Bridging the Wealth Divide: Expanding Homeownership in Communities of Color and Rural America. Sara Morgan Fahe / #OFNCONF #CDFIsINVEST

|

|

|

- Norma Welch

- 5 years ago

- Views:

Transcription

1 Bridging the Wealth Divide: Expanding Homeownership in Communities of Color and Rural America Sara Morgan Fahe /

2 Bridging the Wealth Divide: Expanding Homeownership in Communities of Color and Rural America

3 Where Fahe Works Fahe and our Members create transformational change in: KY, TN, VA, WV, AL, MD Fahe is on a mission to eliminate persistent poverty in Appalachia. We provide our Network of 50+ local leaders with the resources of finance, collaboration, innovation, advocacy, and communication to help craft long-lasting solutions for the needs of our region. Fahe coordinates a network of 502 Direct packaging partners in: AL, DE, FL, GA, IN, KY, MD, MI, MS, NY, NC, OH, PA, SC, TN, VA, WV, VT Fahe declared a Champion of Rural Housing by USDA streamlines the delivery of 502 Direct affordable home loans and uplifts our nation's rural area alongside 40+ packaging partners in18 states. Fahe is licensed to originate and service loans in: KY, TN, VA, WV, IN, AL, FL, MI, MS, and soon ME Fahe delivers housing capital and supports long-term success for homeowners through quality customer care and personalized account management. (1/1/17)

4 Barriers to Homeowenrship Housing Stock Appraisal gap Lenders Homebuyer ready borrowers

5 How Fahe Works Fahe is on a mission to eliminate persistent poverty in Appalachia. We do this by providing our Network of 50+ local leaders with the resources of finance, collaboration, innovation, advocacy, and communication which allows them to bring leadership, housing, education, health and social services, and economic opportunity to Appalachia. By working hand-in-hand with our Membership we help the people of Appalachia craft long-lasting solutions for the needs in our region. Finance Collaboration Innovation Advocacy Communication Local Leaders Leadership Housing Education Health and Social Services Economic Opportunity

6 Products Loan Program Credit Score Income Limits Ratios LTV Property Eligibility Lender Requirements USDA Guaranteed 620+ for all borrowers True no score w/ 3 alternative credit trade lines Family Size 1-4 $78, $103,200 29/41 100% gov/eligibility/welcomeaction.do GUS accept or refer with conditions accpetable of credit waiver FHA 620+ for all borrowers None 31/ % All areas eligible DU Accept VA 640+ for all borrowers True no score w/ 3 alternative credit trade lines None 41 back 100% All areas eligible VA Eligibility DD214 Conventional 680+ None 36/45 80% None DU Accept Conventional No MI 680+ $97,650 28/45 97% KY Properties DU Accept Home Possible % AMI per census tract (unless property is located in a underserved area then there are no income limits) epossible/eligibility.html 29/41 97% (down payment assistance avaliable) None AUS Accept USDA Direct 640+ for all borrowers True no score w/ 3 alternative credit trade lines 80% AMI for household size 29/41 100% gov/eligibility/welcomeaction.do N/A Project Reinvest Qualify for First Mortgage through Fahe 100% AMI 105% None Qualify for First Mortgage through Fahe

7 Delivery System Fahe As Direct Lender Local Partner as Standard Broker Local Partner as Basic Broker Local Partner as Homebuyer Counselor Homebuyer Ed If needed If needed If needed Yes Certification via Member/Partner NMLS Licensed Yes Yes Yes No Person Take An Application Yes Yes Yes No Rate Lock Yes Yes-Broker chooses rate and days locked Yes-No choice in rate, only days locked Initial docs Yes Yes No No originated in Process the Yes Yes No No application Underwrite Yes No No No Close in the name Yes No No No Industry Practice Yes Yes Yes Yes-Fahe differs here in that we recognize NWA Certificates where industry only recognizes HUD No Earn 3.5-4% 1.5%-2.5% chosen by Broker 1% $375.00

8 361loans of $43,179, grants of $342,247 Direct Homebuyer Lending Impact 94% First time homebuyers 48% Female headed households 20% Minority households 868 people Average AMI of 59%

9 Impact Invested $291M in Appalachia in FY2017. Manages more than $1.15 Billion in assets Served nearly 80,000 people last year Touched 25,000 homes.

10 Sara Morgan Chief Operating Officer Fahe 319 Oak Street Berea, KY Thank you

11 Bridging the Wealth Divide: Expanding Homeownership in Communities of Color and Rural America Vicky García Latino Credit Union /

12 The New Immigrant Experience: The Struggle to enter the financial mainstream

13 NC s Latino population grew more than 1,000% ( ) 800, , % 378, % 4.7% 76,726 1%

14 By 2020, NC s Latino population is projected to reach 1.3 million or 12% of the population [CATEGORY NAME] [PERCENTAG E] [CATEGORY NAME] [PERCENTAGE ] [CATEGORY NAME] [PERCENTAGE] [CELLREF] [PERCENTAGE] [CATEGORY NAME] [PERCENTAGE] [CATEGORY NAME] [PERCENTAGE]

15 Hardships Latinos Face in NC: Language Barrier - Cultural Discrimination Housing & Lending Fear of Deportation and Law Enforcement Robbery - Fraud

16 Latinos Become Trapped in Informal and Cash Economies Unbanked No Credit History Informal Financial Sector Expensive Dangerous Substandard

17 I used to carry my money and hide it in small packets at home. It wasn t until I was robbed at gunpoint with my son at my side that I realized I needed to put my money in a safer place. At LCCU, they help me understand how things work and make me feel comfortable. -Roberto, member since 2001

18 In NC 314,326 Latinos live in households that earn 50,000 or less $32,000 Median Income $50,000 to $74,999 17% $75,000 or more 15% 0 to $49,000 68% Homeownership (household heads) In owner-occupied homes (in thousands) 86 In renter-occupied homes (in thousands) 116 Homeownership rate 42.6% vs. 74.2% Whites and 47.9% African American Source: Pew Hispanic Center tabulations of the 2011 ACS (1% IPUMS sample). More information on the source data and sampling error is available at and

19 Needed to create a product to benefit the community: Bilingual Service Available with SSN or ITIN Same competitive rates and low fees for all members No PMI or unnecessary fees Affordable financing available without credit history We keep the loans in our portfolio Financial Education available

20 Alternative forms of ID No or limited credit history Rental history Utility bills Diverse sources of income Good savings

21 Two Products: 5 year ARM Up to 30 years Max LTV of 95% Fixed Up to 20 years Max LTV of 90%

22 Impact: TOTAL FINANCING (millions) $174 $192 FIRST TIME HOME BUYERS $141 $92 $112 82% ITIN HOLDERS DELINQUENCY: 1.10% NET CHARGE OFFS SINCE 2004: 0.69% 86%

23 LATINO CREDIT UNION: ETHICAL FINANCIAL PRODUCTS & EDUCATION TO EMPOWER COMMUNITIES $256 million in assets 103% growth in 5 years $528 million total financing 99% repayment 19,302 participants 1,674 graduates

24 Before You Go Please complete your session evaluation! You can find it in the Conference app.

25 Bridging the Wealth Divide: Expanding Homeownership in Communities of Color and Rural America James Hunter Hope Credit Union /

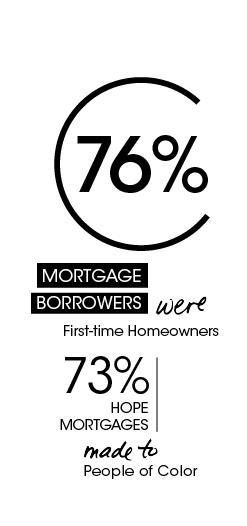

26 ¼ of Nation s Persistent Poverty Counties are Located in the Mid South

27 Affordable Housing Product (AHP) Manual Underwriting Holistic approach using non traditional trade lines Maximum 42% DTI Minimum FICO Score 580 Up to 100% Loan to Value (LTV) No Mortgage Insurance (MI)

Source: National Association of")

28 HOPE s Financing Impact 100% LTV financing % of mortgages HOPE mortgages with >96.5% LTV 1/11-6/17, % of mortgages originated (total n=1078) Source: National Association of Realtors

29

30 2017 national avg. credit scores: Conventional loan: 753 VA: 708; FHA: 684 Hope: Source: Home Buying Institute

31 Medium HH income: Homebuyers nationally, 2016: $86,100 Hope, : $47,390 Source: National Association of Realtors

32

33 HOPE s Impact Is Even More Pronounced When Compared with Home Buyers Nationally Racial minorities % of home buyers First-time home buyers* % of home buyers Source: National Association of Realtors *For HOPE, borrowers not refinancing or who haven t purchased a home in the last 3 years are assumed to be first-time home buyers.

34 HOPE s Mortgage Portfolio is Improving Lives Across the Mid South $2.7M+ Mortgages to first-time homebuyers Households with income less than $50,000 Borrowers with credit scores under 620 Equity built from borrowers paying down principal

35 Thank You! James Hunter SVP, Mortgage Lending Hope Credit Union 4 Old River Place Jackson, MS james.hunter@hopecu.org

Moving Single-Family Financing Initiatives Forward I m HOME Conference October 2-4, 2017

Moving Single-Family Financing Initiatives Forward I m HOME Conference October 2-4, 2017 Where Fahe Works Fahe and our Members create transformational change in: KY, TN, VA, WV, AL, MD Fahe is on a mission

Moving Single-Family Financing Initiatives Forward I m HOME Conference October 2-4, 2017 Where Fahe Works Fahe and our Members create transformational change in: KY, TN, VA, WV, AL, MD Fahe is on a mission

Chapter 9 Product Matrix

Table of Contents Chapter 9 Product Matrix... 1 CONVENTIONAL CONFORMING LOANS... 2 Secondary Market ARM (Adjustable Rate Mortgage) Loans... 4 HARP (Fannie DU Refi Plus and Freddie Open Access)... 5 FHA/VA

Table of Contents Chapter 9 Product Matrix... 1 CONVENTIONAL CONFORMING LOANS... 2 Secondary Market ARM (Adjustable Rate Mortgage) Loans... 4 HARP (Fannie DU Refi Plus and Freddie Open Access)... 5 FHA/VA

Who is Lending and Who is Getting Loans?

Trends in 1-4 Family Lending in New York City An ANHD White Paper February 2016 As much as New York City is a city of renters, nearly a third of New Yorkers own their own homes. Responsible, affordable

Trends in 1-4 Family Lending in New York City An ANHD White Paper February 2016 As much as New York City is a city of renters, nearly a third of New Yorkers own their own homes. Responsible, affordable

Close More Loans with HomeReady Mortgage An Overview for Loan Officers. Dial- in for audio:

Close More Loans with HomeReady Mortgage An Overview for Loan Officers Dial- in for audio: 1-866-845-1266 Seminar guidelines Please do not place the call on hold at any time. Please place your phone on

Close More Loans with HomeReady Mortgage An Overview for Loan Officers Dial- in for audio: 1-866-845-1266 Seminar guidelines Please do not place the call on hold at any time. Please place your phone on

HomeReady Mortgage. Overview for Loan Officers May Fannie Mae. Trademarks of Fannie Mae. 1

HomeReady Mortgage Overview for Loan Officers May 2017 2016 Fannie Mae. Trademarks of Fannie Mae. 1 An Important note about the seminar content While every effort has been made to ensure the reliability

HomeReady Mortgage Overview for Loan Officers May 2017 2016 Fannie Mae. Trademarks of Fannie Mae. 1 An Important note about the seminar content While every effort has been made to ensure the reliability

Close More Loans with HomeReady Mortgage

Close More Loans with HomeReady Mortgage Overview for Loan Officers May 2, 2017, 2 3:30 p.m. ET Dial-in number: 800-779-8492 Participant passcode: 4344988 2017 Fannie Mae. Trademarks of Fannie Mae. 1 Seminar

Close More Loans with HomeReady Mortgage Overview for Loan Officers May 2, 2017, 2 3:30 p.m. ET Dial-in number: 800-779-8492 Participant passcode: 4344988 2017 Fannie Mae. Trademarks of Fannie Mae. 1 Seminar

Close More Loans with HomeReady Mortgage An Overview for Loan Officers. Dial- in for audio: Attendee passcode:

Close More Loans with HomeReady Mortgage An Overview for Loan Officers Dial- in for audio: 1-800-779-8492 Attendee passcode: 4344988 Seminar guidelines Please do not place the call on hold at any time.

Close More Loans with HomeReady Mortgage An Overview for Loan Officers Dial- in for audio: 1-800-779-8492 Attendee passcode: 4344988 Seminar guidelines Please do not place the call on hold at any time.

High LTV Lending Conference

High LTV Lending Conference Eric Belsky May 213 Chapel Hill, NC Homeownership Has Mattered Profoundly to Wealth Accumulation Even After Crude Control for Income 12 Median Net Worth of Middle Income Quintile

High LTV Lending Conference Eric Belsky May 213 Chapel Hill, NC Homeownership Has Mattered Profoundly to Wealth Accumulation Even After Crude Control for Income 12 Median Net Worth of Middle Income Quintile

Purchase: Conventional, FHA, USDA, VA. Refinance: Conventional, FHA, USDA, VA. Emerging Banker

http://www.uhwholesale.com File Type Purchase: Conventional, FHA, USDA, VA Refinance: Conventional, FHA, USDA, VA Closing Doc Turn Times Initial CD will be issued when all Prior to Approval conditions

http://www.uhwholesale.com File Type Purchase: Conventional, FHA, USDA, VA Refinance: Conventional, FHA, USDA, VA Closing Doc Turn Times Initial CD will be issued when all Prior to Approval conditions

Challenges and Opportunities for Low Downpayment Lending

Challenges and Opportunities for Low Downpayment Lending Roberto G. Quercia UNC Center for Community Capital University of North Carolina at Chapel Hill Chapel Hill NC, May 17, 2013 Research Funded by

Challenges and Opportunities for Low Downpayment Lending Roberto G. Quercia UNC Center for Community Capital University of North Carolina at Chapel Hill Chapel Hill NC, May 17, 2013 Research Funded by

Define USDA products and features Introduce Planet Home Lending s USDA product offerings Learn how to determine property and borrower eligibility

Define USDA products and features Introduce Planet Home Lending s USDA product offerings Learn how to determine property and borrower eligibility Review credit, income, asset and appraisal guidelines Tips

Define USDA products and features Introduce Planet Home Lending s USDA product offerings Learn how to determine property and borrower eligibility Review credit, income, asset and appraisal guidelines Tips

Expanding Homeownership Responsibly National Federation of Community Development Credit Unions. Sandra Heidinger September 2017

Expanding Homeownership Responsibly National Federation of Community Development Credit Unions Sandra Heidinger September 2017 A Better Freddie Mac and a better housing finance system For families...innovating

Expanding Homeownership Responsibly National Federation of Community Development Credit Unions Sandra Heidinger September 2017 A Better Freddie Mac and a better housing finance system For families...innovating

Rate Lock Hours: 7:30-4:00 PST Toll Free: (866) WHOLESALE RATESHEET Lock Desk: (866) FHA Loan Programs

WHOLESALE RATESHEET Lock Desk: (866) FHA Loan Programs") FHA Loan Programs FHA 30yr Fixed FHA 30yr Fixed High Balance FHA 15yr Fixed F30F H30F F15F 5.000 (6.000) (6.000) (6.000) (6.000) 4.625 (5.596) (5.471) (5.346) (5.221) 4.125 (4.870) (4.729) (4.566) (4.406)

FHA Loan Programs FHA 30yr Fixed FHA 30yr Fixed High Balance FHA 15yr Fixed F30F H30F F15F 5.000 (6.000) (6.000) (6.000) (6.000) 4.625 (5.596) (5.471) (5.346) (5.221) 4.125 (4.870) (4.729) (4.566) (4.406)

Purchase: Conventional, FHA, USDA, VA. Refinance: Conventional, FHA, USDA, VA. Emerging Banker

http://www.uhwholesale.com File Type Purchase: Conventional, FHA, USDA, VA Refinance: Conventional, FHA, USDA, VA Closing Doc Turn Times Initial CD will be issued when all Prior to Approval conditions

http://www.uhwholesale.com File Type Purchase: Conventional, FHA, USDA, VA Refinance: Conventional, FHA, USDA, VA Closing Doc Turn Times Initial CD will be issued when all Prior to Approval conditions

Expanding Homeownership Responsibly with Freddie Mac Home Possible. February 2017

Expanding Homeownership Responsibly with Freddie Mac Home Possible February 2017 Presenter Dennis J. Smith Joined Freddie Mac in September 2015 as Affordable Lending Manager Works with lenders, nonprofits

Expanding Homeownership Responsibly with Freddie Mac Home Possible February 2017 Presenter Dennis J. Smith Joined Freddie Mac in September 2015 as Affordable Lending Manager Works with lenders, nonprofits

Expanding Homeownership Responsibly with Freddie Mac Home Possible. Nadja Vital MBA Central FL, Nov.8, 2017

Expanding Homeownership Responsibly with Freddie Mac Home Possible Nadja Vital MBA Central FL, Nov.8, 2017 A Better Freddie Mac and a better housing finance system For families...innovating to improve

Expanding Homeownership Responsibly with Freddie Mac Home Possible Nadja Vital MBA Central FL, Nov.8, 2017 A Better Freddie Mac and a better housing finance system For families...innovating to improve

WHOLESALE BORROWER PAID COMPENSATION RATE SHEET. Liberty Savings Bank Contact Information

Rate Sheet Date: Rate Sheet Price Code: 3/8/2019 3453 *Effective at 11:00 am EST WHOLESALE BORROWER PAID COMPENSATION RATE SHEET FOR LENDER PAID, BROKER MUST DEDUCT COMPENSATION Liberty Savings Bank Contact

Rate Sheet Date: Rate Sheet Price Code: 3/8/2019 3453 *Effective at 11:00 am EST WHOLESALE BORROWER PAID COMPENSATION RATE SHEET FOR LENDER PAID, BROKER MUST DEDUCT COMPENSATION Liberty Savings Bank Contact

First Time Homebuyers

First Time Homebuyers Presented By: Rich Goodwin, Vice President of Mortgage Lending Copyright 2000-2014 Guaranteed Rate. All rights reserved. Our Competitive Advantage Fast and transparent mortgage process

First Time Homebuyers Presented By: Rich Goodwin, Vice President of Mortgage Lending Copyright 2000-2014 Guaranteed Rate. All rights reserved. Our Competitive Advantage Fast and transparent mortgage process

FNMA Home Affordable Refinance Program (HARP) Transaction Type Number of Units Fixed Rate Max LTV/CLTV

Transaction Type Number of Units Fixed Rate Max LTV/CLTV") FNMA Conventional Conforming Product Offering Transaction Type Number of Fixed Rate Cash-Out Refinance Second Home Adjustable Rate 1 Unit 97/97% 90/90% 2 Unit 85/85% 75/75% 3 4 75/75% 65/65% 1 Unit 80/80%

FNMA Conventional Conforming Product Offering Transaction Type Number of Fixed Rate Cash-Out Refinance Second Home Adjustable Rate 1 Unit 97/97% 90/90% 2 Unit 85/85% 75/75% 3 4 75/75% 65/65% 1 Unit 80/80%

Real Estate Professional Training The Key to Serving First-time Homebuyers. Why Should VHDA Train Real Estate Professionals?

Real Estate Professional Training The Key to Serving First-time Homebuyers January, 2018 Linda Wine 0 Why Should VHDA Train Real Estate Professionals? You are often the first contact for a first-time homebuyer

Real Estate Professional Training The Key to Serving First-time Homebuyers January, 2018 Linda Wine 0 Why Should VHDA Train Real Estate Professionals? You are often the first contact for a first-time homebuyer

How to Originate and Deliver HomeReady Mortgages

How to Originate and Deliver HomeReady Mortgages 2016 Fannie Mae. Trademarks of Fannie Mae. An Important Note about the Seminar Content While every effort has been made to ensure the reliability of the

How to Originate and Deliver HomeReady Mortgages 2016 Fannie Mae. Trademarks of Fannie Mae. An Important Note about the Seminar Content While every effort has been made to ensure the reliability of the

Mortgage. A Beginner s. Rates. Guide

Mortgage Rates A Beginner s Guide US Mortgage Corporation (NMLS ID#3901). Corporate Office is located at 201 Old Country Road, Suite 140, Melville, NY 11747; 631-580-2600 or (800) 562-6715 (LOANS15). Licensed

Mortgage Rates A Beginner s Guide US Mortgage Corporation (NMLS ID#3901). Corporate Office is located at 201 Old Country Road, Suite 140, Melville, NY 11747; 631-580-2600 or (800) 562-6715 (LOANS15). Licensed

The Way to Greater Efficiency. Correspondent Lending

The Way to Greater Efficiency Correspondent Lending High-level service and partnership that uniquely leverages technology, processes and people to ensure effi cient and timely loan purchases Meeting the

The Way to Greater Efficiency Correspondent Lending High-level service and partnership that uniquely leverages technology, processes and people to ensure effi cient and timely loan purchases Meeting the

% % >80% & 95%

Wholesale Division US Bank Home Mortgage Wholesale Pricing Effective: 2/13/18 98.500 98.5 HELP DESK 800-200-5881 Page: 1 of 5 CONVENTIONAL FIXED RATE LOANS 6 30 45 60 75 LOAN SIZE AND STATE ADJUSTMENT

Wholesale Division US Bank Home Mortgage Wholesale Pricing Effective: 2/13/18 98.500 98.5 HELP DESK 800-200-5881 Page: 1 of 5 CONVENTIONAL FIXED RATE LOANS 6 30 45 60 75 LOAN SIZE AND STATE ADJUSTMENT

State of the Housing Market

State of the Housing Market 2 Freddie Mac s Mission Freddie Mac makes homeownership and rental housing more accessible and affordable by providing liquidity, stability, and affordability to the U.S. housing

State of the Housing Market 2 Freddie Mac s Mission Freddie Mac makes homeownership and rental housing more accessible and affordable by providing liquidity, stability, and affordability to the U.S. housing

May 17, Housing Sector Overview

May 17, 2017 Housing Sector Overview Housing Finance Policy Center May 17, 2017 AFFORDABLE HOUSING: In general, housing for which the occupant(s) is/are paying no more than 30 percent of his or her income

May 17, 2017 Housing Sector Overview Housing Finance Policy Center May 17, 2017 AFFORDABLE HOUSING: In general, housing for which the occupant(s) is/are paying no more than 30 percent of his or her income

WHOLESALE BORROWER PAID COMPENSATION RATE SHEET. Liberty Savings Bank Contact Information

Rate Sheet Date: Rate Sheet Price Code: *Effective at 11:00 am EST 09/14/2018 3319 WHOLESALE BORROWER PAID COMPENSATION RATE SHEET FOR LENDER PAID, BROKER MUST DEDUCT COMPENSATION Liberty Savings Bank

Rate Sheet Date: Rate Sheet Price Code: *Effective at 11:00 am EST 09/14/2018 3319 WHOLESALE BORROWER PAID COMPENSATION RATE SHEET FOR LENDER PAID, BROKER MUST DEDUCT COMPENSATION Liberty Savings Bank

Native American Indian Housing Council 2018 Annual Conference. San Diego, CA May 30, Collaborating with Fannie Mae to Expand Affordable Housing

Native American Indian Housing Council 2018 Annual Conference San Diego, CA May 30, 2018 Collaborating with Fannie Mae to Expand Affordable Housing 2017 Fannie Mae. Trademarks of Fannie Mae. 1 Agenda Who

Native American Indian Housing Council 2018 Annual Conference San Diego, CA May 30, 2018 Collaborating with Fannie Mae to Expand Affordable Housing 2017 Fannie Mae. Trademarks of Fannie Mae. 1 Agenda Who

Partner Overview. Springboard CDFI background and Nationwide Mortgage Collaborative

Partner Overview Springboard CDFI background and Nationwide Mortgage Collaborative Springboard CDFI Bridging the wealth gap in America by providing scaled solutions and access to capital; with a focus

Partner Overview Springboard CDFI background and Nationwide Mortgage Collaborative Springboard CDFI Bridging the wealth gap in America by providing scaled solutions and access to capital; with a focus

Grow Your Business with Freddie Mac Home Possible Mortgages. Jenneese Worley, Account Executive, Nadja Vital, Affordable Manager

Grow Your Business with Freddie Mac Home Possible Mortgages Jenneese Worley, Account Executive, Nadja Vital, Affordable Manager June 9, 2016 Single-Family 2016 priorities 1. Look for better ways to provide

Grow Your Business with Freddie Mac Home Possible Mortgages Jenneese Worley, Account Executive, Nadja Vital, Affordable Manager June 9, 2016 Single-Family 2016 priorities 1. Look for better ways to provide

FNMA HomeReady & Loan Programs 97%

HomeReady FNMA Standard 97% Description Program DU Eligibility Huron Valley Financial product offering for Fannie Mae 97% is three products offered: 97% Fannie Mae Home Ready Fannie Mae Standard 97% Fannie

HomeReady FNMA Standard 97% Description Program DU Eligibility Huron Valley Financial product offering for Fannie Mae 97% is three products offered: 97% Fannie Mae Home Ready Fannie Mae Standard 97% Fannie

Expanding Homeownership Responsibly with Freddie Mac Home Possible

Expanding Homeownership Responsibly with Freddie Mac Home Possible March 23, 2017 A Better Freddie Mac and a better housing finance system For families...innovating to improve the liquidity, stability

Expanding Homeownership Responsibly with Freddie Mac Home Possible March 23, 2017 A Better Freddie Mac and a better housing finance system For families...innovating to improve the liquidity, stability

Mortgage Services III, L.L.C.

(Bank & Credit Union Partners Only) Market conditions are generally: (compared to previous price sheet) Slightly Worse! December 8, 2017 Rate Sheet Updated as of: CONFORMING -- FIXED RATE PROGRAMS #300000-30

(Bank & Credit Union Partners Only) Market conditions are generally: (compared to previous price sheet) Slightly Worse! December 8, 2017 Rate Sheet Updated as of: CONFORMING -- FIXED RATE PROGRAMS #300000-30

Enhance Your Financial Security. With a Home Equity Conversion Mortgage

Enhance Your Financial Security With a Home Equity Conversion Mortgage Liberty Home Equity Solutions, Inc. 10951 White Rock Road, Suite 200 Rancho Cordova, CA 95670 800.976.6211 www.reverse.org Unlock

Enhance Your Financial Security With a Home Equity Conversion Mortgage Liberty Home Equity Solutions, Inc. 10951 White Rock Road, Suite 200 Rancho Cordova, CA 95670 800.976.6211 www.reverse.org Unlock

Crescent Mortgage Company 5901 Peachtree Dunwoody Road NE, Bldg C, Suite 250 Atlanta, GA 30328

(800) 851-0263 www.crescentexpress.net Wednesday, February 20, 2013 Crescent Mortgage Company 5901 Peachtree Dunwoody Road NE, Bldg C, Suite 250 Atlanta, GA 30328 EST Market Update: 2/20/2013 MBA Mortgage

(800) 851-0263 www.crescentexpress.net Wednesday, February 20, 2013 Crescent Mortgage Company 5901 Peachtree Dunwoody Road NE, Bldg C, Suite 250 Atlanta, GA 30328 EST Market Update: 2/20/2013 MBA Mortgage

Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328

(800) 851-0263 www.crescentmortgage.com Tuesday, June 12, 2018 Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328 ET Market Update: 6/12/2018 May Consumer

(800) 851-0263 www.crescentmortgage.com Tuesday, June 12, 2018 Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328 ET Market Update: 6/12/2018 May Consumer

Mortgage Services III, L.L.C.

Home Office Ph. #: 888-664-9108 Oakbrook Office Ph. #: 630-396-3553 Pricing E-Fax #: 309-807-0717 Web Site: www.msiloans.biz Pricing E-Mail: msipricing@msiloans.biz (Bank & Credit Union Partners Only)

Home Office Ph. #: 888-664-9108 Oakbrook Office Ph. #: 630-396-3553 Pricing E-Fax #: 309-807-0717 Web Site: www.msiloans.biz Pricing E-Mail: msipricing@msiloans.biz (Bank & Credit Union Partners Only)

<logo> Offered through 21 st Century Home Loans WHOLESALE DIVISION

CHF ACCESS Training Offered through 21 st Century Home Loans WHOLESALE DIVISION Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie

CHF ACCESS Training Offered through 21 st Century Home Loans WHOLESALE DIVISION Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie

Mortgage Services III, L.L.C.

Home Office Ph. #: 888-664-9108 Oakbrook Office Ph. #: 630-396-3553 Pricing E-Fax #: 309-807-0717 Web Site: www.msiloans.biz Pricing E-Mail: msipricing@msiloans.biz (Bank & Credit Union Partners Only)

Home Office Ph. #: 888-664-9108 Oakbrook Office Ph. #: 630-396-3553 Pricing E-Fax #: 309-807-0717 Web Site: www.msiloans.biz Pricing E-Mail: msipricing@msiloans.biz (Bank & Credit Union Partners Only)

Expanding Homeownership Responsibly with Freddie Mac. March 2, 2017

Expanding Homeownership Responsibly with Freddie Mac March 2, 2017 A Better Freddie Mac and a better housing finance system For homebuyers...innovating to improve the liquidity, stability and affordability

Expanding Homeownership Responsibly with Freddie Mac March 2, 2017 A Better Freddie Mac and a better housing finance system For homebuyers...innovating to improve the liquidity, stability and affordability

Niche Loan Programs. Featured Loan. Zero Down Loan

Niche Loan Programs To cater the different needs of out clients Shining Star Funding offers diverse Niche Loan Programs. Contact our mortgage specialist to review which product best suits your financial

Niche Loan Programs To cater the different needs of out clients Shining Star Funding offers diverse Niche Loan Programs. Contact our mortgage specialist to review which product best suits your financial

Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328

(800) 851-0263 www.crescentmortgage.com Thursday, April 11, 2019 Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328 ET Market Update: 4/11/2019 Producer

(800) 851-0263 www.crescentmortgage.com Thursday, April 11, 2019 Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328 ET Market Update: 4/11/2019 Producer

Role of HFAs and FHA in supporting homeownership

Role of HFAs and FHA in supporting homeownership Ed Golding Housing Finance Policy Center Urban Institute HFA Institute Washington, DC January 12, 2018 Introduction Homeownership has been supported by

Role of HFAs and FHA in supporting homeownership Ed Golding Housing Finance Policy Center Urban Institute HFA Institute Washington, DC January 12, 2018 Introduction Homeownership has been supported by

Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328

(800) 851-0263 www.crescentmortgage.com Monday, March 25, 2019 Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328 ET Market Update: 3/25/2019 Chicago Fed

(800) 851-0263 www.crescentmortgage.com Monday, March 25, 2019 Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328 ET Market Update: 3/25/2019 Chicago Fed

Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328

(800) 851-0263 www.crescentmortgage.com Tuesday, April 16, 2019 Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328 ET Market Update: 4/16/2019 Industrial

(800) 851-0263 www.crescentmortgage.com Tuesday, April 16, 2019 Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328 ET Market Update: 4/16/2019 Industrial

FNMA s HomeReady Program

FNMA s HomeReady Program (rev. 6/30/2016) Presented by J.J. Sawicki, CMP Merrimack Mortgage Co. LLC Overview Help meet the diverse needs of today s buyers with FNMA s enhanced affordable lending program,

FNMA s HomeReady Program (rev. 6/30/2016) Presented by J.J. Sawicki, CMP Merrimack Mortgage Co. LLC Overview Help meet the diverse needs of today s buyers with FNMA s enhanced affordable lending program,

Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328

(800) 851-0263 www.crescentmortgage.com Thursday, March 21, 2019 Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328 ET Market Update: 3/21/2019 Philly

(800) 851-0263 www.crescentmortgage.com Thursday, March 21, 2019 Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328 ET Market Update: 3/21/2019 Philly

Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328

(800) 851-0263 www.crescentmortgage.com Friday, April 19, 2019 Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328 ET Market Update: 4/19/2019 Bond Market

(800) 851-0263 www.crescentmortgage.com Friday, April 19, 2019 Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328 ET Market Update: 4/19/2019 Bond Market

Refinance Report August 2012

This report contains data on refinance program activity of Fannie Mae and Freddie Mac (the Enterprises) through. Report Highlights Refinance volume continued to be strong in August as 30-year mortgage

This report contains data on refinance program activity of Fannie Mae and Freddie Mac (the Enterprises) through. Report Highlights Refinance volume continued to be strong in August as 30-year mortgage

ditech BUSINESS LENDING HOMEREADY MORTGAGE PRODUCT

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING HOMEREADY MORTGAGE PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10-30 year term in annual increments Fully amortizing

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING HOMEREADY MORTGAGE PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10-30 year term in annual increments Fully amortizing

Hit the Books: First Time Homebuyer Programs from FNMA and FHLMC

Hit the Books: First Time Homebuyer Programs from FNMA and FHLMC Two common first time homebuyer programs are MyCommunityMortgage from FNMA and Home Possible from FHLMC. This reference will help you understand

Hit the Books: First Time Homebuyer Programs from FNMA and FHLMC Two common first time homebuyer programs are MyCommunityMortgage from FNMA and Home Possible from FHLMC. This reference will help you understand

GUILD MORTGAGE COMPANY Loan program cheat sheet. 100% Financing REHAB PROGRAM 97% FINANCING PROGRAMS CONFORMING ARMS NON CONFORMING ARMS

GUILD MORTGAGE COMPANY Loan program cheat sheet Mar-09 100% Financing REHAB PROGRAM USDA - Rural Housing FHA 203K Streamline VA 97% FINANCING PROGRAMS CONFORMING ARMS FNMA FLEX Win World FNMA My Community

GUILD MORTGAGE COMPANY Loan program cheat sheet Mar-09 100% Financing REHAB PROGRAM USDA - Rural Housing FHA 203K Streamline VA 97% FINANCING PROGRAMS CONFORMING ARMS FNMA FLEX Win World FNMA My Community

Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328

(800) 851-0263 www.crescentmortgage.com Wednesday, March 20, 2019 Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328 ET Market Update: 3/20/2019 Price

(800) 851-0263 www.crescentmortgage.com Wednesday, March 20, 2019 Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328 ET Market Update: 3/20/2019 Price

7389 Florida Blvd., Suite 200A Baton Rouge, LA NMLS #

Version 2018.May 7389 Florida Blvd., Suite 200A Baton Rouge, LA 70806 855.476.8441 NMLS #64997 www.gmfspartners.com 2014, GMFS LLC. All Rights Reserved. GMFS is a registered trade name of GMFS LLC., NMLS

Version 2018.May 7389 Florida Blvd., Suite 200A Baton Rouge, LA 70806 855.476.8441 NMLS #64997 www.gmfspartners.com 2014, GMFS LLC. All Rights Reserved. GMFS is a registered trade name of GMFS LLC., NMLS

Caliber RESPA/TILA Fee Guide By Fee Name

203 (k) Architectural and Engineering Fee Section C. Can Shop No 203 (k) Contingency Reserve Section H. Other No 203 (k) Repairs Section H. Other No 203 (k) Title Update Fee Section C. Can Shop Yes 203K

203 (k) Architectural and Engineering Fee Section C. Can Shop No 203 (k) Contingency Reserve Section H. Other No 203 (k) Repairs Section H. Other No 203 (k) Title Update Fee Section C. Can Shop Yes 203K

Mortgage Services III, L.L.C.

Home Office Ph. #: 888-664-9108 Oakbrook Office Ph. #: 630-396-3553 Pricing E-Fax #: 309-807-0717 Web Site: www.msiloans.biz Pricing E-Mail: msipricing@msiloans.biz Bloomington Office Ph. #: 888-664-9108

Home Office Ph. #: 888-664-9108 Oakbrook Office Ph. #: 630-396-3553 Pricing E-Fax #: 309-807-0717 Web Site: www.msiloans.biz Pricing E-Mail: msipricing@msiloans.biz Bloomington Office Ph. #: 888-664-9108

LPA HOME POSSIBLE. Home Possible

LPA HOME POSSIBLE Description: Product Term HPML Loan Purpose Acceptable Property Types Home Possible Home Possible (HP) is a Freddie Mac Community Lending program is designed to meet the needs of low-

LPA HOME POSSIBLE Description: Product Term HPML Loan Purpose Acceptable Property Types Home Possible Home Possible (HP) is a Freddie Mac Community Lending program is designed to meet the needs of low-

Written for state Housing Finance Agencies (HFAs), this report furthers the work of the Innovations in Manufactured Homes (I M HOME) initiative s

, this report furthers the work of the Innovations in Manufactured Homes (I M HOME) initiative s") Written for state Housing Finance Agencies (HFAs), this report furthers the work of the Innovations in Manufactured Homes (I M HOME) initiative s explorations into manufactured home mortgage data. This

Written for state Housing Finance Agencies (HFAs), this report furthers the work of the Innovations in Manufactured Homes (I M HOME) initiative s explorations into manufactured home mortgage data. This

Minnesota Housing: A Path to Successful Homeownership. A Path to Homeownership & Family Self-Sufficiency (REP)

") Minnesota Housing: A Path to Successful Homeownership Minnesota Housing: Real Estate Program A Path to Homeownership & Family Self-Sufficiency (REP) Today s conversation Who we are Why we re here Increasing

Minnesota Housing: A Path to Successful Homeownership Minnesota Housing: Real Estate Program A Path to Homeownership & Family Self-Sufficiency (REP) Today s conversation Who we are Why we re here Increasing

Eye on the South Carolina Housing Market presented at 2008 HBA of South Carolina State Convention August 1, 2008

Eye on the South Carolina Housing Market presented at 28 HBA of South Carolina State Convention August 1, 28 Robert Denk Assistant Staff Vice President, Forecasting & Analysis 2, US Single Family Housing

Eye on the South Carolina Housing Market presented at 28 HBA of South Carolina State Convention August 1, 28 Robert Denk Assistant Staff Vice President, Forecasting & Analysis 2, US Single Family Housing

Mortgage Terms Glossary

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

Mortgage Terms Glossary Adjustable-Rate Mortgage (ARM) A mortgage where the interest rate is not fixed, but changes during the life of the loan in line with movements in an index rate. You may also see

FHLMC Only Conforming and Maximum DTI is the more restrictive of Loan Product Advisor or 50%.

AUS (Automated Underwriting System) GENERAL POLICY OVERLAYS FHA, VA, CONVENTIONAL and USDA FHA, VA & Conventional AUS approval recommendation is required for all FHA, VA, (Purchase and Non-Streamline/Non-IRRRL

AUS (Automated Underwriting System) GENERAL POLICY OVERLAYS FHA, VA, CONVENTIONAL and USDA FHA, VA & Conventional AUS approval recommendation is required for all FHA, VA, (Purchase and Non-Streamline/Non-IRRRL

Basics in Mortgage Lending Test for Loan Officers

Basics in Mortgage Lending Test for Loan Officers Name: Date: Company Name: 1. The purpose of the Equal Credit Opportunity Act is: To discourage predatory lending To create new avenues and programs for

Basics in Mortgage Lending Test for Loan Officers Name: Date: Company Name: 1. The purpose of the Equal Credit Opportunity Act is: To discourage predatory lending To create new avenues and programs for

7389 Florida Blvd., Suite 200A Baton Rouge, LA NMLS #

Version 2018.October 7389 Florida Blvd., Suite 200A Baton Rouge, LA 70806 855.476.8441 NMLS #64997 www.gmfspartners.com 2014, GMFS LLC. All Rights Reserved. GMFS is a registered trade name of GMFS LLC.,

Version 2018.October 7389 Florida Blvd., Suite 200A Baton Rouge, LA 70806 855.476.8441 NMLS #64997 www.gmfspartners.com 2014, GMFS LLC. All Rights Reserved. GMFS is a registered trade name of GMFS LLC.,

Cash Assistance Mortgage Training

HOMEOWNERSHIP Cash Assistance Mortgage Training January 2019 NHHFA.org Today s Agenda What s New with the Cash Assistance Mortgage The Value of Cash Assistance About the Cash Assistance Mortgage Participating

HOMEOWNERSHIP Cash Assistance Mortgage Training January 2019 NHHFA.org Today s Agenda What s New with the Cash Assistance Mortgage The Value of Cash Assistance About the Cash Assistance Mortgage Participating

Update On Mortgage Originations, Delinquency and Foreclosures In Maryland

Update On Mortgage Originations, Delinquency and Foreclosures In Maryland The Reinvestment Fund builds wealth and opportunity for low-wealth people and places through the promotion of socially and environmentally

Update On Mortgage Originations, Delinquency and Foreclosures In Maryland The Reinvestment Fund builds wealth and opportunity for low-wealth people and places through the promotion of socially and environmentally

GOVERNMENT LOANS 30 YR FIXED RATE 30 YEAR 3/1 2.0/2.25 MARGIN 30 YEAR FIXED RATE FHA CONFORMING JUMBO 203 (K) 30 YEAR FIXED

30 YEAR FIXED") GOVERNMENT LOANS PAGE 1 OF 8 30 YEAR FIXED 30 YR FIXED RATE 30 YEAR 3/1 2.0/2.25 MARGIN 30 YEAR FIXED RATE FHA CONFORMING JUMBO FHA/VA ARMS 1001 FHA 2001 VA 1004 FHA Buydown 3001 RHS 1020 203K Streamline

GOVERNMENT LOANS PAGE 1 OF 8 30 YEAR FIXED 30 YR FIXED RATE 30 YEAR 3/1 2.0/2.25 MARGIN 30 YEAR FIXED RATE FHA CONFORMING JUMBO FHA/VA ARMS 1001 FHA 2001 VA 1004 FHA Buydown 3001 RHS 1020 203K Streamline

In Baltimore City today, 20% of households live in poverty, but more than half of the

Building Economic Opportunity in Baltimore: A Data Profile Baltimore Highlights In Baltimore City today, 20% of households live in poverty, but more than half of the city s population 55% is financially

Building Economic Opportunity in Baltimore: A Data Profile Baltimore Highlights In Baltimore City today, 20% of households live in poverty, but more than half of the city s population 55% is financially

The 2017 Economic Outlook Summit

The 2017 Economic Outlook Summit Southeast Fairfax Development Corporation Mount Vernon-Lee Chamber of Commerce Frank Nothaft, CoreLogic SVP & Chief Economist April 6, 2017 2017 Market: Less Affordability

The 2017 Economic Outlook Summit Southeast Fairfax Development Corporation Mount Vernon-Lee Chamber of Commerce Frank Nothaft, CoreLogic SVP & Chief Economist April 6, 2017 2017 Market: Less Affordability

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year

Assistance Program: City of Jacksonville Head Start to Homeownership Program Code: DFLJAHOME

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fannie Mae Fixed 30 year Conforming

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fannie Mae Fixed 30 year Conforming

Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328

(800) 851-0263 www.crescentmortgage.com Tuesday, March 26, 2019 Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328 ET Market Update: 3/26/2019 Housing

(800) 851-0263 www.crescentmortgage.com Tuesday, March 26, 2019 Crescent Mortgage Company 6600 Peachtree Dunwoody Rd NE, 600 Embassy Row Ste #650, Atlanta, GA 30328 ET Market Update: 3/26/2019 Housing

Comparative Revenues and Revenue Forecasts Prepared By: Bureau of Legislative Research Fiscal Services Division State of Arkansas

Comparative Revenues and Revenue Forecasts 2010-2014 Prepared By: Bureau of Legislative Research Fiscal Services Division State of Arkansas Comparative Revenues and Revenue Forecasts This data shows tax

Comparative Revenues and Revenue Forecasts 2010-2014 Prepared By: Bureau of Legislative Research Fiscal Services Division State of Arkansas Comparative Revenues and Revenue Forecasts This data shows tax

Assistance Program: City of Tampa Mortgage Assistance Program Code: DFLTAMPA

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year

Purchase Special:.250 Price Improvement on 30day Locks*

Rev 3.1 RS ID: 7:21 AM Zone 2 AZ, CO, DC, FL, GA, ID, IL, IN, KY, LA, MA, MD, MI, MO, NC, MN, MT, ND, NH, NJ, OH, OK, PA, SC, TN, TX, Extensions Fee Buyout Option 3-Day 0.063 14-Day 0.250 $50

Rev 3.1 RS ID: 7:21 AM Zone 2 AZ, CO, DC, FL, GA, ID, IL, IN, KY, LA, MA, MD, MI, MO, NC, MN, MT, ND, NH, NJ, OH, OK, PA, SC, TN, TX, Extensions Fee Buyout Option 3-Day 0.063 14-Day 0.250 $50

THDA Homebuyer Education Initiative Customer Intake Form

Sample 3 Date Case# (Trainer completes) Trainer Organization County (Trainer completes) THDA Homebuyer Education Initiative Customer Intake Form Please provide information about yourself for customer tracking

Sample 3 Date Case# (Trainer completes) Trainer Organization County (Trainer completes) THDA Homebuyer Education Initiative Customer Intake Form Please provide information about yourself for customer tracking

Ability To Repay (ATR) Creditors must determine that borrowers have a reasonable ability to repay a loan based on consideration and verification of

Creditors must determine that borrowers have a reasonable ability to repay a loan based on consideration and verification of") Ability To Repay (ATR) Creditors must determine that borrowers have a reasonable ability to repay a loan based on consideration and verification of factors indicative of a consumer s credit capacity, including:

Ability To Repay (ATR) Creditors must determine that borrowers have a reasonable ability to repay a loan based on consideration and verification of factors indicative of a consumer s credit capacity, including:

AGENDA State of the industry First Time Homebuyer definition Pre-qualification letter vs Pre-approval letters Mortgage qualification guidelines Unders

AGENDA State of the industry First Time Homebuyer definition Pre-qualification letter vs Pre-approval letters Mortgage qualification guidelines Understanding Credit Programs Impact of TRID (TILA Respa

AGENDA State of the industry First Time Homebuyer definition Pre-qualification letter vs Pre-approval letters Mortgage qualification guidelines Understanding Credit Programs Impact of TRID (TILA Respa

HOMEBUYER WORKSHOP REGISTRATION FORM

HOMEBUYER WORKSHOP REGISTRATION FORM Organization: Workshop location: Workshop Date(s): Instructions: Please fill out as completely as possible. Home Buyer Name: (Please print) First MI Last Address: Zip:

HOMEBUYER WORKSHOP REGISTRATION FORM Organization: Workshop location: Workshop Date(s): Instructions: Please fill out as completely as possible. Home Buyer Name: (Please print) First MI Last Address: Zip:

BUILDING STRONGER COMMUNITIES TOGETHER: IMMIGRANTS AND ASSET BUILDING FLORIDA PHILANTHROPY NETWORK SUMMIT FEBRUARY 2017

BUILDING STRONGER COMMUNITIES TOGETHER: IMMIGRANTS AND ASSET BUILDING 1 FLORIDA PHILANTHROPY NETWORK SUMMIT FEBRUARY 2017 GCIR PROVIDES A FORUM FOR FUNDERS TO: Learn about current issues through in-depth

BUILDING STRONGER COMMUNITIES TOGETHER: IMMIGRANTS AND ASSET BUILDING 1 FLORIDA PHILANTHROPY NETWORK SUMMIT FEBRUARY 2017 GCIR PROVIDES A FORUM FOR FUNDERS TO: Learn about current issues through in-depth

Conventional 97% LTV Options updated 12/5/2018 Freddie Mac HomeOne Mortgage 97% LTV

Max Mortgage Credit Score Max 620, but due to MI requirements borrowers under 680 may benefit from FHA Financing due to MI amounts price comparison is strongly suggested 97% 1 unit 95% for 2 4 unit owner

Max Mortgage Credit Score Max 620, but due to MI requirements borrowers under 680 may benefit from FHA Financing due to MI amounts price comparison is strongly suggested 97% 1 unit 95% for 2 4 unit owner

Assistance Program: City of North Lauderdale Purchase Assistance Program Code: DFLLAUDER

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

Efforts to Improve Homeownership Opportunities for Hispanics

Efforts to Improve Homeownership Opportunities for Hispanics Case Studies of Three Market Areas U.S. Department of Housing and Urban Development Office of Policy Development and Research Efforts to Improve

Efforts to Improve Homeownership Opportunities for Hispanics Case Studies of Three Market Areas U.S. Department of Housing and Urban Development Office of Policy Development and Research Efforts to Improve

STEPS to getting an affordable home loan

4 STEPS to getting an affordable home loan 1 www.idahohousing.com 1 Start the process by finding a lender. Before you start house hunting, it s a good idea to pre-qualify for financing so you can be certain

4 STEPS to getting an affordable home loan 1 www.idahohousing.com 1 Start the process by finding a lender. Before you start house hunting, it s a good idea to pre-qualify for financing so you can be certain

Housing Counseling Work Plan (January 2017)

") Agency Background: Housing Counseling Work Plan (January 2017) Parkview Services (PARKVIEW) was established in 1967, as Parkview Homes for Exceptional Children to serve families with children with developmental

Agency Background: Housing Counseling Work Plan (January 2017) Parkview Services (PARKVIEW) was established in 1967, as Parkview Homes for Exceptional Children to serve families with children with developmental

PRODUCT MATRICES. For Information on any of our products, please contact:

Correspondent Lending PRODUCT MATRICES March 2016 For general underwriting questions and scenarios or product guideline interpretation, call the Underwriting Help Line at (866) 807-6049 For status, pricing,

Correspondent Lending PRODUCT MATRICES March 2016 For general underwriting questions and scenarios or product guideline interpretation, call the Underwriting Help Line at (866) 807-6049 For status, pricing,

Property Information

IMN DIRECT CAPITAL FUNDING Office: 404-228-5756 Email: cheryl@onesotpfunding.net LOAN APPLICATION Property Information Street Address City State Zip Purchase Price $ Estimated Property Value $ Requested

IMN DIRECT CAPITAL FUNDING Office: 404-228-5756 Email: cheryl@onesotpfunding.net LOAN APPLICATION Property Information Street Address City State Zip Purchase Price $ Estimated Property Value $ Requested

National Wholesale Rate Sheet

Effective Fri 03/15/2019 9:36 AM EST AL, AR, DC, DE, IA, IN, KS, KY, LA, MI, MN, MO, MS, NC, ND, NE, OH, OK, SC, SD, TN, WI, WV Check out our Smart Series Pricing Specials! SmartEdge, SmartEdge+, and SmartCondo

Effective Fri 03/15/2019 9:36 AM EST AL, AR, DC, DE, IA, IN, KS, KY, LA, MI, MN, MO, MS, NC, ND, NE, OH, OK, SC, SD, TN, WI, WV Check out our Smart Series Pricing Specials! SmartEdge, SmartEdge+, and SmartCondo

GSFA PLATINUM PROGRAM CONVENTIONAL GUIDELINES SUMMARY

OVERVIEW The GSFA Conventional Down Payment Assistance Program (DAP) is a competitively priced Conventional loan program that does not require a minimum down payment from the homebuyer(s). GSFA provides

OVERVIEW The GSFA Conventional Down Payment Assistance Program (DAP) is a competitively priced Conventional loan program that does not require a minimum down payment from the homebuyer(s). GSFA provides

FIRST TIME HOME BUYER S GUIDE TO FINANCING

FIRST TIME HOME BUYER S GUIDE TO FINANCING FIRST TIME HOME BUYER S GUIDE TO FINANCING CONTENTS Overview/Mortgage Solutions Financial Mission... 2 Get the Loan First: Pre-Approval... 3 What is FICO?...

FIRST TIME HOME BUYER S GUIDE TO FINANCING FIRST TIME HOME BUYER S GUIDE TO FINANCING CONTENTS Overview/Mortgage Solutions Financial Mission... 2 Get the Loan First: Pre-Approval... 3 What is FICO?...

Property Information

LOAN APPLICATION Page 1 of 7 Property Information Street Address City State Zip Purchase Price $ Estimated Property Value $ Requested Loan $ OR Requested LTV % What is the estimated property value based

LOAN APPLICATION Page 1 of 7 Property Information Street Address City State Zip Purchase Price $ Estimated Property Value $ Requested Loan $ OR Requested LTV % What is the estimated property value based

Flanagan State Banks Guide to FHA Disclosures

This reference guide outlines the packet that is provided for Initial Disclosures when using FSB Mortgagebot for disclosing. The documents are listed in the order the system prints the forms. Form Name

This reference guide outlines the packet that is provided for Initial Disclosures when using FSB Mortgagebot for disclosing. The documents are listed in the order the system prints the forms. Form Name

MHANY MANAGEMENT, INC. FIRST TIME HOMEBUYER/REFINANCE PROGRAM

MHANY MANAGEMENT, INC. FIRST TIME HOMEBUYER/REFINANCE PROGRAM MHANY Management, Inc. (MHANY) helps low and moderate income individuals and families so they can obtain and keep affordable, stable, safe,

MHANY MANAGEMENT, INC. FIRST TIME HOMEBUYER/REFINANCE PROGRAM MHANY Management, Inc. (MHANY) helps low and moderate income individuals and families so they can obtain and keep affordable, stable, safe,

19 FREQUENTLY ASKED QUESTIONS

19 FREQUENTLY ASKED QUESTIONS TERMS & CONDITIONS Q. What is the Total Debt To Income ratio allowed under the Program? A. The Total Debt To Income ratio cannot exceed 50.00%, unless other restrictions apply.

19 FREQUENTLY ASKED QUESTIONS TERMS & CONDITIONS Q. What is the Total Debt To Income ratio allowed under the Program? A. The Total Debt To Income ratio cannot exceed 50.00%, unless other restrictions apply.

NOTICE OF FUNDS AVAILABILITY RE: NEW MEXICO MORTGAGE FINANCE AUTHORITY (TAX-EXEMPT) FIRST HOME MBS PROGRAM JANUARY 2016

FIRST HOME MBS PROGRAM JANUARY 2016") NOTICE OF FUNDS AVAILABILITY RE: NEW MEXICO MORTGAGE FINANCE AUTHORITY (TAX-EXEMPT) FIRST HOME MBS PROGRAM JANUARY 2016 The New Mexico Mortgage Finance Authority ("MFA") has funds available under its single

NOTICE OF FUNDS AVAILABILITY RE: NEW MEXICO MORTGAGE FINANCE AUTHORITY (TAX-EXEMPT) FIRST HOME MBS PROGRAM JANUARY 2016 The New Mexico Mortgage Finance Authority ("MFA") has funds available under its single

Assistance Program: Marion County Homebuyer Purchase Assistance Program Code: DFLMARION

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

31% 41% 11% 50% 18% PROFILE ASSETS & OPPORTUNITY PROFILE: SAN FRANCISCO KEY HIGHLIGHTS ABOUT THE PROFILE ASSETS & OPPORTUNITY

ASSETS & OPPORTUNITY PROFILE: SAN FRANCISCO ASSETS & OPPORTUNITY PROFILE KEY HIGHLIGHTS 31% of San Francisco residents live in asset poverty Cities have long been thought of as places of opportunity for

ASSETS & OPPORTUNITY PROFILE: SAN FRANCISCO ASSETS & OPPORTUNITY PROFILE KEY HIGHLIGHTS 31% of San Francisco residents live in asset poverty Cities have long been thought of as places of opportunity for

Your Guide to Home Financing

Your Guide to Home Financing FURLONG TEAM 952-232-4133 www.furlongteam.com NMLS 275939 NMLS 225504 step 1- getting pre-approved How much home can you afford? Before you picture yourself living in a home,

Your Guide to Home Financing FURLONG TEAM 952-232-4133 www.furlongteam.com NMLS 275939 NMLS 225504 step 1- getting pre-approved How much home can you afford? Before you picture yourself living in a home,

Assistance Program: City of Los Angeles Low Income Purchase Assistance Program (LIPA) Zero Interest Code: DCALIPADP

Zero Interest Code: DCALIPADP") HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

Mortgage Assistance Program (MAP)

") Mortgage Assistance Program (MAP) A Briefing to the Housing Committee Housing Department September 16, 2008 KEY FOCUS AREA: ECONOMIC VIBRANCY Purpose To provide an update of the Mortgage Assistance Program

Mortgage Assistance Program (MAP) A Briefing to the Housing Committee Housing Department September 16, 2008 KEY FOCUS AREA: ECONOMIC VIBRANCY Purpose To provide an update of the Mortgage Assistance Program