AUDIT UNDP DOMINICAN REPUBLIC

|

|

|

- Margaret Thomas

- 6 years ago

- Views:

Transcription

Report No.")

1 UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP DOMINICAN REPUBLIC DESARROLLO LOCAL TRANSFRONTERIZO EN ACOMPAÑAMIENTO AL PROGRAMA BINACIONAL (Directly Implemented Project, Output No ) Report No Issue Date: 17 September 2014

2 United Nations Development Programme Office of Audit and Investigations Report on the audit of UNDP Dominican Republic Desarrollo Local Transfronterizo en Acompañamiento al Programa Binacional (Output No ) Executive Summary The UNDP Office of Audit and Investigations (OAI), from 16 June to 4 July 2014, through Moore Stephens LLP (the audit firm), conducted an audit of Desarrollo Local Transfronterizo en Acompañamiento al Programa Binacional, Output No (the Project), which is directly implemented and managed by the UNDP Country Office in Dominican Republic (the Office). This was the first audit of the Project. The audit firm conducted a financial audit to express an opinion on whether the financial statements present fairly, in all material aspects, the Project s operations. The audit covered the Project s Combined Delivery Report, which includes expenditure for the period from 1 January 2012 to 31 December 2013 and the accompanying Funds Utilization statement 1 as of 31 December 2013 as well as Statement of Assets as of 31 December The audit did not cover the Statement of Cash Position as no separate bank account was established and maintained for the Project. The audit was conducted under the general supervision of OAI in conformance with the International Standards for the Professional Practice of Internal Auditing. Audit results Based on the audit report and corresponding management letter submitted by the audit firm, the results are summarized in the table below: Amount (in $ 000) Project Expenditure Opinion NFI* (in $ 000) Amount (in $ 000) Project Assets Opinion NFI (in $ 000) 849 Qualified Unqualified - *NFI = Net Financial Impact The audit firm qualified its opinion on project expenditure due to financial findings totalling $ 45,000 which represent amounts that were either (i) not in conformity with the approved budget, (ii) not for the approved purposes of the project, (iii) not in compliance with the relevant regulations and rules or (iv) not supported by properly approved vouchers and other supporting documents. Key recommendations: Total = 4, high priority = 1 For high (critical) priority recommendations, prompt action is required to ensure that UNDP is not exposed to high risks. Failure to take action could result in major negative consequences for UNDP. The high (critical) priority recommendation is presented below: 1 The Funds Utilization statement includes the balance, as at a given date, of five items: (a) outstanding advances received by the project; (b) depreciated fixed assets used at the project level; (c) inventory held at the project level; (d) prepayments made by the project; and (e) outstanding commitments held at the project level. Audit Report No. 1355, 17 September 2014: UNDP Dominican Republic, DIM Output No Page i

3

4 UNITED NATIONS DEVELOPMENT PROGRAMME (UNDP) AUDIT REPORT 8 September 2014 FINANCIAL AUDIT OF THE UNDP DIRECTLY IMPLEMENTED (DIM) PROJECT DESARROLLO LOCAL TRANSFRONTERIZO EN ACOMPAÑAMIENTO AL PROGRAMA BINACIONAL Project name: UNDP Country Office: Desarrollo local transfronterizo en acompañamiento al programa binacional Dominican Republic Atlas Project number: Atlas Output number: Auditor: Moore Stephens LLP Period subject to audit: 1 January 2012 to 31 December

5 Financial Audit report of the UNDP DIM project Desarrollo local transfronterizo en acompañamiento al programa binacional Table of Contents EXECUTIVE SUMMARY...3 THE AUDIT ENGAGEMENT...4 AUDIT OPINIONS...5 STATEMENT OF EXPENDITURE... 5 STATEMENT OF FIXED ASSETS... 6 STATEMENT OF CASH POSITION... 7 MANAGEMENT LETTER...8 ANNEXES...14 ANNEX 1: COMBINED DELIVERY REPORTS ANNEX 2: STATEMENT OF FIXED ASSETS ANNEX 3: AUDIT FINDING PRIORITY RATINGS

6 Financial Audit report of the UNDP DIM project Desarrollo local transfronterizo en acompañamiento al programa binacional EXECUTIVE SUMMARY Moore Stephens LLP conducted the financial audit of Desarrollo local transfronterizo en acompañamiento al programa binacional (Project ID and Output ) (the project), directly implemented by UNDP Dominican Republic for the period from 1 January 2012 to 31 December The audit was undertaken on behalf of UNDP, Office of Audit and Investigations (OAI). We have issued audit opinions as follows: Statement of Expenditure Statement of Fixed Assets Statement of Cash Position Qualified Unqualified Not applicable As a result of our audit, we have raised four audit findings with a financial impact totalling $ 45, as summarised below: No. Description Priority Financial impact $ 1 Consulting costs not for project purposes Medium 5, Lack of monthly reports from consultants Medium - 3 Overtime payments paid in respect of a different project Medium 1, Expenditure reversal charged to the project not supported by documentation High 38, Total 45, Mark Henderson Partner Moore Stephens LLP 150 Aldersgate Street London EC1A 4AB 8 September

7 Financial Audit report of the UNDP DIM project Desarrollo local transfronterizo en acompañamiento al programa binacional THE AUDIT ENGAGEMENT Audit Objectives and Scope The objective of the financial audit was to express an opinion on the DIM project s financial statements which include: Expressing an opinion on whether the financial expenses incurred by the project between 1 January 2012 and 31 December 2013 and the funds utilization as at 31 December 2013 are fairly presented in accordance with UNDP accounting policies and that the expenses incurred were: (i) in conformity with the approved project budgets; (ii) for the approved purposes of the project; (iii) in compliance with the relevant regulations and rules, policies and procedures of UNDP; and (iv) supported by properly approved vouchers and other supporting documents. The Combined Delivery Report (CDR) and the accompanying Funds Utilization statement are the mandatory and official statements upon which the audit opinion should be expressed. Other forms of statement of expenses that may be prepared by a project office are not accepted. Expressing an opinion on whether the statement of fixed assets presents fairly the balance of assets of the UNDP project as at 31 December This statement must include all assets available as at 31 December 2013 and not only those purchased in a given period. Where a DIM project does not have any assets or equipment, it will not be necessary to express such an opinion. Expressing an opinion on whether the statement of cash held by the project presents fairly the cash and bank balance of UNDP project as at 31 December Disbursements made against a DIM project are usually financed from the regular country office bank accounts. Exceptionally, a dedicated bank account may be opened and used solely for the cash transactions of a DIM project, e.g. if the project is in a remote location. The audit firm is required to express an opinion on the Statement of Cash only where a dedicated bank account for the DIM project has been established. In cases where the cash transactions of the audited DIM project are made through the country office bank accounts, this type of opinion is not required. The scope of the audit relates only to transactions concluded and recorded against the UNDP DIM project between 1 January 2011 and 31 December The scope of the audit did not include: Activities and expenses incurred or undertaken at the level of responsible parties, unless the inclusion of these expenses is specifically required in the request for proposal; and Expenses processed and approved in locations outside the country such as UNDP Regional Centres and UNDP Headquarters and where the supporting documentation is not retained at the level of the UNDP country office. 4

8 Financial Audit report of the UNDP DIM project Desarrollo local transfronterizo en acompañamiento al programa binacional AUDIT OPINIONS Independent Auditor s Report to UNDP OAI - Financial Audit Statement of Expenditure Qualified Opinion We have audited the accompanying Combined Delivery Report and Funds Utilization statements ( the statement ) totalling $ 848,793 of the UNDP project , Output Desarrollo local transfronterizo en acompañamiento al programa binacional ( the project ) for the period from 1 January 2012 to 31 December Management is responsible for the preparation of the statement for the Desarrollo local transfronterizo en acompañamiento al programa binacional project and for such internal control as management determines is necessary to enable the preparation of a statement that is free from material misstatement, whether due to fraud or error. Our responsibility is to express an opinion on the statement based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the statement is free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the statement. The procedures selected depend on the auditor s judgment, including the assessment of the risks of material misstatement of the statement, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the project s preparation of the statement in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the project s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the presentation of the statement. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Basis for Qualified Opinion We have made financial findings totalling $ 45, as set out in the Management Letter section of our report, which represent amounts included in the Combined Delivery Reports presented to us for audit which, in our opinion, were either (i) not in conformity with the approved budget; (ii) not for the approved purposes of the project; (iii) not in compliance with the relevant regulations and rules, policies and procedures of UNDP; or (iv) not supported by properly approved vouchers and other supporting documents. These findings represent 5.3 % of the total expenditure amount reported and are therefore considered material in the context of our audit. Qualified Opinion In our opinion, the accompanying Combined Delivery Report and Funds Utilization statements, except for the matter described in the Basis for Qualified Opinion paragraph, present fairly in all material respects the expenditure of $ 848,793 incurred by the UNDP project Output Desarrollo local transfronterizo en acompañamiento al programa binacional for the period 1 January 2012 to 31 December 2013 in accordance with UNDP accounting policies. 5

9 Financial Audit report of the UNDP DIM project Desarrollo local transfronterizo en acompañamiento al programa binacional Independent Auditor s Report to UNDP OAI - Financial Audit Statement of Fixed Assets We have audited the accompanying Statement of Fixed Assets ( the Statement ) of the DIM project Desarrollo Local Transfronterizo en acompañamiento al Programa Binacional ( the project ) representing the balance of inventory held under Atlas Project number and Atlas Output number as at 31 December This Statement includes all assets an equipment available at 31 December 2013 and not only those purchased between 1 January 2012 and 31 December Management is responsible for the preparation of the statement for the Desarrollo local transfronterizo en acompañamiento al programa binacional project and for such internal control as management determines is necessary to enable the preparation of a statement that is free from material misstatement, whether due to fraud or error. Our responsibility is to express an opinion on the statement based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the statement is free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the statement. The procedures selected depend on the auditor s judgment, including the assessment of the risks of material misstatement of the statement, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the project s preparation of the statement in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the project s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the presentation of the statement. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Unqualified Opinion In our opinion, the attached Statement of Fixed Assets presents fairly, in all material respects, the balance of inventory of the UNDP project Desarrollo Local Transfronterizo en acompañamiento al Programa Binacional amounting to $ 71, as at 31 December 2013 in accordance with UNDP accounting policies. 6

10 Financial Audit report of the UNDP DIM project Desarrollo local transfronterizo en acompañamiento al programa binacional Independent Auditor s Report to UNDP OAI - Financial Audit Statement of Cash Position We noted that the UNDP project Output Desarrollo local transfronterizo en acompañamiento al programa binacional did not have a dedicated bank account for DIM project activities subject to audit and accordingly a Statement of Cash Position was not produced. 7

11 Financial Audit report of the UNDP DIM project Desarrollo local transfronterizo en acompañamiento al programa binacional MANAGEMENT LETTER The findings related to the audit of the financial statements are discussed in our management letter below: Finding n : 1 Title: Consulting costs not for project purposes Observation: During our audit we identified expenditure charged to the project for 50% of the cost of international consulting work regarding mechanisms of territorial articulation (ART). This concerned the design of a training cycle about methodology and instruments of the UNDP s ART initiative for officers of the programmatic area and provincial work groups in territories where the ART project was operating (Dajabón, Elias Piña, Enriquillo, Monte Plata). The terms of reference, as well as the contract request of the consultant who was appointed for the assignment, make reference to the ART programme (project ) and not PDLT We were not provided with evidence or explanations to support the basis for attributing a percentage of the cost to the PDLT project. According to the contract, the total cost of the consulting was $ 11,200. Expenditure was charged as follows: Date Account Description Ref Amount $ 13-Mar Local consult.-sht term - tech DOM ACCR-DST 2, Apr Local consult.-sht term - tech DOM ACCR-DST 3,500 Total 5,600 b Priority: Medium Recommendation: UNDP should ensure that all the payments are supported by valid contracts and amendments corresponding to the project to which they are being charged, or that further documentation is available to support the costs that have been charged to the project. Management comments: Finding indeed correct for the period. 8

12 Financial Audit report of the UNDP DIM project Desarrollo local transfronterizo en acompañamiento al programa binacional Finding n : 2 Title: Lack of monthly reports from consultants Observation: During our audit we were not provided with evidence of compliance with the section of the Terms of Reference of contracts requiring of consultants the presentation of monthly reports, as follows: Reports containing a detailed summary of the activities performed, main results, problems found, solutions applied, number of beneficiaries and parties involved. Furthermore, we did not receive alternative documentation which could have supported the work performed by the consultants, such as timesheets or activity logs. This documentation was missing in the case of the consultants relating to transactions DOM ACCR-DST, DOM ACCR-DST and DOM ACCR-DST. Priority: Medium Recommendation: UNDP should ensure that consultants comply with their contract and that there is evidence to support payments to consultants. Management comments: Correct, the terms of references of the consultants did require a monthly activities report, something however not typical of Service Contracts. 9

13 Financial Audit report of the UNDP DIM project Desarrollo local transfronterizo en acompañamiento al programa binacional Finding n : 3 Title: Overtime payments paid in respect of a different project Observation: We observed overtime being paid and charged to this project although it was approved and agreed for a different project. Furthermore, we also couldn t find evidence that a due authorization process was followed for these payments, as stated in the Guide Applicable to Service Consultants: Overtime pay must be requested and approved by the supervisor in advance of the extra work period to be performed, subject to the availability of funds. The cost of overtime pay must be funded from the same source as the SC itself. UNDP Offices must ensure that sufficient funds exist for functions that may reasonably expect payment of overtime. The payments made were as follows: Account Date Ref Description Amount $ may-13 DOM ACCR-DST Horas extras abril aug-13 DOM ACCR-DST Horas extras mes julio sep-13 DOM ACCR-DST Pago horas extra agosto oct-13 DOM ACCR-DST Horas extras septiembre nov-13 DOM ACCR-DST Horas extras mes octubre feb mar-13 DOM ACCR-DST DOM ACCR-DST Horas extras enero Horas extras febrero jul-13 DOM ACCR-DST Horas extras jun.frontera/art sep-13 DOM ACCR-DST Horas extras mes julio sep-13 DOM ACCR-DST Horas extras agosto oct-13 DOM ACCR-DST Horas extras septiembre nov-13 DOM ACCR-DST Horas extras mes octubre Total 1, Priority: Medium 10

14 Financial Audit report of the UNDP DIM project Desarrollo local transfronterizo en acompañamiento al programa binacional Recommendation: UNDP should ensure that the payments for overtime correspond to staff actually appointed for the project and that the correct authorisation processes are followed. Management comments: Correct. Note: payments adjusted as of January 2014 with the division between ART and PDLT that the office undertook. 11

15 Financial Audit report of the UNDP DIM project Desarrollo local transfronterizo en acompañamiento al programa binacional Finding n : 4 Title: Expenditure reversal charged to the project not supported by documentation Observation: We observed expenditure transferred to the project via reversal of expenditure from project (ART). There was no supporting information which would explain or justify these journal entries, and how they related to the objectives to the project, to the AWP, to the budget or to whom the payments were made since the vendor field is blank in all of them. Details are as follows: Account Date Account Description Description Amount $ dec-12 Intl Consultants-Sht Term-Tech Reversión de gastos del proyecto al , sep-13 Local Consult.-Sht Term-Tech Revirtiendo gastos del proy al , sep-13 Service Contracts- Individuals Revirtiendo gastos del proy al sep-13 Service Contracts- Individuals Revirtiendo gastos del proy al , sep-13 Service Contracts- Individuals Revirtiendo gastos del proy al , oct-13 DAILY SUBSISTENCE ALLOW-INTL REVERSION DEL AL , sep-13 Daily Subsistence Allow- Local Revirtiendo gastos del proy al sep-13 Daily Subsistence Allow- Local Revirtiendo gastos del proy al sep-13 Daily Subsistence Allow- Local Revirtiendo gastos del proy al sep-13 Daily Subsistence Allow- Local Revirtiendo gastos del proyecto al (36.90) sep-13 Hospitality-Special Events Revirtiendo gastos del proy al sep-13 Hospitality-Special Events Revirtiendo gastos del proy al oct-13 Maint, Oper of Transport Equip REVERSION DV , sep-13 Maint, Oper of Transport Equip Revirtiendo gastos del proy al

16 Financial Audit report of the UNDP DIM project Desarrollo local transfronterizo en acompañamiento al programa binacional sep-13 Maint, Oper of Transport Equip Revirtiendo gastos del proyecto al (652.83) sep-13 Sundry Revirtiendo gastos del proy al Total 38, Priority: High Recommendation: UNDP should ensure that journal adjustments are backed up by appropriate supporting documents to evidence that such costs relate to the project and are accurately recorded. Management comments: UNDP has been focusing, since the change in coordination and management of the project in January 2014, on the thorough management of expenditures and project activity consistency. Mark Henderson Partner Moore Stephens LLP 150 Aldersgate Street London EC1A 4AB 8 September

17 Financial Audit report of the UNDP DIM project Desarrollo local transfronterizo en acompañamiento al programa binacional Annexes 14

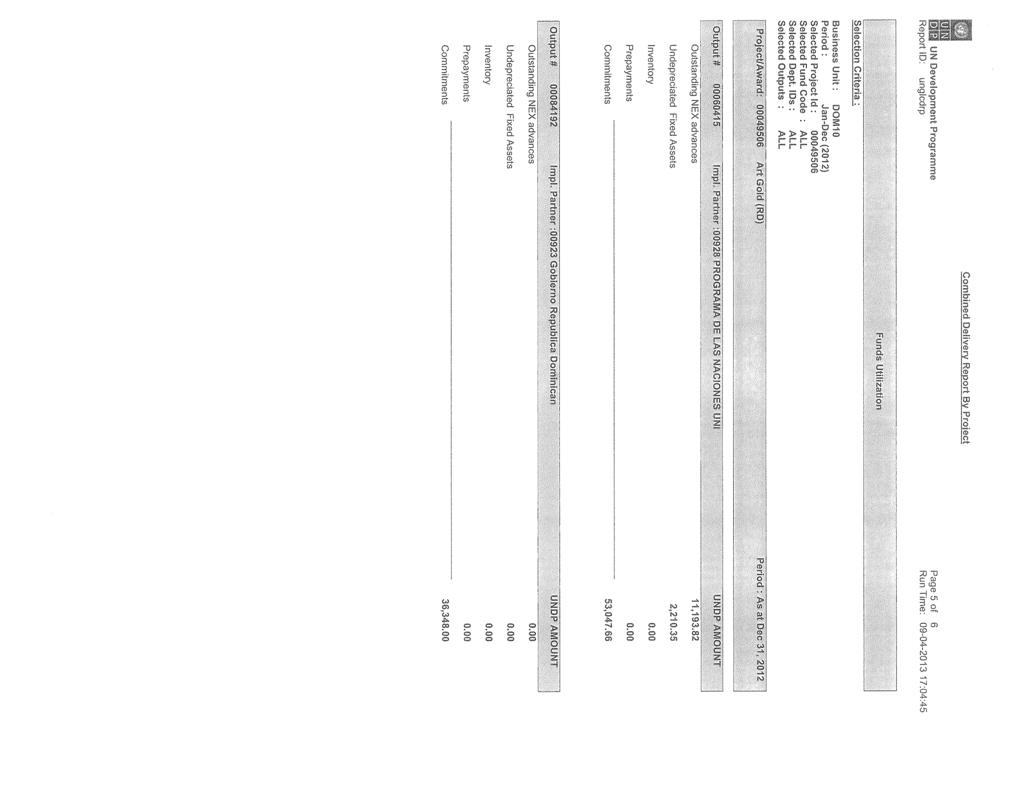

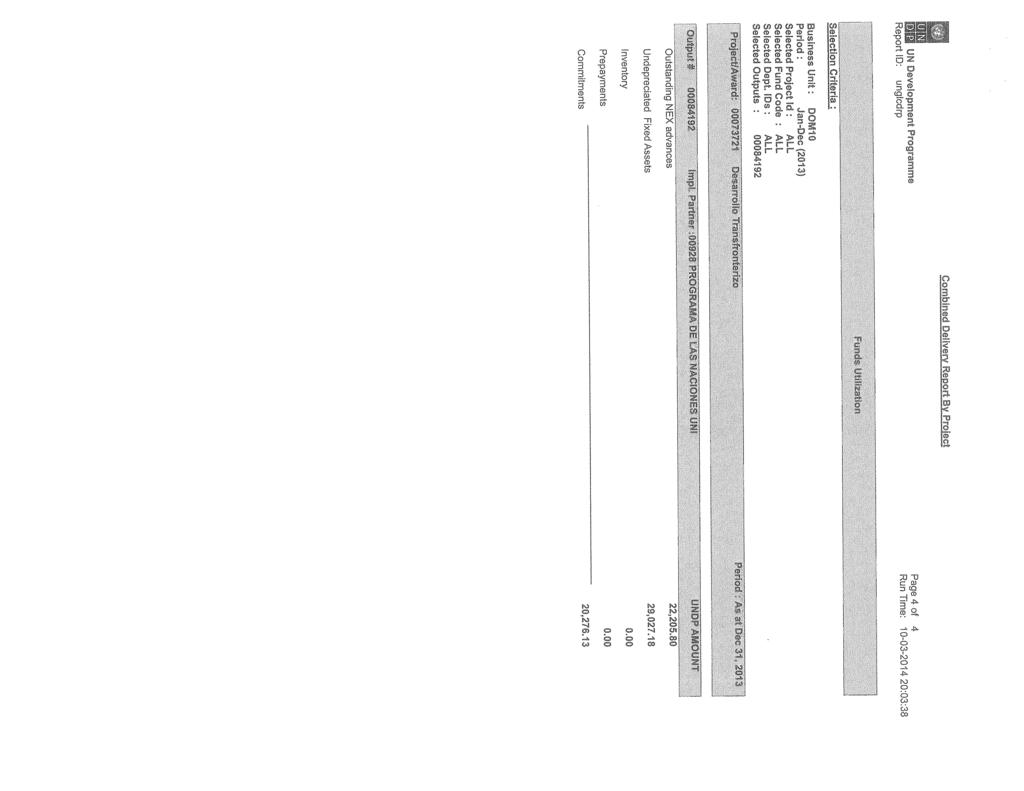

18 Financial Audit report of the UNDP DIM project Desarrollo local transfronterizo en acompañamiento al programa binacional Annex 1: Combined Delivery Reports 2012 and 2013 Note that in 2012, the project s expenditure was recorded in the CDR for Project ID (ART Gold). Refer to page 3 of the CDR for expenditure totalling $ 111, which is specific to the project under audit. 15

19

20

21

22

23

24

25

26

27

28

29 Financial Audit report of the UNDP DIM project Desarrollo local transfronterizo en acompañamiento al programa binacional Annex 2: Statement of Fixed Assets 26

30

31

32 Financial Audit report of the UNDP DIM project Desarrollo local transfronterizo en acompañamiento al programa binacional Annex 3: Audit finding priority ratings The following categories of priorities are used: High (Critical) Medium (Important) Low Action is considered imperative to ensure that UNDP is not exposed to high risks. Failure to take action could result in major consequences and issues. Action is considered necessary to avoid exposure to significant risks. Failure to take action could result in significant consequences. Action is considered desirable and should result in enhanced control or better value for money. Low priority recommendations, if any, are dealt with by the Auditors directly with the Office management, during the exit meeting and through a separate memo subsequent to the fieldwork. Therefore, low priority recommendations are not included in the audit report. 29

AUDIT UNDP BANGLADESH. Comprehensive Disaster Management Programme Phase II (Project No , Output Nos )

") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP BANGLADESH Comprehensive Disaster Management Programme Phase II (Project No. 58919, Output Nos. 73416) Report No. 1472

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP BANGLADESH Comprehensive Disaster Management Programme Phase II (Project No. 58919, Output Nos. 73416) Report No. 1472

UNITED NATIONS DEVELOPMENT PROGRAMME (UNDP) AUDIT REPORT. 31 July 2017 FINANCIAL AUDIT OF THE UNDP DIRECTLY IMPLEMENTED (DIM) PROJECT

AUDIT REPORT. 31 July 2017 FINANCIAL AUDIT OF THE UNDP DIRECTLY IMPLEMENTED (DIM) PROJECT") UNITED NATIONS DEVELOPMENT PROGRAMME (UNDP) AUDIT REPORT 31 July 2017 FINANCIAL AUDIT OF THE UNDP DIRECTLY IMPLEMENTED (DIM) PROJECT Sustainable Energy Activities UNDP Country Office: Lebanon Atlas Project

UNITED NATIONS DEVELOPMENT PROGRAMME (UNDP) AUDIT REPORT 31 July 2017 FINANCIAL AUDIT OF THE UNDP DIRECTLY IMPLEMENTED (DIM) PROJECT Sustainable Energy Activities UNDP Country Office: Lebanon Atlas Project

AUDIT UNDP NIGERIA. DEMOCRATIC GOVERNANCE FOR DEVELOPMENT: DEEPENING DEMOCRACY IN NIGERIA (Directly Implemented Project No , Output No.

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP NIGERIA DEMOCRATIC GOVERNANCE FOR DEVELOPMENT: DEEPENING DEMOCRACY IN NIGERIA (Directly Implemented Project No. 56855,

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP NIGERIA DEMOCRATIC GOVERNANCE FOR DEVELOPMENT: DEEPENING DEMOCRACY IN NIGERIA (Directly Implemented Project No. 56855,

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT. 20 September 2017

FINANCIAL AUDIT REPORT. 20 September 2017") UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 20 September 2017 PROJECT NAME: PALESTINIAN MATURITY PROGRAM PROJECT NUMBER: 96457 COUNTRY: ISRAEL AUDITOR: MOORE STEPHENS LLP

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 20 September 2017 PROJECT NAME: PALESTINIAN MATURITY PROGRAM PROJECT NUMBER: 96457 COUNTRY: ISRAEL AUDITOR: MOORE STEPHENS LLP

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT. 27 February 2017

FINANCIAL AUDIT REPORT. 27 February 2017") UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 27 February 2017 PROJECT NAME: EMERGENCY SUPPORT FOR HEALTH RESPONSE CAPACITY IN UKRAINE PROJECT NUMBER: 00011980 COUNTRY: SERBIA

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 27 February 2017 PROJECT NAME: EMERGENCY SUPPORT FOR HEALTH RESPONSE CAPACITY IN UKRAINE PROJECT NUMBER: 00011980 COUNTRY: SERBIA

Report on Financial Audit of UNDP Directly Implemented Project Managed by UNDP Programme of Assistance to the Palestinian People (PAPP)

") Report on Financial Audit of UNDP Directly Implemented Project Managed by UNDP Programme of Assistance to the Palestinian People (PAPP) Construction of Khan Younis Waste Water Treatment Plant Project ID

Report on Financial Audit of UNDP Directly Implemented Project Managed by UNDP Programme of Assistance to the Palestinian People (PAPP) Construction of Khan Younis Waste Water Treatment Plant Project ID

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT. 26 August 2016

FINANCIAL AUDIT REPORT. 26 August 2016") UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 26 August 2016 PROJECT NAME: MODERNIZATION AND IMPROVEMENT OF POLICING PROJECT (MIPP) PROJECT NUMBER: 00093090 COUNTRY: NEPAL AUDITOR:

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 26 August 2016 PROJECT NAME: MODERNIZATION AND IMPROVEMENT OF POLICING PROJECT (MIPP) PROJECT NUMBER: 00093090 COUNTRY: NEPAL AUDITOR:

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 14 FEBRUARY 2018

FINANCIAL AUDIT REPORT 14 FEBRUARY 2018") UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 14 FEBRUARY 2018 PROJECT NAME: MODERNIZATION AND IMPROVEMENT OF POLICING PROJECT (MIPP) PROJECT NUMBER: 93090 COUNTRY: NEPAL AUDITOR:

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 14 FEBRUARY 2018 PROJECT NAME: MODERNIZATION AND IMPROVEMENT OF POLICING PROJECT (MIPP) PROJECT NUMBER: 93090 COUNTRY: NEPAL AUDITOR:

AUDIT UNDP PROGRAMME OF ASSISTANCE TO THE PALESTINIAN PEOPLE. PROCUREMENT OF DRUGS TO GAZA (Directly Implemented Project No , Output No.

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP PROGRAMME OF ASSISTANCE TO THE PALESTINIAN PEOPLE PROCUREMENT OF DRUGS TO GAZA (Directly Implemented Project No. 74904,

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP PROGRAMME OF ASSISTANCE TO THE PALESTINIAN PEOPLE PROCUREMENT OF DRUGS TO GAZA (Directly Implemented Project No. 74904,

United Nations Development Programme (UNDP)

") United Nations Development Programme (UNDP) Report of the Independent Auditor on the United Nations Development Program (UNDP) Directly Implemented (DIM) Project ID 78266 Output ID 88627 Restauration de

United Nations Development Programme (UNDP) Report of the Independent Auditor on the United Nations Development Program (UNDP) Directly Implemented (DIM) Project ID 78266 Output ID 88627 Restauration de

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT. 4 September 2015

FINANCIAL AUDIT REPORT. 4 September 2015") INTERNAL AUDIT AND INVESTIGATIONS GROUP UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 4 September 2015 PROJECT NAME: SMALL GRANTS PROGAMME (SGP) OPERATIONAL PHASE 5 PROJECT

INTERNAL AUDIT AND INVESTIGATIONS GROUP UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 4 September 2015 PROJECT NAME: SMALL GRANTS PROGAMME (SGP) OPERATIONAL PHASE 5 PROJECT

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT. 4 September 2015

FINANCIAL AUDIT REPORT. 4 September 2015") UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 4 September 2015 PROJECT NAME: SMALL GRANTS PROGAMME (SGP) OPERATIONAL PHASE 5 PROJECT NUMBER: 00078697 COUNTRY: CÔTE D'IVOIRE

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 4 September 2015 PROJECT NAME: SMALL GRANTS PROGAMME (SGP) OPERATIONAL PHASE 5 PROJECT NUMBER: 00078697 COUNTRY: CÔTE D'IVOIRE

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT UNDP LEBANON

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP LEBANON EARLY RECOVERY FOR DISPLACED SYRIANS, LEBANESE HOSTING COMMUNITIES SUPPORT PROJECT (Directly Implemented Project

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP LEBANON EARLY RECOVERY FOR DISPLACED SYRIANS, LEBANESE HOSTING COMMUNITIES SUPPORT PROJECT (Directly Implemented Project

AUDIT UNDP EGYPT. STRENGTHENING OF THE DEMOCRATIC PROCESS IN EGYPT (Directly Implemented Project No )

") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP EGYPT STRENGTHENING OF THE DEMOCRATIC PROCESS IN EGYPT (Directly Implemented Project No. 79914) Report No. 1253 Issue

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP EGYPT STRENGTHENING OF THE DEMOCRATIC PROCESS IN EGYPT (Directly Implemented Project No. 79914) Report No. 1253 Issue

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT. 12 December 2014

FINANCIAL AUDIT REPORT. 12 December 2014") UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 12 December 2014 PROJECT NAME: PROJECT NUMBER: 00073243 COUNTRY: AUDITOR: CONSERVACIÓN DE LA BIODIVERSIDAD, PARTICIPACION DE ACTORES

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 12 December 2014 PROJECT NAME: PROJECT NUMBER: 00073243 COUNTRY: AUDITOR: CONSERVACIÓN DE LA BIODIVERSIDAD, PARTICIPACION DE ACTORES

AUDIT UNDP UKRAINE. EU BORDER ASSISTANCE MISSION - 9 (Directly Implemented Project No ) Report No Issue Date: 9 December 2013

Report No Issue Date: 9 December 2013") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP UKRAINE EU BORDER ASSISTANCE MISSION - 9 (Directly Implemented Project No. 79895) Report No. 1199 Issue Date: 9 December

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP UKRAINE EU BORDER ASSISTANCE MISSION - 9 (Directly Implemented Project No. 79895) Report No. 1199 Issue Date: 9 December

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT. 4 September 2015

FINANCIAL AUDIT REPORT. 4 September 2015") UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 4 September 2015 PROJECT NAME: SMALL GRANTS PROGRAMME (SGP) OPERATIONAL PHASE 5 PROJECT NUMBER: 00078647 COUNTRY: ARMENIA AUDITOR:

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 4 September 2015 PROJECT NAME: SMALL GRANTS PROGRAMME (SGP) OPERATIONAL PHASE 5 PROJECT NUMBER: 00078647 COUNTRY: ARMENIA AUDITOR:

AUDIT UNDP PROGRAMME OF ASSISTANCE TO THE PALESTINIAN PEOPLE

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP PROGRAMME OF ASSISTANCE TO THE PALESTINIAN PEOPLE COMMUNITY RESILIENCE AND DEVELOPMENT PROGRAMME (Directly Implemented

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP PROGRAMME OF ASSISTANCE TO THE PALESTINIAN PEOPLE COMMUNITY RESILIENCE AND DEVELOPMENT PROGRAMME (Directly Implemented

AUDIT. UNDP Pakistan. Early Recovery Programme in Pakistan (Directly Implemented Project No ) Report No. 990 Issue Date: 19 June 2013

Report No. 990 Issue Date: 19 June 2013") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP Pakistan Early Recovery Programme in Pakistan (Directly Implemented Project No. 76295) Report No. 990 Issue Date: 19

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP Pakistan Early Recovery Programme in Pakistan (Directly Implemented Project No. 76295) Report No. 990 Issue Date: 19

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT. 01 March 2018

FINANCIAL AUDIT REPORT. 01 March 2018") UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 01 March 2018 PROJECT NAME: REHABILITATION OF EMERGENCY ROAD INFRASTRUCTURES ON GULLI TO BOUT ROAD, SUDAN PROJECT NUMBER: 00086142

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 01 March 2018 PROJECT NAME: REHABILITATION OF EMERGENCY ROAD INFRASTRUCTURES ON GULLI TO BOUT ROAD, SUDAN PROJECT NUMBER: 00086142

TERMS OF REFERENCE FOR AUDITS OF NIM/NGO PROJECTS

United Nations Development Programme Office of Audit and Investigations Annex I TERMS OF REFERENCE FOR AUDITS OF NIM/NGO PROJECTS 2014 02 November 2014 TABLE OF CONTENTS Page INTRODUCTION... 3 A. Background...

United Nations Development Programme Office of Audit and Investigations Annex I TERMS OF REFERENCE FOR AUDITS OF NIM/NGO PROJECTS 2014 02 November 2014 TABLE OF CONTENTS Page INTRODUCTION... 3 A. Background...

AUDIT UNDP CYPRUS. SUPPORT TO COMMITTEE ON MISSING PERSONS (Directly Implemented Project, Output No ) Report No Issue Date: 26 June 2014

Report No Issue Date: 26 June 2014") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP CYPRUS SUPPORT TO COMMITTEE ON MISSING PERSONS (Directly Implemented Project, Output No. 84969) Report No. 1361 Issue

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP CYPRUS SUPPORT TO COMMITTEE ON MISSING PERSONS (Directly Implemented Project, Output No. 84969) Report No. 1361 Issue

AUDIT UNDP COUNTRY OFFICE AFGHANISTAN FINANCIAL MANAGEMENT. Report No Issue Date: 10 December 2013

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AFGHANISTAN FINANCIAL MANAGEMENT Report No. 1233 Issue Date: 10 December 2013 Table of Contents Executive Summary i I. Introduction

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AFGHANISTAN FINANCIAL MANAGEMENT Report No. 1233 Issue Date: 10 December 2013 Table of Contents Executive Summary i I. Introduction

AUDIT UNDP NEPAL. Comprehensive Disaster Risk Management Programme (Directly Implemented Project No )

") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP NEPAL Comprehensive Disaster Risk Management Programme (Directly Implemented Project No. 77652) Report No. 1200 Issue

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP NEPAL Comprehensive Disaster Risk Management Programme (Directly Implemented Project No. 77652) Report No. 1200 Issue

Rural Renewable Energy Agency (RREA) Financial Audit Report. for the period from 1 March 2016 to 30 June Project ID: P

Financial Audit Report. for the period from 1 March 2016 to 30 June Project ID: P") Public Disclosure Authorized Public Disclosure Authorized Rural Renewable Energy Agency (RREA) Financial Audit Report for the period from 1 March 2016 to 30 June 2017 Public Disclosure Authorized Liberia

Public Disclosure Authorized Public Disclosure Authorized Rural Renewable Energy Agency (RREA) Financial Audit Report for the period from 1 March 2016 to 30 June 2017 Public Disclosure Authorized Liberia

AUDIT UNDP REPUBLIC OF CHAD. Programme Conjoint D Appui au Détachement Intégré de Sécurité (Directly Implemented Project No.

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP REPUBLIC OF CHAD Programme Conjoint D Appui au Détachement Intégré de Sécurité (Directly Implemented Project No. 77223)

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP REPUBLIC OF CHAD Programme Conjoint D Appui au Détachement Intégré de Sécurité (Directly Implemented Project No. 77223)

TERMS OF REFERENCE (TOR) FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS

FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS") TERMS OF REFERENCE (TOR) FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS TABLE OF CONTENTS Introduction... 3 A. Background... 7 B. Project Management... 7 C. Consultations with concerned parties...

TERMS OF REFERENCE (TOR) FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS TABLE OF CONTENTS Introduction... 3 A. Background... 7 B. Project Management... 7 C. Consultations with concerned parties...

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT

FINANCIAL AUDIT REPORT") UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 1 OCTOBER 2013 PROJECT NAME: PROJECT NUMBER: 00063004 COUNTRY: AUDITOR: PROJET DE REHABILITATION DU SECTEUR AGRICOLE ET RURAL AU

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) FINANCIAL AUDIT REPORT 1 OCTOBER 2013 PROJECT NAME: PROJECT NUMBER: 00063004 COUNTRY: AUDITOR: PROJET DE REHABILITATION DU SECTEUR AGRICOLE ET RURAL AU

AUDIT UNDP CYPRUS. NEW NICOSIA WASTE WATER TREATMENT PLANT (Directly Implemented Project No ) Report No Issue Date: 21 October 2013

Report No Issue Date: 21 October 2013") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP CYPRUS NEW NICOSIA WASTE WATER TREATMENT PLANT (Directly Implemented Project No. 71757) Report No. 1196 Issue Date:

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP CYPRUS NEW NICOSIA WASTE WATER TREATMENT PLANT (Directly Implemented Project No. 71757) Report No. 1196 Issue Date:

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) INTERNAL AUDIT REPORT. 19 October 2017

INTERNAL AUDIT REPORT. 19 October 2017") UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) INTERNAL AUDIT REPORT 19 October 2017 PROJECT NAME: GLOBAL FUND REGIONAL ARTEMISININ INITIATIVE (RAI) MYANMAR - PRINCIPAL RECIPIENT - UNOPS PROJECT NUMBER:

UNITED NATIONS OFFICE FOR PROJECT SERVICES (UNOPS) INTERNAL AUDIT REPORT 19 October 2017 PROJECT NAME: GLOBAL FUND REGIONAL ARTEMISININ INITIATIVE (RAI) MYANMAR - PRINCIPAL RECIPIENT - UNOPS PROJECT NUMBER:

AUDIT UNDP SIERRA LEONE. Support to the Electoral Cycle in Sierra Leone (Directly Implemented Project, Output No )

") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP SIERRA LEONE (Directly Implemented Project, Output No. 77588) Report No. 1326 Issue Date: 26 June 2014 United Nations

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP SIERRA LEONE (Directly Implemented Project, Output No. 77588) Report No. 1326 Issue Date: 26 June 2014 United Nations

AUDIT UNDP MOLDOVA. BIOMASS HEATING SYSTEM (Directly Implemented Project No ) Report No Issue Date: 21 October 2013

Report No Issue Date: 21 October 2013") UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP MOLDOVA BIOMASS HEATING SYSTEM (Directly Implemented Project No. 77341) Report No. 1197 Issue Date: 21 October 2013

UNITED NATIONS DEVELOPMENT PROGRAMME Office of Audit and Investigations AUDIT OF UNDP MOLDOVA BIOMASS HEATING SYSTEM (Directly Implemented Project No. 77341) Report No. 1197 Issue Date: 21 October 2013

QUESTION 2. QUESTION 3 Which one of the following is most indicative of a flexible short-term financial policy?

QUESTION 1 Compute the cash cycle based on the following information: Average Collection Period = 47 Accounts Payable Period = 40 Average Age of Inventory = 55 QUESTION 2 Jan 41,700 July 39,182 Feb 18,921

QUESTION 1 Compute the cash cycle based on the following information: Average Collection Period = 47 Accounts Payable Period = 40 Average Age of Inventory = 55 QUESTION 2 Jan 41,700 July 39,182 Feb 18,921

XML Publisher Balance Sheet Vision Operations (USA) Feb-02

Feb-02") Page:1 Apr-01 May-01 Jun-01 Jul-01 ASSETS Current Assets Cash and Short Term Investments 15,862,304 51,998,607 9,198,226 Accounts Receivable - Net of Allowance 2,560,786

Page:1 Apr-01 May-01 Jun-01 Jul-01 ASSETS Current Assets Cash and Short Term Investments 15,862,304 51,998,607 9,198,226 Accounts Receivable - Net of Allowance 2,560,786

AUDIT UNDP COUNTRY OFFICE BANGLADESH. Report No Issue Date: 28 May 2015

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN BANGLADESH Report No. 1429 Issue Date: 28 May 2015 Table of Contents Executive Summary i I. About the Office 1 II. Good practice 1 III.

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN BANGLADESH Report No. 1429 Issue Date: 28 May 2015 Table of Contents Executive Summary i I. About the Office 1 II. Good practice 1 III.

AUDIT UNDP AFGHANISTAN. Local Governance Project (Project No ) Report No Issue Date: 23 December 2016

Report No Issue Date: 23 December 2016") UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP AFGHANISTAN Local Governance Project (Project No. 90448) Report No. 1745 Issue Date: 23 December 2016 Table of Contents Executive Summary i I. About the

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP AFGHANISTAN Local Governance Project (Project No. 90448) Report No. 1745 Issue Date: 23 December 2016 Table of Contents Executive Summary i I. About the

Spheria Australian Smaller Companies Fund

29-Jun-18 $ 2.7686 $ 2.7603 $ 2.7520 28-Jun-18 $ 2.7764 $ 2.7681 $ 2.7598 27-Jun-18 $ 2.7804 $ 2.7721 $ 2.7638 26-Jun-18 $ 2.7857 $ 2.7774 $ 2.7690 25-Jun-18 $ 2.7931 $ 2.7848 $ 2.7764 22-Jun-18 $ 2.7771

29-Jun-18 $ 2.7686 $ 2.7603 $ 2.7520 28-Jun-18 $ 2.7764 $ 2.7681 $ 2.7598 27-Jun-18 $ 2.7804 $ 2.7721 $ 2.7638 26-Jun-18 $ 2.7857 $ 2.7774 $ 2.7690 25-Jun-18 $ 2.7931 $ 2.7848 $ 2.7764 22-Jun-18 $ 2.7771

PROFESSIONAL CRICKETERS ASSOCIATION STATEMENT TO MEMBERS 12 MONTHS ENDED 31 DECEMBER 2017

STATEMENT TO MEMBERS 12 MONTHS ENDED 31 DECEMBER 2017 PLAYERS COMMITTEE RESPONSIBILITY FOR THE FINANCIAL STATEMENTS Trade Union rules require the Players Committee to prepare Financial Statements for each

STATEMENT TO MEMBERS 12 MONTHS ENDED 31 DECEMBER 2017 PLAYERS COMMITTEE RESPONSIBILITY FOR THE FINANCIAL STATEMENTS Trade Union rules require the Players Committee to prepare Financial Statements for each

Terms of Reference for Financial Audit of Implementing Partners. UNICEF Nigeria Country Office Expenditures

Terms of Reference for Financial Audit of Implementing Partners UNICEF Nigeria Country Office 2012-2013 Expenditures A. Background and Scope of Audit Harmonized Approach to Cash Transfer (HACT) is a response

Terms of Reference for Financial Audit of Implementing Partners UNICEF Nigeria Country Office 2012-2013 Expenditures A. Background and Scope of Audit Harmonized Approach to Cash Transfer (HACT) is a response

Public Disclosure Authorized. Public Disclosure Authorized

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Montenegro Institutional Development and Agriculture Strengthening Project MIDAS Project ID: P107473 GLOBAL ENVIRONMENT

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Montenegro Institutional Development and Agriculture Strengthening Project MIDAS Project ID: P107473 GLOBAL ENVIRONMENT

1.2 The purpose of the Finance Committee is to assist the Board in fulfilling its oversight responsibilities related to:

Category: BOARD PROCESS Title: Terms of Reference for the Finance Committee Reference Number: AB-331 Last Approved: February 22, 2018 Last Reviewed: February 22, 2018 1. PURPOSE 1.1 Primary responsibility

Category: BOARD PROCESS Title: Terms of Reference for the Finance Committee Reference Number: AB-331 Last Approved: February 22, 2018 Last Reviewed: February 22, 2018 1. PURPOSE 1.1 Primary responsibility

Review of Registered Charites Compliance Rates with Annual Reporting Requirements 2016

Review of Registered Charites Compliance Rates with Annual Reporting Requirements 2016 October 2017 The Charities Regulator, in accordance with the provisions of section 14 of the Charities Act 2009, carried

Review of Registered Charites Compliance Rates with Annual Reporting Requirements 2016 October 2017 The Charities Regulator, in accordance with the provisions of section 14 of the Charities Act 2009, carried

INDEPENDENT AUDITORS REPORT TO THE MEMBERS OF SML ISUZU LIMITED

INDEPENDENT AUDITORS REPORT TO THE MEMBERS OF SML ISUZU LIMITED Report on the Financial Statements We have audited the accompanying financial statements of SML Isuzu Limited ('the Company'), which comprise

INDEPENDENT AUDITORS REPORT TO THE MEMBERS OF SML ISUZU LIMITED Report on the Financial Statements We have audited the accompanying financial statements of SML Isuzu Limited ('the Company'), which comprise

Responsibility Statement... 3 Management Report Statement of Comprehensive Income... 9 Statement of Financial Position...

Responsibility Statement... 3 Management Report... 4... 8 Statement of Comprehensive Income... 9 Statement of Financial Position... 10 Statement of Changes in Equity... 11 Statement of Cash Flows... 12

Responsibility Statement... 3 Management Report... 4... 8 Statement of Comprehensive Income... 9 Statement of Financial Position... 10 Statement of Changes in Equity... 11 Statement of Cash Flows... 12

DESK REVIEW UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN

UNITED NATIONS DEVELOPMENT PROGRAMME DESK REVIEW OF UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN Report No. 1310 Issue Date: 9 October 2014 Table of

UNITED NATIONS DEVELOPMENT PROGRAMME DESK REVIEW OF UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN Report No. 1310 Issue Date: 9 October 2014 Table of

OFFICE OF THE AUDITOR GENERAL

OFFICE OF THE AUDITOR GENERAL THE REPUBLIC OF UGANDA REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF NAMASALE TOWN COUNCIL AMOLATAR DISTRICT FOR THE YEAR ENDED 30 TH JUNE 2015 REPORT OF THE

OFFICE OF THE AUDITOR GENERAL THE REPUBLIC OF UGANDA REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF NAMASALE TOWN COUNCIL AMOLATAR DISTRICT FOR THE YEAR ENDED 30 TH JUNE 2015 REPORT OF THE

AUDIT UNDP COUNTRY OFFICE UGANDA. Report No Issue Date: 22 August 2013

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN UGANDA Report No. 1155 Issue Date: 22 August 2013 Table of Contents Executive Summary i I. Introduction 1 II. About the Office 1 III.

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN UGANDA Report No. 1155 Issue Date: 22 August 2013 Table of Contents Executive Summary i I. Introduction 1 II. About the Office 1 III.

BANK OF GUYANA. BANKING SYSTEM STATISTICAL ABSTRACT Website:

BANK OF GUYANA BANKING SYSTEM STATISTICAL ABSTRACT Website: www.bankofguyana.org.gy RESEARCH DEPARTMENT November 2010 STATISTICAL ABSTRACT TABLES CONTENTS 1. MONETARY AUTHORITY 1.1 Bank of Guyana: Assets

BANK OF GUYANA BANKING SYSTEM STATISTICAL ABSTRACT Website: www.bankofguyana.org.gy RESEARCH DEPARTMENT November 2010 STATISTICAL ABSTRACT TABLES CONTENTS 1. MONETARY AUTHORITY 1.1 Bank of Guyana: Assets

ZAMORANO ELEMENTARY SCHOOL

OIA Report to the Principal, Zamorano Elementary School Office of Internal Audit August, 2015 ZAMORANO ELEMENTARY SCHOOL Review of Associated Student Body Fund Financial Operations Report Number: 16-03

OIA Report to the Principal, Zamorano Elementary School Office of Internal Audit August, 2015 ZAMORANO ELEMENTARY SCHOOL Review of Associated Student Body Fund Financial Operations Report Number: 16-03

DRAFT FOR PUBLIC COMMENT

CITY OF IMPERIAL SUCCESSOR AGENCY FOR THE FORMER REDEVELOPMENT AGENCY DUE DILIGENCE REVIEW PURSUANT TO AB1484 LOW AND MODERATE INCOME HOUSING FUND TABLE OF CONTENTS INDEPENDENT ACCOUNTANTS REPORT 3 ATTACHMENT

CITY OF IMPERIAL SUCCESSOR AGENCY FOR THE FORMER REDEVELOPMENT AGENCY DUE DILIGENCE REVIEW PURSUANT TO AB1484 LOW AND MODERATE INCOME HOUSING FUND TABLE OF CONTENTS INDEPENDENT ACCOUNTANTS REPORT 3 ATTACHMENT

BANK OF GUYANA. BANKING SYSTEM STATISTICAL ABSTRACT Website:

BANK OF GUYANA BANKING SYSTEM STATISTICAL ABSTRACT Website: www.bankofguyana.org.gy RESEARCH DEPARTMENT March 2010 STATISTICAL ABSTRACT TABLES CONTENTS 1. MONETARY AUTHORITY 1.1 Bank of Guyana: Assets

BANK OF GUYANA BANKING SYSTEM STATISTICAL ABSTRACT Website: www.bankofguyana.org.gy RESEARCH DEPARTMENT March 2010 STATISTICAL ABSTRACT TABLES CONTENTS 1. MONETARY AUTHORITY 1.1 Bank of Guyana: Assets

Isle Of Wight half year business confidence report

half year business confidence report half year report contents new company registrations closed companies (dissolved) net company growth uk company share director age director gender naming trends sic

half year business confidence report half year report contents new company registrations closed companies (dissolved) net company growth uk company share director age director gender naming trends sic

INTERNATIONAL STANDARD ON AUDITING 510 INITIAL ENGAGEMENTS OPENING BALANCES CONTENTS

INTERNATIONAL STANDARD ON AUDITING 510 INITIAL ENGAGEMENTS OPENING BALANCES (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction...

INTERNATIONAL STANDARD ON AUDITING 510 INITIAL ENGAGEMENTS OPENING BALANCES (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction...

The Prize Bond Company Limited. Annual Report 2012

The Prize Bond Company Limited Annual Report 2012 Contents Page Chairman s Statement 1 Corporate Information 3 Directors Report 4 Statement of Directors Responsibilities 5 Independent Auditor s Report

The Prize Bond Company Limited Annual Report 2012 Contents Page Chairman s Statement 1 Corporate Information 3 Directors Report 4 Statement of Directors Responsibilities 5 Independent Auditor s Report

Financial Report for the period from 1 October 2015 to 30 September 2016

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Financial Report for the period from 1 October 2015 to 30 September 2016 Community Driven Nutrition Improvement Project

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Financial Report for the period from 1 October 2015 to 30 September 2016 Community Driven Nutrition Improvement Project

OFFICE OF THE AUDITOR GENERAL THE REPUBLIC OF UGANDA

OFFICE OF THE AUDITOR GENERAL THE REPUBLIC OF UGANDA REPORT AND OPINION OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF KOLE DISTRICT LOCAL GOVERNMENT FOR THE YEAR ENDED 0 TH JUNE 201 REPORT AND

OFFICE OF THE AUDITOR GENERAL THE REPUBLIC OF UGANDA REPORT AND OPINION OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF KOLE DISTRICT LOCAL GOVERNMENT FOR THE YEAR ENDED 0 TH JUNE 201 REPORT AND

Assessment Method 1: Evaluate users' training needs.

2013-2014 Assessment Report Associate VP Business & Finance Controller/Financial Reporting Expected Outcome 1: E-journal voucher system users will be trained on applicable topics. The Controller s office

2013-2014 Assessment Report Associate VP Business & Finance Controller/Financial Reporting Expected Outcome 1: E-journal voucher system users will be trained on applicable topics. The Controller s office

Opinions on technical and scientific matters concerning mutual recognition: working procedure for the Biocidal Products Committee (BPC)

") 1 (5) Opinions on technical and scientific matters concerning mutual recognition: working procedure for the Biocidal Products Committee (BPC) The purpose of this document is to establish principles to

1 (5) Opinions on technical and scientific matters concerning mutual recognition: working procedure for the Biocidal Products Committee (BPC) The purpose of this document is to establish principles to

United Nations Development Programme Office of Audit and Investigations TERMS OF REFERENCE FOR AUDITS OF NGO AND NIM PROJECTS

United Nations Development Programme Office of Audit and Investigations TERMS OF REFERENCE FOR AUDITS OF NGO AND NIM PROJECTS TABLE OF CONTENTS Page REQUEST FOR QUOTATION (RFQ)... 4 TERMS OF REFERENCE...

United Nations Development Programme Office of Audit and Investigations TERMS OF REFERENCE FOR AUDITS OF NGO AND NIM PROJECTS TABLE OF CONTENTS Page REQUEST FOR QUOTATION (RFQ)... 4 TERMS OF REFERENCE...

Algo Trading System RTM

Year Return 2016 15,17% 2015 29,57% 2014 18,57% 2013 15,64% 2012 13,97% 2011 55,41% 2010 50,98% 2009 48,29% Algo Trading System RTM 89000 79000 69000 59000 49000 39000 29000 19000 9000 2-Jan-09 2-Jan-10

Year Return 2016 15,17% 2015 29,57% 2014 18,57% 2013 15,64% 2012 13,97% 2011 55,41% 2010 50,98% 2009 48,29% Algo Trading System RTM 89000 79000 69000 59000 49000 39000 29000 19000 9000 2-Jan-09 2-Jan-10

Fiscal Year 2018 Project 1 Annual Budget

Fiscal Year 2018 Project 1 Annual Budget Table of Contents Table Page Summary 3 Summary of Costs Table 1 4 Treasury Related Expenses Table 2 5 Summary of Full Time Equivalent Table 3 6 Positions Cost-to-Cash

Fiscal Year 2018 Project 1 Annual Budget Table of Contents Table Page Summary 3 Summary of Costs Table 1 4 Treasury Related Expenses Table 2 5 Summary of Full Time Equivalent Table 3 6 Positions Cost-to-Cash

ICE LIBOR Holiday Calendar 2019

ICE LIBOR Holiday Calendar Date Day Holiday GBP CHF JPY 01-Jan- Tuesday New Year's Day O O O O O 21-Jan- Monday Martin Luther King's Birthday () P No O/N P P P 18-Feb- Monday President's Day () P No O/N

ICE LIBOR Holiday Calendar Date Day Holiday GBP CHF JPY 01-Jan- Tuesday New Year's Day O O O O O 21-Jan- Monday Martin Luther King's Birthday () P No O/N P P P 18-Feb- Monday President's Day () P No O/N

North York General Hospital Foundation. Financial Statements March 31, 2013

North York General Hospital Foundation Financial Statements March 31, June 20, Independent Auditor s Report To the Members of North York General Hospital Foundation We have audited the accompanying financial

North York General Hospital Foundation Financial Statements March 31, June 20, Independent Auditor s Report To the Members of North York General Hospital Foundation We have audited the accompanying financial

1. Background General information on the initiative... 3

Contents 1. Background... 3 1.1 General information on the initiative... 3 1.2 Implementation modalities... 4 2. Project Budget and funds utilization... 4 2.1 Budget components and utilization... 4 2.2

Contents 1. Background... 3 1.1 General information on the initiative... 3 1.2 Implementation modalities... 4 2. Project Budget and funds utilization... 4 2.1 Budget components and utilization... 4 2.2

Exam 1 Problem Solving Questions Review

Exam 1 Problem Solving Questions Review SECTION 1 The following data were obtained from a recent quarterly report for Dell Computer (in millions): Net revenue $8,028 Cost of revenue $6,580 Inventories:

Exam 1 Problem Solving Questions Review SECTION 1 The following data were obtained from a recent quarterly report for Dell Computer (in millions): Net revenue $8,028 Cost of revenue $6,580 Inventories:

Annual Audit Letter 2016/17 Wiltshire Council

Annual Audit Letter 2016/17 Wiltshire Council kpmg.com/uk December 2017 Contents Report sections Summary 2 The contacts at KPMG in connection with this report are: Appendices 1. Key issues and recommendations

Annual Audit Letter 2016/17 Wiltshire Council kpmg.com/uk December 2017 Contents Report sections Summary 2 The contacts at KPMG in connection with this report are: Appendices 1. Key issues and recommendations

FINANCIAL REPORTING REQUIREMENTS. Eastern Partnership Territorial Cooperation Programme Armenia - Georgia

FINANCIAL REPORTING REQUIREMENTS Eastern Partnership Territorial Cooperation Programme Armenia - Georgia RESPONSIBILITIES The Coordinator is responsible for providing Financial Report and for ensuring

FINANCIAL REPORTING REQUIREMENTS Eastern Partnership Territorial Cooperation Programme Armenia - Georgia RESPONSIBILITIES The Coordinator is responsible for providing Financial Report and for ensuring

Determination (9 /2010) of a Customer Complaint Submitted by a Customer Against Muscat Electricity Distribution Company SAOC

of a Customer Complaint Submitted by a Customer Against Muscat Electricity Distribution Company SAOC") Determination (9 /2010) of a Customer Complaint Submitted by a Customer Against Muscat Electricity Distribution Company SAOC 1. Introduction 1.1 The Authority for Electricity Regulation, Oman (the Authority)

Determination (9 /2010) of a Customer Complaint Submitted by a Customer Against Muscat Electricity Distribution Company SAOC 1. Introduction 1.1 The Authority for Electricity Regulation, Oman (the Authority)

SECTION 2: Participant Medical and Emergency Information

The Gap Year Experience www.gapyearcourse.co.za Course Registration Form SECTION 1: Participant Information Full Name: ID Number: Cell Number: Home Number: Email Address: Residential Address: CODE: Postal

The Gap Year Experience www.gapyearcourse.co.za Course Registration Form SECTION 1: Participant Information Full Name: ID Number: Cell Number: Home Number: Email Address: Residential Address: CODE: Postal

THE LONDON PUBLIC LIBRARY BOARD TRUST FUNDS

Financial Statements of THE LONDON PUBLIC LIBRARY BOARD TRUST FUNDS Year ended December 31, 2016 KPMG LLP 140 Fullarton Street Suite 1400 London ON N6A 5P2 Canada Tel 519 672-4800 Fax 519 672-5684 INDEPENDENT

Financial Statements of THE LONDON PUBLIC LIBRARY BOARD TRUST FUNDS Year ended December 31, 2016 KPMG LLP 140 Fullarton Street Suite 1400 London ON N6A 5P2 Canada Tel 519 672-4800 Fax 519 672-5684 INDEPENDENT

Financial statements o. Judo Canada. March 31. :H4

0 Financial statements o Judo Canada March 31. :H4 March 31, 2014 Table of contents Independent Auditor's Report 1-2 Statement of financial position 3 Statement of changes in net assets 4 Statement of

0 Financial statements o Judo Canada March 31. :H4 March 31, 2014 Table of contents Independent Auditor's Report 1-2 Statement of financial position 3 Statement of changes in net assets 4 Statement of

HUD NSP-1 Reporting Apr 2010 Grantee Report - New Mexico State Program

HUD NSP-1 Reporting Apr 2010 Grantee Report - State Program State Program NSP-1 Grant Amount is $19,600,000 $9,355,381 (47.7%) has been committed $4,010,874 (20.5%) has been expended Grant Number HUD Region

HUD NSP-1 Reporting Apr 2010 Grantee Report - State Program State Program NSP-1 Grant Amount is $19,600,000 $9,355,381 (47.7%) has been committed $4,010,874 (20.5%) has been expended Grant Number HUD Region

Solution to Problem 31 Adjusting entries. Solution to Problem 32 Closing entries.

Solution to Problem 31 Adjusting entries. 1. Utilities expense 27,000 Accounts payable 27,000 2. Rent revenue 4,000 Unearned revenue 4,000 3. Supplies 2,000 Supplies expense 2,000 4. Interest receivable

Solution to Problem 31 Adjusting entries. 1. Utilities expense 27,000 Accounts payable 27,000 2. Rent revenue 4,000 Unearned revenue 4,000 3. Supplies 2,000 Supplies expense 2,000 4. Interest receivable

AUDIT UNDP COUNTRY OFFICE SOMALIA. Report No Issue Date: 20 June 2014

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN SOMALIA Report No. 1299 Issue Date: 20 June 2014 Table of Contents Executive Summary ii I. About the Office 1 II. Audit results 1 A.

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN SOMALIA Report No. 1299 Issue Date: 20 June 2014 Table of Contents Executive Summary ii I. About the Office 1 II. Audit results 1 A.

INVESTMENT PROMOTION ACT (Title amend., SG 37/04)

") INVESTMENT PROMOTION ACT (Title amend., SG 37/04) Prom. SG. 97/24 Oct 1997, corr. SG. 99/29 Oct 1997, suppl. SG. 29/13 Mar 1998, amend. SG. 153/23 Dec 1998, amend. SG. 110/17 Dec 1999, amend. SG. 28/19

INVESTMENT PROMOTION ACT (Title amend., SG 37/04) Prom. SG. 97/24 Oct 1997, corr. SG. 99/29 Oct 1997, suppl. SG. 29/13 Mar 1998, amend. SG. 153/23 Dec 1998, amend. SG. 110/17 Dec 1999, amend. SG. 28/19

ACCT-112 Final Exam Practice Solutions

ACCT-112 Final Exam Practice Solutions Question 1 Jan 1 Cash 200,000 H. Happee, Capital 200,000 Jan 2 Prepaid Insurance 10,000 Cash 10,000 Jan 15 Equipment 15,000 Cash 5,000 Notes Payable 10,000 Jan 30

ACCT-112 Final Exam Practice Solutions Question 1 Jan 1 Cash 200,000 H. Happee, Capital 200,000 Jan 2 Prepaid Insurance 10,000 Cash 10,000 Jan 15 Equipment 15,000 Cash 5,000 Notes Payable 10,000 Jan 30

Performance Report October 2018

Structured Investments Indicative Report October 2018 This report illustrates the indicative performance of all Structured Investment Strategies from inception to 31 October 2018 Matured Investment Strategies

Structured Investments Indicative Report October 2018 This report illustrates the indicative performance of all Structured Investment Strategies from inception to 31 October 2018 Matured Investment Strategies

OFFICE OF THE AUDITOR GENERAL

OFFICE OF THE AUDITOR GENERAL THE REPUBLIC OF UGANDA REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF KOLE DISTRICT LOCAL GOVERNMENT FOR THE YEAR ENDED 30 TH JUNE 2015 REPORT AND OPINION OF

OFFICE OF THE AUDITOR GENERAL THE REPUBLIC OF UGANDA REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF KOLE DISTRICT LOCAL GOVERNMENT FOR THE YEAR ENDED 30 TH JUNE 2015 REPORT AND OPINION OF

DBS Asia Treasures Membership

DBS Asia Treasures Membership Frequently Asked Questions 1. How do I join as a DBS Asia Treasures member? The DBS Asia Treasures membership is by invitation only. The membership may be extended to clients

DBS Asia Treasures Membership Frequently Asked Questions 1. How do I join as a DBS Asia Treasures member? The DBS Asia Treasures membership is by invitation only. The membership may be extended to clients

Independent Auditors Report

Independent Auditors Report Board of Regents Oklahoma Agricultural and Mechanical Colleges We have audited the accompanying statement of net assets of the Oklahoma State University Center for Innovation

Independent Auditors Report Board of Regents Oklahoma Agricultural and Mechanical Colleges We have audited the accompanying statement of net assets of the Oklahoma State University Center for Innovation

SchroderUKRealEstateFundFeederTrust Report and Audited Financial Statements. FortheYearEnded 31 March 2016

SchroderUKRealEstateFundFeederTrust Report and Audited Financial Statements FortheYearEnded 31 March 2016 CONTENTS SchroderUKRealEstateFundFeederTrust Report and Audited Financial Statements for the year

SchroderUKRealEstateFundFeederTrust Report and Audited Financial Statements FortheYearEnded 31 March 2016 CONTENTS SchroderUKRealEstateFundFeederTrust Report and Audited Financial Statements for the year

Initial Audit Engagements Opening Balances

SINGAPORE STANDARD ON AUDITING SSA 510 Initial Audit Engagements Opening Balances This SSA 510 supersedes the SSA 510 Initial Audit Engagements Opening Balances in January 2010. Auditors are required to

SINGAPORE STANDARD ON AUDITING SSA 510 Initial Audit Engagements Opening Balances This SSA 510 supersedes the SSA 510 Initial Audit Engagements Opening Balances in January 2010. Auditors are required to

SedonaOffice Users Conference. San Francisco, CA January 21 24, Deferred Income. Presented by: Bob Esquerra Debbie Stephens

SedonaOffice Users Conference San Francisco, CA January 21 24, 2018 Deferred Income Presented by: Bob Esquerra Debbie Stephens This Page Intentionally Left Blank Page 2 of 20 Table of Contents What is

SedonaOffice Users Conference San Francisco, CA January 21 24, 2018 Deferred Income Presented by: Bob Esquerra Debbie Stephens This Page Intentionally Left Blank Page 2 of 20 Table of Contents What is

Common stock prices 1. New York Stock Exchange indexes (Dec. 31,1965=50)2. Transportation. Utility 3. Finance

2. Transportation. Utility 3. Finance") Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis 000 97 98 99 I90 9 9 9 9 9 9 97 98 99 970 97 97 ""..".'..'.."... 97 97 97 97 977 978 979 980 98 98 98 98 98 98 987 988

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis 000 97 98 99 I90 9 9 9 9 9 9 97 98 99 970 97 97 ""..".'..'.."... 97 97 97 97 977 978 979 980 98 98 98 98 98 98 987 988

Financial & Business Highlights For the Year Ended June 30, 2017

Financial & Business Highlights For the Year Ended June, 17 17 16 15 14 13 12 Profit and Loss Account Operating Revenue 858 590 648 415 172 174 Investment gains net 5 162 909 825 322 516 Other 262 146

Financial & Business Highlights For the Year Ended June, 17 17 16 15 14 13 12 Profit and Loss Account Operating Revenue 858 590 648 415 172 174 Investment gains net 5 162 909 825 322 516 Other 262 146

Integrated Planning, Monitoring and Reporting

1. Purpose This procedure describes the integrated planning, monitoring and ing cycle of the European Chemicals Agency, including the preparation of the Single Programming Document (SPD). This procedure

1. Purpose This procedure describes the integrated planning, monitoring and ing cycle of the European Chemicals Agency, including the preparation of the Single Programming Document (SPD). This procedure

Welcome to this course on Expense Management under IPSAS 1.

Course Name: IPSAS Expense Management - Beginners Page 1 Course Introduction Welcome to this course on Expense Management under IPSAS 1. This course is organised into fourteen independent units, with each

Course Name: IPSAS Expense Management - Beginners Page 1 Course Introduction Welcome to this course on Expense Management under IPSAS 1. This course is organised into fourteen independent units, with each

Foundations of Investing

www.edwardjones.com Member SIPC Foundations of Investing 1 5 HOW CAN I STAY ON TRACK? 4 HOW DO I GET THERE? 1 WHERE AM I TODAY? MY FINANCIAL NEEDS 3 CAN I GET THERE? 2 WHERE WOULD I LIKE TO BE? 2 Develop

www.edwardjones.com Member SIPC Foundations of Investing 1 5 HOW CAN I STAY ON TRACK? 4 HOW DO I GET THERE? 1 WHERE AM I TODAY? MY FINANCIAL NEEDS 3 CAN I GET THERE? 2 WHERE WOULD I LIKE TO BE? 2 Develop

City of Fort Worth. City Council Work Session March 28, 2017

City of Fort Worth City Council Work Session March 28, 2017 Overview Introductions Audit Results Audit Process Required Communications New Standards Discussion 2 Introductions Engagement Leadership Kevin

City of Fort Worth City Council Work Session March 28, 2017 Overview Introductions Audit Results Audit Process Required Communications New Standards Discussion 2 Introductions Engagement Leadership Kevin

REPORT OF THE AUDITOR GENERAL

THE REPUBLIC OF UGANDA REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF UGANDA NATIONAL EDUCATION SUPPORT PROJECT (IDB-FUNDED) (LOAN AGREEMENT NOS: UG-0071 & UG-0076) FOR THE YEAR ENDED 30

THE REPUBLIC OF UGANDA REPORT OF THE AUDITOR GENERAL ON THE FINANCIAL STATEMENTS OF UGANDA NATIONAL EDUCATION SUPPORT PROJECT (IDB-FUNDED) (LOAN AGREEMENT NOS: UG-0071 & UG-0076) FOR THE YEAR ENDED 30

Big Walnut Local School District

Big Walnut Local School District Monthly Financial Report for the month ended September 30, 2013 Prepared By: Felicia Drummey Treasurer BIG WALNUT LOCAL SCHOOL DISTRICT SUMMARY OF YEAR TO DATE FINANCIAL

Big Walnut Local School District Monthly Financial Report for the month ended September 30, 2013 Prepared By: Felicia Drummey Treasurer BIG WALNUT LOCAL SCHOOL DISTRICT SUMMARY OF YEAR TO DATE FINANCIAL

Principles of Takaful

Principles of Takaful 2014 Information for candidates Developing knowledge and skills for the Takaful sector www.cii.co.uk overview Introduction Islamic (or Shariah) finance is a rapidly growing market

Principles of Takaful 2014 Information for candidates Developing knowledge and skills for the Takaful sector www.cii.co.uk overview Introduction Islamic (or Shariah) finance is a rapidly growing market

Financial Audit Procedures

Annex 1. Financial Audit Procedures 1.1 Audit Documentation and Evidence 1.1.1 Audit Documentation (Working Papers) The Auditor should, in accordance with ISA 230, prepare audit documentation that provides:

Annex 1. Financial Audit Procedures 1.1 Audit Documentation and Evidence 1.1.1 Audit Documentation (Working Papers) The Auditor should, in accordance with ISA 230, prepare audit documentation that provides:

Comparative Information Corresponding Figures and Comparative Financial Statements

SINGAPORE STANDARD SSA 710 ON AUDITING Comparative Information Corresponding Figures and Comparative Financial Statements This SSA 710 Comparative Information Corresponding Figures and Comparative Financial

SINGAPORE STANDARD SSA 710 ON AUDITING Comparative Information Corresponding Figures and Comparative Financial Statements This SSA 710 Comparative Information Corresponding Figures and Comparative Financial

Financial Accounting s Conceptual Foundations

Economics /Management 4 Financial Accounting Financial Accounting s Conceptual Foundations L-2 A highly-stylized Information System Basic Functions (all info systems): 1. Collection of transactions data

Economics /Management 4 Financial Accounting Financial Accounting s Conceptual Foundations L-2 A highly-stylized Information System Basic Functions (all info systems): 1. Collection of transactions data

TERMS OF REFERENCE FOR THE FINANCE AND AUDIT COMMITTEE

I. PURPOSE A. The primary function of the Finance and Audit Committee (the Committee ) is to assist the Board in fulfilling its oversight responsibilities by reviewing: i) the accuracy of financial information

I. PURPOSE A. The primary function of the Finance and Audit Committee (the Committee ) is to assist the Board in fulfilling its oversight responsibilities by reviewing: i) the accuracy of financial information

OF MANAGEMENT FOR THE SWANSEA TOWN HALL COMMUNITY CENTRE

F I N A N C I A L S T A T E M E N T S For For the year ended DECEMBER 31, 2014 INDEPENDENT AUDITOR'S REPORT To the Council of the Corporation of the CITY OF TORONTO AND THE BOARD OF MANAGEMENT FOR THE

F I N A N C I A L S T A T E M E N T S For For the year ended DECEMBER 31, 2014 INDEPENDENT AUDITOR'S REPORT To the Council of the Corporation of the CITY OF TORONTO AND THE BOARD OF MANAGEMENT FOR THE

Financial Statements of MOVEMBER CANADA. Year ended April 30, 2018

Financial Statements of MOVEMBER CANADA KPMG LLP Vaughan Metropolitan Centre 100 New Park Place, Suite 1400 Vaughan ON L4K 0J3 Canada Tel 905-265-5900 Fax 905-265-6390 INDEPENDENT AUDITORS' REPORT To the

Financial Statements of MOVEMBER CANADA KPMG LLP Vaughan Metropolitan Centre 100 New Park Place, Suite 1400 Vaughan ON L4K 0J3 Canada Tel 905-265-5900 Fax 905-265-6390 INDEPENDENT AUDITORS' REPORT To the

Guidelines for the preparation of a business plan pursuant to an application for the registration of a new Friendly Society as per Section 5 (1) of

of") Guidelines for the preparation of a business plan pursuant to an as per Section 5 (1) of the Friendly Societies Act, Act No. 25 1956 10 May 2016 Contents 1. INTRODUCTION... 1 2. BUSINESS PLAN FORMAT...

Guidelines for the preparation of a business plan pursuant to an as per Section 5 (1) of the Friendly Societies Act, Act No. 25 1956 10 May 2016 Contents 1. INTRODUCTION... 1 2. BUSINESS PLAN FORMAT...

28 August 2014 DOCUMENT C-M(2014)0050-AS1 IBAN REPORT ON THE AUDIT OF THE FINANCIAL STATEMENTS OF THE NATO PROVIDENT FUND FOR 2013 ACTION SHEET

0050-AS1 IBAN REPORT ON THE AUDIT OF THE FINANCIAL STATEMENTS OF THE NATO PROVIDENT FUND FOR 2013 ACTION SHEET") 28 August 2014 DOCUMENT C-M(2014)0050-AS1 IBAN REPORT ON THE AUDIT OF THE FINANCIAL STATEMENTS OF THE NATO PROVIDENT FUND FOR 2013 ACTION SHEET On 27 August 2014, under the silence procedure, the Council

28 August 2014 DOCUMENT C-M(2014)0050-AS1 IBAN REPORT ON THE AUDIT OF THE FINANCIAL STATEMENTS OF THE NATO PROVIDENT FUND FOR 2013 ACTION SHEET On 27 August 2014, under the silence procedure, the Council