Assumptions, Mistakes, Successes, and Moving Forward: An Empirical Analysis of Foreclosures in North Minneapolis and Foreclosure Policies

|

|

|

- Milton Jennings

- 5 years ago

- Views:

Transcription

1 Assumptions, Mistakes, Successes, and Moving Forward: An Empirical Analysis of Foreclosures in North Minneapolis and Foreclosure Policies CURA Housing Forum Friday, December 18, 2009

2 Thanks and Disclaimers Thank you to Professor Prentiss Cox and Professor Myron Orfield at the University of Minnesota Law School and Professor Jeff Crump. Some of the data presented here today and cited in my paper on this topic was compiled by them, but the analysis and errors are mine. Thank you to the Kirwin Institute on Race for the Study of Race and Ethnicity at Ohio State University for providing a research grant to write this paper and allowing me to serve as an advisory board member.

3 A story

4

5

6

7

8

9 A story as an illustration

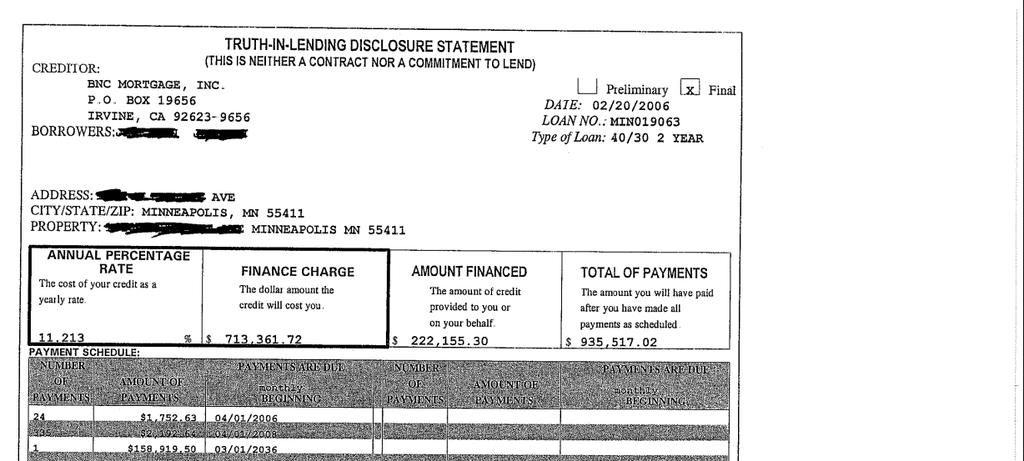

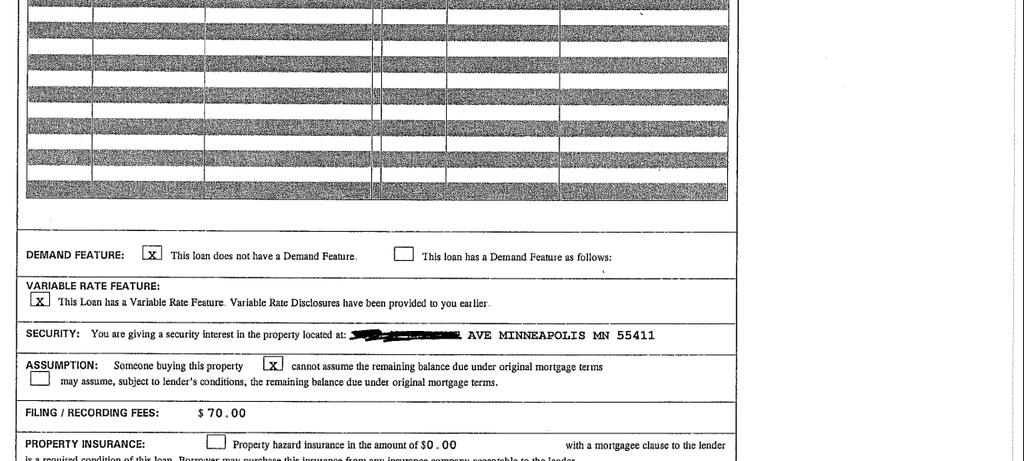

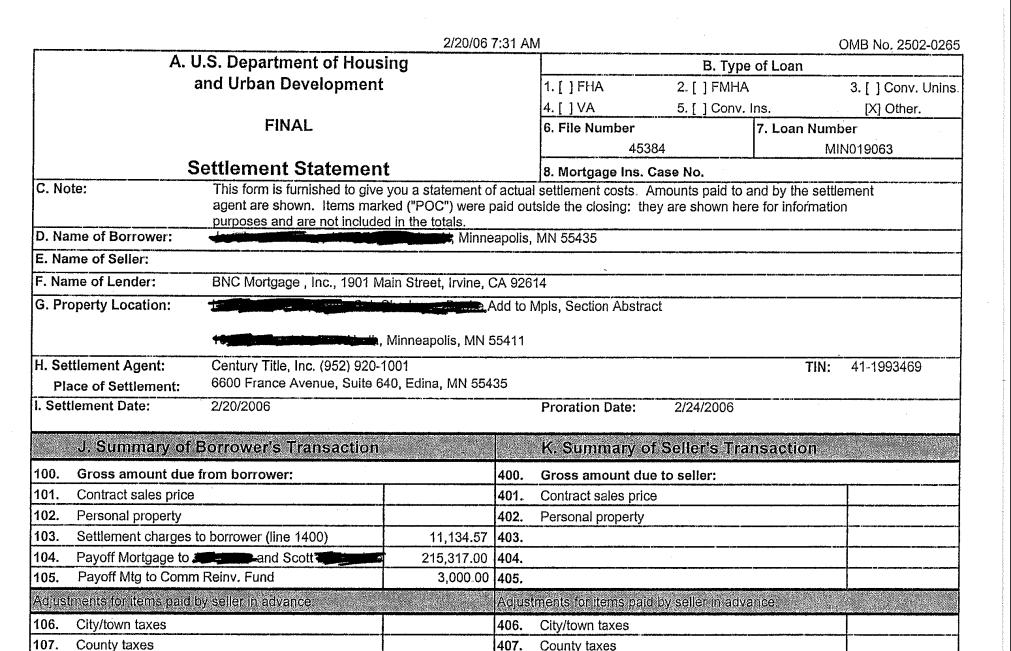

10 Non-Bank Lender owned by Wall Street Investment Firm Person of Color in North Minneapolis Rented part of house to elderly family member Undisclosed/Wrongly Disclosed Mortgage Terms Exorbitant broker and closing fees Mortgage failed within a year

11 Assumptions, Mistakes, and Successes

12 Assumption and Mistake #1: The Foreclosure and Economic Crisis Is Over

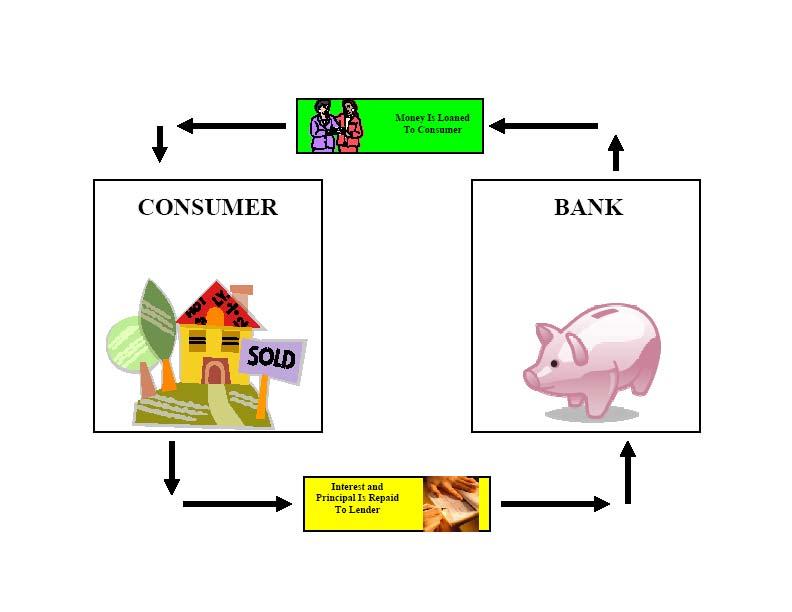

13 $15-$30 $30 billion of ARMs will adjust per month every month until 2012 Congressional Oversight Panel Report (October 9, 2009)

14 National Mortgage Delinquency Rates Congressional Oversight Panel Report (October 9, 2009)

15 National Foreclosure Rates Congressional Oversight Panel Report (October 9, 2009)

16 Unemployment Rate Congressional Oversight Panel Report (October 9, 2009)

17 Assumption and Mistake #2: Lenders Act Rationally

18 Why would a lender do something that is not in its own best interest?

19 Rise of the Non-Bank Lender and Wall Street Investment Firms

20 Traditional Banking Model

21 The New Model

22 Rise of Sub-Prime Lending

23 Institute on Race and Poverty, Communities in Crisis: Race and Mortgage Lending In The Twin Cities at p. 11 (February 2009)

24 Dramatic Change In Lending Patterns and Underwriting 2006 Jumbo+ 17.0% Subprime 22.0% Conform 33.0% Home equity 10.0% Alt-A 18.0%

25 Assumption and Mistake #3: Lenders Properly Underwrote Loans

26 Assumption affects how we modify loans and counsel homeowners. Initial efforts were focused on teaser rate adjustments and freezing adjustable rate mortgage interest rates.

27 Toxic Mortgages Quick To Fail The mean number of months from the date of origination to the date of foreclosure was approximately 21 months for mortgage loans originated in North Minneapolis, meaning that most borrowers were foreclosed upon within two years of origination. 26% of the foreclosed mortgage loans were foreclosed upon less than a year after origination, which meant that the foreclosure process began, at most, nine months after origination.

28 Assumption and Mistake #4: Mortgage Servicers Act Rationally

29 A study released by the Federal Reserve Board in Boston found that less than 8% of seriously delinquent loans received any loan modification. Manuel Adelino, Kristopher Gerardi, and Paul S. Willen, Why Don t t Lenders Renegotiate Home Mortgages? Redefaults, Self-Cures, and Securitization, Public Policy Discussion Papers No , 04, Federal Reserve Bank of Boston (July 6, 2009)

30 More than 51% of modified mortgages resulted in a higher monthly payment; which the vast majority re-defaulted within a year. Roberto G. Quercia, Lei Ding, and Janneke Ratcliffe, Loan Modifications and Redefault Risk: An Examination of Short-term term Impact, Center for Community Capital, The University of North Carolina at Chapel Hill (March See also Office of the Comptroller of the Currency, Comptroller Dugan Highlights Re-Default Rates on Modified Loans, Press Release (December 8, 2008) last visited September 11,

31 Tracking 100 Minneapolis foreclosures The difference between the amount that a lender purchased a property for at the Sheriff s s Sale auction, typically the amount owed on the mortgage loan, and the later sale price was usually a loss of $65,039 (average) or $77,424 (median). As a percentage, the lender later sold the properties for a loss of 25% (average) to a loss of 49% (median).

32 Assumption and Mistake #5: Focus just on homeowners

33 The findings of a University of Minnesota study were that over 60% of the properties that were foreclosed upon were non-homesteaded, exceeding the proportion of rental property in the neighborhood. Yet, the vast majority of initial foreclosure prevention efforts, both local and national, were designed only to help homeowners with little or no mention of renters. Ryan Allen, The Unraveling of the American Dream: Foreclosures in the Immigrant Community of Minneapolis,, Report to Minneapolis Public Schools REA Division at 3 (March 2009) am.pdf;steve Perry, Who s s Getting Hurt? UM Study crunches the numbers on foreclosures in Minneapolis, MinnPost (Feb. 19, 2009)

34 Assumption and Mistake #6: Misapropriaton of Resources Away From Areas of Greatest Need

35 Housing and Economic Recovery Act of Neighborhood Stabilization Program By far the largest recovery program created by the federal government, relating to the vacant and abandoned houses created by the foreclosure crisis, is the Housing and Economic Recovery Act of Specifically, the section of this Act relating to the creation and distribution of National Stabilization Program ( NSP( NSP ) funds. Approximately $6 billion of NSP grants were distributed to states across the country, and the states were then required to give priority emphasis and consideration to those areas with the greatest need. ---Housing and Economic Recovery Act of 2008, P.L , 2301(c)(2) (2008).

36 Funds Not Distributed To Areas of Greatest Need North Minneapolis and certain neighborhoods in Saint Paul have unquestionably u been the State s s most negatively impacted areas by almost any measure, but, based upon the formula developed by the State of Minnesota, at least l $9 million of Minnesota s s $17 million NSP award was automatically directed to other areas s of the state. ($9 million/$100,000 = 90 houses) In fact, the State of Minnesota created its own factor (not suggested or authorized by Congress) to create a formula that is balancing the distribution of funds between the Twin Cities metro area and Greater Minnesota. This balancing is irrelevant to the goal of targeting funds to areas of greatest need, like North Minneapolis, and ignores the reality of the foreclosure crisis

37 VACANT BUILDINGS IN SAINT PAUL Source: Saint Paul Council Research Center

38 Community impact three years later 2700 Penn Ave. N Penn Ave. N Penn Ave. N Penn Ave. N. SOURCE: CPED, Part of presentation originally given by Melissa Manderschied and Elizabeth Ryan, Residential Foreclosures: A Wake Up Call For Real Estate Attorneys (Hennepin County Bar Association, April 26, 2007).

39 Tracking 100 Minneapolis foreclosures The median time from the date of the foreclosure Sheriff s s sale to the date that the property sold to another party was 484 days. Assuming a six month redemption period, it took a lender approximately 304 days or ten months for a property to be sold.

40 Tracking 100 Minneapolis foreclosures 83% of the foreclosed properties had 911 calls post- Sheriff s s Sale. The average number of 911 calls was eight, while the median was five calls per property. The vast majority of 911 calls (74%) occurred after the end of the redemption period when the property was under the control and ownership of either the mortgage loan servicing company or the person who bought the property from the mortgage loan servicing

41 Watch-out for inequitable distribution of stimulus funds. Rather than stimulus funds for transportation being spent where people live (two-thirds thirds of the country lives in large metropolitan areas) urban areas received less than half of transportation stimulus dollars

42

43 Assumption and Mistake #7: Race has nothing to do with it

44 Race by census track Institute on Race and Poverty, Communities in Crisis: Race and Mortgage Lending In The Twin Cities at p. 31 (February 2009)

45 Subprime lending by census track Institute on Race and Poverty, Communities in Crisis: Race and Mortgage Lending In The Twin Cities at p. 32 (February 2009)

46 Foreclosures by census track Institute on Race and Poverty, Communities in Crisis: Race and Mortgage Lending In The Twin Cities at p. 30 (February 2009)

47 A CONCENTRATION OF FORECLOSURES Homes Currently in Foreclosure As Of December 2006 in North Minneapolis

48 Assumption and Mistake #8: The Community Reinvestment Act Did It

49 They Gave your Mortgage to a Less Qualified Minority. In her article, Ms. Coulter argues that the foreclosure and economic crisis was caused by political correctness being forced on the mortgage lending industry in the Clinton era. She then posits that banks were forced to ignore credit scores and lend based on nontraditional measures of credit- worthiness, such as having a good jump shot or having a missing child named Caylee. Ann Coulter, They Gave Your Mortgage to a Less Qualified Minority, HUMAN EVENTS ONLINE, Sept. 24, 2008, available at

50 The most high-risk lending occurred through non-bank lenders that were not even covered by the Community Reinvestment Act. Estimates are that three-quarters of the sub-prime loans that were originated during the real estate boom were originated by non-bank lenders that were not subject to the Community Reinvestment Act and our study of foreclosures in North Minneapolis was consistent with estimate.

51 Most Foreclosures In North Minneapolis Are From Loans Originated By Non-Bank Lenders BNC Mortgage and Argent/Ameriquest originated approximately 29% of mortgage loans foreclosed upon in Over 80% of foreclosed North Minneapolis mortgage loans were originated by lenders who rely heavily, if not exclusively, on independent mortgage brokers facilitating loan transactions for non-bank lenders.

52 Successes Passage of new laws Minnesota Anti-Predatory Lending Act Improved Foreclosure Notices Increase In Renter Protections Inter-Governmental Partnerships Funding For Housing Counselors

53 Bending Toward Justice Determine Where We Are and Assert our Dignity and Worth Identify the basic challenges and structural impediments Develop a program and commit to a path of structural change

MARK IRELAND Foreclosure Relief Law Project, A Program of the Housing Preservation Project PRESENTED BY KIRWAN INSTITUTE

THE FUTURE OF FAIR HOUSING and FAIR CREDIT Sponsored by: W. K. KELLOGG FOUNDATION BENDING TOWARD JUSTICE: AN EMPIRICAL STUDY OF FORECLOSURES IN ONE NEIGHBORHOOD THREE YEARS AFTER IMPACT AND A PROPOSED

THE FUTURE OF FAIR HOUSING and FAIR CREDIT Sponsored by: W. K. KELLOGG FOUNDATION BENDING TOWARD JUSTICE: AN EMPIRICAL STUDY OF FORECLOSURES IN ONE NEIGHBORHOOD THREE YEARS AFTER IMPACT AND A PROPOSED

A Nation of Renters? Promoting Homeownership Post-Crisis. Roberto G. Quercia Kevin A. Park

A Nation of Renters? Promoting Homeownership Post-Crisis Roberto G. Quercia Kevin A. Park 2 Outline of Presentation Why homeownership? The scale of the foreclosure crisis today (20112Q) Mississippi and

A Nation of Renters? Promoting Homeownership Post-Crisis Roberto G. Quercia Kevin A. Park 2 Outline of Presentation Why homeownership? The scale of the foreclosure crisis today (20112Q) Mississippi and

In the first three months of 2007, there

Subprime Lending and Foreclosure in Hennepin and Ramsey Counties by Jeff Crump In the first three months of 2007, there were 678 foreclosure sales in the city of Minneapolis, an increase of more than 100%

Subprime Lending and Foreclosure in Hennepin and Ramsey Counties by Jeff Crump In the first three months of 2007, there were 678 foreclosure sales in the city of Minneapolis, an increase of more than 100%

Increasing homeownership among

Subprime Lending and Foreclosure in Hennepin and Ramsey Counties: An Empirical Analysis by Jeff Crump Increasing homeownership among low-income and minority communities is a major goal of housing policy

Subprime Lending and Foreclosure in Hennepin and Ramsey Counties: An Empirical Analysis by Jeff Crump Increasing homeownership among low-income and minority communities is a major goal of housing policy

Foreclosure Delay and Consumer Credit Performance

Foreclosure Delay and Consumer Credit Performance May 10, 2013 Paul Calem, Julapa Jagtiani & William W. Lang Federal Reserve Bank of Philadelphia The views expressed are those of the authors and do not

Foreclosure Delay and Consumer Credit Performance May 10, 2013 Paul Calem, Julapa Jagtiani & William W. Lang Federal Reserve Bank of Philadelphia The views expressed are those of the authors and do not

THE NSP SUBSTANTIAL AMENDMENT

THE NSP SUBSTANTIAL AMENDMENT Jurisdiction(s): _Pasco County (identify lead entity in case of joint agreements) Jurisdiction Web Address: www.pascocountyfl.net (URL where NSP Substantial Amendment materials

THE NSP SUBSTANTIAL AMENDMENT Jurisdiction(s): _Pasco County (identify lead entity in case of joint agreements) Jurisdiction Web Address: www.pascocountyfl.net (URL where NSP Substantial Amendment materials

The Economic Power of Uncertainty: The Role of Consumer Credit Bureaus

The Economic Power of Uncertainty: The Role of Consumer Credit Bureaus Federal Reserve Forum on Credit Scores December 14, 2007 Matt Fellowes, Fellow The Economic Power of Uncertainty: The Role of Consumer

The Economic Power of Uncertainty: The Role of Consumer Credit Bureaus Federal Reserve Forum on Credit Scores December 14, 2007 Matt Fellowes, Fellow The Economic Power of Uncertainty: The Role of Consumer

The High Cost of Segregation: Exploring the Relationship Between Racial Segregation and Subprime Lending

F u r m a n C e n t e r f o r r e a l e s t a t e & u r b a n p o l i c y N e w Y o r k U n i v e r s i t y s c h o o l o f l aw wa g n e r s c h o o l o f p u b l i c s e r v i c e n o v e m b e r 2 0

F u r m a n C e n t e r f o r r e a l e s t a t e & u r b a n p o l i c y N e w Y o r k U n i v e r s i t y s c h o o l o f l aw wa g n e r s c h o o l o f p u b l i c s e r v i c e n o v e m b e r 2 0

Residential Foreclosures in Minnesota

Residential Foreclosures in Minnesota Winter 2011 Research and Evaluation Unit Residential Foreclosures in Minnesota Introduction Minnesota s foreclosure crisis has destabilized the housing market in

Residential Foreclosures in Minnesota Winter 2011 Research and Evaluation Unit Residential Foreclosures in Minnesota Introduction Minnesota s foreclosure crisis has destabilized the housing market in

Lessons to Learn from CRA Lending

Lessons to Learn from CRA Lending Roberto G. Quercia and Janneke Ratcliffe Reinventing Older Communities Federal Reserve Bank of Philadelphia May 13, 2010 CRA Case Study: CAP Reaching Target Market 46,000

Lessons to Learn from CRA Lending Roberto G. Quercia and Janneke Ratcliffe Reinventing Older Communities Federal Reserve Bank of Philadelphia May 13, 2010 CRA Case Study: CAP Reaching Target Market 46,000

Risky Borrowers or Risky Mortgages?

Risky Borrowers or Risky Mortgages? Lei Ding, Roberto G. Quercia, Janneke Ratcliffe Center for Community Capital, University of North Carolina, Chapel Hill, USA Wei Li Center for Responsible Lending, Durham,

Risky Borrowers or Risky Mortgages? Lei Ding, Roberto G. Quercia, Janneke Ratcliffe Center for Community Capital, University of North Carolina, Chapel Hill, USA Wei Li Center for Responsible Lending, Durham,

Now What? Key Trends from the Mortgage Crisis and Implications for Policy

THE FUTURE OF FAIR HOUSING and FAIR CREDIT Sponsored by: W. K. KELLOGG FOUNDATION Now What? Key Trends from the Mortgage Crisis and Implications for Policy DAN IMMERGLUCK School of City and Regional Planning,

THE FUTURE OF FAIR HOUSING and FAIR CREDIT Sponsored by: W. K. KELLOGG FOUNDATION Now What? Key Trends from the Mortgage Crisis and Implications for Policy DAN IMMERGLUCK School of City and Regional Planning,

Subprime Lending in Washington State

sound research. Bold Solutions.. Policy BrieF. March 9, 2009 The High Cost of Subprime Lending in Washington State By Jeff Chapman Executive Summary In Washington State in 2006, African- American and Hispanic

sound research. Bold Solutions.. Policy BrieF. March 9, 2009 The High Cost of Subprime Lending in Washington State By Jeff Chapman Executive Summary In Washington State in 2006, African- American and Hispanic

End of the American Dream? How Mortgage Defaults and Foreclosures Affect Families and Communities

End of the American Dream? How Mortgage Defaults and Foreclosures Affect Families and Communities J. Michael Collins Assistant Professor, School of Human Ecology Director, Center for Financial Security

End of the American Dream? How Mortgage Defaults and Foreclosures Affect Families and Communities J. Michael Collins Assistant Professor, School of Human Ecology Director, Center for Financial Security

Homeownership Preservation in Maryland

Maryland Department of Housing and Community Development Homeownership Preservation in Maryland A presentation to the Western Maryland 2008 Small Town Symposium and Rural Roundtable April 23, 2008 Martin

Maryland Department of Housing and Community Development Homeownership Preservation in Maryland A presentation to the Western Maryland 2008 Small Town Symposium and Rural Roundtable April 23, 2008 Martin

July 1, 2014 thru September 30, 2014 Performance Report

Grantee: Grant: Ohio B-08-DN-39-0001 July 1, 2014 thru September 30, 2014 Performance Report 1 Grant Number: B-08-DN-39-0001 Grantee Name: Ohio Grant Award Amount: $116,859,223.00 LOCCS Authorized Amount:

Grantee: Grant: Ohio B-08-DN-39-0001 July 1, 2014 thru September 30, 2014 Performance Report 1 Grant Number: B-08-DN-39-0001 Grantee Name: Ohio Grant Award Amount: $116,859,223.00 LOCCS Authorized Amount:

BROWARD HOUSING COUNCIL CRA PERFORMANCE BY BROWARD BANKS IN MEETING HOUSING CREDIT NEEDS

BROWARD HOUSING COUNCIL CRA PERFORMANCE BY BROWARD BANKS IN MEETING HOUSING CREDIT NEEDS CRA IMPLEMENTATION WORKSHOP January 23, 2015 2 South Florida Context Areas of Opportunity Overview of HMDA Data

BROWARD HOUSING COUNCIL CRA PERFORMANCE BY BROWARD BANKS IN MEETING HOUSING CREDIT NEEDS CRA IMPLEMENTATION WORKSHOP January 23, 2015 2 South Florida Context Areas of Opportunity Overview of HMDA Data

1 Anthony B. Sanders, Ph.D. is Professor of Finance at the School of Management at George Mason University

Anthony B. Sanders 1 Oral Testimony House Financial Services Committee March 23, 2010 Hearing on Housing Finance-What Should the New System Be Able to Do? Part I-Government and Stakeholder Perspectives

Anthony B. Sanders 1 Oral Testimony House Financial Services Committee March 23, 2010 Hearing on Housing Finance-What Should the New System Be Able to Do? Part I-Government and Stakeholder Perspectives

Community Development Block Grant Program

U.S. DEPARTMENT OF HOUSING ANn URBAN DEVELOPMENT FOR: FROM: SUBJECT: Housing under Development Block Grant (CDBG) and Neighborhood Stabilization Programs (NSP) This memorandum provides information on how

U.S. DEPARTMENT OF HOUSING ANn URBAN DEVELOPMENT FOR: FROM: SUBJECT: Housing under Development Block Grant (CDBG) and Neighborhood Stabilization Programs (NSP) This memorandum provides information on how

ONLINE APPENDIX. The Vulnerability of Minority Homeowners in the Housing Boom and Bust. Patrick Bayer Fernando Ferreira Stephen L Ross

ONLINE APPENDIX The Vulnerability of Minority Homeowners in the Housing Boom and Bust Patrick Bayer Fernando Ferreira Stephen L Ross Appendix A: Supplementary Tables for The Vulnerability of Minority Homeowners

ONLINE APPENDIX The Vulnerability of Minority Homeowners in the Housing Boom and Bust Patrick Bayer Fernando Ferreira Stephen L Ross Appendix A: Supplementary Tables for The Vulnerability of Minority Homeowners

The Foreclosure Crisis in NYC: Patterns, Origins, and Solutions. Ingrid Gould Ellen

The Foreclosure Crisis in NYC: Patterns, Origins, and Solutions Ingrid Gould Ellen Reasons for Rise in Foreclosures Risky underwriting Over-leveraged borrowers High debt to income ratios Economic downturn

The Foreclosure Crisis in NYC: Patterns, Origins, and Solutions Ingrid Gould Ellen Reasons for Rise in Foreclosures Risky underwriting Over-leveraged borrowers High debt to income ratios Economic downturn

Milwaukee's Housing Crisis: Housing Affordability and Mortgage Lending Practices

University of Wisconsin Milwaukee UWM Digital Commons ETI Publications Employment Training Institute 2007 Milwaukee's Housing Crisis: Housing Affordability and Mortgage Lending Practices John Pawasarat

University of Wisconsin Milwaukee UWM Digital Commons ETI Publications Employment Training Institute 2007 Milwaukee's Housing Crisis: Housing Affordability and Mortgage Lending Practices John Pawasarat

Real Estate Finance: 10/17/2017. Why use a mortgage?

Real Estate Finance: McGraw-Hill/Irwin Laws and Contracts Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Fixed rate (Monthly charge is 1/12 of stated annual rate) Adjustable rate

Real Estate Finance: McGraw-Hill/Irwin Laws and Contracts Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Fixed rate (Monthly charge is 1/12 of stated annual rate) Adjustable rate

The Impact of Foreclosures on Economic Recovery in Virginia

The Impact of Foreclosures on Economic Recovery in Virginia February, 2012 Brian Koziol Housing Policy and Research Analyst www.phonehome.org 804.354.0641 Where you live makes all the difference About

The Impact of Foreclosures on Economic Recovery in Virginia February, 2012 Brian Koziol Housing Policy and Research Analyst www.phonehome.org 804.354.0641 Where you live makes all the difference About

Targeting Neighborhood Stabilization Funds to Community Need: An Assessment of Georgia s Proposed Funding Allocations

Targeting Neighborhood Stabilization Funds to Community Need: An Assessment of Georgia s Proposed Funding Allocations Presented to the Georgia Department of Community Affairs November 28, 2008 Dr. Michael

Targeting Neighborhood Stabilization Funds to Community Need: An Assessment of Georgia s Proposed Funding Allocations Presented to the Georgia Department of Community Affairs November 28, 2008 Dr. Michael

Testimony of Dean Baker. Before the Subcommittee on Housing and Community Opportunity of the House Financial Services Committee

Testimony of Dean Baker Before the Subcommittee on Housing and Community Opportunity of the House Financial Services Committee Hearing on the Recently Announced Revisions to the Home Affordable Modification

Testimony of Dean Baker Before the Subcommittee on Housing and Community Opportunity of the House Financial Services Committee Hearing on the Recently Announced Revisions to the Home Affordable Modification

Foreclosure. Counseling Program Report. Prepared by Karen Duggleby, MSW, LISW Minnesota Homeownership Center

Foreclosure 2014 Counseling Program Report Prepared by Karen Duggleby, MSW, LISW Minnesota Homeownership Center Acknowledgements The Minnesota Homeownership Center is profoundly grateful for the dedicated

Foreclosure 2014 Counseling Program Report Prepared by Karen Duggleby, MSW, LISW Minnesota Homeownership Center Acknowledgements The Minnesota Homeownership Center is profoundly grateful for the dedicated

Quo Vadis? Where To for Affordable Mortgage Finance?

Quo Vadis? Where To for Affordable Mortgage Finance? Remarks by Roberto G. Quercia to Fannie Mae s Affordable Housing Advisory Council Washington, D.C. April 17, 2012 It has been a long time since I gave

Quo Vadis? Where To for Affordable Mortgage Finance? Remarks by Roberto G. Quercia to Fannie Mae s Affordable Housing Advisory Council Washington, D.C. April 17, 2012 It has been a long time since I gave

N A A H L NATIONAL ASSOCIATION OF AFFORDABLE HOUSING LENDERS CRA DID NOT CONTRIBUTE TO THE MORTGAGE CRISIS

N A A H L NATIONAL ASSOCIATION OF AFFORDABLE HOUSING LENDERS CRA DID NOT CONTRIBUTE TO THE MORTGAGE CRISIS WHAT IS CRA? Congress enacted the Community Reinvestment Act (CRA) in 1977 to encourage insured

N A A H L NATIONAL ASSOCIATION OF AFFORDABLE HOUSING LENDERS CRA DID NOT CONTRIBUTE TO THE MORTGAGE CRISIS WHAT IS CRA? Congress enacted the Community Reinvestment Act (CRA) in 1977 to encourage insured

The Current Foreclosure Crisis Trends and Roadblocks to Recovery

The Current Foreclosure Crisis Trends and Roadblocks to Recovery American Planning Association February 22, 2011 Geoff Smith Senior Vice President Woodstock Institute Chicago, Illinois gsmith@woodstockinst.org

The Current Foreclosure Crisis Trends and Roadblocks to Recovery American Planning Association February 22, 2011 Geoff Smith Senior Vice President Woodstock Institute Chicago, Illinois gsmith@woodstockinst.org

Community Development Block Grants: Legislative Proposals to Assist Communities Affected by Home Foreclosures

Order Code RS22919 July 15, 2008 Community Development Block Grants: Legislative Proposals to Assist Communities Affected by Home Foreclosures Summary Eugene Boyd and Oscar R. Gonzales Analysts in Federalism

Order Code RS22919 July 15, 2008 Community Development Block Grants: Legislative Proposals to Assist Communities Affected by Home Foreclosures Summary Eugene Boyd and Oscar R. Gonzales Analysts in Federalism

The Mortgage Industry

Financing Residential Real Estate Lesson 4: The Mortgage Industry Introduction In this lesson, we will cover: steps in the residential mortgage process; participants in the process, including loan originators

Financing Residential Real Estate Lesson 4: The Mortgage Industry Introduction In this lesson, we will cover: steps in the residential mortgage process; participants in the process, including loan originators

High LTV Lending Conference

High LTV Lending Conference Eric Belsky May 213 Chapel Hill, NC Homeownership Has Mattered Profoundly to Wealth Accumulation Even After Crude Control for Income 12 Median Net Worth of Middle Income Quintile

High LTV Lending Conference Eric Belsky May 213 Chapel Hill, NC Homeownership Has Mattered Profoundly to Wealth Accumulation Even After Crude Control for Income 12 Median Net Worth of Middle Income Quintile

Challenges and Opportunities for Low Downpayment Lending

Challenges and Opportunities for Low Downpayment Lending Roberto G. Quercia UNC Center for Community Capital University of North Carolina at Chapel Hill Chapel Hill NC, May 17, 2013 Research Funded by

Challenges and Opportunities for Low Downpayment Lending Roberto G. Quercia UNC Center for Community Capital University of North Carolina at Chapel Hill Chapel Hill NC, May 17, 2013 Research Funded by

RE: The Federal Housing Finance Agency s proposed housing goals for Fannie Mae and Freddie Mac for

CENTER FOR COMMUNITY CAPITAL UNIVERSITY OF NORTH CAROLINA AT CHAPEL HILL Dr. Roberto G. Quercia, Director 1700 Martin Luther King Blvd Janneke H. Ratcliffe, Executive Director CB 3452 Ste 129 Room 128

CENTER FOR COMMUNITY CAPITAL UNIVERSITY OF NORTH CAROLINA AT CHAPEL HILL Dr. Roberto G. Quercia, Director 1700 Martin Luther King Blvd Janneke H. Ratcliffe, Executive Director CB 3452 Ste 129 Room 128

Things My Mortgage Broker Never Told Me: Escrow, Property Taxes, and Mortgage Delinquency

Things My Mortgage Broker Never Told Me: Escrow, Property Taxes, and Mortgage Delinquency Nathan B. Anderson UIC & Institute of Govt and Public Affairs Jane K. Dokko Federal Reserve Board May 2009 Two

Things My Mortgage Broker Never Told Me: Escrow, Property Taxes, and Mortgage Delinquency Nathan B. Anderson UIC & Institute of Govt and Public Affairs Jane K. Dokko Federal Reserve Board May 2009 Two

Understanding the subprime crisis

Understanding the subprime crisis A review of recent research at the Boston Fed Paul Willen Federal Reserve Bank of Boston Brandeis University, October 21, 2009 Willen (Boston Fed) Boston Fed Subprime

Understanding the subprime crisis A review of recent research at the Boston Fed Paul Willen Federal Reserve Bank of Boston Brandeis University, October 21, 2009 Willen (Boston Fed) Boston Fed Subprime

Homeownership, the Great Recession, and Wealth: Evidence from the Survey of Consumer Finance Michal Grinstein-Weiss Clinton Key

Homeownership, the Great Recession, and Wealth: Evidence from the Survey of Consumer Finance Michal Grinstein-Weiss Clinton Key Presented at The Federal Reserve Bank of St. Louis 6 February 2013 The American

Homeownership, the Great Recession, and Wealth: Evidence from the Survey of Consumer Finance Michal Grinstein-Weiss Clinton Key Presented at The Federal Reserve Bank of St. Louis 6 February 2013 The American

Residential Foreclosures in Minnesota

Residential s in Minnesota Spring 2013 Planning, Research, and Evaluation Residential s in Minnesota Introduction Minnesota s foreclosure crisis has destabilized the housing market in many parts of the

Residential s in Minnesota Spring 2013 Planning, Research, and Evaluation Residential s in Minnesota Introduction Minnesota s foreclosure crisis has destabilized the housing market in many parts of the

Minnesota Housing: A Path to Successful Homeownership. A Path to Homeownership & Family Self-Sufficiency (REP)

") Minnesota Housing: A Path to Successful Homeownership Minnesota Housing: Real Estate Program A Path to Homeownership & Family Self-Sufficiency (REP) Today s conversation Who we are Why we re here Increasing

Minnesota Housing: A Path to Successful Homeownership Minnesota Housing: Real Estate Program A Path to Homeownership & Family Self-Sufficiency (REP) Today s conversation Who we are Why we re here Increasing

9 Ways To Stop Foreclosure. Don t Let Time RUN OUT!

9 Ways To Stop Foreclosure Don t Let Time RUN OUT! Q.B. Homes - Great Success Realty. Saar (Sam) Elazar, Licensed Real Estate Salesperson CDPE Certified Distress Property Expert 140-21 Queens Blvd. (Ground

9 Ways To Stop Foreclosure Don t Let Time RUN OUT! Q.B. Homes - Great Success Realty. Saar (Sam) Elazar, Licensed Real Estate Salesperson CDPE Certified Distress Property Expert 140-21 Queens Blvd. (Ground

Don t Raise the Federal Debt Ceiling, Torpedo the U.S. Housing Market

Don t Raise the Federal Debt Ceiling, Torpedo the U.S. Housing Market Failure to Act Would Have Serious Consequences for Housing Just as the Market Is Showing Signs of Recovery Christian E. Weller May

Don t Raise the Federal Debt Ceiling, Torpedo the U.S. Housing Market Failure to Act Would Have Serious Consequences for Housing Just as the Market Is Showing Signs of Recovery Christian E. Weller May

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners May 2011 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners May 2011 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

SECTION FIVE: FORECLOSURE AND LENDING CHARACTERISTICS

SECTION FIVE: FORECLOSURE AND LENDING CHARACTERISTICS Legend Regulated Affiliate of Regulated Unregulated 0 Miles 10 Foreclosures by Type of Lending Institution This map shows the type of lending institutions

SECTION FIVE: FORECLOSURE AND LENDING CHARACTERISTICS Legend Regulated Affiliate of Regulated Unregulated 0 Miles 10 Foreclosures by Type of Lending Institution This map shows the type of lending institutions

Minnesota Home Ownership Center 2008 FORECLOSURE COUNSELING PROGRAM REPORT

Minnesota Home Ownership Center 2008 FORECLOSURE COUNSELING PROGRAM REPORT Karen Duggleby, M.S.W. and Kim Skobba, Ph.D. April 2009 1 P a g e Acknowledgements The Minnesota Home Ownership Center staff would

Minnesota Home Ownership Center 2008 FORECLOSURE COUNSELING PROGRAM REPORT Karen Duggleby, M.S.W. and Kim Skobba, Ph.D. April 2009 1 P a g e Acknowledgements The Minnesota Home Ownership Center staff would

Why is Non-Bank Lending Highest in Communities of Color?

Why is Non-Bank Lending Highest in Communities of Color? An ANHD White Paper October 2017 New York is a city of renters, but nearly a third of New Yorkers own their own homes. The stock of 2-4 family homes

Why is Non-Bank Lending Highest in Communities of Color? An ANHD White Paper October 2017 New York is a city of renters, but nearly a third of New Yorkers own their own homes. The stock of 2-4 family homes

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners November 2012 U.S. Department U.S Department of Housing of Housing and Urban and Urban Development Development

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners November 2012 U.S. Department U.S Department of Housing of Housing and Urban and Urban Development Development

Testimony of Michael D. Calhoun President, Center for Responsible Lending. Before the House Committee on Financial Services

Testimony of Michael D. Calhoun President, Center for Responsible Lending Before the House Committee on Financial Services Hearing: A Legislative Proposal to Protect American Taxpayers and Homeowners by

Testimony of Michael D. Calhoun President, Center for Responsible Lending Before the House Committee on Financial Services Hearing: A Legislative Proposal to Protect American Taxpayers and Homeowners by

35% 26% 57% 51% PROFILE. CIty of durham: Assets & opportunity ProfILe. key highlights. ABoUt the ProfILe ASSETS & OPPORTUNITY

CIty of durham: Assets & opportunity ProfILe ASSETS & OPPORTUNITY PROFILE key highlights 35% of Durham County households live in asset poverty Cities have long been thought of as places of opportunity

CIty of durham: Assets & opportunity ProfILe ASSETS & OPPORTUNITY PROFILE key highlights 35% of Durham County households live in asset poverty Cities have long been thought of as places of opportunity

Hopefully the biggest part of the housing decline will be over by the end of the year."

Reuters Hopefully the biggest part of the housing decline will be over by the end of the year." - U.S. Treasury Secretary Henry Paulson Source: Reuters News 6/24/08 Reuters We are at the beginning of the

Reuters Hopefully the biggest part of the housing decline will be over by the end of the year." - U.S. Treasury Secretary Henry Paulson Source: Reuters News 6/24/08 Reuters We are at the beginning of the

U.S. Housing Markets: Looking Back, Looking Forward

U.S. Housing Markets: Looking Back, Looking Forward Dr. Raphael Bostic Assistant Secretary, Office of Policy Development and Research U.S. Department of Housing and Urban Development Special Thanks Ed

U.S. Housing Markets: Looking Back, Looking Forward Dr. Raphael Bostic Assistant Secretary, Office of Policy Development and Research U.S. Department of Housing and Urban Development Special Thanks Ed

A Case for Post-Purchase Support Programs as Part of Minnesota s Emerging Markets Homeownership Initiative

FEDERAL RESERVE BANK OF MINNEAPOLIS COMMUNITY AFFAIRS REPORT Report No. 2005-1 A Case for Post-Purchase Support Programs as Part of Minnesota s Emerging Markets Homeownership Initiative Richard M. Todd

FEDERAL RESERVE BANK OF MINNEAPOLIS COMMUNITY AFFAIRS REPORT Report No. 2005-1 A Case for Post-Purchase Support Programs as Part of Minnesota s Emerging Markets Homeownership Initiative Richard M. Todd

Foreclosure Prevention: Homeowner Counseling Efforts in North Carolina Cities. Mira Schainker. Spring 2009

Foreclosure Prevention: Homeowner Counseling Efforts in North Carolina Cities By Mira Schainker Spring 2009 A paper submitted to the faculty of the University of North Carolina at Chapel Hill in partial

Foreclosure Prevention: Homeowner Counseling Efforts in North Carolina Cities By Mira Schainker Spring 2009 A paper submitted to the faculty of the University of North Carolina at Chapel Hill in partial

The Subprime Crisis:

The Subprime Crisis: Can problems in a small part of the mortgage market disrupt the entire economy? Paul Willen Federal Reserve Bank of Boston Boston Fed Regional Community and Banking Conference, October

The Subprime Crisis: Can problems in a small part of the mortgage market disrupt the entire economy? Paul Willen Federal Reserve Bank of Boston Boston Fed Regional Community and Banking Conference, October

July 1, 2011 thru September 30, 2011 Performance Report

Grantee: St Petersburg, FL Grant: B-08-MN-12-0026 July 1, 2011 thru September 30, 2011 Performance Report 1 Grant Number: B-08-MN-12-0026 Grantee Name: St Petersburg, FL Grant Amount: $9,498,962.00 Grant

Grantee: St Petersburg, FL Grant: B-08-MN-12-0026 July 1, 2011 thru September 30, 2011 Performance Report 1 Grant Number: B-08-MN-12-0026 Grantee Name: St Petersburg, FL Grant Amount: $9,498,962.00 Grant

Paying More for the American Dream III

Paying More for the American Dream III Promoting Responsible Lending to Lower-Income Communities and Communities of Color April 2009 A Joint Report By: California Reinvestment Coalition Community Reinvestment

Paying More for the American Dream III Promoting Responsible Lending to Lower-Income Communities and Communities of Color April 2009 A Joint Report By: California Reinvestment Coalition Community Reinvestment

Subprime Originations and Foreclosures in New York State: A Case Study of Nassau, Suffolk, and Westchester Counties.

Subprime Originations and Foreclosures in New York State: A Case Study of Nassau, Suffolk, and Westchester Counties Cambridge, MA Lexington, MA Hadley, MA Bethesda, MD Washington, DC Chicago, IL Cairo,

Subprime Originations and Foreclosures in New York State: A Case Study of Nassau, Suffolk, and Westchester Counties Cambridge, MA Lexington, MA Hadley, MA Bethesda, MD Washington, DC Chicago, IL Cairo,

HOUSING & MORTGAGE COUNSELOR

HOUSING & MORTGAGE COUNSELOR COMPENSATION: (based on substantial production incentives) Mortgage Counselor: $60,000 to $100,000+ Housing Counselor: $40,000 to $55,000+ CONTACT: HR Department: jobs@naca.com

HOUSING & MORTGAGE COUNSELOR COMPENSATION: (based on substantial production incentives) Mortgage Counselor: $60,000 to $100,000+ Housing Counselor: $40,000 to $55,000+ CONTACT: HR Department: jobs@naca.com

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners April 2012 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners April 2012 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

Some thoughts on housing and the economy

Some thoughts on housing and the economy Paul Willen Federal Reserve Bank of Boston Exploring Impediments to a Real Estate Recovery Federal Reserve Bank of Atlanta December 1, 2011 Willen (Boston Fed)

Some thoughts on housing and the economy Paul Willen Federal Reserve Bank of Boston Exploring Impediments to a Real Estate Recovery Federal Reserve Bank of Atlanta December 1, 2011 Willen (Boston Fed)

CRA: A Framework for the Future. Remarks by. Elizabeth A. Duke. Member. Board of Governors of the Federal Reserve System

For release on delivery Noon EST February 24, 2009 CRA: A Framework for the Future Remarks by Elizabeth A. Duke Member Board of Governors of the Federal Reserve System at Revisiting the CRA: A Policy Discussion

For release on delivery Noon EST February 24, 2009 CRA: A Framework for the Future Remarks by Elizabeth A. Duke Member Board of Governors of the Federal Reserve System at Revisiting the CRA: A Policy Discussion

National Foreclosure Mitigation Counseling Program

National Foreclosure Mitigation Counseling Program National Foreclosure Mitigation Counseling Program Congressional Update Activity through January 31, 2010 Executive Summary NeighborWorks America (as

National Foreclosure Mitigation Counseling Program National Foreclosure Mitigation Counseling Program Congressional Update Activity through January 31, 2010 Executive Summary NeighborWorks America (as

TRENDS IN DELINQUENCIES AND FORECLOSURES IN SOUTHERN CALIFORNIA

TRENDS IN DELINQUENCIES AND FORECLOSURES IN SOUTHERN CALIFORNIA April 2009 Melody Nava, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising

TRENDS IN DELINQUENCIES AND FORECLOSURES IN SOUTHERN CALIFORNIA April 2009 Melody Nava, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising

Program Assessment Report 2017

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Evaluating Affordable

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp Evaluating Affordable

Group 14 Dallas Hall, Chuck Dobson, Guy Tahye, Tunde Olabiyi

In order to understand how we have gotten to the point where government intervention is needed to save our financial markets, it is necessary to look back and examine the many causes that lead to this

In order to understand how we have gotten to the point where government intervention is needed to save our financial markets, it is necessary to look back and examine the many causes that lead to this

Randall S Kroszner: Loan modifications and foreclosure prevention

Randall S Kroszner: Loan modifications and foreclosure prevention Testimony by Mr Randall S Kroszner, Member of the Board of Governors of the US Federal Reserve System, before the Committee on Financial

Randall S Kroszner: Loan modifications and foreclosure prevention Testimony by Mr Randall S Kroszner, Member of the Board of Governors of the US Federal Reserve System, before the Committee on Financial

Why is the Country Facing a Financial Crisis?

Why is the Country Facing a Financial Crisis? Prepared by: Julie L. Stackhouse Senior Vice President Federal Reserve Bank of St. Louis November 3, 2008 The views expressed in this presentation are the

Why is the Country Facing a Financial Crisis? Prepared by: Julie L. Stackhouse Senior Vice President Federal Reserve Bank of St. Louis November 3, 2008 The views expressed in this presentation are the

Reviewed and Approved

Action Plan Grantee: Grant: New Mexico B-08-DN-35-0001 LOCCS Authorized Amount: Grant Award Amount: $ 19,600,000.00 $ 19,600,000.00 Status: Reviewed and Approved Estimated PI/RL Funds: $ 9,498,219.17 Total

Action Plan Grantee: Grant: New Mexico B-08-DN-35-0001 LOCCS Authorized Amount: Grant Award Amount: $ 19,600,000.00 $ 19,600,000.00 Status: Reviewed and Approved Estimated PI/RL Funds: $ 9,498,219.17 Total

A Look Behind the Numbers: Foreclosures in Allegheny County, PA

Page1 Introduction This is the second report in a series that looks at the geographic distribution of foreclosures in counties located within the Federal Reserve s Fourth District. In this report we focus

Page1 Introduction This is the second report in a series that looks at the geographic distribution of foreclosures in counties located within the Federal Reserve s Fourth District. In this report we focus

36% 50% 11% 59% 35% PROFILE ASSETS & OPPORTUNITY PROFILE: CHARLOTTE KEY HIGHLIGHTS ABOUT THE PROFILE ASSETS & OPPORTUNITY

ASSETS & OPPORTUNITY PROFILE: CHARLOTTE ASSETS & OPPORTUNITY PROFILE KEY HIGHLIGHTS 36% of Charlotte households live in asset poverty Cities have long been thought of as places of opportunity for low-income

ASSETS & OPPORTUNITY PROFILE: CHARLOTTE ASSETS & OPPORTUNITY PROFILE KEY HIGHLIGHTS 36% of Charlotte households live in asset poverty Cities have long been thought of as places of opportunity for low-income

Preliminary Staff Report

DRAFT: COMMENTS INVITED Financial Crisis Inquiry Commission Preliminary Staff Report THE COMMUNITY REINVESTMENT ACT AND THE MORTGAGE CRISIS APRIL 7, 2010 This preliminary staff report is submitted to the

DRAFT: COMMENTS INVITED Financial Crisis Inquiry Commission Preliminary Staff Report THE COMMUNITY REINVESTMENT ACT AND THE MORTGAGE CRISIS APRIL 7, 2010 This preliminary staff report is submitted to the

October 22, Joseph A. Smith Office of Mortgage Settlement Oversight 301 Fayetteville St., Suite 1801 Raleigh, NC Via electronic mail

October 22, 2012 Joseph A. Smith Office of Mortgage Settlement Oversight 301 Fayetteville St., Suite 1801 Raleigh, NC 27601 Via electronic mail Dear Mr. Smith: Thank you again for speaking with members

October 22, 2012 Joseph A. Smith Office of Mortgage Settlement Oversight 301 Fayetteville St., Suite 1801 Raleigh, NC 27601 Via electronic mail Dear Mr. Smith: Thank you again for speaking with members

Fact Sheet. Mississippi Home of Your Own (HOYO) HOMEBUYER ASSISTANCE PROGRAM (HOME)

HOMEBUYER ASSISTANCE PROGRAM (HOME)") MISSISSIPPI HOME OF YOUR OWN MHC HOMEBUYER ASSISTANCE PROGRAM Toll-free 1.888.671.0051 or 601.266.4097 or 601.266.6038 Mississippi Home of Your Own (HOYO) HOMEBUYER ASSISTANCE PROGRAM (HOME) Mississippi

MISSISSIPPI HOME OF YOUR OWN MHC HOMEBUYER ASSISTANCE PROGRAM Toll-free 1.888.671.0051 or 601.266.4097 or 601.266.6038 Mississippi Home of Your Own (HOYO) HOMEBUYER ASSISTANCE PROGRAM (HOME) Mississippi

TRENDS IN DELINQUENCIES AND FORECLOSURES IN

TRENDS IN DELINQUENCIES AND FORECLOSURES IN SOUTHERN CALIFORNIA August 2009 Melody Nava, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends

TRENDS IN DELINQUENCIES AND FORECLOSURES IN SOUTHERN CALIFORNIA August 2009 Melody Nava, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends

The Great Recession Hits Home: Asset Depletion and Foreclosure in Boston

The Great Recession Hits Home: Asset Depletion and Foreclosure in Boston Dr. Hannah Thomas, Ph.D., SSRC Emerging Scholar Dr. Curtis Skinner, Ph.D., Discussant Emerging Scholars Webinar #8 Thursday, September

The Great Recession Hits Home: Asset Depletion and Foreclosure in Boston Dr. Hannah Thomas, Ph.D., SSRC Emerging Scholar Dr. Curtis Skinner, Ph.D., Discussant Emerging Scholars Webinar #8 Thursday, September

U.S. Foreclosure Outlook. To: Company Name Here Date: Goes Here

U.S. Foreclosure Outlook To: Company Name Here Date: Goes Here A brief note on methodology RealtyTrac collects foreclosure documents, postings and published notices from about 2,200 counties nationwide.

U.S. Foreclosure Outlook To: Company Name Here Date: Goes Here A brief note on methodology RealtyTrac collects foreclosure documents, postings and published notices from about 2,200 counties nationwide.

Subprime Crisis Update on Federal Government Response

Subprime Crisis Update on Federal Government Response With Congress in a brief recess, now is an opportune time to provide a brief update on federal activities surrounding the continuing subprime mortgage

Subprime Crisis Update on Federal Government Response With Congress in a brief recess, now is an opportune time to provide a brief update on federal activities surrounding the continuing subprime mortgage

FORECLOSURE. Minnesota Foreclosure Partners Council. Fix Housing Fix the Economy

FORECLOSURE Minnesota Foreclosure Partners Council Fix Housing Fix the Economy Presenters: Warren Hanson, president & CEO, Greater Minnesota Housing Fund (GMHF) Michelle Vojacek, Foreclosure Program Coordinator,

FORECLOSURE Minnesota Foreclosure Partners Council Fix Housing Fix the Economy Presenters: Warren Hanson, president & CEO, Greater Minnesota Housing Fund (GMHF) Michelle Vojacek, Foreclosure Program Coordinator,

FINAL REPORT PREDATORY LENDING STUDY GROUP FOR ATTORNEY GENERAL LORI SWANSON

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp FINAL REPORT PREDATORY

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp FINAL REPORT PREDATORY

Who is Lending and Who is Getting Loans?

Trends in 1-4 Family Lending in New York City An ANHD White Paper February 2016 As much as New York City is a city of renters, nearly a third of New Yorkers own their own homes. Responsible, affordable

Trends in 1-4 Family Lending in New York City An ANHD White Paper February 2016 As much as New York City is a city of renters, nearly a third of New Yorkers own their own homes. Responsible, affordable

TRENDS IN DELINQUENCIES AND FORECLOSURES IN CALIFORNIA

TRENDS IN DELINQUENCIES AND FORECLOSURES IN CALIFORNIA April 2009 Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures House

TRENDS IN DELINQUENCIES AND FORECLOSURES IN CALIFORNIA April 2009 Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures House

HOUSING & MORTGAGE COUNSELOR

HOUSING & MORTGAGE COUNSELOR COMPENSATION: (based on substantial production incentives) Mortgage Counselor: $60,000 to $100,000+ Housing Counselor: $40,000 to $55,000+ CONTACT: HR Department: jobs@naca.com

HOUSING & MORTGAGE COUNSELOR COMPENSATION: (based on substantial production incentives) Mortgage Counselor: $60,000 to $100,000+ Housing Counselor: $40,000 to $55,000+ CONTACT: HR Department: jobs@naca.com

TESTIMONY OF BRUCE MARKS. Chief Executive Officer. Neighborhood Assistance Corporation of America (NACA)

") TESTIMONY OF BRUCE MARKS Chief Executive Officer Neighborhood Assistance Corporation of America (NACA) My name is Bruce Marks. I am Chief Executive Officer of the Neighborhood Assistance Corporation of

TESTIMONY OF BRUCE MARKS Chief Executive Officer Neighborhood Assistance Corporation of America (NACA) My name is Bruce Marks. I am Chief Executive Officer of the Neighborhood Assistance Corporation of

Home Financing in Kansas City and Its Contribution to Low- and Moderate-Income Neighborhood Development

FEBRUARY 2007 Home Financing in Kansas City and Its Contribution to Low- and Moderate-Income Neighborhood Development JAMES HARVEY AND KENNETH SPONG James Harvey is a policy economist and Kenneth Spong

FEBRUARY 2007 Home Financing in Kansas City and Its Contribution to Low- and Moderate-Income Neighborhood Development JAMES HARVEY AND KENNETH SPONG James Harvey is a policy economist and Kenneth Spong

Real Estate Market. Lawrence Yun, Ph.D. Presentation to New England REALTORS Conference. February 2, 2010 NATIONAL ASSOCIATION OF REALTORS

Real Estate Market Trends & Outlook Lawrence Yun, Ph.D. Chief Economist NATIONAL ASSOCIATION OF REALTORS Presentation to New England REALTORS Conference February 2, 2010 Housing Stimulus Impact Tax Credit

Real Estate Market Trends & Outlook Lawrence Yun, Ph.D. Chief Economist NATIONAL ASSOCIATION OF REALTORS Presentation to New England REALTORS Conference February 2, 2010 Housing Stimulus Impact Tax Credit

A Homeowner s Last Gasp: Looking at the Redemption Process in Hennepin County, Minnesota

Macalester College DigitalCommons@Macalester College Geography Honors Projects Geography Department Spring 2009 A Homeowner s Last Gasp: Looking at the Redemption Process in Hennepin County, Minnesota

Macalester College DigitalCommons@Macalester College Geography Honors Projects Geography Department Spring 2009 A Homeowner s Last Gasp: Looking at the Redemption Process in Hennepin County, Minnesota

METROPOLITAN PHILADELPHIA INDICATORS PROJECT

METROPOLITAN PHILADELPHIA INDICATORS PROJECT FORECLOSURE RISK AND THE PHILADELPHIA REGION: THE CONTINUING SAGA This report addresses the pattern of foreclosure risk in the greater Philadelphia region that

METROPOLITAN PHILADELPHIA INDICATORS PROJECT FORECLOSURE RISK AND THE PHILADELPHIA REGION: THE CONTINUING SAGA This report addresses the pattern of foreclosure risk in the greater Philadelphia region that

RE: Servicer Compliance with Newly Enacted Statutory Changes to the New York State Mortgage Foreclosure Law / Chapter 507 of the Laws of 2009

By E mail March 2, 2010 RE: Servicer Compliance with Newly Enacted Statutory Changes to the New York State Mortgage Foreclosure Law / Chapter 507 of the Laws of 2009 Dear SONYMA Servicer: On December 15,

By E mail March 2, 2010 RE: Servicer Compliance with Newly Enacted Statutory Changes to the New York State Mortgage Foreclosure Law / Chapter 507 of the Laws of 2009 Dear SONYMA Servicer: On December 15,

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

Real Estate Loan Losses, Bank Failure and Emerging Regulation 2010 William C. Handorf, Ph. D. Current Professor of Finance The George Washington University Consultant Banks Central Banks Corporations Director

A look Behind the numbers Winter Behind the numbers. A Look. Distressed Loans in Ohio:

A look Behind the numbers Winter 2013 Published By The Federal Reserve Bank of Cleveland Behind the numbers A Look written by Lisa Nelson and Francisca G.-C. Richter 9 147 3 Distressed Loans in Ohio: Recent

A look Behind the numbers Winter 2013 Published By The Federal Reserve Bank of Cleveland Behind the numbers A Look written by Lisa Nelson and Francisca G.-C. Richter 9 147 3 Distressed Loans in Ohio: Recent

in North Carolina House Select Committee on Rising Home Foreclosures January 23, 2008

Rising Foreclosures in North Carolina House Select Committee on Rising Home Foreclosures January 23, 2008 Mark E. Pearce, Deputy Commissioner NC Office of the Commissioner of Banks NCCOB s regulation of

Rising Foreclosures in North Carolina House Select Committee on Rising Home Foreclosures January 23, 2008 Mark E. Pearce, Deputy Commissioner NC Office of the Commissioner of Banks NCCOB s regulation of

What s My Note Worth? The Note Value Handbook

What s My Note Worth? The Note Value Handbook Inside Information Regarding Valuation of your Seller Financed Note in the Note Investor Market Compiled and published by Nationwide Secured Capital Retail

What s My Note Worth? The Note Value Handbook Inside Information Regarding Valuation of your Seller Financed Note in the Note Investor Market Compiled and published by Nationwide Secured Capital Retail

Homeownership. The State of the Nation s Housing 2009

Homeownership Entering 9, foreclosures were at a record high, price declines were keeping many would-be buyers on the sidelines, and tighter underwriting standards were preventing many of those ready to

Homeownership Entering 9, foreclosures were at a record high, price declines were keeping many would-be buyers on the sidelines, and tighter underwriting standards were preventing many of those ready to

Homeowner Affordability and Stability Plan Fact Sheet

Homeowner Affordability and Stability Plan Fact Sheet The deep contraction in the economy and in the housing market has created devastating consequences for homeowners and communities throughout the country.

Homeowner Affordability and Stability Plan Fact Sheet The deep contraction in the economy and in the housing market has created devastating consequences for homeowners and communities throughout the country.

Analyzing Trends in Subprime Originations and Foreclosures: A Case Study of the Boston Metro Area

Analyzing Trends in Originations and : A Case Study of the Boston Metro Area Cambridge, MA Lexington, MA Hadley, MA Bethesda, MD Washington, DC Chicago, IL Cairo, Egypt Johannesburg, South Africa September

Analyzing Trends in Originations and : A Case Study of the Boston Metro Area Cambridge, MA Lexington, MA Hadley, MA Bethesda, MD Washington, DC Chicago, IL Cairo, Egypt Johannesburg, South Africa September

WHAT THE REALLY HAPPENED...

WHAT THE F#@K REALLY HAPPENED... THE ECONOMIC CRISIS OF 08 EDMOND GRADY A BANKER IS A FELLOW WHO LENDS YOU HIS UMBRELLA WHEN THE SUN IS SHINING, BUT WANTS IT BACK THE MINUTE IT BEGINS TO RAIN. MARK TWAIN

WHAT THE F#@K REALLY HAPPENED... THE ECONOMIC CRISIS OF 08 EDMOND GRADY A BANKER IS A FELLOW WHO LENDS YOU HIS UMBRELLA WHEN THE SUN IS SHINING, BUT WANTS IT BACK THE MINUTE IT BEGINS TO RAIN. MARK TWAIN

during the Financial Crisis

Minority borrowers, Subprime lending and Foreclosures during the Financial Crisis Stephen L Ross University of Connecticut The work presented is joint with Patrick Bayer, Fernando Ferreira and/or Yuan

Minority borrowers, Subprime lending and Foreclosures during the Financial Crisis Stephen L Ross University of Connecticut The work presented is joint with Patrick Bayer, Fernando Ferreira and/or Yuan

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

Weakness in the U.S. Housing Market Likely to Persist in 2008

Weakness in the U.S. Housing Market Likely to Persist in 2008 Commentary by Sondra Albert, Chief Economist AFL-CIO Housing Investment Trust January 29, 2008 The national housing market entered 2008 mired

Weakness in the U.S. Housing Market Likely to Persist in 2008 Commentary by Sondra Albert, Chief Economist AFL-CIO Housing Investment Trust January 29, 2008 The national housing market entered 2008 mired

Community Reinvestment Act Compliance: Creating Partnerships to Serve. Communities in Minneapolis and St. Paul

Community Reinvestment Act Compliance: Creating Partnerships to Serve Communities in Minneapolis and St. Paul Prepared by David King Graduate Research Assistant, University of Minnesota Conducted on behalf

Community Reinvestment Act Compliance: Creating Partnerships to Serve Communities in Minneapolis and St. Paul Prepared by David King Graduate Research Assistant, University of Minnesota Conducted on behalf