AUDIT UNDP NEPAL. Comprehensive Disaster Risk Management Programme (Directly Implemented Project No )

|

|

|

- Randall Sherman

- 5 years ago

- Views:

Transcription

Report No.")

1 UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP NEPAL Comprehensive Disaster Risk Management Programme (Directly Implemented Project No ) Report No Issue Date: 29 November 2013

2 United Nations Development Programme Office of Audit and Investigations Report on the audit of UNDP Nepal Comprehensive Disaster Risk Management Programme (Project No ) Executive Summary From 2 September to 7 October 2013, the Office of Audit and Investigations (OAI) of the United Nations Development Programme (UNDP), through T R Upadhya & Co. (the audit firm), conducted an audit of the Comprehensive Disaster Risk Management Programme, Project No (the Project), which is directly implemented and managed by the UNDP Country Office in Nepal (the Office). The audit was conducted under the general supervision of OAI in conformance with the International Standards for the Professional Practice of Internal Auditing. The last audit of the Office was conducted by OAI in The Project reported expenditure totalling $6.4 million during the period from 1 January to 31 December The following donors contributed to the Project: Department for International Development, UNDP, World Bank, European Commission - Humanitarian Aid and Civil Protection and UNISDR. Audit scope and objectives The audit firm conducted a financial audit to express an opinion on whether the financial statements present fairly, in all material aspects, the Project s operations. The audit covered the Project s Statement of Expenditure (Combined Delivery Report) for the period from 1 January to 31 December 2012 and the Statement of Assets as of 31 December Audit results Based on the audit report and corresponding management letter submitted by the audit firm, the results are summarized in the table below: Amount (in $ 000) Project Expenditure Opinion NFI (in $ 000) Amount (in $ 000) Project Assets Opinion NFI (in $ 000) 6,396 Qualified 529* 335 Adverse 335 NFI = Net Financial Impact *The NFI for Project expenditure is the sum of $700,344 (expenses of $325,034 incorrectly recorded as assets and expenses of $375,310 incurred by Responsible Parties not reflected in the Combined Delivery Report), less $171,314 (value added tax of $120,608, excess GMS charged to the Combined Delivery Report of $29,054 and vehicles costing $21,652 charged to expenses instead of capitalizing) The audit firm qualified its opinion on project expenditure due to incorrect classification of donor codes, incorrect recording of expenses as assets, and failure to record expenses in the Combined Delivery Report. The audit firm issued an adverse opinion on project assets due to incorrect recording of expenses as assets and failure to record fixed assets in the statement of assets. Key issues and recommendations The audit raised five issues and resulted in five recommendations, all of which were ranked high (critical) priority, meaning Prompt action is required to ensure that UNDP is not exposed to high risks. Failure to take action could result in major negative consequences for UNDP and may affect the organization at the global level. Audit Report No. 1200, 29 November 2013: UNDP Nepal - DIM Project No Page i

3

4 INDEPENDENT AUDITORS REPORT FINANCIAL AUDIT OF COMPREHENSIVE DISASTER RISK MANAGEMENT PROGRAMME ( CDRMP ) UNITED NATIONS DISASTER RISK MANAGEMENT PROGRAMME PROJECT ID/ AWARD NUMBER: / For the period 1 January 2012 to 31 December 2012 Performed By: T R Upadhya & Co. Issued Date: 20 November 2013 This document contains 50 pages (Including cover page) Annexure contains 2 pages

5 TABLE OF CONTENTS Page No. Transmittal Letter Abbreviations Part I: Executive Summary 1. Background 2. Purpose of the audit 3. Objective of the audit 4. Scope of the audit 5. Scope limitation 6. Methodology 7. Audit results 8. Management response 9. Follow up of prior audit recommendations 10. Acknowledgement Part II: Audit Opinion 1. Opinion on Combined Delivery Report and Funds Utilisation Statement 2. Opinion on Statement of Fixed Assets Certified Combined Delivery Report Certified Statement of Fixed Assets Part III: Management Letter Annexure Definition of Audit Opinion Summary of Excess Expenditure Charged in CDR

6

7 List of Abbreviations and Acronyms ADPC Asian Disaster Preparedness Centre AFO Administrative Finance Officer AINGOs Association of International Non Governmental Organisations APF Armed Police Force AWP Annual Work Plan BCPR Bureau for Crisis Prevention and Recovery CBDMP Community Based Disaster Management Programme CBDRM Community Based Disaster Risk Management Programme CBO Community Based Organisations CDRMP Comprehensive Disaster Risk Management Programme CDR Combined Delivery Report CO Country Office DDC District Development Committee DP-net Disaster Preparedness Network DfID Department for International Development, UK DRR Disaster Risk Reduction DRM Disaster Risk Management GoN Government of Nepal GMS General Management Services GRN Good Receipt Note IGP Inspector General of Police IPSAS International Public Sector Accounting Standard LoA Letter of Agreement LTA Long Term Agreement M&E Monitoring & Evaluation MoU Memorandum of Understanding MoHA Ministry of Home Affairs MoLD Ministry of Local Development MoPPW Ministry of Physical Planning and Works NBC National Building Code NDRRA National Disaster Risk Reduction Advisor NGO Non Governmental Organisation NRCS Nepal Red Cross Society NRs Nepalese Rupees NSET National Society for Earthquake Technology PCA Project Cash Advance PEB Project Executive Board PISU Project Implementation Support Unit PO Purchase Order $ US Dollars SC Save the Children UNDP United Nations Development Programme VAT Value Added Taxes WB The World Bank

8

9 5. Scope limitation The scope of the audit does not include: Activities and expenses incurred or undertaken at the level of other donors and partners ; and Expenses processed and approved in locations outside the country such as UNDP Regional Centres and UNDP Headquarters and where the supporting documentation is not retained at the level of the UNDP Nepal Country Office. 6. Methodology The following methodology was followed for the audit: a) Held meetings with UNDP Nepal Country Office, project officials and relevant officials of the Government of Nepal; b) Reviewed the contract agreement and appropriate amendments, budgets, and written procedures by UNDP, standard provisions annexed to agreement, correspondence and minutes of meetings; c) Obtained an understanding of the accounting, administrative and internal control systems of the project using questionnaires and interviews; d) Devised and performed appropriate tests on the transactions and balances recorded in the financial statements; e) Designed appropriate audit steps and procedures to provide reasonable assurance of detecting errors, irregularities, and illegal acts that could have a direct and material effect on the results of our audit. We were also aware of the possibility of illegal acts that could have an indirect and material effect on the results of our audit; f) Tested the effectiveness of administrative controls applied by the project management to ensure compliance with applicable laws, regulations and subcontract terms of agreement; g) Verified unliquidated advances and pending reimbursement as on the closing date of respective reporting period; h) Reviewed bank balances as on closing date of reporting period; and i) Reviewed the status of inventory of non expendable equipment and commodities held as on the date of reporting period. 7. Audit results 7.1 Opinion on the Combined Delivery Report We have issued a qualified audit opinion on the CDR and the funds utilisation statement for the period 1 January 2012 to 31 December 2012 due to the following reasons which has resulted in total understatement amounting to $529,030 in the CDR: a) Incorrect fund code used for recording expenses in the CDR amounting to $444,122. (Refer Section of ML) b) Understatement of expenses by $325,034 due to incorrectly recording of equipment purchased for the Armed Police Force and Emergency Operation Centre as assets in Atlas. (Refer Section 3 of ML) 2 P age

10 c) Expenditure of $98,560 incurred for Government Agencies and UN Agencies have been incorrectly reported in CDR under UNDP Expenses. In addition, adjustments of $749,344 made through General Ledger Journal Entry ( GLJE ) for Micro Capital Grants were incorrectly reflected under UNDP Expenses instead of the Government Expenses. d) Value Added Taxes ( VAT ) amounting to $120,608 paid on procurement of goods and services have been charged as expenses instead of recording as receivables which have resulted in expenses in the CDR to be overstated by $120,608. (Refer Section of ML) e) Expenses of $375,310 incurred by the Responsible Parties in the year 2012 was not accrued and reflected in the CDR as required by International Public Sector Accounting Standard, resulting in understatement of the expenses for the year (Refer Section of ML) f) Excess expenses of $29,054 charged to the project resulting in overstatement in CDR. (Refer Annexure 2) g) The accuracy of the depreciation of $12,909 charged in the CDR could not be ascertained in the absence of the fair presentation of the fixed assets in the CDR and overstatement of expenses by incorrectly charging the cost of 2 vehicles costing $21,652 as expenses instead of capitalising these as fixed assets. (Refer Section 3 of ML) 7.2 Opinion on the Statement of Fixed Assets We have issued an adverse audit opinion on Statement of Fixed Assets as it does not give a true and fair view of the balance of inventory amounting to $335, reported as at 31 December 2012 due to the following reasons: a) Equipment costing $325,034 purchased for the Armed Police Force and other government agencies and required to be expensed off were incorrectly recorded as fixed assets in the Atlas and the Statement. b) 2 vehicles costing $21,652 were charged as expenses in the CDR instead of capitalising the same as fixed assets and incorporating it in the Statement of Fixed Assets. All the above matters have been reported under Section 3 of the management letter in Part III of this report. 7.3 Internal controls and compliance During the course of our audit, certain issues were noted that can be considered as material weaknesses and reported under Part III Management Letter of the report in detail and the principal issues summarised hereunder. The audit findings with high risk category have been included in the management letter in Part III of this report and other observations with medium and low risk categories have been reported to the project separately for corrective actions. 8. Management response The project management through its written responses have generally agreed on our audit observations and recommendations and their full responses and action plan for corrective action can be found in the respective section under management comments in Part III of this report. 3 P age

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42 III. Management Letter Table of Contents Page No. 1. Project Management Project Finances Donor Reporting Financial and Cash Management Payment and Voucher Approval Process Payment Process Assets Management P age

43 1. Project Management 1.1 Project Finances Expenses not reported in CDR Observations As per the financial audit of the Government Expenses reported in the CDR for the period from 1 January 2012 to 31 December 2012 submitted by the independent auditor, following expenses were not reported in the CDR by the project resulting in understatement of the government expenses and the total expenses in the CDR for the year ended 31 December 2012 by $375, Partner Code Expenses incurred in 2012 ($) Remarks , The expenditure report from the partner was not obtained and recorded for the month of December 2012 on the ground that project has neither released the fund nor the partner has reported the expenditure for that period. The project has not released additional funds to the partner on the ground that the contract with the partner was about to expire on 22 December Hence the partner is not supposed to incur the expenses without receiving the funds from the project. However, the expenses related to the same period was claimed and refunded by the project in June 2013 and reflected in CDR of , Expense report was not submitted by the partner and hence not reported in CDR and reflected as National Execution (NEX) advances as of 31 December Expense report was not submitted by the partner and hence not reported in CDR and reflected as National Execution (NEX) advances as of 31 December , The entire advance amount released in the name of partner was already recorded as expense in CDR of 2011 however the expense was actually incurred in the period from January to June Total 375, Risk/ Priority High Recommendation The project should prescribe the proper cut off and mandatory provision regarding the reporting of expenses against the NEX advances to ensure accurate reporting of expenditure in CDR of the respective period. With the implementation of IPSAS, the expenses have to be reported on accrual basis, accordingly all expenditure accrued at year end should be recorded and reported in the CDR for the fair presentation of the financial statements. 36 P age

44 Management Comments and Action Plan Agreed Partner code 10620: It was discussed and agreed with the partner through correspondence to extend the project cooperation agreement beyond 22 December Based on this agreement, the partner continued implementing the agreed activities. However, the actual amendment of the PCA to that effect could not happen within December Hence the expenditure made by the partner in December 2012 was not recorded in our books of From now onwards, the project will ensure the IPSAS compliance while recording the partner organisation expenditure. Partner code 124: The partner did not submit the report on time to UNDP for Atlas recording and thus the expenditure was not recorded in our books of The project will ensure that the partner organisations will submit their financial reports on time. Partner code 2965: The expenditures were relating to 15 December to 31 December 2012, and the financial report was submitted on 31 December. Hence the expenditure was recorded in UNDP books only in 2013 considering the materiality of the amount. Partner code 9682: This issue has been highlighted in the NIM audit of the partner organisation and the action has already been implemented. 37 P age

45 1.2 Donor Reporting Unfunded programme expenses incorrectly reported under DfID Fund Observations During the year, the project has procured Search and Rescue Equipment costing $391, for the Armed Police Force ( APF ) and requested reimbursement of $380,707 only from the World Bank. Further, it was noted that the project had incorrectly recorded expenses amounting to $163, in the CDR and assets amounting to $255, in the statement of Fixed Asset under the DfID fund code instead of World Bank fund code. Further, expenses of $25,288 incurred under activity 3 National and Local Vulnerabilities funded by the UNDP TRAC fund and BCPR funds were also incorrectly reported under the fund code (Programme Cost Sharing) i.e., DfID funding and also the GMS charge of $1, recovered from DfID as management fees based on the expense reported which was not correct. Risk/ Priority High Recommendation The project management should ensure that unauthorised use of donor funds are not be made without the prior approval of the donors and that expenses are reported in the correct account code against the proper funding source in the CDR for correct reporting to donor and fair presentation of CDR. And request the amount paid to the vendor for the procurement of equipments not the amount committed (as per PO). GMS charge should be charged at the agreed rates to the budget of the donors who have agreed to fund the activity and not the other donor. The incorrect charge recovered from DfID should be credited to the DfID funding with a receivable from the World Bank and UNDP TRAC and BCPR. Management Comments and Action Plan Agreed Loss to project: The agreement with World Bank fund is under reimbursable basis. The payment was in NPR. The invoice was submitted to World Bank right after the Purchase Order was raised. However, the actual expenditure was higher than the original Purchase Order amount due to fluctuation of exchange rate between USD and NPR. The financial report to World Bank based on actual expenditure including GMS will be submitted to World Bank. Wrong recording in Atlas: There was wrong recording of assets in Atlas, and UNDP CO communicated this with GSSC team to rectify the transaction. However, the rectification posted by GSSC also created a problem in ATLAS recording. This issue is well noted by UNDP CO and proactive actions are being taken in guidance and consultation with HQ to rectify the issue. Use of DFID funds: The project used DfID fund for short-term purpose for the procurement of Search and Rescue equipment until the reimbursement would be received from the World Bank. DfID funds have been adjusted immediately after receiving the World Bank funds. 38 P age

46 Expenses of $25,288 incurred under activity 3 National and Local Vulnerabilities funded by the UNDP TRAC fund and BCPR funds was wrongly charged to DfID fund and this will be rectified in The project management and concerned CO units will ensure GMS compliance while submitting report to donors. Project Management will also ensure the appropriate recording of expenditure and assets in Atlas. 39 P age

47 2. Financial and Cash Management 2.1 Payment and Voucher Approval Process Value Added Taxes ( VAT ) charged as expense Observation As per the agreement between the Government of Nepal ( GoN ) and the UNDP Nepal, UNDP Nepal can claim for the refund of VAT paid by the project after following the due process prescribed in the VAT rules and regulations. It was noted that the project has incorrectly expensed off VAT paid on procurement of goods and services amounting to NRs 12,608,019 ($120,608 approx.) rather than accounting for VAT under a receivable account and claiming for refund from the Inland Revenue Department. Due to ineffective monitoring over the procurements made through VAT invoices by the concerned staff ineligible expenses of $120,608 has been charged to the project resulting in financial loss to the project and overstatement of the project expenses in Risk/ Priority High Recommendation The project should ensure that the VAT paid for goods and services procured by the project should be recorded as receivable and monitored separately instead of expensing it to the project. UNDP CO should file refund for VAT of $120,608 with the revenue authorities. Management Comments and Action Plan Agreed UNDP CO notes that VAT amount was wrongly recorded in expenditure account. The project has already started recording VAT in receivable account with effect from January Although the VAT is recorded in expenditure account, the project is maintaining separate record to list all VAT receivable from tax office. The project has already submitted the claim of VAT pertaining to 2012 to tax office and is waiting for refund. After receiving the VAT refund, it will be credited to project account. 40 P age

48 2.2 Payment Process Weaknesses in the payment process Observations Payments should be verified before disbursements for the accuracy of the charge of account codes, vendor details, the amount to be paid and that proper documentary evidences are attached for the payments to be made, propriety of the expenses and that the evidence of goods have been received or not. On review the payments process by selection of payment vouchers on a sample basis the following discrepancies were noted indicating that effective controls over the payment process are not operating in the project and the Country Office ( CO ): a) Payment made to the wrong vendor The project awarded the contract to provide professional services for implementation of Nepal national building code through automation of building plan approval and monitoring system in Nepal to a vendor on 25 July However, without proper checking of the contract and the name of the vendor, PO was raised incorrectly in the name of another vendor which resulted in payment of $45, (1 st instalment of 20% of the contract) to be released to the unauthorised vendor. b) Payment made without receiving payment request/deliverables from vendor A vendor was awarded a contract (Contract No. PISU/PROF/09/2011& 10/2011) for providing mason training and payments were to be made on submission of deliverables. It was noted that payments were made by the project without receiving the request for payment and submission of the deliverables as follows: Mason Training/Contract No. Amount Paid ($) Remarks PISU/PROF/09/ ,720 The contract stipulated that 50% will be released on submission of deliverables 2, 3, 4, 6 and final report of 5 to the satisfaction of the project. The request was made for release of 40% of the contract value as all the deliverables had not been submitted but the project has released 50% of the contract value on 3 September 2012 resulting in excess payment $10,144. Though the same was subsequently recovered from the Vendor on 18 October PISU/PROF/10/ ,191 Payment of 3 rd instalment of 30% without receiving any request and submission of deliverables of mid-term reports and recommendation for payment was not documented by the programme officer. Total 88,911 c) Payment for goods and services made without complying with the terms of the contract In the following instances, payments have been processed by the project without receiving the recommendation for payment or receiving the final deliverables: 41 P age

49 Amount ($) Voucher No. and Date Remarks 92, / 28/6/2012 Payment made without obtaining the recommendation from the related programme staff confirming that all documents were received as per the contract. Payment for deliverable IV.1 was made on 28 June 2012 though the due date of the same was only on December 2012 as per the amended contract dated 10 October (NRs 22,100) 1, (NRs 92,400) 10, (NRs 1,007,750) / 2/7/ / 2/7/ / 10/12/ % of the remaining contract amount is due for payment only upon receipt of final report but the recommendation for the payment was made without receiving the final report and also the payment was made accordingly. As per the contract, 20% of the contract amount will be due for payment upon submission and approval of the final report. However, final payment of Rs 1,007,750 was made before the completion of work i.e. Community pre-positioning of basic kits was purchased only in 2013 which was the plan for the year ,491.3 Total Risk/ Priority High Recommendation The project should exercise due diligence in the verification of the contract and the invoices and ensure that payment requests are supported by documentary evidences include the required deliverables before processing payments. The authorised personnel making the recommendations should ensure that all the above documents are included in the payment request prior to making the recommendation for payments. The finance unit should ensure that the vendor s name, banking details matches with the PO and the vendor database including the contract prior to releasing the payments. Management Comments and Action Plan Agreed a) PO was raised incorrectly in the name of a wrong vendor. The discrepancy was realised while reconciling contractual service companies on a regular basis. Consequently, an immediate action was taken by the project along with PISU to refund the released fund the fund was duly deposited into UNDP Bank account on 14 October 2012 by reversing the expenses recorded in the books of account of wrong vendor. The PO of wrong vendor was cancelled and new PO was raised in the name of right vendor. b1).this payment was made mistakenly without receiving one deliverables, which was only realised while reconciling the contractual service companies on a regular basis. It was immediately rectified by receiving the excess amount ($10,144) from the vendor and deposited in the UNDP Bank Account dated 14 October This amount was paid later only after receiving required deliverables. Therefore, there was no double payment. Since the exceeded payment of $10,144 was adjusted on 18 October 2012, there was no need to adjust with second instalment. 42 P age

50 b2) Referring PISU/PROF/10/2011, this issue has been overlooked. The concerned project officer will critically examine all deliverables before releasing any payment. The project finance will also ensure the achievement of milestone before recommending for payment. c) The concerned project officer will critically examine all deliverables before releasing the payment. The project finance team will also ensure the achievement of milestone before recommending for payment. 43 P age

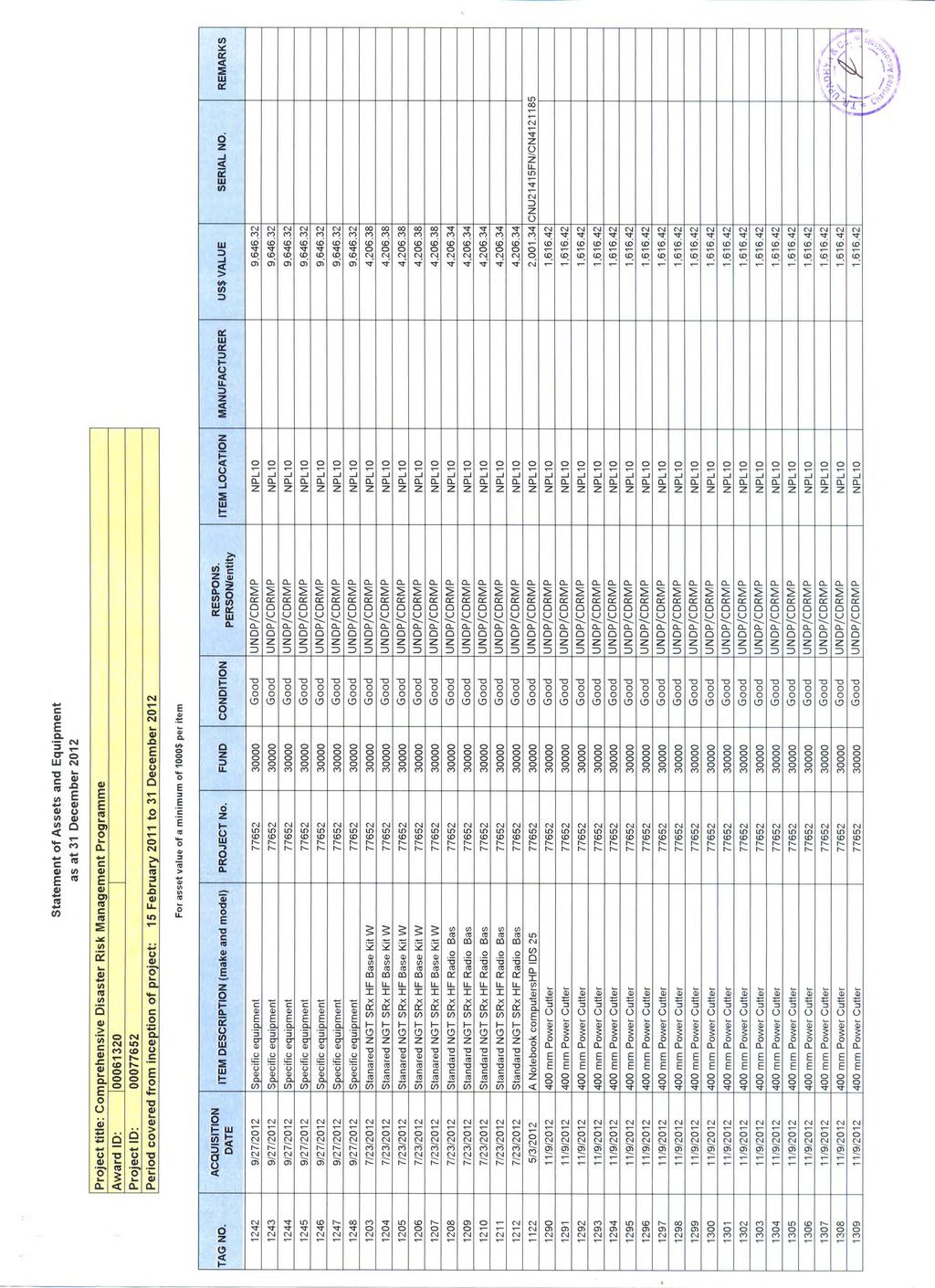

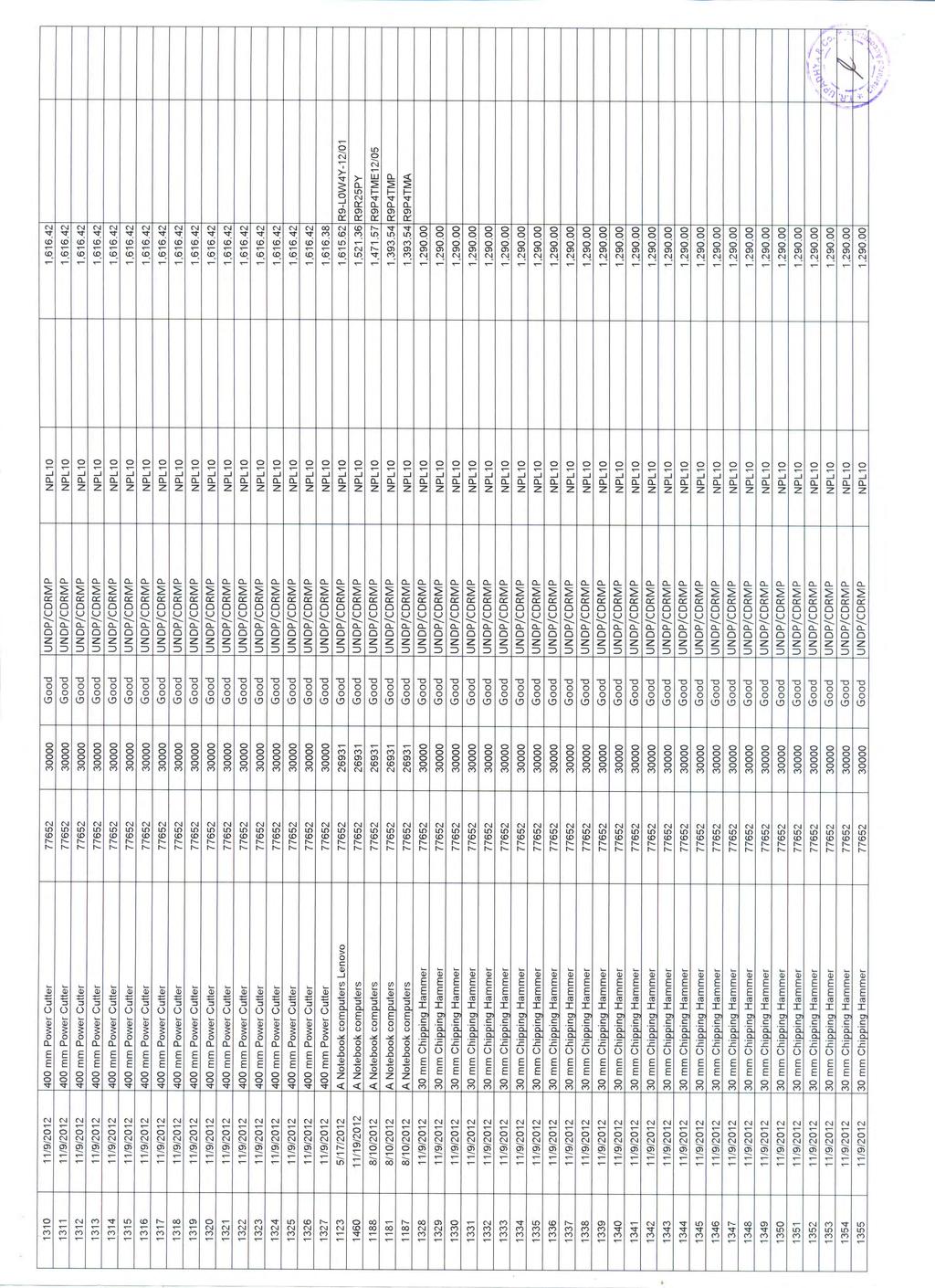

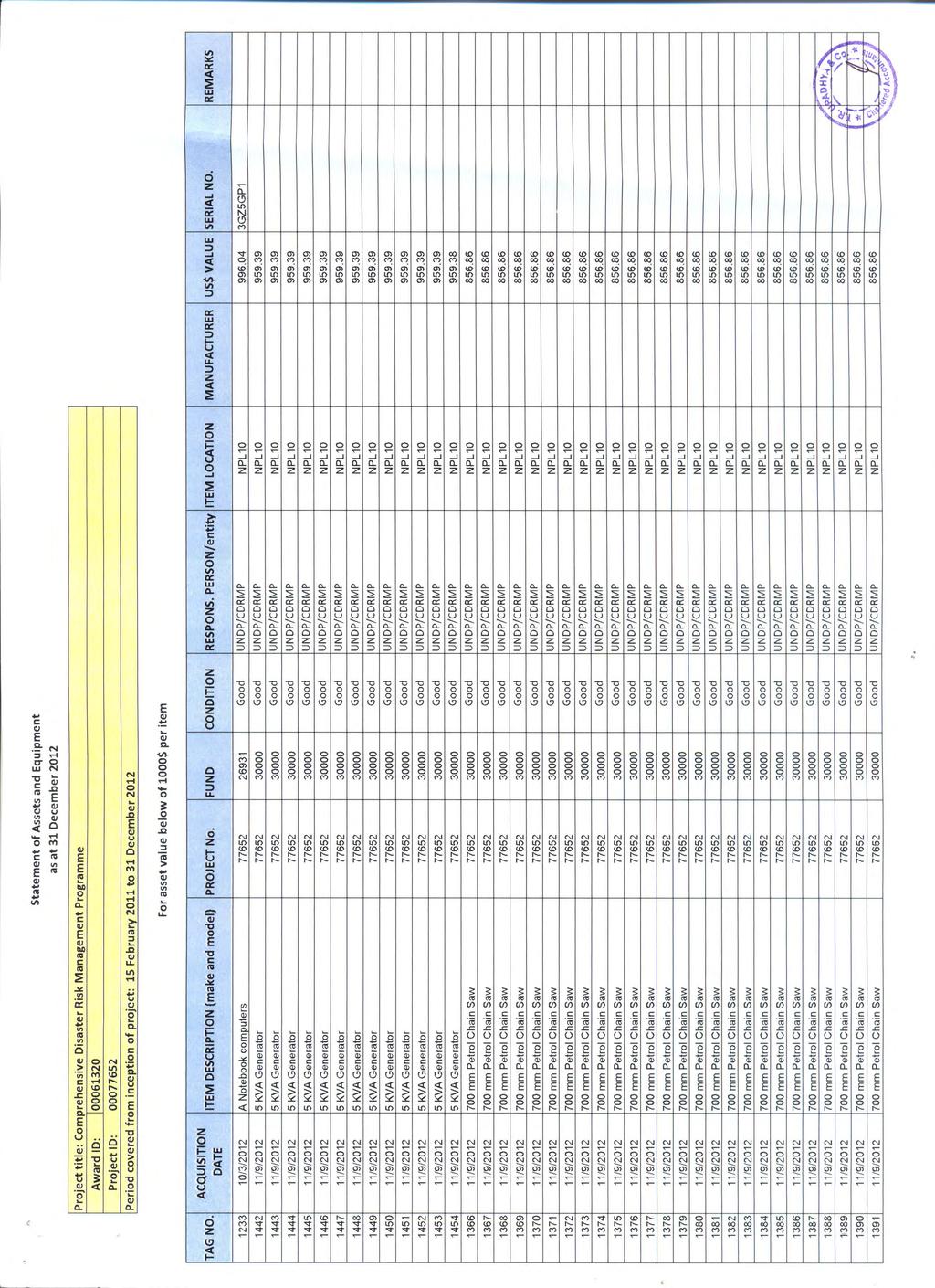

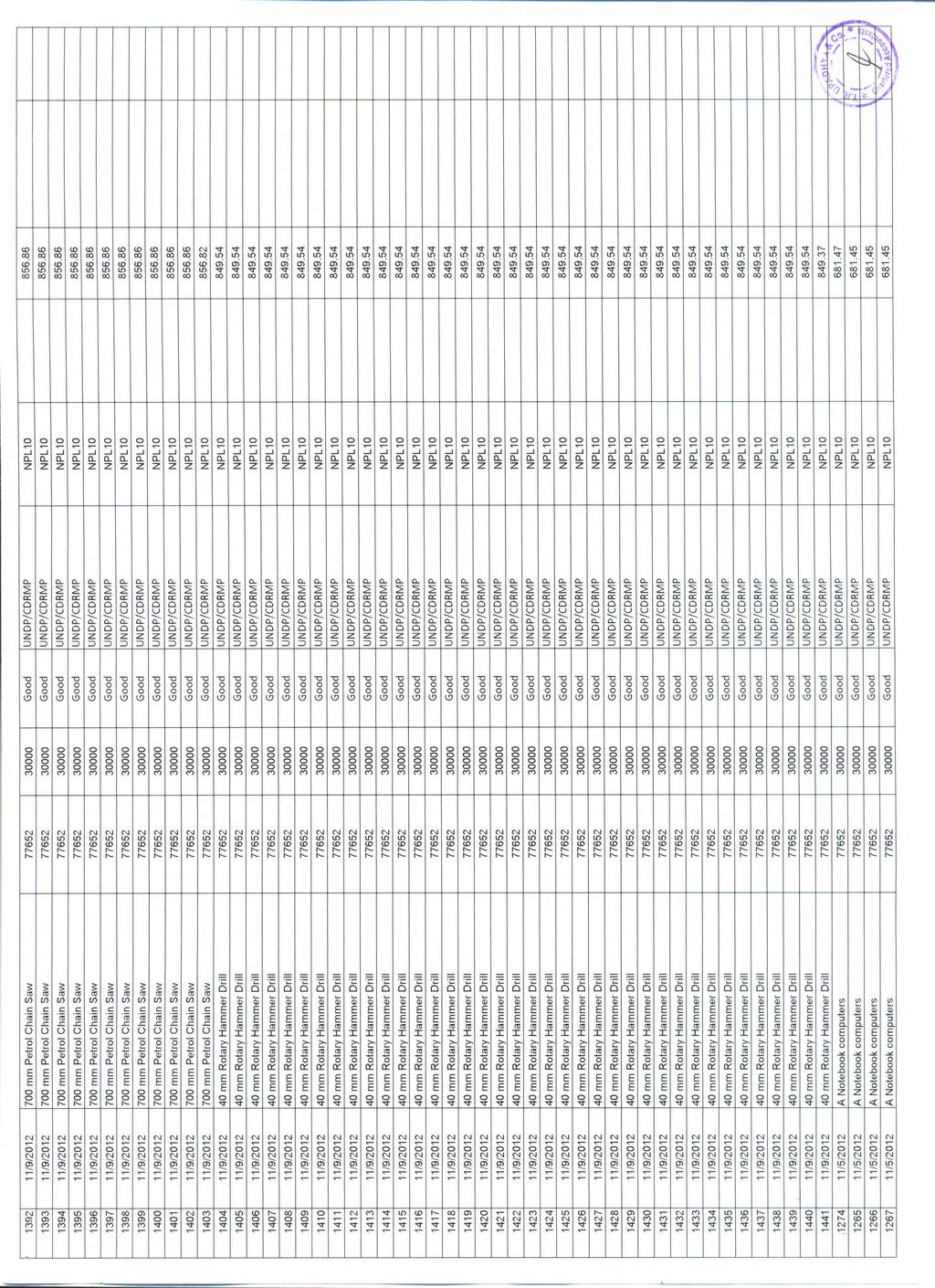

51 3. Assets Management Observation Capital assets with a value of $500 or more and a minimum life expectancy of three years should be recorded correctly as assets in Atlas and should be depreciated on a straight line method. The statement of fixed assets should present fairly the balance of fixed assets of the project as on 31 December Our review of the fixed assets records controls over its safe custody and the statement of fixed assets revealed the following discrepancies: 2 vehicles costing $21,652 has been fully expensed in the CDR instead capitalising them as assets. Various emergency rescue and response equipment purchased for the project amounting to $325,034 have been recorded as assets, although these should have been expensed off in the CDR. The accuracy of depreciation charged in the CDR of $12,909 could not be ascertained as the assets reported were not accurate. It was explained that the errors were due to wrong selection of Catalogue (UNDP and Non UNDP Catalogue) at the time of recording in the Atlas and lack of sufficient training to staff on the segregation of capital items with non capital items. The statement of fixed assets does not present fairly the balance of fixed assets of CDRMP as at 31 December Risk/ Priority High Recommendations The project should provide additional training to its staff to classify the assets as a capital assets or expense and record it properly in the statement of fixed assets for fair presentation of the balance of fixed assets. Management comments and action plan The issue occurred due to wrong selection of assets catalogue in ATLAS. Project/CO is in consultation with HQ to expensed these items in The project will correct the entry by capitalising these items. Country Office will provide orientation on assets recording to project staff based on IPSAS. 44 P age

52 Annexure 1 Definitions of Audit Opinion Type of Audit Opinion Clean Qualified Adverse Disclaimer Conditions An unqualified audit opinion is expressed when the auditor concludes that the financial statements give a true fair view or are presented fairly, in all material respects, in accordance with the applicable financial reporting framework. A qualified opinion is expressed when the auditor concludes than an unqualified opinion cannot be expressed but the effect of any disagreement with management, or limitation on scope is not so material and pervasive as to require as adverse opinion or a disclaimer of opinion. A qualified opinion is expressed as being except for the effects of the matter to which the qualification relates. An adverse opinion is expressed by an auditor when the financial statements are significantly misrepresented, misstated, and do not accurately reflect the expenses incurred and reported in the financial statements (UNDP CDR), Statement of Cash, Statement of Assets and Equipment ). An adverse opinion is expressed when the effect of a disagreement is so material and pervasive to the financial statements that the auditor concludes that a qualification of the report is not adequate to disclose the misleading or incomplete nature of the financial statements. A disclaimer of opinion is expressed when possible effect of a limitation on scope is so material and pervasive that the auditor has not been able to obtain sufficient appropriate audit evidence and accordingly is unable to express an opinion on the financial statements.

53 Annexure 2 Summary of Excess Expenditure Charged in CDR S.No. Particulars 1. GMS Charge for procurement of equipment from World Bank for APF recorded in DfID 2. GMS Charge expenses incurred for UNDP Track and BCPR Fund charged to DfID ML Ref. No. Amount in $ , ,654 Total 29,054

AUDIT UNDP BANGLADESH. Comprehensive Disaster Management Programme Phase II (Project No , Output Nos )

") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP BANGLADESH Comprehensive Disaster Management Programme Phase II (Project No. 58919, Output Nos. 73416) Report No. 1472

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP BANGLADESH Comprehensive Disaster Management Programme Phase II (Project No. 58919, Output Nos. 73416) Report No. 1472

Terms of Reference for Financial Audit of Implementing Partners. UNICEF Nigeria Country Office Expenditures

Terms of Reference for Financial Audit of Implementing Partners UNICEF Nigeria Country Office 2012-2013 Expenditures A. Background and Scope of Audit Harmonized Approach to Cash Transfer (HACT) is a response

Terms of Reference for Financial Audit of Implementing Partners UNICEF Nigeria Country Office 2012-2013 Expenditures A. Background and Scope of Audit Harmonized Approach to Cash Transfer (HACT) is a response

TERMS OF REFERENCE FOR AUDITS OF NIM/NGO PROJECTS

United Nations Development Programme Office of Audit and Investigations Annex I TERMS OF REFERENCE FOR AUDITS OF NIM/NGO PROJECTS 2014 02 November 2014 TABLE OF CONTENTS Page INTRODUCTION... 3 A. Background...

United Nations Development Programme Office of Audit and Investigations Annex I TERMS OF REFERENCE FOR AUDITS OF NIM/NGO PROJECTS 2014 02 November 2014 TABLE OF CONTENTS Page INTRODUCTION... 3 A. Background...

AUDIT UNDP NIGERIA. DEMOCRATIC GOVERNANCE FOR DEVELOPMENT: DEEPENING DEMOCRACY IN NIGERIA (Directly Implemented Project No , Output No.

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP NIGERIA DEMOCRATIC GOVERNANCE FOR DEVELOPMENT: DEEPENING DEMOCRACY IN NIGERIA (Directly Implemented Project No. 56855,

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP NIGERIA DEMOCRATIC GOVERNANCE FOR DEVELOPMENT: DEEPENING DEMOCRACY IN NIGERIA (Directly Implemented Project No. 56855,

AUDIT. UNDP Pakistan. Early Recovery Programme in Pakistan (Directly Implemented Project No ) Report No. 990 Issue Date: 19 June 2013

Report No. 990 Issue Date: 19 June 2013") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP Pakistan Early Recovery Programme in Pakistan (Directly Implemented Project No. 76295) Report No. 990 Issue Date: 19

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP Pakistan Early Recovery Programme in Pakistan (Directly Implemented Project No. 76295) Report No. 990 Issue Date: 19

AUDIT UNDP COUNTRY OFFICE AFGHANISTAN FINANCIAL MANAGEMENT. Report No Issue Date: 10 December 2013

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AFGHANISTAN FINANCIAL MANAGEMENT Report No. 1233 Issue Date: 10 December 2013 Table of Contents Executive Summary i I. Introduction

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AFGHANISTAN FINANCIAL MANAGEMENT Report No. 1233 Issue Date: 10 December 2013 Table of Contents Executive Summary i I. Introduction

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT. 26 August 2016

FINANCIAL AUDIT REPORT. 26 August 2016") UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 26 August 2016 PROJECT NAME: MODERNIZATION AND IMPROVEMENT OF POLICING PROJECT (MIPP) PROJECT NUMBER: 00093090 COUNTRY: NEPAL AUDITOR:

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 26 August 2016 PROJECT NAME: MODERNIZATION AND IMPROVEMENT OF POLICING PROJECT (MIPP) PROJECT NUMBER: 00093090 COUNTRY: NEPAL AUDITOR:

TERMS OF REFERENCE (TOR) FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS

FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS") TERMS OF REFERENCE (TOR) FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS TABLE OF CONTENTS Introduction... 3 A. Background... 7 B. Project Management... 7 C. Consultations with concerned parties...

TERMS OF REFERENCE (TOR) FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS TABLE OF CONTENTS Introduction... 3 A. Background... 7 B. Project Management... 7 C. Consultations with concerned parties...

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 14 FEBRUARY 2018

FINANCIAL AUDIT REPORT 14 FEBRUARY 2018") UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 14 FEBRUARY 2018 PROJECT NAME: MODERNIZATION AND IMPROVEMENT OF POLICING PROJECT (MIPP) PROJECT NUMBER: 93090 COUNTRY: NEPAL AUDITOR:

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 14 FEBRUARY 2018 PROJECT NAME: MODERNIZATION AND IMPROVEMENT OF POLICING PROJECT (MIPP) PROJECT NUMBER: 93090 COUNTRY: NEPAL AUDITOR:

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) INTERNAL AUDIT REPORT. 19 October 2017

INTERNAL AUDIT REPORT. 19 October 2017") UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) INTERNAL AUDIT REPORT 19 October 2017 PROJECT NAME: GLOBAL FUND REGIONAL ARTEMISININ INITIATIVE (RAI) MYANMAR - PRINCIPAL RECIPIENT - UNOPS PROJECT NUMBER:

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) INTERNAL AUDIT REPORT 19 October 2017 PROJECT NAME: GLOBAL FUND REGIONAL ARTEMISININ INITIATIVE (RAI) MYANMAR - PRINCIPAL RECIPIENT - UNOPS PROJECT NUMBER:

AUDIT OF THE FUND ACCOUNTABILITY STATEMENT OF USAID RESOURCES MANAGED BY MERCY CORPS AND IMPLEMENTED BY PUBLIC AID ORGANIZATION ( PAO ) UNDER

UNDER") AUDIT OF THE FUND ACCOUNTABILITY STATEMENT OF USAID RESOURCES MANAGED BY MERCY CORPS AND IMPLEMENTED BY PUBLIC AID ORGANIZATION ( PAO ) UNDER COOPERATIVE AGREEMENT NUMBER AID-267-A-00-12-00001, CFDA #

AUDIT OF THE FUND ACCOUNTABILITY STATEMENT OF USAID RESOURCES MANAGED BY MERCY CORPS AND IMPLEMENTED BY PUBLIC AID ORGANIZATION ( PAO ) UNDER COOPERATIVE AGREEMENT NUMBER AID-267-A-00-12-00001, CFDA #

DESK REVIEW UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN

UNITED NATIONS DEVELOPMENT PROGRAMME DESK REVIEW OF UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN Report No. 1310 Issue Date: 9 October 2014 Table of

UNITED NATIONS DEVELOPMENT PROGRAMME DESK REVIEW OF UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN Report No. 1310 Issue Date: 9 October 2014 Table of

External Audit. April 2012

External Audit April 2012 Audit Definition Ex post review of the books of account, financial statements, records of transactions & financial systems Examines the adequacy of accounting systems & procedures,

External Audit April 2012 Audit Definition Ex post review of the books of account, financial statements, records of transactions & financial systems Examines the adequacy of accounting systems & procedures,

AUDIT UNDP REPUBLIC OF CHAD. Programme Conjoint D Appui au Détachement Intégré de Sécurité (Directly Implemented Project No.

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP REPUBLIC OF CHAD Programme Conjoint D Appui au Détachement Intégré de Sécurité (Directly Implemented Project No. 77223)

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP REPUBLIC OF CHAD Programme Conjoint D Appui au Détachement Intégré de Sécurité (Directly Implemented Project No. 77223)

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT UNDP LEBANON

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP LEBANON EARLY RECOVERY FOR DISPLACED SYRIANS, LEBANESE HOSTING COMMUNITIES SUPPORT PROJECT (Directly Implemented Project

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP LEBANON EARLY RECOVERY FOR DISPLACED SYRIANS, LEBANESE HOSTING COMMUNITIES SUPPORT PROJECT (Directly Implemented Project

Report on Financial Audit of UNDP Directly Implemented Project Managed by UNDP Programme of Assistance to the Palestinian People (PAPP)

") Report on Financial Audit of UNDP Directly Implemented Project Managed by UNDP Programme of Assistance to the Palestinian People (PAPP) Construction of Khan Younis Waste Water Treatment Plant Project ID

Report on Financial Audit of UNDP Directly Implemented Project Managed by UNDP Programme of Assistance to the Palestinian People (PAPP) Construction of Khan Younis Waste Water Treatment Plant Project ID

AUDIT UNDP DOMINICAN REPUBLIC

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP DOMINICAN REPUBLIC DESARROLLO LOCAL TRANSFRONTERIZO EN ACOMPAÑAMIENTO AL PROGRAMA BINACIONAL (Directly Implemented

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP DOMINICAN REPUBLIC DESARROLLO LOCAL TRANSFRONTERIZO EN ACOMPAÑAMIENTO AL PROGRAMA BINACIONAL (Directly Implemented

Control activities that are part of the process are detailed in the riskcontrol

Policy Title Previous title (if any) Cash Transfers to Implementing Partners N/A Policy objective Target audience Risk control matrix Checklist The policy and procedures outline the process for management

Policy Title Previous title (if any) Cash Transfers to Implementing Partners N/A Policy objective Target audience Risk control matrix Checklist The policy and procedures outline the process for management

UNITED NATIONS DEVELOPMENT PROGRAMME (UNDP) AUDIT REPORT. 31 July 2017 FINANCIAL AUDIT OF THE UNDP DIRECTLY IMPLEMENTED (DIM) PROJECT

AUDIT REPORT. 31 July 2017 FINANCIAL AUDIT OF THE UNDP DIRECTLY IMPLEMENTED (DIM) PROJECT") UNITED NATIONS DEVELOPMENT PROGRAMME (UNDP) AUDIT REPORT 31 July 2017 FINANCIAL AUDIT OF THE UNDP DIRECTLY IMPLEMENTED (DIM) PROJECT Sustainable Energy Activities UNDP Country Office: Lebanon Atlas Project

UNITED NATIONS DEVELOPMENT PROGRAMME (UNDP) AUDIT REPORT 31 July 2017 FINANCIAL AUDIT OF THE UNDP DIRECTLY IMPLEMENTED (DIM) PROJECT Sustainable Energy Activities UNDP Country Office: Lebanon Atlas Project

REPORT 2013/142. Audit of accounts receivable and payable in the United Nations Operation in Côte d Ivoire

INTERNAL AUDIT DIVISION REPORT 2013/142 Audit of accounts receivable and payable in the United Nations Operation in Côte d Ivoire Overall results relating to the effective management of accounts receivable

INTERNAL AUDIT DIVISION REPORT 2013/142 Audit of accounts receivable and payable in the United Nations Operation in Côte d Ivoire Overall results relating to the effective management of accounts receivable

AUDIT REPORT FINANCIAL STATEMENTS FOR 2016 SEE CHANGE NET FOUNDATION SARAJEVO

AUDIT REPORT FINANCIAL STATEMENTS FOR 2016 SEE CHANGE NET FOUNDATION SARAJEVO Sarajevo, June 2017. CONTENTS Page 1 DECLARATION OF FULL DISCLOSURE 3 2 INDEPENDENT AUDITOR'S OPINION 4 3 INTRODUCTION 5 4

AUDIT REPORT FINANCIAL STATEMENTS FOR 2016 SEE CHANGE NET FOUNDATION SARAJEVO Sarajevo, June 2017. CONTENTS Page 1 DECLARATION OF FULL DISCLOSURE 3 2 INDEPENDENT AUDITOR'S OPINION 4 3 INTRODUCTION 5 4

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT. 4 September 2015

FINANCIAL AUDIT REPORT. 4 September 2015") UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 4 September 2015 PROJECT NAME: SMALL GRANTS PROGRAMME (SGP) OPERATIONAL PHASE 5 PROJECT NUMBER: 00078647 COUNTRY: ARMENIA AUDITOR:

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 4 September 2015 PROJECT NAME: SMALL GRANTS PROGRAMME (SGP) OPERATIONAL PHASE 5 PROJECT NUMBER: 00078647 COUNTRY: ARMENIA AUDITOR:

AUDIT UNDP PROGRAMME OF ASSISTANCE TO THE PALESTINIAN PEOPLE. PROCUREMENT OF DRUGS TO GAZA (Directly Implemented Project No , Output No.

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP PROGRAMME OF ASSISTANCE TO THE PALESTINIAN PEOPLE PROCUREMENT OF DRUGS TO GAZA (Directly Implemented Project No. 74904,

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP PROGRAMME OF ASSISTANCE TO THE PALESTINIAN PEOPLE PROCUREMENT OF DRUGS TO GAZA (Directly Implemented Project No. 74904,

AUDIT UNDP SIERRA LEONE. Support to the Electoral Cycle in Sierra Leone (Directly Implemented Project, Output No )

") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP SIERRA LEONE (Directly Implemented Project, Output No. 77588) Report No. 1326 Issue Date: 26 June 2014 United Nations

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP SIERRA LEONE (Directly Implemented Project, Output No. 77588) Report No. 1326 Issue Date: 26 June 2014 United Nations

STATEMENT OF WORK FOR RECIPIENT CONTRACTED AUDIT OF USAID RESOURCES MANAGED BY THE WEST AFRICAN HEALTH ORGANIZATION (WAHO)

") STATEMENT OF WORK FOR RECIPIENT CONTRACTED AUDIT OF USAID RESOURCES MANAGED BY THE WEST AFRICAN HEALTH ORGANIZATION (WAHO) AUDIT OF USAID RESOURCES MANAGED BY WEST AFRICAN HEALTH ORGANIZATION UNDER THE

STATEMENT OF WORK FOR RECIPIENT CONTRACTED AUDIT OF USAID RESOURCES MANAGED BY THE WEST AFRICAN HEALTH ORGANIZATION (WAHO) AUDIT OF USAID RESOURCES MANAGED BY WEST AFRICAN HEALTH ORGANIZATION UNDER THE

AUDIT UNDP PROGRAMME OF ASSISTANCE TO THE PALESTINIAN PEOPLE

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP PROGRAMME OF ASSISTANCE TO THE PALESTINIAN PEOPLE COMMUNITY RESILIENCE AND DEVELOPMENT PROGRAMME (Directly Implemented

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP PROGRAMME OF ASSISTANCE TO THE PALESTINIAN PEOPLE COMMUNITY RESILIENCE AND DEVELOPMENT PROGRAMME (Directly Implemented

Atlas Financial Closure Instructions

Atlas Financial Closure Instructions 1. Atlas Financial Closure Instructions refers to the process of completing the input of all accounting entries to the UNDP general ledger. This includes the recording

Atlas Financial Closure Instructions 1. Atlas Financial Closure Instructions refers to the process of completing the input of all accounting entries to the UNDP general ledger. This includes the recording

AUDIT UNDP EGYPT. STRENGTHENING OF THE DEMOCRATIC PROCESS IN EGYPT (Directly Implemented Project No )

") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP EGYPT STRENGTHENING OF THE DEMOCRATIC PROCESS IN EGYPT (Directly Implemented Project No. 79914) Report No. 1253 Issue

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP EGYPT STRENGTHENING OF THE DEMOCRATIC PROCESS IN EGYPT (Directly Implemented Project No. 79914) Report No. 1253 Issue

AUDIT UNDP COUNTRY OFFICE BANGLADESH. Report No Issue Date: 28 May 2015

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN BANGLADESH Report No. 1429 Issue Date: 28 May 2015 Table of Contents Executive Summary i I. About the Office 1 II. Good practice 1 III.

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN BANGLADESH Report No. 1429 Issue Date: 28 May 2015 Table of Contents Executive Summary i I. About the Office 1 II. Good practice 1 III.

United Nations Development Programme (UNDP)

") United Nations Development Programme (UNDP) Report of the Independent Auditor on the United Nations Development Program (UNDP) Directly Implemented (DIM) Project ID 78266 Output ID 88627 Restauration de

United Nations Development Programme (UNDP) Report of the Independent Auditor on the United Nations Development Program (UNDP) Directly Implemented (DIM) Project ID 78266 Output ID 88627 Restauration de

Welcome to this course on Expense Management under IPSAS 1.

Course Name: IPSAS Expense Management - Beginners Page 1 Course Introduction Welcome to this course on Expense Management under IPSAS 1. This course is organised into fourteen independent units, with each

Course Name: IPSAS Expense Management - Beginners Page 1 Course Introduction Welcome to this course on Expense Management under IPSAS 1. This course is organised into fourteen independent units, with each

STANDARD STATEMENT OF WORK FOR FINANCIAL AUDITS OF NON-U.S. ORGANIZATIONS CONTRACTED BY THE RECIPIENT

STANDARD STATEMENT OF WORK FOR FINANCIAL AUDITS OF NON-U.S. ORGANIZATIONS CONTRACTED BY THE RECIPIENT OBJECTIVES AND GENERAL STATEMENT OF WORK AUDIT OF USAID RESOURCES MANAGED BY Dairy & Rural Development

STANDARD STATEMENT OF WORK FOR FINANCIAL AUDITS OF NON-U.S. ORGANIZATIONS CONTRACTED BY THE RECIPIENT OBJECTIVES AND GENERAL STATEMENT OF WORK AUDIT OF USAID RESOURCES MANAGED BY Dairy & Rural Development

REPORT 2015/072 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/072 Audit of minimum operating residential security standards entitlements for staff in the United Nations Operation in Côte d Ivoire Overall results relating to the

INTERNAL AUDIT DIVISION REPORT 2015/072 Audit of minimum operating residential security standards entitlements for staff in the United Nations Operation in Côte d Ivoire Overall results relating to the

Spencer CPA & Associates, P.L.L.C.

Spencer CPA & Associates, P.L.L.C. PO Box 2560 74 East Main Street Buckhannon, WV 26201 Buckhannon, WV 26201 Phone: (304)472-1928 Fax: (304)472-1951 Member: American Institute of Certified Public Accountants

Spencer CPA & Associates, P.L.L.C. PO Box 2560 74 East Main Street Buckhannon, WV 26201 Buckhannon, WV 26201 Phone: (304)472-1928 Fax: (304)472-1951 Member: American Institute of Certified Public Accountants

WISCONSIN HOUSING AND ECONOMIC DEVELOPMENT AUTHORITY Low Income Housing Tax Credit (LIHTC) Program COST CERTIFICATION AUDIT GUIDE

Program COST CERTIFICATION AUDIT GUIDE") WISCONSIN HOUSING AND ECONOMIC DEVELOPMENT AUTHORITY Low Income Housing Tax Credit (LIHTC) Program COST CERTIFICATION AUDIT GUIDE REVISED NOVEMBER 13, 2007 BACKGROUND Owners of Projects consisting of more

WISCONSIN HOUSING AND ECONOMIC DEVELOPMENT AUTHORITY Low Income Housing Tax Credit (LIHTC) Program COST CERTIFICATION AUDIT GUIDE REVISED NOVEMBER 13, 2007 BACKGROUND Owners of Projects consisting of more

AUDIT UNDP COUNTRY OFFICE SOMALIA. Report No Issue Date: 20 June 2014

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN SOMALIA Report No. 1299 Issue Date: 20 June 2014 Table of Contents Executive Summary ii I. About the Office 1 II. Audit results 1 A.

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN SOMALIA Report No. 1299 Issue Date: 20 June 2014 Table of Contents Executive Summary ii I. About the Office 1 II. Audit results 1 A.

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT. 4 September 2015

FINANCIAL AUDIT REPORT. 4 September 2015") INTERNAL AUDIT AND INVESTIGATIONS GROUP UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 4 September 2015 PROJECT NAME: SMALL GRANTS PROGAMME (SGP) OPERATIONAL PHASE 5 PROJECT

INTERNAL AUDIT AND INVESTIGATIONS GROUP UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 4 September 2015 PROJECT NAME: SMALL GRANTS PROGAMME (SGP) OPERATIONAL PHASE 5 PROJECT

AUDIT UNDP UKRAINE. EU BORDER ASSISTANCE MISSION - 9 (Directly Implemented Project No ) Report No Issue Date: 9 December 2013

Report No Issue Date: 9 December 2013") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP UKRAINE EU BORDER ASSISTANCE MISSION - 9 (Directly Implemented Project No. 79895) Report No. 1199 Issue Date: 9 December

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP UKRAINE EU BORDER ASSISTANCE MISSION - 9 (Directly Implemented Project No. 79895) Report No. 1199 Issue Date: 9 December

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT. 20 September 2017

FINANCIAL AUDIT REPORT. 20 September 2017") UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 20 September 2017 PROJECT NAME: PALESTINIAN MATURITY PROGRAM PROJECT NUMBER: 96457 COUNTRY: ISRAEL AUDITOR: MOORE STEPHENS LLP

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 20 September 2017 PROJECT NAME: PALESTINIAN MATURITY PROGRAM PROJECT NUMBER: 96457 COUNTRY: ISRAEL AUDITOR: MOORE STEPHENS LLP

We will be acting as the accountants and business advisors for the following entities and individuals:

Letter of engagement On behalf of the directors and staff of Kendons Scott Macdonald Limited we would like to formally welcome you/thank you for your continued support as a client of our Firm. This letter

Letter of engagement On behalf of the directors and staff of Kendons Scott Macdonald Limited we would like to formally welcome you/thank you for your continued support as a client of our Firm. This letter

Regulation on the implementation of the European Economic Area (EEA) Financial Mechanism

Financial Mechanism") the European Economic Area (EEA) Financial Mechanism 2014-2021 Adopted by the EEA Financial Mechanism Committee pursuant to Article 10.5 of Protocol 38c to the EEA Agreement on 8 September 2016 and confirmed

the European Economic Area (EEA) Financial Mechanism 2014-2021 Adopted by the EEA Financial Mechanism Committee pursuant to Article 10.5 of Protocol 38c to the EEA Agreement on 8 September 2016 and confirmed

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT. 4 September 2015

FINANCIAL AUDIT REPORT. 4 September 2015") UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 4 September 2015 PROJECT NAME: SMALL GRANTS PROGAMME (SGP) OPERATIONAL PHASE 5 PROJECT NUMBER: 00078697 COUNTRY: CÔTE D'IVOIRE

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 4 September 2015 PROJECT NAME: SMALL GRANTS PROGAMME (SGP) OPERATIONAL PHASE 5 PROJECT NUMBER: 00078697 COUNTRY: CÔTE D'IVOIRE

OIC/GA-IOFS/2016/FIN.REG FINANCIAL REGULATIONS OF THE ISLAMIC ORGANIZATION FOR FOOD SECURITY

OIC/GA-IOFS/2016/FIN.REG FINANCIAL REGULATIONS OF THE ISLAMIC ORGANIZATION FOR FOOD SECURITY FINANCIAL REGULATIONS OF THE ISLAMIC ORGANISATION FOR FOOD SECURITY C O N T E N T S PAGE CHAPTER: I SCOPE AND

OIC/GA-IOFS/2016/FIN.REG FINANCIAL REGULATIONS OF THE ISLAMIC ORGANIZATION FOR FOOD SECURITY FINANCIAL REGULATIONS OF THE ISLAMIC ORGANISATION FOR FOOD SECURITY C O N T E N T S PAGE CHAPTER: I SCOPE AND

Presentation to the Financial Administrator Development Program MSU Financial Statements and External Audit

Presentation to the Financial Administrator Development Program MSU Financial Statements and External Audit October 30, 2012 Katie A. Thornton, Associate, Plante Moran Gregory J. Deppong, Controller, MSU

Presentation to the Financial Administrator Development Program MSU Financial Statements and External Audit October 30, 2012 Katie A. Thornton, Associate, Plante Moran Gregory J. Deppong, Controller, MSU

ENGAGEMENTS TO REVIEW FINANCIAL STATEMENTS (Effective for reviews of financial statements for periods beginning on or after April 1, 2010)

") SRE 2400* ENGAGEMENTS TO REVIEW FINANCIAL STATEMENTS (Effective for reviews of financial statements for periods beginning on or after April 1, 2010) Contents Paragraph(s) Introduction...1-2 Objective of

SRE 2400* ENGAGEMENTS TO REVIEW FINANCIAL STATEMENTS (Effective for reviews of financial statements for periods beginning on or after April 1, 2010) Contents Paragraph(s) Introduction...1-2 Objective of

United Nations Development Programme Cambodia Office

REQUEST FOR PROPOSAL TO SELECT AUDIT FIRM FOR AUDIT OF NEX OR NGO PROJECTS United Nations Development Programme Cambodia Office NOTE: WHEN SUBMITTING YOUR BID DOCUMENTS, PLEASE CAREFULLY PLACE THE TECHNICAL

REQUEST FOR PROPOSAL TO SELECT AUDIT FIRM FOR AUDIT OF NEX OR NGO PROJECTS United Nations Development Programme Cambodia Office NOTE: WHEN SUBMITTING YOUR BID DOCUMENTS, PLEASE CAREFULLY PLACE THE TECHNICAL

VILLAGE OF ROME ADAMS COUNTY TABLE OF CONTENTS. Independent Auditor s Report... 1

VILLAGE OF ROME ADAMS COUNTY TABLE OF CONTENTS TITLE PAGE Independent Auditor s Report... 1 Combined Statement of Receipts, Disbursements, and Changes in Fund Balances (Cash Basis) - All Governmental Fund

VILLAGE OF ROME ADAMS COUNTY TABLE OF CONTENTS TITLE PAGE Independent Auditor s Report... 1 Combined Statement of Receipts, Disbursements, and Changes in Fund Balances (Cash Basis) - All Governmental Fund

United Nations Development Programme Office of Audit and Investigations TERMS OF REFERENCE FOR AUDITS OF NGO AND NIM PROJECTS

United Nations Development Programme Office of Audit and Investigations TERMS OF REFERENCE FOR AUDITS OF NGO AND NIM PROJECTS TABLE OF CONTENTS Page REQUEST FOR QUOTATION (RFQ)... 4 TERMS OF REFERENCE...

United Nations Development Programme Office of Audit and Investigations TERMS OF REFERENCE FOR AUDITS OF NGO AND NIM PROJECTS TABLE OF CONTENTS Page REQUEST FOR QUOTATION (RFQ)... 4 TERMS OF REFERENCE...

A8.900 ACCOUNTING FOR RESEARCH & TRAINING CONTRACTS & GRANTS. A8.930 Services with the Research Corporation of the University of Hawai i

Prepared by Contracts and Grants Management Office. This replaces Administrative Procedure No. A8.930 dated July 1993. A8.930 August 1993 A8.900 ACCOUNTING FOR RESEARCH & TRAINING CONTRACTS & GRANTS P

Prepared by Contracts and Grants Management Office. This replaces Administrative Procedure No. A8.930 dated July 1993. A8.930 August 1993 A8.900 ACCOUNTING FOR RESEARCH & TRAINING CONTRACTS & GRANTS P

MSU Financial Statements and External Audit

Presentation to the Financial Administrator Development Program MSU Financial Statements and External Audit What s Your Role? October 28, 2014 Katie A. Thornton, Senior Manager, Plante Moran Gregory J.

Presentation to the Financial Administrator Development Program MSU Financial Statements and External Audit What s Your Role? October 28, 2014 Katie A. Thornton, Senior Manager, Plante Moran Gregory J.

GUIDELINES ON WHOLESALE FUNDS

GUIDELINES ON WHOLESALE FUNDS Issued by: Securities Commission Effective Date: 18 February 2009 CONTENTS 1.0 APPLICATION OF GUIDELINES 1 2.0 DEFINITIONS 1 3.0 ROLE AND DUTIES OF THE FUND MANAGER 6 4.0

GUIDELINES ON WHOLESALE FUNDS Issued by: Securities Commission Effective Date: 18 February 2009 CONTENTS 1.0 APPLICATION OF GUIDELINES 1 2.0 DEFINITIONS 1 3.0 ROLE AND DUTIES OF THE FUND MANAGER 6 4.0

STANDARD STATEMENT OF WORK FOR FINANCIAL AUDITS OF NON-U.S. ORGANIZATIONS CONTRACTED BY THE RECIPIENT

Page 1 STANDARD STATEMENT OF WORK FOR FINANCIAL AUDITS OF NON-U.S. ORGANIZATIONS CONTRACTED BY THE RECIPIENT OBJECTIVES AND GENERAL STATEMENT OF WORK AUDIT OF USAID RESOURCES MANAGED BY SINDH RURAL SUPPORT

Page 1 STANDARD STATEMENT OF WORK FOR FINANCIAL AUDITS OF NON-U.S. ORGANIZATIONS CONTRACTED BY THE RECIPIENT OBJECTIVES AND GENERAL STATEMENT OF WORK AUDIT OF USAID RESOURCES MANAGED BY SINDH RURAL SUPPORT

United Nations Development Group (UNDG)

") United Nations Development Group (UNDG) Proposed Revisions to the Harmonized Approach to Cash Transfers (HACT) Framework Audit & Assurance APPENDICES 17 September 2013 kpmg.com Contents Appendix 1 Listing

United Nations Development Group (UNDG) Proposed Revisions to the Harmonized Approach to Cash Transfers (HACT) Framework Audit & Assurance APPENDICES 17 September 2013 kpmg.com Contents Appendix 1 Listing

Rural Renewable Energy Agency (RREA) Financial Audit Report. for the period from 1 March 2016 to 30 June Project ID: P

Financial Audit Report. for the period from 1 March 2016 to 30 June Project ID: P") Public Disclosure Authorized Public Disclosure Authorized Rural Renewable Energy Agency (RREA) Financial Audit Report for the period from 1 March 2016 to 30 June 2017 Public Disclosure Authorized Liberia

Public Disclosure Authorized Public Disclosure Authorized Rural Renewable Energy Agency (RREA) Financial Audit Report for the period from 1 March 2016 to 30 June 2017 Public Disclosure Authorized Liberia

Improving the Accuracy of Defense Finance and Accounting Service Columbus 741 and 743 Accounts Payable Reports

Report No. D-2011-022 December 10, 2010 Improving the Accuracy of Defense Finance and Accounting Service Columbus 741 and 743 Accounts Payable Reports Report Documentation Page Form Approved OMB No. 0704-0188

Report No. D-2011-022 December 10, 2010 Improving the Accuracy of Defense Finance and Accounting Service Columbus 741 and 743 Accounts Payable Reports Report Documentation Page Form Approved OMB No. 0704-0188

HOUSING AUTHORITY OF THE CITY OF WESTWEGO, LOUISIANA INDEPENDENT AUDITOR'S REPORT YEAR ENDED JUNE 30, 2005

RECEIVED i r: p sr;.*. r\\i r '. t im Tr.p ' '.1, ' -!!., '. -.;, v S f ^ n 06JUN-5 AH 10:51 HOUSING AUTHORITY OF THE CITY OF WESTWEGO, LOUISIANA INDEPENDENT AUDITOR'S REPORT YEAR ENDED JUNE 30, 2005 Under

RECEIVED i r: p sr;.*. r\\i r '. t im Tr.p ' '.1, ' -!!., '. -.;, v S f ^ n 06JUN-5 AH 10:51 HOUSING AUTHORITY OF THE CITY OF WESTWEGO, LOUISIANA INDEPENDENT AUDITOR'S REPORT YEAR ENDED JUNE 30, 2005 Under

Spencer CPA & Associates, P.L.L.C.

Spencer CPA & Associates, P.L.L.C. PO Box 2560 74 East Main Street Buckhannon, WV 26201 Buckhannon, WV 26201 Phone: (304)472-1928 Fax: (304)472-1951 Member: American Institute of Certified Public Accountants

Spencer CPA & Associates, P.L.L.C. PO Box 2560 74 East Main Street Buckhannon, WV 26201 Buckhannon, WV 26201 Phone: (304)472-1928 Fax: (304)472-1951 Member: American Institute of Certified Public Accountants

AUDIT UNDP CYPRUS. SUPPORT TO COMMITTEE ON MISSING PERSONS (Directly Implemented Project, Output No ) Report No Issue Date: 26 June 2014

Report No Issue Date: 26 June 2014") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP CYPRUS SUPPORT TO COMMITTEE ON MISSING PERSONS (Directly Implemented Project, Output No. 84969) Report No. 1361 Issue

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP CYPRUS SUPPORT TO COMMITTEE ON MISSING PERSONS (Directly Implemented Project, Output No. 84969) Report No. 1361 Issue

or institution which in turn is a member of the International Federation of Accountants (IFAC).

.") Terms of Reference for an Expenditure Verification of a Grant Contract for Estonia - Latvia- Russia Cross Border Cooperation Programme within the European Neighbourhood and Partnership Instrument 2007-2013

Terms of Reference for an Expenditure Verification of a Grant Contract for Estonia - Latvia- Russia Cross Border Cooperation Programme within the European Neighbourhood and Partnership Instrument 2007-2013

Recommendation: Management should review their year-end procedures for recording assets and liabilities.

Rushton ACCOUNTING & BUSINESS ADVISORS CERTIFIED PUBLIC ACCOUNTANTS Honorable Chairman and Members of the Board of Commissioners Fannin County, Georgia In planning and performing our audit of the financial

Rushton ACCOUNTING & BUSINESS ADVISORS CERTIFIED PUBLIC ACCOUNTANTS Honorable Chairman and Members of the Board of Commissioners Fannin County, Georgia In planning and performing our audit of the financial

Piotr Pyziak, Consultant, CFRR

Piotr Pyziak, Consultant, CFRR 16 March 2017, Vienna Audit Training of Trainers Road to Europe: Program of Accounting Reform and Institutional Strengthening EU-REPARIS is funded by the European Union and

Piotr Pyziak, Consultant, CFRR 16 March 2017, Vienna Audit Training of Trainers Road to Europe: Program of Accounting Reform and Institutional Strengthening EU-REPARIS is funded by the European Union and

Campus Financial Sub-Certification - Explanation

Campus Financial Sub-Certification - Explanation 1. Within the areas for which I am responsible, all transactions, agreements and amounts have been properly reflected in the University s accounting records.

Campus Financial Sub-Certification - Explanation 1. Within the areas for which I am responsible, all transactions, agreements and amounts have been properly reflected in the University s accounting records.

GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings. September 30, 2001 and 2000

Schedule of Findings. September 30, 2001 and 2000") GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings CURRENT YEAR (2001) FINDINGS Finding No. 2001-1 Verification of Disability Annuitants 4GCA, Chapter 8, Article 1, 8127(a)

GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings CURRENT YEAR (2001) FINDINGS Finding No. 2001-1 Verification of Disability Annuitants 4GCA, Chapter 8, Article 1, 8127(a)

AUDIT UNDP COUNTRY OFFICE UGANDA. Report No Issue Date: 22 August 2013

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN UGANDA Report No. 1155 Issue Date: 22 August 2013 Table of Contents Executive Summary i I. Introduction 1 II. About the Office 1 III.

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN UGANDA Report No. 1155 Issue Date: 22 August 2013 Table of Contents Executive Summary i I. Introduction 1 II. About the Office 1 III.

LANE TRANSIT DISTRICT EUGENE, OREGON AUDIT OF FEDERAL AWARDS

LANE TRANSIT DISTRICT EUGENE, OREGON AUDIT OF FEDERAL AWARDS Fiscal Year Ended June 30, 2017 LANE TRANSIT DISTRICT, OREGON TABLE OF CONTENTS Page Report of Independent Auditors on Internal Control over

LANE TRANSIT DISTRICT EUGENE, OREGON AUDIT OF FEDERAL AWARDS Fiscal Year Ended June 30, 2017 LANE TRANSIT DISTRICT, OREGON TABLE OF CONTENTS Page Report of Independent Auditors on Internal Control over

Fin-621 Final term Solved Papers by Fahad Yusha Cell: and

FINALTERM EXAMINATION Spring 2010 FIN621- Financial Statement Analysis (Session - 1) : 90 min Marks: 69 Question No: 1 ( Marks: 1 ) - Please choose one Which one of the following is NOT a type of adjusting

FINALTERM EXAMINATION Spring 2010 FIN621- Financial Statement Analysis (Session - 1) : 90 min Marks: 69 Question No: 1 ( Marks: 1 ) - Please choose one Which one of the following is NOT a type of adjusting

OFFICE OF THE INSPECTOR GENERAL DEFENSE FINANCE AND ACCOUNTING SERVICE WORK ON THE ARMY FY 1993 FINANCIAL STATEMENTS

^>^^^;v^^^x*^^^^^^^>>kä+^>mw^^>.^^^w^^^m'>m'!, x : OFFICE OF THE INSPECTOR GENERAL DEFENSE FINANCE AND ACCOUNTING SERVICE WORK ON THE ARMY FY 1993 FINANCIAL STATEMENTS» Report No. 94-168 July 6, 1994 :

^>^^^;v^^^x*^^^^^^^>>kä+^>mw^^>.^^^w^^^m'>m'!, x : OFFICE OF THE INSPECTOR GENERAL DEFENSE FINANCE AND ACCOUNTING SERVICE WORK ON THE ARMY FY 1993 FINANCIAL STATEMENTS» Report No. 94-168 July 6, 1994 :

UN-Habitat Policy For Implementing Partners. UN-Habitat. Policy For. Partners

UN-Habitat Policy For Implementing Partners 01 Version Date Author/Reviewer Status V1 06.12.2016 Mohamed Robleh Circulated for SMB comments V2 27.01.2017 Andrew Cox Approved For further information, please

UN-Habitat Policy For Implementing Partners 01 Version Date Author/Reviewer Status V1 06.12.2016 Mohamed Robleh Circulated for SMB comments V2 27.01.2017 Andrew Cox Approved For further information, please

Aljunied- Hougang Town Council

Aljunied- Hougang Town Council KPMG LLP This report contains 18 pages 2017 KPMG LLP (Registration No: T08LL1267L), an accounting limited liability partnership registered in Singapore under the Limited

Aljunied- Hougang Town Council KPMG LLP This report contains 18 pages 2017 KPMG LLP (Registration No: T08LL1267L), an accounting limited liability partnership registered in Singapore under the Limited

Professional Bridging Examination. Paper III PBE Auditing and Information Systems

Professional Bridging Examination Pilot Examination Paper Paper III PBE Auditing and Information Systems Questions & Answers Booklet The suggested answers given in this booklet are purposely made to give

Professional Bridging Examination Pilot Examination Paper Paper III PBE Auditing and Information Systems Questions & Answers Booklet The suggested answers given in this booklet are purposely made to give

THE UNITED REPUBLIC OF TANZANIA NATIONAL AUDIT OFFICE (NAO)

") THE UNITED REPUBLIC OF TANZANIA NATIONAL AUDIT OFFICE (NAO) REPORT OF THE CONTROLLER AND AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF THE HIGH COURT COMMERCIAL COURT DIVISION FOR THE YEAR ENDED 30 TH

THE UNITED REPUBLIC OF TANZANIA NATIONAL AUDIT OFFICE (NAO) REPORT OF THE CONTROLLER AND AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF THE HIGH COURT COMMERCIAL COURT DIVISION FOR THE YEAR ENDED 30 TH

SIGAR JULY. Special Inspector General for Afghanistan Reconstruction

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR Financial Audit 13-6 USDA s Program to Help Advance the Revitalization of Afghanistan s Agricultural Sector: Audit of Costs Incurred

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR Financial Audit 13-6 USDA s Program to Help Advance the Revitalization of Afghanistan s Agricultural Sector: Audit of Costs Incurred

Minneapolis Public Schools Special District No. 1. Reports on Government Auditing Standards, Uniform Guidance and Legal Compliance.

Reports on Government Auditing Standards, Uniform Guidance and Legal Compliance June 30, 2016 Table of Contents Schedule of Expenditures of Federal Awards 1 Notes to the Schedule of Expenditures of Federal

Reports on Government Auditing Standards, Uniform Guidance and Legal Compliance June 30, 2016 Table of Contents Schedule of Expenditures of Federal Awards 1 Notes to the Schedule of Expenditures of Federal

Aljunied- Hougang Town Council

Aljunied- Hougang Town Council KPMG LLP This report contains 18 pages 2018 KPMG LLP (Registration No: T08LL1267L), an accounting limited liability partnership registered in Singapore under the Limited

Aljunied- Hougang Town Council KPMG LLP This report contains 18 pages 2018 KPMG LLP (Registration No: T08LL1267L), an accounting limited liability partnership registered in Singapore under the Limited

EUROPEAN COMMISSION DG Regional Policy DG Employment, Social Affairs and Equal Opportunities

Final version of 07/12/2011 EUROPEAN COMMISSION DG Regional Policy DG Employment, Social Affairs and Equal Opportunities COCOF_11-0041-01-EN GUIDANCE ON TREATMENT OF ERRORS DISCLOSED IN THE ANNUAL CONTROL

Final version of 07/12/2011 EUROPEAN COMMISSION DG Regional Policy DG Employment, Social Affairs and Equal Opportunities COCOF_11-0041-01-EN GUIDANCE ON TREATMENT OF ERRORS DISCLOSED IN THE ANNUAL CONTROL

ANNEX A - I. Note: it is important that each tenderer has read the Working Practice and its annexes very carefully.

ANNEX A - I Note: it is important that each tenderer has read the Working Practice and its annexes very carefully. WORKING PRACTICE 1.GENERAL INFORMATION 1.1.THE AUDIT CO-ORDINATOR 1.1.1.The Audit Co-ordinator

ANNEX A - I Note: it is important that each tenderer has read the Working Practice and its annexes very carefully. WORKING PRACTICE 1.GENERAL INFORMATION 1.1.THE AUDIT CO-ORDINATOR 1.1.1.The Audit Co-ordinator

REPORT OF THE AUDIT OF THE BREATHITT COUNTY SHERIFF

REPORT OF THE AUDIT OF THE BREATHITT COUNTY SHERIFF For The Year Ended December 31, 2007 CRIT LUALLEN AUDITOR OF PUBLIC ACCOUNTS www.auditor.ky.gov 105 SEA HERO ROAD, SUITE 2 FRANKFORT, KY 40601-5404 TELEPHONE

REPORT OF THE AUDIT OF THE BREATHITT COUNTY SHERIFF For The Year Ended December 31, 2007 CRIT LUALLEN AUDITOR OF PUBLIC ACCOUNTS www.auditor.ky.gov 105 SEA HERO ROAD, SUITE 2 FRANKFORT, KY 40601-5404 TELEPHONE

INDEPENDENT AUDITOR S REPORT

INDEPENDENT AUDITOR S REPORT To The Members of Report on the Financial Statements We have audited the accompanying standalone financial statements of ( the Company ), which comprise the Balance Sheet as

INDEPENDENT AUDITOR S REPORT To The Members of Report on the Financial Statements We have audited the accompanying standalone financial statements of ( the Company ), which comprise the Balance Sheet as

Strategic report. Corporate governance. Financial statements. Financial statements

Strategic report Corporate governance Financial statements 76 Statement of Directors responsibilities 77 Independent auditor s report to the members of Tesco PLC 85 Group income statement 86 Group statement

Strategic report Corporate governance Financial statements 76 Statement of Directors responsibilities 77 Independent auditor s report to the members of Tesco PLC 85 Group income statement 86 Group statement

AUDIT UNDP AFGHANISTAN. Local Governance Project (Project No ) Report No Issue Date: 23 December 2016

Report No Issue Date: 23 December 2016") UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP AFGHANISTAN Local Governance Project (Project No. 90448) Report No. 1745 Issue Date: 23 December 2016 Table of Contents Executive Summary i I. About the

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP AFGHANISTAN Local Governance Project (Project No. 90448) Report No. 1745 Issue Date: 23 December 2016 Table of Contents Executive Summary i I. About the

Reports Required in Accordance with Office of Management and Budget Circular A-133

Financial Statements (With Summarized Financial Information for the Year Ended December 31, 2010) and Report Thereon Reports Required in Accordance with Office of Management and Budget Circular A-133 TABLE

Financial Statements (With Summarized Financial Information for the Year Ended December 31, 2010) and Report Thereon Reports Required in Accordance with Office of Management and Budget Circular A-133 TABLE

Financial Audit Procedures

Annex 1. Financial Audit Procedures 1.1 Audit Documentation and Evidence 1.1.1 Audit Documentation (Working Papers) The Auditor should, in accordance with ISA 230, prepare audit documentation that provides:

Annex 1. Financial Audit Procedures 1.1 Audit Documentation and Evidence 1.1.1 Audit Documentation (Working Papers) The Auditor should, in accordance with ISA 230, prepare audit documentation that provides:

Internal Audit of the Lao People s Democratic Republic Country Office

Internal Audit of the Lao People s Democratic Republic Country Office March 2013 Office of Internal Audit and Investigations (OIAI) Report 2013/04 Audit of the Lao People s Democratic Republic Country

Internal Audit of the Lao People s Democratic Republic Country Office March 2013 Office of Internal Audit and Investigations (OIAI) Report 2013/04 Audit of the Lao People s Democratic Republic Country

TEXOMA AREA PARATRANSIT SYSTEM, INC. AUDITED FINANCIAL STATEMENTS Year Ended September 30, 2014

TEXOMA AREA PARATRANSIT SYSTEM, INC. AUDITED FINANCIAL STATEMENTS Year Ended September 30, 2014 TABLE OF CONTENTS September 30, 2014 PAGE INDEPENDENT AUDITOR S REPORT... 1 STATEMENT OF NET POSITION...

TEXOMA AREA PARATRANSIT SYSTEM, INC. AUDITED FINANCIAL STATEMENTS Year Ended September 30, 2014 TABLE OF CONTENTS September 30, 2014 PAGE INDEPENDENT AUDITOR S REPORT... 1 STATEMENT OF NET POSITION...

kpmg CAMBODIAN RURAL DEVELOPMENT TEAM ( CRDT ) Management Letter for the year ended 31 December 2015

Management Letter for the year ended 31 December 2015") CAMBODIAN RURAL DEVELOPMENT TEAM ( CRDT ) Contents Page 1. Develop a comparison between budget and actual expenses 1 2. Improve control over non-expandable equipment 2 3. Improve control over cost sharing

CAMBODIAN RURAL DEVELOPMENT TEAM ( CRDT ) Contents Page 1. Develop a comparison between budget and actual expenses 1 2. Improve control over non-expandable equipment 2 3. Improve control over cost sharing

(h) (i) (J) (k) (l) (m) (n) (o) (p) (q) (r) (s) "Regular revenue" means the revenue collected and recovered as per the records maintained in the office. "Irregular revenue" means the revenue to be received

(h) (i) (J) (k) (l) (m) (n) (o) (p) (q) (r) (s) "Regular revenue" means the revenue collected and recovered as per the records maintained in the office. "Irregular revenue" means the revenue to be received

World Bank HIV/AIDS Program

blic Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized World Bank HIV/AIDS Program A Guidance Note on Disbursement Procedures This document was

blic Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized World Bank HIV/AIDS Program A Guidance Note on Disbursement Procedures This document was

Report of the Public Accounts Committee on the: Report of the Auditor General on the Financial Statement Audit of the Tuvalu Whole of Government for

Report of the Public Accounts Committee on the: Report of the Auditor General on the Financial Statement Audit of the Tuvalu Whole of Government for the years ended 31 December 2009, 31 December 2010 and

Report of the Public Accounts Committee on the: Report of the Auditor General on the Financial Statement Audit of the Tuvalu Whole of Government for the years ended 31 December 2009, 31 December 2010 and

Audit Report Internal Financial Controls. GF-OIG March 2015 Geneva, Switzerland

Audit Report Internal Financial Controls GF-OIG-15-005 Table of Contents I. Background... 2 II. Scope and Rating... 3 III. Executive Summary... 4 IV. Findings and agreed actions... 6 V. Table of Agreed

Audit Report Internal Financial Controls GF-OIG-15-005 Table of Contents I. Background... 2 II. Scope and Rating... 3 III. Executive Summary... 4 IV. Findings and agreed actions... 6 V. Table of Agreed

Results of operation: (in thousand pesos)

") AUDIT OBSERVATIONS AND RECOMMENDATIONS 1. Concerns on PPI s financial position PPI s financial position and results of operation for CY 2014 shows its inability to meet its liabilities and finance its

AUDIT OBSERVATIONS AND RECOMMENDATIONS 1. Concerns on PPI s financial position PPI s financial position and results of operation for CY 2014 shows its inability to meet its liabilities and finance its

South Sudan Common Humanitarian Fund (South Sudan CHF) Terms of Reference (TOR)

Terms of Reference (TOR)") South Sudan Common Humanitarian Fund (South Sudan CHF) Terms of Reference (TOR) 14 February 2012 List of Acronyms AA Administrative Agent AB Advisory Board CAP Consolidated Appeal Process CHF Common Humanitarian

South Sudan Common Humanitarian Fund (South Sudan CHF) Terms of Reference (TOR) 14 February 2012 List of Acronyms AA Administrative Agent AB Advisory Board CAP Consolidated Appeal Process CHF Common Humanitarian

Stock Audit of Bank Borrowers CA Pranjal Joshi

Stock Audit of Bank Borrowers CA Pranjal Joshi Introduction Working capital finance in the form of cash credit against the security of hypothecation of stock and debtors is one of the most common modes

Stock Audit of Bank Borrowers CA Pranjal Joshi Introduction Working capital finance in the form of cash credit against the security of hypothecation of stock and debtors is one of the most common modes

ECCLESIA, INC. D/B/A ECCLESIA COLLEGE AUDITED FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION FOR THE YEARS ENDED MAY 31, 2016 AND 2015

EIN NUMBER: XX-XXX5244 OPE ID NUMBER: 03076300 DUNS NUMBER: 072470958 ECCLESIA, INC. AUDITED FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION FOR THE YEARS ENDED MAY 31, 2016 AND 2015 R. Michael LaBounty

EIN NUMBER: XX-XXX5244 OPE ID NUMBER: 03076300 DUNS NUMBER: 072470958 ECCLESIA, INC. AUDITED FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION FOR THE YEARS ENDED MAY 31, 2016 AND 2015 R. Michael LaBounty

DuPage County, Illinois

DuPage County, Illinois Report on Internal Controls November 30, 2014 DUPAGE COUNTY, ILLINOIS TABLE OF CONTENTS Auditor s Letter 1-2 County Board Comments Material Weakness Finance Department Accounting

DuPage County, Illinois Report on Internal Controls November 30, 2014 DUPAGE COUNTY, ILLINOIS TABLE OF CONTENTS Auditor s Letter 1-2 County Board Comments Material Weakness Finance Department Accounting

Department of Defense

OFFICE OF THE INSPECTOR GENERAL DEFENSE BUSINESS OPERATIONS FUND- COMMUNICATION INFORMATION SERVICES ACTIVITY FINANCIAL STATEMENTS FOR FY 1992 Report No. 93-153 August 6, 1993 r, r w >TT > T < T >>» T

OFFICE OF THE INSPECTOR GENERAL DEFENSE BUSINESS OPERATIONS FUND- COMMUNICATION INFORMATION SERVICES ACTIVITY FINANCIAL STATEMENTS FOR FY 1992 Report No. 93-153 August 6, 1993 r, r w >TT > T < T >>» T

FINANCIAL STATEMENTS 2018

FINANCIAL STATEMENTS 2018 CONTENTS 2 Auditor s Report 7 Directors Responsibility Statement 8 Statement of Comprehensive Income 9 Statement of Financial Position 10 Statement of Changes in Equity 11 Statement

FINANCIAL STATEMENTS 2018 CONTENTS 2 Auditor s Report 7 Directors Responsibility Statement 8 Statement of Comprehensive Income 9 Statement of Financial Position 10 Statement of Changes in Equity 11 Statement

EARLY LEARNING COALITION OF NORTHWEST FLORIDA, INC. Financial Statements and Independent Auditor's Report. June 30, 2010 and 2009

EARLY LEARNING COALITION OF NORTHWEST FLORIDA, INC. Financial Statements and Independent Auditor's Report June 30, 2010 and 2009 EARLY LEARNING COALITION OF NORTHWEST FLORIDA, INC. Financial Statements

EARLY LEARNING COALITION OF NORTHWEST FLORIDA, INC. Financial Statements and Independent Auditor's Report June 30, 2010 and 2009 EARLY LEARNING COALITION OF NORTHWEST FLORIDA, INC. Financial Statements

To the Honorable Mayor and Members of the City Council of the City of San Diego, California: