, Vice President September 20, 2012 THANK YOU 2 DISCLAIMER Certain statements provided herein are based solely on the opinions of American

Domestic Casualty & Property State of the Market Lance J. Ewing, Vice President September 20, 2012 THANK YOU 2 DISCLAIMER Certain statements provided herein are based solely on the opinions of American

Large Limits Playbook. Building Successful Partnerships with Large Limit Clients

Large Limits Playbook Building Successful Partnerships with Large Limit Clients Unlocking $2.5 Billion in Capacity As organizations grow, so does their need for quality, uniform insurance coverage limits.

Large Limits Playbook Building Successful Partnerships with Large Limit Clients Unlocking $2.5 Billion in Capacity As organizations grow, so does their need for quality, uniform insurance coverage limits.

Captive Insurance Company FAQs

Captive Insurance Company FAQs What is a Captive Insurance Company? A captive is a closely held company in the business of insurance owned and controlled by one or more entities that are the exclusive

Captive Insurance Company FAQs What is a Captive Insurance Company? A captive is a closely held company in the business of insurance owned and controlled by one or more entities that are the exclusive

Business Continuity Management and ERM

Business Continuity Management and ERM Partnership for Emergency Planning Kansas City Marshall Toburen GRC Strategist ERM, ORM, 3PM RSA A division of EMC 2 June 18, 2014 1 Agenda Intro State of ERM Today

Business Continuity Management and ERM Partnership for Emergency Planning Kansas City Marshall Toburen GRC Strategist ERM, ORM, 3PM RSA A division of EMC 2 June 18, 2014 1 Agenda Intro State of ERM Today

A Captive Primer: What they are and how they work. Educate Evaluate Elevate

A Captive Primer: What they are and how they work Educate Evaluate Elevate Presentation Objectives History of captives & what they are How captives are used & what makes a good prospect The Captive Wrap

A Captive Primer: What they are and how they work Educate Evaluate Elevate Presentation Objectives History of captives & what they are How captives are used & what makes a good prospect The Captive Wrap

PC2: Introduction to Captives

PC2: Introduction to Captives Martin Eveleigh Chairman, Atlas Insurance Management Kirk Mooneyham Managing Director, Wilmington Trust SP Services, Inc. What is a Captive Insurance Company? A captive insurance

PC2: Introduction to Captives Martin Eveleigh Chairman, Atlas Insurance Management Kirk Mooneyham Managing Director, Wilmington Trust SP Services, Inc. What is a Captive Insurance Company? A captive insurance

Captive Insurance Arrangements For Small Companies

Captive Insurance Arrangements For Small Companies Ronald H. Snyder ZERMATT INSURANCE GROUP, INC. 101 Convention Center Dr. Ste P-109 Las Vegas, NV 84109 What is a Captive Insurance Company? A Captive

Captive Insurance Arrangements For Small Companies Ronald H. Snyder ZERMATT INSURANCE GROUP, INC. 101 Convention Center Dr. Ste P-109 Las Vegas, NV 84109 What is a Captive Insurance Company? A Captive

Project Theft Management,

Project Theft Management, by applying best practises of Project Risk Management Philip Rosslee, BEng. PrEng. MBA PMP PMO Projects South Africa PMO Projects Group www.pmo-projects.co.za philip.rosslee@pmo-projects.com

Project Theft Management, by applying best practises of Project Risk Management Philip Rosslee, BEng. PrEng. MBA PMP PMO Projects South Africa PMO Projects Group www.pmo-projects.co.za philip.rosslee@pmo-projects.com

Casualty Catastrophes Asia Pacific Insurance Conference October 2017

Casualty Catastrophes Asia Pacific Insurance Conference October 2017 Cameron Green Chief Executive Officer Willis Re Australia Asia Pacific Management Team Global Casualty Practice Group Background 3 4

Casualty Catastrophes Asia Pacific Insurance Conference October 2017 Cameron Green Chief Executive Officer Willis Re Australia Asia Pacific Management Team Global Casualty Practice Group Background 3 4

Long-term care services. Strategies and tools to manage risk and build your business in long-term care insurance

Long-term care services Strategies and tools to manage risk and build your business in long-term care insurance A commitment to long-term care Whether you re entering new markets, developing new products,

Long-term care services Strategies and tools to manage risk and build your business in long-term care insurance A commitment to long-term care Whether you re entering new markets, developing new products,

Exam ERM-ILA. Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES

Enterprise Risk Management Individual Life & Annuities Extension Exam ERM-ILA Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination

Enterprise Risk Management Individual Life & Annuities Extension Exam ERM-ILA Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination

The Real World: Dealing With Parameter Risk. Alice Underwood Senior Vice President, Willis Re March 29, 2007

The Real World: Dealing With Parameter Risk Alice Underwood Senior Vice President, Willis Re March 29, 2007 Agenda 1. What is Parameter Risk? 2. Practical Observations 3. Quantifying Parameter Risk 4.

The Real World: Dealing With Parameter Risk Alice Underwood Senior Vice President, Willis Re March 29, 2007 Agenda 1. What is Parameter Risk? 2. Practical Observations 3. Quantifying Parameter Risk 4.

Solving Cyber Risk. Security Metrics and Insurance. Jason Christopher March 2017

Solving Cyber Risk Security Metrics and Insurance Jason Christopher March 2017 How We Try to Address Cyber Risk What is Cyber Risk? Definitions Who should be concerned? Key categories of cyber risk Cyber

Solving Cyber Risk Security Metrics and Insurance Jason Christopher March 2017 How We Try to Address Cyber Risk What is Cyber Risk? Definitions Who should be concerned? Key categories of cyber risk Cyber