INTERNAL AUDIT DIVISION REPORT 2017/038. Audit of general services contracts management in the United Nations Mission in the Republic of South Sudan

|

|

|

- Candace White

- 5 years ago

- Views:

Transcription

1 INTERNAL AUDIT DIVISION REPORT 2017/038 Audit of general services contracts management in the United Nations Mission in the Republic of South Sudan The Mission needed to implement costeffective arrangements for accommodating visitors and staff in transit, improve management of a hotel being leased, and strengthen controls over contract management 19 May 2017 Assignment No. AP2016/633/07

2 Audit of general services contracts management in the United Nations Mission in the Republic of South Sudan EXECUTIVE SUMMARY The objective of the audit was to assess the adequacy and effectiveness of governance, risk management and control processes over general services contracts management in the United Nations Mission in the Republic of South Sudan (UNMISS). The audit covered the period from 1 July 2013 to 31 December 2016 and included a review of: contract development, implementation and closure related to contracts for provision of leased hotel accommodation, three catering services contracts, duty-free commissary services, camp support services, fumigation and pest control, among others. UNMISS needed to implement cost-effective arrangements for accommodating visitors and staff in transit, improve management of a hotel being leased to minimize losses being incurred, and strengthen controls over general services contract management processes. OIOS made eight recommendations. To address issues identified in the audit, UNMISS needed to: Revisit the need to continue to lease a hotel at an annual cost of $560,000 that had a 50 per cent occupancy rate, and implement cost-effective arrangements to provide safe and secure temporary accommodation for staff and visitors and those in transit by considering other viable options such as constructing visitors accommodations or assigning private security personnel, within the existing security contract, to hotels cleared by the Department of Safety and Security; Review and reconcile the room occupancy records at the leased hotel and the General Services Section records with the cashier s and Finance Section recovery records and initiate the recovery of all uncollected room charges; Develop and implement guidance on managing activities related to the lease of temporary accommodation; Document reasons for waiving the requirement for security instruments and monitor the validity of all performance bonds for the duration of the respective contracts; Ensure contractors compliance with the requirement for appropriate insurance policies for their staff and assets; Obtain competitive prices of items sold at the duty-free commissary services and ensure the required customer surveys at cafeterias and at the duty-free commissary services are concluded to assess and, if necessary, improve the quality of services provided by contractors; Ensure contract performance review meetings include assessment of vendors compliance with agreed performance standards and quality of work and, where appropriate, use specific indicators and evaluation criteria; and Prepare closure reports for concluded contracts. UNMISS accepted the recommendations and has initiated action on some of them.

3 CONTENTS Page I. BACKGROUND 1 II. AUDIT OBJECTIVE, SCOPE AND METHODOLOGY 1 III. OVERALL CONCLUSION 1 IV. AUDIT RESULTS 2-8 A. Temporary accommodation for staff 2-3 B. Contract management 3-8 V. ACKNOWLEDGEMENT 8 ANNEX I APPENDIX I Status of audit recommendations Management response

4 Audit of general services contracts management in the United Nations Mission in the Republic of South Sudan I. BACKGROUND 1. The Office of Internal Oversight Services (OIOS) conducted an audit of general services contracts management in the United Nations Mission in the Republic of South Sudan (UNMISS). 2. The United Nations Procurement Manual defines contract management as the ongoing monitoring and management of vendors performance and obligations under contracts for goods, services or works. The Contracts Management Unit of the General Services Section (GSS) is responsible for providing oversight and monitoring of general services contracts. The Unit is headed by a staff at the P-3 level who directly reports to the Deputy Chief of GSS at the P-4 level. The Unit has three authorized posts, comprising two international staff and one United Nations volunteer. 3. From July 2013 to June 2016, the Mission had 20 general services contracts with a total not-toexceed amount of $21.2 million. As of December 2016, the GSS had 12 active contracts with a total notto-exceed amount of $11.2 million including for the provision of leased hotel accommodation for exclusive use by the Mission, three catering services contracts, duty-free commissary services, camp support services, fumigation and pest control. 4. Comments provided by UNMISS are incorporated in italics. II. AUDIT OBJECTIVE, SCOPE AND METHODOLOGY 5. The objective of the audit was to assess the adequacy and effectiveness of governance, risk management and control processes over general services contracts management in UNMISS. 6. This audit was included in the 2016 risk-based work plan of OIOS due to the operational and financial risks related to management of general services contracts in UNMISS. 7. OIOS conducted this audit from June 2016 to January The audit covered management of active general services contracts during the period from 1 July 2013 to 31 December Based on an activity-level risk assessment, the audit covered higher and medium risk areas in managing general services contracts, which included the development, implementation and closure of contracts related to provision of leased hotel accommodation, three catering services contracts, camp support services, fumigation and pest control, among others. 8. The audit methodology included: (a) assessment of internal controls, (b) interviews of key personnel, (c) review of relevant documentation, (d) test of controls on a sample basis using judgmental sampling, and (e) site visits to select contractors premises in Juba. III. OVERALL CONCLUSION 9. UNMISS needed to implement cost-effective arrangements for accommodating visitors and staff in transit and improve the current management of a leased hotel to minimize losses being incurred. UNMISS also needed to strengthen controls over its general services contracts management processes such as: documenting reasons for waiving security instruments; monitoring contractors compliance with

5 contractual terms; conducting adequate performance reviews with contractors; conducting customer surveys for the duty-free commissary and catering services; and preparing contract closure reports. IV. AUDIT RESULTS A. Temporary accommodation for staff Need for more cost-effective arrangements for the accommodation of visitors and staff in transit 10. United Nations Financial Regulation 5.12 requires the Mission to consider best value for money in procuring goods and services. 11. Due to the security situation in Juba following the December 2013 crisis, UNMISS leased a hotel to temporarily accommodate staff on travel status at an annual rental of $725,000. The contract was for a period of one year from 22 January 2014 to 21 January Due to exigency, the procurement for the leased hotel accommodation did not follow a formal solicitation process, and instead UNMISS entered into a memorandum of undertaking with the vendor pending signing of a lease contract. The lease was subsequently signed for one year to January 2015, longer than initially expected, as the Mission did not have plans to build new accommodations. After review by the Local and Headquarters Committees on Contracts and approval by the Assistant Secretary-General for Central Support Services, the Mission extended the lease: (a) for 11 months to 21 January 2016 at $725,000; and (b) for 12 months to 21 January 2017 at $623, In January 2017, the Mission requested for Headquarters Committee on Contracts review and the Assistant Secretary-General for Central Support Services approval to extend the lease for three more years at an annual rental of $561,150. This request was made even though the hotel only had an occupancy rate of 50 per cent, and resulted in the Mission incurring avoidable costs. 13. OIOS appreciates that UNMISS needed to provide safe and secure accommodation for staff visiting the Mission or in transit to a Mission location, which was guided by the Department of Safety and Security (DSS) security risk assessment. However, UNMISS was unable to provide OIOS with evidence that they had adequately considered other viable options prior to the lease renewals, such as: (a) constructing additional self-contained prefabricated structures similar to those used by UNMISS staff within the Tomping compound; (b) constructing transit accommodations (permanent/prefabricated) within the United Nations House; and (c) assigning private security personnel (within the existing security contract) to augment the security in selected hotels (as at 27 January 2017, DSS had cleared nine hotels for residential accommodation and four hotels for workshops and conferences only). 14. As a result, UNMISS proposed to continue to lease a hotel at an annual cost of $561,150 for up to three years that only had an occupancy rate of 50 per cent, without establishing sufficient cost-recovery mechanisms and addressing low occupancy rates. The lease arrangement therefore resulted in a financial loss of $1.3 million over a three-year period as indicated in Table 1. 2

6 Table 1: Comparison of revenues and costs for the lease for the period Total Total revenue reported to Local Committee $698,891 $606,204 $446,033 $1,751,128 on Contracts by GSS Unrecovered room charges* (245,458) (103,712) (66,005) (415,175) Lease payment (725,000) (725,000) (623,500) (2,073,500) Fuel provided by the Mission (129,600) (129,600) (129,600) (388,800) Engineering works performed by the Mission (162,714) (162,714) Surplus/(Loss) ($563,881) ($352,108) ($373,072) ($1,289,061) * This represents amounts reported in GSS revenue reports that could not be vouched to payments in Umoja. The aggregate amount of unrecovered room charges from 2014 to 2016 as per the Finance Section was even higher at $500,000. (1) UNMISS should revisit the need to continue to lease a hotel at an annual cost of over $500,000, which has only a 50 per cent occupancy rate, and take action to implement costeffective arrangements to provide safe and secure temporary accommodation for staff and visitors and those in transit by considering other viable options such as constructing visitors accommodations or assigning private security personnel within the existing security contract to hotels cleared by the Department of Safety and Security. UNMISS accepted recommendation 1and stated that given the existing political and security situation in Juba, there were no immediate plans to discontinue the lease of the hotel because it was in a strategic and secure location in close proximity to the Juba International Airport; it served as a safe haven and secondary evacuation point for staff from other field offices; and complemented UNMISS transit accommodation capacity. The Mission also stated that future use of the hotel would be reviewed taking into account its strategic and operational requirements as dictated by the political and security situation in the country, and the economic viability of the lease. UNMISS would also continue to allocate resources toward improving the existing transit accommodation including by the construction of 150 prefabricated units in Tomping, a number of which would be allocated as transit units. Recommendation 1 remains open pending receipt of evidence that the Mission has considered and implemented cost-effective arrangements to provide safe and secure temporary accommodation for staff and visitors and those in transit. B. Contract management Inadequate procedures over the leasing of accommodation for visitors and staff in transit 15. The Mission is required to establish and implement adequate controls to account for revenues generated from its leased hotel property and to offset the cost of leasing the hotel which included $2,073,500 in lease payments and $388,800 for cost of fuel provided. UNMISS procedures require GSS to manage room occupancy with the vendor, authorize all those staying in the leased hotel and recover all amounts due. GSS is also required to: (a) prepare monthly summaries of invoices and payments; (b) provide the Finance Section with a monthly summary report of unpaid room invoices to be recovered from staff through payroll deduction; and (c) obtain daily occupancy reports from the vendor. 16. A review of hotel bookings and occupancy reports for the period January 2016 to December 2016, review of 36 monthly invoice/payment summary records as well as analysis of revenues and costs of operating the lease for the period 2014 to 2016 indicated that GSS prepared periodic invoice and payment summaries, but they did not perform a number of other required functions effectively as follows: 3

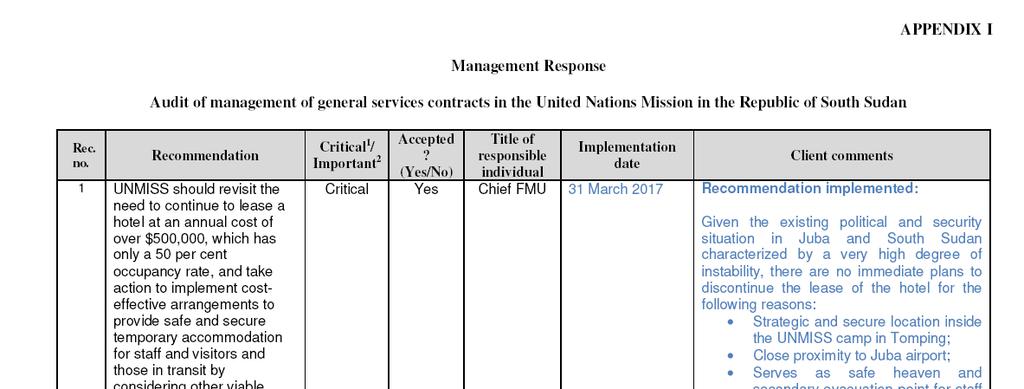

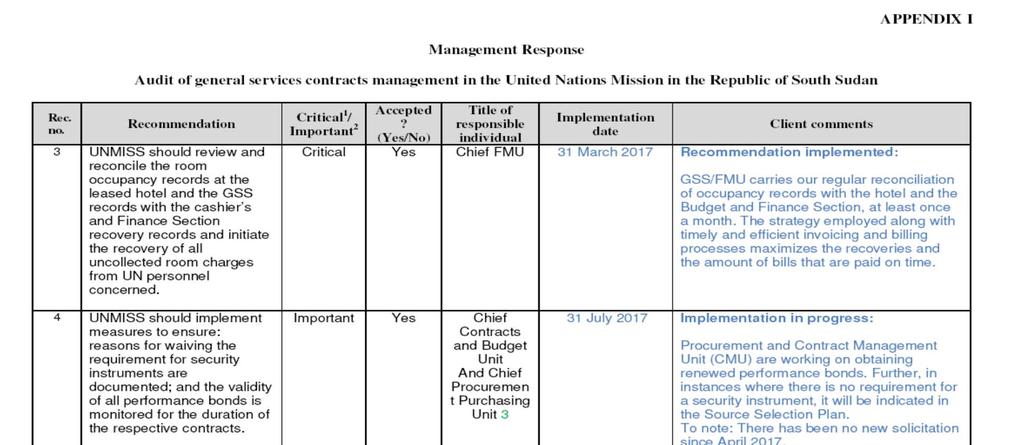

7 Although the room occupancy rate dropped from 100 per cent in 2014 to an average of 50 per cent as at October 2016, the Mission did not consider how to minimize the losses being incurred; GSS was not recovering unpaid room charges that had accumulated to over $400,000 as shown in Table 1; The Mission did not implement adequate controls to mitigate the risk of guests staying in the hotel or extending their stay without GSS authorization and room charges not being paid to the Finance Section; GSS did not reconcile room occupancy reports from the hotel with payments received by the Finance Section to promptly identify and recover unpaid room charges; and The Finance Section did not reconcile invoice and payment summaries prepared by GSS with Umoja to ensure that all payments were accounted for. 17. As a result, the Mission: (a) was contracting hotel accommodation at a significant loss, calculated by OIOS at nearly $1.3 million over three years; and (b) did not have adequate procedures in place to mitigate the risk of losses, which had accumulated to over $400,000 due to unpaid invoices as indicated in Table 1. For instance, OIOS noted 32 guests that were included in the hotel s daily occupancy report but were not included in the GSS occupancy reports and the related recovery records. 18. The above occurred because the Mission had not conducted a comprehensive management review of the lease and issued and implemented guidance and procedures on managing activities related to the lease. (2) UNMISS should develop and implement guidance on managing the activities related to the lease for the temporary accommodation of staff and visitors to minimize losses resulting from unpaid invoices and personnel occupying rooms without authorization. UNMISS accepted recommendation 2 and stated that it had promulgated Mission Directive No. 2017/002 on 3 March 2017, providing details governing management of the leased hotel as charges for various categories of staff. Mission Directive No. 2017/002 did not fully address the need for stronger controls in the operation of the leased hotel accommodation. Recommendation 2 remains open pending receipt of more comprehensive guidance and procedures on the operation, management and accounting for the leased hotel accommodation and evidence that measures have been implemented to minimize losses from the hotel lease. (3) UNMISS should review and reconcile the room occupancy records at the leased hotel and the General Services Section records with the cashier s and Finance Section recovery records and initiate the recovery of all uncollected room charges from United Nations personnel concerned. UNMISS accepted recommendation 3 and stated that GSS and the Finance Section carried out monthly reconciliation of their records. Recommendation 3 remains open pending receipt of evidence that GSS and the Finance Section have reconciled room occupancy and collection records from 2014 to 2016 and the Mission initiated recovery of uncollected hotel room revenues for the period. 4

8 Performance bonds were not monitored effectively 19. The United Nations General Conditions of Contracts require UNMISS to obtain and maintain valid performance bonds to protect the United Nations against the risk of loss in the event a contractor fails to perform its obligations under a contract. The Procurement Manual requires the Chief Procurement Officer to approve and document all decisions to exclude requirements for security instruments such as performance bonds, and the Contracts Management Unit to ensure the validity of these instruments for the duration of the related contracts. 20. OIOS review of 13 active general services contracts indicated that six contracts with an aggregate value of $8.6 million required vendors to post performance bonds. At the time of audit in June 2016, the performance bonds for three of these six contracts had expired. UNMISS subsequently obtained a bond for one of the contracts on 8 September 2016, but did not obtain updated bonds for the other two contracts. The other seven contracts with an aggregate value of $2.6 million did not require performance bonds because the Mission waived the requirement. However, the Chief Procurement Officer did not document the reasons for waiving the requirement. 21. The above resulted because UNMISS had not implemented effective monitoring procedures to ensure the required bonds were valid during the entire contract period and to ensure the Chief Procurement Officer documented reasons for waiving bond requirements. Consequently, there was risk of financial loss in the event contractors failed to meet their contractual obligations. (4) UNMISS should implement measures to ensure: reasons for waiving the requirement for security instruments are documented; and the validity of all performance bonds is monitored for the duration of the respective contracts. UNMISS accepted recommendation 4 and stated that it would document the reasons for waiving the requirement for security instruments in source selection plans. The Mission also stated that the Contracts Management Unit and the Procurement Section would work together to ensure that renewed performance bonds were obtained. Recommendation 4 remains open pending receipt of evidence that the Mission documents reasons for waiving the requirement for security instruments in source selection plans and that it was monitoring s the security instruments to ensure they remain valid for the duration of the contracts. Need to enforce contractual provisions relating to submission of insurance policies 22. The United Nations General Conditions of Contracts require UNMISS to enforce the requirement for contractors to maintain liability insurance for their equipment and property, and workers compensation for their employees. 23. A review of all 29 general services contracts indicated that only the lease for the hotel for accommodating staff on travel status and the contract for duty-free commissary services required insurance policies. The lease for the hotel required UNMISS to obtain from the contractor: (a) comprehensive insurance for the premises covering all risks such as fire, explosion, civil strife, earthquake, flood and war; and (b) proof of public liability insurance covering UNMISS as an additional insured party from claims against the Mission. The contract for the duty-free commissary services required the Mission to obtain from the contractor proof of accident and life insurance for its employees. UNMISS did not obtain the required comprehensive coverage and was unable to provide evidence that the Mission had accident and life insurance coverage from the two contractors. 5

9 24. The above resulted because GSS did not take steps to enforce the requirements for insurance coverage. Due to the absence of the required insurance coverage for contractors assets and their employees, there was a reputational risk and risk of financial loss that may result from claims against UNMISS for the actions of contractors. (5) UNMISS should monitor and enforce contractors compliance with the requirement for appropriate insurance policies. UNMISS accepted recommendation 5 and stated that GSS has developed and was in the process of implementing a mechanism to ensure contractors compliance with documentation requirements including the submission of insurance policies, where required, to ensure that required documents were submitted and received without exception. Recommendation 5 remains open pending receipt of evidence that UNMISS has implemented measures to ensure contractors compliance with documentation requirements including the submission of insurance policies and was monitoring the submission of required insurance documents. Need to conduct price and customer surveys 25. The three contracts for catering and duty-free commissary services require UNMISS to conduct: (a) periodic customer surveys to obtain customers feedback on the quality of services provided by the contractors; and (b) price surveys to confirm the competitiveness of the prices of goods sold at the dutyfree facility and to claim for a rebate should the prices be found to be unreasonably higher than the prices offered by other suppliers. 26. GSS had carried out one price survey with respect to the prices of food served by the caterers in UNMISS compounds. The Mission however had not conducted any: (a) customer surveys to obtain feedback on the quality of services of the duty-free commissary services contractor and all three catering service contractors in UNMISS Headquarters in Juba; and (b) formal surveys of prices of commonly used items in the duty-free commissary. As a result, the Mission missed the opportunity to take prompt corrective actions to improve the quality of services provided by the contractors and to exercise its right to claim rebates from the duty-free commissary services contractor. A comparison of the prices of 21 common items sold in the duty-free commissary with prices of similar items in one of the largest retail outlets in Juba indicated that the prices offered by the contractor were higher, on average, by 52 per cent. 27. The above occurred because the Mission had not taken appropriate actions such as clarifying responsibilities and developing and implementing an action plan to ensure the required surveys were conducted. UNMISS advised that the contract did not explicitly allocate responsibility for the task or state the frequency of the reviews. (6) UNMISS should take appropriate actions such as clarifying responsibilities and implementing an action plan to obtain competitive prices of items sold at the duty-free commissary and ensure the required customer surveys for the duty-free commissary service and cafeterias are conducted to assess and, if necessary, improve the quality of services provided by contractors. UNMISS accepted recommendation 6 and stated that GSS had conducted an informal survey of the items sold in the duty-free commissary and used the related results to encourage competition by allowing a local supplier to open a supermarket within the United Nations House compound. The Mission also advised that formal surveys would be conducted to assess the outcome of its decision and GSS would review the terms of reference for the duty-free commissary services to include additional responsibility related to monitoring and evaluation of goods and services. 6

10 Recommendation 6 remains open pending receipt of evidence that the Mission has conducted the required price and customer satisfaction surveys and taken prompt corrective actions, where necessary, related to the services provided by contractors and prices offered by the duty-free commissary. Monitoring and evaluation of vendors performance needed improvement 28. The Procurement Manual requires UNMISS to regularly monitor and review contractors performance against key performance indicators (KPIs) and submit to the Director of Mission Support contract performance reports in the frequency specified in the respective contracts. The Manual also requires: (a) the Contracts Management Unit and the responsible self-accounting unit to hold regular performance review meetings with contractors and maintain adequate records on contracts management activities; and (b) end users to develop specific performance measurement criteria against which vendors performance could be monitored and measured. 29. OIOS reviewed 20 locally procured contracts and noted that for six contracts, although the Mission conducted contractors performance review meetings and carried out inspections of contractors premises, the meetings mainly focused on addressing problems reported by the contractors and GSS did not assess their performance against established KPIs. For another seven contracts, GSS was not monitoring performance against the KPIs specifically developed and agreed with the contractors. Instead, GSS relied on self-assessments carried out by the contractors without independently verifying their accuracy. 30. GSS also did not regularly report to the Director of Mission Support on contractors performance. For instance, during the audit period, GSS: prepared only one performance evaluation report for one of two contracts that required monthly performance reviews and only one performance evaluation report for one of four contracts that required quarterly reviews each; and did not assess the performance of vendors for six contracts that had expired during the audit period. 31. The above occurred because GSS did not take adequate and effective steps such as implementing a timetable for performance review meetings to evaluate the contractors performance and prepare the related reports. GSS started requiring contractors to provide information on KPIs in March 2016 after a change in management of the Contracts Management Unit of GSS but it was not yet taking proactive action to obtain the required data and independently assess the performance of contractors. 32. As a result of the lack of adequate performance monitoring and reporting, there was an increased risk that the Mission did not promptly identify poor performance and take appropriate remedial action in a timely manner. For instance, OIOS observed some delays in the services provided in one of the cafeterias as well as unavailability of some stock items in the duty-free commissary. (7) UNMISS should take action to ensure required performance review meetings are held and contractors performance is assessed, measured and reported against agreed key performance indicators. UNMISS accepted recommendation 7 and stated that contractors had been requested to meet performance standards in accordance with the agreed KPIs. The Mission added that contract focal points would assess, measure and document performance against the KPIs and results would be reflected in the contractors performance evaluation reports. Recommendation 7 remains open pending receipt of evidence that UNMISS is holding performance review meetings and contractors performance is being assessed, measured and reported against agreed KPIs. 7

11 Contract closure reports were not prepared 33. The Department of Peacekeeping Operations/Department of Field Support Contract Management Policy requires UNMISS to evaluate the contractors performance and prepare closure reports. 34. A review of 13 of 20 general services contracts that expired during the audit period indicated that UNMISS only evaluated the performance of two contractors and prepared a closure report for one of these two contractors. The Mission had not evaluated the performance of 11 of the 13 expired contracts and prepared the related closure reports for the other 12 expired contracts. This was because the Contracts Management Unit did not take action to ensure the performance evaluation of contractors was done following the completion of the contract. 35. As a result, lessons learned and best practices were not documented and there was a risk of: (a) financial loss that may result from non-recovery of equipment provided by the Mission to the contractors; and (b) rehiring contractors who performed poorly. (8) UNMISS should implement procedures to ensure that the performance of contractors managed by the General Services Section is assessed upon expiration of the contract and that closure reports are prepared for concluded contracts. UNMISS accepted recommendation 8 and stated that standard operating procedures for contract close-out was being drafted. This would emphasize the need for a contract close-out report to be prepared and completed within three months following contract expiration. Recommendation 8 remains open pending receipt of evidence that UNMISS has implemented procedures for evaluating the performance of contractors and is preparing the related closure reports following the expiration or termination of contracts. V. ACKNOWLEDGEMENT 36. OIOS wishes to express its appreciation to the management and staff of UNMISS for the assistance and cooperation extended to the auditors during this assignment. (Signed) Eleanor T. Burns Director, Internal Audit Division Office of Internal Oversight Services 8

12 ANNEX I STATUS OF AUDIT RECOMMENDATIONS Audit of general services contracts management in the United Nations Mission in the Republic of South Sudan Rec. no. Recommendation 1 UNMISS should revisit the need to continue to lease a hotel at an annual cost of over $500,000, which has only a 50 per cent occupancy rate, and take action to implement cost-effective arrangements to provide safe and secure temporary accommodation for staff and visitors and those in transit by considering other viable options such as constructing visitors accommodations or assigning private security personnel within the existing security contract to hotels cleared by the Department of Safety and Security. 2 UNMISS should develop and implement guidance on managing the activities related to the lease for the temporary accommodation of staff and visitors to minimize losses resulting from unpaid invoices and personnel occupying rooms without authorization. 3 UNMISS should review and reconcile the room occupancy records at the leased hotel and the GSS records with the cashier s and Finance Section recovery records and initiate the recovery of all uncollected room charges from United Nations personnel concerned. 4 UNMISS should implement measures to ensure: reasons for waiving the requirement for security Critical 1 / C/ Important 2 O 3 Actions needed to close recommendation Important O Receipt of evidence that the Mission has considered and implemented cost-effective arrangements to provide safe and secure temporary accommodation for staff and visitors and those in transit. Important O Receipt more comprehensive guidance and procedures on the operation, management and accounting for the leased hotel accommodation and evidence that measures have been implemented to minimize losses from the hotel lease. Important O Receipt of evidence that GSS and the Finance Section have reconciled room occupancy and collection records from 2014 to 2016 and the Mission initiated recovery of uncollected hotel room revenues for the period. Important O Receipt of evidence that the Mission documents reasons for waiving the requirement for security Implementation date 4 30 June June June July Critical recommendations address critical and/or pervasive deficiencies in governance, risk management or control processes, such that reasonable assurance cannot be provided with regard to the achievement of control and/or business objectives under review. 2 Important recommendations address important (but not critical or pervasive) deficiencies in governance, risk management or control processes, such that reasonable assurance may be at risk regarding the achievement of control and/or business objectives under review. 3 C = closed, O = open 4 Date provided by UNMISS in response to recommendations.

13 ANNEX I STATUS OF AUDIT RECOMMENDATIONS Audit of general services contracts management in the United Nations Mission in the Republic of South Sudan Rec. no. Recommendation instruments are documented; and the validity of all performance bonds is monitored for the duration of the respective contracts. 5 UNMISS should monitor and enforce contractors compliance with the requirement for appropriate insurance policies. 6 UNMISS should take appropriate actions such as clarifying responsibilities and implementing an action plan to obtain competitive prices of items sold at the duty-free commissary and ensure the required customer surveys for the duty-free commissary service and cafeterias are conducted to assess and, if necessary, improve the quality of services provided by contractors. 7 UNMISS should take action to ensure required performance review meetings are held and contractors performance is assessed, measured and reported against agreed key performance indicators. 8 UNMISS should implement procedures to ensure that the performance of contractors managed by the General Services Section is assessed upon expiration of the contract and that closure reports are prepared for concluded contracts. Critical 1 / C/ Important 2 O 3 Actions needed to close recommendation instruments in source selection plans and that it was monitoring the security instruments to ensure they remain valid for the duration of the contracts.. Important O Receipt of evidence that UNMISS has implemented measures to ensure contractors compliance with documentation requirements including the submission of insurance policies and was monitoring the submission of required insurance documents Important O Receipt of evidence that the Mission has conducted the required price and customer satisfaction surveys and taken prompt corrective actions, where necessary, related to the services provided by contractors and prices offered by the duty-free commissary Important O Receipt of evidence that UNMISS is holding performance review meetings and contractors performance is being assessed, measured and reported against agreed KPIs. Important O Receipt of evidence that UNMISS has implemented procedures for evaluating the performance of contractors and is preparing the related closure reports following the expiration or termination of contracts. Implementation date 4 31 July June June June

14 APPENDIX I Management Response

15

16

17

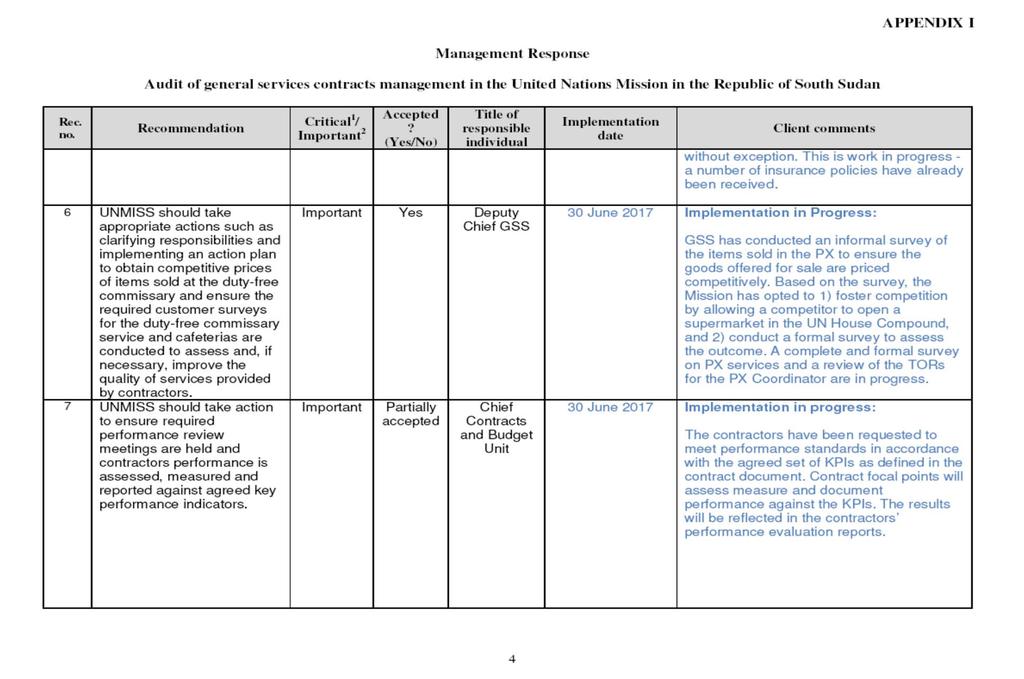

18

19

REPORT 2016/088 INTERNAL AUDIT DIVISION. Audit of rations management in the United Nations Mission in the Republic of South Sudan

INTERNAL AUDIT DIVISION REPORT 2016/088 Audit of rations management in the United Nations Mission in the Republic of South Sudan Overall results relating to the effective management of rations were initially

INTERNAL AUDIT DIVISION REPORT 2016/088 Audit of rations management in the United Nations Mission in the Republic of South Sudan Overall results relating to the effective management of rations were initially

REPORT 2015/123 INTERNAL AUDIT DIVISION. Audit of the management of engineering projects in the United Nations Mission in the Republic of South Sudan

INTERNAL AUDIT DIVISION REPORT 2015/123 Audit of the management of engineering projects in the United Nations Mission in the Republic of South Sudan Overall results relating to the effective management

INTERNAL AUDIT DIVISION REPORT 2015/123 Audit of the management of engineering projects in the United Nations Mission in the Republic of South Sudan Overall results relating to the effective management

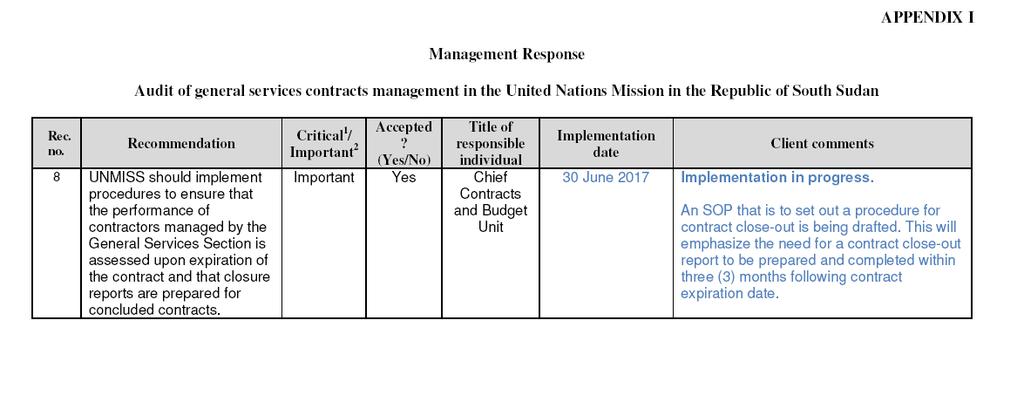

REPORT 2016/038 INTERNAL AUDIT DIVISION. Audit of the Office for the Coordination of Humanitarian Affairs operations in South Sudan

INTERNAL AUDIT DIVISION REPORT 2016/038 Audit of the Office for the Coordination of Humanitarian Affairs operations in South Sudan Overall results relating to the effective management of operations in

INTERNAL AUDIT DIVISION REPORT 2016/038 Audit of the Office for the Coordination of Humanitarian Affairs operations in South Sudan Overall results relating to the effective management of operations in

REPORT 2013/142. Audit of accounts receivable and payable in the United Nations Operation in Côte d Ivoire

INTERNAL AUDIT DIVISION REPORT 2013/142 Audit of accounts receivable and payable in the United Nations Operation in Côte d Ivoire Overall results relating to the effective management of accounts receivable

INTERNAL AUDIT DIVISION REPORT 2013/142 Audit of accounts receivable and payable in the United Nations Operation in Côte d Ivoire Overall results relating to the effective management of accounts receivable

INTERNAL AUDIT DIVISION REPORT 2017/073. Audit of accounts receivable and payable in the United Nations Operation in Côte d voire

INTERNAL AUDIT DIVISION REPORT 2017/073 Audit of accounts receivable and payable in the United Nations Operation in Côte d voire There was a need for comprehensive review of accounts receivable and to

INTERNAL AUDIT DIVISION REPORT 2017/073 Audit of accounts receivable and payable in the United Nations Operation in Côte d voire There was a need for comprehensive review of accounts receivable and to

REPORT 2014/107 INTERNAL AUDIT DIVISION. Audit of quick-impact projects in the African Union-United Nations Hybrid Operation in Darfur

INTERNAL AUDIT DIVISION REPORT 2014/107 Audit of quick-impact projects in the African Union-United Nations Hybrid Operation in Darfur Overall results relating to the management of quick-impact projects

INTERNAL AUDIT DIVISION REPORT 2014/107 Audit of quick-impact projects in the African Union-United Nations Hybrid Operation in Darfur Overall results relating to the management of quick-impact projects

REPORT 2014/134 INTERNAL AUDIT DIVISION. Audit of financial and administrative functions in the United Nations Truce Supervision Organization

INTERNAL AUDIT DIVISION REPORT 2014/134 Audit of financial and administrative functions in the United Nations Truce Supervision Organization Overall results relating to the effectiveness of financial and

INTERNAL AUDIT DIVISION REPORT 2014/134 Audit of financial and administrative functions in the United Nations Truce Supervision Organization Overall results relating to the effectiveness of financial and

REPORT 2015/072 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/072 Audit of minimum operating residential security standards entitlements for staff in the United Nations Operation in Côte d Ivoire Overall results relating to the

INTERNAL AUDIT DIVISION REPORT 2015/072 Audit of minimum operating residential security standards entitlements for staff in the United Nations Operation in Côte d Ivoire Overall results relating to the

INTERNAL AUDIT DIVISION REPORT 2017/126. Audit of trust fund activities in the African Union-United Nations Hybrid Operation in Darfur

INTERNAL AUDIT DIVISION REPORT 2017/126 Audit of trust fund activities in the African Union-United Nations Hybrid Operation in Darfur The Mission needed to enhance its supervision of project site inspections

INTERNAL AUDIT DIVISION REPORT 2017/126 Audit of trust fund activities in the African Union-United Nations Hybrid Operation in Darfur The Mission needed to enhance its supervision of project site inspections

INTERNAL AUDIT DIVISION REPORT 2017/136. Audit of finance and human resources management in the United Nations Disengagement Observer Force

INTERNAL AUDIT DIVISION REPORT 2017/136 Audit of finance and human resources management in the United Nations Disengagement Observer Force The Mission needed to enhance budget monitoring and review the

INTERNAL AUDIT DIVISION REPORT 2017/136 Audit of finance and human resources management in the United Nations Disengagement Observer Force The Mission needed to enhance budget monitoring and review the

REPORT 2014/070 INTERNAL AUDIT DIVISION. Audit of civil affairs activities in the. United Nations Stabilization Mission in Haiti

INTERNAL AUDIT DIVISION REPORT 2014/070 Audit of civil affairs activities in the United Nations Stabilization Mission in Haiti Overall results relating to the effective management of civil affairs activities

INTERNAL AUDIT DIVISION REPORT 2014/070 Audit of civil affairs activities in the United Nations Stabilization Mission in Haiti Overall results relating to the effective management of civil affairs activities

INTERNAL AUDIT DIVISION REPORT 2017/025

INTERNAL AUDIT DIVISION REPORT 2017/025 Audit of quick impact projects in the United Nations Multidimensional Integrated Stabilization Mission in the Central African Republic There was a need to strengthen

INTERNAL AUDIT DIVISION REPORT 2017/025 Audit of quick impact projects in the United Nations Multidimensional Integrated Stabilization Mission in the Central African Republic There was a need to strengthen

REPORT 2015/085 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/085 Audit of the United Nations Stabilization Mission in Haiti s trust fund to strengthen specialized sexual and gender-based crimes police cells and units within the

INTERNAL AUDIT DIVISION REPORT 2015/085 Audit of the United Nations Stabilization Mission in Haiti s trust fund to strengthen specialized sexual and gender-based crimes police cells and units within the

REPORT 2015/041 INTERNAL AUDIT DIVISION. Audit of the United Nations Mine Action Service of the Department of Peacekeeping Operations

INTERNAL AUDIT DIVISION REPORT 2015/041 Audit of the United Nations Mine Action Service of the Department of Peacekeeping Operations Overall results relating to the effective management of mine action

INTERNAL AUDIT DIVISION REPORT 2015/041 Audit of the United Nations Mine Action Service of the Department of Peacekeeping Operations Overall results relating to the effective management of mine action

INTERNAL AUDIT DIVISION REPORT 2017/139

INTERNAL AUDIT DIVISION REPORT 2017/139 Audit of budget formulation and monitoring in the United Nations Multidimensional Integrated Stabilization Mission in the Central African Republic MINUSCA needed

INTERNAL AUDIT DIVISION REPORT 2017/139 Audit of budget formulation and monitoring in the United Nations Multidimensional Integrated Stabilization Mission in the Central African Republic MINUSCA needed

REPORT 2016/081 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/081 Audit of selected subprogrammes and related technical cooperation projects in the Economic and Social Commission for Western Asia Overall results relating to the

INTERNAL AUDIT DIVISION REPORT 2016/081 Audit of selected subprogrammes and related technical cooperation projects in the Economic and Social Commission for Western Asia Overall results relating to the

REPORT 2016/012 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/012 Audit of the management of the technical cooperation project on Information and Communication Technologies in Africa Phase II in the Economic Commission for Africa

INTERNAL AUDIT DIVISION REPORT 2016/012 Audit of the management of the technical cooperation project on Information and Communication Technologies in Africa Phase II in the Economic Commission for Africa

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/078

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/078 Audit of the United Nations Environment Programme s Secretariat of the Convention on Biological Diversity Overall results relating to the provision of efficient

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/078 Audit of the United Nations Environment Programme s Secretariat of the Convention on Biological Diversity Overall results relating to the provision of efficient

INTERNAL AUDIT DIVISION REPORT 2016/155. Audit of the United Nations Human Settlements Programme project management process

INTERNAL AUDIT DIVISION REPORT 2016/155 Audit of the United Nations Human Settlements Programme project management process Established policies and procedures need to be further strengthened, particularly

INTERNAL AUDIT DIVISION REPORT 2016/155 Audit of the United Nations Human Settlements Programme project management process Established policies and procedures need to be further strengthened, particularly

REPORT 2015/079 INTERNAL AUDIT DIVISION. Audit of United Nations Office on Drugs and Crime operations in Peru

INTERNAL AUDIT DIVISION REPORT 2015/079 Audit of United Nations Office on Drugs and Crime operations in Peru Overall results relating to the management of operations in Peru were initially assessed as

INTERNAL AUDIT DIVISION REPORT 2015/079 Audit of United Nations Office on Drugs and Crime operations in Peru Overall results relating to the management of operations in Peru were initially assessed as

REPORT 2015/178 INTERNAL AUDIT DIVISION. Audit of the United Nations Human Settlements Programme Regional Office for Arab States

INTERNAL AUDIT DIVISION REPORT 2015/178 Audit of the United Nations Human Settlements Programme Regional Office for Arab States Overall results relating to Regional Office for Arab States operations were

INTERNAL AUDIT DIVISION REPORT 2015/178 Audit of the United Nations Human Settlements Programme Regional Office for Arab States Overall results relating to Regional Office for Arab States operations were

REPORT 2016/054 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/054 Audit of selected subprogrammes and related technical cooperation projects in the Economic Commission for Europe Overall results relating to the effective management

INTERNAL AUDIT DIVISION REPORT 2016/054 Audit of selected subprogrammes and related technical cooperation projects in the Economic Commission for Europe Overall results relating to the effective management

REPORT 2016/105 INTERNAL AUDIT DIVISION. Audit of investment management in the Office of Programme Planning, Budget and Accounts

INTERNAL AUDIT DIVISION REPORT 2016/105 Audit of investment management in the Office of Programme Planning, Budget and Accounts Overall results relating to the effective management of investments were

INTERNAL AUDIT DIVISION REPORT 2016/105 Audit of investment management in the Office of Programme Planning, Budget and Accounts Overall results relating to the effective management of investments were

INTERNAL AUDIT DIVISION REPORT 2017/003

INTERNAL AUDIT DIVISION REPORT 2017/003 Audit of the management of the sustainable development subprogramme in the Department of Economic and Social Affairs The Division for Sustainable Development needed

INTERNAL AUDIT DIVISION REPORT 2017/003 Audit of the management of the sustainable development subprogramme in the Department of Economic and Social Affairs The Division for Sustainable Development needed

REPORT 2017/148. Audit of budget formulation and monitoring in the United Nations Interim Force in Lebanon

INTERNAL AUDIT DIVISION REPORT 2017/148 Audit of budget formulation and monitoring in the United Nations Interim Force in Lebanon The Mission aligned its budget with its mandate and improved budget monitoring,

INTERNAL AUDIT DIVISION REPORT 2017/148 Audit of budget formulation and monitoring in the United Nations Interim Force in Lebanon The Mission aligned its budget with its mandate and improved budget monitoring,

REPORT 2015/095 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/095 Review of recurrent issues identified in recent internal audit engagements for the Office for the Coordination of Humanitarian Affairs 8 September 2015 Assignment

INTERNAL AUDIT DIVISION REPORT 2015/095 Review of recurrent issues identified in recent internal audit engagements for the Office for the Coordination of Humanitarian Affairs 8 September 2015 Assignment

INTERNAL AUDIT DIVISION REPORT 2018/014. Audit of quick-impact projects in the African Union-United Nation Hybrid Operation in Darfur

INTERNAL AUDIT DIVISION REPORT 2018/014 Audit of quick-impact projects in the African Union-United Nation Hybrid Operation in Darfur The Mission needed to ensure that completed projects are used, field

INTERNAL AUDIT DIVISION REPORT 2018/014 Audit of quick-impact projects in the African Union-United Nation Hybrid Operation in Darfur The Mission needed to ensure that completed projects are used, field

INTERNAL AUDIT DIVISION REPORT 2018/052. Audit of liquidation activities at the International Criminal Tribunal for the former Yugoslavia

INTERNAL AUDIT DIVISION REPORT 2018/052 Audit of liquidation activities at the International Criminal Tribunal for the former Yugoslavia Overall, liquidation activities were performed satisfactorily 31

INTERNAL AUDIT DIVISION REPORT 2018/052 Audit of liquidation activities at the International Criminal Tribunal for the former Yugoslavia Overall, liquidation activities were performed satisfactorily 31

REPORT 2014/153 INTERNAL AUDIT DIVISION. Audit of the United Nations Office for Disaster Risk Reduction

INTERNAL AUDIT DIVISION REPORT 2014/153 Audit of the United Nations Office for Disaster Risk Reduction Overall results relating to the effective management of the United Nations Office for Disaster Risk

INTERNAL AUDIT DIVISION REPORT 2014/153 Audit of the United Nations Office for Disaster Risk Reduction Overall results relating to the effective management of the United Nations Office for Disaster Risk

REPORT 2016/062 INTERNAL AUDIT DIVISION. Audit of the management of trust funds at the United Nations Framework Convention on Climate Change

INTERNAL AUDIT DIVISION REPORT 2016/062 Audit of the management of trust funds at the United Nations Framework Convention on Climate Change Overall results relating to the effective management of trust

INTERNAL AUDIT DIVISION REPORT 2016/062 Audit of the management of trust funds at the United Nations Framework Convention on Climate Change Overall results relating to the effective management of trust

REPORT 2014/068 INTERNAL AUDIT DIVISION. Audit of the United Nations Office on Drugs and Crime Intelligence and Law Enforcement Systems project

INTERNAL AUDIT DIVISION REPORT 2014/068 Audit of the United Nations Office on Drugs and Crime Intelligence and Law Enforcement Systems project Overall results relating to management of the Intelligence

INTERNAL AUDIT DIVISION REPORT 2014/068 Audit of the United Nations Office on Drugs and Crime Intelligence and Law Enforcement Systems project Overall results relating to management of the Intelligence

DESK REVIEW UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN

UNITED NATIONS DEVELOPMENT PROGRAMME DESK REVIEW OF UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN Report No. 1310 Issue Date: 9 October 2014 Table of

UNITED NATIONS DEVELOPMENT PROGRAMME DESK REVIEW OF UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN Report No. 1310 Issue Date: 9 October 2014 Table of

REPORT 2016/030 INTERNAL AUDIT DIVISION. Audit of project management at the United Nations Institute for Training and Research

INTERNAL AUDIT DIVISION REPORT 2016/030 Audit of project management at the United Nations Institute for Training and Research Overall results relating to effective management of projects were initially

INTERNAL AUDIT DIVISION REPORT 2016/030 Audit of project management at the United Nations Institute for Training and Research Overall results relating to effective management of projects were initially

REPORT 2014/051 INTERNAL AUDIT DIVISION. Audit of the process of reporting cases of fraud or presumptive fraud in financial statements

INTERNAL AUDIT DIVISION REPORT 2014/051 Audit of the process of reporting cases of fraud or presumptive fraud in financial statements Overall results relating to the completeness and accuracy of reporting

INTERNAL AUDIT DIVISION REPORT 2014/051 Audit of the process of reporting cases of fraud or presumptive fraud in financial statements Overall results relating to the completeness and accuracy of reporting

REPORT 2014/024 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2014/024 Audit of the United Nations Environment Programme Secretariat of the Basel, Rotterdam and Stockholm Conventions Overall results relating to the efficient and effective

INTERNAL AUDIT DIVISION REPORT 2014/024 Audit of the United Nations Environment Programme Secretariat of the Basel, Rotterdam and Stockholm Conventions Overall results relating to the efficient and effective

REPORT 2014/015 INTERNAL AUDIT DIVISION. Audit of selected guaranteed maximum price contracts in the Office of Capital Master Plan

INTERNAL AUDIT DIVISION REPORT 2014/015 Audit of selected guaranteed maximum price contracts in the Office of Capital Master Plan Overall results relating to the audit of selected guaranteed maximum price

INTERNAL AUDIT DIVISION REPORT 2014/015 Audit of selected guaranteed maximum price contracts in the Office of Capital Master Plan Overall results relating to the audit of selected guaranteed maximum price

REPORT 2014/147 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2014/147 Audit of administration of selected pension benefits by the Geneva Office of the United Nations Joint Staff Pension Fund Overall results relating to the effective

INTERNAL AUDIT DIVISION REPORT 2014/147 Audit of administration of selected pension benefits by the Geneva Office of the United Nations Joint Staff Pension Fund Overall results relating to the effective

REPORT 2015/094 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/094 Audit of management of external portfolio managers for small capitalization investments in the Investment Management Division of the United Nations Joint Staff Pension

INTERNAL AUDIT DIVISION REPORT 2015/094 Audit of management of external portfolio managers for small capitalization investments in the Investment Management Division of the United Nations Joint Staff Pension

May 2018 FC 170/15. Hundred and Seventieth Session. Rome, May Update on Commissary Closure and Related Matters

May 2018 FC 170/15 E FINANCE COMMITTEE Hundred and Seventieth Session Rome, 21-25 May 2018 Update on Commissary Closure and Related Matters Queries on the substantive content of this document may be addressed

May 2018 FC 170/15 E FINANCE COMMITTEE Hundred and Seventieth Session Rome, 21-25 May 2018 Update on Commissary Closure and Related Matters Queries on the substantive content of this document may be addressed

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/068

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/068 Audit of the management of United Nations Joint Staff Pension Fund Investment Management Division s back office operations Overall results relating to the

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/068 Audit of the management of United Nations Joint Staff Pension Fund Investment Management Division s back office operations Overall results relating to the

REPORT 2014/062. Audit of the United Nations Environment Programme Ozone Secretariat FINAL OVERALL RATING: PARTIALLY SATISFACTORY

INTERNAL AUDIT DIVISION REPORT 2014/062 Audit of the United Nations Environment Programme Ozone Secretariat Overall results relating to the provision of efficient and effective support services by the

INTERNAL AUDIT DIVISION REPORT 2014/062 Audit of the United Nations Environment Programme Ozone Secretariat Overall results relating to the provision of efficient and effective support services by the

REPORT 2016/098 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/098 Audit of the arrangements for fleet management at the Office of the United Nations High Commissioner for Refugees Overall results relating to the effective management

INTERNAL AUDIT DIVISION REPORT 2016/098 Audit of the arrangements for fleet management at the Office of the United Nations High Commissioner for Refugees Overall results relating to the effective management

GUIDELINE ON OUTSOURCING

GL14 GUIDELINE ON OUTSOURCING Insurance Authority Contents Page 1. Introduction..... 1 2. Application of this Guideline........ 1 3. Interpretation... 2 4. Legal and Regulatory Obligations.. 3 5. Essential

GL14 GUIDELINE ON OUTSOURCING Insurance Authority Contents Page 1. Introduction..... 1 2. Application of this Guideline........ 1 3. Interpretation... 2 4. Legal and Regulatory Obligations.. 3 5. Essential

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/091. Audit of the United Nations Peacebuilding Support Office

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/091 Audit of the United Nations Peacebuilding Support Office Overall results relating to the effective support of the Peacebuilding Support Office to the Peacebuilding

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/091 Audit of the United Nations Peacebuilding Support Office Overall results relating to the effective support of the Peacebuilding Support Office to the Peacebuilding

ARTICLE 8: BASIC SERVICES

THE SCOPE OF SERVICES ADDED BY THIS AMENDMENT IS FOR A CM AT RISK PROJECT ONLY. THE SCOPE OF SERVICES SPECIFIED BELOW INCLUDES ARTICLES 8.1, 8.3, 8.4, 8.5, 8.6, 8.7 AND 8.8. THE SERVICES SPECIFIED IN ARTICLE

THE SCOPE OF SERVICES ADDED BY THIS AMENDMENT IS FOR A CM AT RISK PROJECT ONLY. THE SCOPE OF SERVICES SPECIFIED BELOW INCLUDES ARTICLES 8.1, 8.3, 8.4, 8.5, 8.6, 8.7 AND 8.8. THE SERVICES SPECIFIED IN ARTICLE

REPORT 2015/174 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/174 Audit of management of selected subprogrammes and related capacity development projects in the United Nations Economic and Social Commission for Asia and the Pacific

INTERNAL AUDIT DIVISION REPORT 2015/174 Audit of management of selected subprogrammes and related capacity development projects in the United Nations Economic and Social Commission for Asia and the Pacific

INTERNAL AUDIT DIVISION REPORT 2018/058. Audit of the management of the regular programme of technical cooperation

INTERNAL AUDIT DIVISION REPORT 2018/058 Audit of the management of the regular programme of technical cooperation There was a need to enhance complementarity of activities related to the regular programme

INTERNAL AUDIT DIVISION REPORT 2018/058 Audit of the management of the regular programme of technical cooperation There was a need to enhance complementarity of activities related to the regular programme

AUDIT UNDP COUNTRY OFFICE AFGHANISTAN FINANCIAL MANAGEMENT. Report No Issue Date: 10 December 2013

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AFGHANISTAN FINANCIAL MANAGEMENT Report No. 1233 Issue Date: 10 December 2013 Table of Contents Executive Summary i I. Introduction

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AFGHANISTAN FINANCIAL MANAGEMENT Report No. 1233 Issue Date: 10 December 2013 Table of Contents Executive Summary i I. Introduction

REPORT 2015/115 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/115 Audit of the statistics subprogramme and related technical cooperation projects in the Economic Commission for Africa Overall results relating to effective management

INTERNAL AUDIT DIVISION REPORT 2015/115 Audit of the statistics subprogramme and related technical cooperation projects in the Economic Commission for Africa Overall results relating to effective management

INTERNAL AUDIT DIVISION REPORT 2019/010. Audit of management of the Transport International Routier Trust Fund at the Economic Commission for Europe

INTERNAL AUDIT DIVISION REPORT 2019/010 Audit of management of the Transport International Routier Trust Fund at the Economic Commission for Europe Controls over governance and financial management need

INTERNAL AUDIT DIVISION REPORT 2019/010 Audit of management of the Transport International Routier Trust Fund at the Economic Commission for Europe Controls over governance and financial management need

Internal Audit of WFP Operations in the Republic of Mali

Fighting Hunger Worldwide Internal Audit of WFP Operations in the Republic of of the Inspector General Internal Audit Report AR/14/05 Contents Page I. Executive Summary 3 II. Context and Scope 5 III. Results

Fighting Hunger Worldwide Internal Audit of WFP Operations in the Republic of of the Inspector General Internal Audit Report AR/14/05 Contents Page I. Executive Summary 3 II. Context and Scope 5 III. Results

STAFF REPORT. March 19, Audit Committee. Auditor General

STAFF REPORT March 19, 2004 To: From: Subject: Audit Committee Auditor General Economic Development, Culture and Tourism Department Review of Receivables Relating to Parks and Recreation Operations and

STAFF REPORT March 19, 2004 To: From: Subject: Audit Committee Auditor General Economic Development, Culture and Tourism Department Review of Receivables Relating to Parks and Recreation Operations and

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/053. Audit of the management of the ecosystem sub-programme in the United Nations Environment Programme

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/053 Audit of the management of the ecosystem sub-programme in the United Nations Environment Programme Overall results relating to effective management of the

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/053 Audit of the management of the ecosystem sub-programme in the United Nations Environment Programme Overall results relating to effective management of the

Audit of Controls over Department of Convention and Event Services Cash Receipts and Collections 1

Memorandum CITY OF DALLAS (Report No. A15-001) DATE: October 31, 2014 TO: Honorable Mayor and Members of the City Council SUBJECT: Audit of Controls over Department of Convention and Event Services Cash

Memorandum CITY OF DALLAS (Report No. A15-001) DATE: October 31, 2014 TO: Honorable Mayor and Members of the City Council SUBJECT: Audit of Controls over Department of Convention and Event Services Cash

Internal Auditor s Report. The County Council and County Executive of Wicomico County, Maryland:

Wicomico County, Maryland OFFICE OF THE INTERNAL AUDITOR P.O. BOX 870 SALISBURY, MARYLAND 21803-0870 410-548-4696 FAX 410-548-7872 Steve Roser, CPA Internal Auditor Internal Auditor s Report The County

Wicomico County, Maryland OFFICE OF THE INTERNAL AUDITOR P.O. BOX 870 SALISBURY, MARYLAND 21803-0870 410-548-4696 FAX 410-548-7872 Steve Roser, CPA Internal Auditor Internal Auditor s Report The County

Allegany County Public Schools

Financial Management Practices Audit Report Allegany County Public Schools January 2013 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Financial Management Practices Audit Report Allegany County Public Schools January 2013 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

The accompanying notes are an integral part of these financial statements.

SIN3MIVIS 1VONVNI3 Page 1 ADOPTAPLATOON SOLDIER SUPPORT EFFORT, INC. Statement of Financial Position As of 12/31/2016 Assets Cash and cash equivalents $ 1,459,353 Accounts receivables 117,346 Prepaid 8,252

SIN3MIVIS 1VONVNI3 Page 1 ADOPTAPLATOON SOLDIER SUPPORT EFFORT, INC. Statement of Financial Position As of 12/31/2016 Assets Cash and cash equivalents $ 1,459,353 Accounts receivables 117,346 Prepaid 8,252

AUDIT REPORT. Travel and Hospitality

AUDIT REPORT Travel and Hospitality Table of Contents 1.0 Executive Summary... 1 1.1 Background and Context... 1 1.2 Overall Assessment / Audit Opinion... 1 1.3 Strengths... 2 1.4 Main Observations...

AUDIT REPORT Travel and Hospitality Table of Contents 1.0 Executive Summary... 1 1.1 Background and Context... 1 1.2 Overall Assessment / Audit Opinion... 1 1.3 Strengths... 2 1.4 Main Observations...

Case 1:12-cv RMC Document 14 Filed 04/04/12 Page 1 of 92

Case 1:12-cv-00361-RMC Document 14 Filed 04/04/12 Page 1 of 92 Case 1:12-cv-00361-RMC Document 14 Filed 04/04/12 Page 2 of 92 Case 1:12-cv-00361-RMC Document 14 Filed 04/04/12 Page 3 of 92 Case 1:12-cv-00361-RMC

Case 1:12-cv-00361-RMC Document 14 Filed 04/04/12 Page 1 of 92 Case 1:12-cv-00361-RMC Document 14 Filed 04/04/12 Page 2 of 92 Case 1:12-cv-00361-RMC Document 14 Filed 04/04/12 Page 3 of 92 Case 1:12-cv-00361-RMC

Case 1:12-cv RMC Document 11 Filed 04/04/12 Page 1 of 86

Case 1:12-cv-00361-RMC Document 11 Filed 04/04/12 Page 1 of 86 Case 1:12-cv-00361-RMC Document 11 Filed 04/04/12 Page 2 of 86 Case 1:12-cv-00361-RMC Document 11 Filed 04/04/12 Page 3 of 86 Case 1:12-cv-00361-RMC

Case 1:12-cv-00361-RMC Document 11 Filed 04/04/12 Page 1 of 86 Case 1:12-cv-00361-RMC Document 11 Filed 04/04/12 Page 2 of 86 Case 1:12-cv-00361-RMC Document 11 Filed 04/04/12 Page 3 of 86 Case 1:12-cv-00361-RMC

TRI-COUNTY SATELLITE T.V., INC. D/B/A ICONNECTYOU TERMS AND CONDITIONS FOR HIGH SPEED INTERNET SERVICE

Page 1 of 5 TRI-COUNTY SATELLITE T.V., INC. D/B/A ICONNECTYOU TERMS AND CONDITIONS FOR HIGH SPEED INTERNET SERVICE 1. Agreement. Your Service Agreement ( Agreement ) with Tri-County Satellite T.V., Inc.

Page 1 of 5 TRI-COUNTY SATELLITE T.V., INC. D/B/A ICONNECTYOU TERMS AND CONDITIONS FOR HIGH SPEED INTERNET SERVICE 1. Agreement. Your Service Agreement ( Agreement ) with Tri-County Satellite T.V., Inc.

AIPHS Financial Procedures

AIPHS Financial Procedures 1. Bank Accounts Shall remain at Community Bank of the Bay and East West Bank. The Board president along with the Superintendent of AIM Schools, shall have signatory power. 2.

AIPHS Financial Procedures 1. Bank Accounts Shall remain at Community Bank of the Bay and East West Bank. The Board president along with the Superintendent of AIM Schools, shall have signatory power. 2.

CITY OF BLOOMINGTON, ILLINOIS MANAGEMENT LETTER. April 30, 2010

CITY OF BLOOMINGTON, ILLINOIS MANAGEMENT LETTER April 30, 2010 October 6, 2010 Honorable Mayor and Members of the City Council 109 East Olive St. Bloomington, Illinois 61702 In planning and performing

CITY OF BLOOMINGTON, ILLINOIS MANAGEMENT LETTER April 30, 2010 October 6, 2010 Honorable Mayor and Members of the City Council 109 East Olive St. Bloomington, Illinois 61702 In planning and performing

Audit Report 2018-A-0003 Town of Manalapan Water Utility Department February 13, 2018

PALM BEACH COUNTY John A. Carey Inspector General Inspector General Accredited Enhancing Public Trust in Government Audit Report Town of Manalapan Water Utility Department February 13, 2018 Insight Oversight

PALM BEACH COUNTY John A. Carey Inspector General Inspector General Accredited Enhancing Public Trust in Government Audit Report Town of Manalapan Water Utility Department February 13, 2018 Insight Oversight

3.14. Supportive Services for People with Disabilities. Chapter 3 Section. Background. Ministry of Community and Social Services

Chapter 3 Section 3.14 Ministry of Community and Social Services Supportive Services for People with Disabilities Background Figure 1: Supportive Services Expenditures, 2010/11 Source of data: Ministry

Chapter 3 Section 3.14 Ministry of Community and Social Services Supportive Services for People with Disabilities Background Figure 1: Supportive Services Expenditures, 2010/11 Source of data: Ministry

Development Fund for Iraq. Appendix

Appendix For the period to 31 December 2003 KPMG Bahrain June 2004 This report contains 16 pages 1 Overall Control Environment Development Fund for Iraq 1.1 General background 1.1.1 The DFI was established

Appendix For the period to 31 December 2003 KPMG Bahrain June 2004 This report contains 16 pages 1 Overall Control Environment Development Fund for Iraq 1.1 General background 1.1.1 The DFI was established

FIJI HOLIDAYS BOOKING TERMS AND CONDITIONS

FIJI HOLIDAYS BOOKING TERMS AND CONDITIONS 1 BACKGROUND The Booking Conditions form the basis of your contract with Fiji Holidays. Please read them carefully as they set your and our respective rights

FIJI HOLIDAYS BOOKING TERMS AND CONDITIONS 1 BACKGROUND The Booking Conditions form the basis of your contract with Fiji Holidays. Please read them carefully as they set your and our respective rights

KAREN E. RUSHING. FOLLOW UP of. Utilities Installment. Payment Program

KAREN E. RUSHING Clerk of the Circuit Court and County Comptroller FOLLOW UP of Utilities Installment Payment Program Original Audit Report Issued September 30, 2013 Audit Services Karen E. Rushing Clerk

KAREN E. RUSHING Clerk of the Circuit Court and County Comptroller FOLLOW UP of Utilities Installment Payment Program Original Audit Report Issued September 30, 2013 Audit Services Karen E. Rushing Clerk

Board of Public Works Interagency Committee on School Construction

Audit Report Board of Public Works Interagency Committee on School Construction April 2013 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any

Audit Report Board of Public Works Interagency Committee on School Construction April 2013 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any

REPORT 2015/009 INTERNAL AUDIT DIVISION. Audit of a donor-funded project implemented by the International Trade Centre in Côte d Ivoire

INTERNAL AUDIT DIVISION REPORT 2015/009 Audit of a donor-funded project implemented by the International Trade Centre in Côte d Ivoire Overall results relating to the effective management of the donor-funded

INTERNAL AUDIT DIVISION REPORT 2015/009 Audit of a donor-funded project implemented by the International Trade Centre in Côte d Ivoire Overall results relating to the effective management of the donor-funded

Accounts Receivable and Debt Collection Processes. Internal Controls and Compliance Audit

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp O L A OFFICE OF THE

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp O L A OFFICE OF THE

DESERT COMMUNITY COLLEGE DISTRICT General Terms and Conditions

DESERT COMMUNITY COLLEGE DISTRICT www.collegeofthedesert.edu General Terms and Conditions 1. PURCHASE ORDER DEFINED: The term purchase order as used in these terms conditions means the document entitled

DESERT COMMUNITY COLLEGE DISTRICT www.collegeofthedesert.edu General Terms and Conditions 1. PURCHASE ORDER DEFINED: The term purchase order as used in these terms conditions means the document entitled

Framework Convention on Climate Change. Report of the United Nations Board of Auditors

United Nations Framework Convention on Climate Change FCCC/SBI/2010/14 Distr.: General 15 October 2010 English only Subsidiary Body for Implementation Thirty-third session Cancun, 30 November to 4 December

United Nations Framework Convention on Climate Change FCCC/SBI/2010/14 Distr.: General 15 October 2010 English only Subsidiary Body for Implementation Thirty-third session Cancun, 30 November to 4 December

All travelers are to comply with the following travel and business expense reimbursement policies and procedural guidelines.

Title: Travel and Business Expense Reimbursement Policy Code: 5-200-050 Date: 1-18-06rev Approved: WPL Policy General The Boston College Travel and Business Expense Reimbursement Policy provides guidelines

Title: Travel and Business Expense Reimbursement Policy Code: 5-200-050 Date: 1-18-06rev Approved: WPL Policy General The Boston College Travel and Business Expense Reimbursement Policy provides guidelines

DNE PLUMBING & HEATING TERMS AND CONDITIONS

BACKGROUND: DNE PLUMBING & HEATING TERMS AND CONDITIONS These Terms and Conditions are the standard terms which apply to the provision of plumbing or Heating services by DNE Plumbing & Heating ( the Trader

BACKGROUND: DNE PLUMBING & HEATING TERMS AND CONDITIONS These Terms and Conditions are the standard terms which apply to the provision of plumbing or Heating services by DNE Plumbing & Heating ( the Trader

Financial reports and audited financial statements and reports of the Board of Auditors for the period ended 31 December 2009

United Nations A/65/498 General Assembly Distr.: General 8 October 2010 Original: English Sixty-fifth session Agenda item 127 Financial reports and audited financial statements, and reports of the Board

United Nations A/65/498 General Assembly Distr.: General 8 October 2010 Original: English Sixty-fifth session Agenda item 127 Financial reports and audited financial statements, and reports of the Board

September 2017 FC 169/4. Hundred and Sixty-ninth Session. Rome, 6-10 November Audited Accounts - FAO Commissary 2016

September 2017 FC 169/4 E FINANCE COMMITTEE Hundred and Sixty-ninth Session Rome, 6-10 November 2017 Audited Accounts - FAO Commissary 2016 Queries on the substantive content of this document may be addressed

September 2017 FC 169/4 E FINANCE COMMITTEE Hundred and Sixty-ninth Session Rome, 6-10 November 2017 Audited Accounts - FAO Commissary 2016 Queries on the substantive content of this document may be addressed

CONNECTICUT NATURAL GAS CORPORATION RULES AND REGULATIONS

The following terms and conditions apply to all gas rates, and to the supply of gas service. A copy of these Rules and Regulations is on file with the Public Utilities Regulatory Authority (the Authority

The following terms and conditions apply to all gas rates, and to the supply of gas service. A copy of these Rules and Regulations is on file with the Public Utilities Regulatory Authority (the Authority

ARCHIVED - Limited Annual Assurance Compliance Audit Hospitality and Travel

N A T I O N A L R E S E A R C H C O U N C I L C A N A D A ARCHIVED - Limited Annual Assurance Compliance Audit Hospitality and Travel 2006-07 This PDF file has been archived on the Web. Archived Content

N A T I O N A L R E S E A R C H C O U N C I L C A N A D A ARCHIVED - Limited Annual Assurance Compliance Audit Hospitality and Travel 2006-07 This PDF file has been archived on the Web. Archived Content

ROUGH DIAMOND SUPPLY AGREEMENT 1

2015-2018 ROUGH DIAMOND SUPPLY AGREEMENT 1 GLOBAL SIGHTHOLDER SALES (INTERNATIONAL), GLOBAL SIGHTHOLDER SALES (BOTSWANA), SIGHTHOLDER SALES SOUTH AFRICA AND THE SUPPLY OF CANADIAN UN-AGGREGATED GOODS FOR

2015-2018 ROUGH DIAMOND SUPPLY AGREEMENT 1 GLOBAL SIGHTHOLDER SALES (INTERNATIONAL), GLOBAL SIGHTHOLDER SALES (BOTSWANA), SIGHTHOLDER SALES SOUTH AFRICA AND THE SUPPLY OF CANADIAN UN-AGGREGATED GOODS FOR

Delinquency Management for Mortgages Secured by Primary Residences

Delinquency Management for Mortgages Secured by Primary Residences This reference guide highlights Freddie Mac s requirements for managing delinquent mortgages secured by a borrower s primary residence.

Delinquency Management for Mortgages Secured by Primary Residences This reference guide highlights Freddie Mac s requirements for managing delinquent mortgages secured by a borrower s primary residence.

LONG TERM AIRCRAFT CHARTER AGREEMENT NO. PD/C--/-- BETWEEN THE UNITED NATIONS AND Carrier's Name

LONG TERM AIRCRAFT CHARTER AGREEMENT NO. BETWEEN THE UNITED NATIONS AND Carrier's Name THIS LONG TERM AIRCRAFT CHARTER AGREEMENT is made this -- day of -- by and between THE UNITED NATIONS, an international

LONG TERM AIRCRAFT CHARTER AGREEMENT NO. BETWEEN THE UNITED NATIONS AND Carrier's Name THIS LONG TERM AIRCRAFT CHARTER AGREEMENT is made this -- day of -- by and between THE UNITED NATIONS, an international

If the text is contradictory to the Finnish text, the latter will be followed.

General terms and conditions for package travel If the text is contradictory to the Finnish text, the latter will be followed. These terms and conditions have been agreed between the Association of Finnish

General terms and conditions for package travel If the text is contradictory to the Finnish text, the latter will be followed. These terms and conditions have been agreed between the Association of Finnish

Dear Ms. Lawrence and Members of the Board of Commissioners:

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

3.08. OntarioBuys Program. Chapter 3 Section. Background. Ministry of Finance

Chapter 3 Section 3.08 Ministry of Finance OntarioBuys Program Chapter 3 VFM Section 3.08 Background OntarioBuys is a government initiative launched in 2004 to achieve savings in the procurement of goods

Chapter 3 Section 3.08 Ministry of Finance OntarioBuys Program Chapter 3 VFM Section 3.08 Background OntarioBuys is a government initiative launched in 2004 to achieve savings in the procurement of goods

Office of Inspector General University of South Florida

Office of Inspector General University of South Florida Project # A-1718DOE-017 November 2018 Executive Summary In accordance with the Department of Education s fiscal year (FY) 2017-18 audit plan, the

Office of Inspector General University of South Florida Project # A-1718DOE-017 November 2018 Executive Summary In accordance with the Department of Education s fiscal year (FY) 2017-18 audit plan, the

ARLINGTON COUNTY, VIRGINIA. County Board Agenda Item Meeting of October 21, 2017

ARLINGTON COUNTY, VIRGINIA County Board Agenda Item Meeting of October 21, 2017 DATE: October 12, 2017 SUBJECT: Memorandum of Understanding (MOU) between Arlington County and the City of Alexandria for

ARLINGTON COUNTY, VIRGINIA County Board Agenda Item Meeting of October 21, 2017 DATE: October 12, 2017 SUBJECT: Memorandum of Understanding (MOU) between Arlington County and the City of Alexandria for

ABA Film Services Ltd. Terms and Conditions of Hire

ABA Film Services Ltd Terms and Conditions of Hire 1 INTERPRETATION 1.1 In these conditions the following words have the following meanings: Contract means a contract which incorporates these conditions

ABA Film Services Ltd Terms and Conditions of Hire 1 INTERPRETATION 1.1 In these conditions the following words have the following meanings: Contract means a contract which incorporates these conditions

Name Neighborhood Association