End of the American Dream? How Mortgage Defaults and Foreclosures Affect Families and Communities

|

|

|

- Claire Dickerson

- 5 years ago

- Views:

Transcription

1 End of the American Dream? How Mortgage Defaults and Foreclosures Affect Families and Communities J. Michael Collins Assistant Professor, School of Human Ecology Director, Center for Financial Security University of Wisconsin Madison

2 Overview How did we get here? A look at Wisconsin and Dane county specifically Impacts on Families & Neighborhoods Policy responses Community efforts

3 Looking Back Historically Ownership = Good Mortgage has evolved dramatically The housing boom and mortgage explosion Income trends and home equity as consumption Subprime lending, predatory lending and the first wave of foreclosures - Unemployment and further waves - Roles of trigger events - health, income, 'shocks

4 Foreclosures Trending Back Up

5 Number of Foreclosure Filings State of Wisconsin Foreclosure Filings A 344% increase since ,725 28, , , , ,820 10,352 10,703 10,562 11,648 6, Based on filings reported in the Wisconsin Circuit Court Consolidated Court Automation Programs case management system.

6

7 Number of Foreclosure Filings 1,800 Dane County Annual Foreclosure Filings 1,600 1,550 1,400 1,200 1,203 1, Based on filings reported in the Wisconsin Circuit Court Consolidated Court Automation Programs case management system.

8 Percent Change in Foreclosure Filings 12.0% 10.0% 9.6% Dane County State of Wisconsin 8.0% 6.0% 5.8% 5.2% 4.0% 2.0% 1.6% 0.0% 0.7% 0.2% 0.3% -2.0% Change Q to Q % Change Q to Q Change Q to Q Change Q1-Q to Q1- Q Based on filings reported in the Wisconsin Circuit Court Consolidated Court Automation Programs case management system.

9 Source: Dane County Foreclosure Task Force

10 Neighborhood Effects Less incentive to maintain or upgrade properties Properties may sit vacant, attracting vandalism and crime signaling that the neighborhood is in a state of decline Increase in the number of properties on the market at a given time Properties may sell at a discount, both at auctions or preforeclosure sales, affecting the price of comparables used to estimate neighboring property values

11 Milwaukee Foreclosed Homes

12 Jeff Becker Dane County Foreclosure Density

13 Jeff Becker Tract Foreclosure Rate Unemployment Rate Income % 10.8% $34, % 5.6% $42, % 8.5% $29, % 4.5% $44, % 5.9% $53,631

14 Dane County Home Price < Bubble $210,000 $214,000 $217,900 $215,000 $200,700 $200, Data courtesy of Wisconsin Realtors Association

15 Foreclosures and Unemployment % REO by Zip Code Unemployment rate ( 2010) <5% 5-10% 10-15% >15% All <5% 5-10% 10-15% >15% All

16 Common Themes of Interviews with People in Foreclosure Process School aged kids minimize disruption Relationship issues Pride management with family & peers Lack of trust in institutions Some exceptions for helpful counselors / agencies Communication / Education is challenge Lack internet, limited phone, time constrained Interest in budgeting (reformed spendthrifts)

17 Financially Strapped I am on unemployment and I am about ready to declare bankruptcy. I can t do consumer credit counseling b/c I am not employed. All my unemployment checks go toward paying my two mortgages. I am $19k in debt. I would like to save but I need to work in order to save. - married woman in 40s By late delinquency (180+ days) Tapped out family Cashed in / borrowed from 401k Austerity budgeting

18 Emotional Toll I had a job where I could work overtime when I wanted. So I bought a lot of toys (motorcycle, trucks, etc.). Then they got repossessed. I found it devastating. It was so embarrassing. Now I have one vehicle the one that is most practical and it is hard. I did not realize my unemployment would be so long. I did not think it would happen to me. male in 50s Unwilling to reveal extent of needs Not seeking advice in community

19 Hard to Reach / Not Accessing Information I have access to the internet through the library. I simply cannot afford it at home. There is a lot of waiting and stuff so it makes it difficult. I do have an internet account at work but limited so I can t really do a search at work. - Single mother in 30s Reaching people phone, mail, web all limited

20 When during the month are people looking for help? Referrals by Week 0 Week 1 Week 2 Week 3 Week 4 Source: MortgageKeeper.org, 2010 Referrals by Counselors

21 Most Common: Food, Job, Utilities Unemployment Assistance 3% Pharmaceutical Costs 7% Senior Citizen Services Home Repair 3% 3% Childcare 2% Legal Services 9% Services Referred Other 7% Food Assistance Programs 19% Job Training 18% National Hotlines 11% Heating/Utility Costs 18% Source: MortgageKeeper.org, Referrals by Counselors

22 Typology of Consumers in Distress (Negative Trigger Events) Income disruption, but potential to work Job loss/cutback (relocation options) Divorce (child support issues) Widow/er (may have limited work options) Disability Chronic (DI application process) Health crisis Acute or ongoing expenses (medical debt management) Investor (not all are speculators) tenant eviction issues subsidized units Small business failure (non-real estate) Sale / bankruptcy (special issues if farm) Strategic defaulters

23 Providing Services Prevention People not in default, but worried Early Intervention Missed 1-2 payments Late Intervention Missed 3+ payments Transitional Support Short sale or foreclosure auction

24 Foreclosure Prevention and Response Create a Foreclosure Prevention Hotline Relocation Assistance and Social Services Understand Why Foreclosures Matter Homeownership Education and Counseling Foreclosure Prevention Counseling Work with Lenders and Servicers for Better Loan Modifications Expanded Legal Services Low-Interest Refinance Loans Protections for Tenants Credit Repair for Former Homeowners BEFORE Mortgage Delinquency DURING Mortgage Delinquency AFTER Foreclosure Anti- Predatory Lending Laws Oversight of Mortgage Brokers and Lenders Monitor Downpayment Passthroughs Develop a Coordinated Response Strategy Short-Term Emergency Loans Moratorium or Other Extension Refinancing with Flexible Underwriting Requirements Secure and Maintain Foreclosed Properties Streamline Private Section Disposition of Vacant Properties Acquire, Rehab, and Manage Foreclosed Homes

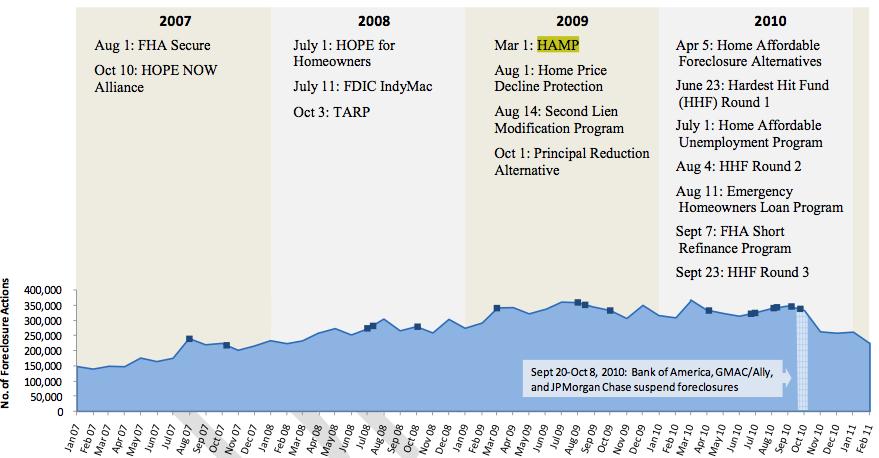

25 Policy Responses Hope Now (2007) FHA Hope for Homeowners (2008) HAMP (2009) revised numerous times HARP (2009) Hardest Hit Funds (2010) AG Settlement (2012)

26

27

28 Data for Wisconsin ommunityindicators/indicators_links.cfm#q2_ 2010

29 Local Resources Wisconsin Housing and Economic Development Authority Dane County Foreclosure Prevention Taskforce

452-3328 Federal Deposit Insurance Corporation (FDIC) (877) ASK-FDIC (925-4618); www.fdic.gov.")

30 Help Hotlines / Websites Credit Counseling: Mortgage Counseling: HOPE UW Extension: Wisconsin Department of Financial Institutions (800) Federal Deposit Insurance Corporation (FDIC) (877) ASK-FDIC ( ); Federal Trade Commission (877) FTC-HELP( );

31 GRAASKAMP CENTER FOR REAL ESTATE

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners November 2012 U.S. Department U.S Department of Housing of Housing and Urban and Urban Development Development

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners November 2012 U.S. Department U.S Department of Housing of Housing and Urban and Urban Development Development

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners May 2011 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners May 2011 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners April 2012 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners April 2012 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners August 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners August 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

FORECLOSURE PREVENTION PRINCIPAL REDUCTION AND. Preliminary Report, Findings and Recommendations from the IDT. Seattle City Council March 26, 2014

1 PRINCIPAL REDUCTION AND FORECLOSURE PREVENTION Preliminary Report, Findings and Recommendations from the IDT Seattle City Council March 26, 2014 2 IDT Scope of Work Resolution 31495 directed IDT to explore

1 PRINCIPAL REDUCTION AND FORECLOSURE PREVENTION Preliminary Report, Findings and Recommendations from the IDT Seattle City Council March 26, 2014 2 IDT Scope of Work Resolution 31495 directed IDT to explore

FORECLOSURE. I don t think I can make my mortgage payments but I don t want to go through a foreclosure. What are some of my options?

FORECLOSURE When you borrow money to buy a house or land, the creditor usually takes a security interest in the property you buy This means that if you don t pay, the creditor can foreclose upon (or take

FORECLOSURE When you borrow money to buy a house or land, the creditor usually takes a security interest in the property you buy This means that if you don t pay, the creditor can foreclose upon (or take

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

The Mortgage Industry

Financing Residential Real Estate Lesson 4: The Mortgage Industry Introduction In this lesson, we will cover: steps in the residential mortgage process; participants in the process, including loan originators

Financing Residential Real Estate Lesson 4: The Mortgage Industry Introduction In this lesson, we will cover: steps in the residential mortgage process; participants in the process, including loan originators

Mortgage Delinquencies and Foreclosures: Hawaii

Mortgage Delinquencies and Foreclosures: Hawaii Craig Nolte Community Development Department Federal Reserve Bank of San Francisco October 16, 2008 Do not cite or reproduce without permission. Overview

Mortgage Delinquencies and Foreclosures: Hawaii Craig Nolte Community Development Department Federal Reserve Bank of San Francisco October 16, 2008 Do not cite or reproduce without permission. Overview

FORECLOSURE PREVENTION

FORECLOSURE PREVENTION 1/1/2012 Resource Guide Brought to you by: NAACP Economic Department 1816 12 th Street, NW Washington DC 20009 www.naacp.org/econ Foreclosure prevention R E S O U R C E G U I D E

FORECLOSURE PREVENTION 1/1/2012 Resource Guide Brought to you by: NAACP Economic Department 1816 12 th Street, NW Washington DC 20009 www.naacp.org/econ Foreclosure prevention R E S O U R C E G U I D E

The Current Foreclosure Crisis Trends and Roadblocks to Recovery

The Current Foreclosure Crisis Trends and Roadblocks to Recovery American Planning Association February 22, 2011 Geoff Smith Senior Vice President Woodstock Institute Chicago, Illinois gsmith@woodstockinst.org

The Current Foreclosure Crisis Trends and Roadblocks to Recovery American Planning Association February 22, 2011 Geoff Smith Senior Vice President Woodstock Institute Chicago, Illinois gsmith@woodstockinst.org

Mortgage Delinquencies and Foreclosures: Hawaii

Mortgage Delinquencies and Foreclosures: Hawaii Presentation prepared by Carolina Reid, Ph.D. Community Development Department Federal Reserve Bank of San Francisco July 21, 2008 Analysis of First American

Mortgage Delinquencies and Foreclosures: Hawaii Presentation prepared by Carolina Reid, Ph.D. Community Development Department Federal Reserve Bank of San Francisco July 21, 2008 Analysis of First American

U.S. Foreclosure Outlook. To: Company Name Here Date: Goes Here

U.S. Foreclosure Outlook To: Company Name Here Date: Goes Here A brief note on methodology RealtyTrac collects foreclosure documents, postings and published notices from about 2,200 counties nationwide.

U.S. Foreclosure Outlook To: Company Name Here Date: Goes Here A brief note on methodology RealtyTrac collects foreclosure documents, postings and published notices from about 2,200 counties nationwide.

Early Delinquency Intervention

Early Delinquency Intervention Saving Your Home From Foreclosure There are many reasons homeowners face difficulty in making mortgage payments: unexpected expenses, loss of overtime, unemployment, overspending,

Early Delinquency Intervention Saving Your Home From Foreclosure There are many reasons homeowners face difficulty in making mortgage payments: unexpected expenses, loss of overtime, unemployment, overspending,

Early Delinquency Intervention SAVING YOUR HOME FROM FORECLOSURE

Early Delinquency Intervention SAVING YOUR HOME FROM FORECLOSURE BALANCE offers a variety of free and low-cost services to help you get out of debt, design a money management plan, and achieve your financial

Early Delinquency Intervention SAVING YOUR HOME FROM FORECLOSURE BALANCE offers a variety of free and low-cost services to help you get out of debt, design a money management plan, and achieve your financial

Homeowner Affordability and Stability Plan Fact Sheet

Homeowner Affordability and Stability Plan Fact Sheet The deep contraction in the economy and in the housing market has created devastating consequences for homeowners and communities throughout the country.

Homeowner Affordability and Stability Plan Fact Sheet The deep contraction in the economy and in the housing market has created devastating consequences for homeowners and communities throughout the country.

Short Sale Seller Advisory. Before Proceeding with a Short Sale. Arizona Department of Real Estate. Arizona Association of REALTORS

A short sale is a real estate transaction in which the sales price is insufficient to pay the loan(s) encumbering the property in addition to the costs of sale and the seller is unable to pay the difference.

A short sale is a real estate transaction in which the sales price is insufficient to pay the loan(s) encumbering the property in addition to the costs of sale and the seller is unable to pay the difference.

In the first three months of 2007, there

Subprime Lending and Foreclosure in Hennepin and Ramsey Counties by Jeff Crump In the first three months of 2007, there were 678 foreclosure sales in the city of Minneapolis, an increase of more than 100%

Subprime Lending and Foreclosure in Hennepin and Ramsey Counties by Jeff Crump In the first three months of 2007, there were 678 foreclosure sales in the city of Minneapolis, an increase of more than 100%

Early Delinquency Intervention: Saving Your Home From Foreclosure

Early Delinquency Intervention: Saving Your Home From Foreclosure There are many circumstances in a homeowner s life that could result in missed mortgage payments: unexpected expenses, loss of overtime,

Early Delinquency Intervention: Saving Your Home From Foreclosure There are many circumstances in a homeowner s life that could result in missed mortgage payments: unexpected expenses, loss of overtime,

THDA Homebuyer Education Initiative Customer Intake Form

Sample 3 Date Case# (Trainer completes) Trainer Organization County (Trainer completes) THDA Homebuyer Education Initiative Customer Intake Form Please provide information about yourself for customer tracking

Sample 3 Date Case# (Trainer completes) Trainer Organization County (Trainer completes) THDA Homebuyer Education Initiative Customer Intake Form Please provide information about yourself for customer tracking

THE POLICY RESPONSE TO FORECLOSURES:

THE POLICY RESPONSE TO FORECLOSURES: WHAT CAN STATE AND LOCAL ACTORS DO? PRESENTATION TO THE MISSOURI HOMEOWNERSHIP PRESERVATION SUMMIT JANUARY 14, 2010 JEFFERSON CITY, MISSOURI Spillover Effects of Foreclosures

THE POLICY RESPONSE TO FORECLOSURES: WHAT CAN STATE AND LOCAL ACTORS DO? PRESENTATION TO THE MISSOURI HOMEOWNERSHIP PRESERVATION SUMMIT JANUARY 14, 2010 JEFFERSON CITY, MISSOURI Spillover Effects of Foreclosures

Making Home Affordable Working Together to Help Homeowners

Making Home Affordable Working Together to Help Homeowners MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure. Transition from Home Ownership Historically

Making Home Affordable Working Together to Help Homeowners MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure. Transition from Home Ownership Historically

How to Stop and Avoid Foreclosure in Today's Market

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

How to Stop and Avoid Foreclosure in Today's Market

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

TRENDS IN DELINQUENCIES AND FORECLOSURES IN SOUTHERN CALIFORNIA

TRENDS IN DELINQUENCIES AND FORECLOSURES IN SOUTHERN CALIFORNIA April 2009 Melody Nava, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising

TRENDS IN DELINQUENCIES AND FORECLOSURES IN SOUTHERN CALIFORNIA April 2009 Melody Nava, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising

Assumptions, Mistakes, Successes, and Moving Forward: An Empirical Analysis of Foreclosures in North Minneapolis and Foreclosure Policies

Assumptions, Mistakes, Successes, and Moving Forward: An Empirical Analysis of Foreclosures in North Minneapolis and Foreclosure Policies CURA Housing Forum Friday, December 18, 2009 Thanks and Disclaimers

Assumptions, Mistakes, Successes, and Moving Forward: An Empirical Analysis of Foreclosures in North Minneapolis and Foreclosure Policies CURA Housing Forum Friday, December 18, 2009 Thanks and Disclaimers

The Impact of Foreclosures on Economic Recovery in Virginia

The Impact of Foreclosures on Economic Recovery in Virginia February, 2012 Brian Koziol Housing Policy and Research Analyst www.phonehome.org 804.354.0641 Where you live makes all the difference About

The Impact of Foreclosures on Economic Recovery in Virginia February, 2012 Brian Koziol Housing Policy and Research Analyst www.phonehome.org 804.354.0641 Where you live makes all the difference About

Managing Your Money: "Housing and Public Policy the Bubble, Present, and Future

Managing Your Money: "Housing and Public Policy the Bubble, Present, and Future PLATO (Participatory Learning and Teaching Organization) J. Michael Collins UW Madison Center for Financial Security Overview

Managing Your Money: "Housing and Public Policy the Bubble, Present, and Future PLATO (Participatory Learning and Teaching Organization) J. Michael Collins UW Madison Center for Financial Security Overview

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO February 2009 Craig Nolte, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO February 2009 Craig Nolte, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

U.S. Housing Markets: Looking Back, Looking Forward

U.S. Housing Markets: Looking Back, Looking Forward Dr. Raphael Bostic Assistant Secretary, Office of Policy Development and Research U.S. Department of Housing and Urban Development Special Thanks Ed

U.S. Housing Markets: Looking Back, Looking Forward Dr. Raphael Bostic Assistant Secretary, Office of Policy Development and Research U.S. Department of Housing and Urban Development Special Thanks Ed

The Housing Authority of Billings. SECTION 8 HOMEOWNERSHIP HANDBOOK For HAB and MDOC Section 8 participants

The Housing Authority of Billings SECTION 8 HOMEOWNERSHIP HANDBOOK For HAB and MDOC Section 8 participants Contact: Carrie Sharp, FSS/Home Ownership Coordinator Housing Authority of Billings 2415 1 st

The Housing Authority of Billings SECTION 8 HOMEOWNERSHIP HANDBOOK For HAB and MDOC Section 8 participants Contact: Carrie Sharp, FSS/Home Ownership Coordinator Housing Authority of Billings 2415 1 st

35% 26% 57% 51% PROFILE. CIty of durham: Assets & opportunity ProfILe. key highlights. ABoUt the ProfILe ASSETS & OPPORTUNITY

CIty of durham: Assets & opportunity ProfILe ASSETS & OPPORTUNITY PROFILE key highlights 35% of Durham County households live in asset poverty Cities have long been thought of as places of opportunity

CIty of durham: Assets & opportunity ProfILe ASSETS & OPPORTUNITY PROFILE key highlights 35% of Durham County households live in asset poverty Cities have long been thought of as places of opportunity

How to stop, avoid, or navigate through a foreclosure

How to stop, avoid, or navigate through a foreclosure Table of contents In this blueprint we ve mapped out the best options for you to receive the help you deserve. 1. Introduction 2. Understanding The

How to stop, avoid, or navigate through a foreclosure Table of contents In this blueprint we ve mapped out the best options for you to receive the help you deserve. 1. Introduction 2. Understanding The

TRENDS IN DELINQUENCIES AND FORECLOSURES IN

TRENDS IN DELINQUENCIES AND FORECLOSURES IN ARIZONA April 2009 Jan Bontrager, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

TRENDS IN DELINQUENCIES AND FORECLOSURES IN ARIZONA April 2009 Jan Bontrager, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

Homeownership Preservation in Maryland

Maryland Department of Housing and Community Development Homeownership Preservation in Maryland A presentation to the Western Maryland 2008 Small Town Symposium and Rural Roundtable April 23, 2008 Martin

Maryland Department of Housing and Community Development Homeownership Preservation in Maryland A presentation to the Western Maryland 2008 Small Town Symposium and Rural Roundtable April 23, 2008 Martin

Instructions for Completing the Short Sale Package. Send Ocwen the completed package and supporting documentation

Instructions for Completing the Short Sale Package Step 1 Complete all the enclosed attachments Exhibit G Borrowers Response package Step 2 Send Ocwen the completed package and supporting documentation

Instructions for Completing the Short Sale Package Step 1 Complete all the enclosed attachments Exhibit G Borrowers Response package Step 2 Send Ocwen the completed package and supporting documentation

EARLY DELINQUENCY INTERVENTION WORKBOOK

EARLY DELINQUENCY INTERVENTION WORKBOOK If you are having financial difficulties, being able to maintain a mortgage payment can be stressful. In such trying times, it can be hard to make rational decisions

EARLY DELINQUENCY INTERVENTION WORKBOOK If you are having financial difficulties, being able to maintain a mortgage payment can be stressful. In such trying times, it can be hard to make rational decisions

Short Sales. Vice President. Lincoln, Nebraska April 12, 2011

Short Sales A guide to working with Wells Fargo Abel Fregoso, Jr Vice President National Field Short Sales Manager Lincoln, Nebraska April 12, 2011 Strategic Partnership Wells Fargo and Our REALTOR Partners

Short Sales A guide to working with Wells Fargo Abel Fregoso, Jr Vice President National Field Short Sales Manager Lincoln, Nebraska April 12, 2011 Strategic Partnership Wells Fargo and Our REALTOR Partners

TRENDS IN DELINQUENCIES

TRENDS IN DELINQUENCIES AND FORECLOSURES IN UTAH January 2009 Jan Bontrager, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

TRENDS IN DELINQUENCIES AND FORECLOSURES IN UTAH January 2009 Jan Bontrager, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

Houston Housing Authority HOMEOWNERSHIP PROGRAM PLAN

Houston Housing Authority HOMEOWNERSHIP PROGRAM PLAN Revised June 2017 Houston Housing Authority HOUSING CHOICE VOUCHER HOMEOWNERSHIP PROGRAM PROGRAM GUIDE TABLES OF CONTENTS Program Description Eligibility

Houston Housing Authority HOMEOWNERSHIP PROGRAM PLAN Revised June 2017 Houston Housing Authority HOUSING CHOICE VOUCHER HOMEOWNERSHIP PROGRAM PROGRAM GUIDE TABLES OF CONTENTS Program Description Eligibility

The Home Ownership Preservation Initiative in Chicago: Reducing Foreclosures through Strategic Partnerships

WNERSH RESERVATN NTATVE The Home wnership reservation nitiative in Chicago: Reducing Foreclosures through Strategic artnerships WNERSH RESERVATN NTATVE Who is NHS? The mission of NHS is to help neighborhoods

WNERSH RESERVATN NTATVE The Home wnership reservation nitiative in Chicago: Reducing Foreclosures through Strategic artnerships WNERSH RESERVATN NTATVE Who is NHS? The mission of NHS is to help neighborhoods

NEIGHBORHOOD HOUSING & DEVELOPMENT CORPORATION 633 NW 8 TH AVE. GAINESVILLE, FL TELEPHONE (352) FAX (352)

FAX (352)") NEIGHBORHOOD HOUSING & DEVELOPMENT CORPORATION 633 NW 8 TH AVE. GAINESVILLE, FL 32601 TELEPHONE (352)380-9119 FAX (352)380-9170 WWW.GNHDC.ORG Dear Homeowner, We re so glad you took that tough first step

NEIGHBORHOOD HOUSING & DEVELOPMENT CORPORATION 633 NW 8 TH AVE. GAINESVILLE, FL 32601 TELEPHONE (352)380-9119 FAX (352)380-9170 WWW.GNHDC.ORG Dear Homeowner, We re so glad you took that tough first step

TRENDS IN DELINQUENCIES AND FORECLOSURES IN

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO April 2009 Craig Nolte, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

TRENDS IN DELINQUENCIES AND FORECLOSURES IN IDAHO April 2009 Craig Nolte, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

Early Delinquency Intervention Workbook

Early Delinquency Intervention Workbook If you are having financial difficulties, being able to maintain a mortgage payment can be stressful. In such trying times, it can be hard to make rational decisions

Early Delinquency Intervention Workbook If you are having financial difficulties, being able to maintain a mortgage payment can be stressful. In such trying times, it can be hard to make rational decisions

HOPE NOW: Mortgage Servicers Completed 850,000 Loan Modifications for Homeowners in 2012

February 7, 2013 Media Contact: Brad Dwin (410) 303-6391 brad@hopenow.com HOPE NOW: Mortgage Servicers Completed 850,000 Loan Modifications for Homeowners in 2012 Short Sales Top 420,000 for the Year (WASHINGTON,

February 7, 2013 Media Contact: Brad Dwin (410) 303-6391 brad@hopenow.com HOPE NOW: Mortgage Servicers Completed 850,000 Loan Modifications for Homeowners in 2012 Short Sales Top 420,000 for the Year (WASHINGTON,

The Foreclosure Crisis in NYC: Patterns, Origins, and Solutions. Ingrid Gould Ellen

The Foreclosure Crisis in NYC: Patterns, Origins, and Solutions Ingrid Gould Ellen Reasons for Rise in Foreclosures Risky underwriting Over-leveraged borrowers High debt to income ratios Economic downturn

The Foreclosure Crisis in NYC: Patterns, Origins, and Solutions Ingrid Gould Ellen Reasons for Rise in Foreclosures Risky underwriting Over-leveraged borrowers High debt to income ratios Economic downturn

THE NSP SUBSTANTIAL AMENDMENT

THE NSP SUBSTANTIAL AMENDMENT Jurisdiction(s): _Pasco County (identify lead entity in case of joint agreements) Jurisdiction Web Address: www.pascocountyfl.net (URL where NSP Substantial Amendment materials

THE NSP SUBSTANTIAL AMENDMENT Jurisdiction(s): _Pasco County (identify lead entity in case of joint agreements) Jurisdiction Web Address: www.pascocountyfl.net (URL where NSP Substantial Amendment materials

TRENDS IN DELINQUENCIES AND FORECLOSURES IN CALIFORNIA

TRENDS IN DELINQUENCIES AND FORECLOSURES IN CALIFORNIA April 2009 Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures House

TRENDS IN DELINQUENCIES AND FORECLOSURES IN CALIFORNIA April 2009 Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures House

l b l d b 5. What is the document submission deadline? What will I need to provide?

Frequently Asked Questions ATTENTION HOMEOWNERS IMPORTANT PROGRAM UPDATE Applications for Florida Hardest-Hit Fund Programs will close January 31, 2018. If you have not yet completed the application process

Frequently Asked Questions ATTENTION HOMEOWNERS IMPORTANT PROGRAM UPDATE Applications for Florida Hardest-Hit Fund Programs will close January 31, 2018. If you have not yet completed the application process

Information on Avoiding Foreclosure

Information on Avoiding Foreclosure Learn more About Options to Avoid Foreclosure The variety of options summarized below may help you keep your home. For example, you may be eligible to modify your mortgage,

Information on Avoiding Foreclosure Learn more About Options to Avoid Foreclosure The variety of options summarized below may help you keep your home. For example, you may be eligible to modify your mortgage,

Foreclosure Prevention Counseling Workshop

Foreclosure Prevention Counseling Workshop Counselor role and process The counselor will look at all of your documents to assess your situation The counselor will lay out all of your options The counselor

Foreclosure Prevention Counseling Workshop Counselor role and process The counselor will look at all of your documents to assess your situation The counselor will lay out all of your options The counselor

Seller Advisory. Short Sale TABLE OF CONTENTS. 1 Before Proceeding with a Short Sale. 3 Options other than Short Sale. 5 Short Sale Considerations

TABLE OF CONTENTS 1 Before Proceeding with a Short Sale 1 Understand a Lender s Options upon Loan Default 1 Be Aware of Predatory Rescue Scams & Short Sale Fraud 2 Report Suspected Scams 2 Contact a free

TABLE OF CONTENTS 1 Before Proceeding with a Short Sale 1 Understand a Lender s Options upon Loan Default 1 Be Aware of Predatory Rescue Scams & Short Sale Fraud 2 Report Suspected Scams 2 Contact a free

Testimony of Dean Baker. Before the Subcommittee on Housing and Community Opportunity of the House Financial Services Committee

Testimony of Dean Baker Before the Subcommittee on Housing and Community Opportunity of the House Financial Services Committee Hearing on the Recently Announced Revisions to the Home Affordable Modification

Testimony of Dean Baker Before the Subcommittee on Housing and Community Opportunity of the House Financial Services Committee Hearing on the Recently Announced Revisions to the Home Affordable Modification

THE HOUSING & ECONOMIC RECOVERY ACT OF 2008 H.R (DETAILED SUMMARY) DIVISION A. TITLE I REFORM OF REGULATION OF ENTERPRISES

DIVISION A. TITLE I REFORM OF REGULATION OF ENTERPRISES") THE HOUSING & ECONOMIC RECOVERY ACT OF 2008 H.R. 3221 (DETAILED SUMMARY) DIVISION A. TITLE I REFORM OF REGULATION OF ENTERPRISES Subtitle A Improvement of Safety and Soundness Supervision. Establishes

THE HOUSING & ECONOMIC RECOVERY ACT OF 2008 H.R. 3221 (DETAILED SUMMARY) DIVISION A. TITLE I REFORM OF REGULATION OF ENTERPRISES Subtitle A Improvement of Safety and Soundness Supervision. Establishes

The Mortgage Resolution Fund

The Mortgage Resolution Fund Creating a Safety Net for Delinquent Homeowners and Distressed Communities Florida Housing Finance Corporation Board of Directors October 14, 2011 Overview MRF Mission Distressed

The Mortgage Resolution Fund Creating a Safety Net for Delinquent Homeowners and Distressed Communities Florida Housing Finance Corporation Board of Directors October 14, 2011 Overview MRF Mission Distressed

An Attorney s Options for Handling Clients in Trouble with Real Estate. Aka: Forbearance to Bankruptcy and Everything in Between

An Attorney s Options for Handling Clients in Trouble with Real Estate Aka: Forbearance to Bankruptcy and Everything in Between Erica Crohn Minchella ~ Attorney at Law 7538 St. Louis Ave Skokie, IL 60076

An Attorney s Options for Handling Clients in Trouble with Real Estate Aka: Forbearance to Bankruptcy and Everything in Between Erica Crohn Minchella ~ Attorney at Law 7538 St. Louis Ave Skokie, IL 60076

MHANY MANAGEMENT, INC. FIRST TIME HOMEBUYER/REFINANCE PROGRAM

MHANY MANAGEMENT, INC. FIRST TIME HOMEBUYER/REFINANCE PROGRAM MHANY Management, Inc. (MHANY) helps low and moderate income individuals and families so they can obtain and keep affordable, stable, safe,

MHANY MANAGEMENT, INC. FIRST TIME HOMEBUYER/REFINANCE PROGRAM MHANY Management, Inc. (MHANY) helps low and moderate income individuals and families so they can obtain and keep affordable, stable, safe,

The Five-Point Plan. Creating a Sustainable Path to Minority Homeownership

The Five-Point Plan Creating a Sustainable Path to Minority Homeownership The National Association of Hispanic Real Estate Professionals, The Asian Real Estate Association of America and the National Association

The Five-Point Plan Creating a Sustainable Path to Minority Homeownership The National Association of Hispanic Real Estate Professionals, The Asian Real Estate Association of America and the National Association

HOME SWEET HOME COMMUNITY REDEVELOPMENT CORPORATION

Customer Intake Form CUSTOMER 1 P age HOME SWEET HOME COMMUNITY REDEVELOPMENT CORPORATION Please print Name: Address: City: State: Zip Code: Date of Birth: / / Social Security: - - Gender: Male Female

Customer Intake Form CUSTOMER 1 P age HOME SWEET HOME COMMUNITY REDEVELOPMENT CORPORATION Please print Name: Address: City: State: Zip Code: Date of Birth: / / Social Security: - - Gender: Male Female

INTRODUCTION. Check out our 7 Steps to Home Ownership overview page, then dive in to our guide to Randolph s ideal mortgage experience.

INTRODUCTION When it comes to referring your valued clients to a mortgage lender, we know you have choices. At Randolph Savings Bank we strive to establish your confidence in us, build long term relationships,

INTRODUCTION When it comes to referring your valued clients to a mortgage lender, we know you have choices. At Randolph Savings Bank we strive to establish your confidence in us, build long term relationships,

HOMEBUYER WORKSHOP REGISTRATION FORM

HOMEBUYER WORKSHOP REGISTRATION FORM Organization: Workshop location: Workshop Date(s): Instructions: Please fill out as completely as possible. Home Buyer Name: (Please print) First MI Last Address: Zip:

HOMEBUYER WORKSHOP REGISTRATION FORM Organization: Workshop location: Workshop Date(s): Instructions: Please fill out as completely as possible. Home Buyer Name: (Please print) First MI Last Address: Zip:

SECTION 8 HOMEOWNERSHIP PROGRAM

SECTION 8 HOMEOWNERSHIP PROGRAM 1.0 INTRODUCTION This administrative plan has been prepared as an addendum to the existing Section 8 Administrative Plan. This Plan addresses those areas that are pertinent

SECTION 8 HOMEOWNERSHIP PROGRAM 1.0 INTRODUCTION This administrative plan has been prepared as an addendum to the existing Section 8 Administrative Plan. This Plan addresses those areas that are pertinent

Making Home Affordable

Making Home Affordable Working Together to Help Homeowners Response to the Crisis MHA is part of Administration approach to promoting stability for housing market, homeowners. Homeowner Affordability and

Making Home Affordable Working Together to Help Homeowners Response to the Crisis MHA is part of Administration approach to promoting stability for housing market, homeowners. Homeowner Affordability and

HOME SWEET HOME COMMUNITY REDEVELOPMENT CORPORATION Rebuilding our community one day at a time Customer Intake Form

Customer Intake Form CUSTOMER Please print Name: City: State: Zip Code: Date of Birth: / / Social Security: - - Gender: Male Female Handicapped? Yes or No Home: ( ) - Work: ( ) - Cell: ( ) - E-mail: Race

Customer Intake Form CUSTOMER Please print Name: City: State: Zip Code: Date of Birth: / / Social Security: - - Gender: Male Female Handicapped? Yes or No Home: ( ) - Work: ( ) - Cell: ( ) - E-mail: Race

H.E.L.P. COMMUNITY DEVELOPMENT CORP. Foreclosure Counseling Program DOCUMENT CHECKLIST

H.E.L.P. COMMUNITY DEVELOPMENT CORP. Foreclosure Counseling Program DOCUMENT CHECKLIST PLEASE COMPLETE ITEMS 1 AND 2 BELOW AND FAX OR MAIL BACK TO OUR OFFICE. Complete the INTAKE FORMS as thoroughly as

H.E.L.P. COMMUNITY DEVELOPMENT CORP. Foreclosure Counseling Program DOCUMENT CHECKLIST PLEASE COMPLETE ITEMS 1 AND 2 BELOW AND FAX OR MAIL BACK TO OUR OFFICE. Complete the INTAKE FORMS as thoroughly as

Procedures on Submitting a Loan Application:

Procedures on Submitting a Loan Application: The first step in the mortgage process is to complete the following loan application and credit authorization. The loan application, which provides your personal

Procedures on Submitting a Loan Application: The first step in the mortgage process is to complete the following loan application and credit authorization. The loan application, which provides your personal

Foreclosure. Counseling Program Report. Prepared by Karen Duggleby, MSW, LISW Minnesota Homeownership Center

Foreclosure 2014 Counseling Program Report Prepared by Karen Duggleby, MSW, LISW Minnesota Homeownership Center Acknowledgements The Minnesota Homeownership Center is profoundly grateful for the dedicated

Foreclosure 2014 Counseling Program Report Prepared by Karen Duggleby, MSW, LISW Minnesota Homeownership Center Acknowledgements The Minnesota Homeownership Center is profoundly grateful for the dedicated

HOPE NOW Alliance. Statement for the Record. Committee on Oversight and Government Reform. U.S. House of Representatives. Hearing

HOPE NOW Alliance Statement for the Record Committee on Oversight and Government Reform U.S. House of Representatives Hearing Foreclosure Prevention Part II: Are Loan Servicers Honoring Their Commitments

HOPE NOW Alliance Statement for the Record Committee on Oversight and Government Reform U.S. House of Representatives Hearing Foreclosure Prevention Part II: Are Loan Servicers Honoring Their Commitments

Fannie Mae Reports Third-Quarter 2011 Results

Contact: Number: Katherine Constantinou 202-752-5403 5552a Resource Center: 1-800-732-6643 Date: November 8, 2011 Fannie Mae Reports Third-Quarter 2011 Results Company Focused on Providing Liquidity to

Contact: Number: Katherine Constantinou 202-752-5403 5552a Resource Center: 1-800-732-6643 Date: November 8, 2011 Fannie Mae Reports Third-Quarter 2011 Results Company Focused on Providing Liquidity to

STEPS to getting an affordable home loan

4 STEPS to getting an affordable home loan 1 www.idahohousing.com 1 Start the process by finding a lender. Before you start house hunting, it s a good idea to pre-qualify for financing so you can be certain

4 STEPS to getting an affordable home loan 1 www.idahohousing.com 1 Start the process by finding a lender. Before you start house hunting, it s a good idea to pre-qualify for financing so you can be certain

One Industry s Risk is Another Community s Loss: The Impact of Clustered Mortgage Foreclosures on Neighborhood Property Values in Philadelphia

One Industry s Risk is Another Community s Loss: The Impact of Clustered Mortgage Foreclosures on Neighborhood Property Values in Philadelphia Presentation before the Federal Reserve Bank of Philadelphia

One Industry s Risk is Another Community s Loss: The Impact of Clustered Mortgage Foreclosures on Neighborhood Property Values in Philadelphia Presentation before the Federal Reserve Bank of Philadelphia

HUD NATIONAL SERVICING CENTER

HUD NATIONAL SERVICING CENTER Revisions to FHA's Loss Mitigation Home Disposition Options Preforeclosure Sale & Deed-in-Lieu Working Together to Help Families Stay in Their Homes Presented by : FHA National

HUD NATIONAL SERVICING CENTER Revisions to FHA's Loss Mitigation Home Disposition Options Preforeclosure Sale & Deed-in-Lieu Working Together to Help Families Stay in Their Homes Presented by : FHA National

[Address of Borrower] [Loan #] [Date] RE: Acknowledgement of Request for Short Sale

![[Address of Borrower] [Loan #] [Date] RE: Acknowledgement of Request for Short Sale](/thumbs/90/103076486.jpg "[Address of Borrower] [Loan #] [Date] RE: Acknowledgement of Request for Short Sale") [Name of Servicer] [Address of Servicer] [Loan #] [Servicer FAX] [Servicer Email] [Name of Borrower] [Name of Co-Borrower] [Address of Borrower] [Borrower Phone] [Borrower Email] [Date] RE: Acknowledgement

[Name of Servicer] [Address of Servicer] [Loan #] [Servicer FAX] [Servicer Email] [Name of Borrower] [Name of Co-Borrower] [Address of Borrower] [Borrower Phone] [Borrower Email] [Date] RE: Acknowledgement

Dear Prospective Homeowner,

Dear Prospective Homeowner, Thank you for expressing an interest in partnering with Habitat for Humanity to help build and occupy a new home. The application process of our homeownership program is detailed

Dear Prospective Homeowner, Thank you for expressing an interest in partnering with Habitat for Humanity to help build and occupy a new home. The application process of our homeownership program is detailed

Financial Literacy and Your Financial Security. Academic Staff Institute April 1, 2014

Financial Literacy and Your Financial Security Academic Staff Institute April 1, 2014 What Does Financial Security Mean For You? What makes for Financial Security? Common Survey Question Let s say you

Financial Literacy and Your Financial Security Academic Staff Institute April 1, 2014 What Does Financial Security Mean For You? What makes for Financial Security? Common Survey Question Let s say you

How To Sell Your House FAST - Quick Sale

How To Sell Your House FAST - Quick Sale Tips for selling your house fast Presented By: Firstname Lastname Phone: (469)-573-4965 Page 1 Page 2 In today's real estate market, more houses are sitting on

How To Sell Your House FAST - Quick Sale Tips for selling your house fast Presented By: Firstname Lastname Phone: (469)-573-4965 Page 1 Page 2 In today's real estate market, more houses are sitting on

Fannie Mae Reports Net Income of $5.1 Billion for Second Quarter 2012

Contact: Pete Bakel Resource Center: 1-800-732-6643 202-752-2034 Date: August 8, 2012 Fannie Mae Reports Net Income of $5.1 Billion for Second Quarter 2012 Net Income of $7.8 Billion for First Half 2012

Contact: Pete Bakel Resource Center: 1-800-732-6643 202-752-2034 Date: August 8, 2012 Fannie Mae Reports Net Income of $5.1 Billion for Second Quarter 2012 Net Income of $7.8 Billion for First Half 2012

TRIP, NeighborWorks HomeOwnership Center & Rensselaer County Housing Resources

TRIP, NeighborWorks HomeOwnership Center & Rensselaer County Housing Resources Information for First Time Home Buyers 2015 Our History Troy Rehabilitation & Improvement Program (TRIP), Inc was established

TRIP, NeighborWorks HomeOwnership Center & Rensselaer County Housing Resources Information for First Time Home Buyers 2015 Our History Troy Rehabilitation & Improvement Program (TRIP), Inc was established

Uniform Residential Loan Application

This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable. Co-Borrower information must

This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable. Co-Borrower information must

M O D I F I C AT I O N PA M P H L E T

THE STATE BAR OF TEXAS LOAN M O D I F I C AT I O N SCAM PA M P H L E T As the number of foreclosures grows, many thieves are swindling money from homeowners by preying upon fears of losing a home. The

THE STATE BAR OF TEXAS LOAN M O D I F I C AT I O N SCAM PA M P H L E T As the number of foreclosures grows, many thieves are swindling money from homeowners by preying upon fears of losing a home. The

This Month in Real Estate

Keller Williams Research This Month in Real Estate Released: December 4, 2009 Commentary. 2 The Numbers That Drive Real Estate 3 Recent Government Action. 9 Topics for Buyers and Sellers. 15 1 Steps to

Keller Williams Research This Month in Real Estate Released: December 4, 2009 Commentary. 2 The Numbers That Drive Real Estate 3 Recent Government Action. 9 Topics for Buyers and Sellers. 15 1 Steps to

Uniform Residential Loan Application

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as or, as applicable. information

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as or, as applicable. information

The Perfect Storm. Subprime crisis. How the foreclosure process works... pg. 2. FORECLOSURE SCAMS How to avoid predators... pg. 3

Subprime crisis The Perfect Storm How the foreclosure process works... pg. FORECLOSURE SCAMS How to avoid predators... pg. WHIRLWIND FORECLOSURE SALE 5 steps of buying a foreclosed property... pg. SEEKING

Subprime crisis The Perfect Storm How the foreclosure process works... pg. FORECLOSURE SCAMS How to avoid predators... pg. WHIRLWIND FORECLOSURE SALE 5 steps of buying a foreclosed property... pg. SEEKING

Freddie Mac Issuer Session. STACR and Other Credit Risk Transfer Updates: Servicing and REO Disposition Practices

Freddie Mac Issuer Session STACR and Other Credit Risk Transfer Updates: Servicing and REO Disposition Practices September 17, 2015 STACR and Other Credit Risk Transfer Updates: Servicing and REO Disposition

Freddie Mac Issuer Session STACR and Other Credit Risk Transfer Updates: Servicing and REO Disposition Practices September 17, 2015 STACR and Other Credit Risk Transfer Updates: Servicing and REO Disposition

Jan. 8, 2009 Page 1 of 6. C.A.R. Mortgage Update

C.A.R. Mortgage Update This week s C.A.R. Mortgage Update contains information about FHA loans, falling mortgage rates, downpayment assistance programs (DAPs), jumbo loans, mortgage securities, and IndyMac

C.A.R. Mortgage Update This week s C.A.R. Mortgage Update contains information about FHA loans, falling mortgage rates, downpayment assistance programs (DAPs), jumbo loans, mortgage securities, and IndyMac

Uniform Residential Loan Application

This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as or Co-, as applicable. Co- information must also be provided (and

This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as or Co-, as applicable. Co- information must also be provided (and

Housing Risk. Policy Issues & Responses

Housing Risk Policy Issues & Responses Fifth Annual Risk Management Conference Federal Reserve Bank of Chicago April 11, 2012 Bill Longbrake Executive in Residence Robert H. Smith School of Business, University

Housing Risk Policy Issues & Responses Fifth Annual Risk Management Conference Federal Reserve Bank of Chicago April 11, 2012 Bill Longbrake Executive in Residence Robert H. Smith School of Business, University

1. Host series of Pre foreclosure workshops, housing fairs, homeownership education classes, and home repair seminars

Pre-Purchase/ Post-Purchase education and counseling is a vital part of the new home buyer education process because it supports successful long-term self-sufficiency. Rhodes Porter understands the first

Pre-Purchase/ Post-Purchase education and counseling is a vital part of the new home buyer education process because it supports successful long-term self-sufficiency. Rhodes Porter understands the first

Uniform Residential Loan Application

This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable. Co-Borrower information must

This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable. Co-Borrower information must

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac Hearing of the U.S. Senate Committee on Banking, Housing and Urban Affairs Chairman Dodd, Ranking

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac Hearing of the U.S. Senate Committee on Banking, Housing and Urban Affairs Chairman Dodd, Ranking

CITY OF BOCA RATON SHIP APPLICATION PACKAGE WE ARE ACCEPTING SHIP APPLICATIONS ON AN ONGOING BASIS, UNTIL FURTHER NOTICE.

Courtesy of http://www.downpaymentsolutions.com CITY OF BOCA RATON SHIP APPLICATION PACKAGE WE ARE ACCEPTING SHIP APPLICATIONS ON AN ONGOING BASIS, UNTIL FURTHER NOTICE. BEFORE SUBMITTING YOUR APPLICATION,

Courtesy of http://www.downpaymentsolutions.com CITY OF BOCA RATON SHIP APPLICATION PACKAGE WE ARE ACCEPTING SHIP APPLICATIONS ON AN ONGOING BASIS, UNTIL FURTHER NOTICE. BEFORE SUBMITTING YOUR APPLICATION,

Foreclosure Prevention Process

NHS of the Fox Valley One American Way Elgin, IL 60120 (847) 695-0399 (847) 695-0711 foxvalleyinfo@nhschicago.org Foreclosure Prevention Process How to OBTAIN a one-to-one consultation with a HUD-certified

NHS of the Fox Valley One American Way Elgin, IL 60120 (847) 695-0399 (847) 695-0711 foxvalleyinfo@nhschicago.org Foreclosure Prevention Process How to OBTAIN a one-to-one consultation with a HUD-certified

Counseling Agreement, Privacy Policy, and Conflict of Interest Disclosure Statement

Counseling Agreement, Privacy Policy, and Conflict of Interest Disclosure Statement 1. I understand that Fifth Ward CRC provides foreclosure mitigation counseling after which I will receive a written action

Counseling Agreement, Privacy Policy, and Conflict of Interest Disclosure Statement 1. I understand that Fifth Ward CRC provides foreclosure mitigation counseling after which I will receive a written action

Co-Borrower. I. TYPE OF MORTGAGE AND TERMS OF LOAN Other (explain): Agency Case Number. Amortization Type: Fixed Rate GPM

: Agency Case Number. Amortization Type: Fixed Rate GPM") This application is designed to be completed by the applicant(s) with the Lender's assistance. Applicants should complete this form as "" or "," as applicable. information must also be provided (and the

This application is designed to be completed by the applicant(s) with the Lender's assistance. Applicants should complete this form as "" or "," as applicable. information must also be provided (and the

Uniform Residential Loan Application

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as or Co-, as applicable. Co- information

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as or Co-, as applicable. Co- information

Supplemental Directive November 3, Home Affordable Modification Program Borrower Notices

Supplemental Directive 09-08 November 3, 2009 Home Affordable Modification Program Borrower Notices Background In Supplemental Directive 09-01, the Treasury Department (Treasury) announced the eligibility,

Supplemental Directive 09-08 November 3, 2009 Home Affordable Modification Program Borrower Notices Background In Supplemental Directive 09-01, the Treasury Department (Treasury) announced the eligibility,

October 22, Joseph A. Smith Office of Mortgage Settlement Oversight 301 Fayetteville St., Suite 1801 Raleigh, NC Via electronic mail

October 22, 2012 Joseph A. Smith Office of Mortgage Settlement Oversight 301 Fayetteville St., Suite 1801 Raleigh, NC 27601 Via electronic mail Dear Mr. Smith: Thank you again for speaking with members

October 22, 2012 Joseph A. Smith Office of Mortgage Settlement Oversight 301 Fayetteville St., Suite 1801 Raleigh, NC 27601 Via electronic mail Dear Mr. Smith: Thank you again for speaking with members

KEY REASONS FOR PROPERTY OWNERS TO DO A SHORT SALE:

KEY REASONS FOR PROPERTY OWNERS TO DO A SHORT SALE: to minimize the potential damage to their credit that a foreclosure or bankruptcy might cause to maintain control of the sale of their home including

KEY REASONS FOR PROPERTY OWNERS TO DO A SHORT SALE: to minimize the potential damage to their credit that a foreclosure or bankruptcy might cause to maintain control of the sale of their home including

Uniform Residential Loan Application

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable.

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender s assistance. Applicants should complete this form as Borrower or Co-Borrower, as applicable.

Short Sales/Foreclosures/REOs

Short Sales/Foreclosures/REOs In today s economic times the occurrence of Short Sales, Foreclosures and REOs has become common. Below is a description of these property statuses. Short Sale: A short sale

Short Sales/Foreclosures/REOs In today s economic times the occurrence of Short Sales, Foreclosures and REOs has become common. Below is a description of these property statuses. Short Sale: A short sale