Let s trace the budgets through for a company called the Hayes Company. Sales Budget The first budget prepared, comes from the Sales Forecast

|

|

|

- Lawrence Carr

- 5 years ago

- Views:

Transcription

1 Let s trace the budgets through for a company called the Hayes Company. Sales Budget The first budget prepared, comes from the Sales Forecast Expected sales volume: 3,000 units in the first quarter with 500-unit increases in each succeeding quarter. Sales price: $60 per unit. Production Budget Shows units that must be produced to meet anticipated sales Hayes Co. believes it can meet future sales needs with an ending inventory of 20% of next quarter s budgeted sales volume.

and cost of direct labor needed to meet production requirements Direct labor hours are determined from the production budget.")

2 Direct Materials Budget Shows both quantity and cost of direct materials to be purchased Because of its close proximity to suppliers, Hayes Company maintains an ending inventory of raw materials equal to 10% of the next quarter s production requirements. The manufacture of each Rightride requires 2 pounds of raw materials, and the expected cost per pound is $4. Assume that the desired ending direct materials amount is 1,020 pounds for the fourth quarter of Direct Labor Budget Shows quantity (hours) and cost of direct labor needed to meet production requirements Direct labor hours are determined from the production budget. At Hayes Company, two hours of direct labor are required to produce each unit of finished goods. The anticipated hourly wage rate is $10.

3 Manufacturing Overhead Budget Distinguishes between fixed and variable overhead costs Hayes Company expects variable costs to fluctuate with production volume on the basis of the following rates per direct labor hour: indirect materials $1.00, indirect labor $1.40, utilities $0.40, and maintenance $0.20. Thus, for the 6,200 direct labor hours to produce 3,100 units, budgeted indirect materials are $6,200 (6,200 x $1), and budgeted indirect labor is $8,680 (6,200 x $1.40). Hayes also recognizes that some maintenance is fixed. The amounts reported for fixed costs are assumed.

. Hayes expects sales in the first quarter to be 3,000 units.")

4 Selling and Administrative Expense Budget Projects anticipated operating expenses; broken out by fixed and variable costs Variable expense rates per unit of sales are sales commissions $3 and freight-out $1. Variable expenses per quarter are based on the unit sales from the sales budget (Illustration 9-3). Hayes expects sales in the first quarter to be 3,000 units. Fixed expenses are based on assumed data. Budgeted Income Statement Shows expected profitability of operations and is a way to evaluate company performance To find the cost of goods sold, it is first necessary to determine the total unit cost of producing one Rightride, as follows. Second, determine Cost of Goods Sold by multiplying units sold times unit cost: 15,000 units x $44 = $660,000

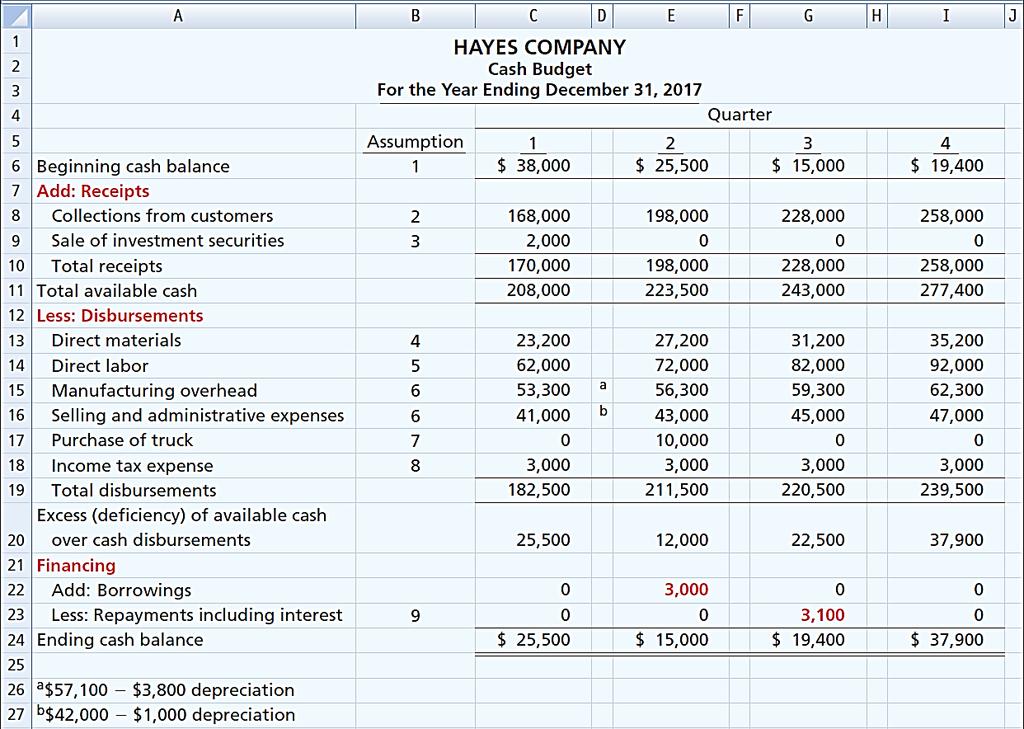

Section and Cash Payments for direct materials Hayes Company Assumptions 1. The January 1, 2017, cash balance is expected to be $38,000.")

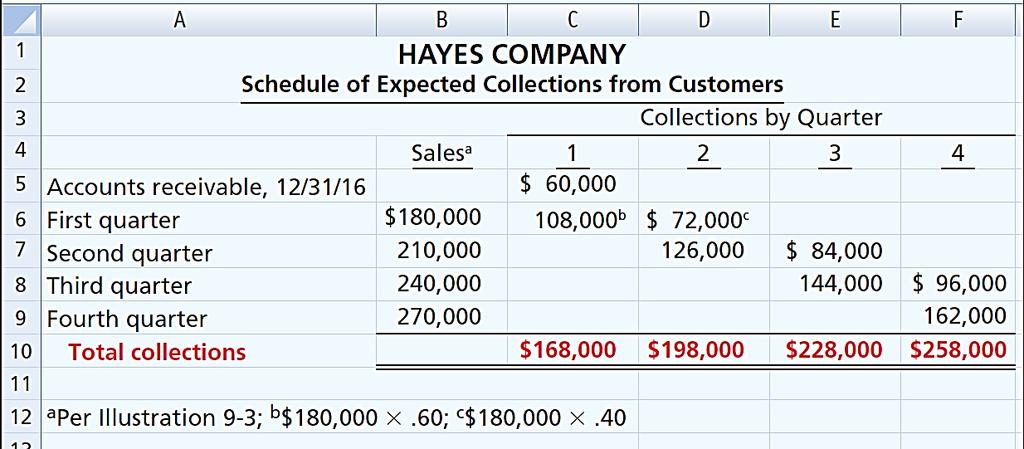

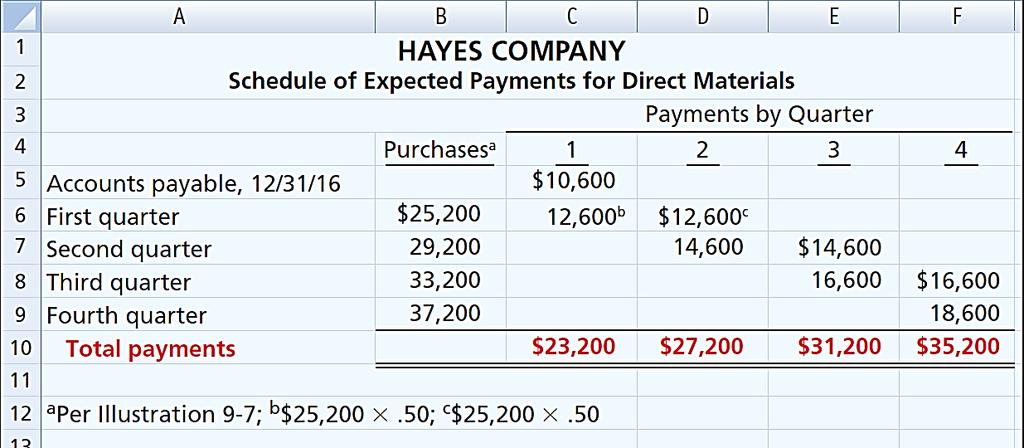

5 All data for the income statement come from the individual operating budgets except the following: (1) interest expense is expected to be $100, and (2) income taxes are estimated to be $12,000. Cash Budget: Cash Receipts (schedule of collections) Section and Cash Payments for direct materials Hayes Company Assumptions 1. The January 1, 2017, cash balance is expected to be $38,000. Hayes wishes to maintain a balance of at least $15, Sales (Illustration 9-3): 60% are collected in the quarter sold and 40% are collected in the following quarter. Accounts receivable of $60,000 at December 31, 2016, are expected to be collected in full in the first quarter of Short-term investments are expected to be sold for $2,000 cash in the first quarter. 4. Direct materials (Illustration 9-7): 50% are paid in the quarter purchased and 50% are paid in the following quarter. Accounts payable of $10,600 at December 31, 2016, are expected to be paid in full in the first quarter of Direct labor (Illustration 9-9): 100% is paid in the quarter incurred. 6. Manufacturing overhead (Illustration 9-10) and selling and administrative expenses (Illustration 9-11): All items except depreciation are paid in the quarter incurred. 7. Management plans to purchase a truck in the second quarter for $10,000 cash. 8. Hayes makes equal quarterly payments of its estimated annual income taxes. 9. Loans are repaid in the earliest quarter in which there is sufficient cash (that is, when the cash on hand exceeds the $15,000 minimum required balance). Prepare a schedule of collections from customers.

6

7

8 Budgeted Balance Sheet Developed from budgeted balance sheet for preceding year and budgets for current year Pertinent data from the budgeted balance sheet at December 31, 2016, are as follows. Buildings and equipment $182,000 Common stock 225,000 Accumulated depreciation 28,800 Retained earnings 46,480

Budgetary Planning. Managerial Accounting, Fourth Edition. Chapter 9-2

9-1 CHAPTER 9 Budgetary Planning Managerial Accounting, Fourth Edition 9-2 Study Objectives 1. Indicate the benefits of budgeting. 2. State the essentials of effective budgeting. 3. Identify the budgets

9-1 CHAPTER 9 Budgetary Planning Managerial Accounting, Fourth Edition 9-2 Study Objectives 1. Indicate the benefits of budgeting. 2. State the essentials of effective budgeting. 3. Identify the budgets

Spring Manufacturing Company Sales Budget 2007

8-56 Comprehensive Profit Plan (90 minutes) 1. Sales Budget Sales Budget Sales (in units) 12,000 9,000 21,000 x Selling Price Per Unit $150 $220 Total Sales Revenue $1,800,000 $1,980,000 $3,780,000 2.

8-56 Comprehensive Profit Plan (90 minutes) 1. Sales Budget Sales Budget Sales (in units) 12,000 9,000 21,000 x Selling Price Per Unit $150 $220 Total Sales Revenue $1,800,000 $1,980,000 $3,780,000 2.

Exam: RR - Budgeting; Standard Cost Accounting

Exam: 061572RR - Budgeting; Standard Cost Accounting When you have completed your exam and reviewed your answers, click Submit Exam. Answers will not be recorded until you hit Submit Exam. If you need

Exam: 061572RR - Budgeting; Standard Cost Accounting When you have completed your exam and reviewed your answers, click Submit Exam. Answers will not be recorded until you hit Submit Exam. If you need

Standard Cost System Practice Problems

When setting up a standard cost system, the concepts of standards in material, labor, and overhead must be explored in a simple manner to start the process. Practice Standard Cost Variances: Simple Example

When setting up a standard cost system, the concepts of standards in material, labor, and overhead must be explored in a simple manner to start the process. Practice Standard Cost Variances: Simple Example

LO 1: Budgeting. Terms Budget Sales forecast Budget committee Participative budgeting Budgetary slack

Terms Budget Sales forecast Budget committee Participative budgeting Budgetary slack LO 1: Budgeting Long-range planning Master budget Operating budget Financial budget Benefits of Budgeting: Planning

Terms Budget Sales forecast Budget committee Participative budgeting Budgetary slack LO 1: Budgeting Long-range planning Master budget Operating budget Financial budget Benefits of Budgeting: Planning

STANDARD COSTS AND VARIANCE ANALYSIS

STANDARD COSTS AND VARIANCE ANALYSIS Key Terms and Concepts to Know Static or Planning Budgets Used for planning purposes Prepared at the beginning of the period Based on one projected level of activity

STANDARD COSTS AND VARIANCE ANALYSIS Key Terms and Concepts to Know Static or Planning Budgets Used for planning purposes Prepared at the beginning of the period Based on one projected level of activity

Feature Story. Was This the Next Amazon.com? Not Quite

Chapter 9 Budgetary Planning Feature Story Was This the Next Amazon.com? Not Quite So you came up with a great idea for a product. You started a company, and you are selling stuff so fast that you can

Chapter 9 Budgetary Planning Feature Story Was This the Next Amazon.com? Not Quite So you came up with a great idea for a product. You started a company, and you are selling stuff so fast that you can

Budgeted production = (expected sales) + (expected ending inventory) (expected beginning inventory)

+ (expected ending inventory) (expected beginning inventory)") The correct answer is: 86,000 units. Budgeted production is calculated as follows: Budgeted production = (expected sales) + (expected ending inventory) (expected beginning inventory) The expected ending

The correct answer is: 86,000 units. Budgeted production is calculated as follows: Budgeted production = (expected sales) + (expected ending inventory) (expected beginning inventory) The expected ending

BUDGETING AND PROFIT PLANNING

BUDGETING AND PROFIT PLANNING Key Terms and Concepts to Know Profit Planning and Budgeting: Profit plan is the steps taken by the business to achieve their planned levels of profits. Budget is a quantitative

BUDGETING AND PROFIT PLANNING Key Terms and Concepts to Know Profit Planning and Budgeting: Profit plan is the steps taken by the business to achieve their planned levels of profits. Budget is a quantitative

January 10,000 units February 15,000 units. 15,000 units

In Class #9.1 Prepare the sales budget Royal Company is preparing budgets for the quarter ending June 30 th. Actual sales for January to March are as follows: Month Sales Budget January 10,000 units February

In Class #9.1 Prepare the sales budget Royal Company is preparing budgets for the quarter ending June 30 th. Actual sales for January to March are as follows: Month Sales Budget January 10,000 units February

Budgeting planning. Breakers, Inc. is preparing budgets for the quarter ending June 30. Budgeted sales for the next five months are:

Budgeting planning We use budgets as a target that we hope or expect to achieve. These are financial and non-financial in nature, but typically offer some quantitative measure We will begin by talking

Budgeting planning We use budgets as a target that we hope or expect to achieve. These are financial and non-financial in nature, but typically offer some quantitative measure We will begin by talking

I Team-based approach to budgeting

I-21.03 Team-based approach to budgeting The electronic spreadsheet version of this problem includes a template based upon the existing budget as displayed within Chapter 21 of the textbook. You may find

I-21.03 Team-based approach to budgeting The electronic spreadsheet version of this problem includes a template based upon the existing budget as displayed within Chapter 21 of the textbook. You may find

Profit Planning: REVISION

Profit Planning: REVISION rue / False Questions No statement /F 1 he production budget is typically prepared prior to the sales budget. F 2 One benefit of budgeting is that it coordinates the activities

Profit Planning: REVISION rue / False Questions No statement /F 1 he production budget is typically prepared prior to the sales budget. F 2 One benefit of budgeting is that it coordinates the activities

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47

Time: 60 min Marks: 47") MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240)

Uses of Accounting Information II (ACC 240)") Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review 1) Beginning Raw Materials Inventory $ 3,000 Ending Raw Materials Inventory 4,500 Purchases of Raw Materials

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review 1) Beginning Raw Materials Inventory $ 3,000 Ending Raw Materials Inventory 4,500 Purchases of Raw Materials

Case 07-2 Western Aluminum

Case 07-2 Western Aluminum In conjunction with the annual audit, the controller of Western Aluminum, Inc. ( W or the Company ), provided the audit engagement team with background information about the

Case 07-2 Western Aluminum In conjunction with the annual audit, the controller of Western Aluminum, Inc. ( W or the Company ), provided the audit engagement team with background information about the

2. The budget or schedule that provides necessary input data for the direct-labor budget is the

Student ID: 22099108 Exam: 061683RR - Planning, Performance, Evaluation, and Control When you have completed your exam and reviewed your answers, click Submit Exam. Answers will not be recorded until you

Student ID: 22099108 Exam: 061683RR - Planning, Performance, Evaluation, and Control When you have completed your exam and reviewed your answers, click Submit Exam. Answers will not be recorded until you

No. of Branches (11) Answer (9) questions only

Answer (9) questions only") Answer all Questions First Question: True or False No. of Branches (11) Answer (9) questions only ( /09) (6-9 Minutes) 1- Jacob's Manufacturing sales is equal to production. If Jacob's Manufacturing presented

Answer all Questions First Question: True or False No. of Branches (11) Answer (9) questions only ( /09) (6-9 Minutes) 1- Jacob's Manufacturing sales is equal to production. If Jacob's Manufacturing presented

Chapter 7: FLEXIBLE BUDGETS

Chapter 7: FLEXIBLE BUDGETS & VARIANCE ANALYSIS Horngren 13e 1 Learning Objective 1: Distinguish a static budget... the master budget based on output planned at start of period from a flexible budget...

Chapter 7: FLEXIBLE BUDGETS & VARIANCE ANALYSIS Horngren 13e 1 Learning Objective 1: Distinguish a static budget... the master budget based on output planned at start of period from a flexible budget...

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240)

Uses of Accounting Information II (ACC 240)") Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review (Yellow) 1) Beginning Raw Materials Inventory $ 1 Ending Raw Materials Inventory 3 Purchases of Raw Materials

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review (Yellow) 1) Beginning Raw Materials Inventory $ 1 Ending Raw Materials Inventory 3 Purchases of Raw Materials

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240)

Uses of Accounting Information II (ACC 240)") Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review (Blue) 1) Beginning Raw Materials Inventory $ 3 Ending Raw Materials Inventory 5 Purchases of Raw Materials

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review (Blue) 1) Beginning Raw Materials Inventory $ 3 Ending Raw Materials Inventory 5 Purchases of Raw Materials

MBP1133 Managerial Accounting Prepared by Dr Khairul Anuar

1 MBP1133 Managerial Accounting Prepared by Dr Khairul Anuar L9 Master Budgeting www.notes638.wordpress.com 2 Learning Objective 1 Understand why organizations budget and the processes they use to create

1 MBP1133 Managerial Accounting Prepared by Dr Khairul Anuar L9 Master Budgeting www.notes638.wordpress.com 2 Learning Objective 1 Understand why organizations budget and the processes they use to create

Financial Management Bachelors of Business (Specialized in Finance) Tutorial Questions Chapter 1: Introduction to Cost Accounting

Tutorial Questions Chapter 1: Introduction to Cost Accounting") Financial Management Bachelors of Business (Specialized in Finance) Tutorial Questions Chapter 1: Introduction to Cost Accounting 1 Practice Questions Question 1 Cost Accounting System is neither unnecessary

Financial Management Bachelors of Business (Specialized in Finance) Tutorial Questions Chapter 1: Introduction to Cost Accounting 1 Practice Questions Question 1 Cost Accounting System is neither unnecessary

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240)

Uses of Accounting Information II (ACC 240)") Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review 1) Beginning Raw Materials Inventory $ 1 Ending Raw Materials Inventory 3 Purchases of Raw Materials 6 Direct

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review 1) Beginning Raw Materials Inventory $ 1 Ending Raw Materials Inventory 3 Purchases of Raw Materials 6 Direct

Write your answers in blue or black ink/ballpoint. Pencil may be used only for graphs, charts, diagrams, etc.

Series 3 Examination 2008 COST ACCOUNTING Level 3 Friday 6 June Subject Code: 3016 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your answers

Series 3 Examination 2008 COST ACCOUNTING Level 3 Friday 6 June Subject Code: 3016 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your answers

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240)

Uses of Accounting Information II (ACC 240)") Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review 1) Beginning Raw Materials Inventory $ 1,000 Ending Raw Materials Inventory 2,500 Purchases of Raw Materials

Managerial Accounting (ACC 212) Uses of Accounting Information II (ACC 240) Final Exam Review 1) Beginning Raw Materials Inventory $ 1,000 Ending Raw Materials Inventory 2,500 Purchases of Raw Materials

1 Exam Prep Builder s Guide to Accounting (2)

") 1 Exam Prep Builder s Guide to Accounting (2) 1. All the following are normally required for a loan application except. A. an income statement B. a balance sheet C. a tax return D. retained earnings 2.

1 Exam Prep Builder s Guide to Accounting (2) 1. All the following are normally required for a loan application except. A. an income statement B. a balance sheet C. a tax return D. retained earnings 2.

Chapter 4: Job Costing

Chapter 4: Job Costing Costing System Terminology: Cost Object Anything for which a separate measurement of costs is desired. Direct Cost Costs that are related to a particular cost object in an economically

Chapter 4: Job Costing Costing System Terminology: Cost Object Anything for which a separate measurement of costs is desired. Direct Cost Costs that are related to a particular cost object in an economically

Product costing (process costing) In Class Exercise

In Class Exercise") Product costing (process costing) In Class Exercise makes stained glass lamps. Production process uses two departments: cutting department and assembly department where they are put together. Record the

Product costing (process costing) In Class Exercise makes stained glass lamps. Production process uses two departments: cutting department and assembly department where they are put together. Record the

Planning and Control. Control involves the steps taken by management that attempt to ensure the objectives are attained.

Profit Planning Planning and Control Planning -- involves developing objectives and preparing various budgets to achieve these objectives. Control involves the steps taken by management that attempt to

Profit Planning Planning and Control Planning -- involves developing objectives and preparing various budgets to achieve these objectives. Control involves the steps taken by management that attempt to

P8_Practice Test Paper_Syl12_Dec2013_Set 1

Full Marks: 100 Paper 8 : Cost Accounting and Financial Management Time : 3 hours This question paper is divided into two sections, Section A- Cost Accounting (60 marks) and Section B - Financial Management

Full Marks: 100 Paper 8 : Cost Accounting and Financial Management Time : 3 hours This question paper is divided into two sections, Section A- Cost Accounting (60 marks) and Section B - Financial Management

(AA22) COST ACCOUNTING AND REPORTING

COST ACCOUNTING AND REPORTING") All Rights Reserved ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA AA2 EXAMINATION - JANUARY 2017 (AA22) COST ACCOUNTING AND REPORTING Instructions to candidates (Please Read Carefully): (1) Time Allowed:

All Rights Reserved ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA AA2 EXAMINATION - JANUARY 2017 (AA22) COST ACCOUNTING AND REPORTING Instructions to candidates (Please Read Carefully): (1) Time Allowed:

Multiple Choice Questions

Multiple Choice Questions 1. The difference between the actual price and the standard price, multiplied by the actual quantity of materials purchased is the a) direct labor price variance b) direct labor

Multiple Choice Questions 1. The difference between the actual price and the standard price, multiplied by the actual quantity of materials purchased is the a) direct labor price variance b) direct labor

Elements of costing (ELCO) Question and answer book

Question and answer book") Elements of costing (ELCO) Question and answer book October 2018 AAT is a registered charity. No. 1050724 Questions Question 1 If the total cost of 3,000 units is 6,750 and the total cost of 3,900 units

Elements of costing (ELCO) Question and answer book October 2018 AAT is a registered charity. No. 1050724 Questions Question 1 If the total cost of 3,000 units is 6,750 and the total cost of 3,900 units

322 Roll No : 1 : Time allowed : 3 hours Maximum marks : 100

2/2013/CMA (N/S) Roll No : 1 : Time allowed : 3 hours Maximum marks : 100 Total number of questions : 6 Total number of printed pages : 7 NOTE : 1. Answer ALL Questions. 2. All working notes should be

2/2013/CMA (N/S) Roll No : 1 : Time allowed : 3 hours Maximum marks : 100 Total number of questions : 6 Total number of printed pages : 7 NOTE : 1. Answer ALL Questions. 2. All working notes should be

Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced Level

Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced Level ACCOUNTING 9706/31 Paper 3 Structured Questions October/November 2017 3 hours No Additional Materials

Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced Level ACCOUNTING 9706/31 Paper 3 Structured Questions October/November 2017 3 hours No Additional Materials

CS Executive Programme Module - I December Paper - 2 : Cost and Management Accounting

ISBN : 978-93-5034-747-8 Solved Scanner Appendix CS Executive Programme Module - I December - 2013 Paper - 2 : Cost and Management Accounting Chapter - 1 : Introduction to Cost and Management Accounting

ISBN : 978-93-5034-747-8 Solved Scanner Appendix CS Executive Programme Module - I December - 2013 Paper - 2 : Cost and Management Accounting Chapter - 1 : Introduction to Cost and Management Accounting

HANDOUT FOR WEEK 3 UNDERSTANDING THE INCOME STATEMENT. (Profit and loss statement)

") HANDOUT FOR WEEK 3 UNDERSTANDING THE INCOME STATEMENT Introduction (Profit and loss statement) The financial account system generates and important report that captures the financial performance of the

HANDOUT FOR WEEK 3 UNDERSTANDING THE INCOME STATEMENT Introduction (Profit and loss statement) The financial account system generates and important report that captures the financial performance of the

Chapter 16 Fundamentals of Variance Analysis

Chapter 16 Fundamentals of Variance Analysis True / False Questions 1. In essence, the terms "master budget" and "operating budget" mean the same thing and can be used interchangeably. True False 2. Variances

Chapter 16 Fundamentals of Variance Analysis True / False Questions 1. In essence, the terms "master budget" and "operating budget" mean the same thing and can be used interchangeably. True False 2. Variances

Prepare the following budgets for the year, showing both quarterly and total figures:

Page 1 of 7 Question 1 Mynor Corporation manufactures and sells a seasonal product that has peak sales in the third quarter. The following information concerns operation for Year 2-the coming year-and

Page 1 of 7 Question 1 Mynor Corporation manufactures and sells a seasonal product that has peak sales in the third quarter. The following information concerns operation for Year 2-the coming year-and

D.K.M COLLEGE FOR WOMEN (AUTONOMOUS),VELLORE-1. PG & RESEARCH DEPARTMENT OF COMMERCE ACCOUNTING AND BUSINESS FOR MANAGERS BSC - ISM

,VELLORE-1. PG & RESEARCH DEPARTMENT OF COMMERCE ACCOUNTING AND BUSINESS FOR MANAGERS BSC - ISM") D.K.M COLLEGE FOR WOMEN (AUTONOMOUS),VELLORE1. PG & RESEARCH DEPARTMENT OF COMMERCE ACCOUNTING AND BUSINESS FOR MANAGERS BSC ISM UNIT I SECTION A 2 MARKS 1. Define Accounting. 2. What is Journal? 3. Write

D.K.M COLLEGE FOR WOMEN (AUTONOMOUS),VELLORE1. PG & RESEARCH DEPARTMENT OF COMMERCE ACCOUNTING AND BUSINESS FOR MANAGERS BSC ISM UNIT I SECTION A 2 MARKS 1. Define Accounting. 2. What is Journal? 3. Write

Job Costing Cost Accounting Horngreen, Datar, Foster 1

Job Costing 1 Building Block Concepts of Costing Systems The following five terms constitute the building blocks that will be used in this chapter: 1 A cost object is anything for which a separate measurement

Job Costing 1 Building Block Concepts of Costing Systems The following five terms constitute the building blocks that will be used in this chapter: 1 A cost object is anything for which a separate measurement

24 Control through standard costs

24 Control through standard costs 24.1 Learning objectives After studying this chapter, you should be able to: Discuss the nature of standard costs, including how standards are set. Define budgets and

24 Control through standard costs 24.1 Learning objectives After studying this chapter, you should be able to: Discuss the nature of standard costs, including how standards are set. Define budgets and

McGraw-Hill /Irwin McGraw-Hill /Irwin McGraw-Hill /Irwin McGraw-Hill /Irwin Advantages McGraw-Hill /Irwin McGraw-Hill /Irwin

7-1 Today s LEcture Management Accounting Lecture 11 (Chapter 7) Profit Planning n What is a n Why and how organizations n ing n Sales n Production n Sales & Administration n Balance Sheet Items n Working

7-1 Today s LEcture Management Accounting Lecture 11 (Chapter 7) Profit Planning n What is a n Why and how organizations n ing n Sales n Production n Sales & Administration n Balance Sheet Items n Working

The Basic Framework of Budgeting

7-1 The Basic Framework of Budgeting A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. 1. The act of preparing a budget

7-1 The Basic Framework of Budgeting A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. 1. The act of preparing a budget

BALIUAG UNIVERSITY CPA REVIEW MANAGEMENT ADVISORY SERVICES STANDARD COST AND VARIANCE ANALYSIS THEORY

STANDARD COST AND VARIANCE ANALYSIS THEORY 1. How is labor rate variance computed? a. The difference between standard and actual rate multiplied by actual hours b. The difference between standard and actual

STANDARD COST AND VARIANCE ANALYSIS THEORY 1. How is labor rate variance computed? a. The difference between standard and actual rate multiplied by actual hours b. The difference between standard and actual

Write your answers in blue or black ink/ballpoint. Pencil may be used only for graphs, charts, diagrams, etc.

Series 4 Examination 2008 COST ACCOUNTING Level 3 Tuesday 11 November Subject Code: 3016 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Series 4 Examination 2008 COST ACCOUNTING Level 3 Tuesday 11 November Subject Code: 3016 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

WEEK 6 OPERATING BUDGETS (MANUFACTURING ORGANISATIONS) Case Study. The budgets that you need to prepare include:

Case Study. The budgets that you need to prepare include:") WEEK 6 OPERATING BUDGETS (MANUFACTURING ORGANISATIONS) Case Study manufactures cardboard boxes which are used for transporting very special toys to toy stores all around Australia. You have already been

WEEK 6 OPERATING BUDGETS (MANUFACTURING ORGANISATIONS) Case Study manufactures cardboard boxes which are used for transporting very special toys to toy stores all around Australia. You have already been

PTP_Intermediate_Syllabus 2012_Dec 2015_Set 2 Paper 8: Cost Accounting & Financial Management

Paper 8: Cost Accounting & Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Pg 1 LEVEL B PTP_Intermediate_Syllabus 2012_Dec

Paper 8: Cost Accounting & Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Pg 1 LEVEL B PTP_Intermediate_Syllabus 2012_Dec

MTP_Intermediate_Syllabus 2012_Jun2017_Set 2 Paper 8- Cost Accounting & Financial Management

Paper 8- Cost Accounting & Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-8: Cost Accounting & Financial

Paper 8- Cost Accounting & Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-8: Cost Accounting & Financial

The Economic Impact of Rail Improvements to the Port of Corpus Christi, Texas

The Economic Impact of Rail Improvements to the Port of Corpus Christi, Texas Prepared For: Prepared By: October 17, 2011 1 Table of Contents Executive Summary... 3 Background... 4 Methodology... 5 Definition

The Economic Impact of Rail Improvements to the Port of Corpus Christi, Texas Prepared For: Prepared By: October 17, 2011 1 Table of Contents Executive Summary... 3 Background... 4 Methodology... 5 Definition

COST ANALYSIS. Semester II 2010/11

COST ANALYSIS Semester II 2010/11 A function that defines the minimum possible cost of producing each output level when variable factors are employed in the cost minimizing manner Historical cost: The

COST ANALYSIS Semester II 2010/11 A function that defines the minimum possible cost of producing each output level when variable factors are employed in the cost minimizing manner Historical cost: The

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Advanced Subsidiary Level and Advanced Level

*1011372598* UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Advanced Subsidiary Level and Advanced Level ACCOUNTING 9706/12 Paper 1 Multiple Choice October/November

*1011372598* UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Advanced Subsidiary Level and Advanced Level ACCOUNTING 9706/12 Paper 1 Multiple Choice October/November

Download full Test Bank for Accounting and Finance for Non Specialists 6th Edition by Atrill and McLaney

Download full Test Bank for Accounting and Finance for Non Specialists 6th Edition by Atrill and McLaney https://digitalcontentmarket.org/download/test-bank-for-accountingand-finance-for-non-specialists-6th-edition-by-atrill-and-mclaney

Download full Test Bank for Accounting and Finance for Non Specialists 6th Edition by Atrill and McLaney https://digitalcontentmarket.org/download/test-bank-for-accountingand-finance-for-non-specialists-6th-edition-by-atrill-and-mclaney

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Advanced Subsidiary Level and Advanced Level

*8018806549* UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Advanced Subsidiary Level and Advanced Level ACCOUNTING 9706/02 Paper 2 Structured Questions May/June 2007

*8018806549* UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Advanced Subsidiary Level and Advanced Level ACCOUNTING 9706/02 Paper 2 Structured Questions May/June 2007

Manufacturing Accounts

All questions copyright of Cambridge International Examinations 1 Manufacturing Accounts All questions copyright of Cambridge International Examinations 2 2 1 The following balances were extracted from

All questions copyright of Cambridge International Examinations 1 Manufacturing Accounts All questions copyright of Cambridge International Examinations 2 2 1 The following balances were extracted from

Add: manufacturing overhead costs in inventory under absorption costing +27,000 Net operating income under absorption costing $4,727,000

THE HONG KONG POLYTECHNIC UNIVERSITY HONG KONG COMMUNITY COLLEGE Subject Title : Cost Accounting Subject Code : CCN2111 Session : Semester One, 2018/19 Numerical Answer Question B1 Required production

THE HONG KONG POLYTECHNIC UNIVERSITY HONG KONG COMMUNITY COLLEGE Subject Title : Cost Accounting Subject Code : CCN2111 Session : Semester One, 2018/19 Numerical Answer Question B1 Required production

Project Cost Management

PDHonline Course P104 (8 PDH) Project Cost Management Instructor: William J. Scott, P.E. 2012 PDH Online PDH Center 5272 Meadow Estates Drive Fairfax, VA 22030-6658 Phone & Fax: 703-988-0088 www.pdhonline.org

PDHonline Course P104 (8 PDH) Project Cost Management Instructor: William J. Scott, P.E. 2012 PDH Online PDH Center 5272 Meadow Estates Drive Fairfax, VA 22030-6658 Phone & Fax: 703-988-0088 www.pdhonline.org

Income Statement. for the financial year ended 31 March 2011

Income Statement for the financial year ended 31 March Continuing operations Revenue 5 1,220,183 1,141,964 Other income 6 3,776 2,350 Share of net loss of associate accounted for using the equity method

Income Statement for the financial year ended 31 March Continuing operations Revenue 5 1,220,183 1,141,964 Other income 6 3,776 2,350 Share of net loss of associate accounted for using the equity method

PAPER 10: COST & MANAGEMENT ACCOUNTANCY

PAPER 10: COST & MANAGEMENT ACCOUNTANCY Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 LEVEL B MTP_Intermediate_Syllabus 2012_Jun2015_Set

PAPER 10: COST & MANAGEMENT ACCOUNTANCY Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 LEVEL B MTP_Intermediate_Syllabus 2012_Jun2015_Set

Analyzing Financial Performance Reports

Analyzing Financial Performance Reports Calculating Variances Effective systems identify variances down to the lowest level of management. Variances are hierarchical. As shown in Exhibit 10.2, they begin

Analyzing Financial Performance Reports Calculating Variances Effective systems identify variances down to the lowest level of management. Variances are hierarchical. As shown in Exhibit 10.2, they begin

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Advanced Subsidiary Level and Advanced Level

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Advanced Subsidiary Level and Advanced Level *7802200239* ACCOUNTING 9706/22 Paper 2 Structured Questions May/June 2012

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Advanced Subsidiary Level and Advanced Level *7802200239* ACCOUNTING 9706/22 Paper 2 Structured Questions May/June 2012

Preparing and using budgets

Osborne Books Tutor Zone Preparing and using budgets Chapter activities Osborne Books Limited, 2013 2 p r e p a r i n g a n d u s i n g b u d g e t s t u t o r z o n e 1 The budgeting environment 1.1 Match

Osborne Books Tutor Zone Preparing and using budgets Chapter activities Osborne Books Limited, 2013 2 p r e p a r i n g a n d u s i n g b u d g e t s t u t o r z o n e 1 The budgeting environment 1.1 Match

COST ACCOUNTING STANDARD ON MATERIAL COST

CAS-6 (REVISED 2017) COST ACCOUNTING STANDARD ON MATERIAL COST The following is the COST ACCOUNTING STANDARD 6 (CAS 6) (Revised 2017) issued by the Council of The Institute of Cost Accountants of India

CAS-6 (REVISED 2017) COST ACCOUNTING STANDARD ON MATERIAL COST The following is the COST ACCOUNTING STANDARD 6 (CAS 6) (Revised 2017) issued by the Council of The Institute of Cost Accountants of India

B.COM II ADVANCED AND COST ACCOUNTING

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

(AA22) COST ACCOUNTING AND REPORTING

COST ACCOUNTING AND REPORTING") All Rights Reserved ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA AA2 EXAMINATION - JULY 2016 (AA22) COST ACCOUNTING AND REPORTING Instructions to candidates (Please Read Carefully): (1) Time Allowed:

All Rights Reserved ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA AA2 EXAMINATION - JULY 2016 (AA22) COST ACCOUNTING AND REPORTING Instructions to candidates (Please Read Carefully): (1) Time Allowed:

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Advanced Level

*1480859732* UNIVERSITY OF MRIGE INTERNTIONL EXMINTIONS General ertificate of Education dvanced Level OUNTING 9706/33 Paper 3 Multiple hoice October/November 2011 1 hour dditional Materials: Multiple hoice

*1480859732* UNIVERSITY OF MRIGE INTERNTIONL EXMINTIONS General ertificate of Education dvanced Level OUNTING 9706/33 Paper 3 Multiple hoice October/November 2011 1 hour dditional Materials: Multiple hoice

FINALTERM EXAMINATION Spring 2010 MGT402- Cost & Management Accounting (Session - 4) Solved by Mehreen Humayun vuzs Team.

Solved by Mehreen Humayun vuzs Team.") FINALTERM EXAMINATION Spring 2010 MGT402- Cost & Management Accounting (Session - 4) Solved by Mehreen Humayun vuzs Team Time: 90 min Marks: 69 Question No: 1 ( Marks: 1 ) - Please choose one Cost of finished

FINALTERM EXAMINATION Spring 2010 MGT402- Cost & Management Accounting (Session - 4) Solved by Mehreen Humayun vuzs Team Time: 90 min Marks: 69 Question No: 1 ( Marks: 1 ) - Please choose one Cost of finished

Managerial Work4Me Accounting Simulations. Problem Seven

Managerial Work4Me Accounting Simulations 1 st Web-Based Edition Problem Seven Profit Planning Page 1 INTRODUCTION Starlight Packaging produces a single product that it sells to public storage facilities.

Managerial Work4Me Accounting Simulations 1 st Web-Based Edition Problem Seven Profit Planning Page 1 INTRODUCTION Starlight Packaging produces a single product that it sells to public storage facilities.

Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced Level

Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced Level ACCOUNTING 9706/22 Paper 2 Structured Questions May/June 2016 1 hour 30 minutes Candidates answer on

Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced Level ACCOUNTING 9706/22 Paper 2 Structured Questions May/June 2016 1 hour 30 minutes Candidates answer on

MARK SCHEME for the October/November 2014 series 9706 ACCOUNTING

CAMBRIDGE INTERNATIONAL EXAMINATIONS Cambridge International Advanced Subsidiary and Advanced Level MARK SCHEME for the October/November 2014 series 9706 ACCOUNTING 9706/22 Paper 2 (Structured Questions

CAMBRIDGE INTERNATIONAL EXAMINATIONS Cambridge International Advanced Subsidiary and Advanced Level MARK SCHEME for the October/November 2014 series 9706 ACCOUNTING 9706/22 Paper 2 (Structured Questions

Online Course Manual By Craig Pence. Module 7

Online Course Manual By Craig Pence Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled

Online Course Manual By Craig Pence Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled

Basic Concepts: Assets & Liabilities

Basic Concepts: Assets & Liabilities I. Accounting for Inventories & Cost of Goods Sold ( COGS ) A. Valuing Inventories & COGS - Inventories are valued at lower of acquisition cost or market (LCM) - Cost

Basic Concepts: Assets & Liabilities I. Accounting for Inventories & Cost of Goods Sold ( COGS ) A. Valuing Inventories & COGS - Inventories are valued at lower of acquisition cost or market (LCM) - Cost

MOCK TEST PAPER 1 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING

: GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING") MOCK TEST PAPER 1 INTERMEDIATE (IPC): GROUP I Test Series: February, 2014 PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING Question No. 1 is compulsory. Attempt any five questions

MOCK TEST PAPER 1 INTERMEDIATE (IPC): GROUP I Test Series: February, 2014 PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING Question No. 1 is compulsory. Attempt any five questions

P8_Practice Test Paper_Syl12_Dec13_Set 3

Paper 8 : Cost Accounting and Financial Management Full Marks: 100 Time : 3 hours This question paper is divided into two sections, Section A- Cost Accounting (60 marks) and Section B - Financial Management

Paper 8 : Cost Accounting and Financial Management Full Marks: 100 Time : 3 hours This question paper is divided into two sections, Section A- Cost Accounting (60 marks) and Section B - Financial Management

Final Examination Semester 2 / Year 2011

Southern College Kolej Selatan 南方学院 Final Examination Semester 2 / Year 2011 COURSE : BASIC COSTING COURSE CODE : ACCT2013 TIME : 2 1/2 HOURS DEPARTMENT : FINANCE AND ACCOUNTING LECTURER : GAN HWI SIN

Southern College Kolej Selatan 南方学院 Final Examination Semester 2 / Year 2011 COURSE : BASIC COSTING COURSE CODE : ACCT2013 TIME : 2 1/2 HOURS DEPARTMENT : FINANCE AND ACCOUNTING LECTURER : GAN HWI SIN

Short-Term Financial Planning

Short-Term Financial Planning ...it will if it does not have the cash to meet monthly payroll, quarterly taxes and overdue bills.. Short-Term Financial Planning How to do a lot right things and still get

Short-Term Financial Planning ...it will if it does not have the cash to meet monthly payroll, quarterly taxes and overdue bills.. Short-Term Financial Planning How to do a lot right things and still get

ACCA. Paper F2 and FMA. Management Accounting December 2014 to June Interim Assessment Answers

ACCA Paper F2 and FMA Management Accounting December 204 to June 205 Interim Assessment Answers To gain maximum benefit, do not refer to these answers until you have completed the interim assessment questions

ACCA Paper F2 and FMA Management Accounting December 204 to June 205 Interim Assessment Answers To gain maximum benefit, do not refer to these answers until you have completed the interim assessment questions

CHAPTER 4 JOB COSTING

CHAPTER 4 JOB COSTING 4-1 Define cost pool, cost tracing, cost allocation, and cost-allocation base. Cost pool a grouping of individual indirect cost items. Cost tracing the assigning of direct costs to

CHAPTER 4 JOB COSTING 4-1 Define cost pool, cost tracing, cost allocation, and cost-allocation base. Cost pool a grouping of individual indirect cost items. Cost tracing the assigning of direct costs to

PROJECTED FINANCIAL STATEMENTS FORMAT FOR ENERGY PROJECTS

PROJECTED FINANCIAL STATEMENTS FORMAT FOR ENERGY PROJECTS Projected Income Statement With Income Tax Holiday (ITH) Incentives* With ITH Incentives Sales Less: Sales Commissions and Discounts Net Sales

PROJECTED FINANCIAL STATEMENTS FORMAT FOR ENERGY PROJECTS Projected Income Statement With Income Tax Holiday (ITH) Incentives* With ITH Incentives Sales Less: Sales Commissions and Discounts Net Sales

PAPER 8: COST ACCOUNTING & FINANCIAL MANAGEMENT

PAPER 8: COST ACCOUNTING & FINANCIAL MANAGEMENT Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 LEVEL B MTP_Intermediate_Syllabus 2012_Dec2015_Set

PAPER 8: COST ACCOUNTING & FINANCIAL MANAGEMENT Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 LEVEL B MTP_Intermediate_Syllabus 2012_Dec2015_Set

Introduction to Managerial Accounting and Job Order Cost Systems p. 1 The Differences Between Managerial and Financial Accounting p.

Introduction to Managerial Accounting and Job Order Cost Systems p. 1 The Differences Between Managerial and Financial Accounting p. 2 The Management Accountant in the Organization p. 4 Manufacturing Cost

Introduction to Managerial Accounting and Job Order Cost Systems p. 1 The Differences Between Managerial and Financial Accounting p. 2 The Management Accountant in the Organization p. 4 Manufacturing Cost

Tiill now you have learnt about the financial

Cash Flow Statement 6 LEARNING OBJECTIVES After studying this chapter, you will be able to : state the purpose and preparation of statement of cash flow statement; distinguish between operating activities,

Cash Flow Statement 6 LEARNING OBJECTIVES After studying this chapter, you will be able to : state the purpose and preparation of statement of cash flow statement; distinguish between operating activities,

Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced Level

*1440226124* Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced Level ACCOUNTING 9706/22 Paper 2 Structured Questions October/November 2014 1 hour 30 minutes

*1440226124* Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced Level ACCOUNTING 9706/22 Paper 2 Structured Questions October/November 2014 1 hour 30 minutes

POLYDEX PHARMACEUTICALS LIMITED

POLYDEX PHARMACEUTICALS LIMITED QUARTERLY DISCLOSURE REPORT INDEX ITEM I Name of Issuer Page 3 ITEM II Share Structure Page 3 ITEM III Consolidated Financial Statements Interim Financial Statements Page

POLYDEX PHARMACEUTICALS LIMITED QUARTERLY DISCLOSURE REPORT INDEX ITEM I Name of Issuer Page 3 ITEM II Share Structure Page 3 ITEM III Consolidated Financial Statements Interim Financial Statements Page

Cost Accounting, 14e (Horngren/Datar/Rajan) Chapter 8 Flexible Budgets, Overhead Cost Variances, and Management Control

Chapter 8 Flexible Budgets, Overhead Cost Variances, and Management Control") Cost Accounting, 14e (Horngren/Datar/Rajan) Chapter 8 Flexible Budgets, Overhead Cost Variances, and Management Control Objective 8.1 1) Overhead costs have been increasing due to all of the following

Cost Accounting, 14e (Horngren/Datar/Rajan) Chapter 8 Flexible Budgets, Overhead Cost Variances, and Management Control Objective 8.1 1) Overhead costs have been increasing due to all of the following

Chapter 2 Job-Order Costing: Calculating Unit Product Costs

Managerial Accounting 16th Edition Garrison Solutions Manual Full Download: http://testbanklive.com/download/managerial-accounting-16th-edition-garrison-solutions-manual/ Chapter 2 Job-Order Costing: Calculating

Managerial Accounting 16th Edition Garrison Solutions Manual Full Download: http://testbanklive.com/download/managerial-accounting-16th-edition-garrison-solutions-manual/ Chapter 2 Job-Order Costing: Calculating

Accounting for Management: Concepts & Tools v.2.0- Course Transcript Presented by: TeachUcomp, Inc.

Accounting for Management: Concepts & Tools v.2.0- Course Transcript Presented by: TeachUcomp, Inc. Course Introduction Welcome to Accounting for Management: Concepts and Tools, a presentation of TeachUcomp,

Accounting for Management: Concepts & Tools v.2.0- Course Transcript Presented by: TeachUcomp, Inc. Course Introduction Welcome to Accounting for Management: Concepts and Tools, a presentation of TeachUcomp,

MEASURING GDP AND ECONOMIC GROWTH. Objectives. Gross Domestic Product. An Economic Barometer. Gross Domestic Product. Gross Domestic Product CHAPTER

MEASURING GDP AND ECONOMIC CHAPTER GROWTH Objectives After studying this chapter, you will able to Define GDP and use the circular flow model to explain why GDP equals aggregate expenditure and aggregate

MEASURING GDP AND ECONOMIC CHAPTER GROWTH Objectives After studying this chapter, you will able to Define GDP and use the circular flow model to explain why GDP equals aggregate expenditure and aggregate

Pricing for Services

Pricing for Services 1. Introduction This aid discusses costing and pricing of services to assure that each job earns a reasonable profit. The figures used in the tables and examples do not reflect what

Pricing for Services 1. Introduction This aid discusses costing and pricing of services to assure that each job earns a reasonable profit. The figures used in the tables and examples do not reflect what

JOHN B. SANFILIPPO & SON, INC. NEWS RELEASE

JOHN B. SANFILIPPO & SON, INC. NEWS RELEASE COMPANY CONTACT: Michael J. Valentine Chief Financial Officer 847-214-4509 FOR IMMEDIATE RELEASE MONDAY, NOVEMBER 5, 2007 Net Loss for the First Quarter 2008

JOHN B. SANFILIPPO & SON, INC. NEWS RELEASE COMPANY CONTACT: Michael J. Valentine Chief Financial Officer 847-214-4509 FOR IMMEDIATE RELEASE MONDAY, NOVEMBER 5, 2007 Net Loss for the First Quarter 2008

Examinations for Academic Year Semester I / Academic Year 2015 Semester II. 1. This question paper consists of Section A and Section B.

PROGRAMME COHORT BSc (Hons) Human Resource Management BSc (Hons) Management BHRM/14B/FT BMAN/15A/FT B1, B2 Examinations for Academic Year 2015 2016 Semester I / Academic Year 2015 Semester II MODULE: COST

PROGRAMME COHORT BSc (Hons) Human Resource Management BSc (Hons) Management BHRM/14B/FT BMAN/15A/FT B1, B2 Examinations for Academic Year 2015 2016 Semester I / Academic Year 2015 Semester II MODULE: COST

Cost Accounting: A Managerial Emphasis, 16e, Global Edition (Horngren) Chapter 4 Job Costing

Chapter 4 Job Costing") Cost Accounting: A Managerial Emphasis, 16e, Global Edition (Horngren) Chapter 4 Job Costing 4.1 Objective 4.1 1) A cost is considered direct if it can be traced to a particular cost object in a cost effective

Cost Accounting: A Managerial Emphasis, 16e, Global Edition (Horngren) Chapter 4 Job Costing 4.1 Objective 4.1 1) A cost is considered direct if it can be traced to a particular cost object in a cost effective

Name of business Statement of cash flows for the financial year end 31 December 20X1 (DIRECT METHOD) Inflow /(outflow)

Inflow /(outflow)") Name of business Statement of cash flows for the financial year end 31 December 201 (DIRECT METHOD) Calc Notes Inflow /(outflow) CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers C1 Cash

Name of business Statement of cash flows for the financial year end 31 December 201 (DIRECT METHOD) Calc Notes Inflow /(outflow) CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers C1 Cash

SU 2.1 Accounts Receivable

Part 1 Study Unit 2 SU 2.1 Accounts Receivable Overview Recording receivables, which coincides with revenue recognition, is consistent with the accrual method of accounting. Current Receivables will be

Part 1 Study Unit 2 SU 2.1 Accounts Receivable Overview Recording receivables, which coincides with revenue recognition, is consistent with the accrual method of accounting. Current Receivables will be

Price and Volume Measures Rebasing & Linking

Regional Course on 2008 SNA (Special Topics): Improving Exhaustiveness of GDP coverage 31 August 4 September 2015 Daejeon, Republic of Korea Price and Volume Measures Rebasing & Linking Alick Nyasulu Statistical

Regional Course on 2008 SNA (Special Topics): Improving Exhaustiveness of GDP coverage 31 August 4 September 2015 Daejeon, Republic of Korea Price and Volume Measures Rebasing & Linking Alick Nyasulu Statistical

FNSACC503A: Assessment 2

FNSACC503A: Assessment 2 What you have to do This assessment will test your understanding of budgeting principles and the preparation of sales budgets, operational budgets and cash budgets for a Manufacturing

FNSACC503A: Assessment 2 What you have to do This assessment will test your understanding of budgeting principles and the preparation of sales budgets, operational budgets and cash budgets for a Manufacturing

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 11 & 13. Chapter 11: Standard Costs and Variance Analysis

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 11 & 13 Chapter 11: Standard Costs and Variance Analysis Variance Analysis: calculating variances and investigating

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 11 & 13 Chapter 11: Standard Costs and Variance Analysis Variance Analysis: calculating variances and investigating

Deshbandhu Polymer Limited Statement of Financial Position as at 31 March 2016 Unaudited

Statement of Financial Position as at 31 March 2016 Unaudited Assets Non-Current Assets Note March 31, 2016 June 30, 2015 Taka Taka Property, Plant & Equipment 4 358,848,266 367,468,030 Investment 677,932

Statement of Financial Position as at 31 March 2016 Unaudited Assets Non-Current Assets Note March 31, 2016 June 30, 2015 Taka Taka Property, Plant & Equipment 4 358,848,266 367,468,030 Investment 677,932

Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced Level

*3484335703* ambridge International Examinations ambridge International dvanced Subsidiary and dvanced Level OUNTING 9706/13 Paper 1 Multiple hoice October/November 2017 1 hour dditional Materials: Multiple

*3484335703* ambridge International Examinations ambridge International dvanced Subsidiary and dvanced Level OUNTING 9706/13 Paper 1 Multiple hoice October/November 2017 1 hour dditional Materials: Multiple