Standard 4 pounds Quantity $ 7.50/pound Standard Cost $30.00

|

|

|

- Samson Osborn Walton

- 5 years ago

- Views:

Transcription

1 Part 1 Study Unit 7

2 Fausto Company employs a standard cost system in which direct materials inventory is carried at standard cost. The company has established the following standard for the materials costs of one unit of product: Standard 4 pounds Quantity $ 7.50/pound Standard Cost $30.00 During June, the company purchased 166,100 pounds of direct material at a total cost of $1,362,020. The company manufactured 34,600 units of product during June using 140,450 pounds of direct materials. The price variance for the direct materials acquired by the company during June is (Do not round intermediate calculations.): $98,315 favorable. $116,270 favorable. $116,270 unfavorable. $98,315 unfavorable.

3 Fausto Company employs a standard cost system in which direct materials inventory is carried at standard cost. The company has established the following standard for the materials costs of one unit of product: Standard 4 pounds Quantity $ 7.50/pound Standard Cost $30.00 During June, the company purchased 166,100 pounds of direct material at a total cost of $1,362,020. The company manufactured 34,600 units of product during June using 140,450 pounds of direct materials. The price variance for the direct materials acquired by the company during June is (Do not round intermediate calculations.): $98,315 favorable. $116,270 favorable. $116,270 unfavorable. $98,315 unfavorable. First, determine the actual price per unit of materials as follows. Total cost of $1,362,020 total pounds of 166,100 = $8.20 per pound. Then, the price variance for the direct material acquired by the company is determined as follows. Materials price variance = AQ (AP SP). Materials price variance = 166,100 ($8.20 $7.50) = $116,270 (U).

4 Fausto Company employs a standard cost system in which direct materials inventory is carried at standard cost. The company has established the following standard for the materials costs of one unit of product: Standard Quantity Standard Price Standard Cost 3 pounds $ 7.8/pound $23.4 During June, the company purchased 166,700 pounds of direct material at a total cost of $1,466,960. The company manufactured 47,200 units of product during June using 143,950 pounds of direct materials. The direct material quantity variance for June is: $18,330 unfavorable. $20,680 favorable. $18,330 favorable. $20,680 unfavorable.

5 Fausto Company employs a standard cost system in which direct materials inventory is carried at standard cost. The company has established the following standard for the materials costs of one unit of product: Standard Quantity Standard Price Standard Cost 3 pounds $ 7.8/pound $23.4 During June, the company purchased 166,700 pounds of direct material at a total cost of $1,466,960. The company manufactured 47,200 units of product during June using 143,950 pounds of direct materials. The direct material quantity variance for June is: $18,330 unfavorable. $20,680 favorable. $18,330 favorable. $20,680 unfavorable. First, determine the standard quantity allowed as follows. Total units of 47,200 units standard quantity of 3 pounds per unit = 141,600 pounds. Then, the direct material quantity variance is determined as follows. Materials quantity variance = SP (AQ SQ). Materials quantity variance = $7.80 (143, ,600) = $18,330 (U).

6 SU 7.5 Mix Variances Mix Variance Isolates the effects of using the ACTUAL mix instead of the STANDARD mix. Mix variance = ATQ x (SPSM SPAM) Actual Total Quantity x Std mix of inputs Actual mix Favorable variances = Actual mix < Std mix

7 SU 7.5 Yield Variances Yield Variance Isolates the effects of differences between the ATQ of inputs and the STQ. Yield variance = (STQ ATQ) x SPSM Std Total Qty - Actual Total Qty x Std mix of inputs Favorable variances = Actual Total Qty < Std Total Qty Review page 266

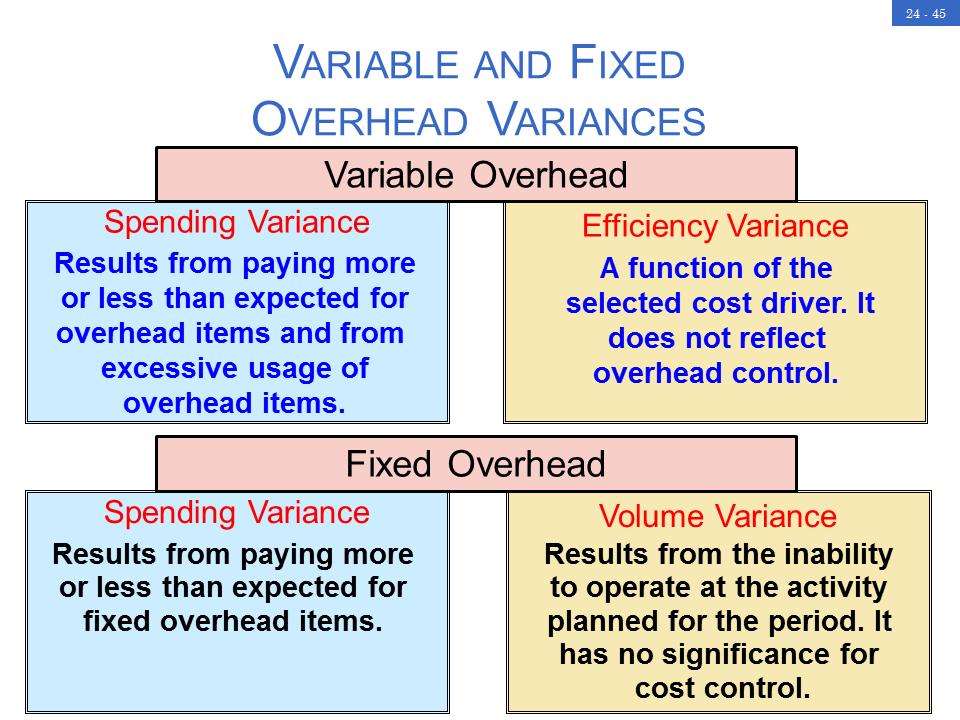

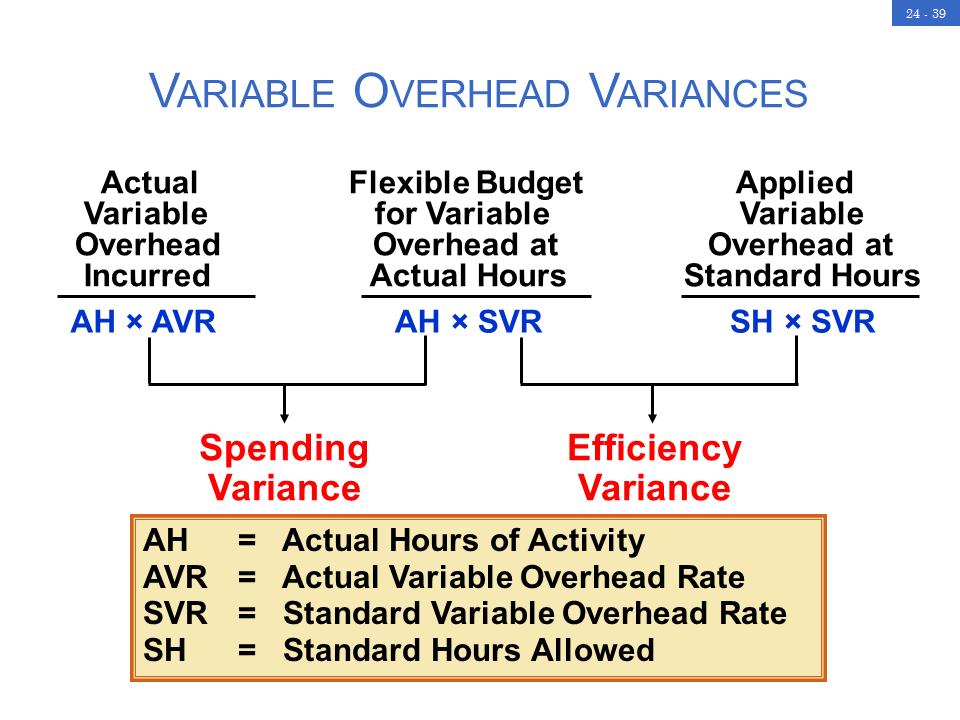

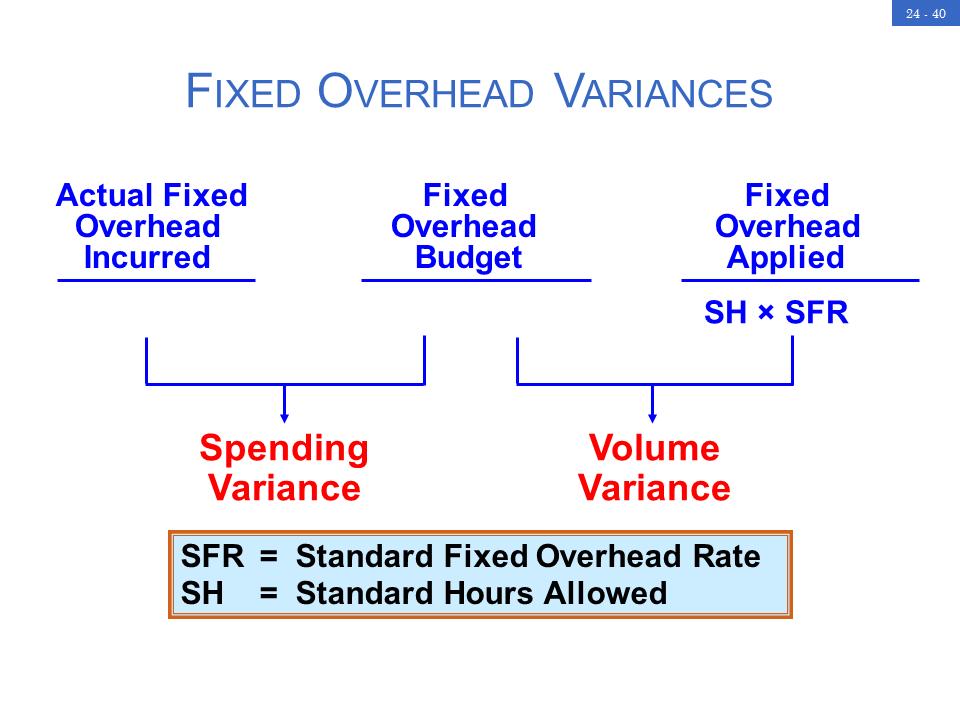

8 SU 7.6 Overhead Variances Total Overhead Variance consists of four variances. -Total Variable overhead variances = flexible budget variance -Spending variance difference between actual variable overhead and (budgeted application rate x the actual amount of input) -Variance is favorable if actual production spending < std spending -Efficiency variance budgeted application rate times the difference between the actual input and the standard input allowed for actual output. -Total Fixed overhead variances -Spending Variances difference between actual fixed overhead and the amount budgeted. Same as fixed overhead flexible budget variance. The fixed overhead is the same over the relevant range of output. -Production volume variance (Idle capacity variance) difference between budgeted fixed overhead and the product of the budgeted application rate and the standard input allowed for the actual output. -Review page 269 Analysis of Overhead Variances

9

10

11

12 Houghton Company maintains warehouses that stock items carried by its e-retailer clients. When one of Houghton's clients receives an order from an online customer, the order is forwarded to Houghton. Houghton then pulls the item from the warehouse, packs it and ships it to the customer. Houghton uses a predetermined variable overhead rate based on direct labor-hours. According to the company's records,.08 direct labor-hours are required to fulfill an order for one item and the variable overhead rate is $6.25 per direct-labor hour. During July, Houghton shipped 290,000 orders using 23,000 direct labor-hours. The company incurred a total of $141,450 in variable overhead costs. The variable overhead efficiency variance during July was: $2,300 unfavorable. $1,250 favorable. $2,300 favorable. $1,250 unfavorable.

13 Houghton Company maintains warehouses that stock items carried by its e- retailer clients. When one of Houghton's clients receives an order from an online customer, the order is forwarded to Houghton. Houghton then pulls the item from the warehouse, packs it and ships it to the customer. Houghton uses a predetermined variable overhead rate based on direct labor-hours. According to the company's records,.08 direct labor-hours are required to fulfill an order for one item and the variable overhead rate is $6.25 per directlabor hour. During July, Houghton shipped 290,000 orders using 23,000 direct labor-hours. The company incurred a total of $141,450 in variable overhead costs. The variable overhead efficiency variance during July was: $2,300 unfavorable. $1,250 favorable. $2,300 favorable. $1,250 unfavorable. The variable overhead (VOH) efficiency variance during July is determined as follows. VOH efficiency variance = SR (AH SH). VOH efficiency variance = $6.25 per hour (23,000 hours 23,200 hours) = $1,250 (F).

14 Problem 7.6 Water Control Systems manufactures water pumps and uses a standard cost system. The standard overhead costs per water pump are based on direct labor hours and are as follows: Variable overhead (4 hours at $8 per hour) $32 Fixed overhead (4 hours at $5* per hour) 20 Total overhead cost per unit $52 * Based on a capacity of 100,000 direct labor hours per month. The following information is available for the month of November: 22,000 pumps were produced although 25,000 had been scheduled for production. 94,000 direct labor hours were worked at a total cost of $940,000. The standard direct labor rate is $9 per hour. The standard direct labor time per unit is four hours. Variable overhead costs were $740,000. Fixed overhead costs were $540,000 Water Control s variable overhead spending variance for November was A. $48,000 unfavorable. B. $60,000 favorable. C. $40,000 unfavorable. D. $12,000 favorable.

15 Problem 7.6 Water Control s variable overhead spending variance for November was D. $12,000 favorable. The variable overhead spending variance is the difference between actual variable overhead and the variable overhead based on the standard rate and the actual activity level. Thus, the variable overhead spending variance was $12,000 favorable [(94,000 actual hours $8 standard rate) $740,000 actual cost]. A. $48,000 unfavorable. Answer A is incorrect. The variable overhead efficiency variance is $48,000 unfavorable. B. $60,000 favorable. Answer B is incorrect. The variance of $60,000 favorable is based on 100,000 hours, not the actual hours of 94,000. C. $40,000 unfavorable. Answer C is incorrect. The fixed overhead spending variance is $40,000 unfavorable.

16 PROBLEM 7.6 #2 A fixed overhead volume variance based on standard direct labor hours measures A. Deviation from standard direct labor hour capacity. B. Deviation from the normal, or denominator, level of direct labor hours. C. Fixed overhead use. D. Fixed overhead efficiency.

17 Problem 7.6 #2: A fixed overhead volume variance based on standard direct labor hours measures B. Deviation from the normal, or denominator, level of direct labor hours. The fixed overhead volume variance measures the effect of not operating at the budgeted (denominator) activity level. It is the difference between budgeted fixed costs and the product of the standard fixed overhead application rate and the standard activity level for the actual output. A favorable variance means that activity was greater than expected and that fixed overhead was overapplied. It might be caused by, for example, hiring more workers to provide an extra shift. An unfavorable volume variance means that activity was less than budgeted (overhead was underapplied), for example, because of insufficient sales or a labor strike. Accordingly, the volume variance is usually outside the control of production management. Moreover, unlike other variances, it does not directly reflect a difference between actual and budgeted expenditure of resources. A. Deviation from standard direct labor hour capacity. Answer A is incorrect. The volume variance is not related to direct labor. C. Fixed overhead use. Answer C is incorrect. The volume variance is not related to overhead use. D. Fixed overhead efficiency. Answer D is incorrect. The volume variance is not related to overhead efficiency.

18 Problem 7.6 #3 Nanjones Company manufactures a line of products distributed nationally through wholesalers. Presented below are planned manufacturing data for the year and actual data for November of the current year. The company applies overhead based on planned machine hours using a predetermined annual rate. A. $6,000 unfavorable. B. $6,000 favorable. C. $2,000 favorable. D. $14,000 unfavorable.

19 Problem 7.6 #3 Answer C. $2,000 favorable. Answer C is correct. The variable overhead spending variance equals the difference between actual variable overhead and the product of the actual input and the budgeted application rate. At a variable overhead application rate (standard cost) of $10 per machine hour ($2,400, ,000 hours), the total standard cost for the 21,600 actual hours was $216,000. Given actual costs of $214,000, the favorable variance is $2,000. Answer A is incorrect. The variance is favorable. Answer B is incorrect. The amount of $6,000 is based on planned machine hours of 22,000. Answer D is incorrect. The variance is favorable.

20 Problem 7.7 Standard Costs Actual Costs Direct Material 600,000 units of materials at $2.00 each 700,000 units at $1.90 Direct Labor 60,000 hours allowed for actual output at $7 per hour 65,000 hours at $7.20 Overhead $8.00 per direct labor hour on normal capacity of 50,000 direct labor hours: $6.00 for variable overhead $2.00 for fixed overhead $396,000 variable $130,000 fixed

21 Problem 7.7 Calculate the following: 1) Material Price Variance AQ x (SP-AP) 2) Material Quantity Variance (SQ-AQ) x SP 3) Labor Rate Variance AQ x (SP-AP) 4) Labor Efficiency Variance (SQ-AQ) x SP 5) Variable Overhead Spending Variance (AQxSP)-AC 6) Variable Overhead Efficiency Variance(SQ-AQ)xSP 7) Fixed Overhead Spending Variance Flexible/Static budget Actual costs incurred 8) Fixed Overhead Efficiency Variance (Std hours allowed for actual outputs x Std rate) x Flexible/Static budget

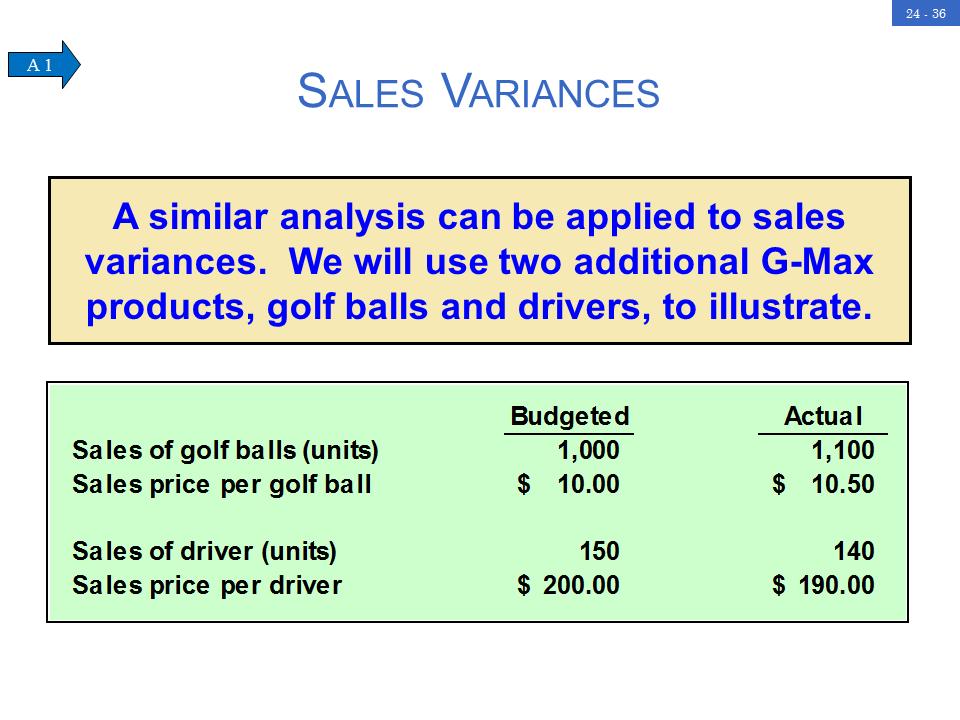

22 SU 7.8 Sales Variances Single Product Sales Variances -Evaluating the production and selling functions. -Differences are either price variance or volume variance -Sales volume variance = Sum of the sales quantity and mix variance -For a single product the sales mix variance is zero.

23 SU 7.8 Sales Variances Multiproduct Sales Price Variance -Used with two more products. -Calculate as single and add the results -Or - -Multiply the actual total units sold x the difference between: -the weighted-average price based on actual units sold at actual unit price and the weighted-average price based on actual units sold at budgeted prices.

24 SU 7.8 Sales Variances Multiproduct Sales Quantity Variance -Used with two more products. -Calculate as single and add the results -Or - -Calculate the difference between: -Actual total unit sales x the budgeted weighted-average UCM for the actual mix. -Budgeted total unit sales times the budgeted weighted-average UCM for the budgeted mix. -Can be separated into Sales quantity and Sales mix variances.

25 SU 7.8 Sales Variances Sales quantity variances BCM based on Actual Unit Sales BCM based on Budgeted Unit Sales Sales mix variances Actual units sold - BCM based on Actual mix BCM for the budgeted mix and actual total unit sales. Review page 273.

26

27

28 Problem Review Page 288 #37 Page 286 #38

Multiple Choice Questions

Multiple Choice Questions 1. The difference between the actual price and the standard price, multiplied by the actual quantity of materials purchased is the a) direct labor price variance b) direct labor

Multiple Choice Questions 1. The difference between the actual price and the standard price, multiplied by the actual quantity of materials purchased is the a) direct labor price variance b) direct labor

STANDARD COSTS AND VARIANCE ANALYSIS

STANDARD COSTS AND VARIANCE ANALYSIS Key Terms and Concepts to Know Static or Planning Budgets Used for planning purposes Prepared at the beginning of the period Based on one projected level of activity

STANDARD COSTS AND VARIANCE ANALYSIS Key Terms and Concepts to Know Static or Planning Budgets Used for planning purposes Prepared at the beginning of the period Based on one projected level of activity

Standard Cost System Practice Problems

When setting up a standard cost system, the concepts of standards in material, labor, and overhead must be explored in a simple manner to start the process. Practice Standard Cost Variances: Simple Example

When setting up a standard cost system, the concepts of standards in material, labor, and overhead must be explored in a simple manner to start the process. Practice Standard Cost Variances: Simple Example

Part 1 Study Unit 10. Cost And Variance Measures. By Ronald Schmidt, CMA, CFM

Part 1 Study Unit 10 Cost And Variance Measures By Ronald Schmidt, CMA, CFM Variance Analysis and overview A budget communicates to employees the organization s operational and strategic objectives Considerations:

Part 1 Study Unit 10 Cost And Variance Measures By Ronald Schmidt, CMA, CFM Variance Analysis and overview A budget communicates to employees the organization s operational and strategic objectives Considerations:

Flexible Budgets and Overhead Analysis

9-1 Today s Agenda Management Accounting Lecture 16 (Chapter 9) n What is a Flexible Budget n Flexible versus Static Budget n Shortcomings of Static Budgets Flexible Budgets and Overhead Analysis n Advantages

9-1 Today s Agenda Management Accounting Lecture 16 (Chapter 9) n What is a Flexible Budget n Flexible versus Static Budget n Shortcomings of Static Budgets Flexible Budgets and Overhead Analysis n Advantages

MGMT-027 Q4 17. The purpose of a flexible budget is to: C. update the static planning budget to reflect the actual level of activity of the period.

MGMT-027 Q4 17. The purpose of a flexible budget is to: C. update the static planning budget to reflect the actual level of activity of the period. 21. Salyers Family Inn is a bed and breakfast establishment

MGMT-027 Q4 17. The purpose of a flexible budget is to: C. update the static planning budget to reflect the actual level of activity of the period. 21. Salyers Family Inn is a bed and breakfast establishment

Standard Costs and Variances

10-1 Standard Costs and Variances Chapter 10 10-2 Standard Costs Standards are benchmarks or norms for measuring performance. In managerial accounting, two types of standards are commonly used. Quantity

10-1 Standard Costs and Variances Chapter 10 10-2 Standard Costs Standards are benchmarks or norms for measuring performance. In managerial accounting, two types of standards are commonly used. Quantity

Flexible Budgets and Standard Costing QUESTIONS

Chapter 21 Flexible Budgets and Standard Costing QUESTIONS 1. Fixed budget performance reports have limited usefulness because they do not reflect differences in revenues and variable costs that can occur

Chapter 21 Flexible Budgets and Standard Costing QUESTIONS 1. Fixed budget performance reports have limited usefulness because they do not reflect differences in revenues and variable costs that can occur

Chapter 10 Standard Costs and Variances

Chapter 10 Standard Costs and Variances Solutions to Questions 10-1 A quantity standard indicates how much of an input should be used to make a unit of output. A price standard indicates how much the input

Chapter 10 Standard Costs and Variances Solutions to Questions 10-1 A quantity standard indicates how much of an input should be used to make a unit of output. A price standard indicates how much the input

ACCY 121 Chapter 16 Practice Quiz Fundamentals of Variance Analysis (1)

") ACCY 121 Chapter 16 Practice Quiz Fundamentals of Variance Analysis (1) 101. The Hageness Company has had great difficulty in controlling overhead costs. At a recent convention, the president heard about

ACCY 121 Chapter 16 Practice Quiz Fundamentals of Variance Analysis (1) 101. The Hageness Company has had great difficulty in controlling overhead costs. At a recent convention, the president heard about

Add: manufacturing overhead costs in inventory under absorption costing +27,000 Net operating income under absorption costing $4,727,000

THE HONG KONG POLYTECHNIC UNIVERSITY HONG KONG COMMUNITY COLLEGE Subject Title : Cost Accounting Subject Code : CCN2111 Session : Semester One, 2018/19 Numerical Answer Question B1 Required production

THE HONG KONG POLYTECHNIC UNIVERSITY HONG KONG COMMUNITY COLLEGE Subject Title : Cost Accounting Subject Code : CCN2111 Session : Semester One, 2018/19 Numerical Answer Question B1 Required production

Chapter 11 Flexible Budgets and Overhead Analysis

Chapter 11 Flexible Budgets and Overhead Analysis Solutions to Questions 11-1 A static budget is a budget prepared for a single level of activity. The static budget is not adjusted even if the activity

Chapter 11 Flexible Budgets and Overhead Analysis Solutions to Questions 11-1 A static budget is a budget prepared for a single level of activity. The static budget is not adjusted even if the activity

Illustrative Example Xander Barkley s XYX Company manufactures a single product. The standard cost card for one unit is as follows:

Appendix 11A General Ledger Entries to Record Variances 11A-1 General Ledger Entries to Record Variances Although standard costs and variances can be computed and used by management without being formally

Appendix 11A General Ledger Entries to Record Variances 11A-1 General Ledger Entries to Record Variances Although standard costs and variances can be computed and used by management without being formally

Module 3 Introduction

Module 3 Introduction Module 3 Introduction This module is designed to further enhance knowledge about management accounting techniques. In particular, the student is introduced to the role of budgeting,

Module 3 Introduction Module 3 Introduction This module is designed to further enhance knowledge about management accounting techniques. In particular, the student is introduced to the role of budgeting,

ACC406 Tip Sheet. Direct Labour (DL): labour that is directly attributable to the goods and service that are being produced by a firm.

: labour that is directly attributable to the goods and service that are being produced by a firm.") ACC406 Tip Sheet Definitions Direct Cost: a cost that can be easily allocated to a certain object. Variable Cost (VC): a cost that changes in direct relation to output (output increases VC increases) Fixed

ACC406 Tip Sheet Definitions Direct Cost: a cost that can be easily allocated to a certain object. Variable Cost (VC): a cost that changes in direct relation to output (output increases VC increases) Fixed

THE HONG KONG POLYTECHNIC UNIVERSITY HONG KONG COMMUNITY COLLEGE

THE HONG KONG POLYTECHNIC UNIVERSITY HONG KONG COMMUNITY COLLEGE Subject Title : Cost Accounting Subject Code : CCN2111 Session : Semester Two, 2017/18 Numerical answers Question B1 (a) The company's DL

THE HONG KONG POLYTECHNIC UNIVERSITY HONG KONG COMMUNITY COLLEGE Subject Title : Cost Accounting Subject Code : CCN2111 Session : Semester Two, 2017/18 Numerical answers Question B1 (a) The company's DL

Solution to Problem 1 Material and labor variances

Professor Authored Problem Solutions Advanced Cost Accounting Acct 647 Variances Solution to Problem 1 Material and labor variances 1. Compute material price and quantity variances Std Cost = applied cost

Professor Authored Problem Solutions Advanced Cost Accounting Acct 647 Variances Solution to Problem 1 Material and labor variances 1. Compute material price and quantity variances Std Cost = applied cost

Introduction and Meaning Concept Advantages & Limitations Objectives of Standard Costing Preliminary Establishment Types of Standard

Standard Costing Introduction and Meaning Concept Advantages & Limitations Objectives of Standard Costing Preliminary Establishment Types of Standard Differences Standard Cost Card/Sheet Meaning of Analysis

Standard Costing Introduction and Meaning Concept Advantages & Limitations Objectives of Standard Costing Preliminary Establishment Types of Standard Differences Standard Cost Card/Sheet Meaning of Analysis

Both Isitya and Ikopi renders more net profit after further processing and should therefore be processed further.

OCT/NOV MAC2601 1.1 C Units purchased: 1 200 units Purchase price R6.80 Freight charges 0.68 Total 7.48 Value is therefore equal to 1200 units*7.48=r8 976 1.2 B 1.3 B 200 000 / 40 000 = R5 per machine

OCT/NOV MAC2601 1.1 C Units purchased: 1 200 units Purchase price R6.80 Freight charges 0.68 Total 7.48 Value is therefore equal to 1200 units*7.48=r8 976 1.2 B 1.3 B 200 000 / 40 000 = R5 per machine

Flexible Budgets, Variances, and Management Control: I

Flexible Budgets, Variances, and Management Control: I Static and Flexible Budgets A static budget is a budget prepared for only one level of activity. It is based on the level of output planned at the

Flexible Budgets, Variances, and Management Control: I Static and Flexible Budgets A static budget is a budget prepared for only one level of activity. It is based on the level of output planned at the

24 Control through standard costs

24 Control through standard costs 24.1 Learning objectives After studying this chapter, you should be able to: Discuss the nature of standard costs, including how standards are set. Define budgets and

24 Control through standard costs 24.1 Learning objectives After studying this chapter, you should be able to: Discuss the nature of standard costs, including how standards are set. Define budgets and

Flexible Budgets and Standard Costing Variance Analysis

Flexible Budgets and Standard Costing Variance Analysis 1 Static Budgets and Performance Reports CheeseCo 2 Preparing a Flexible Budget Cost Total Flexible Budgets Formula Fixed 8,000 10,000 12,000 per

Flexible Budgets and Standard Costing Variance Analysis 1 Static Budgets and Performance Reports CheeseCo 2 Preparing a Flexible Budget Cost Total Flexible Budgets Formula Fixed 8,000 10,000 12,000 per

Flexible Budgets. and Standard Costing Variance Analysis. Static Budgets and Performance Reports. Flexible Budget Performance Report

Static Budgets and Performance Reports Flexible Budgets CheeseCo and Standard Costing Variance Analysis 1 2 Preparing a Flexible Budget Cost Total Flexible Budgets Formula Fixed 8,000 10,000 12,000 per

Static Budgets and Performance Reports Flexible Budgets CheeseCo and Standard Costing Variance Analysis 1 2 Preparing a Flexible Budget Cost Total Flexible Budgets Formula Fixed 8,000 10,000 12,000 per

ACC406 Tip Sheet. 1) Planning: It is the process of creating a set of plans that a company intends to achieve a particular goal.

Planning: It is the process of creating a set of plans that a company intends to achieve a particular goal.") ACC406 Tip Sheet Chapter 1 Managerial Accounting: It is simply the process of reporting accounting information for a company s internal users such as managers, sales staff and etc. for decision making.

ACC406 Tip Sheet Chapter 1 Managerial Accounting: It is simply the process of reporting accounting information for a company s internal users such as managers, sales staff and etc. for decision making.

HOMEWORK. 1,40,000 20,000 (4,20,000 4,00,000) = 84,000 (F) WN 2: Calculation of effect on profit due to increase in market share

= 84,000 (F) WN 2: Calculation of effect on profit due to increase in market share") A.1. A.2. HOMEWORK WN 1: Calculation of effect on the profit due to market size Increasein profitduetogrowth = Growth in unitsdueto size increase Growth in units(total) 1,40,000 = 12,000(4,00,0003%) 20,000

A.1. A.2. HOMEWORK WN 1: Calculation of effect on the profit due to market size Increasein profitduetogrowth = Growth in unitsdueto size increase Growth in units(total) 1,40,000 = 12,000(4,00,0003%) 20,000

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 11 & 13. Chapter 11: Standard Costs and Variance Analysis

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 11 & 13 Chapter 11: Standard Costs and Variance Analysis Variance Analysis: calculating variances and investigating

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 11 & 13 Chapter 11: Standard Costs and Variance Analysis Variance Analysis: calculating variances and investigating

Chapter 16 Fundamentals of Variance Analysis

Chapter 16 Fundamentals of Variance Analysis True / False Questions 1. In essence, the terms "master budget" and "operating budget" mean the same thing and can be used interchangeably. True False 2. Variances

Chapter 16 Fundamentals of Variance Analysis True / False Questions 1. In essence, the terms "master budget" and "operating budget" mean the same thing and can be used interchangeably. True False 2. Variances

Disclaimer: This resource package is for studying purposes only EDUCATIO N

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 9: Budgeting The Basic Framework of Budgeting Master budget - a summary of a company s plans in which specific targets

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 9: Budgeting The Basic Framework of Budgeting Master budget - a summary of a company s plans in which specific targets

You were introduced to Standard Costing in the earlier stages of your studies in which you understood the following;

6 Standard Costing LEARNING OBJECTIVES : After studying this unit you will be able to : Understand terms as standard Cost, standard Costing, standard Hour Understand how a standard costing system operates

6 Standard Costing LEARNING OBJECTIVES : After studying this unit you will be able to : Understand terms as standard Cost, standard Costing, standard Hour Understand how a standard costing system operates

ACT 2131 (PJJ) TUTORIAL 6

TUTORIAL 6") ACT 2131 (PJJ) TUTORIAL 6 1. Describe the relationship that unit standards have with flexible budgeting. 2. Why is historical experience often a poor basis for establishing standards? 3. What are ideal

ACT 2131 (PJJ) TUTORIAL 6 1. Describe the relationship that unit standards have with flexible budgeting. 2. Why is historical experience often a poor basis for establishing standards? 3. What are ideal

REVIEW FOR EXAM NO. 3, ACCT-2302 (SAC) (Chapters 20-22)

(Chapters 20-22)") REVIEW FOR EXAM NO. 3, ACCT-2302 (SAC) (Chapters 20-22) A. Chapter 20 (Master Budgets and Performance Planning). 1. Budget. a. A plan detailing the acquisition and use of financial and other resources

REVIEW FOR EXAM NO. 3, ACCT-2302 (SAC) (Chapters 20-22) A. Chapter 20 (Master Budgets and Performance Planning). 1. Budget. a. A plan detailing the acquisition and use of financial and other resources

Page 1. 9 Standard. planning. cost and different. and. activity assumed in. different to $30 for. different particula

Standard Costing By Dr. Michael Constas Page 1 9 Standard Costing: A Functional-Based Control Approach Companies prepare cost budgets as part of their planning process. These budgets assume a given level

Standard Costing By Dr. Michael Constas Page 1 9 Standard Costing: A Functional-Based Control Approach Companies prepare cost budgets as part of their planning process. These budgets assume a given level

Chapter 23 Flexible Budgets and Standard Cost Systems

Chapter 23 Flexible Budgets and Standard Cost Systems Review Questions 1. What is a variance? A variance is the difference between an actual amount and the budgeted amount. 2. Explain the difference between

Chapter 23 Flexible Budgets and Standard Cost Systems Review Questions 1. What is a variance? A variance is the difference between an actual amount and the budgeted amount. 2. Explain the difference between

Performance. MCQs. Gleim Book. Gleim CD. IMA - Retired IMA - Retired Contains: in a random basis

Performance MCQs Contains: in a random basis Gleim Book Gleim CD IMA - Retired 2005 IMA - Retired 2008 By: Mohamed hengoo to dvd4arab.com members [1] Gleim #: 7.6.118 -- Source: Publisher Using the three-variance

Performance MCQs Contains: in a random basis Gleim Book Gleim CD IMA - Retired 2005 IMA - Retired 2008 By: Mohamed hengoo to dvd4arab.com members [1] Gleim #: 7.6.118 -- Source: Publisher Using the three-variance

VARIANCE ANALYSIS: ILLUSTRATION

VARIANCE ANALYSIS: ILLUSTRATION The following information relates to the production of product Alpha for the month of August Standard Cost Card Budgeted production overhead based on 10,000 units $ $ Selling

VARIANCE ANALYSIS: ILLUSTRATION The following information relates to the production of product Alpha for the month of August Standard Cost Card Budgeted production overhead based on 10,000 units $ $ Selling

b Multiple Choice Questions: 1 The scarce factor of production is known as: d a) Key factor b) Limiting factor c) Critical factor d) All of the above

Key factor b) Limiting factor c) Critical factor d) All of the above") Q.1 a State whether True or False: [Any 8] 1 Functional Budget is a Budget which is established for use over a short period of time. FALSE 2 Total Fixed cost remains constant irrespective of change in

Q.1 a State whether True or False: [Any 8] 1 Functional Budget is a Budget which is established for use over a short period of time. FALSE 2 Total Fixed cost remains constant irrespective of change in

PESIT Bangalore South Campus Hosur road, 1km before Electronic City, Bengaluru -100

INTERNAL ASSESSMENT TEST 3 Date : 09/11/2016 Max Marks : 50 Subject & Code : Cost Management (14MBAFM305) Section : Finance Name of faculty : Dr.R.Duraipandian Time: 8:30 10:00 AM Note: Answer all questions

INTERNAL ASSESSMENT TEST 3 Date : 09/11/2016 Max Marks : 50 Subject & Code : Cost Management (14MBAFM305) Section : Finance Name of faculty : Dr.R.Duraipandian Time: 8:30 10:00 AM Note: Answer all questions

Trainee Accountant Webinar. F2 Management Accounting. Variance Analysis

Trainee Accountant Webinar F2 Management Accounting Variance Analysis Presented By: Rosemarie Kelly, Examiner CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets,

Trainee Accountant Webinar F2 Management Accounting Variance Analysis Presented By: Rosemarie Kelly, Examiner CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets,

In Class #8.1 Coverage of manufacturing overhead, standard cost system Required 1 Solution Exhibit 8-1 shows the computations. Summary details are:

In Class #8.1 Coverage of manufacturing overhead, standard cost system Required 1 Solution Exhibit 8-1 shows the computations. Summary details are: Actual Flexible Budget Output units 49,200 49,200 Allocation

In Class #8.1 Coverage of manufacturing overhead, standard cost system Required 1 Solution Exhibit 8-1 shows the computations. Summary details are: Actual Flexible Budget Output units 49,200 49,200 Allocation

Costing Group 1 Important Questions for IPCC November 2017 (Chapters 10 12)

") Costing Group 1 Important Questions for IPCC November 2017 (Chapters 10 12) CHAPTER 10 STANDARD COSTING 1. The standard material cost for a normal mix of one tonne of product Captain based on: Raw Material

Costing Group 1 Important Questions for IPCC November 2017 (Chapters 10 12) CHAPTER 10 STANDARD COSTING 1. The standard material cost for a normal mix of one tonne of product Captain based on: Raw Material

ACCY 121 Chapter 16 Practice Quiz Fundamentals of Variance Analysis

ACCY 121 Chapter 16 Practice Quiz Fundamentals of Variance Analysis 101. The Hageness Company has had great difficulty in controlling overhead costs. At a recent convention, the president heard about a

ACCY 121 Chapter 16 Practice Quiz Fundamentals of Variance Analysis 101. The Hageness Company has had great difficulty in controlling overhead costs. At a recent convention, the president heard about a

CONCEPTS AND FORMULAE

CHAPTER 6 Standard Costing Basic Concepts 6.1 Meaning of Variance Analysis BASIC CONCEPTS AND FORMULAE Variance analysis is the analysis of the cost variances into its component parts with appropriate

CHAPTER 6 Standard Costing Basic Concepts 6.1 Meaning of Variance Analysis BASIC CONCEPTS AND FORMULAE Variance analysis is the analysis of the cost variances into its component parts with appropriate

a) It is important to note that Famba will only receive the commission on the ticket price of R (2000 x 12.5% commission = R250)

It is important to note that Famba will only receive the commission on the ticket price of R (2000 x 12.5% commission = R250)") QUESTION 1: a) It is important to note that Famba will only receive the commission on the ticket price of R2 000. (2000 x 12.5% commission = R250) Breakeven (units) = Fixed cost Marginal income (MI) =

QUESTION 1: a) It is important to note that Famba will only receive the commission on the ticket price of R2 000. (2000 x 12.5% commission = R250) Breakeven (units) = Fixed cost Marginal income (MI) =

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47

Time: 60 min Marks: 47") MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

Budget & Budgetary Control

4 Budget & Budgetary Control Question 1 A Company manufactures two Products A and B by making use of two types of materials, viz., X and Y. Product A requires 10 units of X and 3 units of Y. Product B

4 Budget & Budgetary Control Question 1 A Company manufactures two Products A and B by making use of two types of materials, viz., X and Y. Product A requires 10 units of X and 3 units of Y. Product B

9706 ACCOUNTING. Mark schemes should be read in conjunction with the question paper and the Principal Examiner Report for Teachers.

CAMBRIDGE INTERNATIONAL EXAMINATIONS GCE Advanced Level MARK SCHEME for the May/June 2013 series 9706 ACCOUNTING 9706/43 Paper 4 (Problem Solving Supplement), maximum raw mark 120 This mark scheme is published

CAMBRIDGE INTERNATIONAL EXAMINATIONS GCE Advanced Level MARK SCHEME for the May/June 2013 series 9706 ACCOUNTING 9706/43 Paper 4 (Problem Solving Supplement), maximum raw mark 120 This mark scheme is published

BALIUAG UNIVERSITY CPA REVIEW MANAGEMENT ADVISORY SERVICES STANDARD COST AND VARIANCE ANALYSIS THEORY

STANDARD COST AND VARIANCE ANALYSIS THEORY 1. How is labor rate variance computed? a. The difference between standard and actual rate multiplied by actual hours b. The difference between standard and actual

STANDARD COST AND VARIANCE ANALYSIS THEORY 1. How is labor rate variance computed? a. The difference between standard and actual rate multiplied by actual hours b. The difference between standard and actual

Purushottam Sir. Formulas of Costing

Purushottam Sir Formulas of Costing Material Maximum Stock Level= Re-order level + Re-order quantity (Minimum consumption Minimum reorder period) Minimum Stock Level= Re-order level (Average lead time

Purushottam Sir Formulas of Costing Material Maximum Stock Level= Re-order level + Re-order quantity (Minimum consumption Minimum reorder period) Minimum Stock Level= Re-order level (Average lead time

CHAPTER 8 FLEXIBLE BUDGETS, OVERHEAD COST VARIANCES, AND MANAGEMENT CONTROL

CHAPTER 8 FLEXIBLE BUDGETS, OVERHEAD COST VARIANCES, AND MANAGEMENT CONTROL 8-1 Effective planning of variable overhead costs involves: 1. Planning to undertake only those variable overhead activities

CHAPTER 8 FLEXIBLE BUDGETS, OVERHEAD COST VARIANCES, AND MANAGEMENT CONTROL 8-1 Effective planning of variable overhead costs involves: 1. Planning to undertake only those variable overhead activities

CHAPTER 8: PERFORMANCE EVALUATION Pearson Education. All rights reserved.

CHAPTER 8: PERFORMANCE EVALUATION Learning Objectives 1. Explain static budgets and static-budget variances 2. Develop flexible budgets and compute flexiblebudget variances and sales-volume variances 3.

CHAPTER 8: PERFORMANCE EVALUATION Learning Objectives 1. Explain static budgets and static-budget variances 2. Develop flexible budgets and compute flexiblebudget variances and sales-volume variances 3.

Analyzing Financial Performance Reports

Analyzing Financial Performance Reports Calculating Variances Effective systems identify variances down to the lowest level of management. Variances are hierarchical. As shown in Exhibit 10.2, they begin

Analyzing Financial Performance Reports Calculating Variances Effective systems identify variances down to the lowest level of management. Variances are hierarchical. As shown in Exhibit 10.2, they begin

STANDARD COSTING. Samir K Mahajan

STANDARD COSTING Samir K Mahajan Standard Costing Historical costs: Historical costing or actual costing is a system where costs are ascertained after they are incurred. It is a post-mortem of the costs.

STANDARD COSTING Samir K Mahajan Standard Costing Historical costs: Historical costing or actual costing is a system where costs are ascertained after they are incurred. It is a post-mortem of the costs.

PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART-I: COST ACCOUNTING QUESTIONS

Material PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART-I: COST ACCOUNTING QUESTIONS 1. Banerjee Brothers (BB) supplies surgical gloves to nursing homes and polyclinics in the city. These surgical

Material PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART-I: COST ACCOUNTING QUESTIONS 1. Banerjee Brothers (BB) supplies surgical gloves to nursing homes and polyclinics in the city. These surgical

Solved Answer COST & F.M. CA IPCC Nov

Solved Answer COST & F.M. CA IPCC Nov. 2009 1 1. Answer any five of the following : [5x2=10 marks] (i) Define the following : (a) Imputed cost (b) Capitalised cost. (ii) Calculate efficiency, and activity

Solved Answer COST & F.M. CA IPCC Nov. 2009 1 1. Answer any five of the following : [5x2=10 marks] (i) Define the following : (a) Imputed cost (b) Capitalised cost. (ii) Calculate efficiency, and activity

b) To answer any questing dealing with variances work out the rates and the cost per unit i.e. work out the standard cost per unit.

To answer any questing dealing with variances work out the rates and the cost per unit i.e. work out the standard cost per unit.") QUESTION ONE a) Basic Standards These are standards which are kept unaltered over a long period of time and may be out of date. These are used to show changes in efficiency or performance over a long period

QUESTION ONE a) Basic Standards These are standards which are kept unaltered over a long period of time and may be out of date. These are used to show changes in efficiency or performance over a long period

Chapter 8 Responsibility Accounting Chapter Review Solutions

Management Accounting in Australia - Solutions Chapter 8 Responsibility Accounting Chapter Review Solutions 1 F 220,500 Fixed 216,000 21,000 x $18.90 V 170,940 Variable 21,000 x $8.10 170,100 $391,440

Management Accounting in Australia - Solutions Chapter 8 Responsibility Accounting Chapter Review Solutions 1 F 220,500 Fixed 216,000 21,000 x $18.90 V 170,940 Variable 21,000 x $8.10 170,100 $391,440

LINEAR PROGRAMMING C H A P T E R 7

LINEAR PROGRAMMING C H A P T E R 7 INTRODUCTION In decision making, when there is only one limiting factor (scarce resource), we can rank the products according the contribution per unit of scarce resource.

LINEAR PROGRAMMING C H A P T E R 7 INTRODUCTION In decision making, when there is only one limiting factor (scarce resource), we can rank the products according the contribution per unit of scarce resource.

STANDARD COSTING. Samir K Mahajan

STANDARD COSTING Samir K Mahajan Standard Costing Historical costs: Historical costing or actual costing is a system where costs are ascertained after they are incurred. It is a post-mortem of the costs.

STANDARD COSTING Samir K Mahajan Standard Costing Historical costs: Historical costing or actual costing is a system where costs are ascertained after they are incurred. It is a post-mortem of the costs.

December CS Executive Programme Module - I Paper - 2

December - 2015 CS Executive Programme Module - I Paper - 2 (New Syllabus) Cost and Management Accounting Total number of questions: 100 Maximum marks: 100 Assertion A: 1. In management accounting, firm

December - 2015 CS Executive Programme Module - I Paper - 2 (New Syllabus) Cost and Management Accounting Total number of questions: 100 Maximum marks: 100 Assertion A: 1. In management accounting, firm

Particulars VIP Middle Last = = % of 60 = 30

Ans. 1: 1. Basic Computations Less: Less: Gross Seats Free Seats Net Saleable Seats Particulars VIP Middle Last Firm Booking by Troupe 3 3 = 9 1 3 = 3 6 5% of 6 = 3 18 2 = 36 Nil 36 5% of 36 = 18 6 3 =

Ans. 1: 1. Basic Computations Less: Less: Gross Seats Free Seats Net Saleable Seats Particulars VIP Middle Last Firm Booking by Troupe 3 3 = 9 1 3 = 3 6 5% of 6 = 3 18 2 = 36 Nil 36 5% of 36 = 18 6 3 =

COPYRIGHT PAGE. Published by: Flat World Knowledge, Inc th St NW Washington, DC 20036

COPYRIGHT PAGE Published by: Flat World Knowledge, Inc. 1111 19 th St NW Washington, DC 20036 2016 by Flat World Knowledge, Inc. All rights reserved. Your use of this work is subject to the License Agreement

COPYRIGHT PAGE Published by: Flat World Knowledge, Inc. 1111 19 th St NW Washington, DC 20036 2016 by Flat World Knowledge, Inc. All rights reserved. Your use of this work is subject to the License Agreement

Principles of Management Accounting (MAC2601)

") MAC2601/103/1/2013 Principles of Management Accounting (MAC2601) TUTOIAL LETTE 103 General exam guidelines and additional questions for practice DEPATMENT OF MANAGEMENT ACCOUNTING CONTENTS 1. INTODUCTION...

MAC2601/103/1/2013 Principles of Management Accounting (MAC2601) TUTOIAL LETTE 103 General exam guidelines and additional questions for practice DEPATMENT OF MANAGEMENT ACCOUNTING CONTENTS 1. INTODUCTION...

Chapter 11. Standard costs for control: flexible budgets and. manufacturing overhead

Chapter 11 Standard costs for control: flexible budgets and manufacturing overhead Copyright 2003 McGraw-Hill Australia Pty Ltd, PPTs t/a Management Accounting: An Australian Perspective 3/e by Langfield-Smith,

Chapter 11 Standard costs for control: flexible budgets and manufacturing overhead Copyright 2003 McGraw-Hill Australia Pty Ltd, PPTs t/a Management Accounting: An Australian Perspective 3/e by Langfield-Smith,

SUGGESTED SOLUTION INTERMEDIATE N 2018 EXAM

SUGGESTED SOLUTION INTERMEDIATE N 2018 EXAM SUBJECT- COSTING Test Code CIN 5013 Date: 02.09.2018 Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 ANSWER-1

SUGGESTED SOLUTION INTERMEDIATE N 2018 EXAM SUBJECT- COSTING Test Code CIN 5013 Date: 02.09.2018 Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 ANSWER-1

Standard Cost. Types of Standards

Standard Cost A standard cost is the predetermined cost of manufacturing a single unit or a number of product units during a specific period in the immediate future. It is the planned cost of a product

Standard Cost A standard cost is the predetermined cost of manufacturing a single unit or a number of product units during a specific period in the immediate future. It is the planned cost of a product

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING Answer all questions.

Question 1 (i) (ii) PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING Answer all questions. What is Cost accounting? Enumerate its important objectives. Distinguish between Fixed

Question 1 (i) (ii) PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING Answer all questions. What is Cost accounting? Enumerate its important objectives. Distinguish between Fixed

Online Course Manual By Craig Pence. Module 7

Online Course Manual By Craig Pence Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled

Online Course Manual By Craig Pence Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled

Bob Livingston, PhD Cindy Moriarty Jerry Ramos

MANAGERIAL ACCOUNTING _ Bob Livingston, PhD Cindy Moriarty Jerry Ramos Chapter 10: How Do Managers Evaluate Performance Using Cost Variance Analysis? 10.1 Flexible Budgets 10.2 Standard Costs 10.3 Direct

MANAGERIAL ACCOUNTING _ Bob Livingston, PhD Cindy Moriarty Jerry Ramos Chapter 10: How Do Managers Evaluate Performance Using Cost Variance Analysis? 10.1 Flexible Budgets 10.2 Standard Costs 10.3 Direct

Paper P1 Performance Operations Russian Diploma Post Exam Guide November 2012 Exam. General Comments

General Comments This paper was generally well attempted by candidates, as evidenced by the overall pass rate. The one question which posed a significant challenge was Question 3, where candidates had

General Comments This paper was generally well attempted by candidates, as evidenced by the overall pass rate. The one question which posed a significant challenge was Question 3, where candidates had

SAPAN PARIKHCOMMERCE CLASSES

A.1 A Match the following (Any 08) [Rewrite the sentence] GROUP A GROUP B 1) Labour efficiency Variance A) Pre-determined cost 2) Imputed Cost B) Limiting Factor 3) Profit C) No Profit, No Loss stage 4)

A.1 A Match the following (Any 08) [Rewrite the sentence] GROUP A GROUP B 1) Labour efficiency Variance A) Pre-determined cost 2) Imputed Cost B) Limiting Factor 3) Profit C) No Profit, No Loss stage 4)

2018 LAST MINUTE CPA EXAM NOTES

2018 LAST MINUTE CPA EXAM NOTES Page intentionally left blank 2018 LAST MINUTE CPA EXAM NOTES BEC (Volume 1) Copyright 2018 by Glomont LLC. First edition Notice of Rights. All rights reserved. No part

2018 LAST MINUTE CPA EXAM NOTES Page intentionally left blank 2018 LAST MINUTE CPA EXAM NOTES BEC (Volume 1) Copyright 2018 by Glomont LLC. First edition Notice of Rights. All rights reserved. No part

CHAPTER 13 BUDGETING AND STANDARD COST SYSTEMS

CHAPTER 13 BUDGETING AND STANDARD COST SYSTEMS CLASS DISCUSSION QUESTIONS 1. The three major objectives of budgeting are (1) to establish specific goals for future operations, (2) to direct and coordinate

CHAPTER 13 BUDGETING AND STANDARD COST SYSTEMS CLASS DISCUSSION QUESTIONS 1. The three major objectives of budgeting are (1) to establish specific goals for future operations, (2) to direct and coordinate

TOPPER S INSTITUTE [COSTING] RTP 16 TOPPER S INSTITUE CA INTER COST MGT. ACCOUNTING - RTP

![TOPPER S INSTITUTE [COSTING] RTP 16 TOPPER S INSTITUE CA INTER COST MGT. ACCOUNTING - RTP](/thumbs/80/82165207.jpg "TOPPER S INSTITUTE [COSTING] RTP 16 TOPPER S INSTITUE CA INTER COST MGT. ACCOUNTING - RTP") TOPPER S INSTITUTE [COSTING] RTP 16 TOPPER S INSTITUE CA INTER COST MGT. ACCOUNTING - RTP Q1. is compulsory, Attempt any Five questions from the remaining Six questions Working Notes should form part of

TOPPER S INSTITUTE [COSTING] RTP 16 TOPPER S INSTITUE CA INTER COST MGT. ACCOUNTING - RTP Q1. is compulsory, Attempt any Five questions from the remaining Six questions Working Notes should form part of

Required: (a) Calculate total wages and average wages per worker per month, under the each scenario, when

Calculate total wages and average wages per worker per month, under the each scenario, when") PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I: COST ACCOUNTING QUESTIONS Material 1. Aditya Brothers supplies surgical gloves to nursing homes and polyclinics in the city. These surgical gloves

PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I: COST ACCOUNTING QUESTIONS Material 1. Aditya Brothers supplies surgical gloves to nursing homes and polyclinics in the city. These surgical gloves

Financial Management. 2 June Marking Scheme

Financial Management 2 June 2015 Marking Scheme This marking scheme has been prepared as a guide only to markers. This is not a set of model answers, or the exclusive answers to the questions, and there

Financial Management 2 June 2015 Marking Scheme This marking scheme has been prepared as a guide only to markers. This is not a set of model answers, or the exclusive answers to the questions, and there

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 M BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION INTERMEDIATE M 19 EXAM SUBJECT- COSTING Test Code - PIN 5043 M BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

MISC QUESTIONS FOR STUDENTS

MISC QUESTIONS FOR STUDENTS Question 1: Lee Electronics manufactures four types of electronic products A, B, C and D. All these products have a good demand in the market. The following figures are given

MISC QUESTIONS FOR STUDENTS Question 1: Lee Electronics manufactures four types of electronic products A, B, C and D. All these products have a good demand in the market. The following figures are given

Standard Costing and Budgetary Control CA

Standard Costing and Budgetary Control CA Past Years Exam Answers Answer to Q.1 (Nov, 2008) SP SQAO M 1 ` 6/kg. 500 kgs. = ` 3,000 SP AQ M 2 ` 6/kg. 450 kgs. = ` 2,700 AP AQ M 3 ` 8/kg. 450 kgs. = ` 3,600

Standard Costing and Budgetary Control CA Past Years Exam Answers Answer to Q.1 (Nov, 2008) SP SQAO M 1 ` 6/kg. 500 kgs. = ` 3,000 SP AQ M 2 ` 6/kg. 450 kgs. = ` 2,700 AP AQ M 3 ` 8/kg. 450 kgs. = ` 3,600

Gleim CPA Review Updates to Business 2011 Edition, 1st Printing March 10, 2011

Page 1 of 6 Gleim CPA Review Updates to Business 2011 Edition, 1st Printing March 10, 2011 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown

Page 1 of 6 Gleim CPA Review Updates to Business 2011 Edition, 1st Printing March 10, 2011 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Variances A variance is the difference between a planned, budgeted, or standard cost and the actual cost incurred.

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Variances A variance is the difference between a planned, budgeted, or standard cost and the actual cost incurred.

Free of Cost ISBN : Scanner Appendix. CS Executive Programme Module - I December Paper - 2 : Cost and Management Accounting

Free of Cost ISBN : 978-93-5034-831-4 Solved Scanner Appendix CS Executive Programme Module - I December - 2013 Paper - 2 : Cost and Management Accounting Chapter - 1: Introduction to Cost and Management

Free of Cost ISBN : 978-93-5034-831-4 Solved Scanner Appendix CS Executive Programme Module - I December - 2013 Paper - 2 : Cost and Management Accounting Chapter - 1: Introduction to Cost and Management

Preparing and using budgets

Osborne Books Tutor Zone Preparing and using budgets Chapter activities Osborne Books Limited, 2013 2 p r e p a r i n g a n d u s i n g b u d g e t s t u t o r z o n e 1 The budgeting environment 1.1 Match

Osborne Books Tutor Zone Preparing and using budgets Chapter activities Osborne Books Limited, 2013 2 p r e p a r i n g a n d u s i n g b u d g e t s t u t o r z o n e 1 The budgeting environment 1.1 Match

SUGGESTED SOLUTIONS Fundamentals of Management Accounting and Business Finance Certificate in Accounting and Business II Examination March 2013

SUGGESTED SOLUTIONS 05204 Fundamentals of Management Accounting and Business Finance Certificate in Accounting and Business II Examination March 2013 THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA

SUGGESTED SOLUTIONS 05204 Fundamentals of Management Accounting and Business Finance Certificate in Accounting and Business II Examination March 2013 THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA

Q. 2 Forecast Statement: Rupees

SUGGESTED ANSWERS SPRING 25 EXAMINATIONS 1 of 7 Q. 2 Forecast Statement: Hotels Marts Budgeted gross contribution margin 496,000 464,000 ( each) Budgeted variable costs: Sales reps commission (W-2) 34,560

SUGGESTED ANSWERS SPRING 25 EXAMINATIONS 1 of 7 Q. 2 Forecast Statement: Hotels Marts Budgeted gross contribution margin 496,000 464,000 ( each) Budgeted variable costs: Sales reps commission (W-2) 34,560

Exercise E21-1 page 932. (a) Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000

Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000") Exercise E21-1 (a) Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000 Employer Fringe Benefits Payable 4,000 (b) Work in Process Inventory 92,700 Manufacturing Overhead

Exercise E21-1 (a) Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000 Employer Fringe Benefits Payable 4,000 (b) Work in Process Inventory 92,700 Manufacturing Overhead

5_MGT402_Spring_2010_Final_Term_Solved_paper

5_MGT402_Spring_2010_Final_Term_Solved_paper http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one BDH produced 30,500 units of Kisty (a product). Each unit of Kisty takes two units

5_MGT402_Spring_2010_Final_Term_Solved_paper http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one BDH produced 30,500 units of Kisty (a product). Each unit of Kisty takes two units

Student Learning Outcomes

Chapter 11 Flexible Budgeting and the Management of Overhead andsupport Activity Costs ACG 6309 Dr. Chula King Student Learning Outcomes Distinguish between static and flexible budgets and explain the

Chapter 11 Flexible Budgeting and the Management of Overhead andsupport Activity Costs ACG 6309 Dr. Chula King Student Learning Outcomes Distinguish between static and flexible budgets and explain the

Management Accounting Fundamentals Module 8 Fixed overhead analysis and reporting for control

Management Accounting Fundamentals Module 8 Fixed overhead analysis and reporting for control Lectures and handouts by: Shirley Mauger, MBA, HB Comm, CGA Module 8 - Table of Contents Part Content 1 8.1

Management Accounting Fundamentals Module 8 Fixed overhead analysis and reporting for control Lectures and handouts by: Shirley Mauger, MBA, HB Comm, CGA Module 8 - Table of Contents Part Content 1 8.1

SAMPLE QUESTIONS - PART 2

Section A. Budget Preparation SAMPLE QUESTIONS - PART 2 1. Trumbull Company has budgeted sales on account of $120,000 for July, $210,000 for August, and $195,000 for September. Collection experience indicates

Section A. Budget Preparation SAMPLE QUESTIONS - PART 2 1. Trumbull Company has budgeted sales on account of $120,000 for July, $210,000 for August, and $195,000 for September. Collection experience indicates

BATCH All Batches. DATE: MAXIMUM MARKS: 100 TIMING: 3 Hours. PAPER 3 : Cost Accounting

BATCH All Batches DATE: 25.09.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 3 : Cost Accounting Q. No. 1 is compulsory. Wherever necessary suitable assumptions should be made by the candidates. Working

BATCH All Batches DATE: 25.09.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 3 : Cost Accounting Q. No. 1 is compulsory. Wherever necessary suitable assumptions should be made by the candidates. Working

CMA. Financial Reporting, Planning, Performance, and Control

2019 Edition CMA Preparatory Program Part 1 Financial Reporting, Planning, Performance, and Control Manufacturing Input Variances Sample Brian Hock, CMA, CIA and Lynn Roden, CMA HOCK international, LLC

2019 Edition CMA Preparatory Program Part 1 Financial Reporting, Planning, Performance, and Control Manufacturing Input Variances Sample Brian Hock, CMA, CIA and Lynn Roden, CMA HOCK international, LLC

C9: Accounting and Finance Course

LECTURER MANUAL C9: Accounting and Finance Course Lecturer Manual [Add institute name here] [Add School/Department name here] Copyright Commonwealth of Learning 2012 All rights reserved. No part of this

LECTURER MANUAL C9: Accounting and Finance Course Lecturer Manual [Add institute name here] [Add School/Department name here] Copyright Commonwealth of Learning 2012 All rights reserved. No part of this

Practice Costing and Operation Control

Note to student: Some of the following activities will require the student to use a calculator. Scenario: You are an accountant for Scrumptious, a large food manufacturing plant, and you work in the accounting

Note to student: Some of the following activities will require the student to use a calculator. Scenario: You are an accountant for Scrumptious, a large food manufacturing plant, and you work in the accounting

Chapter 2 Job-Order Costing: Calculating Unit Product Costs

Managerial Accounting 16th Edition Garrison Solutions Manual Full Download: http://testbanklive.com/download/managerial-accounting-16th-edition-garrison-solutions-manual/ Chapter 2 Job-Order Costing: Calculating

Managerial Accounting 16th Edition Garrison Solutions Manual Full Download: http://testbanklive.com/download/managerial-accounting-16th-edition-garrison-solutions-manual/ Chapter 2 Job-Order Costing: Calculating

Answer to MTP_Intermediate_Syl2016_June2017_Set 2 Paper 10- Cost & Management Accounting and Financial Management

Paper 10- Cost & Management Accounting and Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-10: Cost & Management

Paper 10- Cost & Management Accounting and Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-10: Cost & Management

Part 2 : 11/11/10 07:41:20

Question 1 - CMA 694 3-29 - Performance Measurement Part 2 : 11/11/10 07:41:20 One approach to measuring divisional performance is return on investment. Return on investment is expressed as operating income

Question 1 - CMA 694 3-29 - Performance Measurement Part 2 : 11/11/10 07:41:20 One approach to measuring divisional performance is return on investment. Return on investment is expressed as operating income

MTP_ Inter _Syllabus 2016_ Dec 2017_Set 2 Paper 10 Cost & Management Accounting and Financial Management

Paper 10 Cost & Management Accounting and Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 10 Cost & Management

Paper 10 Cost & Management Accounting and Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 10 Cost & Management

SUGGESTED SOLUTION FINAL MAY 2014 EXAM

SUGGESTED SOLUTION FINAL MAY 2014 EXAM ADVANCED MANAGEMENT ACCOUNTING Prelims (Test Code - F N J 3 0 5) (Date : 08 April, 2014) Head Office :Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai

SUGGESTED SOLUTION FINAL MAY 2014 EXAM ADVANCED MANAGEMENT ACCOUNTING Prelims (Test Code - F N J 3 0 5) (Date : 08 April, 2014) Head Office :Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai

SUGGESTED SOLUTIONS. KE2 Management Accounting Information. March All Rights Reserved

SUGGESTED SOLUTIONS KE2 Management Accounting Information March 2015 All Rights Reserved SECTION 1 Answer 01 1(a) 1.1 Relevant Learning Outcome/s: 1.1.2 Correct answer: C Direct cost can either be variable

SUGGESTED SOLUTIONS KE2 Management Accounting Information March 2015 All Rights Reserved SECTION 1 Answer 01 1(a) 1.1 Relevant Learning Outcome/s: 1.1.2 Correct answer: C Direct cost can either be variable

Answer to MTP_Intermediate_Syl2016_June2018_Set 1 Paper 8- Cost Accounting

Paper 8- Cost Accounting DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Cost Accounting Full Marks: 100 Time allowed: 3 hours Section- A Answer the following

Paper 8- Cost Accounting DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Cost Accounting Full Marks: 100 Time allowed: 3 hours Section- A Answer the following