Delivering Clarity to Credit Unions Through Expertise and Experience

|

|

|

- Leona Martin

- 5 years ago

- Views:

Transcription

1 Jeff Owen, The Rochdale Group September 2012 Delivering Clarity to Credit Unions Through Expertise and Experience Enterprise Risk Management Lending Execution and Risk Management Merger Strategy and Realization Credit Union Capital Markets Compliance Strategic Planning and Execution Regulatory Response Activity 1

2 AGENDA Introduction to ERM Roles and Responsibilities Risk Appetite Economic Capital Risk Centric Strategic Planning Implementing an ERM Program Introduction to ERM 2

3 What is ERM? a process, effected by an entity's board of directors, management and other personnel, applied in strategy setting and across the enterprise, designed to identify potential events that may affect the entity, and manage risks to be within its risk appetite, to provide reasonable assurance regarding the achievement of entity objectives. Source: COSO Enterprise Risk Management Integrated Framework COSO. 5 What is RISK? 6 3

4 Risk versus Return Risk and return is an inseparable concept Risk Adjusted Return Zone 1 Insufficient Risk Taking Zone 2 Optimal Risk Taking Zone 3 Excessive Risk Taking Risk Level 7 Traditional Risk Management Credit unions are in the business of risk taking Generally has been a silo d approach: Loan underwriting Asset liability management Business continuity Branch security Vendor management All reviewed independently by line management, internal auditors, external auditors and regulators 8 4

5 It is no longer, what did I know It is all about what SHOULD I have known! Risk checklist Compliance assessment Isolated technology solution One time project What ERM is NOT! 5

6 Just to level set, ERM is Strategic and bottom line oriented Much more than a compliance and regulatory activity Intended to provide access to better information in a more timely manner, allowing for enhanced decision making Why ERM? Provides comprehensive view of organizational risk for enhanced decision making Creates value by improving the financial/risk relationship Reduces regulatory burden and improves the relationship with auditors Minimizes organizational/personal liability 12 6

7 A Conceptual View of Risk Management Evolution of ERM Business environment Regulatory pressure Member/consumer expectations Technology Competition Political environment World wide economic crisis 7

8 Science of ERM Involves the methods and processes to identify, measure and manage risks and/or seize opportunities related to the achievement of the organization s goals and objectives Why it Makes Sense Opportunity for sustained success is only as good as the collective ability to make the right decisions Each improved decision positively impacts the brand and financial standing It is impossible to effectively manage what you don t see and measure 8

9 What to Expect from ERM Improved transparency Understanding risk profile Elimination of silos Improved strategic alignment Proactive focus on risk identification and goal accomplishment Risk weighted view of capital adequacy Improved understanding of return on capital deployment What it Takes Commitment of board and management Up front time commitment Establishment of risk management committee Implementation of risk repository and reporting system 9

10 ERM Opportunities Strategic Improve strategy execution and performance Understand capital adequacy Set risk tolerance Management Enhance financial returns Identify prospective emerging risks Provide organizational awareness and cross functional transparency Audit Establish risk weighted focus Support secondary review of controls/response mitigation Regulatory Vet risk management strategy Strengthen communication Justify processes in a practical, pragmatic manner Implementation Project Phase I Set the Stage Phase II Identify and Assess Exposures Phase III Measure and Manage Phase IV Mature 10

11 11

12 12

13 Economic Capital Failures of The Past Lack of transparency Minimal senior management engagement No Board commitment or involvement Reactive risk processes Immature and wavering risk tolerance and risk appetite 13

14 What Credit Unions Say Seize new opportunities (merger, indirect lending) Leverage the risks we are already taking Eliminate silos and brought management team together Provide the board with an enhanced understanding of strategic direction, risk profile of the organization and overall alignment of the organization Ensure appropriate deployment of resources (capital, human, etc.) Key Questions Is your organization consistently operating within an acceptable risk level? Can you confidently list major risks from all across the organization, address their impact on the organization and articulate the current responses to those risks? Do the other key decision makers in the organization agree on your assessment? Do you understand key risks in the current strategic direction and goals? Are you confident that you know all that you should know about your credit union? 14

15 In the End It s about improving financial returns on your efforts and maximizing the deployment of resources by delivering proactive and measured data Roles & Responsibilities 15

16 Fundamental Shift in Thinking 31 Board Key Management Focus Operations What could threaten our survival? What could undermine our strategy? What could derail our project? Strategic Flexibility Strategy Commitment Target Achievement Risk Centric Scenario Planning Strategy Assessment Tactical and Operational Execution Plans 32 16

17 The Board s Role Responsible for setting strategy to maximize member value in a prudent and financially sound manner Comes down to setting and managing objectives in light of key risks within acceptable tolerances ERM provides the information needed to improve strategy and monitoring of results 33 How Should the Board Support ERM? Set risk culture and tone Allocate necessary resources Ensure process diligence Validate risk appetite Understand and balance strategy and risk 34 17

18 Management s Role Understand and communicate risk culture and tone Deploy necessary resources Ensure process diligence Define risk appetite Proactively identify and manage risks Ensure process transparency (vertically and horizontally) Staff s Role Open and honest communication of key risks Awareness of emerging risks Implementation of responses to address unmitigated risks 18

19 Audit and Regulators Review of responses to ensure they are performing as intended Feed key risks back into ERM process BREAK 19

What is our general appetite for risk in different risk categories")

20 Risk Appetite Risk Appetite How much we are willing to lose in one event (setting of individual limits) How much we are willing to risk losing in total (general risk philosophy) What is our general appetite for risk in different risk categories 40 20

21 Risk Appetite Quantitative vs. qualitative We will and/or will not do Bands vs. hard stops Expectations of members Dialogue establish over time 41 Risk Appetite 42 21

22 Risk Appetite 43 Risk Appetite 44 22

, in most cases that success is interconnected with increased opportunity for loss The process of thinking through and assessing the willingness to accept certain types of risk")

23 Risk Appetite In summary While there are a range of outcomes the credit union could experience, there are limits that help define the preferred risk appetite While we all desire and hope for the most positive outcome(s), in most cases that success is interconnected with increased opportunity for loss The process of thinking through and assessing the willingness to accept certain types of risk provides general direction to the credit union as it strives to achieve its objectives 45 Risk Appetite Slightly favor existing over prospective members 23

24 Risk Appetite Example Risk Statements: Credit Union will fully understand program risk before launch Credit Union has a very low risk tolerance to regulatory non compliance, but will not back down from challenging examiners when appropriate Credit Union seeks to exploit technology by rapidly deploying stable technologies Credit Union seeks to be innovative in process and conservative in practice 47 Risk Appetite Prepare risk appetite statements within each of the risk areas: Strategic: Offer a reasonable range of services, at average prices, with a concentration on existing members. Provide examples of actions that match/conflict with the statements, trying to tie in some of the credit union s actual exposures: This might fit the appetite: Offer indirect lending rates within 0.25% of competitor rates This doesn t fit the appetite: Advertise loan specials that undercut competitor rates by 1% or more 24

25 Risk Appetite Exercise Risk categories o Strategic o Transaction o Compliance o Reputation o o o Credit Liquidity Interest Rate What are some example risk statements of high willingness to accept risk under each category, and examples of low willingness to accept risk under each category What are some examples of actions within each 49 Economic Capital 25

26 Introduction to Economic Capital Economic capital is an estimate of the equity needed to survive a near worst case loss scenario Financial institutions assess economic capital for several reasons Multiple approaches to economic capital 51 Economic Capital Ratio Recommend comparing a credit union s actual capital to its economic capital: Economic Capital Ratio = Actual Capital / Economic Capital A credit union s risk appetite helps determine the target level for each credit union You could use economic capital in conjunction with your risk appetite to set an overall risk limit for the credit union 52 26

27 Economic Capital Ratio Assume you have $16 million in capital, $200 million in assets and economic capital of $10 million (Ratio of actual to economic capital = 1.60) Next, assume your risk appetite is such that the lowest capital class you would accept even after a near worst case loss scenario is undercapitalized, or a minimum net worth ratio of 4% 53 Economic Capital Ratio Risk and capital calculations: Current capital $16 million Less: Economic capital 10 million Less: minimum capital level at 4% 8 million Excess (Deficit) capital ($2 million) This means that the credit union has insufficient capital given its risk level and risk appetite 54 27

28 ERM and Strategic Planning Risk Centric Strategic Planning Uses long term orientation Identifies key risk scenarios that might affect the credit union s business model, results or other operating parameters Identifies impact, likelihood and velocity of each scenario Considers ability of current strategic positioning to address each scenario Arrives at key focus issues to ensure long term success 28

29 Risk Centric Strategic Planning Take a few minutes to work individually Identify and write down 10 long term issues for credit unions Rate the potential impact of each issue: From 1 (low) to 10 (high) Assess the likelihood of each situation over the next 10 years: From 1 (unlikely) to 10 (certain) Estimate the velocity of occurrence: From 1 (the issue will occur slowly) to 10 (quickly) Afterward, we will discuss the various issues and severity (I x L x V) of each scenario Follow up Compare the long term scenarios identified against the current environment at your credit union: Strategic objectives and implementation plans Existing risk responses at the credit union Assess the degree of alignment of the objectives and responses in addressing the key scenarios Make changes in the strategic objectives, implementation plans, and risk responses to better position the credit union to focus on and address the scenarios 29

30 Scenarios From Past Credit Union Conference Scenario Average Impact Average Likelihood Average Velocity Response Count I x L x V Access to market liquidity Technology Security Succession Planning BOD/Mgt Long term Rate Depression Over Regulation NCUSIF Losses Inflationary / Rising Rates Loss of Mortgage Agencies Profitability Concerns Technology Mobile Terrorism Increased BOD Requirements Inability to maintain loan growth Economic Recession Charter consolidation (CU& Bank) Environmental crisis CU mergers Technology Web Membership Lose Boomers Membership Attract Gen Y Increased Non Traditional Competition BREAK 30

31 Implementing an ERM Program: Taking it Back Functional Area Risk Assessment Identify significant operating/admin areas Conduct ERM session for each area, including a discussion of the risks that can influence the area s or the credit union s ability to meet its objectives 62 31

32 Risk Identification Identify the material events, having negative consequences, that can transpire within the functional area s responsibility: Exposures, uncertainties and missed opportunities Consider internal and external factors: Natural disasters to employee fraud Develop scenarios to demonstrate each risk Primary Risk Categories Potential impacts on earnings or capital from: Reputation Strategic Adverse business decisions, improper implementation of decisions, or lack of responsiveness to industry changes Negative public opinion or perception Compliance Violations of, or nonconformance with, laws, rules, regulations, prescribed practices, internal policies and procedures, or ethical standards Liquidity Operational/ Transaction Fraud or error that results in an inability to deliver products or services, maintain a competitive position, and manage information Credit Failure of obligor to repay loan or investment Inability to meet obligations when they come due, without incurring material costs or unacceptable losses Interest Rate Changes in interest rates and rate relationships 64 32

33 Assessment Factors Impact Potential magnitude, in the absence of responses, measured consistently against assets and capital Likelihood The frequency with which an event may occur in a given time period, again in the absence of responses Mitigation The degree to which the organization s responses manage down the impact or likelihood

34 Controls Over Responses Actual processing often differs from documented procedures Controls help ensure that responses to risks are carried out as intended Examples include policies and procedures, internal audit reviews, etc. During the sessions, you will likely discuss the controls that support the responses: However, the initial ERM implementation is not intended as an audit of the controls over risk responses Inherent Versus Residual Risk Inherent Risk = Impact x Likelihood: This is the exposure before responses Residual Risk = Inherent Risk x Mitigation: Exposure after responses The difference is the benefit of the responses This approach supports cost benefit analysis of the credit union s responses 68 34

35 Global Scenarios Some risks affect all areas of the organization: Business continuity events Significant changes in external factors that influence the credit union The ERM team should ask all areas to assess the potential impacts of and responses to such scenarios The result will be valuable information to support the BCP and ALM processes Risk Management Committee Forum to discuss risk issues Cross-functional composition to provide multidimensional view across credit union Monthly or quarterly meetings Generally reports to the Board or a Board committee Often combined with ALCO, business priorities, credit or other committee 35

36 Periodic ERM Reporting Reporting usually involves two primary mechanisms: Risk Management Committee packets Board and senior management ERM reports RMCO packets: Agenda Minutes Risk Action Plan (list of key risks being monitored with updates) 36

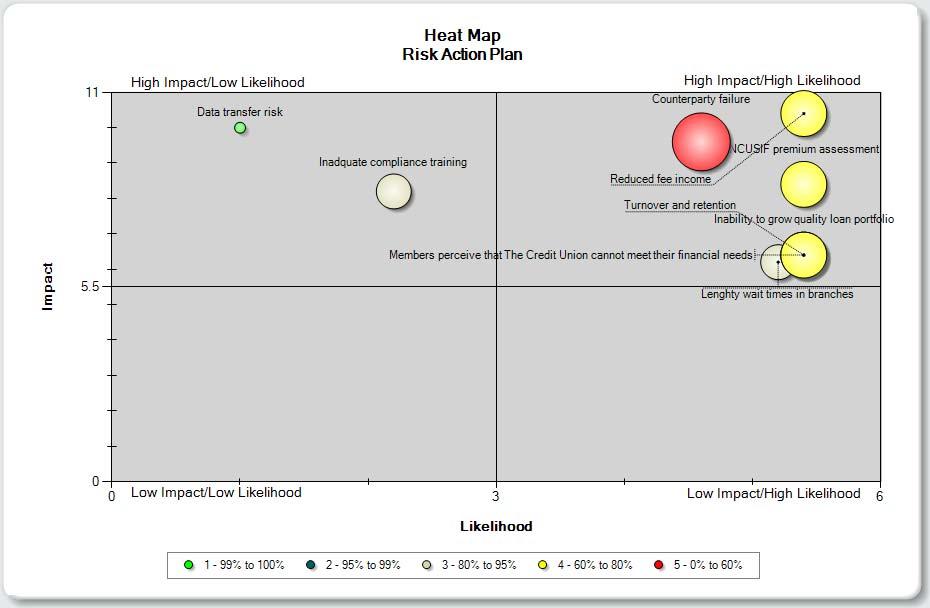

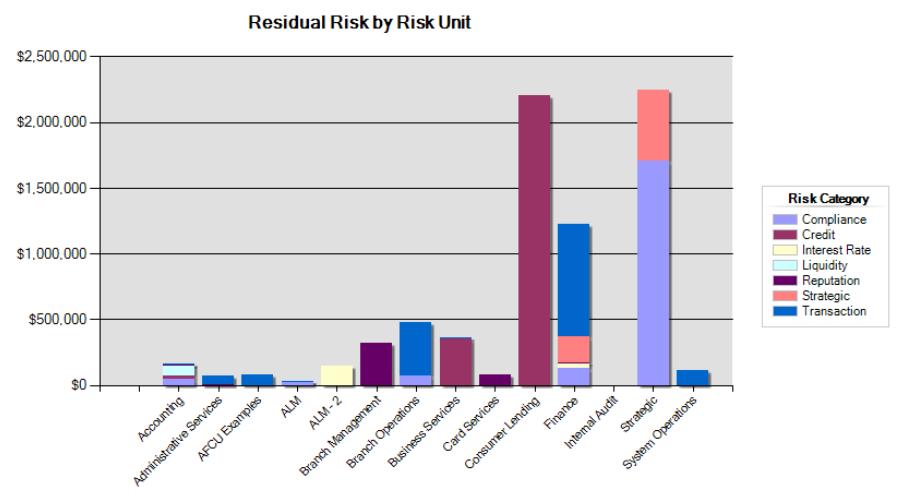

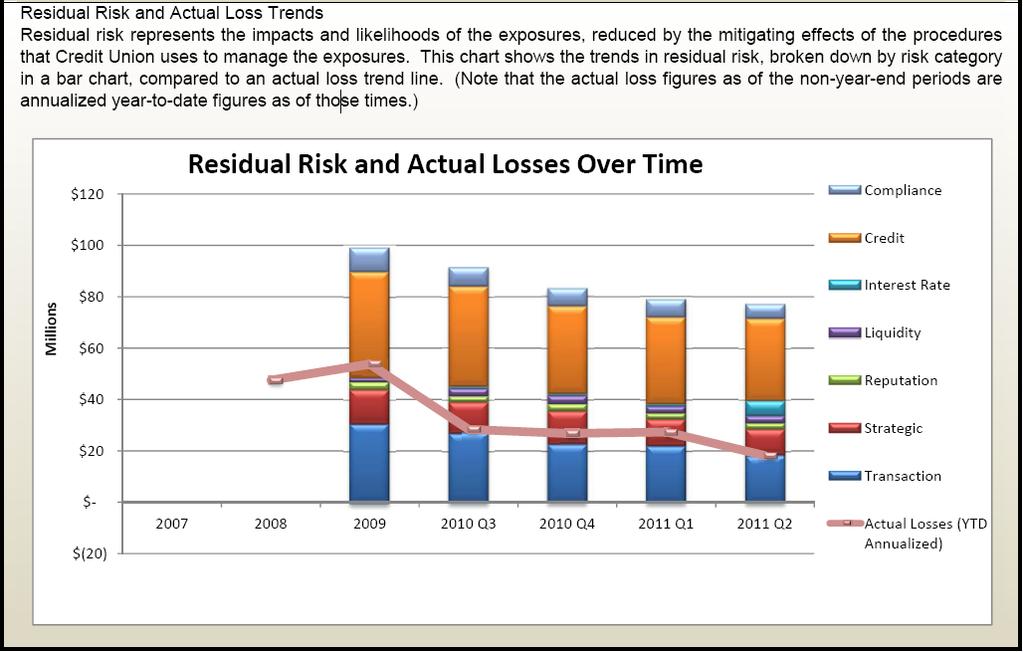

37 Board and Senior Management Reports Goal is to present the credit union s overall risk profile Begin report with a brief narrative of the overall risk position, status of ERM process, and major increases and decreases in exposures Next, include several additional ERM reports: Strategic area heat map Largest Residual Risk Exposures by Risk Category report Emerging Risks report Residual Risk by Risk Unit report Qualitative Measures Risk Action Plan 37

38 38

39 39

40 ERM Policy Department Procedures Training Materials ERM Reporting Templates ERM Committee Materials Other Key Components 40

41 To Summarize: It s about improving financial returns on your efforts and maximizing the deployment of resources by delivering proactive and measured data Start somewhere Begin small and allow the process to mature over time Get board, management and staff engaged Questions Jeff Owen The Rochdale Group jowen@rochdalegroup.com 41

An Introduction to Enterprise Risk Management. Mark Brown, SVP, Chief Financial Officer First Carolina Corporate Credit Union

An Introduction to Enterprise Risk Management Mark Brown, SVP, Chief Financial Officer First Carolina Corporate Credit Union Introduction Mark Brown First Carolina Corporate Credit Union, SVP/CFO since

An Introduction to Enterprise Risk Management Mark Brown, SVP, Chief Financial Officer First Carolina Corporate Credit Union Introduction Mark Brown First Carolina Corporate Credit Union, SVP/CFO since

ก ก Tools and Techniques for Enterprise Risk Management (ERM)

") ก ก Tools and Techniques for Enterprise Risk Management (ERM) COSO ERM ISO ERM 31 2554 10:45 12:15.. 301, 302, 307 ก ก COSO Internal Control ERM Integrated Framework Application Technique ISO 31000 Guide

ก ก Tools and Techniques for Enterprise Risk Management (ERM) COSO ERM ISO ERM 31 2554 10:45 12:15.. 301, 302, 307 ก ก COSO Internal Control ERM Integrated Framework Application Technique ISO 31000 Guide

Applying COSO s Enterprise Risk Management Integrated Framework. September 29, 2004

Applying COSO s Enterprise Risk Management Integrated Framework September 29, 2004 Today s organizations are concerned about: Risk Management Governance Control Assurance (and Consulting) ERM Defined:

Applying COSO s Enterprise Risk Management Integrated Framework September 29, 2004 Today s organizations are concerned about: Risk Management Governance Control Assurance (and Consulting) ERM Defined:

Working through Risk Appetite

28 th National Risk Management Training Conference Working through Risk Appetite Marilyn Smith Head U.S. Policy & Governance BMO Financial Corp./BMO Harris Bank Fiduciary Governance April 30 2013 Working

28 th National Risk Management Training Conference Working through Risk Appetite Marilyn Smith Head U.S. Policy & Governance BMO Financial Corp./BMO Harris Bank Fiduciary Governance April 30 2013 Working

BERGRIVIER MUNICIPALITY. Risk Management Risk Appetite Framework

BERGRIVIER MUNICIPALITY Risk Management Risk Appetite Framework APRIL 2018 1 Document review and approval Revision history Version Author Date reviewed 1 2 3 4 5 This document has been reviewed by Version

BERGRIVIER MUNICIPALITY Risk Management Risk Appetite Framework APRIL 2018 1 Document review and approval Revision history Version Author Date reviewed 1 2 3 4 5 This document has been reviewed by Version

ACUIA Region 3 Meeting Enterprise Risk Management. Henry Robaszewski Director of Risk Management October 7, 2016

ACUIA Region 3 Meeting Enterprise Risk Management Henry Robaszewski Director of Risk Management October 7, 2016 Henry Robaszewski, Director of Risk Management Joined BCU in 2008 In Finance Department,

ACUIA Region 3 Meeting Enterprise Risk Management Henry Robaszewski Director of Risk Management October 7, 2016 Henry Robaszewski, Director of Risk Management Joined BCU in 2008 In Finance Department,

Applying COSO s Enterprise Risk Management Integrated Framework

Applying COSO s Enterprise Risk Management Integrated Framework COSO COSO stands for the Committee Of Sponsoring Organizations of the Treadway Commission. The sponsoring organizations are: Institute of

Applying COSO s Enterprise Risk Management Integrated Framework COSO COSO stands for the Committee Of Sponsoring Organizations of the Treadway Commission. The sponsoring organizations are: Institute of

Summary Enterprise Risk Management Framework

Summary Enterprise Risk Management Framework Last Updated: September 26, 2016 CONTENTS I. Overview II. III. Risk Management Philosophy General Risk Management Activities Board of Directors Risk Management

Summary Enterprise Risk Management Framework Last Updated: September 26, 2016 CONTENTS I. Overview II. III. Risk Management Philosophy General Risk Management Activities Board of Directors Risk Management

ENTERPRISE RISK MANAGEMENT (ERM) POLICY Republic Glass Holdings Corporation. Purpose. Goals

POLICY Republic Glass Holdings Corporation. Purpose. Goals") Purpose This Enterprise Risk Management Policy (the ERM policy) provides the framework for managing risks across ( RGHC or the Company ). It contains the policies to guide employees, management and the

Purpose This Enterprise Risk Management Policy (the ERM policy) provides the framework for managing risks across ( RGHC or the Company ). It contains the policies to guide employees, management and the

New Products and Business Initiatives. 27th National Risk Management Training Conference

New Products and Business Initiatives 27th National Risk Management Training Conference Gregory J. Lyons May 1, 2013 Agenda Succeeding in a difficult regulatory environment Why offer, when, and who should

New Products and Business Initiatives 27th National Risk Management Training Conference Gregory J. Lyons May 1, 2013 Agenda Succeeding in a difficult regulatory environment Why offer, when, and who should

Enterprise Risk Management Integrated Framework

ISACA S IT Audit, Information Security & Risk Insights Africa 2014, Alisa Hotel Enterprise Risk Management Integrated Framework Tony Bediako May 20, 2014 Today s organizations are concerned about: Risk

ISACA S IT Audit, Information Security & Risk Insights Africa 2014, Alisa Hotel Enterprise Risk Management Integrated Framework Tony Bediako May 20, 2014 Today s organizations are concerned about: Risk

ENTERPRISE RISK MANAGEMENT Framework

STANDARDS OF SOUND BUSINESS AND FINANCIAL PRACTICES ENTERPRISE RISK MANAGEMENT Framework January 2018 Ce document est également disponible en français. Notice This document is intended as a reference tool

STANDARDS OF SOUND BUSINESS AND FINANCIAL PRACTICES ENTERPRISE RISK MANAGEMENT Framework January 2018 Ce document est également disponible en français. Notice This document is intended as a reference tool

FIRMA Nashville Tennessee April 21, 2015

FIRMA Nashville Tennessee April 21, 2015 Brian J. Pinkerton T. Kevin Whalen Enterprise risk management (ERM) is the process of planning, organizing, leading, and controlling the activities of an organization

FIRMA Nashville Tennessee April 21, 2015 Brian J. Pinkerton T. Kevin Whalen Enterprise risk management (ERM) is the process of planning, organizing, leading, and controlling the activities of an organization

Aligning Risk Management with CU Business Strategy

Aligning Risk Management with CU Business Strategy Managing your most pressing risks CUNA Mutual Group Proprietary Reproduction, Adaptation or Distribution Prohibited 2016 CUNA Mutual Group, All Rights

Aligning Risk Management with CU Business Strategy Managing your most pressing risks CUNA Mutual Group Proprietary Reproduction, Adaptation or Distribution Prohibited 2016 CUNA Mutual Group, All Rights

The Components of a Sound Emerging Risk Management Framework

North American CRO Council The Components of a Sound Emerging Risk Management Framework December 6, 2012 2012 North American CRO Council Incorporated chairperson@crocouncil.org North American CRO Council

North American CRO Council The Components of a Sound Emerging Risk Management Framework December 6, 2012 2012 North American CRO Council Incorporated chairperson@crocouncil.org North American CRO Council

Best Practices in ENTERPRISE RISK MANAGEMENT. [ Managing Risks Holistically ]

![Best Practices in ENTERPRISE RISK MANAGEMENT. [ Managing Risks Holistically ]](/thumbs/96/127953398.jpg "Best Practices in ENTERPRISE RISK MANAGEMENT. [ Managing Risks Holistically ]") Best Practices in ENTERPRISE RISK MANAGEMENT [ Managing Risks Holistically ] INTRODUCTIONS MODERATOR: Bob Lipps, JD, CPA PANELISTS: Ron Wilcox Abel Pomar Karen Gordon, Esq. THE EVOLUTION OF RISK Traditional

Best Practices in ENTERPRISE RISK MANAGEMENT [ Managing Risks Holistically ] INTRODUCTIONS MODERATOR: Bob Lipps, JD, CPA PANELISTS: Ron Wilcox Abel Pomar Karen Gordon, Esq. THE EVOLUTION OF RISK Traditional

Perpetual s Risk Management Framework

Perpetual s Risk Management Framework Perpetual s Risk Management Framework Context Perpetual Limited (Perpetual) is a diversified financial services firm, listed on the Australian Securities Exchange.

Perpetual s Risk Management Framework Perpetual s Risk Management Framework Context Perpetual Limited (Perpetual) is a diversified financial services firm, listed on the Australian Securities Exchange.

RISK OVERSIGHT COMMITTEE CHARTER

RISK OVERSIGHT COMMITTEE CHARTER I. PURPOSE The Risk Oversight Committee has been established by the Board of Directors to assist it in the effective discharge of its function in overseeing the risk management

RISK OVERSIGHT COMMITTEE CHARTER I. PURPOSE The Risk Oversight Committee has been established by the Board of Directors to assist it in the effective discharge of its function in overseeing the risk management

Summary of Risk Management Policy PT Bank CIMB Niaga Tbk

Summary of Risk Management Policy PT Bank CIMB Niaga Tbk The Policy is effective since obtain approval from the Board of Commisssioner (BoC) in May 2018 Risk management is an essential part of operational

Summary of Risk Management Policy PT Bank CIMB Niaga Tbk The Policy is effective since obtain approval from the Board of Commisssioner (BoC) in May 2018 Risk management is an essential part of operational

Sections of the ORSA Report

Lessons Learned From Orsa Reviews Impact on Risk Focused Examination NAIC Insurance Summit INS Companies Joe Fritsch, Director INS Companies Don Carbone, Exam Manager INS Companies Sections of the ORSA

Lessons Learned From Orsa Reviews Impact on Risk Focused Examination NAIC Insurance Summit INS Companies Joe Fritsch, Director INS Companies Don Carbone, Exam Manager INS Companies Sections of the ORSA

GOV : Enterprise Risk Management Policy

Name: Responsibility: Complements: Enterprise Risk Management Framework Coordinator, Enterprise Risk Management GOV-080-005: Enterprise Risk Management Policy Draft Date: November 2006; January 2012 Revised

Name: Responsibility: Complements: Enterprise Risk Management Framework Coordinator, Enterprise Risk Management GOV-080-005: Enterprise Risk Management Policy Draft Date: November 2006; January 2012 Revised

Enterprise Risk Management (ERM) & Compliance

& Compliance") Enterprise Risk Management (ERM) & Compliance Mid Atlantic Regional Meeting, May 1, 2015 Society of Corporate Compliance and Ethics Jason Lunday, consultant Compliance Opportunities in ERM Increase compliance

Enterprise Risk Management (ERM) & Compliance Mid Atlantic Regional Meeting, May 1, 2015 Society of Corporate Compliance and Ethics Jason Lunday, consultant Compliance Opportunities in ERM Increase compliance

Procedures for Management of Risk

Procedures for Management of Policy Sponsor: Name of Parent Policy: Policy Contact: Procedure Contact: Vice President Finance and Administration Enterprise Management Policy Vice President Finance and

Procedures for Management of Policy Sponsor: Name of Parent Policy: Policy Contact: Procedure Contact: Vice President Finance and Administration Enterprise Management Policy Vice President Finance and

ENTERPRISE RISK MANAGEMENT (ERM) GOVERNANCE POLICY PEDERNALES ELECTRIC COOPERATIVE, INC.

GOVERNANCE POLICY PEDERNALES ELECTRIC COOPERATIVE, INC.") 1. Purpose: 1.1. Pedernales Electric Cooperative ( PEC ) is committed to delivering low-cost, reliable and safe energy solutions for the benefit of our members. In order to improve the likelihood of achieving

1. Purpose: 1.1. Pedernales Electric Cooperative ( PEC ) is committed to delivering low-cost, reliable and safe energy solutions for the benefit of our members. In order to improve the likelihood of achieving

360 Degrees of Enterprise Risk Management

360 Degrees of Enterprise Risk Management Monday, June 17, 2013 2:00 PM 3:15 PM Presented by: Jennifer F. Burke Partner Crowe Horwath LLP 144 N. Broadway Lexington, KY 40507 859.280.5160 (o) 859.221.2613

360 Degrees of Enterprise Risk Management Monday, June 17, 2013 2:00 PM 3:15 PM Presented by: Jennifer F. Burke Partner Crowe Horwath LLP 144 N. Broadway Lexington, KY 40507 859.280.5160 (o) 859.221.2613

Navigating the New Normal Enterprise Risk Management After e-risk Identification and Assessment

Navigating the New Normal Enterprise Risk Management After e-risk Identification and Assessment Agenda ERM After e-ria ERM Level Setting ERM Fundamentals So Now What? Next-Step Considerations Overview

Navigating the New Normal Enterprise Risk Management After e-risk Identification and Assessment Agenda ERM After e-ria ERM Level Setting ERM Fundamentals So Now What? Next-Step Considerations Overview

Kidsafe NSW Risk Management Plan. August 2014

Kidsafe NSW Risk Management Plan August 2014 Document Control Document Approval Name & Position Signature Date Document Version Control Version Status Date Prepared By Comments Document Reviewers Name

Kidsafe NSW Risk Management Plan August 2014 Document Control Document Approval Name & Position Signature Date Document Version Control Version Status Date Prepared By Comments Document Reviewers Name

Energize Your Enterprise Risk Management

Energize Your Enterprise Risk Management Presented By Mark Caiazzo, CISA, CISM, CRISC Tammy Michaud, CPA May 15, 2017 Reviewed: Agenda Enterprise Risk Management Defined Benefits of ERM Key Components

Energize Your Enterprise Risk Management Presented By Mark Caiazzo, CISA, CISM, CRISC Tammy Michaud, CPA May 15, 2017 Reviewed: Agenda Enterprise Risk Management Defined Benefits of ERM Key Components

RESERVE BANK OF MALAWI

RESERVE BANK OF MALAWI GUIDELINES ON INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS (ICAAP) Bank Supervision Department March 2013 Table of Contents 1.0 INTRODUCTION... 2 2.0 MANDATE... 2 3.0 RATIONALE...

RESERVE BANK OF MALAWI GUIDELINES ON INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS (ICAAP) Bank Supervision Department March 2013 Table of Contents 1.0 INTRODUCTION... 2 2.0 MANDATE... 2 3.0 RATIONALE...

Fraud Risk Management

Fraud Risk Management Fraud Risk Assessment Part 2 2017 Association of Certified Fraud Examiners, Inc. Fraud Risk Assessment Frameworks Frameworks are helpful for performing, evaluating, and reporting

Fraud Risk Management Fraud Risk Assessment Part 2 2017 Association of Certified Fraud Examiners, Inc. Fraud Risk Assessment Frameworks Frameworks are helpful for performing, evaluating, and reporting

RISK COMMITTEE TERMS OF REFERENCE. The Board has resolved to establish a Committee of the Board to be known as the Risk Committee.

RISK COMMITTEE TERMS OF REFERENCE Constitution The Board has resolved to establish a Committee of the Board to be known as the Risk Committee. Objective To identify and monitor risks to the Society s strategy,

RISK COMMITTEE TERMS OF REFERENCE Constitution The Board has resolved to establish a Committee of the Board to be known as the Risk Committee. Objective To identify and monitor risks to the Society s strategy,

Utah Bankers Association Executive Development Program Audit and Compliance Risk Management: The Continuous Program Cycle

Utah Bankers Association Executive Development Program Audit and Compliance Risk Management: The Continuous Program Cycle Presenter: David McCrea Manager U.S. Compliance Program Finacle/EdgeVerve Competition

Utah Bankers Association Executive Development Program Audit and Compliance Risk Management: The Continuous Program Cycle Presenter: David McCrea Manager U.S. Compliance Program Finacle/EdgeVerve Competition

Susan Schmidt Bies: Enterprise perspectives in financial institution supervision

Susan Schmidt Bies: Enterprise perspectives in financial institution supervision Remarks by Ms Susan Schmidt Bies, Member of the Board of Governors of the US Federal Reserve System, at the University of

Susan Schmidt Bies: Enterprise perspectives in financial institution supervision Remarks by Ms Susan Schmidt Bies, Member of the Board of Governors of the US Federal Reserve System, at the University of

Insurance Contracts for 831(b) Enterprise Risk Captives Policies and Pooling Agreements

Enterprise Risk Captives Policies and Pooling Agreements") Insurance Contracts for 831(b) Enterprise Risk Captives Policies and Pooling Agreements Jeffrey K. Simpson John R. Capasso Brian Johnson Gordon, Fournaris & Mammarella, P.A. Captive Planning Associates,

Insurance Contracts for 831(b) Enterprise Risk Captives Policies and Pooling Agreements Jeffrey K. Simpson John R. Capasso Brian Johnson Gordon, Fournaris & Mammarella, P.A. Captive Planning Associates,

Certified Enterprise Risk Professional (CERP) Test Content Outline

Test Content Outline") Certified Enterprise Risk Professional (CERP) Test Content Outline SECTION 1: RISK GOVERNANCE Domain 1: Board and Senior Management Oversight (8%) Task 1: Provide relevant, timely, and accurate information

Certified Enterprise Risk Professional (CERP) Test Content Outline SECTION 1: RISK GOVERNANCE Domain 1: Board and Senior Management Oversight (8%) Task 1: Provide relevant, timely, and accurate information

Basel II Pillar 3- Qualitative Disclosure

Basel II Pillar 3- Qualitative Disclosure 1. Scope This qualitative disclosure applies to Alinma bank, Saudi Arabia. Alinma bank is a Saudi joint stock company formed in accordance with Royal Decree No.

Basel II Pillar 3- Qualitative Disclosure 1. Scope This qualitative disclosure applies to Alinma bank, Saudi Arabia. Alinma bank is a Saudi joint stock company formed in accordance with Royal Decree No.

ENTERPRISE RISK MANAGEMENT (ERM) The Conceptual Framework

The Conceptual Framework") ENTERPRISE RISK MANAGEMENT (ERM) The Conceptual Framework ENTERPRISE RISK MANAGEMENT (ERM) ERM Definition The Conceptual Frameworks: CAS and COSO Risk Categories Implementing ERM Why ERM? ERM Maturity

ENTERPRISE RISK MANAGEMENT (ERM) The Conceptual Framework ENTERPRISE RISK MANAGEMENT (ERM) ERM Definition The Conceptual Frameworks: CAS and COSO Risk Categories Implementing ERM Why ERM? ERM Maturity

The OCEG Open Risk Classification using XBRL

The OCEG Open Risk Classification using XBRL Yuji Furusho Fujitsu Research Institute Agenda Overview Governance Risk and Compliance Brief Introduction Standards Initiatives Business Standards, XBRL and

The OCEG Open Risk Classification using XBRL Yuji Furusho Fujitsu Research Institute Agenda Overview Governance Risk and Compliance Brief Introduction Standards Initiatives Business Standards, XBRL and

MEMORANDUM. To: From: Metrolinx Board of Directors Robert Siddall Chief Financial Officer Date: September 14, 2017 ERM Policy and Framework

MEMORANDUM To: From: Metrolinx Board of Directors Robert Siddall Chief Financial Officer Date: September 14, 2017 Re: ERM Policy and Framework Executive Summary Attached are the draft Enterprise Risk Management

MEMORANDUM To: From: Metrolinx Board of Directors Robert Siddall Chief Financial Officer Date: September 14, 2017 Re: ERM Policy and Framework Executive Summary Attached are the draft Enterprise Risk Management

RISK APPETITE OVERVIEW

PUBLIC SECTOR PENSION INVESTMENT BOARD ( PSP INVESTMENTS ) RISK APPETITE OVERVIEW February 10, 2017 PSP-Legal 2684702-1 Introduction Maintaining a risk aware culture in which undue risks are avoided and

PUBLIC SECTOR PENSION INVESTMENT BOARD ( PSP INVESTMENTS ) RISK APPETITE OVERVIEW February 10, 2017 PSP-Legal 2684702-1 Introduction Maintaining a risk aware culture in which undue risks are avoided and

Draft Guideline. Corporate Governance. Category: Sound Business and Financial Practices. I. Purpose and Scope of the Guideline. Date: November 2017

Draft Guideline Subject: Category: Sound Business and Financial Practices Date: November 2017 I. Purpose and Scope of the Guideline This guideline communicates OSFI s expectations with respect to corporate

Draft Guideline Subject: Category: Sound Business and Financial Practices Date: November 2017 I. Purpose and Scope of the Guideline This guideline communicates OSFI s expectations with respect to corporate

Amex Bank of Canada. Basel III Pillar III Disclosures December 31, AXP Internal Page 1 of 15

December 31, 2013 AXP Internal Page 1 of 15 Table of Contents 1 Scope of application 3 2 Capital structure and adequacy 4 3 Credit risk management 6 4 Asset liability management 11 Structural interest

December 31, 2013 AXP Internal Page 1 of 15 Table of Contents 1 Scope of application 3 2 Capital structure and adequacy 4 3 Credit risk management 6 4 Asset liability management 11 Structural interest

Executive Board Annual Session Rome, May 2015 POLICY ISSUES ENTERPRISE RISK For approval MANAGEMENT POLICY WFP/EB.A/2015/5-B

Executive Board Annual Session Rome, 25 28 May 2015 POLICY ISSUES Agenda item 5 For approval ENTERPRISE RISK MANAGEMENT POLICY E Distribution: GENERAL WFP/EB.A/2015/5-B 10 April 2015 ORIGINAL: ENGLISH

Executive Board Annual Session Rome, 25 28 May 2015 POLICY ISSUES Agenda item 5 For approval ENTERPRISE RISK MANAGEMENT POLICY E Distribution: GENERAL WFP/EB.A/2015/5-B 10 April 2015 ORIGINAL: ENGLISH

Business Auditing - Enterprise Risk Management. October, 2018

Business Auditing - Enterprise Risk Management October, 2018 Contents The present document is aimed to: 1 Give an overview of the Risk Management framework 2 Illustrate an ERM model Page 2 What is a risk?

Business Auditing - Enterprise Risk Management October, 2018 Contents The present document is aimed to: 1 Give an overview of the Risk Management framework 2 Illustrate an ERM model Page 2 What is a risk?

Enterprise Risk Management

Enterprise Risk Management Navigating the Enterprise Risk Management Landscape Alp E. Can Director of Enterprise Risk Management, FHLBank Atlanta North Carolina Bankers Association August 31, 2016 Building

Enterprise Risk Management Navigating the Enterprise Risk Management Landscape Alp E. Can Director of Enterprise Risk Management, FHLBank Atlanta North Carolina Bankers Association August 31, 2016 Building

UNITED NATIONS JOINT STAFF PENSION FUND. Enterprise-wide Risk Management Policy

UNITED NATIONS JOINT STAFF PENSION FUND Enterprise-wide Risk Management Policy 15 April 2016 Page 1 Table of Contents Page Preface I. Introduction 3 II. Definition 4 III. UNSJFP Enterprise-wide Risk Management

UNITED NATIONS JOINT STAFF PENSION FUND Enterprise-wide Risk Management Policy 15 April 2016 Page 1 Table of Contents Page Preface I. Introduction 3 II. Definition 4 III. UNSJFP Enterprise-wide Risk Management

Understanding Enterprise Risk Management: An Overview

Understanding Enterprise Risk Management: An Overview 05/2016 What is Risk? An uncertain event It exists in the future Has a cause and effect Impacts objectives Its effect may be positive and/or negative

Understanding Enterprise Risk Management: An Overview 05/2016 What is Risk? An uncertain event It exists in the future Has a cause and effect Impacts objectives Its effect may be positive and/or negative

Business Continuity Management and ERM

Business Continuity Management and ERM Partnership for Emergency Planning Kansas City Marshall Toburen GRC Strategist ERM, ORM, 3PM RSA A division of EMC 2 June 18, 2014 1 Agenda Intro State of ERM Today

Business Continuity Management and ERM Partnership for Emergency Planning Kansas City Marshall Toburen GRC Strategist ERM, ORM, 3PM RSA A division of EMC 2 June 18, 2014 1 Agenda Intro State of ERM Today

Pillar 3 Disclosure Statement

Pillar 3 Disclosure Statement Last Updated: December, 2017 Disclosure Statement This Pillar 3 Disclosure as at September 30, 2017 contains statements that are considered "forwardlooking statements," including

Pillar 3 Disclosure Statement Last Updated: December, 2017 Disclosure Statement This Pillar 3 Disclosure as at September 30, 2017 contains statements that are considered "forwardlooking statements," including

Guidance Note. Securitization. March Ce document est aussi disponible en français. Revised in October 2018

Guidance Note Securitization March 2018 Revised in October 2018 Ce document est aussi disponible en français. Applicability The Guidance Note: Securitization (Guidance Note) is for use by all credit unions

Guidance Note Securitization March 2018 Revised in October 2018 Ce document est aussi disponible en français. Applicability The Guidance Note: Securitization (Guidance Note) is for use by all credit unions

Risk Management. Policy No. 14. Document uncontrolled when printed DOCUMENT CONTROL. SSAA Vic

Document uncontrolled when printed Policy No. 14 Risk Management DOCUMENT CONTROL Version: Date approved by Board: On behalf of Board: Jack Wegman 17 March 2015 26 March 2015 Denis Moroney President Next

Document uncontrolled when printed Policy No. 14 Risk Management DOCUMENT CONTROL Version: Date approved by Board: On behalf of Board: Jack Wegman 17 March 2015 26 March 2015 Denis Moroney President Next

ITrade Global (CY) Ltd Regulated by the Cyprus Securities and Exchange Commission License no. 298/16

Ltd Regulated by the Cyprus Securities and Exchange Commission License no. 298/16") Regulated by the Cyprus Securities and Exchange Commission License no. 298/16 DISCLOSURE AND MARKET DISCIPLINE REPORT FOR 2017 April 2018 Contents 1. INTRODUCTION 3 1.1. THE COMPANY 4 1.2. REGULATORY SUPERVISION

Regulated by the Cyprus Securities and Exchange Commission License no. 298/16 DISCLOSURE AND MARKET DISCIPLINE REPORT FOR 2017 April 2018 Contents 1. INTRODUCTION 3 1.1. THE COMPANY 4 1.2. REGULATORY SUPERVISION

Enterprise Risk Management (ERM)

") Southeastern Actuaries Conference Enterprise Risk Management (ERM) November 16, 2007 ING. Your future. Made easier. Agenda ERM Are you doing it? Definition of ERM What is it? Industry Overview What is

Southeastern Actuaries Conference Enterprise Risk Management (ERM) November 16, 2007 ING. Your future. Made easier. Agenda ERM Are you doing it? Definition of ERM What is it? Industry Overview What is

ERM + STRATEGIC PLANNING. February 2016 IBAT

ERM + STRATEGIC PLANNING February 2016 IBAT RISK CATEGORIES OCC defines eight categories + three Credit Risk Interest Rate Risk Liquidity Risk Operational Risk Price Risk Compliance Risk Strategic Risk

ERM + STRATEGIC PLANNING February 2016 IBAT RISK CATEGORIES OCC defines eight categories + three Credit Risk Interest Rate Risk Liquidity Risk Operational Risk Price Risk Compliance Risk Strategic Risk

What Is Asset/Liability Management?

A BEGINNERS GUIDE TO ASSET\LIABILITY MANAGEMENT, RISK APPETITE AND CAPITAL PLANNING David Koch President\CEO dkoch@farin.com 800-236-3724 ext. 4217 What Is Asset/Liability Management? Asset/liability management

A BEGINNERS GUIDE TO ASSET\LIABILITY MANAGEMENT, RISK APPETITE AND CAPITAL PLANNING David Koch President\CEO dkoch@farin.com 800-236-3724 ext. 4217 What Is Asset/Liability Management? Asset/liability management

Enterprise Risk Management for Water Utilities. Justin Carlton, CMA, MBA Financial Analyst Tualatin Valley Water District

Enterprise Risk Management for Water Utilities Justin Carlton, CMA, MBA Financial Analyst Tualatin Valley Water District Enterprise Risk Management for Water Utilities Washington County, Oregon 2 Presentation

Enterprise Risk Management for Water Utilities Justin Carlton, CMA, MBA Financial Analyst Tualatin Valley Water District Enterprise Risk Management for Water Utilities Washington County, Oregon 2 Presentation

2014 Own Risk and Solvency Assessment (ORSA) Feedback Pilot Project Observations of the Group Solvency Issues (E) Working Group

Feedback Pilot Project Observations of the Group Solvency Issues (E) Working Group") 2014 Own Risk and Solvency Assessment (ORSA) Feedback Pilot Project Observations of the Group Solvency Issues (E) Working Group During October 2014 through June 2015, a third ORSA Feedback Pilot Project

2014 Own Risk and Solvency Assessment (ORSA) Feedback Pilot Project Observations of the Group Solvency Issues (E) Working Group During October 2014 through June 2015, a third ORSA Feedback Pilot Project

Capital & Risk Management Pillar 3 Disclosures

Capital & Risk Management Pillar 3 Disclosures 31st December 2017 Company Registration no. 06736473 Contents Introduction...3 Activities and Scope...3 Regulatory framework for disclosures...4 Basis and

Capital & Risk Management Pillar 3 Disclosures 31st December 2017 Company Registration no. 06736473 Contents Introduction...3 Activities and Scope...3 Regulatory framework for disclosures...4 Basis and

BIDVEST BANK LIMITED BASEL III CONSOLIDATED PILLAR III DISCLOSURE AS AT 30 JUNE 2017

BIDVEST BANK LIMITED BASEL III CONSOLIDATED PILLAR III DISCLOSURE AS AT 30 JUNE 2017 TABLE OF CONTENTS 0 1. Pillar III public disclosure 1.1 Introduction 1 1.2 Goals and objectives 1 1.3 Appropriateness

BIDVEST BANK LIMITED BASEL III CONSOLIDATED PILLAR III DISCLOSURE AS AT 30 JUNE 2017 TABLE OF CONTENTS 0 1. Pillar III public disclosure 1.1 Introduction 1 1.2 Goals and objectives 1 1.3 Appropriateness

ENTERPRISE RISK MANAGEMENT POLICY FRAMEWORK

ANNEXURE A ENTERPRISE RISK MANAGEMENT POLICY FRAMEWORK CONTENTS 1. Enterprise Risk Management Policy Commitment 3 2. Introduction 4 3. Reporting requirements 5 3.1 Internal reporting processes for risk

ANNEXURE A ENTERPRISE RISK MANAGEMENT POLICY FRAMEWORK CONTENTS 1. Enterprise Risk Management Policy Commitment 3 2. Introduction 4 3. Reporting requirements 5 3.1 Internal reporting processes for risk

Risk Management at the Deutsche Bundesbank March 2011

Risk Management at the Deutsche Bundesbank March 2011 (C) Deutsche Bundesbank - Division Organisation 1 Agenda Definition of risk management [3] Factors of influence to review the RM set up [4] The Framework

Risk Management at the Deutsche Bundesbank March 2011 (C) Deutsche Bundesbank - Division Organisation 1 Agenda Definition of risk management [3] Factors of influence to review the RM set up [4] The Framework

Risk Management. Webinar - July 2017

Risk Management Webinar - July 2017 Compiled by: Raaghieb Najjaar, Yaeesh Yasseen & Rashied Small Adapted and Facilitated by: Professor Enslin J. van Rooyen Risk Management - June 2017 2 Defining Risk

Risk Management Webinar - July 2017 Compiled by: Raaghieb Najjaar, Yaeesh Yasseen & Rashied Small Adapted and Facilitated by: Professor Enslin J. van Rooyen Risk Management - June 2017 2 Defining Risk

Risk Management. Seminar June Compiled by: Raaghieb Najjaar, Yaeesh Yasseen & Rashied Small

Risk Management Seminar June 2017 Compiled by: Raaghieb Najjaar, Yaeesh Yasseen & Rashied Small Defining Risk Risk reflects the chance that the actual event may be different than the planned / expected

Risk Management Seminar June 2017 Compiled by: Raaghieb Najjaar, Yaeesh Yasseen & Rashied Small Defining Risk Risk reflects the chance that the actual event may be different than the planned / expected

MINDA INDUSTRIES LIMITED RISK MANAGEMENT POLICY

` MINDA INDUSTRIES LIMITED RISK MANAGEMENT POLICY MINDA INDUSTRIES LIMITED RISK MANAGEMENT POLICY 1. Vision To develop organizational wide capabilities in Risk Management so as to ensure a consistent,

` MINDA INDUSTRIES LIMITED RISK MANAGEMENT POLICY MINDA INDUSTRIES LIMITED RISK MANAGEMENT POLICY 1. Vision To develop organizational wide capabilities in Risk Management so as to ensure a consistent,

INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE. Nepal Rastra Bank Bank Supervision Department. August 2012 (updated July 2013)

") INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE Nepal Rastra Bank Bank Supervision Department August 2012 (updated July 2013) Table of Contents Page No. 1. Introduction 1 2. Internal Capital Adequacy

INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE Nepal Rastra Bank Bank Supervision Department August 2012 (updated July 2013) Table of Contents Page No. 1. Introduction 1 2. Internal Capital Adequacy

How Internal Audit Can Help Promote Effective ERM

How Internal Audit Can Help Promote Effective ERM Alan N. Siegfried, MBA, CPA, CIA, CISA, CBA, CRMA, CFSA, CCSA, CITP, CGMA, CSP June 18, 2014 Alan Siegfried Professional Bio Principal and Managing Director,

How Internal Audit Can Help Promote Effective ERM Alan N. Siegfried, MBA, CPA, CIA, CISA, CBA, CRMA, CFSA, CCSA, CITP, CGMA, CSP June 18, 2014 Alan Siegfried Professional Bio Principal and Managing Director,

President s Choice Bank

Basel III Pillar 3 Disclosures President s Choice Bank Page 1 of 16 President s Choice Bank BASEL III PILLAR 3 DISCLOSURES March 31, 2017 Basel III Pillar 3 Disclosures President s Choice Bank Page 2 of

Basel III Pillar 3 Disclosures President s Choice Bank Page 1 of 16 President s Choice Bank BASEL III PILLAR 3 DISCLOSURES March 31, 2017 Basel III Pillar 3 Disclosures President s Choice Bank Page 2 of

Risk Management: Process and Culture in ESB

Risk Management: Process and Culture in ESB Marie Sinnott Group Compliance, Risk and Environment Manager esb.ie ESB s Risk Profile esb.ie ESB Overview: Vertically Integrated Utility Networks Generation

Risk Management: Process and Culture in ESB Marie Sinnott Group Compliance, Risk and Environment Manager esb.ie ESB s Risk Profile esb.ie ESB Overview: Vertically Integrated Utility Networks Generation

President s Choice Bank

Basel III Pillar 3 Disclosures President s Choice Bank Page 1 of 16 President s Choice Bank BASEL III PILLAR 3 DISCLOSURES September 30, 2017 Basel III Pillar 3 Disclosures President s Choice Bank Page

Basel III Pillar 3 Disclosures President s Choice Bank Page 1 of 16 President s Choice Bank BASEL III PILLAR 3 DISCLOSURES September 30, 2017 Basel III Pillar 3 Disclosures President s Choice Bank Page

Enterprise Risk Management by Many Other Names is Still Enterprise Risk Management David K. Whatley UTH Advisors April 15,2008

Enterprise Risk Management by Many Other Names is Still Enterprise Risk Management David K. Whatley UTH Advisors April 15,2008 UTH Advisors 2008 1 What is Enterprise Risk Management? Why don t more companies

Enterprise Risk Management by Many Other Names is Still Enterprise Risk Management David K. Whatley UTH Advisors April 15,2008 UTH Advisors 2008 1 What is Enterprise Risk Management? Why don t more companies

BERMUDA MONETARY AUTHORITY THE INSURANCE CODE OF CONDUCT FEBRUARY 2010

Table of Contents 0. Introduction..2 1. Preliminary...3 2. Proportionality principle...3 3. Corporate governance...4 4. Risk management..9 5. Governance mechanism..17 6. Outsourcing...21 7. Market discipline

Table of Contents 0. Introduction..2 1. Preliminary...3 2. Proportionality principle...3 3. Corporate governance...4 4. Risk management..9 5. Governance mechanism..17 6. Outsourcing...21 7. Market discipline

Desjardins Trust Inc. Financial Information and Information on Risk Management (unaudited)

") Desjardins Trust Inc. Financial Information and Information on Risk Management (unaudited) For the period ended September 30, 2017 TABLE OF CONTENTS Page Page Notes to readers Capital Use of this document

Desjardins Trust Inc. Financial Information and Information on Risk Management (unaudited) For the period ended September 30, 2017 TABLE OF CONTENTS Page Page Notes to readers Capital Use of this document

Enterprise Risk Management

Enterprise Risk Management Southeastern Actuaries Conference Rebecca Scotchie June 2011 ERM is 2 1 Agenda What is ERM? Why is risk management important? ERM maturity model/evolution of ERM ERM Framework

Enterprise Risk Management Southeastern Actuaries Conference Rebecca Scotchie June 2011 ERM is 2 1 Agenda What is ERM? Why is risk management important? ERM maturity model/evolution of ERM ERM Framework

Enterprise Risk Management Focusing on the Right Risks

2014 CliftonLarsonAllen LLP Enterprise Risk Management Focusing on the Right Risks VGFOA 2015 Fall Conference October 22, 2015 CLAconnect.com Session Objectives 1.Identify factors driving the need for

2014 CliftonLarsonAllen LLP Enterprise Risk Management Focusing on the Right Risks VGFOA 2015 Fall Conference October 22, 2015 CLAconnect.com Session Objectives 1.Identify factors driving the need for

Excess liquidity can restrict NorthPark s profitability and have an adverse effect on its capital position.

Purpose Liquidity Risk is defined as the current and prospective risk to NorthPark Community Credit Union s (NorthPark) earnings and capital position. Potential risk develops when NorthPark s experiences

Purpose Liquidity Risk is defined as the current and prospective risk to NorthPark Community Credit Union s (NorthPark) earnings and capital position. Potential risk develops when NorthPark s experiences

Dodd-Frank Act Stress Test Results. October 20, 2017

Dodd-Frank Act Stress Test Results October 20, 2017 Overview Synovus Financial Corp. (Synovus or the Company) regularly evaluates financial and capital forecasts under various economic scenarios as part

Dodd-Frank Act Stress Test Results October 20, 2017 Overview Synovus Financial Corp. (Synovus or the Company) regularly evaluates financial and capital forecasts under various economic scenarios as part

Risk Management in Italy: State of the art and perspectives. PMI Rome Italy Chapter

Risk Management in Italy: State of the art and perspectives Marco Giorgino, Full Professor of Global Risk Management, Politecnico di Milano PMI Rome Italy Chapter November, 5 th 2009 Agenda 2» What is

Risk Management in Italy: State of the art and perspectives Marco Giorgino, Full Professor of Global Risk Management, Politecnico di Milano PMI Rome Italy Chapter November, 5 th 2009 Agenda 2» What is

Risk Committee Charter. Bank of Queensland

Risk Committee Charter Bank of Queensland Issue Date: 28 June 2018 1 Purpose The Bank of Queensland Limited (BOQ) Risk Committee (Committee) has been established by the BOQ Board (the Board) to: (a) assist

Risk Committee Charter Bank of Queensland Issue Date: 28 June 2018 1 Purpose The Bank of Queensland Limited (BOQ) Risk Committee (Committee) has been established by the BOQ Board (the Board) to: (a) assist

Risk Management Policy and Framework

Risk Management Policy and Framework Risk Management Policy Statement ALS recognises that the effective management of risks is a fundamental component of good corporate governance and is vital for the

Risk Management Policy and Framework Risk Management Policy Statement ALS recognises that the effective management of risks is a fundamental component of good corporate governance and is vital for the

REPUTATION RISK ON THE RISE

Financial Services POINT OF VIEW REPUTATION RISK ON THE RISE AUTHORS Tom Ivell, Partner Hanjo Seibert, Principal Joshua Marks, Engagement Manager REPUTATION RISK ON THE RISE Reputation risk is generally

Financial Services POINT OF VIEW REPUTATION RISK ON THE RISE AUTHORS Tom Ivell, Partner Hanjo Seibert, Principal Joshua Marks, Engagement Manager REPUTATION RISK ON THE RISE Reputation risk is generally

University Risk Management Policy

Preamble University Risk Management Policy Approving Authority: Board of Governors Original Approval Date: June 7, 2007 Date of Most Recent Review/Revision: October 20, 2017 Responsible Officer: Vice-President

Preamble University Risk Management Policy Approving Authority: Board of Governors Original Approval Date: June 7, 2007 Date of Most Recent Review/Revision: October 20, 2017 Responsible Officer: Vice-President

REGULATORY GUIDELINE Liquidity Risk Management Principles TABLE OF CONTENTS. I. Introduction II. Purpose and Scope III. Principles...

REGULATORY GUIDELINE Liquidity Risk Management Principles SYSTEM COMMUNICATION NUMBER Guideline 2015-02 ISSUE DATE June 2015 TABLE OF CONTENTS I. Introduction... 1 II. Purpose and Scope... 1 III. Principles...

REGULATORY GUIDELINE Liquidity Risk Management Principles SYSTEM COMMUNICATION NUMBER Guideline 2015-02 ISSUE DATE June 2015 TABLE OF CONTENTS I. Introduction... 1 II. Purpose and Scope... 1 III. Principles...

Guideline. Earthquake Exposure Sound Practices. I. Purpose and Scope. No: B-9 Date: February 2013

Guideline Subject: No: B-9 Date: February 2013 I. Purpose and Scope Catastrophic losses from exposure to earthquakes may pose a significant threat to the financial wellbeing of many Property & Casualty

Guideline Subject: No: B-9 Date: February 2013 I. Purpose and Scope Catastrophic losses from exposure to earthquakes may pose a significant threat to the financial wellbeing of many Property & Casualty

President s Choice Bank

Basel III Pillar 3 Disclosures President s Choice Bank Page 1 of 16 President s Choice Bank BASEL III PILLAR 3 DISCLOSURES June 30, 2018 Basel III Pillar 3 Disclosures President s Choice Bank Page 2 of

Basel III Pillar 3 Disclosures President s Choice Bank Page 1 of 16 President s Choice Bank BASEL III PILLAR 3 DISCLOSURES June 30, 2018 Basel III Pillar 3 Disclosures President s Choice Bank Page 2 of

Risk Management Policy and Procedures.

Risk Management Policy and Procedures. Rev Date Purpose of Issue/Description of Change Date 1. June 2006 Initial Issue 2. November 2009 Revised and updated 6 th November 2009 3. September 2010 Revised

Risk Management Policy and Procedures. Rev Date Purpose of Issue/Description of Change Date 1. June 2006 Initial Issue 2. November 2009 Revised and updated 6 th November 2009 3. September 2010 Revised

CHARTER OF THE RISK AND COMPLIANCE JOINT COMMITTEE OF THE BOARDS OF DIRECTORS OF FIFTH THIRD BANCORP AND FIFTH THIRD BANK

CHARTER OF THE RISK AND COMPLIANCE JOINT COMMITTEE OF THE BOARDS OF DIRECTORS OF FIFTH THIRD BANCORP AND FIFTH THIRD BANK As Approved by the Board of Directors of Fifth Third Bancorp on June 20, 2017 and

CHARTER OF THE RISK AND COMPLIANCE JOINT COMMITTEE OF THE BOARDS OF DIRECTORS OF FIFTH THIRD BANCORP AND FIFTH THIRD BANK As Approved by the Board of Directors of Fifth Third Bancorp on June 20, 2017 and

An Inclusive and Data-Rich Approach to Infrastructure Development

Network-Level Analysis An Inclusive and Data-Rich Approach to Infrastructure Development By Israr Ahmad and John Murray The state of a community s capital infrastructure is inextricably linked with its

Network-Level Analysis An Inclusive and Data-Rich Approach to Infrastructure Development By Israr Ahmad and John Murray The state of a community s capital infrastructure is inextricably linked with its

Corporate Governance of Federally-Regulated Financial Institutions

Draft Guideline Subject: -Regulated Financial Institutions Category: Sound Business and Financial Practices Date: I. Purpose and Scope of the Guideline The purpose of this guideline is to set OSFI s expectations

Draft Guideline Subject: -Regulated Financial Institutions Category: Sound Business and Financial Practices Date: I. Purpose and Scope of the Guideline The purpose of this guideline is to set OSFI s expectations

ERM and ORSA Assuring a Necessary Level of Risk Control

ERM and ORSA Assuring a Necessary Level of Risk Control Dave Ingram, MAAA, FSA, CERA, FRM, PRM Chair of IAA Enterprise & Financial Risk Committee Executive Vice President, Willis Re September, 2012 1 DISCLAIMER

ERM and ORSA Assuring a Necessary Level of Risk Control Dave Ingram, MAAA, FSA, CERA, FRM, PRM Chair of IAA Enterprise & Financial Risk Committee Executive Vice President, Willis Re September, 2012 1 DISCLAIMER

RISK MANAGEMENT - CORPORATE COMPLIANCE & ETHICS

RISK MANAGEMENT - CORPORATE COMPLIANCE & ETHICS Presenter CLAIRE GOMEZ MILLER CIA CRMA FCCA CA BOARD DIRECTOR/AUDITCOMMITTEE MEMBER UNITEDINDEPENDENT PETROLEUM MARKETING COMPANY LIMITED TRINIDAD AND TOBAGO

RISK MANAGEMENT - CORPORATE COMPLIANCE & ETHICS Presenter CLAIRE GOMEZ MILLER CIA CRMA FCCA CA BOARD DIRECTOR/AUDITCOMMITTEE MEMBER UNITEDINDEPENDENT PETROLEUM MARKETING COMPANY LIMITED TRINIDAD AND TOBAGO

Enhancing Our Risk Appetite Framework. A Case Study

Enhancing Our Risk Appetite Framework A Case Study Desired Outcomes 1. An approach to developing a risk appetite framework and risk appetite statement. 2. Understanding how a risk appetite framework can

Enhancing Our Risk Appetite Framework A Case Study Desired Outcomes 1. An approach to developing a risk appetite framework and risk appetite statement. 2. Understanding how a risk appetite framework can

Risk Architecture: Agenda. Leon Bloom, Partner, Deloitte & Touche LLP

Risk Architecture: Alignment of Investor Objectives and Strategic and Business Objectives and Risk Appetite and Limits Leon Bloom, Partner, Deloitte & Touche LLP lebloom@deloitte.ca Agenda Alignment of

Risk Architecture: Alignment of Investor Objectives and Strategic and Business Objectives and Risk Appetite and Limits Leon Bloom, Partner, Deloitte & Touche LLP lebloom@deloitte.ca Agenda Alignment of

Quantitative and Qualitative Disclosures about Market Risk.

Item 7A. Quantitative and Qualitative Disclosures about Market Risk. Risk Management. Risk Management Policy and Control Structure. Risk is an inherent part of the Company s business and activities. The

Item 7A. Quantitative and Qualitative Disclosures about Market Risk. Risk Management. Risk Management Policy and Control Structure. Risk is an inherent part of the Company s business and activities. The

Capital Speedboat Session 2. Charting your way through troubling waters FARIN & Associates Inc. Agenda

Capital Speedboat 2013 - Session 2 Charting your way through troubling waters 1 Agenda Session 2 Defining Stress Tests Stress vs. Scenario Testing Sensitivity Testing Scenarios Silos Scenario Testing Building

Capital Speedboat 2013 - Session 2 Charting your way through troubling waters 1 Agenda Session 2 Defining Stress Tests Stress vs. Scenario Testing Sensitivity Testing Scenarios Silos Scenario Testing Building

Critical Reflection of Two State-of-the-Art Risk Management Frameworks (SRM004)

") Critical Reflection of Two State-of-the-Art Risk Management Frameworks (SRM004) Speakers: Dr. Kathrin Anne Meier, Chief Risk Officer, Allianz Global Corporate & Specialty John Adams, VP Global ERM, PepsiCo

Critical Reflection of Two State-of-the-Art Risk Management Frameworks (SRM004) Speakers: Dr. Kathrin Anne Meier, Chief Risk Officer, Allianz Global Corporate & Specialty John Adams, VP Global ERM, PepsiCo

CORPORATE RISK MANAGEMENT POLICY

11/8/2017 INFORMAÇÃO INTERNA ÍNDICE 1 PURPOSE... 3 2 SCOPE... 3 3 REFERENCES... 3 4 CONCEPTS... 4 5 GUIDELINES... 6 6 RESPONSABILITIES... 8 7 CONTROL INFORMATION... 14 2 INFORMAÇÃO INTERNA 1 PURPOSE The

11/8/2017 INFORMAÇÃO INTERNA ÍNDICE 1 PURPOSE... 3 2 SCOPE... 3 3 REFERENCES... 3 4 CONCEPTS... 4 5 GUIDELINES... 6 6 RESPONSABILITIES... 8 7 CONTROL INFORMATION... 14 2 INFORMAÇÃO INTERNA 1 PURPOSE The

RISK MANAGEMENT - CORPORATE COMPLIANCE & ETHICS

RISK MANAGEMENT - CORPORATE COMPLIANCE & ETHICS Presenter CLAIRE GOMEZ MILLER CIA CRMA FCCA CA BOARD DIRECTOR/AUDIT COMMITTEEMEMBER UNITEDINDEPENDENTPETROLEUM MARKETINGCOMPANYLIMITED TRINIDAD AND TOBAGO

RISK MANAGEMENT - CORPORATE COMPLIANCE & ETHICS Presenter CLAIRE GOMEZ MILLER CIA CRMA FCCA CA BOARD DIRECTOR/AUDIT COMMITTEEMEMBER UNITEDINDEPENDENTPETROLEUM MARKETINGCOMPANYLIMITED TRINIDAD AND TOBAGO

Practical aspects of determining and applying a risk appetite for SMEs

Practical aspects of determining and applying a risk appetite for SMEs By Tim Timchur acis, Director, ActivePro Consulting Pty Ltd Important to determine appetite for risk before determining what risk

Practical aspects of determining and applying a risk appetite for SMEs By Tim Timchur acis, Director, ActivePro Consulting Pty Ltd Important to determine appetite for risk before determining what risk

Risk Management at Central Bank of Nepal

Risk Management at Central Bank of Nepal A. Introduction to Supervisory Risk Management Framework in Banks Nepal Rastra Bank(NRB) Act, 2058, section 35 (a) requires the NRB management is to design and

Risk Management at Central Bank of Nepal A. Introduction to Supervisory Risk Management Framework in Banks Nepal Rastra Bank(NRB) Act, 2058, section 35 (a) requires the NRB management is to design and

Enterprise Risk Management Examples of Financial loss quantification

Enterprise Risk Management Examples of Financial loss quantification Quantification of the financial impact is not a straightforward exercise. Qualitative data analysis as well as in depth understanding

Enterprise Risk Management Examples of Financial loss quantification Quantification of the financial impact is not a straightforward exercise. Qualitative data analysis as well as in depth understanding