Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley

|

|

|

- April Leonard

- 6 years ago

- Views:

Transcription

1 Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries: some with leverage constraints (banks) some with equity (skin-in-the-game) constraints (funds) in order to determine the cyclicality of each type and of the overall financial sector. Result: In the model and in the data: Banking sector: Pro-cyclical leverage Non-banking fin. sector: Acyclical leverage. Overall financial sector: Pro-cyclical leverage. Implication: Among intermediary asset pricing models, those focusing on leverage constraints are more relevant that those focusing on intermediary wealth for understanding aggregate dynamics.

2 Background: 1) Why are models with financial intermediaries needed? 2) What is the essence of intermediary asset pricing models? 3) What other empirical evidence is there for/against either type of model? Comments: 1) We re not inherently interested in intermediary leverage. Add results on asset prices, real economic evidence and policy. 2) What s achieved by combining the two types of models into one? How is this best done? 3) What is missing in the models with have so far?

3 Background 1: Why do we need intermediary asset pricing models? Risk premia increase much more following financial crises than recessions. Muir (2014) uses data from for 14 countries (180 non-financial recessions and 45 financial crisis)

4 This is hard to reconcile with consumption based models (consumption falls about the same in financial crisis and recessions and consumption volatility is similar)

5 Background 2: What is the essence of intermediary asset pricing models? From limited participation to intermediary asset pricing It s hard for households to figure out how to invest in risky assets. Literature on limited stock market participation: Recognizes that many households don t hold risky assets. Focuses on how this concentrates risk among stock holders. Shows empirically that consumption-based models do better when focusing on stockholders: Richest 1/3 of stockholders have beta of 3 on aggregate consumption You can explain the equity premium with 1/3 the risk aversion. You can also get time-varying risk premia since wealth shares of stockholders fluctuate over time.

6 How do intermediaries fit into this? The riskless asset is in zero net supply. In order for non-stockholders to do any saving in the riskless asset, stockholders issue riskless assets to non-stockholders. Financial intermediaries are not modelled explicitly. Implicitly, stockholders set up banks to issue riskless assets (deposits) to non-stockholders. Banks then holds risky assets on behalf of stockholders. So stockholders hold some risky asset directly and some indirectly via banks. Stockholder leverage via banks contributes further to increase the risk premium on risky assets (and on bank equity).

7 Literature on intermediary asset pricing, the net worth models (He and Krishnamurthy (2013)): Investing in risky assets is so hard that most is done via intermediaries and someone has to manage the intermediaries. Constraint: Intermediary managers wealth constrains size of intermediary s overall equity, for moral hazard reasons. - Stockholders Euler equation is now non-standard: Sometimes they cannot invest more in intermediary equity even though exp returns look attractive. - When the constraint binds for stockholders, the risk premium is higher than in a standard limited participation setting and it s time-varying. - Intermediary managers Euler equation is standard and always holds so you can use that to easily see the main points.

8 Risk premium based on manager s Euler equation: (in the log utility case). where α t I is the risky asset share of the intermediary (risky assets/equity), which equals its leverage (since it doesn t hold riskless asset as an asset). Constraint: Risky asset market clearing when constraint binds: Dynamics: Less manager wealth, w t, relative to the value of the risky asset P t Larger intermediary risky asset share (leverage) needed to clear the risky asset market Higher risk premium to induce bank manager to do this. Important: In a crisis, w t /P t falls because the manager is invested 100% in intermediary equity which is a leveraged position in the risky asset.

9

10

11 Which part of the financial sector is this a realistic model of? Banks. He and Krishnamurthy (2013) argue that if you want to think about the cyclicality of risk premia, you have to think about the intermediary in their model as a bank: ``Importantly for the present analysis, in accord with our model the intermediaries that are the buyers during the crisis (i.e. banks) do so by borrowing and increasing leverage. Our model does not capture the other aspect of this process, as reflected in the behavior of the hedge fund sector, that some parts of the financial sector reduce asset holdings and deleverage.

12 He and Krishnamurthy discuss Ang, Gorovyy, Van-Inwegen (2010) s evidence on market value leverage: - Banks increase market value leverage in crisis. That fits the HK model - Hedge funds reduce market value leverage in crisis. That doesn t fit the HK model.

13 Now, why do Adrian and Boyarchenko (and Shin and Moench) think this type of model is the wrong way to think about crisis and the financial sector? They agree that financial sector market leverage is counter-cyclical, but think we should focus on book leverage and the financial sector s book leverage is procyclical: In bad times volatility increases, therefore banks delever and shrink, and the reduced risk-bearing capacity of banks is what drives up risk premia.

14 A graph from Adrian, Moench and Shin (2013) to illustrate how book and market leverage of banks (and of the overall US financial sector) have completely different cyclicality:

15 Why do they think we should focus on book leverage? Essentially start from the idea that: Someone has to regulate the intermediary (bank). The key constraint on intermediaries is a regulatory constraint on leverage (Basel), which is based on book leverage. Regulatory constraint on book leverage (θt=book assets/book equity) (=market value leverage in the model but that s not the point): where

16 Earlier Adrian and Boyarchenko paper: Bank s constraint is assumed to always bind (bank manager risk aversion is assumed close to zero). Bank managers Euler equation is therefore not standard. The risk premia on bank stock and on risky capital becomes a function of the Lagrange multiplier on the bank s leverage constraint. This Lagrange multiplier is increasing in how fun it is to be a bank, i.e. a function of the expected excess return on the risky asset over bank debt and the sensitivities of capital returns and bank debt returns to the underlying two shocks (productivity, preferences). Risk premia are linear function of the sensitivities of the capital returns to the underlying shocks and of the state variables which are bank leverage and the share of wealth owned by bank managers (as opposed to households).

17 This is not a closed form solution, but graphically the equity excess return is negatively related to leverage growth and leverage growth is negatively related to (endogenously) increased risk (shock sensitivities). (Why no t-stats?) (Why lag sometimes?) (R2 is low in both model and data this doesn t explain much of actual fluctuations in leverage).

18 Background 3: What other empirical evidence is there for/ against either type of model? Adrian, Moench and Shin (2013) perform time-series and cross-sectional asset pricing tests and argue that book equity-based measures work best AR(1) innovations of growth rates of equity as pricing factor Lagged growth rates as predictors. Consider: - book vs. market equity, - leverage vs. equity - broker-dealers vs. banks. Find that broker-dealer book leverage works best. But in favor of net worth and market value models, Muir (2014) shows that intermediary market equity/gdp works well for predicting stock excess returns. And intermediary mkt. equity works in cross-sect asset pricing tests Intermediary=SIC code 6 (finance, insurance, real estate).

19 He and Krishnamurthy argue that it s incorrect to think about the banking sector as shrinking during the worst part of the crisis. (From Arvind s comments on Adrian and Shin, NBER MA). Why did banks not shrink? - Firms and securitization conduits drawdowns of pre-committed credit lines. - Banks purchased MBS from others.

20 Comment 1: We re not inherently interested in intermediary leverage. Add results on asset prices, real activity and policy. ``Modeling the equilibrium dynamics of He and Krishnamurthy [2012b, 2013] and Adrian and Boyarchenko [2012] within the same economy is relevant, as both banks and funds are important financial intermediaries, though their balance sheet behavior is very different. The empirical evidence presented here suggests that both bank sector dynamics and fund sector dynamics co-exist, and that bank sector dynamics are particularly important in understanding the evolution of pricing, volatility, and real activity. ``In general equilibrium, the dynamic properties of the two sectors interact in such a way that the bank sector exhibits endogenously procyclical leverage, while the fund sector is acyclical. The dynamic properties of the nonbank sector are markedly different from He and Krishnamurthy [2013], as household allocate optimally between the bank and nonbank sectors in our setting. These findings matter for normative questions, as the cyclicality of leverage matters for policy conclusions.

21 So it seems like the paper wants to be about: - Intermediary leverage - Asset pricing - Real activity - Optimal policy Currently it is mainly about intermediation leverage: o There s no matching of asset prices from the model and asset prices in the data - What is the level and dynamics of risk premia? - How volatile are prices on bank s long-term debt? o There s no assessment about real activity: - How much do leverage constrained banks affect output and consumption volatility relative to skin-in-the game constrained funds?

22 o There s no policy analysis He and Krishnamurthy considered which policies are most effective at quickly reducing risk premia, standing in a financial crisis: a) Low short rates (standard monetary policy) b) Asset purchases (unconventional monetary policy) c) Equity injections (a) and (c) are found to be more successful (theoretically). Is that different here? Is something new going on here? For example, should you inject equity only in banks, not in the fund sector?

23 Comment 2: What s achieved by combining the two types of models into one? How should this be done? From Tobias perspective, why not just ignore the He and Krishnamurthy model and related intermediary net worth models? Because not all parts of the financial sector face book leverage constraints. Perhaps the He and Krishnamurthy model could be relevant for those who don t? As noted above, HK model cannot mainly be about hedge funds. Consistent with that, the current paper doesn t include hedge funds in the fund sector: In the Flow of Funds hedge funds are part of the household sector. But then what is the fund sector? Is the HK model a plausible description of that? I think no.

24 What is everything in Flow of Funds Table L.107 that s not banks or broker-dealers? Fin. assets, 2013 ($B) Total financial business 82,199 L.108 Monetary authority 4,074 L.110 U.S.-chartered depository institutions, excluding credit unions 12,803 L.111 Foreign banking offices in U.S. 2,037 L.112 Banks in U.S.-affiliated areas 85 L.113 Credit unions 1,003 L.114 Property-casualty insurance companies 1,531 L.115 Life insurance companies 5,977 L.117.b Private pension funds, defined benefit 3,069 L.117.c Private pension funds, defined contribution 4,905 L.118 State and local government employee retirement funds 4,846 L.119 Federal government employee retirement funds 3,531 L.120 Money market mutual funds 2,678 L.121 Mutual Funds 11,545 L.122 Closed-end and exchange-traded funds 284 L.123 GSEs 6,361 L.124 Agency- and GSE-backed mortgage pools 1,569 L.125 Issuers of asset-backed securities 1,615 L.126 Finance companies 1,473 L.127 Real estate investment trusts 507 L.128 Security brokers and dealers 3,408 L.129 Holding companies 4,276 L.130 Funding corporations 2,023 Not included: Hedge funds (I used data from FSOC (2014)) 2,600

25 The Fed: Surely not what HK tried to model. The Fed s equity is not determined by a moral hazard constraint to make Yellen put in high effort Pension/retirement funds/mutual funds: They have no leverage. Cannot be the focus of a discussion about the cyclicality of the non-banking sector s leverage. Insurance companies: They have leverage. But is their constraint not closer to a regulatory constraint? (Ralph & Moto s work). GSEs? The rest? HK left that out of their table of the financial sector so clearly didn t intend their model to apply to that. So, if the HK-type sector ends up with acyclical leverage in the model, is that the reason non-banks have acyclical leverage in the data? I think no. My suggestion: Have one financial sector with two constraints: Skin-inthe-game and leverage.

26 If they want to keep the current setup, then the results need clarification. In particular, exactly why does the fund sector end up with acyclical leverage in the model in equilibrium? - Either the fund s net worth constraint is often not binding. - Or w/p doesn t fall in crisis so the risky asset can be held with no increase in fund leverage. - Or the capital demand of the banking sector picks up in crisis, but we know that s not the case since the banking sector is procyclical in the model. One cannot figure this out from the paper: - It s not shown how frequently the fund sector s constraint binds nor how frequently the bank sector s constraint binds. - It s not shown whether funds in equilibrium have a positive or negative weight on the riskless asset. Remember that this is the key determinant of whether w/p drops in crisis.

27 Also, I m not a big fan of how they model bank debt: In reality, here is how I would think of the need for leverage regulation: - Depositors (non-stockholders) want riskless deposits - The bank equity holders (managers and other stockholders) would like to commit ex ante to keeping deposits riskless, but cannot. - Role for deposit insurance. Then need for regulation to limit bank risk taking. That s not what s going on in paper: Banks issue floating rate long bonds. A sequence of short-term deposits is not the same as a floating-rate long-term bond: - Households cannot reduce their bond investments when they want. The coupon has to adjust instead of the quantity. - And banks don t earn a safety-premium on issuing ultra-safe debt. That interacts with the last issue I want to mention: Treasuries.

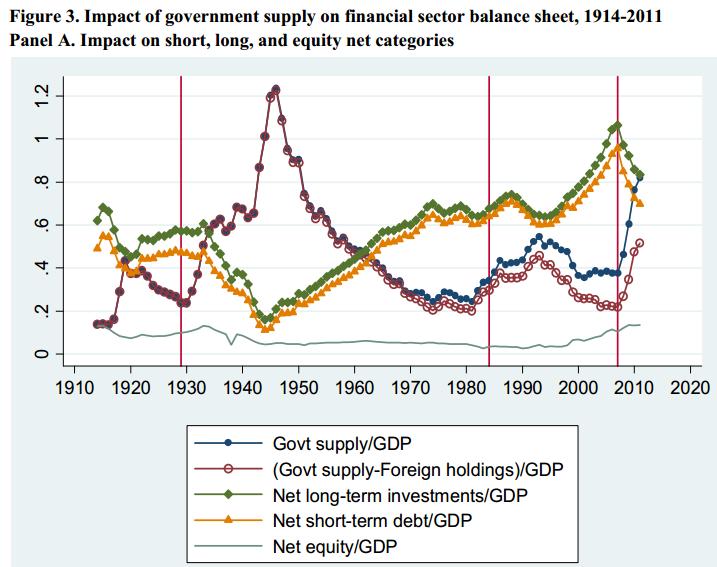

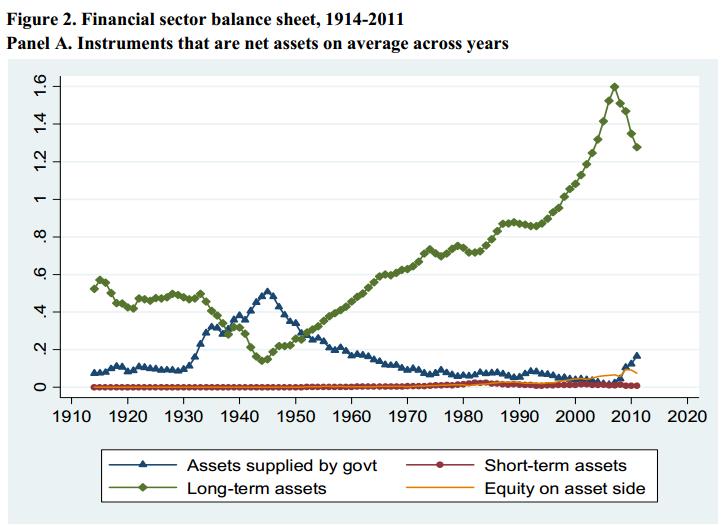

28 Comment 3: What s still missing in these intermediary asset pricing models? The government: Treasury supply, reserve supply Fluctuations in Treasury supply are large relative to the size of the financial sector Also substantial movement in Fed supply of reserves backed by MBS (or gold) In crisis (financial crisis/recession/war), government supply/gdp goes up a lot. So does the fin. sectors holdings of govt. supplied assets. - Regression: Fin. sector Govt. holdings/gdp on Treasuries/GDP, beta= Regression: Fin. sector lending/gdp on Treasuries/GDP, beta=-0.5. Interesting to think about this with a leverage constrained bank: - Govt. holdings have low risk-weights so become attractive exactly when the constraint is tight. And that s exactly when the govt. adds supply. - So adding Treasuries may make the overall financial sector size less procyclical, but its lending more procyclical.

29

30

Should Unconventional Monetary Policies Become Conventional?

Should Unconventional Monetary Policies Become Conventional? Dominic Quint and Pau Rabanal Discussant: Annette Vissing-Jorgensen, University of California Berkeley and NBER Question: Should LSAPs be used

Should Unconventional Monetary Policies Become Conventional? Dominic Quint and Pau Rabanal Discussant: Annette Vissing-Jorgensen, University of California Berkeley and NBER Question: Should LSAPs be used

Short-term debt and financial crises: What we can learn from U.S. Treasury supply

Short-term debt and financial crises: What we can learn from U.S. Treasury supply Arvind Krishnamurthy Northwestern-Kellogg and NBER Annette Vissing-Jorgensen Berkeley-Haas, NBER and CEPR 1. Motivation

Short-term debt and financial crises: What we can learn from U.S. Treasury supply Arvind Krishnamurthy Northwestern-Kellogg and NBER Annette Vissing-Jorgensen Berkeley-Haas, NBER and CEPR 1. Motivation

``Liquidity requirements, liquidity choice and financial stability by Diamond and Kashyap. Discussant: Annette Vissing-Jorgensen, UC Berkeley

``Liquidity requirements, liquidity choice and financial stability by Diamond and Kashyap Discussant: Annette Vissing-Jorgensen, UC Berkeley Idea: Study liquidity regulation in a model where it serves

``Liquidity requirements, liquidity choice and financial stability by Diamond and Kashyap Discussant: Annette Vissing-Jorgensen, UC Berkeley Idea: Study liquidity regulation in a model where it serves

Banking, Liquidity Transformation, and Bank Runs

Banking, Liquidity Transformation, and Bank Runs ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 30 Readings GLS Ch. 28 GLS Ch. 30 (don t worry about model

Banking, Liquidity Transformation, and Bank Runs ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 30 Readings GLS Ch. 28 GLS Ch. 30 (don t worry about model

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Monetary Policy and Reaching for Income by Daniel, Garlappi and Xiao. Discussant: Annette Vissing-Jorgensen, UC Berkeley.

Monetary Policy and Reaching for Income by Daniel, Garlappi and Xiao Discussant: Annette Vissing-Jorgensen, UC Berkeley April 28, 2018 Findings: Following lower Fed funds rate (over 3 years). 1) Mutual

Monetary Policy and Reaching for Income by Daniel, Garlappi and Xiao Discussant: Annette Vissing-Jorgensen, UC Berkeley April 28, 2018 Findings: Following lower Fed funds rate (over 3 years). 1) Mutual

A Model of Capital and Crises

A Model of Capital and Crises Zhiguo He Booth School of Business, University of Chicago Arvind Krishnamurthy Northwestern University and NBER AFA, 2011 ntroduction ntermediary capital can a ect asset prices.

A Model of Capital and Crises Zhiguo He Booth School of Business, University of Chicago Arvind Krishnamurthy Northwestern University and NBER AFA, 2011 ntroduction ntermediary capital can a ect asset prices.

The Federal Reserve in the 21st Century Financial Stability Policies

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

Discussion by J.C.Rochet (SFI,UZH and TSE) Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk

Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk") Discussion by J.C.Rochet (SFI,UZH and TSE) Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk 1 Objectives of the paper Develop a theoretical model of bank lending that allows to

Discussion by J.C.Rochet (SFI,UZH and TSE) Prepared for the Swissquote Conference 2012 on Liquidity and Systemic Risk 1 Objectives of the paper Develop a theoretical model of bank lending that allows to

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

Leverage Across Firms, Banks and Countries

Şebnem Kalemli-Özcan, Bent E. Sørensen and Sevcan Yeşiltaş University of Houston and NBER, University of Houston and CEPR, and Johns Hopkins University Dallas Fed Conference on Financial Frictions and

Şebnem Kalemli-Özcan, Bent E. Sørensen and Sevcan Yeşiltaş University of Houston and NBER, University of Houston and CEPR, and Johns Hopkins University Dallas Fed Conference on Financial Frictions and

The Federal Reserve in the 21st Century Financial Stability Policies

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

Banks Risk Exposures

Banks Risk Exposures Juliane Begenau Monika Piazzesi Martin Schneider Stanford Stanford & NBER Stanford & NBER Cambridge Oct 11, 213 Begenau, Piazzesi, Schneider () Cambridge Oct 11, 213 1 / 32 Modern

Banks Risk Exposures Juliane Begenau Monika Piazzesi Martin Schneider Stanford Stanford & NBER Stanford & NBER Cambridge Oct 11, 213 Begenau, Piazzesi, Schneider () Cambridge Oct 11, 213 1 / 32 Modern

Liquidity and Leverage

Tobias Adrian Federal Reserve Bank of New York Hyun Song Shin Princeton University European Central Bank, November 29, 2007 The views expressed in this presentation are those of the authors and do not

Tobias Adrian Federal Reserve Bank of New York Hyun Song Shin Princeton University European Central Bank, November 29, 2007 The views expressed in this presentation are those of the authors and do not

A Macroeconomic Model with Financially Constrained Producers and Intermediaries

A Macroeconomic Model with Financially Constrained Producers and Intermediaries Simon Gilchrist Boston Univerity and NBER Federal Reserve Bank of San Francisco March 31st, 2017 Overview: Model that combines

A Macroeconomic Model with Financially Constrained Producers and Intermediaries Simon Gilchrist Boston Univerity and NBER Federal Reserve Bank of San Francisco March 31st, 2017 Overview: Model that combines

Multi-Dimensional Monetary Policy

Multi-Dimensional Monetary Policy Michael Woodford Columbia University John Kuszczak Memorial Lecture Bank of Canada Annual Research Conference November 3, 2016 Michael Woodford (Columbia) Multi-Dimensional

Multi-Dimensional Monetary Policy Michael Woodford Columbia University John Kuszczak Memorial Lecture Bank of Canada Annual Research Conference November 3, 2016 Michael Woodford (Columbia) Multi-Dimensional

II. Determinants of Asset Demand. Figure 1

University of California, Merced EC 121-Money and Banking Chapter 5 Lecture otes Professor Jason Lee I. Introduction Figure 1 shows the interest rates for 3 month treasury bills. As evidenced by the figure,

University of California, Merced EC 121-Money and Banking Chapter 5 Lecture otes Professor Jason Lee I. Introduction Figure 1 shows the interest rates for 3 month treasury bills. As evidenced by the figure,

Endogenous risk in a DSGE model with capital-constrained financial intermediaries

Endogenous risk in a DSGE model with capital-constrained financial intermediaries Hans Dewachter (NBB-KUL) and Raf Wouters (NBB) NBB-Conference, Brussels, 11-12 October 2012 PP 1 motivation/objective introduce

Endogenous risk in a DSGE model with capital-constrained financial intermediaries Hans Dewachter (NBB-KUL) and Raf Wouters (NBB) NBB-Conference, Brussels, 11-12 October 2012 PP 1 motivation/objective introduce

How did Too Big to Fail become such a problem for broker-dealers? Speculation by Andy Atkeson March 2014

How did Too Big to Fail become such a problem for broker-dealers? Speculation by Andy Atkeson March 2014 Proximate Cause By 2008, Broker Dealers had big balance sheets Historical experience with rapid

How did Too Big to Fail become such a problem for broker-dealers? Speculation by Andy Atkeson March 2014 Proximate Cause By 2008, Broker Dealers had big balance sheets Historical experience with rapid

Outline. 1. Overall Impression. 2. Summary. Discussion of. Volker Wieland. Congratulations!

ECB Conference Global Financial Linkages, Transmission of Shocks and Asset Prices Frankfurt, December 1-2, 2008 Discussion of Real effects of the subprime mortgage crisis by Hui Tong and Shang-Jin Wei

ECB Conference Global Financial Linkages, Transmission of Shocks and Asset Prices Frankfurt, December 1-2, 2008 Discussion of Real effects of the subprime mortgage crisis by Hui Tong and Shang-Jin Wei

Financial Amplification, Regulation and Long-term Lending

Financial Amplification, Regulation and Long-term Lending Michael Reiter 1 Leopold Zessner 2 1 Instiute for Advances Studies, Vienna 2 Vienna Graduate School of Economics Barcelona GSE Summer Forum ADEMU,

Financial Amplification, Regulation and Long-term Lending Michael Reiter 1 Leopold Zessner 2 1 Instiute for Advances Studies, Vienna 2 Vienna Graduate School of Economics Barcelona GSE Summer Forum ADEMU,

Fiduciary Insights LEVERAGING PORTFOLIOS EFFICIENTLY

LEVERAGING PORTFOLIOS EFFICIENTLY WHETHER TO USE LEVERAGE AND HOW BEST TO USE IT TO IMPROVE THE EFFICIENCY AND RISK-ADJUSTED RETURNS OF PORTFOLIOS ARE AMONG THE MOST RELEVANT AND LEAST UNDERSTOOD QUESTIONS

LEVERAGING PORTFOLIOS EFFICIENTLY WHETHER TO USE LEVERAGE AND HOW BEST TO USE IT TO IMPROVE THE EFFICIENCY AND RISK-ADJUSTED RETURNS OF PORTFOLIOS ARE AMONG THE MOST RELEVANT AND LEAST UNDERSTOOD QUESTIONS

Bank Lending Shocks and the Euro Area Business Cycle

Bank Lending Shocks and the Euro Area Business Cycle Gert Peersman Ghent University Motivation SVAR framework to examine macro consequences of disturbances specific to bank lending market in euro area

Bank Lending Shocks and the Euro Area Business Cycle Gert Peersman Ghent University Motivation SVAR framework to examine macro consequences of disturbances specific to bank lending market in euro area

Financial Crises and Asset Prices. Tyler Muir June 2017, MFM

Financial Crises and Asset Prices Tyler Muir June 2017, MFM Outline Financial crises, intermediation: What can we learn about asset pricing? Muir 2017, QJE Adrian Etula Muir 2014, JF Haddad Muir 2017 What

Financial Crises and Asset Prices Tyler Muir June 2017, MFM Outline Financial crises, intermediation: What can we learn about asset pricing? Muir 2017, QJE Adrian Etula Muir 2014, JF Haddad Muir 2017 What

Global Pricing of Risk and Stabilization Policies

Global Pricing of Risk and Stabilization Policies Tobias Adrian Daniel Stackman Erik Vogt Federal Reserve Bank of New York The views expressed here are the authors and are not necessarily representative

Global Pricing of Risk and Stabilization Policies Tobias Adrian Daniel Stackman Erik Vogt Federal Reserve Bank of New York The views expressed here are the authors and are not necessarily representative

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

Global Imbalances and Financial Fragility

Global Imbalances and Financial Fragility By Ricardo J. Caballero and Arvind Krishnamurthy American Economic Review Papers and Proceedings May, 2009 The U.S. is currently engulfed in the most severe financial

Global Imbalances and Financial Fragility By Ricardo J. Caballero and Arvind Krishnamurthy American Economic Review Papers and Proceedings May, 2009 The U.S. is currently engulfed in the most severe financial

Overborrowing, Financial Crises and Macro-prudential Policy

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin Enrique G. Mendoza University of Maryland & NBER The case for macro-prudential policies Credit booms are

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin Enrique G. Mendoza University of Maryland & NBER The case for macro-prudential policies Credit booms are

Business cycle fluctuations Part II

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

The Financial Sector Functions of money Medium of exchange Measure of value Store of value Method of deferred payment

The Financial Sector Functions of money Medium of exchange - avoids the double coincidence of wants Measure of value - measures the relative values of different goods and services Store of value - kept

The Financial Sector Functions of money Medium of exchange - avoids the double coincidence of wants Measure of value - measures the relative values of different goods and services Store of value - kept

Review Material for Exam I

Class Materials from January-March 2014 Review Material for Exam I Econ 331 Spring 2014 Bernardo Topics Included in Exam I Money and the Financial System Money Supply and Monetary Policy Credit Market

Class Materials from January-March 2014 Review Material for Exam I Econ 331 Spring 2014 Bernardo Topics Included in Exam I Money and the Financial System Money Supply and Monetary Policy Credit Market

A Continuous-Time Asset Pricing Model with Habits and Durability

A Continuous-Time Asset Pricing Model with Habits and Durability John H. Cochrane June 14, 2012 Abstract I solve a continuous-time asset pricing economy with quadratic utility and complex temporal nonseparabilities.

A Continuous-Time Asset Pricing Model with Habits and Durability John H. Cochrane June 14, 2012 Abstract I solve a continuous-time asset pricing economy with quadratic utility and complex temporal nonseparabilities.

ECON Intermediate Macroeconomic Theory

ECON 3510 - Intermediate Macroeconomic Theory Fall 2015 Mankiw, Macroeconomics, 8th ed., Chapter 12 Chapter 12: Aggregate Demand 2: Applying the IS-LM Model Key points: Policy in the IS LM model: Monetary

ECON 3510 - Intermediate Macroeconomic Theory Fall 2015 Mankiw, Macroeconomics, 8th ed., Chapter 12 Chapter 12: Aggregate Demand 2: Applying the IS-LM Model Key points: Policy in the IS LM model: Monetary

Macroprudential Bank Capital Regulation in a Competitive Financial System

Macroprudential Bank Capital Regulation in a Competitive Financial System Milton Harris, Christian Opp, Marcus Opp Chicago, UPenn, University of California Fall 2015 H 2 O (Chicago, UPenn, UC) Macroprudential

Macroprudential Bank Capital Regulation in a Competitive Financial System Milton Harris, Christian Opp, Marcus Opp Chicago, UPenn, University of California Fall 2015 H 2 O (Chicago, UPenn, UC) Macroprudential

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko The views presented here are the authors and are not representative of the views of the Federal Reserve Bank of New

A Solution to Two Paradoxes of International Capital Flows. Jiandong Ju and Shang-Jin Wei. Discussion by Fabio Ghironi

A Solution to Two Paradoxes of International Capital Flows Jiandong Ju and Shang-Jin Wei Discussion by Fabio Ghironi NBER Summer Institute International Finance and Macroeconomics Program July 10-14, 2006

A Solution to Two Paradoxes of International Capital Flows Jiandong Ju and Shang-Jin Wei Discussion by Fabio Ghironi NBER Summer Institute International Finance and Macroeconomics Program July 10-14, 2006

Bailouts, Bail-ins and Banking Crises

Bailouts, Bail-ins and Banking Crises Todd Keister Rutgers University Yuliyan Mitkov Rutgers University & University of Bonn 2017 HKUST Workshop on Macroeconomics June 15, 2017 The bank runs problem Intermediaries

Bailouts, Bail-ins and Banking Crises Todd Keister Rutgers University Yuliyan Mitkov Rutgers University & University of Bonn 2017 HKUST Workshop on Macroeconomics June 15, 2017 The bank runs problem Intermediaries

Problem set 1 Answers: 0 ( )= [ 0 ( +1 )] = [ ( +1 )]

![Problem set 1 Answers: 0 ( )= [ 0 ( +1 )] = [ ( +1 )]](/thumbs/90/101609040.jpg "Problem set 1 Answers: 0 ( )= [ 0 ( +1 )] = [ ( +1 )]") Problem set 1 Answers: 1. (a) The first order conditions are with 1+ 1so 0 ( ) [ 0 ( +1 )] [( +1 )] ( +1 ) Consumption follows a random walk. This is approximately true in many nonlinear models. Now we

Problem set 1 Answers: 1. (a) The first order conditions are with 1+ 1so 0 ( ) [ 0 ( +1 )] [( +1 )] ( +1 ) Consumption follows a random walk. This is approximately true in many nonlinear models. Now we

The Federal Reserve System and Open Market Operations

Chapter 15 MODERN PRINCIPLES OF ECONOMICS Third Edition The Federal Reserve System and Open Market Operations Outline What Is the Federal Reserve System? The U.S. Money Supplies Fractional Reserve Banking,

Chapter 15 MODERN PRINCIPLES OF ECONOMICS Third Edition The Federal Reserve System and Open Market Operations Outline What Is the Federal Reserve System? The U.S. Money Supplies Fractional Reserve Banking,

9. Real business cycles in a two period economy

9. Real business cycles in a two period economy Index: 9. Real business cycles in a two period economy... 9. Introduction... 9. The Representative Agent Two Period Production Economy... 9.. The representative

9. Real business cycles in a two period economy Index: 9. Real business cycles in a two period economy... 9. Introduction... 9. The Representative Agent Two Period Production Economy... 9.. The representative

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Stanford University and NBER Bank of Canada, August 2017 He and Krishnamurthy (Chicago,

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Stanford University and NBER Bank of Canada, August 2017 He and Krishnamurthy (Chicago,

Notes II: Consumption-Saving Decisions, Ricardian Equivalence, and Fiscal Policy. Julio Garín Intermediate Macroeconomics Fall 2018

Notes II: Consumption-Saving Decisions, Ricardian Equivalence, and Fiscal Policy Julio Garín Intermediate Macroeconomics Fall 2018 Introduction Intermediate Macroeconomics Consumption/Saving, Ricardian

Notes II: Consumption-Saving Decisions, Ricardian Equivalence, and Fiscal Policy Julio Garín Intermediate Macroeconomics Fall 2018 Introduction Intermediate Macroeconomics Consumption/Saving, Ricardian

Chapter 20 (9) Financial Globalization: Opportunity and Crisis

Financial Globalization: Opportunity and Crisis") Chapter 20 (9) Financial Globalization: Opportunity and Crisis Preview Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital

Chapter 20 (9) Financial Globalization: Opportunity and Crisis Preview Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital

Global Imbalances and Financial Fragility

Global Imbalances and Financial Fragility Ricardo J. Caballero and Arvind Krishnamurthy December 16, 2008 Abstract The U.S. is currently engulfed in the most severe financial crisis since the Great Depression.

Global Imbalances and Financial Fragility Ricardo J. Caballero and Arvind Krishnamurthy December 16, 2008 Abstract The U.S. is currently engulfed in the most severe financial crisis since the Great Depression.

A Macroeconomic Framework for Quantifying Systemic Risk

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER December 2013 He and Krishnamurthy (Chicago, Northwestern)

A Macroeconomic Framework for Quantifying Systemic Risk Zhiguo He, University of Chicago and NBER Arvind Krishnamurthy, Northwestern University and NBER December 2013 He and Krishnamurthy (Chicago, Northwestern)

Banks Risk Exposures

Banks Risk Exposures Juliane Begenau Monika Piazzesi Martin Schneider Stanford Stanford & NBER Stanford & NBER SED 212 Piazzesi () SED 212 1 / 33 Matching models to data: Consumption: easy model: specify

Banks Risk Exposures Juliane Begenau Monika Piazzesi Martin Schneider Stanford Stanford & NBER Stanford & NBER SED 212 Piazzesi () SED 212 1 / 33 Matching models to data: Consumption: easy model: specify

Household Finance Session: Annette Vissing-Jorgensen, Northwestern University

Household Finance Session: Annette Vissing-Jorgensen, Northwestern University This session is about household default, with a focus on: (1) Credit supply to individuals who have defaulted: Brevoort and

Household Finance Session: Annette Vissing-Jorgensen, Northwestern University This session is about household default, with a focus on: (1) Credit supply to individuals who have defaulted: Brevoort and

Leverage Restrictions in a Business Cycle Model. Lawrence J. Christiano Daisuke Ikeda

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Background Increasing interest in the following sorts of questions: What restrictions should be placed on bank leverage?

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Background Increasing interest in the following sorts of questions: What restrictions should be placed on bank leverage?

MA Advanced Macroeconomics: 12. Default Risk, Collateral and Credit Rationing

MA Advanced Macroeconomics: 12. Default Risk, Collateral and Credit Rationing Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) Default Risk and Credit Rationing Spring 2016 1 / 39 Moving

MA Advanced Macroeconomics: 12. Default Risk, Collateral and Credit Rationing Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) Default Risk and Credit Rationing Spring 2016 1 / 39 Moving

Financial Fragility A Global-Games Approach Itay Goldstein Wharton School, University of Pennsylvania

Financial Fragility A Global-Games Approach Itay Goldstein Wharton School, University of Pennsylvania Financial Fragility and Coordination Failures What makes financial systems fragile? What causes crises

Financial Fragility A Global-Games Approach Itay Goldstein Wharton School, University of Pennsylvania Financial Fragility and Coordination Failures What makes financial systems fragile? What causes crises

Notes VI - Models of Economic Fluctuations

Notes VI - Models of Economic Fluctuations Julio Garín Intermediate Macroeconomics Fall 2017 Intermediate Macroeconomics Notes VI - Models of Economic Fluctuations Fall 2017 1 / 33 Business Cycles We can

Notes VI - Models of Economic Fluctuations Julio Garín Intermediate Macroeconomics Fall 2017 Intermediate Macroeconomics Notes VI - Models of Economic Fluctuations Fall 2017 1 / 33 Business Cycles We can

Comments on Credit Frictions and Optimal Monetary Policy, by Cúrdia and Woodford

Comments on Credit Frictions and Optimal Monetary Policy, by Cúrdia and Woodford Olivier Blanchard August 2008 Cúrdia and Woodford (CW) have written a topical and important paper. There is no doubt in

Comments on Credit Frictions and Optimal Monetary Policy, by Cúrdia and Woodford Olivier Blanchard August 2008 Cúrdia and Woodford (CW) have written a topical and important paper. There is no doubt in

Financial Crises and Lending of Last Resort in Open Economies

Financial Crises and Lending of Last Resort in Open Economies by Luigi Bocola and Guido Lorenzoni Discussion by: Fabrizio Perri Minneapolis Fed Macro Finance Society Workshop Federal Reserve Bank of Chicago,

Financial Crises and Lending of Last Resort in Open Economies by Luigi Bocola and Guido Lorenzoni Discussion by: Fabrizio Perri Minneapolis Fed Macro Finance Society Workshop Federal Reserve Bank of Chicago,

Federal Reserve Bank of New York Staff Reports. Dodd-Frank One Year On: Implications for Shadow Banking

Federal Reserve Bank of New York Staff Reports Dodd-Frank One Year On: Implications for Shadow Banking Tobias Adrian Staff Report no. 533 December 2011 This paper presents preliminary findings and is being

Federal Reserve Bank of New York Staff Reports Dodd-Frank One Year On: Implications for Shadow Banking Tobias Adrian Staff Report no. 533 December 2011 This paper presents preliminary findings and is being

Capital Adequacy and Liquidity in Banking Dynamics

Capital Adequacy and Liquidity in Banking Dynamics Jin Cao Lorán Chollete October 9, 2014 Abstract We present a framework for modelling optimum capital adequacy in a dynamic banking context. We combine

Capital Adequacy and Liquidity in Banking Dynamics Jin Cao Lorán Chollete October 9, 2014 Abstract We present a framework for modelling optimum capital adequacy in a dynamic banking context. We combine

Supplementary Appendix to Financial Intermediaries and the Cross Section of Asset Returns

Supplementary Appendix to Financial Intermediaries and the Cross Section of Asset Returns Tobias Adrian tobias.adrian@ny.frb.org Erkko Etula etula@post.harvard.edu Tyler Muir t-muir@kellogg.northwestern.edu

Supplementary Appendix to Financial Intermediaries and the Cross Section of Asset Returns Tobias Adrian tobias.adrian@ny.frb.org Erkko Etula etula@post.harvard.edu Tyler Muir t-muir@kellogg.northwestern.edu

The Effects of Quantitative Easing on Interest Rates: Channels and Implications for Policy

The Effects of Quantitative Easing on Interest Rates: Channels and Implications for Policy Arvind Krishnamurthy Northwestern University and NBER Annette Vissing-Jorgensen Northwestern University, CEPR

The Effects of Quantitative Easing on Interest Rates: Channels and Implications for Policy Arvind Krishnamurthy Northwestern University and NBER Annette Vissing-Jorgensen Northwestern University, CEPR

The U.S. Treasury Premium, by Wenxin Du, Joanne Im and Jesse Schreger Discussant: Annette Vissing-Jorgensen, UC Berkeley and NBER

The U.S. Treasury Premium, by Wenxin Du, Joanne Im and Jesse Schreger Discussant: Annette Vissing-Jorgensen, UC Berkeley and NBER Question: Over the 2000-2016 period, how special are U.S. Treasuries relative

The U.S. Treasury Premium, by Wenxin Du, Joanne Im and Jesse Schreger Discussant: Annette Vissing-Jorgensen, UC Berkeley and NBER Question: Over the 2000-2016 period, how special are U.S. Treasuries relative

MGT411 Money & Banking Latest Solved Quizzes By

MGT411 Money & Banking Latest Solved Quizzes By http://vustudents.ning.com Which of the following is true of a nation's central bank? It makes important decisions about the nation's tax and public spending

MGT411 Money & Banking Latest Solved Quizzes By http://vustudents.ning.com Which of the following is true of a nation's central bank? It makes important decisions about the nation's tax and public spending

Development Economics Part II Lecture 7

Development Economics Part II Lecture 7 Risk and Insurance Theory: How do households cope with large income shocks? What are testable implications of different models? Empirics: Can households insure themselves

Development Economics Part II Lecture 7 Risk and Insurance Theory: How do households cope with large income shocks? What are testable implications of different models? Empirics: Can households insure themselves

Financial Frictions in Macroeconomics. Lawrence J. Christiano Northwestern University

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Securities, etc. Bank Debt Bank Equity Frictions between

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Securities, etc. Bank Debt Bank Equity Frictions between

Consumption. ECON 30020: Intermediate Macroeconomics. Prof. Eric Sims. Fall University of Notre Dame

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Fall 2016 1 / 36 Microeconomics of Macro We now move from the long run (decades and longer) to the medium run

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Fall 2016 1 / 36 Microeconomics of Macro We now move from the long run (decades and longer) to the medium run

COPYRIGHTED MATERIAL.

Contents Preface CHAPTER 1 Introduction 1 What You Will Learn in This Chapter 1 Overview 1 Where We Are Going in This Book 2 Contributions Made by the Financial System 4 Transfers of Resources from Surplus

Contents Preface CHAPTER 1 Introduction 1 What You Will Learn in This Chapter 1 Overview 1 Where We Are Going in This Book 2 Contributions Made by the Financial System 4 Transfers of Resources from Surplus

In understanding the behavior of aggregate demand we must take a close look at its individual components: Figure 1, Aggregate Demand

The Digital Economist Lecture 4 -- The Real Economy and Aggregate Demand The concept of aggregate demand is used to understand and measure the ability, and willingness, of individuals and institutions

The Digital Economist Lecture 4 -- The Real Economy and Aggregate Demand The concept of aggregate demand is used to understand and measure the ability, and willingness, of individuals and institutions

1. Allocates scarce capital among competing uses 2. Spreads/shares risk 3. Facilitates inter-temporal trade

Chapter 2: The Financial System What it is: What it does: A network of financial intermediaries (banks, S&Ls, credit unions, etc.), facilitators (credit rating agencies, appraisers, etc.), and markets

Chapter 2: The Financial System What it is: What it does: A network of financial intermediaries (banks, S&Ls, credit unions, etc.), facilitators (credit rating agencies, appraisers, etc.), and markets

Discussion of Liquidity, Moral Hazard, and Interbank Market Collapse

Discussion of Liquidity, Moral Hazard, and Interbank Market Collapse Tano Santos Columbia University Financial intermediaries, such as banks, perform many roles: they screen risks, evaluate and fund worthy

Discussion of Liquidity, Moral Hazard, and Interbank Market Collapse Tano Santos Columbia University Financial intermediaries, such as banks, perform many roles: they screen risks, evaluate and fund worthy

Comments on Three Papers on Banking and the Macroeconomy

Comments on Three Papers on Banking and the Macroeconomy John V. Duca Associate Director of Research and Vice President Federal Reserve Bank of Dallas * Adjunct Professor Southern Methodist University

Comments on Three Papers on Banking and the Macroeconomy John V. Duca Associate Director of Research and Vice President Federal Reserve Bank of Dallas * Adjunct Professor Southern Methodist University

THE ECONOMICS OF BANK CAPITAL

THE ECONOMICS OF BANK CAPITAL Edoardo Gaffeo Department of Economics and Management University of Trento OUTLINE What we are talking about, and why Banks are «special», and their capital is «special» as

THE ECONOMICS OF BANK CAPITAL Edoardo Gaffeo Department of Economics and Management University of Trento OUTLINE What we are talking about, and why Banks are «special», and their capital is «special» as

The Safe-Asset Share*

The Safe-Asset Share* Gary Gorton Yale and NBER Stefan Lewellen Yale Andrew Metrick Yale and NBER January 17, 2012 Prepared for AER Papers & Proceedings, 2012. Abstract: We document that the percentage

The Safe-Asset Share* Gary Gorton Yale and NBER Stefan Lewellen Yale Andrew Metrick Yale and NBER January 17, 2012 Prepared for AER Papers & Proceedings, 2012. Abstract: We document that the percentage

Lecture 12: Too Big to Fail and the US Financial Crisis

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

Lecture 12: Too Big to Fail and the US Financial Crisis October 25, 2016 Prof. Wyatt Brooks Beginning of the Crisis Why did banks want to issue more loans in the mid-2000s? How did they increase the issuance

The Federal Reserve and Open Market Operations PRINCIPLES OF ECONOMICS (ECON 210) BEN VAN KAMMEN, PHD

BEN VAN KAMMEN, PHD") The Federal Reserve and Open Market Operations PRINCIPLES OF ECONOMICS (ECON 210) BEN VAN KAMMEN, PHD What is the Federal Reserve System? The Federal Reserve: Creates money (widely accepted means of payment:

The Federal Reserve and Open Market Operations PRINCIPLES OF ECONOMICS (ECON 210) BEN VAN KAMMEN, PHD What is the Federal Reserve System? The Federal Reserve: Creates money (widely accepted means of payment:

Macroeconomic Models with Financial Frictions

Macroeconomic Models with Financial Frictions Jesús Fernández-Villaverde University of Pennsylvania December 2, 2012 Jesús Fernández-Villaverde (PENN) Macro-Finance December 2, 2012 1 / 26 Motivation I

Macroeconomic Models with Financial Frictions Jesús Fernández-Villaverde University of Pennsylvania December 2, 2012 Jesús Fernández-Villaverde (PENN) Macro-Finance December 2, 2012 1 / 26 Motivation I

Discussion of Exits from Recessions by Bordo and Landon-Lane

Discussion of Exits from Recessions by Bordo and Landon-Lane Robert J. Gordon Northwestern University, NBER, and CEPR SNB Conference on Monetary Policy after the Financial Crisis, Zurich, 24 September

Discussion of Exits from Recessions by Bordo and Landon-Lane Robert J. Gordon Northwestern University, NBER, and CEPR SNB Conference on Monetary Policy after the Financial Crisis, Zurich, 24 September

Global Financial Cycle

Global Financial Cycle Hélène Rey London Business School & NBER & CEPR IMF 2017 Prepared for Jacques Polak ARC 18th 1 / 31 Global Financial Cycle Fluctuations in financial activity (risk taking, credit

Global Financial Cycle Hélène Rey London Business School & NBER & CEPR IMF 2017 Prepared for Jacques Polak ARC 18th 1 / 31 Global Financial Cycle Fluctuations in financial activity (risk taking, credit

Remapping the Flow of Funds

Remapping the Flow of Funds Juliane Begenau Stanford Monika Piazzesi Stanford & NBER April 2012 Martin Schneider Stanford & NBER The Flow of Funds Accounts are a crucial data source on credit market positions

Remapping the Flow of Funds Juliane Begenau Stanford Monika Piazzesi Stanford & NBER April 2012 Martin Schneider Stanford & NBER The Flow of Funds Accounts are a crucial data source on credit market positions

What is Cyclical in Credit Cycles?

What is Cyclical in Credit Cycles? Rui Cui May 31, 2014 Introduction Credit cycles are growth cycles Cyclicality in the amount of new credit Explanations: collateral constraints, equity constraints, leverage

What is Cyclical in Credit Cycles? Rui Cui May 31, 2014 Introduction Credit cycles are growth cycles Cyclicality in the amount of new credit Explanations: collateral constraints, equity constraints, leverage

Stabilization Policies: Equity Injections into Banks or Purchases of Assets?

Stabilization Policies: Equity Injections into Banks or Purchases of Assets? Michael Kühl 27-28 October 216 Annual Global Conference of the European Banking Institute The presentation represents the personal

Stabilization Policies: Equity Injections into Banks or Purchases of Assets? Michael Kühl 27-28 October 216 Annual Global Conference of the European Banking Institute The presentation represents the personal

Banking Regulation: The Risk of Migration to Shadow Banking

Banking Regulation: The Risk of Migration to Shadow Banking Sam Hanson Harvard University and NBER September 26, 2016 Micro- vs. Macro-prudential regulation Micro-prudential: Regulated banks should have

Banking Regulation: The Risk of Migration to Shadow Banking Sam Hanson Harvard University and NBER September 26, 2016 Micro- vs. Macro-prudential regulation Micro-prudential: Regulated banks should have

Topic 3: International Risk Sharing and Portfolio Diversification

Topic 3: International Risk Sharing and Portfolio Diversification Part 1) Working through a complete markets case - In the previous lecture, I claimed that assuming complete asset markets produced a perfect-pooling

Topic 3: International Risk Sharing and Portfolio Diversification Part 1) Working through a complete markets case - In the previous lecture, I claimed that assuming complete asset markets produced a perfect-pooling

ECON 3303 Money and Banking Final Exam. MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

ECON 3303 Money and Banking Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If Treasury deposits at the Fed are predicted to fall,

ECON 3303 Money and Banking Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If Treasury deposits at the Fed are predicted to fall,

I. The Money Market. A. Money Demand (M d ) Handout 9

Handout 9") University of California-Davis Economics 1B-Intro to Macro Handout 9 TA: Jason Lee Email: jawlee@ucdavis.edu In the last chapter we developed the aggregate demand/aggregate supply model and used it to

University of California-Davis Economics 1B-Intro to Macro Handout 9 TA: Jason Lee Email: jawlee@ucdavis.edu In the last chapter we developed the aggregate demand/aggregate supply model and used it to

Unit: Monetary Policy

Unit: Monetary Policy 2 3 Showing the Effects of Monetary Policy Graphically Three Related Graphs: Ø Money Market Ø Investment Demand Ø AD/AS Interest Rate (i) S&D of Money S M S M1 Interest Rate (i) Investment

Unit: Monetary Policy 2 3 Showing the Effects of Monetary Policy Graphically Three Related Graphs: Ø Money Market Ø Investment Demand Ø AD/AS Interest Rate (i) S&D of Money S M S M1 Interest Rate (i) Investment

Liquidity and the Threat of Fraudulent Assets

Liquidity and the Threat of Fraudulent Assets Yiting Li, Guillaume Rocheteau, Pierre-Olivier Weill May 2015 Liquidity and the Threat of Fraudulent Assets Yiting Li, Guillaume Rocheteau, Pierre-Olivier

Liquidity and the Threat of Fraudulent Assets Yiting Li, Guillaume Rocheteau, Pierre-Olivier Weill May 2015 Liquidity and the Threat of Fraudulent Assets Yiting Li, Guillaume Rocheteau, Pierre-Olivier

LEVERAGE AND LIQUIDITY DRY-UPS: A FRAMEWORK AND POLICY IMPLICATIONS. Denis Gromb LBS, LSE and CEPR. Dimitri Vayanos LSE, CEPR and NBER

LEVERAGE AND LIQUIDITY DRY-UPS: A FRAMEWORK AND POLICY IMPLICATIONS Denis Gromb LBS, LSE and CEPR Dimitri Vayanos LSE, CEPR and NBER June 2008 Gromb-Vayanos 1 INTRODUCTION Some lessons from recent crisis:

LEVERAGE AND LIQUIDITY DRY-UPS: A FRAMEWORK AND POLICY IMPLICATIONS Denis Gromb LBS, LSE and CEPR Dimitri Vayanos LSE, CEPR and NBER June 2008 Gromb-Vayanos 1 INTRODUCTION Some lessons from recent crisis:

Optimal monetary and macro-pru policies

Discussion of Kiley and Sim s Optimal monetary and macro-pru policies Oreste Tristani European Central Bank Federal Reserve Bank of San Francisco Conference on Monetary Policy and Financial Markets, 28

Discussion of Kiley and Sim s Optimal monetary and macro-pru policies Oreste Tristani European Central Bank Federal Reserve Bank of San Francisco Conference on Monetary Policy and Financial Markets, 28

Intermediary Asset Pricing

Intermediary Asset Pricing Z. He and A. Krishnamurthy - AER (2012) Presented by Omar Rachedi 18 September 2013 Introduction Motivation How to account for risk premia? Standard models assume households

Intermediary Asset Pricing Z. He and A. Krishnamurthy - AER (2012) Presented by Omar Rachedi 18 September 2013 Introduction Motivation How to account for risk premia? Standard models assume households

Credit Shocks and the U.S. Business Cycle. Is This Time Different? Raju Huidrom University of Virginia. Midwest Macro Conference

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

5 The risk-taking channel

5 The risk-taking channel Adrian, Tobias and Hyun Song Shin (2010), The changing nature of financial intermediation and the financial crisis of 2007-09, Annual Review of Economics, (also available as Fed

5 The risk-taking channel Adrian, Tobias and Hyun Song Shin (2010), The changing nature of financial intermediation and the financial crisis of 2007-09, Annual Review of Economics, (also available as Fed

The lender of last resort: liquidity provision versus the possibility of bail-out

The lender of last resort: liquidity provision versus the possibility of bail-out Rob Nijskens Sylvester C.W. Eijffinger June 24, 2010 The lender of last resort: liquidity versus bail-out 1 /20 Motivation:

The lender of last resort: liquidity provision versus the possibility of bail-out Rob Nijskens Sylvester C.W. Eijffinger June 24, 2010 The lender of last resort: liquidity versus bail-out 1 /20 Motivation:

Maturity Transformation and Liquidity

Maturity Transformation and Liquidity Patrick Bolton, Tano Santos Columbia University and Jose Scheinkman Princeton University Motivation Main Question: Who is best placed to, 1. Transform Maturity 2.

Maturity Transformation and Liquidity Patrick Bolton, Tano Santos Columbia University and Jose Scheinkman Princeton University Motivation Main Question: Who is best placed to, 1. Transform Maturity 2.

Leverage Restrictions in a Business Cycle Model. March 13-14, 2015, Macro Financial Modeling, NYU Stern.

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Northwestern University Bank of Japan March 13-14, 2015, Macro Financial Modeling, NYU Stern. Background Wish to address

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda Northwestern University Bank of Japan March 13-14, 2015, Macro Financial Modeling, NYU Stern. Background Wish to address

Operationalizing the Selection and Application of Macroprudential Instruments

Operationalizing the Selection and Application of Macroprudential Instruments Presented by Tobias Adrian, Federal Reserve Bank of New York Based on Committee for Global Financial Stability Report 48 The

Operationalizing the Selection and Application of Macroprudential Instruments Presented by Tobias Adrian, Federal Reserve Bank of New York Based on Committee for Global Financial Stability Report 48 The

Chapter Eleven. Chapter 11 The Economics of Financial Intermediation Why do Financial Intermediaries Exist

Chapter Eleven Chapter 11 The Economics of Financial Intermediation Why do Financial Intermediaries Exist Countries With Developed Financial Systems Prosper Basic Facts of Financial Structure 1. Direct

Chapter Eleven Chapter 11 The Economics of Financial Intermediation Why do Financial Intermediaries Exist Countries With Developed Financial Systems Prosper Basic Facts of Financial Structure 1. Direct

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 52

The Financial System 1 / 52") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

FRBSF ECONOMIC LETTER

FRBSF ECONOMIC LETTER 211-15 May 16, 211 What Is the Value of Bank Output? BY TITAN ALON, JOHN FERNALD, ROBERT INKLAAR, AND J. CHRISTINA WANG Financial institutions often do not charge explicit fees for

FRBSF ECONOMIC LETTER 211-15 May 16, 211 What Is the Value of Bank Output? BY TITAN ALON, JOHN FERNALD, ROBERT INKLAAR, AND J. CHRISTINA WANG Financial institutions often do not charge explicit fees for

LECTURE 8 Monetary Policy at the Zero Lower Bound: Quantitative Easing. October 10, 2018

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 8 Monetary Policy at the Zero Lower Bound: Quantitative Easing October 10, 2018 Announcements Paper proposals due on Friday (October 12).

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 8 Monetary Policy at the Zero Lower Bound: Quantitative Easing October 10, 2018 Announcements Paper proposals due on Friday (October 12).

The Demand and Supply of Safe Assets (Premilinary)

") The Demand and Supply of Safe Assets (Premilinary) Yunfan Gu August 28, 2017 Abstract It is documented that over the past 60 years, the safe assets as a percentage share of total assets in the U.S. has

The Demand and Supply of Safe Assets (Premilinary) Yunfan Gu August 28, 2017 Abstract It is documented that over the past 60 years, the safe assets as a percentage share of total assets in the U.S. has

Leverage Restrictions in a Business Cycle Model

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda SAIF, December 2014. Background Increasing interest in the following sorts of questions: What restrictions should be

Leverage Restrictions in a Business Cycle Model Lawrence J. Christiano Daisuke Ikeda SAIF, December 2014. Background Increasing interest in the following sorts of questions: What restrictions should be

Financial Crises, Dollarization and Lending of Last Resort in Open Economies

Financial Crises, Dollarization and Lending of Last Resort in Open Economies Luigi Bocola Stanford, Minneapolis Fed, and NBER Guido Lorenzoni Northwestern and NBER Restud Tour Reunion Conference May 2018

Financial Crises, Dollarization and Lending of Last Resort in Open Economies Luigi Bocola Stanford, Minneapolis Fed, and NBER Guido Lorenzoni Northwestern and NBER Restud Tour Reunion Conference May 2018

Chapter Fourteen. Chapter 10 Regulating the Financial System 5/6/2018. Financial Crisis

Chapter Fourteen Chapter 10 Regulating the Financial System Financial Crisis Disruptions to financial systems are frequent and widespread around the world. Why? Financial systems are fragile and vulnerable

Chapter Fourteen Chapter 10 Regulating the Financial System Financial Crisis Disruptions to financial systems are frequent and widespread around the world. Why? Financial systems are fragile and vulnerable