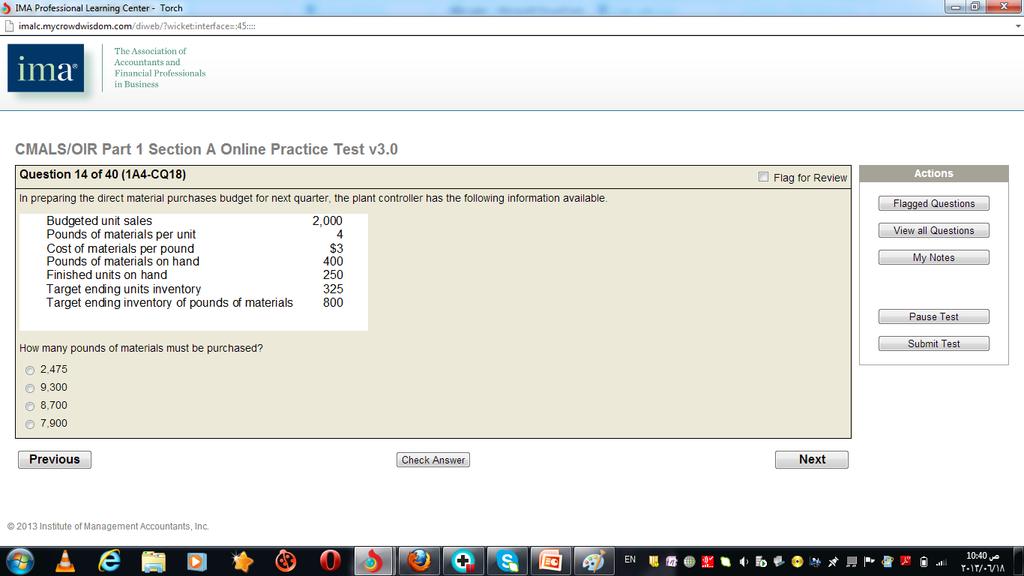

Budgeted production = (expected sales) + (expected ending inventory) (expected beginning inventory)

|

|

|

- Byron McLaughlin

- 6 years ago

- Views:

Transcription

1

2

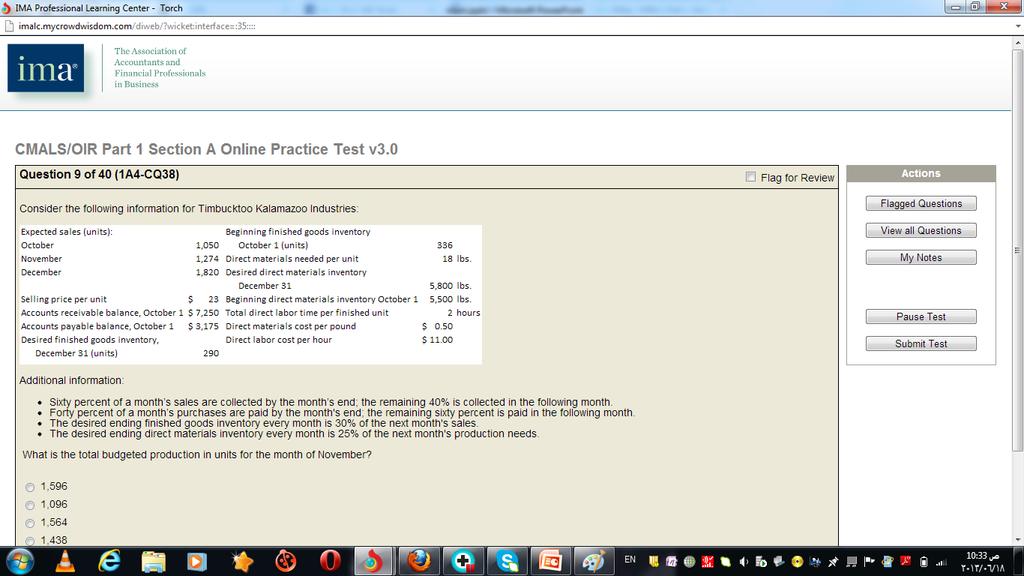

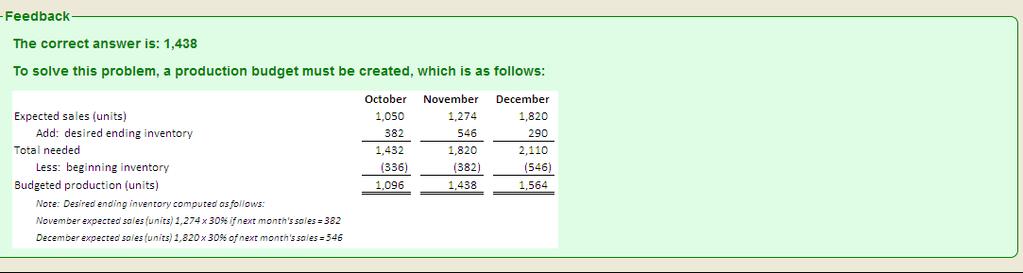

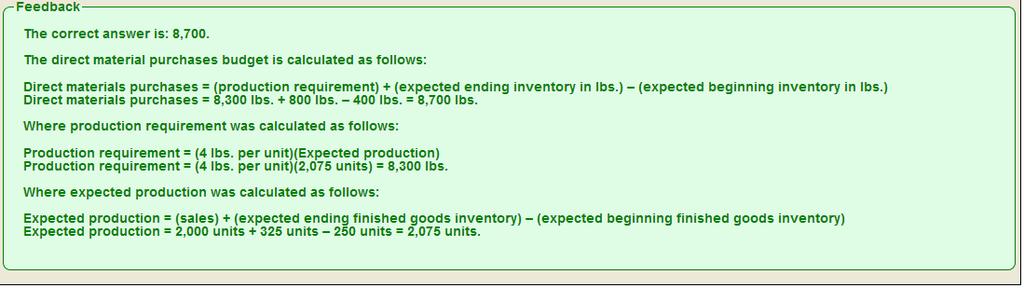

3 The correct answer is: 86,000 units. Budgeted production is calculated as follows: Budgeted production = (expected sales) + (expected ending inventory) (expected beginning inventory) The expected ending inventory for each quarter equals 50% of the next quarter s expected sales. Since the finished goods inventory at the end of the first quarter is 8,000 less than it should be, the budgeted production for the second quarter is calculated as follows: Budgeted production, second quarter = 72,000 units + 0.5(84,000 units) [0.5(72,000 units) 8,000 units] Budgeted production, second quarter = 72,000 units + 42,000 units [36,000 units - 8,000 units] Budgeted production, second quarter = 114,000 units 28,000 units = 86,000 units

4

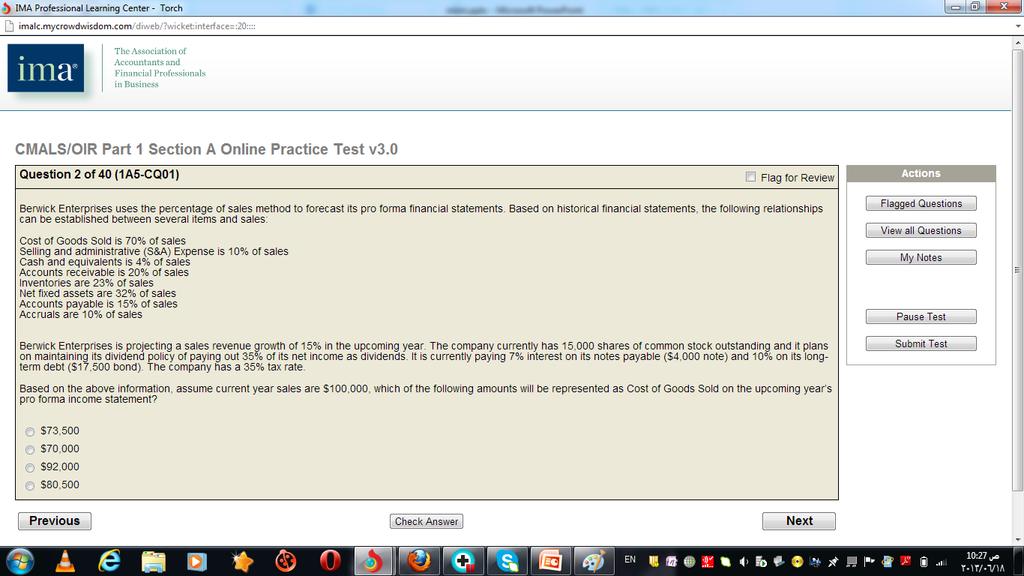

5 The correct answer is: $80,500 For the current year, sales are $100,000, and the projected growth rate in sales is 15%, thus $100,000 x 1.13 = $115,000. Since Cost of Goods Sold (COGS) is 70% of sales, the projected COGS would be $80,500 ($115,000 x 70%).

6

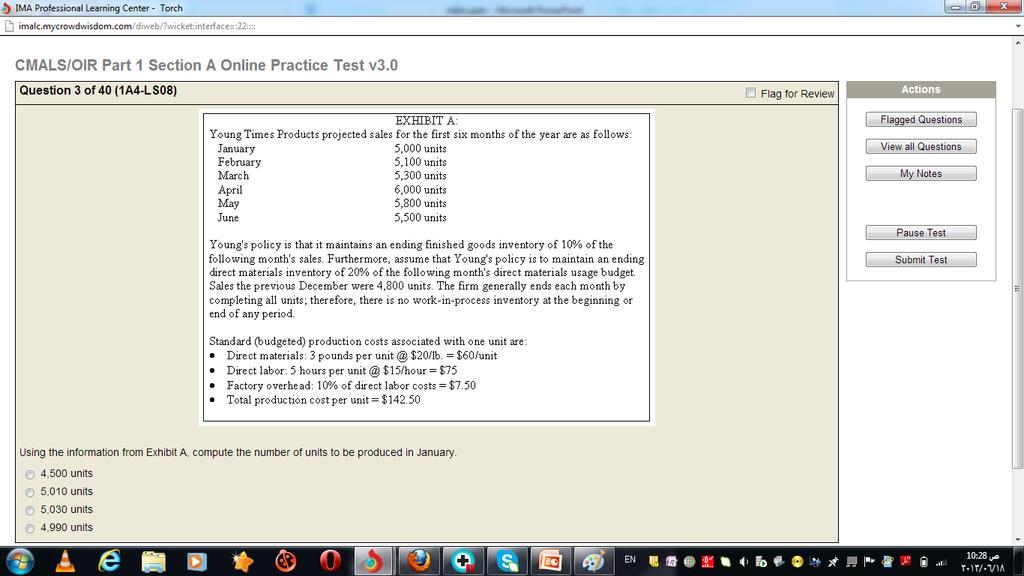

7 The correct answer is: 5,010 units The number of units to be produced equals sales (5,000 units) plus desired ending inventory (10% of 5,100 = 510) less beginning inventory (10% of 5,000 = 500) = 5,010 units.

8

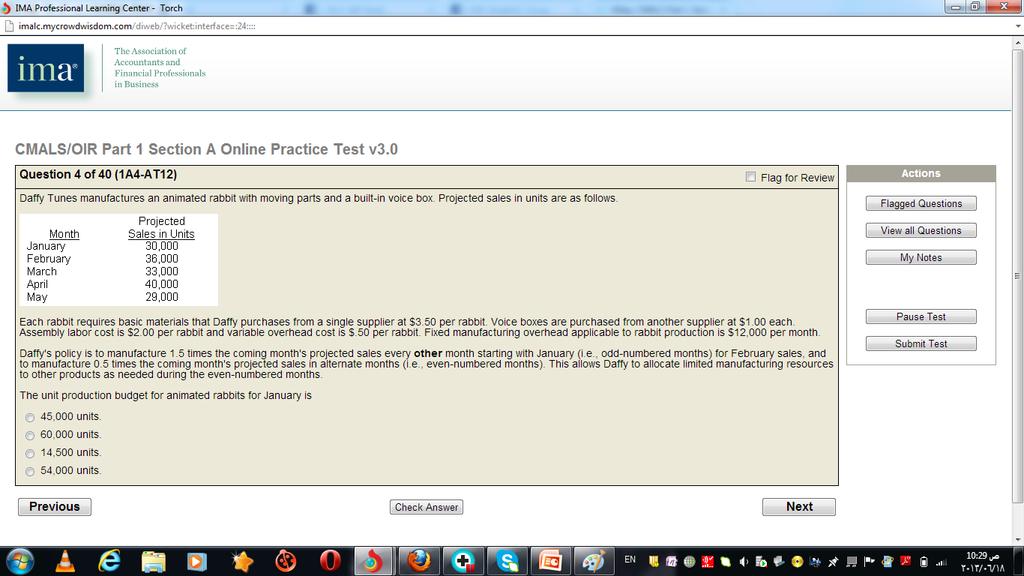

9 The correct answer is: 54,000 units. The production in odd numbered months is 1.5 times the projected sales for the following month. Therefore, the production budget for January is 1.5 times the projected sales for February or 1.5(36,000 units) = 54,000 units.

10

11 The correct answer is: Sales forecast Without an accurate sales forecast, all other budget elements will be inaccurate because production levels, purchases, etc., are set to match expected sales.

12

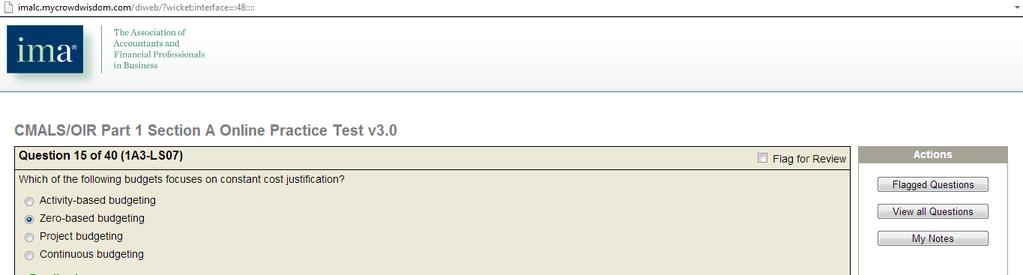

13 The correct answer is: zero-based budgeting. Zero-based budgeting (ZBB) requires that the cost of each item or program in the budget be rejustified with each new budget. ZBB ranks items and programs by how vital they are to the company. The base for each budget line item or program is zero.

14

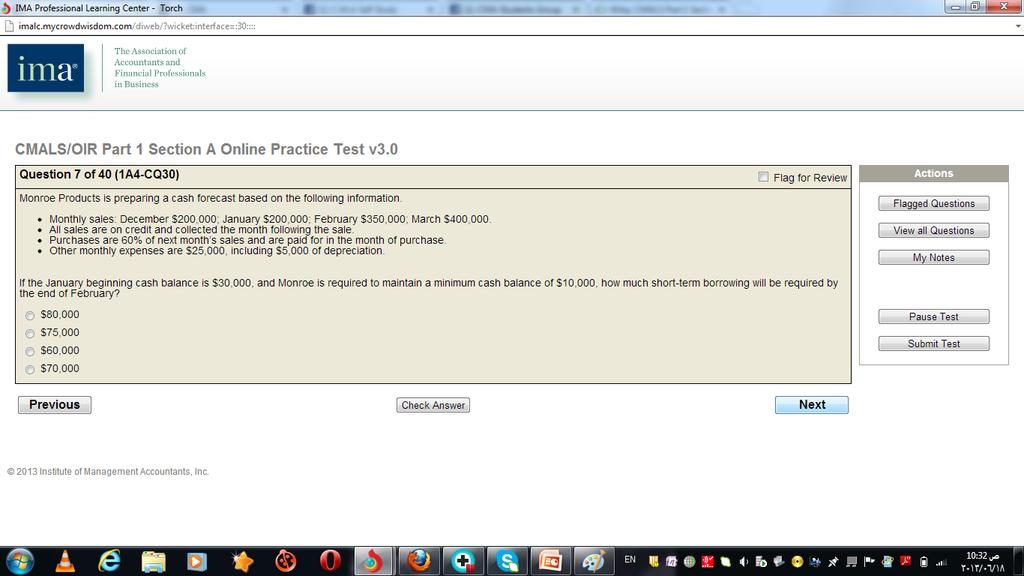

15 The correct answer is: $70,000.Monroe can expect to borrow $10,000 in January and $60,000 in February for a total of $70,000. The expected cash balance at the end of January is calculated as follows: Expected cash balance, end of January = (beginning balance) + (cash receipts from December sales) (cash disbursements) (monthly cash expenses) Cash disbursements = 60% of February purchases Monthly cash expenses for January = $25, $5,000 depreciation expense Expected cash balance, end of January = $30,000 + $200,000 (0.6)($350,000) - $20,000 Expected cash balance, end of January = $210,000 $210,000 = $0 Therefore, $10,000 needs to be borrowed in January to provide a $10,000 beginning balance for February. The expected cash balance at the end of February is calculated as follows: Expected cash balance, end of February = (beginning balance) + (cash receipts from January sales) (cash disbursements) (monthly cash expenses) Cash disbursements = 60% of March purchases Monthly cash expenses for February = $25,000 $5,000 depreciation expense Expected cash balance, end of February = $10,000 + $200,000 (0.6)($400,000) ($20,000) Expected cash balance, end of February = $190,000 $240,000 = -$50,000 Therefore, Monroe would need to borrow $60,000 in February to provide a $10,000 beginning balance for March.

16

17 The correct answer is: Cash budget An operating budget is broken down into the different operational budgets of the organization, including a sales budget, production budget, direct materials budget, direct labor budget, overhead budget, cost of goods sold budget, and selling and administrative expense budget. A cash budget is one of the subsets of the financial budget.

18

19

20

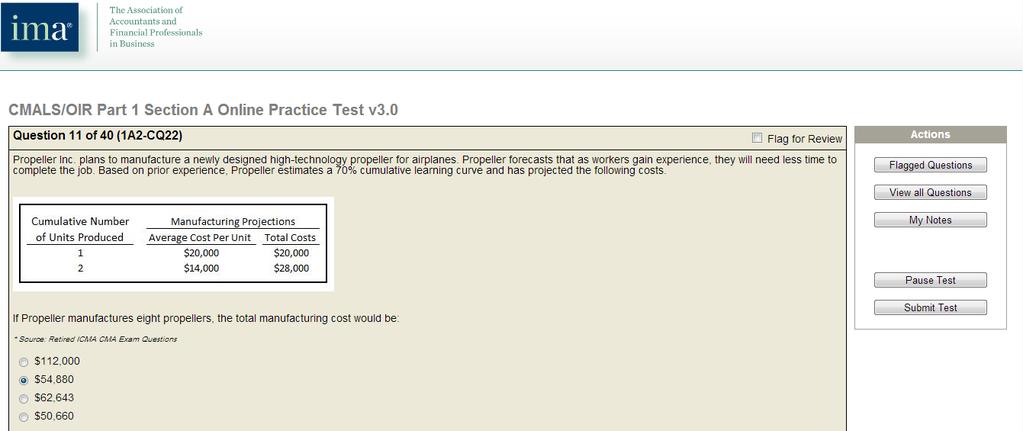

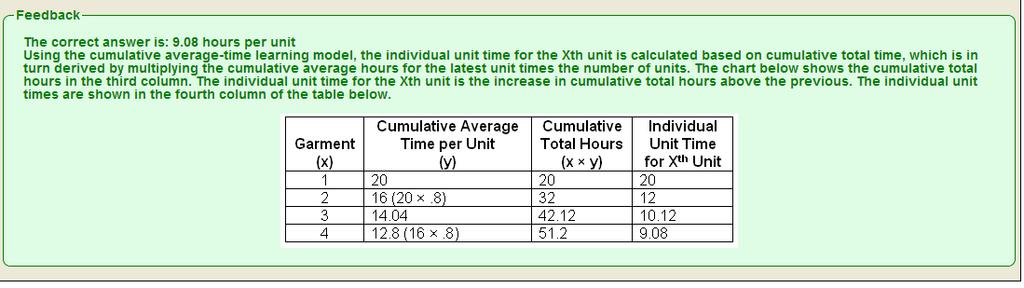

21 The correct answer is: 80.0%. Using a cumulative average time learning curve, as the cumulative output doubles, the cumulative average direct labor hours per unit becomes the learning curve percentage times the previous cumulative average direct labor hours per unit. So, if the first lot used 5,000 direct labor hours and the second lot required 3,000 direct labor hours, then the total for the 2 lots would be 8,000 direct labor hours and the cumulative average hours for the two lots would be 4,000 direct labor hours (8,000 direct labor hours / 2). Therefore, the learning curve percentage would be calculated by taking the cumulative average hours for the two lots (4,000 direct labor hours) and dividing it by the number of direct labor hours used for the first lot (5,000), or 4,000 / 5,000 = 0.8, or 80%.

22

23

24

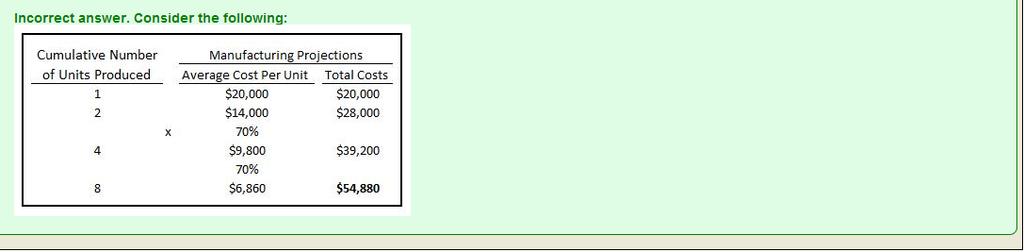

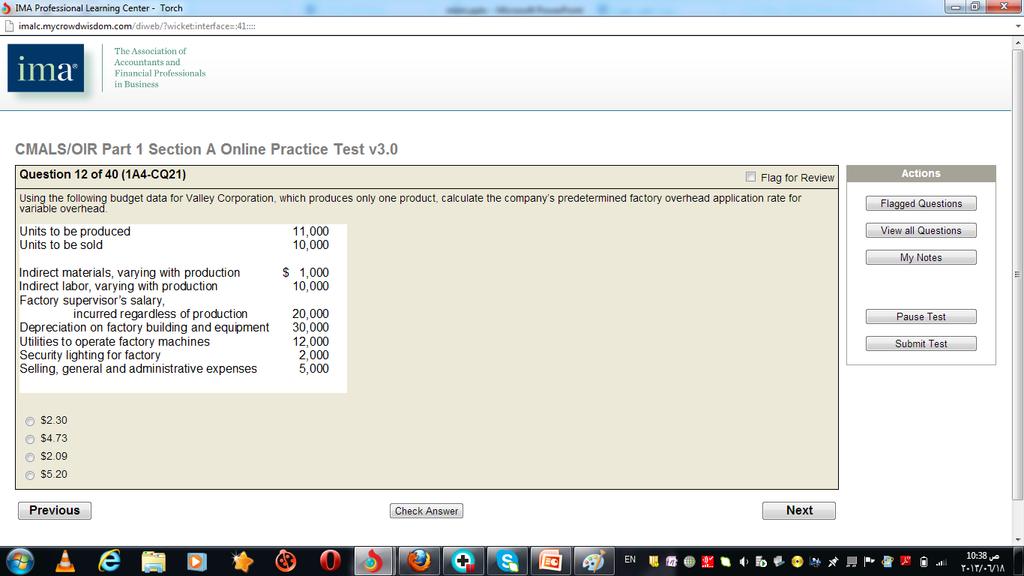

25 The correct answer is: $2.09. The variable overhead rate per unit is calculated by taking the expected variable overhead and dividing it by the expected production in units. The expected variable overhead consists of indirect materials, indirect labor, and utilities, and is calculated as follows: Variable overhead = ($1,000 + $10,000 + $12,000) Variable overhead = $23,000 Since expected production is 11,000 units, the variable overhead rate = $23,000 / 11,000 units = $2.09 per unit.

26

27

28

29

30

31

32

33 The correct answer is: $27/unit The standard cost is determined using the "should cost" amounts: (8 pounds x $1.50) + (0.5 x $10) + (0.5 x $20) = $27/unit.

34

35 The correct answer is: Combination approach In an authoritative budget (top-down budget), top management sets everything from strategic goals down to the individual items of the budget for each department and expects lower managers and employees to adhere to the budget and meet the goals. In a participative budget (bottom-up or self-imposed budget), managers at all levels and certain key employees cooperate to set budgets for their areas, and top management usually retains final approval. The ideal process combines the features of each and falls somewhere between these methods.

36

37 The correct answer is: estimating declining costs based on increased learning. Learning curve analysis is a systematic method for estimating declining costs based on increased learning by the business, group, or individual. As experience is gained, the worker or business becomes more efficient at production, which decreases costs.

38

39 That s incorrect. Since department managers have the most detailed knowledge about organizational operations, they should use this information as the building blocks of the operating budget. In the development of the operating budget, it is important that the department managers have a primary impact on the operating budgets as they have the most knowledge necessary to make an informed decision of the resources necessary to operate the department effectively.

40

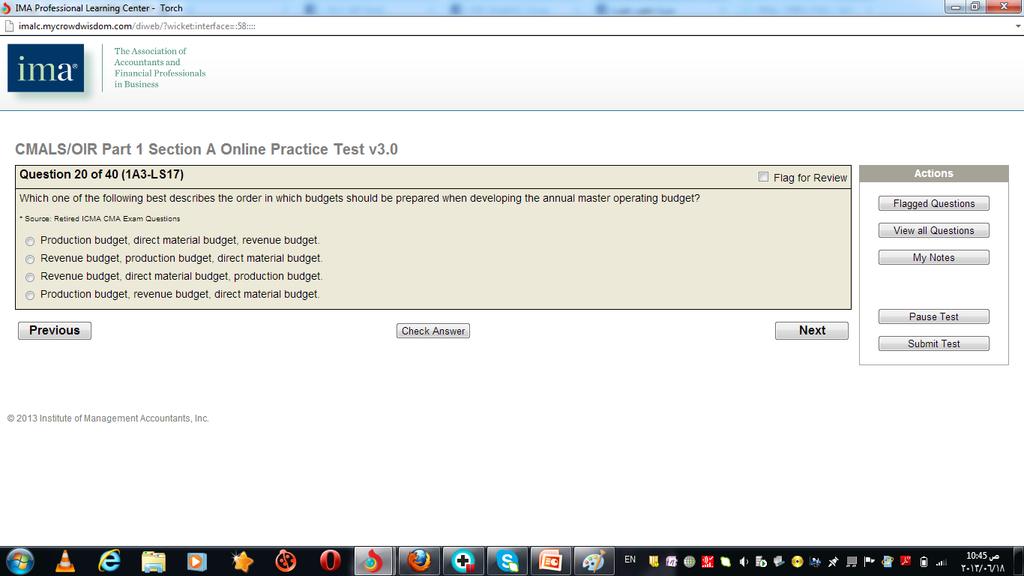

41 That s incorrect. The correct chronological order in budget preparation always starts with the sales budget, production budget, purchases budget (including direct materials), cost of goods sold budget, and administrative budget.

42

43 The correct answer is: Employees may be confused due to less-clear operating guidelines. Regular revisions usually provide more clear operating guidelines. The other options are all risks of regular revisions.

44

45

46

47 The correct answer is: $600,000. Cost of goods sold is calculated as follows: Cost of goods sold = (cost of goods manufactured) + (beginning finished goods inventory) (ending finished goods inventory) Cost of goods sold = $700,000 + $100,000 $200,000 Cost of goods sold = $600,000

48

49 That s correct! Freight charges paid for the delivery of raw materials to the company. The overhead budget includes those items that can not be directly traced back to the product itself, therefore, items such as overtime paid to the workers who perform production scheduling, cost of glue used to secure the attachment of the legs to the tables, and fringe benefits paid to the production supervisor are all inclusive overhead costs.

50

51 The correct answer is: 151 televisions. The formula for exponential smoothing is: F(t+1) = α [A(t)] + (1 α)[f (t)] Where: F = the forecast A = the actual t = the current time period α = the smoothing constant February forecast = F(t) = 148 February actual = A(t) = 158 March forecast = F(t+1) = (0.3)(158) + (1-0.3)(148) F(t+1) = (148) F(t+1) = = 151

52

53 The correct answer is: The budget would be set too low and the sales force would be less motivated to surpass those goals Employing prior year results as the following year s budget provides no expectation for improvement. Another reason for not using historical results as a budget is that past performance is not always indicative of future results. A budget process attempts to predict and account for future changes, both positive and negative. Relying only on raw historical data leads to a sense that the past year must always be the benchmark.

54

55 Incorrect answer. The correct answer is: limit unauthorized expenditures. Feedback: Advantages of management control systems include the forcing of management to plan, providing performance critera, and the promotion of communications and coordination within the organization.

56

57

58

59

60

61 The correct answer is: Show prospective investors how they will earn an appropriate rate of return. Prospective investors use financial statements, both historical and pro forma, to estimate the statement issuer s future economic performance (cash flows and income) and to estimate the expected return on an investment in the issuer s securities. The prospective investor compares the expected return to his/her required rate of return to see if it is appropriate.

62

63 The correct answer is: loan proceeds. Loan proceeds are a cash receipt. All of the other choices are cash disbursements.

64

65 The correct answer is: Continuous budgeting A continuous budget adds a new period on the end of the budget at the end of each period such as a month so that the budgets remain up to date with the operating environment. A monthly continuous budget also breaks down a large budgeting process into 12 easily manageable steps.

66

67 The correct answer is: rolling budget. A rolling budget (or continuous budget) is a plan that always covers a specified future period by adding a period in the future and dropping the period just ended. It forces management to continuously focus on the future specified time period. The time period is always the same length, but the actual time period covered by the budget moves forward with the passage of time.

68

69 That s correct! Learning curve analysis. With learning curve analysis, the more that a process is performed, the less time it takes to complete that process.

70

71 The correct answer is: In-depth interviews of each area the manager controls In order to justify what items to continue funding, managers must conduct in-depth reviews of each area under their control.

72

73

74

75

76

77 The correct answer is: Activity-based budgeting Machine hours is a volume-based cost driver, and number of setups is an activity-based cost driver. The only possible budgeting system allowing such inputs is an activity-based budget.

78

79

80

81 The correct answer is: Top management support. Top managers determine and significantly influence how budgets are perceived in their companies. Top management initiates the planning and budgeting process and approves policies and procedures regulating it, which makes its support a crucial success factor for the budgeting process.

82

2018 LAST MINUTE CPA EXAM NOTES

2018 LAST MINUTE CPA EXAM NOTES Page intentionally left blank 2018 LAST MINUTE CPA EXAM NOTES BEC (Volume 1) Copyright 2018 by Glomont LLC. First edition Notice of Rights. All rights reserved. No part

2018 LAST MINUTE CPA EXAM NOTES Page intentionally left blank 2018 LAST MINUTE CPA EXAM NOTES BEC (Volume 1) Copyright 2018 by Glomont LLC. First edition Notice of Rights. All rights reserved. No part

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material. Chapter 10: Static and Flexible Budgets

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 10: Static and Flexible Budgets Budget: formalized financial plan for operations of an organization for a specified

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 10: Static and Flexible Budgets Budget: formalized financial plan for operations of an organization for a specified

STANDARD COSTS AND VARIANCE ANALYSIS

STANDARD COSTS AND VARIANCE ANALYSIS Key Terms and Concepts to Know Static or Planning Budgets Used for planning purposes Prepared at the beginning of the period Based on one projected level of activity

STANDARD COSTS AND VARIANCE ANALYSIS Key Terms and Concepts to Know Static or Planning Budgets Used for planning purposes Prepared at the beginning of the period Based on one projected level of activity

Disclaimer: This resource package is for studying purposes only EDUCATIO N

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 1 Managerial accounting vs. financial accounting Qualities Financial Accounting Managerial Accounting Reports Externally

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 1 Managerial accounting vs. financial accounting Qualities Financial Accounting Managerial Accounting Reports Externally

Let s trace the budgets through for a company called the Hayes Company. Sales Budget The first budget prepared, comes from the Sales Forecast

Let s trace the budgets through for a company called the Hayes Company. Sales Budget The first budget prepared, comes from the Sales Forecast Expected sales volume: 3,000 units in the first quarter with

Let s trace the budgets through for a company called the Hayes Company. Sales Budget The first budget prepared, comes from the Sales Forecast Expected sales volume: 3,000 units in the first quarter with

Planning and Control. Control involves the steps taken by management that attempt to ensure the objectives are attained.

Profit Planning Planning and Control Planning -- involves developing objectives and preparing various budgets to achieve these objectives. Control involves the steps taken by management that attempt to

Profit Planning Planning and Control Planning -- involves developing objectives and preparing various budgets to achieve these objectives. Control involves the steps taken by management that attempt to

LO 1: Budgeting. Terms Budget Sales forecast Budget committee Participative budgeting Budgetary slack

Terms Budget Sales forecast Budget committee Participative budgeting Budgetary slack LO 1: Budgeting Long-range planning Master budget Operating budget Financial budget Benefits of Budgeting: Planning

Terms Budget Sales forecast Budget committee Participative budgeting Budgetary slack LO 1: Budgeting Long-range planning Master budget Operating budget Financial budget Benefits of Budgeting: Planning

Budgetary Planning. Managerial Accounting, Fourth Edition. Chapter 9-2

9-1 CHAPTER 9 Budgetary Planning Managerial Accounting, Fourth Edition 9-2 Study Objectives 1. Indicate the benefits of budgeting. 2. State the essentials of effective budgeting. 3. Identify the budgets

9-1 CHAPTER 9 Budgetary Planning Managerial Accounting, Fourth Edition 9-2 Study Objectives 1. Indicate the benefits of budgeting. 2. State the essentials of effective budgeting. 3. Identify the budgets

Spring Manufacturing Company Sales Budget 2007

8-56 Comprehensive Profit Plan (90 minutes) 1. Sales Budget Sales Budget Sales (in units) 12,000 9,000 21,000 x Selling Price Per Unit $150 $220 Total Sales Revenue $1,800,000 $1,980,000 $3,780,000 2.

8-56 Comprehensive Profit Plan (90 minutes) 1. Sales Budget Sales Budget Sales (in units) 12,000 9,000 21,000 x Selling Price Per Unit $150 $220 Total Sales Revenue $1,800,000 $1,980,000 $3,780,000 2.

Glossary of Budgeting and Planning Terms

Budgeting Basics and Beyond, Third Edition By Jae K. Shim and Joel G. Siegel Copyright 2009 by John Wiley & Sons, Inc.. Glossary of Budgeting and Planning Terms Active Financial Planning Software Budgeting

Budgeting Basics and Beyond, Third Edition By Jae K. Shim and Joel G. Siegel Copyright 2009 by John Wiley & Sons, Inc.. Glossary of Budgeting and Planning Terms Active Financial Planning Software Budgeting

BUDGET- CONCEPTS AND METHODOLOGIES

Budgeting Concepts and Methodologies Application & Awareness 1 BUDGET- CONCEPTS AND METHODOLOGIES WWW.CMAEXAMSTUDY.COM WWW.IMANET.ORG 2 Agenda Introduction of 3FOLD Budget Budgeting Role, Process and Approaches

Budgeting Concepts and Methodologies Application & Awareness 1 BUDGET- CONCEPTS AND METHODOLOGIES WWW.CMAEXAMSTUDY.COM WWW.IMANET.ORG 2 Agenda Introduction of 3FOLD Budget Budgeting Role, Process and Approaches

CHAPTER 6. Master Budgeting and Responsibility Accounting

CHAPTER 6 Master Budgeting and Responsibility Accounting 1 Budget Defined The quantitative expression of a proposed plan of action by management for a specified period, and An aid to coordinating what

CHAPTER 6 Master Budgeting and Responsibility Accounting 1 Budget Defined The quantitative expression of a proposed plan of action by management for a specified period, and An aid to coordinating what

CMA Exam Support Package

CMA Exam Support Package Part 1 Copyright 2010 By Institute of Certified Management Accountants CMA Part 1 Financial Planning, Performance and Control Examination Practice Questions Section A: Planning,

CMA Exam Support Package Part 1 Copyright 2010 By Institute of Certified Management Accountants CMA Part 1 Financial Planning, Performance and Control Examination Practice Questions Section A: Planning,

Master Budget and Responsibility Accounting

Master Budget and Responsibility Accounting 1 Budgeting Cycle Performance planning Providing a frame of reference Investigating variations Corrective action Planning again 2 The Master Budget Master Budget

Master Budget and Responsibility Accounting 1 Budgeting Cycle Performance planning Providing a frame of reference Investigating variations Corrective action Planning again 2 The Master Budget Master Budget

ACC406 Tip Sheet. 1) Planning: It is the process of creating a set of plans that a company intends to achieve a particular goal.

Planning: It is the process of creating a set of plans that a company intends to achieve a particular goal.") ACC406 Tip Sheet Chapter 1 Managerial Accounting: It is simply the process of reporting accounting information for a company s internal users such as managers, sales staff and etc. for decision making.

ACC406 Tip Sheet Chapter 1 Managerial Accounting: It is simply the process of reporting accounting information for a company s internal users such as managers, sales staff and etc. for decision making.

Profit Planning: REVISION

Profit Planning: REVISION rue / False Questions No statement /F 1 he production budget is typically prepared prior to the sales budget. F 2 One benefit of budgeting is that it coordinates the activities

Profit Planning: REVISION rue / False Questions No statement /F 1 he production budget is typically prepared prior to the sales budget. F 2 One benefit of budgeting is that it coordinates the activities

PART 1 Financial Planning, Performance and Control

PART 1 Financial Planning, Performance and Control Section A. Planning, Budgeting and Forecasting (30% - Levels A, B, and C) Section A, Planning, Budgeting and Forecasting, represents 30% of the exam,

PART 1 Financial Planning, Performance and Control Section A. Planning, Budgeting and Forecasting (30% - Levels A, B, and C) Section A, Planning, Budgeting and Forecasting, represents 30% of the exam,

The Basic Framework of Budgeting

7-1 The Basic Framework of Budgeting A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. 1. The act of preparing a budget

7-1 The Basic Framework of Budgeting A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period. 1. The act of preparing a budget

Accounting for Management: Concepts & Tools v.2.0- Course Transcript Presented by: TeachUcomp, Inc.

Accounting for Management: Concepts & Tools v.2.0- Course Transcript Presented by: TeachUcomp, Inc. Course Introduction Welcome to Accounting for Management: Concepts and Tools, a presentation of TeachUcomp,

Accounting for Management: Concepts & Tools v.2.0- Course Transcript Presented by: TeachUcomp, Inc. Course Introduction Welcome to Accounting for Management: Concepts and Tools, a presentation of TeachUcomp,

MBP1133 Managerial Accounting Prepared by Dr Khairul Anuar

1 MBP1133 Managerial Accounting Prepared by Dr Khairul Anuar L9 Master Budgeting www.notes638.wordpress.com 2 Learning Objective 1 Understand why organizations budget and the processes they use to create

1 MBP1133 Managerial Accounting Prepared by Dr Khairul Anuar L9 Master Budgeting www.notes638.wordpress.com 2 Learning Objective 1 Understand why organizations budget and the processes they use to create

Index COPYRIGHTED MATERIAL

A ABC (activity-based costing). See also costs; peanut butter costing allocating indirect costs, 77 78 allocations to cost pools, 79 analyzing cost activities, 78 79 applying to bottlenecks, 353 applying

A ABC (activity-based costing). See also costs; peanut butter costing allocating indirect costs, 77 78 allocations to cost pools, 79 analyzing cost activities, 78 79 applying to bottlenecks, 353 applying

Budgeting planning. Breakers, Inc. is preparing budgets for the quarter ending June 30. Budgeted sales for the next five months are:

Budgeting planning We use budgets as a target that we hope or expect to achieve. These are financial and non-financial in nature, but typically offer some quantitative measure We will begin by talking

Budgeting planning We use budgets as a target that we hope or expect to achieve. These are financial and non-financial in nature, but typically offer some quantitative measure We will begin by talking

TRADITIONAL ABSORPTION V ACTIVITY BASED COSTING

TRADITIONAL ABSORPTION V ACTIVITY BASED COSTING A company manufactures two products: X and Y. Information is available as follows: (a) Product Total production Labour time per unit X 1,000 0.5 hours Y

TRADITIONAL ABSORPTION V ACTIVITY BASED COSTING A company manufactures two products: X and Y. Information is available as follows: (a) Product Total production Labour time per unit X 1,000 0.5 hours Y

McGraw-Hill /Irwin McGraw-Hill /Irwin McGraw-Hill /Irwin McGraw-Hill /Irwin Advantages McGraw-Hill /Irwin McGraw-Hill /Irwin

7-1 Today s LEcture Management Accounting Lecture 11 (Chapter 7) Profit Planning n What is a n Why and how organizations n ing n Sales n Production n Sales & Administration n Balance Sheet Items n Working

7-1 Today s LEcture Management Accounting Lecture 11 (Chapter 7) Profit Planning n What is a n Why and how organizations n ing n Sales n Production n Sales & Administration n Balance Sheet Items n Working

Cost Accounting: A Managerial Emphasis, 16e, Global Edition (Horngren) Chapter 4 Job Costing

Chapter 4 Job Costing") Cost Accounting: A Managerial Emphasis, 16e, Global Edition (Horngren) Chapter 4 Job Costing 4.1 Objective 4.1 1) A cost is considered direct if it can be traced to a particular cost object in a cost effective

Cost Accounting: A Managerial Emphasis, 16e, Global Edition (Horngren) Chapter 4 Job Costing 4.1 Objective 4.1 1) A cost is considered direct if it can be traced to a particular cost object in a cost effective

FINALTERM EXAMINATION Spring 2009 MGT402- Cost & Management Accounting (Session - 3) Question No: 1 ( Marks: 1 ) - Please choose one All of the following are a part of Planning Process EXCEPT: Identifying

FINALTERM EXAMINATION Spring 2009 MGT402- Cost & Management Accounting (Session - 3) Question No: 1 ( Marks: 1 ) - Please choose one All of the following are a part of Planning Process EXCEPT: Identifying

CMA Exam Support Practice Questions Part I

CMA Exam Support Practice Questions Part I 1. Which of the following types of budget systems most strongly supports the objective of improving communication and promoting coordination? a. Bottom up, flexible

CMA Exam Support Practice Questions Part I 1. Which of the following types of budget systems most strongly supports the objective of improving communication and promoting coordination? a. Bottom up, flexible

Essential Learning for CTP Candidates Carolinas Cash Adventure 2018 Session #CTP-09

Carolinas Cash Adventure 2018: CTP Track Cash ing & Risk Management Session #9 (Tues. 9:15 10:15 am) ETM5-Chapter 14: Cash Flow ing Essentials of Treasury Management, 5th Ed. (ETM5) is published by the

Carolinas Cash Adventure 2018: CTP Track Cash ing & Risk Management Session #9 (Tues. 9:15 10:15 am) ETM5-Chapter 14: Cash Flow ing Essentials of Treasury Management, 5th Ed. (ETM5) is published by the

Budgeting. MCQs. Gleim Book. Gleim CD. IMA - Retired IMA - Retired Contains: in a random basis. By: Mohamed hengoo to dvd4arab.

Budgeting MCQs Contains: in a random basis Gleim Book Gleim CD IMA - Retired 2005 IMA - Retired 2008 By: Mohamed hengoo to dvd4arab.com members [1] Gleim #: 2.4.208 -- Source: CIA 589 IV-12 A company has

Budgeting MCQs Contains: in a random basis Gleim Book Gleim CD IMA - Retired 2005 IMA - Retired 2008 By: Mohamed hengoo to dvd4arab.com members [1] Gleim #: 2.4.208 -- Source: CIA 589 IV-12 A company has

Excel-Based Budgeting for Cash Flows: Cash Is King!

BUDGETING Part 4 of 6 Excel-Based Budgeting for Cash Flows: Cash Is King! By Teresa Stephenson, CMA, and Jason Porter Budgeting. It seems that no matter how much we talk about it, how much time we put

BUDGETING Part 4 of 6 Excel-Based Budgeting for Cash Flows: Cash Is King! By Teresa Stephenson, CMA, and Jason Porter Budgeting. It seems that no matter how much we talk about it, how much time we put

REVIEW FOR FINAL EXAM, ACCT-2302 (SAC)

") 1. Types of Cost Classification REVIEW FOR FINAL EXAM, ACCT-2302 (SAC) CHAPTER 16 a. By Behavior: (1) Variable Cost - constant per unit, changes proportionally with volume. (2) Fixed Cost - fixed in total

1. Types of Cost Classification REVIEW FOR FINAL EXAM, ACCT-2302 (SAC) CHAPTER 16 a. By Behavior: (1) Variable Cost - constant per unit, changes proportionally with volume. (2) Fixed Cost - fixed in total

Final Examination Semester 2 / Year 2011

Southern College Kolej Selatan 南方学院 Final Examination Semester 2 / Year 2011 COURSE : BASIC COSTING COURSE CODE : ACCT2013 TIME : 2 1/2 HOURS DEPARTMENT : FINANCE AND ACCOUNTING LECTURER : GAN HWI SIN

Southern College Kolej Selatan 南方学院 Final Examination Semester 2 / Year 2011 COURSE : BASIC COSTING COURSE CODE : ACCT2013 TIME : 2 1/2 HOURS DEPARTMENT : FINANCE AND ACCOUNTING LECTURER : GAN HWI SIN

Managerial Accounting Prof. Dr. Varadraj Bapat Department School of Management Indian Institute of Technology, Bombay

Managerial Accounting Prof. Dr. Varadraj Bapat Department School of Management Indian Institute of Technology, Bombay Lecture - 30 Budgeting and Standard Costing In our last session, we had discussed about

Managerial Accounting Prof. Dr. Varadraj Bapat Department School of Management Indian Institute of Technology, Bombay Lecture - 30 Budgeting and Standard Costing In our last session, we had discussed about

Modern Budgeting for Profit Planning & Control

Modern Budgeting for Profit Planning & Control Course Description The course is intended for business professionals engaged in budgeting, financial planning, forecasting, profit planning, and control.

Modern Budgeting for Profit Planning & Control Course Description The course is intended for business professionals engaged in budgeting, financial planning, forecasting, profit planning, and control.

PTP_Intermediate_Syllabus 2012_Jun2014_Set 1

Paper 8: Cost Accounting & Financial Management Time Allowed: 3 Hours Full Marks: 100 Question.1 Section A-Cost Accounting (Answer Question No. 1 which is compulsory and any three from the rest in this

Paper 8: Cost Accounting & Financial Management Time Allowed: 3 Hours Full Marks: 100 Question.1 Section A-Cost Accounting (Answer Question No. 1 which is compulsory and any three from the rest in this

MTP_Intermediate_Syllabus 2008_Jun2015_Set 2

Paper 8: Cost & Management Accounting Time Allowed: 3 Hours Full Marks: 100 Question No 1 is Compulsory. Answers any five Questions from the rest. Working Notes should form part of the answer. Question.1

Paper 8: Cost & Management Accounting Time Allowed: 3 Hours Full Marks: 100 Question No 1 is Compulsory. Answers any five Questions from the rest. Working Notes should form part of the answer. Question.1

Financial Management Bachelors of Business (Specialized in Finance) Tutorial Questions Chapter 1: Introduction to Cost Accounting

Tutorial Questions Chapter 1: Introduction to Cost Accounting") Financial Management Bachelors of Business (Specialized in Finance) Tutorial Questions Chapter 1: Introduction to Cost Accounting 1 Practice Questions Question 1 Cost Accounting System is neither unnecessary

Financial Management Bachelors of Business (Specialized in Finance) Tutorial Questions Chapter 1: Introduction to Cost Accounting 1 Practice Questions Question 1 Cost Accounting System is neither unnecessary

accounts receivable: dollar amount due from customers from sales made on open account.

GLOSSARY 1 above-the-line: income items related to core operations. Typically assumed to have high predictive power for future earnings. accrual accounting: system of accounting that purports to measure

GLOSSARY 1 above-the-line: income items related to core operations. Typically assumed to have high predictive power for future earnings. accrual accounting: system of accounting that purports to measure

Chapter 10 Standard Costs and Variances

Chapter 10 Standard Costs and Variances Solutions to Questions 10-1 A quantity standard indicates how much of an input should be used to make a unit of output. A price standard indicates how much the input

Chapter 10 Standard Costs and Variances Solutions to Questions 10-1 A quantity standard indicates how much of an input should be used to make a unit of output. A price standard indicates how much the input

Chapter 11 BUDGETING. 1. Introduction. 2. Benefits of budgeting. 3. Principal budget factor

September-December 2016 Examinations ACCA F5 41 Chapter 11 BUDGETING 1. Introduction Budgeting is an essential tool for the management accounting in both planning and controlling future activity. In this

September-December 2016 Examinations ACCA F5 41 Chapter 11 BUDGETING 1. Introduction Budgeting is an essential tool for the management accounting in both planning and controlling future activity. In this

I Team-based approach to budgeting

I-21.03 Team-based approach to budgeting The electronic spreadsheet version of this problem includes a template based upon the existing budget as displayed within Chapter 21 of the textbook. You may find

I-21.03 Team-based approach to budgeting The electronic spreadsheet version of this problem includes a template based upon the existing budget as displayed within Chapter 21 of the textbook. You may find

THE HONG KONG POLYTECHNIC UNIVERSITY HONG KONG COMMUNITY COLLEGE

THE HONG KONG POLYTECHNIC UNIVERSITY HONG KONG COMMUNITY COLLEGE Subject Title : Cost Accounting Subject Code : CCN2111 Session : Semester Two, 2017/18 Numerical answers Question B1 (a) The company's DL

THE HONG KONG POLYTECHNIC UNIVERSITY HONG KONG COMMUNITY COLLEGE Subject Title : Cost Accounting Subject Code : CCN2111 Session : Semester Two, 2017/18 Numerical answers Question B1 (a) The company's DL

Disclaimer: This resource package is for studying purposes only EDUCATIO N

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 9: Budgeting The Basic Framework of Budgeting Master budget - a summary of a company s plans in which specific targets

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 9: Budgeting The Basic Framework of Budgeting Master budget - a summary of a company s plans in which specific targets

OPERATIONAL CASE STUDY NOVEMBER 2016 EXAM ANSWERS. Variant 2. The November 2016 exam can be viewed at

OPERATIONAL CASE STUDY NOVEMBER 2016 EXAM ANSWERS Variant 2 The November 2016 exam can be viewed at https://connect.cimaglobal.com/resources/november-2016- operational-case-study-variant-2 SECTION 1 EFFECTIVE

OPERATIONAL CASE STUDY NOVEMBER 2016 EXAM ANSWERS Variant 2 The November 2016 exam can be viewed at https://connect.cimaglobal.com/resources/november-2016- operational-case-study-variant-2 SECTION 1 EFFECTIVE

Free of Cost ISBN : Appendix. CMA (CWA) Inter Gr. II (Solution upto Dec & Questions of June 2013 included)

Inter Gr. II (Solution upto Dec & Questions of June 2013 included)") Free of Cost ISBN : 978-93-5034-631-0 Appendix CMA (CWA) Inter Gr. II (Solution upto Dec. 2012 & Questions of June 2013 included) Paper - 8 : Cost and Management Accounting Chapter - 3 : Labour Accounting

Free of Cost ISBN : 978-93-5034-631-0 Appendix CMA (CWA) Inter Gr. II (Solution upto Dec. 2012 & Questions of June 2013 included) Paper - 8 : Cost and Management Accounting Chapter - 3 : Labour Accounting

Online Course Manual By Craig Pence. Module 7

Online Course Manual By Craig Pence Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled

Online Course Manual By Craig Pence Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 M BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 M BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

PROJECTED FINANCIAL STATEMENTS FORMAT FOR ENERGY PROJECTS

PROJECTED FINANCIAL STATEMENTS FORMAT FOR ENERGY PROJECTS Projected Income Statement With Income Tax Holiday (ITH) Incentives* With ITH Incentives Sales Less: Sales Commissions and Discounts Net Sales

PROJECTED FINANCIAL STATEMENTS FORMAT FOR ENERGY PROJECTS Projected Income Statement With Income Tax Holiday (ITH) Incentives* With ITH Incentives Sales Less: Sales Commissions and Discounts Net Sales

Job Costing Cost Accounting Horngreen, Datar, Foster 1

Job Costing 1 Building Block Concepts of Costing Systems The following five terms constitute the building blocks that will be used in this chapter: 1 A cost object is anything for which a separate measurement

Job Costing 1 Building Block Concepts of Costing Systems The following five terms constitute the building blocks that will be used in this chapter: 1 A cost object is anything for which a separate measurement

Fundamentals of Product and Service Costing:

Fundamentals of Product and Service Costing: Practice Quiz Questions 1 Multiple Choice 1. Which of the following statements is correct? a) A cost flow diagram is helpful by providing a graphical representation

Fundamentals of Product and Service Costing: Practice Quiz Questions 1 Multiple Choice 1. Which of the following statements is correct? a) A cost flow diagram is helpful by providing a graphical representation

explain why organisations use budgeting and how budgetary systems fit within the performance hierarchy

Budgeting Outcome By the end of this session you should be able to: explain why organisations use budgeting and how budgetary systems fit within the performance hierarchy describe the factors which influence

Budgeting Outcome By the end of this session you should be able to: explain why organisations use budgeting and how budgetary systems fit within the performance hierarchy describe the factors which influence

Preparing and using budgets

Osborne Books Tutor Zone Preparing and using budgets Chapter activities Osborne Books Limited, 2013 2 p r e p a r i n g a n d u s i n g b u d g e t s t u t o r z o n e 1 The budgeting environment 1.1 Match

Osborne Books Tutor Zone Preparing and using budgets Chapter activities Osborne Books Limited, 2013 2 p r e p a r i n g a n d u s i n g b u d g e t s t u t o r z o n e 1 The budgeting environment 1.1 Match

FINALTERM EXAMINATION. Spring MGT402- Cost & Management Accounting (Session - 2)

") FINALTERM EXAMINATION Spring 2009 MGT402- Cost & Management Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one All of the following indicate the problems in traditional budget EXCEPT:

FINALTERM EXAMINATION Spring 2009 MGT402- Cost & Management Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one All of the following indicate the problems in traditional budget EXCEPT:

Financial Statements, Forecasts, and Planning Chapter 6

C H A P T E R 6 Financial Statements, Forecasts, and Planning Chapter 6 Chapter Objectives Identify the elements of the balance sheet. Identify the elements of the income statement. Discuss the cash flow

C H A P T E R 6 Financial Statements, Forecasts, and Planning Chapter 6 Chapter Objectives Identify the elements of the balance sheet. Identify the elements of the income statement. Discuss the cash flow

BUDGETING AND PROFIT PLANNING

BUDGETING AND PROFIT PLANNING Key Terms and Concepts to Know Profit Planning and Budgeting: Profit plan is the steps taken by the business to achieve their planned levels of profits. Budget is a quantitative

BUDGETING AND PROFIT PLANNING Key Terms and Concepts to Know Profit Planning and Budgeting: Profit plan is the steps taken by the business to achieve their planned levels of profits. Budget is a quantitative

CHAPTER 4 JOB COSTING

CHAPTER 4 JOB ING 4-1 Cost pool a grouping of individual cost items. Cost tracing the assigning of direct costs to the chosen cost object. Cost allocation the assigning of indirect costs to the chosen

CHAPTER 4 JOB ING 4-1 Cost pool a grouping of individual cost items. Cost tracing the assigning of direct costs to the chosen cost object. Cost allocation the assigning of indirect costs to the chosen

Budget & Budgetary Control

4 Budget & Budgetary Control Question 1 A Company manufactures two Products A and B by making use of two types of materials, viz., X and Y. Product A requires 10 units of X and 3 units of Y. Product B

4 Budget & Budgetary Control Question 1 A Company manufactures two Products A and B by making use of two types of materials, viz., X and Y. Product A requires 10 units of X and 3 units of Y. Product B

The budgeted information on the two business opportunities that Green Bush records are currently considering investing in is as follows:

ICB Cost and Management Accounting Playlist Handbook SECTION A: REVISION VIDEO QUESTIONS Break-even analysis The budgeted information on the two business opportunities that Green Bush records are currently

ICB Cost and Management Accounting Playlist Handbook SECTION A: REVISION VIDEO QUESTIONS Break-even analysis The budgeted information on the two business opportunities that Green Bush records are currently

MANAGEMENT INFORMATION

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 3 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 3 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

Answer ALL questions in Section A and TWO questions from Section B. Section A carries a weight of 40%; Section B carries a weight of 60%

UNIVERSITY OF EAST ANGLIA School of Business Studies May/June PG Examination 2015-16 ACCOUNTING AND FINANCIAL ANALYSIS NBS-M056 Time allowed: 2 hours Answer ALL questions in Section A and TWO questions

UNIVERSITY OF EAST ANGLIA School of Business Studies May/June PG Examination 2015-16 ACCOUNTING AND FINANCIAL ANALYSIS NBS-M056 Time allowed: 2 hours Answer ALL questions in Section A and TWO questions

COST ACCOUNTING INTERVIEW QUESTIONS

www.globalcma.in Learning Platform for Cost Accountants (CMA) Explain cost sheet? Cost Sheet is a periodical statement of cost designed to show in detail the various elements of cost of goods produced

www.globalcma.in Learning Platform for Cost Accountants (CMA) Explain cost sheet? Cost Sheet is a periodical statement of cost designed to show in detail the various elements of cost of goods produced

Introduction to Finance. 1 March Examination Paper. Time: 3 hours

Introduction to Finance 1 March 2016 Examination Paper Answer any FOUR (4) questions. Clearly cross out surplus answers. Failure to do this will result in only the first FOUR (4) answers being marked.

Introduction to Finance 1 March 2016 Examination Paper Answer any FOUR (4) questions. Clearly cross out surplus answers. Failure to do this will result in only the first FOUR (4) answers being marked.

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

Accounting For Decision Making

Accounting For Decision Making Topic 7 Costing products and services Goals for this session Explain why managers need estimates of the costs of both responsibility centres and products; Describe the basic

Accounting For Decision Making Topic 7 Costing products and services Goals for this session Explain why managers need estimates of the costs of both responsibility centres and products; Describe the basic

WEEK 6 OPERATING BUDGETS (MANUFACTURING ORGANISATIONS) Case Study. The budgets that you need to prepare include:

Case Study. The budgets that you need to prepare include:") WEEK 6 OPERATING BUDGETS (MANUFACTURING ORGANISATIONS) Case Study manufactures cardboard boxes which are used for transporting very special toys to toy stores all around Australia. You have already been

WEEK 6 OPERATING BUDGETS (MANUFACTURING ORGANISATIONS) Case Study manufactures cardboard boxes which are used for transporting very special toys to toy stores all around Australia. You have already been

Module 3 Introduction

Module 3 Introduction Module 3 Introduction This module is designed to further enhance knowledge about management accounting techniques. In particular, the student is introduced to the role of budgeting,

Module 3 Introduction Module 3 Introduction This module is designed to further enhance knowledge about management accounting techniques. In particular, the student is introduced to the role of budgeting,

ACCA F2 FLASH NOTES. Describe a pie chart?

ACCA F2 FLASH NOTES Describe a pie chart? A pie chart is a circle that is divided into segments representing each type of observation. The size of each segment is proportional to the proportion of the

ACCA F2 FLASH NOTES Describe a pie chart? A pie chart is a circle that is divided into segments representing each type of observation. The size of each segment is proportional to the proportion of the

MOLONEY A.M. SYSTEMS THE FINANCIAL MODELLING MODULE A BRIEF DESCRIPTION

MOLONEY A.M. SYSTEMS THE FINANCIAL MODELLING MODULE A BRIEF DESCRIPTION Dec 2005 1.0 Summary of Financial Modelling Process: The Moloney Financial Modelling software contained within the excel file Model

MOLONEY A.M. SYSTEMS THE FINANCIAL MODELLING MODULE A BRIEF DESCRIPTION Dec 2005 1.0 Summary of Financial Modelling Process: The Moloney Financial Modelling software contained within the excel file Model

INDUSTRIAL BUDGETING AND COST ANALYSIS

C h a p t e r INDUSTRIAL BUDGETING AND COST ANALYSIS 10.1 INTRODUCTION Everybody is familiar with the idea of a plan. Not only in business, but in private life also people make plans though there are considerable

C h a p t e r INDUSTRIAL BUDGETING AND COST ANALYSIS 10.1 INTRODUCTION Everybody is familiar with the idea of a plan. Not only in business, but in private life also people make plans though there are considerable

Chapter 10 Static and Flexible Budgets

Cost Management Measuring, Monitoring, and Motivating Performance Chapter 10 Static and Flexible Budgets Prepared by Gail Kaciuba Midwestern State University Eldenburg & Wolcott s Cost Management, 1e Slide

Cost Management Measuring, Monitoring, and Motivating Performance Chapter 10 Static and Flexible Budgets Prepared by Gail Kaciuba Midwestern State University Eldenburg & Wolcott s Cost Management, 1e Slide

PMP. Preparation Training. Cost Management. Your key in Successful Project Management. Cost Management Processes. Chapter 7 6/7/2005

PMP Preparation Training Your key in Successful Project Management Akram Al-Najjar, PMP Cost Management Processes Chapter 7 Cost Management Slide 2 1 AGENDA What is Cost Management? Cost Management Processes

PMP Preparation Training Your key in Successful Project Management Akram Al-Najjar, PMP Cost Management Processes Chapter 7 Cost Management Slide 2 1 AGENDA What is Cost Management? Cost Management Processes

Chapter 9 Activity-Based Costing

Chapter 9 Activity-Based Costing SUMMARY This chapter deals with the allocation of indirect costs to products. Product cost information helps managers make numerous decisions, such as pricing, keeping

Chapter 9 Activity-Based Costing SUMMARY This chapter deals with the allocation of indirect costs to products. Product cost information helps managers make numerous decisions, such as pricing, keeping

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay Lecture - 29 Budget and Budgetary Control Dear students, we have completed 13 modules.

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay Lecture - 29 Budget and Budgetary Control Dear students, we have completed 13 modules.

Forecasting for Financial Planning

Forecasting for Financial Planning 1 Learning Objectives The importance of forecasting to business success. The financial forecasting process. Preparation of pro forma financial statements. The importance

Forecasting for Financial Planning 1 Learning Objectives The importance of forecasting to business success. The financial forecasting process. Preparation of pro forma financial statements. The importance

PERFORMANCE MEASUREMENT (1) FINANCIAL PERFORMANCE:

FINANCIAL PERFORMANCE:") PERFORMANCE MEASUREMENT (1) FINANCIAL PERFORMANCE: GROWTH: Revenue / Profits / EBITDA / Market Share PROFITABILITY: Absolute profit / ROCE / Profit margin GEARING: Gearing ratio LIQUIDITY: Current ratio

PERFORMANCE MEASUREMENT (1) FINANCIAL PERFORMANCE: GROWTH: Revenue / Profits / EBITDA / Market Share PROFITABILITY: Absolute profit / ROCE / Profit margin GEARING: Gearing ratio LIQUIDITY: Current ratio

Prepare the following budgets for the year, showing both quarterly and total figures:

Page 1 of 7 Question 1 Mynor Corporation manufactures and sells a seasonal product that has peak sales in the third quarter. The following information concerns operation for Year 2-the coming year-and

Page 1 of 7 Question 1 Mynor Corporation manufactures and sells a seasonal product that has peak sales in the third quarter. The following information concerns operation for Year 2-the coming year-and

MERMAID. Manufacturers of surf gear Established The firm

BOARDIES @ MERMAID Manufacturers of surf gear Established 1960 The firm Boardies @ Mermaid (Boardies) is a manufacturer of items of surf gear. What began as a small family business has now grown into a

BOARDIES @ MERMAID Manufacturers of surf gear Established 1960 The firm Boardies @ Mermaid (Boardies) is a manufacturer of items of surf gear. What began as a small family business has now grown into a

Sensitivity = NPV / PV of key input

SECTION A 20 MARKS Question One 1.1 The answer is D 1.2 The answer is C Sensitivity measures the percentage change in a key input (for example initial outlay, direct material, direct labour, residual value)

SECTION A 20 MARKS Question One 1.1 The answer is D 1.2 The answer is C Sensitivity measures the percentage change in a key input (for example initial outlay, direct material, direct labour, residual value)

Business Introducing Financial Statements. Professor Sergio Janczak, Ph.D KC 1

Business 1220 Introducing Financial Statements Professor Sergio Janczak, Ph.D. 2008-9 KC 1 Introducing Financial Statements Types of Financial Statements 1. Balance Sheet 2. The Statement of Earnings or

Business 1220 Introducing Financial Statements Professor Sergio Janczak, Ph.D. 2008-9 KC 1 Introducing Financial Statements Types of Financial Statements 1. Balance Sheet 2. The Statement of Earnings or

FEEDBACK TUTORIAL LETTER ASSIGNMENT 2 COST AND MANAGEMENT ACCONTING 102 CMA512S

FEEDBACK TUTORIAL LETTER 2 nd SEMESTER 2017 ASSIGNMENT 2 COST AND MANAGEMENT ACCONTING 102 CMA512S 1 COURSE: COST AND MANAGEMENT ACCOUNTING 102 COURSE CODE: CMA512S TUTORIAL LETTER: 01/2017 DATE: 08/2017

FEEDBACK TUTORIAL LETTER 2 nd SEMESTER 2017 ASSIGNMENT 2 COST AND MANAGEMENT ACCONTING 102 CMA512S 1 COURSE: COST AND MANAGEMENT ACCOUNTING 102 COURSE CODE: CMA512S TUTORIAL LETTER: 01/2017 DATE: 08/2017

Managerial Accounting Using QuickBooks Pro TM

Managerial Accounting Using QuickBooks Pro TM This manual is intended as a reference in furthering knowledge of management accounting for agricultural producers using QuickBooks Pro TM. Historically, agricultural

Managerial Accounting Using QuickBooks Pro TM This manual is intended as a reference in furthering knowledge of management accounting for agricultural producers using QuickBooks Pro TM. Historically, agricultural

Mock One. Performance Management F5PM-MK1-Z16-A. Answers & Marking Scheme. Becker Study School DeVry/Becker Educational Development Corp.

Mock One Performance Management F5PM-MK-Z6-A Answers & Marking Scheme 206 DeVry/Becker Educational Development Corp. Question Answer Mark Question Answer Mark Section A Section B D 6 A 2 C 7 A 3 C 8 A

Mock One Performance Management F5PM-MK-Z6-A Answers & Marking Scheme 206 DeVry/Becker Educational Development Corp. Question Answer Mark Question Answer Mark Section A Section B D 6 A 2 C 7 A 3 C 8 A

Profit Planning DISCUSSION QUESTIONS

9 DISCUSSION QUESTIONS 1. Budgets are the quantitative expressions of plans. Budgets are used to translate the goals and strategies of an organization into operational terms. 2. Control is the process

9 DISCUSSION QUESTIONS 1. Budgets are the quantitative expressions of plans. Budgets are used to translate the goals and strategies of an organization into operational terms. 2. Control is the process

MGT402 Cost & Management Accounting. Composed By Faheem Saqib MIDTERM EXAMINATION. Spring MGT402- Cost & Management Accounting (Session - 1)

") MGT402 Cost & Management Accounting Composed By Faheem Saqib 14 Midterm Papers 3 of 2010 & 11 of 2009 For more Help Rep At Faheem_saqib2003@yahoo.com Faheem.saqib2003@gmail.com 0334-6034849 MIDTERM EXAMINATION

MGT402 Cost & Management Accounting Composed By Faheem Saqib 14 Midterm Papers 3 of 2010 & 11 of 2009 For more Help Rep At Faheem_saqib2003@yahoo.com Faheem.saqib2003@gmail.com 0334-6034849 MIDTERM EXAMINATION

2. Identify four factors of management intention in regard to the cash flow budget.

Answer on Question #54480, Economics / Other 1. What are the two types of information available to complete the budget? Describe the benefits and disadvantages of them and give an example of each. 2. Identify

Answer on Question #54480, Economics / Other 1. What are the two types of information available to complete the budget? Describe the benefits and disadvantages of them and give an example of each. 2. Identify

Part 1 Study Unit 10. Cost And Variance Measures. By Ronald Schmidt, CMA, CFM

Part 1 Study Unit 10 Cost And Variance Measures By Ronald Schmidt, CMA, CFM Variance Analysis and overview A budget communicates to employees the organization s operational and strategic objectives Considerations:

Part 1 Study Unit 10 Cost And Variance Measures By Ronald Schmidt, CMA, CFM Variance Analysis and overview A budget communicates to employees the organization s operational and strategic objectives Considerations:

Chapter 16 Fundamentals of Variance Analysis

Chapter 16 Fundamentals of Variance Analysis True / False Questions 1. In essence, the terms "master budget" and "operating budget" mean the same thing and can be used interchangeably. True False 2. Variances

Chapter 16 Fundamentals of Variance Analysis True / False Questions 1. In essence, the terms "master budget" and "operating budget" mean the same thing and can be used interchangeably. True False 2. Variances

ACCTG 533, Section 1: Module 1: Costs and Cost Allocation: Lecture 1: Costs and Cost Behavior

ACCTG 533, Section 1: Module 1: Costs and Cost Allocation: Lecture 1: Costs and Cost Behavior Costs and Cost Behavior Costs and Cost Behavior. Cost [Graphic Shown] a sacrifice or giving up of resources

ACCTG 533, Section 1: Module 1: Costs and Cost Allocation: Lecture 1: Costs and Cost Behavior Costs and Cost Behavior Costs and Cost Behavior. Cost [Graphic Shown] a sacrifice or giving up of resources

Chinese Costing Practices?

How Accurate Are Chinese Costing Practices? This is the third of three articles based on the recently completed study by the Institute of Management Accountants (IMA ) of the state of management accounting

How Accurate Are Chinese Costing Practices? This is the third of three articles based on the recently completed study by the Institute of Management Accountants (IMA ) of the state of management accounting

Many companies in the 80 s used this milking philosophy to extract money from the company and then sell it off to someone else.

Someone looking at a company and considering purchasing it is not going to be too impressed with the company paying out large dividends. Those dividends will go to the investors, the current owners. The

Someone looking at a company and considering purchasing it is not going to be too impressed with the company paying out large dividends. Those dividends will go to the investors, the current owners. The

COMPARING BUDGETING TECHNIQUES

COMPARING BUDGETING TECHNIQUES The budgeting process is an essential component of management control systems, as it provides a system of planning, coordination and control for management. It is often an

COMPARING BUDGETING TECHNIQUES The budgeting process is an essential component of management control systems, as it provides a system of planning, coordination and control for management. It is often an

1 Introduction to Cost and

1 Introduction to Cost and Management Accounting This Chapter Includes Concept of Cost; Management Accounting and its Evolution of Cost Accounting evolution, Meaning, Objectives, Costing, Cost Accounting

1 Introduction to Cost and Management Accounting This Chapter Includes Concept of Cost; Management Accounting and its Evolution of Cost Accounting evolution, Meaning, Objectives, Costing, Cost Accounting

Chap 14. Evaluating Financial Viability

Chap 14. Evaluating Financial Viability Dr. Jack M. Wilson Distinguished Professor of Higher Education, Emerging Technologies, and Innovation Financial Management Key Questions How are we doing? Are we

Chap 14. Evaluating Financial Viability Dr. Jack M. Wilson Distinguished Professor of Higher Education, Emerging Technologies, and Innovation Financial Management Key Questions How are we doing? Are we

Business Ratios. Current Ratio

Current Ratio Business Ratios Measures whether or not the firm has enough resources to pay its debt over the next 12 months formula: Current Ratio = Current Assets Current Liabilities Acceptable ratios

Current Ratio Business Ratios Measures whether or not the firm has enough resources to pay its debt over the next 12 months formula: Current Ratio = Current Assets Current Liabilities Acceptable ratios

SAMPLE QUESTIONS - PART 2

Section A. Budget Preparation SAMPLE QUESTIONS - PART 2 1. Trumbull Company has budgeted sales on account of $120,000 for July, $210,000 for August, and $195,000 for September. Collection experience indicates

Section A. Budget Preparation SAMPLE QUESTIONS - PART 2 1. Trumbull Company has budgeted sales on account of $120,000 for July, $210,000 for August, and $195,000 for September. Collection experience indicates

MARK SCHEME for the May/June 2010 question paper for the guidance of teachers 9706 ACCOUNTING

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS GCE Advanced Subsidiary Level and GCE Advanced Level MARK SCHEME for the May/June 200 question paper for the guidance of teachers 9706 ACCOUNTING 9706/22

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS GCE Advanced Subsidiary Level and GCE Advanced Level MARK SCHEME for the May/June 200 question paper for the guidance of teachers 9706 ACCOUNTING 9706/22

IMPORTANT INFORMATION:

Economics 1B ECS1601 Semester 1 Department of Economics IMPORTANT INFORMATION: This tutorial letter contains solutions to assignment 03 BARCODE SOLUTIONS TO ASSIGNMENT 03 QUESTIONS SEMESTER 1, 2017 3.1

Economics 1B ECS1601 Semester 1 Department of Economics IMPORTANT INFORMATION: This tutorial letter contains solutions to assignment 03 BARCODE SOLUTIONS TO ASSIGNMENT 03 QUESTIONS SEMESTER 1, 2017 3.1

POPULAR SYSTEM OF COSTING

Inspira- Journal of Modern Management & Entrepreneurship (JMME) 149 ISSN : 2231 167X, General Impact Factor : 2.3982, Volume 08, No. 01, January, 2018, pp. 149-154 POPULAR SYSTEM OF COSTING Dr. Prabhu

Inspira- Journal of Modern Management & Entrepreneurship (JMME) 149 ISSN : 2231 167X, General Impact Factor : 2.3982, Volume 08, No. 01, January, 2018, pp. 149-154 POPULAR SYSTEM OF COSTING Dr. Prabhu

Institute of Certified Management Accountants of Sri Lanka

Copyright Reserved Serial No Foundation Level Pilot Paper Instructions to Candidates 1. Time allowed is two (2) hours. 2. Total 100 Marks. 3. Answer all questions. 4. Encircle the number of your choice

Copyright Reserved Serial No Foundation Level Pilot Paper Instructions to Candidates 1. Time allowed is two (2) hours. 2. Total 100 Marks. 3. Answer all questions. 4. Encircle the number of your choice

Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced Level

*3484335703* ambridge International Examinations ambridge International dvanced Subsidiary and dvanced Level OUNTING 9706/13 Paper 1 Multiple hoice October/November 2017 1 hour dditional Materials: Multiple

*3484335703* ambridge International Examinations ambridge International dvanced Subsidiary and dvanced Level OUNTING 9706/13 Paper 1 Multiple hoice October/November 2017 1 hour dditional Materials: Multiple