For September 2017 Payout

|

|

|

- Alyson Woods

- 5 years ago

- Views:

Transcription

1 finmagm Abstract For September 2017 Payout

2 CARE has rated more than 335 Asset Backed Securitisation (ABS) / Mortgage Backed Securitisation (MBS) pools across 42 s and pools aggregating to around Rs. 64,000 crore covering various asset classes, which include - Auto Loans, Commercial Vehicle loans, Construction Equipment loans, Two Wheeler loans, Personal Loans, Microfinance loans and Mortgage Loans. This report analyses the performance of all rated transactions live as on recent date. It covers the characteristics of pools at the time of origination and their key performance indicators. Key performance indicators include 90+ DPD levels, 180+ DPD levels, Cumulative Collection Efficiency Ratio, Prepayments etc. CARE also calculates the Break-even ratio to determine the minimum collection efficiency required on pools future cash flow to be able to serve the payouts on time. It also covers the Credit Enhancement Utilization and Coverage at 90+ DPD levels & 180+ DPD levels. Detailed performance report and interpretation of each term are briefed in the later sections. All the securitisation pools rated by CARE have either maintained the initial rating assigned to them or have been upgraded. All the pools so far continue to be comfortably placed in terms of low utilization of credit enhancements. Break-even and Enhancement coverage for all the rated pool shows that they are comfortably placed. 1

3 Contents S.No Index Page No I Terminologies 3 II Acronym 6 III -Wise Pools Performance Asirvad Microfinance Private Limited 12 Aptus Value Housing Finance Limited 18 Arohan Financial Services Private Ltd. 21 Annapurna Microfinance Private Limited 23 Bharat Financial Inclusion Ltd 28 Cholamandalam Investment Finance Company Ltd. 35 Dewan Housing Finance Limited 37 Equitas Small Finance Bank Limited 51 ESAF Microfinance 54 HDFC Limited 64 Hinduja Leyland Finance Limited 74 Indiabulls Housing Finance Company Ltd. 77 IKF Finance Limited 91 India Shelter Finance Corporation Ltd. 99 Light Microfinance 101 Magma Fincorp Limited 103 Magma ITL Finance Ltd 106 Shriram City Union Finance Limited 108 Shriram Transport Finance Company Limited 110 Suryodaya Micro Finance Ltd. 114 S V Creditline Pvt Ltd. 116 Varam Capital Pvt Ltd. 118 Visage Holdings and Finance Private Limited 120 2

4 Terminologies Commencement Month: Date from which pool receivables have been transferred. : Whether the pool receivables were transferred at their par value or at a premium. If there is some new structure, then it is suitably mentioned. Pool Principal: The pool principal outstanding at the time of securitisation. Future Payout: Total obligation towards PTC holders or the acquirer at the time of securitisation. Future Receivables: Total cash flows arising from the assigned pool. : The total number of contracts in a pool. Average Maturity: It is calculated as weighted average maturity of all future cash flow. Average Seasoning: Weighted average seasoning of the pool as on cut off date. : Principal outstanding of all those loans in a pool which are in overdue category. It is expressed as % of initial pool principal outstanding. It is presented sequentially as current, one month overdue and two months overdue. For example, if the Pool has 98% current contracts, 1% one month overdue and 1% two month overdue. The will appear as 98%, 1%, 1%. Cash Collateral: Cash Collateral (CC) is the total amount of credit protection available in the form of cash or corporate undertaking divided by the pool receivables (in the case of premium transactions) or pool principal (in the case of par transactions). Cash collateral is further divided into first loss and second loss (wherever applicable). Liquidity Facility: This facility is used for meeting temporary shortfall in the collection. This facility can be used only for the overdue pertaining to all the contracts which are due for 90 days or less (less than 90 dpd). Excess Interest Spread: It is difference between scheduled interest cash flow from underlying obligors and schedule interest payout to investor / acquirer. It is calculated as a % of initial principal outstanding. (No. of Month * Monthly Pool Cash Flow) Sum of Pool Cash Flow Pool Interest Cash Flow Investor Interest Payout Initial Principal Outstanding Pool Maturity: Last payout date to the investor or the date on which last payment to the investor is to be made. Months Post Securitisation: Months elapsed after the securitisation. Balance Tenure: Number of months for which investor / acquirer payout is outstanding in the transaction. Amortisation: Amount of pool got amortised as a percentage of original assigned pool. 3

5 30+/ 90+/ 180+ (% of Initial POS / FP): It is a ratio of sum of pool principal outstanding (POS) or future receivables (FR) of all those contracts which are more than 30/90/180 days past dues (dpd) and overdue amount pertaining to those contracts and loss from repossessed assets (wherever available) to the initial POS / future payouts (FP). Future POS / FR (30+/ 90+/ 180+dpd) + Amount (30+/ 90+/ 180+dpd) + Repo Loss Initial POS / FP 30+/ 90+/ 180+ (% of Balance POS / FP): It is a ratio of future POS / FR of all those contracts which are more than 30/90/180dpd to the balance pool POS / FP. Future POS / FR (30+/ 90+/ 180+dpd) Balance POS/ FP as a % of Initial POS / FP: It is a ratio of overdue amount of all the contracts overdue as on date to initial POS / FP. Amount Initial POS / FP Cash Collateral as % of Balance POS: It is ratio of outstanding cash collateral as on date as a % of principal outstanding as on date. Outstandingcash collateral Balance POS Liquidity Facility as % of Balance POS: It is ratio of outstanding liquidity facility as on date as a % of principal outstanding as on date. Outstandingliquidity facility Balance POS Balance cash collateral: Outstanding cash collateral as a % of initial cash collateral. Outstanding Cash Collateral Initial cash collateral Break Even : Minimum collection efficiency required from future billings (excluding overdues) to serve the investors. Future Payouts Available cash collateral Future Billing Break Even (First Loss Facility): Minimum collection efficiency required from future billings (excluding overdues) to serve the investor keeping second loss facility unutilised at the end of the transaction. Future Payouts Available first loss facility (cash collateral) Future Billing 4

6 Overall Credit Enhancement coverage at 30+/ 90+/ 180+dpd: This ratio explains the credit enhancement coverage available to the future receivables of above 30/90/180dpd contracts. 1- Break even collection efficiency 30+/ 90+/ 180+dpd (% of Balance POS) First Loss Enhancement coverage at 90+/ 180+dpd: This ratio explains the first loss enhancement coverage available to the future receivables of above 90/180dpd contracts. 1- Break even collection efficiency (First Loss Facility) 90+/180+dpd (% of Balance POS) Cumulative Prepayment: This ratio explains the cumulative prepayment in the pool. Cumulative Prepayment Initial POS / FP Cumulative (): This ratio explains the cumulative collection in the pool. Cumulative Collection till date (exclusive of prepayments) Cumulative Monthly Billing Monthly (): This ratio explains the monthly collection in the pool. Total Monthly Collections (exclusive of prepayments) Monthly Billing Fortnightly (FCE): This ratio explains the fortnightly collection in the pool. Total Fortnightly Collections (exclusive of prepayments) Fortnightly Billing 5

7 Acronym ABS Amt AP CC DPD EIS FLF FL FP FR LF MBS FCE OC PTC POS SLF Asset Backed Securities Amount Assignee Payout Break-even Cash Collateral/ Credit Collateral Cumulative Days Past Due Excess Interest Spread First Loss Facility First Loss Future Payouts Future Receivables Liquidity Facility Mortgage Backed Securities Monthly Fortnightly Over Collateralization Pass through Certificate Principal Outstanding Second Loss Facility Not Applicable 6

8 Rating Withdrawal: No Transaction Name 1 IKF Finance Limited Asirvad Microfinance Pvt. Ltd. Asirvad Microfinance Pvt. Ltd. Asirvad Microfinance Pvt. Ltd. Bharat Financial Inclusion Limited 6 Magma Fincorp Limited Volturnus CV IFMR Capital 2016 Dufresne IFMR Capital 2016 Travis IFMR Capital 2016 Casca IFMR Capital 2016 Facilities / Instrument A1 PTCs A2 PTCs A1 PTCs A2 PTCs A1 PTCs A2 PTCs A1 PTCs A2 PTCs Month of Withdrawal Jan 18 Jan 18 Jan 18 Dec 17 IMLRT Jan 16 A PTCs Dec 17 MFL Securitisation Trust XXVIII 7 S V Creditline Ltd Amako IFMR Capital Indiabulls Hosuing Finance Limited Indiabulls Hosuing Finance Limited Indiabulls Hosuing Finance Limited Indiabulls Hosuing Finance Limited Equitas Small Finance Bank Limited ESAF Microfinance Private Limited ESAF Microfinance Private Limited Light Microfinance Private Limited Bharat Financial Inclusion Limited A1 PTCs A2 PTCs SLF LF A1 PTCs A2 PTCs Dec 17 Dec 17 IBFSL DA Mar12 II A PTCs Oct 17 IBFSL DA Sep 11 I A PTCs Oct 17 Innovation Trust XI A PTCs Oct 17 Innovation Trust VIII A PTCs Oct 17 EMF Microloans Pool Series X - March 2016 A PTCs Sep-17 Cedar MFI Trust 25 A PTCs Sep-17 Cedar MFI Trust 26 A PTCs Aug-17 Tachyon Trust 2016 A PTCs Aug-17 IMLRT March 2016 A A PTCs Jul-17 7

9 Provisional Rating: List of provisional rating cases assigned by CARE which are yet to convert to final rating provided below. The rating shall be confirmed, once the final documents received. The executed documents should confirm to the structure/conditions as provided at the time of the initial rating. No Asirvad Microfinance Limited Satin Credircare Limited Home Credit India Finance Ltd Light Microfinance Private Limited Annapurna Microfinance Private Limited Fusion Microfinance Private Limited Spandana Sphoorty Finance limited Spandana Sphoorty Finance limited Asirvad Microfinance Limited ESAF Small Finance Bank Transaction Name Daenerys IFMR Capital 2017 Vivriti Rey Tarini IFMR Capital 2017 Aguamenti IFMR Capital 2017 Vivriti Asensio Olenna IFMR Capital 2017 Abhilasha Shree Vivriti Matic Cedar Inclusive Finance Trust 1 Rating assigned month Nov-17 Nov-17 Nov-17 Nov-17 Nov-17 Nov-17 Nov-17 Nov-17 Dec-17 Dec-17 Instrument Series A1 PTCs Series A2 PTCs Series A1 PTCs Series A2 PTCs Series A1 PTCs Series A2 PTCs Series A1 PTCs Series A2 PTCs Series A PTCs Series A1 PTCs Series A2 PTCs Series A PTCs Series A PTCs Series A1 PTCs Series A2 PTCs Series A1 PTCs Series A2 PTCs Series A3 PTCs Amount (Rs Crs) Ratings assigned Provisional CARE AA- (SO) Provisional CARE A- (SO) Provisional CARE A- (SO) Provisional CARE BBB (SO) Provisional CARE A- (SO) Provisional CARE BBB- (SO) Provisional CARE BBB+ (SO) Provisional CARE BBB (SO) Provisional CARE A- (SO) Provisional CARE A- (SO) Provisional CARE BBB (SO) Provisional CARE A+ (SO) Provisional CARE A+ (SO) Provisional CARE A+ (SO) Provisional CARE BBB+ (SO) Provisional CARE A- (SO) Provisional CARE BBB+ (SO) Provisional CARE BBB- (SO) Documents pending YES YES YES YES YES YES YES YES YES YES 8

10 No Fusion Microfinance Private Limited Fusion Microfinance Private Limited Hinduja Leyland Finance Hinduja Leyland Finance Transaction Name Vivriti Windu Rosetta IFMR Capital 2017 Gemini CV Trust II Dec 2017 Ramnos IFMR Capital 2017 Rating assigned month Dec-17 Dec-17 Dec-17 Dec-17 Instrument Series A PTCs Series A PTCs Series A1 PTCs Amount (Rs Crs) SLF 20.1 Series A1 PTCs SLF Ratings assigned Provisional CARE A- (SO) Provisional CARE A (SO) Provisional CARE AAA (SO) Provisional CARE A- (SO) Provisional CARE AAA (SO) Provisional CARE BBB+ (SO) Documents pending YES YES YES YES 9

11 Sr. No. 1 2 Rating Transition: Indiabulls Housing Finance Limited Indiabulls Housing Finance Limited Transaction Name IBHFL DA Mar 12 I IBHFL DA Mar 12 II Instrument Assignee Payout Assignee Payout Month of Upgrade Oct 17 Oct 17 Rating/Credit Opinion CARE AAA (SO) CARE AAA (SO) Remarks Upgraded from CARE AA+ (SO) Upgraded from CARE AA+ (SO) 3 Dewan Housing Finance Ltd Nirmaan RMBS Trust - Series I Series A1 PTCs Series A2 PTCs Oct'17 CARE AAA (SO) CARE AAA (SO) Reaffirmed Upgraded from CARE AA (SO) 4 Dewan Housing Finance Ltd Nirmaan RMBS Trust - Series II Series A1 PTCs Series A2 PTCs Dec'17 CARE AAA (SO) CARE AAA (SO) Reaffirmed Upgraded from CARE AA- (SO) 5 Dewan Housing Finance Ltd Nirmaan RMBS Trust - Series III Series A1 PTCs Series A2 PTCs Dec'17 CARE AAA (SO) CARE AAA (SO) Reaffirmed Upgraded from CARE AA (SO) 6 Dewan Housing Finance Ltd Nirmaan RMBS Trust - Series IV Series A1 PTCs Series A2 PTCs Dec'17 CARE AAA (SO) CARE AAA (SO) Reaffirmed Upgraded from CARE AA (SO) 10

12 Sr. No Credit Enhancement Reset: Transaction Name Instrument Dewan Housing Finance Ltd Dewan Housing Finance Ltd Dewan Housing Finance Ltd Dewan Housing Finance Ltd Nirmaan RMBS Trust - Series I Nirmaan RMBS Trust - Series II Nirmaan RMBS Trust - Series III Nirmaan RMBS Trust - Series IV Month of Reset Principal Outstanding (Rs. Cr.) Rating/Credit Opinion Series A1 PTCs CARE AAA (SO) Oct'17 Series A2 PTCs 0.65 CARE AAA (SO) Series A1 PTCs CARE AAA (SO) Dec'17 Series A2 PTCs 4.71 CARE AAA (SO) Series A1 PTCs CARE AAA (SO) Dec'17 Series A2 PTCs 6.08 CARE AAA (SO) Series A1 PTCs CARE AAA (SO) Dec'17 Series A2 PTCs 3.21 CARE AAA (SO) 11

13 Asirvad Microfinance Limited (AMFPL 5 Pools) Key financial indicators For the year ended as on 31st March (12m, A) (12m, A) (12m, A) Total Income (in Rs. Cr) Profit After Tax (in Rs. Cr) Net worth (in Rs. Cr) Gross NPA ratio (%) Capital Adequacy Ratio (CAR) (%) P*=Provisional, A=Audited Total income stood at Rs. 363 Crores in FY17 as compared to Rs. 156 Crore in FY16, a growth of 133% The Gross NPA ratio increased from 0.11% as on March 31, 2016 to 4.56% as on March 31 st AMFPL reported regulatory CAR of 20.60% as on FY17. 12

14 Rating Dufresne IFMR Capital 2016 Asirvad Microfinance Limited (AMFL) Withdrawn Microfinance (100%) Jun-16 CC as % of initial POS 4.5% Par First Loss Credit Facility 54.5 Second Loss Credit Facility Series A1 Principal (Rs Cr) 47.9 LF as % of initial POS 62.8 Series A2 Principal (subordinated to A1) (Rs Cr) ,654 EIS 8.7% Average Maturity (Fortnights) 33.6 OC 2.0% Average Seasoning' (Fortnights) 9.6 Pool Maturity Apr %, 0% Maturity (months) 22 Months Post Securitisation Balance Tenure (Months) Pool Amortisation % % Amortisation (Series A1 Principal) % Amortisation (Series A2 Principal) 51.4% 30+ (% of Initial POS) 4.9% 8.0% 90+ (% of Initial POS) 3.6% 5.6% 30+ (% of Balance POS) 30.1% 16.0% 90+ (% of Balance POS) 16.5% 9.6% Amt (% of Initial POS) 10.1% 7.0% CC as % of Balance POS 113.6% 26.5% FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 90.9% 92.9% (3 month average) 77.0% 86.5% Break even 71.6% Break even (FLF) Overall enhancement coverage (30+ DPD) 1.8 Overall enhancement coverage (90+ DPD) 2.9 FL enhancement Coverage (30+ DPD) FL enhancement Coverage (90+ DPD) Cumulative Prepayment 3.4% 2.2% 12.0% 30+ dpd 90+ dpd 120% 9.0% 6.0% 80% 3.0% 40% M1 M4 M7 M10 M13 0% M1 M4 M7 M10 M13 13

15 Rating Casca IFMR Capital 2016 Asirvad Microfinance Limited (AMFL) Withdrawn Microfinance (100%) Jul-16 CC as % of initial POS 4.5% Par First Loss Credit Facility 66.7 Second Loss Credit Facility Series A1 Principal (Rs Cr) 58.7 LF as % of initial POS 76.4 Series A2 Principal (subordinated to A1) (Rs Cr) ,158 EIS 8.5% Average Maturity (Months) 15.3 OC 2.0% Average Seasoning' (Months) 6.7 Pool Maturity May %, 0% Maturity (months) 23 Months Post Securitisation Balance Tenure (Months) 6 9 Pool Amortisation 99.3% 86.2% Amortisation (Series A1 Principal) % Amortisation (Series A2 Principal) 79.3% 30+ (% of Initial POS) 4.1% 5.9% 90+ (% of Initial POS) 3.8% 4.7% 30+ (% of Balance POS) 68.0% 15.8% 90+ (% of Balance POS) 55.7% 10.8% Amt (% of Initial POS) 3.9% 4.5% CC as % of Balance POS 619.9% 32.6% FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 95.7% 95.4% (3 month average) 97.8% 97.5% Break even 56.1% Break even (FLF) Overall enhancement coverage (30+ DPD) 2.8 Overall enhancement coverage (90+ DPD) 4.1 FL enhancement Coverage (30+ DPD) FL enhancement Coverage (90+ DPD) Cumulative Prepayment 9.6% 7.1% 8.0% 30+ dpd 90+ dpd 120% 6.0% 4.0% 80% 2.0% 40% M1 M4 M7 M10 M13 0% M1 M4 M7 M10 M13 14

16 Rating Travis IFMR Capital 2016 Asirvad Microfinance Limited (AMFL) Withdrawn Microfinance (100%) Sep-16 CC as % of initial POS 4.0% Par First Loss Credit Facility 50.6 Second Loss Credit Facility Series A1 Principal (Rs Cr) 44.0 LF as % of initial POS 57.2 Series A2 Principal (subordinated to A1) (Rs Cr) ,626 EIS 7.7% Average Maturity (Months) 15.6 OC 4.0% Average Seasoning' (Months) 6.9 Pool Maturity Jun %, 0% Maturity (months) 21 Months Post Securitisation 12 9 Balance Tenure (Months) 9 12 Pool Amortisation 92.3% 76.2% Amortisation (Series A1 Principal) % Amortisation (Series A2 Principal) 61.2% 30+ (% of Initial POS) 1 6.8% 90+ (% of Initial POS) 6.3% 4.4% 30+ (% of Balance POS) 39.0% 12.9% 90+ (% of Balance POS) 13.4% 7.0% Amt (% of Initial POS) 8.3% 5.6% CC as % of Balance POS 51.6% 16.8% FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 91.7% 93.8% (3 month average) 80.6% 90.8% Break even 36.5% 63.0% Break even (FLF) Overall enhancement coverage (30+ DPD) 2.9 Overall enhancement coverage (90+ DPD) 5.3 FL enhancement Coverage (30+ DPD) FL enhancement Coverage (90+ DPD) Cumulative Prepayment 4.3% 2.6% 12.0% 30+ dpd 90+ dpd 110% 8.0% 80% 4.0% 50% M1 M3 M5 M7 M9 M11 20% M1 M3 M5 M7 M9 M11 15

17 Rating Brewster IFMR Capital 2016 Asirvad Microfinance Limited (AMFL) Series A1 PTC- CARE A (SO) and Series A2 PTC- CARE BBB+ (SO) Microfinance (100%) Jun-17 CC as % of initial POS 5.2% Par First Loss Credit Facility 52.1 Second Loss Credit Facility Series A1 Principal (Rs Cr) 43.8 LF as % of initial POS 58.0 Series A2 Principal (subordinated to A1) (Rs Cr) ,894 EIS 8.4% Average Maturity (Months) 14.9 OC 13.0% Average Seasoning' (Months) 8.6 Pool Maturity Mar %, 0% Maturity (months) 21 Months Post Securitisation 3 - Balance Tenure (Months) 18 - Pool Amortisation 33.2% - Amortisation (Series A1 Principal) 39.7% - Amortisation (Series A2 Principal) (% of Initial POS) 0.3% (% of Initial POS) (% of Balance POS) 0.3% (% of Balance POS) - Amt (% of Initial POS) 0.2% - CC as % of Balance POS 7.8% - FLF as % of Balance POS - LF as % of Balance POS - Balance CC (unutilized) 10 - Balance FLF (unutilized) - Balance LF (unutilized) % - (3 month average) 99.2% - Break even 67.6% - Break even (FLF) - Overall enhancement coverage (30+ DPD) >30 - Overall enhancement coverage (90+ DPD) >30 - FL enhancement Coverage (30+ DPD) - FL enhancement Coverage (90+ DPD) - Cumulative Prepayment 1.3% - 16

18 Rating Canopus IFMR Capital 2016 Asirvad Microfinance Limited (AMFL) Series A1 PTC- CARE A (SO) and Series A2 PTC- CARE A- (SO) Microfinance (100%) Jul-17 CC as % of initial POS 4.4% Par First Loss Credit Facility 51.2 Second Loss Credit Facility Series A1 Principal (Rs Cr) 43.0 LF as % of initial POS 57.6 Series A2 Principal (subordinated to A1) (Rs Cr) ,601 EIS 9.2% Average Maturity (Months) 14.7 OC 13.0% Average Seasoning' (Months) 6.9 Pool Maturity Apr %, 0% Maturity (months) 21 Months Post Securitisation 2 - Balance Tenure (Months) 19 - Pool Amortisation 19.1% - Amortisation (Series A1 Principal) 22.8% - Amortisation (Series A2 Principal) (% of Initial POS) 0.1% (% of Initial POS) (% of Balance POS) 0.1% (% of Balance POS) - Amt (% of Initial POS) 0.1% - CC as % of Balance POS 5.4% - FLF as % of Balance POS - LF as % of Balance POS - Balance CC (unutilized) 10 - Balance FLF (unutilized) - Balance LF (unutilized) % - (3 month average) - Break even 72.8% - Break even (FLF) - Overall enhancement coverage (30+ DPD) >30 - Overall enhancement coverage (90+ DPD) - FL enhancement Coverage (30+ DPD) - FL enhancement Coverage (90+ DPD) - Cumulative Prepayment 0.9% - 17

19 Aptus Value Housing Finance Limited (AVHFIL - 2 Pools) Key financial indicators For the year ended as on 31st March (12m, A) (12m, A) (12m, A) Total Income (in Rs. Cr) Profit After Tax (in Rs. Cr) Net worth (in Rs. Cr) Gross NPA ratio (%) Capital Adequacy Ratio (CAR) (%) P*=Provisional, A=Audited Total income stood at Rs Cr in FY17, as compared to Rs. 78 Crore in FY16. The Gross NPA ratio increased from 0.41% as on March 31, 2016 to 0.45% as on March 31 st AMFPL reported regulatory CAR of 98.07% as on FY17. 18

20 Rating Ariel SBL IFMR Capital 2015 Aptus Value Housing Finance India Limited (AVHFIL) Series A1 PTC - CARE A- (SO) and Series A2 PTC - CARE BBB+ (SO) Small Business Loans (100%) Jan-16 CC as % of initial POS 2.5% Par First Loss Credit Facility 14.2 Second Loss Credit Facility Series A1 Principal (Rs Cr) 12.6 LF as % of initial POS 24.2 Series A2 Principal (subordinated to A1) (Rs Cr) EIS 42.1% Average Maturity (months) 63.1 OC 9.0% Average Seasoning' (months) 24.6 Pool Maturity Feb Maturity (months) 133 Months Post Securitisation Pool Amortisation Amortisation (Series A1 Principal) Amortisation (Series A2 Principal) 53.3% 59.9% 47.8% 53.7% 90+ (% of Initial POS) 2.1% 1.1% 180+ (% of Initial POS) 1.0% 0.7% 90+ (% of Balance POS) 2.4% 1.0% 180+ (% of Balance POS) 0.6% 0.4% Amt (% of Initial POS) 1.1% 0.8% CC as % of Balance POS 5.4% 4.8% FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 94.1% 94.5% (3 month average) 92.0% 94.4% Break even 57.4% 59.2% Break even (FLF) Overall enhancement coverage (90+ DPD) 17.7 >30 Overall enhancement coverage (180+ DPD) >30 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 33.6% 31.0% 5.0% 90+ dpd 180+ dpd 120% 4.0% 3.0% 2.0% 100% 80% 1.0% 60% M1 M4 M7 M10 M13 M16 M19 40% M1 M4 M7 M10 M13 M16 M19 19

21 Rating Attis SBL IFMR Capital 2016 Aptus Value Housing Finance India Limited (AVHFIL) Series A1 PTC - CARE A- (SO) and Series A2 PTC - CARE BBB (SO) Small Business Loans (100%) Feb-16 CC as % of initial POS 2.5% Par First Loss Credit Facility 25.9 Second Loss Credit Facility Series A1 Principal (Rs Cr) 23.1 LF as % of initial POS 48.2 Series A2 Principal (subordinated to A1) (Rs Cr) EIS 47.7% Average Maturity (months) 83.3 OC 9.0% Average Seasoning' (months) 16.3 Pool Maturity Feb Maturity (months) 108 Months Post Securitisation Pool Amortisation 39.9% 33.5% Amortisation (Series A1 Principal) 44.9% 37.6% Amortisation (Series A2 Principal) 90+ (% of Initial POS) 0.6% 0.4% 180+ (% of Initial POS) 0.3% 0.3% 90+ (% of Balance POS) 0.4% 0.2% 180+ (% of Balance POS) Amt (% of Initial POS) 0.5% 0.4% CC as % of Balance POS 4.2% 3.8% FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 93.9% 94.2% (3 month average) 92.1% 91.8% Break even 61.3% 63.1% Break even (FLF) Overall enhancement coverage (90+ DPD) >30 >30 Overall enhancement coverage (180+ DPD) >30 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 27.5% 22.9% 5.0% 90+ dpd 180+ dpd 120% 4.0% 3.0% 100% 2.0% 1.0% 80% M1 M4 M7 M10 M13 M16 M19 60% M1 M4 M7 M10 M13 M16 M19 20

22 Arohan Financial Services Private Limited (Arohan 1 Pools) Key Financial Indicators For the year ended as on 31st March (12m, A) (12m, A) (12m, A) Total Income (in Rs. Cr) Profit After Tax (in Rs. Cr) Net worth (in Rs. Cr) Gross NPA Capital Adequacy Ratio (CAR) P*=Provisional, A=Audited Total Income of Arohan has increased by 64% in FY17 to Rs crore with PAT increasing by 26.54%. With capital infusion during FY17, the capital adequacy increased to 39.35% as on March The Gross NPA remained stable at 0.36%. 21

23 Rating Mace IFMR Capital 2017 Arohan Financial Services Private Limited (AFSPL) Series A1 PTC - CARE A- (SO) and Series A2 PTC - CARE BBB+ (SO) Microfinance (100%) Mar-17 CC as % of initial POS 5.8% Par First Loss Credit Facility 35.8 Second Loss Credit Facility Series A1 Principal (Rs Cr) 31.8 LF as % of initial POS 39.3 Series A2 Principal (subordinated to A1) (Rs Cr) ,408 EIS 7.7% Average Maturity (Months) 8.8 OC 9.5% Average Seasoning' (Months) 7.0 Pool Maturity Dec %, 0% Maturity (months) 21 Months Post Securitisation 6 3 Balance Tenure (Months) Pool Amortisation 71.9% 41.4% Amortisation (Series A1 Principal) 82.5% 46.6% Amortisation (Series A2 Principal) 30+ (% of Initial POS) 1.1% 0.7% 90+ (% of Initial POS) 0.4% 30+ (% of Balance POS) 1.7% 0.9% 90+ (% of Balance POS) 0.6% Amt (% of Initial POS) 0.9% 0.8% CC as % of Balance POS 20.6% 9.9% FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 98.8% 98.2% (3 month average) 99.6% 98.2% Break even 38.6% 68.4% Break even (FLF) Overall enhancement coverage (30+ DPD) >30 > 30 Overall enhancement coverage (90+ DPD) >30 FL enhancement Coverage (30+ DPD) FL enhancement Coverage (90+ DPD) Cumulative Prepayment 2.6% 1.9% 3.0% 30+ dpd 90+ dpd 120% 2.0% 90% 1.0% 60% M1 M2 M3 M4 M5 M6 30% M1 M2 M3 M4 M5 M6 22

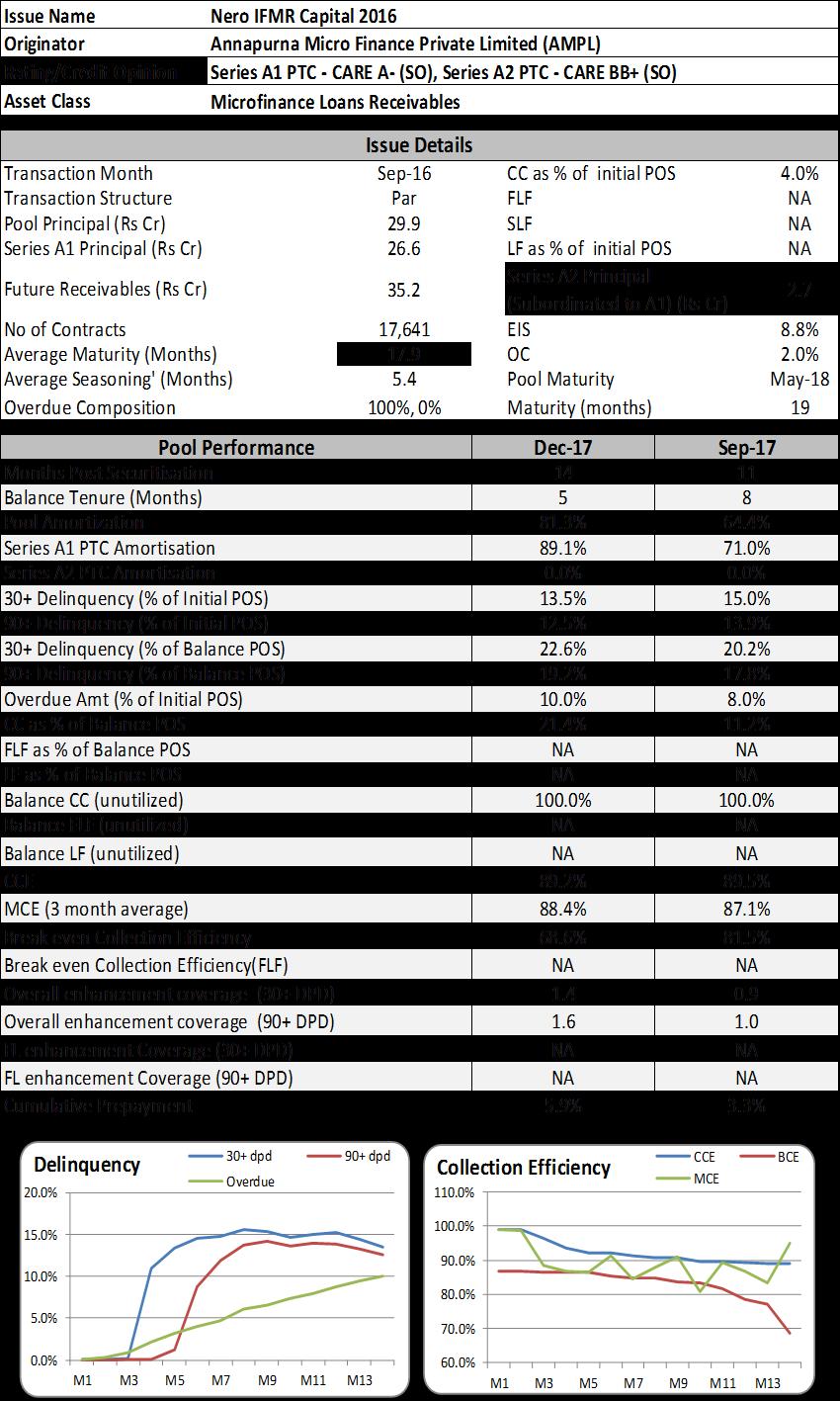

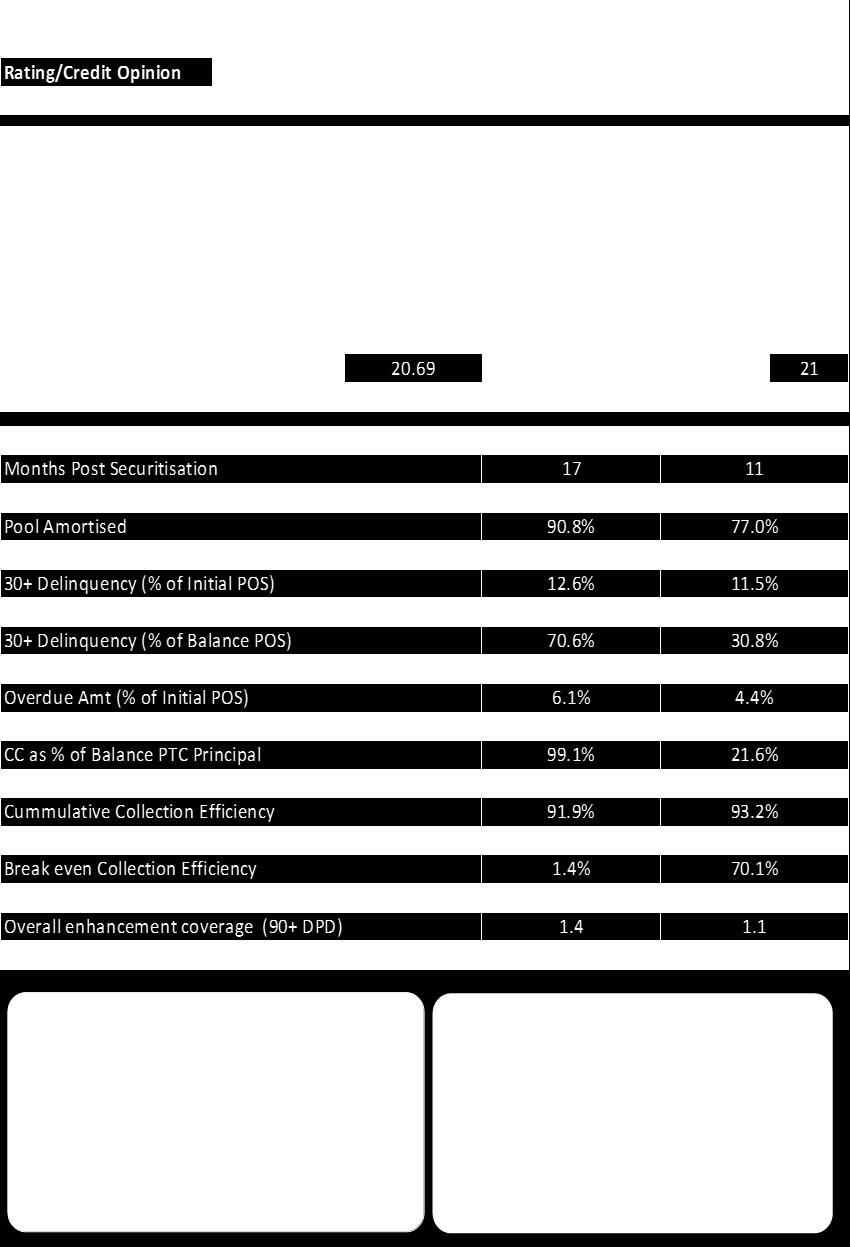

24 Annapurna Microfinance Private Limited (AMPL 4 Pools) Key financial indicators For the year ended as on 31st March (12m, A) (12m, A) (12m, A) Total Income (in Rs. Cr) Profit After Tax (in Rs. Cr) Net worth (in Rs. Cr) Gross NPA ratio (%) Capital Adequacy Ratio (CAR) (%) P*=Provisional, A=Audited Total income stood at Rs Crore in FY16 as compare to crore as in FY15. The Gross NPA ratio reduced from 0.10% as on March 31, 2015 to 0.07% as on March 31 st AMFPL reported regulatory CAR of 19.43% as on FY16. 23

25 24

26 25

27 Rating/Credit Opinion Gale IFMR Capital 2016 Annapurna Micro Finance Private Limited (AMPL) Series A1 PTC - CARE A- (SO), Series A2 PTC - CARE BB (SO) Microfinance Loans Receivables Series A1 Principal (Rs Cr) Average Maturity (Months) Average Seasoning' (Months) Dec-16 CC as % of initial POS 4.5% Par FLF 25.4 SLF 22.6 LF as % of initial POS 29.7 Series A2 Principal (Subordinated to A1) (Rs Cr) ,736 EIS 9.0% 16.4 OC 1.0% 5.9 Pool Maturity Aug %, 0% Maturity (months) 19 Months Post Securitisation 8 5 Balance Tenure (Months) Pool Amortization 55.5% 35.6% Series A1 PTC Amortisation 63.4% 41.0% Series A2 PTC Amortisation 30+ (% of Initial POS) 2.2% 1.8% 90+ (% of Initial POS) 30+ (% of Balance POS) 1.6% 2.8% 1.2% 2.0% 90+ (% of Balance POS) 1.8% 1.2% Amt (% of Initial POS) CC as % of Balance POS FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 1.0% 10.1% % 0.6% 7.0% % (3 month average) 99.6% 100.4% Break even 78.2% 84.8% Break even (FLF) Overall enhancement coverage (30+ DPD) Overall enhancement coverage (90+ DPD) FL enhancement Coverage (30+ DPD) FL enhancement Coverage (90+ DPD) Cumulative Prepayment 3.8% 1.0% 4.0% 30+ dpd 90+ dpd % % 1.0% M1 M2 M3 M4 M5 M6 M7 M8 6 M1 M2 M3 M4 M5 M6 M7 M8 26

28 Rating/Credit Opinion Herrera IFMR Capital 2017 Annapurna Micro Finance Private Limited (AMPL) Series A1 PTC - CARE A- (SO), Series A2 PTC - CARE BB+ (SO) Microfinance Loans Receivables Series A1 Principal (Rs Cr) Average Maturity (Months) Average Seasoning' (Months) Mar-17 CC as % of initial POS 6.0% Par FLF 47.6 SLF 41.5 LF as % of initial POS 55.6 Series A2 Principal (Subordinated to A1) (Rs Cr) ,677 EIS 10.7% 15.6 OC 4.0% 4.8 Pool Maturity Nov %, 0% Maturity (months) 20 Months Post Securitisation 6 3 Balance Tenure (Months) Pool Amortization 42.0% 21.9% Series A1 PTC Amortisation Series A2 PTC Amortisation 49.2% 25.8% 30+ (% of Initial POS) 90+ (% of Initial POS) 30+ (% of Balance POS) 90+ (% of Balance POS) Amt (% of Initial POS) CC as % of Balance POS 0.4% 0.2% 0.5% 0.2% 0.1% 10.3% 0.2% 0.1% 0.2% 0.1% 0.1% 7.7% FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.7% 99.7% (3 month average) Break even 100.3% 76.5% 99.8% 80.7% Break even (FLF) Overall enhancement coverage (30+ DPD) >30 >30 Overall enhancement coverage (90+ DPD) >30 >30 FL enhancement Coverage (30+ DPD) FL enhancement Coverage (90+ DPD) Cumulative Prepayment 0.9% 0.1% 2.0% 30+ dpd 90+ dpd % % 0.5% M1 M2 M3 M4 M5 M6 6 M1 M2 M3 M4 M5 M6 27

29 Bharat Financial Inclusion Limited (erstwhile SKS Microfinance Ltd) (BFIL 6 Pools) Key Financial Indicators For the year ended as on 31st March (12m, A) (12m, A) (12m, A) Total Income (in Rs. Cr) 803 1, Profit After Tax (in Rs. Cr) Net worth (in Rs. Cr) 1,041 1,378 2,442 Gross NPA/Gross Advances(%) Capital Adequacy Ratio (CAR) P*=Provisional, A=Audited Total income for the FY17 increased by 30.81% to Rs. 1,728 crores from Rs. 1,321 crores in FY16. BFIL has registered net profit of Rs. 290 crores for FY17. Asset quality deteriorated post demonetisation with Gross NPA increasing to 6.0% in FY17. BFIL continues to have comfortable capital adequacy ratio (CAR) at 33.5% 28

30 Rating Indian Microfinance Loan Receivables Trust November 2015 Bharat Financial Inclusion Ltd (Erstwhile SKS Microfinance Ltd) Withdrawn Microfinance Loans PTC Series A Principal (Rs Cr) Average Maturity (Weeks) Average Seasoning' (Weeks) Nov-15 CC as % of initial POS 5.0% Par FLF SLF LF as % of initial POS EIS 11.8% 1,09, OC Pool Maturity 8.0% Jul %, 0% Maturity (months) 20 Pool Performance Jul-17 Jun-17 Months Post Securitisation Balance Tenure (Months) 0 1 Pool Amortisation % Series A PTC Amortisation % 30+ (% of Initial POS) 2.2% 2.4% 90+ (% of Initial POS) 2.1% 2.1% 30+ (% of Balance POS) 16.0% 90+ (% of Balance POS) 10.9% Amt (% of Initial POS) 2.2% 2.3% CC as % of Balance POS 566.7% CC as % of Balance PTC Principal 712.8% Balance CC (unutilized) % 97.9% (3 month average) 99.9% 94.2% Break even Overall enhancement coverage (30+ DPD) Overall enhancement coverage (90+ DPD) Cumulative Prepayment 1.9% 1.9% 3.0% 30+ dpd 90+ dpd 120% 2.0% 90% 60% 1.0% 30% M1 M4 M7 M10 M13 M16 M19 0% M2 M5 M8 M11 M14 M17 M20 29

31 Rating Indian Microfinance Loan Receivables Trust January 2016 Bharat Financial Inclusion Ltd (Erstwhile SKS Microfinance Ltd) Withdrawn Microfinance Loans PTC Series A Principal (Rs Cr) Average Maturity (Weeks) Average Seasoning (Weeks) Jan-16 CC as % of initial 5.0% Par FLF SLF LF as % of initial POS EIS 6.7% 5,49, OC Pool Maturity 7.5% Nov %, 0% Maturity (months) 22 Months Post Securitisation Balance Tenure (Months) 2 5 Pool Amortisation 98.7% 94.1% Series A PTC Amortisation 98.7% 94.3% 30+ (% of Initial POS) 1.0% 1.2% 90+ (% of Initial POS) 1.0% 0.9% 30+ (% of Balance POS) 9.5% 8.9% 90+ (% of Balance POS) 7.2% 5.7% Amt (% of Initial POS) 0.9% 0.7% CC as % of Balance POS 397.6% 85.2% CC as % of Balance PTC Principal 409.0% 94.5% Balance CC (unutilized) % 99.3% (3 month average) 94.4% 94.9% Break even 8.5% Overall enhancement coverage (30+ DPD) 10.3 Overall enhancement coverage (90+ DPD) 15.9 Cumulative Prepayment 2.1% 1.9% 2.0% 30+ dpd 90+ dpd 120% 1.5% 1.0% 80% 0.5% 40% M1 M4 M7 M10 M13 M16 M19 0% M1 M4 M7 M10 M13 M16 M19 30

32 Rating Indian Microfinance Loan Receivables Trust March 2016 B Bharat Financial Inclusion Ltd (Erstwhile SKS Microfinance Ltd) Series A PTC - CARE AAA (SO) Microfinance Loans PTC Series A Principal (Rs Cr) Average Maturity (Weeks) Average Seasoning' (Weeks) Mar-16 CC as % of initial POS 5.0% Par First Loss Credit Facility Second Loss Credit Facility LF as % of initial POS EIS 6.8% 4,02, Principal Subordination as a % of Pool Principal Pool Maturity 7.5% Jan %, 0% Maturity (months) 22 Months Post Securitisation Balance Tenure (Months) 4 7 Pool Amortisation 94.0% 88.2% Series A PTC Amortisation 93.9% 88.2% 30+ (% of Initial POS) 1.9% 2.1% 90+ (% of Initial POS) 1.7% 1.5% 30+ (% of Balance POS) 10.3% 9.8% 90+ (% of Balance POS) 7.8% 6.3% Amt (% of Initial POS) 1.4% 1.0% CC as % of Balance POS 82.7% 42.4% CC as % of Balance PTC Principal 88.8% 46.3% Balance CC (unutilized) % 99.0% (3 month average) 93.6% 94.1% Break even 9.4% 46.2% Overall enhancement coverage (30+ DPD) Overall enhancement coverage (90+ DPD) Cumulative Prepayment 1.8% 1.7% 3.0% 30+ dpd 90+ dpd 120% 2.0% 80% 1.0% 40% M1 M4 M7 M10 M13 M16 0% M1 M3 M5 M7 M9 M11 M13 M15 M17 31

33 Rating Indian Microfinance Loan Receivables Trust September 2016 Bharat Financial Inclusion Limited Series A PTC - CARE AA (SO) Microfinance Loans PTC Series A Principal (Rs Cr) Average Maturity (Weeks) Average Seasoning' (Weeks) Sep-16 CC as % of initial POS 5.0% Par First Loss Credit Facility Second Loss Credit Facility 99.6 LF as % of initial POS EIS 6.8% 53, Principal Subordination as a % of Pool Principal Pool Maturity 7.75% Jun %, 0% Maturity (months) 22 Months Post Securitisation Balance Tenure (Months) 9 12 Pool Amortisation 79.0% 71.7% Series A PTC Amortisation 79.0% 71.7% 30+ (% of Initial POS) 7.0% 7.2% 90+ (% of Initial POS) 6.0% 5.6% 30+ (% of Balance POS) 13.2% 11.8% 90+ (% of Balance POS) 9.5% 7.8% Amt (% of Initial POS) 4.2% 3.9% CC as % of Balance POS 23.8% 17.6% CC as % of Balance PTC Principal 25.8% 19.2% Balance CC (unutilized) % 95.1% (3 month average) 96.4% 95.1% Break even 56.1% 63.5% Overall enhancement coverage (30+ DPD) Overall enhancement coverage (90+ DPD) Cumulative Prepayment 0.9% 0.8% 8.0% 6.0% 4.0% 2.0% 30+ dpd 90+ dpd M1 M3 M5 M7 M9 M11 M13 120% 100% 80% 60% 40% M1 M3 M5 M7 M9 M11 M13 32

34 Rating Indian Microfinance Loan Receivables Trust March 2017 Bharat Financial Inclusion Limited Series A PTC - CARE AA (SO) Microfinance Loans PTC Series A Principal (Rs Cr) Average Maturity (Weeks) Average Seasoning' (Weeks) Mar-17 CC as % of initial POS 6.3% Par First Loss Credit Facility Second Loss Credit Facility LF as % of initial POS EIS 7.9% 1,27, Principal Subordination as a % of Pool Principal Pool Maturity 8.50% Jan %, 0% Maturity (months) 22 Months Post Securitisation 6 3 Balance Tenure (Months) Pool Amortisation Series A PTC Amortisation 40.8% 40.8% 19.9% 19.9% 30+ (% of Initial POS) 0.4% 0.3% 90+ (% of Initial POS) 0.3% 30+ (% of Balance POS) 0.5% 0.3% 90+ (% of Balance POS) 0.3% Amt (% of Initial POS) 0.2% 0.1% CC as % of Balance POS 10.6% 7.9% CC as % of Balance PTC Principal 11.6% 8.6% Balance CC (unutilized) % 99.7% (3 month average) 99.4% 99.7% Break even 78.0% 79.5% Overall enhancement coverage (30+ DPD) >30 >30 Overall enhancement coverage (90+ DPD) >30 >30 Cumulative Prepayment 0.5% 0.2% 1.5% 30+ dpd 90+ dpd 120% 1.0% 100% 0.5% 80% M1 M2 M3 M4 M5 M6 60% M1 M2 M3 M4 M5 M6 33

35 Rating Indian Microfinance Loan Receivables Trust July 2017 Bharat Financial Inclusion Limited Series A PTC - CARE AA (SO) Microfinance Loans PTC Series A Principal (Rs Cr) Average Maturity (Weeks) Average Seasoning' (Weeks) Aug-17 CC as % of initial POS 5.7% Par First Loss Credit Facility Second Loss Credit Facility LF as % of initial POS EIS 8.3% 1,23, Principal Subordination as a % of Pool Principal Pool Maturity 8.00% Apr %, 0% Maturity (months) 21 Months Post Securitisation 2 - Balance Tenure (Months) 19 - Pool Amortisation 9.8% - Series A PTC Amortisation 9.8% (% of Initial POS) (% of Initial POS) (% of Balance POS) (% of Balance POS) - Amt (% of Initial POS) - CC as % of Balance POS 6.3% - CC as % of Balance PTC Principal 6.9% - Balance CC (unutilized) % - (3 month average) - Break even 78.8% - Overall enhancement coverage (30+ DPD) > 30 - Overall enhancement coverage (90+ DPD) - Cumulative Prepayment 0.1% - 34

36 Cholamandalam Investment Finance Company Ltd. (CIFCL 1 Pool) Key Financial Indicators For the year ended as on 31st March (12m, A) (12m, A) (12m, A) Total Income (in Rs. Cr) 3,691 4,193 4,660 Profit After Tax (in Rs. Cr) Net worth (in Rs. Cr) 3,172 3,657 4,313 Gross NPA (%) Capital Adequacy Ratio (CAR) P*=Provisional, A=Audited During FY16, CIFCL reported an operating income of Rs. 4,660 crore (growth of 11.14% yoy) and PAT of Rs. 719 crore (growth of 26.58% y-o-y) The overall asset quality of CIFCL had seen deterioration over the years. The gross NPA has increased to 5.69% in FY17 and compared to 3.53% in FY16. The CAR declined marginally to 18.64% as on March 31, 2017 as against 19.68% as on March 31,

37 Rating/Credit Opinion Platinum Trust Jan -14 Cholamandalam Investment and Finance Company Ltd. (CIFCL) Series A PTCs - CARE AAA (SO) Loan Against property Average Maturity (Months) Average Seasoning' (Months) Jan-14 CC as % of initial POS 10.5% Par FLF SLF LF as % of initial POS 413 EIS 40.3% 62.8 Over Collateral 15.0 Pool Maturity Dec %, 0% Maturity (months) 168 Months Post Securitisation Amortisation 76.4% 73.0% 90+ (% of Initial POS) 7.5% 6.5% 180+ (% of Initial POS) 7.1% 5.7% 90+ (% of Balance POS) 20.6% 16.5% 180+ (% of Balance POS) 18.8% 14.0% Amt (% of Initial POS) 2.7% 2.1% CC as % of Balance POS 44.5% 39.0% FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 94.2% 94.8% (3 month average) 82.1% 101.8% Break even 54.3% 57.5% Break even (FLF) Overall enhancement coverage (90+ DPD) Overall enhancement coverage (180+ DPD) FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 61.6% 59.2% 8.0% 6.0% 4.0% 2.0% 90+ dpd 180+ dpd M1 M7 M13 M19 M25 M31 M37 M M1 M7 M13 M19 M25 M31 M37 M43 36

38 Dewan Housing Finance Limited (DHFL 13 Pools) Key Financial Indicators For the year ended as on 31st March (12m, A) (12m, A) (12m, A) Total Income (in Rs. Cr) 5,982 7,317 10,827 Profit After Tax (in Rs. Cr) ,896 Net worth (in Rs. Cr) 4,636 4,981 7,989 Gross NPA (%) Capital Adequacy Ratio (CAR) (%) DHFL reported PAT of Rs. 2,896 crore on total income of Rs. 10,827 crore during FY17 as compared to PAT of Rs. 729 crore on total income of Rs. 7,317 crore during FY16. DHFL reported Gross NPA ratio of 0.94% in FY17. Over the years DHFL has developed the expertise in lending in the low-middle income group segment while maintaining stable asset quality parameters. DHFL reported the CAR of 19.34% as on March 31, 2017, as compared to 16.74% as on March 31,

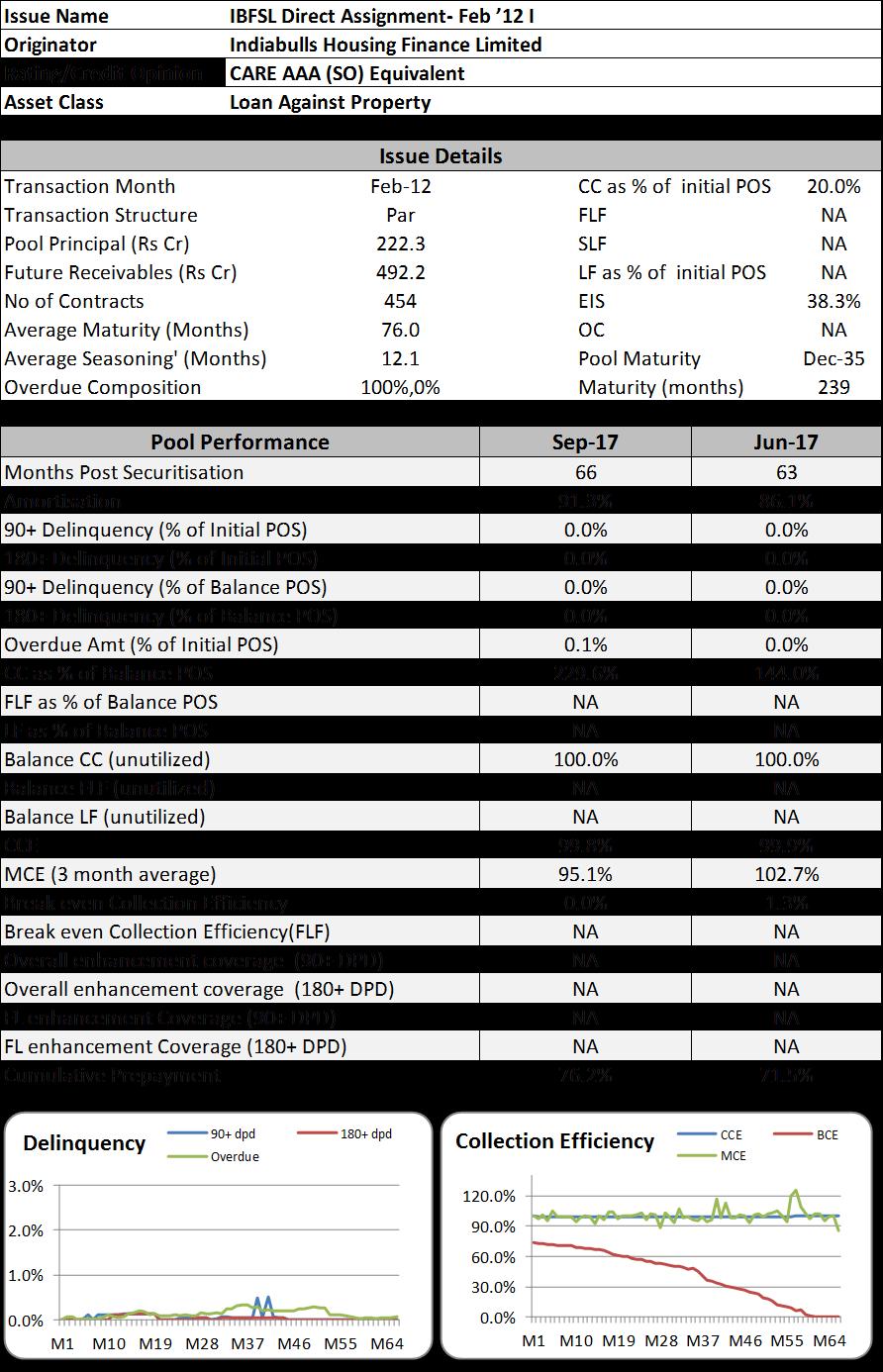

39 Rating/Credit Opinion DHFL Direct Assignment Mar'12 I Dewan Housing Finance Limited Assignee Payout - CARE AAA (SO) Equivalent Housing Loans Receivables Average Maturity (Months) Average Seasoning' (Months) Mar-12 CC as % of initial POS 15.5% Par FLF SLF LF as % of initial POS 3,853 EIS 10.3% 91.0 OC 12.8 Pool Maturity Mar %, 0% Maturity (months) 240 Months Post Securitisation Amortisation 65.4% 63.6% 90+ (% of Initial POS) 0.2% 0.4% 180+ (% of Initial POS) 0.2% 0.3% 90+ (% of Balance POS) 0.4% 0.8% 180+ (% of Balance POS) 0.4% 0.6% Amt (% of Initial POS) 0.1% 0.1% CC as % of Balance POS 44.8% 42.5% FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.7% 99.7% (3 month average) 101.5% 100.5% Break even 66.3% 67.8% Break even (FLF) Overall enhancement coverage (90+ DPD) >30 >30 Overall enhancement coverage (180+ DPD) >30 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 43.8% 42.9% 5.0% 4.0% 3.0% 2.0% 1.0% 90+ dpd 180+ dpd M1 M11 M21 M31 M41 M51 M M1 M11 M21 M31 M41 M51 M61 \ 38

40 Rating/Credit Opinion DHFL Direct Assignment Mar'12 II Dewan Housing Finance Limited Assignee Payout - CARE AAA (SO) Equivalent Housing Loans Receivables Average Maturity (Months) Average Seasoning' (Months) Mar-12 CC as % of initial POS 13.0% Par FLF SLF LF as % of initial POS 3,874 EIS 20.9% 92.4 OC 16.6 Pool Maturity Mar %, 0% Maturity (months) 300 Months Post Securitisation Amortisation 66.5% 64.3% 90+ (% of Initial POS) 0.2% 0.2% 180+ (% of Initial POS) 0.2% 0.2% 90+ (% of Balance POS) 0.4% 0.4% 180+ (% of Balance POS) 0.3% 0.3% Amt (% of Initial POS) 0.1% 0.1% CC as % of Balance POS 38.8% 36.4% FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.6% 99.6% (3 month average) 99.4% 10 Break even 68.3% 70.1% Break even (FLF) Overall enhancement coverage (90+ DPD) >30 >30 Overall enhancement coverage (180+ DPD) >30 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 45.7% 44.4% 5.0% 4.0% 3.0% 2.0% 1.0% 90+ dpd 180+ dpd M1 M14 M27 M40 M53 M M1 M14 M27 M40 M53 M66 39

41 Rating/Credit Opinion DHFL Direct Assignment Mar'12 III Dewan Housing Finance Limited Assignee Payout - CARE AAA (SO) Equivalent Housing Loans Receivables Average Maturity (Months) Average Seasoning' (Months) Mar-12 CC as % of initial POS 14.0% Par FLF SLF LF as % of initial POS 1,444 EIS 12.5% 90.5 OC 17.1 Pool Maturity Mar %, 0% Maturity (months) 240 Months Post Securitisation Amortisation 67.1% 64.7% 90+ (% of Initial POS) 0.4% 0.7% 180+ (% of Initial POS) 0.3% 0.5% 90+ (% of Balance POS) 0.9% 1.4% 180+ (% of Balance POS) 0.6% 1.0% Amt (% of Initial POS) 0.2% 0.2% CC as % of Balance POS 42.6% 39.6% FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.6% 99.6% (3 month average) 100.5% 100.2% Break even 68.2% 70.1% Break even (FLF) Overall enhancement coverage (90+ DPD) > Overall enhancement coverage (180+ DPD) > FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 46.7% 45.1% 5.0% 4.0% 3.0% 2.0% 1.0% 90+ dpd 180+ dpd M1 M11 M21 M31 M41 M51 M61 110% 100% 90% 80% 70% 60% M1 M11 M21 M31 M41 M51 M61 40

42 Rating/Credit opinion Nirmaan RMBS Trust - Series II Dewan Housing Finance Limited Series A1 PTCs - CARE AAA(SO) & Series A2 PTC - CARE AA- (SO) Housing Loans Receivables Jun-13 CC as % of initial POS 8.0% Par FLF SLF Series A1 Principal (Rs Cr) LF as % of initial POS Average Maturity (Months) Average Seasoning' (Months) Series A2 Principal (subordinated to A1) (Rs Cr) ,110 EIS 33.6% OC 4.0% 17.9 Pool Maturity Jun %, 0% Maturity (months) 300 Months Post Securitisation Pool Amortisation % % Amortisation (Series A1 Principal) 59.0% 56.8% Amortisation (Series A2 Principal) 59.0% 56.8% 90+ (% of Initial POS) 0.2% 0.2% 180+ (% of Initial POS) 0.1% 0.1% 90+ (% of Balance POS) 0.4% 0.4% 180+ (% of Balance POS) 0.3% 0.2% Amt (% of Initial POS) 0.1% 0.1% CC as % of Balance POS 19.5% 18.5% FLF as % of Balance POS LF as % of Balance POS Balance LF (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.6% 99.6% (3 month average) 100.1% 100.3% Break even 78.1% 78.7% Break even (FLF) Overall enhancement coverage (90+ DPD) >30 >30 Overall enhancement coverage (180+ DPD) >30 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 46.6% 45.2% 5.0% 4.0% 3.0% 2.0% 1.0% 90+ dpd 180+ dpd M1 M8 M15 M22 M29 M36 M43 M50 110% 100% 90% 80% 70% M1 M8 M15 M22 M29 M36 M43 M50 41

43 Rating/Credit Opinion Nirmaan RMBS Trust - Series III Dewan Housing Finance Limited Series A1 PTCs - CARE AAA(SO) & Series A2 PTC - CARE AA (SO) Housing Loans Receivables Aug-13 CC as % of initial POS 8.4% Par FLF SLF Series A1 Principal (Rs Cr) LF as % of initial POS Series A2 Principal (subordinated to A1) (Rs Cr) ,791 EIS 23.2% Average Maturity (Months) 98.6 OC Average Seasoning' (Months) 33.4 Pool Maturity May %, 0% Maturity (months) 299 Months Post Securitisation Pool Amortisation 62.0% 59.4% Amortisation (Series A1 Principal) 62.0% 59.4% Amortisation (Series A2 Principal) 62.0% 59.4% 90+ (% of Initial POS) 0.2% 0.3% 180+ (% of Initial POS) 0.2% 0.2% 90+ (% of Balance POS) 0.5% 0.6% 180+ (% of Balance POS) 0.4% 0.5% Amt (% of Initial POS) 0.1% 0.1% CC as % of Balance POS 21.0% 19.7% FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.8% 99.8% (3 month average) 100.2% 100.1% Break even 78.0% 78.9% Break even (FLF) Overall enhancement coverage (90+ DPD) >30 >30 Overall enhancement coverage (180+ DPD) >30 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 46.5% 44.8% 5.0% 4.0% 3.0% 2.0% 1.0% 90+ dpd 180+ dpd M1 M7 M13 M19 M25 M31 M37 M43 M49 110% 100% 90% 80% 70% M1 M7 M13 M19 M25 M31 M37 M43 M49 42

44 Rating/Credit Opinion Nirmaan RMBS Trust - Series IV Dewan Housing Finance Limited Series A1 PTCs - CARE AAA(SO) & Series A2 PTC - CARE AA (SO) Housing Loans Receivables Nov-13 CC as % of initial POS 8.0% Par FLF SLF Series A1 Principal (Rs Cr) LF as % of initial POS Series A2 Principal (subordinated to A1) (Rs Cr) 7.8 2,135 EIS 29.5% Average Maturity (Months) OC 4.0% Average Seasoning' (Months) 37.2 Pool Maturity Oct %, 0% Maturity (months) 360 Pool Performance Sep-17 Sep-17 Months Post Securitisation Pool Amortisation 57.3% 54.9% Amortisation (Series A1 Principal) 57.3% 54.9% Amortisation (Series A2 Principal) 57.3% 54.9% 90+ (% of Initial POS) 0.2% 0.4% 180+ (% of Initial POS) 0.2% 0.3% 90+ (% of Balance POS) 0.4% 0.7% 180+ (% of Balance POS) 0.4% 0.6% Amt (% of Initial POS) 0.1% 0.1% CC as % of Balance POS 18.7% 17.8% FLF as % of Balance POS LF as % of Balance POS Balance LF (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.8% 99.8% (3 month average) 100.5% 99.5% Break even 78.6% 79.3% Break even (FLF) Overall enhancement coverage (90+ DPD) >30 >30 Overall enhancement coverage (180+ DPD) >30 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 42.3% 40.8% 5.0% 4.0% 3.0% 2.0% 1.0% 90+ dpd 180+ dpd M1 M6 M11 M16 M21 M26 M31 M36 M41 M46 110% 100% 90% 80% 70% M1 M6 M11 M16 M21 M26 M31 M36 M41 M46 43

45 Rating/Credit opinion Nirmaan RMBS Trust - Series III Dewan Housing Finance Limited Series A1 PTCs - CARE AAA(SO) & Series A2 PTC - CARE AA (SO) Housing Loans Receivables Mar-14 CC as % of initial POS 8.8% Par FLF 92.2 SLF Series A1 PTC Principal (Rs Cr) 88.5 LF as % of initial POS Series A2 Principal (subordinated to A1) (Rs Cr) EIS 34.7% Average Maturity (Months) OC 4.0% Average Seasoning' (Months) 22.8 Pool Maturity Feb %, 0% Maturity (months) 299 Months Post Securitisation Pool Amortisation 47.2% 44.3% Amortisation (Series A1 Principal) 47.2% 44.3% Amortisation (Series A2 Principal) 47.2% 44.3% 90+ (% of Initial POS) 180+ (% of Initial POS) 90+ (% of Balance POS) 180+ (% of Balance POS) Amt (% of Initial POS) CC as % of Balance POS 16.6% 15.7% FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.9% 99.9% (3 month average) 99.7% 101.8% Break even 80.4% 80.7% Break even (FLF) Overall enhancement coverage (90+ DPD) Overall enhancement coverage (180+ DPD) FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 35.6% 33.7% 5.0% 90+ dpd 180+ dpd 110% 4.0% 100% 3.0% 2.0% 1.0% 90% 80% M1 M6 M11 M16 M21 M26 M31 M36 M41 70% M1 M6 M11 M16 M21 M26 M31 M36 M41 44

46 Rating/Credit Opinion Nirmaan RMBS Trust - Series IV Dewan Housing Finance Limited Series A PTCs - CARE AAA(SO) Housing Loans Receivables Average Maturity (Months) Average Seasoning' (Months) Mar-14 CC as % of initial POS 7.5% Par FLF 37.8 SLF 87.4 LF as % of initial POS 288 EIS 32.7% Mortgage Guarantee by IMGC Pool Maturity Dec %, 0% Maturity (months) 297 Months Post Securitisation Pool Amortisation 49.4% 46.0% Series A PTC Amortisation 49.4% 46.0% 90+ (% of Initial POS) 180+ (% of Initial POS) 90+ (% of Balance POS) 180+ (% of Balance POS) Amt (% of Initial POS) 0.1% CC as % of Balance POS 15.2% 14.2% FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.9% 99.9% (3 month average) 99.9% 99.6% Break even 80.6% 81.6% Break even (FLF) Overall enhancement coverage (90+ DPD) Overall enhancement coverage (180+ DPD) FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 35.7% 33.3% 5.0% 4.0% 3.0% 2.0% 1.0% 90+ dpd 180+ dpd M1 M6 M11 M16 M21 M26 M31 M36 M M1 M6 M11 M16 M21 M26 M31 M36 M41 45

47 Rating/Credit Opinion Nirmaan RMBS Trust - Series I Dewan Housing Finance Limited Series A1 PTCs - CARE AAA(SO) & Series A2 PTC - CARE AA (SO) Housing Loans Receivables Feb-15 CC as % of initial POS 10.5% Par FLF SLF Series A1 PTC Principal (Rs Cr) LF as % of initial POS Average Maturity (Months) Average Seasoning' (Months) Series A2 Principal (subordinated to A1) (Rs Cr) 6.4 1,596 EIS 29.1% OC 3.0% 22.5 Pool Maturity Feb %, 0% Maturity (months) 300 Months Post Securitisation Pool Amortisation 36.6% 33.6% Amortisation (Series A1 Principal) 36.6% 33.6% Amortisation (Series A2 Principal) 36.6% 33.6% 90+ (% of Initial POS) 0.3% 0.2% 180+ (% of Initial POS) 0.3% 0.2% 90+ (% of Balance POS) 0.5% 0.2% 180+ (% of Balance POS) 0.5% 0.2% Amt (% of Initial POS) 0.1% 0.1% CC as % of Balance POS 16.6% 15.8% FLF as % of Balance POS LF as % of Balance POS Balance LF (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.7% 99.8% (3 month average) 99.4% 99.9% Break even 80.3% 80.7% Break even (FLF) Overall enhancement coverage (90+ DPD) >30 >30 Overall enhancement coverage (180+ DPD) >30 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 27.5% 25.4% 5.0% 90+ dpd 180+ dpd 110% 4.0% 100% 3.0% 2.0% 1.0% 90% 80% M1 M6 M11 M16 M21 M26 M31 70% M1 M6 M11 M16 M21 M26 M31 46

48 Rating/Credit Opinion Nirmaan RMBS Trust - Series II Dewan Housing Finance Limited Series A1 PTCs - CARE AAA(SO) & Series A2 PTC - CARE AA (SO) Housing Loans Receivables Mar-15 CC as % of initial POS 7.8% Par FLF SLF Series A1 PTC Principal (Rs Cr) LF as % of initial POS Series A2 Principal (subordinated to A1) (Rs Cr) 9.4 4,228 EIS 26.6% Average Maturity (Months) 94.2 OC 3.0% Average Seasoning' (Months) 28.9 Pool Maturity Apr %, 0% Maturity (months) 242 Months Post Securitisation Pool Amortisation 39.0% 35.3% Amortisation (Series A1 Principal) 39.0% 35.3% Amortisation (Series A2 Principal) 39.0% 35.3% 90+ (% of Initial POS) 0.1% 0.2% 180+ (% of Initial POS) 0.1% 0.2% 90+ (% of Balance POS) 0.2% 0.3% 180+ (% of Balance POS) 0.2% 0.2% Amt (% of Initial POS) 0.1% 0.1% CC as % of Balance POS 12.8% 12.1% FLF as % of Balance POS LF as % of Balance POS Balance LF (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.8% 99.8% (3 month average) 99.8% 99.7% Break even 82.1% 82.5% Break even (FLF) Overall enhancement coverage (90+ DPD) >30 >30 Overall enhancement coverage (180+ DPD) >30 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 21.9% 19.8% 5.0% 4.0% 3.0% 2.0% 1.0% 90+ dpd 180+ dpd M1 M6 M11 M16 M21 M M1 M6 M11 M16 M21 M26 47

49 Rating/Credit Opinion Nirmaan RMBS Trust - Series I Dewan Housing Finance Limited Series A PTCs - CARE AAA(SO) Housing Loans Receivables Average Maturity (Months) Average Seasoning' (Months) Jun-16 CC as % of initial POS 9.5% Par FLF SLF LF as % of initial POS EIS Pool Maturity 22.3% May %, 0% Maturity (months) 300 Months Post Securitisation Pool Amortisation 20.1% 15.6% Series A PTC Amortisation 20.1% 15.6% 90+ (% of Initial POS) 0.1% 0.1% 180+ (% of Initial POS) 0.1% 90+ (% of Balance POS) 0.1% 0.1% 180+ (% of Balance POS) 0.1% Amt (% of Initial POS) 0.1% 0.1% CC as % of Balance POS 11.9% 11.3% FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.4% 99.5% (3 month average) 99.2% 99.0% Break even 80.2% 84.4% Break even (FLF) Overall enhancement coverage (90+ DPD) >30 >30 Overall enhancement coverage (180+ DPD) >30 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 12.8% 1 5.0% 90+ dpd 180+ dpd % 3.0% 2.0% 1.0% M1 M3 M5 M7 M9 M11 M13 M15 7 M1 M3 M5 M7 M9 M11 M13 M15 48

50 Rating/Credit Opinion Nirmaan RMBS Trust - Series II Dewan Housing Finance Limited Series A PTCs - CARE AAA(SO), Second Loss Facility - CARE A- (SO) equivalent Housing Loans Receivables Average Maturity (Months) Average Seasoning' (Months) Sep-16 CC as % of initial POS 9.3% Par FLF 5.0% SLF 4.3% LF as % of initial POS 1, EIS Pool Maturity 17.2% Aug %, 0% Maturity (months) 300 Months Post Securitisation 12 9 Pool Amortisation 14.7% 10.7% Series A PTC Amortisation 14.7% 10.7% 90+ (% of Initial POS) 0.2% 0.2% 180+ (% of Initial POS) 0.1% 90+ (% of Balance POS) 0.3% 0.2% 180+ (% of Balance POS) 0.1% Amt (% of Initial POS) 0.1% CC as % of Balance POS 10.8% 10.4% FLF as % of Balance POS 5.9% 5.6% LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.6% 99.6% (3 month average) 99.7% 99.7% Break even 86.3% 86.3% Break even (FLF) 89.0% 88.9% Overall enhancement coverage (90+ DPD) >30 >30 Overall enhancement coverage (180+ DPD) >30 FL enhancement Coverage (90+ DPD) >30 >30 FL enhancement Coverage (180+ DPD) >30 Cumulative Prepayment 8.8% 6.5% 5.0% 90+ dpd 180+ dpd % 3.0% 2.0% 1.0% M1 M3 M5 M7 M9 M11 7 M1 M3 M5 M7 M9 M11 49

51 Rating/Credit Opinion Nirmaan RMBS Trust - Series I Dewan Housing Finance Limited Series A1 PTCs - CARE AAA(SO) & Series A2 PTC - CARE AA (SO) Loan Against Property (LAP) Feb-14 CC as % of initial POS 14.5% Par FLF 80.2 SLF Series A1 Principal (Rs Cr) 77.0 LF as % of initial POS Average Maturity (Months) Average Seasoning' (Months) Series A2 Principal (subordinated to A1) (Rs Cr) EIS 42.0% 83.5 OC 4.0% 30.1 Pool Maturity Apr %, 0% Maturity (months) 266 Months Post Securitisation Pool Amortisation % % Amortisation (Series A1 Principal) 79.8% 78.8% Amortisation (Series A2 Principal) 79.8% 78.8% 90+ (% of Initial POS) 2.1% 180+ (% of Initial POS) 2.1% 90+ (% of Balance POS) 7.7% 180+ (% of Balance POS) 7.7% Amt (% of Initial POS) 0.2% 0.6% CC as % of Balance POS 71.7% 68.2% FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) % Balance FLF (unutilized) Balance LF (unutilized) 100.4% 98.3% (3 month average) 127.6% 93.9% Break even 42.9% 45.6% Break even (FLF) Overall enhancement coverage (90+ DPD) 7.1 Overall enhancement coverage (180+ DPD) 7.1 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 69.6% 69.0% 5.0% 90+ dpd 180+ dpd 200% 4.0% 3.0% 2.0% 1.0% M1 M7 M13 M19 M25 M31 M37 M43 150% 100% 50% 0% M1 M7 M13 M19 M25 M31 M37 M43 50

52 Equitas Small Finance Bank Limited (2 Pool) Key Financial Indicators For the year ended as on 31st March 2015 * 2016 * 2017 * (12m, A) (12m, A) (12m, A) Total Income (in Rs. Cr) 749 1,115 1,557 Profit After Tax (in Rs. Cr) Tangible Net worth (in Rs. Cr) 1,248 1,341 2,231 Gross NPA ratio (%) P=Provisional, A=Audited *includes financials of the wholly owned subsidiaries (EFL, EMFL, EHL & Equitas Technologies Private Limited [ETPL]). The gross NPA level has increased from 1.34% as of 31 st March, 2016 (30+ DPD for EMFL & 150+ DPD for EFL) to 3.54% as of 31 st March The reported PAT in FY16 was Rs. 167crores, while in FY17 it was Rs.159 crores. In FY16 the reported Total Income for the company was Rs. 1,115crores, while in FY17 it was Rs. 1,557crores. 51

53 Rating/Credit Opinion EMF Microloans Pool Series X - March 2016 Equitas Small Finance Bank Ltd. (Erstwhile Equitas Microfinance Private Limited) Withdrawn Microfinance Loans Average Maturity (Months) Average Seasoning' (Months) Mar-16 CC as % of initial POS 1 Par First Loss Credit Facility 80.0 Second Loss Credit 93.1 LF as % of initial POS 68,740 EIS 10.6% 8.0 OC 8.5 Pool Maturity Dec-17 NIL Maturity (months) 22 Pool Performance Jun-17 Jun-17 Months Post Securitisation Balance Tenure (Months) 6 7 Pool Amortisation 91.4% 88.9% 30+ (% of Initial POS) 0.6% 0.6% 90+ (% of Initial POS) 0.5% 0.5% 30+ (% of Balance POS) 2.1% 1.9% 90+ (% of Balance POS) 1.4% 1.3% Amt (% of Initial POS) 0.4% 0.4% CC as % of Balance POS 116.4% 90.3% CC as % of Balance PTC Principal 116.4% 90.3% Balance CC (unutilized) % 99.59% (3 month average) 98.2% 98.3% Break even 8.5% Overall enhancement coverage (30+ DPD) >30 Overall enhancement coverage (90+ DPD) >30 Cumulative Prepayment 8.2% 7.9% 30+DPD 90+DPD 2.0% 1.0% M1 M3 M5 M7 M9 M11 M13 M M1 M3 M5 M7 M9 M11 M13 M15 52

54 Rating Despina CV IFMR Capital 2016 Equitas Small Finance Bank Ltd. (Erstwhile Equitas Finance Limited) Series A1 PTC - CARE AAA (SO) and Series A2 PTC - CARE AAA (SO) CV (100%) Aug-16 CC as % of initial POS 6.9% Par First Loss Credit Facility Second Loss Credit Facility Series A1 Principal (Rs Cr) LF as % of initial POS Series A2 Principal (subordinated to A1) (Rs Cr) ,257 EIS 10.9% Average Maturity (Weeks) 15.5 OC 8.0% Average Seasoning' (Weeks) 19.4 Pool Maturity Aug Maturity (months) 24 Months Post Securitisation Balance Tenure (Months) Pool Amortization 86.4% 75.6% Amortisation (Series A1 Principal) 94.1% 82.0% Amortisation (Series A2 Principal) 90+ (% of Initial POS) 1.6% 1.4% 180+ (% of Initial POS) 0.9% 0.6% 90+ (% of Balance POS) 4.7% 2.7% 180+ (% of Balance POS) 2.3% 0.9% Amt (% of Initial POS) 2.1% 2.0% CC as % of Balance POS 50.5% 28.0% FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 97.2% 96.9% (3 month average) 99.6% 100.4% Break even 4.3% 41.0% Break even (FLF) Overall enhancement coverage (90+ DPD) Overall enhancement coverage (180+ DPD) >30 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 24.2% 21.3% 5.0% 90+ dpd 180+ dpd 120% 4.0% 3.0% 2.0% 90% 60% 1.0% 30% M1 M3 M5 M7 M9 M11 M13 0% M1 M3 M5 M7 M9 M11 M13 53

55 ESAF Microfinance and Investments Pvt. Ltd. (EMFIPL 9 Pools) Key Financial Indicators For the year ended as on 31st March (12m, A) (12m, A) (12m, A) Total Income (in Rs. Cr) Profit After Tax (in Rs. Cr) Net worth (in Rs. Cr) Gross NPA Capital Adequacy Ratio (CAR) P*=Provisional, A=Audited Income of EMFIPL has increased by 58% Y-o-Y to Rs 318 crore backed by growth in AUM during the above period. Capital adequacy stood at 21.30% comprising of Tier-I capital of 16.70% as on March 31, Gross NPA ratio stood at 0.24% as on March 31,

56 Rating/Credit Opinion Series A Principal Average Maturity (Weeks) Average Seasoning' (Weeks) Cedar MFI Trust 25 ESAF Microfinance & Investments (P) Ltd Withdrawn Microfinance Loans Feb-16 CC as % of initial POS 5.0% Par First Loss Credit Facility Second Loss Credit Facility LF as % of initial POS EIS 10.5% 49,018 OC 4.5% Pool Maturity Oct Maturity (months) %, Pool Performance Aug-17 Jun-17 Months Post Securitisation Balance Tenure (Months) 4 6 Pool Amortised 91.9% 84.7% Series A PTC Amortised % 30+ (% of Initial POS) 4.5% 4.1% 90+ (% of Initial POS) 4.3% 3.7% 30+ (% of Balance POS) 29.5% 16.0% 90+ (% of Balance POS) 27.5% 14.1% Amt (% of Initial POS) 2.1% 1.7% CC as % of Balance POS 32.8% CC as % of Balance PTC Principal 52.7% Balance CC (unutilized) 10 Cummulative 97.1% 97.6% (3 month average) 90.8% 91.6% Break even 31.7% Overall enhancement coverage (30+ DPD) 4.3 Overall enhancement coverage (90+ DPD) 4.8 Cumulative Prepayment 6.3% 4.7% 6.0% 30+ dpd 90+ dpd Collection Efficiecny % 4.0% 80.00% 2.0% 50.00% M1 M4 M7 M10 M13 M % M1 M4 M7 M10 M13 M16 55

57 Rating/Credit Opinion Series A Principal Average Maturity (Weeks) Average Seasoning' (Weeks) Cedar MFI Trust 26 ESAF Microfinance & Investments (P) Ltd Withdrawn Microfinance Loans Mar-16 CC as % of initial POS 5.0% Par First Loss Credit Facility Second Loss Credit Facility LF as % of initial POS EIS 8.5% 78,697 OC 7.0% Pool Maturity Dec Maturity (months) %, Pool Performance Jul-17 Jun-17 Months Post Securitisation Balance Tenure (Months) 4 5 Pool Amortised 91.9% 89.7% Series A PTC Amortised 93.1% 90.9% 30+ (% of Initial POS) 2.7% 2.6% 90+ (% of Initial POS) 2.4% 2.2% 30+ (% of Balance POS) 19.9% 15.7% 90+ (% of Balance POS) 17.0% 12.9% Amt (% of Initial POS) 1.1% 1.0% CC as % of Balance POS 48.5% CC as % of Balance PTC Principal 58.9% Balance CC (unutilized) 10 Cummulative 98.4% 98.5% (3 month average) 91.4% 91.8% Break even 38.1% Overall enhancement coverage (30+ DPD) 3.9 Overall enhancement coverage (90+ DPD) 4.8 Cumulative Prepayment 6.4% 5.8% 3.0% 30+ dpd 90+ dpd Collection Efficiecny % 2.0% 80.00% 1.0% 50.00% M1 M4 M7 M10 M13 M % M1 M4 M7 M10 M13 M16 56

58 Rating/Credit Opinion Series A Principal Average Maturity (Weeks) Average Seasoning' (Weeks) Cedar MFI Trust 29 ESAF Microfinance & Investments (P) Ltd Series A PTC - CARE BBB (SO) Microfinance Loans Jun-16 CC as % of initial POS 4.2% Par FLF SLF LF as % of initial POS EIS 7.7% OC 5.0% Pool Maturity Mar Maturity (months) %, Months Post Securitisation Balance Tenure (Months) 6 9 Pool Amortised 77.1% 65.5% Series A PTC Amortised 83.3% 70.1% 30+ (% of Initial POS) 8.4% 7.8% 90+ (% of Initial POS) 7.8% 6.7% 30+ (% of Balance POS) 21.7% 15.0% 90+ (% of Balance POS) 19.7% 12.2% Amt (% of Initial POS) 3.4% 2.7% CC as % of Balance POS 18.4% 12.2% CC as % of Balance PTC Principal 26.5% 14.8% Balance CC (unutilized) Cummulative 93.3% 93.7% (3 month average) 90.7% 90.6% Break even 53.6% 71.2% Overall enhancement coverage (30+ DPD) Overall enhancement coverage (90+ DPD) Cumulative Prepayment 3.7% 2.3% 9.0% 30+ dpd 90+ dpd Collection Efficiecny % 6.0% 90.00% 3.0% 70.00% M1 M3 M5 M7 M9 M11 M13 M % M1 M3 M5 M7 M9 M11 M13 M15 57

59 Rating/Credit Opinion Series A Principal Average Maturity (Weeks) Average Seasoning' (Weeks) Cedar MFI Trust 31 ESAF Microfinance & Investments (P) Ltd Series A PTC - CARE BBB (SO) Microfinance Loans Jul-16 CC as % of initial POS 3.75% Par FLF SLF LF as % of initial POS EIS 10.1% OC 5.0% Pool Maturity Mar Maturity (months) %, Months Post Securitisation Balance Tenure (Months) 7 10 Pool Amortised 71.2% 60.6% Series A PTC Amortised 78.7% 66.5% 30+ (% of Initial POS) 13.0% 12.2% 90+ (% of Initial POS) 12.5% 11.1% 30+ (% of Balance POS) 26.2% 19.8% 90+ (% of Balance POS) 24.9% 17.5% Amt (% of Initial POS) 5.4% 4.4% CC as % of Balance POS 13.0% 9.5% CC as % of Balance PTC Principal 18.5% 11.8% Balance CC (unutilized) Cummulative 91.8% 92.4% (3 month average) 88.8% 87.7% Break even 64.5% 74.7% Overall enhancement coverage (30+ DPD) Overall enhancement coverage (90+ DPD) Cumulative Prepayment 2.0% 1.3% 16.0% 30+ dpd 90+ dpd Collection Efficiecny % 12.0% 8.0% 4.0% M1 M4 M7 M10 M % 70.00% 50.00% M1 M4 M7 M10 M13 58

60 Rating/Credit Opinion Series A Principal Average Maturity (Weeks) Average Seasoning' (Weeks) Cedar MFI Trust 32 ESAF Microfinance & Investments (P) Ltd Series A PTC - CARE BBB (SO) Microfinance Loans Jul-16 CC as % of initial POS 4.0% Par FLF SLF LF as % of initial POS EIS 10.3% OC 5.0% Pool Maturity Mar Maturity (months) %, Months Post Securitisation Balance Tenure (Months) 7 10 Pool Amortised 73.1% 60.6% Series A PTC Amortised 79.4% 65.1% 30+ (% of Initial POS) 5.1% 4.6% 90+ (% of Initial POS) 4.7% 3.8% 30+ (% of Balance POS) 11.9% 8.2% 90+ (% of Balance POS) 10.7% 6.4% Amt (% of Initial POS) 1.9% 1.4% CC as % of Balance POS 14.9% 10.1% CC as % of Balance PTC Principal 20.5% 12.1% Balance CC (unutilized) Cummulative 96.8% 97.2% (3 month average) 94.4% 94.2% Break even 63.1% 77.2% Overall enhancement coverage (30+ DPD) Overall enhancement coverage (90+ DPD) Cumulative Prepayment 3.5% 2.0% 6.0% 30+ dpd 90+ dpd Collection Efficiecny % 4.0% 90.00% 2.0% 70.00% M1 M3 M5 M7 M9 M11 M % M1 M3 M5 M7 M9 M11 M13 59

61 60

62 Rating/Credit Opinion Series A Principal Average Maturity (Weeks) Average Seasoning' (Weeks) Cedar MFI Trust 34 ESAF Microfinance & Investments (P) Ltd Series A PTC - CARE BBB (SO) Microfinance Loans Sep-16 CC as % of initial POS 3.75% Par FLF SLF LF as % of initial POS EIS 8.3% OC 5.0% Pool Maturity Jun Maturity (months) %, Months Post Securitisation 12 9 Balance Tenure (Months) 9 12 Pool Amortised 73.3% 64.3% Series A PTC Amortised 80.8% 71.0% 30+ (% of Initial POS) 11.0% 10.9% 90+ (% of Initial POS) 10.6% 9.5% 30+ (% of Balance POS) 23.3% 18.2% 90+ (% of Balance POS) 21.9% 15.4% Amt (% of Initial POS) 4.8% 4.5% CC as % of Balance POS 14.0% 10.5% CC as % of Balance PTC Principal 20.5% 13.6% Balance CC (unutilized) Cummulative 91.9% 91.9% (3 month average) 91.9% 88.0% Break even 59.6% 78.7% Overall enhancement coverage (30+ DPD) Overall enhancement coverage (90+ DPD) Cumulative Prepayment 2.6% 2.0% 12.0% 30+ dpd 90+ dpd Collection Efficiecny % 8.0% 90.00% 4.0% 70.00% M1 M3 M5 M7 M % M1 M3 M5 M7 M9 M11 61

63 Rating/Credit Opinion Series A Principal Average Maturity (Weeks) Average Seasoning' (Weeks) Cedar MFI Trust 35 ESAF Microfinance & Investments (P) Ltd Series A PTC - CARE BBB (SO) Microfinance Loans Oct-16 CC as % of initial POS 3.75% Par FLF SLF LF as % of initial POS EIS 8.55% OC 5.0% Pool Maturity Jul Maturity (months) %, Months Post Securitisation 11 8 Balance Tenure (Months) Pool Amortised 67.5% 54.5% Series A PTC Amortised 74.9% 60.8% 30+ (% of Initial POS) 11.1% 10.6% 90+ (% of Initial POS) 10.7% 9.2% 30+ (% of Balance POS) 19.1% 14.3% 90+ (% of Balance POS) 18.1% 12.1% Amt (% of Initial POS) 4.9% 4.2% CC as % of Balance POS 11.6% 8.2% CC as % of Balance PTC Principal 15.7% 10.1% Balance CC (unutilized) Cummulative 91.4% 91.4% (3 month average) 91.8% 89.1% Break even 65.6% 83.3% Overall enhancement coverage (30+ DPD) Overall enhancement coverage (90+ DPD) Cumulative Prepayment 2.7% 1.3% 12.0% 30+ dpd 90+ dpd Collection Efficiecny % 8.0% 90.00% 4.0% 70.00% M1 M4 M7 M % M1 M4 M7 M10 62

64 Rating/Credit Opinion Series A Principal Average Maturity (Months) Average Seasoning' (Months) Cedar MFI Trust 36 ESAF Microfinance & Investments (P) Ltd Series A PTC - CARE BBB (SO) Microfinance Loans Feb-17 CC as % of initial POS 4.50% Par FLF SLF LF as % of initial POS EIS 8.7% OC 5.0% Pool Maturity Dec Maturity (months) %, Months Post Securitisation 8 5 Balance Tenure (Months) Pool Amortised 61.1% 38.0% Series A PTC Amortised 65.1% 40.8% 30+ (% of Initial POS) 0.7% 0.4% 90+ (% of Initial POS) 0.5% 0.2% 30+ (% of Balance POS) 1.0% 0.5% 90+ (% of Balance POS) 0.8% 0.2% Amt (% of Initial POS) 0.3% 0.1% CC as % of Balance POS 11.6% 7.3% CC as % of Balance PTC Principal 13.6% 8.0% Balance CC (unutilized) Cummulative 99.4% 99.5% (3 month average) 99.2% 99.4% Break even 69.4% 79.2% Overall enhancement coverage (30+ DPD) 29.8 >30 Overall enhancement coverage (90+ DPD) >30 >30 Cumulative Prepayment 2.8% 0.5% 1.0% 30+ dpd 90+ dpd Collection Efficiecny % 90.00% 0.5% 70.00% M1 M3 M5 M % M1 M3 M5 M7 63

65 HDFC Ltd 9 (Pools) Key Financial Indicators For the year ended as on 31st March (12m, A) (12m, A) (12m, A) Total Income (in Rs. Cr) 27,471 30,957 33,160 Profit After Tax (in Rs. Cr) 5,990 7, Net worth (in Rs. Cr) 30,970 34,121 39,645 Gross NPA (%) Capital Adequacy Ratio (CAR) (%) P*=Provisional, A=Audited As on 31 st March 2017 the Total Income was Rs. 33,160crores. HDFC reported Gross NPA ratio of 0.79% as on March 31, HDFC reported Capital Adequacy Ratio (CAR) of 14.50% (Tier I CAR: 11.80%) as on March 31,

66 Rating/Credit Opinion HDFC's Assignment of Receivables of Mar' 09 HDFC Limited Assignee Payout - CARE AAA (SO) Equivalent Second Loss Facility - AA+ (SO) Equivalent Housing Loan Average Maturity (Months) Average Seasoning' (Months) Mar-09 CC as % of initial POS 7.5% Par FLF 2.5% SLF 5.0% LF as % of initial POS 14,764 EIS 25.9% 94.0 OC Nil 19.2 Pool Maturity Feb %, 16.4% Maturity (months) 299 Months Post Securitisation Amortisation 86.5% 85.4% 90+ (% of Initial POS) 0.4% 0.4% 180+ (% of Initial POS) 0.2% 0.2% 90+ (% of Balance POS) 2.0% 2.1% 180+ (% of Balance POS) 1.0% 1.0% Amt (% of Initial POS) 0.2% 0.2% CC as % of Balance POS 55.4% 51.5% FLF as % of Balance POS 18.5% 17.2% LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.8% 99.8% (3 month average) 100.7% 100.7% Break even 53.3% 56.4% Break even (FLF) 79.7% 80.7% Overall enhancement coverage (90+ DPD) Overall enhancement coverage (180+ DPD) >30 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 49.6% 49.2% 1.0% 0.5% M1 90+ dpd 180+ dpd M13 M25 M37 M49 M61 M73 M85 M M1 M13 M25 M37 M49 M61 M73 M85 M97 65

67 Rating/Credit Opinion HDFC's Assignment of Receivables of May' 09-I HDFC Limited Assignee Payout - CARE AAA (SO) Equivalent Second Loss Facility - AA+ (SO) Equivalent Housing Loan Average Maturity (Months) Average Seasoning' (Months) May-09 CC as % of initial POS 12.0% Par FLF 5.5% SLF 6.5% LF as % of initial POS 3,945 EIS 11.2% 89.3 OC Nil 2.4 Pool Maturity Jan %,4.4%,0.3% Maturity (months) 248 Months Post Securitisation Amortisation 79.4% 78.0% 90+ (% of Initial POS) 0.7% 0.7% 180+ (% of Initial POS) 0.3% 0.2% 90+ (% of Balance POS) 3.0% 2.6% 180+ (% of Balance POS) 1.2% 0.7% Amt (% of Initial POS) 0.2% 0.2% CC as % of Balance POS 58.2% 54.7% FLF as % of Balance POS 26.6% 25.0% LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.7% 99.7% (3 month average) 98.7% 101.1% Break even 56.2% 59.0% Break even (FLF) 77.8% 79.0% Overall enhancement coverage (90+ DPD) Overall enhancement coverage (180+ DPD) >30 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 44.2% 43.7% 1.5% 1.0% 0.5% M1 90+ dpd 180+ dpd M13 M25 M37 M49 M61 M73 M85 M M1 M13 M25 M37 M49 M61 M73 M85 M97 66

68 Rating/Credit Opinion HDFC's Assignment of Receivables of May' 09-II HDFC Limited Assignee Payout - CARE AAA (SO) Equivalent Second Loss Facility - AAA (SO) Equivalent Housing Loan Average Maturity (Months) Average Seasoning' (Months) May-09 CC as % of initial POS 1 Par FLF 4.3% SLF 5.8% LF as % of initial POS 3,384 EIS 12.4% 95.4 OC Nil 7.4 Pool Maturity Nov %,3.8%,0.3% Maturity (months) 294 Months Post Securitisation Amortisation 84.9% 83.8% 90+ (% of Initial POS) 0.5% 0.5% 180+ (% of Initial POS) 0.4% 0.4% 90+ (% of Balance POS) 2.7% 2.2% 180+ (% of Balance POS) 1.5% 1.5% Amt (% of Initial POS) 0.3% 0.3% CC as % of Balance POS 66.5% 61.9% FLF as % of Balance POS 28.3% 26.3% LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.7% 99.7% (3 month average) 99.5% 99.2% Break even 49.4% 53.0% Break even (FLF) 76.3% 77.8% Overall enhancement coverage (90+ DPD) Overall enhancement coverage (180+ DPD) >30 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 54.6% 54.2% 1.0% 90+ dpd 180+ dpd %

69 Rating/Credit Opinion HDFC's Assignment of Receivables of Dec' 09-I HDFC Limited Assignee Payout - CARE AAA (SO) Equivalent Second Loss Facility - AA+ (SO) Equivalent Housing Loan Average Maturity (Months) Average Seasoning' (Months) Dec-09 CC as % of initial POS 12.9% Par FLF 5.7% SLF 7.2% LF as % of initial POS 3,243 EIS 9.8% 84.6 OC Nil 8.3 Pool Maturity Sep %, 0.2% Maturity (months) 240 Months Post Securitisation Amortisation 78.2% 76.9% 90+ (% of Initial POS) 0.7% 0.7% 180+ (% of Initial POS) 0.3% 0.4% 90+ (% of Balance POS) 2.5% 2.5% 180+ (% of Balance POS) 1.2% 1.2% Amt (% of Initial POS) 0.2% 0.2% CC as % of Balance POS 59.3% 55.8% FLF as % of Balance POS 26.4% 24.9% LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) % (3 month average) 100.8% 99.8% Break even 56.0% 58.8% Break even (FLF) 78.6% 79.9% Overall enhancement coverage (90+ DPD) Overall enhancement coverage (180+ DPD) >30 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 43.6% 43.1% 1.0% 0.5% 90+ dpd 180+ dpd M1 M11 M21 M31 M41 M51 M61 M71 M81 M M1 M11M21M31M41M51M61M71M81M91 68

70 Rating/Credit Opinion HDFC's Assignment of Receivables of Dec' 09-II HDFC Limited Assignee Payout - CARE AAA (SO) Equivalent Second Loss Facility - AAA (SO) Equivalent Housing Loan Average Maturity (Months) Average Seasoning' (Months) Dec-09 CC as % of initial POS 9.8% Par FLF 3.7% SLF 6.1% LF as % of initial POS 13,248 EIS 14.5% 76.4 OC Nil 36.2 Pool Maturity Aug %, 0.3% Maturity (months) 251 Months Post Securitisation Amortisation 84.9% 83.7% 90+ (% of Initial POS) 0.3% 0.3% 180+ (% of Initial POS) 0.1% 0.2% 90+ (% of Balance POS) 1.5% 1.7% 180+ (% of Balance POS) 0.7% 0.7% Amt (% of Initial POS) 0.1% 0.2% CC as % of Balance POS 64.5% 59.7% FLF as % of Balance POS 24.8% 23.0% LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.8% 99.8% (3 month average) 101.4% 100.8% Break even 48.4% 52.2% Break even (FLF) 77.3% 78.7% Overall enhancement coverage (90+ DPD) Overall enhancement coverage (180+ DPD) 71.9 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) 31.6 >30 Cumulative Prepayment 46.5% 46.1% 1.0% 0.5% 90+ dpd 180+ dpd M1 M11 M21 M31 M41 M51 M61 M71 M81 M M1 M11M21M31M41M51M61M71M81M91 69

71 Rating/Credit Opinion HDFC Direct Assignment Oct' 10-I HDFC Limited Assignee Payout - CARE AAA (SO) Equivalent Second Loss Facility - A+ (SO) Equivalent Housing Loan Average Maturity (Months) Average Seasoning' (Months) Nov-10 CC as % of initial POS 10.5% Par FLF 4.2% SLF 6.3% LF as % of initial POS 2,982 EIS 12.0% 97.7 OC Nil 2.3 Pool Maturity Aug %, 8.2%, 0.1% Maturity (months) 238 Months Post Securitisation Amortisation 63.6% 61.6% 90+ (% of Initial POS) 0.6% 0.6% 180+ (% of Initial POS) 0.3% 90+ (% of Balance POS) 1.4% 180+ (% of Balance POS) 0.7% Amt (% of Initial POS) 0.2% CC as % of Balance POS 28.8% FLF as % of Balance POS 11.5% LF as % of Balance POS Balance CC (unutilized) 10 Balance FLF (unutilized) 10 Balance LF (unutilized) 99.9% (3 month average) 101.0% Break even 76.3% Break even (FLF) 88.0% Overall enhancement coverage (90+ DPD) 16.6 Overall enhancement coverage (180+ DPD) >30 FL enhancement Coverage (90+ DPD) 8.4 FL enhancement Coverage (180+ DPD) Cumulative Prepayment 36.5% 0.3% 1.3% 0.6% 0.2% 27.3% 10.9% % 100.7% 77.5% 88.4% 17.8 > % 3.0% 90+ dpd 180+ dpd % % 8 M1 M16 M31 M46 M61 M76 6 M1 M16 M31 M46 M61 M76 70

72 Rating/Credit Opinion HDFC Direct Assignment Oct' 10-II HDFC Limited Assignee Payout - CARE AAA (SO) Equivalent Second Loss Facility - A+ (SO) Equivalent Housing Loan Average Maturity (Months) Average Seasoning' (Months) Nov-10 CC as % of initial POS 10.5% Par FLF 4.2% SLF 6.3% LF as % of initial POS 9,974 EIS 12.0% 95.4 OC Nil 1.1 Pool Maturity Aug %, 8.6% Maturity (months) 238 Months Post Securitisation Amortisation 69.6% 67.9% 90+ (% of Initial POS) 0.6% 0.7% 180+ (% of Initial POS) 0.3% 0.3% 90+ (% of Balance POS) 1.7% 1.8% 180+ (% of Balance POS) 0.7% 0.6% Amt (% of Initial POS) 0.2% 0.2% CC as % of Balance POS 34.6% 32.7% FLF as % of Balance POS 13.8% 13.1% LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.8% 99.8% (3 month average) 101.5% 101.7% Break even 72.3% 73.9% Break even (FLF) 86.4% 87.0% Overall enhancement coverage (90+ DPD) Overall enhancement coverage (180+ DPD) >30 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 39.9% 39.1% 3.0% 2.0% 1.0% 90+ dpd 180+ dpd M1 M12 M23 M34 M45 M56 M67 M M1 M12 M23 M34 M45 M56 M67 M78 71

73 Rating/Credit Opinion HDFC Direct Assignment Sep' 11 HDFC Limited Assignee Payout - CARE AAA (SO) Equivalent Second Loss Facility - A+ (SO) Equivalent Housing Loan Average Maturity (Months) Average Seasoning' (Months) Sep-11 CC as % of initial POS 9.3% Par FLF 4.1% SLF 5.2% LF as % of initial POS 4,191 EIS 7.6% OC Nil 11.0 Pool Maturity Dec %,5.13%, 0.15% Maturity (months) 278 Months Post Securitisation Amortisation 61.9% 60.1% 90+ (% of Initial POS) 0.5% 0.5% 180+ (% of Initial POS) 0.2% 0.2% 90+ (% of Balance POS) 1.1% 1.0% 180+ (% of Balance POS) 0.4% 0.4% Amt (% of Initial POS) 0.2% 0.2% CC as % of Balance POS 24.4% 23.3% FLF as % of Balance POS 10.8% 10.3% LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 99.9% 99.9% (3 month average) 100.5% 98.5% Break even 81.3% 82.2% Break even (FLF) 90.3% 90.7% Overall enhancement coverage (90+ DPD) Overall enhancement coverage (180+ DPD) >30 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 37.5% 36.7% 3.0% 90+ dpd 180+ dpd % % 9 M1 M11 M21 M31 M41 M51 M61 M71 8 M1 M11 M21 M31 M41 M51 M61 M71 72

74 Rating/Credit Opinion HDFC Direct Assignment Oct' 11 HDFC Limited Assignee Payout - CARE AAA (SO) Equivalent Second Loss Facility - A+ (SO) Equivalent Housing Loan Average Maturity (Months) Average Seasoning' (Months) Oct-11 CC as % of initial POS 8.8% Par FLF 3.6% SLF 5.2% LF as % of initial POS 15,568 EIS 16.3% OC Nil 22.2 Pool Maturity Apr %,17.47%, 1.55% Maturity (months) 344 Months Post Securitisation Amortisation 67.7% 65.7% 90+ (% of Initial POS) 0.7% 0.7% 180+ (% of Initial POS) 0.3% 0.3% 90+ (% of Balance POS) 1.8% 1.9% 180+ (% of Balance POS) 0.8% 0.8% Amt (% of Initial POS) 0.2% 0.2% CC as % of Balance POS 27.5% 25.9% FLF as % of Balance POS 11.3% 10.6% LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) % 99.99% (3 month average) 100.5% 101.0% Break even 76.3% 77.8% Break even (FLF) 87.1% 87.7% Overall enhancement coverage (90+ DPD) Overall enhancement coverage (180+ DPD) > FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 39.2% 38.3% 3.0% 90+ dpd 180+ dpd 2.0% 1.0% M1 M11 M21 M31 M41 M51 M61 M M1 M11 M21 M31 M41 M51 M61 M71 73

75 Hinduja Leyland Finance Ltd (2 Pools) Key Financial Indicators For the year ended as on 31st March (12m, A) (12m, A) (12m, A) Total Income (in Rs. Cr) 814 1, Profit After Tax (in Rs. Cr) Net worth (in Rs. Cr) 917 1, Gross NPA (%) Capital Adequacy Ratio (CAR) P*=Provisional, A=Audited During FY17, HLF registered 29.67% growth in total income driven by strong growth in AUM. Gross NPA increased from Rs.3.48% on March 31, 2016 to 5.45% as on March 31, HLF has maintained capital adequacy above the NBFC s regulatory requirement. HLF reported CAR of 16.20% as on March 31, 2017 as compared to 16.19% as on March 31,

76 Rating/Credit Opinion Aeries CV Trust March 2015 Hinduja Leyland Finance Ltd. Series A PTCs - CARE AAA (SO) MHCV (48.24%),SCV (20.12%),LCV(8.31%),Tractor(8.16%),Others (15.19%) Average Maturity (Months) Average Seasoning' (Months) Mar-15 CC as % of initial POS 14.0% Par FLF SLF LF as % of initial POS 4,682 EIS 7.2% 16.0 OC 14.2 Pool Maturity Mar %, 0.95% Maturity (months) 48 Months Post Securitisation Balance Tenure (Months) Amortisation 91.8% 87.1% 90+ (% of Initial POS) 0.2% 0.2% 180+ (% of Initial POS) 0.2% 0.2% 90+ (% of Balance POS) 0.5% 0.3% 180+ (% of Balance POS) 0.5% 0.3% Amt (% of Initial POS) 2.1% 2.4% CC as % of Balance POS 170.6% 108.6% FLF as % of Balance POS LF as % of Balance POS Balance CC (unutilized) Balance FLF (unutilized) Balance LF (unutilized) 97.3% 97.0% (3 month average) 102.1% 102.6% Break even Break even (FLF) Overall enhancement coverage (90+ DPD) >30 >30 Overall enhancement coverage (180+ DPD) >30 >30 FL enhancement Coverage (90+ DPD) FL enhancement Coverage (180+ DPD) Cumulative Prepayment 23.5% 22.6% 90+ dpd 180+ dpd 4.0% 3.0% 2.0% 1.0% M1 M7 M13 M19 M M1 M7 M13 M19 M24 75