Cash Assistance Mortgage Training

|

|

|

- June Miller

- 5 years ago

- Views:

Transcription

1 HOMEOWNERSHIP Cash Assistance Mortgage Training January 2019 NHHFA.org

2 Today s Agenda What s New with the Cash Assistance Mortgage The Value of Cash Assistance About the Cash Assistance Mortgage Participating Lender's Role Processing the Cash Assistance Mortgage Using the Cash Assistance Mortgage with Home Flex Plus and the NEW Home Preferred Plus Questions and Answers NHHFA.ORG/LENDERS 2

3 Disclaimer: The information in this material is for training and illustrative purposes only. The training material is not comprehensive and is not a legal or program document. The full Cash Assistance Mortgage Policy, February 19, 2019, and other program documents and contracts should be consulted for the complete requirements for this program. 3

4 What s New With the Cash Assistance Mortgage Program? 4

5 Big Picture: About the Cash Assistance Mortgage Cash Assistance Mortgage is mostly the same for both the Home Flex Plus and Home Preferred Plus! Disclosures Documents Underwriting Requesting Cash Assistance Income Limit Home Flex Plus Same Same Different Same $126, Home Preferred Plus Same Same Different Same 80% of Fannie Mae s AMI for the property* *See separate training on the new Home Preferred Income Limits. 5

6 Good News! Two 1 st mortgage loan products can now be combined with New Hampshire Housing s Cash Assistance Mortgage: Home Flex Plus (FHA, USDA/RD, VA); and Home Preferred Plus (NEW PROGRAM! conventional). Borrower can use the Cash Assistance for downpayment and closing costs. Helps low- and moderate-income homebuyers purchase a home. 6

7 The Value of Cash Assistance 7

8 Value of Cash Assistance Cash Assistance available for downpayment and closing costs on both Government insured and conventional loans. Helps get your borrowers: Get into a home earlier prices and rates may rise Cash Assistance tax free Provide economic benefit 5 to 7 year break even Retain reserves keep money for the unexpected Helps low- and moderate-income homebuyers purchase a home. 8

9 About the Cash Assistance Mortgage 9

10 Must Have a New Hampshire Housing 1 st Mortgage Home Flex Plus (FHA, VA or USDA Rural Development) Home Preferred Plus Note: Cash Assistance is only available with Home Preferred w/mi; not available with Home Preferred No MI. 10

11 About the Cash Assistance Mortgage New Hampshire Housing is the lender on the Cash Assistance Mortgage Cash Assistance Mortgage Actual recorded 2 nd mortgage No interest No periodic payments No fees to borrower Forgiven in full after four years, provided no Repayment Event 11

12 Cash Assistance Mortgage Forgiveness Date Full amount of Cash Assistance is forgiven on the fourth anniversary of the Cash Assistance Mortgage closing date, provided no Repayment Event. Example: Closing date: Forgiveness date: March 1, 2019 March 1,

13 Full amount of the Cash Assistance Mortgage will be repayable to New Hampshire Housing during the first four years if any of the following Repayment Events happen: Borrower repays or refinances the first mortgage; Borrower sells the home; or Borrower files bankruptcy. Notes: Cash Assistance Mortgage Repayment Events New Hampshire Housing will not subordinate the Cash Assistance Mortgage. Repayment obligation on refinance applies even if refinancing with New Hampshire Housing. Cash Assistance Mortgage will not be released as part of a modification or bankruptcy. 13

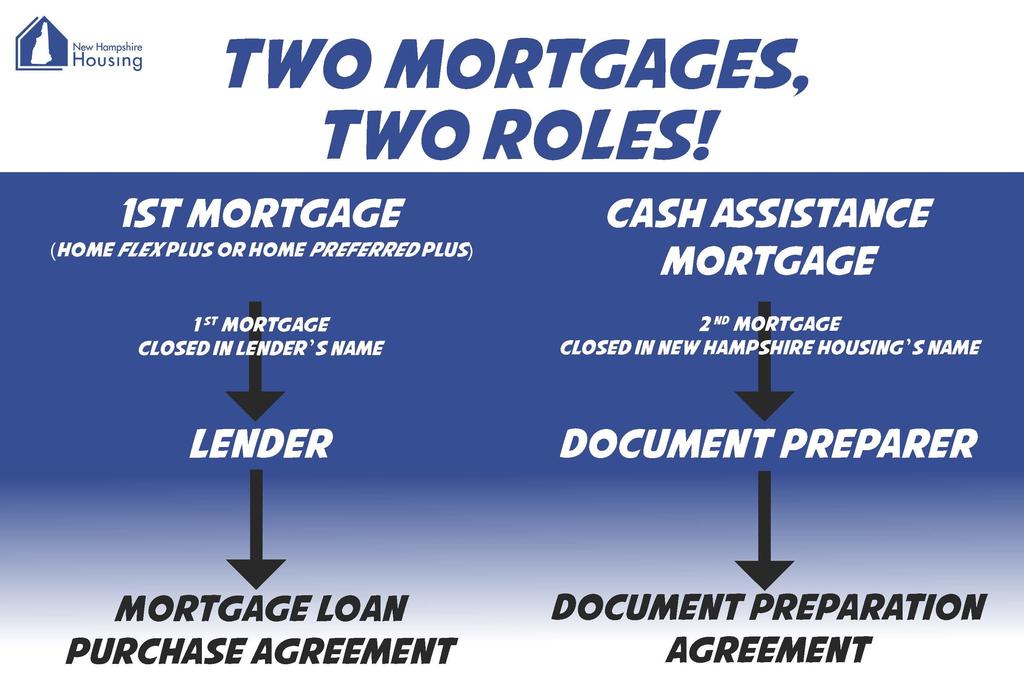

14 About the Cash Assistance Mortgage Participating Lender s Roles: 1. Participating Lender 1 st mortgage Home Flex Plus Mortgage or Home Preferred Plus 2. Document Preparer 2 nd mortgage Cash Assistance Mortgage 14

15 15

16 Two Defined Roles New Hampshire Housing will be the lender on the Cash Assistance Mortgage because New Hampshire Housing wants to: Preserve public-entity status Preserve housing finance agency (HFA) exemptions NMLS HMDA ATR/QM FHA CFPB For Home Flex Plus Have specific FHA Cash Assistance requirements 16

17 Participating Lender's Role 17

18 Participating Lender's Role 1 st Mortgage Participating Lender's Role: Lender 1 st mortgage product Home Flex Plus/Home Preferred Plus Must meet New Hampshire Housing s program guidelines Loan to be sold to New Hampshire Housing Governed by the Mortgage Loan Purchase Agreement 18

19 Participating Lender's Role Document Preparer Participating Lender's Role Cash Assistance Mortgage: Document Preparer not the lender. Loan is being made by New Hampshire Housing. The Document Preparer administers certain documents on behalf of New Hampshire Housing. Document Preparer will provide the borrower with disclosures as instructed by New Hampshire Housing. 19

20 Participating Lender's Role Document Preparer To offer the Home Flex Plus or Home Preferred Plus program, a Participating Lender must sign the: Document Preparation Agreement - Cash Assistance Mortgage Program This agreement: Defines roles; Preserves special HFA status and exemptions; and Protects the Participating Lender. 20

21 About the Cash Assistance Mortgage Processing the Cash Assistance Mortgage 21

22 Processing the Cash Assistance Mortgage Cash Assistance Mortgage is mostly the same for both the Home Flex Plus and Home Preferred Plus! Disclosures Documents Underwriting Requesting Cash Assistance Income Limit Home Flex Plus Same Same Different Same $126, Home Preferred Plus Same Same Different Same 80% of Fannie Mae s AMI for the property 22

23 Document Preparer Disclosures (Same) Document preparation on New Hampshire Housing s behalf. This includes: required closing disclosures, mortgage and promise to pay and recording. 1. Program Disclosure (Document Preparer) 2. Loan Estimate (Document Preparer) 3. Closing Disclosures (Document Preparer) 4. Cash Assistance Mortgage (New Hampshire Housing complete this) 23

24 IMPORTANT! New Hampshire Housing uses the Cash Assistance Wire Transfer Request form to create the Cash Assistance Mortgage. The Cash Assistance Wire Transfer Request form is a key document and must be filled out correctly: Borrower s name(s) Must Match first mortgage!!!!!! Cash Assistance amount Closing date Document Preparer Cash Assistance Mortgage 24

25 Document Preparer Cash Assistance Mortgage: The Fine Print (Same) New Hampshire Housing is the Lender. Document Preparer is not making a credit decision or exercising discretion No separate loan application is needed for the Cash Assistance Mortgage (Source of DPA Secured Borrower Funds ). Loan Reservation No separate loan reservation needed. Program Disclosure Provide with Loan Estimate. Loan Estimate and Closing Disclosure Show New Hampshire Housing as the Lender. New Hampshire Housing is exempt from paying recording fees (See RSA 204-C:49). 25

26 Processing the Cash Assistance Mortgage Cash Assistance Mortgage is mostly the same for both the Home Flex Plus and Home Preferred Plus! Disclosures Documents Underwriting Requesting Cash Assistance Income Limit Home Flex Plus Different Same $126, Home Preferred Plus Different Same 80% of Fannie Mae s AMI for the property 26

27 Using the Cash Assistance Mortgage with Home Flex Plus 27

28 About Home Flex Plus About Home Flex Plus 2% or 3% Cash Assistance based on loan amount Minimum 620 credit score Any DTI over 50% must be approve/eligible and have a minimum credit score of 680 Homebuyer education required Follow FHA, VA or USDA RD guidelines Home Flex Plus Factsheet 28

29 Cash Assistance Mortgage Entering in LOS/AUS FHA When entering the Home Flex Plus, source of downpayment must be Secured Borrowed Funds Cash Assistance must be shown as Subordinate financing. Do not list Cash Assistance as an asset or gift funds. 29

FHA 92900 LT - Must show as Secondary Financing from")

30 Cash Assistance Mortgage Entering in LOS/AUS FHA Question h. must be: Yes (Y) FHA LT - Must show as Secondary Financing from Gov t Source 30

31 Cash Assistance Mortgage Important Note FHA Remember: There is no maximum Combined Loan-to-Value (CLTV) for secondary financing loans provided by Governmental Entities. 30

32 Entering Cash Assistance Mortgage The Fine Print LTV/CLTV Per FHA guidelines, there is no maximum CLTV when subordinate financing is from a housing finance agency such as New Hampshire Housing [See FHA Handbook 4000.II(A)(4)(d)(1)(b)]. Your findings must show the DPA as a subordinate lien, and you will receive the following note in DO: This loan casefile may be ineligible for HFA financing as the CLTV exceeds 96.5% on a purchase transaction. Please refer to the Online version of FHA Single Family Housing Policy Handbook to determine if the source of the secondary financing allows the CLTV to exceed 96.5%." 32

33 Cash Assistance Mortgage Entering in LOS/AUS RD-GUS 1003: GUS: 33

34 Requesting Cash Assistance Funds Home Flex Plus Read the Cash Assistance Mortgage policy! Failure to follow the policy could result in: No FHA insurance; New Hampshire Housing will not buy the loan; and/or Participating Lender must repay New Hampshire Housing for Cash Assistance. The process is exactly the same. 34

35 Requesting Cash Assistance Funds Home Flex Plus Lender must request Cash Assistance funds by submitting the Cash Assistance Wire Transfer Request by 12:00 noon at least two (2) business days prior to closing. Wire Transfer Request form (See example) IMPORTANT REMINDER: Home Flex Plus 1 st mortgage must comply with all New Hampshire Housing requirements. New Hampshire Housing uses this document to prepare the Cash Assistance Mortgage (Must match 1 st mortgage) 35

36 Processing the Cash Assistance Mortgage Cash Assistance Mortgage is mostly the same for both the Home Flex Plus and Home Preferred Plus! Disclosures Documents Underwriting Requesting Cash Assistance Home Flex Plus Different Same Home Preferred Plus Different Same 36

37 Using the Cash Assistance Mortgage with Home Preferred Plus 37

38 About About Home Home Preferred Plus Plus 3% Cash Assistance based on loan amount Income limit: 80% or less of Area Median Income (AMI) See: Lookup Tool Minimum 620 credit score Any DTI over 50% must be approve/eligible and have a minimum credit score of 680 Homebuyer education required for first-time homebuyers Maximum LTV: 97% for 1-unit/CLTV 105% 95% for 2-4 units/cltv 105% Follow Fannie Mae Selling guide Home Preferred Plus Factsheet 38

39 About About Home Home Preferred Plus Plus New Hampshire Housing has designed the Home Preferred Plus program consistent with the Fannie Mae Selling Guide. Additionally, the Cash Assistance Mortgage complies with Fannie Mae s Community Seconds requirements. 39

40 About Home Preferred Plus When entering the Cash Assistance Mortgage in DO, choose the dropdown choice: Payments deferred 5 or more years and fully forgiven. Please note, while the full amount of Cash Assistance is forgiven on the fourth anniversary of the Cash Assistance Mortgage closing date (provided no Repayment Event), New Hampshire Housing has confirmed with Fannie Mae that the lender must choose Payment deferred 5 or more years and fully forgiven for the Community Seconds Repayment Structure in DO. This way DO does not impute any Cash Assistance payments in underwriting. 40

41 Cash Assistance Mortgage Entering in DO Fannie Mae Fill in the Community Lending Information section. Enter Community Seconds data. Note: The first mortgage does not have to be a Community Lending product. Take the following steps: a. If you are using HomeReady for the 1 st mortgage, select Home Preferred in the Community Lending Product field. b. Select Yes in the Community Seconds field. Otherwise the system defaults to No for this field. c. If you are using a Community Seconds mortgage, you must select the appropriate option from the Community Seconds Repayment Structure drop-down list. d. You may select the County, but it is no longer used to determine the income limit. The census tract is used to determine the income limit. If DO is unable to determine the census tract, then you may enter the FIPS Code associated to the property, which would then be used to determine the income limit (see next step). 41

42 Cash Assistance Mortgage Entering in DO Fannie Mae 1. Click Details of Transaction in the navigation bar. The Details of Transaction screen appears. Enter the subordinate lien amount in the j. Subordinate Financing field. 42

43 Cash Assistance Mortgage Entering in DO Fannie Mae 2. Click Additional Data in the navigation bar. Locate the Community Lending Information section. 43

44 Cash Assistance Mortgage Entering in DO Fannie Mae 3. For the NHHFA Cash Assistance Mortgage, choose Payments deferred 5 or more years and fully forgiven Home Preferred Please note, while the full amount of Cash Assistance is forgiven on the fourth anniversary of the Cash Assistance Mortgage closing date (provided no Repayment Event) New Hampshire Housing has confirmed with Fannie Mae that the lender must choose Payment deferred 5 or more years and fully forgiven for the Community Seconds Repayment Structure in DO. 44

code which is a unique code assigned to all geographic areas by the U.S. Census Bureau.")

45 Cash Assistance Mortgage Entering in DO Fannie Mae 4. DO will determine the income eligibility requirements based on the census tract in which the property is located. If DO is unable to determine the census tract, the lender may provide the Federal Information Processing Standard (FIPS) code which is a unique code assigned to all geographic areas by the U.S. Census Bureau. 5. When you have finished entering all the necessary data, click Submit. 45

46 Requesting Cash Assistance Funds Home Preferred Plus Read the Cash Assistance Mortgage policy! Failure to follow the policy could result in: New Hampshire Housing will not buy the loan; and/or Participating Lender must repay New Hampshire Housing for Cash Assistance. Note: The Cash Assistance Mortgage is a loan, no gift letter. 46

47 Requesting Cash Assistance Funds Home Preferred Plus Lender must request Cash Assistance funds by submitting the Cash Assistance Wire Transfer Request by 12:00 noon at least two (2) business days prior to closing. Wire Transfer Request form (See example) IMPORTANT REMINDER: Home Preferred Plus 1 st mortgage must comply with all New Hampshire Housing requirements. New Hampshire Housing uses this document to prepare the Cash Assistance Mortgage (Must match 1 st mortgage) 47

48 Cash Assistance Mortgage Reference Documents: Home Flex Plus with Cash Assistance Product Sheet Home Preferred with Cash Assistance Product Sheet Document Preparation Agreement CashAssistance Mortgage Program Disclosure Model Loan Estimate ModelClosing Disclosure CashAssistanceWire Transfer Request Lender Exception Request and Acknowledgement New Hampshire Housing Letter on Legally Liable/Obligated Questions? nhhfa.org/lenders Cash Assistance Mortgage Training 48

Chapter 9 Product Matrix

Table of Contents Chapter 9 Product Matrix... 1 CONVENTIONAL CONFORMING LOANS... 2 Secondary Market ARM (Adjustable Rate Mortgage) Loans... 4 HARP (Fannie DU Refi Plus and Freddie Open Access)... 5 FHA/VA

Table of Contents Chapter 9 Product Matrix... 1 CONVENTIONAL CONFORMING LOANS... 2 Secondary Market ARM (Adjustable Rate Mortgage) Loans... 4 HARP (Fannie DU Refi Plus and Freddie Open Access)... 5 FHA/VA

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year

Assistance Program: City of North Lauderdale Purchase Assistance Program Code: DFLLAUDER

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

HomeReady. Eligibility 1 UNIT 2 TO 4 UNITS. Purchase or Limited Cash-Out Refinance. Loan Purpose. Occupancy and Property Type Borrower Income Limits

HomeReady 1 UNIT 2 TO 4 UNITS Loan Purpose Purchase or Limited Cash-Out Refinance Eligibility Occupancy and Property Type Borrower Income Limits Minimum Borrower Contribution Acceptable Sources of Funds

HomeReady 1 UNIT 2 TO 4 UNITS Loan Purpose Purchase or Limited Cash-Out Refinance Eligibility Occupancy and Property Type Borrower Income Limits Minimum Borrower Contribution Acceptable Sources of Funds

Assistance Program: City of Austin Shared Equity Down Payment Assistance Code: DTXSHARED

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

ditech BUSINESS LENDING HOMEREADY MORTGAGE PRODUCT

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING HOMEREADY MORTGAGE PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10-30 year term in annual increments Fully amortizing

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING HOMEREADY MORTGAGE PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10-30 year term in annual increments Fully amortizing

Assistance Program: City of Tampa Mortgage Assistance Program Code: DFLTAMPA

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year

19 FREQUENTLY ASKED QUESTIONS

19 FREQUENTLY ASKED QUESTIONS TERMS & CONDITIONS Q. What is the Total Debt To Income ratio allowed under the Program? A. The Total Debt To Income ratio cannot exceed 50.00%, unless other restrictions apply.

19 FREQUENTLY ASKED QUESTIONS TERMS & CONDITIONS Q. What is the Total Debt To Income ratio allowed under the Program? A. The Total Debt To Income ratio cannot exceed 50.00%, unless other restrictions apply.

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

Assistance Program: City of Dallas Homebuyer Assistance Program Category 1 Code: DTXCODMAP

Product Description HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year Conforming Product (DU) Fannie Mae Housing

Product Description HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year Conforming Product (DU) Fannie Mae Housing

Assistance Program: Marion County Homebuyer Purchase Assistance Program Code: DFLMARION

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

FNMA HomeReady & Loan Programs 97%

HomeReady FNMA Standard 97% Description Program DU Eligibility Huron Valley Financial product offering for Fannie Mae 97% is three products offered: 97% Fannie Mae Home Ready Fannie Mae Standard 97% Fannie

HomeReady FNMA Standard 97% Description Program DU Eligibility Huron Valley Financial product offering for Fannie Mae 97% is three products offered: 97% Fannie Mae Home Ready Fannie Mae Standard 97% Fannie

Close More Loans with HomeReady Mortgage An Overview for Loan Officers. Dial- in for audio:

Close More Loans with HomeReady Mortgage An Overview for Loan Officers Dial- in for audio: 1-866-845-1266 Seminar guidelines Please do not place the call on hold at any time. Please place your phone on

Close More Loans with HomeReady Mortgage An Overview for Loan Officers Dial- in for audio: 1-866-845-1266 Seminar guidelines Please do not place the call on hold at any time. Please place your phone on

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY

Product Description Allowable Origination Channel HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year Conforming

Product Description Allowable Origination Channel HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year Conforming

UNDERWRITING Secondary Financing. U.S. Bank Home Mortgage MRBP Division Master Servicer

UNDERWRITING Secondary Financing U.S. Bank Home Mortgage MRBP Division Master Servicer FHA 203b, 221 (d) (2) 203k VA USDA/RD Fannie Mae MyCommunityMortgage Suite of Products (97/100/Community Solutions/HomeChoice)

UNDERWRITING Secondary Financing U.S. Bank Home Mortgage MRBP Division Master Servicer FHA 203b, 221 (d) (2) 203k VA USDA/RD Fannie Mae MyCommunityMortgage Suite of Products (97/100/Community Solutions/HomeChoice)

Assistance Program: City of Los Angeles Low Income Purchase Assistance Program (LIPA) Zero Interest Code: DCALIPADP

Zero Interest Code: DCALIPADP") HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

FNMA s HomeReady Program

FNMA s HomeReady Program (rev. 6/30/2016) Presented by J.J. Sawicki, CMP Merrimack Mortgage Co. LLC Overview Help meet the diverse needs of today s buyers with FNMA s enhanced affordable lending program,

FNMA s HomeReady Program (rev. 6/30/2016) Presented by J.J. Sawicki, CMP Merrimack Mortgage Co. LLC Overview Help meet the diverse needs of today s buyers with FNMA s enhanced affordable lending program,

ELIGIBILITY MATRIX. Table of Contents. Standard Eligibility Requirements - Desktop Underwriter Page 2

ELIGIBILITY MATRIX The Eligibility Matrix provides the comprehensive LTV, CLTV, and HCLTV ratio requirements for conventional first mortgages eligible for delivery to Fannie Mae. The Eligibility Matrix

ELIGIBILITY MATRIX The Eligibility Matrix provides the comprehensive LTV, CLTV, and HCLTV ratio requirements for conventional first mortgages eligible for delivery to Fannie Mae. The Eligibility Matrix

19 FREQUENTLY ASKED QUESTIONS

19 FREQUENTLY ASKED QUESTIONS TERMS & CONDITIONS Q. What is the Total Debt To Income ratio allowed under the Program? A. The Total Debt To Income ratio cannot exceed 50.00%, unless other restrictions apply.

19 FREQUENTLY ASKED QUESTIONS TERMS & CONDITIONS Q. What is the Total Debt To Income ratio allowed under the Program? A. The Total Debt To Income ratio cannot exceed 50.00%, unless other restrictions apply.

Assistance Program: Palm Beach County SHIP Purchase Assistance Program Code: DFLPBCSMS

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

Close More Loans with HomeReady Mortgage An Overview for Loan Officers. Dial- in for audio: Attendee passcode:

Close More Loans with HomeReady Mortgage An Overview for Loan Officers Dial- in for audio: 1-800-779-8492 Attendee passcode: 4344988 Seminar guidelines Please do not place the call on hold at any time.

Close More Loans with HomeReady Mortgage An Overview for Loan Officers Dial- in for audio: 1-800-779-8492 Attendee passcode: 4344988 Seminar guidelines Please do not place the call on hold at any time.

Assistance Program: Hernando County SHIP Down Payment Assistance Program Code: DFLHCSHIP

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year

HomeReady Mortgage. Overview for Loan Officers May Fannie Mae. Trademarks of Fannie Mae. 1

HomeReady Mortgage Overview for Loan Officers May 2017 2016 Fannie Mae. Trademarks of Fannie Mae. 1 An Important note about the seminar content While every effort has been made to ensure the reliability

HomeReady Mortgage Overview for Loan Officers May 2017 2016 Fannie Mae. Trademarks of Fannie Mae. 1 An Important note about the seminar content While every effort has been made to ensure the reliability

Assistance Program: City of Phoenix Open Doors Homeownership Program Code: DAZPXODHP

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

AmeriSave Wholesale USDA Effective Date: February 2017 USDA 30 Rural Housing 30 Year Fixed Only

AmeriSave Wholesale USDA Effective Date: February 2017 Product Term: USDA 30 Rural Housing 30 Year Fixed Only Loan Purpose Loan Amount Eligible Borrowers Ineligible Borrowers Purchase Guaranteed: $424,100

AmeriSave Wholesale USDA Effective Date: February 2017 Product Term: USDA 30 Rural Housing 30 Year Fixed Only Loan Purpose Loan Amount Eligible Borrowers Ineligible Borrowers Purchase Guaranteed: $424,100

HomeReady Conforming Fixed Program Summary

HomeReady Conforming Fixed Program Summary HomeReady Matrix with Mortgage Insurance Guideline Overlays: PURCHASE AND RATE TERM REFINANCE Occupancy Units FICO/Score LTV/CLTV/HCLTV Primary Residence 1 620

HomeReady Conforming Fixed Program Summary HomeReady Matrix with Mortgage Insurance Guideline Overlays: PURCHASE AND RATE TERM REFINANCE Occupancy Units FICO/Score LTV/CLTV/HCLTV Primary Residence 1 620

GSFA PLATINUM PROGRAM FHA GUIDELINES SUMMARY

OVERVIEW The GSFA Government Down Payment Assistance Program (DAP) is a competitively priced loan program that does not require a minimum down payment from the homebuyer(s). GSFA Platinum is designed to

OVERVIEW The GSFA Government Down Payment Assistance Program (DAP) is a competitively priced loan program that does not require a minimum down payment from the homebuyer(s). GSFA Platinum is designed to

Assistance Program: Pima County HOME Down Payment Assistance Loan Code: DAZFHRDPA

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

13 DOWNPAYMENT PROGRAMS

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Home Advantage 0% Downpayment Assistance Program

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Home Advantage 0% Downpayment Assistance Program

Assistance Program: City of Tuscaloosa Home Purchase Assistance Program Code: DALTUSHPP

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

LOANS MUST BE RUN THROUGH GUS*

AmeriSave USDA USDA 30 Rural Housing 30 year Fixed Only *ALL LOANS MUST BE RUN THROUGH GUS* Loan Purpose Loan Amount Eligible Borrowers Ineligible Borrowers Purchase Guaranteed: $453,100 US Citizens n-occupant

AmeriSave USDA USDA 30 Rural Housing 30 year Fixed Only *ALL LOANS MUST BE RUN THROUGH GUS* Loan Purpose Loan Amount Eligible Borrowers Ineligible Borrowers Purchase Guaranteed: $453,100 US Citizens n-occupant

Assistance Program: Pasco County Homebuyer Assistance Program Code: DFLPCYHAP

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year

ELIGIBILITY MATRIX. Table of Contents. Standard Eligibility Requirements - Desktop Underwriter Page 2

The Eligibility Matrix provides the comprehensive LTV, CLTV, and HCLTV ratio requirements for conventional first mortgages eligible for delivery to Fannie Mae. The Eligibility Matrix also includes credit

The Eligibility Matrix provides the comprehensive LTV, CLTV, and HCLTV ratio requirements for conventional first mortgages eligible for delivery to Fannie Mae. The Eligibility Matrix also includes credit

Valley National Bank Special Products and Services HCDNNJ HCA Training 8/16/18

Valley National Bank Special Products and Services HCDNNJ HCA Training 8/16/18 Jerry Flach (973) 305-8800 x 4252 gflach@valleynationalbank.com Sofi Cordero (973) 305-8800 x 8884 scordero@valleynationalbank.com

Valley National Bank Special Products and Services HCDNNJ HCA Training 8/16/18 Jerry Flach (973) 305-8800 x 4252 gflach@valleynationalbank.com Sofi Cordero (973) 305-8800 x 8884 scordero@valleynationalbank.com

SECTION 9 HFA PREFERRED TM PROGRAM

SECTION 9 HFA PREFERRED TM PROGRAM 9.1 Eligible Loan Purpose 9.2 Principal Residence Requirement; Owner-Occupancy 9.3 Eligible Property Types 9.4 Sales Price Limits 9.5 Closing Costs 9.6 Interest Rate

SECTION 9 HFA PREFERRED TM PROGRAM 9.1 Eligible Loan Purpose 9.2 Principal Residence Requirement; Owner-Occupancy 9.3 Eligible Property Types 9.4 Sales Price Limits 9.5 Closing Costs 9.6 Interest Rate

Delaware State Housing Authority. Demystifying the Advantage 4 Loan Program

Delaware State Housing Authority Demystifying the Advantage 4 Loan Program DSHA is committed to follow all aspects of the Fair Housing Act in our efforts to promote responsible homeownership and obtaining

Delaware State Housing Authority Demystifying the Advantage 4 Loan Program DSHA is committed to follow all aspects of the Fair Housing Act in our efforts to promote responsible homeownership and obtaining

Colorado Housing Assistance Corporation Mortgage Assistance Program for the State of Colorado.

DATE: 4/4/2018 SUBJECT: Colorado Housing Assistance Corporation Mortgage Assistance Program for the State of Colorado. Attached is a Fact Sheet for the above referenced program, available for homes purchased

DATE: 4/4/2018 SUBJECT: Colorado Housing Assistance Corporation Mortgage Assistance Program for the State of Colorado. Attached is a Fact Sheet for the above referenced program, available for homes purchased

Hit the Books: First Time Homebuyer Programs from FNMA and FHLMC

Hit the Books: First Time Homebuyer Programs from FNMA and FHLMC Two common first time homebuyer programs are MyCommunityMortgage from FNMA and Home Possible from FHLMC. This reference will help you understand

Hit the Books: First Time Homebuyer Programs from FNMA and FHLMC Two common first time homebuyer programs are MyCommunityMortgage from FNMA and Home Possible from FHLMC. This reference will help you understand

Shared Equity Portfolio Analysis January November Fannie Mae. Trademarks of Fannie Mae.

Shared Equity Portfolio Analysis January 2014 - November 2018 2019 Fannie Mae. Trademarks of Fannie Mae. Introduction Shared equity programs preserve affordable homeownership opportunities by allowing

Shared Equity Portfolio Analysis January 2014 - November 2018 2019 Fannie Mae. Trademarks of Fannie Mae. Introduction Shared equity programs preserve affordable homeownership opportunities by allowing

FNMA Home Affordable Refinance Program (HARP) Transaction Type Number of Units Fixed Rate Max LTV/CLTV

Transaction Type Number of Units Fixed Rate Max LTV/CLTV") FNMA Conventional Conforming Product Offering Transaction Type Number of Fixed Rate Cash-Out Refinance Second Home Adjustable Rate 1 Unit 97/97% 90/90% 2 Unit 85/85% 75/75% 3 4 75/75% 65/65% 1 Unit 80/80%

FNMA Conventional Conforming Product Offering Transaction Type Number of Fixed Rate Cash-Out Refinance Second Home Adjustable Rate 1 Unit 97/97% 90/90% 2 Unit 85/85% 75/75% 3 4 75/75% 65/65% 1 Unit 80/80%

Assistance Program: County of San Diego Homebuyer Downpayment & Closing Cost Assistance (DCCA)/CalHome Code: DCASDDCCA

/CalHome Code: DCASDDCCA") HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

WCDA LOAN PRODUCT MATRIX

The matrix below compares the components of the various first mortgage loan and down payment assistance loan products offered by WCDA. This matrix is designed to provide guidance for these products and

The matrix below compares the components of the various first mortgage loan and down payment assistance loan products offered by WCDA. This matrix is designed to provide guidance for these products and

Assistance Program: City of Jacksonville Head Start to Homeownership Program Code: DFLJAHOME

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fannie Mae Fixed 30 year Conforming

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fannie Mae Fixed 30 year Conforming

SONYMA Conventional Plus Correspondent Term Sheet

Product Type 30 Year Fixed Rate Mortgage. Sales Focus This program combines the flexibility offered by Fannie Mae s HomeReady Mortgage along with SONYMA s Down Payment Assistance Loan (DPAL). It is designed

Product Type 30 Year Fixed Rate Mortgage. Sales Focus This program combines the flexibility offered by Fannie Mae s HomeReady Mortgage along with SONYMA s Down Payment Assistance Loan (DPAL). It is designed

Stockton Mortgage Funding HomeReady Fixed Rate Mortgage Product

1. PRODUCT DESCRIPTION Conventional C onforming fixed rate m ortgage DU Version 9.3 10, 15, 20, or 30 year terms for product 30 year term only for product Fully amortizing Qualified Mortgage (QM) Safe

1. PRODUCT DESCRIPTION Conventional C onforming fixed rate m ortgage DU Version 9.3 10, 15, 20, or 30 year terms for product 30 year term only for product Fully amortizing Qualified Mortgage (QM) Safe

Disclaimer This Disclaimer applies to all content provided through CHFA webinars or other training events. The training content provided is intended

chfa products Disclaimer This Disclaimer applies to all content provided through CHFA webinars or other training events. The training content provided is intended to help explain CHFA s programs, but should

chfa products Disclaimer This Disclaimer applies to all content provided through CHFA webinars or other training events. The training content provided is intended to help explain CHFA s programs, but should

Cook County Bureau of Economic Development Department of Planning and Development. Cook County Program Guidelines by Loan Type At-a-Glance

Cook County Bureau of Economic Development Department of Planning and Development Cook County Program Guidelines by Loan Type At-a-Glance Government Loans Freddie Mac (FRE) Eligible Loans Eligible Loans

Cook County Bureau of Economic Development Department of Planning and Development Cook County Program Guidelines by Loan Type At-a-Glance Government Loans Freddie Mac (FRE) Eligible Loans Eligible Loans

How to Originate and Deliver HomeReady Mortgages

How to Originate and Deliver HomeReady Mortgages 2016 Fannie Mae. Trademarks of Fannie Mae. An Important Note about the Seminar Content While every effort has been made to ensure the reliability of the

How to Originate and Deliver HomeReady Mortgages 2016 Fannie Mae. Trademarks of Fannie Mae. An Important Note about the Seminar Content While every effort has been made to ensure the reliability of the

Conventional and Government Program Overlays. OVERLAYS All Programs

4506-T/1040s Requirements Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses and/or unreimbursed expenses, 2 years of tax transcripts and 2 years 1040s will

4506-T/1040s Requirements Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses and/or unreimbursed expenses, 2 years of tax transcripts and 2 years 1040s will

Assistance Program: Miami Dade County PHCD Affordable Housing First Time Homebuyer Program Code: DFLMIAMCY

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

2 TERMS AND CONDITIONS

2 TERMS AND CONDITIONS All Home Advantage loans must be delivered to Lakeview Loan Servicing. Each Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate FHA 203(b), 234 (c), HUD 184,

2 TERMS AND CONDITIONS All Home Advantage loans must be delivered to Lakeview Loan Servicing. Each Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate FHA 203(b), 234 (c), HUD 184,

GSFA PLATINUM PROGRAM CONVENTIONAL GUIDELINES SUMMARY

OVERVIEW The GSFA Conventional Down Payment Assistance Program (DAP) is a competitively priced Conventional loan program that does not require a minimum down payment from the homebuyer(s). GSFA provides

OVERVIEW The GSFA Conventional Down Payment Assistance Program (DAP) is a competitively priced Conventional loan program that does not require a minimum down payment from the homebuyer(s). GSFA provides

UHM Production Bulletin

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-01 HUD: FHA has announced

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-01 HUD: FHA has announced

USDA / GUS Basics for Success

USDA / GUS Basics for Success INDEX BENEFITS OF MSF USDA HOUSEHOLD ELIGIBILITY ASSETS AND LIABILITIES INTRODUCTION INCOME ELIGIBILITY TRANSACTION DETAILS OVERVIEW LOAN TERMS ADDITIONAL DATA GUS DECISION

USDA / GUS Basics for Success INDEX BENEFITS OF MSF USDA HOUSEHOLD ELIGIBILITY ASSETS AND LIABILITIES INTRODUCTION INCOME ELIGIBILITY TRANSACTION DETAILS OVERVIEW LOAN TERMS ADDITIONAL DATA GUS DECISION

HOMEREADY. Table of Contents

Table of Contents 1. Table of Contents... 1 2. Overview... 2 3. Product Codes... 2 4. Accessory Unit Income... 2 5. Boarder Income... 2 6. Borrower Income Limits and Calculations... 3 7. DU Loan Case Files:

Table of Contents 1. Table of Contents... 1 2. Overview... 2 3. Product Codes... 2 4. Accessory Unit Income... 2 5. Boarder Income... 2 6. Borrower Income Limits and Calculations... 3 7. DU Loan Case Files:

13 DOWNPAYMENT PROGRAMS

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Opportunity Down Payment Assistance Program can

13 DOWNPAYMENT PROGRAMS DOWNPAYMENT ASSISTANCE PROGRAMS These guidelines apply to all downpayment assistance loans offered at the Commission Details for Opportunity Down Payment Assistance Program can

Ability To Repay (ATR) Creditors must determine that borrowers have a reasonable ability to repay a loan based on consideration and verification of

Creditors must determine that borrowers have a reasonable ability to repay a loan based on consideration and verification of") Ability To Repay (ATR) Creditors must determine that borrowers have a reasonable ability to repay a loan based on consideration and verification of factors indicative of a consumer s credit capacity, including:

Ability To Repay (ATR) Creditors must determine that borrowers have a reasonable ability to repay a loan based on consideration and verification of factors indicative of a consumer s credit capacity, including:

10/23/17. Chenoa Fund Program

10/23/17 Chenoa Fund Program Disclaimer While every effort has been made to ensure the reliability of the webinar content, PRMG s product profiles and their updates, are the official statements of PRMG

10/23/17 Chenoa Fund Program Disclaimer While every effort has been made to ensure the reliability of the webinar content, PRMG s product profiles and their updates, are the official statements of PRMG

2 TERMS AND CONDITIONS

2 TERMS AND CONDITIONS All Home Advantage loans must be delivered to Lakeview Loan Servicing. Each Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate FHA 203(b), 234 (c), HUD 184,

2 TERMS AND CONDITIONS All Home Advantage loans must be delivered to Lakeview Loan Servicing. Each Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate FHA 203(b), 234 (c), HUD 184,

ditech BUSINESS LENDING HOMEREADY LPMI FIXED RATE MORTGAGE PRODUCT

1. PRODUCT DESCRIPTI ON ditech BUSINESS LENDING HOMEREADY LPMI FIXED RATE MORTGAGE PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.2 Servicing retained 10, 15, 20, or 30 year terms Manufactured

1. PRODUCT DESCRIPTI ON ditech BUSINESS LENDING HOMEREADY LPMI FIXED RATE MORTGAGE PRODUCT Conventional Conforming fixed rate mortgage DU Version 10.2 Servicing retained 10, 15, 20, or 30 year terms Manufactured

Close More Loans with HomeReady Mortgage

Close More Loans with HomeReady Mortgage Overview for Loan Officers May 2, 2017, 2 3:30 p.m. ET Dial-in number: 800-779-8492 Participant passcode: 4344988 2017 Fannie Mae. Trademarks of Fannie Mae. 1 Seminar

Close More Loans with HomeReady Mortgage Overview for Loan Officers May 2, 2017, 2 3:30 p.m. ET Dial-in number: 800-779-8492 Participant passcode: 4344988 2017 Fannie Mae. Trademarks of Fannie Mae. 1 Seminar

Conventional 97% LTV Options updated 12/5/2018 Freddie Mac HomeOne Mortgage 97% LTV

Max Mortgage Credit Score Max 620, but due to MI requirements borrowers under 680 may benefit from FHA Financing due to MI amounts price comparison is strongly suggested 97% 1 unit 95% for 2 4 unit owner

Max Mortgage Credit Score Max 620, but due to MI requirements borrowers under 680 may benefit from FHA Financing due to MI amounts price comparison is strongly suggested 97% 1 unit 95% for 2 4 unit owner

2 TERMS AND CONDITIONS

2 TERMS AND CONDITIONS All House Key loans must be delivered to Lakeview Loan Servicing, LLC Each House Key Program Mortgage Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate

2 TERMS AND CONDITIONS All House Key loans must be delivered to Lakeview Loan Servicing, LLC Each House Key Program Mortgage Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate

Conventional and Government Program Overlays

Financed Properties Minimum Loan Amount $60,000 OVERLAYS All Programs Limited to a maximum of 4 loans to one borrower and up to $1.5MM. Power of Attorney Texas 50(a)(6) & 50(f) Allowed for active duty

Financed Properties Minimum Loan Amount $60,000 OVERLAYS All Programs Limited to a maximum of 4 loans to one borrower and up to $1.5MM. Power of Attorney Texas 50(a)(6) & 50(f) Allowed for active duty

ELIGIBILITY MATRIX. Effective Dates: Refer to the ARM Enhancements section of Selling Guide Announcement SEL

ELIGIBILITY MATRIX The Eligibility Matrix provides the comprehensive LTV, CLTV, and HCLTV ratio requirements for conventional first mortgages eligible for delivery to Fannie Mae. The Eligibility Matrix

ELIGIBILITY MATRIX The Eligibility Matrix provides the comprehensive LTV, CLTV, and HCLTV ratio requirements for conventional first mortgages eligible for delivery to Fannie Mae. The Eligibility Matrix

IHDA Commitment / Reservation Manual

r The Homeownership Department IHDA Commitment / Reservation Manual Revised April, 2015 Revised September, 2015 Revised March, 2016 Revised August, 2016 Revised October, 2016 Revised June, 2017 Revised

r The Homeownership Department IHDA Commitment / Reservation Manual Revised April, 2015 Revised September, 2015 Revised March, 2016 Revised August, 2016 Revised October, 2016 Revised June, 2017 Revised

Conventional and Government Program Overlays

Financed Properties OVERLAYS All Programs Limited to maximum 2 loans to one borrower, one must be primary residence Minimum Loan Amount $60,000 Allowed for active duty military personnel, military contractors,

Financed Properties OVERLAYS All Programs Limited to maximum 2 loans to one borrower, one must be primary residence Minimum Loan Amount $60,000 Allowed for active duty military personnel, military contractors,

Conventional and Government Program Overlays. OVERLAYS All Programs

4506-T/1040s Requirements Asset Verification Comparable Sales Credit Inquiries Delinquent Child Support Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses

4506-T/1040s Requirements Asset Verification Comparable Sales Credit Inquiries Delinquent Child Support Financed Properties OVERLAYS All Programs If TRV (Tax Return Verification) reveals C or E losses

CONVENTIONAL PROGRAM SUMMARY HOMENOW $0 DOWN MORTGAGE PROGRAM PROGRAM SPONSOR DESCRIPTION OF PROGRAM PROGRAM AREA ELIGIBLE LENDERS

CONVENTIONAL PROGRAM SUMMARY HOMENOW $0 DOWN MORTGAGE PROGRAM PROGRAM SPONSOR DESCRIPTION OF PROGRAM PROGRAM AREA ELIGIBLE LENDERS Montana Community Development Corporation, doing business as MoFi www.mofi.org

CONVENTIONAL PROGRAM SUMMARY HOMENOW $0 DOWN MORTGAGE PROGRAM PROGRAM SPONSOR DESCRIPTION OF PROGRAM PROGRAM AREA ELIGIBLE LENDERS Montana Community Development Corporation, doing business as MoFi www.mofi.org

The Chase Guaranteed Rural Housing Purchase Program Features

PROGRAM ELIGIBILITY Borrower Eligibility In order to be eligible for a Rural Development guaranteed loan, the Borrowers adjusted household income cannot exceed the maximum allowable income limit set forth

PROGRAM ELIGIBILITY Borrower Eligibility In order to be eligible for a Rural Development guaranteed loan, the Borrowers adjusted household income cannot exceed the maximum allowable income limit set forth

ditech BUSINESS LENDING CONFORMING FIXED RATE PRODUCT (FANNIE MAE ELIGIBLE)

") 1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage DU Version 10.2 Servicing retained 10 to 30 year term in annual increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans

1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage DU Version 10.2 Servicing retained 10 to 30 year term in annual increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans

ditech BUSINESS LENDING CONFORMING FIXED RATE PRODUCT (FANNIE MAE ELIGIBLE)

") 1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10 to 30 year term in annual increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans

1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10 to 30 year term in annual increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans

ELIGIBILITY MATRIX. Effective Dates: Refer to the Selling Guide for effective dates applicable to high LTV refinances.

ELIGIBILITY MATRIX The Eligibility Matrix provides the comprehensive LTV, CLTV, and HCLTV ratio requirements for conventional first mortgages eligible for delivery to Fannie Mae. The Eligibility Matrix

ELIGIBILITY MATRIX The Eligibility Matrix provides the comprehensive LTV, CLTV, and HCLTV ratio requirements for conventional first mortgages eligible for delivery to Fannie Mae. The Eligibility Matrix

999 West Street, Rocky Hill, CT Phone: (860) Fax: (860) Website:

Fax: (860) Website:") 999 West Street, Rocky Hill, CT 06067-4005 Phone: (860) 721-9501 Fax: (860) 571-3550 Website: www.chfa.org Table of Contents Loan Program Outlines & Underwriting Guides......... Pages 2-7 203(k) - FHA

999 West Street, Rocky Hill, CT 06067-4005 Phone: (860) 721-9501 Fax: (860) 571-3550 Website: www.chfa.org Table of Contents Loan Program Outlines & Underwriting Guides......... Pages 2-7 203(k) - FHA

999 West Street, Rocky Hill, CT Phone: (860) Fax: (860) Website:

Fax: (860) Website:") 999 West Street, Rocky Hill, CT 06067-4005 Phone: (860) 721-9501 Fax: (860) 571-3550 Website: www.chfa.org Table of Contents Loan Program Outlines & Underwriting Guides......... Pages 2-7 203(k) - FHA

999 West Street, Rocky Hill, CT 06067-4005 Phone: (860) 721-9501 Fax: (860) 571-3550 Website: www.chfa.org Table of Contents Loan Program Outlines & Underwriting Guides......... Pages 2-7 203(k) - FHA

Ohio Housing & U.S. Bank Home Mortgage- MRBP Division. Product and Underwriting Guidelines

Ohio Housing & U.S. Bank Home Mortgage- MRBP Division Product and Underwriting Guidelines Lou Caresani 2013 Disclaimer This presentation is for basic informational purposes only. It does not modify or

Ohio Housing & U.S. Bank Home Mortgage- MRBP Division Product and Underwriting Guidelines Lou Caresani 2013 Disclaimer This presentation is for basic informational purposes only. It does not modify or

MAGNOLIA BANK CORRESPONDENT FUNDING RURAL DEVELOPMENT PRODUCT SUMMARY

RURAL DEVELOPMENT FIXED RATE (DELEGATED CLIENTS ONLY) 1. PRODUCT DESCRIPTION USDA Fixed Rate Mortgage 30 year term Fully amortizing 2. PRODUCT CODE 3. INDEX 4. MARGIN 5. ANNUAL/ADJUSTMEN T CAP 6. LIFE

RURAL DEVELOPMENT FIXED RATE (DELEGATED CLIENTS ONLY) 1. PRODUCT DESCRIPTION USDA Fixed Rate Mortgage 30 year term Fully amortizing 2. PRODUCT CODE 3. INDEX 4. MARGIN 5. ANNUAL/ADJUSTMEN T CAP 6. LIFE

IHDA Commitment / Reservation Manual

r The Homeownership Department IHDA Commitment / Reservation Manual Revised April, 2015 Revised September, 2015 Revised March, 2016 Revised August, 2016 Revised October, 2016 Revised June, 2017 The Illinois

r The Homeownership Department IHDA Commitment / Reservation Manual Revised April, 2015 Revised September, 2015 Revised March, 2016 Revised August, 2016 Revised October, 2016 Revised June, 2017 The Illinois

Wholesale Overlay Matrix

Wholesale Matrix The Matrix is a summary of Pacific Union Financial, LLC, dba thelender (Pacific Union, dba thelender) guideline overlays. This document should be used in conjunction with Pacific Union,

Wholesale Matrix The Matrix is a summary of Pacific Union Financial, LLC, dba thelender (Pacific Union, dba thelender) guideline overlays. This document should be used in conjunction with Pacific Union,

Delaware State Housing Authority. Homeownership Loan Programs Lender Training

Delaware State Housing Authority Homeownership Loan Programs Lender Training DSHA is committed to follow all aspects of the Fair Housing Act in our efforts to promote responsible homeownership and obtaining

Delaware State Housing Authority Homeownership Loan Programs Lender Training DSHA is committed to follow all aspects of the Fair Housing Act in our efforts to promote responsible homeownership and obtaining

Participating Lender Training

Participating Lender Training 1 CHFA S MISSION To provide housing opportunities for low and moderate - income people in Connecticut and to aid economic development. 2 www.chfa.org 3 CHFA AND BOND COMPLIANCE

Participating Lender Training 1 CHFA S MISSION To provide housing opportunities for low and moderate - income people in Connecticut and to aid economic development. 2 www.chfa.org 3 CHFA AND BOND COMPLIANCE

Moving Single-Family Financing Initiatives Forward I m HOME Conference October 2-4, 2017

Moving Single-Family Financing Initiatives Forward I m HOME Conference October 2-4, 2017 Where Fahe Works Fahe and our Members create transformational change in: KY, TN, VA, WV, AL, MD Fahe is on a mission

Moving Single-Family Financing Initiatives Forward I m HOME Conference October 2-4, 2017 Where Fahe Works Fahe and our Members create transformational change in: KY, TN, VA, WV, AL, MD Fahe is on a mission

PennyMac Correspondent Group Fannie Mae HomeReady Product Profile Overlays to Fannie Mae are underlined

PennyMac Correspondent Group Fannie Mae HomeReady Product Profile 06.15.18 Overlays to Fannie Mae are underlined Fannie Mae - DU Approval Owner-Occupied Only, Purchase and Rate & Term Refinance, Fixed

PennyMac Correspondent Group Fannie Mae HomeReady Product Profile 06.15.18 Overlays to Fannie Mae are underlined Fannie Mae - DU Approval Owner-Occupied Only, Purchase and Rate & Term Refinance, Fixed

Down Payment Assistance Programs

Down Payment Assistance Programs Schedule an Appointment 6 8 hour Homebuyers Education Course 2-hour Pre-Purchase Counseling The Homeowners Employment Corporation 2440 Wall Street, SE Suite B-2 Conyers,

Down Payment Assistance Programs Schedule an Appointment 6 8 hour Homebuyers Education Course 2-hour Pre-Purchase Counseling The Homeowners Employment Corporation 2440 Wall Street, SE Suite B-2 Conyers,

HomeNow $0 Down Program Guidelines

HomeNow $0 Down Program Guidelines July 1, 2016 Last Revision June, 2018 Program Offered by: Program Administered by: REVISIONS TABLE Section Page Revision Date Addition of Fannie Mae HomeReady Conventional

HomeNow $0 Down Program Guidelines July 1, 2016 Last Revision June, 2018 Program Offered by: Program Administered by: REVISIONS TABLE Section Page Revision Date Addition of Fannie Mae HomeReady Conventional

FNMA Conforming Mortgage

Topic Program Description Products AUS method Eligible States Maximum Loan Amounts Agency Conforming Loan Limits Product Guideline This is base Fannie Mae mortgage parameters for primary, second and investor

Topic Program Description Products AUS method Eligible States Maximum Loan Amounts Agency Conforming Loan Limits Product Guideline This is base Fannie Mae mortgage parameters for primary, second and investor

DELAWARE STATE HOUSING AUTHORITY (DSHA) HOMEOWNERSHIP LOAN PROGRAM NOTICE Effective May 1, 2018

HOMEOWNERSHIP LOAN PROGRAM NOTICE Effective May 1, 2018") DELAWARE STATE HOUSING AUTHORITY (DSHA) HOMEOWNERSHIP LOAN PROGRAM NOTICE Effective May 1, 2018 The sections of this Program Notice marked with an asterisk (*) are general summaries of provisions contained

DELAWARE STATE HOUSING AUTHORITY (DSHA) HOMEOWNERSHIP LOAN PROGRAM NOTICE Effective May 1, 2018 The sections of this Program Notice marked with an asterisk (*) are general summaries of provisions contained

Correspondent Overlay Matrix

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

7.1 Genworth-Insured Refinance Program (04/03/09)

") Genworth Mortgage Insurance 7.1 Genworth-Insured Refinance Program (04/03/09) The Genworth-Insured Refinance Program provides expanded underwriting guidelines for rate/term refinances of Genworth-insured

Genworth Mortgage Insurance 7.1 Genworth-Insured Refinance Program (04/03/09) The Genworth-Insured Refinance Program provides expanded underwriting guidelines for rate/term refinances of Genworth-insured

FHLMC Only Conforming and Maximum DTI is the more restrictive of Loan Product Advisor or 50%.

AUS (Automated Underwriting System) GENERAL POLICY OVERLAYS FHA, VA, CONVENTIONAL and USDA FHA, VA & Conventional AUS approval recommendation is required for all FHA, VA, (Purchase and Non-Streamline/Non-IRRRL

AUS (Automated Underwriting System) GENERAL POLICY OVERLAYS FHA, VA, CONVENTIONAL and USDA FHA, VA & Conventional AUS approval recommendation is required for all FHA, VA, (Purchase and Non-Streamline/Non-IRRRL

VA FULLY AMORTIZING FIXED, HIGH BALANCE & JUMBO PROGRAM

VA FULLY AMORTIZING FIXED, HIGH BALANCE & JUMBO PROGRAM PROGRAM SPECIFICATIONS Description A mortgage loan program established by the United States Department of Veterans Affairs to help veterans and their

VA FULLY AMORTIZING FIXED, HIGH BALANCE & JUMBO PROGRAM PROGRAM SPECIFICATIONS Description A mortgage loan program established by the United States Department of Veterans Affairs to help veterans and their

SMART SOLUTION BULLETIN #18

SMART SOLUTION BULLETIN #18 October 26, 2018 TO: SMART SOLUTION PARTICIPATING LENDERS FROM: Betty Temple Putnam, Sr. Vice President of Single Family Operations RE: Program Document Revisions This bulletin

SMART SOLUTION BULLETIN #18 October 26, 2018 TO: SMART SOLUTION PARTICIPATING LENDERS FROM: Betty Temple Putnam, Sr. Vice President of Single Family Operations RE: Program Document Revisions This bulletin

Define USDA products and features Introduce Planet Home Lending s USDA product offerings Learn how to determine property and borrower eligibility

Define USDA products and features Introduce Planet Home Lending s USDA product offerings Learn how to determine property and borrower eligibility Review credit, income, asset and appraisal guidelines Tips

Define USDA products and features Introduce Planet Home Lending s USDA product offerings Learn how to determine property and borrower eligibility Review credit, income, asset and appraisal guidelines Tips

NOTICE OF FUNDS AVAILABILITY RE: NEW MEXICO MORTGAGE FINANCE AUTHORITY (TAX-EXEMPT) FIRST HOME MBS PROGRAM JANUARY 2016

FIRST HOME MBS PROGRAM JANUARY 2016") NOTICE OF FUNDS AVAILABILITY RE: NEW MEXICO MORTGAGE FINANCE AUTHORITY (TAX-EXEMPT) FIRST HOME MBS PROGRAM JANUARY 2016 The New Mexico Mortgage Finance Authority ("MFA") has funds available under its single

NOTICE OF FUNDS AVAILABILITY RE: NEW MEXICO MORTGAGE FINANCE AUTHORITY (TAX-EXEMPT) FIRST HOME MBS PROGRAM JANUARY 2016 The New Mexico Mortgage Finance Authority ("MFA") has funds available under its single

Rural Housing Refinances

Rural Housing Refinances Rev. 11/16/2016 Presented by J.J. Sawicki, CMP/ AVP of Training and Development at Merrimack Mortgage Rural Housing Refinance Programs If you have originated an RD loan in the

Rural Housing Refinances Rev. 11/16/2016 Presented by J.J. Sawicki, CMP/ AVP of Training and Development at Merrimack Mortgage Rural Housing Refinance Programs If you have originated an RD loan in the

UHM Production Bulletin

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: HUD 92900-A As announced in Mortgagee Letter 2016-06, the updated 92900-A (HUD/VA

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: HUD 92900-A As announced in Mortgagee Letter 2016-06, the updated 92900-A (HUD/VA

EverBank Wholesale Lending

EverBank Wholesale Lending LOAN PROGRAM CODE PRODUCT OVERVIEW LOAN TYPE LOAN TERMS ELIGIBLE PROPERTY TYPES INELIGIBLE PROPERTY TYPES OCCUPANCY 30 Year - 30FNMC 15 Year - 15FNMC The FNMA MyCommunity products

EverBank Wholesale Lending LOAN PROGRAM CODE PRODUCT OVERVIEW LOAN TYPE LOAN TERMS ELIGIBLE PROPERTY TYPES INELIGIBLE PROPERTY TYPES OCCUPANCY 30 Year - 30FNMC 15 Year - 15FNMC The FNMA MyCommunity products

NOTICE OF FUNDS AVAILABILITY RE: NEW MEXICO MORTGAGE FINANCE AUTHORITY 2017 SERIES B (TAX-EXEMPT) FIRST HOME MBS PROGRAM November 16, 2017

FIRST HOME MBS PROGRAM November 16, 2017") NOTICE OF FUNDS AVAILABILITY RE: NEW MEXICO MORTGAGE FINANCE AUTHORITY 2017 SERIES B (TAX-EXEMPT) FIRST HOME MBS PROGRAM November 16, 2017 The New Mexico Mortgage Finance Authority ("MFA") has funds available

NOTICE OF FUNDS AVAILABILITY RE: NEW MEXICO MORTGAGE FINANCE AUTHORITY 2017 SERIES B (TAX-EXEMPT) FIRST HOME MBS PROGRAM November 16, 2017 The New Mexico Mortgage Finance Authority ("MFA") has funds available

<logo> Offered through 21 st Century Home Loans WHOLESALE DIVISION

CHF ACCESS Training Offered through 21 st Century Home Loans WHOLESALE DIVISION Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie

CHF ACCESS Training Offered through 21 st Century Home Loans WHOLESALE DIVISION Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie

Fannie Mae (DU) Conventional Loan Matrix

Conventional Loan Matrix") PURCHASE/ LIMITED CASH OUT REFINANCES STANDARD and HIGH BALANCE LOAN AMOUNTS Occupancy Maximum* LTV Maximum* CLTV Min FICO* Max Ratios Minimum Cash Investments Mortgage/ Rental History Reserves 1 Unit

PURCHASE/ LIMITED CASH OUT REFINANCES STANDARD and HIGH BALANCE LOAN AMOUNTS Occupancy Maximum* LTV Maximum* CLTV Min FICO* Max Ratios Minimum Cash Investments Mortgage/ Rental History Reserves 1 Unit