Low Interest Rate Policy and Financial Stability

|

|

|

- Silas Reed

- 5 years ago

- Views:

Transcription

1 Low Interest Rate Policy and Financial Stability David Andolfatto Fernando Martin Aleksander Berentsen The views expressed here are our own and should not be attributed to the Federal Reserve Bank of St. Louis or the Federal Reserve System.

2 Motivation Does low-interest-rate monetary policy (LIMP) promote financial stability or instability? There are opposing views. One view is that LIMP induces reach-for-yield into higher risk assets. Promotes instability, esp. if financed with short-term debt (Stein, 2013). Another view is that LIMP encourages banks to hold more cash reserves. Promotes stability, since banks more likely to become narrow banks (Cochrane, 2014).

3 What we do The question we address requires a model of money and banking. Money is modeled as an exchange medium (Lagos-Wright, 2005). Dynamic general equilibrium framework (easy to make DSGE). Steady-state analysis so R policy equivalent to Π policy (Fisher effect). Bank is modeled as risk-sharing arrangement (Diamond-Dybvig, 1983). Demandable debt is a solution to private information problem, but opens the door to bank-runs (multiple equilibria).

4 Model Discrete time, infinite horizon, subjective discount factor β. Each period divided into 3 subperiods: morning, afternoon, evening. Two groups of agents: investors and workers. Investors face i.i.d. shock that determines type within period. impatient/patient want consumption in afternoon/evening. π denotes fraction of impatient, shock realized in afternoon.

5 Model Investors produce output in morning (consumer and capital goods) and consume in afternoon/evening (depending on type). Capital goods k yield afternoon output ξk or evening output Rk (assume 0 ξ < 1 < R). Workers want to consume in morning, able to work in afternoon. Afternoon output can be costlessly stored to the evening. Since ξ < 1, afternoon output supplied more effi ciently by workers relative to scrapping capital produced by investors.

6 Model Investor and worker preferences, resp. E 0 t=0 β t [ y 0,t + πu(c 1,t ) + (1 π)u(c 2,t ) ] E 0 t=0 β t [ c 0,t y 1,t ] Resource constraints (assuming no scrapping), c 0,t + k t = y 0,t πc 1,t y 1,t (1 π)c 2,t Rk t

7 Effi cient allocation Investors produce consumer and capital goods in morning. Consumer goods used to reward workers in the morning. Capital goods used to finance investor consumption in the evening. Workers produce output in the afternoon to service impatient investors. Effi ciency implies risk-sharing among investors (workers are risk-neutral).

8 Steps in our analysis Step 1: Competitive monetary eqm with ex post securities market. Investors accumulate money and capital in the morning, then trade money for capital in the afternoon after realizing their types. Markets are incomplete along two dimensions. No ex ante insurance market & ex post securities market closed with probability η (market freeze). Industry standard is η = 1 (illiquid capital). Liquidating capital when sec. mkt. closed means scrapping (firesale).

9 Steps in our analysis Step 2: Construct a Diamond-Dybvig bank assuming no bank runs. Demonstrate two dimensions along which welfare improved. (i) improved risk-sharing and (ii) bypass sec. mkt. (avoid firesales). Demonstrate that (i) above entails fractional reserve banking. Bank funds assets (cash + capital) with liabilities redeemable on demand for cash. Optimal contract anticipates that only fraction π will withdraw early, but fractional reserves implies bank run eqm.

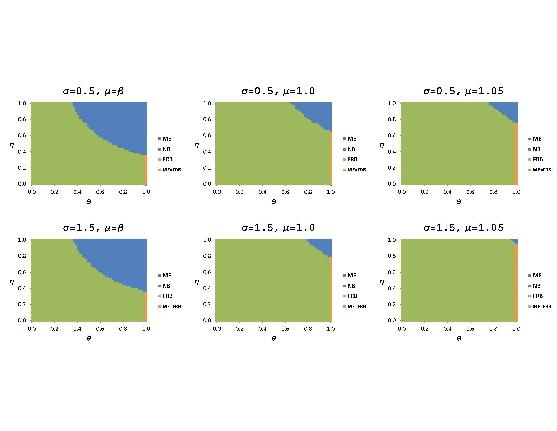

10 Steps in our analysis Step 3: Construct Diamond-Dybvig bank assuming runs occur w.p. θ. We think of societies as potentially differing in θ (social fragility). Bank offers investors deposit contracts that maximizes ex ante welfare for a given parameter configuration (θ, µ, η). We identify regions in the parameter space where narrow banking is preferred. We investigate how these regions depend on interest (inflation) rate policy.

11 Steps in our analysis Step 4: In an extension, we plan to specify more general belief functions. i.e., let θ be a function of economic variables. Jeremy Stein specification θ is decreasing function of yield differential between money and capital. John Cochrane specification θ is decreasing fuction of currency-deposit ratio.

12 Workers Workers in our model behave the same in all versions of the model. Workers have linear preferences, their decisions essentially pin down eqm pricing relationships. Let p m t, pa t denote price of output in morning and afternoon, resp. The following no-arbitrage-condition must hold: 1/p a t = β/pm t+1, or (p a t /p m t ) = ( p m t+1 /pm t ) /β = (µ/β) = R n R n is the nominal interest rate and R n = µ/β is the Fisher equation.

13 Monetary equilibrium with securities market New money injected as lump-sum transfers to workers each morning. Let p k t denote price of capital in security market (if it is open) and let ρ p k t /pa t. Let ( c 1, c 2 ) denote allocation when the securities market is open (ĉ 1, ĉ 2 ) when closed. Let k I denote sales of capital by impatient depositor, let k P denote purchases of capital by patient depositor (assuming market is open).

14 Monetary equilibrium with securities market Investor maximizes chooses consumption and x, k, k I, k P to maximize x k +(1 η) [πu( c 1 ) + (1 π)u( c 2 )]+η [πu (ĉ 1 ) + (1 π)u(ĉ 2 )] subject to (β/µ)x + ρk I + ξ ( k k I) c 1 k k I 0 (β/µ)x ρk P + R(k + k P ) c 2 (β/µ)x ρk P 0

15 Monetary equilibrium with securities market Lemma: In a stationary monetary equilibrium, ξ ρ R for any η [0, 1). Proposition: A stationary monetary equilibrium implements the first best allocation if and only if η = 0, µ = β and u (c 1 )c 1 = u (c 2 )c 2. Result above shows that monetary equilibrium implements the first best allocation in only a razor-edge case. Sec. mkt. always open, Friedman rule, and (e.g.) log preferences. In general, welfare gains will be possible under FRB system.

16 Fractional reserve bank Bank offers depositors a security that overcomes absence of liquid secondary market for capital. This new security a demand deposit liability grants depositors the option to convert deposits for cash; permits depositors to avoid firesale events that inflicted investors in monetary economy. But even if secondary market is always open (η = 0) a bank can still improve welfare by offering superior risk-sharing. Banks help complete the missing ex ante insurance market.

17 Fractional reserve bank assuming no bank run Banks offer depositors a contract that maximizes max { x k + πu(c 1 ) + (1 π)u(c 2 )} (β/µ) x πc 1 Rk + [(β/µ) x πc 1 ] (1 π)c 2 c 2 c 1 0 Proposition: In a FRB equilibrium absent bank runs, the Friedman rule µ = β implements the first-best allocation and the currency-to-deposit ratio x/(x + k) increases/decreases with inflation as u (c)c/u (c) 1.

18 Financial fragility Well-known that demandable debt structures can be fragile (suffer from multiplicity of equilibria). Unique implementation possible with suffi ciently rich contract space. We assume that banks cannot credibly commit to suspend withdrawals when cash reserves are exhausted. Then a bank run equilibrium is possible, with bank run defined as: patient investors misrepresenting themselves as impatient en masse.

19 Social fragility We index societies by a parameter θ [0, 1]. Formally, θ is probability of sunspot that triggers a bank-run. We think of θ as indexing the propensity of a society to act on rumors and coordinate on bad outcomes. Low θ societies are inherently stable. High θ societies inherently unstable. Distinction between inherent instability and manufactured instability.

20 Fractional reserve banking when bank runs are expected Bank offers depostors contract that maximizes { x k + (1 θ) [πu(c1 ) + (1 π)u(c 2 )] + (1 η) θ[πu( c 1 ) + (1 π)u( c 2 )] + ηθ[u(πĉ 1 ) + (1 π)u(ĉ 2 )] } (β/µ) x πc 1 Rk + [(β/µ) x πc 1 ] (1 π)c 2 (β/µ)x + ρk B + ξ(k k B ) c 1 (β/µ)x + ρk B + ξ(k k B ) + (R ρ)k P c 2 (β/µ)x + ξk ĉ 1 (β/µ)x + Rk ĉ 2 k k B 0 (β/µ)x + ρk B + ξ(k k B ) ρk P 0 c 2 c 1 0

21 Fractional reserve banking when bank runs are expected Proposition: In a FRB system with θ (0, 1], then banks are generally able to meet all their obligations in the event of a run if the securities market is open. Formally, c 1 = c 1 and c 2 = c 2. When secondary market is available, orderly disposal of capital is possible, so bank run does not necessarily result in firesales. Proposition: A FRB system with θ (0, 1] implements the first-best allocation if and only if η = 0, µ = β and u (c 1 )c 1 = u (c 2 )c 2. Franchise value of bank W B (θ, η, µ) is decreasing in (θ, η, µ).

22 Fractional reserve banking when bank runs are expected Benefit of FRB is higher in high inflation (high interest rate) economy. High µ implies low real return on cash (FRB economizes on cash). Benefits of fractional reserve banking are greatly diminished in socially unstable societies (high θ economies). Especially in economies with very illiquid capital markets (high η economies). FRB may be dominated by a narrow banking structure in low µ, high θ, η economies.

23 Narrow bank Narrow bank: all demandable debt is backed 100% with cash reserves. Unlike FRB, narrow bank can meet short-term obligations in every state of the world. Consequently, runs are impossible (at cost of excess reserves, poorer risk-sharing). W N (µ) max { x k + πu(c 1 ) + (1 π)u(c 2 )} (β/µ) x c 1 Rk + [(β/µ) x πc 1 ] (1 π)c 2 W N (µ) is independent of θ, η and decreasing in inflation µ.

24 The choice of banking regime Proposition. There exists ˆθ(η, µ) satisfying W B (ˆθ, η, µ) = W N (µ) such that W B (ˆθ, η, µ) > W N (µ) for θ < ˆθ and W B (ˆθ, η, µ) < W N (µ) for θ > ˆθ. Moreover, ˆθ(η, µ) is strictly increasing in µ. Inherently fragile societies prefer more stable banking regimes. Inherently stable societies prefer more unstable banking regimes. Moreover, high inflation economies encourage unstable banking regimes. Interests of investors not necessarily aligned with those of workers.

25

26 The belief function In models with multiple equilibria, the belief parameter can be anything and still be consistent with rational expectations. Nothing in theory dictates θ being purely exogenous. We could in principle assume any belief function θ = B(x), where x includes model parameters and endogenous variables. We have experimented with two belief functions, one which implies θ a decreasing function of µ (Stein) and one which implies θ a decreasing function of µ (Cochrane).

27 When reach-for-yield promotes instability

28 Extensions Model liquidation costs more realistically (OTC market structure, disruption in payment system,...). Introduce a role for bank capital (equity), study Basel III regulations (capital adequacy ratio). Consider multibank model with interbank market. Multibank model across two countries, with and without a common currency.

Financial Fragility in Monetary Economies

Financial Fragility in Monetary Economies David Andolfatto Federal Reserve Bank of St. Louis and Simon Fraser University Aleksander Berentsen University of Basel Fernando M. Martin Federal Reserve Bank

Financial Fragility in Monetary Economies David Andolfatto Federal Reserve Bank of St. Louis and Simon Fraser University Aleksander Berentsen University of Basel Fernando M. Martin Federal Reserve Bank

Financial Fragility in Monetary Economies

Financial Fragility in Monetary Economies David Andolfatto Federal Reserve Bank of St. Louis and Simon Fraser University Aleksander Berentsen University of Basel Fernando M. Martin Federal Reserve Bank

Financial Fragility in Monetary Economies David Andolfatto Federal Reserve Bank of St. Louis and Simon Fraser University Aleksander Berentsen University of Basel Fernando M. Martin Federal Reserve Bank

Essential interest-bearing money

Essential interest-bearing money David Andolfatto Federal Reserve Bank of St. Louis The Lagos-Wright Model Leading framework in contemporary monetary theory Models individuals exposed to idiosyncratic

Essential interest-bearing money David Andolfatto Federal Reserve Bank of St. Louis The Lagos-Wright Model Leading framework in contemporary monetary theory Models individuals exposed to idiosyncratic

ON THE SOCIETAL BENEFITS OF ILLIQUID BONDS IN THE LAGOS-WRIGHT MODEL. 1. Introduction

ON THE SOCIETAL BENEFITS OF ILLIQUID BONDS IN THE LAGOS-WRIGHT MODEL DAVID ANDOLFATTO Abstract. In the equilibria of monetary economies, individuals may have different intertemporal marginal rates of substitution,

ON THE SOCIETAL BENEFITS OF ILLIQUID BONDS IN THE LAGOS-WRIGHT MODEL DAVID ANDOLFATTO Abstract. In the equilibria of monetary economies, individuals may have different intertemporal marginal rates of substitution,

A Model with Costly Enforcement

A Model with Costly Enforcement Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) Costly-Enforcement December 25, 2012 1 / 43 A Model with Costly

A Model with Costly Enforcement Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) Costly-Enforcement December 25, 2012 1 / 43 A Model with Costly

Banks and Liquidity Crises in Emerging Market Economies

Banks and Liquidity Crises in Emerging Market Economies Tarishi Matsuoka Tokyo Metropolitan University May, 2015 Tarishi Matsuoka (TMU) Banking Crises in Emerging Market Economies May, 2015 1 / 47 Introduction

Banks and Liquidity Crises in Emerging Market Economies Tarishi Matsuoka Tokyo Metropolitan University May, 2015 Tarishi Matsuoka (TMU) Banking Crises in Emerging Market Economies May, 2015 1 / 47 Introduction

A unified framework for optimal taxation with undiversifiable risk

ADEMU WORKING PAPER SERIES A unified framework for optimal taxation with undiversifiable risk Vasia Panousi Catarina Reis April 27 WP 27/64 www.ademu-project.eu/publications/working-papers Abstract This

ADEMU WORKING PAPER SERIES A unified framework for optimal taxation with undiversifiable risk Vasia Panousi Catarina Reis April 27 WP 27/64 www.ademu-project.eu/publications/working-papers Abstract This

Credit Market Competition and Liquidity Crises

Credit Market Competition and Liquidity Crises Elena Carletti Agnese Leonello European University Institute and CEPR University of Pennsylvania May 9, 2012 Motivation There is a long-standing debate on

Credit Market Competition and Liquidity Crises Elena Carletti Agnese Leonello European University Institute and CEPR University of Pennsylvania May 9, 2012 Motivation There is a long-standing debate on

Assessing the Impact of Central Bank Digital Currency on Private Banks

Assessing the Impact of Central Bank Digital Currency on Private Banks David Andolfatto Federal Reserve Bank of St. Louis CEU Budapest October 2018 Disclaimer The views expressed here are my own and should

Assessing the Impact of Central Bank Digital Currency on Private Banks David Andolfatto Federal Reserve Bank of St. Louis CEU Budapest October 2018 Disclaimer The views expressed here are my own and should

In Diamond-Dybvig, we see run equilibria in the optimal simple contract.

Ennis and Keister, "Run equilibria in the Green-Lin model of financial intermediation" Journal of Economic Theory 2009 In Diamond-Dybvig, we see run equilibria in the optimal simple contract. When the

Ennis and Keister, "Run equilibria in the Green-Lin model of financial intermediation" Journal of Economic Theory 2009 In Diamond-Dybvig, we see run equilibria in the optimal simple contract. When the

Essential Interest-Bearing Money

Essential Interest-Bearing Money David Andolfatto September 7, 2007 Abstract In this paper, I provide a rationale for why money should earn interest; or, what amounts to the same thing, why risk-free claims

Essential Interest-Bearing Money David Andolfatto September 7, 2007 Abstract In this paper, I provide a rationale for why money should earn interest; or, what amounts to the same thing, why risk-free claims

Expectations vs. Fundamentals-based Bank Runs: When should bailouts be permitted?

Expectations vs. Fundamentals-based Bank Runs: When should bailouts be permitted? Todd Keister Rutgers University Vijay Narasiman Harvard University October 2014 The question Is it desirable to restrict

Expectations vs. Fundamentals-based Bank Runs: When should bailouts be permitted? Todd Keister Rutgers University Vijay Narasiman Harvard University October 2014 The question Is it desirable to restrict

Models of Directed Search - Labor Market Dynamics, Optimal UI, and Student Credit

Models of Directed Search - Labor Market Dynamics, Optimal UI, and Student Credit Florian Hoffmann, UBC June 4-6, 2012 Markets Workshop, Chicago Fed Why Equilibrium Search Theory of Labor Market? Theory

Models of Directed Search - Labor Market Dynamics, Optimal UI, and Student Credit Florian Hoffmann, UBC June 4-6, 2012 Markets Workshop, Chicago Fed Why Equilibrium Search Theory of Labor Market? Theory

Banks and Liquidity Crises in an Emerging Economy

Banks and Liquidity Crises in an Emerging Economy Tarishi Matsuoka Abstract This paper presents and analyzes a simple model where banking crises can occur when domestic banks are internationally illiquid.

Banks and Liquidity Crises in an Emerging Economy Tarishi Matsuoka Abstract This paper presents and analyzes a simple model where banking crises can occur when domestic banks are internationally illiquid.

A Baseline Model: Diamond and Dybvig (1983)

") BANKING AND FINANCIAL FRAGILITY A Baseline Model: Diamond and Dybvig (1983) Professor Todd Keister Rutgers University May 2017 Objective Want to develop a model to help us understand: why banks and other

BANKING AND FINANCIAL FRAGILITY A Baseline Model: Diamond and Dybvig (1983) Professor Todd Keister Rutgers University May 2017 Objective Want to develop a model to help us understand: why banks and other

To sell or to borrow?

To sell or to borrow? A Theory of Bank Liquidity Management MichałKowalik FRB of Boston Disclaimer: The views expressed herein are those of the author and do not necessarily represent those of the Federal

To sell or to borrow? A Theory of Bank Liquidity Management MichałKowalik FRB of Boston Disclaimer: The views expressed herein are those of the author and do not necessarily represent those of the Federal

Central Bank Purchases of Private Assets

Central Bank Purchases of Private Assets Stephen D. Williamson Washington University in St. Louis Federal Reserve Banks of Richmond and St. Louis September 29, 2013 Abstract A model is constructed in which

Central Bank Purchases of Private Assets Stephen D. Williamson Washington University in St. Louis Federal Reserve Banks of Richmond and St. Louis September 29, 2013 Abstract A model is constructed in which

Sunspot Bank Runs and Fragility: The Role of Financial Sector Competition

Sunspot Bank Runs and Fragility: The Role of Financial Sector Competition Jiahong Gao Robert R. Reed August 9, 2018 Abstract What are the trade-offs between financial sector competition and fragility when

Sunspot Bank Runs and Fragility: The Role of Financial Sector Competition Jiahong Gao Robert R. Reed August 9, 2018 Abstract What are the trade-offs between financial sector competition and fragility when

A Tale of Fire-Sales and Liquidity Hoarding

University of Zurich Department of Economics Working Paper Series ISSN 1664-741 (print) ISSN 1664-75X (online) Working Paper No. 139 A Tale of Fire-Sales and Liquidity Hoarding Aleksander Berentsen and

University of Zurich Department of Economics Working Paper Series ISSN 1664-741 (print) ISSN 1664-75X (online) Working Paper No. 139 A Tale of Fire-Sales and Liquidity Hoarding Aleksander Berentsen and

Financial Fragility and the Exchange Rate Regime Chang and Velasco JET 2000 and NBER 6469

Financial Fragility and the Exchange Rate Regime Chang and Velasco JET 2000 and NBER 6469 1 Introduction and Motivation International illiquidity Country s consolidated nancial system has potential short-term

Financial Fragility and the Exchange Rate Regime Chang and Velasco JET 2000 and NBER 6469 1 Introduction and Motivation International illiquidity Country s consolidated nancial system has potential short-term

Bank Runs, Deposit Insurance, and Liquidity

Bank Runs, Deposit Insurance, and Liquidity Douglas W. Diamond University of Chicago Philip H. Dybvig Washington University in Saint Louis Washington University in Saint Louis August 13, 2015 Diamond,

Bank Runs, Deposit Insurance, and Liquidity Douglas W. Diamond University of Chicago Philip H. Dybvig Washington University in Saint Louis Washington University in Saint Louis August 13, 2015 Diamond,

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Comprehensive Examination: Macroeconomics Fall, 2016

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 2016 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements, state

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 2016 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements, state

Bailouts, Bail-ins and Banking Crises

Bailouts, Bail-ins and Banking Crises Todd Keister Rutgers University Yuliyan Mitkov Rutgers University & University of Bonn 2017 HKUST Workshop on Macroeconomics June 15, 2017 The bank runs problem Intermediaries

Bailouts, Bail-ins and Banking Crises Todd Keister Rutgers University Yuliyan Mitkov Rutgers University & University of Bonn 2017 HKUST Workshop on Macroeconomics June 15, 2017 The bank runs problem Intermediaries

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Preliminary Examination: Macroeconomics Spring, 2007

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Preliminary Examination: Macroeconomics Spring, 2007 Instructions: Read the questions carefully and make sure to show your work. You

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Preliminary Examination: Macroeconomics Spring, 2007 Instructions: Read the questions carefully and make sure to show your work. You

Discussion Liquidity requirements, liquidity choice and financial stability by Doug Diamond

Discussion Liquidity requirements, liquidity choice and financial stability by Doug Diamond Guillaume Plantin Sciences Po Plantin Liquidity requirements 1 / 23 The Diamond-Dybvig model Summary of the paper

Discussion Liquidity requirements, liquidity choice and financial stability by Doug Diamond Guillaume Plantin Sciences Po Plantin Liquidity requirements 1 / 23 The Diamond-Dybvig model Summary of the paper

Nominal Exchange Rates Obstfeld and Rogoff, Chapter 8

Nominal Exchange Rates Obstfeld and Rogoff, Chapter 8 1 Cagan Model of Money Demand 1.1 Money Demand Demand for real money balances ( M P ) depends negatively on expected inflation In logs m d t p t =

Nominal Exchange Rates Obstfeld and Rogoff, Chapter 8 1 Cagan Model of Money Demand 1.1 Money Demand Demand for real money balances ( M P ) depends negatively on expected inflation In logs m d t p t =

Bank Instability and Contagion

Money Market Funds Intermediation, Bank Instability and Contagion Marco Cipriani, Antoine Martin, Bruno M. Parigi Prepared for seminar at the Banque de France, Paris, December 2012 Preliminary and incomplete

Money Market Funds Intermediation, Bank Instability and Contagion Marco Cipriani, Antoine Martin, Bruno M. Parigi Prepared for seminar at the Banque de France, Paris, December 2012 Preliminary and incomplete

1 The Solow Growth Model

1 The Solow Growth Model The Solow growth model is constructed around 3 building blocks: 1. The aggregate production function: = ( ()) which it is assumed to satisfy a series of technical conditions: (a)

1 The Solow Growth Model The Solow growth model is constructed around 3 building blocks: 1. The aggregate production function: = ( ()) which it is assumed to satisfy a series of technical conditions: (a)

Problem set Fall 2012.

Problem set 1. 14.461 Fall 2012. Ivan Werning September 13, 2012 References: 1. Ljungqvist L., and Thomas J. Sargent (2000), Recursive Macroeconomic Theory, sections 17.2 for Problem 1,2. 2. Werning Ivan

Problem set 1. 14.461 Fall 2012. Ivan Werning September 13, 2012 References: 1. Ljungqvist L., and Thomas J. Sargent (2000), Recursive Macroeconomic Theory, sections 17.2 for Problem 1,2. 2. Werning Ivan

Monetary Policy with Asset-Backed Money

University of Zurich Department of Economics Working Paper Series ISSN 1664-7041 (print) ISSN 1664-705X (online) Working Paper No. 198 Monetary Policy with Asset-Backed Money David Andolfatto, Aleksander

University of Zurich Department of Economics Working Paper Series ISSN 1664-7041 (print) ISSN 1664-705X (online) Working Paper No. 198 Monetary Policy with Asset-Backed Money David Andolfatto, Aleksander

Bank Runs: The Pre-Deposit Game

Bank Runs: The Pre-Deposit Game Karl Shell Cornell University Yu Zhang Xiamen University July 31, 2017 We thank Huberto Ennis, Chao Gu, Todd Keister, and Jim Peck for their helpful comments. Corresponding

Bank Runs: The Pre-Deposit Game Karl Shell Cornell University Yu Zhang Xiamen University July 31, 2017 We thank Huberto Ennis, Chao Gu, Todd Keister, and Jim Peck for their helpful comments. Corresponding

Revision Lecture Microeconomics of Banking MSc Finance: Theory of Finance I MSc Economics: Financial Economics I

Revision Lecture Microeconomics of Banking MSc Finance: Theory of Finance I MSc Economics: Financial Economics I April 2005 PREPARING FOR THE EXAM What models do you need to study? All the models we studied

Revision Lecture Microeconomics of Banking MSc Finance: Theory of Finance I MSc Economics: Financial Economics I April 2005 PREPARING FOR THE EXAM What models do you need to study? All the models we studied

Maturity Transformation and Liquidity

Maturity Transformation and Liquidity Patrick Bolton, Tano Santos Columbia University and Jose Scheinkman Princeton University Motivation Main Question: Who is best placed to, 1. Transform Maturity 2.

Maturity Transformation and Liquidity Patrick Bolton, Tano Santos Columbia University and Jose Scheinkman Princeton University Motivation Main Question: Who is best placed to, 1. Transform Maturity 2.

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Comprehensive Examination: Macroeconomics Spring, 2016

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Spring, 2016 Section 1. Suggested Time: 45 Minutes) For 3 of the following 6 statements,

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Spring, 2016 Section 1. Suggested Time: 45 Minutes) For 3 of the following 6 statements,

A Diamond-Dybvig Model in which the Level of Deposits is Endogenous

A Diamond-Dybvig Model in which the Level of Deposits is Endogenous James Peck The Ohio State University A. Setayesh The Ohio State University January 28, 2019 Abstract We extend the Diamond-Dybvig model

A Diamond-Dybvig Model in which the Level of Deposits is Endogenous James Peck The Ohio State University A. Setayesh The Ohio State University January 28, 2019 Abstract We extend the Diamond-Dybvig model

Interest on Reserves, Interbank Lending, and Monetary Policy: Work in Progress

Interest on Reserves, Interbank Lending, and Monetary Policy: Work in Progress Stephen D. Williamson Federal Reserve Bank of St. Louis May 14, 015 1 Introduction When a central bank operates under a floor

Interest on Reserves, Interbank Lending, and Monetary Policy: Work in Progress Stephen D. Williamson Federal Reserve Bank of St. Louis May 14, 015 1 Introduction When a central bank operates under a floor

1 Dynamic programming

1 Dynamic programming A country has just discovered a natural resource which yields an income per period R measured in terms of traded goods. The cost of exploitation is negligible. The government wants

1 Dynamic programming A country has just discovered a natural resource which yields an income per period R measured in terms of traded goods. The cost of exploitation is negligible. The government wants

Bailouts, Bail-ins and Banking Crises

Bailouts, Bail-ins and Banking Crises Todd Keister Yuliyan Mitkov September 20, 206 We study the interaction between a government s bailout policy during a banking crisis and individual banks willingness

Bailouts, Bail-ins and Banking Crises Todd Keister Yuliyan Mitkov September 20, 206 We study the interaction between a government s bailout policy during a banking crisis and individual banks willingness

Sentiments and Aggregate Fluctuations

Sentiments and Aggregate Fluctuations Jess Benhabib Pengfei Wang Yi Wen June 15, 2012 Jess Benhabib Pengfei Wang Yi Wen () Sentiments and Aggregate Fluctuations June 15, 2012 1 / 59 Introduction We construct

Sentiments and Aggregate Fluctuations Jess Benhabib Pengfei Wang Yi Wen June 15, 2012 Jess Benhabib Pengfei Wang Yi Wen () Sentiments and Aggregate Fluctuations June 15, 2012 1 / 59 Introduction We construct

Optimal Negative Interest Rates in the Liquidity Trap

Optimal Negative Interest Rates in the Liquidity Trap Davide Porcellacchia 8 February 2017 Abstract The canonical New Keynesian model features a zero lower bound on the interest rate. In the simple setting

Optimal Negative Interest Rates in the Liquidity Trap Davide Porcellacchia 8 February 2017 Abstract The canonical New Keynesian model features a zero lower bound on the interest rate. In the simple setting

Consumption and Asset Pricing

Consumption and Asset Pricing Yin-Chi Wang The Chinese University of Hong Kong November, 2012 References: Williamson s lecture notes (2006) ch5 and ch 6 Further references: Stochastic dynamic programming:

Consumption and Asset Pricing Yin-Chi Wang The Chinese University of Hong Kong November, 2012 References: Williamson s lecture notes (2006) ch5 and ch 6 Further references: Stochastic dynamic programming:

A model to help guide monetary (and fiscal) policy-making that isn t a sticky-price Ricardian cashless NK model. David Andolfatto

policy-making that isn t a sticky-price Ricardian cashless NK model. David Andolfatto") A model to help guide monetary (and fiscal) policy-making that isn t a sticky-price Ricardian cashless NK model David Andolfatto Overlapping generations model Two types of young, workers and investors.

A model to help guide monetary (and fiscal) policy-making that isn t a sticky-price Ricardian cashless NK model David Andolfatto Overlapping generations model Two types of young, workers and investors.

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Comprehensive Examination: Macroeconomics Fall, 2010

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 2010 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements, state

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 2010 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements, state

Experimental Evidence of Bank Runs as Pure Coordination Failures

Experimental Evidence of Bank Runs as Pure Coordination Failures Jasmina Arifovic (Simon Fraser) Janet Hua Jiang (Bank of Canada and U of Manitoba) Yiping Xu (U of International Business and Economics)

Experimental Evidence of Bank Runs as Pure Coordination Failures Jasmina Arifovic (Simon Fraser) Janet Hua Jiang (Bank of Canada and U of Manitoba) Yiping Xu (U of International Business and Economics)

Financial Fragility A Global-Games Approach Itay Goldstein Wharton School, University of Pennsylvania

Financial Fragility A Global-Games Approach Itay Goldstein Wharton School, University of Pennsylvania Financial Fragility and Coordination Failures What makes financial systems fragile? What causes crises

Financial Fragility A Global-Games Approach Itay Goldstein Wharton School, University of Pennsylvania Financial Fragility and Coordination Failures What makes financial systems fragile? What causes crises

Liquidity and Solvency Risks

Liquidity and Solvency Risks Armin Eder a Falko Fecht b Thilo Pausch c a Universität Innsbruck, b European Business School, c Deutsche Bundesbank WebEx-Presentation February 25, 2011 Eder, Fecht, Pausch

Liquidity and Solvency Risks Armin Eder a Falko Fecht b Thilo Pausch c a Universität Innsbruck, b European Business School, c Deutsche Bundesbank WebEx-Presentation February 25, 2011 Eder, Fecht, Pausch

Central Bank Purchases of Private Assets

Central Bank Purchases of Private Assets Stephen D. Williamson Federal Reserve Bank of St. Louis Washington University in St. Louis July 30, 2014 Abstract A model is constructed in which consumers and

Central Bank Purchases of Private Assets Stephen D. Williamson Federal Reserve Bank of St. Louis Washington University in St. Louis July 30, 2014 Abstract A model is constructed in which consumers and

Supplement to the lecture on the Diamond-Dybvig model

ECON 4335 Economics of Banking, Fall 2016 Jacopo Bizzotto 1 Supplement to the lecture on the Diamond-Dybvig model The model in Diamond and Dybvig (1983) incorporates important features of the real world:

ECON 4335 Economics of Banking, Fall 2016 Jacopo Bizzotto 1 Supplement to the lecture on the Diamond-Dybvig model The model in Diamond and Dybvig (1983) incorporates important features of the real world:

Exam Fall 2004 Prof.: Ricardo J. Caballero

Exam 14.454 Fall 2004 Prof.: Ricardo J. Caballero Question #1 -- Simple Labor Market Search Model (20 pts) Assume that the labor market is described by the following model. Population is normalized to

Exam 14.454 Fall 2004 Prof.: Ricardo J. Caballero Question #1 -- Simple Labor Market Search Model (20 pts) Assume that the labor market is described by the following model. Population is normalized to

Estimating a Dynamic Oligopolistic Game with Serially Correlated Unobserved Production Costs. SS223B-Empirical IO

Estimating a Dynamic Oligopolistic Game with Serially Correlated Unobserved Production Costs SS223B-Empirical IO Motivation There have been substantial recent developments in the empirical literature on

Estimating a Dynamic Oligopolistic Game with Serially Correlated Unobserved Production Costs SS223B-Empirical IO Motivation There have been substantial recent developments in the empirical literature on

Inflation & Welfare 1

1 INFLATION & WELFARE ROBERT E. LUCAS 2 Introduction In a monetary economy, private interest is to hold not non-interest bearing cash. Individual efforts due to this incentive must cancel out, because

1 INFLATION & WELFARE ROBERT E. LUCAS 2 Introduction In a monetary economy, private interest is to hold not non-interest bearing cash. Individual efforts due to this incentive must cancel out, because

Monetary and Financial Macroeconomics

Monetary and Financial Macroeconomics Hernán D. Seoane Universidad Carlos III de Madrid Introduction Last couple of weeks we introduce banks in our economies Financial intermediation arises naturally when

Monetary and Financial Macroeconomics Hernán D. Seoane Universidad Carlos III de Madrid Introduction Last couple of weeks we introduce banks in our economies Financial intermediation arises naturally when

Essential interest-bearing money

Essential interest-bearing money David Andolfatto Federal Reserve Bank of St. Louis, Research Division, P.O. Box 442, St. Louis, MO 63166-0422, USA and Department of Economics, Simon Fraser University,

Essential interest-bearing money David Andolfatto Federal Reserve Bank of St. Louis, Research Division, P.O. Box 442, St. Louis, MO 63166-0422, USA and Department of Economics, Simon Fraser University,

Low Real Interest Rates and the Zero Lower Bound

Low Real Interest Rates and the Zero Lower Bound Stephen D. Williamson Federal Reserve Bank of St. Louis October 2016 Abstract How do low real interest rates constrain monetary policy? Is the zero lower

Low Real Interest Rates and the Zero Lower Bound Stephen D. Williamson Federal Reserve Bank of St. Louis October 2016 Abstract How do low real interest rates constrain monetary policy? Is the zero lower

1 No capital mobility

University of British Columbia Department of Economics, International Finance (Econ 556) Prof. Amartya Lahiri Handout #7 1 1 No capital mobility In the previous lecture we studied the frictionless environment

University of British Columbia Department of Economics, International Finance (Econ 556) Prof. Amartya Lahiri Handout #7 1 1 No capital mobility In the previous lecture we studied the frictionless environment

Banks and Liquidity Crises in Emerging Market Economies

Banks and Liquidity Crises in Emerging Market Economies Tarishi Matsuoka April 17, 2015 Abstract This paper presents and analyzes a simple banking model in which banks have access to international capital

Banks and Liquidity Crises in Emerging Market Economies Tarishi Matsuoka April 17, 2015 Abstract This paper presents and analyzes a simple banking model in which banks have access to international capital

Economic Growth: Lecture 11, Human Capital, Technology Diffusion and Interdependencies

14.452 Economic Growth: Lecture 11, Human Capital, Technology Diffusion and Interdependencies Daron Acemoglu MIT December 1, 2009. Daron Acemoglu (MIT) Economic Growth Lecture 11 December 1, 2009. 1 /

14.452 Economic Growth: Lecture 11, Human Capital, Technology Diffusion and Interdependencies Daron Acemoglu MIT December 1, 2009. Daron Acemoglu (MIT) Economic Growth Lecture 11 December 1, 2009. 1 /

Liquidity, Monetary Policy, and the Financial Crisis: A New Monetarist Approach

Liquidity, Monetary Policy, and the Financial Crisis: A New Monetarist Approach By STEPHEN D. WILLIAMSON A model of public and private liquidity is constructed that integrates financial intermediation

Liquidity, Monetary Policy, and the Financial Crisis: A New Monetarist Approach By STEPHEN D. WILLIAMSON A model of public and private liquidity is constructed that integrates financial intermediation

Regulatory Arbitrage and Systemic Liquidity Crises

Regulatory Arbitrage and Systemic Liquidity Crises Stephan Luck & Paul Schempp Princeton University and MPI for Research on Collective Goods Federal Reserve Bank of Atlanta The Role of Liquidity in the

Regulatory Arbitrage and Systemic Liquidity Crises Stephan Luck & Paul Schempp Princeton University and MPI for Research on Collective Goods Federal Reserve Bank of Atlanta The Role of Liquidity in the

Appendix: Common Currencies vs. Monetary Independence

Appendix: Common Currencies vs. Monetary Independence A The infinite horizon model This section defines the equilibrium of the infinity horizon model described in Section III of the paper and characterizes

Appendix: Common Currencies vs. Monetary Independence A The infinite horizon model This section defines the equilibrium of the infinity horizon model described in Section III of the paper and characterizes

Working Paper Series. Rehypothecation and Liquidity. David Andolfatto Fernando Martin and Shengxing Zhang

RESEARCH DIVISION Working Paper Series Rehypothecation and Liquidity David Andolfatto Fernando Martin and Shengxing Zhang Working Paper 2015-003D https://doi.org/10.20955/wp.2015.003 July 2017 FEDERAL

RESEARCH DIVISION Working Paper Series Rehypothecation and Liquidity David Andolfatto Fernando Martin and Shengxing Zhang Working Paper 2015-003D https://doi.org/10.20955/wp.2015.003 July 2017 FEDERAL

ADVANCED MACROECONOMIC TECHNIQUES NOTE 7b

316-406 ADVANCED MACROECONOMIC TECHNIQUES NOTE 7b Chris Edmond hcpedmond@unimelb.edu.aui Aiyagari s model Arguably the most popular example of a simple incomplete markets model is due to Rao Aiyagari (1994,

316-406 ADVANCED MACROECONOMIC TECHNIQUES NOTE 7b Chris Edmond hcpedmond@unimelb.edu.aui Aiyagari s model Arguably the most popular example of a simple incomplete markets model is due to Rao Aiyagari (1994,

Monetary Economics: Problem Set #6 Solutions

Monetary Economics Problem Set #6 Monetary Economics: Problem Set #6 Solutions This problem set is marked out of 00 points. The weight given to each part is indicated below. Please contact me asap if you

Monetary Economics Problem Set #6 Monetary Economics: Problem Set #6 Solutions This problem set is marked out of 00 points. The weight given to each part is indicated below. Please contact me asap if you

Chapter 8 Liquidity and Financial Intermediation

Chapter 8 Liquidity and Financial Intermediation Main Aims: 1. Study money as a liquid asset. 2. Develop an OLG model in which individuals live for three periods. 3. Analyze two roles of banks: (1.) correcting

Chapter 8 Liquidity and Financial Intermediation Main Aims: 1. Study money as a liquid asset. 2. Develop an OLG model in which individuals live for three periods. 3. Analyze two roles of banks: (1.) correcting

Money, Output, and the Nominal National Debt. Bruce Champ and Scott Freeman (AER 1990)

") Money, Output, and the Nominal National Debt Bruce Champ and Scott Freeman (AER 1990) OLG model Diamond (1965) version of Samuelson (1958) OLG model Let = 1 population of young Representative young agent

Money, Output, and the Nominal National Debt Bruce Champ and Scott Freeman (AER 1990) OLG model Diamond (1965) version of Samuelson (1958) OLG model Let = 1 population of young Representative young agent

Fiscal and Monetary Policies: Background

Fiscal and Monetary Policies: Background Behzad Diba University of Bern April 2012 (Institute) Fiscal and Monetary Policies: Background April 2012 1 / 19 Research Areas Research on fiscal policy typically

Fiscal and Monetary Policies: Background Behzad Diba University of Bern April 2012 (Institute) Fiscal and Monetary Policies: Background April 2012 1 / 19 Research Areas Research on fiscal policy typically

Keynesian Inefficiency and Optimal Policy: A New Monetarist Approach

Keynesian Inefficiency and Optimal Policy: A New Monetarist Approach Stephen D. Williamson Washington University in St. Louis Federal Reserve Banks of Richmond and St. Louis May 29, 2013 Abstract A simple

Keynesian Inefficiency and Optimal Policy: A New Monetarist Approach Stephen D. Williamson Washington University in St. Louis Federal Reserve Banks of Richmond and St. Louis May 29, 2013 Abstract A simple

Money Inventories in Search Equilibrium

MPRA Munich Personal RePEc Archive Money Inventories in Search Equilibrium Aleksander Berentsen University of Basel 1. January 1998 Online at https://mpra.ub.uni-muenchen.de/68579/ MPRA Paper No. 68579,

MPRA Munich Personal RePEc Archive Money Inventories in Search Equilibrium Aleksander Berentsen University of Basel 1. January 1998 Online at https://mpra.ub.uni-muenchen.de/68579/ MPRA Paper No. 68579,

Lastrapes Fall y t = ỹ + a 1 (p t p t ) y t = d 0 + d 1 (m t p t ).

y t = d 0 + d 1 (m t p t ).") ECON 8040 Final exam Lastrapes Fall 2007 Answer all eight questions on this exam. 1. Write out a static model of the macroeconomy that is capable of predicting that money is non-neutral. Your model should

ECON 8040 Final exam Lastrapes Fall 2007 Answer all eight questions on this exam. 1. Write out a static model of the macroeconomy that is capable of predicting that money is non-neutral. Your model should

Payments, Credit & Asset Prices

Payments, Credit & Asset Prices Monika Piazzesi Stanford & NBER Martin Schneider Stanford & NBER CITE August 13, 2015 Piazzesi & Schneider Payments, Credit & Asset Prices CITE August 13, 2015 1 / 31 Dollar

Payments, Credit & Asset Prices Monika Piazzesi Stanford & NBER Martin Schneider Stanford & NBER CITE August 13, 2015 Piazzesi & Schneider Payments, Credit & Asset Prices CITE August 13, 2015 1 / 31 Dollar

Liquidity Regulation and Unintended Financial Transformation in China

Liquidity Regulation and Unintended Financial Transformation in China Kinda Cheryl Hachem Zheng (Michael) Song Chicago Booth Chinese University of Hong Kong First Research Workshop on China s Economy April

Liquidity Regulation and Unintended Financial Transformation in China Kinda Cheryl Hachem Zheng (Michael) Song Chicago Booth Chinese University of Hong Kong First Research Workshop on China s Economy April

Bailouts, Bail-ins and Banking Crises

Bailouts, Bail-ins and Banking Crises Todd Keister Rutgers University todd.keister@rutgers.edu Yuliyan Mitkov Rutgers University ymitkov@economics.rutgers.edu June 11, 2017 We study the interaction between

Bailouts, Bail-ins and Banking Crises Todd Keister Rutgers University todd.keister@rutgers.edu Yuliyan Mitkov Rutgers University ymitkov@economics.rutgers.edu June 11, 2017 We study the interaction between

Public Information and Effi cient Capital Investments: Implications for the Cost of Capital and Firm Values

Public Information and Effi cient Capital Investments: Implications for the Cost of Capital and Firm Values P O. C Department of Finance Copenhagen Business School, Denmark H F Department of Accounting

Public Information and Effi cient Capital Investments: Implications for the Cost of Capital and Firm Values P O. C Department of Finance Copenhagen Business School, Denmark H F Department of Accounting

MFE Macroeconomics Week 8 Exercises

MFE Macroeconomics Week 8 Exercises 1 Liquidity shocks over a unit interval A representative consumer in a Diamond-Dybvig model has wealth 1 at date 0. They will need liquidity to consume at a random time

MFE Macroeconomics Week 8 Exercises 1 Liquidity shocks over a unit interval A representative consumer in a Diamond-Dybvig model has wealth 1 at date 0. They will need liquidity to consume at a random time

Deposits and Bank Capital Structure

Deposits and Bank Capital Structure Franklin Allen 1 Elena Carletti 2 Robert Marquez 3 1 University of Pennsylvania 2 Bocconi University 3 UC Davis June 2014 Franklin Allen, Elena Carletti, Robert Marquez

Deposits and Bank Capital Structure Franklin Allen 1 Elena Carletti 2 Robert Marquez 3 1 University of Pennsylvania 2 Bocconi University 3 UC Davis June 2014 Franklin Allen, Elena Carletti, Robert Marquez

Bank Leverage and Social Welfare

Bank Leverage and Social Welfare By LAWRENCE CHRISTIANO AND DAISUKE IKEDA We describe a general equilibrium model in which there is a particular agency problem in banks. The agency problem arises because

Bank Leverage and Social Welfare By LAWRENCE CHRISTIANO AND DAISUKE IKEDA We describe a general equilibrium model in which there is a particular agency problem in banks. The agency problem arises because

International Journal of Economic Theory

doi: 10.1111/ijet.108 International Journal of Economic Theory On sunspots, bank runs, and Glass Steagall Karl Shell and Yu Zhang We analyze the pre-deposit game in a two-depositor banking model. The Glass

doi: 10.1111/ijet.108 International Journal of Economic Theory On sunspots, bank runs, and Glass Steagall Karl Shell and Yu Zhang We analyze the pre-deposit game in a two-depositor banking model. The Glass

PhD Qualifier Examination

PhD Qualifier Examination Department of Agricultural Economics May 29, 2015 Instructions This exam consists of six questions. You must answer all questions. If you need an assumption to complete a question,

PhD Qualifier Examination Department of Agricultural Economics May 29, 2015 Instructions This exam consists of six questions. You must answer all questions. If you need an assumption to complete a question,

The Societal Benefit of a Financial Transaction Tax

University of Zurich Department of Economics Working Paper Series ISSN 1664-7041 (print) ISSN 1664-705X (online) Working Paper No. 176 The Societal Benefit of a Financial Transaction Tax Aleksander Berentsen,

University of Zurich Department of Economics Working Paper Series ISSN 1664-7041 (print) ISSN 1664-705X (online) Working Paper No. 176 The Societal Benefit of a Financial Transaction Tax Aleksander Berentsen,

Chapter 6. Endogenous Growth I: AK, H, and G

Chapter 6 Endogenous Growth I: AK, H, and G 195 6.1 The Simple AK Model Economic Growth: Lecture Notes 6.1.1 Pareto Allocations Total output in the economy is given by Y t = F (K t, L t ) = AK t, where

Chapter 6 Endogenous Growth I: AK, H, and G 195 6.1 The Simple AK Model Economic Growth: Lecture Notes 6.1.1 Pareto Allocations Total output in the economy is given by Y t = F (K t, L t ) = AK t, where

Sentiments and Aggregate Fluctuations

Sentiments and Aggregate Fluctuations Jess Benhabib Pengfei Wang Yi Wen March 15, 2013 Jess Benhabib Pengfei Wang Yi Wen () Sentiments and Aggregate Fluctuations March 15, 2013 1 / 60 Introduction The

Sentiments and Aggregate Fluctuations Jess Benhabib Pengfei Wang Yi Wen March 15, 2013 Jess Benhabib Pengfei Wang Yi Wen () Sentiments and Aggregate Fluctuations March 15, 2013 1 / 60 Introduction The

Inflation. David Andolfatto

Inflation David Andolfatto Introduction We continue to assume an economy with a single asset Assume that the government can manage the supply of over time; i.e., = 1,where 0 is the gross rate of money

Inflation David Andolfatto Introduction We continue to assume an economy with a single asset Assume that the government can manage the supply of over time; i.e., = 1,where 0 is the gross rate of money

Foreign Competition and Banking Industry Dynamics: An Application to Mexico

Foreign Competition and Banking Industry Dynamics: An Application to Mexico Dean Corbae Pablo D Erasmo 1 Univ. of Wisconsin FRB Philadelphia June 12, 2014 1 The views expressed here do not necessarily

Foreign Competition and Banking Industry Dynamics: An Application to Mexico Dean Corbae Pablo D Erasmo 1 Univ. of Wisconsin FRB Philadelphia June 12, 2014 1 The views expressed here do not necessarily

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Comprehensive Examination: Macroeconomics Spring, 2009

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Spring, 2009 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements,

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Spring, 2009 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements,

Credit Booms, Financial Crises and Macroprudential Policy

Credit Booms, Financial Crises and Macroprudential Policy Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 219 1 The views expressed in this paper are those

Credit Booms, Financial Crises and Macroprudential Policy Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 219 1 The views expressed in this paper are those

Pseudo-Wealth Fluctuations and Aggregate Demand Effects

Pseudo-Wealth Fluctuations and Aggregate Demand Effects American Economic Association, Boston Martin M. Guzman Joseph E. Stiglitz January 5, 2015 Motivation Two analytical puzzles from the perspective

Pseudo-Wealth Fluctuations and Aggregate Demand Effects American Economic Association, Boston Martin M. Guzman Joseph E. Stiglitz January 5, 2015 Motivation Two analytical puzzles from the perspective

ACTIVE FISCAL, PASSIVE MONEY EQUILIBRIUM IN A PURELY BACKWARD-LOOKING MODEL

ACTIVE FISCAL, PASSIVE MONEY EQUILIBRIUM IN A PURELY BACKWARD-LOOKING MODEL CHRISTOPHER A. SIMS ABSTRACT. The active money, passive fiscal policy equilibrium that the fiscal theory of the price level shows

ACTIVE FISCAL, PASSIVE MONEY EQUILIBRIUM IN A PURELY BACKWARD-LOOKING MODEL CHRISTOPHER A. SIMS ABSTRACT. The active money, passive fiscal policy equilibrium that the fiscal theory of the price level shows

Monetary Fiscal Policy Interactions under Implementable Monetary Policy Rules

WILLIAM A. BRANCH TROY DAVIG BRUCE MCGOUGH Monetary Fiscal Policy Interactions under Implementable Monetary Policy Rules This paper examines the implications of forward- and backward-looking monetary policy

WILLIAM A. BRANCH TROY DAVIG BRUCE MCGOUGH Monetary Fiscal Policy Interactions under Implementable Monetary Policy Rules This paper examines the implications of forward- and backward-looking monetary policy

Solutions to Problem Set 1

Solutions to Problem Set Theory of Banking - Academic Year 06-7 Maria Bachelet maria.jua.bachelet@gmail.com February 4, 07 Exercise. An individual consumer has an income stream (Y 0, Y ) and can borrow

Solutions to Problem Set Theory of Banking - Academic Year 06-7 Maria Bachelet maria.jua.bachelet@gmail.com February 4, 07 Exercise. An individual consumer has an income stream (Y 0, Y ) and can borrow

ECON 4325 Monetary Policy and Business Fluctuations

ECON 4325 Monetary Policy and Business Fluctuations Tommy Sveen Norges Bank January 28, 2009 TS (NB) ECON 4325 January 28, 2009 / 35 Introduction A simple model of a classical monetary economy. Perfect

ECON 4325 Monetary Policy and Business Fluctuations Tommy Sveen Norges Bank January 28, 2009 TS (NB) ECON 4325 January 28, 2009 / 35 Introduction A simple model of a classical monetary economy. Perfect

General Examination in Macroeconomic Theory SPRING 2016

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory SPRING 2016 You have FOUR hours. Answer all questions Part A (Prof. Laibson): 60 minutes Part B (Prof. Barro): 60

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory SPRING 2016 You have FOUR hours. Answer all questions Part A (Prof. Laibson): 60 minutes Part B (Prof. Barro): 60

Multitask, Accountability, and Institutional Design

Multitask, Accountability, and Institutional Design Scott Ashworth & Ethan Bueno de Mesquita Harris School of Public Policy Studies University of Chicago 1 / 32 Motivation Multiple executive tasks divided

Multitask, Accountability, and Institutional Design Scott Ashworth & Ethan Bueno de Mesquita Harris School of Public Policy Studies University of Chicago 1 / 32 Motivation Multiple executive tasks divided

MACROECONOMICS. Prelim Exam

MACROECONOMICS Prelim Exam Austin, June 1, 2012 Instructions This is a closed book exam. If you get stuck in one section move to the next one. Do not waste time on sections that you find hard to solve.

MACROECONOMICS Prelim Exam Austin, June 1, 2012 Instructions This is a closed book exam. If you get stuck in one section move to the next one. Do not waste time on sections that you find hard to solve.

The Dire Effects of the Lack of Monetary and Fiscal Coordination 1

The Dire Effects of the Lack of Monetary and Fiscal Coordination 1 Francesco Bianchi and Leonardo Melosi Duke University and FRB of Chicago The views in this paper are solely the responsibility of the

The Dire Effects of the Lack of Monetary and Fiscal Coordination 1 Francesco Bianchi and Leonardo Melosi Duke University and FRB of Chicago The views in this paper are solely the responsibility of the

A key characteristic of financial markets is that they are subject to sudden, convulsive changes.

10.6 The Diamond-Dybvig Model A key characteristic of financial markets is that they are subject to sudden, convulsive changes. Such changes happen at both the microeconomic and macroeconomic levels. At

10.6 The Diamond-Dybvig Model A key characteristic of financial markets is that they are subject to sudden, convulsive changes. Such changes happen at both the microeconomic and macroeconomic levels. At

Currency and Checking Deposits as Means of Payment

Currency and Checking Deposits as Means of Payment Yiting Li December 2008 Abstract We consider a record keeping cost to distinguish checking deposits from currency in a model where means-of-payment decisions

Currency and Checking Deposits as Means of Payment Yiting Li December 2008 Abstract We consider a record keeping cost to distinguish checking deposits from currency in a model where means-of-payment decisions

Monetary Economics. Chapter 5: Properties of Money. Prof. Aleksander Berentsen. University of Basel

Monetary Economics Chapter 5: Properties of Money Prof. Aleksander Berentsen University of Basel Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 5 1 / 40 Structure of this chapter

Monetary Economics Chapter 5: Properties of Money Prof. Aleksander Berentsen University of Basel Ed Nosal and Guillaume Rocheteau Money, Payments, and Liquidity - Chapter 5 1 / 40 Structure of this chapter

Essential Interest-Bearing Money (2008)

") MPRA Munich Personal RePEc Archive Essential Interest-Bearing Money (2008) David Andolfatto Simon Fraser University 3. May 2008 Online at http://mpra.ub.uni-muenchen.de/8565/ MPRA Paper No. 8565, posted

MPRA Munich Personal RePEc Archive Essential Interest-Bearing Money (2008) David Andolfatto Simon Fraser University 3. May 2008 Online at http://mpra.ub.uni-muenchen.de/8565/ MPRA Paper No. 8565, posted

Interest Rates and Currency Prices in a Two-Country World. Robert E. Lucas, Jr. 1982

Interest Rates and Currency Prices in a Two-Country World Robert E. Lucas, Jr. 1982 Contribution Integrates domestic and international monetary theory with financial economics to provide a complete theory

Interest Rates and Currency Prices in a Two-Country World Robert E. Lucas, Jr. 1982 Contribution Integrates domestic and international monetary theory with financial economics to provide a complete theory

Research Division Federal Reserve Bank of St. Louis Working Paper Series

Research Division Federal Reserve Bank of St. Louis Working Paper Series Scarce Collateral, the Term Premium, and Quantitative Easing Stephen D. Williamson Working Paper 2014-008A http://research.stlouisfed.org/wp/2014/2014-008.pdf

Research Division Federal Reserve Bank of St. Louis Working Paper Series Scarce Collateral, the Term Premium, and Quantitative Easing Stephen D. Williamson Working Paper 2014-008A http://research.stlouisfed.org/wp/2014/2014-008.pdf