Bailouts, Bail-ins and Banking Crises

|

|

|

- Marilynn Mosley

- 5 years ago

- Views:

Transcription

1 Bailouts, Bail-ins and Banking Crises Todd Keister Rutgers University Yuliyan Mitkov Rutgers University & University of Bonn 2017 HKUST Workshop on Macroeconomics June 15, 2017

2 The bank runs problem Intermediaries offer deposits that can be withdrawn: on demand (or at short notice) at face value (or not very state contingent) In a run, investors know (or fear) a response is coming i.e., failure or resolution in which remaining investors lose money want to withdraw before this response Key element of the story: the response is delayed there is a period when the run is underway but the bank continues to operate as normal 1

3 Why the delay? Puzzle: the run is making investors as a group worse off why doesn t the response come more quickly? Traditional answer: incomplete contracts between banks and investors difficult to write and enforce state-contingent contracts or incompleteness needed to address other incentive problems legal issues (how to change contracts, impose losses) creates delay If so: focus of policy should be on improving these contracts creating legal structures under which better contracts are feasible much effort in this direction (bail-ins, Co-cos, orderly resolution) prime example: Money Market Mutual Fund reforms in the U.S. 2

4 Our paper Suppose efforts to improve contracts between banks and investors are perfectly successful Would that solve the bank-runs problem? existing literature suggests the answer should be yes we argue: answer is likely no Study an environment with no contracting frictions with a bank bailing-in investors in a crisis is feasible (and desirable) govt. can provide bailouts and lacks commitment Show: Bailouts delay bail-ins result: a bank run (and delayed response) can still arise we then study macroprudential policy in this setting 3

5 The model environment 4

6 Investors t = 0,1,2 Investors: i 0,1 in each of many locations k endowed with 1 at t = 0, nothing later Utility: u c 1 + ω i c 2 + v g where ω i = 0 1 means investor is impatient patient Type ω i is revealed at t = 1, private information Diamond-Dybvig plus public good π = prob. of being impatient for each investor = fraction of impatient investors at t = 1 5

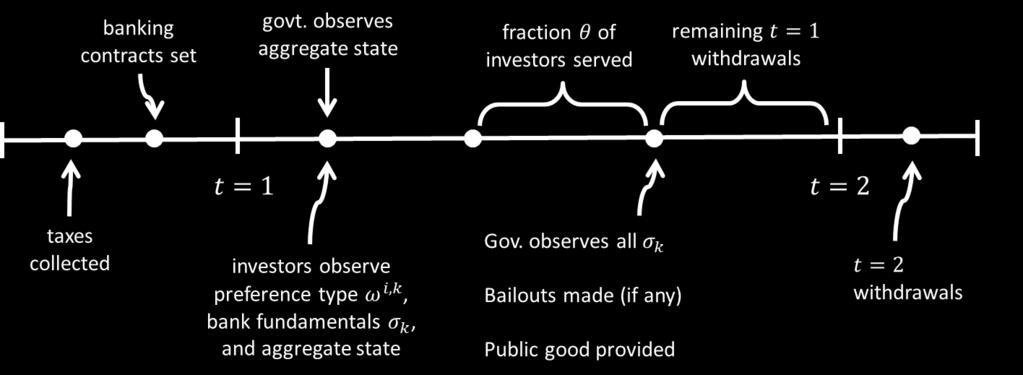

7 Banks Representative bank in each location accepts deposits at t = 0; allows withdrawals at t = 1 or t = 2 sets (fully-state-contingent) contract t = 0 Investment yields return 1 R > 1 at t = 1 t = 2 if sound, but Some assets turn out to be worthless at t = 1 fraction n of banks lose fraction σ of their assets two aggregate states: n = 0 (good) and n > 0 (bad) investors observe both aggregate and bank-specific state 6

8 Government Fiscal policy: t = 0 : taxes endowments t = 1 : provides public good and (possibly) bailouts to weak banks bailouts are chosen as best response to the situation at hand (no commitment) Information: observes aggregate state at the beginning of t = 1, but observes bank-specific states σ k with a lag, after θ withdrawals captures the time needed to do detailed examinations bailouts are made after some withdrawals have taken place 7

9 Timeline 8

10 The constrained efficient allocation 9

11 A planner s problem Suppose a planner could operate all banks plus the govt. and can observe investors types and dictate withdrawal decisions but is subject to same restrictions on fiscal policy Note: planner will have patient investors withdraw at t = 2 Sound banks: choose consumption for each impatient investor (c 1S ) and for each patient investor (c 2S ) to solve max ππ c 1S + 1 π u c 2S s. t. πc 1S + 1 π c 2S R 1 τ 10

12 A planner s problem Suppose a planner could operate all banks plus the govt. and can observe investors types and dictate withdrawal decisions but is subject to same restrictions on fiscal policy Note: planner will have patient investors withdraw at t = 2 Sound banks: choose consumption for each impatient investor (c 1S ) and for each patient investor (c 2S ) to solve s. t. max ππ c 1S + 1 π u c 2S πc 1S + 1 π c 2S R 1 τ solution: c 1S, c 2S with c 1S < c 2S 10

13 Weak banks: max π u c 1W + 1 π u c 2W s. t. πc 1W + 1 π c 2W R 1 τ 1 σ + b losses bailout Bailouts efficiently distribute resources between g and c: v τ nn = u c 1W = Ru c 1W 11

14 Weak banks: max π u c 1W + 1 π u c 2W solution: c 1W, c 2W with c 1W < c 2W s. t. πc 1W + 1 π c 2W R 1 τ 1 σ + b losses bailout Bailouts efficiently distribute resources between g and c: v τ nn = u c 1W = Ru c 1W 11

15 Weak banks: max π u c 1W + 1 π u c 2W solution: c 1W, c 2W with c 1W < c 2W s. t. πc 1W + 1 π c 2W R 1 τ 1 σ + b losses bailout Bailouts efficiently distribute resources between g and c: v τ nn = u c 1W = Ru c 1W Properties of the constrained efficient allocation: bailouts: b > 0 for all weak banks combined with bail-ins: c 1W, c 2W c 1S, c 2S no incentive to run: c 1j < c 2j for j = S, W 11

16 Equilibrium allocations 12

17 Banking contracts At t = 0, banking contract specifies early payment c 1 k as a function of realized fundamental σ k and withdrawal demand Simplified model: restrict c k 1 c 1S, c 1W interpretation: can operate as normal c 1S or bail-in investors c 1W < c 1S Govt initially does not observe banks realized states σ k activating the bail-in clause is at the bank s discretion After θ investors have withdrawn, govt observes all σ k decides on bailout payments remaining resources are allocated efficiently within each bank 13

18 Equilibrium behavior Q: Is the constrained efficient allocation an equilibrium? Suppose all other banks follow: c 1S if c 1W σ k = 0 σ k = σ Consider the choice of an individual weak bank i Would it choose to follow this same strategy? that is, bail in its investors and pay c 1W? Or to deviate? by delaying the response and paying c 1S? 14

19 If bank i chooses to bail in: 15

20 If bank i chooses to delay: Deviation to c 1S is profitable 16

21 Results Result 1: The constrained efficient allocation is not an equilibrium Any equilibrium involves a delayed response by weak banks in other words: bailouts delay bail-ins 17

22 Results Result 1: The constrained efficient allocation is not an equilibrium Any equilibrium involves a delayed response by weak banks in other words: bailouts delay bail-ins If all weak banks choose to delay more assets are liquidated in period 1 putting more strain on the government budget the bailout policy will satisfy v τ nn = u c 1W = Ru c 1W lower consumption levels for remaining investors in weak banks 17

23 When all weak banks delay: If c 2W falls below c 1S patient investors will not wait 18

24 Results Result 2: For some parameter values, there exists an equilibrium in which investors run on all weak banks The delayed response can amplify the real shock in two ways directly: resources allocated inefficiently indirectly: causes a run additional liquidation of investment 19

25 Results Result 2: For some parameter values, there exists an equilibrium in which investors run on all weak banks The delayed response can amplify the real shock in two ways directly: resources allocated inefficiently indirectly: causes a run additional liquidation of investment Note: a strategic complementarity arises across banks here if investors are running on other weak banks bailout received by my bank will be smaller increases the incentive to run on my bank This is different from the usual complementarity within a bank 19

26 Results Result 3: For some parameter values, there are multiple equilibria 20

27 Macroprudential policy 21

28 What should policy makers do in this type of environment? We consider three types of prudential policy 1) a cap on banks early payments 2) increasing tax revenue (to provide more fiscal space ) 3) eliminating bailouts Each policy can raise welfare for some parameter values but none of them implement the constrained efficient allocation 22

29 1) Suppose the govt. can limit early payments in the bad state c k 1 c, c 1W where c c 1S is a policy choice Interpretations: a) restriction on paying dividends (for all banks) b) requiring contingent debt with a systemic trigger Result 4: Optimal policy often has c < c 1S Intuition: moves weak banks closer to constrained optimum also distorts allocation in sound banks, but loss is second order 23

30 In some cases, optimal cap eliminates the run equilibrium if c is low enough, weak banks will preserve enough resources that patient investors will choose to wait in this case, the (ex post) optimal bailout ~ deposit insurance 24

31 2) Increasing the tax rate τ When weak banks delay bailing in their investors bailout payments will be larger than in the planner s allocation leading to a lower level of the public good Raising the tax rate has two potential benefits 1) it eases the govt budget constraint in the bad state 2) and may eliminate the run equilibrium because a govt with more fiscal space will provide larger bailouts Result 5: Optimal policy always has τ > τ can be used together with a cap on early payments 25

32 3) Eliminating bailouts If govt can credibly commit to a no bailouts policy which is a big if, but suppose it is possible weak banks will have no incentive to delay will choose to immediately bail in their investors when there is no delay no bank run will occur However, this policy prevents socially-valuable risk sharing public good consumption remains high in a crisis even while the private consumption of investors in weak banks is low 26

33 Result 6: Eliminating bailouts raises welfare for some parameter values, but not for others most useful when other policy tools do not eliminate the run equilibrium 27

34 A more general model 28

35 The general case Suppose we allow banks to set any c k 1 c (not just c or c 1W ) In addition, govt. can examine a fraction α < 1 of banks if bank is found to be weak put into early resolution This setting creates a signaling game weak banks want to set c 1 k high to receive larger bailouts but also want to hide as govt tries to infer which banks are bad Results are qualitatively unchanged: constrained efficient allocation is not an equilibrium there is a pooling equilibrium with delay all banks choose c 1S in some cases, this equilibrium also has a bank run 29

36 Conclusions 30

37 Take-aways One aim of financial stability policy: make a quicker response to a crisis possible much effort has gone into reforms of this type could potentially solve the bank runs problem But will a quick response actually occur? it would likely depend on (private) information of banks need to think about their incentive to act vs. delay We argue there is cause for concern bailouts delay bail-ins this delay can lead to a bank run Role for prudential policy even if tools are very blunt 31

Bailouts, Bail-ins and Banking Crises

Bailouts, Bail-ins and Banking Crises Todd Keister Yuliyan Mitkov September 20, 206 We study the interaction between a government s bailout policy during a banking crisis and individual banks willingness

Bailouts, Bail-ins and Banking Crises Todd Keister Yuliyan Mitkov September 20, 206 We study the interaction between a government s bailout policy during a banking crisis and individual banks willingness

Bailouts, Bail-ins and Banking Crises

Bailouts, Bail-ins and Banking Crises Todd Keister Rutgers University todd.keister@rutgers.edu Yuliyan Mitkov Rutgers University ymitkov@economics.rutgers.edu June 11, 2017 We study the interaction between

Bailouts, Bail-ins and Banking Crises Todd Keister Rutgers University todd.keister@rutgers.edu Yuliyan Mitkov Rutgers University ymitkov@economics.rutgers.edu June 11, 2017 We study the interaction between

Expectations vs. Fundamentals-based Bank Runs: When should bailouts be permitted?

Expectations vs. Fundamentals-based Bank Runs: When should bailouts be permitted? Todd Keister Rutgers University Vijay Narasiman Harvard University October 2014 The question Is it desirable to restrict

Expectations vs. Fundamentals-based Bank Runs: When should bailouts be permitted? Todd Keister Rutgers University Vijay Narasiman Harvard University October 2014 The question Is it desirable to restrict

A Baseline Model: Diamond and Dybvig (1983)

") BANKING AND FINANCIAL FRAGILITY A Baseline Model: Diamond and Dybvig (1983) Professor Todd Keister Rutgers University May 2017 Objective Want to develop a model to help us understand: why banks and other

BANKING AND FINANCIAL FRAGILITY A Baseline Model: Diamond and Dybvig (1983) Professor Todd Keister Rutgers University May 2017 Objective Want to develop a model to help us understand: why banks and other

Expectations vs. Fundamentals-driven Bank Runs: When Should Bailouts be Permitted?

Expectations vs. Fundamentals-driven Bank Runs: When Should Bailouts be Permitted? Todd Keister Rutgers University todd.keister@rutgers.edu Vijay Narasiman Harvard University vnarasiman@fas.harvard.edu

Expectations vs. Fundamentals-driven Bank Runs: When Should Bailouts be Permitted? Todd Keister Rutgers University todd.keister@rutgers.edu Vijay Narasiman Harvard University vnarasiman@fas.harvard.edu

Expectations versus Fundamentals: Does the Cause of Banking Panics Matter for Prudential Policy?

Federal Reserve Bank of New York Staff Reports Expectations versus Fundamentals: Does the Cause of Banking Panics Matter for Prudential Policy? Todd Keister Vijay Narasiman Staff Report no. 519 October

Federal Reserve Bank of New York Staff Reports Expectations versus Fundamentals: Does the Cause of Banking Panics Matter for Prudential Policy? Todd Keister Vijay Narasiman Staff Report no. 519 October

Optimal Credit Market Policy. CEF 2018, Milan

Optimal Credit Market Policy Matteo Iacoviello 1 Ricardo Nunes 2 Andrea Prestipino 1 1 Federal Reserve Board 2 University of Surrey CEF 218, Milan June 2, 218 Disclaimer: The views expressed are solely

Optimal Credit Market Policy Matteo Iacoviello 1 Ricardo Nunes 2 Andrea Prestipino 1 1 Federal Reserve Board 2 University of Surrey CEF 218, Milan June 2, 218 Disclaimer: The views expressed are solely

Bailouts and Financial Fragility

Bailouts and Financial Fragility Todd Keister Department of Economics Rutgers University todd.keister@rutgers.edu August 11, 2015 Abstract Should policy makers be prevented from bailing out investors in

Bailouts and Financial Fragility Todd Keister Department of Economics Rutgers University todd.keister@rutgers.edu August 11, 2015 Abstract Should policy makers be prevented from bailing out investors in

In Diamond-Dybvig, we see run equilibria in the optimal simple contract.

Ennis and Keister, "Run equilibria in the Green-Lin model of financial intermediation" Journal of Economic Theory 2009 In Diamond-Dybvig, we see run equilibria in the optimal simple contract. When the

Ennis and Keister, "Run equilibria in the Green-Lin model of financial intermediation" Journal of Economic Theory 2009 In Diamond-Dybvig, we see run equilibria in the optimal simple contract. When the

A Model with Costly Enforcement

A Model with Costly Enforcement Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) Costly-Enforcement December 25, 2012 1 / 43 A Model with Costly

A Model with Costly Enforcement Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) Costly-Enforcement December 25, 2012 1 / 43 A Model with Costly

Financial Fragility A Global-Games Approach Itay Goldstein Wharton School, University of Pennsylvania

Financial Fragility A Global-Games Approach Itay Goldstein Wharton School, University of Pennsylvania Financial Fragility and Coordination Failures What makes financial systems fragile? What causes crises

Financial Fragility A Global-Games Approach Itay Goldstein Wharton School, University of Pennsylvania Financial Fragility and Coordination Failures What makes financial systems fragile? What causes crises

Supplement to the lecture on the Diamond-Dybvig model

ECON 4335 Economics of Banking, Fall 2016 Jacopo Bizzotto 1 Supplement to the lecture on the Diamond-Dybvig model The model in Diamond and Dybvig (1983) incorporates important features of the real world:

ECON 4335 Economics of Banking, Fall 2016 Jacopo Bizzotto 1 Supplement to the lecture on the Diamond-Dybvig model The model in Diamond and Dybvig (1983) incorporates important features of the real world:

Motivation: Two Basic Facts

Motivation: Two Basic Facts 1 Primary objective of macroprudential policy: aligning financial system resilience with systemic risk to promote the real economy Systemic risk event Financial system resilience

Motivation: Two Basic Facts 1 Primary objective of macroprudential policy: aligning financial system resilience with systemic risk to promote the real economy Systemic risk event Financial system resilience

Banks and Liquidity Crises in Emerging Market Economies

Banks and Liquidity Crises in Emerging Market Economies Tarishi Matsuoka Tokyo Metropolitan University May, 2015 Tarishi Matsuoka (TMU) Banking Crises in Emerging Market Economies May, 2015 1 / 47 Introduction

Banks and Liquidity Crises in Emerging Market Economies Tarishi Matsuoka Tokyo Metropolitan University May, 2015 Tarishi Matsuoka (TMU) Banking Crises in Emerging Market Economies May, 2015 1 / 47 Introduction

Maturity Transformation and Liquidity

Maturity Transformation and Liquidity Patrick Bolton, Tano Santos Columbia University and Jose Scheinkman Princeton University Motivation Main Question: Who is best placed to, 1. Transform Maturity 2.

Maturity Transformation and Liquidity Patrick Bolton, Tano Santos Columbia University and Jose Scheinkman Princeton University Motivation Main Question: Who is best placed to, 1. Transform Maturity 2.

Bailouts, Bank Runs, and Signaling

Bailouts, Bank Runs, and Signaling Chunyang Wang Peking University January 27, 2013 Abstract During the recent financial crisis, there were many bank runs and government bailouts. In many cases, bailouts

Bailouts, Bank Runs, and Signaling Chunyang Wang Peking University January 27, 2013 Abstract During the recent financial crisis, there were many bank runs and government bailouts. In many cases, bailouts

Federal Reserve Bank of New York Staff Reports

Federal Reserve Bank of New York Staff Reports Commitment and Equilibrium Bank Runs Huberto M. Ennis Todd Keister Staff Report no. 274 January 2007 Revised May 2007 This paper presents preliminary findings

Federal Reserve Bank of New York Staff Reports Commitment and Equilibrium Bank Runs Huberto M. Ennis Todd Keister Staff Report no. 274 January 2007 Revised May 2007 This paper presents preliminary findings

On Diamond-Dybvig (1983): A model of liquidity provision

: A model of liquidity provision") On Diamond-Dybvig (1983): A model of liquidity provision Eloisa Campioni Theory of Banking a.a. 2016-2017 Eloisa Campioni (Theory of Banking) On Diamond-Dybvig (1983): A model of liquidity provision a.a.

On Diamond-Dybvig (1983): A model of liquidity provision Eloisa Campioni Theory of Banking a.a. 2016-2017 Eloisa Campioni (Theory of Banking) On Diamond-Dybvig (1983): A model of liquidity provision a.a.

Monetary Economics: Problem Set #6 Solutions

Monetary Economics Problem Set #6 Monetary Economics: Problem Set #6 Solutions This problem set is marked out of 00 points. The weight given to each part is indicated below. Please contact me asap if you

Monetary Economics Problem Set #6 Monetary Economics: Problem Set #6 Solutions This problem set is marked out of 00 points. The weight given to each part is indicated below. Please contact me asap if you

Revision Lecture Microeconomics of Banking MSc Finance: Theory of Finance I MSc Economics: Financial Economics I

Revision Lecture Microeconomics of Banking MSc Finance: Theory of Finance I MSc Economics: Financial Economics I April 2005 PREPARING FOR THE EXAM What models do you need to study? All the models we studied

Revision Lecture Microeconomics of Banking MSc Finance: Theory of Finance I MSc Economics: Financial Economics I April 2005 PREPARING FOR THE EXAM What models do you need to study? All the models we studied

Exam Fall 2004 Prof.: Ricardo J. Caballero

Exam 14.454 Fall 2004 Prof.: Ricardo J. Caballero Question #1 -- Simple Labor Market Search Model (20 pts) Assume that the labor market is described by the following model. Population is normalized to

Exam 14.454 Fall 2004 Prof.: Ricardo J. Caballero Question #1 -- Simple Labor Market Search Model (20 pts) Assume that the labor market is described by the following model. Population is normalized to

Regulatory Arbitrage and Systemic Liquidity Crises

Regulatory Arbitrage and Systemic Liquidity Crises Stephan Luck & Paul Schempp Princeton University and MPI for Research on Collective Goods Federal Reserve Bank of Atlanta The Role of Liquidity in the

Regulatory Arbitrage and Systemic Liquidity Crises Stephan Luck & Paul Schempp Princeton University and MPI for Research on Collective Goods Federal Reserve Bank of Atlanta The Role of Liquidity in the

Macroeconomics 4 Notes on Diamond-Dygvig Model and Jacklin

4.454 - Macroeconomics 4 Notes on Diamond-Dygvig Model and Jacklin Juan Pablo Xandri Antuna 4/22/20 Setup Continuum of consumers, mass of individuals each endowed with one unit of currency. t = 0; ; 2

4.454 - Macroeconomics 4 Notes on Diamond-Dygvig Model and Jacklin Juan Pablo Xandri Antuna 4/22/20 Setup Continuum of consumers, mass of individuals each endowed with one unit of currency. t = 0; ; 2

On the Optimality of Financial Repression

On the Optimality of Financial Repression V.V. Chari, Alessandro Dovis and Patrick Kehoe Conference in honor of Robert E. Lucas Jr, October 2016 Financial Repression Regulation forcing financial institutions

On the Optimality of Financial Repression V.V. Chari, Alessandro Dovis and Patrick Kehoe Conference in honor of Robert E. Lucas Jr, October 2016 Financial Repression Regulation forcing financial institutions

Lecture 26 Exchange Rates The Financial Crisis. Noah Williams

Lecture 26 Exchange Rates The Financial Crisis Noah Williams University of Wisconsin - Madison Economics 312/702 Money and Exchange Rates in a Small Open Economy Now look at relative prices of currencies:

Lecture 26 Exchange Rates The Financial Crisis Noah Williams University of Wisconsin - Madison Economics 312/702 Money and Exchange Rates in a Small Open Economy Now look at relative prices of currencies:

Government Safety Net, Stock Market Participation and Asset Prices

Government Safety Net, Stock Market Participation and Asset Prices Danilo Lopomo Beteto November 18, 2011 Introduction Goal: study of the effects on prices of government intervention during crises Question:

Government Safety Net, Stock Market Participation and Asset Prices Danilo Lopomo Beteto November 18, 2011 Introduction Goal: study of the effects on prices of government intervention during crises Question:

Sunspot Bank Runs and Fragility: The Role of Financial Sector Competition

Sunspot Bank Runs and Fragility: The Role of Financial Sector Competition Jiahong Gao Robert R. Reed August 9, 2018 Abstract What are the trade-offs between financial sector competition and fragility when

Sunspot Bank Runs and Fragility: The Role of Financial Sector Competition Jiahong Gao Robert R. Reed August 9, 2018 Abstract What are the trade-offs between financial sector competition and fragility when

Endogenous Systemic Liquidity Risk

Endogenous Systemic Liquidity Risk Jin Cao & Gerhard Illing 2nd IJCB Financial Stability Conference, Banco de España June 17, 2010 Outline Introduction The myths of liquidity Summary of the paper The Model

Endogenous Systemic Liquidity Risk Jin Cao & Gerhard Illing 2nd IJCB Financial Stability Conference, Banco de España June 17, 2010 Outline Introduction The myths of liquidity Summary of the paper The Model

Bank Runs and Institutions: The Perils of Intervention

Bank Runs and Institutions: The Perils of Intervention Huberto M. Ennis Research Department Federal Reserve Bank of Richmond Huberto.Ennis@rich.frb.org Todd Keister Research and Statistics Group Federal

Bank Runs and Institutions: The Perils of Intervention Huberto M. Ennis Research Department Federal Reserve Bank of Richmond Huberto.Ennis@rich.frb.org Todd Keister Research and Statistics Group Federal

Feedback Effect and Capital Structure

Feedback Effect and Capital Structure Minh Vo Metropolitan State University Abstract This paper develops a model of financing with informational feedback effect that jointly determines a firm s capital

Feedback Effect and Capital Structure Minh Vo Metropolitan State University Abstract This paper develops a model of financing with informational feedback effect that jointly determines a firm s capital

A key characteristic of financial markets is that they are subject to sudden, convulsive changes.

10.6 The Diamond-Dybvig Model A key characteristic of financial markets is that they are subject to sudden, convulsive changes. Such changes happen at both the microeconomic and macroeconomic levels. At

10.6 The Diamond-Dybvig Model A key characteristic of financial markets is that they are subject to sudden, convulsive changes. Such changes happen at both the microeconomic and macroeconomic levels. At

Banks and Liquidity Crises in an Emerging Economy

Banks and Liquidity Crises in an Emerging Economy Tarishi Matsuoka Abstract This paper presents and analyzes a simple model where banking crises can occur when domestic banks are internationally illiquid.

Banks and Liquidity Crises in an Emerging Economy Tarishi Matsuoka Abstract This paper presents and analyzes a simple model where banking crises can occur when domestic banks are internationally illiquid.

Do Low Interest Rates Sow the Seeds of Financial Crises?

Do Low nterest Rates Sow the Seeds of Financial Crises? Simona Cociuba, University of Western Ontario Malik Shukayev, Bank of Canada Alexander Ueberfeldt, Bank of Canada Second Boston University-Boston

Do Low nterest Rates Sow the Seeds of Financial Crises? Simona Cociuba, University of Western Ontario Malik Shukayev, Bank of Canada Alexander Ueberfeldt, Bank of Canada Second Boston University-Boston

Monetary and Financial Macroeconomics

Monetary and Financial Macroeconomics Hernán D. Seoane Universidad Carlos III de Madrid Introduction Last couple of weeks we introduce banks in our economies Financial intermediation arises naturally when

Monetary and Financial Macroeconomics Hernán D. Seoane Universidad Carlos III de Madrid Introduction Last couple of weeks we introduce banks in our economies Financial intermediation arises naturally when

Global Financial Systems Chapter 8 Bank Runs and Deposit Insurance

Global Financial Systems Chapter 8 Bank Runs and Deposit Insurance Jon Danielsson London School of Economics 2018 To accompany Global Financial Systems: Stability and Risk http://www.globalfinancialsystems.org/

Global Financial Systems Chapter 8 Bank Runs and Deposit Insurance Jon Danielsson London School of Economics 2018 To accompany Global Financial Systems: Stability and Risk http://www.globalfinancialsystems.org/

Macroprudential Policies in a Low Interest-Rate Environment

Macroprudential Policies in a Low Interest-Rate Environment Margarita Rubio 1 Fang Yao 2 1 University of Nottingham 2 Reserve Bank of New Zealand. The views expressed in this paper do not necessarily reflect

Macroprudential Policies in a Low Interest-Rate Environment Margarita Rubio 1 Fang Yao 2 1 University of Nottingham 2 Reserve Bank of New Zealand. The views expressed in this paper do not necessarily reflect

14.02 Quiz 1, Spring 2012

14.0 Quiz 1, Spring 01 Time Allowed: 90 minutes 1 True/ False Questions: (5 points each) Note: Your answers should be justified by a brief explanation. A simple T/F answer won t get you any points. 1.

14.0 Quiz 1, Spring 01 Time Allowed: 90 minutes 1 True/ False Questions: (5 points each) Note: Your answers should be justified by a brief explanation. A simple T/F answer won t get you any points. 1.

Federal Reserve Tools for Managing Rates and Reserves

Federal Reserve Tools for Managing Rates and Reserves David Skeie* Federal Reserve Bank of New York and Board of Governors of the Federal Reserve System (with Antoine Martin, James McAndrews and Ali Palida)

Federal Reserve Tools for Managing Rates and Reserves David Skeie* Federal Reserve Bank of New York and Board of Governors of the Federal Reserve System (with Antoine Martin, James McAndrews and Ali Palida)

Financial Fragility and the Exchange Rate Regime Chang and Velasco JET 2000 and NBER 6469

Financial Fragility and the Exchange Rate Regime Chang and Velasco JET 2000 and NBER 6469 1 Introduction and Motivation International illiquidity Country s consolidated nancial system has potential short-term

Financial Fragility and the Exchange Rate Regime Chang and Velasco JET 2000 and NBER 6469 1 Introduction and Motivation International illiquidity Country s consolidated nancial system has potential short-term

The Federal Reserve in the 21st Century Financial Stability Policies

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

Financial Economics Field Exam August 2011

Financial Economics Field Exam August 2011 There are two questions on the exam, representing Macroeconomic Finance (234A) and Corporate Finance (234C). Please answer both questions to the best of your

Financial Economics Field Exam August 2011 There are two questions on the exam, representing Macroeconomic Finance (234A) and Corporate Finance (234C). Please answer both questions to the best of your

The Federal Reserve in the 21st Century Financial Stability Policies

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

Rules versus discretion in bank resolution

Rules versus discretion in bank resolution Ansgar Walther (Oxford) Lucy White (HBS) May 2016 The post-crisis agenda Reducing the costs associated with failure of systemic banks: 1 Reduce probability of

Rules versus discretion in bank resolution Ansgar Walther (Oxford) Lucy White (HBS) May 2016 The post-crisis agenda Reducing the costs associated with failure of systemic banks: 1 Reduce probability of

Liquidity Regulation and Unintended Financial Transformation in China

Liquidity Regulation and Unintended Financial Transformation in China Kinda Cheryl Hachem Zheng (Michael) Song Chicago Booth Chinese University of Hong Kong First Research Workshop on China s Economy April

Liquidity Regulation and Unintended Financial Transformation in China Kinda Cheryl Hachem Zheng (Michael) Song Chicago Booth Chinese University of Hong Kong First Research Workshop on China s Economy April

Global Games and Financial Fragility:

Global Games and Financial Fragility: Foundations and a Recent Application Itay Goldstein Wharton School, University of Pennsylvania Outline Part I: The introduction of global games into the analysis of

Global Games and Financial Fragility: Foundations and a Recent Application Itay Goldstein Wharton School, University of Pennsylvania Outline Part I: The introduction of global games into the analysis of

Illiquidity and Interest Rate Policy

Illiquidity and Interest Rate Policy Douglas Diamond and Raghuram Rajan University of Chicago Booth School of Business and NBER 2 Motivation Illiquidity and insolvency are likely when long term assets

Illiquidity and Interest Rate Policy Douglas Diamond and Raghuram Rajan University of Chicago Booth School of Business and NBER 2 Motivation Illiquidity and insolvency are likely when long term assets

Lecture 25 Unemployment Financial Crisis. Noah Williams

Lecture 25 Unemployment Financial Crisis Noah Williams University of Wisconsin - Madison Economics 702 Changes in the Unemployment Rate What raises the unemployment rate? Anything raising reservation wage:

Lecture 25 Unemployment Financial Crisis Noah Williams University of Wisconsin - Madison Economics 702 Changes in the Unemployment Rate What raises the unemployment rate? Anything raising reservation wage:

1 Dynamic programming

1 Dynamic programming A country has just discovered a natural resource which yields an income per period R measured in terms of traded goods. The cost of exploitation is negligible. The government wants

1 Dynamic programming A country has just discovered a natural resource which yields an income per period R measured in terms of traded goods. The cost of exploitation is negligible. The government wants

On the use of leverage caps in bank regulation

On the use of leverage caps in bank regulation Afrasiab Mirza Department of Economics University of Birmingham a.mirza@bham.ac.uk Frank Strobel Department of Economics University of Birmingham f.strobel@bham.ac.uk

On the use of leverage caps in bank regulation Afrasiab Mirza Department of Economics University of Birmingham a.mirza@bham.ac.uk Frank Strobel Department of Economics University of Birmingham f.strobel@bham.ac.uk

Impact of Imperfect Information on the Optimal Exercise Strategy for Warrants

Impact of Imperfect Information on the Optimal Exercise Strategy for Warrants April 2008 Abstract In this paper, we determine the optimal exercise strategy for corporate warrants if investors suffer from

Impact of Imperfect Information on the Optimal Exercise Strategy for Warrants April 2008 Abstract In this paper, we determine the optimal exercise strategy for corporate warrants if investors suffer from

Contagious Adverse Selection

Stephen Morris and Hyun Song Shin European University Institute, Florence 17 March 2011 Credit Crisis of 2007-2009 A key element: some liquid markets shut down Market Con dence I We had it I We lost it

Stephen Morris and Hyun Song Shin European University Institute, Florence 17 March 2011 Credit Crisis of 2007-2009 A key element: some liquid markets shut down Market Con dence I We had it I We lost it

A Macroeconomic Model with Financial Panics

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

PROBLEM SET 6 ANSWERS

PROBLEM SET 6 ANSWERS 6 November 2006. Problems.,.4,.6, 3.... Is Lower Ability Better? Change Education I so that the two possible worker abilities are a {, 4}. (a) What are the equilibria of this game?

PROBLEM SET 6 ANSWERS 6 November 2006. Problems.,.4,.6, 3.... Is Lower Ability Better? Change Education I so that the two possible worker abilities are a {, 4}. (a) What are the equilibria of this game?

How Effectively Can Debt Covenants Alleviate Financial Agency Problems?

How Effectively Can Debt Covenants Alleviate Financial Agency Problems? Andrea Gamba Alexander J. Triantis Corporate Finance Symposium Cambridge Judge Business School September 20, 2014 What do we know

How Effectively Can Debt Covenants Alleviate Financial Agency Problems? Andrea Gamba Alexander J. Triantis Corporate Finance Symposium Cambridge Judge Business School September 20, 2014 What do we know

Appendix: Common Currencies vs. Monetary Independence

Appendix: Common Currencies vs. Monetary Independence A The infinite horizon model This section defines the equilibrium of the infinity horizon model described in Section III of the paper and characterizes

Appendix: Common Currencies vs. Monetary Independence A The infinite horizon model This section defines the equilibrium of the infinity horizon model described in Section III of the paper and characterizes

Federal Reserve Bank of New York Staff Reports

Federal Reserve Bank of New York Staff Reports Run Equilibria in a Model of Financial Intermediation Huberto M. Ennis Todd Keister Staff Report no. 32 January 2008 This paper presents preliminary findings

Federal Reserve Bank of New York Staff Reports Run Equilibria in a Model of Financial Intermediation Huberto M. Ennis Todd Keister Staff Report no. 32 January 2008 This paper presents preliminary findings

Banks and Liquidity Crises in Emerging Market Economies

Banks and Liquidity Crises in Emerging Market Economies Tarishi Matsuoka April 17, 2015 Abstract This paper presents and analyzes a simple banking model in which banks have access to international capital

Banks and Liquidity Crises in Emerging Market Economies Tarishi Matsuoka April 17, 2015 Abstract This paper presents and analyzes a simple banking model in which banks have access to international capital

Fire sales, inefficient banking and liquidity ratios

Fire sales, inefficient banking and liquidity ratios Axelle Arquié September 1, 215 [Link to the latest version] Abstract In a Diamond and Dybvig setting, I introduce a choice by households between the

Fire sales, inefficient banking and liquidity ratios Axelle Arquié September 1, 215 [Link to the latest version] Abstract In a Diamond and Dybvig setting, I introduce a choice by households between the

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Low Interest Rate Policy and Financial Stability

Low Interest Rate Policy and Financial Stability David Andolfatto Fernando Martin Aleksander Berentsen The views expressed here are our own and should not be attributed to the Federal Reserve Bank of St.

Low Interest Rate Policy and Financial Stability David Andolfatto Fernando Martin Aleksander Berentsen The views expressed here are our own and should not be attributed to the Federal Reserve Bank of St.

Market Design. Econ University of Notre Dame

Market Design Econ 400.40 University of Notre Dame What is market design? Increasingly, economists are asked not just to study or explain or interpret markets, but to design them. This requires different

Market Design Econ 400.40 University of Notre Dame What is market design? Increasingly, economists are asked not just to study or explain or interpret markets, but to design them. This requires different

Answers to Microeconomics Prelim of August 24, In practice, firms often price their products by marking up a fixed percentage over (average)

") Answers to Microeconomics Prelim of August 24, 2016 1. In practice, firms often price their products by marking up a fixed percentage over (average) cost. To investigate the consequences of markup pricing,

Answers to Microeconomics Prelim of August 24, 2016 1. In practice, firms often price their products by marking up a fixed percentage over (average) cost. To investigate the consequences of markup pricing,

Bank Runs, Welfare and Policy Implications

Bank Runs, Welfare and Policy Implications Haibin Zhu First draft: September 2000 This draft: April 2002 I thank Craig Furfine, Philip Lowe, Enrique Mendoza, Pietro Peretto, Kostas Tsatsaronis, Diego Valderrama

Bank Runs, Welfare and Policy Implications Haibin Zhu First draft: September 2000 This draft: April 2002 I thank Craig Furfine, Philip Lowe, Enrique Mendoza, Pietro Peretto, Kostas Tsatsaronis, Diego Valderrama

d. Find a competitive equilibrium for this economy. Is the allocation Pareto efficient? Are there any other competitive equilibrium allocations?

Answers to Microeconomics Prelim of August 7, 0. Consider an individual faced with two job choices: she can either accept a position with a fixed annual salary of x > 0 which requires L x units of labor

Answers to Microeconomics Prelim of August 7, 0. Consider an individual faced with two job choices: she can either accept a position with a fixed annual salary of x > 0 which requires L x units of labor

Credit Market Competition and Liquidity Crises

Credit Market Competition and Liquidity Crises Elena Carletti Agnese Leonello European University Institute and CEPR University of Pennsylvania May 9, 2012 Motivation There is a long-standing debate on

Credit Market Competition and Liquidity Crises Elena Carletti Agnese Leonello European University Institute and CEPR University of Pennsylvania May 9, 2012 Motivation There is a long-standing debate on

A Macroeconomic Model with Financially Constrained Producers and Intermediaries

A Macroeconomic Model with Financially Constrained Producers and Intermediaries Simon Gilchrist Boston Univerity and NBER Federal Reserve Bank of San Francisco March 31st, 2017 Overview: Model that combines

A Macroeconomic Model with Financially Constrained Producers and Intermediaries Simon Gilchrist Boston Univerity and NBER Federal Reserve Bank of San Francisco March 31st, 2017 Overview: Model that combines

Principles of Banking (III): Macroeconomics of Banking (1) Introduction

: Macroeconomics of Banking (1) Introduction") Principles of Banking (III): Macroeconomics of Banking (1) Jin Cao (Norges Bank Research, Oslo & CESifo, München) Outline 1 2 Disclaimer (If they care about what I say,) the views expressed in this manuscript

Principles of Banking (III): Macroeconomics of Banking (1) Jin Cao (Norges Bank Research, Oslo & CESifo, München) Outline 1 2 Disclaimer (If they care about what I say,) the views expressed in this manuscript

Managing Confidence in Emerging Market Bank Runs

WP/04/235 Managing Confidence in Emerging Market Bank Runs Se-Jik Kim and Ashoka Mody 2004 International Monetary Fund WP/04/235 IMF Working Paper European Department and Research Department Managing Confidence

WP/04/235 Managing Confidence in Emerging Market Bank Runs Se-Jik Kim and Ashoka Mody 2004 International Monetary Fund WP/04/235 IMF Working Paper European Department and Research Department Managing Confidence

Financial Crises, Dollarization and Lending of Last Resort in Open Economies

Financial Crises, Dollarization and Lending of Last Resort in Open Economies Luigi Bocola Stanford, Minneapolis Fed, and NBER Guido Lorenzoni Northwestern and NBER Restud Tour Reunion Conference May 2018

Financial Crises, Dollarization and Lending of Last Resort in Open Economies Luigi Bocola Stanford, Minneapolis Fed, and NBER Guido Lorenzoni Northwestern and NBER Restud Tour Reunion Conference May 2018

Why are Banks Highly Interconnected?

Why are Banks Highly Interconnected? Alexander David Alfred Lehar University of Calgary Fields Institute - 2013 David and Lehar () Why are Banks Highly Interconnected? Fields Institute - 2013 1 / 35 Positive

Why are Banks Highly Interconnected? Alexander David Alfred Lehar University of Calgary Fields Institute - 2013 David and Lehar () Why are Banks Highly Interconnected? Fields Institute - 2013 1 / 35 Positive

A Diamond-Dybvig Model in which the Level of Deposits is Endogenous

A Diamond-Dybvig Model in which the Level of Deposits is Endogenous James Peck The Ohio State University A. Setayesh The Ohio State University January 28, 2019 Abstract We extend the Diamond-Dybvig model

A Diamond-Dybvig Model in which the Level of Deposits is Endogenous James Peck The Ohio State University A. Setayesh The Ohio State University January 28, 2019 Abstract We extend the Diamond-Dybvig model

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Preliminary Examination: Macroeconomics Fall, 2009

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Preliminary Examination: Macroeconomics Fall, 2009 Instructions: Read the questions carefully and make sure to show your work. You

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Preliminary Examination: Macroeconomics Fall, 2009 Instructions: Read the questions carefully and make sure to show your work. You

BIS Working Papers. Bank runs, welfare and policy implications. No 107. Monetary and Economic Department. Abstract. by Haibin Zhu.

BIS Working Papers No 17 Bank runs, welfare and policy implications by Haibin Zhu Monetary and Economic Department December 21 Abstract This paper proposes a model in which bank runs are closely related

BIS Working Papers No 17 Bank runs, welfare and policy implications by Haibin Zhu Monetary and Economic Department December 21 Abstract This paper proposes a model in which bank runs are closely related

Deflation, Credit Collapse and Great Depressions. Enrique G. Mendoza

Deflation, Credit Collapse and Great Depressions Enrique G. Mendoza Main points In economies where agents are highly leveraged, deflation amplifies the real effects of credit crunches Credit frictions

Deflation, Credit Collapse and Great Depressions Enrique G. Mendoza Main points In economies where agents are highly leveraged, deflation amplifies the real effects of credit crunches Credit frictions

Microeconomic Theory II Preliminary Examination Solutions Exam date: August 7, 2017

Microeconomic Theory II Preliminary Examination Solutions Exam date: August 7, 017 1. Sheila moves first and chooses either H or L. Bruce receives a signal, h or l, about Sheila s behavior. The distribution

Microeconomic Theory II Preliminary Examination Solutions Exam date: August 7, 017 1. Sheila moves first and chooses either H or L. Bruce receives a signal, h or l, about Sheila s behavior. The distribution

A Macroeconomic Model with Financially Constrained Producers and Intermediaries

A Macroeconomic Model with Financially Constrained Producers and Intermediaries Authors: Vadim, Elenev Tim Landvoigt and Stijn Van Nieuwerburgh Discussion by: David Martinez-Miera ECB Research Workshop

A Macroeconomic Model with Financially Constrained Producers and Intermediaries Authors: Vadim, Elenev Tim Landvoigt and Stijn Van Nieuwerburgh Discussion by: David Martinez-Miera ECB Research Workshop

Bank Runs, Prudential Tools and Social Welfare in a Global Game General Equilibrium Model

Bank Runs, Prudential Tools and Social Welfare in a Global Game General Equilibrium Model Daisuke Ikeda Bank of England 10 April 2018 Financial crises: predictability, causes and consequences The views

Bank Runs, Prudential Tools and Social Welfare in a Global Game General Equilibrium Model Daisuke Ikeda Bank of England 10 April 2018 Financial crises: predictability, causes and consequences The views

Discussion of A Pigovian Approach to Liquidity Regulation

Discussion of A Pigovian Approach to Liquidity Regulation Ernst-Ludwig von Thadden University of Mannheim The regulation of bank liquidity has been one of the most controversial topics in the recent debate

Discussion of A Pigovian Approach to Liquidity Regulation Ernst-Ludwig von Thadden University of Mannheim The regulation of bank liquidity has been one of the most controversial topics in the recent debate

Overborrowing, Financial Crises and Macro-prudential Policy

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin Enrique G. Mendoza University of Maryland & NBER The case for macro-prudential policies Credit booms are

Overborrowing, Financial Crises and Macro-prudential Policy Javier Bianchi University of Wisconsin Enrique G. Mendoza University of Maryland & NBER The case for macro-prudential policies Credit booms are

Bailouts, Time Inconsistency and Optimal Regulation

Federal Reserve Bank of Minneapolis Research Department Sta Report November 2009 Bailouts, Time Inconsistency and Optimal Regulation V. V. Chari University of Minnesota and Federal Reserve Bank of Minneapolis

Federal Reserve Bank of Minneapolis Research Department Sta Report November 2009 Bailouts, Time Inconsistency and Optimal Regulation V. V. Chari University of Minnesota and Federal Reserve Bank of Minneapolis

The lender of last resort: liquidity provision versus the possibility of bail-out

The lender of last resort: liquidity provision versus the possibility of bail-out Rob Nijskens Sylvester C.W. Eijffinger June 24, 2010 The lender of last resort: liquidity versus bail-out 1 /20 Motivation:

The lender of last resort: liquidity provision versus the possibility of bail-out Rob Nijskens Sylvester C.W. Eijffinger June 24, 2010 The lender of last resort: liquidity versus bail-out 1 /20 Motivation:

Pinning down the price level with the government balance sheet

Eco 342 Fall 2011 Chris Sims Pinning down the price level with the government balance sheet September 20, 2011 c 2011 by Christopher A. Sims. This document is licensed under the Creative Commons Attribution-NonCommercial-ShareAlike

Eco 342 Fall 2011 Chris Sims Pinning down the price level with the government balance sheet September 20, 2011 c 2011 by Christopher A. Sims. This document is licensed under the Creative Commons Attribution-NonCommercial-ShareAlike

LEVERAGE AND LIQUIDITY DRY-UPS: A FRAMEWORK AND POLICY IMPLICATIONS. Denis Gromb LBS, LSE and CEPR. Dimitri Vayanos LSE, CEPR and NBER

LEVERAGE AND LIQUIDITY DRY-UPS: A FRAMEWORK AND POLICY IMPLICATIONS Denis Gromb LBS, LSE and CEPR Dimitri Vayanos LSE, CEPR and NBER June 2008 Gromb-Vayanos 1 INTRODUCTION Some lessons from recent crisis:

LEVERAGE AND LIQUIDITY DRY-UPS: A FRAMEWORK AND POLICY IMPLICATIONS Denis Gromb LBS, LSE and CEPR Dimitri Vayanos LSE, CEPR and NBER June 2008 Gromb-Vayanos 1 INTRODUCTION Some lessons from recent crisis:

Externalities 1 / 40

Externalities 1 / 40 Outline Introduction Public Goods: Positive Externalities Policy Responses Persuasion Pigovian Subsidies and Taxes The Second Best Take Aways 2 / 40 Key Ideas What is an externality?

Externalities 1 / 40 Outline Introduction Public Goods: Positive Externalities Policy Responses Persuasion Pigovian Subsidies and Taxes The Second Best Take Aways 2 / 40 Key Ideas What is an externality?

Economia Finanziaria e Monetaria

Economia Finanziaria e Monetaria Lezione 11 Ruolo degli intermediari: aspetti micro delle crisi finanziarie (asimmetrie informative e modelli di business bancari/ finanziari) 1 0. Outline Scaletta della

Economia Finanziaria e Monetaria Lezione 11 Ruolo degli intermediari: aspetti micro delle crisi finanziarie (asimmetrie informative e modelli di business bancari/ finanziari) 1 0. Outline Scaletta della

Experimental Evidence of Bank Runs as Pure Coordination Failures

Experimental Evidence of Bank Runs as Pure Coordination Failures Jasmina Arifovic (Simon Fraser) Janet Hua Jiang (Bank of Canada and U of Manitoba) Yiping Xu (U of International Business and Economics)

Experimental Evidence of Bank Runs as Pure Coordination Failures Jasmina Arifovic (Simon Fraser) Janet Hua Jiang (Bank of Canada and U of Manitoba) Yiping Xu (U of International Business and Economics)

Externalities 1 / 40

Externalities 1 / 40 Key Ideas What is an externality? Externalities create opportunities for Pareto improving policy Externalities require active and ongoing policy interventions The optimal (second best)

Externalities 1 / 40 Key Ideas What is an externality? Externalities create opportunities for Pareto improving policy Externalities require active and ongoing policy interventions The optimal (second best)

International Trade Lecture 14: Firm Heterogeneity Theory (I) Melitz (2003)

Melitz (2003)") 14.581 International Trade Lecture 14: Firm Heterogeneity Theory (I) Melitz (2003) 14.581 Week 8 Spring 2013 14.581 (Week 8) Melitz (2003) Spring 2013 1 / 42 Firm-Level Heterogeneity and Trade What s wrong

14.581 International Trade Lecture 14: Firm Heterogeneity Theory (I) Melitz (2003) 14.581 Week 8 Spring 2013 14.581 (Week 8) Melitz (2003) Spring 2013 1 / 42 Firm-Level Heterogeneity and Trade What s wrong

The Ramsey Model. Lectures 11 to 14. Topics in Macroeconomics. November 10, 11, 24 & 25, 2008

The Ramsey Model Lectures 11 to 14 Topics in Macroeconomics November 10, 11, 24 & 25, 2008 Lecture 11, 12, 13 & 14 1/50 Topics in Macroeconomics The Ramsey Model: Introduction 2 Main Ingredients Neoclassical

The Ramsey Model Lectures 11 to 14 Topics in Macroeconomics November 10, 11, 24 & 25, 2008 Lecture 11, 12, 13 & 14 1/50 Topics in Macroeconomics The Ramsey Model: Introduction 2 Main Ingredients Neoclassical

Practice Problems 1: Moral Hazard

Practice Problems 1: Moral Hazard December 5, 2012 Question 1 (Comparative Performance Evaluation) Consider the same normal linear model as in Question 1 of Homework 1. This time the principal employs

Practice Problems 1: Moral Hazard December 5, 2012 Question 1 (Comparative Performance Evaluation) Consider the same normal linear model as in Question 1 of Homework 1. This time the principal employs

Bank Runs, Deposit Insurance, and Liquidity

Bank Runs, Deposit Insurance, and Liquidity Douglas W. Diamond University of Chicago Philip H. Dybvig Washington University in Saint Louis Washington University in Saint Louis August 13, 2015 Diamond,

Bank Runs, Deposit Insurance, and Liquidity Douglas W. Diamond University of Chicago Philip H. Dybvig Washington University in Saint Louis Washington University in Saint Louis August 13, 2015 Diamond,

Crises and Prices: Information Aggregation, Multiplicity and Volatility

: Information Aggregation, Multiplicity and Volatility Reading Group UC3M G.M. Angeletos and I. Werning November 09 Motivation Modelling Crises I There is a wide literature analyzing crises (currency attacks,

: Information Aggregation, Multiplicity and Volatility Reading Group UC3M G.M. Angeletos and I. Werning November 09 Motivation Modelling Crises I There is a wide literature analyzing crises (currency attacks,

1 Two Period Exchange Economy

University of British Columbia Department of Economics, Macroeconomics (Econ 502) Prof. Amartya Lahiri Handout # 2 1 Two Period Exchange Economy We shall start our exploration of dynamic economies with

University of British Columbia Department of Economics, Macroeconomics (Econ 502) Prof. Amartya Lahiri Handout # 2 1 Two Period Exchange Economy We shall start our exploration of dynamic economies with

``Liquidity requirements, liquidity choice and financial stability by Diamond and Kashyap. Discussant: Annette Vissing-Jorgensen, UC Berkeley

``Liquidity requirements, liquidity choice and financial stability by Diamond and Kashyap Discussant: Annette Vissing-Jorgensen, UC Berkeley Idea: Study liquidity regulation in a model where it serves

``Liquidity requirements, liquidity choice and financial stability by Diamond and Kashyap Discussant: Annette Vissing-Jorgensen, UC Berkeley Idea: Study liquidity regulation in a model where it serves

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Preliminary Examination: Macroeconomics Spring, 2007

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Preliminary Examination: Macroeconomics Spring, 2007 Instructions: Read the questions carefully and make sure to show your work. You

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Preliminary Examination: Macroeconomics Spring, 2007 Instructions: Read the questions carefully and make sure to show your work. You

Microeconomics of Banking: Lecture 3

Microeconomics of Banking: Lecture 3 Prof. Ronaldo CARPIO Oct. 9, 2015 Review of Last Week Consumer choice problem General equilibrium Contingent claims Risk aversion The optimal choice, x = (X, Y ), is

Microeconomics of Banking: Lecture 3 Prof. Ronaldo CARPIO Oct. 9, 2015 Review of Last Week Consumer choice problem General equilibrium Contingent claims Risk aversion The optimal choice, x = (X, Y ), is

Managing Capital Flows in the Presence of External Risks

Managing Capital Flows in the Presence of External Risks Ricardo Reyes-Heroles Federal Reserve Board Gabriel Tenorio The Boston Consulting Group IEA World Congress 2017 Mexico City, Mexico June 20, 2017

Managing Capital Flows in the Presence of External Risks Ricardo Reyes-Heroles Federal Reserve Board Gabriel Tenorio The Boston Consulting Group IEA World Congress 2017 Mexico City, Mexico June 20, 2017

The Race for Priority

The Race for Priority Martin Oehmke London School of Economics FTG Summer School 2017 Outline of Lecture In this lecture, I will discuss financing choices of financial institutions in the presence of a

The Race for Priority Martin Oehmke London School of Economics FTG Summer School 2017 Outline of Lecture In this lecture, I will discuss financing choices of financial institutions in the presence of a

Macroeconomia 1 Class 14a revised Diamond Dybvig model of banks

Macroeconomia 1 Class 14a revised Diamond Dybvig model of banks Prof. McCandless UCEMA November 25, 2010 How to model (think about) liquidity Model of Diamond and Dybvig (Journal of Political Economy,

Macroeconomia 1 Class 14a revised Diamond Dybvig model of banks Prof. McCandless UCEMA November 25, 2010 How to model (think about) liquidity Model of Diamond and Dybvig (Journal of Political Economy,

Government Guarantees and Financial Stability

Government Guarantees and Financial Stability F. Allen E. Carletti I. Goldstein A. Leonello Bocconi University and CEPR University of Pennsylvania Government Guarantees and Financial Stability 1 / 21 Introduction

Government Guarantees and Financial Stability F. Allen E. Carletti I. Goldstein A. Leonello Bocconi University and CEPR University of Pennsylvania Government Guarantees and Financial Stability 1 / 21 Introduction