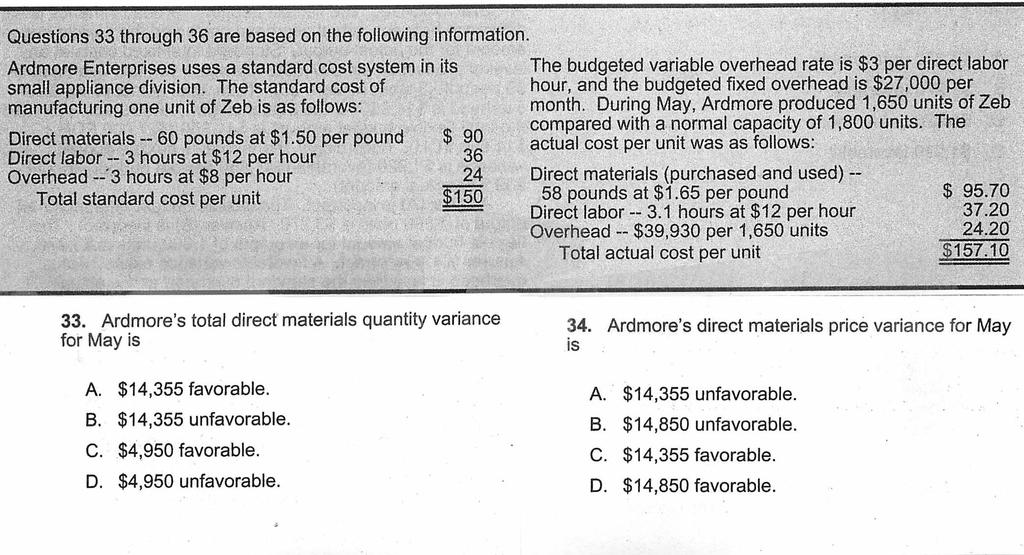

Part 1 Study Unit 10. Cost And Variance Measures. By Ronald Schmidt, CMA, CFM

|

|

|

- Whitney Blake

- 5 years ago

- Views:

Transcription

1 Part 1 Study Unit 10 Cost And Variance Measures By Ronald Schmidt, CMA, CFM

2 Variance Analysis and overview A budget communicates to employees the organization s operational and strategic objectives Considerations: Evaluations system must be used to monitor progress Feedback must be timely

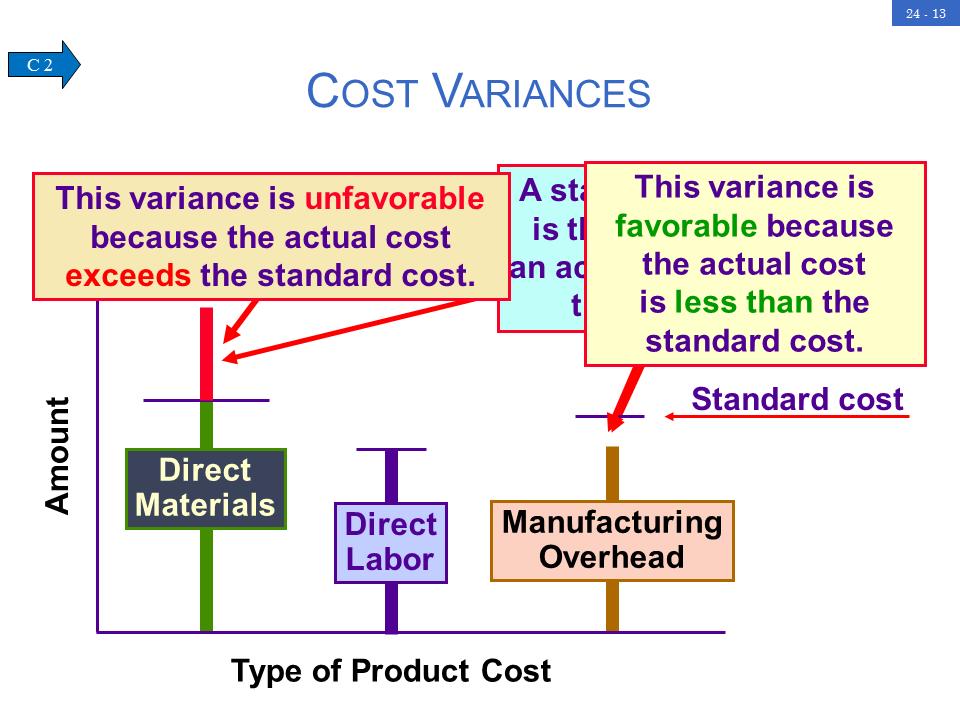

3 Variance Analysis and overview Variance analysis is the basis of any performance evaluation system. On the cost side, a favorable variance occurs when actual costs are less than standard costs. An unfavorable variance occurs when actual costs are greater than standard costs. On the revenue side, a favorable variance occurs when actual revenues are greater than budgeted revenues. An unfavorable variance occurs when actual revenues are less than budgeted revenues.

4 Variance Analysis and overview The significance of variances depends not only on their amount but also on their direction, frequency, and trend. It enables management by exception the practice of giving attention primarily to significant deviations from expectations. Assignment of responsibility = Budget owner Cost centers = cost drivers = controllable costs Allocation / indirect costs Crucial part of variance analysis is the assignment of responsibility to those most likely to have information that will help find solutions. Constructive approach is to promote learning and continuous in manufacturing, not to assign blame.

5 Variance Analysis overview Objectives of the budget: performance? Budget vs. Actual, evaluate the trend, and develop a rolling Forecast

6

7

8

9

10

11 Flexible budget and sales-volume variance Static budget = flexible budget and sales volume variance Flexible budget variance Diff. between the actual results and the budgeted amount for the actual activity level. The costs that should have been incurred given the actual level of production. The actual level of production is based on the actual output while still using the standard level of inputs. Variance could be due to: Selling Price Input costs Input quantities

12 Flexible budget and sales-volume variance The sales-volume variance is the difference between the flexible budget and static budget amounts if selling prices and costs are constant.

13 Flexible budget and sales-volume See page 343 variance ACTUAL RESULTS = ACTUAL INPUTS x ACTUAL PRICE FLEXIBLE BUDGET = ACTUAL INPUTS x STANDARD PRICE STATIC BUDGET = BUDGETED INPUTS x STANDARD PRICE

14 SU 10.1 Practice Question 1 The purpose of identifying manufacturing variances and assigning their responsibility to a person/department should be to A B C D Use the knowledge about the variances to promote learning and continuous improvement in the manufacturing operations. Trace the variances to finished goods so that the inventory can be properly valued at year-end. Determine the proper cost of the products produced so that selling prices can be adjusted accordingly. Pinpoint fault for operating problems in the organization.

15 SU 10.1 Practice Question 1 Answer Correct Answer: A The purpose of identifying and assigning responsibility for variances is to determine who is likely to have information that will enable management to find solutions. The constructive approach is to promote learning and continuous improvement in manufacturing operations, not to assign blame. However, information about variances may be useful in evaluating managers performance.

16 SU 10.1 Practice Question 2 A difference between standard costs used for cost control and the budgeted costs of the same manufacturing effort can exist because A B C D Standard costs represent what costs should be, whereas budgeted costs are expected actual costs. Budgeted costs are historical costs, whereas standard costs are based on engineering studies. Budgeted costs include some slack, whereas standard costs do not. Standard costs include some slack, whereas budgeted costs do not.

17 SU 10.1 Practice Question 2 Answer Correct Answer: A In the long run, these costs should be the same. In the short run, however, they may differ because standard costs represent what costs should be, whereas budgeted costs are expected actual costs. Budgeted costs may vary widely from standard costs in certain months, but, for an annual budget period, the amounts should be similar.

18 SU 10.1 Practice Question 3 The controller of a company holds a monthly meeting where any department that has a 10% unfavorable variance to budget must explain the variance and develop a plan to remedy the situation. This is an example of A Activity-based management. B Cost management. C Continuous improvement. D Management by exception.

19 SU 10.1 Practice Question 3 Answer Correct Answer: D Variance analysis is an important tool for the management accountant. It enables management by exception, which is the practice of giving attention primarily to significant deviations from expectations. Managers must use their judgment to determine the most efficient use of their limited time. Concentrating on operations that are not performing within expected limits is likely to yield the best ratio of benefits to costs.

20

21

22

23

24

25 Remember Flexible budget = Actual level of production x standard costs

26

27 Components of the flexible Budget DM variance Price variance Quantity or usage variance Materials mix variance / yield variance DL variance Rate variance Efficiency variance Labor mix variance / yield variance MOH variance (By Jim Clemons) 4 way analysis VOH spending variance VOH efficiency variance FOH spending variance (budget variance) FOH production-volume variance

28

29

30 Flexible budget Remember a flexible budget adjusts for changes in the volume of activity. It can be adapted to any level of production. Flexible budget variances result from variations in the efficiency and effectiveness of producing actual output. They are the differences between actual results and flexible budget amounts. See example on page 343

31 SU 10.2 Question 1 A manufacturing firm planned to manufacture and sell 100,000 units of product during the year at a variable cost per unit of $4.00 and a fixed cost per unit of $2.00. The firm fell short of its goal and only manufactured 80,000 units at a total incurred cost of $515,000. The firm s manufacturing cost variance was A. $85,000 favorable. B. $35,000 unfavorable. C. $5,000 favorable. D. $5,000 unfavorable.

32 SU 10.2 Question 1 Answer Correct Answer: C The company planned to produce 100,000 units at $6 each ($4 variable + $2 fixed cost), or a total of $600,000, consisting of $400,000 of variable costs and $200,000 of fixed costs. Total production was only 80,000 units at a total cost of $515,000. The flexible budget for a production level of 80,000 units includes variable costs of $320,000 (80,000 units $4). Fixed costs would remain at $200,000. Thus, the total flexible budget costs are $520,000. Given that actual costs were only $515,000, the variance is $5,000 favorable.

33 SU 10.2 Question 2 To monitor total cost, total revenue, and net profit based upon production levels, a manager should use A. B. C. Both flexible budgeting and standard costing. Static budgeting but not standard costing. Standard costing but not flexible budgeting. D. Static budgeting and standard costing.

34 SU 10.2 Question 2 Answer Correct Answer: A A flexible budget is a set of static budgets prepared in anticipation of varying levels of activity. Unlike a static budget, the use of a flexible budget permits effective evaluation of actual results when actual and expected production differ. Setting cost standards facilitates preparation of a flexible budget. For example, a standard unit variable cost is useful in determining the total variable cost for a given output.

35

36

37

38 DM / DL variances DL rate variance AQ x (AP SP) DL efficiency variance SP x (AQ SQ) Mix and yield variances Substitutable products Weighted average standard price Standard mix of inputs (SPSM) Actual mix of inputs (SPAM) Mix variance = ATQ x (SPSM SPAM) Yield variance = (STQ ATQ) x SPSM MIX + YIELD variances = EFFICIENCY variance

39

40

41

42

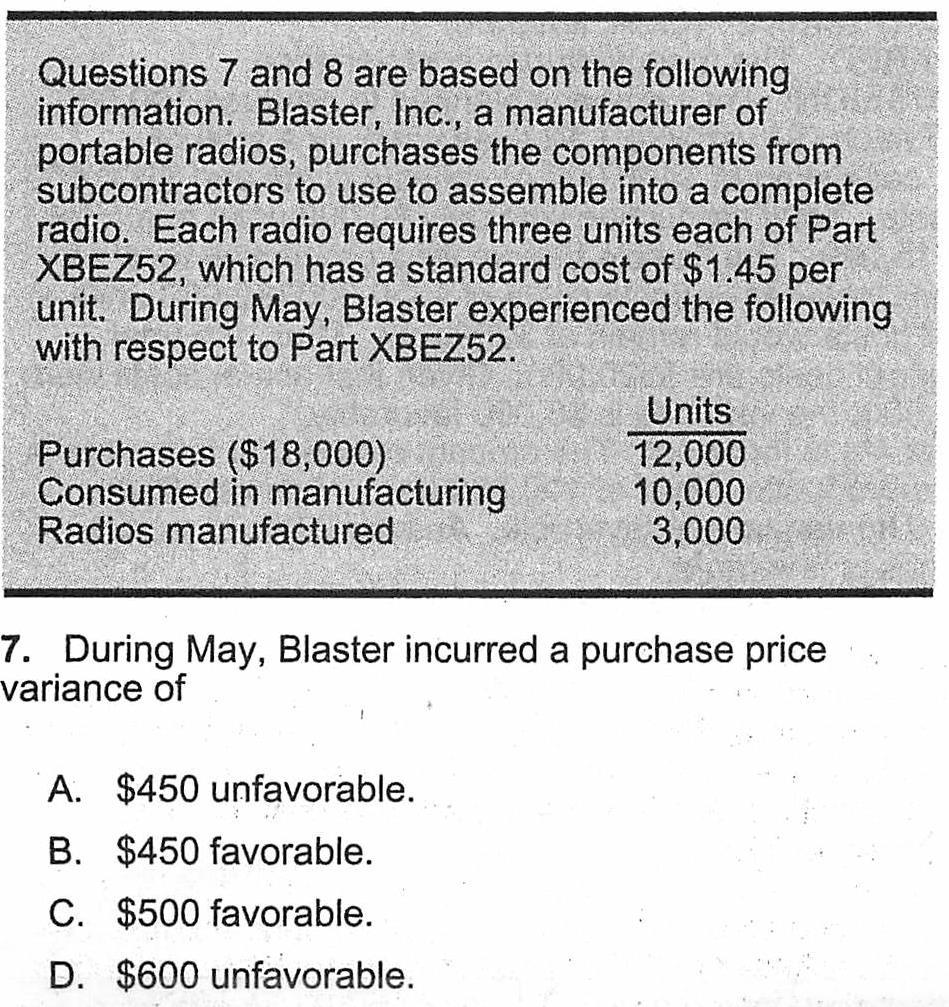

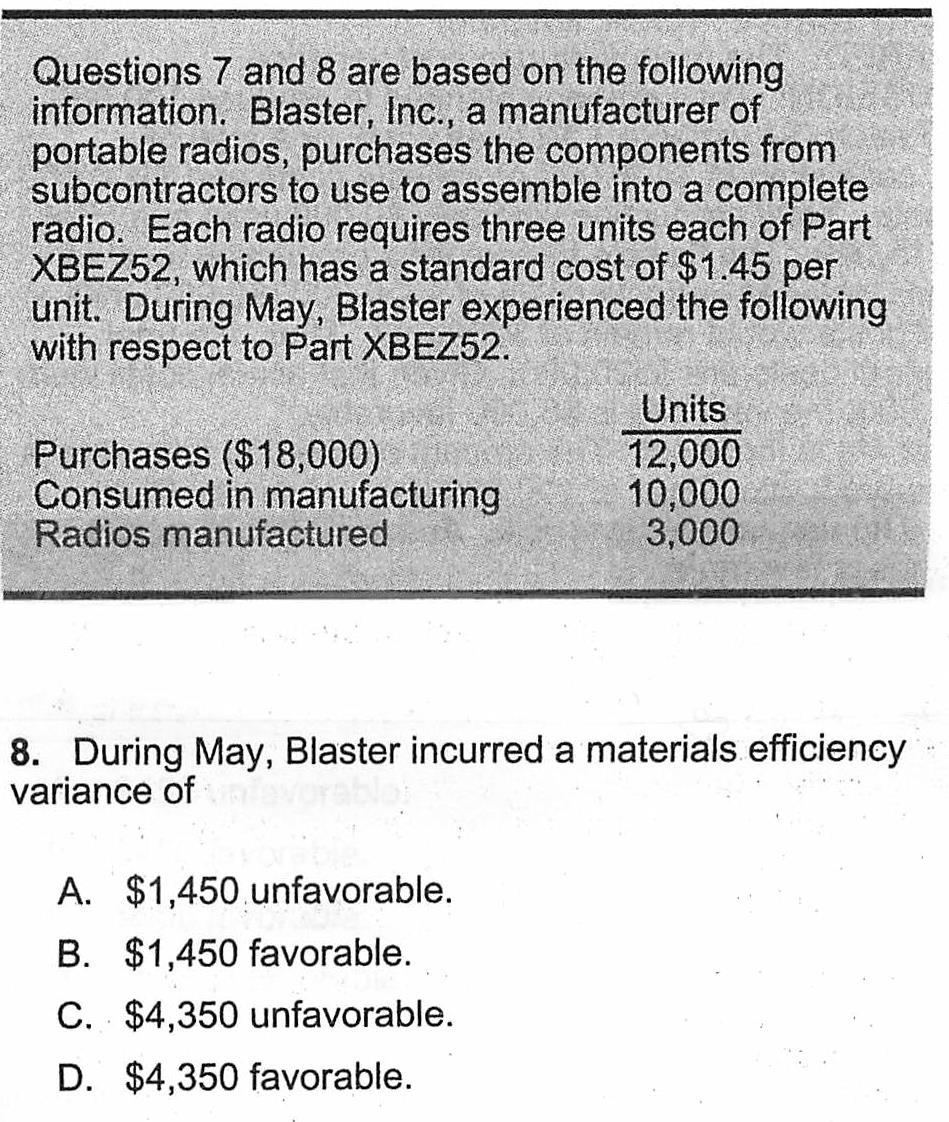

43 SU 10.3 Question 1 Blaster, Inc., a manufacturer of portable radios, purchases the components from subcontractors to use to assemble into a complete radio. Each radio requires three units each of Part XBEZ52, which has a standard cost of $1.45 per unit. During May, Blaster experienced the following with respect to Part XBEZ52. Units Purchases ($18,000) 12,000 Consumed in manufacturing 10,000 Radios manufactured 3,000

44 SU 10.3 Question 1 (cont.) During May, Blaster incurred a purchase price variance of During May, Blaster incurred a purchase price variance of A. $450 unfavorable. B. $450 favorable. C. $500 favorable. D. $600 unfavorable

45 SU 10.3 Question 1 Answer Correct Answer: D Blaster s purchase price variance is calculated as follows: Purchase price variance = AQ (SP AP) = 12,000 parts ($1.45 $1.50) = 12,000 $0.05 = $600 unfavorable Incorrect Answers: A: The standard quantity needed for the actual output times the $.05 unfavorable price variance per part equals $450 unfavorable. B: The variance is unfavorable, and $450 is the amount of the variance that relates only to the standard input for the actual output. C: The variance is unfavorable. Furthermore, the variance is based on the quantity purchased, not the quantity consumed. [Note: The materials price variance is sometimes isolated at the time of transfer to production.]

46 SU 10.3 Question 2 Blaster, Inc., a manufacturer of portable radios, purchases the components from subcontractors to use to assemble into a complete radio. Each radio requires three units each of Part XBEZ52, which has a standard cost of $1.45 per unit. During May, Blaster experienced the following with respect to Part XBEZ52. Units Purchases ($18,000) 12,000 Consumed in manufacturing 10,000 Radios manufactured 3,000

47 SU 10.3 Question 2 (cont.) During May, Blaster incurred a materials efficiency variance of A. $1,450 unfavorable. B. $1,450 favorable. C. $4,350 unfavorable. D. $4,350 favorable.

48 SU 10.3 Question 2 Answer Correct Answer: A Standard usage was three parts per radio at $1.45 each. For a production level of 3,000 units, the total materials needed equaled 9,000 parts, but materials actually used totaled 10,000 parts. Thus, the variance is $1,450 unfavorable {SP (AQ SQ) = [$1.45 standard cost per part (10,000 actually used 9,000 standard usage)]}. Incorrect Answers: B: The variance is unfavorable. The actual quantity used exceeded the standard input allowed. C: Assuming that 12,000 parts were consumed results in $4,350 unfavorable. D: Assuming that 12,000 parts were consumed and that the variance is favorable results in $4,350 favorable.

49

50

51

52

53

54

55 SU 10.4 Question 1 Under a standard cost system, direct labor price variances are usually not attributable to A. Union contracts approved before the budgeting cycle. B. Labor rate predictions. C. The use of a single average standard rate. The assignment of different D. skill levels of workers than planned.

56 SU 10.4 Question 1 Answer Correct Answer: A The direct labor price (rate) variance is the actual hours worked times the difference between the standard rate and the actual rate paid. This difference may be attributable to (1) a change in labor rates since the establishment of the standards, (2) using a single average standard rate despite different rates earned among different employees, (3) assigning higher-paid workers to jobs estimated to require lower-paid workers (or vice versa), or (4) paying hourly rates, but basing standards on piecework rates (or vice versa). The difference should not be caused by a union contract approved before the budgeting cycle because such rates would have been incorporated into the standards. Incorrect Answers: B: Predictions about labor rates may have been inaccurate. C: Using a single average standard rate may lead to variances if some workers are paid more than others and the proportions of hours worked differ from estimates. D: Assigning higher paid (and higher skilled) workers to jobs not requiring such skills leads to an unfavorable variance.

57 SU 10.4 Question 2 Zazoo, Inc. specializes in reviewing and editing technical magazine articles. Zazoo sets the following standards for evaluating the performance of the professional staff: Annual budgeted fixed costs for normal capacity level of 10,000 articles reviewed and edited $600,000 Standard professional hours per 10 articles 200 hours Flexible budget of standard labor costs to process $10,000,000 10,000 articles The following data apply to the 9,500 articles that were actually reviewed and edited during the current year. Total hours used by professional staff 192,000 hours Flexible costs $9,120,000 Total cost $9,738,000 Zazoo s labor efficiency variance for the year is

58 SU 10.4 Question 2 (cont.) Zazoo s labor efficiency variance for the year is A. $100,000 unfavorable. B. $238,000 unfavorable. C. $380,000 favorable. D. $500,000 favorable

59 SU 10.4 Question 2 Answer Correct Answer: A The labor efficiency variance is the standard cost per hour times the difference between standard and actual hour. The standard labor rate is $50 per hour, and the standard time allowed for 9,500 articles is 190,000 hours (9,500 20). Actual hours worked totaled 192,000. Thus, an unfavorable variance of 2,000 hours occurred. The unfavorable labor efficiency variance is therefore $100,000 (2,000 hours $50). Incorrect Answers: B: The difference between the standard labor cost ($9,500,000) and total actual (fixed + variable) cost ($9,738,000) is $238,000. C: The variance is unfavorable. D: The efficiency variance is based on standard hours for actual production levels--in this case, 190,000 hours.

60 Conclusion key take away What could explain favorable / unfavorable variances? Better purchase price (supplier concentration) Lower quality input (outsource other country) Better technology = more efficiency (turnaround, bottleneck) Higher-skilled workers (PhD, training, turnover, benefits, union) Less scrap / spoilage = Lean sigma (waste) Economies of scale (volume) Inflation cost of living (tax, insurance, rent) Cost of capital, risk, exchange rate External factors (competitors, demand, distribution) Components of the product (spare parts)

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

Standard 4 pounds Quantity $ 7.50/pound Standard Cost $30.00

Part 1 Study Unit 7 Fausto Company employs a standard cost system in which direct materials inventory is carried at standard cost. The company has established the following standard for the materials costs

Part 1 Study Unit 7 Fausto Company employs a standard cost system in which direct materials inventory is carried at standard cost. The company has established the following standard for the materials costs

STANDARD COSTS AND VARIANCE ANALYSIS

STANDARD COSTS AND VARIANCE ANALYSIS Key Terms and Concepts to Know Static or Planning Budgets Used for planning purposes Prepared at the beginning of the period Based on one projected level of activity

STANDARD COSTS AND VARIANCE ANALYSIS Key Terms and Concepts to Know Static or Planning Budgets Used for planning purposes Prepared at the beginning of the period Based on one projected level of activity

Chapter 23 Flexible Budgets and Standard Cost Systems

Chapter 23 Flexible Budgets and Standard Cost Systems Review Questions 1. What is a variance? A variance is the difference between an actual amount and the budgeted amount. 2. Explain the difference between

Chapter 23 Flexible Budgets and Standard Cost Systems Review Questions 1. What is a variance? A variance is the difference between an actual amount and the budgeted amount. 2. Explain the difference between

Illustrative Example Xander Barkley s XYX Company manufactures a single product. The standard cost card for one unit is as follows:

Appendix 11A General Ledger Entries to Record Variances 11A-1 General Ledger Entries to Record Variances Although standard costs and variances can be computed and used by management without being formally

Appendix 11A General Ledger Entries to Record Variances 11A-1 General Ledger Entries to Record Variances Although standard costs and variances can be computed and used by management without being formally

Disclaimer: This resource package is for studying purposes only EDUCATIO N

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 9: Budgeting The Basic Framework of Budgeting Master budget - a summary of a company s plans in which specific targets

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 9: Budgeting The Basic Framework of Budgeting Master budget - a summary of a company s plans in which specific targets

Flexible Budgets and Standard Costing QUESTIONS

Chapter 21 Flexible Budgets and Standard Costing QUESTIONS 1. Fixed budget performance reports have limited usefulness because they do not reflect differences in revenues and variable costs that can occur

Chapter 21 Flexible Budgets and Standard Costing QUESTIONS 1. Fixed budget performance reports have limited usefulness because they do not reflect differences in revenues and variable costs that can occur

Multiple Choice Questions

Multiple Choice Questions 1. The difference between the actual price and the standard price, multiplied by the actual quantity of materials purchased is the a) direct labor price variance b) direct labor

Multiple Choice Questions 1. The difference between the actual price and the standard price, multiplied by the actual quantity of materials purchased is the a) direct labor price variance b) direct labor

Online Course Manual By Craig Pence. Module 7

Online Course Manual By Craig Pence Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled

Online Course Manual By Craig Pence Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled

CHAPTER 8 FLEXIBLE BUDGETS, OVERHEAD COST VARIANCES, AND MANAGEMENT CONTROL

CHAPTER 8 FLEXIBLE BUDGETS, OVERHEAD COST VARIANCES, AND MANAGEMENT CONTROL 8-1 Effective planning of variable overhead costs involves: 1. Planning to undertake only those variable overhead activities

CHAPTER 8 FLEXIBLE BUDGETS, OVERHEAD COST VARIANCES, AND MANAGEMENT CONTROL 8-1 Effective planning of variable overhead costs involves: 1. Planning to undertake only those variable overhead activities

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material. Chapter 10: Static and Flexible Budgets

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 10: Static and Flexible Budgets Budget: formalized financial plan for operations of an organization for a specified

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 10: Static and Flexible Budgets Budget: formalized financial plan for operations of an organization for a specified

Page 1. 9 Standard. planning. cost and different. and. activity assumed in. different to $30 for. different particula

Standard Costing By Dr. Michael Constas Page 1 9 Standard Costing: A Functional-Based Control Approach Companies prepare cost budgets as part of their planning process. These budgets assume a given level

Standard Costing By Dr. Michael Constas Page 1 9 Standard Costing: A Functional-Based Control Approach Companies prepare cost budgets as part of their planning process. These budgets assume a given level

Part 2 : 11/11/10 07:41:20

Question 1 - CMA 694 3-29 - Performance Measurement Part 2 : 11/11/10 07:41:20 One approach to measuring divisional performance is return on investment. Return on investment is expressed as operating income

Question 1 - CMA 694 3-29 - Performance Measurement Part 2 : 11/11/10 07:41:20 One approach to measuring divisional performance is return on investment. Return on investment is expressed as operating income

ACC406 Tip Sheet. 1) Planning: It is the process of creating a set of plans that a company intends to achieve a particular goal.

Planning: It is the process of creating a set of plans that a company intends to achieve a particular goal.") ACC406 Tip Sheet Chapter 1 Managerial Accounting: It is simply the process of reporting accounting information for a company s internal users such as managers, sales staff and etc. for decision making.

ACC406 Tip Sheet Chapter 1 Managerial Accounting: It is simply the process of reporting accounting information for a company s internal users such as managers, sales staff and etc. for decision making.

Module 3 Introduction

Module 3 Introduction Module 3 Introduction This module is designed to further enhance knowledge about management accounting techniques. In particular, the student is introduced to the role of budgeting,

Module 3 Introduction Module 3 Introduction This module is designed to further enhance knowledge about management accounting techniques. In particular, the student is introduced to the role of budgeting,

Chapter 10 Standard Costs and Variances

Chapter 10 Standard Costs and Variances Solutions to Questions 10-1 A quantity standard indicates how much of an input should be used to make a unit of output. A price standard indicates how much the input

Chapter 10 Standard Costs and Variances Solutions to Questions 10-1 A quantity standard indicates how much of an input should be used to make a unit of output. A price standard indicates how much the input

Chapter 11 Flexible Budgets and Overhead Analysis

Chapter 11 Flexible Budgets and Overhead Analysis Solutions to Questions 11-1 A static budget is a budget prepared for a single level of activity. The static budget is not adjusted even if the activity

Chapter 11 Flexible Budgets and Overhead Analysis Solutions to Questions 11-1 A static budget is a budget prepared for a single level of activity. The static budget is not adjusted even if the activity

2018 LAST MINUTE CPA EXAM NOTES

2018 LAST MINUTE CPA EXAM NOTES Page intentionally left blank 2018 LAST MINUTE CPA EXAM NOTES BEC (Volume 1) Copyright 2018 by Glomont LLC. First edition Notice of Rights. All rights reserved. No part

2018 LAST MINUTE CPA EXAM NOTES Page intentionally left blank 2018 LAST MINUTE CPA EXAM NOTES BEC (Volume 1) Copyright 2018 by Glomont LLC. First edition Notice of Rights. All rights reserved. No part

Index COPYRIGHTED MATERIAL

A ABC (activity-based costing). See also costs; peanut butter costing allocating indirect costs, 77 78 allocations to cost pools, 79 analyzing cost activities, 78 79 applying to bottlenecks, 353 applying

A ABC (activity-based costing). See also costs; peanut butter costing allocating indirect costs, 77 78 allocations to cost pools, 79 analyzing cost activities, 78 79 applying to bottlenecks, 353 applying

Lecture 16 Flexible Budgets and Variance Analysis

Economics, Management and Entrepreneurship Prof. Pratap K. J. Mohapatra Department of Industrial Engineering & Management Indian Institute of Technology - Kharagpur Lecture 16 Flexible Budgets and Variance

Economics, Management and Entrepreneurship Prof. Pratap K. J. Mohapatra Department of Industrial Engineering & Management Indian Institute of Technology - Kharagpur Lecture 16 Flexible Budgets and Variance

24 Control through standard costs

24 Control through standard costs 24.1 Learning objectives After studying this chapter, you should be able to: Discuss the nature of standard costs, including how standards are set. Define budgets and

24 Control through standard costs 24.1 Learning objectives After studying this chapter, you should be able to: Discuss the nature of standard costs, including how standards are set. Define budgets and

Engineering Economics and Financial Accounting

Engineering Economics and Financial Accounting Unit 4: Costing Major Topics are: Job Costing Operating Costing Process Costing Standard Costing (Variance Analysis) Gross Domestic Product (GDP) Job Costing

Engineering Economics and Financial Accounting Unit 4: Costing Major Topics are: Job Costing Operating Costing Process Costing Standard Costing (Variance Analysis) Gross Domestic Product (GDP) Job Costing

Standard Costing and Variance Analysis

Standard Costing and Variance Analysis Standard Costing Standard cost is predetermined cost agreed earlier under specific working conditions. Standard costing is a technique which establishes predetermined

Standard Costing and Variance Analysis Standard Costing Standard cost is predetermined cost agreed earlier under specific working conditions. Standard costing is a technique which establishes predetermined

Solution to Problem 1 Material and labor variances

Professor Authored Problem Solutions Advanced Cost Accounting Acct 647 Variances Solution to Problem 1 Material and labor variances 1. Compute material price and quantity variances Std Cost = applied cost

Professor Authored Problem Solutions Advanced Cost Accounting Acct 647 Variances Solution to Problem 1 Material and labor variances 1. Compute material price and quantity variances Std Cost = applied cost

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 11 & 13. Chapter 11: Standard Costs and Variance Analysis

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 11 & 13 Chapter 11: Standard Costs and Variance Analysis Variance Analysis: calculating variances and investigating

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 11 & 13 Chapter 11: Standard Costs and Variance Analysis Variance Analysis: calculating variances and investigating

ACC406 Tip Sheet. Direct Labour (DL): labour that is directly attributable to the goods and service that are being produced by a firm.

: labour that is directly attributable to the goods and service that are being produced by a firm.") ACC406 Tip Sheet Definitions Direct Cost: a cost that can be easily allocated to a certain object. Variable Cost (VC): a cost that changes in direct relation to output (output increases VC increases) Fixed

ACC406 Tip Sheet Definitions Direct Cost: a cost that can be easily allocated to a certain object. Variable Cost (VC): a cost that changes in direct relation to output (output increases VC increases) Fixed

MGMT-027 Q4 17. The purpose of a flexible budget is to: C. update the static planning budget to reflect the actual level of activity of the period.

MGMT-027 Q4 17. The purpose of a flexible budget is to: C. update the static planning budget to reflect the actual level of activity of the period. 21. Salyers Family Inn is a bed and breakfast establishment

MGMT-027 Q4 17. The purpose of a flexible budget is to: C. update the static planning budget to reflect the actual level of activity of the period. 21. Salyers Family Inn is a bed and breakfast establishment

PESIT Bangalore South Campus Hosur road, 1km before Electronic City, Bengaluru -100

INTERNAL ASSESSMENT TEST 3 Date : 09/11/2016 Max Marks : 50 Subject & Code : Cost Management (14MBAFM305) Section : Finance Name of faculty : Dr.R.Duraipandian Time: 8:30 10:00 AM Note: Answer all questions

INTERNAL ASSESSMENT TEST 3 Date : 09/11/2016 Max Marks : 50 Subject & Code : Cost Management (14MBAFM305) Section : Finance Name of faculty : Dr.R.Duraipandian Time: 8:30 10:00 AM Note: Answer all questions

Introduction and Meaning Concept Advantages & Limitations Objectives of Standard Costing Preliminary Establishment Types of Standard

Standard Costing Introduction and Meaning Concept Advantages & Limitations Objectives of Standard Costing Preliminary Establishment Types of Standard Differences Standard Cost Card/Sheet Meaning of Analysis

Standard Costing Introduction and Meaning Concept Advantages & Limitations Objectives of Standard Costing Preliminary Establishment Types of Standard Differences Standard Cost Card/Sheet Meaning of Analysis

Chapter 10 Static and Flexible Budgets

Cost Management Measuring, Monitoring, and Motivating Performance Chapter 10 Static and Flexible Budgets Prepared by Gail Kaciuba Midwestern State University Eldenburg & Wolcott s Cost Management, 1e Slide

Cost Management Measuring, Monitoring, and Motivating Performance Chapter 10 Static and Flexible Budgets Prepared by Gail Kaciuba Midwestern State University Eldenburg & Wolcott s Cost Management, 1e Slide

CMA. Financial Reporting, Planning, Performance, and Control

2019 Edition CMA Preparatory Program Part 1 Financial Reporting, Planning, Performance, and Control Manufacturing Input Variances Sample Brian Hock, CMA, CIA and Lynn Roden, CMA HOCK international, LLC

2019 Edition CMA Preparatory Program Part 1 Financial Reporting, Planning, Performance, and Control Manufacturing Input Variances Sample Brian Hock, CMA, CIA and Lynn Roden, CMA HOCK international, LLC

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 M BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 M BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

MODULE 4 PLANNING AND CONTROL

MODULE 4 PLANNING AND CONTROL OUTLINES The purpose of budgetary control system Alternative approaches to budgeting, including incremental budgeting, Zero-based budgeting, Activity-based budgeting, rolling

MODULE 4 PLANNING AND CONTROL OUTLINES The purpose of budgetary control system Alternative approaches to budgeting, including incremental budgeting, Zero-based budgeting, Activity-based budgeting, rolling

Chapter 16 Fundamentals of Variance Analysis

Chapter 16 Fundamentals of Variance Analysis True / False Questions 1. In essence, the terms "master budget" and "operating budget" mean the same thing and can be used interchangeably. True False 2. Variances

Chapter 16 Fundamentals of Variance Analysis True / False Questions 1. In essence, the terms "master budget" and "operating budget" mean the same thing and can be used interchangeably. True False 2. Variances

In Class #8.1 Coverage of manufacturing overhead, standard cost system Required 1 Solution Exhibit 8-1 shows the computations. Summary details are:

In Class #8.1 Coverage of manufacturing overhead, standard cost system Required 1 Solution Exhibit 8-1 shows the computations. Summary details are: Actual Flexible Budget Output units 49,200 49,200 Allocation

In Class #8.1 Coverage of manufacturing overhead, standard cost system Required 1 Solution Exhibit 8-1 shows the computations. Summary details are: Actual Flexible Budget Output units 49,200 49,200 Allocation

Managerial Accounting Prof. Dr. Varadraj Bapat Department School of Management Indian Institute of Technology, Bombay

Managerial Accounting Prof. Dr. Varadraj Bapat Department School of Management Indian Institute of Technology, Bombay Lecture - 30 Budgeting and Standard Costing In our last session, we had discussed about

Managerial Accounting Prof. Dr. Varadraj Bapat Department School of Management Indian Institute of Technology, Bombay Lecture - 30 Budgeting and Standard Costing In our last session, we had discussed about

WEEK 6 OPERATING BUDGETS (MANUFACTURING ORGANISATIONS) Case Study. The budgets that you need to prepare include:

Case Study. The budgets that you need to prepare include:") WEEK 6 OPERATING BUDGETS (MANUFACTURING ORGANISATIONS) Case Study manufactures cardboard boxes which are used for transporting very special toys to toy stores all around Australia. You have already been

WEEK 6 OPERATING BUDGETS (MANUFACTURING ORGANISATIONS) Case Study manufactures cardboard boxes which are used for transporting very special toys to toy stores all around Australia. You have already been

ACCY 121 Chapter 16 Practice Quiz Fundamentals of Variance Analysis (1)

") ACCY 121 Chapter 16 Practice Quiz Fundamentals of Variance Analysis (1) 101. The Hageness Company has had great difficulty in controlling overhead costs. At a recent convention, the president heard about

ACCY 121 Chapter 16 Practice Quiz Fundamentals of Variance Analysis (1) 101. The Hageness Company has had great difficulty in controlling overhead costs. At a recent convention, the president heard about

Standard Cost System Practice Problems

When setting up a standard cost system, the concepts of standards in material, labor, and overhead must be explored in a simple manner to start the process. Practice Standard Cost Variances: Simple Example

When setting up a standard cost system, the concepts of standards in material, labor, and overhead must be explored in a simple manner to start the process. Practice Standard Cost Variances: Simple Example

VARIANCE ANALYSIS: ILLUSTRATION

VARIANCE ANALYSIS: ILLUSTRATION The following information relates to the production of product Alpha for the month of August Standard Cost Card Budgeted production overhead based on 10,000 units $ $ Selling

VARIANCE ANALYSIS: ILLUSTRATION The following information relates to the production of product Alpha for the month of August Standard Cost Card Budgeted production overhead based on 10,000 units $ $ Selling

Costing Group 1 Important Questions for IPCC November 2017 (Chapters 10 12)

") Costing Group 1 Important Questions for IPCC November 2017 (Chapters 10 12) CHAPTER 10 STANDARD COSTING 1. The standard material cost for a normal mix of one tonne of product Captain based on: Raw Material

Costing Group 1 Important Questions for IPCC November 2017 (Chapters 10 12) CHAPTER 10 STANDARD COSTING 1. The standard material cost for a normal mix of one tonne of product Captain based on: Raw Material

December CS Executive Programme Module - I Paper - 2

December - 2015 CS Executive Programme Module - I Paper - 2 (New Syllabus) Cost and Management Accounting Total number of questions: 100 Maximum marks: 100 Assertion A: 1. In management accounting, firm

December - 2015 CS Executive Programme Module - I Paper - 2 (New Syllabus) Cost and Management Accounting Total number of questions: 100 Maximum marks: 100 Assertion A: 1. In management accounting, firm

COST ACCOUNTING STANDARD ON MATERIAL COST

CAS-6 (REVISED 2017) COST ACCOUNTING STANDARD ON MATERIAL COST The following is the COST ACCOUNTING STANDARD 6 (CAS 6) (Revised 2017) issued by the Council of The Institute of Cost Accountants of India

CAS-6 (REVISED 2017) COST ACCOUNTING STANDARD ON MATERIAL COST The following is the COST ACCOUNTING STANDARD 6 (CAS 6) (Revised 2017) issued by the Council of The Institute of Cost Accountants of India

(a) Calculate planning and operating variances following the recognition of the learning curve effect. (6 marks)

Calculate planning and operating variances following the recognition of the learning curve effect. (6 marks)") SECTION A 50 MARKS Question One (a) Calculate planning and operating variances following the recognition of the learning curve effect. (6 marks) Flexed budget Actual output Revised flexed budget Output

SECTION A 50 MARKS Question One (a) Calculate planning and operating variances following the recognition of the learning curve effect. (6 marks) Flexed budget Actual output Revised flexed budget Output

b) To answer any questing dealing with variances work out the rates and the cost per unit i.e. work out the standard cost per unit.

To answer any questing dealing with variances work out the rates and the cost per unit i.e. work out the standard cost per unit.") QUESTION ONE a) Basic Standards These are standards which are kept unaltered over a long period of time and may be out of date. These are used to show changes in efficiency or performance over a long period

QUESTION ONE a) Basic Standards These are standards which are kept unaltered over a long period of time and may be out of date. These are used to show changes in efficiency or performance over a long period

322 Roll No : 1 : Time allowed : 3 hours Maximum marks : 100

2/2013/CMA (N/S) Roll No : 1 : Time allowed : 3 hours Maximum marks : 100 Total number of questions : 6 Total number of printed pages : 7 NOTE : 1. Answer ALL Questions. 2. All working notes should be

2/2013/CMA (N/S) Roll No : 1 : Time allowed : 3 hours Maximum marks : 100 Total number of questions : 6 Total number of printed pages : 7 NOTE : 1. Answer ALL Questions. 2. All working notes should be

ACT 2131 (PJJ) TUTORIAL 6

TUTORIAL 6") ACT 2131 (PJJ) TUTORIAL 6 1. Describe the relationship that unit standards have with flexible budgeting. 2. Why is historical experience often a poor basis for establishing standards? 3. What are ideal

ACT 2131 (PJJ) TUTORIAL 6 1. Describe the relationship that unit standards have with flexible budgeting. 2. Why is historical experience often a poor basis for establishing standards? 3. What are ideal

CHAPTER 8: PERFORMANCE EVALUATION Pearson Education. All rights reserved.

CHAPTER 8: PERFORMANCE EVALUATION Learning Objectives 1. Explain static budgets and static-budget variances 2. Develop flexible budgets and compute flexiblebudget variances and sales-volume variances 3.

CHAPTER 8: PERFORMANCE EVALUATION Learning Objectives 1. Explain static budgets and static-budget variances 2. Develop flexible budgets and compute flexiblebudget variances and sales-volume variances 3.

Performance. MCQs. Gleim Book. Gleim CD. IMA - Retired IMA - Retired Contains: in a random basis

Performance MCQs Contains: in a random basis Gleim Book Gleim CD IMA - Retired 2005 IMA - Retired 2008 By: Mohamed hengoo to dvd4arab.com members [1] Gleim #: 7.6.118 -- Source: Publisher Using the three-variance

Performance MCQs Contains: in a random basis Gleim Book Gleim CD IMA - Retired 2005 IMA - Retired 2008 By: Mohamed hengoo to dvd4arab.com members [1] Gleim #: 7.6.118 -- Source: Publisher Using the three-variance

Standard Costs and Variances

10-1 Standard Costs and Variances Chapter 10 10-2 Standard Costs Standards are benchmarks or norms for measuring performance. In managerial accounting, two types of standards are commonly used. Quantity

10-1 Standard Costs and Variances Chapter 10 10-2 Standard Costs Standards are benchmarks or norms for measuring performance. In managerial accounting, two types of standards are commonly used. Quantity

THE MASTER BUDGET ET R BUDGE VERVIEW OV. Horngren 13e

Chapter 6: THE MASTER BUDGET Horngren 13e 1 ET R BUDGE W OF THE MASTER VERVIEW OV 2 3 Learning Objective 1: Describe the master budget... The master budget is the initial budget prepared p before the start

Chapter 6: THE MASTER BUDGET Horngren 13e 1 ET R BUDGE W OF THE MASTER VERVIEW OV 2 3 Learning Objective 1: Describe the master budget... The master budget is the initial budget prepared p before the start

Purushottam Sir. Formulas of Costing

Purushottam Sir Formulas of Costing Material Maximum Stock Level= Re-order level + Re-order quantity (Minimum consumption Minimum reorder period) Minimum Stock Level= Re-order level (Average lead time

Purushottam Sir Formulas of Costing Material Maximum Stock Level= Re-order level + Re-order quantity (Minimum consumption Minimum reorder period) Minimum Stock Level= Re-order level (Average lead time

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

Free of Cost ISBN : Appendix. CMA (CWA) Inter Gr. II (Solution upto Dec & Questions of June 2013 included)

Inter Gr. II (Solution upto Dec & Questions of June 2013 included)") Free of Cost ISBN : 978-93-5034-631-0 Appendix CMA (CWA) Inter Gr. II (Solution upto Dec. 2012 & Questions of June 2013 included) Paper - 8 : Cost and Management Accounting Chapter - 3 : Labour Accounting

Free of Cost ISBN : 978-93-5034-631-0 Appendix CMA (CWA) Inter Gr. II (Solution upto Dec. 2012 & Questions of June 2013 included) Paper - 8 : Cost and Management Accounting Chapter - 3 : Labour Accounting

MANAGEMENT INFORMATION

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 1 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 1 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

CHAPTER 8 Budgetary Control and Variance Analysis

CHAPTER 8 Budgetary Control and Variance Analysis Learning Objectives After studying this chapter, you will be able to: 1. Understand how companies use budgets for control. 2. Perform variance analysis.

CHAPTER 8 Budgetary Control and Variance Analysis Learning Objectives After studying this chapter, you will be able to: 1. Understand how companies use budgets for control. 2. Perform variance analysis.

MOCK EXAMINATION PRINCIPLES OF ACCOUNTS A-LEVEL PAPER 2

HONG KONG ASSOCIATION FOR BUSINESS EDUCATION HONG KONG INSTITUTE OF VOCATIONAL EDUCATION (CHAI WAN & TUEN MUN) HONG KONG ADVANCED LEVEL EXAMINATION 2009 MOCK EXAMINATION PRINCIPLES OF ACCOUNTS A-LEVEL

HONG KONG ASSOCIATION FOR BUSINESS EDUCATION HONG KONG INSTITUTE OF VOCATIONAL EDUCATION (CHAI WAN & TUEN MUN) HONG KONG ADVANCED LEVEL EXAMINATION 2009 MOCK EXAMINATION PRINCIPLES OF ACCOUNTS A-LEVEL

BUSINESS FINANCIAL & ACCOUNTING SKILLS

BUSINESS FINANCIAL & ACCOUNTING SKILLS SECTOR / ACCOUNTING AND FINANCE NON-TECHNICAL & CERTIFIED TRAINING COURSE This training seminar addresses key issues, such as cost analysis, continuous improvement

BUSINESS FINANCIAL & ACCOUNTING SKILLS SECTOR / ACCOUNTING AND FINANCE NON-TECHNICAL & CERTIFIED TRAINING COURSE This training seminar addresses key issues, such as cost analysis, continuous improvement

(AA22) COST ACCOUNTING AND REPORTING

COST ACCOUNTING AND REPORTING") All Rights Reserved ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA AA2 EXAMINATION - JANUARY 2017 (AA22) COST ACCOUNTING AND REPORTING Instructions to candidates (Please Read Carefully): (1) Time Allowed:

All Rights Reserved ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA AA2 EXAMINATION - JANUARY 2017 (AA22) COST ACCOUNTING AND REPORTING Instructions to candidates (Please Read Carefully): (1) Time Allowed:

Answer to MTP_Intermediate_ Syllabus 2012_December 2016_Set2. Paper 10- Cost & Management Accountancy

Paper 10- Cost & Management Accountancy Page 1 of 14 Paper 10- Cost & Management Accountancy Full Marks: 100 Time allowed: 3 Hours Section A 1. Answer Question No.1 which is compulsory carrying 5 Marks

Paper 10- Cost & Management Accountancy Page 1 of 14 Paper 10- Cost & Management Accountancy Full Marks: 100 Time allowed: 3 Hours Section A 1. Answer Question No.1 which is compulsory carrying 5 Marks

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING Answer all questions.

Question 1 (i) (ii) PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING Answer all questions. What is Cost accounting? Enumerate its important objectives. Distinguish between Fixed

Question 1 (i) (ii) PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING Answer all questions. What is Cost accounting? Enumerate its important objectives. Distinguish between Fixed

You were introduced to Standard Costing in the earlier stages of your studies in which you understood the following;

6 Standard Costing LEARNING OBJECTIVES : After studying this unit you will be able to : Understand terms as standard Cost, standard Costing, standard Hour Understand how a standard costing system operates

6 Standard Costing LEARNING OBJECTIVES : After studying this unit you will be able to : Understand terms as standard Cost, standard Costing, standard Hour Understand how a standard costing system operates

CPA COMPETENCY MAP STUDY NOTES SAMPLE EXCERPTS

CPA COMPETENCY MAP STUDY NOTES SAMPLE EXCERPTS 2019 Edition To contact us or to order a copy of the book: Densmore Consulting Services Inc. PO Box 21027 Dartmouth, NS B2W 6B2 Phone: 1-844-434-3812 (toll

CPA COMPETENCY MAP STUDY NOTES SAMPLE EXCERPTS 2019 Edition To contact us or to order a copy of the book: Densmore Consulting Services Inc. PO Box 21027 Dartmouth, NS B2W 6B2 Phone: 1-844-434-3812 (toll

Cost Analysis and Estimating for Engineering and Management

Cost Analysis and Estimating for Engineering and Management Chapter 4 Accounting Analysis Ch 4-1 Overview Accounting Records, Transactions, Reports Depreciation What It Is, Uses, Calculations Budgeting

Cost Analysis and Estimating for Engineering and Management Chapter 4 Accounting Analysis Ch 4-1 Overview Accounting Records, Transactions, Reports Depreciation What It Is, Uses, Calculations Budgeting

B292 Revision Part 4

B292 Revision Part 4 EX 1 The following represent four independent situations from which one amount is missing. Products Annual Quantity Carrying (Holding) Cost/Unit Ordering Cost/Order EOQ A 4,500 $1

B292 Revision Part 4 EX 1 The following represent four independent situations from which one amount is missing. Products Annual Quantity Carrying (Holding) Cost/Unit Ordering Cost/Order EOQ A 4,500 $1

PELLISSIPPI STATE TECHNICAL COMMUNITY COLLEGE MASTER SYLLABUS COST ACCOUNTING ACC 2360

PELLISSIPPI STATE TECHNICAL COMMUNITY COLLEGE MASTER SYLLABUS COST ACCOUNTING ACC 2360 Class Hours: 3.0 Credit Hours: 3.0 Laboratory Hours: 0.0 Date Revised: Spring 02 NOTE: This course is NOT designed

PELLISSIPPI STATE TECHNICAL COMMUNITY COLLEGE MASTER SYLLABUS COST ACCOUNTING ACC 2360 Class Hours: 3.0 Credit Hours: 3.0 Laboratory Hours: 0.0 Date Revised: Spring 02 NOTE: This course is NOT designed

SUGGESTED ANSWERS SPRING 2015 EXAMINATIONS 1 of 7 FUNDAMENTALS OF COST & MANAGEMENT ACCOUNTING SEMESTER-2

SUGGESTED ANSWERS SPRING 2015 EXAMINATIONS 1 of 7 Q. 2 (a) The Role of the Management Accountant: The management accountant plays a critical role in providing information to management to assist in planning,

SUGGESTED ANSWERS SPRING 2015 EXAMINATIONS 1 of 7 Q. 2 (a) The Role of the Management Accountant: The management accountant plays a critical role in providing information to management to assist in planning,

state the objectives of variance analysis understand the linkage between individual variances and the difference between budgeted and actual profit

1 INTRODUCTION In this lesson we explain the objective of analysis and provide a practical example of how the difference between budgeted and actual profit can be broken down into its constituent elements

1 INTRODUCTION In this lesson we explain the objective of analysis and provide a practical example of how the difference between budgeted and actual profit can be broken down into its constituent elements

Speaker Biography Travis Harms, CPA/ABV, CFA

Speaker Biography Travis Harms, CPA/ABV, CFA Travis W. Harms leads Mercer Capital's Financial Reporting Valuation Group. His practice focuses on providing public and private clients with fair value opinions

Speaker Biography Travis Harms, CPA/ABV, CFA Travis W. Harms leads Mercer Capital's Financial Reporting Valuation Group. His practice focuses on providing public and private clients with fair value opinions

Budgeted production = (expected sales) + (expected ending inventory) (expected beginning inventory)

+ (expected ending inventory) (expected beginning inventory)") The correct answer is: 86,000 units. Budgeted production is calculated as follows: Budgeted production = (expected sales) + (expected ending inventory) (expected beginning inventory) The expected ending

The correct answer is: 86,000 units. Budgeted production is calculated as follows: Budgeted production = (expected sales) + (expected ending inventory) (expected beginning inventory) The expected ending

Learning Objectives. Define accrued expenditures. Identify examples of accrued expenditures

Accrual Reporting Learning Objectives Define accrued expenditures Identify examples of accrued expenditures Determine when and how accruals are reported at all levels, including the subrecipient level

Accrual Reporting Learning Objectives Define accrued expenditures Identify examples of accrued expenditures Determine when and how accruals are reported at all levels, including the subrecipient level

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47

Time: 60 min Marks: 47") MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

SECTION ONE. a) Briefly explain the meaning of the following terms as used in standard costing: i) Basic standards (2 marks) ii) Current standards

Briefly explain the meaning of the following terms as used in standard costing: i) Basic standards (2 marks) ii) Current standards") QUESTION ONE SECTION ONE a) Briefly explain the meaning of the following terms as used in standard costing: i) Basic standards ii) Current standards iii) Ideal standards iv) Normal standards b) The following

QUESTION ONE SECTION ONE a) Briefly explain the meaning of the following terms as used in standard costing: i) Basic standards ii) Current standards iii) Ideal standards iv) Normal standards b) The following

Cost Accounting: A Managerial Emphasis, 16e, Global Edition (Horngren) Chapter 4 Job Costing

Chapter 4 Job Costing") Cost Accounting: A Managerial Emphasis, 16e, Global Edition (Horngren) Chapter 4 Job Costing 4.1 Objective 4.1 1) A cost is considered direct if it can be traced to a particular cost object in a cost effective

Cost Accounting: A Managerial Emphasis, 16e, Global Edition (Horngren) Chapter 4 Job Costing 4.1 Objective 4.1 1) A cost is considered direct if it can be traced to a particular cost object in a cost effective

CORNERSTONES. of Managerial Accounting. Dan L. Heitger. Maryanne M. Mowen. Don R. Hansen. Miami University ~ Oxford. Oklahoma State University

FUNDAMENTAL CORNERSTONES of Managerial Accounting Dan L. Heitger Miami University ~ Oxford Maryanne M. Mowen Oklahoma State University ;... ^.. _ ;... Don R. Hansen Oklahoma State University THOMSON SOUTH-WESTERN

FUNDAMENTAL CORNERSTONES of Managerial Accounting Dan L. Heitger Miami University ~ Oxford Maryanne M. Mowen Oklahoma State University ;... ^.. _ ;... Don R. Hansen Oklahoma State University THOMSON SOUTH-WESTERN

Accounting For Decision Making

Accounting For Decision Making Topic 7 Costing products and services Goals for this session Explain why managers need estimates of the costs of both responsibility centres and products; Describe the basic

Accounting For Decision Making Topic 7 Costing products and services Goals for this session Explain why managers need estimates of the costs of both responsibility centres and products; Describe the basic

THE MASTER BUDGET ET R BUDGE VERVIEW OV. Horngren 13e

Chapter 6: THE MASTER BUDGET Horngren 13e 1 ET R BUDGE W OF THE MASTER VERVIEW OV 2 3 Learning Objective 1: Describe the master budget... The master budget is the initial budget prepared p before the start

Chapter 6: THE MASTER BUDGET Horngren 13e 1 ET R BUDGE W OF THE MASTER VERVIEW OV 2 3 Learning Objective 1: Describe the master budget... The master budget is the initial budget prepared p before the start

MGT402 Subjective Material

MGT402 Subjective Material Question No: 49 ( Marks: 3 ) A company is considering publishing a limited edition book bound in special leather. It has in stock the leather bought some years ago for Rs. 1,000.

MGT402 Subjective Material Question No: 49 ( Marks: 3 ) A company is considering publishing a limited edition book bound in special leather. It has in stock the leather bought some years ago for Rs. 1,000.

SUGGESTED SOLUTIONS/ ANSWERS WINTER 2018 EXAMINATIONS 1 of 7 MANAGEMENT ACCOUNTING [M5] MANAGERIAL LEVEL-2 MARKS

![SUGGESTED SOLUTIONS/ ANSWERS WINTER 2018 EXAMINATIONS 1 of 7 MANAGEMENT ACCOUNTING [M5] MANAGERIAL LEVEL-2 MARKS](/thumbs/95/123099856.jpg "SUGGESTED SOLUTIONS/ ANSWERS WINTER 2018 EXAMINATIONS 1 of 7 MANAGEMENT ACCOUNTING [M5] MANAGERIAL LEVEL-2 MARKS") SUGGESTED SOLUTIONS/ ANSWERS WINTER 2018 EXAMINATIONS 1 of 7 Question No. 2 (a) (i) Daily Break-even Volume in Lunches and Dinners: Contribution Margin on Lunches and Dinners: Variable cost percentage

SUGGESTED SOLUTIONS/ ANSWERS WINTER 2018 EXAMINATIONS 1 of 7 Question No. 2 (a) (i) Daily Break-even Volume in Lunches and Dinners: Contribution Margin on Lunches and Dinners: Variable cost percentage

TRADITIONAL ABSORPTION V ACTIVITY BASED COSTING

TRADITIONAL ABSORPTION V ACTIVITY BASED COSTING A company manufactures two products: X and Y. Information is available as follows: (a) Product Total production Labour time per unit X 1,000 0.5 hours Y

TRADITIONAL ABSORPTION V ACTIVITY BASED COSTING A company manufactures two products: X and Y. Information is available as follows: (a) Product Total production Labour time per unit X 1,000 0.5 hours Y

Management Accounting. Pilot Paper 3 Questions and Suggested Solutions

Management Accounting Pilot Paper 3 Questions and Suggested Solutions NOTES TO USERS ABOUT PILOT PAPERS Pilot papers are published by Accounting Technicians Ireland. They are intended to provide guidance

Management Accounting Pilot Paper 3 Questions and Suggested Solutions NOTES TO USERS ABOUT PILOT PAPERS Pilot papers are published by Accounting Technicians Ireland. They are intended to provide guidance

REVIEW FOR FINAL EXAM, ACCT-2302 (SAC)

") 1. Types of Cost Classification REVIEW FOR FINAL EXAM, ACCT-2302 (SAC) CHAPTER 16 a. By Behavior: (1) Variable Cost - constant per unit, changes proportionally with volume. (2) Fixed Cost - fixed in total

1. Types of Cost Classification REVIEW FOR FINAL EXAM, ACCT-2302 (SAC) CHAPTER 16 a. By Behavior: (1) Variable Cost - constant per unit, changes proportionally with volume. (2) Fixed Cost - fixed in total

ACG 3024 Accounting for Non-Financial Majors Homework Portfolio (This is an individual assignment)

") ACG 3024 Accounting for Non-Financial Majors Homework Portfolio (This is an individual assignment) Make sure you complete the homework portfolio version assigned to you from your sign-in on the Florida

ACG 3024 Accounting for Non-Financial Majors Homework Portfolio (This is an individual assignment) Make sure you complete the homework portfolio version assigned to you from your sign-in on the Florida

Glossary of Budgeting and Planning Terms

Budgeting Basics and Beyond, Third Edition By Jae K. Shim and Joel G. Siegel Copyright 2009 by John Wiley & Sons, Inc.. Glossary of Budgeting and Planning Terms Active Financial Planning Software Budgeting

Budgeting Basics and Beyond, Third Edition By Jae K. Shim and Joel G. Siegel Copyright 2009 by John Wiley & Sons, Inc.. Glossary of Budgeting and Planning Terms Active Financial Planning Software Budgeting

Let s trace the budgets through for a company called the Hayes Company. Sales Budget The first budget prepared, comes from the Sales Forecast

Let s trace the budgets through for a company called the Hayes Company. Sales Budget The first budget prepared, comes from the Sales Forecast Expected sales volume: 3,000 units in the first quarter with

Let s trace the budgets through for a company called the Hayes Company. Sales Budget The first budget prepared, comes from the Sales Forecast Expected sales volume: 3,000 units in the first quarter with

SUGGESTED SOLUTIONS. KE2 Management Accounting Information. September All Rights Reserved

SUGGESTED SOLUTIONS KE2 Management Accounting Information September 2016 All Rights Reserved SECTION 1 Answer 01 1.1 Relevant Learning Outcome: 1.1.1 Define the terms cost, cost unit, composite cost units,

SUGGESTED SOLUTIONS KE2 Management Accounting Information September 2016 All Rights Reserved SECTION 1 Answer 01 1.1 Relevant Learning Outcome: 1.1.1 Define the terms cost, cost unit, composite cost units,

HOMEWORK. 1,40,000 20,000 (4,20,000 4,00,000) = 84,000 (F) WN 2: Calculation of effect on profit due to increase in market share

= 84,000 (F) WN 2: Calculation of effect on profit due to increase in market share") A.1. A.2. HOMEWORK WN 1: Calculation of effect on the profit due to market size Increasein profitduetogrowth = Growth in unitsdueto size increase Growth in units(total) 1,40,000 = 12,000(4,00,0003%) 20,000

A.1. A.2. HOMEWORK WN 1: Calculation of effect on the profit due to market size Increasein profitduetogrowth = Growth in unitsdueto size increase Growth in units(total) 1,40,000 = 12,000(4,00,0003%) 20,000

Index. Cambridge University Press Short Introduction to Accounting Richard Barker Index More information

accountants, roles, 4 5 accounting applications, 11 12 approaches, 8 9 building blocks, 64 coverage, 9 divisiveness of, 3 foundations of, 11, 65 83 importance of, 1 3 incompleteness, 7 knowledge of, 1

accountants, roles, 4 5 accounting applications, 11 12 approaches, 8 9 building blocks, 64 coverage, 9 divisiveness of, 3 foundations of, 11, 65 83 importance of, 1 3 incompleteness, 7 knowledge of, 1

Rupees Product RAX (552,000 x Rs.360) 198,720,

198,720,") Question No. 2 (a) Break-even Sales Revenue: SUGGESTED SOLUTIONS/ ANSWERS SPRING 2017 EXAMINATIONS 1 of 8 Calculation of total contribution: Product RAX (552,000 x Rs.216) 119,232,000 0.5 Product MAX (1,200,000

Question No. 2 (a) Break-even Sales Revenue: SUGGESTED SOLUTIONS/ ANSWERS SPRING 2017 EXAMINATIONS 1 of 8 Calculation of total contribution: Product RAX (552,000 x Rs.216) 119,232,000 0.5 Product MAX (1,200,000

CHAPTER 13 BUDGETING AND STANDARD COST SYSTEMS

CHAPTER 13 BUDGETING AND STANDARD COST SYSTEMS CLASS DISCUSSION QUESTIONS 1. The three major objectives of budgeting are (1) to establish specific goals for future operations, (2) to direct and coordinate

CHAPTER 13 BUDGETING AND STANDARD COST SYSTEMS CLASS DISCUSSION QUESTIONS 1. The three major objectives of budgeting are (1) to establish specific goals for future operations, (2) to direct and coordinate

FINALTERM EXAMINATION Spring 2010 MGT402- Cost & Management Accounting (Session - 4) Solved by Mehreen Humayun vuzs Team.

Solved by Mehreen Humayun vuzs Team.") FINALTERM EXAMINATION Spring 2010 MGT402- Cost & Management Accounting (Session - 4) Solved by Mehreen Humayun vuzs Team Time: 90 min Marks: 69 Question No: 1 ( Marks: 1 ) - Please choose one Cost of finished

FINALTERM EXAMINATION Spring 2010 MGT402- Cost & Management Accounting (Session - 4) Solved by Mehreen Humayun vuzs Team Time: 90 min Marks: 69 Question No: 1 ( Marks: 1 ) - Please choose one Cost of finished

LINEAR PROGRAMMING C H A P T E R 7

LINEAR PROGRAMMING C H A P T E R 7 INTRODUCTION In decision making, when there is only one limiting factor (scarce resource), we can rank the products according the contribution per unit of scarce resource.

LINEAR PROGRAMMING C H A P T E R 7 INTRODUCTION In decision making, when there is only one limiting factor (scarce resource), we can rank the products according the contribution per unit of scarce resource.

Chapter 23 Performance Evaluation for Decentralized Operations Study Guide Solutions Fill-in-the-Blank Equations. Exercises

Chapter 23 Performance Evaluation for Decentralized Operations Study Guide Solutions Fill-in-the-Blank Equations 1. Service department expense 2. Income from operations 3. Profit margin 4. Invested assets

Chapter 23 Performance Evaluation for Decentralized Operations Study Guide Solutions Fill-in-the-Blank Equations 1. Service department expense 2. Income from operations 3. Profit margin 4. Invested assets

ALL IN ONE MGT 402 MIDTERM PAPERS MORE THAN ( 10 )

") ALL IN ONE MGT 402 MIDTERM PAPERS MORE THAN ( 10 ) MIDTERM EXAMINATION MGT402- Cost & Management Accounting Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process costing to calculate

ALL IN ONE MGT 402 MIDTERM PAPERS MORE THAN ( 10 ) MIDTERM EXAMINATION MGT402- Cost & Management Accounting Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process costing to calculate

Course # Cost Management : Accounting and Control

Course # 171023 Cost Management : Accounting and Control based on the electronic.pdf file(s): Cost Management : Accounting and Control by: Dr. Jae K. Shim, Ph.D., 2009, 306 pages 20 CPE Credit Hours Accounting

Course # 171023 Cost Management : Accounting and Control based on the electronic.pdf file(s): Cost Management : Accounting and Control by: Dr. Jae K. Shim, Ph.D., 2009, 306 pages 20 CPE Credit Hours Accounting

UNIVERSITY OF TOLEDO INTERNAL AUDIT DEPARTMENT DEVELOP BUDGETS

The following control objectives provide a basis for strengthening your control environment for the process of developing budgets. When you select an objective, you will access a list of the associated

The following control objectives provide a basis for strengthening your control environment for the process of developing budgets. When you select an objective, you will access a list of the associated

Institute of Certified Management Accountants of Sri Lanka

Copyright Reserved Serial No Foundation Level Pilot Paper Instructions to Candidates 1. Time allowed is two (2) hours. 2. Total 100 Marks. 3. Answer all questions. 4. Encircle the number of your choice

Copyright Reserved Serial No Foundation Level Pilot Paper Instructions to Candidates 1. Time allowed is two (2) hours. 2. Total 100 Marks. 3. Answer all questions. 4. Encircle the number of your choice

5_MGT402_Spring_2010_Final_Term_Solved_paper

5_MGT402_Spring_2010_Final_Term_Solved_paper http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one BDH produced 30,500 units of Kisty (a product). Each unit of Kisty takes two units

5_MGT402_Spring_2010_Final_Term_Solved_paper http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one BDH produced 30,500 units of Kisty (a product). Each unit of Kisty takes two units

International Financial Markets Prices and Policies. Second Edition Richard M. Levich. Overview. ❿ Measuring Economic Exposure to FX Risk

International Financial Markets Prices and Policies Second Edition 2001 Richard M. Levich 16C Measuring and Managing the Risk in International Financial Positions Chap 16C, p. 1 Overview ❿ Measuring Economic

International Financial Markets Prices and Policies Second Edition 2001 Richard M. Levich 16C Measuring and Managing the Risk in International Financial Positions Chap 16C, p. 1 Overview ❿ Measuring Economic

10,000 units x 24 = 240,000, or 5,000 hours x 48 = 240,000. the actual price of materials per kilogram

NVQ/SVQ Level 4 in Accounting Contributing to the Management of Performance and Enhancement of Value (PEV) (2003 standards) June 2006 SUGGESTED ANSWERS Note: The suggested answers may, in parts, be longer

NVQ/SVQ Level 4 in Accounting Contributing to the Management of Performance and Enhancement of Value (PEV) (2003 standards) June 2006 SUGGESTED ANSWERS Note: The suggested answers may, in parts, be longer

Preparing and using budgets

Osborne Books Tutor Zone Preparing and using budgets Chapter activities Osborne Books Limited, 2013 2 p r e p a r i n g a n d u s i n g b u d g e t s t u t o r z o n e 1 The budgeting environment 1.1 Match

Osborne Books Tutor Zone Preparing and using budgets Chapter activities Osborne Books Limited, 2013 2 p r e p a r i n g a n d u s i n g b u d g e t s t u t o r z o n e 1 The budgeting environment 1.1 Match