DEALERSHIP REFERENCE GUIDE December 12

|

|

|

- Kelly Wilkins

- 6 years ago

- Views:

Transcription

1 DEALERSHIP REFERENCE GUIDE December

2 Table of Contents Section A What is the ZERO Plan Page 4 Description of the Program A-1 What Products are Eligible for Financing A-2 Contact Information for the Dealership A-3 Section B Dealership Sales Tools Pages 5-9 Dealer Sales Tool CD B-1 How to use the Dealer Sales Tool CD B-2 Contents of the Dealer Sales Tool CD B-3 Updates B-4 How to Save the dealership name in the Forms Builder B-5 Find Everything at B-6 Section C ZERO Plan Terms and Guidelines Pages Balance to Finance Determines the Terms C-1 Determine the Remaining Coverage Terms C-2 Down Payment Requirement C-3 Customer Repayment Term C-4 Dealership Fee to use the ZERO Plan C-4 Sample of Exhibit A Terms and Guidelines C-6 Section D Other Rules and Guidelines Pages Matching of Sales Price D-1 Matching of Dates D-2 Multiple Purchasers D-3 Information on Forms D-4 Use of Current Forms or Forms Builder D-5 Multiple Products on Single Note D-6 Dealership Representations Regarding Program D-7 Lien Holder Requirement D-8 Section E Customer Payment Options Pages Two Options to Present to Customers E-1 Sample of Customer Repayment Form E-2 Section F Creating the Required Forms Pages Two Forms to Create F-1 Three Methods to Complete Forms F-2 Instructions on Completing Forms F-3 Section G How the Dealership Gets Paid Pages Review of Required Documents G-1 Creating the Document Packet G-2 Delivery to Universal Lenders G-3 Calculation of Dealer Proceeds & Payment G-4 FACT SHEET Dealer Cash Flow G-5-2 -

3 Section H Customer Service Page 22 It Starts at the Dealership H-1 Collection Notices H-2 Customer CURE Letter and Dealership involvement H-3 Paid Account H-4 Section I Cancellation of Financed Products Pages Dealership Responsibility I-1 Calculation of Refund What is Due to Universal Lenders I-2 Cancellation Due to Customer Request I-3 Sample Request to Cancel Customer Request I-4 Sample Request to Cancel Universal Lenders Request I-5 Right to Offset I-6 FACT SHEET Effect of Cancellation on Dealer Profit I-7 Section J ZERO Plan Menu Page Description of Program J-1-3 -

4 Section A What is The ZERO Plan A-1 Description of the Program The ZERO Plan is a zero percent payment program designed specifically for the automotive, RV and power sports industries. The ZERO Plan is a turn key program that gives retailers the opportunity to offer zero percent financing to their customers to aid in the sale of ancillary products such as extended service contracts. A-2 What Products Are Eligible for Financing The products that are eligible for financing using The ZERO Plan must first be approved by Universal Lenders LLC. A list of approved products can be found in the password protected area at In general, products that allow for the customer to cancel the coverage and receive a pro rated refund of unearned premium are eligible provided they recognize a lien holder s right to cancel the coverage for non payment by the customer. Examples of products that may meet this criterion are Extended Service Contracts, Tire & Wheel Protection, Ding & Dent Protection. To determine if a product meets the eligibility criterion please contact Universal Lenders LLC. A-3 Contact Information for Dealership Use Contact Information on Universal Lenders LLC Phone Fax info@universallenders.net Website Mail 1140 W Lake Street Suite 202 Oak Park IL or P.O. Box 4179 Oak Park IL Hours Monday - Friday 9:00 AM to 6:00 PM CST - 4 -

5 Section B Dealership Sales Tools B-1 Dealership Sales Tool CD When a dealership enrolls in The ZERO Plan a Dealership Sales Tool CD is delivered to the dealership with an initial supply of forms in a start-up kit. This CD contains files that are invaluable to the dealership s rollout of The ZERO Plan program and supplies tools for the continuing success of the program. B-2 How to Use the Dealership Sales Tool CD The Dealership Sales Tool CD requires a window based computer, Microsoft Word and Adobe Reader 9.0 or newer (available for free download at Most companies have windows based computers loaded with the Adobe reader and Microsoft Word. The CD contains one folder called The ZERO Plan. Once the disk is loaded an installation program will install the files and put an icon on your desktop for easy access. This CD should be installed on each computer where The ZERO Plan is to be used. B-3 Contents of the Dealership Sales Tool CD A Menu System that you may want to use to aid in selling service contracts or vehicle products to service customers or CASH buyers. A Sales Pricing Program (displayed in Excel or HTML Format) that will compute a product policy sales price if you enter the product cost and desired profit net of our fee. Open the folder named Compute Sales Price Tools ZERO Plan logos for use in promotional materials, dealer websites and brochures. Open the folder named ZERO Plan Logos A Forms Builder document which allows you to print the Note & Contract and Payment Authorization Form from their PC to a printer bypassing the DMS system. Open the folder named Current Forms. See B-5 below for instructions on how to add your dealership information to the Forms Builder. Current versions of the Note & Contract and Customer Payment Form are available should you run out of your forms supply. Open the folder named Current Forms FACT Sheets that answer all the common questions about The ZERO Plan. Open the folder named Fact Sheets - 5 -

6 Create a Dealer Brochure. Use this tool to customize a ZERO Plan brochure to fit your needs or use as a proof to have the brochure professionally printed. Open the folder named Create a Brochure ZERO Plan Terms and Guidelines. Contains the current guidelines to be used when pricing a product using 0% financing. Complete Dealership Reference Guide. Answers any and all questions concerning The ZERO Plan from A to Z. B-4 Updates Each year (or sooner if necessary) the dealership will receive a new Dealership Sales Tool CD updated with the most current information, forms and new programs. Generally the updates are sent to the Controller or Office Manager. Please update all personal computers as soon as possible B-5 How to Add Your Dealership s information to the Forms Builder. Normally the dealership will never save any entered data in the Forms Builder so that each time the Forms Builder is opened is clear of all prior transactions and is ready for the transaction at hand. The only exception to this is when the dealership saves their own information in the Forms Builder so that the retailer name, address and representative information does not have to be entered for each transaction In order to accomplish the saving of this retailer information please follow the steps below. 1. Find the ZERO Plan Forms Builder on the desktop and click it to open

7 2. Once the forms builder is displayed enter your dealership s name and address as shown below. Then enter your name in the box to the right as shown below. Once the entries are complete click the SAVE icon located on the left side of the task bar as shown. 3. Close ZERO Plan folder. When using the ZERO PLAN Forms Builder in the future the dealership and employee name will displayed and not have to be entered each time a sale is entered

: It is suggested that dealership employees refer customer questions to customer section of our website.")

8 B-6 Find Everything at Universal Lenders LLC provides a website for both the ZERO Plan customer and our business partners. Below is a screen shot of the Customer Section(Sample dated ): It is suggested that dealership employees refer customer questions to customer section of our website. If one of our FAQ items does not address their question they can Universal Lenders LLC with their specific concern

9 The Business partner section is password protected. When your dealership enrolled with Universal Lenders a password and user name were assigned. If you do not know your dealership s password or user name please contact us. Once the user name and password are entered the following screen displays: As you can see from the screen shot above this site has everything a dealership will need to utilize their ZERO Plan product to help them increase sales and provide customer service. Should you have any questions about our website please contact our office

10 Section C ZERO Plan Terms & Guidelines Note: At the end of this section you will find C-6 Sample Terms & Guidelines. This is a sample of what is supplied to each dealership. The Terms and Guidelines are normally updated once a year and the dealership will receive an updated and current version at that time. The sample found in C-6 may not be the most current version. Please refer to the sample as you review C-1 thru C-5 C-1 Balance to Finance Determines the Terms To determine which Terms are to be used for a transaction you must first determine if the transaction has a customer Balance to Finance (Definition: Sale price + Sales Tax Down Payment) that is under $ If the customer Balance to Finance is under $ then the table with a heading of Balance to Finance Under $ should be used. If the customer Balance to Finance is over $ then the table headed Balance to Finance : Over $ should be used. C-2 Determine the Remaining Coverage Term The table requires that you determine how many months and miles of the remaining term of the product coverage the customer is going to receive. Normally the stated months and mileage of coverage, such as 60 months or 75,000 miles, begin on the sale date of the product and from the current mileage on the vehicle. The term Remaining is important in some cases. If the product s start point goes back in time to a delivery date instead of the product sale date or if the mileage coverage starts at zero miles instead of the miles on the vehicle at the time of sale, then you must determine how many months and miles a customer will receive from the sale date of the product policy. Once you determine the Remaining coverage you can determine the remaining terms. If the Service Contract effective date is more than a year past then prior authorization is required from Universal Lenders. C-3 Down Payment Requirement The down payment requirement found in the table is a Minimum Down Payment Requirement. The more money a customer pays as a down payment the more likely the customer is to pay all of his installment payments which in turn will reduce profit charge backs. Also you will see in C-5 below that the Dealer Fee may be reduced as the customer pays more money as a down payment. The Down Payment is calculated by multiplying the minimum required down payment percentage by the Total Sales Price (Definition: Sale Price + Sales Tax)

11 C-4 Customer Repayment Term The table will determine which monthly repayment term will apply to the transaction. For those policies with at least 36 months or miles of remaining coverage the customer repayment term may be 9, 12, 15, 18 or 24 months. For a customer to be eligible to receive 15 or 18 month repayment terms the Balance to Finance must be at least $ To keep the Dealer Fee low the dealership should attempt to keep the repayment term at 12 months even if a customer is eligible to choose 15 or 18 months. C-5 Dealership Fee to use The ZERO Plan The table determines the amount of fees a dealership pays to use The ZERO Plan. For Balance to Finance (Definition: Sale price + Sales Tax Down Payment) amounts under $ there is a flat dollar fee. For Balance to Finance amounts $ or more the dealer fee is calculated as a percentage of the Balance to Finance. To determine the fee that applies to your dealership you also must be aware of the volume of business that Universal funds each month. When monthly volumes averages 6 contracts per month a discounted fee schedule applies..when the volume exceeds 20 contracts per month the lowest fees apply. Commonly owned dealerships or groups can combine their monthly volume to secure the lowest rates. In the sample found in C-6 the Level A Dealer Fee is 11% for 12 months. As an example, if the Balance to Finance is $ then the Dealer Fee would be $ (Calculation: $2000 multiplied by 11% = $220.00). The fee is paid when the dealership receives the proceeds from the sale of the Customer Note to Universal Lenders LLC. Using the example above if the Balance to Finance is $ and the Dealer Fee is $ then when the Customer Note is presented to Universal Lenders LLC for purchase the dealership will receive a check for $ which represents the Balance to Finance less the Dealer Fee

12 C-6 Sample Terms and Guidelines

13 Section D Other Rules and Guidelines D-1 Matching the Sales Price The sales price found on the product policy plus any sales tax must match the sales price and sales tax entered on the Customer Note & Contract. D-2 Matching of Dates The date found on the product policy must match the date entered on the Customer Note & Contract. D-3 Multiple Purchasers If the product policy has listed more than one purchaser then all the purchasers need to be entered on the Customer Note & Contract. There also needs to be additional and unique residence, social security number and telephones information entered on the customer Note & Contract for each purchaser. D-4 Information on Forms The Customer Note & Contract is the legal document that requires the customer to make payments on the product sold by the dealership. Every data field found on the Customer Note & Contract needs to be filled in with customer, dealer, financial or product information. There are no fields that may be left blank! If you are unclear what to enter then contact Universal Lenders LLC. D-5 Use of Current Forms or Form Builders Universal Lenders LLC supplies its dealerships with Customer Note & Contract forms and Customer Payment Authorization forms. In the alternative, Universal Lenders LLC also supplies a Forms Builder program that a dealership can use to create customer forms on plain paper. When a new version of the forms or Forms Builder program is supplied to the dealership they should be used immediately. All older version forms should be discarded. If a dealership is using the Forms Builder then the newest version of the program should be used immediately. The most current versions of all our forms may be found in the password protected portion of our website at

14 D-6 Multiple Products on a Single Note One Customer Note & Contract can finance more then one approved product policy. To determine which set of Terms and Guidelines apply to a multi product Customer Note & Contract the product policy with the shortest monthly term and miles sets the requirements. As an example if the multiple products financed on a single Customer Note & Contract consisted of a 7 year/75000 mile service contract, a 5 year/60,000 mile Tire & Wheel policy and a 2 year/24000 mile Dent & Ding policy and the total sale price of the three exceeded $ , then the Terms & Guidelines found in the $ and Over Table for 24 month/24000 mile coverage term would apply. In addition each of the three administrators, Agreement Numbers and Product Descriptions would need to be included on the Customer Note & Contract form. D-7 Dealership Representations Regarding the Program Each dealership offering The ZERO Plan has executed a dealer agreement which states: The ZERO Plan is intended to provide that the customer will incur no finance charge when purchasing a Vehicle Product. Dealer accordingly agrees to offer customers the same price on all Vehicle Products whether they choose to participate in the ZERO Plan to finance a portion of the price or they choose to pay the full price in cash or its equivalent. Dealer agrees that under no circumstances will there be a price reduction on a Vehicle Product offered to a customer who elects not to participate in the ZERO Plan. There are many State and Federal laws and regulations governing consumer transactions. Failure of dealership employees to adhere to the dealer agreement provisions could put the dealership at risk of legal liability. D-8 Lien Holder Requirement Every product policy financed using The ZERO Plan must list Universal Lenders LLC as the Lien Holder on the product policy form. The form must also list the address of Universal Lenders LLC. This requirement is absolutely necessary and no Customer Note & Contract will be purchased from the dealership without Universal Lenders LLC noted as the Lien Holder

15 Section E Customer Payment Options E-1 Three Options to present to the Customers There are three options for making loan payments a customer may choose from. They are: MONTHLY REMITTANCE Customer is supplied with a coupon book to remit their payments monthly via the mail. The customer will receive their coupon book when Universal Lenders LLC receives the loan document package from the dealership. AUTOMATIC WITHDRAWAL Also known as ACH Payment, this option allows Universal Lenders LLC to withdraw the monthly payment from the customer s checking or savings account. This option requires the customer to sign a Customer Payment Authorization Form. This form needs to be included in the loan document package sent to Universal Lenders LLC. A sample of the form can be found in E-2 below. CREDIT CARD PAYMENT Payments will be charged to the customer s credit card each month on the due date. This option requires the customer to sign a Customer Payment Authorization Form. There is a $4.00 per transaction convenience fee charged each time a payment is taken. This form needs to be included in the loan document package sent to Universal Lenders LLC

16 E-2 Sample of Customer Payment Authorization Form

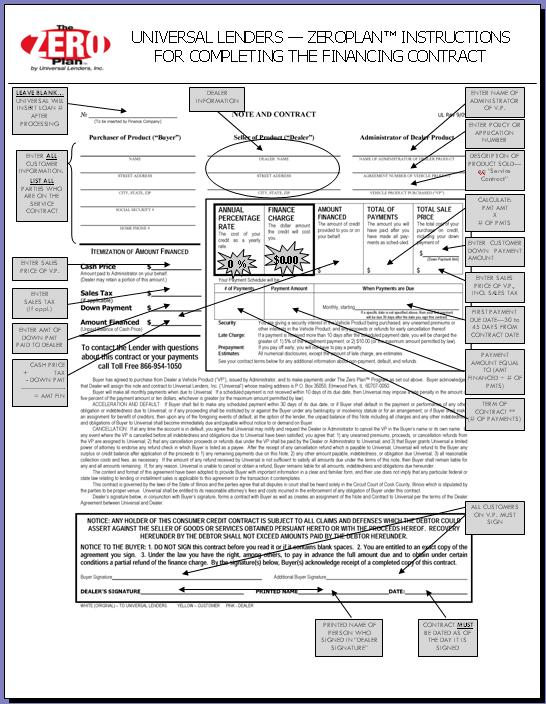

17 Section F Creating the Required Customer Forms F-1 Forms to Create There are three forms that Universal Lenders LLC supplies the dealership with. The Customer Note & Contract is the principle form. Much like a retail installment contract, the Customer Note & Contract is the legal agreement between the customer, the dealership and Universal Lenders LLC which binds the customer to making monthly payments to pay for the vehicle product policy. The second form is the Customer Payment Authorization Form. This form is only required when a customer chooses to make their monthly payments thru automatic withdrawal (ACH) or credit card. Please refer to Section E above for further discussion on this form. The third form is an addendum to the Note & Contract that is only used when a non cancellable product is financed using the ZERO Plan. F-2 Four Methods to Create the Forms The dealership can choose from four acceptable methods for creating the two forms described above. 1. The forms can be handwritten. This is the least desirable option because handwriting can be difficult to read and mistakes can be made calculating the financial information. 2. The forms can be created by the dealership s DMS provider. ADP and Reynolds & Reynolds always have the current forms in their forms library. The dealership can request the forms from their provider and have the forms created thru the DMS provided forms printing program. This option is preferable when the transaction occurs at the time of sale in the business office. It is more difficult to use this option when the transaction takes place on the service drive, thru a business call center or in the sales departments after the sale of the vehicle has occurred. 3. The forms can be created using the Forms Builder program. Universal Lenders LLC supplies each dealership with a Forms Builder program which is loaded on the employee s computer. This method works best for all the potential transaction scenarios. This program is supplied on the Dealer Sales Tool CD referenced in Section B above. 4. The forms can be created with the ZERO Plan Menu. Review Section J below for complete details. The ZERO Plan Menu incorporates the forms builder described in 3 above

18 F-3 Instructions on Completing the Two Forms Below are the detailed instructions on how to complete each form. Although these sample instruction forms may not be the newest version of each form the information that is required will be the same. Current versions can always be found on our website at

19 - 19 -

20 Section G How the Dealership Gets Paid G-1 Review of the Required Documents After the transaction has occurred and before the documents are delivered to Universal Lenders LLC it is suggested that the documents be reviewed for completeness and accuracy. Although it is Universal Lenders LLC objective to never return a loan package to a dealership, certain discrepancies can not be corrected at the Universal offices and will require that the documents be returned to the dealership. Please refer to Sections C and D above to reference the guidelines that should be checked before the document package is sent. G-2 Creating the Document Package The required documents for every loan presented to Universal Lenders LLC for payment are (i)the Customer Note & Contract, (ii)a copy of the vehicle policy(s) for each policy financed under the Customer Note & Contract, (iii) a copy of the drivers license or state issued picture identification for each signer of the Customer Note & Contract and (iv)the Addendum required for non cancellable products. If the customer(s) request a payment option using automatic withdrawal or Credit Card (See Section E above) the Customer Payment Authorization form is required as well. G-3 Delivery to Universal Lenders LLC The Document Package must be received at least 2 weeks before the first payment. The method that the document package is sent to Universal Lenders LLC determines how the payment is sent back to the dealership. If the document package is mailed then the dealer payment will be mailed. If the document package is delivered by an overnight service then the dealer payment will be sent via an overnight service. The preferred method is for the dealership to send the document package via an overnight service to insure that the original documents arrive in a timely fashion and the delivery can be tracked. Getting customers to return to the dealership to re-execute documents due to lost mail could result in a lost sale. Please refer to Section A for Universal Lenders LLC s address. G-4 Calculation of Dealer Proceeds and Payment Once the documents are received, Universal Lenders LLC will process the document package and issue payment to the dealership within seven business days. This commitment could be delayed if there are problems with the paperwork that requires additional time to correct

21 The dealership will receive an amount that is equal to the Amount to Finance found on the Customer Note & Contract less (or minus) the service fee charged by Universal Lenders LLC. The amount of the fee can be found on the most current Exhibit A to the Dealer Agreement issued by Universal Lenders LLC from time to time and referenced in Section C Terms and Guidelines above. G-5 FACT SHEET Dealer Cash Flow Universal Lenders LLC issues FACT SHEETS to answer frequently asked questions. All the FACT SHEETS can be found on the Dealer Sales Tool CD. This particular FACT SHEET may help you understand the contents of this section

22 Section H Customer Service H-1 It Starts at the Dealership It is Universal Lenders LLC intent to provide excellent customer service to the dealership s clients. The dealership should make sure the customer knows that Universal Lenders LLC is going to service their loan. The customer should be directed to the toll free phone number and address located on the Customer Note & Contract in the event they need to contact Universal Lenders LLC. It is also suggested that the dealership clearly explain that any questions involving claims and coverage of the product policy financed should be directed to the dealership and not Universal Lenders LLC. It should be clear that Universal Lenders LLC can only help with any questions about their monthly payments. Customer service starts with good communication. H-2 Collection Notices In order to reduce cancellations and profit charge backs due to customer payment defaults Universal Lenders LLC has an aggressive collection plan in place. The following correspondence reminds the customers that payments are due on time: A friendly reminder note is mailed when an account is 5 days delinquent. A Late notice is mailed when an account becomes 10 days delinquent. A certified letter with return receipt requested is mailed when an account reaches 20 days delinquent. It clearly states that payment is due within 10 days or their policy will be cancelled. This letter is referred to as a customer CURE letter. A supervisory phone call prior to cancellation. H-3 Customer CURE Letter and Dealership Involvement When the customer is mailed the CURE letter Universal Lenders LLC also faxes a copy of the CURE letter to the designated employee at the selling dealership. When a dealership is enrolled, the dealership designates an employee to receive the faxed copies of CURE letters. Universal Lenders LLC suggests that a dealership employee contact the customer in an attempt to stop a pending cancellation and chargeback. It has been proven that dealership involvement will reduce profit charge backs and cancellations

23 Section I Cancellation of Financed Products I-1 Dealership Responsibility Every dealership authorized to use The ZERO Plan has signed a dealer agreement with Universal Lenders LLC. The portion of the dealer agreement that deals with policy cancellation is found in Section C Dealer Responsibilities Paragraph 8. It reads: Upon cancellation of a VSA by the customer or for a default by the customer under the terms of the Note, Dealer agrees to timely issue a full pro rata refund based upon time, and not upon elapsed miles, made payable solely to Universal or to cause the Administrator to timely issue a full pro rata refund based upon time, and not upon elapsed miles, to Universal pursuant to the terms and conditions of the VSA. In addition, should the terms of a VSA call for a reduction in the pro rata refund amount for any claims paid under the policy, Dealer agrees to disregard these terms and pay the full pro rata refund without regard to the reduction of the refund amount by the amount of any claims paid*. *The executed Agreements contain the exact language agreed to by the parties and supersedes the above sample language. In summary the dealership when presented with a cancellation request issued by Universal Lenders LLC will timely issue the cancellation refund check made payable to Universal Lenders LLC. The calculation must be pro rated based upon time and not upon miles. In addition the calculation cannot reduce the refund amount by the amount of any paid claims. I-2 Calculation of the Refund What is Due to Universal Lenders LLC When Universal Lenders LLC notifies the dealership of a request to cancel the product policy the notification will include the amount of the current customer balance which is always less than the specific calculation for the refund based on the specific language from the product policy. The notification is faxed to the dealership and then mailed. A sample of these requests (one at customer request and one at Universal s request) can be found below in I-4 and I-6 The notification will inform the dealership of the amount of the customer account balance. In most cases the customer account balance is less then the calculated cancellation refund amount. Universal Lenders will not ask for an amount over the calculated refund per the Policy. The dealership will determine what to do with the Customer Surplus (definition: Cancellation Refund Amount minus the Customer Account Balance) based on their own state laws

24 I-3 Cancellation Due to Customer Request When a customer informs us that it is their wish to cancel the product policy and payoff their account at Universal Lenders LLC we ask the customer to put their request in writing. When the written request is received the dealership is informed via fax and mail. Universal Lenders LLC will request a check be issued for the customer account balance amount to payoff the account. The dealership needs to issue the check and send it to Universal Lenders LLC within 10 days. When the dealership receives the notification it can attempt to contact the customer to stop their request and retain its profit. Should the customer have a change of heart then a written request from the customer to reinstate the loan must be sent to Universal Lenders LLC. I-4 Cancellation Due to Customer Default In the event of a customer default, Universal Lenders LLC will notify the dealership to cancel the product policy and to issue a check to Universal Lenders LLC. The requested cancellation amount is calculated per I-2 above but is in all cases the amount that the customer owes Universal Lenders LLC at the time of the default. The dealership needs to issue the check and send it to Universal Lenders LLC within 10 days. A sample copy of the cancellation notification is found in I-5 below

25 I-5 Sample of Cancellation Request Due to a Customer Default

26 I-6 Right to Offset The dealer agreement gives Universal Lenders LLC the right to offset monies that Universal Lenders LLC owes the dealership in order to fund cancellation requests that have not been paid in a timely fashion by the dealership. Universal Lenders LLC will only utilize the right to offset after numerous requests for dealership payment. There is a $50.00 fee that will assessed by Universal Lenders should the additional work of offsetting be required

27 I-7 FACT SHEET-Effect of Cancellation on Dealer Profit Universal Lenders LLC issues FACT SHEETS to answer frequently asked questions. All the FACT SHEETS can be found on the Dealer Sales Tool CD. This particular FACT SHEET may help you understand the contents of this section. Most Service Contract policies contain language that make the Administrator legally responsible for cancelling the Service Contract upon request by the consumer and to refund to the consumer the pro rata remaining portion of the purchase price of the service contract less an administrative fee. The Administrator normally has a dealer agreement with the selling dealer which requires the dealer to process cancellations on the Administrator's behalf. Example Sale: 24 month mile Service Contract Purchase price= $ Cost = $ Dealer Profit = $ month Cancellation fee= $50.00 Refund Calculation Summary Customer Request: Customer requests a cancellation with miles on the vehicle and12 months after delivery (50% pro rata usage). The Dealer calculates a consumer refund based on 50% prorated use equaling $600.00( x 50%). A cancellation fee reduces the consumer refund to If the customer proves that the lien holder has been satisfied (Loan paid off) the dealer issues a check directly to the customer. Universal Lenders LLC (Universal) Requested Cancellation due to non payment: Cancellation Effect on Profit Customer Refund Surplus: The method of calculating the refund amount is the same as the Customer Requested Cancellation above. When the customer defaults on his loan to Universal then Universal will contact the Dealer and request a cancellation. The Dealer will issue a check made payable solely to Universal for the amount of the customer balance owed to Universal. The amount requested is less then the customer refund. After the Dealer has issued the full refund there will be a calculation made to determine what the Administrator owes the Dealer for the premium the Dealer paid to the Administrator to purchase the service contract. In the example above the dealer will seek from the Administrator 50% of the cost of the service contract purchase price totaling $ less the cancellation fee they collected (< x 50%> ). The cancellation s effect on the dealer s original profit is that the dealer retains of their profit (50% of Profit) In most cases Universal will request a refund check from the dealer which is less then the customer refund based on the policy calculation. It will be the dealership s decision on what to do with the surplus (Calculated Refund Amount Universal Requested Amount) based on their own state laws and regulations

28 Section J ZERO Plan Menu The most difficult sale for most Retailers is the Cash transaction where the customer arrives with a check from their credit union, bank or outside lender. Retailers are used to selling F&I Protection Products using a payment close as presented with the numerous Menu Systems. Menu selling has historically only been successful with those customers where the Retailer arranged financing. Selling product packages without a payment option is very difficult. Here are the results of an independent survey conducted by Automotive News. To assist our Retailers in selling F&I Products using the ZERO Plan program we now offer the ZERO Plan Menu to each of our Retailers on an optional basis. To learn more about this dynamic sales tool please continue

29 ZERO Plan Menu The Ultimate Closing Tool for Cash Buyers & Service Drive Customers Program Description: Designed to be a stand alone menu presentation for cash buyers and service drive customers. The intension is not to replace the current menu system at the Retailer but to increase the penetration of F&I Product sales by using a specialized presentation. Internet Based and Powered by Universal Lenders Technology Partner VisionMenu. Setup, training and customer support are all included. Retailer has complete flexibility to design the product packages and pricing of each package or component within the package. Retailer can set which ZERO Plan payments & terms are displayed. The ZERO Plan Menu will complete and print the ZERO Plan forms when a package is sold. Quick and easy entry powers this menu..no more than a minute before Menu is presented. Contact Universal Lenders to enroll in this Revenue Generating Program!

UNIVERSAL LENDERS LLC

Agent Presentation About Universal Lenders and the ZERO Plan Strategy to Increase Dealership Profit and Agent Commission Step by Step. The ZERO Plan Process Fees and Funding Sample Transactions www.the-zero-plan.com

Agent Presentation About Universal Lenders and the ZERO Plan Strategy to Increase Dealership Profit and Agent Commission Step by Step. The ZERO Plan Process Fees and Funding Sample Transactions www.the-zero-plan.com

Installment Payment Program (IPP)

") Installment Payment Program (IPP) IPP Guidelines The Installment Payment Program (IPP) gives customers the option to purchase Extended Service Plan coverage in 5, 11 and 17 monthly installments using their

Installment Payment Program (IPP) IPP Guidelines The Installment Payment Program (IPP) gives customers the option to purchase Extended Service Plan coverage in 5, 11 and 17 monthly installments using their

PLANNED MAINTENANCE Dealer Administrator Manual

PLANNED MAINTENANCE Dealer Administrator Manual 2009 H-D. Harley-Davidson and the Bar & Shield logo are among the trademarks of H-D Michigan, Inc. HDPM-DAM Rev 11/09 The Planned Maintenance Portal www.hdplan.com

PLANNED MAINTENANCE Dealer Administrator Manual 2009 H-D. Harley-Davidson and the Bar & Shield logo are among the trademarks of H-D Michigan, Inc. HDPM-DAM Rev 11/09 The Planned Maintenance Portal www.hdplan.com

Plan Sponsor Administrative Manual

Plan Sponsor Administrative Manual V 3.1 Sponsor Access Website January 2017 Table of Contents Welcome Overview... p 5 How to Use this Manual... p 5 Enrollment Overview... p 7 Online Enrollment Description...

Plan Sponsor Administrative Manual V 3.1 Sponsor Access Website January 2017 Table of Contents Welcome Overview... p 5 How to Use this Manual... p 5 Enrollment Overview... p 7 Online Enrollment Description...

econtracting Faster funding. Fewer hassles. Improved cash flow. Higher CSI. A Quick Reference User Guide

Faster funding. Fewer hassles. Improved cash flow. Higher CSI. econtracting A Quick Reference User Guide For additional questions, contact DealerTrack at 1.877.357.8725 What is econtracting? What does

Faster funding. Fewer hassles. Improved cash flow. Higher CSI. econtracting A Quick Reference User Guide For additional questions, contact DealerTrack at 1.877.357.8725 What is econtracting? What does

PriceMyLoan.com Lender AE Guide. Revision 0707

PriceMyLoan.com Revision 0707 PriceMyLoan INTRODUCTION... 3 CUSTOMER SUPPORT... 3 VIEWING LOAN SUBMISSIONS... 4 AUTOMATIC EMAIL NOTIFICATIONS... 5 PRICING ENGINE COMMON SCENARIOS... 6 Running the LPE on

PriceMyLoan.com Revision 0707 PriceMyLoan INTRODUCTION... 3 CUSTOMER SUPPORT... 3 VIEWING LOAN SUBMISSIONS... 4 AUTOMATIC EMAIL NOTIFICATIONS... 5 PRICING ENGINE COMMON SCENARIOS... 6 Running the LPE on

AHFC Electronic Contracting Frequently Asked Questions V0.1

V0.1 Published on 09/18/2017 Introduction The following cover a range of questions that dealers may ask as AHFC launches its electronic contracting solution, icontracting. This document will answer questions

V0.1 Published on 09/18/2017 Introduction The following cover a range of questions that dealers may ask as AHFC launches its electronic contracting solution, icontracting. This document will answer questions

Payment Portal Registration Quick Guide

Payment Portal Registration Quick Guide Paying your rent is fast and easy with Invitation Homes online portal! Step 1: To register online and create your account, visit www.. Hover over the Current Residents

Payment Portal Registration Quick Guide Paying your rent is fast and easy with Invitation Homes online portal! Step 1: To register online and create your account, visit www.. Hover over the Current Residents

Loan Servicing Procedures Guide

Loan Servicing Procedures Guide Multifamily Capital Markets Newmark Knight Frank provides post-closing services to you for your loan. Your entire relationship is overseen by your Portfolio Manager. As

Loan Servicing Procedures Guide Multifamily Capital Markets Newmark Knight Frank provides post-closing services to you for your loan. Your entire relationship is overseen by your Portfolio Manager. As

Leveraged Online User Guide

Leveraged Online User Guide Overview This brochure is a tool to help navigate you through the Online Service. Leverage Online is a secure Online Service that allows you to: monitor your loan facilities

Leveraged Online User Guide Overview This brochure is a tool to help navigate you through the Online Service. Leverage Online is a secure Online Service that allows you to: monitor your loan facilities

Chapter Three Contribution Remittance

Chapter Three Contribution Remittance Chapter Three Highlights Now that the enrollment process has taken place and all of the appropriate forms have been completed, the next step is to establish deductions

Chapter Three Contribution Remittance Chapter Three Highlights Now that the enrollment process has taken place and all of the appropriate forms have been completed, the next step is to establish deductions

LENDER SOFTWARE PRO USER GUIDE

LENDER SOFTWARE PRO USER GUIDE You will find illustrated step-by-step examples in these instructions. We recommend you print out these instructions and read at least pages 4 to 20 before you start using

LENDER SOFTWARE PRO USER GUIDE You will find illustrated step-by-step examples in these instructions. We recommend you print out these instructions and read at least pages 4 to 20 before you start using

CREATE/SEARCH/UPDATE A CUSTOMER

CREATE/SEARCH/UPDATE A CUSTOMER 1) To create a New Application you must start with a Customer Search a. Click on the Customer link on the menu bar. b. In the Legal Name box, type either the full customer

CREATE/SEARCH/UPDATE A CUSTOMER 1) To create a New Application you must start with a Customer Search a. Click on the Customer link on the menu bar. b. In the Legal Name box, type either the full customer

SHEFFIELD FINANCIAL PROGRAM GUIDELINES

SHEFFIELD FINANCIAL PROGRAM GUIDELINES These Program Guidelines provide dealers with tips on offering simple, streamlined financing that improves both the dealer and borrower experience. Following the

SHEFFIELD FINANCIAL PROGRAM GUIDELINES These Program Guidelines provide dealers with tips on offering simple, streamlined financing that improves both the dealer and borrower experience. Following the

The values within the DMS can be held as consolidated totals if required, as any individual items can be extracted from the Service Plan System.

VERSION 3.1.1 The principle idea of the accounting system is to mirror the balance sheet values held within the edynamix Service Plan system with those held on the Dealer Management System (DMS) balance

VERSION 3.1.1 The principle idea of the accounting system is to mirror the balance sheet values held within the edynamix Service Plan system with those held on the Dealer Management System (DMS) balance

All other fees remain unchanged.

As of September 15, 2014, the following modifications to the DirectSERVICE Investment Program For Stockholders of AT&T Inc. will go into effect. This Program is sponsored and administered by Computershare

As of September 15, 2014, the following modifications to the DirectSERVICE Investment Program For Stockholders of AT&T Inc. will go into effect. This Program is sponsored and administered by Computershare

DTE Energy retirees: Welcome to PayFlex

DTE Energy retirees: Welcome to PayFlex You are enrolled in a Retiree Reimbursement Account (RRA). Your new RRA comes with some great tools to help you manage your account. Through the PayFlex member website,

DTE Energy retirees: Welcome to PayFlex You are enrolled in a Retiree Reimbursement Account (RRA). Your new RRA comes with some great tools to help you manage your account. Through the PayFlex member website,

Greenshades Garnishments User Guide

Greenshades Garnishments User Guide 1. 1. General Overview... 4 1.1. About this Guide... 4 1.2. How Greenshades Garnishments Works... 4 1.3. Default Deduction Setup within GP... 5 1.4. Employee Deduction

Greenshades Garnishments User Guide 1. 1. General Overview... 4 1.1. About this Guide... 4 1.2. How Greenshades Garnishments Works... 4 1.3. Default Deduction Setup within GP... 5 1.4. Employee Deduction

The following Key Features describe important functions in the Account and Loan Transfer service.

Account and Loan Transfer The Account Transfer service makes moving funds between accounts secure and simple. The user will find processing Multi-Entry Transfers and defining Recurring Transfers as easy

Account and Loan Transfer The Account Transfer service makes moving funds between accounts secure and simple. The user will find processing Multi-Entry Transfers and defining Recurring Transfers as easy

Private Party Purchase Cover Sheet

Private Party Purchase Cover Sheet To: Lending Operations From: FARM BUREAU AGENT E-mail: LendingFax@farmbureaubank.com Contact Number: ( ) - Fax: 800.499.4950 Email: farmbureau@agent.com Date: Total Number

Private Party Purchase Cover Sheet To: Lending Operations From: FARM BUREAU AGENT E-mail: LendingFax@farmbureaubank.com Contact Number: ( ) - Fax: 800.499.4950 Email: farmbureau@agent.com Date: Total Number

Consumer Internet Banking Agreement

Consumer Internet Banking Agreement 1. AGREEMENT. This agreement contains the terms and conditions that govern accessing or using the Consumer Internet Banking, Bill Payment Services, E-bill Service and

Consumer Internet Banking Agreement 1. AGREEMENT. This agreement contains the terms and conditions that govern accessing or using the Consumer Internet Banking, Bill Payment Services, E-bill Service and

HomePath Online Offers Guide for Public Entity and Non-Profit Buyers

HomePath Online Offers Guide for Public Entity and Non-Profit Buyers 2017 Fannie Mae. Trademarks of Fannie Mae. July 2017 1 Table of Contents Introduction... 3 HomePath Online Offers User Support... 3

HomePath Online Offers Guide for Public Entity and Non-Profit Buyers 2017 Fannie Mae. Trademarks of Fannie Mae. July 2017 1 Table of Contents Introduction... 3 HomePath Online Offers User Support... 3

Your. Getting Reimbursed Guide

Your Getting Reimbursed Guide Table of Contents Introduction to Getting Reimbursed........... 4 Managing your HRA online................ 5 The Reimbursement Process............... 8 Getting Started with

Your Getting Reimbursed Guide Table of Contents Introduction to Getting Reimbursed........... 4 Managing your HRA online................ 5 The Reimbursement Process............... 8 Getting Started with

Plan Sponsor Website Guide

Plan Sponsor Website Guide Accessing Your Account... p 1 Summary... p 2 Your Participants... p 3 Participant Loans... p 6 Participant Withdrawals... p 8 Plan Asset Details... p 9 Plan Information... p

Plan Sponsor Website Guide Accessing Your Account... p 1 Summary... p 2 Your Participants... p 3 Participant Loans... p 6 Participant Withdrawals... p 8 Plan Asset Details... p 9 Plan Information... p

Payment Center Quick Start Guide

Payment Center Quick Start Guide Self Enrollment, Online Statements and Online Payments Bank of America Merrill Lynch May 2014 Notice to Recipient This manual contains proprietary and confidential information

Payment Center Quick Start Guide Self Enrollment, Online Statements and Online Payments Bank of America Merrill Lynch May 2014 Notice to Recipient This manual contains proprietary and confidential information

Agency Bulletin. Great news for our Personal Lines policyholders and agents! August 9, 2012 BULLETIN NO. 5268

August 9, 2012 BULLETIN NO. 5268 TO: Merchants Insurance Group Personal Lines Agents SUBJECT: Introduction of epolicy and ebill Delivery Service Agency Bulletin Great news for our Personal Lines policyholders

August 9, 2012 BULLETIN NO. 5268 TO: Merchants Insurance Group Personal Lines Agents SUBJECT: Introduction of epolicy and ebill Delivery Service Agency Bulletin Great news for our Personal Lines policyholders

4 - Reporting Wages & Contributions

Illinois Municipal Retirement Fund Reporting Wages & Contributions / SECTION 4 4 - Reporting Wages & Contributions REPORTING WAGES & CONTRIBUTIONS... 119 4.00 INTRODUCTION... 119 4.10 GENERAL EXPLANATIONS...

Illinois Municipal Retirement Fund Reporting Wages & Contributions / SECTION 4 4 - Reporting Wages & Contributions REPORTING WAGES & CONTRIBUTIONS... 119 4.00 INTRODUCTION... 119 4.10 GENERAL EXPLANATIONS...

OregonSaves Employer Handbook

OregonSaves Employer Handbook A Guide to Your Role and Responsibilities October 2017 OregonSaves is overseen by the Oregon Retirement Savings Board. Ascensus College Savings Recordkeeping Services, LLC

OregonSaves Employer Handbook A Guide to Your Role and Responsibilities October 2017 OregonSaves is overseen by the Oregon Retirement Savings Board. Ascensus College Savings Recordkeeping Services, LLC

Manage your business accounts the easy way with AccèsD Affaires

c00 Manage your business accounts General information about accounts and transactions c01 The tab groups menus of the chequing accounts, investments, RRSPs and loans registered in your business profile.

c00 Manage your business accounts General information about accounts and transactions c01 The tab groups menus of the chequing accounts, investments, RRSPs and loans registered in your business profile.

IRAdirect User Guide Fully-Administered Program

IRAdirect User Guide Fully-Administered Program It is understood that the publisher is not engaged in rendering legal or accounting services. Every effort has been made to ensure the accuracy of the material

IRAdirect User Guide Fully-Administered Program It is understood that the publisher is not engaged in rendering legal or accounting services. Every effort has been made to ensure the accuracy of the material

Mellon Investor Services. Investor Services Program for Shareholders of Target Corporation

Mellon Investor Services Investor Services Program for Shareholders of Target Corporation Program Sponsored and Administered by Mellon Bank, N.A. Not by Target Corporation Effective August 1, 2005 Dear

Mellon Investor Services Investor Services Program for Shareholders of Target Corporation Program Sponsored and Administered by Mellon Bank, N.A. Not by Target Corporation Effective August 1, 2005 Dear

HomePath Online Offers Guide for Selling Agents

HomePath Online Offers Guide for Selling Agents 2012 Fannie Mae. Trademarks of Fannie Mae FM 0912 1 Table of Contents Introduction...3 Online Offers User Support...3 Your Account...4 Registering on HomePath.com...4

HomePath Online Offers Guide for Selling Agents 2012 Fannie Mae. Trademarks of Fannie Mae FM 0912 1 Table of Contents Introduction...3 Online Offers User Support...3 Your Account...4 Registering on HomePath.com...4

Non-ERISA Loan Application and Agreement

The Variable Annuity Life Insurance Company (VALIC), Houston, Texas Non-ERISA Loan Application and Agreement For VALIC Annuity Accounts Only All Plan Types Mail Completed Forms to: VALIC Document Control

The Variable Annuity Life Insurance Company (VALIC), Houston, Texas Non-ERISA Loan Application and Agreement For VALIC Annuity Accounts Only All Plan Types Mail Completed Forms to: VALIC Document Control

GENERAL What s changing? AHFC is providing an optional ACH payment method that dealers can use to pay off any type of customer account.

GENERAL What s changing? AHFC is providing an optional ACH payment method that dealers can use to pay off any type of customer account. What s not changing? Do dealers have to sign up or enroll to use

GENERAL What s changing? AHFC is providing an optional ACH payment method that dealers can use to pay off any type of customer account. What s not changing? Do dealers have to sign up or enroll to use

Health Savings Account - HSA Employer Guide

Health Savings Account - HSA Employer Guide October 2013 Table of Contents Month, Welcome Year... 3 What Do You Need to Do Now?... 3 Employer Role With Respect to HSAs... 4 Security... 4 Fees and Billing...

Health Savings Account - HSA Employer Guide October 2013 Table of Contents Month, Welcome Year... 3 What Do You Need to Do Now?... 3 Employer Role With Respect to HSAs... 4 Security... 4 Fees and Billing...

Travelers. Electronic Policy View

Travelers Electronic Policy View 1 Contents INTRODUCTION 3 ACCESSING ELECTRONIC POLICY VIEW 4 CUSTOMER SEARCH SCREEN 5 TRANSACTION SUMMARY SCREEN 6 SAVING A TRANSACTION 7 POLICY PRESENTMENT VIEW 8 FREQUENTLY

Travelers Electronic Policy View 1 Contents INTRODUCTION 3 ACCESSING ELECTRONIC POLICY VIEW 4 CUSTOMER SEARCH SCREEN 5 TRANSACTION SUMMARY SCREEN 6 SAVING A TRANSACTION 7 POLICY PRESENTMENT VIEW 8 FREQUENTLY

Plan Sponsor User Guide

Plan Sponsor User Guide Getting Started with PensionEdge Plus This guide is designed to provide you with a quick understanding of the many features of the PensionEdge Plus portal. The portal allows you

Plan Sponsor User Guide Getting Started with PensionEdge Plus This guide is designed to provide you with a quick understanding of the many features of the PensionEdge Plus portal. The portal allows you

QuickBooks Pro Manual

QuickBooks Pro Manual for Development Organisations Fifth version prepared December 2009 for users of QuickBooks Pro 2006. For limited circulation within Mango and selected NGOs (further information from

QuickBooks Pro Manual for Development Organisations Fifth version prepared December 2009 for users of QuickBooks Pro 2006. For limited circulation within Mango and selected NGOs (further information from

PriceMyLoan.com Broker s Guide. Revision 0705

PriceMyLoan.com Revision 0705 PriceMyLoan Introduction... 3 Create a New File... 4 Upload a Fannie Mae File... 5 Upload a Calyx Point File... 5 Loan Request Interface... 6 Loan Officer Info... 6 Credit

PriceMyLoan.com Revision 0705 PriceMyLoan Introduction... 3 Create a New File... 4 Upload a Fannie Mae File... 5 Upload a Calyx Point File... 5 Loan Request Interface... 6 Loan Officer Info... 6 Credit

CONTRIBUTION GUIDELINES & ELECTRONIC SPECIFICATIONS

CONTRIBUTION GUIDELINES & ELECTRONIC SPECIFICATIONS This section discusses where and how to send contributions. We do not limit the number or frequency of contributions you may submit. Certain contracts

CONTRIBUTION GUIDELINES & ELECTRONIC SPECIFICATIONS This section discusses where and how to send contributions. We do not limit the number or frequency of contributions you may submit. Certain contracts

TRAVEL PORTAL INSTRUCTIONS

TRAVEL PORTAL INSTRUCTIONS Date: June 22, 2018 Version: Version 3.1 Prepared By: Berkley Canada Table of Contents 1 ACCESSING THE PORTAL... 3 1.1 LOGIN & LOGOUT... 3 1.2 RESET YOUR PASSWORD... 3 2 THE

TRAVEL PORTAL INSTRUCTIONS Date: June 22, 2018 Version: Version 3.1 Prepared By: Berkley Canada Table of Contents 1 ACCESSING THE PORTAL... 3 1.1 LOGIN & LOGOUT... 3 1.2 RESET YOUR PASSWORD... 3 2 THE

Vermilion County, Illinois. Payables Manual. November 2015 Edition

Vermilion County, Illinois Payables Manual November 2015 Edition 1 TABLE OF CONTENTS CHANGES TO PAYABLES PROCESSING AND NOTES FOR YOUR INFORMATION & USE... 3 PAYABLES PROCESSING TIPS AND PROCEDURES...

Vermilion County, Illinois Payables Manual November 2015 Edition 1 TABLE OF CONTENTS CHANGES TO PAYABLES PROCESSING AND NOTES FOR YOUR INFORMATION & USE... 3 PAYABLES PROCESSING TIPS AND PROCEDURES...

FREQUENTLY ASKED QUESTIONS

FREQUENTLY ASKED QUESTIONS The information provided in these FAQ s is for research purposes only and is not legal advice from the Alabama League of Municipalities, Municipal Inter-cept Services, LLC, their

FREQUENTLY ASKED QUESTIONS The information provided in these FAQ s is for research purposes only and is not legal advice from the Alabama League of Municipalities, Municipal Inter-cept Services, LLC, their

ebanking Agreement and Disclosure

ebanking Agreement and Disclosure This document contains two parts. Part A contains your consent to receive electronic communications from Cathay Bank. Part B sets forth the terms of our ebanking service.

ebanking Agreement and Disclosure This document contains two parts. Part A contains your consent to receive electronic communications from Cathay Bank. Part B sets forth the terms of our ebanking service.

TO: Merchants Insurance Group Commercial Lines Agents [EXCEPT NEW YORK]

![TO: Merchants Insurance Group Commercial Lines Agents [EXCEPT NEW YORK]](/thumbs/76/73744052.jpg "TO: Merchants Insurance Group Commercial Lines Agents [EXCEPT NEW YORK]") February 13, 2017 BULLETIN NO. 5622 TO: Merchants Insurance Group Commercial Lines Agents [EXCEPT NEW YORK] SUBJECT: Introduction of New Credit Card Payment Vendor Agency Bulletin Effective February 13,

February 13, 2017 BULLETIN NO. 5622 TO: Merchants Insurance Group Commercial Lines Agents [EXCEPT NEW YORK] SUBJECT: Introduction of New Credit Card Payment Vendor Agency Bulletin Effective February 13,

1. Welcome to BenefitBridge. To access the BenefitBridge portal, login to BenefitBridge from the internet. 2. In the internet address bar, type:

1. Welcome to BenefitBridge. To access the BenefitBridge portal, login to BenefitBridge from the internet. 2. In the internet address bar, type: www.benefitbridge.com/egusd 1 1. If you are a returning

1. Welcome to BenefitBridge. To access the BenefitBridge portal, login to BenefitBridge from the internet. 2. In the internet address bar, type: www.benefitbridge.com/egusd 1 1. If you are a returning

2012 STOCK OPTION FACT SHEET

2012 STOCK OPTION FACT SHEET SPECIAL ANNOUNCEMENT INTRODUCTION On December 31, 2011, BNY Mellon Shareowner Services ( BNY Mellon ) was acquired by Computershare. At this time, no changes have occurred

2012 STOCK OPTION FACT SHEET SPECIAL ANNOUNCEMENT INTRODUCTION On December 31, 2011, BNY Mellon Shareowner Services ( BNY Mellon ) was acquired by Computershare. At this time, no changes have occurred

County of San Bernardino Retirement Medical Trust (RMT) Plan

Plan") County of San Bernardino Retirement Medical Trust (RMT) Plan One of the benefits offered to eligible employees by the County of San Bernardino is the Retirement Medical Trust (RMT) plan. This is an account

County of San Bernardino Retirement Medical Trust (RMT) Plan One of the benefits offered to eligible employees by the County of San Bernardino is the Retirement Medical Trust (RMT) plan. This is an account

Credit Card set up and processing.

Credit Card set up and processing. This lesson includes 1. Default settings 0:30 2. Enable credit card processing for member application 4:38 3. MIC Bill Pay 6:27 4. Event Setup 9:17 5. Back office payment

Credit Card set up and processing. This lesson includes 1. Default settings 0:30 2. Enable credit card processing for member application 4:38 3. MIC Bill Pay 6:27 4. Event Setup 9:17 5. Back office payment

Manulife One. Client Guide

Manulife One Client Guide 1 Welcome to Manulife Bank... Manulife One is as much an innovative approach to managing your finances as it is a mortgage. This guide will assist you in getting the most out

Manulife One Client Guide 1 Welcome to Manulife Bank... Manulife One is as much an innovative approach to managing your finances as it is a mortgage. This guide will assist you in getting the most out

Administrative Guide for Workplace Voluntary Benefits

Administrative Guide for Workplace Voluntary Benefits 4456 7/09 Great benefits feel good You invest in your employees and care about their future. You provide benefits that both you and your employees

Administrative Guide for Workplace Voluntary Benefits 4456 7/09 Great benefits feel good You invest in your employees and care about their future. You provide benefits that both you and your employees

Bill Pay User Guide FSCB Business

Bill Pay User Guide FSCB Business 1 Table of Contents Enrollment Process... 3 Home Page... 4 Attention Required... 5 Shortcut Method... 5 Scheduled... 5 History... 5 Since You Last Logged In... 5 Payees

Bill Pay User Guide FSCB Business 1 Table of Contents Enrollment Process... 3 Home Page... 4 Attention Required... 5 Shortcut Method... 5 Scheduled... 5 History... 5 Since You Last Logged In... 5 Payees

FLORIDA SURPLUS LINES SERVICE OFFICE. IPC Procedures Manual

FLORIDA SURPLUS LINES SERVICE OFFICE IPC Procedures Manual December 2016 TABLE OF CONTENTS 1. INTRODUCTION... 4 1.1. Purpose of this Document...4 1.2. Intended Audience...4 1.3. FSLSO Contact Information...4

FLORIDA SURPLUS LINES SERVICE OFFICE IPC Procedures Manual December 2016 TABLE OF CONTENTS 1. INTRODUCTION... 4 1.1. Purpose of this Document...4 1.2. Intended Audience...4 1.3. FSLSO Contact Information...4

Hertha Longo, CSA Matt Wade

Hertha Longo, CSA Matt Wade Census and financial forecasting tool to assist religious institutes in decision-making and planning for the future Available on CD for purchase by religious institutes only

Hertha Longo, CSA Matt Wade Census and financial forecasting tool to assist religious institutes in decision-making and planning for the future Available on CD for purchase by religious institutes only

Fees There are currently no separate monthly or transaction fees assessed by the Bank for use of the Online Banking Service including the External

Online Banking Account Agreement General This Online Banking Agreement (Agreement) for accessing your TrustTexas Bank, SSB account(s) via the Internet explains the terms and conditions of Online Banking.

Online Banking Account Agreement General This Online Banking Agreement (Agreement) for accessing your TrustTexas Bank, SSB account(s) via the Internet explains the terms and conditions of Online Banking.

smart South Carolina Deferred Compensation Program Plan Service Center Guide

South Carolina Deferred Compensation Program Retire from work, not life. smart Plan Service Center Guide Your Resource for Plan Administration Details on how to process your payroll with the South Carolina

South Carolina Deferred Compensation Program Retire from work, not life. smart Plan Service Center Guide Your Resource for Plan Administration Details on how to process your payroll with the South Carolina

New York Guide to List Billing WELCOME TO DEARBORN NATIONAL. Life Insurance Company of New York

www.dearbornnational.com WELCOME TO DEARBORN NATIONAL UNDERWRITTEN BY DEARBORN NATIONAL LIFE INSURANCE COMPANY OF NEW YORK New York Guide to List Billing Life Insurance Company of New York Products and

www.dearbornnational.com WELCOME TO DEARBORN NATIONAL UNDERWRITTEN BY DEARBORN NATIONAL LIFE INSURANCE COMPANY OF NEW YORK New York Guide to List Billing Life Insurance Company of New York Products and

PO Box Providence, RI Toll Free Phone: ONLINE BANKING DISCLOSURE & AGREEMENT

PO Box 6808 - Providence, RI 02940 Toll Free Phone: 1-800-398-8472 ONLINE BANKING DISCLOSURE & AGREEMENT General Online Banking: You may: Perform account inquiries on checking, savings, certificate and

PO Box 6808 - Providence, RI 02940 Toll Free Phone: 1-800-398-8472 ONLINE BANKING DISCLOSURE & AGREEMENT General Online Banking: You may: Perform account inquiries on checking, savings, certificate and

Jewelry Care Plans: Montage

Table of Contents Introduction... 2 Program Coverage... 2 Jewelry Care... 2 Watch Care... 2 Program Terms... 2 Licensing... 2 Partner Contact Information... 2 Setting Up the Care Program... 2 System Options...

Table of Contents Introduction... 2 Program Coverage... 2 Jewelry Care... 2 Watch Care... 2 Program Terms... 2 Licensing... 2 Partner Contact Information... 2 Setting Up the Care Program... 2 System Options...

Welcome to Midland States Bank

Welcome to Midland States Bank Contents What s Next... 4 Conversion at a Glance... 5 Questions?... 5 Customer Care Center... 5 Customer Information Web Page... 6 Important Dates and Information... 6 Balances

Welcome to Midland States Bank Contents What s Next... 4 Conversion at a Glance... 5 Questions?... 5 Customer Care Center... 5 Customer Information Web Page... 6 Important Dates and Information... 6 Balances

On Line Lien Registrations. Personal Property Security Registry - Purpose and Content

Personal Property Security Registry - Purpose and Content The Personal Property Security Registry contains liens registered against personal property, such as motor vehicles. Secured parties are typically

Personal Property Security Registry - Purpose and Content The Personal Property Security Registry contains liens registered against personal property, such as motor vehicles. Secured parties are typically

Separately Managed Accounts. ANZ Trustees Investment Management Service Private Portfolios. Investor User Guide

Separately Managed Accounts ANZ Trustees Investment Management Service Private Portfolios Investor User Guide Contents Audience... 2 Objectives... 2 Related documentation... 2 Before you begin... 2 Disclaimer...

Separately Managed Accounts ANZ Trustees Investment Management Service Private Portfolios Investor User Guide Contents Audience... 2 Objectives... 2 Related documentation... 2 Before you begin... 2 Disclaimer...

WORKING WITH THE PAYMENT CENTER

WORKING WITH THE PAYMENT CENTER SECTION 1: ACCESSING THE PAYMENT CENTER Access mystar at https://mystar.sfccmo.edu with Chrome, Firefox, Internet Explorer 10 or Internet Explorer 11. Important Note: At

WORKING WITH THE PAYMENT CENTER SECTION 1: ACCESSING THE PAYMENT CENTER Access mystar at https://mystar.sfccmo.edu with Chrome, Firefox, Internet Explorer 10 or Internet Explorer 11. Important Note: At

On-Line Banking Agreement (Consumers Only) Please Retain For Your Records

Please Retain For Your Records") On-Line Banking Agreement (Consumers Only) Please Retain For Your Records In consideration of First State Bank Central Texas (the Bank ), issuing Login Codes, Passwords, PINS, and/or other access codes

On-Line Banking Agreement (Consumers Only) Please Retain For Your Records In consideration of First State Bank Central Texas (the Bank ), issuing Login Codes, Passwords, PINS, and/or other access codes

Getting started. UltraBranch Business Edition. alaskausa.org

Getting started UltraBranch Business Edition alaskausa.org Contents 2 4 6 8 9 11 13 14 15 21 22 23 24 Key features Getting started Company permissions Setting & exceeding limits Configuring ACH & tax payments

Getting started UltraBranch Business Edition alaskausa.org Contents 2 4 6 8 9 11 13 14 15 21 22 23 24 Key features Getting started Company permissions Setting & exceeding limits Configuring ACH & tax payments

Taking Care of Business

2018-19 Taking Care of Business University of St. Thomas Business Office THE UNIVERSITY OF ST THOMAS RESERVES THE RIGHT TO ADD, AMEND, OR REVOKE ANY OF THE CONTAINED RULES, POLICIES, REGULATIONS AND INSTRUCTIONS,

2018-19 Taking Care of Business University of St. Thomas Business Office THE UNIVERSITY OF ST THOMAS RESERVES THE RIGHT TO ADD, AMEND, OR REVOKE ANY OF THE CONTAINED RULES, POLICIES, REGULATIONS AND INSTRUCTIONS,

Then, complete a salary reduction agreement form by either going on-line or by contacting PlanConnect at the phone number indicated below.

Welcome! We re PlanConnect Your Employer s 403(b) Plan Administrator PlanConnect is the third-party administrator for employees of Huron City Schools for its 403(b) plan. We have been working with Huron

Welcome! We re PlanConnect Your Employer s 403(b) Plan Administrator PlanConnect is the third-party administrator for employees of Huron City Schools for its 403(b) plan. We have been working with Huron

GENERAL What s changing? AHFC is providing an optional ACH payment method that dealers can use to pay off any customer account.

GENERAL What s changing? AHFC is providing an optional ACH payment method that dealers can use to pay off any customer account. What s not changing? Do dealers have to sign up or enroll to use ACH Payoff?

GENERAL What s changing? AHFC is providing an optional ACH payment method that dealers can use to pay off any customer account. What s not changing? Do dealers have to sign up or enroll to use ACH Payoff?

Dealertrack unifi TM QUICK REFERENCE GUIDE

Dealertrack unifi TM QUICK REFERENCE GUIDE GET THE MOST OUT OF Dealertrack unifi TM Start, Structure, Finance and Transact the deal all in one online deal jacket. Efficiency Gain more insight into your

Dealertrack unifi TM QUICK REFERENCE GUIDE GET THE MOST OUT OF Dealertrack unifi TM Start, Structure, Finance and Transact the deal all in one online deal jacket. Efficiency Gain more insight into your

Bank to Bank Transfer Application

MEMBER FDIC EQUAL HOUSING LENDER Bank to Bank Transfer Application I am applying for authorization to transfer funds between my Blackhawk Bank checking/savings account(s) and my checking/savings account(s)

MEMBER FDIC EQUAL HOUSING LENDER Bank to Bank Transfer Application I am applying for authorization to transfer funds between my Blackhawk Bank checking/savings account(s) and my checking/savings account(s)

MI Policy Origination and Servicing Guide. Effective December 1, 2011

Origination and Effective Revision notes Revision notes for Section 3.4 A Home Affordable Refinance Program 2 Revision notes Table of Contents and Servicing Descriptions 1 Introduction....6 1.1 Insuring

Origination and Effective Revision notes Revision notes for Section 3.4 A Home Affordable Refinance Program 2 Revision notes Table of Contents and Servicing Descriptions 1 Introduction....6 1.1 Insuring

Standard Insurance Company. SI CTAdp 1 of 49 (5/14)

") Administration Guide for District-Paid Group Insurance Plans Endorsed by California Educators Insurance Plan (CEIP) for California Teachers Association (CTA) Standard Insurance Company SI 14724-CTAdp 1

Administration Guide for District-Paid Group Insurance Plans Endorsed by California Educators Insurance Plan (CEIP) for California Teachers Association (CTA) Standard Insurance Company SI 14724-CTAdp 1

Alliance Insured Services W A R R A N T Y C O M P A N Y

Alliance Insured Services W A R R A N T Y C O M P A N Y Alliance Insured Services Dealer Owned Portfolio At AIS, we come from an industry in which an administrator is in the driver s seat of the dealer

Alliance Insured Services W A R R A N T Y C O M P A N Y Alliance Insured Services Dealer Owned Portfolio At AIS, we come from an industry in which an administrator is in the driver s seat of the dealer

Leveraged Online User Guide

Leveraged Online User Guide Adviser Use Only Overview This brochure is a tool to help licensed advisers and dealer groups navigate through the Online Service. Leverage Online is a secure Online Service

Leveraged Online User Guide Adviser Use Only Overview This brochure is a tool to help licensed advisers and dealer groups navigate through the Online Service. Leverage Online is a secure Online Service

Electronic Banking Service Agreement and Disclosure

Electronic Banking Service Agreement and Disclosure What is Covered by this Agreement This Agreement between you and First Priority Bank governs the use of our Electronic and Internet Banking and Bill

Electronic Banking Service Agreement and Disclosure What is Covered by this Agreement This Agreement between you and First Priority Bank governs the use of our Electronic and Internet Banking and Bill

UCAA Expansion Application Insurer User Guide December 2017

UCAA Expansion Application Insurer User Guide December 2017 2017 National Association of Insurance Commissioners All rights reserved. Revised Edition National Association of Insurance Commissioners NAIC

UCAA Expansion Application Insurer User Guide December 2017 2017 National Association of Insurance Commissioners All rights reserved. Revised Edition National Association of Insurance Commissioners NAIC

HomePath Online Offers Guide for Listing Agents

HomePath Online Offers Guide for Listing Agents 2016 Fannie Mae. Trademarks of Fannie Mae. June 2016 1 Table of Contents Introduction... 3 HomePath Online Offers User Support... 3 Registration and Login...

HomePath Online Offers Guide for Listing Agents 2016 Fannie Mae. Trademarks of Fannie Mae. June 2016 1 Table of Contents Introduction... 3 HomePath Online Offers User Support... 3 Registration and Login...

employee savings investment plan (ESIP) summary plan description effective january 1, 2017 human energy. yours. TM

summary plan description effective january 1, 2017 human energy. yours. TM") employee savings investment plan (ESIP) summary plan description effective january 1, 2017 human energy. yours. TM This summary plan description (SPD) describes the Chevron ( the plan or the ESIP ). It

employee savings investment plan (ESIP) summary plan description effective january 1, 2017 human energy. yours. TM This summary plan description (SPD) describes the Chevron ( the plan or the ESIP ). It

The Taxpayers Guide to Brooklyn Taxes

The Taxpayers Guide to Brooklyn Taxes Jocelyne Ruffo - Revenue Collector April Lamothe - Assistant Revenue Collector Telephone # (860) 779-3411, option 5 Fax # 779-7853 Tax Collector PO Box 253 Brooklyn,

The Taxpayers Guide to Brooklyn Taxes Jocelyne Ruffo - Revenue Collector April Lamothe - Assistant Revenue Collector Telephone # (860) 779-3411, option 5 Fax # 779-7853 Tax Collector PO Box 253 Brooklyn,

Frequently Asked Questions about Retiree Reimbursement Accounts (RRAs)

") Frequently Asked Questions about Retiree Reimbursement Accounts (RRAs) 1. Do I need to do anything to sign up for an RRA? No. You re automatically enrolled in the RRA. If you want to use the online tools,

Frequently Asked Questions about Retiree Reimbursement Accounts (RRAs) 1. Do I need to do anything to sign up for an RRA? No. You re automatically enrolled in the RRA. If you want to use the online tools,

OPEN YOUR NEW ACCOUNT. Apply online in minutes or visit your local branch to open your new DuPont Community Credit Union account.

Make Your Move SWITCH YOUR CHECKING ACCOUNT TO DCCU You can make the move to DuPont Community Credit Union in three easy steps. Everything you need is provided in this Switch Kit, including helpful tips

Make Your Move SWITCH YOUR CHECKING ACCOUNT TO DCCU You can make the move to DuPont Community Credit Union in three easy steps. Everything you need is provided in this Switch Kit, including helpful tips

2018 HEALTHCARE FSA PROGRAM WITH PAYFLEX (AETNA)

") 2018 HEALTHCARE FSA PROGRAM WITH PAYFLEX (AETNA) Whether you are newly enrolling for 2018 or re-enrolling for 2018, you ll find the information here very helpful in understanding your FSA plan and the

2018 HEALTHCARE FSA PROGRAM WITH PAYFLEX (AETNA) Whether you are newly enrolling for 2018 or re-enrolling for 2018, you ll find the information here very helpful in understanding your FSA plan and the

RIVER CITY BANK CONSENT TO RECEIVE ELECTRONIC COMMUNICATIONS & ONLINE BANKING TERMS AND CONDITIONS. Consent to Receive Electronic Communications

RIVER CITY BANK CONSENT TO RECEIVE ELECTRONIC COMMUNICATIONS & ONLINE BANKING TERMS AND CONDITIONS Consent to Receive Electronic Communications This document includes consumer disclosures required under

RIVER CITY BANK CONSENT TO RECEIVE ELECTRONIC COMMUNICATIONS & ONLINE BANKING TERMS AND CONDITIONS Consent to Receive Electronic Communications This document includes consumer disclosures required under

PNC HSA Funding & Contribution Guide for Employers

PNC HSA Funding & Contribution Guide for Employers How to set up and send employer-directed HSA Contributions with PNC Bank 20180924AHNJ Document Updates The table below details updates made to the document

PNC HSA Funding & Contribution Guide for Employers How to set up and send employer-directed HSA Contributions with PNC Bank 20180924AHNJ Document Updates The table below details updates made to the document

Welcome to the BenefitWallet HSA!

2016 2017 Conduent Xerox HR Solutions, Business Services, LLC. All rights LLC. All reserved. rights reserved. BenefitWallet Conduent, is a Conduent trademark Agile of Xerox Star Corporation and BenefitWallet

2016 2017 Conduent Xerox HR Solutions, Business Services, LLC. All rights LLC. All reserved. rights reserved. BenefitWallet Conduent, is a Conduent trademark Agile of Xerox Star Corporation and BenefitWallet

Online Banking Agreement.

ONLINE BANKING / BILL PAYING AGREEMENT 1. The Services: Use of Liberty National Bank's Online Banking Services requires at least one eligible deposit or loan account with us. If you have more than one

ONLINE BANKING / BILL PAYING AGREEMENT 1. The Services: Use of Liberty National Bank's Online Banking Services requires at least one eligible deposit or loan account with us. If you have more than one

ALLEGANY CO-OP INSURANCE COMPANY. Agency Interface. Choice Connect User Guide

ALLEGANY CO-OP INSURANCE COMPANY Agency Interface Choice Connect User Guide ALLEGANY CO-OP INSURANCE COMPANY Choice Connect User Guide Allegany Co-op Insurance Company 9 North Branch Road Cuba NY 14727

ALLEGANY CO-OP INSURANCE COMPANY Agency Interface Choice Connect User Guide ALLEGANY CO-OP INSURANCE COMPANY Choice Connect User Guide Allegany Co-op Insurance Company 9 North Branch Road Cuba NY 14727

Electronic Funds Transfer Disclosure Statement and Agreement

ESL Federal Credit Union Electronic Funds Transfer Disclosure Statement and Agreement ESL ATM Card ESL Visa Check Card ESL Visa Health Savings Account Card TEL-E$L Automated Clearing House (ACH) Transactions

ESL Federal Credit Union Electronic Funds Transfer Disclosure Statement and Agreement ESL ATM Card ESL Visa Check Card ESL Visa Health Savings Account Card TEL-E$L Automated Clearing House (ACH) Transactions

Financial year end 2018

page 1 Financial year end 2018 User guide June 2018 page 2 Contents About this document 3 Objectives...3 Related documentation...3 Updates to this document...3 EOFY summary 4 Locking the overnight recalculation

page 1 Financial year end 2018 User guide June 2018 page 2 Contents About this document 3 Objectives...3 Related documentation...3 Updates to this document...3 EOFY summary 4 Locking the overnight recalculation

WHAT YOU SHOULD KNOW ABOUT YOUR CHAPTER 13 CASE

A MESSAGE FROM THE CHAPTER 13 STAFF The Chapter 13 staff understands that making the decision to file bankruptcy was not easy. Some of the many factors which cause people to file bankruptcy include loss

A MESSAGE FROM THE CHAPTER 13 STAFF The Chapter 13 staff understands that making the decision to file bankruptcy was not easy. Some of the many factors which cause people to file bankruptcy include loss

PROSPECTUS Program highlights include:

PROSPECTUS The Home Depot, Inc. is pleased to offer you the opportunity to participate in DepotDirect, a convenient and low-cost stock purchase program available for new investors to make an initial investment

PROSPECTUS The Home Depot, Inc. is pleased to offer you the opportunity to participate in DepotDirect, a convenient and low-cost stock purchase program available for new investors to make an initial investment

THE HAWAII LEMON LAW AND THE STATE CERTIFIED ARBITRATION PROGRAM

THE HAWAII LEMON LAW AND THE STATE CERTIFIED ARBITRATION PROGRAM A Consumer Handbook Published by the Department of Commerce and Consumer Affairs State Certified Arbitration Program 235 S. Beretania Street,

THE HAWAII LEMON LAW AND THE STATE CERTIFIED ARBITRATION PROGRAM A Consumer Handbook Published by the Department of Commerce and Consumer Affairs State Certified Arbitration Program 235 S. Beretania Street,

2015 rates for New Jersey consumers will be effective January 1, 2015

Great news! Announcing 2015 New Jersey rate information for AARP Medicare Supplement Insurance Plans 2015 rates for New Jersey consumers will be effective January 1, 2015 Read on for important details

Great news! Announcing 2015 New Jersey rate information for AARP Medicare Supplement Insurance Plans 2015 rates for New Jersey consumers will be effective January 1, 2015 Read on for important details

Take control of your auto loan

Take control of your auto loan A step-by-step guide Consumer Financial Protection Bureau How can this guide help you? While many people shop around for the best deal they can get on their vehicle, not

Take control of your auto loan A step-by-step guide Consumer Financial Protection Bureau How can this guide help you? While many people shop around for the best deal they can get on their vehicle, not

2018 HEALTH CARE FSA PROGRAM WITH PAYFLEX (AETNA)