U.S. Foreclosure Outlook. To: Company Name Here Date: Goes Here

|

|

|

- Robyn Gray

- 5 years ago

- Views:

Transcription

1 U.S. Foreclosure Outlook To: Company Name Here Date: Goes Here

2 A brief note on methodology RealtyTrac collects foreclosure documents, postings and published notices from about 2,200 counties nationwide. Counties account for over 92 percent of all U.S. housing units Data is collected primarily by network of abstractors Monthly counts are based on date the document/posting/notice was uploaded into the RealtyTrac database, not the recording date

3 -2010 Foreclosure Review An historically unprecedented cycle First wave not started by usual economic trends, but by unsustainable home prices and high-risk monetary and underwriting practices Sub-prime loans started the wave, and provided the Properties with foreclosure filings have exceeded 300,000 for 20 consecutive months through Oct March 2010 was the highest month ever in terms of foreclosure activity, with over 367,000 U.S. households receiving a foreclosure notice That will trend will be broken in November because of -

4 U.S. foreclosure activity over last five years U.S. Monthly Foreclosure Activity Default Auction REO March 2010 highest monthly total with 367,

5 120,000 Default Auction REO SB 1137 takes effect in Sep ,000 80,000 60,000 40,000 20,000 - Apr- 05 Jun- 05 Aug- 05 Oct- 05 Dec- 05 Feb- 06 Apr- 06 Jun- 06 Aug- 06 Oct- 06 Dec- 06 Feb- 07 Apr- 07 Jun- 07 Aug- 07 Oct- 07 Dec- 07 Feb- 08 Apr- 08 Jun- 08 Aug- 08 Oct- 08 Dec- 08 Feb- 09 Apr- 09 Jun- 09 Aug- 09 Oct- 09 Dec- 09 Feb- 10 Apr- 10 Jun- 10 Aug- 10 Oct- 10

6 U.S. Total Foreclosure Sales Activity # of Sales Pct. of All Sales 400, , , Total Foreclosure Sales 250, , , Percent of All Sales 100, , Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q2 Q3 0.00

7 Where we are U.S. foreclosure activity has decreased on annual basis in five of last seven months New foreclosure starts have decreased on annual basis for nine straight months But risk remains in market High unemployment Underwater homeowners (20% plus) Toxic loans still lingering Backlog of bank-owned inventory

8 Where we are: Foreclosure Starts decreasing 120% Annual Percent Change in Foreclosure Activity by Type Default YOY Auction YOY REO YOY 100% 80% 60% 40% 20% 0% - 20% - 40%

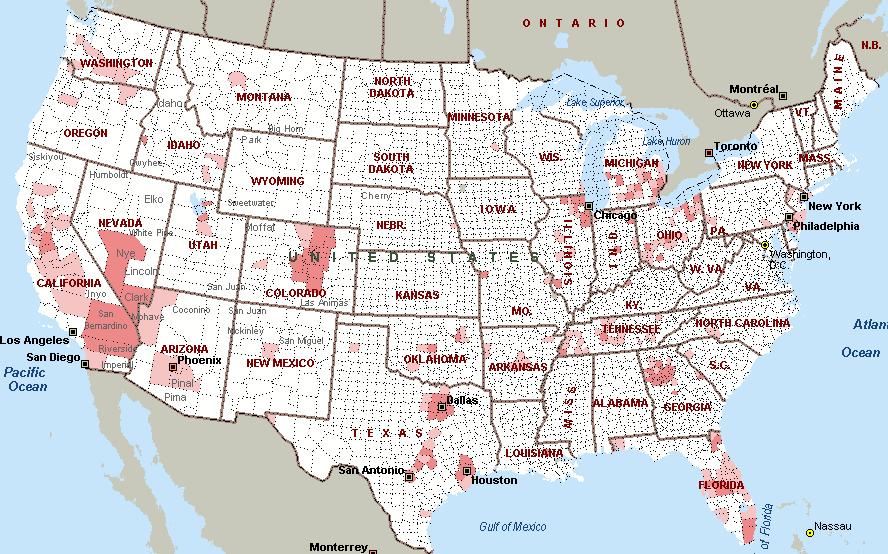

9 Where we are: Top 10 State Foreclosure Rates

10 Where we are: backlog of bank-owned inventory RealtyTrac New REO Activity RealtyTrac # of REO Sales 350, ,000 Since Q2 2005, 1.7 million more REOs have been created than have been sold 250, , , ,000 50, Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q4

11 Where we are: more shadow inventory 59% of the housing market, or 7.1 million, are in some stage of distress Prope rties in Foreclosure Process, 1,200,000, 10% Exhisting Home Sales, 4,530,000, 38% New Home Sales, 307,000, 3% Delinquent, 5,000,000, 41% R EO, 900,000, 8%

12 Where we are: toxic loans lingering 14 SOURCE: Amherst Securities, Loan Performance

13 Foreclosure levels remain at a high plateau in 2011 Unemployment will drive high levels of foreclosure activity through 2011 Resetting option ARMs could also contribute to continued high foreclosure levels Foreclosure activity turns corner 2012 to 2014 Optimistically, levels could start declining consistently in 2012, which would match the typical seven-year window we have seen with high foreclosure cycles in the past. Pessimistically, the cycle pushed out up to two years years in getting the distressed inventory cleared.

14 U.S. Properties with FC Filings Total FC Filings 4,500,000 4,000,000 3,957,643 4,000,000 4,100,000 3,500,000 3,000,000 3,157,806 2,824,674 2,900,000 3,000,000 2,500,000 2,203,295 2,330,483 2,000,000 1,500,000 1,259,118 1,285,873 1,000, , , (p) 2011 (p)

15 Charting foreclosures by county To: Company Name Here Date: Goes Here

16 Charting foreclosure rates by county October 2010

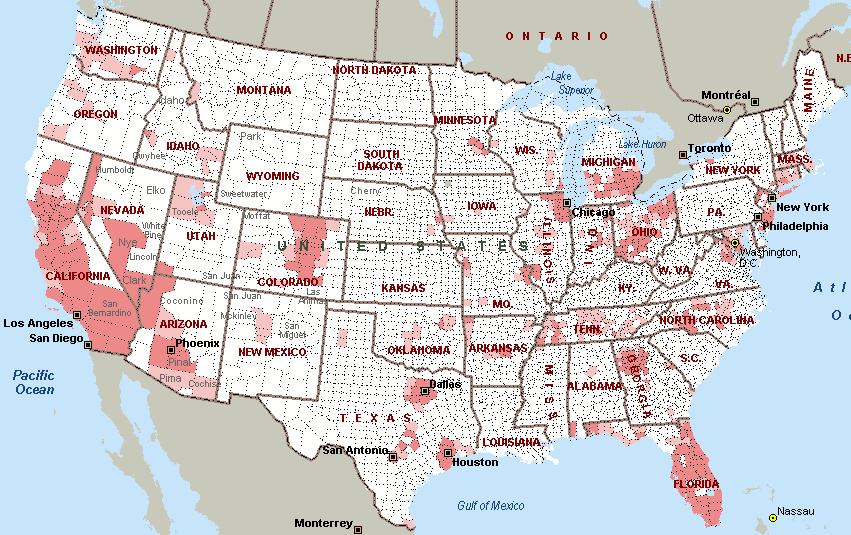

17 2006

18 2007

19 2008

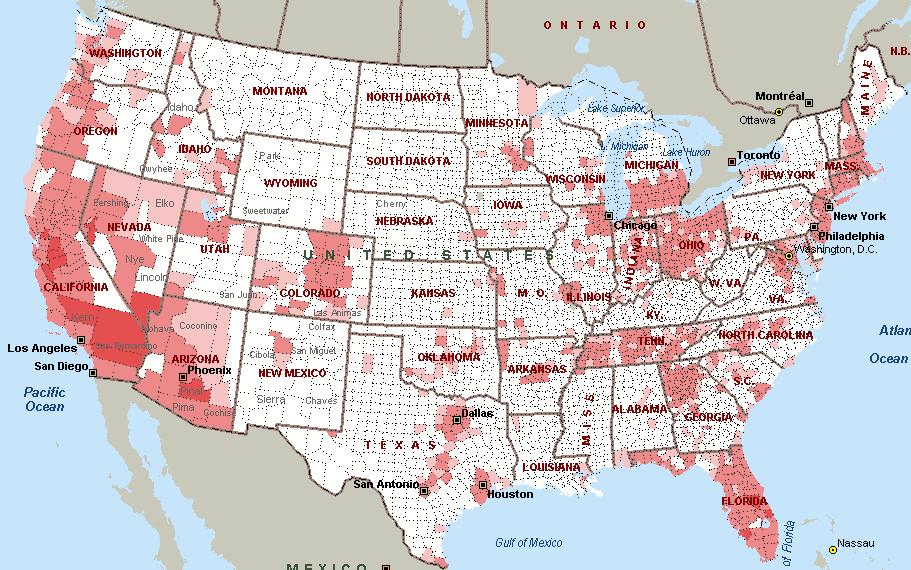

20 2009

21 2010 Year-End Projection

22 Hope for first-time homebuyers

23 Contact Information Daren Blomquist Director of Marketing Communications To: Company Name Here Ext. 115 Date: Goes Here

24 A TOOLKIT TO AVOID FORECLOSURE

25 TRIAGE PROCESS This Toolkit is an electronic format of information compiled from: Foreclosure Prevention Certification training through NeighborWorks and the Virginia Housing and Development Authority The Virginia Foreclosure Prevention Task Force The National Consumer Law Center and Legal Services of Northern Virginia Making Home Affordable The information can be used for information and referral services or for more intense foreclosure prevention counseling services.

26 Steps in the Triage Process Steps I and II can be used when making referrals to other agencies for foreclosure counseling Determine what type of mortgage the homeowner has: VHDA FHA Veterans Administration Can refer homeowner to the Making Home Affordable web site for a self- assessment, mortgage reduction calculator, checklist for documents, and how to find a free HUD- approved housing counselor

27 Steps in the Triage Process Additional resources for homeowners who are victims of foreclosure scams Information regarding renters in foreclosed properties There is a link to the Foreclosure Timeline to determine where the homeowner is on it

28 Steps in the Triage Process Steps III and IV cover the information gathering stage and the workout options that may be possible Links to documents that need to be gathered and forms such as the sample of a Qualified Written Request and a Foreclosure Prevention Services Agreement Predatory loan checklist. If it is identified as a predatory loan, refer to a Legal Aid Society or pro bono program to determine if the mortgage is in violation of the Truth in Lending Act Link to a Spending Plan to review with the homeowner. Can they can afford to keep the home? What changes can be made? Link to the Loss Mitigation Checklist for the counselor

29 Steps in the Triage Process Programs available through Making Home Affordable (for a power point on program specifics, go to: unselor/presentations/mhacounselorpresenglish.pdf) Loan modification (HAMP) The waterfall process Second Lien modification Unemployment Program under HAMP, not under HUD Principal Reduction Alternative Foreclosure Alternatives (HAFA)

30 Steps in the Triage Process If none of the Making Home Affordable programs will work, go to V for standard workout options Throughout the document, there are links to web sites, definitions, and forms to aid the housing counselor. There is coverage of just the concepts, as well as going into detail

31 Resource List and Appendix The Web Resources list covers where to find valuable information and check for updates, such as: Loan Scam Alert Loan Port NeighborWorks and HUD Capital Area Foreclosure Network NPV Test The Appendix also has hyperlinks for the documents to provide quick access. The toolkit provides a portable collection of materials needed to provide information and take steps to avoid foreclosure

32 December 9, 2010

33 Program Overview Implemented on January 12, 1009 by the Honorable Joseph M. James, President Judge via an administrative order. Judge James, Sheriff Mullen, the Allegheny County Bar Association and several non-profit organizations are owed the credit for creating this program! Partnership between: Civil Division Court & Judges behalf) Allegheny County Bar Association & Neighborhood Legal Services Association 8 non-profit HUD-certified Housing Counseling Agencies

34 Program Objective Provide a single unified process for the amicable resolution of mortgage foreclosure proceedings through court intervention, counseling and conciliation.

35 Eligibility Requirements Mortgage Foreclosure complaint has Department of Court Records, Civil Division. A unique identifier was created for the docket number, which always starts with a MG. This has been key to identifying the eligible cases. Property must be owner-occupied, no other properties are eligible.

36 How it works. Complaint Filed: Mortgage Foreclosure Complaint is filed against the borrower. Filed in our courts and Urgent Notice: In the foreclosure documents, at the contact the Save Your Home Hotline, and explains that this is a free program to help borrowers resolve contains a toll-free number for the borrower to call.

37 How it works, continued Hotline: The borrower calls the hotline, which is staffed by Economic Development staff, and the hotline staff briefly explain the program, and then schedule the borrower with one of the 8 housing counseling agencies. Work out housing counseling agencies availability ahead-of-time, so we can schedule on the first and only phone call Schedule 1 week out, so that the counseling agency can send the borrower a list of information to bring to the appointment, so as to make the appointment efficient & effective. Hold: Place a hold on the mortgage foreclosure case, such that the bank may NOT continue with their mortgage foreclosure proceedings. This protects the borrower, while they attempt to work things out with the assistance of their housing counselor.

38 How it works, continued Housing Counseling: Borrower meets with and works with their assigned housing counselor. Housing Counselors look at financials, and the global situation, and either encourage the borrower and/or help the borrower to submit a modification package to the bank, or decide on an alternative strategy. Court time: Once the bank or the borrower becomes unresponsive or uncooperative, we schedule the case for a conciliation hearing before the judge. The borrower, their happened, and decides if there is a deal to be made, or if all parties have truly reached an impasse. Sometimes an extension is granted.

39 How it works, continued Ultimately there are 2 outcomes: Case is settled & discontinued: which means a deal was reached between the borrower and bank/lender. Case is removed:which means that no deal was reached, and it does not appear that a deal can be reached. The hold is lifted, and the bank can continue with the foreclosure proceedings. Outcomes are ordered by the Judge, and as such final.

40 Program Statistics As of October: 1,531 cases were entered into the program 33% participation 214 had been settled & discontinued 261 had been removed 1,056 were still active and working with their counseling agencies.

41 Unique Program attributes -. While all who receive the unique court-identifier are eligible, they must call the hotline to participate. If they do not call, they are not eligible. The have a certain timeframe (20 days) to call, or the bank/lender can continue with the foreclosure process. Housing Counseling is key hits-the- someone can really save their home is done. This is tough & thankless work! Legal Services: Referrals are made for free legal services to income-eligible borrowers upon their request, but usually only if it seems that there was something improper done to set up the original mortgage.

42 New programs: Some of the state/federal program help some people, but -size-fits all pandora that some think. Banks/Lenders: Banks/Lenders are often slow to respond or non-responsive, and are always asked for updated borrower documentation. They also loose a especially local counsel, can be very helpful. Not everyone can save their home counselors to exit gracefully is sometimes the tactic employed. Housing Counseling is Key: Having the borrowers meet with and spend time with the housing counselors to go over where their mortgage is, how it got their, what their household financials are, how they got there, and what can be done to save their home is key. For those who have been able to save their homes, the time & analysis of the trained & certified housing counselors has been key. Buying time is key: By placing a hold on the mortgage foreclosure process so that the borrowers can work on and work out their situation is key. Court time is key: right before of at a conciliation hearing. The pressure of going before a judge, throwing a borrower out is critical.

43 Questions/Comments Cassandra Collinge Manager, Consumer Programs Allegheny County Economic Development 425 Sixth Avenue, Suite 800 Pittsburgh, PA

Eligibility Requirements

December 9, 2010 Program Overview Implemented on January 12, 1009 by the Honorable Joseph M. James, President Judge via an administrative order. Judge James, Sheriff Mullen, the Allegheny County Bar Association

December 9, 2010 Program Overview Implemented on January 12, 1009 by the Honorable Joseph M. James, President Judge via an administrative order. Judge James, Sheriff Mullen, the Allegheny County Bar Association

Homeownership Preservation in Maryland

Maryland Department of Housing and Community Development Homeownership Preservation in Maryland A presentation to the Western Maryland 2008 Small Town Symposium and Rural Roundtable April 23, 2008 Martin

Maryland Department of Housing and Community Development Homeownership Preservation in Maryland A presentation to the Western Maryland 2008 Small Town Symposium and Rural Roundtable April 23, 2008 Martin

HOPE NOW. Snapshot Industry Extrapolations and HAMP Metrics

Snapshot Industry Extrapolations and HAMP Metrics Three Month Q4-2016 Q1-2017 Q2-2017 Q3-2017 Q4-2017 Oct-17 Nov-17 Dec-17 Total Completed Modifications 85,357 89,213 78,302 54,318 56,355 19,400 18,819

Snapshot Industry Extrapolations and HAMP Metrics Three Month Q4-2016 Q1-2017 Q2-2017 Q3-2017 Q4-2017 Oct-17 Nov-17 Dec-17 Total Completed Modifications 85,357 89,213 78,302 54,318 56,355 19,400 18,819

HOPE NOW. Snapshot Industry Extrapolations and HAMP Metrics

Snapshot Industry Extrapolations and HAMP Metrics Three Month Q2-215 Q3-215 Q4-215 Q1-216 Q2-216 Jun-16 Jul-16 Aug-16 Total Completed Modifications 119,658 97,773 84,798 86,167 1,198 41,872 34,815 36,6

Snapshot Industry Extrapolations and HAMP Metrics Three Month Q2-215 Q3-215 Q4-215 Q1-216 Q2-216 Jun-16 Jul-16 Aug-16 Total Completed Modifications 119,658 97,773 84,798 86,167 1,198 41,872 34,815 36,6

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners August 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners August 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

FORECLOSURE PREVENTION PRINCIPAL REDUCTION AND. Preliminary Report, Findings and Recommendations from the IDT. Seattle City Council March 26, 2014

1 PRINCIPAL REDUCTION AND FORECLOSURE PREVENTION Preliminary Report, Findings and Recommendations from the IDT Seattle City Council March 26, 2014 2 IDT Scope of Work Resolution 31495 directed IDT to explore

1 PRINCIPAL REDUCTION AND FORECLOSURE PREVENTION Preliminary Report, Findings and Recommendations from the IDT Seattle City Council March 26, 2014 2 IDT Scope of Work Resolution 31495 directed IDT to explore

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners May 2011 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners May 2011 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

End of the American Dream? How Mortgage Defaults and Foreclosures Affect Families and Communities

End of the American Dream? How Mortgage Defaults and Foreclosures Affect Families and Communities J. Michael Collins Assistant Professor, School of Human Ecology Director, Center for Financial Security

End of the American Dream? How Mortgage Defaults and Foreclosures Affect Families and Communities J. Michael Collins Assistant Professor, School of Human Ecology Director, Center for Financial Security

Review of Northern Virginia Market Conditions and Trends

Review of Northern Virginia Market Conditions and Trends Prepared for Northern Virginia Area Association of Realtors November 12, 2011 Virginia Housing Development Authority Northern Virginia s existing

Review of Northern Virginia Market Conditions and Trends Prepared for Northern Virginia Area Association of Realtors November 12, 2011 Virginia Housing Development Authority Northern Virginia s existing

Servicing Alignment Initiative Overview for Freddie Mac Servicers

Servicing Alignment Initiative Overview for Freddie Mac Servicers Consistent requirements and processes for servicing delinquent mortgages Working at the direction of, and in concert with, the Federal

Servicing Alignment Initiative Overview for Freddie Mac Servicers Consistent requirements and processes for servicing delinquent mortgages Working at the direction of, and in concert with, the Federal

HOPE NOW. Snapshot Industry Extrapolations and HAMP Metrics

Year over Year Q2-211 to H1 212 Q2-211 Q3-211 Q4-211 Q1-212 Q2-212 Apr-212 May-212 Jun-212 Q2-212 Total Completed Modifications 251,424 255,667 24,523 23,463 182,6 56,922 61,489 63,594-28% 385,468 HAMP

Year over Year Q2-211 to H1 212 Q2-211 Q3-211 Q4-211 Q1-212 Q2-212 Apr-212 May-212 Jun-212 Q2-212 Total Completed Modifications 251,424 255,667 24,523 23,463 182,6 56,922 61,489 63,594-28% 385,468 HAMP

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

The Impact of Foreclosures on Economic Recovery in Virginia

The Impact of Foreclosures on Economic Recovery in Virginia February, 2012 Brian Koziol Housing Policy and Research Analyst www.phonehome.org 804.354.0641 Where you live makes all the difference About

The Impact of Foreclosures on Economic Recovery in Virginia February, 2012 Brian Koziol Housing Policy and Research Analyst www.phonehome.org 804.354.0641 Where you live makes all the difference About

Short Sales. Vice President. Lincoln, Nebraska April 12, 2011

Short Sales A guide to working with Wells Fargo Abel Fregoso, Jr Vice President National Field Short Sales Manager Lincoln, Nebraska April 12, 2011 Strategic Partnership Wells Fargo and Our REALTOR Partners

Short Sales A guide to working with Wells Fargo Abel Fregoso, Jr Vice President National Field Short Sales Manager Lincoln, Nebraska April 12, 2011 Strategic Partnership Wells Fargo and Our REALTOR Partners

FORECLOSURE. I don t think I can make my mortgage payments but I don t want to go through a foreclosure. What are some of my options?

FORECLOSURE When you borrow money to buy a house or land, the creditor usually takes a security interest in the property you buy This means that if you don t pay, the creditor can foreclose upon (or take

FORECLOSURE When you borrow money to buy a house or land, the creditor usually takes a security interest in the property you buy This means that if you don t pay, the creditor can foreclose upon (or take

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners April 2012 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners April 2012 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

What is the Servicing Alignment Initiative? Overview:

Servicing Alignment Initiative: Freddie Mac Requirements Overview for Housing Counselors Orlando, September 27, 2011 What is the Servicing Alignment Initiative? Overview: Freddie Mac launched a comprehensive

Servicing Alignment Initiative: Freddie Mac Requirements Overview for Housing Counselors Orlando, September 27, 2011 What is the Servicing Alignment Initiative? Overview: Freddie Mac launched a comprehensive

New Servicing Rules under RESPA Early Intervention, Continuous Contact and Loss Mitigation

New Servicing Rules under RESPA Early Intervention, Continuous Contact and Loss Mitigation FIS Regulatory Advisory Services Regulatory.Services@fisglobal.com New Servicing Rules Under RESPA Early Intervention,

New Servicing Rules under RESPA Early Intervention, Continuous Contact and Loss Mitigation FIS Regulatory Advisory Services Regulatory.Services@fisglobal.com New Servicing Rules Under RESPA Early Intervention,

Faith Schwartz Testifies at TARP Foreclosure Mitigation Programs Hearing

October 27, 2010 Media Contact: Brad Dwin (202) 589-1938 brad@hopenow.com Faith Schwartz Testifies at TARP Foreclosure Mitigation Programs Hearing (WASHINGTON, DC) Faith Schwartz, senior adviser, and former

October 27, 2010 Media Contact: Brad Dwin (202) 589-1938 brad@hopenow.com Faith Schwartz Testifies at TARP Foreclosure Mitigation Programs Hearing (WASHINGTON, DC) Faith Schwartz, senior adviser, and former

STANDARD MODIFICATION

Bulletin NUMBER: 2011-16 TO: Freddie Mac Servicers September 12, 2011 SUBJECTS With this Single-Family Seller/Servicer Guide ( Guide ) Bulletin, we are announcing complete requirements related to the Freddie

Bulletin NUMBER: 2011-16 TO: Freddie Mac Servicers September 12, 2011 SUBJECTS With this Single-Family Seller/Servicer Guide ( Guide ) Bulletin, we are announcing complete requirements related to the Freddie

HOPE NOW Alliance. Statement for the Record. Committee on Oversight and Government Reform. U.S. House of Representatives. Hearing

HOPE NOW Alliance Statement for the Record Committee on Oversight and Government Reform U.S. House of Representatives Hearing Foreclosure Prevention Part II: Are Loan Servicers Honoring Their Commitments

HOPE NOW Alliance Statement for the Record Committee on Oversight and Government Reform U.S. House of Representatives Hearing Foreclosure Prevention Part II: Are Loan Servicers Honoring Their Commitments

HOPE NOW Reports 99K Mortgage Solutions for Homeowners in November K Permanent Loan Modifications Completed for the Month

January 27, 2016 Media Contact: Oliver Jakubos (202) 589-2415 Oliver.Jakubos@fsroundtable.org HOPE NOW Reports 99K Mortgage Solutions for Homeowners in November 2015 26K Permanent Loan Modifications Completed

January 27, 2016 Media Contact: Oliver Jakubos (202) 589-2415 Oliver.Jakubos@fsroundtable.org HOPE NOW Reports 99K Mortgage Solutions for Homeowners in November 2015 26K Permanent Loan Modifications Completed

M O D I F I C AT I O N PA M P H L E T

THE STATE BAR OF TEXAS LOAN M O D I F I C AT I O N SCAM PA M P H L E T As the number of foreclosures grows, many thieves are swindling money from homeowners by preying upon fears of losing a home. The

THE STATE BAR OF TEXAS LOAN M O D I F I C AT I O N SCAM PA M P H L E T As the number of foreclosures grows, many thieves are swindling money from homeowners by preying upon fears of losing a home. The

REFORMS Overview of Reforms to Mortgage and Foreclosure Processing Standards in the Settlement

Office of WV Attorney General Darrell McGraw MORTGAGE FORECLOSURE SETTLEMENT REFORMS Overview of Reforms to Mortgage and Foreclosure Processing Standards in the Settlement As negotiated nationally I. RETURN

Office of WV Attorney General Darrell McGraw MORTGAGE FORECLOSURE SETTLEMENT REFORMS Overview of Reforms to Mortgage and Foreclosure Processing Standards in the Settlement As negotiated nationally I. RETURN

Uniform Rules of Practice Circuit Court of Illinois Nineteenth Judicial Circuit

If a l ~ DEC 1 4 2015 Uniform Rules of Practice Circuit Court of Illinois Nineteenth Judicial Circuit ~~ CIRCUIT CLERK Amendment to Rule 19.00, LAKE COUNTY RESIDENTIAL REAL ESTATE MORTGAGE FORECLOSURE

If a l ~ DEC 1 4 2015 Uniform Rules of Practice Circuit Court of Illinois Nineteenth Judicial Circuit ~~ CIRCUIT CLERK Amendment to Rule 19.00, LAKE COUNTY RESIDENTIAL REAL ESTATE MORTGAGE FORECLOSURE

MAINE STATE LEGISLATURE

MAINE STATE LEGISLATURE The following document is provided by the LAW AND LEGISLATIVE DIGITAL LIBRARY at the Maine State Law and Legislative Reference Library http://legislature.maine.gov/lawlib Reproduced

MAINE STATE LEGISLATURE The following document is provided by the LAW AND LEGISLATIVE DIGITAL LIBRARY at the Maine State Law and Legislative Reference Library http://legislature.maine.gov/lawlib Reproduced

FORECLOSURE PREVENTION

FORECLOSURE PREVENTION 1/1/2012 Resource Guide Brought to you by: NAACP Economic Department 1816 12 th Street, NW Washington DC 20009 www.naacp.org/econ Foreclosure prevention R E S O U R C E G U I D E

FORECLOSURE PREVENTION 1/1/2012 Resource Guide Brought to you by: NAACP Economic Department 1816 12 th Street, NW Washington DC 20009 www.naacp.org/econ Foreclosure prevention R E S O U R C E G U I D E

Making Home Affordable

Making Home Affordable Working Together to Help Homeowners Response to the Crisis MHA is part of Administration approach to promoting stability for housing market, homeowners. Homeowner Affordability and

Making Home Affordable Working Together to Help Homeowners Response to the Crisis MHA is part of Administration approach to promoting stability for housing market, homeowners. Homeowner Affordability and

Specialized Loan Servicing LLC ( SLS ) Home Affordable Foreclosure Alternative (HAFA) Matrix

Home Affordable Foreclosure Alternative (HAFA) Matrix") Specialized Loan Servicing LLC ( SLS ) Home Affordable Foreclosure Alternative (HAFA) Matrix All servicers that have signed agreements with the U.S. Department of the Treasury (Treasury) to participate

Specialized Loan Servicing LLC ( SLS ) Home Affordable Foreclosure Alternative (HAFA) Matrix All servicers that have signed agreements with the U.S. Department of the Treasury (Treasury) to participate

Department of Legislative Services Maryland General Assembly 2010 Session

Department of Legislative Services Maryland General Assembly 2010 Session HB 472 FISCAL AND POLICY NOTE Revised House Bill 472 (Delegate Niemann and the Speaker, et al.) (By Request - Administration) Environmental

Department of Legislative Services Maryland General Assembly 2010 Session HB 472 FISCAL AND POLICY NOTE Revised House Bill 472 (Delegate Niemann and the Speaker, et al.) (By Request - Administration) Environmental

Making Home Affordable Working Together to Help Homeowners

Making Home Affordable Working Together to Help Homeowners MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure. Transition from Home Ownership Historically

Making Home Affordable Working Together to Help Homeowners MHA Offers Solutions MHA and related programs work together to help homeowners avoid foreclosure. Transition from Home Ownership Historically

Foreclosure Diversion Program Information Session. Understanding and Preparing for Mediation

Foreclosure Diversion Program Information Session Understanding and Preparing for Mediation *For more detailed information and additional resources, go to the Pine Tree Legal website at www.ptla.org/foreclosure-prevention-toolkit

Foreclosure Diversion Program Information Session Understanding and Preparing for Mediation *For more detailed information and additional resources, go to the Pine Tree Legal website at www.ptla.org/foreclosure-prevention-toolkit

Welcome to your Homeowner s Guide to Success

Welcome to your Homeowner s Guide to Success Hardships create difficult situations and require difficult decisions. If you re experiencing a hardship, you might be wondering what bills to pay and if you

Welcome to your Homeowner s Guide to Success Hardships create difficult situations and require difficult decisions. If you re experiencing a hardship, you might be wondering what bills to pay and if you

Housing Partnership is a HUD Approved Nonprofit Organization

Dear Homeowner(s): Congratulations for taking that tough first step and contacting the Housing Partnership about your mortgage. There is no charge for this program and we advise you consider working with

Dear Homeowner(s): Congratulations for taking that tough first step and contacting the Housing Partnership about your mortgage. There is no charge for this program and we advise you consider working with

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners November 2012 U.S. Department U.S Department of Housing of Housing and Urban and Urban Development Development

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners November 2012 U.S. Department U.S Department of Housing of Housing and Urban and Urban Development Development

Chancery Division Mortgage Foreclosure Mediation Program

STATE OF ILLINOIS CIRCUIT COURT OF COOK COUNTY Chancery Division Mortgage Foreclosure Mediation Program PROGRESS REPORT August 29, 2016 HONORABLE TIMOTHY C. EVANS CHIEF JUDGE CIRCUIT COURT OF COOK COUNTY

STATE OF ILLINOIS CIRCUIT COURT OF COOK COUNTY Chancery Division Mortgage Foreclosure Mediation Program PROGRESS REPORT August 29, 2016 HONORABLE TIMOTHY C. EVANS CHIEF JUDGE CIRCUIT COURT OF COOK COUNTY

Home Mortgage Foreclosures in Maine

Home Mortgage Foreclosures in Maine Find more easy-to-read legal information at www.ptla.org Important Note: This is very general information about home mortgage and foreclosure rules in Maine. It is not

Home Mortgage Foreclosures in Maine Find more easy-to-read legal information at www.ptla.org Important Note: This is very general information about home mortgage and foreclosure rules in Maine. It is not

First wave: Driven by loan terms & home values. Second wave: Driven by unemployment. Various local, state and federal responses

Sustainable Loan Modifications June 2009 J. Michael Collins Introduction Foreclosures at record levels First wave: Driven by loan terms & home values» Concentration in sand states and LMI communities (but

Sustainable Loan Modifications June 2009 J. Michael Collins Introduction Foreclosures at record levels First wave: Driven by loan terms & home values» Concentration in sand states and LMI communities (but

Ohio and Pennsylvania: Two Approaches to Judicial Foreclosure Alternatives

Page1 Introduction 1 As the number of foreclosures continues to rise across the country, many policymakers are creating alternatives to foreclosure. Two counties in the Federal Reserve s Fourth District

Page1 Introduction 1 As the number of foreclosures continues to rise across the country, many policymakers are creating alternatives to foreclosure. Two counties in the Federal Reserve s Fourth District

Florida: An Economic Overview

Florida: An Economic Overview March 31, 2014 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Economy

Florida: An Economic Overview March 31, 2014 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Economy

Information on Avoiding Foreclosure

Information on Avoiding Foreclosure Learn more About Options to Avoid Foreclosure The variety of options summarized below may help you keep your home. For example, you may be eligible to modify your mortgage,

Information on Avoiding Foreclosure Learn more About Options to Avoid Foreclosure The variety of options summarized below may help you keep your home. For example, you may be eligible to modify your mortgage,

ATTACHMENT #1 Special LF&A Meeting of July 16, "Preventing Foreclosure: Potential Tools for Delawareans"

ATTACHMENT #1 Special LF&A Meeting of July 16, 2007 "Preventing Foreclosure: Potential Tools for Delawareans" Outline Sub-prime Snapshot Delaware Emergency Mortgage Assistance Program (DEMAP) Refinance

ATTACHMENT #1 Special LF&A Meeting of July 16, 2007 "Preventing Foreclosure: Potential Tools for Delawareans" Outline Sub-prime Snapshot Delaware Emergency Mortgage Assistance Program (DEMAP) Refinance

Home Mortgage Foreclosures in Maine

Home Mortgage Foreclosures in Maine Find more easy-to-read legal information at www.ptla.org Important Note: This is very general information about home mortgage and foreclosure rules in Maine. It is not

Home Mortgage Foreclosures in Maine Find more easy-to-read legal information at www.ptla.org Important Note: This is very general information about home mortgage and foreclosure rules in Maine. It is not

U.S. Housing Markets: Looking Back, Looking Forward

U.S. Housing Markets: Looking Back, Looking Forward Dr. Raphael Bostic Assistant Secretary, Office of Policy Development and Research U.S. Department of Housing and Urban Development Special Thanks Ed

U.S. Housing Markets: Looking Back, Looking Forward Dr. Raphael Bostic Assistant Secretary, Office of Policy Development and Research U.S. Department of Housing and Urban Development Special Thanks Ed

An Attorney s Options for Handling Clients in Trouble with Real Estate. Aka: Forbearance to Bankruptcy and Everything in Between

An Attorney s Options for Handling Clients in Trouble with Real Estate Aka: Forbearance to Bankruptcy and Everything in Between Erica Crohn Minchella ~ Attorney at Law 7538 St. Louis Ave Skokie, IL 60076

An Attorney s Options for Handling Clients in Trouble with Real Estate Aka: Forbearance to Bankruptcy and Everything in Between Erica Crohn Minchella ~ Attorney at Law 7538 St. Louis Ave Skokie, IL 60076

Review of Regional Market Conditions in the Greater Piedmont Area

Review of Regional Market Conditions in the Greater Piedmont Area Greater Piedmont Area Association of Realtors June 7, 2010 Virginia Housing Development Authority Overview of Current Market Conditions

Review of Regional Market Conditions in the Greater Piedmont Area Greater Piedmont Area Association of Realtors June 7, 2010 Virginia Housing Development Authority Overview of Current Market Conditions

Foreclosures: Introduction and Update

Foreclosures: Introduction and Update Ann M. Anderson Superior Court Judges Summer Conference June 23 26, 2009 Review of Foreclosure Procedure Clerk s Role Judge s Role (Appeal, Injunction) 2008 Legislation

Foreclosures: Introduction and Update Ann M. Anderson Superior Court Judges Summer Conference June 23 26, 2009 Review of Foreclosure Procedure Clerk s Role Judge s Role (Appeal, Injunction) 2008 Legislation

Once we have received and evaluated your information, we will contact you regarding your options and next steps.

We Are Here to Help You It is critical that you work with us on a resolution for any issues that affect your ability to make timely mortgage payments, whether your challenges are temporary or long term.

We Are Here to Help You It is critical that you work with us on a resolution for any issues that affect your ability to make timely mortgage payments, whether your challenges are temporary or long term.

PREPARED REMARKS FOR DAVID H. STEVENS ASSISTANT SECRETARY FOR HOUSING FHA COMMISSIONER U.S

PREPARED REMARKS FOR DAVID H. STEVENS ASSISTANT SECRETARY FOR HOUSING FHA COMMISSIONER U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT AT THE THE WORLD BANK 4 TH GLOBAL CONFERENCE ON HOUSING FINANCE IN

PREPARED REMARKS FOR DAVID H. STEVENS ASSISTANT SECRETARY FOR HOUSING FHA COMMISSIONER U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT AT THE THE WORLD BANK 4 TH GLOBAL CONFERENCE ON HOUSING FINANCE IN

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac Hearing of the U.S. Senate Committee on Banking, Housing and Urban Affairs Chairman Dodd, Ranking

Statement of Donald Bisenius Executive Vice President Single Family Credit Guarantee Business Freddie Mac Hearing of the U.S. Senate Committee on Banking, Housing and Urban Affairs Chairman Dodd, Ranking

The National Mortgage Settlement: July 31, :00 4:00pm

U.S. Department of Housing and Urban Development The National Mortgage Settlement: What Does it Mean for NSP? July 31, 2012 2:00 4:00pm Webinar Objectives Today Provide an overview of the National Mortgage

U.S. Department of Housing and Urban Development The National Mortgage Settlement: What Does it Mean for NSP? July 31, 2012 2:00 4:00pm Webinar Objectives Today Provide an overview of the National Mortgage

Homeownership Protection: Property Taxes Foreclosure Prevention Avoiding Home Scams

Building Generational Wealth Webcast Homeownership Protection: Property Taxes Foreclosure Prevention Avoiding Home Scams Sarah Stein, Staff Attorney, Atlanta Legal Aid Darrius Woods, Equal Justice Works

Building Generational Wealth Webcast Homeownership Protection: Property Taxes Foreclosure Prevention Avoiding Home Scams Sarah Stein, Staff Attorney, Atlanta Legal Aid Darrius Woods, Equal Justice Works

WORRIED. about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA)

") WORRIED about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA) Keeping families in their homes is a top priority for REALTORS. Unfortunately, it is not always

WORRIED about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA) Keeping families in their homes is a top priority for REALTORS. Unfortunately, it is not always

Home Affordable Unemployment Program (UP)

") Home Affordable Unemployment Program (UP) Training for Servicers 1 Agenda 1 2 Phase 1 Phase 2 Phase 3 3 4 Overview UP Process Evaluation Phase Forbearance Period Transition Phase Reporting Requirements

Home Affordable Unemployment Program (UP) Training for Servicers 1 Agenda 1 2 Phase 1 Phase 2 Phase 3 3 4 Overview UP Process Evaluation Phase Forbearance Period Transition Phase Reporting Requirements

Florida: An Economic Overview

Florida: An Economic Overview May 14, 2014 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Economy

Florida: An Economic Overview May 14, 2014 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Economy

Supplemental Directive November 3, Home Affordable Modification Program Borrower Notices

Supplemental Directive 09-08 November 3, 2009 Home Affordable Modification Program Borrower Notices Background In Supplemental Directive 09-01, the Treasury Department (Treasury) announced the eligibility,

Supplemental Directive 09-08 November 3, 2009 Home Affordable Modification Program Borrower Notices Background In Supplemental Directive 09-01, the Treasury Department (Treasury) announced the eligibility,

Effective Foreclosure Timeline Management Reference Guide

Effective Foreclosure Timeline Management Reference Guide A foreclosure timeline is the number of days it takes to process a foreclosure, from the due date of the last paid installment (DDLPI) to the foreclosure

Effective Foreclosure Timeline Management Reference Guide A foreclosure timeline is the number of days it takes to process a foreclosure, from the due date of the last paid installment (DDLPI) to the foreclosure

The Emergency Program to Reduce Home Foreclosures

The Emergency Program to Reduce Home Foreclosures Report to Joint Legislative Commission on Governmental Operations February 13, 2009 Introduction This report is submitted pursuant to the Emergency Program

The Emergency Program to Reduce Home Foreclosures Report to Joint Legislative Commission on Governmental Operations February 13, 2009 Introduction This report is submitted pursuant to the Emergency Program

OVERVIEW GUIDE TO HOME COUNSELOR ONLINE NATIONAL FORECLOSURE MITIGATION COUNSELING (NFMC) FEATURES

FEATURES") OVERVIEW GUIDE TO HOME COUNSELOR ONLINE NATIONAL FORECLOSURE MITIGATION COUNSELING (NFMC) FEATURES WHO SHOULD USE THIS OVERVIEW GUIDE? WHAT IS NFMC? This overview guide contains information for Home Counselor

OVERVIEW GUIDE TO HOME COUNSELOR ONLINE NATIONAL FORECLOSURE MITIGATION COUNSELING (NFMC) FEATURES WHO SHOULD USE THIS OVERVIEW GUIDE? WHAT IS NFMC? This overview guide contains information for Home Counselor

Out of the Shadows: Projected Levels for Future REO Inventory

ECONOMIC COMMENTARY Number 2010-14 October 19, 2010 Out of the Shadows: Projected Levels for Future REO Inventory Guhan Venkatu Nearly one homeowner in ten is more than 90 days delinquent on his mortgage

ECONOMIC COMMENTARY Number 2010-14 October 19, 2010 Out of the Shadows: Projected Levels for Future REO Inventory Guhan Venkatu Nearly one homeowner in ten is more than 90 days delinquent on his mortgage

Glossary. An item of value that you own.

Term A adjustable-rate mortgage (ARM) amortization amortized annual percentage rate (APR) appraisal appreciation assessment fees asset association fees Definition A mortgage loan with an interest rate

Term A adjustable-rate mortgage (ARM) amortization amortized annual percentage rate (APR) appraisal appreciation assessment fees asset association fees Definition A mortgage loan with an interest rate

June 29, 2011 Acting Director Edward DeMarco Federal Housing Finance Agency 1700 G Street, NW, 4th Floor Washington, DC 20552

June 29, 2011 Acting Director Edward DeMarco Federal Housing Finance Agency 1700 G Street, NW, 4th Floor Washington, DC 20552 Dear Acting Director DeMarco, On April 28, 2011, the Federal Housing Finance

June 29, 2011 Acting Director Edward DeMarco Federal Housing Finance Agency 1700 G Street, NW, 4th Floor Washington, DC 20552 Dear Acting Director DeMarco, On April 28, 2011, the Federal Housing Finance

The National Mortgage Settlement: Loan Modifications and Servicing Standards

The National Mortgage Settlement: Loan Modifications and Servicing Standards MHA Trusted Advisor Webinar July 24, 2013 Sarah Bolling Mancini Home Defense Program of the Atlanta Legal Aid Society, Inc.

The National Mortgage Settlement: Loan Modifications and Servicing Standards MHA Trusted Advisor Webinar July 24, 2013 Sarah Bolling Mancini Home Defense Program of the Atlanta Legal Aid Society, Inc.

Short Sale Seller Advisory. Before Proceeding with a Short Sale. Arizona Department of Real Estate. Arizona Association of REALTORS

A short sale is a real estate transaction in which the sales price is insufficient to pay the loan(s) encumbering the property in addition to the costs of sale and the seller is unable to pay the difference.

A short sale is a real estate transaction in which the sales price is insufficient to pay the loan(s) encumbering the property in addition to the costs of sale and the seller is unable to pay the difference.

National Foreclosure Mitigation Counseling Program FINAL Funding Announcement for Round 5 Funds. December 1, 2010

National Foreclosure Mitigation Counseling Program FINAL Funding Announcement for Round 5 Funds December 1, 2010 P a g e National Foreclosure Mitigation Counseling Program Funding Announcement National

National Foreclosure Mitigation Counseling Program FINAL Funding Announcement for Round 5 Funds December 1, 2010 P a g e National Foreclosure Mitigation Counseling Program Funding Announcement National

Making Home Affordable MHA and Impacts from the Consumer Financial Protection Bureaus New Mortgage Servicing Regulations

Making Home Affordable MHA and Impacts from the Consumer Financial Protection Bureaus New Mortgage Servicing Regulations Overview MHA Updates effective January 10, 2014 MHA updated guidance for HAMP, UP,

Making Home Affordable MHA and Impacts from the Consumer Financial Protection Bureaus New Mortgage Servicing Regulations Overview MHA Updates effective January 10, 2014 MHA updated guidance for HAMP, UP,

Foreclosure Process in Minnesota

Foreclosure Process in Minnesota Foreclosure by Advertisement Missed payments 6 weeks before sale 4 weeks before sale Sheriff s Sale Missed payment notices Default / intent to foreclose notice Pre foreclosure

Foreclosure Process in Minnesota Foreclosure by Advertisement Missed payments 6 weeks before sale 4 weeks before sale Sheriff s Sale Missed payment notices Default / intent to foreclose notice Pre foreclosure

WORRIED. about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA)

") WORRIED about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA) About HAFA Keeping families in their homes is a top priority for REALTORS. While there are loan

WORRIED about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA) About HAFA Keeping families in their homes is a top priority for REALTORS. While there are loan

H.E.L.P. COMMUNITY DEVELOPMENT CORP. Foreclosure Counseling Program DOCUMENT CHECKLIST

H.E.L.P. COMMUNITY DEVELOPMENT CORP. Foreclosure Counseling Program DOCUMENT CHECKLIST PLEASE COMPLETE ITEMS 1 AND 2 BELOW AND FAX OR MAIL BACK TO OUR OFFICE. Complete the INTAKE FORMS as thoroughly as

H.E.L.P. COMMUNITY DEVELOPMENT CORP. Foreclosure Counseling Program DOCUMENT CHECKLIST PLEASE COMPLETE ITEMS 1 AND 2 BELOW AND FAX OR MAIL BACK TO OUR OFFICE. Complete the INTAKE FORMS as thoroughly as

First Lien Modification Program Home Affordable Modification Program. Phase 1 Engagement

First Lien Modification Program Home Affordable Modification Program Objective The objective of this three part training series is to assist servicers in the execution of the Home Affordable Modification

First Lien Modification Program Home Affordable Modification Program Objective The objective of this three part training series is to assist servicers in the execution of the Home Affordable Modification

Testimony of Dean Baker. Before the Subcommittee on Housing and Community Opportunity of the House Financial Services Committee

Testimony of Dean Baker Before the Subcommittee on Housing and Community Opportunity of the House Financial Services Committee Hearing on the Recently Announced Revisions to the Home Affordable Modification

Testimony of Dean Baker Before the Subcommittee on Housing and Community Opportunity of the House Financial Services Committee Hearing on the Recently Announced Revisions to the Home Affordable Modification

THE POLICY RESPONSE TO FORECLOSURES:

THE POLICY RESPONSE TO FORECLOSURES: WHAT CAN STATE AND LOCAL ACTORS DO? PRESENTATION TO THE MISSOURI HOMEOWNERSHIP PRESERVATION SUMMIT JANUARY 14, 2010 JEFFERSON CITY, MISSOURI Spillover Effects of Foreclosures

THE POLICY RESPONSE TO FORECLOSURES: WHAT CAN STATE AND LOCAL ACTORS DO? PRESENTATION TO THE MISSOURI HOMEOWNERSHIP PRESERVATION SUMMIT JANUARY 14, 2010 JEFFERSON CITY, MISSOURI Spillover Effects of Foreclosures

Federal Housing Legislation and Dallas Foreclosure Update. A Briefing To The Housing Committee September 2, 2008

Federal Housing Legislation and Dallas Foreclosure Update A Briefing To The Housing Committee September 2, 2008 Purpose To provide: An update on the status of foreclosures in the City of Dallas and the

Federal Housing Legislation and Dallas Foreclosure Update A Briefing To The Housing Committee September 2, 2008 Purpose To provide: An update on the status of foreclosures in the City of Dallas and the

Understanding the National Mortgage Settlement A Guide for Housing Counselors

Understanding the National Mortgage Settlement A Guide for Housing Counselors June 2013 Copyright 2013, National Consumer Law Center, Inc. All rights reserved. This work is copyrighted by the National

Understanding the National Mortgage Settlement A Guide for Housing Counselors June 2013 Copyright 2013, National Consumer Law Center, Inc. All rights reserved. This work is copyrighted by the National

florida ARECS Save Your Deal. Save Your Client. Realtor s Distressed Property Guide Revised January 2017

florida TM ARECS Save Your Deal. Save Your Client. Realtor s Distressed Property Guide Revised January 2017 YOUR JOB DESCRIPTION HAS CHANGED DRAMATICALLY... If your deal is in danger of getting pulled

florida TM ARECS Save Your Deal. Save Your Client. Realtor s Distressed Property Guide Revised January 2017 YOUR JOB DESCRIPTION HAS CHANGED DRAMATICALLY... If your deal is in danger of getting pulled

Florida: An Economic Overview

Florida: An Economic Overview August 21, 2013 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Global

Florida: An Economic Overview August 21, 2013 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Global

National Housing Market Summary

1st 2017 June 2017 HUD PD&R National Housing Market Summary The Housing Market Recovery Showed Progress in the First The housing market improved in the first quarter of 2017. Construction starts rose for

1st 2017 June 2017 HUD PD&R National Housing Market Summary The Housing Market Recovery Showed Progress in the First The housing market improved in the first quarter of 2017. Construction starts rose for

U.S. HOUSING RECOVERY WILL NOT DROWN IN A SEA OF DISTRESSED SALES

OBSERVATION TD Economics February 3, 1 U.S. HOUSING RECOVERY WILL NOT DROWN IN A SEA OF DISTRESSED SALES Highlights The housing market is showing signs of life. Home sales and housing starts are rising

OBSERVATION TD Economics February 3, 1 U.S. HOUSING RECOVERY WILL NOT DROWN IN A SEA OF DISTRESSED SALES Highlights The housing market is showing signs of life. Home sales and housing starts are rising

This Month in Real Estate

Keller Williams Research This Month in Real Estate Released: December 4, 2009 Commentary. 2 The Numbers That Drive Real Estate 3 Recent Government Action. 9 Topics for Buyers and Sellers. 15 1 Steps to

Keller Williams Research This Month in Real Estate Released: December 4, 2009 Commentary. 2 The Numbers That Drive Real Estate 3 Recent Government Action. 9 Topics for Buyers and Sellers. 15 1 Steps to

NATIONAL FORECLOSURE MITIGATION COUNSELING PROGRAM (NFMC)

") APRIL 2014 21.000 NATIONAL FORECLOSURE MITIGATION COUNSELING PROGRAM State Project/Program: NATIONAL FORECLOSURE MITIGATION COUNSELING PROGRAM (NFMC) US Department of Treasury Neighborhood Reinvestment

APRIL 2014 21.000 NATIONAL FORECLOSURE MITIGATION COUNSELING PROGRAM State Project/Program: NATIONAL FORECLOSURE MITIGATION COUNSELING PROGRAM (NFMC) US Department of Treasury Neighborhood Reinvestment

Making Home Affordable Case Escalation Process Training Presentation for Servicers

Making Home Affordable Case Escalation Process Training Presentation for s August July 2014 2014 Making Home Home Affordable Home Affordable July 2016 Objectives Defining Escalated Cases Commonly Escalated

Making Home Affordable Case Escalation Process Training Presentation for s August July 2014 2014 Making Home Home Affordable Home Affordable July 2016 Objectives Defining Escalated Cases Commonly Escalated

LOAN DEFAULT AND FORECLOSURE: A BRIEF GUIDE FOR CALIFORNIA HOMEOWNERS

LOAN DEFAULT AND FORECLOSURE: A BRIEF GUIDE FOR CALIFORNIA HOMEOWNERS Compiled by: UNIVERSITY OF SAN FRANCISCO, SCHOOL OF LAW PREDATORY LENDING CLINIC Provided by: COMMUNITY LEGAL SERVICES IN EAST PALO

LOAN DEFAULT AND FORECLOSURE: A BRIEF GUIDE FOR CALIFORNIA HOMEOWNERS Compiled by: UNIVERSITY OF SAN FRANCISCO, SCHOOL OF LAW PREDATORY LENDING CLINIC Provided by: COMMUNITY LEGAL SERVICES IN EAST PALO

Homeowner Affordability and Stability Plan Fact Sheet

Homeowner Affordability and Stability Plan Fact Sheet The deep contraction in the economy and in the housing market has created devastating consequences for homeowners and communities throughout the country.

Homeowner Affordability and Stability Plan Fact Sheet The deep contraction in the economy and in the housing market has created devastating consequences for homeowners and communities throughout the country.

HOPE NOW Homeownership. Eric Selk Outreach Director HOPE NOW Alliance

HOPE NOW Homeownership Preservation Workshops Eric Selk Outreach Director HOPE NOW Alliance Outline HOPE NOW Overview Outreach Overview Outreach Participation Attendance Partners Results Same Day MHA Survey

HOPE NOW Homeownership Preservation Workshops Eric Selk Outreach Director HOPE NOW Alliance Outline HOPE NOW Overview Outreach Overview Outreach Participation Attendance Partners Results Same Day MHA Survey

A look Behind the numbers Winter Behind the numbers. A Look. Distressed Loans in Ohio:

A look Behind the numbers Winter 2013 Published By The Federal Reserve Bank of Cleveland Behind the numbers A Look written by Lisa Nelson and Francisca G.-C. Richter 9 147 3 Distressed Loans in Ohio: Recent

A look Behind the numbers Winter 2013 Published By The Federal Reserve Bank of Cleveland Behind the numbers A Look written by Lisa Nelson and Francisca G.-C. Richter 9 147 3 Distressed Loans in Ohio: Recent

HUD-9902 Desk Guide. Don't Forget! HUD-9902 Category. How to Complete

Don't Forget! Data is CUMULATIVE! For example, your Q3 report should include all households served from Q1 - Q3. If your agency received HUD approval mid-way through the fiscal year, you should still report

Don't Forget! Data is CUMULATIVE! For example, your Q3 report should include all households served from Q1 - Q3. If your agency received HUD approval mid-way through the fiscal year, you should still report

Florida: An Economic Overview

Florida: An Economic Overview September 15, 2014 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Economy

Florida: An Economic Overview September 15, 2014 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Economy

HFA Mortgage Assistance Programs Servicer Q&A

HFA Mortgage Assistance Programs Servicer Q&A Freddie Mac is reinforcing its on-going commitment to help financially distressed homeowners with Freddie Mac-owned or guaranteed mortgages avoid foreclosure

HFA Mortgage Assistance Programs Servicer Q&A Freddie Mac is reinforcing its on-going commitment to help financially distressed homeowners with Freddie Mac-owned or guaranteed mortgages avoid foreclosure

Fannie Mae and Freddie Mac Have The Same Short Sale Rules and Policies

Fannie Mae and Freddie Mac Have The Same Short Sale Rules and Policies Effective September 1, 2011 There are approximately 3.3 million Americans who are in or close to foreclosure. Fannie Mae and Freddie

Fannie Mae and Freddie Mac Have The Same Short Sale Rules and Policies Effective September 1, 2011 There are approximately 3.3 million Americans who are in or close to foreclosure. Fannie Mae and Freddie

1. Host series of Pre foreclosure workshops, housing fairs, homeownership education classes, and home repair seminars

Pre-Purchase/ Post-Purchase education and counseling is a vital part of the new home buyer education process because it supports successful long-term self-sufficiency. Rhodes Porter understands the first

Pre-Purchase/ Post-Purchase education and counseling is a vital part of the new home buyer education process because it supports successful long-term self-sufficiency. Rhodes Porter understands the first

FHA FIXED RATE AND ADJUSTABLE RATE MORTGAGE

FHA FIXED RATE AND ADJUSTABLE RATE MORTGAGE PRIMARY RESIDENCE PURCHASE /C Amount * 1 Unit/PUD/condo 2 Units ** 96.50% 96.50% FHA Total Mortgage Scorecard DU Approved or 3 to 4 Units ** 96.50% FHA Total

FHA FIXED RATE AND ADJUSTABLE RATE MORTGAGE PRIMARY RESIDENCE PURCHASE /C Amount * 1 Unit/PUD/condo 2 Units ** 96.50% 96.50% FHA Total Mortgage Scorecard DU Approved or 3 to 4 Units ** 96.50% FHA Total

HAMP Resolution Matrix

Homeowner HAMP Eligibility Issues HAMP Resolution Matrix 1 (1) Verify whether the property is owner occupied (for HAMP Tier 2 rental properties, must have missed 2 or more payments). Homeowner is (2) Verify

Homeowner HAMP Eligibility Issues HAMP Resolution Matrix 1 (1) Verify whether the property is owner occupied (for HAMP Tier 2 rental properties, must have missed 2 or more payments). Homeowner is (2) Verify

Home Affordable Foreclosure Alternatives (HAFA) Guidelines and Overview Packet

Guidelines and Overview Packet") Home Affordable Foreclosure Alternatives (HAFA) Guidelines and Overview Packet Distressed Property Institute, LLC 2009. The Distressed Property Institute, LLC assumes no responsibility nor guarantees the

Home Affordable Foreclosure Alternatives (HAFA) Guidelines and Overview Packet Distressed Property Institute, LLC 2009. The Distressed Property Institute, LLC assumes no responsibility nor guarantees the

Florida: An Economic Overview

Florida: An Economic Overview February 5, 2015 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Economy

Florida: An Economic Overview February 5, 2015 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Key Economic Variables Improving Economy

Mary M. Holder Manager, FC Prevention Programs NC Housing Finance Agency

Mary M. Holder Manager, FC Prevention Programs NC Housing Finance Agency Help reduce unnecessary foreclosures by facilitating communication between homeowners, servicers and housing counselors prior to

Mary M. Holder Manager, FC Prevention Programs NC Housing Finance Agency Help reduce unnecessary foreclosures by facilitating communication between homeowners, servicers and housing counselors prior to

How to Stop and Avoid Foreclosure in Today's Market

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

How to Stop and Avoid Foreclosure in Today's Market This Guide Aims To Help You Navigate the foreclosure process [Type the company name] Discover all of your options [Pick the date] Find the solution or

Freddie Mac Standard and Streamlined Modification. Reference Guide. September 2017

Freddie Mac Standard and Streamlined Modification Reference Guide September 2017 This Page Intentionally Left Blank Table of Contents Introduction... 1 What is a Loan Modification?... 1 Freddie Mac Standard

Freddie Mac Standard and Streamlined Modification Reference Guide September 2017 This Page Intentionally Left Blank Table of Contents Introduction... 1 What is a Loan Modification?... 1 Freddie Mac Standard

Home Affordable Modification Program Policies and Procedures Manual

Home Affordable Modification Program Policies and Procedures Manual Policies and procedures herein apply generally to loans subserviced by Franklin Credit Management Corporation, and are integrated with

Home Affordable Modification Program Policies and Procedures Manual Policies and procedures herein apply generally to loans subserviced by Franklin Credit Management Corporation, and are integrated with

The Current Foreclosure Crisis Trends and Roadblocks to Recovery

The Current Foreclosure Crisis Trends and Roadblocks to Recovery American Planning Association February 22, 2011 Geoff Smith Senior Vice President Woodstock Institute Chicago, Illinois gsmith@woodstockinst.org

The Current Foreclosure Crisis Trends and Roadblocks to Recovery American Planning Association February 22, 2011 Geoff Smith Senior Vice President Woodstock Institute Chicago, Illinois gsmith@woodstockinst.org

Quality Right Party Contact and Borrower Solicitation

It is important to establish contact early and often with borrowers who have become delinquent in their mortgage payments and begin considering options that may be appropriate to bring the mortgage current.

It is important to establish contact early and often with borrowers who have become delinquent in their mortgage payments and begin considering options that may be appropriate to bring the mortgage current.