Transmission of Financial and Real Shocks in the Global Economy Using the GVAR

|

|

|

- Rudolf Cole

- 5 years ago

- Views:

Transcription

1 Transmission of Financial and Real Shocks in the Global Economy Using the GVAR Hashem Pesaran University of Cambridge For presentation at Conference on The Big Crunch and the Big Bang, Cambridge, November 21, /11/2008 1

2 Agenda An overview of the global VAR (GVAR) as a framework for the analysis of shocks and their transmission in the global economy. Developing a new GVAR_33 model for the analysis of the effects of shocks on individual. Evaluating the effects of oil and equity price shocks on real economies in the global system. Comparing the responses of euro and non-euro economies to shocks. 16/11/2008 2

3 Global Dimensions of Economic Interactions Macroeconomic policy analysis and risk management require taking account of the increasing interdependencies that exist across markets and countries. National economic issues need to be considered from a global perspective. This invariably means that many different channels of transmission must be taken into account. We are presented with the task of modeling complex high dimensional systems. 16/11/2008 3

4 Patterns of Global Economic and Financial Inter-linkages An Overview There are major differences in cross country correlation of output growths, inflation, and interest rates. (See Tables that follow) Equity returns and long term interest rates are much more closely correlated across countries. US economy remains the dominant source of global economic interdependence. 16/11/2008 4

5 Output Growth Correlations Across Selected Countries in the GVAR Model ( ) China Euro Area Japan Australia Canada UK US China Euro Area Japan Australia Canada UK US /11/2008 5

6 Real Equity Return Correlations Across Selected Countries in the GVAR Model ( ) Euro Area Japan Australia Canada UK US Euro Area Japan Australia Canada UK US /11/2008 6

7 Price Inflation Correlations Across Selected Countries in the GVAR Model ( ) China Euro Area Japan Australia Canada UK US China Euro Area Japan Australia Canada UK US /11/2008 7

8 Correlation of Short Term Interests Across Selected Countries in the GVAR Model ( ) China Euro Area Japan Australia Canada UK US China Euro Area Japan Australia Canada UK US /11/2008 8

9 Correlation of Long Term Interests Across Selected Countries in the GVAR Model ( ) Euro Area Japan Australia Canada UK US Euro Area Japan Australia Canada UK US /11/2008 9

10 Economic Shocks and their Transmissions In economic systems agents acting in their selfinterest tend to respond to shocks, particularly if they are adverse, in a similar manner but with differing degrees, as often seen in swarm behaviour. In the case of the swarms the shock initially affects the outer layer which is then transmitted very rapidly to the rest via neighbourhood effects. In economics the transmission of shocks is far more complex and takes place through a variety of channels: 16/11/

11 16/11/

12 Channels of Transmission of Shocks in Economic Systems Common observed shocks (such as changes in oil prices) Common unobserved factors (such as the diffusion of technological progress) Specific national or sectoral shocks Residual interdependencies (after "common" factors are taken into account) due to social inter-actions or policy and trade spill-over effects 16/11/

13 Genesis of the GVAR Dealing with economic relations in isolation and only for a single market or economy can be misleading, very much like considering the movement of a single wildebeest in isolation from the herd! Multi-layer panel data models provide an appropriate framework for the analysis of complex inter-related systems in economics. But their successful implementation face significant challenges; including data availability and data quality, heterogeneity, unobserved effects, and spatial (or network) interactions. The global VAR modelling approach represents an example of how these challenges can be addressed. Using infinite dimensional VARs Chudik and Pesaran (2008) provide a theoretical motivation. 16/11/

14 Modelling Interactions Within and Between Euro Economies The GAVR developed in Dees et al. (2007, JAE) estimates a 26 country/region model with euro area as a single economy. Recently, with Vanessa Smith, I have constructed a new GVAR model where the main 8 euro economies (Austria, Belgium, France, Italy, Germany, Finland, Netherlands and Spain) are modeled as individual economies in a global context The estimation sample is also extended and covers the period 1979Q1-2006Q4 (as compared to 1979Q1-2003Q4 previously) 16/11/

15 Theoretical Frameworks and Counterfactuals Before presenting the empirical results we begin with an overview of the GVAR model Details can be found in Pesaran, Schuermann and Weiner (2004, JBES), Dees et al. (2007, JAE), Pesaran and Chudik (2008) GVAR links individual country error correction models by means of foreign variables constructed using trade weights. 16/11/

16 Country Specific VARX* Models 16/11/

17 Error Correcting Country Specific Models 16/11/

18 Solving the GVAR 16/11/

19 Solving the GVAR (Continued) 16/11/

20 Solving the GVAR (Continued) 16/11/

21 Empirical Results We begin by examining the data on the euro economies and by comparing them to those prevailing in a group of reference economies: Australia, Canada, Japan, Norway, Sweden, Switzerland, UK and US. Such a comparison allows us to shed light on the quantitative nature of the effects of the introduction of the euro on inflation and output growth across the countries in the euro area. 16/11/

22 Euro Area Currencies Aus tria Belgium Finland France Germany Italy Netherlands Spain Euro 1979Q1 1980Q2 1981Q3 1982Q4 1984Q1 1985Q2 1986Q3 1987Q4 1989Q1 1990Q2 1991Q3 1992Q4 1994Q1 1995Q2 1996Q3 1997Q4 1999Q1 2000Q2 2001Q3 2002Q4 2004Q1 2005Q2 2006Q3 16/11/

23 16/11/ Short Term Rates Q1 1980Q1 1981Q1 1982Q1 1983Q1 1984Q1 1985Q1 1986Q1 1987Q1 1988Q1 1989Q1 1990Q1 1991Q1 1992Q1 1993Q1 1994Q1 1995Q1 1996Q1 1997Q1 1998Q1 1999Q1 2000Q1 2001Q1 2002Q1 2003Q1 2004Q1 2005Q1 2006Q1 Aus tria Belgium Finland France Germany Italy Netherlands Spain Q1 1980Q2 1981Q3 1982Q4 1984Q1 1985Q2 1986Q3 1987Q4 1989Q1 1990Q2 1991Q3 1992Q4 1994Q1 1995Q2 1996Q3 1997Q4 1999Q1 2000Q2 2001Q3 2002Q4 2004Q1 2005Q2 2006Q3 Australia Canada Japan Norway Sweden Switzerland UK US

24 16/11/ Long Term Rates Q1 1980Q1 1981Q1 1982Q1 1983Q1 1984Q1 1985Q1 1986Q1 1987Q1 1988Q1 1989Q1 1990Q1 1991Q1 1992Q1 1993Q1 1994Q1 1995Q1 1996Q1 1997Q1 1998Q1 1999Q1 2000Q1 2001Q1 2002Q1 2003Q1 2004Q1 2005Q1 2006Q1 Austria Belgium France Germany Italy Netherlands Spain Q1 1980Q2 1981Q3 1982Q4 1984Q1 1985Q2 1986Q3 1987Q4 1989Q1 1990Q2 1991Q3 1992Q4 1994Q1 1995Q2 1996Q3 1997Q4 1999Q1 2000Q2 2001Q3 2002Q4 2004Q1 2005Q2 2006Q3 Australia Canada Japan Norw ay Sw eden Sw itzerland UK US

25 16/11/ Inflation Q1 1980Q2 1981Q3 1982Q4 1984Q1 1985Q2 1986Q3 1987Q4 1989Q1 1990Q2 1991Q3 1992Q4 1994Q1 1995Q2 1996Q3 1997Q4 1999Q1 2000Q2 2001Q3 2002Q4 2004Q1 2005Q2 2006Q3 Austria Belgium Finland France Germany Italy Netherlands Spain Q1 1980Q2 1981Q3 1982Q4 1984Q1 1985Q2 1986Q3 1987Q4 1989Q1 1990Q2 1991Q3 1992Q4 1994Q1 1995Q2 1996Q3 1997Q4 1999Q1 2000Q2 2001Q3 2002Q4 2004Q1 2005Q2 2006Q3 Australia Canada Japan Norway Sweden Switzerland UK US

26 16/11/ Output Growth Q1 1980Q2 1981Q3 1982Q4 1984Q1 1985Q2 1986Q3 1987Q4 1989Q1 1990Q2 1991Q3 1992Q4 1994Q1 1995Q2 1996Q3 1997Q4 1999Q1 2000Q2 2001Q3 2002Q4 2004Q1 2005Q2 2006Q3 Austria Belgium Finland France Germany Italy Netherlands Spain Q1 1980Q2 1981Q3 1982Q4 1984Q1 1985Q2 1986Q3 1987Q4 1989Q1 1990Q2 1991Q3 1992Q4 1994Q1 1995Q2 1996Q3 1997Q4 1999Q1 2000Q2 2001Q3 2002Q4 2004Q1 2005Q2 2006Q3 Australia Canada Japan Norw ay Sw eden Sw itzerland UK US

27 Countries and Regions in the GVAR_33 Model Unites States Euro Area Latin America China Germany Brazil Japan France Mexico United Kingdom Italy Argentina Other Developed Economies Spain Chile Canada Netherlands Peru Australia New Zealand Belgium Austria Finland Rest of Asia Rest of W.Europe Rest of the World Korea Sweden India Indonesia Switzerland South Africa Thailand Norway Turkey Philippines Saudi Arabia Malaysia Singapore 16/11/

28 Variables Included in the Individual Country Models Most country specific models include the following endogenous variables 16/11/

29 Trade Weights used to Construct Foreign (Star) Variables Country/ region US EA China Japan UK Rest of W. Europe Sweden Switz. Norway Rest* US EA China Japan UK Sweden Switz Norway /11/

30 Domestic and Foreign Variables Included in Country-Specific Models All Countries Excluding US Variables Endogenous Foreign Endogenous Foreign Real Output y it y it y us,t y us,t Inflation it it us,t us,t US Real Exchange Rate e it p it - - e us,t p us,t Real Equity Price q it q it q us,t - Short-Term Interest Rate S r it S r it S r us,t - Long-Term Interest Rate L r it L r it L r us,t - Oil Price - p t o p t o - 16/11/

31 Properties of GVAR The model has 175 endogenous variables 99 stochastic trends and 76 long-run (cointegrating) relations. It is globally stable; all its roots either lie on or inside the unit circle. Although log-linear with a simple overall structure, GVAR is a large and complicated model which allows for a high degree of interdependence and dynamics. 16/11/

32 Properties of GVAR (continued) Shocks to one country can have marked effects on other countries, depending on their size and the patterns of their trade. GVAR model is quite effective in dealing with the common factor interdependencies and international comovements of business cycles. Unlike the very high cross section correlation of the core variables, the residuals from the GVAR are hardly correlated across countries, with the notable exception of exchange rates. See Table below. The failure of the GVAR to deal with the cross section correlation of exchange rates could be due to the dominant role that the US dollar plays in foreign exchange rate markets. 16/11/

33 Average Pair-wise Cross Section Correlations VAR VARX* Levels 1st diff. residuals residuals Real output US Euro area Inflation US Euro area Real equity prices US Euro area Real exchange rate Short term interest rates US Euro area Long term interest rates US Euro area /11/

34 Uses of the GVAR Model Strategic Asset Management Credit Risk Analysis - It has been used successfully as a global economic engine in conditional credit risk modeling by Pesaran, Schuermann, Treutler, and Weiner, (2006,JMCB),and Pesaran, Schuermann and Treutler (2006, NBER Vol.) Short and Medium Term Forecasting Impulse Response (Counterfactual) Analysis Direct and indirect trade linkages Financial linkages, most notably through interest rates, stock prices and exchange rates, which have proved to be particularly relevant over the recent past. 16/11/

35 Effects of Shocks to US Economy and Oil Prices Three Types of shocks are considered as examples: A positive shock to oil prices A negative shock to US real output A negative shock to US real equity prices We show the impact on the US and the transmission of the shocks to the rest of the world economy 16/11/

36 Effects of a positive unit shock to oil prices. 16/11/

37 Impulse Response of a Positive Unit (+1σ) Shock to Oil Prices on Inflation Across the EA and Reference Countries Austria Belgium Finland France Germany Italy Netherlands Spain Quarters Quarters Japan Austlia Can Nor Swe Switz UK USA 16/11/

38 Impulse Response of a Positive Unit (+1σ) Shock to Oil Prices on Inflation in the EA Quarters EA 16/11/

39 Impulse Response of a Positive Unit (+1σ) Shock to Oil Prices on Real Output Across the EA and Reference Countries Quarters Austria Belgium Finland France Germany Italy Netherlands Spain Japan Austlia Can Nor Swe Switz UK USA Quarters /11/

40 Impulse Response of a Positive Unit (+1σ) Shock to Oil Prices on Real Output in the EA Quarters EA 16/11/

41 Impulse Response of a Positive Unit (+1σ) Shock to Oil Prices on Long Term Interest Rates Across the EA and Reference Countries Quarters Austria Belgium France Germany Italy Netherlands Spain Japan Austlia Can Nor Swe Switz UK USA Quarters 16/11/

42 Impulse Response of a Positive Unit (+1σ) Shock to Oil Prices on Long Term Interest Rates in the EA Quarters EA 16/11/

43 Impulse Response of a Positive Unit (+1σ) Shock to Oil Prices on Real Equity Prices Across the EA and Reference Countries Austria Belgium Finland France Germany Italy Netherlands Spain -8.0 Quarters Japan Austlia Can Nor Swe Switz UK USA /11/ Quarters 43

44 Impulse Response of a Positive Unit (+1σ) Shock to Oil Prices on Real Equity in the EA Quarters EA 16/11/

45 Effects of a negative unit shock to US output 16/11/

46 Impulse Response of a Negative Unit (-1σ) Shock to US Real Output on Oil Prices Quarters USA 16/11/

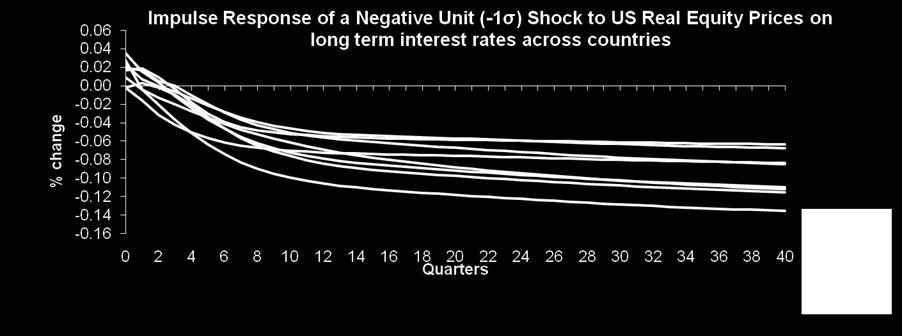

47 Impulse Response of a Negative Unit (-1σ) Shock to US Real Output on Inflation Across the EA and Reference Countries Austria Belgium Finland France Germany Italy Netherlands Spain Quarters Quarters Japan Austlia Can Nor Swe Switz UK USA /11/

48 Impulse Response of a Negative Unit (-1σ) Shock to US Real Output on Inflation in the EA Quarters EA 16/11/

49 Impulse Response of a Negative Unit (-1σ) Shock to US Real Output on Short Term Interest Rates Across the EA and Reference Countries Austria Belgium Finland France Germany Italy Netherlands Spain Quarters Japan Austlia Can Nor Swe Switz UK USA Quarters 16/11/

50 Impulse Response of a Negative Unit (-1σ) Shock to US Real Output on Short Term Interest Rates in the EA Quarters EA 16/11/

51 Impulse Response of a Negative Unit (-1σ) Shock to US Real Output on Long Term Interest Rates Across the EA and Reference Countries Quarters Austria Belgium France Germany Italy Netherlands Spain Japan Austlia Can Nor Swe Switz UK USA Quarters 16/11/

52 Impulse Response of a Negative Unit (-1σ) Shock to US Real Output on Long Term Interest Rates in the EA Quarters EA 16/11/

53 Effects of a negative unit shock to US real equity prices 16/11/

54 Impulse Response of a Negative Unit (-1σ) Shock to US Real Equity Prices on Real Equity Across the EA and Reference Countries Austria Belgium Finland France Germany Italy Netherlands Spain Quarters Japan Austlia Can Nor Swe Switz UK USA /11/ Quarters

55 Impulse Response of a Negative Unit (-1σ) Shock to US Real Equity Prices on Real Equity in the EA Quarters EA 16/11/

56 16/11/

57 16/11/

58 16/11/

59 Conclusions GVAR provides a theoretically coherent framework for modelling the global interactions. The empirical analysis so far suggests that: Financial shocks (equity and bond prices) tend to be transmitted much faster than shocks to real output and/or inflation. Equity and bond markets seem to be far more synchronous as compared to the foreign exchange markets. The effects of output shocks across countries is less synchronous than inflation shocks, which is still less synchronous than the effects of shocks to financial variables. 16/11/

60 Conclusions (continued) Negative shocks to real equity prices in the US are transmitted rapidly to the rest of the world with unfavorable consequences for the real economy. A positive oil price shocks tend to increase inflation, reduce real output, and real equity prices, although the exact quantitative effects vary considerably across economies. Shocks generally take 3-4 years to have their full effects. 16/11/

61 Conclusions (continued) Cross country comparisons often require quite complicated models that can allow for a variety of dynamic interactions, at national and global levels. Financial and real shocks transmit at very different rates. Financial shocks (equity and bond prices tend to be transmitted much faster than shocks to real output and/or inflation. Equity and bond markets seem to be far more synchronous as compared to the foreign exchange markets. 16/11/

62 Conclusions (continued) Comparing the effects of the shocks on the euro area economy and the rest of Europe, results show striking similarities. Effects of oil price shocks tend to be accentuated by monetary policy responses particularly led by the US Thank You! More details available on 16/11/

Uncertainty and Economic Activity: A Global Perspective

Uncertainty and Economic Activity: A Global Perspective Ambrogio Cesa-Bianchi 1 M. Hashem Pesaran 2 Alessandro Rebucci 3 IV International Conference in memory of Carlo Giannini 26 March 2014 1 Bank of

Uncertainty and Economic Activity: A Global Perspective Ambrogio Cesa-Bianchi 1 M. Hashem Pesaran 2 Alessandro Rebucci 3 IV International Conference in memory of Carlo Giannini 26 March 2014 1 Bank of

Debt Financing and Real Output Growth: Is There a Threshold Effect?

Debt Financing and Real Output Growth: Is There a Threshold Effect? M. Hashem Pesaran Department of Economics & USC Dornsife INET, University of Southern California, USA and Trinity College, Cambridge,

Debt Financing and Real Output Growth: Is There a Threshold Effect? M. Hashem Pesaran Department of Economics & USC Dornsife INET, University of Southern California, USA and Trinity College, Cambridge,

Toward a Better Understanding of Macroeconomic Interdependence

16 FEDERAL RESERVE BANK OF DALLAS Globalization and Monetary Policy Institute 014 Annual Report Toward a Better Understanding of Macroeconomic Interdependence By Alexander Chudik The concept of a representative

16 FEDERAL RESERVE BANK OF DALLAS Globalization and Monetary Policy Institute 014 Annual Report Toward a Better Understanding of Macroeconomic Interdependence By Alexander Chudik The concept of a representative

Reporting practices for domestic and total debt securities

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

Corrigendum. OECD Pensions Outlook 2012 DOI: ISBN (print) ISBN (PDF) OECD 2012

ISBN (PDF) OECD 2012") OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

Financial wealth of private households worldwide

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

2013 Global Survey of Accounting Assumptions. for Defined Benefit Plans. Executive Summary

2013 Global Survey of Accounting Assumptions for Defined Benefit Plans Executive Summary Executive Summary In broad terms, accounting standards aim to enable employers to approximate the cost of an employee

2013 Global Survey of Accounting Assumptions for Defined Benefit Plans Executive Summary Executive Summary In broad terms, accounting standards aim to enable employers to approximate the cost of an employee

Is Economic Growth Good for Investors? Jay R. Ritter University of Florida

Is Economic Growth Good for Investors? Jay R. Ritter University of Florida What (modern day) country had the highest per capita income, in the following years? 1500 1650 1800 1870 1900 1920 It is widely

Is Economic Growth Good for Investors? Jay R. Ritter University of Florida What (modern day) country had the highest per capita income, in the following years? 1500 1650 1800 1870 1900 1920 It is widely

2018 Global Survey of Accounting Assumptions. for Defined Benefit Plans. Executive summary

2018 Global Survey of Accounting Assumptions for Defined Benefit Plans Executive summary Executive summary In broad terms, accounting standards aim to enable employers to approximate the cost of an employee

2018 Global Survey of Accounting Assumptions for Defined Benefit Plans Executive summary Executive summary In broad terms, accounting standards aim to enable employers to approximate the cost of an employee

New in 2013: Greater emphasis on capital flows Refinements to EBA methodology Individual country assessments

As in 212: Stock-take: multilaterally consistent assessment of external sector policies of the largest economies Feeds into Article IVs Draws on External Balance Assessment (EBA) methodology/other Identifies

As in 212: Stock-take: multilaterally consistent assessment of external sector policies of the largest economies Feeds into Article IVs Draws on External Balance Assessment (EBA) methodology/other Identifies

Quarterly Investment Update First Quarter 2018

Quarterly Investment Update First Quarter 2018 Dimensional Fund Advisors Canada ULC ( DFA Canada ) is not affiliated with [insert name of Advisor]. DFA Canada is a separate and distinct company. Market

Quarterly Investment Update First Quarter 2018 Dimensional Fund Advisors Canada ULC ( DFA Canada ) is not affiliated with [insert name of Advisor]. DFA Canada is a separate and distinct company. Market

DFA Global Equity Portfolio (Class F) Quarterly Performance Report Q2 2014

Quarterly Performance Report Q2 2014") DFA Global Equity Portfolio (Class F) Quarterly Performance Report Q2 2014 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds.

DFA Global Equity Portfolio (Class F) Quarterly Performance Report Q2 2014 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds.

Quarterly Investment Update First Quarter 2017

Quarterly Investment Update First Quarter 2017 Market Update: A Quarter in Review March 31, 2017 CANADIAN STOCKS INTERNATIONAL STOCKS Large Cap Small Cap Growth Value Large Cap Small Cap Growth Value Emerging

Quarterly Investment Update First Quarter 2017 Market Update: A Quarter in Review March 31, 2017 CANADIAN STOCKS INTERNATIONAL STOCKS Large Cap Small Cap Growth Value Large Cap Small Cap Growth Value Emerging

DFA Global Equity Portfolio (Class F) Performance Report Q3 2018

Performance Report Q3 2018") DFA Global Equity Portfolio (Class F) Performance Report Q3 2018 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q3 2018 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q4 2017

Performance Report Q4 2017") DFA Global Equity Portfolio (Class F) Performance Report Q4 2017 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q4 2017 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q2 2017

Performance Report Q2 2017") DFA Global Equity Portfolio (Class F) Performance Report Q2 2017 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q2 2017 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

The Challenge of Public Pension Reform in Advanced and Emerging Economies

The Challenge of Public Pension Reform in Advanced and Emerging Economies Mauricio Soto Fiscal Affairs Department International Monetary Fund January 212 The views expressed herein are those of the author

The Challenge of Public Pension Reform in Advanced and Emerging Economies Mauricio Soto Fiscal Affairs Department International Monetary Fund January 212 The views expressed herein are those of the author

DFA Global Equity Portfolio (Class F) Performance Report Q3 2015

Performance Report Q3 2015") DFA Global Equity Portfolio (Class F) Performance Report Q3 2015 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q3 2015 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

Corporate Governance and Investment Performance: An International Comparison. B. Burçin Yurtoglu University of Vienna Department of Economics

Corporate Governance and Investment Performance: An International Comparison B. Burçin Yurtoglu University of Vienna Department of Economics 1 Joint Research with Klaus Gugler and Dennis Mueller http://homepage.univie.ac.at/besim.yurtoglu/unece/unece.htm

Corporate Governance and Investment Performance: An International Comparison B. Burçin Yurtoglu University of Vienna Department of Economics 1 Joint Research with Klaus Gugler and Dennis Mueller http://homepage.univie.ac.at/besim.yurtoglu/unece/unece.htm

Global Economic Briefing: Global Liquidity

Global Economic Briefing: Global Liquidity December 21, 217 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 48-664-1333 djohnson@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at

Global Economic Briefing: Global Liquidity December 21, 217 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 48-664-1333 djohnson@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at

EQUITY REPORTING & WITHHOLDING. Updated May 2016

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

DIVERSIFICATION. Diversification

Diversification Helps you capture what global markets offer Reduces risks that have no expected return May prevent you from missing opportunity Smooths out some of the bumps Helps take the guesswork out

Diversification Helps you capture what global markets offer Reduces risks that have no expected return May prevent you from missing opportunity Smooths out some of the bumps Helps take the guesswork out

EDHECinfra Broad Market Index Families

EDHECinfra Broad Market Index Families Unlisted Infrastructure Equity Index Families Global Unlisted Infrastructure Equity Global Project Finance Equity Advanced Markets Unlisted Infrastructure Equity

EDHECinfra Broad Market Index Families Unlisted Infrastructure Equity Index Families Global Unlisted Infrastructure Equity Global Project Finance Equity Advanced Markets Unlisted Infrastructure Equity

San Francisco Retiree Health Care Trust Fund Education Materials on Public Equity

M E K E T A I N V E S T M E N T G R O U P 5796 ARMADA DRIVE SUITE 110 CARLSBAD CA 92008 760 795 3450 fax 760 795 3445 www.meketagroup.com The Global Equity Opportunity Set MSCI All Country World 1 Index

M E K E T A I N V E S T M E N T G R O U P 5796 ARMADA DRIVE SUITE 110 CARLSBAD CA 92008 760 795 3450 fax 760 795 3445 www.meketagroup.com The Global Equity Opportunity Set MSCI All Country World 1 Index

STOXX EMERGING MARKETS INDICES. UNDERSTANDA RULES-BA EMERGING MARK TRANSPARENT SIMPLE

STOXX Limited STOXX EMERGING MARKETS INDICES. EMERGING MARK RULES-BA TRANSPARENT UNDERSTANDA SIMPLE MARKET CLASSIF INTRODUCTION. Many investors are seeking to embrace emerging market investments, because

STOXX Limited STOXX EMERGING MARKETS INDICES. EMERGING MARK RULES-BA TRANSPARENT UNDERSTANDA SIMPLE MARKET CLASSIF INTRODUCTION. Many investors are seeking to embrace emerging market investments, because

FOREIGN ACTIVITY REPORT

FOREIGN ACTIVITY REPORT SECOND QUARTER 2012 TABLE OF CONTENTS Table of Contents... i All Securities Transactions... 2 Highlights... 2 U.S. Transactions in Foreign Securities... 2 Foreign Transactions in

FOREIGN ACTIVITY REPORT SECOND QUARTER 2012 TABLE OF CONTENTS Table of Contents... i All Securities Transactions... 2 Highlights... 2 U.S. Transactions in Foreign Securities... 2 Foreign Transactions in

BRINKER CAPITAL DESTINATIONS TRUST

Important 2018 Tax Information Regarding Your Mutual s BRINKER CAPITAL DESTINATIONS TRUST The following tax information is furnished for informational purposes only. Please consult your tax advisor for

Important 2018 Tax Information Regarding Your Mutual s BRINKER CAPITAL DESTINATIONS TRUST The following tax information is furnished for informational purposes only. Please consult your tax advisor for

Global Select International Select International Select Hedged Emerging Market Select

International Exchange Traded Fund (ETF) Managed Strategies ETFs provide investors a liquid, transparent, and low-cost avenue to equities around the world. Our research has shown that individual country

International Exchange Traded Fund (ETF) Managed Strategies ETFs provide investors a liquid, transparent, and low-cost avenue to equities around the world. Our research has shown that individual country

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile. 4-6 October 2017

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile 4-6 October 2017 Graham Robinson Global Construction Perspectives Global Construction 2030 is the fourth in a series of global studies of the construction

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile 4-6 October 2017 Graham Robinson Global Construction Perspectives Global Construction 2030 is the fourth in a series of global studies of the construction

A short history of debt

A short history of debt In the words of the late Charles Kindleberger, debt/financial crises are a hardy perennial we have been here many times before. Over the past decade and a half the ratio of global

A short history of debt In the words of the late Charles Kindleberger, debt/financial crises are a hardy perennial we have been here many times before. Over the past decade and a half the ratio of global

Important Information

Important Information CDP is an independent not-for-profit organization that has been requesting information relating to carbon and climate change on behalf of investors since 2002. Thousands of organizations

Important Information CDP is an independent not-for-profit organization that has been requesting information relating to carbon and climate change on behalf of investors since 2002. Thousands of organizations

Key Issues in the Design of Capital Gains Tax Regimes: Taxing Non- Residents. 18 July 2014

Key Issues in the Design of Capital Gains Tax Regimes: Taxing Non- Residents 18 July 2014 How do we tax non-residents on capital income? Domestic design issues Tax treaty issues Interrelationship between

Key Issues in the Design of Capital Gains Tax Regimes: Taxing Non- Residents 18 July 2014 How do we tax non-residents on capital income? Domestic design issues Tax treaty issues Interrelationship between

Global Edge: to Manage the Risks of Cross-Border Business. Joel Kurtzman Chairman, Kurtzman Group

Global Edge: Using the Opacity Index to Manage the Risks of Cross-Border Business Joel Kurtzman Chairman, Kurtzman Group Senior Fellow, Milken Institute Approach Today s hypercompetition changes the old

Global Edge: Using the Opacity Index to Manage the Risks of Cross-Border Business Joel Kurtzman Chairman, Kurtzman Group Senior Fellow, Milken Institute Approach Today s hypercompetition changes the old

Global Business Barometer April 2008

Global Business Barometer April 2008 The Global Business Barometer is a quarterly business-confidence index, conducted for The Economist by the Economist Intelligence Unit What are your expectations of

Global Business Barometer April 2008 The Global Business Barometer is a quarterly business-confidence index, conducted for The Economist by the Economist Intelligence Unit What are your expectations of

2010/IEG/WKSP1/002 Overview of IIAs and Treaty-Based Investment Disputes

21/IEG/WKSP1/2 Overview of IIAs and Treaty-Based Investment Disputes Submitted by: UNCTAD Workshop on Dispute Prevention and Preparedness Washington, DC, United States 26-3 July 21 Workshop on dispute

21/IEG/WKSP1/2 Overview of IIAs and Treaty-Based Investment Disputes Submitted by: UNCTAD Workshop on Dispute Prevention and Preparedness Washington, DC, United States 26-3 July 21 Workshop on dispute

The construction of long time series on credit to the private and public sector

29 August 2014 The construction of long time series on credit to the private and public sector Christian Dembiermont 1 Data on credit aggregates have been at the centre of BIS financial stability analysis

29 August 2014 The construction of long time series on credit to the private and public sector Christian Dembiermont 1 Data on credit aggregates have been at the centre of BIS financial stability analysis

EP UNEP/OzL.Pro.WG.1/39/INF/2

UNITED NATIONS EP UNEP/OzL.Pro.WG.1/39/INF/2 Distr.: General 26 May English only United Nations Environment Programme Open-ended Working Group of the Parties to the Montreal Protocol on Substances that

UNITED NATIONS EP UNEP/OzL.Pro.WG.1/39/INF/2 Distr.: General 26 May English only United Nations Environment Programme Open-ended Working Group of the Parties to the Montreal Protocol on Substances that

Guide to Treatment of Withholding Tax Rates. January 2018

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Global Consumer Confidence

Global Consumer Confidence The Conference Board Global Consumer Confidence Survey is conducted in collaboration with Nielsen 4TH QUARTER 2017 RESULTS CONTENTS Global Highlights Asia-Pacific Africa and

Global Consumer Confidence The Conference Board Global Consumer Confidence Survey is conducted in collaboration with Nielsen 4TH QUARTER 2017 RESULTS CONTENTS Global Highlights Asia-Pacific Africa and

26 MAY Boustead Singapore Limited / Boustead Projects Limited Joint FY2015 Financial Results Presentation

26 MAY 2015 Boustead Singapore Limited / Boustead Projects Limited Joint FY2015 Financial Results Presentation Disclaimer This presentation contains certain statements that are not statements of historical

26 MAY 2015 Boustead Singapore Limited / Boustead Projects Limited Joint FY2015 Financial Results Presentation Disclaimer This presentation contains certain statements that are not statements of historical

MERCER SMARTDB TM A SMARTER APPROACH TO MANAGING LONGEVITY RISK

MERCER SMARTDB TM A SMARTER APPROACH TO MANAGING LONGEVITY RISK www.uk.mercer.com/smartdb MERCER SMARTDB TM A SMARTER APPROACH TO MANAGING LONGEVITY RISK Mercer SmartDB TM is a groundbreaking new solution

MERCER SMARTDB TM A SMARTER APPROACH TO MANAGING LONGEVITY RISK www.uk.mercer.com/smartdb MERCER SMARTDB TM A SMARTER APPROACH TO MANAGING LONGEVITY RISK Mercer SmartDB TM is a groundbreaking new solution

COUNTRY COST INDEX JUNE 2013

COUNTRY COST INDEX JUNE 2013 June 2013 Kissell Research Group, LLC 1010 Northern Blvd., Suite 208 Great Neck, NY 11021 www.kissellresearch.com Kissell Research Group Country Cost Index - June 2013 2 Executive

COUNTRY COST INDEX JUNE 2013 June 2013 Kissell Research Group, LLC 1010 Northern Blvd., Suite 208 Great Neck, NY 11021 www.kissellresearch.com Kissell Research Group Country Cost Index - June 2013 2 Executive

Performance Derby: MSCI Regions & Countries STRG, STEG, & LTEG

Performance Derby: MSCI Regions & Countries STRG, STEG, & LTEG February 7, 2018 Dr. Ed Yardeni 516-972-7683 eyardeni@yardeni.com Joe Abbott 732-497-5306 jabbott@yardeni.com Please visit our sites at blog.yardeni.com

Performance Derby: MSCI Regions & Countries STRG, STEG, & LTEG February 7, 2018 Dr. Ed Yardeni 516-972-7683 eyardeni@yardeni.com Joe Abbott 732-497-5306 jabbott@yardeni.com Please visit our sites at blog.yardeni.com

PREDICTING VEHICLE SALES FROM GDP

UMTRI--6 FEBRUARY PREDICTING VEHICLE SALES FROM GDP IN 8 COUNTRIES: - MICHAEL SIVAK PREDICTING VEHICLE SALES FROM GDP IN 8 COUNTRIES: - Michael Sivak The University of Michigan Transportation Research

UMTRI--6 FEBRUARY PREDICTING VEHICLE SALES FROM GDP IN 8 COUNTRIES: - MICHAEL SIVAK PREDICTING VEHICLE SALES FROM GDP IN 8 COUNTRIES: - Michael Sivak The University of Michigan Transportation Research

Summary of key findings

1 VAT/GST treatment of cross-border services: 2017 survey Supplies of e-services to consumers (B2C) (see footnote 1) Supplies of e-services to businesses (B2B) 1(a). Is a non-resident 1(b). If there is

1 VAT/GST treatment of cross-border services: 2017 survey Supplies of e-services to consumers (B2C) (see footnote 1) Supplies of e-services to businesses (B2B) 1(a). Is a non-resident 1(b). If there is

Public Pension Spending Trends and Outlook in Emerging Europe. Benedict Clements Fiscal Affairs Department International Monetary Fund March 2013

Public Pension Spending Trends and Outlook in Emerging Europe Benedict Clements Fiscal Affairs Department International Monetary Fund March 13 Plan of Presentation I. Trends and drivers of public pension

Public Pension Spending Trends and Outlook in Emerging Europe Benedict Clements Fiscal Affairs Department International Monetary Fund March 13 Plan of Presentation I. Trends and drivers of public pension

Corrigendum. Page 41, Table 1.A1.1. Details of pension reforms, September 2013-September 2015 : Columns on Portugal should read as follows:

Pensions at a Glance: OECD and G Indicators DOI: http://dx.doi.org/.787/pension_glance-5-en ISBN 9789644636 (print) ISBN 97896444443 (PDF) OECD 5 Corrigendum Page 4, Table.A.. Details of pension reforms,

Pensions at a Glance: OECD and G Indicators DOI: http://dx.doi.org/.787/pension_glance-5-en ISBN 9789644636 (print) ISBN 97896444443 (PDF) OECD 5 Corrigendum Page 4, Table.A.. Details of pension reforms,

Corporate Governance and

Corporate Governance and Third Edition Jill Solomon )WILEY A John Wiley and Sons, Ltd, Publication Preface Acknowledgements Introducton xv xvii xix Part I Corporate governance: frameworks and mechanisms

Corporate Governance and Third Edition Jill Solomon )WILEY A John Wiley and Sons, Ltd, Publication Preface Acknowledgements Introducton xv xvii xix Part I Corporate governance: frameworks and mechanisms

IMPORTANT TAX INFORMATION

00126803 IMPORTANT TAX INFORMATION Dear Hartford Funds Shareholder: The following information about your enclosed 1099-DIV from Hartford Funds should be used when preparing your 2014 tax return. The information

00126803 IMPORTANT TAX INFORMATION Dear Hartford Funds Shareholder: The following information about your enclosed 1099-DIV from Hartford Funds should be used when preparing your 2014 tax return. The information

Turkey s Saving Deficit Issue From an Institutional Perspective

Turkey s Saving Deficit Issue From an Institutional Perspective Engin KURUN, Ph.D CEO, Ziraat Asset Management Oct. 25th, 2011 - Istanbul 1 PRESENTATION Household and Institutional Savings Institutional

Turkey s Saving Deficit Issue From an Institutional Perspective Engin KURUN, Ph.D CEO, Ziraat Asset Management Oct. 25th, 2011 - Istanbul 1 PRESENTATION Household and Institutional Savings Institutional

Market Briefing: Global Markets

Market Briefing: Global Markets July 6, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at blog. thinking outside the box Table Of Contents Table

Market Briefing: Global Markets July 6, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at blog. thinking outside the box Table Of Contents Table

Global Economic Briefing: Global Inflation

Global Economic Briefing: Global Inflation November, 7 Dr. Edward Yardeni -97-7 eyardeni@ Debbie Johnson -- djohnson@ Mali Quintana -- aquintana@ Please visit our sites at www. blog. thinking outside the

Global Economic Briefing: Global Inflation November, 7 Dr. Edward Yardeni -97-7 eyardeni@ Debbie Johnson -- djohnson@ Mali Quintana -- aquintana@ Please visit our sites at www. blog. thinking outside the

International Statistical Release

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org). Worldwide Investment Fund Assets and Flows Trends in the

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org). Worldwide Investment Fund Assets and Flows Trends in the

HOW TO BE MORE OPPORTUNISTIC

HOW TO BE MORE OPPORTUNISTIC HOW TO BE MORE OPPORTUNISTIC Page 2 Over the last decade, institutional investors across much of the developed world have gradually reduced their exposure to equity markets.

HOW TO BE MORE OPPORTUNISTIC HOW TO BE MORE OPPORTUNISTIC Page 2 Over the last decade, institutional investors across much of the developed world have gradually reduced their exposure to equity markets.

Sovereign Bond Yield Spreads: An International Analysis Giuseppe Corvasce

Sovereign Bond Yield Spreads: An International Analysis Giuseppe Corvasce Rutgers University Center for Financial Statistics and Risk Management Society for Financial Studies 8 th Financial Risks and INTERNATIONAL

Sovereign Bond Yield Spreads: An International Analysis Giuseppe Corvasce Rutgers University Center for Financial Statistics and Risk Management Society for Financial Studies 8 th Financial Risks and INTERNATIONAL

An FSE Listings Inc Article FSE Listings Inc- Frankfurt Stock Exchange Listings

FSE Listings How To Prepare Yourself For Listing On The Frankfurt Stock Exchange Author: Mark Bragg An FSE Listings Inc Article FSE Listings Inc- Frankfurt Stock Exchange Listings List your firm fast with

FSE Listings How To Prepare Yourself For Listing On The Frankfurt Stock Exchange Author: Mark Bragg An FSE Listings Inc Article FSE Listings Inc- Frankfurt Stock Exchange Listings List your firm fast with

International Statistical Release

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org). Worldwide Regulated Open-ended Fund Assets and Flows Trends

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org). Worldwide Regulated Open-ended Fund Assets and Flows Trends

FEES SCHEDULE (COPPER / GOLD)

") FEES SCHEDULE (COPPER / GOLD) Applicable from April 208 excluding discretionary management agreement and investment advisory agreement CBP Quilvest LU EN Fees Schedule Excluding Management April 208 /5

FEES SCHEDULE (COPPER / GOLD) Applicable from April 208 excluding discretionary management agreement and investment advisory agreement CBP Quilvest LU EN Fees Schedule Excluding Management April 208 /5

What is the relationship between financial satisfaction and happiness among older people?

What is the relationship between financial satisfaction and happiness among older people? An analysis using the World Values Survey 1981-2008 Jessica Watson, International Longevity Centre UK @ilcuk This

What is the relationship between financial satisfaction and happiness among older people? An analysis using the World Values Survey 1981-2008 Jessica Watson, International Longevity Centre UK @ilcuk This

World s Best Investment Bank Awards 2018

Global Finance will publish its selections for the 19th Annual World s Best Investment Banks in the April 2018 issue. Winners will be honored at an awards ceremony in New York City in March, and all award

Global Finance will publish its selections for the 19th Annual World s Best Investment Banks in the April 2018 issue. Winners will be honored at an awards ceremony in New York City in March, and all award

The Challenge of Public Pension Reform

The Challenge of Public Pension Reform Baoping Shang Fiscal Affairs Department International Monetary Fund May 4, 212 This presentation represents the views of the author and should not be attributed to

The Challenge of Public Pension Reform Baoping Shang Fiscal Affairs Department International Monetary Fund May 4, 212 This presentation represents the views of the author and should not be attributed to

HEALTH WEALTH CAREER 2016 CA MTCS: MERCER TOTAL COMPENSATION SURVEY FOR THE ENERGY SECTOR OVERVIEW AND SURVEY DEFINITIONS

HEALTH WEALTH CAREER 2016 CA MTCS: MERCER TOTAL COMPENSATION SURVEY FOR THE ENERGY SECTOR OVERVIEW AND SURVEY DEFINITIONS The analysis of the compensation and related information collected is displayed

HEALTH WEALTH CAREER 2016 CA MTCS: MERCER TOTAL COMPENSATION SURVEY FOR THE ENERGY SECTOR OVERVIEW AND SURVEY DEFINITIONS The analysis of the compensation and related information collected is displayed

What Can Macroeconometric Models Say About Asia-Type Crises?

What Can Macroeconometric Models Say About Asia-Type Crises? Ray C. Fair May 1999 Abstract This paper uses a multicountry econometric model to examine Asia-type crises. Experiments are run for Thailand,

What Can Macroeconometric Models Say About Asia-Type Crises? Ray C. Fair May 1999 Abstract This paper uses a multicountry econometric model to examine Asia-type crises. Experiments are run for Thailand,

FEES SCHEDULE (SILVER/PLATINUM)

") FEES SCHEDULE (SILVER/PLATINUM) Applicable from April 208 under an Investment Advisory Agreement CBP Quilvest LU EN Investment Advisory Fees Schedule April 208 /5 ADVISORY MANAGEMENT, CUSTODY FEES AND

FEES SCHEDULE (SILVER/PLATINUM) Applicable from April 208 under an Investment Advisory Agreement CBP Quilvest LU EN Investment Advisory Fees Schedule April 208 /5 ADVISORY MANAGEMENT, CUSTODY FEES AND

All-Country Equity Allocator July 2018

Leila Heckman, Ph.D. lheckman@dcmadvisors.com 917-386-6261 John Mullin, Ph.D. jmullin@dcmadvisors.com 917-386-6262 Allison Hay ahay@dcmadvisors.com 917-386-6264 All-Country Equity Allocator July 2018 A

Leila Heckman, Ph.D. lheckman@dcmadvisors.com 917-386-6261 John Mullin, Ph.D. jmullin@dcmadvisors.com 917-386-6262 Allison Hay ahay@dcmadvisors.com 917-386-6264 All-Country Equity Allocator July 2018 A

IFC / CWDI 2010 Report: Accelerating Board Diversity

IFC / CWDI 2010 Report: Accelerating Board Diversity Comparative Percentages of Women Directors -- Europe Country # of in Survey Percentage of with Women Directors Percent of Women Directors Norway 517

IFC / CWDI 2010 Report: Accelerating Board Diversity Comparative Percentages of Women Directors -- Europe Country # of in Survey Percentage of with Women Directors Percent of Women Directors Norway 517

Methodology Calculating the insurance gap

Methodology Calculating the insurance gap Insurance penetration Methodology 3 Insurance Insurance Penetration Rank Rank Rank penetration penetration difference 2018 2012 change 2018 report 2012 report

Methodology Calculating the insurance gap Insurance penetration Methodology 3 Insurance Insurance Penetration Rank Rank Rank penetration penetration difference 2018 2012 change 2018 report 2012 report

Developing Housing Finance Systems

Developing Housing Finance Systems Veronica Cacdac Warnock IIMB-IMF Conference on Housing Markets, Financial Stability and Growth December 11, 2014 Based on Warnock V and Warnock F (2012). Developing Housing

Developing Housing Finance Systems Veronica Cacdac Warnock IIMB-IMF Conference on Housing Markets, Financial Stability and Growth December 11, 2014 Based on Warnock V and Warnock F (2012). Developing Housing

!!!1!!!!!!!!!!!!!!!!!!!!!!!!!!!!! The Association of Real Estate Funds & Property Funds Research

1 The Association of Real Estate Funds & Property Funds Research Global Real Estate Funds Review H1 216 Contents CONTENTS 2 EXECUTIVE SUMMARY 3 UNLISTED FUND UNIVERSE: OVERVIEW (EX FOF) 6 UNLISTED FUNDS

1 The Association of Real Estate Funds & Property Funds Research Global Real Estate Funds Review H1 216 Contents CONTENTS 2 EXECUTIVE SUMMARY 3 UNLISTED FUND UNIVERSE: OVERVIEW (EX FOF) 6 UNLISTED FUNDS

Best Treasury & Cash Management Providers 2017

Page 1 of 5 In March 2017, Global Finance will publish its selections for the Seventeenth Annual World s Best Treasury & Cash Management Providers. Global Finance will select the best overall global cash

Page 1 of 5 In March 2017, Global Finance will publish its selections for the Seventeenth Annual World s Best Treasury & Cash Management Providers. Global Finance will select the best overall global cash

Aging, the Future of Work and Sustainability of Pension System

Aging, the Future of Work and Sustainability of Pension System WKÖ & Salzburg Global Seminar Event Dénes Kucsera Agenda Austria Vienna, Austria November 5, 2015 Introduction Increasing pressure on the

Aging, the Future of Work and Sustainability of Pension System WKÖ & Salzburg Global Seminar Event Dénes Kucsera Agenda Austria Vienna, Austria November 5, 2015 Introduction Increasing pressure on the

Progress towards Strong, Sustainable and Balanced Growth. Figure 1: Recovery from Financial Crisis (100 = First Quarter of Real GDP Contraction)

") Progress towards Strong, Sustainable and Balanced Growth Figure 1: Recovery from Financial Crisis (100 = First Quarter of Real GDP Contraction) Source: OECD May 2014 Forecast, Haver Analytics, Rogoff and

Progress towards Strong, Sustainable and Balanced Growth Figure 1: Recovery from Financial Crisis (100 = First Quarter of Real GDP Contraction) Source: OECD May 2014 Forecast, Haver Analytics, Rogoff and

Internet Appendix: Government Debt and Corporate Leverage: International Evidence

Internet Appendix: Government Debt and Corporate Leverage: International Evidence Irem Demirci, Jennifer Huang, and Clemens Sialm September 3, 2018 1 Table A1: Variable Definitions This table details the

Internet Appendix: Government Debt and Corporate Leverage: International Evidence Irem Demirci, Jennifer Huang, and Clemens Sialm September 3, 2018 1 Table A1: Variable Definitions This table details the

Travel Insurance and Assistance

Travel Insurance and Assistance Worldwide research covering over 40 countries Series Prospectus Finaccord Web: www.finaccord.com. E-mail: info@finaccord.com 1 Prospectus contents Page What is the research?

Travel Insurance and Assistance Worldwide research covering over 40 countries Series Prospectus Finaccord Web: www.finaccord.com. E-mail: info@finaccord.com 1 Prospectus contents Page What is the research?

IOOF. International Equities Portfolio NZD. Quarterly update

IOOF NZD Quarterly update For the period ended 30 September 2018 Contents Overview 2 Portfolio at glance 3 Performance 4 Asset allocation 6 Overview At IOOF, we have been helping Australians secure their

IOOF NZD Quarterly update For the period ended 30 September 2018 Contents Overview 2 Portfolio at glance 3 Performance 4 Asset allocation 6 Overview At IOOF, we have been helping Australians secure their

At the end of this report, we summarize some important Year-End Considerations which employers should be prepared to address.

Global Report December 2009 Retirement Plan Accounting Assumptions at 2009 This report supplements our June 2009 Global Report, which presented the results of Hewitt Associates global survey of 2008 year-end

Global Report December 2009 Retirement Plan Accounting Assumptions at 2009 This report supplements our June 2009 Global Report, which presented the results of Hewitt Associates global survey of 2008 year-end

Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets

Derivatives Markets") Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for, and Amounts Outstanding as at June 30, March, 2005 Turnover data for, Table

Bank of Canada Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets Turnover for, and Amounts Outstanding as at June 30, March, 2005 Turnover data for, Table

Actuarial Supply & Demand. By i.e. muhanna. i.e. muhanna Page 1 of

By i.e. muhanna i.e. muhanna Page 1 of 8 040506 Additional Perspectives Measuring actuarial supply and demand in terms of GDP is indeed a valid basis for setting the actuarial density of a country and

By i.e. muhanna i.e. muhanna Page 1 of 8 040506 Additional Perspectives Measuring actuarial supply and demand in terms of GDP is indeed a valid basis for setting the actuarial density of a country and

Social Security Benefits Around the World,

Social Security Benefits Around the World, 197-2 Prepared by The Population Reference Bureau for the NIA P-3 Coordinating Center at the Michigan Center on the Demography of Aging, University of Michigan

Social Security Benefits Around the World, 197-2 Prepared by The Population Reference Bureau for the NIA P-3 Coordinating Center at the Michigan Center on the Demography of Aging, University of Michigan

All-Country Equity Allocator February 2018

Leila Heckman, Ph.D. lheckman@dcmadvisors.com 917-386-6261 John Mullin, Ph.D. jmullin@dcmadvisors.com 917-386-6262 Charles Waters cwaters@dcmadvisors.com 917-386-6264 All-Country Equity Allocator February

Leila Heckman, Ph.D. lheckman@dcmadvisors.com 917-386-6261 John Mullin, Ph.D. jmullin@dcmadvisors.com 917-386-6262 Charles Waters cwaters@dcmadvisors.com 917-386-6264 All-Country Equity Allocator February

Overview of Transfer Pricing Regulations. CA Akshay Kenkre

Overview of Transfer Pricing Regulations CA Akshay Kenkre 1 What is Transfer Pricing What is Transfer Price? A Price at which one person transfers physical goods, services, tangible or/ and intangibles

Overview of Transfer Pricing Regulations CA Akshay Kenkre 1 What is Transfer Pricing What is Transfer Price? A Price at which one person transfers physical goods, services, tangible or/ and intangibles

Global growth weakening as some risks materialise

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

Growth has peaked amidst escalating risks

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

Emerging Capital Markets AG907

Emerging Capital Markets AG907 M.Sc. Investment & Finance M.Sc. International Banking & Finance Lecture 2 Corporate Governance in Emerging Capital Markets Ignacio Requejo Glasgow, 2010/2011 Overview of

Emerging Capital Markets AG907 M.Sc. Investment & Finance M.Sc. International Banking & Finance Lecture 2 Corporate Governance in Emerging Capital Markets Ignacio Requejo Glasgow, 2010/2011 Overview of

Table 1: Foreign exchange turnover: Summary of surveys Billions of U.S. dollars. Number of business days

Table 1: Foreign exchange turnover: Summary of surveys Billions of U.S. dollars Total turnover Number of business days Average daily turnover change 1983 103.2 20 5.2 1986 191.2 20 9.6 84.6 1989 299.9

Table 1: Foreign exchange turnover: Summary of surveys Billions of U.S. dollars Total turnover Number of business days Average daily turnover change 1983 103.2 20 5.2 1986 191.2 20 9.6 84.6 1989 299.9

Distribution Capital and the Short and Long Run Import Demand Elasticity M.J. Crucini and J.S. Davis

Distribution Capital and the Short and Long Run Import Demand Elasticity M.J. Crucini and J.S. Davis Discussant: Andrea Rao Board of Governors of the Federal Reserve System CD (2012): Motivation The trade

Distribution Capital and the Short and Long Run Import Demand Elasticity M.J. Crucini and J.S. Davis Discussant: Andrea Rao Board of Governors of the Federal Reserve System CD (2012): Motivation The trade

FDI drops 18% in 2017 as corporate restructurings decline

FDI IN FIGURES April 2018 FDI drops 18% in 2017 as corporate restructurings decline Global FDI flows decreased by 18% to USD 1 411 billion in 2017 compared to 2016. In the fourth quarter of 2017, FDI flows

FDI IN FIGURES April 2018 FDI drops 18% in 2017 as corporate restructurings decline Global FDI flows decreased by 18% to USD 1 411 billion in 2017 compared to 2016. In the fourth quarter of 2017, FDI flows

Economics Program Working Paper Series

Economics Program Working Paper Series Projecting Economic Growth with Growth Accounting Techniques: The Conference Board Global Economic Outlook 2012 Sources and Methods Vivian Chen Ben Cheng Gad Levanon

Economics Program Working Paper Series Projecting Economic Growth with Growth Accounting Techniques: The Conference Board Global Economic Outlook 2012 Sources and Methods Vivian Chen Ben Cheng Gad Levanon

International Statistical Release

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org) Worldwide Investment Fund Assets and Flows Trends in the

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org) Worldwide Investment Fund Assets and Flows Trends in the

Market Briefing: MSCI Stock Market Indexes

Market Briefing: MSCI Stock Market Indexes February 1, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Joe Abbott 732-497-536 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www.

Market Briefing: MSCI Stock Market Indexes February 1, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Joe Abbott 732-497-536 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www.

Marine. Global Programmes. cunninghamlindsey.com. A Cunningham Lindsey service

Marine Global Programmes A Cunningham Lindsey service Marine global presence Marine Global Programmes Cunningham Lindsey approach Managing your needs With 160 marine surveyors and claims managers in 36

Marine Global Programmes A Cunningham Lindsey service Marine global presence Marine Global Programmes Cunningham Lindsey approach Managing your needs With 160 marine surveyors and claims managers in 36

DOMESTIC CUSTODY & TRADING SERVICES

Pricing Structure DOMESTIC CUSTODY & TRADING SERVICES A flat custody fee of 20bps per account type per year is applicable to all holdings and cash, the custody fee is collected each month but will be capped

Pricing Structure DOMESTIC CUSTODY & TRADING SERVICES A flat custody fee of 20bps per account type per year is applicable to all holdings and cash, the custody fee is collected each month but will be capped

Market Briefing: MSCI Stock Market Indexes

Market Briefing: MSCI Stock Market Indexes September 7, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Joe Abbott 732-497-536 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www.

Market Briefing: MSCI Stock Market Indexes September 7, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Joe Abbott 732-497-536 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www.

Travel Insurance and Assistance

Travel Insurance and Assistance Worldwide research covering over 40 countries Series Prospectus Finaccord Ltd., 2016 Web: www.finaccord.com. E-mail: info@finaccord.com 1 Prospectus contents Page What is

Travel Insurance and Assistance Worldwide research covering over 40 countries Series Prospectus Finaccord Ltd., 2016 Web: www.finaccord.com. E-mail: info@finaccord.com 1 Prospectus contents Page What is

MMGPI 2016 Outcomes. Dr David Knox Senior Partner, Mercer

Editions 2016 Top 3 Rankings MMGPI 2016 Outcomes Dr David Knox Senior Partner, Mercer Every retirement system is different! Insurance Private Public Pensions DC Indexation Assets RETIREMENT INCOME SYSTEMS

Editions 2016 Top 3 Rankings MMGPI 2016 Outcomes Dr David Knox Senior Partner, Mercer Every retirement system is different! Insurance Private Public Pensions DC Indexation Assets RETIREMENT INCOME SYSTEMS

The impact of global financial crisis on business cycles in Asian emerging economies by Jarko Fidrmuc and Iikka Korhonen

The impact of global financial crisis on business cycles in Asian emerging economies by Jarko Fidrmuc and Iikka Korhonen Discussion by Radhika Pandey National Institute of Public Finance and Policy, New

The impact of global financial crisis on business cycles in Asian emerging economies by Jarko Fidrmuc and Iikka Korhonen Discussion by Radhika Pandey National Institute of Public Finance and Policy, New

FedEx International Priority. FedEx International Economy 3

SERVICES AND RATES FedEx International Solutions for your business Whether you are shipping documents to meet a deadline, saving money on a regular shipment or moving freight, FedEx offers a suite of transportation

SERVICES AND RATES FedEx International Solutions for your business Whether you are shipping documents to meet a deadline, saving money on a regular shipment or moving freight, FedEx offers a suite of transportation

Burden of Taxation: International Comparisons

Burden of Taxation: International Comparisons Standard Note: SN/EP/3235 Last updated: 15 October 2008 Author: Bryn Morgan Economic Policy & Statistics Section This note presents data comparing the national

Burden of Taxation: International Comparisons Standard Note: SN/EP/3235 Last updated: 15 October 2008 Author: Bryn Morgan Economic Policy & Statistics Section This note presents data comparing the national

Division on Investment and Enterprise

Division on Investment and Enterprise Readers are encouraged to use the data in this publication for non-commercial purposes, provided acknowledgement is explicitly given to UNCTAD, together with the reference

Division on Investment and Enterprise Readers are encouraged to use the data in this publication for non-commercial purposes, provided acknowledgement is explicitly given to UNCTAD, together with the reference

Progress Towards Strong, Sustainable, and Balanced Growth. Figure 1: Recovery From Financial Crisis (100 = First Quarter of Real GDP contraction)

") Progress Towards Strong, Sustainable, and Balanced Growth Figure 1: Recovery From Financial Crisis ( = First Quarter of Real GDP contraction) 13 125 196-26 AE Recessions' Range*** 196-26 AE Recessions**

Progress Towards Strong, Sustainable, and Balanced Growth Figure 1: Recovery From Financial Crisis ( = First Quarter of Real GDP contraction) 13 125 196-26 AE Recessions' Range*** 196-26 AE Recessions**