REPORT 2015/085 INTERNAL AUDIT DIVISION

|

|

|

- Eleanor Baldwin

- 5 years ago

- Views:

Transcription

1 INTERNAL AUDIT DIVISION REPORT 2015/085 Audit of the United Nations Stabilization Mission in Haiti s trust fund to strengthen specialized sexual and gender-based crimes police cells and units within the Haitian National Police Overall results relating to the effective management of the United Nations Stabilization Mission in Haiti s trust fund to strengthen specialized sexual and genderbased crimes police cells and units within the Haitian National Police were initially assessed as partially satisfactory. Implementation of three important recommendations remains in progress FINAL OVERALL RATING: PARTIALLY SATISFACTORY 27 August 2015 Assignment No. AP2014/683/08

2 CONTENTS Page I. BACKGROUND 1 II. OBJECTIVE AND SCOPE 1-2 III. AUDIT RESULTS 2-6 A. Project management 2-4 B. Regulatory framework 4-6 IV. ACKNOWLEDGEMENT 6 ANNEX I APPENDIX I Status of audit recommendations Management response

3 AUDIT REPORT Audit of the United Nations Stabilization Mission in Haiti s trust fund to strengthen specialized sexual and gender-based crimes police cells and units within the Haitian National Police I. BACKGROUND 1. The Office of Internal Oversight Services (OIOS) conducted an audit of the United Nations Stabilization in Haiti s (MINUSTAH) trust fund to strengthen specialized sexual and gender-based crimes police cells and units within the Haitian National Police (HNP). 2. In accordance with its mandate, OIOS provides assurance and advice on the adequacy and effectiveness of the United Nations internal control system, the primary objectives of which are to ensure: (a) efficient and effective operations; (b) accurate financial and operational reporting; (c) safeguarding of assets; and (d) compliance with mandates, regulations and rules. 3. In May 2010, the Department of Peacekeeping Operations (DPKO) requested a donor government for financial support for a three-year project costing about $4.4 million to strengthen specialized sexual and gender-based crimes police cells and units within HNP. This government granted DPKO an amount equivalent to $850,000 in December 2010 to start the project. This first grant was managed by DPKO and was not covered by this audit. After the implementation of the first phase of the project, the donor government accommodated the request of DPKO for further funding (the second grant) in December 2012 for the same amount. 4. The second grant, net of 13 per cent project support cost, was equivalent to $779,630. This grant was allotted to MINUSTAH and covered by this audit. This amount was to be spent on various activities including $380,000 for a five-day sexual and gender-based violence (SGBV) course provided to 500 HNP officers, and $276,000 for the provision of 12 SGBV investigation offices of HNP in the regions. The donor government also agreed to provide additional funding to continue with SGBV projects to build capacity of HNP through training of its officers and building SGBV investigation offices in The project valued at $779,630 was managed by the United Nations police SGBV team within the MINUSTAH SGBV Unit. The SGBV Unit had eight approved police officers posts including a team leader who supervised the implementation of trust fund projects. The staffing cost of the Unit during 1 January 2013 to 31 December 2014 was $837, Comments provided by MINUSTAH are incorporated in italics. II. OBJECTIVE AND SCOPE 7. The audit was conducted to assess the adequacy and effectiveness of MINUSTAH governance, risk management and control processes in providing reasonable assurance regarding the effective management of the MINUSTAH trust fund to strengthen specialized sexual and gender-based crimes police cells and units within HNP. 8. This audit was included in the 2014 risk-based work plan of OIOS at the request of Mission management and because of the risks associated with improper utilization of donor funding. 1

4 9. The key controls tested for the audit were: (a) project management; and (b) regulatory framework. For the purpose of this audit, OIOS defined these key controls as follows: (a) Project management - controls that provide reasonable assurance that there is sufficient project management capacity for proper utilization of the trust fund; and (b) Regulatory framework - controls that provide reasonable assurance that policies and procedures: (i) exist to guide the utilization of the trust fund; (ii) are implemented consistently; and (iii) ensure the reliability and integrity of financial and operational information. 10. The key controls were assessed for the control objectives shown in Table 1. Certain control objectives shown in Table 1 as Not assessed were not relevant to the scope defined for this audit. 11. OIOS conducted the audit from November 2014 to January The audit covered the period from 1 January 2013 to 31 December 2014 and reviewed the SGBV projects implemented from the donor government s December 2012 grant. 12. OIOS conducted an activity-level risk assessment to identify and assess specific risk exposures, and to confirm the relevance of the selected key controls in mitigating associated risks. Through interviews and analytical reviews, OIOS assessed the existence and adequacy of internal controls and conducted necessary tests to determine their effectiveness. III. AUDIT RESULTS 13. The MINUSTAH governance, risk management and control processes examined were initially assessed as partially satisfactory 1 in providing reasonable assurance regarding the effective management of the MINUSTAH trust fund to strengthen specialized sexual and gender-based crimes police cells and units within HNP. OIOS made four recommendations to address the issues identified. MINUSTAH supported HNP in strengthening its operational capability to address sexual and gender-based crimes by: providing training to 639 HNP personnel and organizing seminars for 51 high ranking police officers; and completing the construction of eight SGBV investigation offices. However, MINUSTAH needed to: (a) ensure that estimates for future construction projects consider all cost factors; (b) prepare cost-effective training proposals that showed options were researched, costed and documented; (c) establish procedures to determine the eligibility of trust fund expenses; and (d) segregate trust fund expenses by booking the appropriate commitment items in Umoja. 14. The initial overall rating was based on the assessment of key controls presented in Table 1. The final overall rating is partially satisfactory as implementation of three important recommendations remains in progress. 1 A rating of partially satisfactory means that important (but not critical or pervasive) deficiencies exist in governance, risk management or control processes, such that reasonable assurance may be at risk regarding the achievement of control and/or business objectives under review. 2

5 Table 1: Assessment of key controls Business objective Effective management of the MINUSTAH trust fund to strengthen specialized sexual and gender-based crimes police cells and units within HNP Key controls (a) Project management (b) Regulatory framework Efficient and effective operations Partially satisfactory Partially satisfactory FINAL OVERALL RATING: PARTIALLY SATISFACTORY Control objectives Accurate financial and operational reporting Partially satisfactory Partially satisfactory Safeguarding of assets Not assessed Not assessed Compliance with mandates, regulations and rules Partially satisfactory Partially satisfactory A. Project management Adequate reporting of accomplishments and expenditures 15. The Field Finance Procedure Guidelines and the grant agreement required periodic substantive and financial reporting to the donor. A review of financial reports for calendar years 2013 and 2014 showed that against the planned aggregate budget of $779,630, MINUSTAH incurred $751,649 out of which $380,000 was spent on organizing SGBV trainings and seminars for HNP officers, $259,088 for construction of SGBV investigation offices and the remaining $112,561 for the provision of equipment for training and investigation offices and other operating costs. Further, the SGBV reports, including the one for the quarter ending in 31 March 2014, indicated that MINUSTAH: (a) trained 639 police officers; (b) organized three seminars for 51 high-ranking HNP officers; (c) completed SGBV standard operating procedures for HNP; (d) built and rehabilitated eight dedicated SGBV investigation offices; and (e) provided equipment for training courses and for the investigation offices. Since the reports adequately reflected the accomplishments and expenditure against the grant, OIOS concluded that the Mission implemented controls to ensure compliance with the relevant reporting requirements. Shortfall and delays in building and rehabilitating investigation offices needed to improve 16. The project proposal, based on which the government provided the second grant to the United Nations, provided for the construction of 12 SGBV investigation offices. By December 2014, MINUSTAH completed the construction and rehabilitation of eight investigation offices while the construction of one SGBV training classroom was still in progress. The shortfall in the number of construction projects was due to the underestimation of costs. A review of six of nine cost estimates for construction activities financed by the trust fund indicated that the estimates were done on the basis of market price at Port-au-Prince and did not consider overheads, profit margins and site locations outside the capital. 17. The construction of 12 SGBV offices was proposed to be completed by the end of 2013; however, only three projects were initiated in 2013 and six in The delays were due to inadequate planning and monitoring. The annual project plans did not have targets and timelines for various activities. MINUSTAH advised that the delays were also attributable to other external factors including occasional delays by the contractors. 3

6 (1) MINUSTAH should take steps to: ensure that estimates for future construction projects under the trust fund consider all cost factors, including allowing for contingencies to make sure that estimates are closer to reality; and improve its project work plan by incorporating specific targets and timelines for monitoring timely implementation of projects. MINUSTAH accepted recommendation 1 and stated that it had prepared a detailed assessment report for upcoming trust fund projects incorporating specific targets, timelines and monitoring. Recommendation 1 remains open pending receipt of evidence of improved cost estimates and a copy of the detailed assessment report showing an improved work plan. Project proposals needed improvement 18. United Nations Financial Regulations and Rules require due consideration to be given for best value for money and fairness and integrity for procuring any goods and services. The project proposal provided $380,000 to be used for the training of 500 HNP officers. A review of payment vouchers and SGBV training documents indicated that MINUSTAH incurred $355,000 until December 2014 for the training of 639 HNP officers. Some $300,000 (or about 85 per cent of the training expenses) was spent on hotel facilities and overnight accommodation for participants and instructors. The remaining $55,000 was incurred on training materials, and per diem and backpacks for participants, which on average was $86 per trainee. 19. In the absence of detailed breakdown of the $380,000 for training, OIOS could not ascertain the budget allowed to be spent on hotel costs. Nonetheless, in the opinion of OIOS, spending 85 per cent of the training expenses for hotels in different locations, including in Port-au-Prince where alternative training facilities and accommodation were available, was not cost-effective. MINUSTAH advised that the training courses were organized in good hotels to: provide participants and instructors a better training environment including with necessary accommodation and food; and ensure participants attendance and punctuality. MINUSTAH added that it considered holding the training courses in the HNP School, but it was in use throughout the year; and when not in use to train cadets, it was being repaired to accommodate new cadets. MINUSTAH; however, did not exhaust other less costly alternatives or conduct research to determine whether these training programmes could be held more cost-effectively. (2) MINUSTAH should prepare training proposals that include a detailed breakdown of the budgeted cost of facilities, materials and trainers and ensure that options considered in the implementation of proposals are adequately researched and documented. MINUSTAH accepted recommendation 2 and stated that it had made it mandatory to include detailed breakdown of all costs at the time of submission of project proposals. Recommendation 2 remains open pending receipt of documentation showing detailed breakdown of costs and evidence of adequate research and costing of training proposals. Procedures needed to validate expenditures B. Regulatory framework 20. The donor s grant letter required the funds to be used on activities stipulated in the project proposal. The grant letter also required the trust fund to be used in accordance with the approved United Nations rules and procedures. A review of 42 trust fund related vouchers/invoices valued at $440,550 out of 57 vouchers/invoices valued at $751,649 indicated that certain expenditures were not explicitly 4

7 envisioned in the project proposal. These expenditures included: (a) $31,950 at a rate of $10 per day per trainee as cash payment to 639 trainees in addition to accommodation and meals in hotels for attending the training courses; (b) $3,850 for providing t-shirts to the participants; (c) $4,250 for organizing a ceremony at a hotel in Port-au-Prince to mark the closure of SGBV projects; and (d) $3,618 for refreshments for the inauguration of SGBV offices. However, the Mission spent $707,981 on activities directly related to the project. While MINUSTAH was of the view that all expenditures were directly related to the effective implementation of the project, MINUSTAH did not have procedures in place to review and systematically assess eligibility of all expenditures charged to the trust fund. Instead, MINUSTAH relied on the prudence of the United Nations Police officers in the SGBV Unit. The lack of review procedures increased the risk that some expenditures not directly related to the effective implementation of the project may be charged to the trust fund. (3) MINUSTAH should establish procedures for consistently reviewing the eligibility of trust fund expenses. MINUSTAH accepted recommendation 3 and stated that it would establish procedures to review the eligibility of trust fund expenses through the Project Review Committee. Recommendation 3 remains open pending receipt of evidence of the Project Review Committee s review of the eligibility of trust fund expenses. Payments were processed on time 21. MINUSTAH contracts for projects funded under the trust fund required payments to be made between 15 and 30 days following satisfactory delivery of goods, performance of services and submission of invoices. MINUSTAH processed payments to vendors in the Sun system from 1 January to 31 October 2013 and in Umoja from 1 November 2013 to 31 December A comparison of all payment requests made by the SGBV Unit with actual payment dates indicated that MINUSTAH took an average of 11 and 13 days to process payments in the Sun system and Umoja respectively. OIOS concluded that controls were in place to ensure that payments were processed in a timely manner. Expenses needed to be entered under correct commitment items in Umoja 22. The Field Finance Procedure Guidelines required MINUSTAH to have an effective mechanism to segregate assessed funds and trust funds. The guidelines also required obligations to be accounted properly for the transfer of year-end closing balance. 23. Trust fund expenses in Umoja were entered under wrong commitment items. For example, travel expenses were booked under office supplies, food and accommodation expenses of the trainees were entered under consultancy and in some cases, a single commitment was made in Umoja for various expenses. This occurred because staff were not experienced with the new Umoja system and they focused on the available trust fund balance while booking commitments but did not pay adequate attention to segregating expenses among different commitment items. As a result, various expenditures against planned activities and budgets were not segregated appropriately. 24. OIOS matched the cumulative expenditure relating to trust fund projects for 2013/14 with the transfer of the fund balance from 2013/14 to 2014/15 done in Umoja in July 2014 and noted that the transferred balance was $79,000 less than the amount which should have been available. The Finance Section did not detect this anomaly initially because there was no mechanism in place to reconcile the trust fund balance before the roll-over was made from one fiscal year to another. However, the SGBV Unit detected this discrepancy during the reconciliation of project expenditure against the available 5

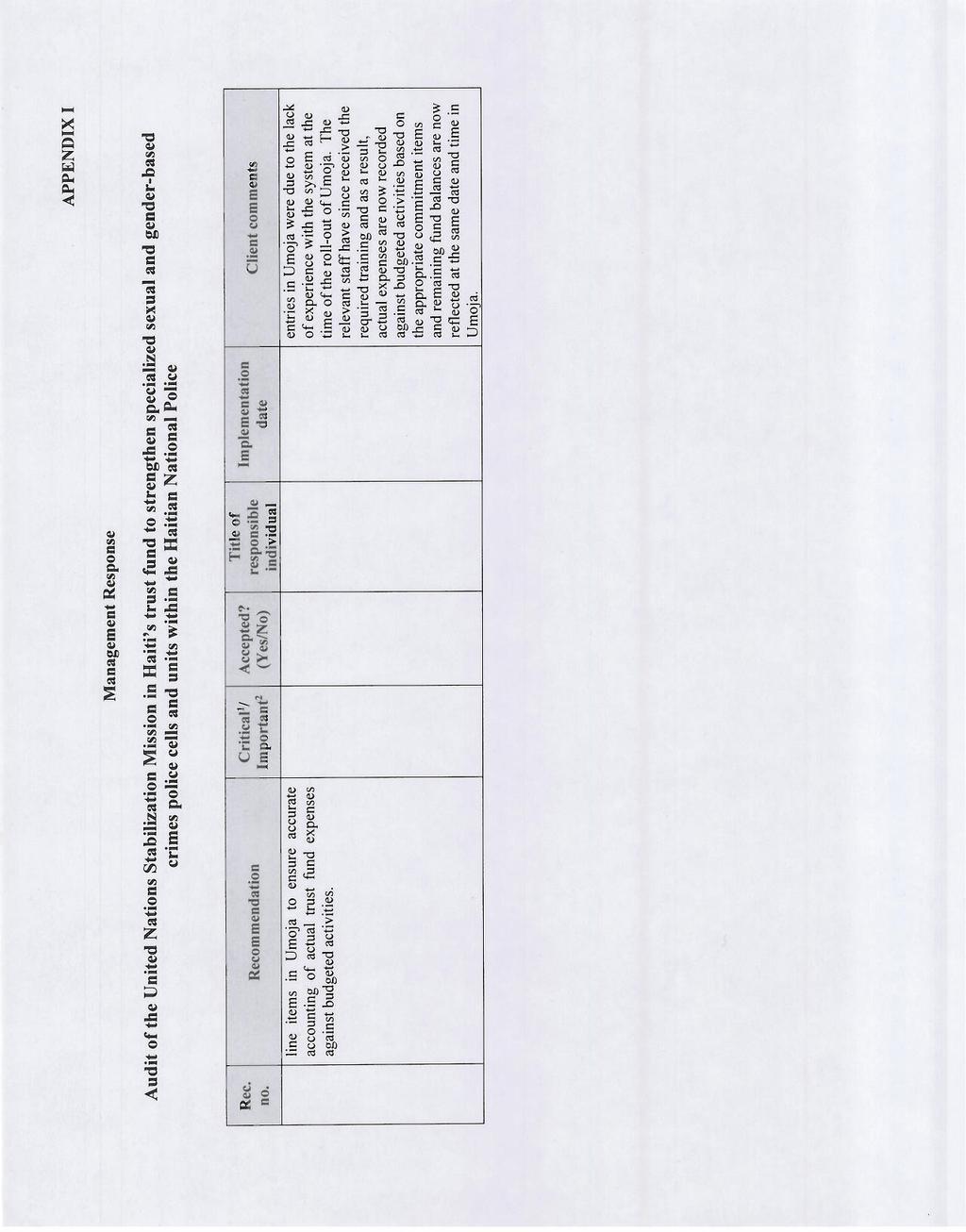

8 balance. The Finance Section identified that this resulted due to incorrect booking of obligations against two purchase requisitions which were eventually cancelled, and rectified the error. (4) MINUSTAH should train its staff members to record commitments under appropriate line items in Umoja to ensure accurate accounting of actual trust fund expenses against budgeted activities. MINUSTAH accepted recommendation 4 and stated that the relevant staff had been trained on the use of Umoja. As a result, actual expenses were now recorded against budgeted activities based on the appropriate commitment items and remaining fund balances were available at any point in time. Based on action taken by MINUSTAH, recommendation 4 has been closed. IV. ACKNOWLEDGEMENT 25. OIOS wishes to express its appreciation to the management and staff of MINUSTAH for the assistance and cooperation extended to the auditors during this assignment. (Signed) David Kanja Assistant Secretary-General for Internal Oversight Services 6

9 ANNEX I STATUS OF AUDIT RECOMMENDATIONS Audit of the United Nations Stabilization Mission in Haiti s trust fund to strengthen specialized sexual and gender-based crimes police cells and units within the Haitian National Police Recom. Recommendation no. 1 MINUSTAH should take steps to: ensure that estimates for future construction projects under the trust fund consider all cost factors, including allowing for contingencies to make sure that estimates are closer to reality; and improve its project work plan by incorporating specific targets and timelines for monitoring timely implementation of projects. 2 MINUSTAH should prepare training proposals that include a detailed breakdown of the budgeted cost of facilities, materials and trainers and ensure that options considered in the implementation of proposals are adequately researched and documented. 3 MINUSTAH should establish procedures for consistently reviewing the eligibility of trust fund expenses. 4 MINUSTAH should train its staff members to record commitments under appropriate line items in Umoja to ensure accurate accounting of actual trust fund expenses against budgeted activities. Critical 1 / C/ Important 2 O 3 Actions needed to close recommendation Important O Receipt of evidence of improved cost estimates and a copy of the detail assessment report encompassing an improved work plan Important O Receipt of documentation showing detail breakdown of costs and evidence of adequate research and costing of training proposals Implementation date 4 31 December December 2015 Important O Receipt of evidence of the Project Review Committee s review of the eligibility of trust fund expenses 31 December 2015 Important C Action taken Implemented 1 Critical recommendations address critical and/or pervasive deficiencies in governance, risk management or control processes, such that reasonable assurance cannot be provided with regard to the achievement of control and/or business objectives under review. 2 Important recommendations address important (but not critical or pervasive) deficiencies in governance, risk management or control processes, such that reasonable assurance may be at risk regarding the achievement of control and/or business objectives under review. 3 C = closed, O = open 4 Date provided by MINUSTAH in response to recommendations. 1

10 APPENDIX I Management Response

11

12

13

REPORT 2014/134 INTERNAL AUDIT DIVISION. Audit of financial and administrative functions in the United Nations Truce Supervision Organization

INTERNAL AUDIT DIVISION REPORT 2014/134 Audit of financial and administrative functions in the United Nations Truce Supervision Organization Overall results relating to the effectiveness of financial and

INTERNAL AUDIT DIVISION REPORT 2014/134 Audit of financial and administrative functions in the United Nations Truce Supervision Organization Overall results relating to the effectiveness of financial and

REPORT 2013/142. Audit of accounts receivable and payable in the United Nations Operation in Côte d Ivoire

INTERNAL AUDIT DIVISION REPORT 2013/142 Audit of accounts receivable and payable in the United Nations Operation in Côte d Ivoire Overall results relating to the effective management of accounts receivable

INTERNAL AUDIT DIVISION REPORT 2013/142 Audit of accounts receivable and payable in the United Nations Operation in Côte d Ivoire Overall results relating to the effective management of accounts receivable

REPORT 2015/041 INTERNAL AUDIT DIVISION. Audit of the United Nations Mine Action Service of the Department of Peacekeeping Operations

INTERNAL AUDIT DIVISION REPORT 2015/041 Audit of the United Nations Mine Action Service of the Department of Peacekeeping Operations Overall results relating to the effective management of mine action

INTERNAL AUDIT DIVISION REPORT 2015/041 Audit of the United Nations Mine Action Service of the Department of Peacekeeping Operations Overall results relating to the effective management of mine action

REPORT 2014/070 INTERNAL AUDIT DIVISION. Audit of civil affairs activities in the. United Nations Stabilization Mission in Haiti

INTERNAL AUDIT DIVISION REPORT 2014/070 Audit of civil affairs activities in the United Nations Stabilization Mission in Haiti Overall results relating to the effective management of civil affairs activities

INTERNAL AUDIT DIVISION REPORT 2014/070 Audit of civil affairs activities in the United Nations Stabilization Mission in Haiti Overall results relating to the effective management of civil affairs activities

REPORT 2014/107 INTERNAL AUDIT DIVISION. Audit of quick-impact projects in the African Union-United Nations Hybrid Operation in Darfur

INTERNAL AUDIT DIVISION REPORT 2014/107 Audit of quick-impact projects in the African Union-United Nations Hybrid Operation in Darfur Overall results relating to the management of quick-impact projects

INTERNAL AUDIT DIVISION REPORT 2014/107 Audit of quick-impact projects in the African Union-United Nations Hybrid Operation in Darfur Overall results relating to the management of quick-impact projects

REPORT 2015/079 INTERNAL AUDIT DIVISION. Audit of United Nations Office on Drugs and Crime operations in Peru

INTERNAL AUDIT DIVISION REPORT 2015/079 Audit of United Nations Office on Drugs and Crime operations in Peru Overall results relating to the management of operations in Peru were initially assessed as

INTERNAL AUDIT DIVISION REPORT 2015/079 Audit of United Nations Office on Drugs and Crime operations in Peru Overall results relating to the management of operations in Peru were initially assessed as

REPORT 2015/072 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/072 Audit of minimum operating residential security standards entitlements for staff in the United Nations Operation in Côte d Ivoire Overall results relating to the

INTERNAL AUDIT DIVISION REPORT 2015/072 Audit of minimum operating residential security standards entitlements for staff in the United Nations Operation in Côte d Ivoire Overall results relating to the

REPORT 2015/123 INTERNAL AUDIT DIVISION. Audit of the management of engineering projects in the United Nations Mission in the Republic of South Sudan

INTERNAL AUDIT DIVISION REPORT 2015/123 Audit of the management of engineering projects in the United Nations Mission in the Republic of South Sudan Overall results relating to the effective management

INTERNAL AUDIT DIVISION REPORT 2015/123 Audit of the management of engineering projects in the United Nations Mission in the Republic of South Sudan Overall results relating to the effective management

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/068

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/068 Audit of the management of United Nations Joint Staff Pension Fund Investment Management Division s back office operations Overall results relating to the

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/068 Audit of the management of United Nations Joint Staff Pension Fund Investment Management Division s back office operations Overall results relating to the

INTERNAL AUDIT DIVISION REPORT 2017/126. Audit of trust fund activities in the African Union-United Nations Hybrid Operation in Darfur

INTERNAL AUDIT DIVISION REPORT 2017/126 Audit of trust fund activities in the African Union-United Nations Hybrid Operation in Darfur The Mission needed to enhance its supervision of project site inspections

INTERNAL AUDIT DIVISION REPORT 2017/126 Audit of trust fund activities in the African Union-United Nations Hybrid Operation in Darfur The Mission needed to enhance its supervision of project site inspections

REPORT 2016/088 INTERNAL AUDIT DIVISION. Audit of rations management in the United Nations Mission in the Republic of South Sudan

INTERNAL AUDIT DIVISION REPORT 2016/088 Audit of rations management in the United Nations Mission in the Republic of South Sudan Overall results relating to the effective management of rations were initially

INTERNAL AUDIT DIVISION REPORT 2016/088 Audit of rations management in the United Nations Mission in the Republic of South Sudan Overall results relating to the effective management of rations were initially

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/091. Audit of the United Nations Peacebuilding Support Office

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/091 Audit of the United Nations Peacebuilding Support Office Overall results relating to the effective support of the Peacebuilding Support Office to the Peacebuilding

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/091 Audit of the United Nations Peacebuilding Support Office Overall results relating to the effective support of the Peacebuilding Support Office to the Peacebuilding

REPORT 2014/153 INTERNAL AUDIT DIVISION. Audit of the United Nations Office for Disaster Risk Reduction

INTERNAL AUDIT DIVISION REPORT 2014/153 Audit of the United Nations Office for Disaster Risk Reduction Overall results relating to the effective management of the United Nations Office for Disaster Risk

INTERNAL AUDIT DIVISION REPORT 2014/153 Audit of the United Nations Office for Disaster Risk Reduction Overall results relating to the effective management of the United Nations Office for Disaster Risk

REPORT 2015/095 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/095 Review of recurrent issues identified in recent internal audit engagements for the Office for the Coordination of Humanitarian Affairs 8 September 2015 Assignment

INTERNAL AUDIT DIVISION REPORT 2015/095 Review of recurrent issues identified in recent internal audit engagements for the Office for the Coordination of Humanitarian Affairs 8 September 2015 Assignment

REPORT 2015/094 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/094 Audit of management of external portfolio managers for small capitalization investments in the Investment Management Division of the United Nations Joint Staff Pension

INTERNAL AUDIT DIVISION REPORT 2015/094 Audit of management of external portfolio managers for small capitalization investments in the Investment Management Division of the United Nations Joint Staff Pension

REPORT 2016/105 INTERNAL AUDIT DIVISION. Audit of investment management in the Office of Programme Planning, Budget and Accounts

INTERNAL AUDIT DIVISION REPORT 2016/105 Audit of investment management in the Office of Programme Planning, Budget and Accounts Overall results relating to the effective management of investments were

INTERNAL AUDIT DIVISION REPORT 2016/105 Audit of investment management in the Office of Programme Planning, Budget and Accounts Overall results relating to the effective management of investments were

REPORT 2014/062. Audit of the United Nations Environment Programme Ozone Secretariat FINAL OVERALL RATING: PARTIALLY SATISFACTORY

INTERNAL AUDIT DIVISION REPORT 2014/062 Audit of the United Nations Environment Programme Ozone Secretariat Overall results relating to the provision of efficient and effective support services by the

INTERNAL AUDIT DIVISION REPORT 2014/062 Audit of the United Nations Environment Programme Ozone Secretariat Overall results relating to the provision of efficient and effective support services by the

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/078

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/078 Audit of the United Nations Environment Programme s Secretariat of the Convention on Biological Diversity Overall results relating to the provision of efficient

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/078 Audit of the United Nations Environment Programme s Secretariat of the Convention on Biological Diversity Overall results relating to the provision of efficient

REPORT 2014/068 INTERNAL AUDIT DIVISION. Audit of the United Nations Office on Drugs and Crime Intelligence and Law Enforcement Systems project

INTERNAL AUDIT DIVISION REPORT 2014/068 Audit of the United Nations Office on Drugs and Crime Intelligence and Law Enforcement Systems project Overall results relating to management of the Intelligence

INTERNAL AUDIT DIVISION REPORT 2014/068 Audit of the United Nations Office on Drugs and Crime Intelligence and Law Enforcement Systems project Overall results relating to management of the Intelligence

REPORT 2015/115 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/115 Audit of the statistics subprogramme and related technical cooperation projects in the Economic Commission for Africa Overall results relating to effective management

INTERNAL AUDIT DIVISION REPORT 2015/115 Audit of the statistics subprogramme and related technical cooperation projects in the Economic Commission for Africa Overall results relating to effective management

INTERNAL AUDIT DIVISION REPORT 2017/136. Audit of finance and human resources management in the United Nations Disengagement Observer Force

INTERNAL AUDIT DIVISION REPORT 2017/136 Audit of finance and human resources management in the United Nations Disengagement Observer Force The Mission needed to enhance budget monitoring and review the

INTERNAL AUDIT DIVISION REPORT 2017/136 Audit of finance and human resources management in the United Nations Disengagement Observer Force The Mission needed to enhance budget monitoring and review the

REPORT 2015/174 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/174 Audit of management of selected subprogrammes and related capacity development projects in the United Nations Economic and Social Commission for Asia and the Pacific

INTERNAL AUDIT DIVISION REPORT 2015/174 Audit of management of selected subprogrammes and related capacity development projects in the United Nations Economic and Social Commission for Asia and the Pacific

INTERNAL AUDIT DIVISION REPORT 2017/038. Audit of general services contracts management in the United Nations Mission in the Republic of South Sudan

INTERNAL AUDIT DIVISION REPORT 2017/038 Audit of general services contracts management in the United Nations Mission in the Republic of South Sudan The Mission needed to implement costeffective arrangements

INTERNAL AUDIT DIVISION REPORT 2017/038 Audit of general services contracts management in the United Nations Mission in the Republic of South Sudan The Mission needed to implement costeffective arrangements

REPORT 2016/054 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/054 Audit of selected subprogrammes and related technical cooperation projects in the Economic Commission for Europe Overall results relating to the effective management

INTERNAL AUDIT DIVISION REPORT 2016/054 Audit of selected subprogrammes and related technical cooperation projects in the Economic Commission for Europe Overall results relating to the effective management

REPORT 2016/081 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/081 Audit of selected subprogrammes and related technical cooperation projects in the Economic and Social Commission for Western Asia Overall results relating to the

INTERNAL AUDIT DIVISION REPORT 2016/081 Audit of selected subprogrammes and related technical cooperation projects in the Economic and Social Commission for Western Asia Overall results relating to the

REPORT 2016/012 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/012 Audit of the management of the technical cooperation project on Information and Communication Technologies in Africa Phase II in the Economic Commission for Africa

INTERNAL AUDIT DIVISION REPORT 2016/012 Audit of the management of the technical cooperation project on Information and Communication Technologies in Africa Phase II in the Economic Commission for Africa

INTERNAL AUDIT DIVISION REPORT 2018/014. Audit of quick-impact projects in the African Union-United Nation Hybrid Operation in Darfur

INTERNAL AUDIT DIVISION REPORT 2018/014 Audit of quick-impact projects in the African Union-United Nation Hybrid Operation in Darfur The Mission needed to ensure that completed projects are used, field

INTERNAL AUDIT DIVISION REPORT 2018/014 Audit of quick-impact projects in the African Union-United Nation Hybrid Operation in Darfur The Mission needed to ensure that completed projects are used, field

INTERNAL AUDIT DIVISION REPORT 2017/073. Audit of accounts receivable and payable in the United Nations Operation in Côte d voire

INTERNAL AUDIT DIVISION REPORT 2017/073 Audit of accounts receivable and payable in the United Nations Operation in Côte d voire There was a need for comprehensive review of accounts receivable and to

INTERNAL AUDIT DIVISION REPORT 2017/073 Audit of accounts receivable and payable in the United Nations Operation in Côte d voire There was a need for comprehensive review of accounts receivable and to

REPORT 2014/015 INTERNAL AUDIT DIVISION. Audit of selected guaranteed maximum price contracts in the Office of Capital Master Plan

INTERNAL AUDIT DIVISION REPORT 2014/015 Audit of selected guaranteed maximum price contracts in the Office of Capital Master Plan Overall results relating to the audit of selected guaranteed maximum price

INTERNAL AUDIT DIVISION REPORT 2014/015 Audit of selected guaranteed maximum price contracts in the Office of Capital Master Plan Overall results relating to the audit of selected guaranteed maximum price

REPORT 2014/147 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2014/147 Audit of administration of selected pension benefits by the Geneva Office of the United Nations Joint Staff Pension Fund Overall results relating to the effective

INTERNAL AUDIT DIVISION REPORT 2014/147 Audit of administration of selected pension benefits by the Geneva Office of the United Nations Joint Staff Pension Fund Overall results relating to the effective

INTERNAL AUDIT DIVISION REPORT 2017/139

INTERNAL AUDIT DIVISION REPORT 2017/139 Audit of budget formulation and monitoring in the United Nations Multidimensional Integrated Stabilization Mission in the Central African Republic MINUSCA needed

INTERNAL AUDIT DIVISION REPORT 2017/139 Audit of budget formulation and monitoring in the United Nations Multidimensional Integrated Stabilization Mission in the Central African Republic MINUSCA needed

REPORT 2016/038 INTERNAL AUDIT DIVISION. Audit of the Office for the Coordination of Humanitarian Affairs operations in South Sudan

INTERNAL AUDIT DIVISION REPORT 2016/038 Audit of the Office for the Coordination of Humanitarian Affairs operations in South Sudan Overall results relating to the effective management of operations in

INTERNAL AUDIT DIVISION REPORT 2016/038 Audit of the Office for the Coordination of Humanitarian Affairs operations in South Sudan Overall results relating to the effective management of operations in

REPORT 2015/178 INTERNAL AUDIT DIVISION. Audit of the United Nations Human Settlements Programme Regional Office for Arab States

INTERNAL AUDIT DIVISION REPORT 2015/178 Audit of the United Nations Human Settlements Programme Regional Office for Arab States Overall results relating to Regional Office for Arab States operations were

INTERNAL AUDIT DIVISION REPORT 2015/178 Audit of the United Nations Human Settlements Programme Regional Office for Arab States Overall results relating to Regional Office for Arab States operations were

REPORT 2014/024 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2014/024 Audit of the United Nations Environment Programme Secretariat of the Basel, Rotterdam and Stockholm Conventions Overall results relating to the efficient and effective

INTERNAL AUDIT DIVISION REPORT 2014/024 Audit of the United Nations Environment Programme Secretariat of the Basel, Rotterdam and Stockholm Conventions Overall results relating to the efficient and effective

REPORT 2014/051 INTERNAL AUDIT DIVISION. Audit of the process of reporting cases of fraud or presumptive fraud in financial statements

INTERNAL AUDIT DIVISION REPORT 2014/051 Audit of the process of reporting cases of fraud or presumptive fraud in financial statements Overall results relating to the completeness and accuracy of reporting

INTERNAL AUDIT DIVISION REPORT 2014/051 Audit of the process of reporting cases of fraud or presumptive fraud in financial statements Overall results relating to the completeness and accuracy of reporting

REPORT 2016/030 INTERNAL AUDIT DIVISION. Audit of project management at the United Nations Institute for Training and Research

INTERNAL AUDIT DIVISION REPORT 2016/030 Audit of project management at the United Nations Institute for Training and Research Overall results relating to effective management of projects were initially

INTERNAL AUDIT DIVISION REPORT 2016/030 Audit of project management at the United Nations Institute for Training and Research Overall results relating to effective management of projects were initially

INTERNAL AUDIT DIVISION REPORT 2016/155. Audit of the United Nations Human Settlements Programme project management process

INTERNAL AUDIT DIVISION REPORT 2016/155 Audit of the United Nations Human Settlements Programme project management process Established policies and procedures need to be further strengthened, particularly

INTERNAL AUDIT DIVISION REPORT 2016/155 Audit of the United Nations Human Settlements Programme project management process Established policies and procedures need to be further strengthened, particularly

REPORT 2016/062 INTERNAL AUDIT DIVISION. Audit of the management of trust funds at the United Nations Framework Convention on Climate Change

INTERNAL AUDIT DIVISION REPORT 2016/062 Audit of the management of trust funds at the United Nations Framework Convention on Climate Change Overall results relating to the effective management of trust

INTERNAL AUDIT DIVISION REPORT 2016/062 Audit of the management of trust funds at the United Nations Framework Convention on Climate Change Overall results relating to the effective management of trust

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/053. Audit of the management of the ecosystem sub-programme in the United Nations Environment Programme

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/053 Audit of the management of the ecosystem sub-programme in the United Nations Environment Programme Overall results relating to effective management of the

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/053 Audit of the management of the ecosystem sub-programme in the United Nations Environment Programme Overall results relating to effective management of the

REPORT 2015/009 INTERNAL AUDIT DIVISION. Audit of a donor-funded project implemented by the International Trade Centre in Côte d Ivoire

INTERNAL AUDIT DIVISION REPORT 2015/009 Audit of a donor-funded project implemented by the International Trade Centre in Côte d Ivoire Overall results relating to the effective management of the donor-funded

INTERNAL AUDIT DIVISION REPORT 2015/009 Audit of a donor-funded project implemented by the International Trade Centre in Côte d Ivoire Overall results relating to the effective management of the donor-funded

REPORT 2017/148. Audit of budget formulation and monitoring in the United Nations Interim Force in Lebanon

INTERNAL AUDIT DIVISION REPORT 2017/148 Audit of budget formulation and monitoring in the United Nations Interim Force in Lebanon The Mission aligned its budget with its mandate and improved budget monitoring,

INTERNAL AUDIT DIVISION REPORT 2017/148 Audit of budget formulation and monitoring in the United Nations Interim Force in Lebanon The Mission aligned its budget with its mandate and improved budget monitoring,

INTERNAL AUDIT DIVISION REPORT 2017/025

INTERNAL AUDIT DIVISION REPORT 2017/025 Audit of quick impact projects in the United Nations Multidimensional Integrated Stabilization Mission in the Central African Republic There was a need to strengthen

INTERNAL AUDIT DIVISION REPORT 2017/025 Audit of quick impact projects in the United Nations Multidimensional Integrated Stabilization Mission in the Central African Republic There was a need to strengthen

DESK REVIEW UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN

UNITED NATIONS DEVELOPMENT PROGRAMME DESK REVIEW OF UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN Report No. 1310 Issue Date: 9 October 2014 Table of

UNITED NATIONS DEVELOPMENT PROGRAMME DESK REVIEW OF UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN Report No. 1310 Issue Date: 9 October 2014 Table of

AUDIT UNDP COUNTRY OFFICE AFGHANISTAN FINANCIAL MANAGEMENT. Report No Issue Date: 10 December 2013

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AFGHANISTAN FINANCIAL MANAGEMENT Report No. 1233 Issue Date: 10 December 2013 Table of Contents Executive Summary i I. Introduction

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AFGHANISTAN FINANCIAL MANAGEMENT Report No. 1233 Issue Date: 10 December 2013 Table of Contents Executive Summary i I. Introduction

AUDIT REPORT. Travel and Hospitality

AUDIT REPORT Travel and Hospitality Table of Contents 1.0 Executive Summary... 1 1.1 Background and Context... 1 1.2 Overall Assessment / Audit Opinion... 1 1.3 Strengths... 2 1.4 Main Observations...

AUDIT REPORT Travel and Hospitality Table of Contents 1.0 Executive Summary... 1 1.1 Background and Context... 1 1.2 Overall Assessment / Audit Opinion... 1 1.3 Strengths... 2 1.4 Main Observations...

INTERNAL AUDIT DIVISION REPORT 2017/003

INTERNAL AUDIT DIVISION REPORT 2017/003 Audit of the management of the sustainable development subprogramme in the Department of Economic and Social Affairs The Division for Sustainable Development needed

INTERNAL AUDIT DIVISION REPORT 2017/003 Audit of the management of the sustainable development subprogramme in the Department of Economic and Social Affairs The Division for Sustainable Development needed

INTERNAL AUDIT DIVISION REPORT 2018/058. Audit of the management of the regular programme of technical cooperation

INTERNAL AUDIT DIVISION REPORT 2018/058 Audit of the management of the regular programme of technical cooperation There was a need to enhance complementarity of activities related to the regular programme

INTERNAL AUDIT DIVISION REPORT 2018/058 Audit of the management of the regular programme of technical cooperation There was a need to enhance complementarity of activities related to the regular programme

AUDIT UNDP AFGHANISTAN. Local Governance Project (Project No ) Report No Issue Date: 23 December 2016

Report No Issue Date: 23 December 2016") UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP AFGHANISTAN Local Governance Project (Project No. 90448) Report No. 1745 Issue Date: 23 December 2016 Table of Contents Executive Summary i I. About the

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP AFGHANISTAN Local Governance Project (Project No. 90448) Report No. 1745 Issue Date: 23 December 2016 Table of Contents Executive Summary i I. About the

INTERNAL AUDIT DIVISION REPORT 2018/052. Audit of liquidation activities at the International Criminal Tribunal for the former Yugoslavia

INTERNAL AUDIT DIVISION REPORT 2018/052 Audit of liquidation activities at the International Criminal Tribunal for the former Yugoslavia Overall, liquidation activities were performed satisfactorily 31

INTERNAL AUDIT DIVISION REPORT 2018/052 Audit of liquidation activities at the International Criminal Tribunal for the former Yugoslavia Overall, liquidation activities were performed satisfactorily 31

AUDIT. UNDP Pakistan. Early Recovery Programme in Pakistan (Directly Implemented Project No ) Report No. 990 Issue Date: 19 June 2013

Report No. 990 Issue Date: 19 June 2013") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP Pakistan Early Recovery Programme in Pakistan (Directly Implemented Project No. 76295) Report No. 990 Issue Date: 19

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP Pakistan Early Recovery Programme in Pakistan (Directly Implemented Project No. 76295) Report No. 990 Issue Date: 19

REPORT 2016/098 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/098 Audit of the arrangements for fleet management at the Office of the United Nations High Commissioner for Refugees Overall results relating to the effective management

INTERNAL AUDIT DIVISION REPORT 2016/098 Audit of the arrangements for fleet management at the Office of the United Nations High Commissioner for Refugees Overall results relating to the effective management

Dear Ms. Lawrence and Members of the Board of Commissioners:

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

Internal / External Job Opening

U N I T E D N A T I O N S N A T I O N S U N I E S INTERIM FORCE IN LEBANON FORCE INTERIMAIRE AU LIBAN Internal / External Job Opening Date: 30 November 2016 Vacancy N : JO/2016/005/A Section : Finance

U N I T E D N A T I O N S N A T I O N S U N I E S INTERIM FORCE IN LEBANON FORCE INTERIMAIRE AU LIBAN Internal / External Job Opening Date: 30 November 2016 Vacancy N : JO/2016/005/A Section : Finance

AUDIT REPORT INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION AUDIT REPORT Governance and organizational structure of the inter-agency secretariat to the United Nations International Strategy for Disaster Risk Reduction (ISDR) The ISDR secretariat

INTERNAL AUDIT DIVISION AUDIT REPORT Governance and organizational structure of the inter-agency secretariat to the United Nations International Strategy for Disaster Risk Reduction (ISDR) The ISDR secretariat

OFFICE OF THE STATE COMPTROLLER

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

UN-Habitat Policy For Implementing Partners. UN-Habitat. Policy For. Partners

UN-Habitat Policy For Implementing Partners 01 Version Date Author/Reviewer Status V1 06.12.2016 Mohamed Robleh Circulated for SMB comments V2 27.01.2017 Andrew Cox Approved For further information, please

UN-Habitat Policy For Implementing Partners 01 Version Date Author/Reviewer Status V1 06.12.2016 Mohamed Robleh Circulated for SMB comments V2 27.01.2017 Andrew Cox Approved For further information, please

Office of the City Auditor. Committed to increasing government efficiency, effectiveness, accountability and transparency

Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date: TABLE OF CONTENTS Executive Summary... ii Background...1 Findings &

Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date: TABLE OF CONTENTS Executive Summary... ii Background...1 Findings &

Terms of Reference for Financial Audit of Implementing Partners. UNICEF Nigeria Country Office Expenditures

Terms of Reference for Financial Audit of Implementing Partners UNICEF Nigeria Country Office 2012-2013 Expenditures A. Background and Scope of Audit Harmonized Approach to Cash Transfer (HACT) is a response

Terms of Reference for Financial Audit of Implementing Partners UNICEF Nigeria Country Office 2012-2013 Expenditures A. Background and Scope of Audit Harmonized Approach to Cash Transfer (HACT) is a response

Module 4 Session 2: Understanding County Audit Reports

Module 4 Session 2: Understanding County Audit Reports KEY TAKEAWAYS AUDIT REPORTS ARE IMPORTANT FOR OVERSIGHT BY BOTH THE PUBLIC AND THE COUNTY ASSEMBLIES AUDIT REPORTS GIVE AN INDEPENDENT OPINION OF

Module 4 Session 2: Understanding County Audit Reports KEY TAKEAWAYS AUDIT REPORTS ARE IMPORTANT FOR OVERSIGHT BY BOTH THE PUBLIC AND THE COUNTY ASSEMBLIES AUDIT REPORTS GIVE AN INDEPENDENT OPINION OF

AUDIT UNDP COUNTRY OFFICE SOMALIA. Report No Issue Date: 20 June 2014

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN SOMALIA Report No. 1299 Issue Date: 20 June 2014 Table of Contents Executive Summary ii I. About the Office 1 II. Audit results 1 A.

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN SOMALIA Report No. 1299 Issue Date: 20 June 2014 Table of Contents Executive Summary ii I. About the Office 1 II. Audit results 1 A.

AUDIT UNDP COUNTRY OFFICE BANGLADESH. Report No Issue Date: 28 May 2015

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN BANGLADESH Report No. 1429 Issue Date: 28 May 2015 Table of Contents Executive Summary i I. About the Office 1 II. Good practice 1 III.

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN BANGLADESH Report No. 1429 Issue Date: 28 May 2015 Table of Contents Executive Summary i I. About the Office 1 II. Good practice 1 III.

STATE OF NEVADA OFFICE OF LIEUTENANT GOVERNOR

STATE OF NEVADA OFFICE OF LIEUTENANT GOVERNOR AUDIT REPORT Table of Contents Page Executive Summary... 1 Introduction... 4 Background... 4 Scope and Objective... 5 Findings and Recommendations... 6 Financial

STATE OF NEVADA OFFICE OF LIEUTENANT GOVERNOR AUDIT REPORT Table of Contents Page Executive Summary... 1 Introduction... 4 Background... 4 Scope and Objective... 5 Findings and Recommendations... 6 Financial

SIGAR JULY. Special Inspector General for Afghanistan Reconstruction

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR Financial Audit 13-6 USDA s Program to Help Advance the Revitalization of Afghanistan s Agricultural Sector: Audit of Costs Incurred

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR Financial Audit 13-6 USDA s Program to Help Advance the Revitalization of Afghanistan s Agricultural Sector: Audit of Costs Incurred

Internal Audit. Orange County Auditor-Controller

Orange County Auditor-Controller Internal Audit Countywide Audit of County Business Travel and Meeting Policy Clerk of the Board of Supervisors For the Fiscal Year Ended June 30, 2017 Audit Number 1626-E

Orange County Auditor-Controller Internal Audit Countywide Audit of County Business Travel and Meeting Policy Clerk of the Board of Supervisors For the Fiscal Year Ended June 30, 2017 Audit Number 1626-E

AUDIT UNDP COUNTRY OFFICE UGANDA. Report No Issue Date: 22 August 2013

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN UGANDA Report No. 1155 Issue Date: 22 August 2013 Table of Contents Executive Summary i I. Introduction 1 II. About the Office 1 III.

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN UGANDA Report No. 1155 Issue Date: 22 August 2013 Table of Contents Executive Summary i I. Introduction 1 II. About the Office 1 III.

STATEMENT OF WORK FOR RECIPIENT CONTRACTED AUDIT OF USAID RESOURCES MANAGED BY THE WEST AFRICAN HEALTH ORGANIZATION (WAHO)

") STATEMENT OF WORK FOR RECIPIENT CONTRACTED AUDIT OF USAID RESOURCES MANAGED BY THE WEST AFRICAN HEALTH ORGANIZATION (WAHO) AUDIT OF USAID RESOURCES MANAGED BY WEST AFRICAN HEALTH ORGANIZATION UNDER THE

STATEMENT OF WORK FOR RECIPIENT CONTRACTED AUDIT OF USAID RESOURCES MANAGED BY THE WEST AFRICAN HEALTH ORGANIZATION (WAHO) AUDIT OF USAID RESOURCES MANAGED BY WEST AFRICAN HEALTH ORGANIZATION UNDER THE

AUDIT UNDP NIGERIA. DEMOCRATIC GOVERNANCE FOR DEVELOPMENT: DEEPENING DEMOCRACY IN NIGERIA (Directly Implemented Project No , Output No.

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP NIGERIA DEMOCRATIC GOVERNANCE FOR DEVELOPMENT: DEEPENING DEMOCRACY IN NIGERIA (Directly Implemented Project No. 56855,

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP NIGERIA DEMOCRATIC GOVERNANCE FOR DEVELOPMENT: DEEPENING DEMOCRACY IN NIGERIA (Directly Implemented Project No. 56855,

Support to Farmers Organisations in Africa Programme (SFOAP) Main Phase Start-up Workshop Fiduciary Aspects Addis Ababa, March 2013

Main Phase Start-up Workshop Fiduciary Aspects Addis Ababa, March 2013") Support to Farmers Organisations in Africa Programme (SFOAP) Main Phase Start-up Workshop Fiduciary Aspects Addis Ababa, 12-15 March 2013 1 FM Seminar Overview FM and Fiduciary Responsibilities Overview;

Support to Farmers Organisations in Africa Programme (SFOAP) Main Phase Start-up Workshop Fiduciary Aspects Addis Ababa, 12-15 March 2013 1 FM Seminar Overview FM and Fiduciary Responsibilities Overview;

FINANCIAL MANAGEMENT ASSESSMENT

Greater Malé Environmental Improvement and Waste Management Project (RRP MLD 51077) EXECUTIVE SUMMARY FINANCIAL MANAGEMENT ASSESSMENT 1. The financial management assessment (FMA) was conducted for the

Greater Malé Environmental Improvement and Waste Management Project (RRP MLD 51077) EXECUTIVE SUMMARY FINANCIAL MANAGEMENT ASSESSMENT 1. The financial management assessment (FMA) was conducted for the

Financial Statements. Contents

Contents 81 Introduction to the Directors statement and independent auditor s reports 82 Statement of Directors responsibilities 83 Independent auditor s report 92 Report of independent registered public

Contents 81 Introduction to the Directors statement and independent auditor s reports 82 Statement of Directors responsibilities 83 Independent auditor s report 92 Report of independent registered public

Office of Inspector General University of South Florida

Office of Inspector General University of South Florida Project # A-1718DOE-017 November 2018 Executive Summary In accordance with the Department of Education s fiscal year (FY) 2017-18 audit plan, the

Office of Inspector General University of South Florida Project # A-1718DOE-017 November 2018 Executive Summary In accordance with the Department of Education s fiscal year (FY) 2017-18 audit plan, the

EACEA. Cluster Meeting

EACEA Cluster Meeting European Policy Experimentations the Way Forward 21 June 2017 Audit Type I & II Certificates Alexandre Virosztek Unit R2 «Legal and Regulatory» 1 Controls & Checks Controls (wide)

EACEA Cluster Meeting European Policy Experimentations the Way Forward 21 June 2017 Audit Type I & II Certificates Alexandre Virosztek Unit R2 «Legal and Regulatory» 1 Controls & Checks Controls (wide)

Dorchester School District Two

Dorchester School District Two Procurement Card Program Policies and Procedures Dorchester School District Two Procurement Card Program INTRODUCTION Welcome to the Dorchester School District Two s Procurement

Dorchester School District Two Procurement Card Program Policies and Procedures Dorchester School District Two Procurement Card Program INTRODUCTION Welcome to the Dorchester School District Two s Procurement

GUIDANCE DOCUMENT ON THE FUNCTIONS OF THE CERTIFYING AUTHORITY. for the programming period

Final version of 25/07/2008 COCOF 08/0014/02-EN GUIDANCE DOCUMENT ON THE FUNCTIONS OF THE CERTIFYING AUTHORITY for the 2007 2013 programming period Table of contents 1. Introduction... 3 2. Main functions

Final version of 25/07/2008 COCOF 08/0014/02-EN GUIDANCE DOCUMENT ON THE FUNCTIONS OF THE CERTIFYING AUTHORITY for the 2007 2013 programming period Table of contents 1. Introduction... 3 2. Main functions

STUDENT ACTIVITY FUND GUIDANCE

STUDENT ACTIVITY FUND GUIDANCE OVERVIEW Student activities require the participation of students. Student activity funds are monies generated by students participation, authorized to be spent by students,

STUDENT ACTIVITY FUND GUIDANCE OVERVIEW Student activities require the participation of students. Student activity funds are monies generated by students participation, authorized to be spent by students,

Financial reports and audited financial statements and reports of the Board of Auditors for the period ended 31 December 2009

United Nations A/65/498 General Assembly Distr.: General 8 October 2010 Original: English Sixty-fifth session Agenda item 127 Financial reports and audited financial statements, and reports of the Board

United Nations A/65/498 General Assembly Distr.: General 8 October 2010 Original: English Sixty-fifth session Agenda item 127 Financial reports and audited financial statements, and reports of the Board

INTERNAL AUDIT DIVISION REPORT 2019/010. Audit of management of the Transport International Routier Trust Fund at the Economic Commission for Europe

INTERNAL AUDIT DIVISION REPORT 2019/010 Audit of management of the Transport International Routier Trust Fund at the Economic Commission for Europe Controls over governance and financial management need

INTERNAL AUDIT DIVISION REPORT 2019/010 Audit of management of the Transport International Routier Trust Fund at the Economic Commission for Europe Controls over governance and financial management need

Audit of Citywide Purchase-Card Use

Report # 2012-06 Jorge Oseguera City Auditor Scott Herbstman Auditor Audit of Citywide Purchase-Card Use While transactions reviewed did not reveal extensive personal purchases, some charges violated policy

Report # 2012-06 Jorge Oseguera City Auditor Scott Herbstman Auditor Audit of Citywide Purchase-Card Use While transactions reviewed did not reveal extensive personal purchases, some charges violated policy

Allegany County Public Schools

Financial Management Practices Audit Report Allegany County Public Schools January 2013 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Financial Management Practices Audit Report Allegany County Public Schools January 2013 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

TERMS OF REFERENCE (TOR) FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS

FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS") TERMS OF REFERENCE (TOR) FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS TABLE OF CONTENTS Introduction... 3 A. Background... 7 B. Project Management... 7 C. Consultations with concerned parties...

TERMS OF REFERENCE (TOR) FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS TABLE OF CONTENTS Introduction... 3 A. Background... 7 B. Project Management... 7 C. Consultations with concerned parties...

Department of Business and Economic Development

Audit Report Department of Business and Economic Development October 2015 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning this

Audit Report Department of Business and Economic Development October 2015 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning this

Accounting System Requirements

Accounting System Requirements Further information is available in the Information for Contractors Manual under Enclosure 2 The views expressed in this presentation are DCAA's views and not necessarily

Accounting System Requirements Further information is available in the Information for Contractors Manual under Enclosure 2 The views expressed in this presentation are DCAA's views and not necessarily

REPORT 2016/017 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/017 Audit of credit risk management in the Investment Management Division of the United Nations Joint Staff Pension Fund Overall results relating to the effective management

INTERNAL AUDIT DIVISION REPORT 2016/017 Audit of credit risk management in the Investment Management Division of the United Nations Joint Staff Pension Fund Overall results relating to the effective management

Audit of the UNESCO Office in Bangkok

Internal Oversight Service Audit Section IOS/AUD/2009/12 Original: English Audit of the UNESCO Office in Bangkok June 2009 Auditors: Craig Nordby Shashank Shekhar Uldis Kremers EXECUTIVE SUMMARY Key Results

Internal Oversight Service Audit Section IOS/AUD/2009/12 Original: English Audit of the UNESCO Office in Bangkok June 2009 Auditors: Craig Nordby Shashank Shekhar Uldis Kremers EXECUTIVE SUMMARY Key Results

AIPHS Financial Procedures

AIPHS Financial Procedures 1. Bank Accounts Shall remain at Community Bank of the Bay and East West Bank. The Board president along with the Superintendent of AIM Schools, shall have signatory power. 2.

AIPHS Financial Procedures 1. Bank Accounts Shall remain at Community Bank of the Bay and East West Bank. The Board president along with the Superintendent of AIM Schools, shall have signatory power. 2.

REPORT ON IMPLEMENTATION OF INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS (IPSAS) Radislav Pretorico

Radislav Pretorico") REPORT ON IMPLEMENTATION OF INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS (IPSAS) Radislav Pretorico Introduction 1. The Fifteenth WMO Congress, in May 2007, approved the adoption of International Public

REPORT ON IMPLEMENTATION OF INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS (IPSAS) Radislav Pretorico Introduction 1. The Fifteenth WMO Congress, in May 2007, approved the adoption of International Public

STANDARD STATEMENT OF WORK FOR FINANCIAL AUDITS OF NON-U.S. ORGANIZATIONS CONTRACTED BY THE RECIPIENT

STANDARD STATEMENT OF WORK FOR FINANCIAL AUDITS OF NON-U.S. ORGANIZATIONS CONTRACTED BY THE RECIPIENT OBJECTIVES AND GENERAL STATEMENT OF WORK AUDIT OF USAID RESOURCES MANAGED BY Dairy & Rural Development

STANDARD STATEMENT OF WORK FOR FINANCIAL AUDITS OF NON-U.S. ORGANIZATIONS CONTRACTED BY THE RECIPIENT OBJECTIVES AND GENERAL STATEMENT OF WORK AUDIT OF USAID RESOURCES MANAGED BY Dairy & Rural Development

HSP/GC/25/5/Add.1 Governing Council of the United Nations Human Settlements Programme. Proposed work programme and budget for the biennium

UNITED NATIONS HSP HSP/GC/25/5/Add.1 Governing Council of the United Nations Human Settlements Programme Distr.: General 2 April 2015 Original: English Twenty-fifth session Nairobi, 1723 April 2015 Item

UNITED NATIONS HSP HSP/GC/25/5/Add.1 Governing Council of the United Nations Human Settlements Programme Distr.: General 2 April 2015 Original: English Twenty-fifth session Nairobi, 1723 April 2015 Item

MEDICAL ASSISTANCE PROGRAMS FRAUD DETECTION FUND LOUISIANA DEPARTMENT OF HEALTH AND OFFICE OF THE LOUISIANA ATTORNEY GENERAL

MEDICAL ASSISTANCE PROGRAMS FRAUD DETECTION FUND LOUISIANA DEPARTMENT OF HEALTH AND OFFICE OF THE LOUISIANA ATTORNEY GENERAL PERFORMANCE AUDIT SERVICES JULY 25, 2018 LOUISIANA LEGISLATIVE AUDITOR 1600

MEDICAL ASSISTANCE PROGRAMS FRAUD DETECTION FUND LOUISIANA DEPARTMENT OF HEALTH AND OFFICE OF THE LOUISIANA ATTORNEY GENERAL PERFORMANCE AUDIT SERVICES JULY 25, 2018 LOUISIANA LEGISLATIVE AUDITOR 1600

Capital Improvement Projects

REPORT # 2011-12 AUDIT Of the Richmond City Department of Parks, Recreation and Community Facilities Capital Improvement Projects TABLE OF CONTENTS Executive Summary..... i Comprehensive List of Recommendations

REPORT # 2011-12 AUDIT Of the Richmond City Department of Parks, Recreation and Community Facilities Capital Improvement Projects TABLE OF CONTENTS Executive Summary..... i Comprehensive List of Recommendations

AUDIT UNDP NEPAL. Comprehensive Disaster Risk Management Programme (Directly Implemented Project No )

") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP NEPAL Comprehensive Disaster Risk Management Programme (Directly Implemented Project No. 77652) Report No. 1200 Issue

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP NEPAL Comprehensive Disaster Risk Management Programme (Directly Implemented Project No. 77652) Report No. 1200 Issue

Control activities that are part of the process are detailed in the riskcontrol

Policy Title Previous title (if any) Cash Transfers to Implementing Partners N/A Policy objective Target audience Risk control matrix Checklist The policy and procedures outline the process for management

Policy Title Previous title (if any) Cash Transfers to Implementing Partners N/A Policy objective Target audience Risk control matrix Checklist The policy and procedures outline the process for management

Internal Audit of WFP Operations in the Republic of Mali

Fighting Hunger Worldwide Internal Audit of WFP Operations in the Republic of of the Inspector General Internal Audit Report AR/14/05 Contents Page I. Executive Summary 3 II. Context and Scope 5 III. Results

Fighting Hunger Worldwide Internal Audit of WFP Operations in the Republic of of the Inspector General Internal Audit Report AR/14/05 Contents Page I. Executive Summary 3 II. Context and Scope 5 III. Results

January 13, Dear Mr. Sweeney and Members of the Board of Fire Commissioners:

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 STEVEN J. HANCOX DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 STEVEN J. HANCOX DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

Transfer Payment Agency Accountability and Governance

MINISTRY OF COMMUNITY AND SOCIAL SERVICES Transfer Payment Agency Accountability and Governance The Ministry of Community and Social Services plans and arranges for a wide variety of social services throughout

MINISTRY OF COMMUNITY AND SOCIAL SERVICES Transfer Payment Agency Accountability and Governance The Ministry of Community and Social Services plans and arranges for a wide variety of social services throughout

Guidance on a common methodology for the assessment of management and control systems in the Member States ( programming period)

") Final version of 12/09/2008 EUROPEAN COMMISSION DIRECTORATE-GENERAL MARITIME AFFAIRS AND FISHERIES EFFC/27/2008 Guidance on a common methodology for the assessment of management and control systems in

Final version of 12/09/2008 EUROPEAN COMMISSION DIRECTORATE-GENERAL MARITIME AFFAIRS AND FISHERIES EFFC/27/2008 Guidance on a common methodology for the assessment of management and control systems in

AUDIT OF THE FUND ACCOUNTABILITY STATEMENT OF USAID RESOURCES MANAGED BY MERCY CORPS AND IMPLEMENTED BY PUBLIC AID ORGANIZATION ( PAO ) UNDER

UNDER") AUDIT OF THE FUND ACCOUNTABILITY STATEMENT OF USAID RESOURCES MANAGED BY MERCY CORPS AND IMPLEMENTED BY PUBLIC AID ORGANIZATION ( PAO ) UNDER COOPERATIVE AGREEMENT NUMBER AID-267-A-00-12-00001, CFDA #

AUDIT OF THE FUND ACCOUNTABILITY STATEMENT OF USAID RESOURCES MANAGED BY MERCY CORPS AND IMPLEMENTED BY PUBLIC AID ORGANIZATION ( PAO ) UNDER COOPERATIVE AGREEMENT NUMBER AID-267-A-00-12-00001, CFDA #

Audit Team: County Auditor: John Hutzler, CIA, CGAP, CCSA Auditor Assigned: Mona Rabii, CIA, CISA, CGAP Latham Stack, CIA, CGAP

February 24, 2014 TO: FROM: SUBJECT: Board of Commissioners John Hutzler, County Auditor Audit of Executive Expenses Attached is the County Auditor s report on Executive Expenses together with the response

February 24, 2014 TO: FROM: SUBJECT: Board of Commissioners John Hutzler, County Auditor Audit of Executive Expenses Attached is the County Auditor s report on Executive Expenses together with the response

Document No: AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF MUNICIPALITY OF KAMENICA FOR THE YEAR ENDED 31 DECEMBER 2017

Document No: 22.29.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF MUNICIPALITY OF KAMENICA FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, May 2018 The National Audit Office of the Republic

Document No: 22.29.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF MUNICIPALITY OF KAMENICA FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, May 2018 The National Audit Office of the Republic

THE UNITED REPUBLIC OF TANZANIA NATIONAL AUDIT OFFICE (NAO)

") THE UNITED REPUBLIC OF TANZANIA NATIONAL AUDIT OFFICE (NAO) REPORT OF THE CONTROLLER AND AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF THE HIGH COURT COMMERCIAL COURT DIVISION FOR THE YEAR ENDED 30 TH

THE UNITED REPUBLIC OF TANZANIA NATIONAL AUDIT OFFICE (NAO) REPORT OF THE CONTROLLER AND AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF THE HIGH COURT COMMERCIAL COURT DIVISION FOR THE YEAR ENDED 30 TH