REPORT 2014/147 INTERNAL AUDIT DIVISION

|

|

|

- Joy Cole

- 5 years ago

- Views:

Transcription

1 INTERNAL AUDIT DIVISION REPORT 2014/147 Audit of administration of selected pension benefits by the Geneva Office of the United Nations Joint Staff Pension Fund Overall results relating to the effective and efficient administration of pension benefits by the Geneva Office of the United Nations Joint Staff Pension Fund were initially assessed as partially satisfactory. Implementation of two important recommendations remains in progress. FINAL OVERALL RATING: PARTIALLY SATISFACTORY 19 December 2014 Assignment No. AS2014/800/01

2 CONTENTS Page I. BACKGROUND 1 II. OBJECTIVE AND SCOPE 1-2 III. AUDIT RESULTS 2-5 Regulatory framework 3-5 IV. ACKNOWLEDGEMENT 5 ANNEX I APPENDIX I Status of audit recommendations Management response

3 AUDIT REPORT Audit of administration of selected pension benefits by the Geneva Office of the United Nations Joint Staff Pension Fund I. BACKGROUND 1. The Office of Internal Oversight Services (OIOS) conducted an audit of administration of selected pension benefits by the Geneva Office of the United Nations Joint Staff Pension Fund (UNJSPF). 2. In accordance with its mandate, OIOS provides assurance and advice on the adequacy and effectiveness of the United Nations internal control system, the primary objectives of which are to ensure: (a) effective and efficient operations; (b) accurate financial and operational reporting; (c) safeguarding of assets; and (d) compliance with mandates, regulations and rules. 3. The UNJSPF was established in 1949, by resolution 248 (III) of the General Assembly, to provide retirement, death, disability and related benefits for staff upon cessation of their services with the United Nations, under the Regulations, Rules and Pension Adjustment System of the UNJSPF. The Geneva Office was established in 1975 and was responsible for administering services to 23 member organizations. Geographical proximity and language commonality of the member organizations were the main considerations in setting up the Office and assigning the client organizations to the Office. In 2013, the Geneva Office awarded 4,673 benefits, corresponding to 40 per cent of total benefits awarded by the Fund for the year. 4. The Geneva Office was headed by the Chief of Office who reported directly to the Chief Executive Officer of the UNJSPF. The Office also had: a Participation and Entitlements Section; a Finance, Client Services and Records Management Section; a Legal Officer; and an Information Systems Officer. Thirty posts were approved for the biennium Pension benefits were processed through the Pension Fund s Administration System (PENSYS) and the supporting documents were stored in Content Manager, the Fund s document imaging system. 6. Comments provided by the UNJSPF Secretariat are incorporated in italics. II. OBJECTIVE AND SCOPE 7. The audit was conducted to assess the adequacy and effectiveness of the UNJSPF Secretariat s governance, risk management and control processes in providing reasonable assurance regarding effective and efficient administration of pension benefits by the Geneva office of the UNJSPF. 8. This audit was included in the 2014 OIOS risk-based work plan due to the financial and reputational risks related to determining the eligibility of beneficiaries and the calculation of pension benefits. 9. The key control tested for the audit was regulatory framework. For the purpose of this audit, OIOS defined regulatory framework as controls that provide reasonable assurance that policies and procedures: (a) exist to guide the operations of the Fund in processing pension benefits; (b) are implemented consistently; and (c) ensure reliability and integrity of financial and operational information. 1

4 10. The key control was assessed for the control objectives shown in Table OIOS conducted the audit from March to May The audit covered the period from 1 January to 31 December The audit reviewed the following: (i) verification of the eligibility of beneficiaries; (ii) accuracy of calculation of selected benefits; and (iii) UNJSPF policy and procedures for fraud prevention and detection. 12. OIOS conducted an activity-level risk assessment to identify and assess specific risk exposures, and to confirm the relevance of the selected key controls in mitigating associated risks. Through interviews, analytical reviews and tests of controls, OIOS assessed the existence and adequacy of internal controls and conducted necessary tests to determine their effectiveness. 13. OIOS reviewed controls using a sample of 50 cases processed in 2013 with total payments of $2.9 million. The selected cases comprised retirements, early retirements, disabilities, withdrawal settlements, residual settlements, validations and restorations. The audit involved: (i) review of policy, procedures and guidelines on pension benefits; (ii) interviews with key staff in Geneva and New York; (iii) re-performance of the calculation of the 50 selected benefit cases; (iv) verification of the eligibility of beneficiaries/participants for the 50 selected cases; (v) walk-through of the PENSYS benefit processing system; (vi) walk-through of the Content Manager records management system; (vii) review of the measurement of the performance benchmark for processing benefits; and (viii) data mining for sampling and analysis purposes. III. AUDIT RESULTS 14. The UNJSPF governance, risk management and control processes examined were initially assessed as partially satisfactory 1 in providing reasonable assurance regarding the effective and efficient administration of pension benefits by the Geneva office of the UNJSPF. 15. OIOS made two recommendations to address issues identified in this audit. Controls for establishing the eligibility of beneficiaries and calculating pension benefits were adequate. The Fund maintained three levels of control in Pension Fund s Administration System for processing benefits and this configuration ensured appropriate segregation of duties. Also, a complete set of supporting documents, used for verification and calculation of benefits purposes, was stored in the Fund s document imaging system. However, updating the Fund s Administration Manual needed to be prioritized to consolidate guidance on administering benefits. The fraud risk assessment also needed to be updated by fully mapping existing controls to potential fraud schemes and addressing any significant gaps. 16. The initial overall rating was based on the assessment of key control presented in Table 1 below. The final overall rating is partially satisfactory as implementation of two important recommendations remains in progress. 1 A rating of partially satisfactory means that important (but not critical or pervasive) deficiencies exist in governance, risk management or control processes, such that reasonable assurance may be at risk regarding the achievement of control and/or business objectives under review. 2

5 Table 1: Assessment of key control Business objective Effective and efficient administration of pension benefits by the Geneva Office of the UNJSPF Key control Regulatory framework Effective and efficient operations Partially satisfactory FINAL OVERALL RATING: PARTIALLY SATISFACTORY Control objectives Accurate financial and operational reporting Partially satisfactory Safeguarding of assets Partially satisfactory Compliance with mandates, regulations and rules Partially satisfactory Regulatory framework Controls over pension benefit calculations were adequate 17. The Regulations, Rules and Pension Adjustment System of the UNJSPF set out the criteria for the calculation of benefits and eligibility of beneficiaries. The provisions regarding the calculation of benefits were embedded into PENSYS. The 1987 UNJSPF Administration Manual and 2007 Geneva Reference Manual required that a participant s basic data be verified, pensionable remuneration report checked and contributions reconciled in PENSYS before the benefit calculation module was run in PENSYS and the reports forwarded to supervisors for review and approval. 18. OIOS selected and reviewed 50 benefit cases comprising 11 retirements, 5 early retirements, 5 disabilities, 13 withdrawal settlements, 4 residual settlements, 8 validations and restorations, and 4 other cases. OIOS reviewed the relevant documents in case files showing the steps followed by the benefit processors and established that all selected cases were verified, reviewed and approved as per the procedures. The audit also verified the accuracy of beneficiary basic data in the system by matching the information with the source documents, e.g. separation notification, payment instruction, etc. Further, OIOS manually recalculated the benefits as outlined in the regulations and rules following the calculation criteria and compared the results with the amounts generated by PENSYS. Based on the reviews and recalculations of benefits OIOS concluded that controls over pension benefit calculations were adequate. Controls over establishing eligibility of beneficiaries were adequate 19. Eligibility criteria for benefits were defined in the Regulations, Rules and Pension Adjustment System of the UNJSPF and stipulated, inter alia, the normal retirement age, number of years of contributory service to qualify for a pension and conditions for receiving a disability benefit. 20. For the same 50 cases selected, OIOS checked all required information in the Participant Basic Data master in PENSYS and reviewed supporting documentation to establish eligibility of beneficiaries such as separation notification, birth certificate and disability report. The review showed that all required information was complete and up-to-date, and supporting documents were available in the beneficiary s folder maintained in the Content Manager system. The audit team also examined selected original documents in the archives and concluded that they were adequately safeguarded in a restricted area with standard security measures against risks of fire and water. Based on these reviews, OIOS concluded that controls for establishing the eligibility of beneficiaries were adequate. 3

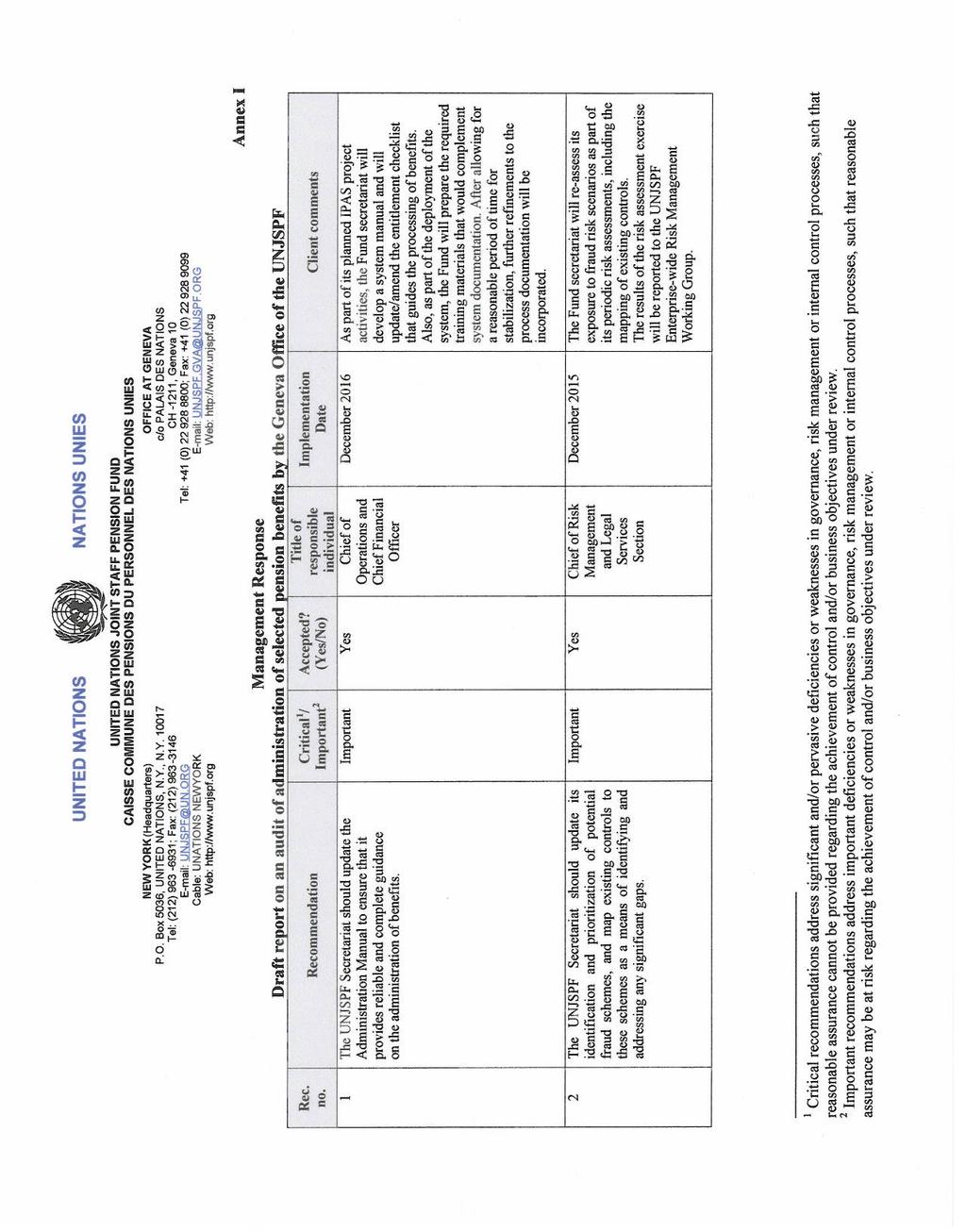

6 The Fund maintained three levels of control in Pension Fund s Administration System for benefit processing 21. Responsibilities for certain functions were required to be assigned to different staff members to ensure proper segregation of duties. 22. UNJSPF configured PENSYS with three levels of controls with the following functions: (i) the calculator; (ii) the auditor; and (iii) the releaser. The calculator ensured that all required information was available, made necessary adjustments if required, and ran the calculation. The auditor verified the accuracy of calculations, and checked that all supporting documents were available. The releaser conducted checks of certain fields to ensure that names, account numbers and payment instructions were correct, and supporting documents were available. The releaser, after the review, forwarded the case to the certifying officer. OIOS verified that all reviewed cases were processed by the three separate roles, in accordance with the established procedures. Based on the reviews, OIOS concluded that controls over segregation of duties relating to benefit processing were adequate. Need to update the Fund s Administration Manual 23. Annex I to the Administrative Rules of UNJSPF stated that the Chief Executive Officer was empowered to issue and revise from time to time as may be necessary, an Administration Manual, which prescribed the procedures and forms to be used for the administration of the Fund. 24. The Fund s Administration Manual was first promulgated in 1971 and last updated in It therefore did not reflect changes to regulations, rules and operational procedures made since then to provide additional guidance on the administration of benefits. These changes covered subjects such as rates used in calculations of benefits; codes that were created for each work type used in PENSYS; recovery of overpayments; processing of retroactive participants; non-receipt and reissuance of cheques; procedures for issuing certificates of entitlement; contributions from member organizations; failure to submit payment instructions; and beneficiaries in receipt of two or more benefits under the regulations. All of these updates were circulated in the form of individual documents, but were not consolidated in a revised manual for ease of reference and to ensure that the correct version of the guidance was being used. OIOS, nevertheless, noted that tables with the latest rates and figures were uploaded in PENSYS to ensure that the system-generated calculations were accurate. 25. UNJSPF management had not prioritized updating the Administration Manual. Lack of unified guidance may result in inefficient practices and the possibility of making errors. (1) The UNJSPF Secretariat should update the Administration Manual to ensure that it provides reliable and complete guidance on the administration of benefits. The UNJSPF Secretariat accepted recommendation 1 and stated that as part of its planned project activities for the Integrated Pension Administration System, the Fund Secretariat would develop a system manual and update/amend the entitlements checklist that would guide the processing of benefits. Recommendation 1 remains open pending receipt of the updated Administration Manual. Need to update fraud risk assessment 26. A fraud risk assessment is often a critical component of an organization s larger enterprise risk management program. Such an assessment generally includes the following five key steps: (i) identifying relevant fraud risk factors; (ii) identifying potential fraud schemes and prioritizing them based on risk; 4

7 (iii) mapping existing controls to potential fraud schemes and identifying gaps; (iv) testing operating effectiveness of fraud prevention and detection controls; and (v) documenting and reporting the fraud risk assessment. 27. Following the Audit Committee s request in its November 2012 and February 2013 meetings that UNJSPF management identify and consider fraud scenarios to ensure that controls were in place, the Fund analyzed its potential exposure to fraud cases that had been perpetrated on other pension funds. The analysis also covered additional scenarios for the UNJSPF Secretariat, which reflected the Fund s unique plan design and global scope. The Fund partly mapped existing controls to the potential fraud schemes and thus did not fully identify all the related gaps. The Fund also did not take further steps to translate the identified gaps into additional pension specific anti-fraud controls. 28. The UNJSPF management had prepared guidance on fraud awareness, reporting and escalation procedures, but this did not provide assurance that adequate controls were in place to address all the potential fraud schemes identified. Without this assurance, management may not be able to effectively manage residual fraud risks. (2) The UNJSPF Secretariat should update its identification and prioritization of potential fraud schemes, and map existing controls to these schemes as a means of identifying and addressing any significant gaps. The UNJSPF Secretariat accepted recommendation 2 and stated that the Fund Secretariat would re-assess its exposure to fraud risk scenarios as part of its periodic risk assessments, including the mapping of existing controls. Recommendation 2 remains open pending receipt of an updated fraud risk assessment that maps existing controls to potential fraud schemes and indicates how significant gaps would be addressed. IV. ACKNOWLEDGEMENT 29. OIOS wishes to express its appreciation to the Management and staff of the United Nations Joint Staff Pension Fund Secretariat for the assistance and cooperation extended to the auditors during this assignment. (Signed) David Kanja Assistant Secretary-General for Internal Oversight Services 5

8 ANNEX I STATUS OF AUDIT RECOMMENDATIONS Audit of administration of selected pension benefits by the Geneva Office of the United Nations Joint Staff Pension Fund Recom. no. Recommendation 1 The UNJSPF Secretariat should update the Administration Manual to ensure that it provides reliable and complete guidance on the administration of benefits. 2 The UNJSPF Secretariat should update its identification and prioritization of potential fraud schemes, and map existing controls to these schemes as a means of identifying and addressing any significant gaps. Critical 2 / C/ Important 3 O 4 Actions needed to close recommendation Important O Submission of the updated Administration Manual. Important O Submission of an updated fraud risk assessment that maps existing controls to potential fraud schemes and indicates how significant gaps would be addressed. Implementation date 5 December 2016 December Critical recommendations address significant and/or pervasive deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance cannot be provided regarding the achievement of control and/or business objectives under review. 3 Important recommendations address important deficiencies or weaknesses in governance, risk management or internal control processes, such that reasonable assurance may be at risk regarding the achievement of control and/or business objectives under review. 4 C = closed, O = open 5 Date provided by the UNJSPF in response to recommendations. 1

9 APPENDIX I Management Response

10

11

12

REPORT 2015/094 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/094 Audit of management of external portfolio managers for small capitalization investments in the Investment Management Division of the United Nations Joint Staff Pension

INTERNAL AUDIT DIVISION REPORT 2015/094 Audit of management of external portfolio managers for small capitalization investments in the Investment Management Division of the United Nations Joint Staff Pension

REPORT 2014/051 INTERNAL AUDIT DIVISION. Audit of the process of reporting cases of fraud or presumptive fraud in financial statements

INTERNAL AUDIT DIVISION REPORT 2014/051 Audit of the process of reporting cases of fraud or presumptive fraud in financial statements Overall results relating to the completeness and accuracy of reporting

INTERNAL AUDIT DIVISION REPORT 2014/051 Audit of the process of reporting cases of fraud or presumptive fraud in financial statements Overall results relating to the completeness and accuracy of reporting

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/091. Audit of the United Nations Peacebuilding Support Office

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/091 Audit of the United Nations Peacebuilding Support Office Overall results relating to the effective support of the Peacebuilding Support Office to the Peacebuilding

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/091 Audit of the United Nations Peacebuilding Support Office Overall results relating to the effective support of the Peacebuilding Support Office to the Peacebuilding

REPORT 2014/153 INTERNAL AUDIT DIVISION. Audit of the United Nations Office for Disaster Risk Reduction

INTERNAL AUDIT DIVISION REPORT 2014/153 Audit of the United Nations Office for Disaster Risk Reduction Overall results relating to the effective management of the United Nations Office for Disaster Risk

INTERNAL AUDIT DIVISION REPORT 2014/153 Audit of the United Nations Office for Disaster Risk Reduction Overall results relating to the effective management of the United Nations Office for Disaster Risk

REPORT 2014/107 INTERNAL AUDIT DIVISION. Audit of quick-impact projects in the African Union-United Nations Hybrid Operation in Darfur

INTERNAL AUDIT DIVISION REPORT 2014/107 Audit of quick-impact projects in the African Union-United Nations Hybrid Operation in Darfur Overall results relating to the management of quick-impact projects

INTERNAL AUDIT DIVISION REPORT 2014/107 Audit of quick-impact projects in the African Union-United Nations Hybrid Operation in Darfur Overall results relating to the management of quick-impact projects

REPORT 2014/134 INTERNAL AUDIT DIVISION. Audit of financial and administrative functions in the United Nations Truce Supervision Organization

INTERNAL AUDIT DIVISION REPORT 2014/134 Audit of financial and administrative functions in the United Nations Truce Supervision Organization Overall results relating to the effectiveness of financial and

INTERNAL AUDIT DIVISION REPORT 2014/134 Audit of financial and administrative functions in the United Nations Truce Supervision Organization Overall results relating to the effectiveness of financial and

REPORT 2013/142. Audit of accounts receivable and payable in the United Nations Operation in Côte d Ivoire

INTERNAL AUDIT DIVISION REPORT 2013/142 Audit of accounts receivable and payable in the United Nations Operation in Côte d Ivoire Overall results relating to the effective management of accounts receivable

INTERNAL AUDIT DIVISION REPORT 2013/142 Audit of accounts receivable and payable in the United Nations Operation in Côte d Ivoire Overall results relating to the effective management of accounts receivable

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/068

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/068 Audit of the management of United Nations Joint Staff Pension Fund Investment Management Division s back office operations Overall results relating to the

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/068 Audit of the management of United Nations Joint Staff Pension Fund Investment Management Division s back office operations Overall results relating to the

REPORT 2014/015 INTERNAL AUDIT DIVISION. Audit of selected guaranteed maximum price contracts in the Office of Capital Master Plan

INTERNAL AUDIT DIVISION REPORT 2014/015 Audit of selected guaranteed maximum price contracts in the Office of Capital Master Plan Overall results relating to the audit of selected guaranteed maximum price

INTERNAL AUDIT DIVISION REPORT 2014/015 Audit of selected guaranteed maximum price contracts in the Office of Capital Master Plan Overall results relating to the audit of selected guaranteed maximum price

REPORT 2014/062. Audit of the United Nations Environment Programme Ozone Secretariat FINAL OVERALL RATING: PARTIALLY SATISFACTORY

INTERNAL AUDIT DIVISION REPORT 2014/062 Audit of the United Nations Environment Programme Ozone Secretariat Overall results relating to the provision of efficient and effective support services by the

INTERNAL AUDIT DIVISION REPORT 2014/062 Audit of the United Nations Environment Programme Ozone Secretariat Overall results relating to the provision of efficient and effective support services by the

REPORT 2016/105 INTERNAL AUDIT DIVISION. Audit of investment management in the Office of Programme Planning, Budget and Accounts

INTERNAL AUDIT DIVISION REPORT 2016/105 Audit of investment management in the Office of Programme Planning, Budget and Accounts Overall results relating to the effective management of investments were

INTERNAL AUDIT DIVISION REPORT 2016/105 Audit of investment management in the Office of Programme Planning, Budget and Accounts Overall results relating to the effective management of investments were

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/078

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/078 Audit of the United Nations Environment Programme s Secretariat of the Convention on Biological Diversity Overall results relating to the provision of efficient

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/078 Audit of the United Nations Environment Programme s Secretariat of the Convention on Biological Diversity Overall results relating to the provision of efficient

REPORT 2015/115 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/115 Audit of the statistics subprogramme and related technical cooperation projects in the Economic Commission for Africa Overall results relating to effective management

INTERNAL AUDIT DIVISION REPORT 2015/115 Audit of the statistics subprogramme and related technical cooperation projects in the Economic Commission for Africa Overall results relating to effective management

REPORT 2015/095 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/095 Review of recurrent issues identified in recent internal audit engagements for the Office for the Coordination of Humanitarian Affairs 8 September 2015 Assignment

INTERNAL AUDIT DIVISION REPORT 2015/095 Review of recurrent issues identified in recent internal audit engagements for the Office for the Coordination of Humanitarian Affairs 8 September 2015 Assignment

REPORT 2016/012 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/012 Audit of the management of the technical cooperation project on Information and Communication Technologies in Africa Phase II in the Economic Commission for Africa

INTERNAL AUDIT DIVISION REPORT 2016/012 Audit of the management of the technical cooperation project on Information and Communication Technologies in Africa Phase II in the Economic Commission for Africa

REPORT 2016/054 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/054 Audit of selected subprogrammes and related technical cooperation projects in the Economic Commission for Europe Overall results relating to the effective management

INTERNAL AUDIT DIVISION REPORT 2016/054 Audit of selected subprogrammes and related technical cooperation projects in the Economic Commission for Europe Overall results relating to the effective management

REPORT 2015/079 INTERNAL AUDIT DIVISION. Audit of United Nations Office on Drugs and Crime operations in Peru

INTERNAL AUDIT DIVISION REPORT 2015/079 Audit of United Nations Office on Drugs and Crime operations in Peru Overall results relating to the management of operations in Peru were initially assessed as

INTERNAL AUDIT DIVISION REPORT 2015/079 Audit of United Nations Office on Drugs and Crime operations in Peru Overall results relating to the management of operations in Peru were initially assessed as

REPORT 2016/062 INTERNAL AUDIT DIVISION. Audit of the management of trust funds at the United Nations Framework Convention on Climate Change

INTERNAL AUDIT DIVISION REPORT 2016/062 Audit of the management of trust funds at the United Nations Framework Convention on Climate Change Overall results relating to the effective management of trust

INTERNAL AUDIT DIVISION REPORT 2016/062 Audit of the management of trust funds at the United Nations Framework Convention on Climate Change Overall results relating to the effective management of trust

REPORT 2015/178 INTERNAL AUDIT DIVISION. Audit of the United Nations Human Settlements Programme Regional Office for Arab States

INTERNAL AUDIT DIVISION REPORT 2015/178 Audit of the United Nations Human Settlements Programme Regional Office for Arab States Overall results relating to Regional Office for Arab States operations were

INTERNAL AUDIT DIVISION REPORT 2015/178 Audit of the United Nations Human Settlements Programme Regional Office for Arab States Overall results relating to Regional Office for Arab States operations were

REPORT 2015/041 INTERNAL AUDIT DIVISION. Audit of the United Nations Mine Action Service of the Department of Peacekeeping Operations

INTERNAL AUDIT DIVISION REPORT 2015/041 Audit of the United Nations Mine Action Service of the Department of Peacekeeping Operations Overall results relating to the effective management of mine action

INTERNAL AUDIT DIVISION REPORT 2015/041 Audit of the United Nations Mine Action Service of the Department of Peacekeeping Operations Overall results relating to the effective management of mine action

REPORT 2016/081 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/081 Audit of selected subprogrammes and related technical cooperation projects in the Economic and Social Commission for Western Asia Overall results relating to the

INTERNAL AUDIT DIVISION REPORT 2016/081 Audit of selected subprogrammes and related technical cooperation projects in the Economic and Social Commission for Western Asia Overall results relating to the

REPORT 2015/072 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/072 Audit of minimum operating residential security standards entitlements for staff in the United Nations Operation in Côte d Ivoire Overall results relating to the

INTERNAL AUDIT DIVISION REPORT 2015/072 Audit of minimum operating residential security standards entitlements for staff in the United Nations Operation in Côte d Ivoire Overall results relating to the

REPORT 2015/085 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/085 Audit of the United Nations Stabilization Mission in Haiti s trust fund to strengthen specialized sexual and gender-based crimes police cells and units within the

INTERNAL AUDIT DIVISION REPORT 2015/085 Audit of the United Nations Stabilization Mission in Haiti s trust fund to strengthen specialized sexual and gender-based crimes police cells and units within the

REPORT 2015/174 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/174 Audit of management of selected subprogrammes and related capacity development projects in the United Nations Economic and Social Commission for Asia and the Pacific

INTERNAL AUDIT DIVISION REPORT 2015/174 Audit of management of selected subprogrammes and related capacity development projects in the United Nations Economic and Social Commission for Asia and the Pacific

REPORT 2014/024 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2014/024 Audit of the United Nations Environment Programme Secretariat of the Basel, Rotterdam and Stockholm Conventions Overall results relating to the efficient and effective

INTERNAL AUDIT DIVISION REPORT 2014/024 Audit of the United Nations Environment Programme Secretariat of the Basel, Rotterdam and Stockholm Conventions Overall results relating to the efficient and effective

REPORT 2014/070 INTERNAL AUDIT DIVISION. Audit of civil affairs activities in the. United Nations Stabilization Mission in Haiti

INTERNAL AUDIT DIVISION REPORT 2014/070 Audit of civil affairs activities in the United Nations Stabilization Mission in Haiti Overall results relating to the effective management of civil affairs activities

INTERNAL AUDIT DIVISION REPORT 2014/070 Audit of civil affairs activities in the United Nations Stabilization Mission in Haiti Overall results relating to the effective management of civil affairs activities

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/053. Audit of the management of the ecosystem sub-programme in the United Nations Environment Programme

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/053 Audit of the management of the ecosystem sub-programme in the United Nations Environment Programme Overall results relating to effective management of the

INTERNAL AUDIT DIVISION AUDIT REPORT 2013/053 Audit of the management of the ecosystem sub-programme in the United Nations Environment Programme Overall results relating to effective management of the

REPORT 2015/009 INTERNAL AUDIT DIVISION. Audit of a donor-funded project implemented by the International Trade Centre in Côte d Ivoire

INTERNAL AUDIT DIVISION REPORT 2015/009 Audit of a donor-funded project implemented by the International Trade Centre in Côte d Ivoire Overall results relating to the effective management of the donor-funded

INTERNAL AUDIT DIVISION REPORT 2015/009 Audit of a donor-funded project implemented by the International Trade Centre in Côte d Ivoire Overall results relating to the effective management of the donor-funded

REPORT 2015/123 INTERNAL AUDIT DIVISION. Audit of the management of engineering projects in the United Nations Mission in the Republic of South Sudan

INTERNAL AUDIT DIVISION REPORT 2015/123 Audit of the management of engineering projects in the United Nations Mission in the Republic of South Sudan Overall results relating to the effective management

INTERNAL AUDIT DIVISION REPORT 2015/123 Audit of the management of engineering projects in the United Nations Mission in the Republic of South Sudan Overall results relating to the effective management

REPORT 2016/088 INTERNAL AUDIT DIVISION. Audit of rations management in the United Nations Mission in the Republic of South Sudan

INTERNAL AUDIT DIVISION REPORT 2016/088 Audit of rations management in the United Nations Mission in the Republic of South Sudan Overall results relating to the effective management of rations were initially

INTERNAL AUDIT DIVISION REPORT 2016/088 Audit of rations management in the United Nations Mission in the Republic of South Sudan Overall results relating to the effective management of rations were initially

INTERNAL AUDIT DIVISION REPORT 2018/052. Audit of liquidation activities at the International Criminal Tribunal for the former Yugoslavia

INTERNAL AUDIT DIVISION REPORT 2018/052 Audit of liquidation activities at the International Criminal Tribunal for the former Yugoslavia Overall, liquidation activities were performed satisfactorily 31

INTERNAL AUDIT DIVISION REPORT 2018/052 Audit of liquidation activities at the International Criminal Tribunal for the former Yugoslavia Overall, liquidation activities were performed satisfactorily 31

REPORT 2016/017 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/017 Audit of credit risk management in the Investment Management Division of the United Nations Joint Staff Pension Fund Overall results relating to the effective management

INTERNAL AUDIT DIVISION REPORT 2016/017 Audit of credit risk management in the Investment Management Division of the United Nations Joint Staff Pension Fund Overall results relating to the effective management

Distr. General JSPB/G.4/Rev.22. Regulations, Rules and Pension Adjustment System of the United Nations Joint Staff Pension Fund

Distr. General JSPB/G.4/Rev.22 Regulations, Rules and Pension Adjustment System of the United Nations Joint Staff Pension Fund United Nations 1 January 2018 Regulations, Rules and Pension Adjustment System

Distr. General JSPB/G.4/Rev.22 Regulations, Rules and Pension Adjustment System of the United Nations Joint Staff Pension Fund United Nations 1 January 2018 Regulations, Rules and Pension Adjustment System

REPORT 2016/030 INTERNAL AUDIT DIVISION. Audit of project management at the United Nations Institute for Training and Research

INTERNAL AUDIT DIVISION REPORT 2016/030 Audit of project management at the United Nations Institute for Training and Research Overall results relating to effective management of projects were initially

INTERNAL AUDIT DIVISION REPORT 2016/030 Audit of project management at the United Nations Institute for Training and Research Overall results relating to effective management of projects were initially

REPORT 2014/068 INTERNAL AUDIT DIVISION. Audit of the United Nations Office on Drugs and Crime Intelligence and Law Enforcement Systems project

INTERNAL AUDIT DIVISION REPORT 2014/068 Audit of the United Nations Office on Drugs and Crime Intelligence and Law Enforcement Systems project Overall results relating to management of the Intelligence

INTERNAL AUDIT DIVISION REPORT 2014/068 Audit of the United Nations Office on Drugs and Crime Intelligence and Law Enforcement Systems project Overall results relating to management of the Intelligence

AUDIT REPORT. Travel and Hospitality

AUDIT REPORT Travel and Hospitality Table of Contents 1.0 Executive Summary... 1 1.1 Background and Context... 1 1.2 Overall Assessment / Audit Opinion... 1 1.3 Strengths... 2 1.4 Main Observations...

AUDIT REPORT Travel and Hospitality Table of Contents 1.0 Executive Summary... 1 1.1 Background and Context... 1 1.2 Overall Assessment / Audit Opinion... 1 1.3 Strengths... 2 1.4 Main Observations...

UNITED NATIONS JOINT STAFF PENSION FUND. Enterprise-wide Risk Management Policy

UNITED NATIONS JOINT STAFF PENSION FUND Enterprise-wide Risk Management Policy 15 April 2016 Page 1 Table of Contents Page Preface I. Introduction 3 II. Definition 4 III. UNSJFP Enterprise-wide Risk Management

UNITED NATIONS JOINT STAFF PENSION FUND Enterprise-wide Risk Management Policy 15 April 2016 Page 1 Table of Contents Page Preface I. Introduction 3 II. Definition 4 III. UNSJFP Enterprise-wide Risk Management

INTERNAL AUDIT DIVISION REPORT 2017/003

INTERNAL AUDIT DIVISION REPORT 2017/003 Audit of the management of the sustainable development subprogramme in the Department of Economic and Social Affairs The Division for Sustainable Development needed

INTERNAL AUDIT DIVISION REPORT 2017/003 Audit of the management of the sustainable development subprogramme in the Department of Economic and Social Affairs The Division for Sustainable Development needed

REPORT 2016/038 INTERNAL AUDIT DIVISION. Audit of the Office for the Coordination of Humanitarian Affairs operations in South Sudan

INTERNAL AUDIT DIVISION REPORT 2016/038 Audit of the Office for the Coordination of Humanitarian Affairs operations in South Sudan Overall results relating to the effective management of operations in

INTERNAL AUDIT DIVISION REPORT 2016/038 Audit of the Office for the Coordination of Humanitarian Affairs operations in South Sudan Overall results relating to the effective management of operations in

The Terms of reference of the Staff Pension Committees (SPCs) and their Secretaries 1. I. Introduction

and their Secretaries 1. I. Introduction") The Terms of reference of the Staff Pension Committees (SPCs) and their Secretaries 1 I. Introduction 1. The United Nations Joint Staff Pension Fund (UNJSPF) was established by the General Assembly of

The Terms of reference of the Staff Pension Committees (SPCs) and their Secretaries 1 I. Introduction 1. The United Nations Joint Staff Pension Fund (UNJSPF) was established by the General Assembly of

UNITED NATIONS JOINT STAFF PENSION FUND AND UNESCO STAFF PENSION COMMITTEE OUTLINE

U General Conference 32nd session, Paris 2003 32 C 32 C/44 21 July 2003 Original: English Item 11.13 of the provisional agenda UNITED NATIONS JOINT STAFF PENSION FUND AND UNESCO STAFF PENSION COMMITTEE

U General Conference 32nd session, Paris 2003 32 C 32 C/44 21 July 2003 Original: English Item 11.13 of the provisional agenda UNITED NATIONS JOINT STAFF PENSION FUND AND UNESCO STAFF PENSION COMMITTEE

GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings. September 30, 2001 and 2000

Schedule of Findings. September 30, 2001 and 2000") GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings CURRENT YEAR (2001) FINDINGS Finding No. 2001-1 Verification of Disability Annuitants 4GCA, Chapter 8, Article 1, 8127(a)

GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings CURRENT YEAR (2001) FINDINGS Finding No. 2001-1 Verification of Disability Annuitants 4GCA, Chapter 8, Article 1, 8127(a)

Regulations and Rules of the United Nations Joint Staff Pension Fund

Distr. GENERAL JSPB/G.4/Rev.l3 UNITED NATIONS Regulations and Rules of the United Nations Joint Staff Pension Fund ICCROM vi ics^if 4y 1 April 1987 Regulations and Rules of the United Nations Joint Staff

Distr. GENERAL JSPB/G.4/Rev.l3 UNITED NATIONS Regulations and Rules of the United Nations Joint Staff Pension Fund ICCROM vi ics^if 4y 1 April 1987 Regulations and Rules of the United Nations Joint Staff

INTERNAL AUDIT DIVISION REPORT 2016/155. Audit of the United Nations Human Settlements Programme project management process

INTERNAL AUDIT DIVISION REPORT 2016/155 Audit of the United Nations Human Settlements Programme project management process Established policies and procedures need to be further strengthened, particularly

INTERNAL AUDIT DIVISION REPORT 2016/155 Audit of the United Nations Human Settlements Programme project management process Established policies and procedures need to be further strengthened, particularly

REPORT 2017/148. Audit of budget formulation and monitoring in the United Nations Interim Force in Lebanon

INTERNAL AUDIT DIVISION REPORT 2017/148 Audit of budget formulation and monitoring in the United Nations Interim Force in Lebanon The Mission aligned its budget with its mandate and improved budget monitoring,

INTERNAL AUDIT DIVISION REPORT 2017/148 Audit of budget formulation and monitoring in the United Nations Interim Force in Lebanon The Mission aligned its budget with its mandate and improved budget monitoring,

Генеральная конферeнция 34-я сессия, Париж 2007 г. 大会第三十四届会议, 巴黎,2007

General Conference 34th session, Paris 2007 Conférence générale 34 e session, Paris 2007 Conferencia General 34 a reunión, París 2007 Генеральная конферeнция 34-я сессия, Париж 2007 г. א א א א א א ٢٠٠٧

General Conference 34th session, Paris 2007 Conférence générale 34 e session, Paris 2007 Conferencia General 34 a reunión, París 2007 Генеральная конферeнция 34-я сессия, Париж 2007 г. א א א א א א ٢٠٠٧

Having regard to the Treaty on the Functioning of the European Union, and in particular Article 291 thereof,

L 244/12 COMMISSION IMPLEMTING REGULATION (EU) No 897/2014 of 18 August 2014 laying down specific provisions for the implementation of cross-border cooperation programmes financed under Regulation (EU)

L 244/12 COMMISSION IMPLEMTING REGULATION (EU) No 897/2014 of 18 August 2014 laying down specific provisions for the implementation of cross-border cooperation programmes financed under Regulation (EU)

Audit Report Internal Financial Controls. GF-OIG March 2015 Geneva, Switzerland

Audit Report Internal Financial Controls GF-OIG-15-005 Table of Contents I. Background... 2 II. Scope and Rating... 3 III. Executive Summary... 4 IV. Findings and agreed actions... 6 V. Table of Agreed

Audit Report Internal Financial Controls GF-OIG-15-005 Table of Contents I. Background... 2 II. Scope and Rating... 3 III. Executive Summary... 4 IV. Findings and agreed actions... 6 V. Table of Agreed

INTERNAL AUDIT DIVISION REPORT 2017/038. Audit of general services contracts management in the United Nations Mission in the Republic of South Sudan

INTERNAL AUDIT DIVISION REPORT 2017/038 Audit of general services contracts management in the United Nations Mission in the Republic of South Sudan The Mission needed to implement costeffective arrangements

INTERNAL AUDIT DIVISION REPORT 2017/038 Audit of general services contracts management in the United Nations Mission in the Republic of South Sudan The Mission needed to implement costeffective arrangements

REPORT 2016/098 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/098 Audit of the arrangements for fleet management at the Office of the United Nations High Commissioner for Refugees Overall results relating to the effective management

INTERNAL AUDIT DIVISION REPORT 2016/098 Audit of the arrangements for fleet management at the Office of the United Nations High Commissioner for Refugees Overall results relating to the effective management

EC/67/SC/CRP.22. Risk management in UNHCR. Executive Committee of the High Commissioner s Programme. Standing Committee 67 th meeting.

Executive Committee of the High Commissioner s Programme Distr.: Restricted 31 August 2016 English Original: English and French Standing Committee 67 th meeting Risk management in UNHCR Summary This paper

Executive Committee of the High Commissioner s Programme Distr.: Restricted 31 August 2016 English Original: English and French Standing Committee 67 th meeting Risk management in UNHCR Summary This paper

INTERNAL AUDIT DIVISION REPORT 2019/010. Audit of management of the Transport International Routier Trust Fund at the Economic Commission for Europe

INTERNAL AUDIT DIVISION REPORT 2019/010 Audit of management of the Transport International Routier Trust Fund at the Economic Commission for Europe Controls over governance and financial management need

INTERNAL AUDIT DIVISION REPORT 2019/010 Audit of management of the Transport International Routier Trust Fund at the Economic Commission for Europe Controls over governance and financial management need

CITY OF EDMONTON BYLAW AUDIT COMMITTEE (CONSOLIDATED ON FEBRUARY 13, 2018)

") CITY OF EDMONTON BYLAW 16097 AUDIT COMMITTEE (CONSOLIDATED ON FEBRUARY 13, 2018) THE CITY OF EDMONTON BYLAW 16097 AUDIT COMMITTEE BYLAW Whereas pursuant to: Section 145 of the Municipal Government Act,

CITY OF EDMONTON BYLAW 16097 AUDIT COMMITTEE (CONSOLIDATED ON FEBRUARY 13, 2018) THE CITY OF EDMONTON BYLAW 16097 AUDIT COMMITTEE BYLAW Whereas pursuant to: Section 145 of the Municipal Government Act,

REPORT MARKET DISCIPLINE REPORT FINANCIAL YEAR Made in accordance with the Cyprus. Securities and Exchange Commission. Directive DI

REPORT Write DISCLOSURE you date here & MARKET DISCIPLINE ADDRESS JFD Brokers Ltd. Kakos Premier Tower Kyrillou Loukareos 70 4156 Limassol, Cyprus TELEPHONE & FAX +357 25878530 +357 25763540 WEB support@jfdbrokers.com

REPORT Write DISCLOSURE you date here & MARKET DISCIPLINE ADDRESS JFD Brokers Ltd. Kakos Premier Tower Kyrillou Loukareos 70 4156 Limassol, Cyprus TELEPHONE & FAX +357 25878530 +357 25763540 WEB support@jfdbrokers.com

Report on FSCO s Compliance Reviews Of Mortgage Administrators. Financial Services Commission of Ontario Licensing and Market Conduct Division

Report on FSCO s Compliance Reviews Of Mortgage Administrators Financial Services Commission of Ontario Licensing and Market Conduct Division June 16, 2011 TABLE OF CONTENTS EXECUTIVE SUMMARY 3 ABOUT FSCO

Report on FSCO s Compliance Reviews Of Mortgage Administrators Financial Services Commission of Ontario Licensing and Market Conduct Division June 16, 2011 TABLE OF CONTENTS EXECUTIVE SUMMARY 3 ABOUT FSCO

Fathom Wealth Management Advisors Ltd Risk Management Disclosures Year Ended 31 December 2016

Fathom Wealth Management Advisors Ltd Risk Management Disclosures Year Ended 31 December 2016 According to Directives DI144-2014-14 and DI144-2014-15 of the Cyprus Securities & Exchange Commission for

Fathom Wealth Management Advisors Ltd Risk Management Disclosures Year Ended 31 December 2016 According to Directives DI144-2014-14 and DI144-2014-15 of the Cyprus Securities & Exchange Commission for

INTERNAL FINANCIAL CONTROL POLICY

INTERNAL FINANCIAL CONTROL POLICY The Board of Directors of Kilitch Drugs (India) Limited has adopted the following Internal Financial Control Policy. Section 134(5)(e) of the Companies Act, 2013 requires,

INTERNAL FINANCIAL CONTROL POLICY The Board of Directors of Kilitch Drugs (India) Limited has adopted the following Internal Financial Control Policy. Section 134(5)(e) of the Companies Act, 2013 requires,

Report on Internal Control

Annex to letter from the General Secretary of the Autorité de contrôle prudentiel to the Director General of the French Association of Credit Institutions and Investment Firms Report on Internal Control

Annex to letter from the General Secretary of the Autorité de contrôle prudentiel to the Director General of the French Association of Credit Institutions and Investment Firms Report on Internal Control

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA FISCAL CONTROL AUDIT REPORT ON NORTH CAROLINA DEPARTMENT OF THE SECRETARY OF STATE RALEIGH, NORTH CAROLINA FOR THE PERIOD JULY 1, 2002 THROUGH JANUARY 31, 2003 OFFICE OF THE STATE

STATE OF NORTH CAROLINA FISCAL CONTROL AUDIT REPORT ON NORTH CAROLINA DEPARTMENT OF THE SECRETARY OF STATE RALEIGH, NORTH CAROLINA FOR THE PERIOD JULY 1, 2002 THROUGH JANUARY 31, 2003 OFFICE OF THE STATE

Audit Report. Canada Small Business Financing Program

Audit Report Canada Small Business Financing Program June 2013 Recommended for Approval to the Deputy Minister by the Departmental Audit Committee on July 10, 2013. Approved by the Deputy Minister on July

Audit Report Canada Small Business Financing Program June 2013 Recommended for Approval to the Deputy Minister by the Departmental Audit Committee on July 10, 2013. Approved by the Deputy Minister on July

AUDIT REPORT INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION AUDIT REPORT Governance and organizational structure of the inter-agency secretariat to the United Nations International Strategy for Disaster Risk Reduction (ISDR) The ISDR secretariat

INTERNAL AUDIT DIVISION AUDIT REPORT Governance and organizational structure of the inter-agency secretariat to the United Nations International Strategy for Disaster Risk Reduction (ISDR) The ISDR secretariat

INTERNAL AUDIT DIVISION REPORT 2017/025

INTERNAL AUDIT DIVISION REPORT 2017/025 Audit of quick impact projects in the United Nations Multidimensional Integrated Stabilization Mission in the Central African Republic There was a need to strengthen

INTERNAL AUDIT DIVISION REPORT 2017/025 Audit of quick impact projects in the United Nations Multidimensional Integrated Stabilization Mission in the Central African Republic There was a need to strengthen

Audited financial statements for the biennium

UNITED NATIONS Distr. GENERAL 1 November 2006 ENGLISH ONLY SUBSIDIARY BODY FOR IMPLEMENTATION Twenty-fifth session Nairobi, 6 14 November 2006 Item 14 (a) of the provisional agenda Administrative, financial

UNITED NATIONS Distr. GENERAL 1 November 2006 ENGLISH ONLY SUBSIDIARY BODY FOR IMPLEMENTATION Twenty-fifth session Nairobi, 6 14 November 2006 Item 14 (a) of the provisional agenda Administrative, financial

INTERNAL FINANCIAL CONTROL POLICY POKARNA LIMITED

INTERNAL FINANCIAL CONTROL POLICY POKARNA LIMITED INTRODUCTION Section 134 (5) (e) of the Companies Act, 2013 requires, the Board of every Listed Company to lay down Internal Financial Controls to be followed

INTERNAL FINANCIAL CONTROL POLICY POKARNA LIMITED INTRODUCTION Section 134 (5) (e) of the Companies Act, 2013 requires, the Board of every Listed Company to lay down Internal Financial Controls to be followed

Guidance on a common methodology for the assessment of management and control systems in the Member States ( programming period)

") Final version of 12/09/2008 EUROPEAN COMMISSION DIRECTORATE-GENERAL MARITIME AFFAIRS AND FISHERIES EFFC/27/2008 Guidance on a common methodology for the assessment of management and control systems in

Final version of 12/09/2008 EUROPEAN COMMISSION DIRECTORATE-GENERAL MARITIME AFFAIRS AND FISHERIES EFFC/27/2008 Guidance on a common methodology for the assessment of management and control systems in

Framework Convention on Climate Change. Report of the United Nations Board of Auditors

United Nations Framework Convention on Climate Change FCCC/SBI/2010/14 Distr.: General 15 October 2010 English only Subsidiary Body for Implementation Thirty-third session Cancun, 30 November to 4 December

United Nations Framework Convention on Climate Change FCCC/SBI/2010/14 Distr.: General 15 October 2010 English only Subsidiary Body for Implementation Thirty-third session Cancun, 30 November to 4 December

Report of the International Civil Service Commission

EXECUTIVE BOARD EB132/39 132nd session 23 November 2012 Provisional agenda item 14.4 Report of the International Civil Service Commission Report by the Secretariat 1. Under its Statute, 1 the International

EXECUTIVE BOARD EB132/39 132nd session 23 November 2012 Provisional agenda item 14.4 Report of the International Civil Service Commission Report by the Secretariat 1. Under its Statute, 1 the International

Guidance for Member States on the Drawing of Management Declaration and Annual Summary

EGESIF_15-0008-02 19/08/2015 EUROPEAN COMMISSION European Structural and Investment Funds Guidance for Member States on the Drawing of Management Declaration and Annual Summary Programming period 2014-2020

EGESIF_15-0008-02 19/08/2015 EUROPEAN COMMISSION European Structural and Investment Funds Guidance for Member States on the Drawing of Management Declaration and Annual Summary Programming period 2014-2020

BANK OF CHINA (CANADA) BASEL III DISCLOSURES AS AT DECEMBER 31, 2013

BASEL III DISCLOSURES AS AT DECEMBER 31, 2013") BANK OF CHINA (CANADA) BASEL III DISCLOSURES AS AT DECEMBER 31, 2013 Table of Contents 1. Scope of Application... 1 2. Capital Management... 2 (a) Capital structure... 2 (b) Capital adequacy ratio... 2

BANK OF CHINA (CANADA) BASEL III DISCLOSURES AS AT DECEMBER 31, 2013 Table of Contents 1. Scope of Application... 1 2. Capital Management... 2 (a) Capital structure... 2 (b) Capital adequacy ratio... 2

12 th June 2012 NOTICE. subject to. respect to enhanced group s risk. or (ii) the and that the. necessary

the and that the. necessary") 12 th June 2012 NOTICE Insurance Group Supervision Statement of Principles The Insurance Group Supervision Statement of Principles ( SoP ) issued in June 2012 sets forth how the Bermuda Monetary Authority

12 th June 2012 NOTICE Insurance Group Supervision Statement of Principles The Insurance Group Supervision Statement of Principles ( SoP ) issued in June 2012 sets forth how the Bermuda Monetary Authority

David E. Moran, Director of Education Practice

Date: June 29, 2018 To: Anne Byrne Ms. Jeanine Rufo, Board President From: Cc: Subject: David E. Moran, Director of Education Practice Audit Committee Ms. Jill Figarella, District Treasurer Dr. Frances

Date: June 29, 2018 To: Anne Byrne Ms. Jeanine Rufo, Board President From: Cc: Subject: David E. Moran, Director of Education Practice Audit Committee Ms. Jill Figarella, District Treasurer Dr. Frances

Security Council. United Nations S/2012/604. Note by the Secretary-General. Distr.: General 3 August Original: English

United Nations S/2012/604 Security Council Distr.: General 3 August 2012 Original: English Note by the Secretary-General The Secretary-General has the honour to transmit herewith to the Security Council,

United Nations S/2012/604 Security Council Distr.: General 3 August 2012 Original: English Note by the Secretary-General The Secretary-General has the honour to transmit herewith to the Security Council,

GAO MANAGEMENT REPORT. Improvements Needed in Controls over the Preparation of the U.S. Consolidated Financial Statements. Report to Agency Officials

GAO United States Government Accountability Office Report to Agency Officials June 2012 MANAGEMENT REPORT Improvements Needed in Controls over the Preparation of the U.S. Consolidated Financial Statements

GAO United States Government Accountability Office Report to Agency Officials June 2012 MANAGEMENT REPORT Improvements Needed in Controls over the Preparation of the U.S. Consolidated Financial Statements

Office of the Secretary of the Executive Board EXECUTIVE BOARD DECISION MONITORING TABLE

Last update: 8 February 2018 Office of the Secretary of the Executive Board EXECUTIVE BOARD DECISION MONITORING TABLE The following matrix keeps track of the implementation of specific and time-bound requests

Last update: 8 February 2018 Office of the Secretary of the Executive Board EXECUTIVE BOARD DECISION MONITORING TABLE The following matrix keeps track of the implementation of specific and time-bound requests

INTERNAL AUDIT DIVISION REPORT 2017/136. Audit of finance and human resources management in the United Nations Disengagement Observer Force

INTERNAL AUDIT DIVISION REPORT 2017/136 Audit of finance and human resources management in the United Nations Disengagement Observer Force The Mission needed to enhance budget monitoring and review the

INTERNAL AUDIT DIVISION REPORT 2017/136 Audit of finance and human resources management in the United Nations Disengagement Observer Force The Mission needed to enhance budget monitoring and review the

Report of the United Nations Board of Auditors. United Nations Framework Convention on Climate Change

United Nations Report of the United Nations Board of Auditors on the financial statements of the United Nations Framework Convention on Climate Change for the year ended 31 December 2017 Contents Chapter

United Nations Report of the United Nations Board of Auditors on the financial statements of the United Nations Framework Convention on Climate Change for the year ended 31 December 2017 Contents Chapter

INTERNAL AUDIT DIVISION REPORT 2017/073. Audit of accounts receivable and payable in the United Nations Operation in Côte d voire

INTERNAL AUDIT DIVISION REPORT 2017/073 Audit of accounts receivable and payable in the United Nations Operation in Côte d voire There was a need for comprehensive review of accounts receivable and to

INTERNAL AUDIT DIVISION REPORT 2017/073 Audit of accounts receivable and payable in the United Nations Operation in Côte d voire There was a need for comprehensive review of accounts receivable and to

Use of Internal Models for Determining Required Capital for Segregated Fund Risks (LICAT)

") Canada Bureau du surintendant des institutions financières Canada 255 Albert Street 255, rue Albert Ottawa, Canada Ottawa, Canada K1A 0H2 K1A 0H2 Instruction Guide Subject: Capital for Segregated Fund

Canada Bureau du surintendant des institutions financières Canada 255 Albert Street 255, rue Albert Ottawa, Canada Ottawa, Canada K1A 0H2 K1A 0H2 Instruction Guide Subject: Capital for Segregated Fund

THE CO-OPERATIVE BANK PLC RISK COMMITTEE. Terms of Reference

THE CO-OPERATIVE BANK PLC RISK COMMITTEE Terms of Reference 1. CONSTITUTION 1.1 The terms of reference of the risk committee (the "Committee") of The Co-operative Bank plc (the "Bank") were approved by

THE CO-OPERATIVE BANK PLC RISK COMMITTEE Terms of Reference 1. CONSTITUTION 1.1 The terms of reference of the risk committee (the "Committee") of The Co-operative Bank plc (the "Bank") were approved by

Northcentral Arkansas Education Service Center

Northcentral Arkansas Education Service Center Regulatory Basis Financial Statements And Other Reports June 30, 2005 LEGISLATIVE JOINT AUDITING COMMITTEE TABLE OF CONTENTS JUNE 30, 2005 Independent Auditor's

Northcentral Arkansas Education Service Center Regulatory Basis Financial Statements And Other Reports June 30, 2005 LEGISLATIVE JOINT AUDITING COMMITTEE TABLE OF CONTENTS JUNE 30, 2005 Independent Auditor's

Message from the Deputy Chief Executive Officer

Newsletter Edition 2 June 2018 Message from the Deputy Chief Executive Officer Last year the 64th UN Pension Board gave the Fund Secretariat clear instructions. Following the introduction and continuing

Newsletter Edition 2 June 2018 Message from the Deputy Chief Executive Officer Last year the 64th UN Pension Board gave the Fund Secretariat clear instructions. Following the introduction and continuing

Distr. GENERAL. A/RES/49/233 1 March 1995 RESOLUTION ADOPTED BY THE GENERAL ASSEMBLY. [on the report of the Fifth Committee (A/49/803/Add.

UNITED NATIONS A General Assembly Distr. GENERAL A/RES/49/233 1 March 1995 Forty-ninth session Agenda item 132 (a) RESOLUTION ADOPTED BY THE GENERAL ASSEMBLY [on the report of the Fifth Committee (A/49/803/Add.1)]

UNITED NATIONS A General Assembly Distr. GENERAL A/RES/49/233 1 March 1995 Forty-ninth session Agenda item 132 (a) RESOLUTION ADOPTED BY THE GENERAL ASSEMBLY [on the report of the Fifth Committee (A/49/803/Add.1)]

INTERNAL AUDIT DIVISION REPORT 2018/014. Audit of quick-impact projects in the African Union-United Nation Hybrid Operation in Darfur

INTERNAL AUDIT DIVISION REPORT 2018/014 Audit of quick-impact projects in the African Union-United Nation Hybrid Operation in Darfur The Mission needed to ensure that completed projects are used, field

INTERNAL AUDIT DIVISION REPORT 2018/014 Audit of quick-impact projects in the African Union-United Nation Hybrid Operation in Darfur The Mission needed to ensure that completed projects are used, field

INTERNAL AUDIT DIVISION REPORT 2018/058. Audit of the management of the regular programme of technical cooperation

INTERNAL AUDIT DIVISION REPORT 2018/058 Audit of the management of the regular programme of technical cooperation There was a need to enhance complementarity of activities related to the regular programme

INTERNAL AUDIT DIVISION REPORT 2018/058 Audit of the management of the regular programme of technical cooperation There was a need to enhance complementarity of activities related to the regular programme

March Guidance on Using the Audited Project Financial Statements (APFS) Standard Review Checklist

Standard Review Checklist") March 2015 Guidance on Using the Audited Project Financial Statements (APFS) Standard Review Checklist Page 1 of 7 REVISED GUIDANCE ON USING THE APFS STANDARD REVIEW CHECKLIST Please note: The review checklist

March 2015 Guidance on Using the Audited Project Financial Statements (APFS) Standard Review Checklist Page 1 of 7 REVISED GUIDANCE ON USING THE APFS STANDARD REVIEW CHECKLIST Please note: The review checklist

The Board of Directors Government of Guam Retirement Fund

Report on Compliance and Internal Control over Financial Reporting Based on an Audit of Financial Statements Performed in Accordance With Government Auditing Standards The Board of Directors Government

Report on Compliance and Internal Control over Financial Reporting Based on an Audit of Financial Statements Performed in Accordance With Government Auditing Standards The Board of Directors Government

Our responsibility is to express an opinion on these financial statements based on our audit.

INDEPENDENT AUDITOR S REPORT TO THE MEMBERS OF PUNARVASU FINANCIAL SERVICES PRIVATE LIMITED (Formerly Known as PUNARVASU HOLDING AND TRADING COMPANY PRIVATE LIMITED) Report on the Financial Statements

INDEPENDENT AUDITOR S REPORT TO THE MEMBERS OF PUNARVASU FINANCIAL SERVICES PRIVATE LIMITED (Formerly Known as PUNARVASU HOLDING AND TRADING COMPANY PRIVATE LIMITED) Report on the Financial Statements

Annexure B. To the [directors of name of benefit administrator] 1 and to the Registrar of Pension Funds

![Annexure B. To the [directors of name of benefit administrator] 1 and to the Registrar of Pension Funds](/thumbs/79/79960023.jpg "Annexure B. To the [directors of name of benefit administrator] 1 and to the Registrar of Pension Funds") Annexure B Report of the Independent Auditor of [name of administrator] on the Conditions in respect of Benefit Administrators on behalf of Pension Funds To the [directors of name of administrator] 1 and

Annexure B Report of the Independent Auditor of [name of administrator] on the Conditions in respect of Benefit Administrators on behalf of Pension Funds To the [directors of name of administrator] 1 and

Department of Public Safety and Correctional Services Criminal Injuries Compensation Board

Audit Report Department of Public Safety and Correctional Services Criminal Injuries Compensation Board October 2014 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY

Audit Report Department of Public Safety and Correctional Services Criminal Injuries Compensation Board October 2014 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY

Summary of the 52 nd Session of the Board of the United Nations Joint Staff Pension Fund (UNJSPF) (Montreal, July 2004)

(Montreal, July 2004)") No.13 Summary of the 52 nd Session of the Board of the United Nations Joint Staff Pension Fund (UNJSPF) (Montreal, 13-23 July 2004) August 2004 The ILO delegation to the 52nd meeting of the UNJSP Board

No.13 Summary of the 52 nd Session of the Board of the United Nations Joint Staff Pension Fund (UNJSPF) (Montreal, 13-23 July 2004) August 2004 The ILO delegation to the 52nd meeting of the UNJSP Board

BERMUDA MONETARY AUTHORITY

BERMUDA MONETARY AUTHORITY BANKING, TRUST & INVESTMENT DEPARTMENT GUIDANCE NOTES THE INVESTMENT BUSINESS ACT 2003 GUIDANCE FOR PROSPECTIVE APPLICANTS February 2011 TABLE OF CONTENTS Page No. 1.0 Introduction

BERMUDA MONETARY AUTHORITY BANKING, TRUST & INVESTMENT DEPARTMENT GUIDANCE NOTES THE INVESTMENT BUSINESS ACT 2003 GUIDANCE FOR PROSPECTIVE APPLICANTS February 2011 TABLE OF CONTENTS Page No. 1.0 Introduction

Whereas UNJSPF and WTOPP have agreed to replace the aforementioned Agreement with a new Transfer Agreement;

Agreement on the transfer of pension rights of participants in the United Nations Joint Staff Pension Fund and of participants in the World Trade Organization Pension Plan Whereas the provisions of article

Agreement on the transfer of pension rights of participants in the United Nations Joint Staff Pension Fund and of participants in the World Trade Organization Pension Plan Whereas the provisions of article

INTERNAL AUDIT DIVISION REPORT 2017/126. Audit of trust fund activities in the African Union-United Nations Hybrid Operation in Darfur

INTERNAL AUDIT DIVISION REPORT 2017/126 Audit of trust fund activities in the African Union-United Nations Hybrid Operation in Darfur The Mission needed to enhance its supervision of project site inspections

INTERNAL AUDIT DIVISION REPORT 2017/126 Audit of trust fund activities in the African Union-United Nations Hybrid Operation in Darfur The Mission needed to enhance its supervision of project site inspections

Office of the State Auditor. Audit Report. Department of the Treasury Bureau of Risk Management Risk Management Interdepartmental Accounts

Office of the State Auditor Audit Report Department of the Treasury Bureau of Risk Management Risk Management Interdepartmental Accounts July 1, 1993 to March 31, 1995 Department of the Treasury Bureau

Office of the State Auditor Audit Report Department of the Treasury Bureau of Risk Management Risk Management Interdepartmental Accounts July 1, 1993 to March 31, 1995 Department of the Treasury Bureau

GUIDELINES ON PRIVATE RETIREMENT SCHEMES SC-GL/PRS-2012 (R1-2017)

") GUIDELINES ON PRIVATE RETIREMENT SCHEMES SC-GL/PRS-2012 (R1-2017) 1 st Issued : 5 April 2012 Revised : 13 July 2017 GUIDELINES ON PRIVATE RETIREMENT SCHEMES Effective Date upon 1 st Issuance: 5 April 2012

GUIDELINES ON PRIVATE RETIREMENT SCHEMES SC-GL/PRS-2012 (R1-2017) 1 st Issued : 5 April 2012 Revised : 13 July 2017 GUIDELINES ON PRIVATE RETIREMENT SCHEMES Effective Date upon 1 st Issuance: 5 April 2012

Fathom Wealth Management Advisors Ltd Risk Management Disclosures Year Ended 31 December 2017

Fathom Wealth Management Advisors Ltd Risk Management Disclosures Year Ended 31 December 2017 According to Directives DI144-2014-14 and DI144-2014-15 of the Cyprus Securities & Exchange Commission for

Fathom Wealth Management Advisors Ltd Risk Management Disclosures Year Ended 31 December 2017 According to Directives DI144-2014-14 and DI144-2014-15 of the Cyprus Securities & Exchange Commission for

STATE OFFICE OF RISK MANAGEMENT Austin, Texas. Annual Internal Audit Report Fiscal Year 2013 TABLE OF CONTENTS. Internal Auditor s Report...

Austin, Texas TABLE OF CONTENTS Page No. Internal Auditor s...1 Introduction...2 Internal Audit Objectives....3 Executive Summary Medical Cost Containment Unit Background... 4-6 Audit Scope/Objective...7

Austin, Texas TABLE OF CONTENTS Page No. Internal Auditor s...1 Introduction...2 Internal Audit Objectives....3 Executive Summary Medical Cost Containment Unit Background... 4-6 Audit Scope/Objective...7

BANK OF CHINA (CANADA) BASEL PILLAR III DISCLOSURES AS AT DECEMBER 31, 2014

BASEL PILLAR III DISCLOSURES AS AT DECEMBER 31, 2014") BANK OF CHINA (CANADA) BASEL PILLAR III DISCLOSURES AS AT DECEMBER 31, 2014 Table of Contents 1. Scope of Application... 5 2. Capital Management... 3 (a) Capital structure... 3 (b) Capital adequacy ratio...

BANK OF CHINA (CANADA) BASEL PILLAR III DISCLOSURES AS AT DECEMBER 31, 2014 Table of Contents 1. Scope of Application... 5 2. Capital Management... 3 (a) Capital structure... 3 (b) Capital adequacy ratio...

REVIEW OF MANAGEMENT AND ADMINISTRATION IN THE WORLD METEOROLOGICAL ORGANIZATION (WMO): ADDITIONAL ISSUES

: ADDITIONAL ISSUES") A.304 Management Letter FINAL 13/3/08 JIU/ML/2008/1 REVIEW OF MANAGEMENT AND ADMINISTRATION IN THE WORLD METEOROLOGICAL ORGANIZATION (WMO): ADDITIONAL ISSUES Prepared by Cihan Terzi Joint Inspection Unit

A.304 Management Letter FINAL 13/3/08 JIU/ML/2008/1 REVIEW OF MANAGEMENT AND ADMINISTRATION IN THE WORLD METEOROLOGICAL ORGANIZATION (WMO): ADDITIONAL ISSUES Prepared by Cihan Terzi Joint Inspection Unit

United Nations Joint Staff Pension Fund

United Nations Joint Staff Pension Fund New York & Geneva May 2010 The United Nations Joint Staff Pension Fund (UNJSPF) Regulations and Rules govern the conditions of participation and the determination

United Nations Joint Staff Pension Fund New York & Geneva May 2010 The United Nations Joint Staff Pension Fund (UNJSPF) Regulations and Rules govern the conditions of participation and the determination