Wednesday, March 5, 2014 Houston, TX. 1:30 2:45 p.m. IMPROVING RISK MANAGEMENT AND INSURANCE PLACEMENTS USING ANALYTICS

|

|

|

- Lee Francis

- 5 years ago

- Views:

Transcription

Chan Senior Vice")

1 Wednesday, March 5, 2014 Houston, TX 1:30 2:45 p.m. IMPROVING RISK MANAGEMENT AND INSURANCE PLACEMENTS USING ANALYTICS Presented by Joe Beesack Senior Vice President, Alternative Risk Solutions Practice Willis Calgary William (Bill) Chan Senior Vice President, Alternative Risk Solutions Practice Willis Calgary The quality of a marketing submission can impact the interest of the underwriter in the account and can drive the breadth of coverage under and cost-effectiveness of the program. Often, when preparing submissions for marketing their accounts, companies rely on traditional peer benchmarking. This session will provide an overview of how to use a specific company s financials to help model the optimal insurance program for the company. Copyright 2014 International Risk Management Institute, Inc. 1

2 Notes This file is set up for duplexed printing. Therefore, there are pages that are intentionally left blank. If you print this file, we suggest that you set your printer to duplex. 2

3 Joe Beesack Senior Vice President, Alternative Risk Solutions Practice Willis Calgary Joe Beesack s primary role is to serve as a practice leader for Statistical and Quantitative Analysis. At the strategic level, he provides statistical, analytical, and financial analysis for projects that aid our clients in making informed decisions to establish the most appropriate risk retention and risk transfer structure to suit their unique needs and objectives. At the operational level, his specific area of specialization is in the creation of computerized applications that reflect the complexities of sophisticated risk financing quantification needs. He has developed numerous analytical tools to enhance the practice s ability to deliver quick and accurate analysis, as well as developed complex conceptual risk quantification models. Prior to joining Willis, Mr. Beesack was the chief analytical officer and senior vice president for all quantitative risk analysis for Aon Reed Stenhouse Inc., specializing in alternative risk financing mechanisms. He completed his honors bachelor of science degree in mathematics at McMaster University, immediately followed by a bachelor of education degree from the University of Windsor, and subsequently obtained his certificate in Canadian Risk Management. William (Bill) Chan Senior Vice President, Alternative Risk Solutions Practice Willis Calgary Bill Chan is also a charter holder with the Chartered Financial Analyst Institute. Mr. Chan began his strategic planning and risk management career with a multinational oil and gas company in Prior to his work in risk management, he worked in strategic planning, statistics, and econometrics. Over the years, his clients have included major corporations from the oil and gas, power generation and distribution, entertainment, hospitality, home building, and agriculture industries, as well as governments at the federal, provincial, territorial, and municipal levels. He provides analysis of risk and the impact it has on a company s financials and can help assess a variety of alternative solutions and risk management tools beyond insurance. Mr. Chan has published articles in risk management trade journals and has spoken at numerous seminars, including those presented by the Institute of Corporate Directors, CRIMS, and SARIMS, in addition to guest lecturing at the University of Calgary. He also teaches risk financing at the University of Calgary, continuing education, and has taught risk management at the Haskayne School of Business. Mr. Chan holds an undergraduate degree in political science, a master s degree in economics, and an M.B.A. 3

4 Notes This file is set up for duplexed printing. Therefore, there are pages that are intentionally left blank. If you print this file, we suggest that you set your printer to duplex. 4

5 Improving Risk M anagement and Insurance Placements Using Analytics Presented By: 1 Joe Beesack Senior Vice President Alternative Risk Solutions Practice Willis Calgary William (Bill) Chan Senior Vice President Alternative Risk Solutions Practice Willis Calgary IRMI.com Improving Risk Management and Insurance Placements Using Analytics IRMI Energy Conference March 4-6, 2014 Houston, TX 5

Analytics for captives Page 1 Analytics and the risk management decision process")

6 Agenda Analytics and the risk management decision process Analytics for insurance purchasing Analytics in enterprise risk management (ERM) Analytics for captives Page 1 Analytics and the risk management decision process Page 2 6

7 How To Think About Risk 1. Understand industry trends, competition and business strategy 2. Define risk tolerance 3. Identify priority exposures and risk scenarios 4. Model loss frequency and severity 5. Quantify Total Cost of Risk for Priority Risks / Define a Crisis 6. Avoidance 7. Mitigation 8. Retention Balance Sheet Captive 9. Transfer To Insurers To Capital or Other Markets R I S K S T R A T E G Y I M P L E M E N T A T I O N Page 3 Analytics The transformation and value derived can be summarized as: Better Decisions Knowledge Information Data The goal is to transform data, through appropriate tools and technologies, to make informed decisions Page 4 7

8 Applications of analytics in risk management: What are my exposures? / What coverages do I need? How much coverage / limit do I need? What is my optimal deductible? How much risk can I assume? Should I access alternative risk solutions? How should I allocate my cost of risk? Page 5 8

9 for insurance purchasing Page 6 Analytics A typical submission to Underwriters addresses these points: Risk Identification Risk Assessment / Quantification / Forecasts Retention Capacity / Loss Forecasts Loss Forecasts / Market Conditions Management knowledge of business and risks Benchmarking with peers What are my exposures? / What coverage do I need? What limits should I buy? What deductible should I have? What is a reasonable range for my premiums? Page 7 9

10 In the context of the insurance purchasing decision: Probabilistic Loss Forecasts can be used to: 1. Evaluate theoretically appropriate attachment points 2. Assess the reasonableness of market quotes 3. Determine appropriate funding levels 4. Determine appropriate annual aggregates 5. Compare total cost of risk for alternative market options 6. Prepare management for the true cost of risk, should soft market pricing be prevalent Page 8 Analytics Example 1: Data available: Company specific loss data Company specific engineering scenario analysis Energy/industry databases Multiple analytical loss models developed to understand and quantify the risk Result: able to demonstrate to markets the low likelihood of event, thereby reducing attachment point without materially increasing premium Page 9 10

11 Example 2: Company loss and exposure data was available for modeling Developed loss model to ascertain appropriate attachment points Compared forecasts to market prices at various attachment points Result: Provided client with a rational basis for program design Lowered total cost of risk for client Page 10 11

12 WITHIN EACH AND EVERY RETENTION Probability Retention 1,000 10,000 25,000 50, , , ,000 1,000,000 2,000,000 25,000,000 of Loss Mean: 195, ,455 1,161,022 1,517,190 1,833,314 2,084,347 2,155,007 2,174,991 2,178,790 2,179,313 Aggregation St. Dev'n: 13,436 72, , , , , , , , ,823 1 Year in: Percentile , ,424 1,157,022 1,511,757 1,822,181 2,055,439 2,115,466 2,123,989 2,124,155 2,124, , ,730 1,218,685 1,603,013 1,950,134 2,234,384 2,317,961 2,332,003 2,332,047 2,332, , ,330 1,252,938 1,653,662 2,026,617 2,342,833 2,441,652 2,465,512 2,466,028 2,466, , ,248 1,275,141 1,693,485 2,080,143 2,419,826 2,528,006 2,557,557 2,560,516 2,560, , ,116 1,338,493 1,791,334 2,227,060 2,629,888 2,769,640 2,820,673 2,824,909 2,824, , ,401 1,391,873 1,873,440 2,338,270 2,785,542 2,973,701 3,058,135 3,073,285 3,073, , ,429 1,408,019 1,897,821 2,375,913 2,837,450 3,034,171 3,130,889 3,150,525 3,150, , ,653 1,431,923 1,928,681 2,420,564 2,899,484 3,121,153 3,225,841 3,250,133 3,250, , ,095 1,444,101 1,948,534 2,450,952 2,941,071 3,177,076 3,286,958 3,316,206 3,316, , ,637 1,458,719 1,975,425 2,486,388 2,994,305 3,230,000 3,343,701 3,394,120 3,394, , ,121 1,496,919 2,051,775 2,578,976 3,163,252 3,394,706 3,554,165 3,619,798 3,619, , ,499 1,622,154 2,210,070 2,894,899 3,560,240 3,892,340 4,208,356 4,480,016 4,518,984 1, EXCESS EACH AND EVERY RETENTION Probability Retention 1,000 10,000 25,000 50, , , ,000 1,000,000 2,000,000 of Loss Mean: 1,983,341 1,431,858 1,018, , ,999 94,966 24,306 4, Aggregation St. Dev'n: 499, , , , , , ,193 64,049 28,243 1 Year in: Percentile 50 1,929,829 1,368, , , , ,132,716 1,567,922 1,134, , ,701 58, ,267,483 1,689,291 1,244, , , , ,358,261 1,776,937 1,322, , , , ,623,127 2,037,785 1,568,520 1,137, , ,133 2, ,869,977 2,269,970 1,793,535 1,358, , , , ,945,293 2,358,368 1,868,747 1,428, , , , ,051,231 2,439,482 1,963,901 1,518,124 1,080, , , ,116,042 2,505,651 2,023,029 1,577,000 1,137, , , ,184,143 2,583,926 2,096,648 1,651,746 1,206, , , ,422,238 2,814,125 2,338,124 1,892,371 1,442, , ,112 51, ,324,845 3,709,884 3,203,934 2,653,887 2,204,671 1,647,822 1,267, , ,000.0 Page 11

13 in Enterprise Risk Management Page 12 Analytics Tools Available Establish The Context Discussions with Client Communicate and Consult Identify Risks Analyze Risks Evaluate Risks Risk Assessment Monitor and Review Risk Assessment Loss Forecasting, Custom Risk Modeling Retention Capacity Analysis Treat Risks Insurance Optimization, Captive Consultation, Risk Mitigation Strategy Page 13 13

14 Discussions with Clients to gain an understanding of the clients : Industry Corporate objectives Position in the energy industry Risk management philosophy and focus (earnings vs cash flow vs profitability; short term vs long term) Risk bearing capacity, tolerance and appetite Page 14 Analytics Analytical Tools: Risk Assessment Probabilistic Loss Forecasting Customized Risk Modeling Risk Bearing Capacity Analysis Captives Page 15 14

15 Risk Assessment What risks do we have? What risks are of a priority concern? What controls do we have in place for those risks? What can we do to mitigate the risks? Part of good corporate governance Page 16 15

1 Negligible Business Objective(s):")

4 Significant 5 Expected (occurs often) Assessment of the risk 5 Catastrophic / Major With treatment measures [As it is now] implemented Risk Underlying")

16 Risk assessment, recruiting, training 5: 4: 3: 2: 1: Time Commitment Control Causes Monitor After Immediate Action Before Contingency Plans 1: 2: 3: 4: 5: P(Event) 1 yr in: ,000,000 Pr 1 yr in: Invest. Cost: 5,000 Paid over: 4 Ann. Benefit: 99,800,000 Ann. Inv. Cost: 1,250 Analytics 16 Risk Assessment Risk Assessment for:abc Company Limited Score Likelihood Score Impact Date: 21-Jun-10 1 Remote (could happen but unlikely) 1 Negligible Business Objective(s): Assessment of the major risks affecting achievement of 2 Unusual (has occurred somewhere) 2 Low ABC Company Limited's growth objectives during the 3 Possible (known to occur occasionally) 3 Moderate next 3 years 4 Probable (known to occur) 4 Significant 5 Expected (occurs often) Assessment of the risk 5 Catastrophic / Major With treatment measures [As it is now] implemented Risk Underlying Triggers Consequences Current Controls Cat Category L I Gross Risk Further Risk Treatment Measures L I Gross Risk No. Vulnerabilities Risk Rank Risk Rank 1 Over-commitment of Acquisition or key client Failure to meet project Surety capacity, Go - No Go, strong 8 Strategy and Risk assessment, recruiting, training resources demand escalates and deadlines and leadership, client surveys policy new major client expectations, loss of future revenue, hiring or promotion of unqualified individuals 2 Emerging markets using Failure to respond to new Loss of market share newer technology entrants to existing Excess capacity markets Competitor analysis Customer feedback 9 Technology / Industry change Likelihood 'Risk Matrix' - Before and After Controls Expected 5 8 Probable 4 8 2, 10, Possible 3 14 Unusual , 17, 18 Control Causes Monitor 6, 7, 10, 12 5, 12 3, 15, 16 4, 7, 9, 11, 18 1, 2, 9 Remote 1 5, 11, Immediate Action 3, 15 1 Contingency Plans Impact Negligible Low Moderate Significant Catastrophic Risk Scores Likelihood Impact Gross Risk Risk Rank Technology / Industry change Analysis by Source of Risk and Stratified by Risk Rank (Before Improvements) Risk No.: 1 Underlying Vulnerabilities: Over-commitment of resources Category: Strategy and policy Triggers: Acquisition or key client demand escalates and new major client Consequences: Failure to meet project deadlines and expectations, loss of future revenue, hiring or promotion of unqualified individuals Before Improvement After Improvement Strategy and policy Products / Services Processes Political / Social People Natural events Investments Likelihood Current Controls: Surety capacity, Go - No Go, strong leadership, client surveys Further Risk Treatment Measures: Responsible: Joe3 Target Date: 1/1/2010 Risk Number: Risk Description: Responsible: Target Date: Last Updated: Cost : Benefit Ratio Event Cost BEFORE Over-commitment of resources Joe3 1 1/1/ : 79, ,000,000,000 Budgeted? Costs Describe investment to complete improvements Capital Cost (Yes/No) Likelihood Impact Budgeted? Approved (Yes/No) (Yes/No) Economic <RR<=25 15<RR<=20 10<RR<=15 5<RR<=10 RR<= Impact Action Deliverables Measure of Success Allocated to Delivery (when) Budget Cost Budget time Event Cost AFTER Page 17

17 Risk Assessment Know: your risks what controls you have in place to mitigate What actions are to be put in place to further mitigate those risks Be prepared to explain these to the market Demonstrates knowledge of the risks you are trying to have insured Page 18 Analytics Analytical Tools: Risk Assessment Probabilistic Loss Forecasting Risk Bearing Capacity Analysis Customized Risk Modeling Captives Page 19 17

18 18 CLAIM AMOUNT ($) Legend Actual Fitted Fitted PERCENTILE Page 20 20

19 19 WITHIN EACH AND EVERY RETENTION Probability Retention 1,000 10,000 25,000 50, , , ,000 1,000,000 2,000,000 25,000,000 of Loss Mean: 195, ,455 1,161,022 1,517,190 1,833,314 2,084,347 2,155,007 2,174,991 2,178,790 2,179,313 Aggregation St. Dev'n: 13,436 72, , , , , , , , ,823 1 Year in: Percentile , ,424 1,157,022 1,511,757 1,822,181 2,055,439 2,115,466 2,123,989 2,124,155 2,124, , ,730 1,218,685 1,603,013 1,950,134 2,234,384 2,317,961 2,332,003 2,332,047 2,332, , ,330 1,252,938 1,653,662 2,026,617 2,342,833 2,441,652 2,465,512 2,466,028 2,466, , ,248 1,275,141 1,693,485 2,080,143 2,419,826 2,528,006 2,557,557 2,560,516 2,560, , ,116 1,338,493 1,791,334 2,227,060 2,629,888 2,769,640 2,820,673 2,824,909 2,824, , ,401 1,391,873 1,873,440 2,338,270 2,785,542 2,973,701 3,058,135 3,073,285 3,073, , ,429 1,408,019 1,897,821 2,375,913 2,837,450 3,034,171 3,130,889 3,150,525 3,150, , ,653 1,431,923 1,928,681 2,420,564 2,899,484 3,121,153 3,225,841 3,250,133 3,250, , ,095 1,444,101 1,948,534 2,450,952 2,941,071 3,177,076 3,286,958 3,316,206 3,316, , ,637 1,458,719 1,975,425 2,486,388 2,994,305 3,230,000 3,343,701 3,394,120 3,394, , ,121 1,496,919 2,051,775 2,578,976 3,163,252 3,394,706 3,554,165 3,619,798 3,619, , ,499 1,622,154 2,210,070 2,894,899 3,560,240 3,892,340 4,208,356 4,480,016 4,518,984 1,000.0 EXCESS EACH AND EVERY RETENTION Probability Retention 1,000 10,000 25,000 50, , , ,000 1,000,000 2,000,000 of Loss Mean: 1,983,341 1,431,858 1,018, , ,999 94,966 24,306 4, Aggregation St. Dev'n: 499, , , , , , ,193 64,049 28,243 1 Year in: Percentile 50 1,929,829 1,368, , , , ,132,716 1,567,922 1,134, , ,701 58, ,267,483 1,689,291 1,244, , , , ,358,261 1,776,937 1,322, , , , ,623,127 2,037,785 1,568,520 1,137, , ,133 2, ,869,977 2,269,970 1,793,535 1,358, , , , ,945,293 2,358,368 1,868,747 1,428, , , , ,051,231 2,439,482 1,963,901 1,518,124 1,080, , , ,116,042 2,505,651 2,023,029 1,577,000 1,137, , , ,184,143 2,583,926 2,096,648 1,651,746 1,206, , , ,422,238 2,814,125 2,338,124 1,892,371 1,442, , ,112 51, ,324,845 3,709,884 3,203,934 2,653,887 2,204,671 1,647,822 1,267, , ,000.0 Page 21

20 Probabilistic Loss Forecasting Understand the underlying data Is it representative of the risk moving forward Agree with the exposure assumptions Agree with the loss assumptions; development, trending Agree with the loss modeling applied Be prepared to articulate this with the markets and be able to discuss pricing in a meaningful and rational basis Page 22 Analytics Analytical Tools: Risk Assessment Probabilistic Loss Forecasting Customized Risk Modeling Risk Bearing Capacity Analysis Captives Page 23 20

21 Custom Risk Modeling Understand the magnitude of potentially severe risks with low likelihood For risks where historical data is not available or not representative of our risks, develop customized, credible loss models of the risk Similar output and application as Probabilistic Loss Forecasts Page 24 21

22 Scenario Based 22 Risk Risk Description Severity Range 1 XYZ has outsourced processing of transactional data to Y Corp. Disgruntled employee of Y erases transactions resulting in legal liability for XYZ Low End of Impact XYZ Corp Risk Register Products Liability High End of Impact Probability of Event (Likelihood Loss Event (x of loss in a out of y given year) years) Frequency 1-a 50.00% b ERASURE OF A SMALL SET OF SPECIFIC 2,500,000 7,500, % TRANSACTIONS 1-c 10.00% d ERASURE OF ONE DAY S TRANSACTIONS FOR A FUND 10,000,000 17,500, % GROUP 1-e 2.00% f ERASURE OF ALL TRANSACTIONS IN A QUARTER FOR A 45,000,000 75,000, % FUND GROUP 1-g 0.40% h 0.20% i 0.10% ,000 x years out of y years Comments Lognormal ( , ) Smoothed Fit Page 25

23 Fitting distributions to the sub-scenarios 1,000 Risk 1: Expected Losses = $2.671M Pr(Loss) < Expected = 88.5% Pr(Loss) > Expected = 11.5% 1, Risk 1: Expected Losses = $2.671M Pr(Loss) < Expected = 88.5% Pr(Loss) > Expected = 11.5% Return Period = Number of Years Between Loss Events (Logarithmic Scale) <--- Higher Freq/Lower Severity Lower Freq/Higher Severity ---> Projected Loss Severity ($Millions) 1-2yr 1-7yr 1-10yr 1-13yr 1-50yr 1-55yr 1-250yr 1-500yr yr Fitted Fitted Severity ($MM) Percentile 1-13yr 1-50yr 1-55yr yr 1-2yr 1-7yr 1-10yr 1-250yr 1-500yr Fitted Page 26

24 Custom Risk Modeling: Conditional relationships Dependency analysis Model predicated on potential paths/outcomes depending on underlying combination of events 24 Outcome 1: 10% 30% Impact A Impact 70% B 20% Impact A Scenario A Outcome 2: 50% Outcome 3: 40% 50% 25% 25% Impact C Impact E Impact D 20% 60% Impact D Impact C Page 27

25 Custom Risk Modeling Identify and understand the potential events Draw on industry and company specific data Identify likelihood and impact ranges Develop representative risk model Quantify risk Communicate it with the market Page 28 Analytics Analytical Tools: Risk Assessment Probabilistic Loss Forecasting Customized Risk Modeling Risk Bearing Capacity Analysis Captives Page 29 25

26 Risk Bearing Capacity Helps us understand: how much financial impairment could be absorbed in risk on an annually recurring basis ability to assume various retention structures Enables Risk Manager / CFO rationalize taking on higher retentions / new risks Page 30 26

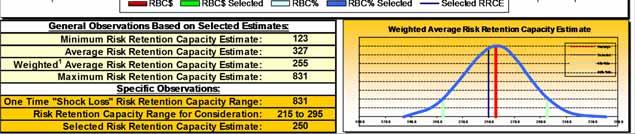

27 Retention Capacity FINANCIAL MEASURES AMOUNTS WEIGHTS ESTIMATED US$(million) MINIMUM MAXIMUM MEDIAN SELECTED RET. CAP. Wgt 1 27 LIQUIDITY: Value Include Cash Balance: 4, % 3.0% 2.0% 2.0% % Inventories: 5, % 4.0% 2.5% 2.5% % Working Capital: 3, % 4.0% 2.5% 2.5% % Operating Cash Flow: 7, % 5.0% 3.5% 3.5% % FINANCIAL STRENGTHS: Shareholders' Equity: 30, % 2.0% 1.3% 1.3% % Total Assets: 60, % 1.5% 0.9% 0.9% % EARNINGS: Gross Revenue: 20, % 1.5% 1.0% 1.0% % Pre-Tax Earnings: 7, % 5.0% 3.0% 3.0% % Page 31

28 Retention Capacity 28 Page 32

29 Retention Capacity 29 Page 33

30 Risk Bearing Capacity Understand your capacity to retain risk Addresses the issue of: Am I buying too much insurance? Can I afford to buy less? Take advantage of hard and soft market insurance cycles Analytics Page 34 How To Think About Risk 1. Understand industry trends, competition and business strategy 2. Define risk tolerance 3. Identify priority exposures and risk scenarios 4. Model loss frequency and severity 5. Quantify Total Cost of Risk for Priority Risks / Define a Crisis 6. Avoidance 7. Mitigation 8. Retention Balance Sheet Captive 9. Transfer To Insurers To Capital or Other Markets R I S K S T R A T E G Y I M P L E M E N T A T I O N Page 35 30

31 for Captives Page 36 Analytics Analytical Tools: Risk Bearing Capacity Analysis Probabilistic Loss Forecasting Risk Assessment Customized Risk Modeling Captives Page 37 31

32 In the context of Captives, analytics can provide the basis for decisions on: Captive Feasibility Value Created by the Captive New Product Development Captive Governance Capital Adequacy Transfer Pricing Audit Preparation and Support Page 38 Analytics Captives Is there a role for a captive in my insurance program A well structured captive demonstrates to markets knowledge and understanding of, and a willingness to participate in, the risks being insured Flexibility in program design Page 39 32

33 Analytics do not replace good business judgment Analytics supplement the business decision process by: making explicit the hidden assumptions encouraging a critical validation for assessment providing a rational basis for program design enabling and providing a framework for organizing knowledge about the business Page 40 Improving Risk Management and Insurance Placements Using Analytics Questions? IRMI Energy Conference March 4-6, 2014 Houston, TX Page 41 33

34 Improving Risk Management and Insurance Placements Using Analytics Thank-you! IRMI Energy Conference March 4-6, 2014 Houston, TX Page 42 34

Tuesday, March 17, 2015 Houston, TX. 3:45 5:00 p.m. CAPTIVATING RISK: ART MARKET AND CAPTIVE SOLUTIONS

Tuesday, March 17, 2015 Houston, TX 3:45 5:00 p.m. : ART MARKET AND CAPTIVE SOLUTIONS Presented by Michael O Neill, CPCU, ARM President and CEO American Contractors Insurance Group Many companies look

Tuesday, March 17, 2015 Houston, TX 3:45 5:00 p.m. : ART MARKET AND CAPTIVE SOLUTIONS Presented by Michael O Neill, CPCU, ARM President and CEO American Contractors Insurance Group Many companies look

SOCIETY OF ACTUARIES Enterprise Risk Management General Insurance Extension Exam ERM-GI

SOCIETY OF ACTUARIES Exam ERM-GI Date: Tuesday, November 1, 2016 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 80 points. This exam consists

SOCIETY OF ACTUARIES Exam ERM-GI Date: Tuesday, November 1, 2016 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 80 points. This exam consists

Enterprise Risk Management Economic Capital Modleing and the Financial Crisis

Risk Management and The Crisis Enterprise Risk Management Economic Capital Modleing and the Financial Crisis What worked and what did not Insurance Industry Continues to Respond to Risk Dynamics Risk Sources

Risk Management and The Crisis Enterprise Risk Management Economic Capital Modleing and the Financial Crisis What worked and what did not Insurance Industry Continues to Respond to Risk Dynamics Risk Sources

ERM in the Rating Process: A Practical Perspective

ERM in the Rating Process: A Practical Perspective Jeffrey Mango, Group Vice President, A.M. Best Michelle Baurkot, Assistant Vice President, A.M. Best Tom Zitelli, Managing Senior Financial Analyst, A.M.

ERM in the Rating Process: A Practical Perspective Jeffrey Mango, Group Vice President, A.M. Best Michelle Baurkot, Assistant Vice President, A.M. Best Tom Zitelli, Managing Senior Financial Analyst, A.M.

Solvency II Detailed guidance notes for dry run process. March 2010

Solvency II Detailed guidance notes for dry run process March 2010 Introduction The successful implementation of Solvency II at Lloyd s is critical to maintain the competitive position and capital advantages

Solvency II Detailed guidance notes for dry run process March 2010 Introduction The successful implementation of Solvency II at Lloyd s is critical to maintain the competitive position and capital advantages

Risk & Analytics. Trends within Insurance Companies Risk Management. Marc Paasch June Willis Towers Watson. All rights reserved.

Risk & Analytics Trends within Insurance Companies Risk Management Marc Paasch June 2017 2017 Willis Towers Watson. All rights reserved. Key drivers & benefits Outcomes from an analytical approach to own

Risk & Analytics Trends within Insurance Companies Risk Management Marc Paasch June 2017 2017 Willis Towers Watson. All rights reserved. Key drivers & benefits Outcomes from an analytical approach to own

ORSA reports: gaps and opportunities

ORSA reports: gaps and opportunities Market benchmarking of ORSA reports for Singapore general insurers Industry-wide Own Risk and Solvency Assessment (ORSA) 1 2 Contents 1 Executive summary 2 Our assessment

ORSA reports: gaps and opportunities Market benchmarking of ORSA reports for Singapore general insurers Industry-wide Own Risk and Solvency Assessment (ORSA) 1 2 Contents 1 Executive summary 2 Our assessment

Delivering Clarity to Credit Unions Through Expertise and Experience

Jeff Owen, The Rochdale Group September 2012 Delivering Clarity to Credit Unions Through Expertise and Experience Enterprise Risk Management Lending Execution and Risk Management Merger Strategy and Realization

Jeff Owen, The Rochdale Group September 2012 Delivering Clarity to Credit Unions Through Expertise and Experience Enterprise Risk Management Lending Execution and Risk Management Merger Strategy and Realization

An Actuarial Evaluation of the Insurance Limits Buying Decision

An Actuarial Evaluation of the Insurance Limits Buying Decision Joe Wieligman Client Executive VP Hylant Travis J. Grulkowski Principal & Consulting Actuary Milliman, Inc. WWW.CHICAGOLANDRISKFORUM.ORG

An Actuarial Evaluation of the Insurance Limits Buying Decision Joe Wieligman Client Executive VP Hylant Travis J. Grulkowski Principal & Consulting Actuary Milliman, Inc. WWW.CHICAGOLANDRISKFORUM.ORG

THE SMART WAY TO ANALYSE YOUR RISKS. DAVID STEBBING Partner, Willis Risk & Analytics

THE SMART WAY TO ANALYSE YOUR RISKS DAVID STEBBING Partner, Willis Risk & Analytics Increasing risks and challenges Commodity market volatility Short-term cashflow planning Profitability of longterm investments

THE SMART WAY TO ANALYSE YOUR RISKS DAVID STEBBING Partner, Willis Risk & Analytics Increasing risks and challenges Commodity market volatility Short-term cashflow planning Profitability of longterm investments

RESERVE BANK OF MALAWI

RESERVE BANK OF MALAWI GUIDELINES ON INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS (ICAAP) Bank Supervision Department March 2013 Table of Contents 1.0 INTRODUCTION... 2 2.0 MANDATE... 2 3.0 RATIONALE...

RESERVE BANK OF MALAWI GUIDELINES ON INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS (ICAAP) Bank Supervision Department March 2013 Table of Contents 1.0 INTRODUCTION... 2 2.0 MANDATE... 2 3.0 RATIONALE...

Overview of S&P s Request for Comment: Insurers: Rating Methodology

Aon Benfield Analytics Overview of S&P s Request for Comment: Insurers: Rating Methodology July 2012 General Overview On July 9, 2012, Standard & Poor s (S&P) released a Request for Comment (RFC) that

Aon Benfield Analytics Overview of S&P s Request for Comment: Insurers: Rating Methodology July 2012 General Overview On July 9, 2012, Standard & Poor s (S&P) released a Request for Comment (RFC) that

Navigating the New Normal Enterprise Risk Management After e-risk Identification and Assessment

Navigating the New Normal Enterprise Risk Management After e-risk Identification and Assessment Agenda ERM After e-ria ERM Level Setting ERM Fundamentals So Now What? Next-Step Considerations Overview

Navigating the New Normal Enterprise Risk Management After e-risk Identification and Assessment Agenda ERM After e-ria ERM Level Setting ERM Fundamentals So Now What? Next-Step Considerations Overview

Guideline. Earthquake Exposure Sound Practices. I. Purpose and Scope. No: B-9 Date: February 2013

Guideline Subject: No: B-9 Date: February 2013 I. Purpose and Scope Catastrophic losses from exposure to earthquakes may pose a significant threat to the financial wellbeing of many Property & Casualty

Guideline Subject: No: B-9 Date: February 2013 I. Purpose and Scope Catastrophic losses from exposure to earthquakes may pose a significant threat to the financial wellbeing of many Property & Casualty

Kidsafe NSW Risk Management Plan. August 2014

Kidsafe NSW Risk Management Plan August 2014 Document Control Document Approval Name & Position Signature Date Document Version Control Version Status Date Prepared By Comments Document Reviewers Name

Kidsafe NSW Risk Management Plan August 2014 Document Control Document Approval Name & Position Signature Date Document Version Control Version Status Date Prepared By Comments Document Reviewers Name

Changes in Agent Distribution Tuesday, September 29, 2015

Changes in Agent Distribution Tuesday, September 29, 2015 Jeff Rieder, CPA, CPCU Partner, Head of Ward Group Ward Group Cincinnati, Ohio Jeff Rieder is partner and head of Ward Group, a management consulting

Changes in Agent Distribution Tuesday, September 29, 2015 Jeff Rieder, CPA, CPCU Partner, Head of Ward Group Ward Group Cincinnati, Ohio Jeff Rieder is partner and head of Ward Group, a management consulting

Examining a Top-Down Approach to Enterprise Risk Management

Examining a Top-Down Approach to Enterprise Risk Management June 25, 2018 12:30 ET Monique Allen Associate General Counsel, Clinical Operations and Privacy Memorial Hermann Health System Houston, Texas

Examining a Top-Down Approach to Enterprise Risk Management June 25, 2018 12:30 ET Monique Allen Associate General Counsel, Clinical Operations and Privacy Memorial Hermann Health System Houston, Texas

The Real World: Dealing With Parameter Risk. Alice Underwood Senior Vice President, Willis Re March 29, 2007

The Real World: Dealing With Parameter Risk Alice Underwood Senior Vice President, Willis Re March 29, 2007 Agenda 1. What is Parameter Risk? 2. Practical Observations 3. Quantifying Parameter Risk 4.

The Real World: Dealing With Parameter Risk Alice Underwood Senior Vice President, Willis Re March 29, 2007 Agenda 1. What is Parameter Risk? 2. Practical Observations 3. Quantifying Parameter Risk 4.

A.M. Best ERM SRQ Response Survey. March 2012

A.M. Best ERM SRQ Response Survey March 2012 Overview of A.M. Best s ERM SRQ section ERM section of SRQ added in 2011 to provide a consistent starting point for analyst discussions Key Questions Responses

A.M. Best ERM SRQ Response Survey March 2012 Overview of A.M. Best s ERM SRQ section ERM section of SRQ added in 2011 to provide a consistent starting point for analyst discussions Key Questions Responses

Aon Risk Solutions. Real Estate Practice. Fact-based Solutions for Real Estate Risk Management. Risk. Reinsurance. Human Resources.

Aon Risk Solutions Real Estate Practice Fact-based Solutions for Real Estate Risk Management Risk. Reinsurance. Human Resources. Do these problems sound familiar? My insurance broker doesn t understand

Aon Risk Solutions Real Estate Practice Fact-based Solutions for Real Estate Risk Management Risk. Reinsurance. Human Resources. Do these problems sound familiar? My insurance broker doesn t understand

Wednesday, March 5, 2014 Houston, TX. 1:30 2:45 p.m. OEE ISSUES AND ANSWERS

Wednesday, March 5, 2014 Houston, TX 1:30 2:45 p.m. OEE ISSUES AND ANSWERS Presented by Scott Barnard Vice President, Southwest Regional Manager Berkley Offshore Underwriting Managers Pascal Ray Senior

Wednesday, March 5, 2014 Houston, TX 1:30 2:45 p.m. OEE ISSUES AND ANSWERS Presented by Scott Barnard Vice President, Southwest Regional Manager Berkley Offshore Underwriting Managers Pascal Ray Senior

Criteria Insurance General: Refined Methodology For Assessing An Insurer's Risk Appetite. Table Of Contents

March 30, 2010 Criteria Insurance General: Refined Methodology For Assessing An Insurer's Risk Appetite Primary Credit Analyst: Marcus Bowser, London +44(207) 176 7052; marcus_bowser@standardandpoors.com

March 30, 2010 Criteria Insurance General: Refined Methodology For Assessing An Insurer's Risk Appetite Primary Credit Analyst: Marcus Bowser, London +44(207) 176 7052; marcus_bowser@standardandpoors.com

OWN RISK AND SOLVENCY ASSESSMENT. ERM Seminar Compliance All Dealing from the same deck now

OWN RISK AND SOLVENCY ASSESSMENT ERM Seminar - 2014 Compliance All Dealing from the same deck now Own and Solvency Assessment! Originated in the UK about 10 years ago Now a global insurance regulatory

OWN RISK AND SOLVENCY ASSESSMENT ERM Seminar - 2014 Compliance All Dealing from the same deck now Own and Solvency Assessment! Originated in the UK about 10 years ago Now a global insurance regulatory

What Outsourcing Has to Offer: Part II

What Outsourcing Has to Offer: Part II California Municipal Treasurers Association Kay Chandler, CFA, President Chandler Asset Management, Inc. What is an Investment Adviser? An investment firm with demonstrated

What Outsourcing Has to Offer: Part II California Municipal Treasurers Association Kay Chandler, CFA, President Chandler Asset Management, Inc. What is an Investment Adviser? An investment firm with demonstrated

Chapter-8 Risk Management

Chapter-8 Risk Management 8.1 Concept of Risk Management Risk management is a proactive process that focuses on identifying risk events and developing strategies to respond and control risks. It is not

Chapter-8 Risk Management 8.1 Concept of Risk Management Risk management is a proactive process that focuses on identifying risk events and developing strategies to respond and control risks. It is not

Putting a value on your company s financial capacity to take risk

Putting a value on your company s financial capacity to take risk Session: SRM009 Price Tag This! Day/Date: Tuesday, April 12, 2016 Speakers: Graeme Harper, Senior Vice President - Global Insurance, FIS

Putting a value on your company s financial capacity to take risk Session: SRM009 Price Tag This! Day/Date: Tuesday, April 12, 2016 Speakers: Graeme Harper, Senior Vice President - Global Insurance, FIS

Enterprise Risk Management Framework: Is It Working Effectively or Is It Window Dressing?

Enterprise Risk Management Framework: Is It Working Effectively or Is It Window Dressing? Joseph F. Morris jmorris@pcicstrategies.com 215-901-0334 www.pcicstrategies.com Property Casualty Insurers Association

Enterprise Risk Management Framework: Is It Working Effectively or Is It Window Dressing? Joseph F. Morris jmorris@pcicstrategies.com 215-901-0334 www.pcicstrategies.com Property Casualty Insurers Association

THE PAST, PRESENT, AND FUTURE OF DEFAULT INSURANCE

WORKSHOP W2 Wednesday, November 9 8:45 a.m. 9:45 a.m. and 10:15 a.m. 11:15 a.m. THE PAST, PRESENT, AND FUTURE OF DEFAULT INSURANCE Presented by Brian Carpenter Executive Vice President Willis Towers Watson

WORKSHOP W2 Wednesday, November 9 8:45 a.m. 9:45 a.m. and 10:15 a.m. 11:15 a.m. THE PAST, PRESENT, AND FUTURE OF DEFAULT INSURANCE Presented by Brian Carpenter Executive Vice President Willis Towers Watson

Comment from past participant

Understanding Asset and Liability Management Comment from past participant The facilitator is very experienced! Chris is able to relate topics with his experience. He provided a lot of real experience

Understanding Asset and Liability Management Comment from past participant The facilitator is very experienced! Chris is able to relate topics with his experience. He provided a lot of real experience

The Tools and Techniques of Life Insurance Planning, Stephen

Course Syllabus Course Develops the concept of insurable risk and its identification; the uses of Description insurance in financial planning to deal with risk; analysis of property, liability, life, medical

Course Syllabus Course Develops the concept of insurable risk and its identification; the uses of Description insurance in financial planning to deal with risk; analysis of property, liability, life, medical

METHODOLOGY For Risk Assessment and Management of PPP Projects

METHODOLOGY For Risk Assessment and Management of PPP Projects December 26, 2013 The publication was produced for review by the United States Agency for International Development. It was prepared by Environmental

METHODOLOGY For Risk Assessment and Management of PPP Projects December 26, 2013 The publication was produced for review by the United States Agency for International Development. It was prepared by Environmental

Success in Implementing Workers Compensation Predictive Models at Zurich Financial Services

Success in Implementing Workers Compensation Predictive Models at Zurich Financial Services Joel Appelbaum Zurich Financial Services Chief Risk Officer of North America Underwriting Transformation May

Success in Implementing Workers Compensation Predictive Models at Zurich Financial Services Joel Appelbaum Zurich Financial Services Chief Risk Officer of North America Underwriting Transformation May

Catastrophe Reinsurance Pricing

Catastrophe Reinsurance Pricing Science, Art or Both? By Joseph Qiu, Ming Li, Qin Wang and Bo Wang Insurers using catastrophe reinsurance, a critical financial management tool with complex pricing, can

Catastrophe Reinsurance Pricing Science, Art or Both? By Joseph Qiu, Ming Li, Qin Wang and Bo Wang Insurers using catastrophe reinsurance, a critical financial management tool with complex pricing, can

CREDIT RATING INFORMATION & SERVICES LIMITED

Rating Methodology INVESTMENT COMPANY CREDIT RATING INFORMATION & SERVICES LIMITED Nakshi Homes (4th & 5th Floor), 6/1A, Segunbagicha, Dhaka 1000, Bangladesh Tel: 717 3700 1, Fax: 956 5783 Email: crisl@bdonline.com

Rating Methodology INVESTMENT COMPANY CREDIT RATING INFORMATION & SERVICES LIMITED Nakshi Homes (4th & 5th Floor), 6/1A, Segunbagicha, Dhaka 1000, Bangladesh Tel: 717 3700 1, Fax: 956 5783 Email: crisl@bdonline.com

The Components of a Sound Emerging Risk Management Framework

North American CRO Council The Components of a Sound Emerging Risk Management Framework December 6, 2012 2012 North American CRO Council Incorporated chairperson@crocouncil.org North American CRO Council

North American CRO Council The Components of a Sound Emerging Risk Management Framework December 6, 2012 2012 North American CRO Council Incorporated chairperson@crocouncil.org North American CRO Council

WRAP-UPS: WHAT KEEPS US UP AT NIGHT

Workshop W1 Wednesday, November 12 8:30 9:45 a.m. and 10:05 11:20 a.m. WRAP-UPS: WHAT KEEPS US UP AT NIGHT Presented by Workshop W1 Richard Resnick President Project Risk Consultants, Inc. Wrap-ups offer

Workshop W1 Wednesday, November 12 8:30 9:45 a.m. and 10:05 11:20 a.m. WRAP-UPS: WHAT KEEPS US UP AT NIGHT Presented by Workshop W1 Richard Resnick President Project Risk Consultants, Inc. Wrap-ups offer

RISK MANAGEMENT ON USACE CIVIL WORKS PROJECTS

RISK MANAGEMENT ON USACE CIVIL WORKS PROJECTS Identify, Quantify, and 237 217 200 237 217 200 Manage 237 217 200 255 255 255 0 0 0 163 163 163 131 132 122 239 65 53 80 119 27 252 174.59 110 135 120 112

RISK MANAGEMENT ON USACE CIVIL WORKS PROJECTS Identify, Quantify, and 237 217 200 237 217 200 Manage 237 217 200 255 255 255 0 0 0 163 163 163 131 132 122 239 65 53 80 119 27 252 174.59 110 135 120 112

Career Risk Management

Dennis Baltz, CPCU ARM SVP Client Advocate Willis Atlanta, GA dennis.baltz@willis.com 404.224.5157 Ryan Grelecki, Esq. Director of Business Development Kredible, Inc. Atlanta, GA ryan@kredible.com 404.625.0773

Dennis Baltz, CPCU ARM SVP Client Advocate Willis Atlanta, GA dennis.baltz@willis.com 404.224.5157 Ryan Grelecki, Esq. Director of Business Development Kredible, Inc. Atlanta, GA ryan@kredible.com 404.625.0773

GUIDELINE ON ENTERPRISE RISK MANAGEMENT

GUIDELINE ON ENTERPRISE RISK MANAGEMENT Insurance Authority Table of Contents Page 1. Introduction 1 2. Application 2 3. Overview of Enterprise Risk Management (ERM) Framework and 4 General Requirements

GUIDELINE ON ENTERPRISE RISK MANAGEMENT Insurance Authority Table of Contents Page 1. Introduction 1 2. Application 2 3. Overview of Enterprise Risk Management (ERM) Framework and 4 General Requirements

Differentiated Pay Plan Submission Template

2014-15 Differentiated Pay Plan Submission Template In June 2013, the State Board of Education passed a revised set of guidelines pursuant to Tenn. Code Ann. 49-3-306(h), which requires districts to create

2014-15 Differentiated Pay Plan Submission Template In June 2013, the State Board of Education passed a revised set of guidelines pursuant to Tenn. Code Ann. 49-3-306(h), which requires districts to create

RenaissanceRe Holdings Ltd.

RenaissanceRe Holdings Ltd. Creating value across market cycles Investor Presentation September 2008 Table of Contents Results Strategic Overview Reinsurance Individual Risk Ventures Hurricane Science

RenaissanceRe Holdings Ltd. Creating value across market cycles Investor Presentation September 2008 Table of Contents Results Strategic Overview Reinsurance Individual Risk Ventures Hurricane Science

Presented by Kristina Narvaez President & CEO ERM Strategies, LLC

Presented by Kristina Narvaez President & CEO ERM Strategies, LLC www.erm-strategies.com Regulations to Support Value Creation Sarbanes Oxley 2002 NYSE 2004 SEC 33-9089 Dodd Frank Section 165 Part C S

Presented by Kristina Narvaez President & CEO ERM Strategies, LLC www.erm-strategies.com Regulations to Support Value Creation Sarbanes Oxley 2002 NYSE 2004 SEC 33-9089 Dodd Frank Section 165 Part C S

Performance Measurement of Supreme Audit Institutions in 4 Anglo-Saxon Countries: Leading by Example

Performance Measurement of Supreme Audit Institutions in 4 Anglo-Saxon Countries: Leading by Example Nobuo AZUMA* Director, Study Division, Board of Audit I. Introduction In Japan, performance measurement

Performance Measurement of Supreme Audit Institutions in 4 Anglo-Saxon Countries: Leading by Example Nobuo AZUMA* Director, Study Division, Board of Audit I. Introduction In Japan, performance measurement

For the attention of: Tax Treaties, Transfer Pricing and Financial Transaction Division, OECD/CTPA. Questions / Paragraph (OECD Discussion Draft)

") NERA Economic Consulting Marble Arch House 66 Seymour Street London W1H 5BT, UK Oliver Wyman One University Square Drive, Suite 100 Princeton, NJ 08540-6455 7 September 2018 For the attention of: Tax Treaties,

NERA Economic Consulting Marble Arch House 66 Seymour Street London W1H 5BT, UK Oliver Wyman One University Square Drive, Suite 100 Princeton, NJ 08540-6455 7 September 2018 For the attention of: Tax Treaties,

REGULATORY GUIDELINE Liquidity Risk Management Principles TABLE OF CONTENTS. I. Introduction II. Purpose and Scope III. Principles...

REGULATORY GUIDELINE Liquidity Risk Management Principles SYSTEM COMMUNICATION NUMBER Guideline 2015-02 ISSUE DATE June 2015 TABLE OF CONTENTS I. Introduction... 1 II. Purpose and Scope... 1 III. Principles...

REGULATORY GUIDELINE Liquidity Risk Management Principles SYSTEM COMMUNICATION NUMBER Guideline 2015-02 ISSUE DATE June 2015 TABLE OF CONTENTS I. Introduction... 1 II. Purpose and Scope... 1 III. Principles...

STRESS TESTING GUIDELINE

c DRAFT STRESS TESTING GUIDELINE November 2011 TABLE OF CONTENTS Preamble... 2 Introduction... 3 Coming into effect and updating... 6 1. Stress testing... 7 A. Concept... 7 B. Approaches underlying stress

c DRAFT STRESS TESTING GUIDELINE November 2011 TABLE OF CONTENTS Preamble... 2 Introduction... 3 Coming into effect and updating... 6 1. Stress testing... 7 A. Concept... 7 B. Approaches underlying stress

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Guidance Paper No. 2.2.x INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS GUIDANCE PAPER ON ENTERPRISE RISK MANAGEMENT FOR CAPITAL ADEQUACY AND SOLVENCY PURPOSES DRAFT, MARCH 2008 This document was prepared

Guidance Paper No. 2.2.x INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS GUIDANCE PAPER ON ENTERPRISE RISK MANAGEMENT FOR CAPITAL ADEQUACY AND SOLVENCY PURPOSES DRAFT, MARCH 2008 This document was prepared

COMMUNIQUE. Page 1 of 13

COMMUNIQUE 16-COM-001 Feb. 1, 2016 Release of Liquidity Risk Management Guiding Principles The Credit Union Prudential Supervisors Association (CUPSA) has released guiding principles for Liquidity Risk

COMMUNIQUE 16-COM-001 Feb. 1, 2016 Release of Liquidity Risk Management Guiding Principles The Credit Union Prudential Supervisors Association (CUPSA) has released guiding principles for Liquidity Risk

Global Enterprise Risk Management in Insurance

Global Enterprise Risk Management in Insurance Caroline Bennet National Leader, Deloitte Actuaries & Consultants Australia Meeting the Challenges of Change 14 th Global Conference of Actuaries 19 th 21

Global Enterprise Risk Management in Insurance Caroline Bennet National Leader, Deloitte Actuaries & Consultants Australia Meeting the Challenges of Change 14 th Global Conference of Actuaries 19 th 21

Pricing Analytics for the Small and Medium Sized Company

Pricing Analytics for the Small and Medium Sized Company The Road to Advanced Pricing Practices 2014 CAS RPM By: Len Llaguno April 1, 2014 2014 Towers Watson. All rights reserved. 0 Antitrust Notice The

Pricing Analytics for the Small and Medium Sized Company The Road to Advanced Pricing Practices 2014 CAS RPM By: Len Llaguno April 1, 2014 2014 Towers Watson. All rights reserved. 0 Antitrust Notice The

Guidance Note: Internal Capital Adequacy Assessment Process (ICAAP) Credit Unions with Total Assets Greater than $1 Billion.

Credit Unions with Total Assets Greater than $1 Billion.") Guidance Note: Internal Capital Adequacy Assessment Process (ICAAP) Credit Unions with Total Assets Greater than $1 Billion January 2018 Ce document est aussi disponible en français. Applicability This

Guidance Note: Internal Capital Adequacy Assessment Process (ICAAP) Credit Unions with Total Assets Greater than $1 Billion January 2018 Ce document est aussi disponible en français. Applicability This

BERMUDA MONETARY AUTHORITY GUIDELINES ON STRESS TESTING FOR THE BERMUDA BANKING SECTOR

GUIDELINES ON STRESS TESTING FOR THE BERMUDA BANKING SECTOR TABLE OF CONTENTS 1. EXECUTIVE SUMMARY...2 2. GUIDANCE ON STRESS TESTING AND SCENARIO ANALYSIS...3 3. RISK APPETITE...6 4. MANAGEMENT ACTION...6

GUIDELINES ON STRESS TESTING FOR THE BERMUDA BANKING SECTOR TABLE OF CONTENTS 1. EXECUTIVE SUMMARY...2 2. GUIDANCE ON STRESS TESTING AND SCENARIO ANALYSIS...3 3. RISK APPETITE...6 4. MANAGEMENT ACTION...6

Captive Finance Firms in a Challenging Economy

Captive Finance Firms in a Challenging Economy Facing the Wave [Type text] The Foundation is the only research organization dedicated solely to the equipment finance industry. The Foundation accomplishes

Captive Finance Firms in a Challenging Economy Facing the Wave [Type text] The Foundation is the only research organization dedicated solely to the equipment finance industry. The Foundation accomplishes

Commodity Risk Management: Supply Chain Best Practices May 24 th,2017: Session Code: JA17

Commodity Risk Management: Supply Chain Best Practices May 24 th,2017: Session Code: JA17 Presented by Michael Irgang Executive Vice President Global Risk Management Corp. 1 Commodity trading is not suitable

Commodity Risk Management: Supply Chain Best Practices May 24 th,2017: Session Code: JA17 Presented by Michael Irgang Executive Vice President Global Risk Management Corp. 1 Commodity trading is not suitable

Information Technology Project Management, Sixth Edition

Management, Sixth Edition Prepared By: Izzeddin Matar. Note: See the text itself for full citations. Understand what risk is and the importance of good project risk management Discuss the elements involved

Management, Sixth Edition Prepared By: Izzeddin Matar. Note: See the text itself for full citations. Understand what risk is and the importance of good project risk management Discuss the elements involved

Defining the Internal Model for Risk & Capital Management under the Solvency II Directive

14 Defining the Internal Model for Risk & Capital Management under the Solvency II Directive Mark Dougherty is an international Senior Corporate Governance and Risk Management professional and Chartered

14 Defining the Internal Model for Risk & Capital Management under the Solvency II Directive Mark Dougherty is an international Senior Corporate Governance and Risk Management professional and Chartered

Office of the City Auditor 2018 Annual Work Plan and Long Term Audit Plan

1200, Scotia Place, Tower 1 10060 Jasper Avenue Edmonton, Alberta T5J 3R8 edmonton.ca/auditor and Long Term Audit Plan November 14, 2017 This page is intentionally blank. Introduction Bylaw 12424, City

1200, Scotia Place, Tower 1 10060 Jasper Avenue Edmonton, Alberta T5J 3R8 edmonton.ca/auditor and Long Term Audit Plan November 14, 2017 This page is intentionally blank. Introduction Bylaw 12424, City

SAN DIEGO CITY EMPLOYEES' RETIREMENT SYSTEM REQUEST FOR PROPOSAL (RFP) FOR GENERAL INVESTMENT CONSULTANT

FOR GENERAL INVESTMENT CONSULTANT") SAN DIEGO CITY EMPLOYEES' RETIREMENT SYSTEM REQUEST FOR PROPOSAL (RFP) FOR GENERAL INVESTMENT CONSULTANT SAN DIEGO CITY EMPLOYEES RETIREMENT SYSTEM GENERAL INVESTMENT CONSULTANT RFP SEPTEMBER 2014 Table

SAN DIEGO CITY EMPLOYEES' RETIREMENT SYSTEM REQUEST FOR PROPOSAL (RFP) FOR GENERAL INVESTMENT CONSULTANT SAN DIEGO CITY EMPLOYEES RETIREMENT SYSTEM GENERAL INVESTMENT CONSULTANT RFP SEPTEMBER 2014 Table

Risk Management Policy and Framework

Risk Management Policy and Framework Risk Management Policy Statement ALS recognises that the effective management of risks is a fundamental component of good corporate governance and is vital for the

Risk Management Policy and Framework Risk Management Policy Statement ALS recognises that the effective management of risks is a fundamental component of good corporate governance and is vital for the

Statement of Guidance for Licensees seeking approval to use an Internal Capital Model ( ICM ) to calculate the Prescribed Capital Requirement ( PCR )

to calculate the Prescribed Capital Requirement ( PCR )") MAY 2016 Statement of Guidance for Licensees seeking approval to use an Internal Capital Model ( ICM ) to calculate the Prescribed Capital Requirement ( PCR ) 1 Table of Contents 1 STATEMENT OF OBJECTIVES...

MAY 2016 Statement of Guidance for Licensees seeking approval to use an Internal Capital Model ( ICM ) to calculate the Prescribed Capital Requirement ( PCR ) 1 Table of Contents 1 STATEMENT OF OBJECTIVES...

Wednesday, March 2, 2016 Houston, TX. 11:00 a.m. 12:15 p.m. OCCUPATIONAL DISEASE EXPOSURES IN THE OIL & GAS INDUSTRY: BRINGING SAFETY TO THE SURFACE

Wednesday, March 2, 2016 Houston, TX 11:00 a.m. 12:15 p.m. OCCUPATIONAL DISEASE EXPOSURES IN THE OIL & GAS INDUSTRY: BRINGING SAFETY TO THE SURFACE Presented by Alex Beaver Energy Underwriting Consultant

Wednesday, March 2, 2016 Houston, TX 11:00 a.m. 12:15 p.m. OCCUPATIONAL DISEASE EXPOSURES IN THE OIL & GAS INDUSTRY: BRINGING SAFETY TO THE SURFACE Presented by Alex Beaver Energy Underwriting Consultant

ERM Benchmark Survey Report A report on PACICC's third ERM benchmarking survey

Property and Casualty Insurance Compensation Corporation Société d indemnisation en matière d assurances IARD ERM Benchmark Survey Report A report on PACICC's third ERM benchmarking survey August 2015

Property and Casualty Insurance Compensation Corporation Société d indemnisation en matière d assurances IARD ERM Benchmark Survey Report A report on PACICC's third ERM benchmarking survey August 2015

Meeting of Bristol Clinical Commissioning Group Governing Body

Meeting of Bristol Clinical Commissioning Group Governing Body To be held on Tuesday 30 June 2015 commencing at 13:30pm at the Greenway Centre, 119 Doncaster Road, BS10 5PY Title: Risk Appetite Statement

Meeting of Bristol Clinical Commissioning Group Governing Body To be held on Tuesday 30 June 2015 commencing at 13:30pm at the Greenway Centre, 119 Doncaster Road, BS10 5PY Title: Risk Appetite Statement

Preparing for the New ERM and Solvency Regulatory Requirements

OWN RISK AND SOLVENCY ASSESSMENT Preparing for the New ERM and Solvency Regulatory Requirements A White Paper from Willis Re Analytics Insurance solvency regulation is moving into new territory. Insurer

OWN RISK AND SOLVENCY ASSESSMENT Preparing for the New ERM and Solvency Regulatory Requirements A White Paper from Willis Re Analytics Insurance solvency regulation is moving into new territory. Insurer

ENMAX CORPORATION 2016 REPORT ON EXECUTIVE COMPENSATION. as of December 31, 2016

ENMAX CORPORATION 2016 REPORT ON EXECUTIVE COMPENSATION as of December 31, 2016 OUR APPROACH TO EXECUTIVE COMPENSATION ENMAX S STRATEGIC DIRECTION ENMAX Corporation (ENMAX) is an energy company headquartered

ENMAX CORPORATION 2016 REPORT ON EXECUTIVE COMPENSATION as of December 31, 2016 OUR APPROACH TO EXECUTIVE COMPENSATION ENMAX S STRATEGIC DIRECTION ENMAX Corporation (ENMAX) is an energy company headquartered

Sections of the ORSA Report

Lessons Learned From Orsa Reviews Impact on Risk Focused Examination NAIC Insurance Summit INS Companies Joe Fritsch, Director INS Companies Don Carbone, Exam Manager INS Companies Sections of the ORSA

Lessons Learned From Orsa Reviews Impact on Risk Focused Examination NAIC Insurance Summit INS Companies Joe Fritsch, Director INS Companies Don Carbone, Exam Manager INS Companies Sections of the ORSA

Own Risk and Solvency Assessment

Own Risk and Solvency Assessment Acumen Conference 2015 Elaine Hultzer, Insurance Audit & Advisory Partner, Deloitte Sati MacLean, Senior P&C Actuarial Manager, Deloitte June 10 th, 2015 Agenda Introduction

Own Risk and Solvency Assessment Acumen Conference 2015 Elaine Hultzer, Insurance Audit & Advisory Partner, Deloitte Sati MacLean, Senior P&C Actuarial Manager, Deloitte June 10 th, 2015 Agenda Introduction

Scouting Ireland Risk Management Framework

No. SID 124A/15 Gasóga na héireann/scouting Ireland Issued Amended 20 th June 2015 Deleted Source: National Management Committee Scouting Ireland Risk Management Framework Revision Date Description # 20/06/2015

No. SID 124A/15 Gasóga na héireann/scouting Ireland Issued Amended 20 th June 2015 Deleted Source: National Management Committee Scouting Ireland Risk Management Framework Revision Date Description # 20/06/2015

Corporate Risk Appetite and Program Structuring White paper 3 of 3

The first paper in this series discussed the impact that loss volatility has on the risk finance decision making process, and the second paper explored the notion of loss dependence and the influence of

The first paper in this series discussed the impact that loss volatility has on the risk finance decision making process, and the second paper explored the notion of loss dependence and the influence of

Beyond Basel II: Leveraging Economic Capital to Achieve Strategic Objectives

Enterprise Risk Management Symposium Beyond Basel II: Leveraging Economic Capital to Achieve Strategic Objectives March 2007 Ashish Dev adev@promontory.com Broader Concept of ERM with EC as the cornerstone

Enterprise Risk Management Symposium Beyond Basel II: Leveraging Economic Capital to Achieve Strategic Objectives March 2007 Ashish Dev adev@promontory.com Broader Concept of ERM with EC as the cornerstone

Applying COSO s Enterprise Risk Management Integrated Framework. September 29, 2004

Applying COSO s Enterprise Risk Management Integrated Framework September 29, 2004 Today s organizations are concerned about: Risk Management Governance Control Assurance (and Consulting) ERM Defined:

Applying COSO s Enterprise Risk Management Integrated Framework September 29, 2004 Today s organizations are concerned about: Risk Management Governance Control Assurance (and Consulting) ERM Defined:

An Overview of the Enterprise Risk Management Process

An Overview of the Enterprise Risk Management Process Laureen Regan, Ph.D. Fox School of Business and Management Temple University What is Enterprise Risk Management? Risk Management is "the culture, processes

An Overview of the Enterprise Risk Management Process Laureen Regan, Ph.D. Fox School of Business and Management Temple University What is Enterprise Risk Management? Risk Management is "the culture, processes

Exploring the New Era of ORSA Enterprise Risk Management (ERM)/ Own Risk and Solvency Assessment (ORSA) Committee

/ Own Risk and Solvency Assessment (ORSA) Committee") Exploring the New Era of ORSA Enterprise Risk Management (ERM)/ Own Risk and Solvency Assessment (ORSA) Committee Copyright 2015 by the American Academy of Actuaries. All Rights Reserved. Presenters Tricia

Exploring the New Era of ORSA Enterprise Risk Management (ERM)/ Own Risk and Solvency Assessment (ORSA) Committee Copyright 2015 by the American Academy of Actuaries. All Rights Reserved. Presenters Tricia

ENTERPRISE RISK MANAGEMENT POLICY FRAMEWORK

ANNEXURE A ENTERPRISE RISK MANAGEMENT POLICY FRAMEWORK CONTENTS 1. Enterprise Risk Management Policy Commitment 3 2. Introduction 4 3. Reporting requirements 5 3.1 Internal reporting processes for risk

ANNEXURE A ENTERPRISE RISK MANAGEMENT POLICY FRAMEWORK CONTENTS 1. Enterprise Risk Management Policy Commitment 3 2. Introduction 4 3. Reporting requirements 5 3.1 Internal reporting processes for risk

Risk Management Framework

Risk Management Framework Anglican Church, Diocese of Perth November 2015 Final ( Table of Contents Introduction... 1 Risk Management Policy... 2 Purpose... 2 Policy... 2 Definitions (from AS/NZS ISO 31000:2009)...

Risk Management Framework Anglican Church, Diocese of Perth November 2015 Final ( Table of Contents Introduction... 1 Risk Management Policy... 2 Purpose... 2 Policy... 2 Definitions (from AS/NZS ISO 31000:2009)...

Navigating the Named Insured Conundrum

Navigating the Named Insured Conundrum 1 Various insurance policies are involved in properly insuring a farm or agribusiness. The named insured under the policy is a critical element because the named

Navigating the Named Insured Conundrum 1 Various insurance policies are involved in properly insuring a farm or agribusiness. The named insured under the policy is a critical element because the named

Paramount Equity Financial Corp. 37 Sandiford Dr, Suite 400 Stouffville, ON L4A 3Z2 Canada

PARAMOUNT EQUITY FINANCIAL CORPORATION Paramount Equity Financial Corporation (PEFC) is a real estate investment firm and Mortgage Administrator that specializes in the origination and administration of

PARAMOUNT EQUITY FINANCIAL CORPORATION Paramount Equity Financial Corporation (PEFC) is a real estate investment firm and Mortgage Administrator that specializes in the origination and administration of

Essential Learning for CTP Candidates NY Cash Exchange 2018 Session #CTP-08

NY Cash Exchange 2018: CTP Track Cash Forecasting & Risk Management Session #8 (Thur. 4:00 5:00 pm) ETM5-Chapter 14: Cash Flow Forecasting ETM5-Chapter 16: Enterprise Risk Management ETM5-Chapter 17: Financial

NY Cash Exchange 2018: CTP Track Cash Forecasting & Risk Management Session #8 (Thur. 4:00 5:00 pm) ETM5-Chapter 14: Cash Flow Forecasting ETM5-Chapter 16: Enterprise Risk Management ETM5-Chapter 17: Financial

ERM and Reserve Risk

ERM and Reserve Risk Alietia Caughron, PhD CNA Insurance Casualty Actuarial Society s 2014 Centennial Celebration and Annual Meeting New York City, NY November 11, 2014 Disclaimer The purpose of this presentation

ERM and Reserve Risk Alietia Caughron, PhD CNA Insurance Casualty Actuarial Society s 2014 Centennial Celebration and Annual Meeting New York City, NY November 11, 2014 Disclaimer The purpose of this presentation

Offered By TAF Center for Actuarial Training 1

Offered By TAF Center for Actuarial Training 1 Developing home-grown and sustainable actuarial capacity for the markets served by TAF Consulting Group Practical, relevant and contextualized actuarial training

Offered By TAF Center for Actuarial Training 1 Developing home-grown and sustainable actuarial capacity for the markets served by TAF Consulting Group Practical, relevant and contextualized actuarial training

Launching ERM: Experiences from Progress Energy

Launching ERM: Experiences from Progress Energy ERM Roundtable Discussion North Carolina State University David Fox Joe McCallister Raymond Phillips April 16, 2004 Progress Energy Overview $8.7B revenues

Launching ERM: Experiences from Progress Energy ERM Roundtable Discussion North Carolina State University David Fox Joe McCallister Raymond Phillips April 16, 2004 Progress Energy Overview $8.7B revenues

Session 026 IF - Model Risk Management. Moderator: Yimin Yang. Presenters: George Alvites Charlie Anderson, Ph.D. Gang Ma, FSA

Session 026 IF - Model Risk Management Moderator: Yimin Yang Presenters: George Alvites Charlie Anderson, Ph.D. Gang Ma, FSA SOA Antitrust Compliance Guidelines SOA Presentation Disclaimer Model Risk Management

Session 026 IF - Model Risk Management Moderator: Yimin Yang Presenters: George Alvites Charlie Anderson, Ph.D. Gang Ma, FSA SOA Antitrust Compliance Guidelines SOA Presentation Disclaimer Model Risk Management

Lloyd s Minimum Standards MS7 Reinsurance Management and Control

Lloyd s Minimum Standards MS7 Reinsurance Management and Control January 2019 2 Contents MS7 Reinsurance Management & Control 3 Minimum Standards and Requirements 3 Management guidance 3 Definitions 3

Lloyd s Minimum Standards MS7 Reinsurance Management and Control January 2019 2 Contents MS7 Reinsurance Management & Control 3 Minimum Standards and Requirements 3 Management guidance 3 Definitions 3

CMP for Special Regs and Safety Issues. 1. INTRODUCTION Purpose Scope Submissions to Australian Sailing:...

CMP Policy - AS i Australian Sailing CMP for Special Regs and Safety Issues 1. INTRODUCTION... 1 1.1. Purpose... 1 1.2. Scope... 1 1.3. Submissions to Australian Sailing:... 1 2. CHANGE MANAGEMENT PROCEDURE

CMP Policy - AS i Australian Sailing CMP for Special Regs and Safety Issues 1. INTRODUCTION... 1 1.1. Purpose... 1 1.2. Scope... 1 1.3. Submissions to Australian Sailing:... 1 2. CHANGE MANAGEMENT PROCEDURE

Quantitative Risk Modelling, Calibration and Continuous Improvement CK UMACHI RISK MANAGEMENT ENGINEER - TIMP PACIFIC GAS & ELECTRIC

Quantitative Risk Modelling, Calibration and Continuous Improvement CK UMACHI RISK MANAGEMENT ENGINEER - TIMP PACIFIC GAS & ELECTRIC Agenda Relative vs Quantitative Risk Models PG&E s Risk Model History

Quantitative Risk Modelling, Calibration and Continuous Improvement CK UMACHI RISK MANAGEMENT ENGINEER - TIMP PACIFIC GAS & ELECTRIC Agenda Relative vs Quantitative Risk Models PG&E s Risk Model History

Tuesday, March 5, 2013 Houston, TX. 2:45 4:00 p.m. ENVIRONMENTAL LIABILITY INSURANCE

Tuesday, March 5, 2013 Houston, TX 2:45 4:00 p.m. ENVIRONMENTAL LIABILITY INSURANCE Presented by Jeffrey M. Hubbard Assistant Vice President, Senior Underwriter XL Insurance Various approaches may be used

Tuesday, March 5, 2013 Houston, TX 2:45 4:00 p.m. ENVIRONMENTAL LIABILITY INSURANCE Presented by Jeffrey M. Hubbard Assistant Vice President, Senior Underwriter XL Insurance Various approaches may be used

Traub Capital Management, LLC. Individualized Money Management

Individualized Money Management Overview: Traub Capital Management Registered Investment Advisor founded in 2003 by Heydon Traub, CFA, CFP * Registered with SEC and use independent custodian to hold assets

Individualized Money Management Overview: Traub Capital Management Registered Investment Advisor founded in 2003 by Heydon Traub, CFA, CFP * Registered with SEC and use independent custodian to hold assets

ERM Mini-Seminar. James Lam President, James Lam & Associates. Sponsored by Society of Actuaries December 9, Filename

ERM Mini-Seminar James Lam President, James Lam & Associates Sponsored by Society of Actuaries December 9, 2003 Filename James Lam s biography Professional President, James Lam & Associates Founder and

ERM Mini-Seminar James Lam President, James Lam & Associates Sponsored by Society of Actuaries December 9, 2003 Filename James Lam s biography Professional President, James Lam & Associates Founder and

MEMORANDUM. To: From: Metrolinx Board of Directors Robert Siddall Chief Financial Officer Date: September 14, 2017 ERM Policy and Framework

MEMORANDUM To: From: Metrolinx Board of Directors Robert Siddall Chief Financial Officer Date: September 14, 2017 Re: ERM Policy and Framework Executive Summary Attached are the draft Enterprise Risk Management

MEMORANDUM To: From: Metrolinx Board of Directors Robert Siddall Chief Financial Officer Date: September 14, 2017 Re: ERM Policy and Framework Executive Summary Attached are the draft Enterprise Risk Management

Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES. Recognized by the Canadian Institute of Actuaries.

Enterprise Risk Management Retirement Benefits Extension Exam ERM-RET Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has

Enterprise Risk Management Retirement Benefits Extension Exam ERM-RET Date: Tuesday, October 30, 2018 Time: 8:30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has

FIN 435 CAPITAL MARKETS AND FIXED INCOME. Spring :30am 9:45am or 4:00pm 5:15pm. Managing Bond Portfolios

FIN 435 CAPITAL MARKETS AND FIXED INCOME Managing Bond Portfolios WHEN Spring 2017 8:30am 9:45am or 4:00pm 5:15pm WHERE SGMH 2308 INTEGRATE A BROAD SET OF BUSINESS RELATED SKILLS INTO AN EFFECTIVE DECISION

FIN 435 CAPITAL MARKETS AND FIXED INCOME Managing Bond Portfolios WHEN Spring 2017 8:30am 9:45am or 4:00pm 5:15pm WHERE SGMH 2308 INTEGRATE A BROAD SET OF BUSINESS RELATED SKILLS INTO AN EFFECTIVE DECISION

1.0 Purpose. Financial Services Commission of Ontario Commission des services financiers de l Ontario. Investment Guidance Notes

Financial Services Commission of Ontario Commission des services financiers de l Ontario SECTION: INDEX NO.: TITLE: APPROVED BY: Investment Guidance Notes IGN-002 Prudent Investment Practices for Derivatives

Financial Services Commission of Ontario Commission des services financiers de l Ontario SECTION: INDEX NO.: TITLE: APPROVED BY: Investment Guidance Notes IGN-002 Prudent Investment Practices for Derivatives

An introduction to Operational Risk

An introduction to Operational Risk John Thirlwell Finance Dublin, 29 March 2006 Setting the scene What is operational risk? Why are we here? The operational risk management framework Basel and the Capital

An introduction to Operational Risk John Thirlwell Finance Dublin, 29 March 2006 Setting the scene What is operational risk? Why are we here? The operational risk management framework Basel and the Capital

Wednesday, March 2, 2016 Houston, TX. 9:30 11:00 a.m. MANAGING AND RESOLVING THE BUSINESS INTERRUPTION CLAIM

Wednesday, March 2, 2016 Houston, TX 9:30 11:00 a.m. MANAGING AND RESOLVING THE BUSINESS INTERRUPTION CLAIM Presented by David Goodwin Partner Covington & Burling Mark O Rear Managing Director Navigant

Wednesday, March 2, 2016 Houston, TX 9:30 11:00 a.m. MANAGING AND RESOLVING THE BUSINESS INTERRUPTION CLAIM Presented by David Goodwin Partner Covington & Burling Mark O Rear Managing Director Navigant

ENMAX CORPORATION 2017 REPORT ON EXECUTIVE COMPENSATION. As of December 31, 2017

ENMAX CORPORATION 2017 REPORT ON EXECUTIVE COMPENSATION As of December 31, 2017 OUR APPROACH TO EXECUTIVE COMPENSATION ENMAX S STRATEGIC DIRECTION ENMAX Corporation (ENMAX) is an energy company headquartered

ENMAX CORPORATION 2017 REPORT ON EXECUTIVE COMPENSATION As of December 31, 2017 OUR APPROACH TO EXECUTIVE COMPENSATION ENMAX S STRATEGIC DIRECTION ENMAX Corporation (ENMAX) is an energy company headquartered

Webinar: Impact of ACOs on MIPS Payments

Webinar: Impact of ACOs on MIPS Payments a HealthcareWebSummit Event, 1PM Eastern, Wednesday, May 17th, 2017 Individual Registration Fee: $95. Post-Event Materials: $45 for attendees; $160 for non-attendees

Webinar: Impact of ACOs on MIPS Payments a HealthcareWebSummit Event, 1PM Eastern, Wednesday, May 17th, 2017 Individual Registration Fee: $95. Post-Event Materials: $45 for attendees; $160 for non-attendees

CNAM Risk Management for Utility Managers

CNAM 2013 Heather McGinnity PEng. Region of Peel Project Manager Roop Lutchman, PEng. GHD Leader, Business Consulting May 07 th, 2013 Agenda 1. Introduction 2. Risk Management Framework 3. Case Study (Lake

CNAM 2013 Heather McGinnity PEng. Region of Peel Project Manager Roop Lutchman, PEng. GHD Leader, Business Consulting May 07 th, 2013 Agenda 1. Introduction 2. Risk Management Framework 3. Case Study (Lake

Applying COSO s Enterprise Risk Management Integrated Framework

Applying COSO s Enterprise Risk Management Integrated Framework COSO COSO stands for the Committee Of Sponsoring Organizations of the Treadway Commission. The sponsoring organizations are: Institute of

Applying COSO s Enterprise Risk Management Integrated Framework COSO COSO stands for the Committee Of Sponsoring Organizations of the Treadway Commission. The sponsoring organizations are: Institute of

Cornerstone US Long/Short Alpha

Cornerstone US Long/Short Alpha Strategy Overview: The investment objective of the Strategy is to earn attractive riskadjusted returns that are uncorrelated with the broad equity market, while seeking

Cornerstone US Long/Short Alpha Strategy Overview: The investment objective of the Strategy is to earn attractive riskadjusted returns that are uncorrelated with the broad equity market, while seeking

RISK MANAGEMENT. Budgeting, d) Timing, e) Risk Categories,(RBS) f) 4. EEF. Definitions of risk probability and impact, g) 5. OPA

Timing, e) Risk Categories,(RBS) f) 4. EEF. Definitions of risk probability and impact, g) 5. OPA") RISK MANAGEMENT 11.1 Plan Risk Management: The process of DEFINING HOW to conduct risk management activities for a project. In Plan Risk Management, the remaining FIVE risk management processes are PLANNED

RISK MANAGEMENT 11.1 Plan Risk Management: The process of DEFINING HOW to conduct risk management activities for a project. In Plan Risk Management, the remaining FIVE risk management processes are PLANNED