Global and Australian economic outlook

|

|

|

- Antony James

- 6 years ago

- Views:

Transcription

1 Economic Research November 2015 Global and Australian economic outlook (Still) the dark side of the boom Stephen Walters Chief Economist Australia and New Zealand J.P. Morgan Australia Limited See the end pages of this presentation for important disclosures.

2 Global GDP growth to be above trend by end 2015 (just) 2

3 but growth downgrades are dominating (again) GDP growth - major economies and zones % over year Change since % of Aust Last change start of '15 (a) Exports Emerging economies India China Asia ex. China/India EMEA EM Latin America Developed economies Australia na United States Canada United Kingdom New Zealand Euro-area Japan Australia's export partners World (Consensus) Source: J.P. Morgan, Consensus Economics. (a) Average growth for 2015 and

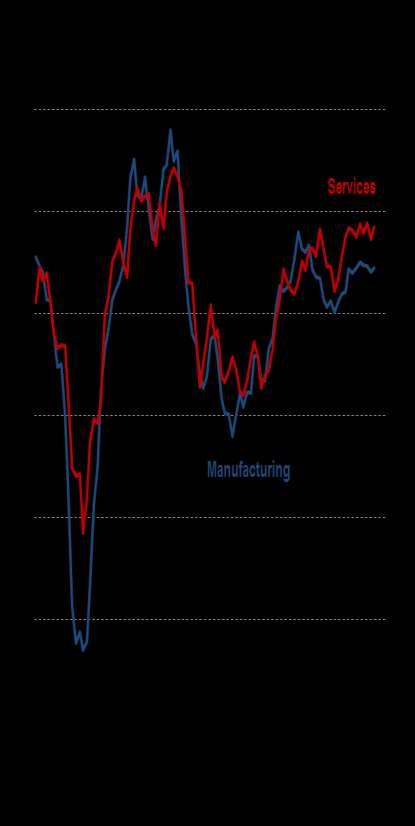

4 Largest downward growth revisions have been in emerging world 4

5 No lift in Aussie trading partner GDP growth expected in

6 Main risk to DM economies comes from spillovers from EM 6

7 Good news? Global interest rates still low as are energy prices 7

8 Wasn t global QE supposed to trigger an inflation explosion? 8

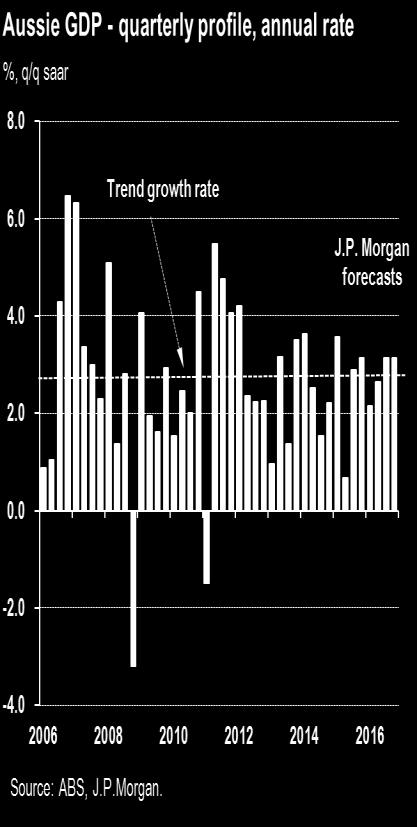

9 Financial market volatility still elevated 9

10 US economy healing progressing ahead of Fed lift-off 10

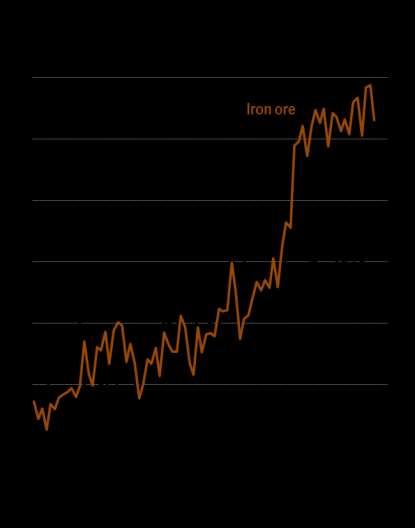

11 Euro area momentum turning and jobless rate falling 11

12 Japan s policy change still a work in progress inflation positive! 12

13 China s GDP growth rate to stabilize from here on policy support 13

14 Share market troubles may threaten household sentiment channel 14

15 Decent GDP growth masking extended income compression 15

16 Recent growth downgrades leave growth close to trend in 2016 Annual change (%) Share of GDP (f) 2016(f) Household spending Government consumption Business investment Government investment Dwelling investment Domestic final demand Change in inventories (cont.) Exports Imports Net Exports (cont.) GDP

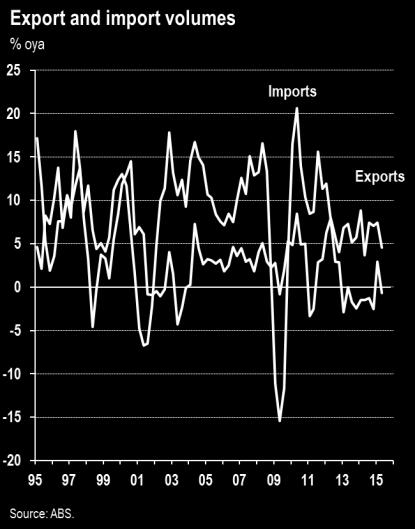

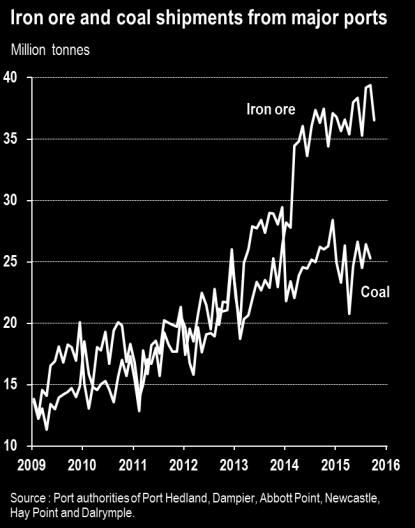

17 Net exports delivering more than half the economy s expansion 17

18 Lucky country - terms of trade boom masked poor productivity 18

19 Boom bust - previous terms of trade booms ended badly Australia: terms of trade and GDP growth GDP, %oya 30 Wool/grain boom 25 Wool boom 20 Wool boom Wool/food boom (Korean war) Wool/grain boom ToT index Coal/iron ore boom WW I WW II Terms of trade (rhs) GDP (lhs) Last recession Recessions Source: RBA, J.P.Morgan

Year of peak % rise - trough to peak % fall - peak to trough 3 years prior to peak 3 years after peak Recession? 1905 26.2-42.8 5.0 3.")

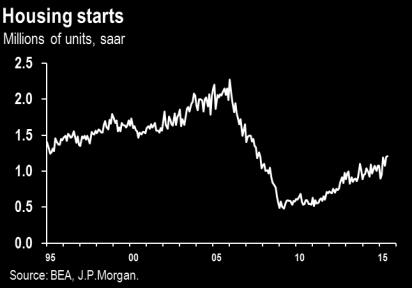

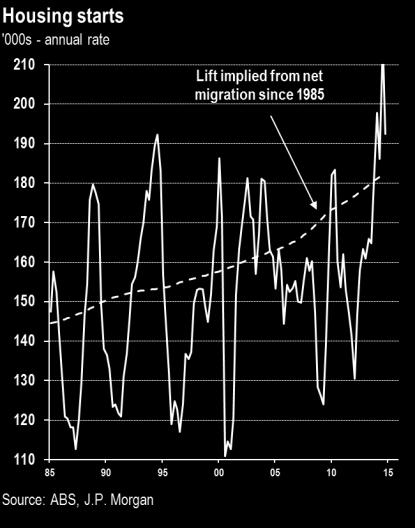

20 But no market economist forecasting recession in Australia! Previous terms of trade experiences Terms of trade GDP growth (%) Year of peak % rise - trough to peak % fall - peak to trough 3 years prior to peak 3 years after peak Recession? Yes Yes Yes Yes No Ave Yes ? 2.5?? 20

21 Boom brought structural headwinds high and rising costs The (high) cost of doing business in Australia % difference, Australia vs. global averages Tax rate (%) Lending rate (%) Multi factor and labour productivity %oya 5 4 Minimum wage (USD) Average wage (USD) 3 2 Output per hour worked Petrol (USc/l) Gas (USD mptu) Electricity (USc/KWH) Multi-factor Source: OECD, World Bank, BP, J.P.Morgan. -50% 0% 50% 100% 150% 200% Source: ABS 21

22 Slipping down the mining capex cliff after unprecedented splurge Mining investment : by country US$ billion Phil. Sth Af. Source: Grattan Institute. USA Peru Rus. Bra. Chile Can. Aust 22

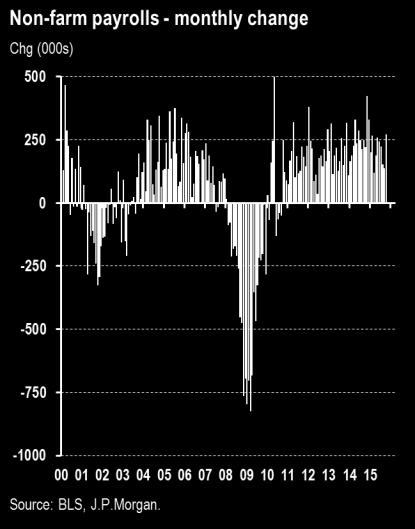

23 Resources pipeline shrinking but mainly via project completions Australia s investment pipeline September 2015 Source: Deloitte Access Economics. 23

24 Exports lifting - supply-side expansion paying dividends 24

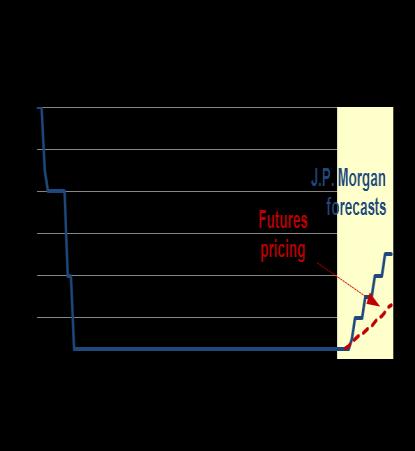

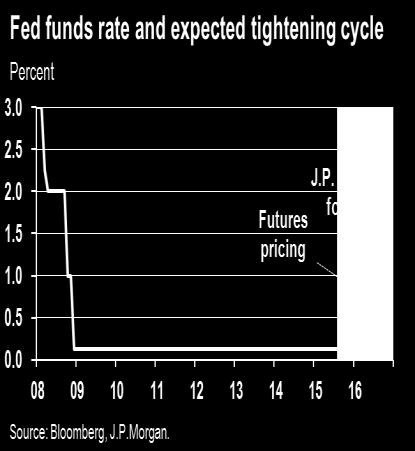

25 China now taking 35% of our merchandise exports 25

26 House price growth is cooling but debt ratio is rising again 26

27 Bubble trouble? No but house price growth to cool in

28 Supply (belatedly) responding record high housing starts 28

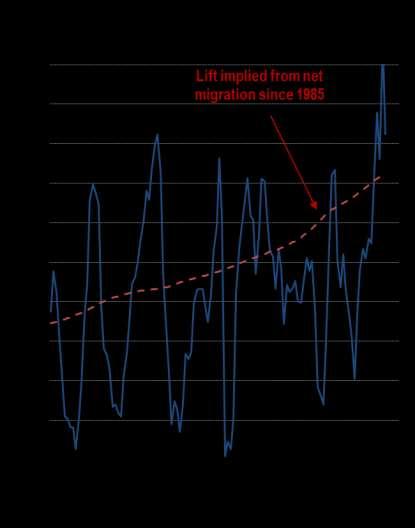

29 The squeeze - households income growing at multi-decade lows 29

")

30 Household (precautionary) savings rate still unusually high 30

31 Jobs growth running at a 5-year high but jobless rate to rise 31

32 Animal spirits, anyone? Cost of capital not the problem for business 32

33 RBA s easing cycle likely over Bank to start hiking in H

34 AUD adjusting but commodity prices down by more! 34

35 Australia one of the nine AAA-rated sovereigns left! Country ^ Nominal GDP share, % Bond market size*, USD Bond market, % of total 10 year bond yield Spread v. Aus. 10yr Germany 35% 1,375 52% Canada 20% % Australia 17% % 2.80 na Switzerland 8% 84 3% Sweden 6% 85 3% Norway 4% 53 2% Denmark 4% 120 5% Singapore 3% 68 3% Luzembourg 3% 58 2% US France UK Netherlands Finland Downgraded by S&P in 2011 Downgraded by Moodys in 2012 Downgraded by Fitch in 2013 Downgraded by S&P in 2013 Downgraded by S&P in 2014 Total 100% 2, % (Ave) (Ave) ^ AAA rated by all three ratings agencies. Conventional bonds only - no linkers or T-bills. Source: Bloomberg, J.P. Morgan. 35

36 NSW now leading state economic performance Unemployment rate (%) Employment growth (%oya) Retail spending (%oya) Capex (%oya) Building approvals (%oya) State final demand (%oya) NSW VIC QLD WA SA TAS

37 State migration flows now smaller NSW and Victoria the winners 37

38 Economic Research November 2015 Global and Australian economic outlook (Still) the dark side of the boom Stephen Walters Chief Economist Australia and New Zealand J.P. Morgan Australia Limited See the end pages of this presentation for important disclosures.

MACRO INVESTMENT OUTLOOK

MACRO INVESTMENT OUTLOOK AUGUST 18 INVESTMENT STRATEGY AND DYNAMIC MARKETS TEAM, MULTI ASSET GROUP GLOBAL SHARES CONSTRAINED BY TRADE WAR FEARS BUT AUSTRALIAN SHARES RELATIVELY RESILIENT 5 Australia -

MACRO INVESTMENT OUTLOOK AUGUST 18 INVESTMENT STRATEGY AND DYNAMIC MARKETS TEAM, MULTI ASSET GROUP GLOBAL SHARES CONSTRAINED BY TRADE WAR FEARS BUT AUSTRALIAN SHARES RELATIVELY RESILIENT 5 Australia -

> Economic risk and implications for

> Economic risk and implications for financial markets Investment Strategy and Economics Multi Asset Group March 212 Outlook for the year ahead > Budget cutbacks in Europe and US, but global monetary easing,

> Economic risk and implications for financial markets Investment Strategy and Economics Multi Asset Group March 212 Outlook for the year ahead > Budget cutbacks in Europe and US, but global monetary easing,

A Global Economic and Market Outlook

A Global Economic and Market Outlook Presented by Dr Chris Caton December 2008 US Housing starts and Permits 2.3 (Millions) Permits Starts 2.1 1.9 1.7 1.5 1.3 1.1 0.9 0.7 96 97 98 99 00 01 02 03 04 05

A Global Economic and Market Outlook Presented by Dr Chris Caton December 2008 US Housing starts and Permits 2.3 (Millions) Permits Starts 2.1 1.9 1.7 1.5 1.3 1.1 0.9 0.7 96 97 98 99 00 01 02 03 04 05

> Macro Investment Outlook

> Macro Investment Outlook Dr Shane Oliver Head of Investment Strategy and Chief Economist October 214 The challenge for investors how to find better yield and returns as bank deposit rates stay low 9

> Macro Investment Outlook Dr Shane Oliver Head of Investment Strategy and Chief Economist October 214 The challenge for investors how to find better yield and returns as bank deposit rates stay low 9

Economic and housing outlook for New South Wales. Warwick Temby, Acting Chief Economist HIA Industry Outlook Breakfast Sydney, August 2017

Economic and housing outlook for New South Wales Warwick Temby, Acting Chief Economist HIA Industry Outlook Breakfast Sydney, August 2017 Risks to residential building moving from global to local World

Economic and housing outlook for New South Wales Warwick Temby, Acting Chief Economist HIA Industry Outlook Breakfast Sydney, August 2017 Risks to residential building moving from global to local World

THE ECONOMY AND CAPITAL MARKETS

THE ECONOMY AND CAPITAL MARKETS Clément Gignac Sr VP & Chief economist ia Financial Group September 2017 Disclaimer Opinions expressed in this presentation are based on actual market conditions and may

THE ECONOMY AND CAPITAL MARKETS Clément Gignac Sr VP & Chief economist ia Financial Group September 2017 Disclaimer Opinions expressed in this presentation are based on actual market conditions and may

The Outlook for the Housing Industry in Western Australia

The Outlook for the Housing Industry in Western Australia Dr Harley Dale HIA Chief Economist HIA Industry Outlook Breakfast Perth March 2011 Overview Policy measures and directions The global backdrop

The Outlook for the Housing Industry in Western Australia Dr Harley Dale HIA Chief Economist HIA Industry Outlook Breakfast Perth March 2011 Overview Policy measures and directions The global backdrop

Australia: which direction?

Australia: which direction? IAG Annual Conference 216 Michael Blythe Chief Economist Managing Director, Economics +(612) 9118 111 michael.blythe@cba.com.au November 216 Australia In Perspective Into our

Australia: which direction? IAG Annual Conference 216 Michael Blythe Chief Economist Managing Director, Economics +(612) 9118 111 michael.blythe@cba.com.au November 216 Australia In Perspective Into our

Clime Asset Management

Clime Asset Management AIA National Investors Conference 2015 Macro Outlook 2015/16 John Abernethy Chief Investment Officer Clime Asset Management Disclaimer The information contained in this document

Clime Asset Management AIA National Investors Conference 2015 Macro Outlook 2015/16 John Abernethy Chief Investment Officer Clime Asset Management Disclaimer The information contained in this document

Queensland Budget

Advancing Queensland s Economy Growing Innovation $300 billion Economy $53 billion Budget Attracting Investment Creating Jobs More than $40 billion infrastructure over 4 years Building Infrastructure 2

Advancing Queensland s Economy Growing Innovation $300 billion Economy $53 billion Budget Attracting Investment Creating Jobs More than $40 billion infrastructure over 4 years Building Infrastructure 2

OUTLOOK FOR THE NEW ZEALAND GOVERNMENT DEBT MARKET. 1 The Treasury

OUTLOOK FOR THE NEW ZEALAND GOVERNMENT DEBT MARKET 1 The Treasury TODAY Economic outlook New Zealand Government: risk/reward Fiscal priorities NZDMO s strategy What to watch for 2 1. ECONOMIC OUTLOOK 3

OUTLOOK FOR THE NEW ZEALAND GOVERNMENT DEBT MARKET 1 The Treasury TODAY Economic outlook New Zealand Government: risk/reward Fiscal priorities NZDMO s strategy What to watch for 2 1. ECONOMIC OUTLOOK 3

Growth has peaked amidst escalating risks

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

The Big Picture. Long-Term Trends in Global Infrastructure Investment and Commodity Prices. Warren Hogan. Chief Economist.

The Big Picture Long-Term Trends in Global Infrastructure Investment and Commodity Prices Warren Hogan Chief Economist May 212 Outline Global Infrastructure Spending Trends Catching up for the industrialised

The Big Picture Long-Term Trends in Global Infrastructure Investment and Commodity Prices Warren Hogan Chief Economist May 212 Outline Global Infrastructure Spending Trends Catching up for the industrialised

A HIGH YIELDING RESILIENT ECONOMY:

A HIGH YIELDING RESILIENT ECONOMY: January 2017 BetaShares Strong Australian Dollar Fund (hedge fund) (ASX: AUDS) The BetaShares Strong Australian Dollar Fund (hedge fund) (ASX: AUDS) and the BetaShares

A HIGH YIELDING RESILIENT ECONOMY: January 2017 BetaShares Strong Australian Dollar Fund (hedge fund) (ASX: AUDS) The BetaShares Strong Australian Dollar Fund (hedge fund) (ASX: AUDS) and the BetaShares

Stronger growth, but risks loom large

OECD ECONOMIC OUTLOOK Stronger growth, but risks loom large Ángel Gurría OECD Secretary-General Álvaro S. Pereira OECD Chief Economist ad interim Paris, 3 May Global growth will be around 4% Investment

OECD ECONOMIC OUTLOOK Stronger growth, but risks loom large Ángel Gurría OECD Secretary-General Álvaro S. Pereira OECD Chief Economist ad interim Paris, 3 May Global growth will be around 4% Investment

All-Country Equity Allocator July 2018

Leila Heckman, Ph.D. lheckman@dcmadvisors.com 917-386-6261 John Mullin, Ph.D. jmullin@dcmadvisors.com 917-386-6262 Allison Hay ahay@dcmadvisors.com 917-386-6264 All-Country Equity Allocator July 2018 A

Leila Heckman, Ph.D. lheckman@dcmadvisors.com 917-386-6261 John Mullin, Ph.D. jmullin@dcmadvisors.com 917-386-6262 Allison Hay ahay@dcmadvisors.com 917-386-6264 All-Country Equity Allocator July 2018 A

2017 Annual Conference. Thursday, 8 June 2017

217 Annual Conference Thursday, 8 June 217 The global markets impact on Australia Thursday, 8 June 217 QIC SLIDES FOR FRONTIER Katrina King 8 th June, 217 GLOBAL INTERACTIONS ARE IMPORTANT The pace of

217 Annual Conference Thursday, 8 June 217 The global markets impact on Australia Thursday, 8 June 217 QIC SLIDES FOR FRONTIER Katrina King 8 th June, 217 GLOBAL INTERACTIONS ARE IMPORTANT The pace of

UDIA NSW Annual State Conference

UDIA NSW Annual State Conference Westpac Institutional Bank Presented by Bill Evans September 217 The Big Issues Inflation and Central Bank policies; Australia s growth challenge; Australia s construction

UDIA NSW Annual State Conference Westpac Institutional Bank Presented by Bill Evans September 217 The Big Issues Inflation and Central Bank policies; Australia s growth challenge; Australia s construction

Australian Economy April Julie Toth Chief Economist Australian Industry Group

Australian Economy April 2018 Julie Toth Chief Economist Australian Industry Group No recession in 26 years (since 1991) but we re still quite slow and fragile. Real GDP grew by only 2.4% in Q4 of 2017

Australian Economy April 2018 Julie Toth Chief Economist Australian Industry Group No recession in 26 years (since 1991) but we re still quite slow and fragile. Real GDP grew by only 2.4% in Q4 of 2017

Victoria University. David Gruen Australian Treasury 23 February Is the resources boom an example of Dutch

The resources boom and structural change in the Australian economy Victoria University David Gruen Australian Treasury February Outline The resources boom Structural change in the Australian traded sector

The resources boom and structural change in the Australian economy Victoria University David Gruen Australian Treasury February Outline The resources boom Structural change in the Australian traded sector

All-Country Equity Allocator February 2018

Leila Heckman, Ph.D. lheckman@dcmadvisors.com 917-386-6261 John Mullin, Ph.D. jmullin@dcmadvisors.com 917-386-6262 Charles Waters cwaters@dcmadvisors.com 917-386-6264 All-Country Equity Allocator February

Leila Heckman, Ph.D. lheckman@dcmadvisors.com 917-386-6261 John Mullin, Ph.D. jmullin@dcmadvisors.com 917-386-6262 Charles Waters cwaters@dcmadvisors.com 917-386-6264 All-Country Equity Allocator February

Monthly Bulletin of Economic Trends: Economic Activity in the Major States

MELBOURNE INSTITUTE Applied Economic & Social Research Monthly Bulletin of Economic Trends: Economic Activity in the Major States October 2018 Released at 11AM on 25 October 2018 Economic Activity in the

MELBOURNE INSTITUTE Applied Economic & Social Research Monthly Bulletin of Economic Trends: Economic Activity in the Major States October 2018 Released at 11AM on 25 October 2018 Economic Activity in the

Global growth weakening as some risks materialise

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

New Zealand Economic Chart Pack. Key New Zealand Macroeconomic and Financial Market Graphs

New Zealand Economic Chart Pack Key New Zealand Macroeconomic and Financial Market Graphs January New Zealand Economic Chart Pack January Page Contents Aggregate Output... Prices... Households... Business...

New Zealand Economic Chart Pack Key New Zealand Macroeconomic and Financial Market Graphs January New Zealand Economic Chart Pack January Page Contents Aggregate Output... Prices... Households... Business...

Key Economic Challenges in Japan and Asia. Changyong Rhee IMF Asia and Pacific Department February

Key Economic Challenges in Japan and Asia Changyong Rhee IMF Asia and Pacific Department February 2017 1 Global and Asia Outlook 2 Global activity strengthening, with rising dispersion and uncertainty

Key Economic Challenges in Japan and Asia Changyong Rhee IMF Asia and Pacific Department February 2017 1 Global and Asia Outlook 2 Global activity strengthening, with rising dispersion and uncertainty

M&G Emerging Markets Bond Fund Claudia Calich, Fund Manager. November 2015

M&G Emerging Markets Bond Fund Claudia Calich, Fund Manager November 2015 Agenda Macro update & government bonds Emerging market corporate bonds Fund positioning Emerging markets risks today Risks Slowing

M&G Emerging Markets Bond Fund Claudia Calich, Fund Manager November 2015 Agenda Macro update & government bonds Emerging market corporate bonds Fund positioning Emerging markets risks today Risks Slowing

Emerging Markets: Fad or New Reality?

Emerging Markets: Fad or New Reality? Agenda 1 2 Why emerging markets matter Medium- and long-term trends 1 Global Outlook Economic forecast summary GDP growth, % CPI inflation, % 21 211 212F 213F 21 211

Emerging Markets: Fad or New Reality? Agenda 1 2 Why emerging markets matter Medium- and long-term trends 1 Global Outlook Economic forecast summary GDP growth, % CPI inflation, % 21 211 212F 213F 21 211

Economic and Market Outlook

Economic and Market Outlook Fourth Quarter 2018 Investment Products: Not FDIC Insured No Bank Guarantee May Lose Value Past performance is no guarantee of future results. Financial term and index definitions

Economic and Market Outlook Fourth Quarter 2018 Investment Products: Not FDIC Insured No Bank Guarantee May Lose Value Past performance is no guarantee of future results. Financial term and index definitions

Financial wealth of private households worldwide

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

OECD ECONOMIC OUTLOOK Moving forward in difficult times. 3 rd December Mauro Pisu OECD Senior Economist

OECD ECONOMIC OUTLOOK Moving forward in difficult times 3 rd December 2015 Mauro Pisu OECD Senior Economist Key issues Global trade weakness Harbinger of further slowing of global GDP growth? China s role

OECD ECONOMIC OUTLOOK Moving forward in difficult times 3 rd December 2015 Mauro Pisu OECD Senior Economist Key issues Global trade weakness Harbinger of further slowing of global GDP growth? China s role

Australia: Economic and Financial Outlook

Australia: Economic and Financial Outlook Greg Noonan Head of Business Markets Queensland & Agribusiness 5 June 2015 Australian economy and financial markets continue to be impacted by a large number of

Australia: Economic and Financial Outlook Greg Noonan Head of Business Markets Queensland & Agribusiness 5 June 2015 Australian economy and financial markets continue to be impacted by a large number of

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York 1 Global macroeconomic trends Major headwinds Risks and uncertainties Policy questions and

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York 1 Global macroeconomic trends Major headwinds Risks and uncertainties Policy questions and

GDP Growth Outlook Heavily Dependent on Consumer Spending. Which Relies on Net Job Gains Plus Modest Pick Up in Wages Growth

GDP Growth Outlook Heavily Dependent on Consumer Spending Which Relies on Net Job Gains Plus Modest Pick Up in Wages Growth Plus Some Recourse to Increased Borrowings. 2 Introduction The only function

GDP Growth Outlook Heavily Dependent on Consumer Spending Which Relies on Net Job Gains Plus Modest Pick Up in Wages Growth Plus Some Recourse to Increased Borrowings. 2 Introduction The only function

Trends and opportunities across regions: Europe

Trends and opportunities across regions: Europe Monday, 6 June 2011 Head of Institutional Fixed Income Europe Three themes shaping global opportunities I. Long term: Spheres of influence are shifting among

Trends and opportunities across regions: Europe Monday, 6 June 2011 Head of Institutional Fixed Income Europe Three themes shaping global opportunities I. Long term: Spheres of influence are shifting among

Outlook Overview: OECD Countries UN LINK Conference, Bangkok October, 2009

Outlook Overview: OECD Countries UN LINK Conference, Bangkok 26 28 October, 2009 Dave Turner OECD, Economics Department OECD Outlook: Outline 1. Recovery underway but will probably be slow 2. Risks and

Outlook Overview: OECD Countries UN LINK Conference, Bangkok 26 28 October, 2009 Dave Turner OECD, Economics Department OECD Outlook: Outline 1. Recovery underway but will probably be slow 2. Risks and

2015 Market Review & Outlook. January 29, 2015

2015 Market Review & Outlook January 29, 2015 Economic Outlook Jason O. Jackman, CFA President & Chief Investment Officer Percentage Interest Rates Unexpectedly Decline 4.5 10-Year Government Yield 4 3.5

2015 Market Review & Outlook January 29, 2015 Economic Outlook Jason O. Jackman, CFA President & Chief Investment Officer Percentage Interest Rates Unexpectedly Decline 4.5 10-Year Government Yield 4 3.5

Chapter 1 International economy

Chapter International economy. Main points from the OECD's Economic Outlook A broad-based recovery has taken hold Asia, the US and the UK have taken the lead. Continental Europe will follow Investment

Chapter International economy. Main points from the OECD's Economic Outlook A broad-based recovery has taken hold Asia, the US and the UK have taken the lead. Continental Europe will follow Investment

The Evolving Role of Trade in Asia: Opening a New Chapter. Fall 2018 REO Background Paper

The Evolving Role of Trade in Asia: Opening a New Chapter Fall 2018 REO Background Paper Outline Trade Tensions and Spillovers: Spotlight on Asia Gains from Liberalization 2 Trade tensions have escalated.

The Evolving Role of Trade in Asia: Opening a New Chapter Fall 2018 REO Background Paper Outline Trade Tensions and Spillovers: Spotlight on Asia Gains from Liberalization 2 Trade tensions have escalated.

Monetary Policy report October 2015

Monetary Policy report October 2015 Chapter 1 Figure 1.1. Repo rate with uncertainty bands Per cent Note. The uncertainty bands for the repo rate are based on the Riksbank s historical forecasting errors

Monetary Policy report October 2015 Chapter 1 Figure 1.1. Repo rate with uncertainty bands Per cent Note. The uncertainty bands for the repo rate are based on the Riksbank s historical forecasting errors

APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES

QUARTERLY INVESTMENT STRATEGY Third Quarter 15 19 APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES Purchasing Managers EMERGING ECONOMIES Purchasing Managers US Eurozone Japan Brazil Russia India China

QUARTERLY INVESTMENT STRATEGY Third Quarter 15 19 APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES Purchasing Managers EMERGING ECONOMIES Purchasing Managers US Eurozone Japan Brazil Russia India China

Economic Imbalances in the post-maastricht Treaty World A Look at Global and European Implications and Investment Conclusions

Economic Imbalances in the post-maastricht Treaty World A Look at Global and European Implications and Investment Conclusions JOHN W. BECK Senior Vice President Co-Director, Global Fixed Income Franklin

Economic Imbalances in the post-maastricht Treaty World A Look at Global and European Implications and Investment Conclusions JOHN W. BECK Senior Vice President Co-Director, Global Fixed Income Franklin

Emerging Markets Outlook

Mark Mobius, Ph.D. Executive Chairman Templeton Emerging Markets Group Emerging Markets Outlook Dealer Use Only / Not for Distribution to the Public Agenda Performance Emerging Markets Equities: Demand

Mark Mobius, Ph.D. Executive Chairman Templeton Emerging Markets Group Emerging Markets Outlook Dealer Use Only / Not for Distribution to the Public Agenda Performance Emerging Markets Equities: Demand

Colonial First State Global Asset Management. Stephen Halmarick Head of Investment Markets Research. 28 September 2009

Colonial First State Global Asset Management Implications of massive sovereign debt issuance Stephen Halmarick Head of Investment Markets Research Colonial First State Global Asset Management 28 September

Colonial First State Global Asset Management Implications of massive sovereign debt issuance Stephen Halmarick Head of Investment Markets Research Colonial First State Global Asset Management 28 September

Since 4Q16, the Fed has just held one meeting without a rate increase skipping only Sept Their challenges are numerous.

Monetary Policy All of the central banks face major challenges. Too high, too low, avoiding inversion and in the case of the Bank of Japan, how to conduct policy at all. US Federal Reserve ECONOMIC & MARKET

Monetary Policy All of the central banks face major challenges. Too high, too low, avoiding inversion and in the case of the Bank of Japan, how to conduct policy at all. US Federal Reserve ECONOMIC & MARKET

The First Phase of the U.S. Recovery and Beyond

The First Phase of the U.S. Recovery and Beyond James Bullard President and CEO Federal Reserve Bank of St. Louis Global Interdependence Center Shanghai, China January 11, 2010 Any opinions expressed here

The First Phase of the U.S. Recovery and Beyond James Bullard President and CEO Federal Reserve Bank of St. Louis Global Interdependence Center Shanghai, China January 11, 2010 Any opinions expressed here

Federal Budget : This Time It s Personal. May 2018

Federal Budget 2018-19: This Time It s Personal May 2018 Executive Summary The Federal Government and the nation s fiscal position have become the beneficiaries of an unexpected windfall primarily in the

Federal Budget 2018-19: This Time It s Personal May 2018 Executive Summary The Federal Government and the nation s fiscal position have become the beneficiaries of an unexpected windfall primarily in the

Is the high Aussie dollar really bad for the Australian and Victorian economies? Professor John Daley August 20, 2012

Is the high Aussie dollar really bad for the Australian and Victorian economies? Professor John Daley August 2, 212 Messages Three factors have pushed up the real exchange rate High Australian incomes,

Is the high Aussie dollar really bad for the Australian and Victorian economies? Professor John Daley August 2, 212 Messages Three factors have pushed up the real exchange rate High Australian incomes,

May market performance. Index. Index. Global economies

JUNE 2016 The recovery in equity and commodity prices from February lows continued into May with the third straight month of equity and commodity price rises. Oil prices continued to move higher, up another

JUNE 2016 The recovery in equity and commodity prices from February lows continued into May with the third straight month of equity and commodity price rises. Oil prices continued to move higher, up another

Global Investment Outlook Russ Koesterich, CFA Managing Director, Global Allocation

Global Investment Outlook Russ Koesterich, CFA Managing Director, Global Allocation 6 Asset performance YTD Source: Thomson Reuters Datastream, BlackRock Investment Institute. Apr, 6 Note: Total return

Global Investment Outlook Russ Koesterich, CFA Managing Director, Global Allocation 6 Asset performance YTD Source: Thomson Reuters Datastream, BlackRock Investment Institute. Apr, 6 Note: Total return

Aggregate Output Prices Households Business Government Taxation External Sector Labour Market...

March Contents Aggregate Output... Prices... Households... Business... Government... Taxation... External Sector... 9 Labour Market... Housing Market... Financial Market... Indicators of Productive Capacity...

March Contents Aggregate Output... Prices... Households... Business... Government... Taxation... External Sector... 9 Labour Market... Housing Market... Financial Market... Indicators of Productive Capacity...

The Great Escape? Douglas Porter, CFA. Deputy Chief Economist & Managing Director, BMO Capital Markets

The Great Escape? Douglas Porter, CFA Deputy Chief Economist & Managing Director, BMO Capital Markets Financial Markets Revive (as of May 3, 21) 16 Stocks 16 15 Canadian Dollar ( ) 15 Commodities 4.5 14

The Great Escape? Douglas Porter, CFA Deputy Chief Economist & Managing Director, BMO Capital Markets Financial Markets Revive (as of May 3, 21) 16 Stocks 16 15 Canadian Dollar ( ) 15 Commodities 4.5 14

What is driving US Treasury yields higher?

What is driving Treasury yields higher? " our programme for reducing our [Fed's] balance sheet, which began in October, is proceeding smoothly. Barring a very significant and unexpected weakening in the

What is driving Treasury yields higher? " our programme for reducing our [Fed's] balance sheet, which began in October, is proceeding smoothly. Barring a very significant and unexpected weakening in the

Financial Market Outlook: Further Stock Gain on Faster GDP Rebound and Earnings Recovery. Year-end Target Raised

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: FurtherStock Gains Likely, Year-end Target Raised. Bond Under Pressure

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: FurtherStock Gains Likely, Year-end Target Raised. Bond Under Pressure

Monthly Bulletin of Economic Trends: Economic Activity in the Major States

MELBOURNE INSTITUTE Applied Economic & Social Research Monthly Bulletin of Economic Trends: Economic Activity in the Major States January 2018 Monthly Bulletin of Economic Trends January 2018 Released

MELBOURNE INSTITUTE Applied Economic & Social Research Monthly Bulletin of Economic Trends: Economic Activity in the Major States January 2018 Monthly Bulletin of Economic Trends January 2018 Released

How Serious of a Threat Is Global Deflation?

How Serious of a Threat Is Global Deflation? Nariman Behravesh Farid Abolfathi John Mothersole Dan Ryan Todd Lee Howard Archer Global Insight Teleconference December 17, 22 199s: A Deflationary Wave The

How Serious of a Threat Is Global Deflation? Nariman Behravesh Farid Abolfathi John Mothersole Dan Ryan Todd Lee Howard Archer Global Insight Teleconference December 17, 22 199s: A Deflationary Wave The

Negative Interest Rate Policies: Sources and Implications

Negative Interest Rate Policies: Sources and Implications November 4, 216 Marc Stocker Based on a recently published CEPR / World Bank Working Paper Disclaimer! The views presented here are those of the

Negative Interest Rate Policies: Sources and Implications November 4, 216 Marc Stocker Based on a recently published CEPR / World Bank Working Paper Disclaimer! The views presented here are those of the

Monthly Bulletin of Economic Trends: Review of the Australian Economy

MELBOURNE INSTITUTE Applied Economic & Social Research Monthly Bulletin of Economic Trends: Review of the Australian Economy March 2018 Released on 22 March 2018 Outlook for Australia 1 Economic Activity

MELBOURNE INSTITUTE Applied Economic & Social Research Monthly Bulletin of Economic Trends: Review of the Australian Economy March 2018 Released on 22 March 2018 Outlook for Australia 1 Economic Activity

: Monetary Economics and the European Union. Lecture 8. Instructor: Prof Robert Hill. The Costs and Benefits of Monetary Union II

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

The Outlook for the Housing Industry in Western Australia

The Outlook for the Housing Industry in Western Australia Dr Harley Dale HIA Chief Economist HIA Industry Outlook Breakfast Perth March 2012 Europe muddles while China rebalances China is looking to rebalance

The Outlook for the Housing Industry in Western Australia Dr Harley Dale HIA Chief Economist HIA Industry Outlook Breakfast Perth March 2012 Europe muddles while China rebalances China is looking to rebalance

The Outlook for the Australian Residential Sector Presentation to Buildex

The Outlook for the Australian Residential Sector Presentation to Buildex Andrew Harvey HIA Senior Economist October 2010 Presentation Outline The economic backdrop global economy domestic economic outlook

The Outlook for the Australian Residential Sector Presentation to Buildex Andrew Harvey HIA Senior Economist October 2010 Presentation Outline The economic backdrop global economy domestic economic outlook

Global Economic Prospects

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

The Outlook for Israel s Economy in Light of Current Global Developments

The Outlook for Israel s Economy in Light of Current Global Developments Dr. Leonardo Leiderman Professor of Economics, Tel-Aviv University and Chief Economic Advisor, Bank Hapoalim To be presented in

The Outlook for Israel s Economy in Light of Current Global Developments Dr. Leonardo Leiderman Professor of Economics, Tel-Aviv University and Chief Economic Advisor, Bank Hapoalim To be presented in

Challenges for financial institutions today. Summary

7 February 6 Challenges for financial institutions today Notes for remarks by Malcolm D Knight, General Manager of the BIS, at a European Financial Services Roundtable meeting, Zurich, 7 February 6 Summary

7 February 6 Challenges for financial institutions today Notes for remarks by Malcolm D Knight, General Manager of the BIS, at a European Financial Services Roundtable meeting, Zurich, 7 February 6 Summary

Economic and Market Outlook

Economic and Market Outlook Third Quarter 2018 Investment Products: Not FDIC Insured No Bank Guarantee May Lose Value Past performance is no guarantee of future results. Financial term and index definitions

Economic and Market Outlook Third Quarter 2018 Investment Products: Not FDIC Insured No Bank Guarantee May Lose Value Past performance is no guarantee of future results. Financial term and index definitions

CBA mortgage book secure

Determined to be better than we ve ever been. Australian residential housing and mortgages CBA mortgage book secure 9 September 2010 Commonwealth Bank of Australia ACN 123 123 124 Overview Concerns of

Determined to be better than we ve ever been. Australian residential housing and mortgages CBA mortgage book secure 9 September 2010 Commonwealth Bank of Australia ACN 123 123 124 Overview Concerns of

The global economy and the Fiji dollar

The global economy and the Fiji dollar David de Garis Senior Treasury Economist Fiji, February 25 Today s talk 2 The global economy Outlook for major currencies and interest rates Australia and New Zealand:

The global economy and the Fiji dollar David de Garis Senior Treasury Economist Fiji, February 25 Today s talk 2 The global economy Outlook for major currencies and interest rates Australia and New Zealand:

AWF Economic Update. What to Expect in 2014: Forecast for BC Businesses and Outlook for the Global Economy Sponsored by: Jill Leversage

AWF Economic Update What to Expect in 2014: Forecast for BC Businesses and Outlook for the Global Economy Sponsored by: Jim Allworth Jill Leversage Jock Finlayson AWF Economic Update What to Expect in

AWF Economic Update What to Expect in 2014: Forecast for BC Businesses and Outlook for the Global Economy Sponsored by: Jim Allworth Jill Leversage Jock Finlayson AWF Economic Update What to Expect in

PRESENTATION BY JACOB A. FRENKEL AT THE FORUM: INTELLIGENCE ON THE WORLD, EUROPE, AND ITALY. Villa d'este, Cernobbio - September 7, 8 and 9, 2012

PRESENTATION BY JACOB A. FRENKEL AT THE FORUM: INTELLIGENCE ON THE WORLD, EUROPE, AND ITALY Villa d'este, Cernobbio - September 7, 8 and 9, 1 Working paper, September 1. Kindly authorized by the Author.

PRESENTATION BY JACOB A. FRENKEL AT THE FORUM: INTELLIGENCE ON THE WORLD, EUROPE, AND ITALY Villa d'este, Cernobbio - September 7, 8 and 9, 1 Working paper, September 1. Kindly authorized by the Author.

Economic Outlook. Macro Research Itaú Unibanco

Economic Outlook Macro Research Itaú Unibanco June, 2013 Agenda Economia Global Heterogeneous growth: U.S. growing faster, Europe in recession. Deceleration in the emerging economies. The Fed signals a

Economic Outlook Macro Research Itaú Unibanco June, 2013 Agenda Economia Global Heterogeneous growth: U.S. growing faster, Europe in recession. Deceleration in the emerging economies. The Fed signals a

San Francisco Retiree Health Care Trust Fund Education Materials on Public Equity

M E K E T A I N V E S T M E N T G R O U P 5796 ARMADA DRIVE SUITE 110 CARLSBAD CA 92008 760 795 3450 fax 760 795 3445 www.meketagroup.com The Global Equity Opportunity Set MSCI All Country World 1 Index

M E K E T A I N V E S T M E N T G R O U P 5796 ARMADA DRIVE SUITE 110 CARLSBAD CA 92008 760 795 3450 fax 760 795 3445 www.meketagroup.com The Global Equity Opportunity Set MSCI All Country World 1 Index

Three-speed recovery. GDP growth. Percent Emerging and developing economies. World

Three-speed recovery GDP growth Percent 1 8 6 4 2-2 -4-6 198 1985 199 1995 2 25 21 215 Source: IMF WEO; Milken Institute. Emerging and developing economies Advanced economies World Output is still below

Three-speed recovery GDP growth Percent 1 8 6 4 2-2 -4-6 198 1985 199 1995 2 25 21 215 Source: IMF WEO; Milken Institute. Emerging and developing economies Advanced economies World Output is still below

NORTH AMERICAN UPDATE

NORTH AMERICAN UPDATE December 6 th, 2018 INNOVATION INSIGHT GROWTH SINCE 1968 TOUGH YEAR FOR RETURNS AROUND THE WORLD Index Year-to-date Performance MSCI World -1.2% MSCI USA 3.9% MSCI Canada -3.9% MSCI

NORTH AMERICAN UPDATE December 6 th, 2018 INNOVATION INSIGHT GROWTH SINCE 1968 TOUGH YEAR FOR RETURNS AROUND THE WORLD Index Year-to-date Performance MSCI World -1.2% MSCI USA 3.9% MSCI Canada -3.9% MSCI

HOUSING MARKETS, BUSINESS CYCLES AND ECONOMIC POLICIES

HOUSING MARKETS, BUSINESS CYCLES AND ECONOMIC POLICIES Austrian National Bank Workshop - Housing Market Challenges in Europe and the US - any solutions available? September 29, 2008 - Vienna Christophe

HOUSING MARKETS, BUSINESS CYCLES AND ECONOMIC POLICIES Austrian National Bank Workshop - Housing Market Challenges in Europe and the US - any solutions available? September 29, 2008 - Vienna Christophe

2011 SECURITIES LENDING OUTLOOK

2011 SECURITIES LENDING OUTLOOK February 8, 2011 Host Paul Wilson International Head of Client Management and Sales, Financing and Markets Products, J.P. Morgan Featured Guest Speaker David Mackie Head

2011 SECURITIES LENDING OUTLOOK February 8, 2011 Host Paul Wilson International Head of Client Management and Sales, Financing and Markets Products, J.P. Morgan Featured Guest Speaker David Mackie Head

STATE UPDATE: VICTORIA JULY 2016 CONTENTS

STATE UPDATE: VICTORIA JULY 1 CONTENTS Key points 3 In Focus: Victoria continues to reap the benefits of strong population growth Consumer & household sector 5 Business sector Commercial property sector

STATE UPDATE: VICTORIA JULY 1 CONTENTS Key points 3 In Focus: Victoria continues to reap the benefits of strong population growth Consumer & household sector 5 Business sector Commercial property sector

Chart 1 Productivity of Major Economies

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2013 2014 2015 2016 Chart 1 Productivity

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2013 2014 2015 2016 Chart 1 Productivity

ADVANCE DEFENSIVE YIELD MULTI-BLEND FUND

ADVANCE DEFENSIVE YIELD MULTI-BLEND FUND As at 30 June 2018 FUND PERFORMANCE * 1 month 3 months 6 months 1 year 2 year (% pa) Since incept (% pa) Growth return (0.76) (1.18) (1.45) (1.60) (0.84) (0.01)

ADVANCE DEFENSIVE YIELD MULTI-BLEND FUND As at 30 June 2018 FUND PERFORMANCE * 1 month 3 months 6 months 1 year 2 year (% pa) Since incept (% pa) Growth return (0.76) (1.18) (1.45) (1.60) (0.84) (0.01)

Jim O Neill Managing Director Head of Global Economics, Commodities and Strategy Research

The BRIC Effect Jim O Neill Managing Director Head of Global Economics, Commodities and Strategy Research March 29 2010 Goldman Sachs Global Economics, Commodities and Strategy Research 2010 1 GDP Forecasts

The BRIC Effect Jim O Neill Managing Director Head of Global Economics, Commodities and Strategy Research March 29 2010 Goldman Sachs Global Economics, Commodities and Strategy Research 2010 1 GDP Forecasts

June market performance. Index. Index. Global economies

JULY 2017 In June markets were influenced by political developments in the UK and US and more hawkish commentary from central bankers suggesting that soft inflation is only transitory. European equities

JULY 2017 In June markets were influenced by political developments in the UK and US and more hawkish commentary from central bankers suggesting that soft inflation is only transitory. European equities

VICTORIAN BUILDING & CONSTRUCTION INDUSTRY OUTLOOK

VICTORIAN BUILDING & CONSTRUCTION INDUSTRY OUTLOOK MARCH 2017 QUARTERLY UPDATE 15 JUNE 2017 PREPARED FOR THE MASTER BUILDERS ASSOCIATION OF VICTORIA STAFF RESPONSIBLE FOR THIS REPORT WERE: Director Senior

VICTORIAN BUILDING & CONSTRUCTION INDUSTRY OUTLOOK MARCH 2017 QUARTERLY UPDATE 15 JUNE 2017 PREPARED FOR THE MASTER BUILDERS ASSOCIATION OF VICTORIA STAFF RESPONSIBLE FOR THIS REPORT WERE: Director Senior

20 July 2018 AUSTRALIAN ECONOMIC DEVELOPMENTS

20 July 2018 AUSTRALIAN ECONOMIC DEVELOPMENTS This week the RBA reiterated its view that there is no case for a near-term change in the cash rate. Eventually the next move in the cash rate would more likely

20 July 2018 AUSTRALIAN ECONOMIC DEVELOPMENTS This week the RBA reiterated its view that there is no case for a near-term change in the cash rate. Eventually the next move in the cash rate would more likely

11 QUESTIONS FOR EQUITY INVESTORS IN 2017

Global Equities 11 QUESTIONS FOR EQUITY INVESTORS IN 2017 January 2017 For investment professionals only. Not for further distribution. The 2 nd Longest US Bull Market In History Could This Be The Record

Global Equities 11 QUESTIONS FOR EQUITY INVESTORS IN 2017 January 2017 For investment professionals only. Not for further distribution. The 2 nd Longest US Bull Market In History Could This Be The Record

NAB QUARTERLY BUSINESS SURVEY 2018 Q2 FAVOURABLE BUSINESS CONDITIONS PERSIST

EMBARGOED UNTIL: 11:3AM AEST, 19 JULY 218 NAB QUARTERLY BUSINESS SURVEY 218 Q2 FAVOURABLE BUSINESS CONDITIONS PERSIST NAB Australian Economics After strengthening to historically high levels in Q1, business

EMBARGOED UNTIL: 11:3AM AEST, 19 JULY 218 NAB QUARTERLY BUSINESS SURVEY 218 Q2 FAVOURABLE BUSINESS CONDITIONS PERSIST NAB Australian Economics After strengthening to historically high levels in Q1, business

AUD-EUR OUTLOOK Risk Appetite is the Key Wednesday, 25 January 2012 The Australian dollar has recently soared to record highs against the euro, reflecting heightened concerns about European sovereign risk,

AUD-EUR OUTLOOK Risk Appetite is the Key Wednesday, 25 January 2012 The Australian dollar has recently soared to record highs against the euro, reflecting heightened concerns about European sovereign risk,

National Monetary Policy Forum. Chris Loewald, Head: Policy Development and Research 10 April 2016 Pretoria

National Monetary Policy Forum Chris Loewald, Head: Policy Development and Research 1 April 1 Pretoria In the April 17 MPR Executive summary & overview of the policy stance Overview of the world economy

National Monetary Policy Forum Chris Loewald, Head: Policy Development and Research 1 April 1 Pretoria In the April 17 MPR Executive summary & overview of the policy stance Overview of the world economy

The case for lower rated corporate bonds

The case for lower rated corporate bonds Marcus Pakenham Fixed income product specialist December 3 Introduction Where should fixed income investors be positioned over the medium term? We expect that government

The case for lower rated corporate bonds Marcus Pakenham Fixed income product specialist December 3 Introduction Where should fixed income investors be positioned over the medium term? We expect that government

Victorian Economic Outlook

Thursday, November 1 Victorian Economic Outlook Summary The Victorian economy has been through difficult conditions over the past few years. GSP grew by.% in 11-1, easing from growth of.7% in 1-11, and

Thursday, November 1 Victorian Economic Outlook Summary The Victorian economy has been through difficult conditions over the past few years. GSP grew by.% in 11-1, easing from growth of.7% in 1-11, and

The Outlook for the Housing Industry in New South Wales

The Outlook for the Housing Industry in New South Wales Dr. Harley Dale HIA Chief Economist HIA Industry Outlook Breakfast Sydney March 2011 Where are we heading? The economic backdrop is improving and...

The Outlook for the Housing Industry in New South Wales Dr. Harley Dale HIA Chief Economist HIA Industry Outlook Breakfast Sydney March 2011 Where are we heading? The economic backdrop is improving and...

Insolvency forecasts. Economic Research August 2017

Insolvency forecasts Economic Research August 2017 Summary We present our new insolvency forecasting model which offers a broader scope of macroeconomic developments to better predict insolvency developments.

Insolvency forecasts Economic Research August 2017 Summary We present our new insolvency forecasting model which offers a broader scope of macroeconomic developments to better predict insolvency developments.

Nordics D e n m a r k, N o r w a y, S w e d e n, F i n l a n d. 1Q17 Economic and Financial Report.

Management Solutions 2017. All rights reserved Nordics D e n m a r k, N o r w a y, S w e d e n, F i n l a n d 1Q17 Economic and Financial Report R & D www.managementsolutions.com www.msmex.com Design and

Management Solutions 2017. All rights reserved Nordics D e n m a r k, N o r w a y, S w e d e n, F i n l a n d 1Q17 Economic and Financial Report R & D www.managementsolutions.com www.msmex.com Design and

Market Review and Outlook. Todd Centurino, CFA

Market Review and Outlook Todd Centurino, CFA Q1 2017 Global Economy: On the Upswing Ranked Returns (%) Emerging Market Equities 11.40 European Equities 7.40 US Equities 6.10 Global Bonds 2.00 US Treasuries

Market Review and Outlook Todd Centurino, CFA Q1 2017 Global Economy: On the Upswing Ranked Returns (%) Emerging Market Equities 11.40 European Equities 7.40 US Equities 6.10 Global Bonds 2.00 US Treasuries

Monetary Policy Divergence and Global Financial Stability: From the Perspective of Demand and Supply of Safe Assets

Monetary Policy Divergence and Global Financial Stability: From the Perspective of Demand and Supply of Safe Assets January, 7 Speech at a Meeting Hosted by the International Bankers Association of Japan

Monetary Policy Divergence and Global Financial Stability: From the Perspective of Demand and Supply of Safe Assets January, 7 Speech at a Meeting Hosted by the International Bankers Association of Japan

FOR 2018 GLOBAL MARKET OUTLOOK PRESS BRIEFING. PROVIDED TO DESIGNATED MEMBERS OF THE PRESS ONLY, NOT FOR FURTHER DISTRIBUTION.

2018 Global Market Outlook Press Briefing GLOBAL FIXED INCOME Mark Vaselkiv Portfolio Manager, CIO, Fixed Income November 14, 2017 FOR 2018 GLOBAL MARKET OUTLOOK PRESS BRIEFING. PROVIDED TO DESIGNATED

2018 Global Market Outlook Press Briefing GLOBAL FIXED INCOME Mark Vaselkiv Portfolio Manager, CIO, Fixed Income November 14, 2017 FOR 2018 GLOBAL MARKET OUTLOOK PRESS BRIEFING. PROVIDED TO DESIGNATED

Global Emerging Markets. Outlook March 2006

Global Emerging Markets Outlook Market Performance from 31.12.1998 to 31.01.2006 360 310 260 210 160 110 60 98 Jun-99 99 Jun-00 00 Jun-01 01 Jun-02 02 Jun-03 03 Jun-04 04 Jun-05 05 MSCI World MSCI EM S&P500

Global Emerging Markets Outlook Market Performance from 31.12.1998 to 31.01.2006 360 310 260 210 160 110 60 98 Jun-99 99 Jun-00 00 Jun-01 01 Jun-02 02 Jun-03 03 Jun-04 04 Jun-05 05 MSCI World MSCI EM S&P500

Financial Market Outlook: Stock Rally Continues with Faster & Stronger GDP Rebound, Earnings Recovery & Liquidity

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Further Stock Gains with Macro Sweet Spot & Earnings Recovery.

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Further Stock Gains with Macro Sweet Spot & Earnings Recovery.

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook September 2013 Financial Market Outlook: Stocks likely to Remain in Modest Uptrend with Low Rates & Plentiful Liquidity, Improving

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook September 2013 Financial Market Outlook: Stocks likely to Remain in Modest Uptrend with Low Rates & Plentiful Liquidity, Improving

JPMorgan Europe Strategic Dividend Fund

AVAILABLE FOR PUBLIC CIRCULATION NEW JPMorgan Europe Strategic Dividend Fund Asset Management Company of the Year, Asia + Important information 1. The Fund invests at least 70% in equity securities of

AVAILABLE FOR PUBLIC CIRCULATION NEW JPMorgan Europe Strategic Dividend Fund Asset Management Company of the Year, Asia + Important information 1. The Fund invests at least 70% in equity securities of

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Bubble, bubble. facilitating debate on the outlook for the markets

Bubble, bubble toil and trouble? 15 February 2011 facilitating debate on the outlook for the markets Kumar Palghat ag a Managing Director Kapstream Capital Two sides to every story 3 2010 bottom line Right

Bubble, bubble toil and trouble? 15 February 2011 facilitating debate on the outlook for the markets Kumar Palghat ag a Managing Director Kapstream Capital Two sides to every story 3 2010 bottom line Right