Terms of Reference for Financial Audit of Implementing Partners. UNICEF Nigeria Country Office Expenditures

|

|

|

- Milton Sharp

- 5 years ago

- Views:

Transcription

is a response of Rome Declaration on Harmonization and Paris Declaration on Aid Effectiveness.")

1 Terms of Reference for Financial Audit of Implementing Partners UNICEF Nigeria Country Office Expenditures A. Background and Scope of Audit Harmonized Approach to Cash Transfer (HACT) is a response of Rome Declaration on Harmonization and Paris Declaration on Aid Effectiveness. This risk management approach allows the UN to shift its efforts away from input monitoring to achievement of programme results and strengthening of national capacities for management and accountability, with a view to gradually shift to the use of national systems. Before implementation of HACT in 2009 by UNDP, UNICEF and UNFPA in Nigeria, macro assessment was done in 2008 on the Public Financial Management of Nigeria. It was followed by Micro Assessment of 61 Implementing Partners (IPs) in September IP refers to institution that signs the Funding Authorization and Certificate of Expenditure (FACE) forms as attached in Annex 1, and it assumes responsibilities for ensuring adequacy of the overall supervision and management of work plan activities funded by the UN Agency, within the framework of the Country Programme Action Plan (CPAP). As from January 2014, the UN Agencies will start a new programme cycle for From the Common Country Assessment (CCA), the United Nation Development Assistant Framework (UNDAF) was developed based on which the Country Programme Document (CDP) was prepared. The CPD was approved by the UNICEF Executive Board. The UNICEF s CPAP for and its one year extension to 2013, was approved by Nigeria federal government through a series of consultation with the Government and other development stake holders. Annual Work Plans (AWPs) with government are developed annually based on the results matrix in the CPAP. UNICEF also supports implementation of the CPAP through nongovernmental organisations. This is done through Programme Cooperation Agreements which contain separate Work Plans with budgets and implementing partners. Based on the AWPs, funds are disbursed to the respective IPs and/or third parties accordingly. Along with the micro assessments, assurance activities, including spot-checks and programmatic monitoring are undertaken to get assurance that the resources disbursed to implementing partners are managed in accordance with the AWPs and applicable rules and regulations. 1

2 The main purpose of the audit will be to assess the existence and functioning of the IPs internal controls for the receipt, recording and disbursement of cash transfers and the fairness of a sample of expenditures reported in the FACE forms 1. The list of IPs to be audited is attached as Annex 2 and has details such as name of IP, address of IP and the amount of funds transferred/received during the year 2012 and More specifically, the audit exercise shall strive to obtain reasonable assurance that: All cash transfers to and from the IP and reported expenditures were based on the AWPs agreed between the respective IPs and UNICEF within the specific period being audited. The AWPs will provide information on the summary of activities for which funding was provided by UNICEF, the intended major results, budgets and total amount disbursed. Expenditures were valid and are supported by adequate and valid documentation. Appropriate and reliable systems for internal controls have been incorporated in the project and are being observed. Financial reports have been accurately stated and fairly presented. Assets for the Programme have been accurately stated and fairly presented. Cash position of the Programme has been accurately stated and fairly presented. Other substantive responsibilities of the IPs, including the submission of periodic monitoring and evaluation reports, have been adequately fulfilled. Any major findings of the micro-assessments or any observations from ongoing programme and financial monitoring have been appropriately addressed. Each accounting and/or reporting in the following areas have been properly addressed: 1. A review of the IP s internal controls. 2. A review of the implementation of recommendations made in the micro-assessment of the IP. 3. Verification of a sample of transactions, drawn from a sample of the FACE Forms. 4. Recommendations to the IP to improve its internal controls. It should be underlined that within the framework of the HACT implementation, the focus of the audit will be on the assessment of the IP s internal controls for the receipt, recording and disbursement of cash transfers and the fairness of a sample of expenditures reported in the FACE forms. The financial audit of the IPs includes a sample of expenditures from different projects/awards that are part of the IP s portfolio which will be reviewed to determine the fairness and accuracy of expenditures reported in the FACE forms. 1 It is not expected that the sample will provide assurance for individual FACE forms. 2

3 The audit will review the IP s internal controls systems and the status of the implementation of recommendations made in the micro-assessments and spot checks. it will also verify supporting documentations to a sample of transactions and make recommendations to the IPs to improve their internal controls. B. Consultations with UNICEF and Implementing Partners Prior to and during the conduct of the audit, the audit team will carry out consultations as outlined below: Meeting with UNICEF for firming up the plan of the audit, and discuss any emerging issues. Entrance meeting attended by UNICEF and IPs and the audit team to discuss any issues/concerns they may have. Follow up meeting with the IPs to elaborate the plan for the audit field work. Upon completion of the draft report, the auditors should first hold a debriefing meeting (known as the Exit Meeting) with the IP and related party as appropriate, to discuss findings and recommendations for future improvements, as well as to seek their feedback thereon. These meetings should be documented by the auditors and shared with the IP s and UNICEF. The auditors will then meet with UNICEF to discuss the draft report prior to its finalization. C. Tasks 1. Review of the Implementing Partner s programme management system In order to facilitate an overall review of the management of the AWPs implementation by the IPs, the auditors will: Review CPAP, AWP(s), FACE Forms and where applicable UNICEF manuals, to determine whether periodicity of FACE form submissions was in accordance with the planned timeline, and whether requests for disbursements and reports on utilization of cash were provided for activities described in AWP(s). Through interviews and review of progress reports prepared by the IP, establish whether activities were implemented as planned. Where activities (timeliness, type, quantity) deviated significantly from the original AWP(s), establish whether this was by mutual agreement between the IP and UNICEF. Determine and comment on the causes for significant delays or changes, if any. Review the IP s system of monitoring progress and review of reports, including field monitoring visit reports and progress reports, to assess whether the IPs met its responsibilities for monitoring as described in the CPAP and AWPs. Review whether recommendations recorded in programme monitoring reports or minutes of meetings between the IPs and UNICEF have been implemented by the IP. 3

4 2. Assessment of the IP s internal controls The auditors will carry out specific tasks that will provide an overall assessment on the functioning of the IP s internal controls, with emphasis on: i. the effectiveness of the system in providing the Implementing Partner s management with useful and timely information for the proper management of the AWP; and ii. the general effectiveness of the internal control system in protecting the assets and resources provided for implementation of AWP activities. These tasks will include: Conduct a general assessment of the IP s internal controls according to international standards. Review whether recommendations made in the micro assessment or spot checks were implemented or, if not, determine the implementation status and reasons. Review FACE Forms, including the records of requests for direct payments if any, to assess whether they were signed by designated officials of the IPs. Review the processes used by the IP for authorizing expenditures and assess whether they are in accordance with the CPAP and AWP. Review the process for procurement/contracting of supplies and services and assess whether it is transparent and competitive. Review the use, control and disposal of non-expendable equipment and assess whether it is in compliance with government policies (or UNICEF manuals, where so specified in the CPAP/AWP); and also, whether the equipment procured met the identified needs and whether it is used in accordance with intended purposes. Review relevant IT systems. Where UNICEF s funds pay for the personnel or consultants, review the process followed for recruiting the Implementing Partner s personnel and consultants and assess whether it is transparent and competitive. Review the Implementing Partner s accounting records and assess their adequacy for maintaining accurate and complete records of receipt of funds provided by UNICEF and disbursements of cash. Interview officials of the Implementing Partner, as necessary, to ensure full understanding of the functioning of the internal control system. 3. Review of a sample of FACE forms and transaction testing The audit team will examine the following documentation to determine whether they were designed to test compliance with the IPs internal controls: Assess whether the funds received from UNICEF were deposited into the IP s bank account by verifying the bank statement. 4

5 Reconcile the expenditure totals, per activity, on the FACE forms to the list of individual transactions (i.e. the IP s accounting records). For each activity, review the nature of expenditure and assess the reasonableness. Discuss any concerns with management. Select a sample for the pre-audit risk assessment provided by UNICEF during the initial consultation, and may depend on the ratings from the micro-assessments of the IP, spot-checks, and any concerns that have arisen during the period under review, materiality, and required confidence level. The use of statistical sampling should be considered as a tool for the audit. Samples should be drawn from sets of transactions stratified by transaction type (including - UNICEF to specify: procurement of supplies and services; institutional contracts; contracting of consultants; salary supplements, where applicable; per diems; travel related expenditure; other type of expenditures; locations) with emphasis on materiality/high value items. Alternatively, random sampling techniques could be considered. The audit includes a sample of expenditures from different programmes that are part of the IP s portfolio which will be reviewed to determine the fairness and accuracy of expenditures reported in the FACE form. For this sample of transactions, carry out a verification of the accuracy and completeness of supporting documentation (e.g vouchers, invoices, purchase orders, receipt of goods, bank transfers/checks, bank statements) to assess whether they are properly authorized, documented, certified and accounted for; and are consistent with the description of the transaction (per the accounting records) and per the AWP. Compare the price paid for goods or services against market benchmarks. Include other appropriate measures of value for money. D. Deliverables The audit report should include at the minimum: An Opinion (see Annex 3) on the functioning of internal controls. An Executive Summary with the key findings, risks and recommendations. A summary of the main identified risks to the management of agreed activities and the use of funds provided by UNICEF, arising from weak internal controls. Any identified specific internal control weaknesses in the financial management of the IP. Recommendations on how the identified risks may be better managed, and how the IP s internal controls can be strengthened. Recommendations should clearly identify those responsible for their implementation within the IP. The comments of the IP should be included in report, under the recommendation. 5

6 Comments on the follow-up to the recommendations from previous micro assessment and spot checks and the management response to those. A list of transactions tested. For any exceptions identified, the report should list the transaction details and the nature of the exception. If applicable, any good practices that was developed by the IP and could be shared with other IPs. An overall risk rating of the IPs internal controls and process to update the micro assessment data. E. Available Facilities and Right of Access The IPs will avail to the auditor all records in respect of the implemented activities under the respective AWPs. The records should include: The signed CPAPs. Signed AWPs, FACE Forms for all four quarters of 2012 and 2013, financial transaction records and Bank Statements kept at the IP's offices and those that are located at other offices. The auditor will have full and complete access at any time to all records and documents (including books of account, legal agreements, minutes of committee meetings, bank records, invoices and contracts, etc.) and all employees of the entity. The auditor also has a right of access to banks, consultants, contractors and other persons or firms engaged by the IP s management. F. Audit Timeframe It has been planned that the audit will commence by 1 April 2014 and the audit field work is scheduled to be completed within two months. The draft audit report should be completed by 31 July 2014 and the final reports of the financial audit of the IPs should be submitted to UNICEF by 31 August 2014 at the latest. 6

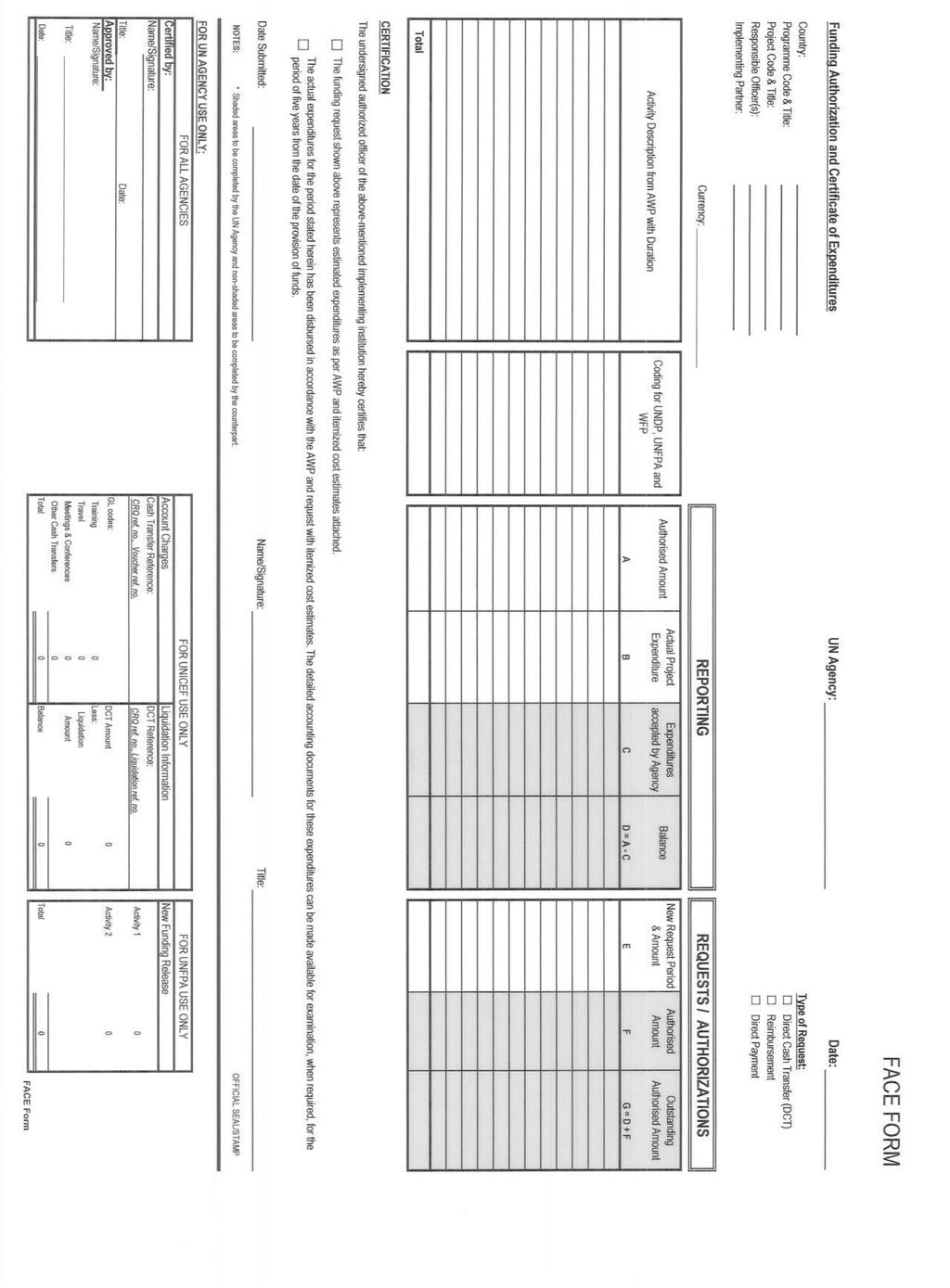

7 Annex 1: Description of FACE Form The financial report that should be audited is the duly completed and signed FACE (Funding Authorization and Certificate of Expenditures) Form. FACE is a report prepared by the Implementing Partners using Excel software. Description of the FACE Form FACE Form consists of the following areas as detailed below: 1. Reporting Area The FACE is a dynamic form that must balance and reconcile from one reporting period to the next. The first column on the new form, Column A, therefore repeats the last one, Column G, from the previously submitted and authorized FACE form. Note that Column C, D, F and G are shaded. They are blank when the FACE is submitted to UNICEF. They are filled out by UNICEF prior to the financial processing of the form. All non-shaded Columns are to be completed by the Implementing Partner. Column A Authorized Amount: Column A will be blank for the first request from an Implementing Partner. It should include the date of the most recent previous authorization. Column B Actual Expenditure: Column B reports the actual expenditures by the Implementing Partner for the period. The expenditures reported by the Implementing Partner are, at this point, still subject to review and approval by UNICEF. The designated official of the Implementing Partner is certifying that these expenditures are reported in accordance with the stipulation of the AWP (Annual Work Plan), CPAP (Country Programme Action Plan) and/or other related agreements with UNICEF. Column C Expenditures Accepted by UNICEF: Column C is used by UNICEF to review and approve, reject or request an amendment to expenditures reported by the Implementing Partner. If the amounts are accepted as reported, no further adjustments to this part of the FACE or communication with the Implementing Partner about these expenditure is required. However, if changes are made (e.g., to query or reject a reported expenditure), then the amount recorded by UNICEF in Column C will differ from that reported in Column B. In this case, the change needs to be communicated to the Implementing Partner. Column D Balance: Column D records the balance of funds authorized for use in the reporting period that remained unspent as of the date of the form. The term unspent can also reflect expenditures which are either known or ongoing as of the date of the FACE, but which cannot be certified by the Implementing Partner due to timing or internal reporting delays. The outstanding balance of funds authorized by activity can be carried forward, reprogrammed or refunded, according to UNICEF policy. 7

8 2. Requests / Authorizations Area Column E New Request Period & Amount: Column E determines the period of the new request, which is normally contiguous to the last reporting period. The Column contains the requests for the authorization to spend or receive funds, by activity and for that period. Each time a request for new or additional funds is submitted, it will be accompanied by an itemized list of expenditures in line with the AWP. This column can also reflect any balance for an activity in column D, which is requested for reprogramming. This will reduce the total amount of the new disbursement request accordingly. Column F Authorised Amount: Column F is used by UNICEF to establish the amounts of funds, by activity, to be disbursed for the new reporting period. This Column is filled in by UNICEF. It can be used to accept, reject or modify the amounts requested in Column E. Any credits for reprogramming will be reflected in this column for reconciliation of the amounts. Column G Outstanding Authorized Amount: Column G is the sum of Columns D and F, and indicates the total outstanding authorized amount. For subsequent period reporting, the amount of this column will be carried forward to the column A of the new FACE form 3. Certification Area The Certification Area is used by the designated official of the Implementing Partner to request funds and/or to certify expenditures. This area requires a date, the signature of the official and his/her title. Annex 3: Definition of Audit Opinions Unqualified (Clean) Opinion An unqualified opinion should be expressed when the auditor concludes that the financial statements give a true and fair view or are presented fairly, in all material respects, in accordance with the applicable financial reporting framework. Modified Unqualified or Emphasis of Matter paragraph In certain circumstances, an auditor s report may be modified by adding an emphasis of matter paragraph to highlight a matter affecting the financial statements which is included in a note to the financial statements that more extensively discusses the matter. The emphasis of matter paragraph would ordinarily refer to the fact that the auditor s opinion is not qualified in this respect, by adding a paragraph to highlight a material matter regarding an ongoing concern or problem or a significant uncertainty. An uncertainty is a matter whose outcome depends on future actions or events not under the direct control of the entity but that may affect the financial statements. 8

9 Qualified Opinion A qualified opinion should be expressed when the auditor concludes that an unqualified opinion cannot be expressed but that the effect of any disagreement with management, or limitation on scope is not so material and pervasive as to require an adverse opinion or a disclaimer of opinion. A qualified opinion should be expressed as being except for the effects of the matter to which the qualification relates. Disclaimer of opinion A disclaimer of opinion should be expressed when the possible effect of a limitation on scope is so material and pervasive that the auditor has not been able to obtain sufficient appropriate audit evidence and accordingly is unable to express an opinion on the financial statements. Adverse An adverse opinion should be expressed when the effect of a disagreement is so material and pervasive to the financial statements that the auditor concludes that a qualification of the report is not adequate to disclose the misleading or incomplete nature of the financial statements. 9

10 Annex 4: Categorization of Audit Findings by Risk Severity High Medium Low Action that is considered imperative to ensure that UNICEF is not exposed to high risks (i.e. failure to take action could result in major consequences and issues). Action that is considered necessary to avoid exposure to significant risks (i.e. failure to take action could result in significant consequences). Action that is considered desirable and should result in enhanced control or better value for money. 10

11 Annex 5: Classification of possible causes of Audit Findings Compliance Guidelines Guidance Human error Resources Failure to comply with prescribed UNICEF regulations, rules and procedures Absence of written procedures to guide staff in the performance of their functions Inadequate or lack of supervision by supervisors Mistakes committed by staff entrusted to perform assigned functions Lack of or inadequate resources (funds, skills, staff, etc.) to carry out an activity or function 11

12 12

TERMS OF REFERENCE FOR AUDITS OF NIM/NGO PROJECTS

United Nations Development Programme Office of Audit and Investigations Annex I TERMS OF REFERENCE FOR AUDITS OF NIM/NGO PROJECTS 2014 02 November 2014 TABLE OF CONTENTS Page INTRODUCTION... 3 A. Background...

United Nations Development Programme Office of Audit and Investigations Annex I TERMS OF REFERENCE FOR AUDITS OF NIM/NGO PROJECTS 2014 02 November 2014 TABLE OF CONTENTS Page INTRODUCTION... 3 A. Background...

TERMS OF REFERENCE (TOR) FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS

FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS") TERMS OF REFERENCE (TOR) FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS TABLE OF CONTENTS Introduction... 3 A. Background... 7 B. Project Management... 7 C. Consultations with concerned parties...

TERMS OF REFERENCE (TOR) FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS TABLE OF CONTENTS Introduction... 3 A. Background... 7 B. Project Management... 7 C. Consultations with concerned parties...

United Nations Development Programme Cambodia Office

REQUEST FOR PROPOSAL TO SELECT AUDIT FIRM FOR AUDIT OF NEX OR NGO PROJECTS United Nations Development Programme Cambodia Office NOTE: WHEN SUBMITTING YOUR BID DOCUMENTS, PLEASE CAREFULLY PLACE THE TECHNICAL

REQUEST FOR PROPOSAL TO SELECT AUDIT FIRM FOR AUDIT OF NEX OR NGO PROJECTS United Nations Development Programme Cambodia Office NOTE: WHEN SUBMITTING YOUR BID DOCUMENTS, PLEASE CAREFULLY PLACE THE TECHNICAL

External Audit. April 2012

External Audit April 2012 Audit Definition Ex post review of the books of account, financial statements, records of transactions & financial systems Examines the adequacy of accounting systems & procedures,

External Audit April 2012 Audit Definition Ex post review of the books of account, financial statements, records of transactions & financial systems Examines the adequacy of accounting systems & procedures,

THE GLOBAL FUND to Fight AIDS, Tuberculosis and Malaria

THE GLOBAL FUND to Fight AIDS, Tuberculosis and Malaria Guidelines for Annual Audits of Program Financial Statements Table of Contents 1. Introduction 2. Operational Policies and Practices 3. Follow-up

THE GLOBAL FUND to Fight AIDS, Tuberculosis and Malaria Guidelines for Annual Audits of Program Financial Statements Table of Contents 1. Introduction 2. Operational Policies and Practices 3. Follow-up

DESK REVIEW UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN

UNITED NATIONS DEVELOPMENT PROGRAMME DESK REVIEW OF UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN Report No. 1310 Issue Date: 9 October 2014 Table of

UNITED NATIONS DEVELOPMENT PROGRAMME DESK REVIEW OF UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN Report No. 1310 Issue Date: 9 October 2014 Table of

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) INTERNAL AUDIT REPORT. 19 October 2017

INTERNAL AUDIT REPORT. 19 October 2017") UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) INTERNAL AUDIT REPORT 19 October 2017 PROJECT NAME: GLOBAL FUND REGIONAL ARTEMISININ INITIATIVE (RAI) MYANMAR - PRINCIPAL RECIPIENT - UNOPS PROJECT NUMBER:

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) INTERNAL AUDIT REPORT 19 October 2017 PROJECT NAME: GLOBAL FUND REGIONAL ARTEMISININ INITIATIVE (RAI) MYANMAR - PRINCIPAL RECIPIENT - UNOPS PROJECT NUMBER:

AUDIT UNDP COUNTRY OFFICE AFGHANISTAN FINANCIAL MANAGEMENT. Report No Issue Date: 10 December 2013

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AFGHANISTAN FINANCIAL MANAGEMENT Report No. 1233 Issue Date: 10 December 2013 Table of Contents Executive Summary i I. Introduction

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AFGHANISTAN FINANCIAL MANAGEMENT Report No. 1233 Issue Date: 10 December 2013 Table of Contents Executive Summary i I. Introduction

UNICEF Spot Check Guidance

UNICEF Spot Check Guidance Document Number: FRG/GUIDANCE/2015/001 Issue Date: 30 June 2015 Issued By: Field Results Group UNICEF Spot Check Guidance FRG/GUIDANCE/2015/001 30 June 2015 Page 1 Contents SUMMARY...

UNICEF Spot Check Guidance Document Number: FRG/GUIDANCE/2015/001 Issue Date: 30 June 2015 Issued By: Field Results Group UNICEF Spot Check Guidance FRG/GUIDANCE/2015/001 30 June 2015 Page 1 Contents SUMMARY...

Internal Audit of the Lao People s Democratic Republic Country Office

Internal Audit of the Lao People s Democratic Republic Country Office March 2013 Office of Internal Audit and Investigations (OIAI) Report 2013/04 Audit of the Lao People s Democratic Republic Country

Internal Audit of the Lao People s Democratic Republic Country Office March 2013 Office of Internal Audit and Investigations (OIAI) Report 2013/04 Audit of the Lao People s Democratic Republic Country

AUDIT UNDP NEPAL. Comprehensive Disaster Risk Management Programme (Directly Implemented Project No )

") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP NEPAL Comprehensive Disaster Risk Management Programme (Directly Implemented Project No. 77652) Report No. 1200 Issue

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP NEPAL Comprehensive Disaster Risk Management Programme (Directly Implemented Project No. 77652) Report No. 1200 Issue

Control activities that are part of the process are detailed in the riskcontrol

Policy Title Previous title (if any) Cash Transfers to Implementing Partners N/A Policy objective Target audience Risk control matrix Checklist The policy and procedures outline the process for management

Policy Title Previous title (if any) Cash Transfers to Implementing Partners N/A Policy objective Target audience Risk control matrix Checklist The policy and procedures outline the process for management

Internal Audit of the Republic of Albania Country Office January Office of Internal Audit and Investigations (OIAI) Report 2017/24

Report 2017/24") Internal Audit of the Republic of Albania Country Office January 2018 Office of Internal Audit and Investigations (OIAI) Report 2017/24 Internal Audit of the Albania Country Office (2017/24) 2 Summary

Internal Audit of the Republic of Albania Country Office January 2018 Office of Internal Audit and Investigations (OIAI) Report 2017/24 Internal Audit of the Albania Country Office (2017/24) 2 Summary

AUDIT UNDP COUNTRY OFFICE BANGLADESH. Report No Issue Date: 28 May 2015

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN BANGLADESH Report No. 1429 Issue Date: 28 May 2015 Table of Contents Executive Summary i I. About the Office 1 II. Good practice 1 III.

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN BANGLADESH Report No. 1429 Issue Date: 28 May 2015 Table of Contents Executive Summary i I. About the Office 1 II. Good practice 1 III.

Audit communication and reporting

Audit communication and reporting Report of the Auditor-General to Parliament or the Provincial Legislature on the financial statements and performance information Content Report on the financial statements

Audit communication and reporting Report of the Auditor-General to Parliament or the Provincial Legislature on the financial statements and performance information Content Report on the financial statements

COMMISSION DELEGATED REGULATION (EU)

") L 148/54 20.5.2014 COMMISSION DELEGATED REGULATION (EU) No 532/2014 of 13 March 2014 supplementing Regulation (EU) No 223/2014 of the European Parliament and of the Council on the Fund for European Aid

L 148/54 20.5.2014 COMMISSION DELEGATED REGULATION (EU) No 532/2014 of 13 March 2014 supplementing Regulation (EU) No 223/2014 of the European Parliament and of the Council on the Fund for European Aid

Professional Bridging Examination. Paper III PBE Auditing and Information Systems

Professional Bridging Examination Pilot Examination Paper Paper III PBE Auditing and Information Systems Questions & Answers Booklet The suggested answers given in this booklet are purposely made to give

Professional Bridging Examination Pilot Examination Paper Paper III PBE Auditing and Information Systems Questions & Answers Booklet The suggested answers given in this booklet are purposely made to give

AUDIT UNDP AFGHANISTAN. Local Governance Project (Project No ) Report No Issue Date: 23 December 2016

Report No Issue Date: 23 December 2016") UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP AFGHANISTAN Local Governance Project (Project No. 90448) Report No. 1745 Issue Date: 23 December 2016 Table of Contents Executive Summary i I. About the

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP AFGHANISTAN Local Governance Project (Project No. 90448) Report No. 1745 Issue Date: 23 December 2016 Table of Contents Executive Summary i I. About the

Glossary of Terms. (From 2001 IFAC Handbook of Auditing and Ethics Pronouncements)

") Appendix 1 Glossary of Terms (From 2001 IFAC Handbook of Auditing and Ethics Pronouncements) Accounting estimate An accounting estimate is an approximation of the amount of an item in the absence of a

Appendix 1 Glossary of Terms (From 2001 IFAC Handbook of Auditing and Ethics Pronouncements) Accounting estimate An accounting estimate is an approximation of the amount of an item in the absence of a

AUDIT UNDP COUNTRY OFFICE UGANDA. Report No Issue Date: 22 August 2013

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN UGANDA Report No. 1155 Issue Date: 22 August 2013 Table of Contents Executive Summary i I. Introduction 1 II. About the Office 1 III.

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN UGANDA Report No. 1155 Issue Date: 22 August 2013 Table of Contents Executive Summary i I. Introduction 1 II. About the Office 1 III.

SRI LANKA AUDITING STANDARD 700 THE AUDITOR S REPORT ON FINANCIAL STATEMENTS CONTENTS

SRI LANKA AUDITING STANDARD 700 THE AUDITOR S REPORT ON FINANCIAL STATEMENTS (Effective for all the audits carried out on or after..) CONTENTS Paragraph Introduction 1-4 Basic Elements of the Auditor s

SRI LANKA AUDITING STANDARD 700 THE AUDITOR S REPORT ON FINANCIAL STATEMENTS (Effective for all the audits carried out on or after..) CONTENTS Paragraph Introduction 1-4 Basic Elements of the Auditor s

United Nations Development Group (UNDG)

") United Nations Development Group (UNDG) Proposed Revisions to the Harmonized Approach to Cash Transfers (HACT) Framework Audit & Assurance APPENDICES 17 September 2013 kpmg.com Contents Appendix 1 Listing

United Nations Development Group (UNDG) Proposed Revisions to the Harmonized Approach to Cash Transfers (HACT) Framework Audit & Assurance APPENDICES 17 September 2013 kpmg.com Contents Appendix 1 Listing

Guidance on a common methodology for the assessment of management and control systems in the Member States ( programming period)

") Final version of 12/09/2008 EUROPEAN COMMISSION DIRECTORATE-GENERAL MARITIME AFFAIRS AND FISHERIES EFFC/27/2008 Guidance on a common methodology for the assessment of management and control systems in

Final version of 12/09/2008 EUROPEAN COMMISSION DIRECTORATE-GENERAL MARITIME AFFAIRS AND FISHERIES EFFC/27/2008 Guidance on a common methodology for the assessment of management and control systems in

United Nations Development Programme Office of Audit and Investigations TERMS OF REFERENCE FOR AUDITS OF NGO AND NIM PROJECTS

United Nations Development Programme Office of Audit and Investigations TERMS OF REFERENCE FOR AUDITS OF NGO AND NIM PROJECTS TABLE OF CONTENTS Page REQUEST FOR QUOTATION (RFQ)... 4 TERMS OF REFERENCE...

United Nations Development Programme Office of Audit and Investigations TERMS OF REFERENCE FOR AUDITS OF NGO AND NIM PROJECTS TABLE OF CONTENTS Page REQUEST FOR QUOTATION (RFQ)... 4 TERMS OF REFERENCE...

Financial Instructions No 1 of 2017 Examination of Payment Vouchers Prior to Disbursement

Financial Instructions Examination of Payment Vouchers Prior to Disbursement Financial Instructions No 1 of 2017 Examination of Payment Vouchers Prior to Disbursement 1. The following financial instructions

Financial Instructions Examination of Payment Vouchers Prior to Disbursement Financial Instructions No 1 of 2017 Examination of Payment Vouchers Prior to Disbursement 1. The following financial instructions

Reporting by Auditors on Compliance with Financial Reporting Standards

STATEMENT OF AUDITING PRACTICE SAP 1014 Reporting by Auditors on Compliance with Financial Reporting Standards This Statement of Auditing Practice was approved by the Council of the Institute of Certified

STATEMENT OF AUDITING PRACTICE SAP 1014 Reporting by Auditors on Compliance with Financial Reporting Standards This Statement of Auditing Practice was approved by the Council of the Institute of Certified

UNICEF Moldova. Terms of Reference

UNICEF Moldova Terms of Reference Individual Consultancy on Public Finance for Development of the National Action Plan for Gradual Implementation of the Sanitary and Hygiene Norms for Preschools Duration

UNICEF Moldova Terms of Reference Individual Consultancy on Public Finance for Development of the National Action Plan for Gradual Implementation of the Sanitary and Hygiene Norms for Preschools Duration

AUDIT UNDP NIGERIA. DEMOCRATIC GOVERNANCE FOR DEVELOPMENT: DEEPENING DEMOCRACY IN NIGERIA (Directly Implemented Project No , Output No.

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP NIGERIA DEMOCRATIC GOVERNANCE FOR DEVELOPMENT: DEEPENING DEMOCRACY IN NIGERIA (Directly Implemented Project No. 56855,

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP NIGERIA DEMOCRATIC GOVERNANCE FOR DEVELOPMENT: DEEPENING DEMOCRACY IN NIGERIA (Directly Implemented Project No. 56855,

Decision on the method of exercising supervision of credit institutions and imposing supervisory measures. Article 1

Pursuant to Article 175, paragraph (3) of the Credit Institutions Act (Official Gazette 159/2013) and Article 43, paragraph (2) item (9) of the Act on the Croatian National Bank (Official Gazette 75/2008

Pursuant to Article 175, paragraph (3) of the Credit Institutions Act (Official Gazette 159/2013) and Article 43, paragraph (2) item (9) of the Act on the Croatian National Bank (Official Gazette 75/2008

AUDIT. UNDP Pakistan. Early Recovery Programme in Pakistan (Directly Implemented Project No ) Report No. 990 Issue Date: 19 June 2013

Report No. 990 Issue Date: 19 June 2013") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP Pakistan Early Recovery Programme in Pakistan (Directly Implemented Project No. 76295) Report No. 990 Issue Date: 19

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP Pakistan Early Recovery Programme in Pakistan (Directly Implemented Project No. 76295) Report No. 990 Issue Date: 19

Financial Policy. Management Committee means the Management Committee of the Council of the City of Windhoek.

Financial Policy Definitions In this policy, unless the context indicates otherwise: Council means the Municipal Council of the City of Windhoek. Management Committee means the Management Committee of

Financial Policy Definitions In this policy, unless the context indicates otherwise: Council means the Municipal Council of the City of Windhoek. Management Committee means the Management Committee of

COMMISSION DECISION. of ON THE MANAGEMENT AND CONTROL OF THE SCHENGEN FACILITY IN CROATIA. (only the English text is authentic)

") EUROPEAN COMMISSION Brussels, 22.4.2013 C(2013) 2159 final COMMISSION DECISION of 22.4.2013 ON THE MANAGEMENT AND CONTROL OF THE SCHENGEN FACILITY IN CROATIA (only the English text is authentic) EN EN

EUROPEAN COMMISSION Brussels, 22.4.2013 C(2013) 2159 final COMMISSION DECISION of 22.4.2013 ON THE MANAGEMENT AND CONTROL OF THE SCHENGEN FACILITY IN CROATIA (only the English text is authentic) EN EN

2 SCOPE OF WORK, RESPONSIBILITIES AND DESCRIPTION OF THE PROPOSED ANALYTICAL WORK

UNITED NATIONS COUNTRY TEAM in TURKEY INDIVIDUAL CONSULTANT PROCUREMENT NOTICE 09.09.2016 Country Description of the Assignment Contracting Office Type of Contract Period of Assignment/Services Turkey

UNITED NATIONS COUNTRY TEAM in TURKEY INDIVIDUAL CONSULTANT PROCUREMENT NOTICE 09.09.2016 Country Description of the Assignment Contracting Office Type of Contract Period of Assignment/Services Turkey

FLC Guidance. Page 1. Version. September *Disclaimer: This is a living document and further content will be developed at a later stage.

FLC Guidance Version September 2017 *Disclaimer: This is a living document and further content will be developed at a later stage. Page 1 Table of Contents... 1 CHAPTER 1 General principles... 3 1.1 Introduction...

FLC Guidance Version September 2017 *Disclaimer: This is a living document and further content will be developed at a later stage. Page 1 Table of Contents... 1 CHAPTER 1 General principles... 3 1.1 Introduction...

Regulation on the implementation of the European Economic Area (EEA) Financial Mechanism

Financial Mechanism") the European Economic Area (EEA) Financial Mechanism 2014-2021 Adopted by the EEA Financial Mechanism Committee pursuant to Article 10.5 of Protocol 38c to the EEA Agreement on 8 September 2016 and confirmed

the European Economic Area (EEA) Financial Mechanism 2014-2021 Adopted by the EEA Financial Mechanism Committee pursuant to Article 10.5 of Protocol 38c to the EEA Agreement on 8 September 2016 and confirmed

REQUIRED DOCUMENT FROM HIRING UNIT

Terms of reference GENERAL INFORMATION Title: Finance Management Technical Assistance Consultant for the Global Fund Principal Recipient Aisyiyah (National Consultant) Project Name: Management and Technical

Terms of reference GENERAL INFORMATION Title: Finance Management Technical Assistance Consultant for the Global Fund Principal Recipient Aisyiyah (National Consultant) Project Name: Management and Technical

REPORT 2015/079 INTERNAL AUDIT DIVISION. Audit of United Nations Office on Drugs and Crime operations in Peru

INTERNAL AUDIT DIVISION REPORT 2015/079 Audit of United Nations Office on Drugs and Crime operations in Peru Overall results relating to the management of operations in Peru were initially assessed as

INTERNAL AUDIT DIVISION REPORT 2015/079 Audit of United Nations Office on Drugs and Crime operations in Peru Overall results relating to the management of operations in Peru were initially assessed as

ANNEX A - I. Note: it is important that each tenderer has read the Working Practice and its annexes very carefully.

ANNEX A - I Note: it is important that each tenderer has read the Working Practice and its annexes very carefully. WORKING PRACTICE 1.GENERAL INFORMATION 1.1.THE AUDIT CO-ORDINATOR 1.1.1.The Audit Co-ordinator

ANNEX A - I Note: it is important that each tenderer has read the Working Practice and its annexes very carefully. WORKING PRACTICE 1.GENERAL INFORMATION 1.1.THE AUDIT CO-ORDINATOR 1.1.1.The Audit Co-ordinator

The Auditor s Report on Financial Statements

Issued December 2007 International Standard on Auditing The Auditor s Report on Financial Statements The Malaysian Institute Of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia)

Issued December 2007 International Standard on Auditing The Auditor s Report on Financial Statements The Malaysian Institute Of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia)

Guidance for Member States on Audit of Accounts

EGESIF_15_0016-02 final 29/01/2015 EUROPEAN COMMISSION European Structural and Investment Funds Guidance for Member States on Audit of Accounts DISCLAIMER: This is a document prepared by the Commission

EGESIF_15_0016-02 final 29/01/2015 EUROPEAN COMMISSION European Structural and Investment Funds Guidance for Member States on Audit of Accounts DISCLAIMER: This is a document prepared by the Commission

Project Document Format for non-cpap Countries or Projects outside a CPAP

Project Document Format for noncpap Countries or Projects outside a CPAP United Nations Development Programme Country: _ Project Document Project Title UNDAF Outcome(s): Expected CP Outcome(s): (Those

Project Document Format for noncpap Countries or Projects outside a CPAP United Nations Development Programme Country: _ Project Document Project Title UNDAF Outcome(s): Expected CP Outcome(s): (Those

AUDIT UNDP COUNTRY OFFICE SOMALIA. Report No Issue Date: 20 June 2014

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN SOMALIA Report No. 1299 Issue Date: 20 June 2014 Table of Contents Executive Summary ii I. About the Office 1 II. Audit results 1 A.

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN SOMALIA Report No. 1299 Issue Date: 20 June 2014 Table of Contents Executive Summary ii I. About the Office 1 II. Audit results 1 A.

GUIDANCE DOCUMENT ON THE FUNCTIONS OF THE CERTIFYING AUTHORITY. for the programming period

Final version of 25/07/2008 COCOF 08/0014/02-EN GUIDANCE DOCUMENT ON THE FUNCTIONS OF THE CERTIFYING AUTHORITY for the 2007 2013 programming period Table of contents 1. Introduction... 3 2. Main functions

Final version of 25/07/2008 COCOF 08/0014/02-EN GUIDANCE DOCUMENT ON THE FUNCTIONS OF THE CERTIFYING AUTHORITY for the 2007 2013 programming period Table of contents 1. Introduction... 3 2. Main functions

COMMISSION DELEGATED REGULATION (EU) /... of

/... of") EUROPEAN COMMISSION Brussels, 16.5.2018 C(2018) 2857 final COMMISSION DELEGATED REGULATION (EU) /... of 16.5.2018 amending Commission Delegated Regulation (EU) No 1042/2014 of 25 July 2014 supplementing

EUROPEAN COMMISSION Brussels, 16.5.2018 C(2018) 2857 final COMMISSION DELEGATED REGULATION (EU) /... of 16.5.2018 amending Commission Delegated Regulation (EU) No 1042/2014 of 25 July 2014 supplementing

Guide to Financial Issues relating to ICT PSP Grant Agreements

DG COMMUNICATIONS NETWORKS, CONTENT AND TECHNOLOGY ICT Policy Support Programme Competitiveness and Innovation Framework Programme Guide to Financial Issues relating to ICT PSP Grant Agreements Version

DG COMMUNICATIONS NETWORKS, CONTENT AND TECHNOLOGY ICT Policy Support Programme Competitiveness and Innovation Framework Programme Guide to Financial Issues relating to ICT PSP Grant Agreements Version

Document No: AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF MUNICIPALITY OF KAMENICA FOR THE YEAR ENDED 31 DECEMBER 2017

Document No: 22.29.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF MUNICIPALITY OF KAMENICA FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, May 2018 The National Audit Office of the Republic

Document No: 22.29.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF MUNICIPALITY OF KAMENICA FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, May 2018 The National Audit Office of the Republic

26 PTA Audit. Overview. The Purpose of an Audit. Compiled Financial Statements

PTA Audit Overview Auditing involves examining financial records and transactions to ensure that receipts have been properly accounted for and expenditures have been properly authorized and recorded in

PTA Audit Overview Auditing involves examining financial records and transactions to ensure that receipts have been properly accounted for and expenditures have been properly authorized and recorded in

AUDIT CERTIFICATE WORKING NOTES 6 TH FRAMEWORK PROGRAMME

AUDIT CERTIFICATE WORKING NOTES 6 TH FRAMEWORK PROGRAMME WORKING NOTES FOR CONTRACTORS AND CERTIFYING ENTITIES MATERIALS PREPARED BY INTERDEPARTMENTAL AUDIT CERTIFICATE WORKING GROUP VERSION 1 APPROVED

AUDIT CERTIFICATE WORKING NOTES 6 TH FRAMEWORK PROGRAMME WORKING NOTES FOR CONTRACTORS AND CERTIFYING ENTITIES MATERIALS PREPARED BY INTERDEPARTMENTAL AUDIT CERTIFICATE WORKING GROUP VERSION 1 APPROVED

IAASB Main Agenda (May 2006) Page Agenda Item PROPOSED CONFORMING AMENDMENTS

Page Agenda Item PROPOSED CONFORMING AMENDMENTS") IAASB Main Agenda (May 2006) Page 2006 957 Agenda Item 7-E PROPOSED CONFORMING AMENDMENTS [Note: Only further changes to the conforming amendments previously exposed, or new conforming amendments, are

IAASB Main Agenda (May 2006) Page 2006 957 Agenda Item 7-E PROPOSED CONFORMING AMENDMENTS [Note: Only further changes to the conforming amendments previously exposed, or new conforming amendments, are

AUDIT OF THE FUND ACCOUNTABILITY STATEMENT OF USAID RESOURCES MANAGED BY MERCY CORPS AND IMPLEMENTED BY PUBLIC AID ORGANIZATION ( PAO ) UNDER

UNDER") AUDIT OF THE FUND ACCOUNTABILITY STATEMENT OF USAID RESOURCES MANAGED BY MERCY CORPS AND IMPLEMENTED BY PUBLIC AID ORGANIZATION ( PAO ) UNDER COOPERATIVE AGREEMENT NUMBER AID-267-A-00-12-00001, CFDA #

AUDIT OF THE FUND ACCOUNTABILITY STATEMENT OF USAID RESOURCES MANAGED BY MERCY CORPS AND IMPLEMENTED BY PUBLIC AID ORGANIZATION ( PAO ) UNDER COOPERATIVE AGREEMENT NUMBER AID-267-A-00-12-00001, CFDA #

STATEMENT OF AUDITING STANDARDS 600 AUDITORS' REPORTS ON FINANCIAL STATEMENTS

STATEMENT OF AUDITING STANDARDS 600 AUDITORS' REPORTS ON FINANCIAL STATEMENTS (Issued August 1994; revised April 2000, June 2001; February 2004, September 2004 (name change), December 2005 and October

STATEMENT OF AUDITING STANDARDS 600 AUDITORS' REPORTS ON FINANCIAL STATEMENTS (Issued August 1994; revised April 2000, June 2001; February 2004, September 2004 (name change), December 2005 and October

OMB CIRCULAR A-133 REPORT ON FEDERAL FINANCIAL ASSISTANCE PROGRAMS

OMB CIRCULAR A-133 REPORT ON FEDERAL FINANCIAL ASSISTANCE PROGRAMS Virgin Islands Port Authority (a component unit of the Government of the United States Virgin Islands) Report of Independent Auditors

OMB CIRCULAR A-133 REPORT ON FEDERAL FINANCIAL ASSISTANCE PROGRAMS Virgin Islands Port Authority (a component unit of the Government of the United States Virgin Islands) Report of Independent Auditors

AUDIT CERTIFICATE GUIDANCE NOTES 6 TH FRAMEWORK PROGRAMME

AUDIT CERTIFICATE GUIDANCE NOTES 6 TH FRAMEWORK PROGRAMME WORKING NOTES FOR CONTRACTORS AND CERTIFYING ENTITIES MATERIALS PREPARED BY INTERDEPARTMENTAL AUDIT CERTIFICATE WORKING GROUP/ COORDINATION GROUP

AUDIT CERTIFICATE GUIDANCE NOTES 6 TH FRAMEWORK PROGRAMME WORKING NOTES FOR CONTRACTORS AND CERTIFYING ENTITIES MATERIALS PREPARED BY INTERDEPARTMENTAL AUDIT CERTIFICATE WORKING GROUP/ COORDINATION GROUP

Internal Audit Report

Internal Audit Report MENORAH HIGH SCHOOL FOR GIRLS 13 July 2017 To: Copied to: Chair of Governors Headteacher Education and Skills Director Commissioning Director (Children and Young People) School Finance

Internal Audit Report MENORAH HIGH SCHOOL FOR GIRLS 13 July 2017 To: Copied to: Chair of Governors Headteacher Education and Skills Director Commissioning Director (Children and Young People) School Finance

Guidance for Member States on Audit of Accounts

EGESIF_15_0016-04 03/12/2018 EUROPEAN COMMISSION European Structural and Investment Funds Guidance for Member States on Audit of Accounts Revision 2018 DISCLAIMER: This is a document prepared by the Commission

EGESIF_15_0016-04 03/12/2018 EUROPEAN COMMISSION European Structural and Investment Funds Guidance for Member States on Audit of Accounts Revision 2018 DISCLAIMER: This is a document prepared by the Commission

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/078

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/078 Audit of the United Nations Environment Programme s Secretariat of the Convention on Biological Diversity Overall results relating to the provision of efficient

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/078 Audit of the United Nations Environment Programme s Secretariat of the Convention on Biological Diversity Overall results relating to the provision of efficient

FAIRFIELD AREA SCHOOL DISTRICT

FAIRFIELD AREA SCHOOL DISTRICT Request for Proposal for Audit Services MARCH 11, 2014 Invitation for Proposal The Fairfield Area School District is soliciting proposals from independent certified public

FAIRFIELD AREA SCHOOL DISTRICT Request for Proposal for Audit Services MARCH 11, 2014 Invitation for Proposal The Fairfield Area School District is soliciting proposals from independent certified public

IFAD Handbook for Financial Reporting and Auditing of IFAD- Financed Projects

- 2018 IFAD Handbook for Financial Reporting and Auditing of IFAD- Financed Projects 1 The IFAD Handbook for Financial Reporting and Auditing for IFAD-Financed Projects is available online for public use

- 2018 IFAD Handbook for Financial Reporting and Auditing of IFAD- Financed Projects 1 The IFAD Handbook for Financial Reporting and Auditing for IFAD-Financed Projects is available online for public use

Guidance document on. management verifications to be carried out by Member States on operations co-financed by

Final version of 05/06/2008 COCOF 08/0020/04-EN Guidance document on management verifications to be carried out by Member States on operations co-financed by the Structural Funds and the Cohesion Fund

Final version of 05/06/2008 COCOF 08/0020/04-EN Guidance document on management verifications to be carried out by Member States on operations co-financed by the Structural Funds and the Cohesion Fund

STATEMENT OF WORK FOR RECIPIENT CONTRACTED AUDIT OF USAID RESOURCES MANAGED BY THE WEST AFRICAN HEALTH ORGANIZATION (WAHO)

") STATEMENT OF WORK FOR RECIPIENT CONTRACTED AUDIT OF USAID RESOURCES MANAGED BY THE WEST AFRICAN HEALTH ORGANIZATION (WAHO) AUDIT OF USAID RESOURCES MANAGED BY WEST AFRICAN HEALTH ORGANIZATION UNDER THE

STATEMENT OF WORK FOR RECIPIENT CONTRACTED AUDIT OF USAID RESOURCES MANAGED BY THE WEST AFRICAN HEALTH ORGANIZATION (WAHO) AUDIT OF USAID RESOURCES MANAGED BY WEST AFRICAN HEALTH ORGANIZATION UNDER THE

UNDP Pakistan Monitoring Policy STRATEGIC MANAGEMENT UNIT UNITED NATIONS DEVELOPMENT PROGRAMME, PAKISTAN

UNDP Pakistan Monitoring Policy STRATEGIC MANAGEMENT UNIT UNITED NATIONS DEVELOPMENT PROGRAMME, PAKISTAN Approved Version April 2014 Contents Contents... 2 1. Key Elements of Results Based Management in

UNDP Pakistan Monitoring Policy STRATEGIC MANAGEMENT UNIT UNITED NATIONS DEVELOPMENT PROGRAMME, PAKISTAN Approved Version April 2014 Contents Contents... 2 1. Key Elements of Results Based Management in

Table of contents. Introduction Regulatory requirements... 3

COCOF 08/0020/02-EN DRAFT Guidance document on management verifications to be carried out by Member States on projects co-financed by the Structural Funds and the Cohesion Fund for the 2007 2013 programming

COCOF 08/0020/02-EN DRAFT Guidance document on management verifications to be carried out by Member States on projects co-financed by the Structural Funds and the Cohesion Fund for the 2007 2013 programming

United Nations Development Programme

United Nations Development Programme Title Project Document Template Document Language English (original), French - Spanish Responsible Unit Bureau for Development Policy/Capacity Development Group Approver

United Nations Development Programme Title Project Document Template Document Language English (original), French - Spanish Responsible Unit Bureau for Development Policy/Capacity Development Group Approver

AUSTIN INDEPENDENT SCHOOL DISTRICT

PURCHASING CARD GENERAL: The purchasing card ("p-card") program was implemented several years ago to establish a more efficient, cost-effective method of purchasing and paying for small dollar transactions

PURCHASING CARD GENERAL: The purchasing card ("p-card") program was implemented several years ago to establish a more efficient, cost-effective method of purchasing and paying for small dollar transactions

Department of Enterprise, Trade & Employment

Department of Enterprise, Trade & Employment Circular No. ESF/PA/1-2001 31 July 2001 FINANCIAL MANAGEMENT AND CONTROL PROCEDURES FOR THE EUROPEAN SOCIAL FUND (ESF) 2000-2006 1. Background The purpose of

Department of Enterprise, Trade & Employment Circular No. ESF/PA/1-2001 31 July 2001 FINANCIAL MANAGEMENT AND CONTROL PROCEDURES FOR THE EUROPEAN SOCIAL FUND (ESF) 2000-2006 1. Background The purpose of

St Minver Lowlands Parish Council

INDEX to FINANCIAL REGULATIONS Section No Heading Sub-Heading 1 General 2 Accounting and Audit Internal and External 3 Annual Estimates Budget and Forward Planning 4 Budgetary Control Incl. Authority to

INDEX to FINANCIAL REGULATIONS Section No Heading Sub-Heading 1 General 2 Accounting and Audit Internal and External 3 Annual Estimates Budget and Forward Planning 4 Budgetary Control Incl. Authority to

Report on the annual accounts of the European Schools for the financial year together with the Schools replies

Report on the annual accounts of the European Schools for the financial year 2016 together with the Schools replies 12, rue Alcide De Gasperi - L - 1615 Luxembourg T (+352) 4398 1 E eca-info@eca.europa.eu

Report on the annual accounts of the European Schools for the financial year 2016 together with the Schools replies 12, rue Alcide De Gasperi - L - 1615 Luxembourg T (+352) 4398 1 E eca-info@eca.europa.eu

CENTRAL FINANCE AND CONTRACTS UNIT (CFCU) POLAND MEMORANDUM OF UNDERSTANDING. Article 1 - Explanatory Statement

POLAND MEMORANDUM OF UNDERSTANDING. Article 1 - Explanatory Statement") CENTRAL FINANCE AND CONTRACTS UNIT (CFCU) POLAND MEMORANDUM OF UNDERSTANDING Article 1 - Explanatory Statement The Establishment of a Central Finance and Contracts Unit (CFCU) is to be seen against the

CENTRAL FINANCE AND CONTRACTS UNIT (CFCU) POLAND MEMORANDUM OF UNDERSTANDING Article 1 - Explanatory Statement The Establishment of a Central Finance and Contracts Unit (CFCU) is to be seen against the

AUDIT UNDP BANGLADESH. Comprehensive Disaster Management Programme Phase II (Project No , Output Nos )

") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP BANGLADESH Comprehensive Disaster Management Programme Phase II (Project No. 58919, Output Nos. 73416) Report No. 1472

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP BANGLADESH Comprehensive Disaster Management Programme Phase II (Project No. 58919, Output Nos. 73416) Report No. 1472

RS Official Gazette, Nos 55/2015, 82/2015, 29/2018 and 15/2019

RS Official Gazette, Nos 55/2015, 82/2015, 29/2018 and 15/2019 Pursuant to Article 80, paragraphs 3 and 10, Article 81, paragraph 5, Article 82, paragraph 5, Article 104, paragraph 5, Article 119, paragraph

RS Official Gazette, Nos 55/2015, 82/2015, 29/2018 and 15/2019 Pursuant to Article 80, paragraphs 3 and 10, Article 81, paragraph 5, Article 82, paragraph 5, Article 104, paragraph 5, Article 119, paragraph

INTERNAL AUDIT DIVISION REPORT 2017/126. Audit of trust fund activities in the African Union-United Nations Hybrid Operation in Darfur

INTERNAL AUDIT DIVISION REPORT 2017/126 Audit of trust fund activities in the African Union-United Nations Hybrid Operation in Darfur The Mission needed to enhance its supervision of project site inspections

INTERNAL AUDIT DIVISION REPORT 2017/126 Audit of trust fund activities in the African Union-United Nations Hybrid Operation in Darfur The Mission needed to enhance its supervision of project site inspections

European GNSS Supervisory Authority

GSA-AB-06-10-07-04 European GNSS Supervisory Authority 7 th meeting of the Administrative Board Brussels, 27 October 2006 Regulation of the European GNSS Supervisory Authority laying down detailed rules

GSA-AB-06-10-07-04 European GNSS Supervisory Authority 7 th meeting of the Administrative Board Brussels, 27 October 2006 Regulation of the European GNSS Supervisory Authority laying down detailed rules

Internal Audit of the WASH programme of the Kenya Country Office

Internal Audit of the WASH programme of the Kenya Country Office February 2015 Office of Internal Audit and Investigations (OIAI) Report 2015/03 Internal Audit of the WASH programme of the Kenya Country

Internal Audit of the WASH programme of the Kenya Country Office February 2015 Office of Internal Audit and Investigations (OIAI) Report 2015/03 Internal Audit of the WASH programme of the Kenya Country

Fiscal Policies and Procedures for County Councils. Responsibilities

Fiscal Policies and Procedures for County Councils Fiscal management policies established for county outreach and extension councils are based on the Missouri Revised Statutes, University of Missouri policies

Fiscal Policies and Procedures for County Councils Fiscal management policies established for county outreach and extension councils are based on the Missouri Revised Statutes, University of Missouri policies

Audit Report Internal Financial Controls. GF-OIG March 2015 Geneva, Switzerland

Audit Report Internal Financial Controls GF-OIG-15-005 Table of Contents I. Background... 2 II. Scope and Rating... 3 III. Executive Summary... 4 IV. Findings and agreed actions... 6 V. Table of Agreed

Audit Report Internal Financial Controls GF-OIG-15-005 Table of Contents I. Background... 2 II. Scope and Rating... 3 III. Executive Summary... 4 IV. Findings and agreed actions... 6 V. Table of Agreed

BURSA MALAYSIA SECURITIES BERHAD

BURSA MALAYSIA SECURITIES BERHAD PRACTICE NOTE 17 CRITERIA AND OBLIGATIONS OF PN17 ISSUERS Details Cross References Effective date: 3 January 2005 Paragraphs 8.03A, 8.04, 16.02 and 16.11 Revision date:

BURSA MALAYSIA SECURITIES BERHAD PRACTICE NOTE 17 CRITERIA AND OBLIGATIONS OF PN17 ISSUERS Details Cross References Effective date: 3 January 2005 Paragraphs 8.03A, 8.04, 16.02 and 16.11 Revision date:

AUDIT OF EXTERNAL OPERATIONS

EUROPEAN COMMISSION Directorate-General for Development and Cooperation EuropeAid Resources in Headquarters and in Delegations Audit and Control AUDIT OF EXTERNAL OPERATIONS PILLAR ASSESSMENTS CONTRACTED

EUROPEAN COMMISSION Directorate-General for Development and Cooperation EuropeAid Resources in Headquarters and in Delegations Audit and Control AUDIT OF EXTERNAL OPERATIONS PILLAR ASSESSMENTS CONTRACTED

5.6 Annual Report. Compliance Checklist for Annual Report November Name of Issuer: Name of Submitter(s): Name of Submitter(s) Organisation:

: Name of Submitter(s) Organisation:") Compliance Checklist for Annual Report Name of Issuer: Name of Submitter(s): Name of Submitter(s) Organisation: Mailing Address of Submitter(s): Contact Number(s) of Submitter(s): Email(s) of Submitter(s):

Compliance Checklist for Annual Report Name of Issuer: Name of Submitter(s): Name of Submitter(s) Organisation: Mailing Address of Submitter(s): Contact Number(s) of Submitter(s): Email(s) of Submitter(s):

Council, 4 December 2014 Proposed changes to Financial Regulations and Scheme of Delegation

Council, 4 December 2014 Proposed changes to Financial Regulations and Scheme of Delegation Executive summary and recommendations Introduction The finance systems upgrade project together with forthcoming

Council, 4 December 2014 Proposed changes to Financial Regulations and Scheme of Delegation Executive summary and recommendations Introduction The finance systems upgrade project together with forthcoming

LEKWA-TEEMANE LOCAL MUNICIPALITY TERMS OF REFERENCE OVERSIGHT COMMITTEE

LEKWA-TEEMANE LOCAL MUNICIPALITY TERMS OF REFERENCE OVERSIGHT COMMITTEE To be read in conjunction with National Treasury MFMA Circular 32 The Oversight Report CONTENTS 1. INTRODUCTION 3 2. BACKGROUND 3

LEKWA-TEEMANE LOCAL MUNICIPALITY TERMS OF REFERENCE OVERSIGHT COMMITTEE To be read in conjunction with National Treasury MFMA Circular 32 The Oversight Report CONTENTS 1. INTRODUCTION 3 2. BACKGROUND 3

UNDG Fiduciary Management Oversight Group (FMOG) Terms of Reference

Terms of Reference") UNDG Fiduciary Management Oversight Group (FMOG) Terms of Reference 5 December 2014 I. Institutional context In 2007, the UN Development Group (UNDG), recognizing the growing importance of Multi- Donor

UNDG Fiduciary Management Oversight Group (FMOG) Terms of Reference 5 December 2014 I. Institutional context In 2007, the UN Development Group (UNDG), recognizing the growing importance of Multi- Donor

Revised 1 Guidance Note on Financial Engineering Instruments under Article 44 of Council Regulation (EC) No 1083/2006

No 1083/2006") REVISED VERSION 08/02/2012 COCOF_10-0014-05-EN EUROPEAN COMMISSION DIRECTORATE-GENERAL REGIONAL POLICY Revised 1 Guidance Note on Financial Engineering Instruments under Article 44 of Council Regulation

REVISED VERSION 08/02/2012 COCOF_10-0014-05-EN EUROPEAN COMMISSION DIRECTORATE-GENERAL REGIONAL POLICY Revised 1 Guidance Note on Financial Engineering Instruments under Article 44 of Council Regulation

530: Accounts Payable Policy

1.0 Purpose. 530: Accounts Payable Policy 1.1. The purpose of Accounts Payable is to ensure that all Tukwila Pool Metropolitan Park District (District) funds are disbursed and recorded in accordance with

1.0 Purpose. 530: Accounts Payable Policy 1.1. The purpose of Accounts Payable is to ensure that all Tukwila Pool Metropolitan Park District (District) funds are disbursed and recorded in accordance with

Mango s Health Check. How healthy is financial management in your not-for-profit organisation?

How healthy is financial management in your not-for-profit organisation? Version 3 2009 Mango 2nd Floor East, Chester House, George Street, Oxford OX1 2AU Phone +44 (0)1865 423818 Fax +44 (0)1865 423560

How healthy is financial management in your not-for-profit organisation? Version 3 2009 Mango 2nd Floor East, Chester House, George Street, Oxford OX1 2AU Phone +44 (0)1865 423818 Fax +44 (0)1865 423560

EXCERPT FROM THE AUDIT REPORT ON THE GENERAL SECRETARIAT OF THE GOVERNMENT

EXCERPT FROM THE AUDIT REPORT ON THE GENERAL SECRETARIAT OF THE GOVERNMENT Type of audit: Audited entity: Subject of audit: Audit duration: Auditing Board members: Financial audit and regularity audit

EXCERPT FROM THE AUDIT REPORT ON THE GENERAL SECRETARIAT OF THE GOVERNMENT Type of audit: Audited entity: Subject of audit: Audit duration: Auditing Board members: Financial audit and regularity audit

1 P a g e LAW ON ACCOUNTING. ("Off. Herald of RS", No. 62/2013)

") LAW ON ACCOUNTING ("Off. Herald of RS", No. 62/2013) I GENERAL PROVISIONS Scope of Application Article 1 This law shall regulate the subjects of application of this law, the classification of legal persons,

LAW ON ACCOUNTING ("Off. Herald of RS", No. 62/2013) I GENERAL PROVISIONS Scope of Application Article 1 This law shall regulate the subjects of application of this law, the classification of legal persons,

Progress report on implementation of the recommendations of the Board of Auditors on the UNICEF accounts for the biennium

Distr.: Limited 12 July 2011 Original: English For information United Nations Children s Fund Executive Board Second regular session 2011 12-15 September 2011 Progress report on implementation of the recommendations

Distr.: Limited 12 July 2011 Original: English For information United Nations Children s Fund Executive Board Second regular session 2011 12-15 September 2011 Progress report on implementation of the recommendations

IFAD Handbook for Financial Reporting and Auditing of IFAD-financed Projects

IFAD Handbook for Financial Reporting and Auditing of IFAD-financed Projects The IFAD Handbook for Financial Reporting and Auditing of is available online for public use and dissemination. It is primarily

IFAD Handbook for Financial Reporting and Auditing of IFAD-financed Projects The IFAD Handbook for Financial Reporting and Auditing of is available online for public use and dissemination. It is primarily

1. The auditing is to be conducted by a chartered or registered accountant appointed by the competent body of the organisation.

Updated May 2018 DPOD Administrative Guidelines Audit Instructions concerning the performance of audits in connection with the administration of grant funds from mini-programmes applicable to single projects

Updated May 2018 DPOD Administrative Guidelines Audit Instructions concerning the performance of audits in connection with the administration of grant funds from mini-programmes applicable to single projects

United Nations Development Programme

ANNEX 3: CONTRACTOR S AUDIT TEAM Name of Staff Bethlehem office Ms. Tania Farrage Mr. Rabee Farrage Ms. Nibal Zugier Ms. Asmahan Ebiat Mr. Waleed Nabhan Ramallah office Mr. Rami Abu Hadid Mr. Elias Amar

ANNEX 3: CONTRACTOR S AUDIT TEAM Name of Staff Bethlehem office Ms. Tania Farrage Mr. Rabee Farrage Ms. Nibal Zugier Ms. Asmahan Ebiat Mr. Waleed Nabhan Ramallah office Mr. Rami Abu Hadid Mr. Elias Amar

INTERNATIONAL AUDITING PRACTICE STATEMENT 1014 REPORTING BY AUDITORS ON COMPLIANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS CONTENTS

INTERNATIONAL PRACTICE STATEMENT 1014 REPORTING BY AUDITORS ON COMPLIANCE WITH (This Statement is effective) CONTENTS Paragraph Introduction... 1 Financial Statements Prepared Solely in Accordance with

INTERNATIONAL PRACTICE STATEMENT 1014 REPORTING BY AUDITORS ON COMPLIANCE WITH (This Statement is effective) CONTENTS Paragraph Introduction... 1 Financial Statements Prepared Solely in Accordance with

PART 2.5 DEPARTMENT OF FISHERIES AND AQUACULTURE FISHERIES TECHNOLOGY AND NEW OPPORTUNITIES PROGRAM

PART 2.5 DEPARTMENT OF FISHERIES AND AQUACULTURE FISHERIES TECHNOLOGY AND NEW OPPORTUNITIES PROGRAM Executive Summary The Department of Fisheries and Aquaculture (the Department) administers the Fisheries

PART 2.5 DEPARTMENT OF FISHERIES AND AQUACULTURE FISHERIES TECHNOLOGY AND NEW OPPORTUNITIES PROGRAM Executive Summary The Department of Fisheries and Aquaculture (the Department) administers the Fisheries

MODEL FOR THE CERTIFICATE ON THE FINANCIAL STATEMENTS

Grant Agreement number: [insert number] [insert acronym] [insert call identifier of the master call] H2020 Model Grant Agreement: Multi-beneficiary General MGA: December 2013 ANNEX 5 MODEL FOR THE CERTIFICATE

Grant Agreement number: [insert number] [insert acronym] [insert call identifier of the master call] H2020 Model Grant Agreement: Multi-beneficiary General MGA: December 2013 ANNEX 5 MODEL FOR THE CERTIFICATE

OIC/GA-IOFS/2016/FIN.REG FINANCIAL REGULATIONS OF THE ISLAMIC ORGANIZATION FOR FOOD SECURITY

OIC/GA-IOFS/2016/FIN.REG FINANCIAL REGULATIONS OF THE ISLAMIC ORGANIZATION FOR FOOD SECURITY FINANCIAL REGULATIONS OF THE ISLAMIC ORGANISATION FOR FOOD SECURITY C O N T E N T S PAGE CHAPTER: I SCOPE AND

OIC/GA-IOFS/2016/FIN.REG FINANCIAL REGULATIONS OF THE ISLAMIC ORGANIZATION FOR FOOD SECURITY FINANCIAL REGULATIONS OF THE ISLAMIC ORGANISATION FOR FOOD SECURITY C O N T E N T S PAGE CHAPTER: I SCOPE AND

Answer to MTP_ Intermediate_Syllabus2016_June2018_Set1 Paper 12- Company Accounts & Audit

Paper 12- Company Accounts & Audit DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 12- Company Accounts & Audit Full Marks: 100 Time allowed: 3

Paper 12- Company Accounts & Audit DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 12- Company Accounts & Audit Full Marks: 100 Time allowed: 3

MODULE 5 AUDIT EXECUTION: FINANCIAL STATEMENT ITEMS SUBSTANTIVE PROCEDURES

MODULE 5 AUDIT EXECUTION: FINANCIAL STATEMENT ITEMS SUBSTANTIVE PROCEDURES OUTLINE Application of specific substantive procedures to test the following categories of assertions: -Assertions relating to

MODULE 5 AUDIT EXECUTION: FINANCIAL STATEMENT ITEMS SUBSTANTIVE PROCEDURES OUTLINE Application of specific substantive procedures to test the following categories of assertions: -Assertions relating to

GUIDANCE NOTE. FOR A MANAGER OF A MANAGED ENTITY (a MOME ) AND CERTAIN MANAGED ENTITIES

AND CERTAIN MANAGED ENTITIES") GUIDANCE NOTE FOR A MANAGER OF A MANAGED ENTITY (a MOME ) AND CERTAIN MANAGED ENTITIES Issued: April 2009 Contents CONTENTS Contents... 3 1 Introduction... 4 2 MoME arrangements... 4 3 Application of

GUIDANCE NOTE FOR A MANAGER OF A MANAGED ENTITY (a MOME ) AND CERTAIN MANAGED ENTITIES Issued: April 2009 Contents CONTENTS Contents... 3 1 Introduction... 4 2 MoME arrangements... 4 3 Application of

Office of Chief of Operations State Procurement Card Program Guidelines- Office of Procurement

Office of Chief of Operations State Procurement Card Program Guidelines- Office of Procurement Introduction The Department of Finance and Administration (DFA) has adopted State Procurement Card Guidelines

Office of Chief of Operations State Procurement Card Program Guidelines- Office of Procurement Introduction The Department of Finance and Administration (DFA) has adopted State Procurement Card Guidelines

REPORT 2016/012 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/012 Audit of the management of the technical cooperation project on Information and Communication Technologies in Africa Phase II in the Economic Commission for Africa

INTERNAL AUDIT DIVISION REPORT 2016/012 Audit of the management of the technical cooperation project on Information and Communication Technologies in Africa Phase II in the Economic Commission for Africa

REPORT. on the annual accounts of the European Asylum Support Office for the financial year 2016, together with the Office s reply (2017/C 417/12)

") 6.12.2017 EN Official Journal of the European Union C 417/79 REPORT on the annual accounts of the European Asylum Support Office for the financial year 2016, together with the Office s reply (2017/C 417/12)

6.12.2017 EN Official Journal of the European Union C 417/79 REPORT on the annual accounts of the European Asylum Support Office for the financial year 2016, together with the Office s reply (2017/C 417/12)