Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

|

|

|

- Jason Patterson

- 6 years ago

- Views:

Transcription

1 Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

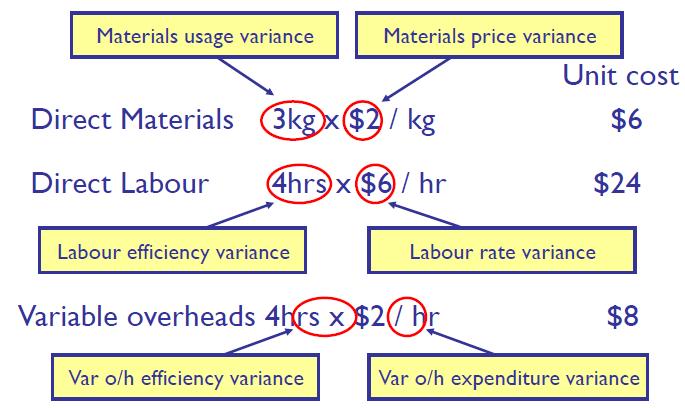

2 Variances A variance is the difference between a planned, budgeted, or standard cost and the actual cost incurred. The same compressions may be made for revenues. The process by which the total difference between standard and actual results is analysed is known as variance analysis.

3 Direct Material Cost Variances The direct material total variance can be subdivided into the direct material variance and the direct material usage variance.

4 Direct Material Cost Variances The direct material total variance is the difference between what the output actually cost and what it should have cost, in terms of material.

5 Direct Material Cost Variances The direct material price variance This is the difference between the standard cost and the actual cost for the actual quantity of material used or purchased. In other words, it is the difference between what the material did cost and what it should have cost.

6 Direct Material Cost Variances The direct material usage variance This is the difference between the standard quantity of materials that should have been used for the number of units actually produced, and the actual quantity of material used, valued at the standard cost per unit of material.

7 Direct Material Cost Variances In other words, it is the difference between how much material should have been used and how much material was used, valued at standard cost.

8 Material Variances & Opening & Closing Inventory Direct material price variances are usually extracted at the time of the receipt of the materials rather than at the time of usage.

9 Direct Labour Cost Variances The direct labour total variance can be subdivided into the direct labour rate variance and the direct labour efficiency variance.

10 Direct Labour Cost Variances The direct labour total variance is the difference between what the output should have cost and what it did cost, in terms of labour.

11 Direct Labour Cost Variances The direct labour rate variance This is similar to the direct material price variance. It is the difference between the standard cost and the actual cost for the actual number of hours paid for.

12 Direct Labour Cost Variances The direct labour efficiency variance This is similar to the direct material usage variance. It is the difference between the hours that should have been worked for the number of units actually produced, and the actual number of hours worked, value at the standard rate per hour.

13 Direct Labour Cost Variances In other words, it is the difference between how many hours should have been worked and how many hours were worked, valued at the standard rate per hour.

14 Variable Production Overhead Variances The variable production OH total variance can be subdivided into the variable production OH expenditure variance and the variable production OH efficiency variance (based on actual hours).

15 Variable Production Overhead Variances The variable production overhead expenditure variance is the difference between the amount of variable production overhead that should have been incurred in the actual hours actively worked, and the actual amount of variable production overhead incurred.

16 Variable Production Overhead Variances The variable production OH efficiency variance is exactly the same in hours, but priced at the variable production OH rate per hour.

17 Fixed Production Overhead Variances The fixed production OH total variance can be subdivided into an expenditure variance and a volume variance. The fixed production OH volume variance can be further subdivided into an efficiency and capacity variance.

18 Under/Over Absorption Absorption rate is calculated as follows: OAR = Budgeted fixed OH/Budgeted activity level

19 Fixed OH Variances Fixed OH total variance is the difference between fixed OH incurred and fixed OH absorbed. In other words, it is the under/over absorbed fixed OH.

20 Fixed OH Variances Fixed OH expenditure variance is the difference between the budgeted fixed OH expenditure and actual fixed OH expenditure.

21 Fixed OH Variances Fixed OH volume variance is the difference between actual and budgeted (planned)volume multiplied by the standard absorption rate per unit.

22 Fixed OH Variances Fixed OH volume efficiency variance is the difference between the number of hours that actual production should have taken, and the number of hours actually taken (that is, worked) multiplied by the standard absorption rate per hour.

23 Fixed OH Variances Fixed OH volume capacity variance is the difference between budgeted (planned) hours of work and the actual hours worked, multiplied by the standard absorption rate per hour.

24 Variances

25 Flexed Budgets & Variances Total variances are the difference between flexed budget figures and actual figures.

26 The Reasons for Cost Variances Variances Favorable Adverse Material price Unforeseen discount received More care taken in purchasing Change in material standard Material usage Material used of higher quality than standard More effective use made of material Errors in allocating material to jobs Price increase Careless purchasing Change in material standard Defective material Excessive waste Theft Stricter quality control Errors in allocating material to jobs

27 The Reasons for Cost Variances Variances Favorable Adverse Labour rate Use of apprentices or other workers at a rate of pay lower than standards Labour efficiency Output produced more quickly than expected because of work motivation, better quality of equipment or materials, or better methods. Errors in allocating time to job Wage rate increase Use of higher grade labour Lost time in excess of standard allowed Output lower than standard set because of deliberate restriction, lack of training, or sub standard material used Errors in allocating time to jobs.

28 The Reasons for Cost Variances Variances Favorable Adverse OH expenditure Saving in cost incurred More economical use of services. OH volume efficiency Labour force working more efficiently. OH volume capacity Labour force working overtime Increase in cost of services used. Excessive use of services. Change in type of service used. Labour force working less efficiently. Machine breakdown, strikes, labour shortages.

29 The Significance of Cost Variances Materiality, controllability, the type of standard being used, the interdependence of variances and the cost of an investigation should be taken into account when deciding whether to investigate reported variances.

30 Remember In general, a favorable cost variance (Fixed OH total variance, Fixed OH expenditure variance & Fixed OH volume efficiency variance) will arise if actual results are less than expected results. BUT

31 Remember A favorable Fixed OH volume variance occurs when actual production is greater than budgeted (planned) production. A favorable Fixed OH volume capacity variance occurs when actual hours of work are greater than budgeted (planned) hours of work.

32 Q & A

Chapter 6 Overheads & Absorption Costing. Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Chapter 6 Overheads & Absorption Costing Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Overheads Overheads is the cost incurred in the course of making a product,

Chapter 6 Overheads & Absorption Costing Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Overheads Overheads is the cost incurred in the course of making a product,

state the objectives of variance analysis understand the linkage between individual variances and the difference between budgeted and actual profit

1 INTRODUCTION In this lesson we explain the objective of analysis and provide a practical example of how the difference between budgeted and actual profit can be broken down into its constituent elements

1 INTRODUCTION In this lesson we explain the objective of analysis and provide a practical example of how the difference between budgeted and actual profit can be broken down into its constituent elements

Revision of management accounting

1 Revision of management accounting The following topics are covered in this chapter: Standard costing Flexible budgeting Absorption and marginal costing 1.1 STANDARD COSTING LEARNING SUMMARY After studying

1 Revision of management accounting The following topics are covered in this chapter: Standard costing Flexible budgeting Absorption and marginal costing 1.1 STANDARD COSTING LEARNING SUMMARY After studying

Trainee Accountant Webinar. F2 Management Accounting. Variance Analysis

Trainee Accountant Webinar F2 Management Accounting Variance Analysis Presented By: Rosemarie Kelly, Examiner CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets,

Trainee Accountant Webinar F2 Management Accounting Variance Analysis Presented By: Rosemarie Kelly, Examiner CPA Ireland Skillnet CPA Ireland Skillnet, is a training network that is funded by Skillnets,

Preparing and using budgets

Osborne Books Tutor Zone Preparing and using budgets Chapter activities Osborne Books Limited, 2013 2 p r e p a r i n g a n d u s i n g b u d g e t s t u t o r z o n e 1 The budgeting environment 1.1 Match

Osborne Books Tutor Zone Preparing and using budgets Chapter activities Osborne Books Limited, 2013 2 p r e p a r i n g a n d u s i n g b u d g e t s t u t o r z o n e 1 The budgeting environment 1.1 Match

VARIANCE ANALYSIS: ILLUSTRATION

VARIANCE ANALYSIS: ILLUSTRATION The following information relates to the production of product Alpha for the month of August Standard Cost Card Budgeted production overhead based on 10,000 units $ $ Selling

VARIANCE ANALYSIS: ILLUSTRATION The following information relates to the production of product Alpha for the month of August Standard Cost Card Budgeted production overhead based on 10,000 units $ $ Selling

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Responsibility A responsibility centre is a function or department of an organization that is headed by a manager

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Responsibility A responsibility centre is a function or department of an organization that is headed by a manager

EXCEL PROFESSIONAL INSTITUTE. LECTURE 9 Holy & Winfred

EXCEL PROFESSIONAL INSTITUTE 1 LECTURE 9 Holy & Winfred 2 Q1. a) Investment Appraisal Lecture 10 &11 i. Types of Investment and Capital Expenditure ii. Objectives of Investment appraisal iii. Investment

EXCEL PROFESSIONAL INSTITUTE 1 LECTURE 9 Holy & Winfred 2 Q1. a) Investment Appraisal Lecture 10 &11 i. Types of Investment and Capital Expenditure ii. Objectives of Investment appraisal iii. Investment

Engineering Economics and Financial Accounting

Engineering Economics and Financial Accounting Unit 4: Costing Major Topics are: Job Costing Operating Costing Process Costing Standard Costing (Variance Analysis) Gross Domestic Product (GDP) Job Costing

Engineering Economics and Financial Accounting Unit 4: Costing Major Topics are: Job Costing Operating Costing Process Costing Standard Costing (Variance Analysis) Gross Domestic Product (GDP) Job Costing

Standard Costing and Budgetary Control

Standard Costing and Budgetary Control CA Past Years Exam Questions Question : 1 (Nov, 2008) UV Limited presents the following information for November. Calculate the cost Variances. Budgeted production

Standard Costing and Budgetary Control CA Past Years Exam Questions Question : 1 (Nov, 2008) UV Limited presents the following information for November. Calculate the cost Variances. Budgeted production

ACCA. Paper F2 and FMA. Management Accounting December 2014 to June Interim Assessment Answers

ACCA Paper F2 and FMA Management Accounting December 204 to June 205 Interim Assessment Answers To gain maximum benefit, do not refer to these answers until you have completed the interim assessment questions

ACCA Paper F2 and FMA Management Accounting December 204 to June 205 Interim Assessment Answers To gain maximum benefit, do not refer to these answers until you have completed the interim assessment questions

10,000 units x 24 = 240,000, or 5,000 hours x 48 = 240,000. the actual price of materials per kilogram

NVQ/SVQ Level 4 in Accounting Contributing to the Management of Performance and Enhancement of Value (PEV) (2003 standards) June 2006 SUGGESTED ANSWERS Note: The suggested answers may, in parts, be longer

NVQ/SVQ Level 4 in Accounting Contributing to the Management of Performance and Enhancement of Value (PEV) (2003 standards) June 2006 SUGGESTED ANSWERS Note: The suggested answers may, in parts, be longer

Analysing costs and revenues

Osborne Books Tutor Zone Analysing costs and revenues Practice assessment 1 Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e This assessment relates to

Osborne Books Tutor Zone Analysing costs and revenues Practice assessment 1 Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e This assessment relates to

Paper F5 ANSWERS TO EXAMPLES

September-December 2016 Examinations ACCA F5 87 Paper F5 ANSWERS TO EXAMPLES Chapter 1 ANSWER TO EXAMPLE 1 (a) Total overheads $190,000 Total labour hours A 20,000 2 = 40,000 B 25,000 1 = 25,000 C 2,000

September-December 2016 Examinations ACCA F5 87 Paper F5 ANSWERS TO EXAMPLES Chapter 1 ANSWER TO EXAMPLE 1 (a) Total overheads $190,000 Total labour hours A 20,000 2 = 40,000 B 25,000 1 = 25,000 C 2,000

MANAGEMENT ACCOUNTING

Series 4 Examination 2009 MANAGEMENT ACCOUNTING Level 3 Tuesday 1 December Subject Code: 3724 S Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry equal marks.

Series 4 Examination 2009 MANAGEMENT ACCOUNTING Level 3 Tuesday 1 December Subject Code: 3724 S Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry equal marks.

Management Accounting. Sample Paper 1 Questions and Suggested Solutions

Management Accounting Sample Paper 1 Questions and Suggested Solutions NOTES TO USERS ABOUT SAMPLE PAPERS Sample papers are published by Accounting Technicians Ireland. They are intended to provide guidance

Management Accounting Sample Paper 1 Questions and Suggested Solutions NOTES TO USERS ABOUT SAMPLE PAPERS Sample papers are published by Accounting Technicians Ireland. They are intended to provide guidance

MANAGEMENT ACCOUNTING Absorption & Marginal Costing

MANAGEMENT ACCOUNTING Absorption & Marginal Costing 1 Prepared by: Yaeesh Yasseen, Jade Jansen, Rashied Small & Lucinda Smidt Reviewed by: Achmad Joseph 2 Job & Process Costing Job costing: Applied when

MANAGEMENT ACCOUNTING Absorption & Marginal Costing 1 Prepared by: Yaeesh Yasseen, Jade Jansen, Rashied Small & Lucinda Smidt Reviewed by: Achmad Joseph 2 Job & Process Costing Job costing: Applied when

B.COM. Part-III (HONS.) Sub. : ADVANCE COST ACCOUNTING MODAL PAPER-I. Time Allowed: 3 Hour Max. Marks: 100

Sub. : ADVANCE COST ACCOUNTING MODAL PAPER-I. Time Allowed: 3 Hour Max. Marks: 100") B.COM. Part-III (HONS.) Sub. : ADVANCE COST ACCOUNTING MODAL PAPER-I Time Allowed: 3 Hour Max. Marks: 100 Q1 (i) (ii) (iii) (iv) (v) (vi) (vii) (viii) (ix) (x) Answers the following questions each having

B.COM. Part-III (HONS.) Sub. : ADVANCE COST ACCOUNTING MODAL PAPER-I Time Allowed: 3 Hour Max. Marks: 100 Q1 (i) (ii) (iii) (iv) (v) (vi) (vii) (viii) (ix) (x) Answers the following questions each having

THE PUBLIC ACCOUNTANTS EXAMINATION COUNCIL OF MALAWI 2011 EXAMINATIONS ACCOUNTING TECHNICIAN PROGRAMME PAPER TC9: COSTING AND BUDGETARY CONTROL

EXAMINATION NO. THE PUBLIC ACCOUNTANTS EXAMINATION COUNCIL OF MALAWI 2011 EXAMINATIONS ACCOUNTING TECHNICIAN PROGRAMME PAPER TC9: COSTING AND BUDGETARY CONTROL TUESDAY 7 JUNE 2011 TIME ALLOWED : 3 HOURS

EXAMINATION NO. THE PUBLIC ACCOUNTANTS EXAMINATION COUNCIL OF MALAWI 2011 EXAMINATIONS ACCOUNTING TECHNICIAN PROGRAMME PAPER TC9: COSTING AND BUDGETARY CONTROL TUESDAY 7 JUNE 2011 TIME ALLOWED : 3 HOURS

STANDARD COSTING. Samir K Mahajan

STANDARD COSTING Samir K Mahajan Standard Costing Historical costs: Historical costing or actual costing is a system where costs are ascertained after they are incurred. It is a post-mortem of the costs.

STANDARD COSTING Samir K Mahajan Standard Costing Historical costs: Historical costing or actual costing is a system where costs are ascertained after they are incurred. It is a post-mortem of the costs.

Write your answers in blue or black ink/ballpoint. Pencil may be used only for graphs, charts, diagrams, etc.

Series 3 Examination 2007 COST ACCOUNTING Level 3 Tuesday 5 June Subject Code: 3716 (S) Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Series 3 Examination 2007 COST ACCOUNTING Level 3 Tuesday 5 June Subject Code: 3716 (S) Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Please ensure your answers are written clearly, or marks may be lost. Do NOT open this paper until you are told to do so by the supervisor.

Cost Accounting ASE3017 Level 3 Tuesday 19 November 2013 Time allowed: 3 hours Information There are 5 questions in this examination. Total marks available: 100 All questions carry equal marks. Please

Cost Accounting ASE3017 Level 3 Tuesday 19 November 2013 Time allowed: 3 hours Information There are 5 questions in this examination. Total marks available: 100 All questions carry equal marks. Please

STANDARD COSTING. Samir K Mahajan

STANDARD COSTING Samir K Mahajan Standard Costing Historical costs: Historical costing or actual costing is a system where costs are ascertained after they are incurred. It is a post-mortem of the costs.

STANDARD COSTING Samir K Mahajan Standard Costing Historical costs: Historical costing or actual costing is a system where costs are ascertained after they are incurred. It is a post-mortem of the costs.

(b) Flexible Budget For The Year Ended 31 May 2003

Flexible Budget For The Year Ended 31 May 2003") Paper 2 Section A Question 1 Flexible budgets recognise the difference in cost behaviour (1) between fixed and variable costs in relation to fluctuations in output, (1) turnover, or other variable factors.

Paper 2 Section A Question 1 Flexible budgets recognise the difference in cost behaviour (1) between fixed and variable costs in relation to fluctuations in output, (1) turnover, or other variable factors.

Write your answers in blue or black ink/ballpoint. Pencil may be used only for graphs, charts, diagrams, etc.

Series 3 Examination 2008 COST ACCOUNTING Level 3 Friday 6 June Subject Code: 3016 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your answers

Series 3 Examination 2008 COST ACCOUNTING Level 3 Friday 6 June Subject Code: 3016 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your answers

ACCY 121 Chapter 16 Practice Quiz Fundamentals of Variance Analysis (1)

") ACCY 121 Chapter 16 Practice Quiz Fundamentals of Variance Analysis (1) 101. The Hageness Company has had great difficulty in controlling overhead costs. At a recent convention, the president heard about

ACCY 121 Chapter 16 Practice Quiz Fundamentals of Variance Analysis (1) 101. The Hageness Company has had great difficulty in controlling overhead costs. At a recent convention, the president heard about

SUGGESTED ANSWERS SPRING 2015 EXAMINATIONS 1 of 7 FUNDAMENTALS OF COST & MANAGEMENT ACCOUNTING SEMESTER-2

SUGGESTED ANSWERS SPRING 2015 EXAMINATIONS 1 of 7 Q. 2 (a) The Role of the Management Accountant: The management accountant plays a critical role in providing information to management to assist in planning,

SUGGESTED ANSWERS SPRING 2015 EXAMINATIONS 1 of 7 Q. 2 (a) The Role of the Management Accountant: The management accountant plays a critical role in providing information to management to assist in planning,

ICAN MID DIET LIVE CLASS FOR MAY DIET 2015 PERFORMANCE MANAGEMENT

ICAN MID DIET LIVE CLASS FOR MAY DIET 2015 PERFORMANCE MANAGEMENT PERFORMANCE MEASUREMENT NON- FINANCIAL MEASUREMENT PERFOMANCE MEASUREMENT OF A NON- PROFIT ORGANISATION DIVISIONAL PERFORMANCE MEASURE

ICAN MID DIET LIVE CLASS FOR MAY DIET 2015 PERFORMANCE MANAGEMENT PERFORMANCE MEASUREMENT NON- FINANCIAL MEASUREMENT PERFOMANCE MEASUREMENT OF A NON- PROFIT ORGANISATION DIVISIONAL PERFORMANCE MEASURE

ARTT Business School Ahmed Raza Mir

Question 1 C Plus I Plus V Plus Selling Price 263 242 237 Direct Material (100) (98) (97) Direct Labour (15) (13) (12) Var OH (23) (19) (16) Var Selling OH (12) (8) (10) Commission (13) (12) (12) CM 100

Question 1 C Plus I Plus V Plus Selling Price 263 242 237 Direct Material (100) (98) (97) Direct Labour (15) (13) (12) Var OH (23) (19) (16) Var Selling OH (12) (8) (10) Commission (13) (12) (12) CM 100

Analysing financial performance

NEW for 2015 Osborne Books Tutor Zone Analysing financial performance Exam preparation exercises I n t r o d u c t i o n These questions have been written as practice for selected numerical tasks from

NEW for 2015 Osborne Books Tutor Zone Analysing financial performance Exam preparation exercises I n t r o d u c t i o n These questions have been written as practice for selected numerical tasks from

B.Com II Cost Accounting

B.Com II Cost Accounting Chapter - 1 Cost Accounting: An Overview of Fundamental Aspects 2009 (1) Discuss the objectives of Cost Accounting. 2011 (1) Discuss importance of cost accounting. 2012 (1) What

B.Com II Cost Accounting Chapter - 1 Cost Accounting: An Overview of Fundamental Aspects 2009 (1) Discuss the objectives of Cost Accounting. 2011 (1) Discuss importance of cost accounting. 2012 (1) What

Session 05. Overhead Analysis Contd.

Session 05 Overhead Analysis Contd. Programme : Executive Diploma in Business & Accounting (EDBA 2014) Course : Cost Analysis in Business Lecturer : Mr. Asanka Ranasinghe BBA (Finance), ACMA, CGMA Contact

Session 05 Overhead Analysis Contd. Programme : Executive Diploma in Business & Accounting (EDBA 2014) Course : Cost Analysis in Business Lecturer : Mr. Asanka Ranasinghe BBA (Finance), ACMA, CGMA Contact

UNIVERSITY OF BOLTON OFF CAMPUS DIVISION THE UNIVERSITY OF BANKING - HCMC VIETNAM BA (HONS) ACCOUNTANCY SEMESTER 1 EXAMINATIONS 2015/16

ACCOUNTANCY SEMESTER 1 EXAMINATIONS 2015/16") OCD006 UNIVERSITY OF BOLTON OFF CAMPUS DIVISION THE UNIVERSITY OF BANKING - HCMC VIETNAM BA (HONS) ACCOUNTANCY SEMESTER 1 EXAMINATIONS 2015/16 STRATEGIC MANAGEMENT ACCOUNTANCY MODULE NO: ACC6005 Date:

OCD006 UNIVERSITY OF BOLTON OFF CAMPUS DIVISION THE UNIVERSITY OF BANKING - HCMC VIETNAM BA (HONS) ACCOUNTANCY SEMESTER 1 EXAMINATIONS 2015/16 STRATEGIC MANAGEMENT ACCOUNTANCY MODULE NO: ACC6005 Date:

4. Management time can be saved and attention directed to areas of most concern.

SOLUTION 1 (i) COST CONTROL This is usually carried out by the formal comparison of actual results with those planned eg budget, standard cost etc and investigating the variances for corrective measures.

SOLUTION 1 (i) COST CONTROL This is usually carried out by the formal comparison of actual results with those planned eg budget, standard cost etc and investigating the variances for corrective measures.

Cost Accounting. Level 3. Model Answers. Series (Code 3016) 1 ASE /2/06

1 ASE /2/06") Cost Accounting Level 3 Model Answers Series 2 2006 (Code 3016) 1 ASE 3016 2 06 1 3016/2/06 >f0t@w9w2`?[6zbkbwgc# Cost Accounting Level 3 Series 2 2006 How to use this booklet Model Answers have been developed

Cost Accounting Level 3 Model Answers Series 2 2006 (Code 3016) 1 ASE 3016 2 06 1 3016/2/06 >f0t@w9w2`?[6zbkbwgc# Cost Accounting Level 3 Series 2 2006 How to use this booklet Model Answers have been developed

LCCI International Qualifications. Cost Accounting Level 3. Model Answers Series (3017)

") LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 3 2009 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 3 2009 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

Analysing cost and revenues

Osborne Books Tutor Zone Analysing cost and revenues Chapter activities Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e 1 An introduction to cost accounting

Osborne Books Tutor Zone Analysing cost and revenues Chapter activities Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e 1 An introduction to cost accounting

Management Accounting. Sample Paper / 2017 Questions and Suggested Solutions

Management Accounting Sample Paper 1 2016 / 2017 Questions and Suggested Solutions NOTES TO USERS ABOUT SAMPLE PAPERS Sample papers are published by Accounting Technicians Ireland. They are intended to

Management Accounting Sample Paper 1 2016 / 2017 Questions and Suggested Solutions NOTES TO USERS ABOUT SAMPLE PAPERS Sample papers are published by Accounting Technicians Ireland. They are intended to

LCCI International Qualifications. Cost Accounting Level 3. Model Answers Series (3017)

") LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 2 2012 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 2 2012 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

2017 EXAMINATIONS ACCOUNTING TECHNICIAN PROGRAMME PAPER TC 9: COSTING & BUDGETARY CONTROL

EXAMINATION NO. 2017 EXAMINATIONS ACCOUNTING TECHNICIAN PROGRAMME PAPER TC 9: COSTING & BUDGETARY CONTROL THURSDAY 1 JUNE 2017 TIME ALLOWED: 3 HOURS 9.00 AM - 12.00 NOON INSTRUCTIONS 1. You are allowed

EXAMINATION NO. 2017 EXAMINATIONS ACCOUNTING TECHNICIAN PROGRAMME PAPER TC 9: COSTING & BUDGETARY CONTROL THURSDAY 1 JUNE 2017 TIME ALLOWED: 3 HOURS 9.00 AM - 12.00 NOON INSTRUCTIONS 1. You are allowed

MGT402 Cost & Management Accounting. Composed By Faheem Saqib MIDTERM EXAMINATION. Spring MGT402- Cost & Management Accounting (Session - 1)

") MGT402 Cost & Management Accounting Composed By Faheem Saqib 14 Midterm Papers 3 of 2010 & 11 of 2009 For more Help Rep At Faheem_saqib2003@yahoo.com Faheem.saqib2003@gmail.com 0334-6034849 MIDTERM EXAMINATION

MGT402 Cost & Management Accounting Composed By Faheem Saqib 14 Midterm Papers 3 of 2010 & 11 of 2009 For more Help Rep At Faheem_saqib2003@yahoo.com Faheem.saqib2003@gmail.com 0334-6034849 MIDTERM EXAMINATION

Analyzing Financial Performance Reports

Analyzing Financial Performance Reports Calculating Variances Effective systems identify variances down to the lowest level of management. Variances are hierarchical. As shown in Exhibit 10.2, they begin

Analyzing Financial Performance Reports Calculating Variances Effective systems identify variances down to the lowest level of management. Variances are hierarchical. As shown in Exhibit 10.2, they begin

Standard Cost. Types of Standards

Standard Cost A standard cost is the predetermined cost of manufacturing a single unit or a number of product units during a specific period in the immediate future. It is the planned cost of a product

Standard Cost A standard cost is the predetermined cost of manufacturing a single unit or a number of product units during a specific period in the immediate future. It is the planned cost of a product

Institute of Certified Management Accountants of Sri Lanka

Copyright Reserved Serial No Foundation Level Pilot Paper Instructions to Candidates 1. Time allowed is two (2) hours. 2. Total 100 Marks. 3. Answer all questions. 4. Encircle the number of your choice

Copyright Reserved Serial No Foundation Level Pilot Paper Instructions to Candidates 1. Time allowed is two (2) hours. 2. Total 100 Marks. 3. Answer all questions. 4. Encircle the number of your choice

Chapter 11. Standard costs for control: flexible budgets and. manufacturing overhead

Chapter 11 Standard costs for control: flexible budgets and manufacturing overhead Copyright 2003 McGraw-Hill Australia Pty Ltd, PPTs t/a Management Accounting: An Australian Perspective 3/e by Langfield-Smith,

Chapter 11 Standard costs for control: flexible budgets and manufacturing overhead Copyright 2003 McGraw-Hill Australia Pty Ltd, PPTs t/a Management Accounting: An Australian Perspective 3/e by Langfield-Smith,

Analysing cost and revenues

Osborne Books Tutor Zone Analysing cost and revenues Chapter activities answers Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e 1 An introduction to cost

Osborne Books Tutor Zone Analysing cost and revenues Chapter activities answers Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e 1 An introduction to cost

Chapter 10 Process Costing Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Chapter 10 Process Costing Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) The Basic of Process Costing Process costing is a costing method used where it is not

Chapter 10 Process Costing Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) The Basic of Process Costing Process costing is a costing method used where it is not

Institute of Certified Bookkeepers

Institute of Certified Bookkeepers Level III Diploma in Costing and Budgeting Introduction: Financial Accounting is the reporting of financial information to users of Financial Statements both internal

Institute of Certified Bookkeepers Level III Diploma in Costing and Budgeting Introduction: Financial Accounting is the reporting of financial information to users of Financial Statements both internal

Intermediate Management Accounting

Intermediate Management Accounting Course map This document outlines the course structure. Course orientation Lesson 1: Welcome Lesson 2: Getting your diploma Lesson 3: How do I study this course? Unit

Intermediate Management Accounting Course map This document outlines the course structure. Course orientation Lesson 1: Welcome Lesson 2: Getting your diploma Lesson 3: How do I study this course? Unit

Answer FOUR questions: THREE from Section A and ONE from Section B

UNIVERSITY OF EAST ANGLIA Norwich Business School Main Series UG Examination 2016-17 MANAGEMENT ACCOUNTING NBS-5007Y Time allowed: 3 hours Answer FOUR questions: THREE from Section A and ONE from Section

UNIVERSITY OF EAST ANGLIA Norwich Business School Main Series UG Examination 2016-17 MANAGEMENT ACCOUNTING NBS-5007Y Time allowed: 3 hours Answer FOUR questions: THREE from Section A and ONE from Section

MTP_Intermediate_Syllabus 2008_Jun2015_Set 2

Paper 8: Cost & Management Accounting Time Allowed: 3 Hours Full Marks: 100 Question No 1 is Compulsory. Answers any five Questions from the rest. Working Notes should form part of the answer. Question.1

Paper 8: Cost & Management Accounting Time Allowed: 3 Hours Full Marks: 100 Question No 1 is Compulsory. Answers any five Questions from the rest. Working Notes should form part of the answer. Question.1

General Certificate of Education Advanced Level Examination June 2010

General Certificate of Education Advanced Level Examination June 2010 Accounting ACCN4 Unit 4 Further Aspects of Management Accounting Thursday 24 June 2010 1.30 pm to 3.30 pm For this paper you must have:

General Certificate of Education Advanced Level Examination June 2010 Accounting ACCN4 Unit 4 Further Aspects of Management Accounting Thursday 24 June 2010 1.30 pm to 3.30 pm For this paper you must have:

Final Examination Semester 2 / Year 2011

Southern College Kolej Selatan 南方学院 Final Examination Semester 2 / Year 2011 COURSE : BASIC COSTING COURSE CODE : ACCT2013 TIME : 2 1/2 HOURS DEPARTMENT : FINANCE AND ACCOUNTING LECTURER : GAN HWI SIN

Southern College Kolej Selatan 南方学院 Final Examination Semester 2 / Year 2011 COURSE : BASIC COSTING COURSE CODE : ACCT2013 TIME : 2 1/2 HOURS DEPARTMENT : FINANCE AND ACCOUNTING LECTURER : GAN HWI SIN

BUSINESS AND MANAGEMENT ACCOUNTING AND FINANCE

BUSINESS AND MANAGEMENT ACCOUNTING AND FINANCE Unit 3.4 Budgeting (Higher Level) Content and Learning Outcomes Content! Types and purpose of budgets! Cash Flow Forecasts! Variance Analysis Learning Outcomes!

BUSINESS AND MANAGEMENT ACCOUNTING AND FINANCE Unit 3.4 Budgeting (Higher Level) Content and Learning Outcomes Content! Types and purpose of budgets! Cash Flow Forecasts! Variance Analysis Learning Outcomes!

7 Solved Mid Term Papers of MGT402 BY.

7 Solved Mid Term Papers of MGT402 BY http://vustudents.ning.com Spring 2009 MGT402- Cost & Management Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process

7 Solved Mid Term Papers of MGT402 BY http://vustudents.ning.com Spring 2009 MGT402- Cost & Management Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process

Required: Calculate the quantity of units completed and transfer-out

Asslam O Alikum MGT 402 SUBJECTIVE FILE SOLVED BY AFAAQ Remember Me In Your Prayers Best regard s Muhammad Afaaq Mba 3 rd Finance Group Afaaq_Tariq@yahoo.com Islamabad 0346-5329264 If u like me than raise

Asslam O Alikum MGT 402 SUBJECTIVE FILE SOLVED BY AFAAQ Remember Me In Your Prayers Best regard s Muhammad Afaaq Mba 3 rd Finance Group Afaaq_Tariq@yahoo.com Islamabad 0346-5329264 If u like me than raise

b) To answer any questing dealing with variances work out the rates and the cost per unit i.e. work out the standard cost per unit.

To answer any questing dealing with variances work out the rates and the cost per unit i.e. work out the standard cost per unit.") QUESTION ONE a) Basic Standards These are standards which are kept unaltered over a long period of time and may be out of date. These are used to show changes in efficiency or performance over a long period

QUESTION ONE a) Basic Standards These are standards which are kept unaltered over a long period of time and may be out of date. These are used to show changes in efficiency or performance over a long period

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47

Time: 60 min Marks: 47") MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

Ordering costs Any two of the following: Postage, Paperwork, Telephone, Internet, , Purchasing Officer's salary

EDUCATION DEVELOPMENT INTERNATIONAL PLC SAMPLE PAPER ANSWERS 2008 COST ACCOUNTING (ASE3017) LEVEL 3 QUESTION 1 (a) (i) Stock holding costs Any two of the following: Insurance, Material handling, Storekeeper's

EDUCATION DEVELOPMENT INTERNATIONAL PLC SAMPLE PAPER ANSWERS 2008 COST ACCOUNTING (ASE3017) LEVEL 3 QUESTION 1 (a) (i) Stock holding costs Any two of the following: Insurance, Material handling, Storekeeper's

MANAGEMENT ACCOUNTING 2. Module Code: ACCT08004

School of Business & Enterprise Paisley & Hamilton Campus Session 015-016 Trimester 1 MANAGEMENT ACCOUNTING Module Code: ACCT08004 Date: 1st January 016 Time: 1400-1600 Answer THREE questions Question

School of Business & Enterprise Paisley & Hamilton Campus Session 015-016 Trimester 1 MANAGEMENT ACCOUNTING Module Code: ACCT08004 Date: 1st January 016 Time: 1400-1600 Answer THREE questions Question

LCCI International Qualifications. Cost Accounting Level 3. Model Answers Series (3017)

") LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 3 2010 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 3 2010 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

Paper T7. Planning, Control and Performance Management. Tuesday 8 December Certified Accounting Technician Examination Advanced Level

Certified Accounting Technician Examination Advanced Level Planning, Control and Performance Management Tuesday 8 December 2009 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper

Certified Accounting Technician Examination Advanced Level Planning, Control and Performance Management Tuesday 8 December 2009 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper

a) It is important to note that Famba will only receive the commission on the ticket price of R (2000 x 12.5% commission = R250)

It is important to note that Famba will only receive the commission on the ticket price of R (2000 x 12.5% commission = R250)") QUESTION 1: a) It is important to note that Famba will only receive the commission on the ticket price of R2 000. (2000 x 12.5% commission = R250) Breakeven (units) = Fixed cost Marginal income (MI) =

QUESTION 1: a) It is important to note that Famba will only receive the commission on the ticket price of R2 000. (2000 x 12.5% commission = R250) Breakeven (units) = Fixed cost Marginal income (MI) =

Paper P1 Management Accounting Performance Evaluation Post Exam Guide November 2008 Exam. General Comments

General Comments The overall result on this paper was reasonable and, while performance was well below the level seen in May 2008, there was a small improvement on the previous November sitting. gained

General Comments The overall result on this paper was reasonable and, while performance was well below the level seen in May 2008, there was a small improvement on the previous November sitting. gained

B.COM II ADVANCED AND COST ACCOUNTING

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

TRADITIONAL ABSORPTION V ACTIVITY BASED COSTING

TRADITIONAL ABSORPTION V ACTIVITY BASED COSTING A company manufactures two products: X and Y. Information is available as follows: (a) Product Total production Labour time per unit X 1,000 0.5 hours Y

TRADITIONAL ABSORPTION V ACTIVITY BASED COSTING A company manufactures two products: X and Y. Information is available as follows: (a) Product Total production Labour time per unit X 1,000 0.5 hours Y

MOCK EXAMINATION PRINCIPLES OF ACCOUNTS A-LEVEL PAPER 2

HONG KONG ASSOCIATION FOR BUSINESS EDUCATION HONG KONG INSTITUTE OF VOCATIONAL EDUCATION (CHAI WAN & TUEN MUN) HONG KONG ADVANCED LEVEL EXAMINATION 2009 MOCK EXAMINATION PRINCIPLES OF ACCOUNTS A-LEVEL

HONG KONG ASSOCIATION FOR BUSINESS EDUCATION HONG KONG INSTITUTE OF VOCATIONAL EDUCATION (CHAI WAN & TUEN MUN) HONG KONG ADVANCED LEVEL EXAMINATION 2009 MOCK EXAMINATION PRINCIPLES OF ACCOUNTS A-LEVEL

(50 Marks) Stores Control Account (1 mark) To Balance b/d 32,000 By W.I.P. Control A/c 1,60,000 To General ledger adjustment

Stores Control Account (1 mark) To Balance b/d 32,000 By W.I.P. Control A/c 1,60,000 To General ledger adjustment") IPCC November 2017 COSTING Test Code 80101 Branch (MULTIPLE) (Date : 17.0.2017) (50 Marks) Note: All questions are compulsory. Question 1 (8 marks) (A) Costing books Stores Control Account (1 mark) To

IPCC November 2017 COSTING Test Code 80101 Branch (MULTIPLE) (Date : 17.0.2017) (50 Marks) Note: All questions are compulsory. Question 1 (8 marks) (A) Costing books Stores Control Account (1 mark) To

5_MGT402_Spring_2010_Final_Term_Solved_paper

5_MGT402_Spring_2010_Final_Term_Solved_paper http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one BDH produced 30,500 units of Kisty (a product). Each unit of Kisty takes two units

5_MGT402_Spring_2010_Final_Term_Solved_paper http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one BDH produced 30,500 units of Kisty (a product). Each unit of Kisty takes two units

(59) MANAGEMENT ACCOUNTING & BUSINESS FINANCE

MANAGEMENT ACCOUNTING & BUSINESS FINANCE") All Rights Reserved THE ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA FINAL EXAMINATION JULY 2013 (59) MANAGEMENT ACCOUNTING & BUSINESS FINANCE Time: 03 hours Instructions to candidates: (1) This

All Rights Reserved THE ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA FINAL EXAMINATION JULY 2013 (59) MANAGEMENT ACCOUNTING & BUSINESS FINANCE Time: 03 hours Instructions to candidates: (1) This

Lecture 16 Flexible Budgets and Variance Analysis

Economics, Management and Entrepreneurship Prof. Pratap K. J. Mohapatra Department of Industrial Engineering & Management Indian Institute of Technology - Kharagpur Lecture 16 Flexible Budgets and Variance

Economics, Management and Entrepreneurship Prof. Pratap K. J. Mohapatra Department of Industrial Engineering & Management Indian Institute of Technology - Kharagpur Lecture 16 Flexible Budgets and Variance

Mock One. Performance Management F5PM-MK1-Z16-A. Answers & Marking Scheme. Becker Study School DeVry/Becker Educational Development Corp.

Mock One Performance Management F5PM-MK-Z6-A Answers & Marking Scheme 206 DeVry/Becker Educational Development Corp. Question Answer Mark Question Answer Mark Section A Section B D 6 A 2 C 7 A 3 C 8 A

Mock One Performance Management F5PM-MK-Z6-A Answers & Marking Scheme 206 DeVry/Becker Educational Development Corp. Question Answer Mark Question Answer Mark Section A Section B D 6 A 2 C 7 A 3 C 8 A

6 Non-integrated, Integrated & Reconciliation of Cost and Financial Accounts

5.43 Activity Based Costing 6 Non-integrated, Integrated & Reconciliation of Cost and Financial Accounts Question 1 Write short note on Cost Ledger Control Account (May, 1996, 4 marks) Answer Cost Ledger

5.43 Activity Based Costing 6 Non-integrated, Integrated & Reconciliation of Cost and Financial Accounts Question 1 Write short note on Cost Ledger Control Account (May, 1996, 4 marks) Answer Cost Ledger

Free of Cost ISBN : Appendix. CMA (CWA) Inter Gr. II (Solution upto Dec & Questions of June 2013 included)

Inter Gr. II (Solution upto Dec & Questions of June 2013 included)") Free of Cost ISBN : 978-93-5034-631-0 Appendix CMA (CWA) Inter Gr. II (Solution upto Dec. 2012 & Questions of June 2013 included) Paper - 8 : Cost and Management Accounting Chapter - 3 : Labour Accounting

Free of Cost ISBN : 978-93-5034-631-0 Appendix CMA (CWA) Inter Gr. II (Solution upto Dec. 2012 & Questions of June 2013 included) Paper - 8 : Cost and Management Accounting Chapter - 3 : Labour Accounting

Examinations for Academic Year Semester I / Academic Year 2015 Semester II. 1. This question paper consists of Section A and Section B.

PROGRAMME COHORT BSc (Hons) Human Resource Management BSc (Hons) Management BHRM/14B/FT BMAN/15A/FT B1, B2 Examinations for Academic Year 2015 2016 Semester I / Academic Year 2015 Semester II MODULE: COST

PROGRAMME COHORT BSc (Hons) Human Resource Management BSc (Hons) Management BHRM/14B/FT BMAN/15A/FT B1, B2 Examinations for Academic Year 2015 2016 Semester I / Academic Year 2015 Semester II MODULE: COST

You were introduced to Standard Costing in the earlier stages of your studies in which you understood the following;

6 Standard Costing LEARNING OBJECTIVES : After studying this unit you will be able to : Understand terms as standard Cost, standard Costing, standard Hour Understand how a standard costing system operates

6 Standard Costing LEARNING OBJECTIVES : After studying this unit you will be able to : Understand terms as standard Cost, standard Costing, standard Hour Understand how a standard costing system operates

Write your answers in blue or black ink/ballpoint. Pencil may be used only for graphs, charts, diagrams, etc.

Series 4 Examination 2008 COST ACCOUNTING Level 3 Tuesday 11 November Subject Code: 3016 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Series 4 Examination 2008 COST ACCOUNTING Level 3 Tuesday 11 November Subject Code: 3016 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

P1 Performance Operations September 2014 examination

Operational Level Paper P1 Performance Operations September 2014 examination Examiner s Answers Note: Some of the answers that follow are fuller and more comprehensive than would be expected from a well-prepared

Operational Level Paper P1 Performance Operations September 2014 examination Examiner s Answers Note: Some of the answers that follow are fuller and more comprehensive than would be expected from a well-prepared

Study the REQUIRED section of each question carefully and extract the data required for your answers from the information supplied.

Series 4 Examination 2010 COST ACCOUNTING Level 3 Monday 6 December Subject Code: 3717/S Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry equal marks. Study

Series 4 Examination 2010 COST ACCOUNTING Level 3 Monday 6 December Subject Code: 3717/S Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry equal marks. Study

Cost Accounting. Level 3. Model Answers. Series (Code 3016) 1 ASE /2/06

1 ASE /2/06") Cost Accounting Level 3 Model Answers Series 3 2007 (Code 3016) 1 ASE 3016 2 06 1 3016/2/06 >f0t@w9w2`?[6zbkbwgc# Cost Accounting Level 3 Series 3 2007 How to use this booklet Model Answers have been developed

Cost Accounting Level 3 Model Answers Series 3 2007 (Code 3016) 1 ASE 3016 2 06 1 3016/2/06 >f0t@w9w2`?[6zbkbwgc# Cost Accounting Level 3 Series 3 2007 How to use this booklet Model Answers have been developed

Standard Costing and Variance Analysis

Standard Costing and Variance Analysis Standard Costing Standard cost is predetermined cost agreed earlier under specific working conditions. Standard costing is a technique which establishes predetermined

Standard Costing and Variance Analysis Standard Costing Standard cost is predetermined cost agreed earlier under specific working conditions. Standard costing is a technique which establishes predetermined

Disclaimer: This resource package is for studying purposes only EDUCATIO N

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 9: Budgeting The Basic Framework of Budgeting Master budget - a summary of a company s plans in which specific targets

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 9: Budgeting The Basic Framework of Budgeting Master budget - a summary of a company s plans in which specific targets

Monday 14 June 2004 (morning) EXAMINATION. Time allowed - 3 hours plus 15 minutes reading time

EXAMINATION. Time allowed - 3 hours plus 15 minutes reading time") NVQ/SVQ Level 4 in Accounting Contributing to the Management of Performance and the Enhancement of Value (PEV) (2003 standards) / Management of Costs and the Enhancement of Value (MCV) (1998 standards)

NVQ/SVQ Level 4 in Accounting Contributing to the Management of Performance and the Enhancement of Value (PEV) (2003 standards) / Management of Costs and the Enhancement of Value (MCV) (1998 standards)

Bsc (Hons) Tourism and Hospitality Management. Cohort: BTHM/16A/FT. Examinations for 2016/2017 Semester I. & 2016 Semester II

Tourism and Hospitality Management. Cohort: BTHM/16A/FT. Examinations for 2016/2017 Semester I. & 2016 Semester II") Bsc (Hons) Tourism and Hospitality Management Cohort: BTHM/16A/FT Examinations for 2016/2017 Semester I & 2016 Semester II MODULE: COST AND MANAGEMENT ACCOUNTING MODULE CODE: ACCF 1104A Duration: 2 Hours

Bsc (Hons) Tourism and Hospitality Management Cohort: BTHM/16A/FT Examinations for 2016/2017 Semester I & 2016 Semester II MODULE: COST AND MANAGEMENT ACCOUNTING MODULE CODE: ACCF 1104A Duration: 2 Hours

Accounting Technicians Ireland 2 nd Year Examination: Autumn 2013 Paper: MANAGEMENT ACCOUNTING

Accounting Technicians Ireland 2 nd Year Examination: Autumn 2013 Paper: MANAGEMENT ACCOUNTING Monday 26 th August 2013-2.30 p.m. to 5.30 p.m. INSTRUCTIONS TO CANDIDATES In this examination paper the /

Accounting Technicians Ireland 2 nd Year Examination: Autumn 2013 Paper: MANAGEMENT ACCOUNTING Monday 26 th August 2013-2.30 p.m. to 5.30 p.m. INSTRUCTIONS TO CANDIDATES In this examination paper the /

Management Accounting

Management Accounting Course map This document outlines the course structure. ACCA: FMA-F2.x Management Accounting Introduction course orientation Lesson 1: Welcome Lesson 2: What, when and why? Lesson

Management Accounting Course map This document outlines the course structure. ACCA: FMA-F2.x Management Accounting Introduction course orientation Lesson 1: Welcome Lesson 2: What, when and why? Lesson

Analysing financial performance

Osborne Books Tutor Zone Analysing financial performance Practice assessment 1 Osborne Books Limited, 2013 2 a n a l y s i n g f i n a n c i a l p e r f o r m a n c e t u t o r z o n e Task 1 The following

Osborne Books Tutor Zone Analysing financial performance Practice assessment 1 Osborne Books Limited, 2013 2 a n a l y s i n g f i n a n c i a l p e r f o r m a n c e t u t o r z o n e Task 1 The following

MOCK TEST PAPER 1 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING

: GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING") MOCK TEST PAPER 1 INTERMEDIATE (IPC): GROUP I Test Series: February, 2014 PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING Question No. 1 is compulsory. Attempt any five questions

MOCK TEST PAPER 1 INTERMEDIATE (IPC): GROUP I Test Series: February, 2014 PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING Question No. 1 is compulsory. Attempt any five questions

AAT (Diploma in Accounting) Level 4. Budgeting

Level 4. Budgeting") AAT (Diploma in Accounting) Level 4 Budgeting Topic The Budgeting Environment Sources of data When preparing for budget exercise, accounting technicians must identify the internal and external source of

AAT (Diploma in Accounting) Level 4 Budgeting Topic The Budgeting Environment Sources of data When preparing for budget exercise, accounting technicians must identify the internal and external source of

ACCA F2 FLASH NOTES. Describe a pie chart?

ACCA F2 FLASH NOTES Describe a pie chart? A pie chart is a circle that is divided into segments representing each type of observation. The size of each segment is proportional to the proportion of the

ACCA F2 FLASH NOTES Describe a pie chart? A pie chart is a circle that is divided into segments representing each type of observation. The size of each segment is proportional to the proportion of the

BALIUAG UNIVERSITY CPA REVIEW MANAGEMENT ADVISORY SERVICES STANDARD COST AND VARIANCE ANALYSIS THEORY

STANDARD COST AND VARIANCE ANALYSIS THEORY 1. How is labor rate variance computed? a. The difference between standard and actual rate multiplied by actual hours b. The difference between standard and actual

STANDARD COST AND VARIANCE ANALYSIS THEORY 1. How is labor rate variance computed? a. The difference between standard and actual rate multiplied by actual hours b. The difference between standard and actual

SUGGESTED SOLUTIONS. KE2 Management Accounting Information. March All Rights Reserved

SUGGESTED SOLUTIONS KE2 Management Accounting Information March 2015 All Rights Reserved SECTION 1 Answer 01 1(a) 1.1 Relevant Learning Outcome/s: 1.1.2 Correct answer: C Direct cost can either be variable

SUGGESTED SOLUTIONS KE2 Management Accounting Information March 2015 All Rights Reserved SECTION 1 Answer 01 1(a) 1.1 Relevant Learning Outcome/s: 1.1.2 Correct answer: C Direct cost can either be variable

Management Accounting

Management Accounting Course map This document outlines the course structure. Duration 10 weeks ACCA: FMA-F2.x Management Accounting Course orientation Start of course survey Lesson 1: Welcome Lesson 2:

Management Accounting Course map This document outlines the course structure. Duration 10 weeks ACCA: FMA-F2.x Management Accounting Course orientation Start of course survey Lesson 1: Welcome Lesson 2:

F2 - Management Accounting ACCA 117 FAQ Theory Questions

F2 - Management Accounting ACCA 117 FAQ Theory Questions 1 1. Define the labour idle time ratio? Idle time ratio = idle hours / total hours x 100% 2. What is the definition of the Internal Rate of Return

F2 - Management Accounting ACCA 117 FAQ Theory Questions 1 1. Define the labour idle time ratio? Idle time ratio = idle hours / total hours x 100% 2. What is the definition of the Internal Rate of Return

ACG 3024 Accounting for Non-Financial Majors Homework Portfolio (This is an individual assignment)

") ACG 3024 Accounting for Non-Financial Majors Homework Portfolio (This is an individual assignment) Make sure you complete the homework portfolio version assigned to you from your sign-in on the Florida

ACG 3024 Accounting for Non-Financial Majors Homework Portfolio (This is an individual assignment) Make sure you complete the homework portfolio version assigned to you from your sign-in on the Florida

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS 1. (i) ABC Ltd. had an opening inventory value of 1760 (550 units valued at 3.20 each) on 1 st April 2010. The following

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS 1. (i) ABC Ltd. had an opening inventory value of 1760 (550 units valued at 3.20 each) on 1 st April 2010. The following

9706 Accounting November 2008

Paper 9706/01 Multiple Choice 1 A 16 B 2 B 17 A 3 B 18 B 4 B 19 C 5 B 20 B 6 D 21 C 7 A 22 B 8 B 23 D 9 D 24 C 10 B 25 B 11 A 26 B 12 A 27 B 13 D 28 A 14 D 29 D 15 B 30 D General comments Many of the 7300

Paper 9706/01 Multiple Choice 1 A 16 B 2 B 17 A 3 B 18 B 4 B 19 C 5 B 20 B 6 D 21 C 7 A 22 B 8 B 23 D 9 D 24 C 10 B 25 B 11 A 26 B 12 A 27 B 13 D 28 A 14 D 29 D 15 B 30 D General comments Many of the 7300

F2 PRACTICE EXAM QUESTIONS

F2 PRACTICE EXAM QUESTIONS SECTION A 1. The following details are available for a company: Budgeted Actual Expenditure $176,400 $250,400 Machine hours 4,000 5,000 Labor hours 3,600 5,400 If the company

F2 PRACTICE EXAM QUESTIONS SECTION A 1. The following details are available for a company: Budgeted Actual Expenditure $176,400 $250,400 Machine hours 4,000 5,000 Labor hours 3,600 5,400 If the company

Part 1 Examination Paper 1.2. Section A 10 C 11 C 2 A 13 C 1 B 15 C 6 C 17 B 18 C 9 D 20 C 21 C 22 D 23 D 24 C 25 C

Answers Part 1 Examination Paper 1.2 Financial Information for Management June 2007 Answers Section A 1 B 2 A 3 A 4 A 5 D 6 C 7 B 8 C 9 D 10 C 11 C 12 A 13 C 14 B 15 C 16 C 17 B 18 C 19 D 20 C 21 C 22

Answers Part 1 Examination Paper 1.2 Financial Information for Management June 2007 Answers Section A 1 B 2 A 3 A 4 A 5 D 6 C 7 B 8 C 9 D 10 C 11 C 12 A 13 C 14 B 15 C 16 C 17 B 18 C 19 D 20 C 21 C 22

Analysing financial performance

Osborne Books Tutor Zone Analysing financial performance Chapter activities Osborne Books Limited, 2013 2 a n a l y s i n g f i n a n c i a l p e r f o r m a n c e t u t o r z o n e 1 Management accounting

Osborne Books Tutor Zone Analysing financial performance Chapter activities Osborne Books Limited, 2013 2 a n a l y s i n g f i n a n c i a l p e r f o r m a n c e t u t o r z o n e 1 Management accounting