Business Outlook for ASEAN Country 2017 Thailand Insurance Symposium December 2016 Bangkok, Thailand. Clarence Wong Chief Economist Asia

|

|

|

- Clement Haynes

- 6 years ago

- Views:

Transcription

1 Business Outlook for ASEAN Country 2017 Thailand Insurance Symposium December 2016 Bangkok, Thailand Clarence Wong Chief Economist Asia

2 Agenda What are our top economic concerns? What does this mean to ASEAN? What will be the key insurance themes for ASEAN countries? 2

3 What are our top economic concerns? 3

4 Top economic risk map that could impact ASEAN Recession in the Euro area: Risks of policy errors, reform complacency, renewed conflicts in Ukraine, geopolitical risks and slowdown in China 20% Sharp growth slowdown in advanced markets due to fallout from Brexit, downside risks in emerging markets and political conflicts 15% 10% Oil price collapse a stabilising force Emerging market Contagion: risks include Fed normalisation, high external debts, low commodity prices etc 15% Medium-term inflation risks 15% 20% Chinese hard landing: Credit risks from a significant slowdown in the property sector are the greatest downside risk Source: Swiss Re Economic Research & Consulting 4

5 Ultra-low monetary policy continues in most advanced markets Central bank rates, monthly data EU United Kingdom United States Weak growth and downside risks are nudging central bankers to keep interest rates lower for longer The scale of negative policy rates has expanded (Euro Area, Denmark, Japan, Sweden and Switzerland) to represent nearly 25% of global GDP Half of the world s sovereign bonds carry negative interest rates* Note: Updated on 28/09/2016 Source: CEIC Interest rate risk * refers to bonds in the S&P Global Developed Sovereign Bond Index 5

6 Strong economic headwinds facing ASEAN Weak trade activities The expected recovery in trade has been slow and unsteady. This could reflect changes in the global value chain, weaker demand from emerging markets and low supply of credit. High debt leverage Economic growth in recent years has been supported by higher debt, both for households and corporations Against the backdrop of slowing trade/economic growth, rising interest rates, debt servicing will become more challenging Fed lift-off Pace has remained cautious due to heightened uncertainty over global economic outlook. Fed tightening will result in capital outflows from Asia and increased financial volatility. China hard-landing China is in the process of going through complex economic adjustments resulting in slower growth. Key concerns include policy errors, mis-communication, systemic financial risks and conflicting objectives. 6 6

7 ASEAN has maintained ~5% growth since financial crisis 6.1% Average real GDP growth rate 5.1% 5.6% 6.6% 5.6% 6.1% 6.6% 4.7% 2.7% Financial Crisis 5.4% 5.3% 7.9% 4.9% 5.9% 5.0% 4.5% 1.8% 4.5% 4.5% Source: Swiss Re Economic Research & Consulting 7

8 but on the back of rising leverage 400% Credit to non-financial sector as % of GDP 300% 200% 100% 0% Japan Hong Kong China Singapore Korea Malaysia Thailand India Indonesia Source: BIS, Swiss Re Economic Research & Consulting

9 Government deficit and leverage have also increased since the GFC 0% Government deficit as % of GDP 120% Government leverage: credit to general government sector as % of GDP 90% -2% 60% -4% 30% -6% 0% Vietnam Myanmar Malaysia Indonesia Thailand Laos Cambodia Philippines Singapore Singapore Philippines Malaysia Thailand Indonesia Source: Oxford Economics, BIS, Swiss Re Economic Research & Consulting 9

10 What does this mean to ASEAN? 10

11 Interest and coupon payments are rising faster than corporate and household income 25% Debt service ratios of private non-financial sector 20% 15% 10% 5% 0% Hong Kong Korea China Japan Malaysia Thailand India Indonesia Source: Bank for International Settlement 11

12 Sensitivity of ASEAN to China trade channel ASEAN-5 China trade exposure* 350, , , , , , , USD million (LHS) Share of total trade (%, RHS) Note: *includes Indonesia, Malaysia, Philippines, Singapore and Thailand Source: CEIC 12

13 Sensitivity of ASEAN to China trade and other channels China has more impact on ASEAN exports than the US and EU (except for the Philippines) a 1ppt rise in growth in China will result in ppt increase in ASEAN exports Channels of Spillovers from a Slowdown in China but ASEAN is still relatively less exposed to China compared to other Asian countries Note: AUS = Australia; IND = India; IDN = Indonesia, JPN = Japan; KOR = Korea; MYS = Malaysia; NZL = New Zealand; PHL = the Philippines; SGP = Singapore; THA = Thailand; TWN = Taiwan Province of China; VNM = Vietnam. Source: IMF 13

14 Limited contribution to growth from trade 8 Contribution to real GDP growth in ASEAN-5 markets (2) H2016 Net exports Domestic demand Source: CEIC, Swiss Re Economic Research & Consulting 14

15 Elevated financial volatility coincides with falling crude oil, commodity prices and USD strength 140 Crude oil, copper and USD indices (1 Jan 2013=100) 300 Bond and stock volatility indices (1 Jan 2013 = 100) Jan-2013 Jul-2013 Jan-2014 Jul-2014 Jan-2015 Jul-2015 Jan-2016 Jul-2016 Jan-2013 Jul-2013 Jan-2014 Jul-2014 Jan-2015 Jul-2015 Jan-2016 Jul-2016 Copper (LME) USD trade weighted index Crude oil (WTI) US treasury volatility index (MOVE) S&P volatility index (VIX) Source: Bloomberg, CEIC, Swiss Re Economic Research & Consulting 15

16 What will be the key insurance themes for ASEAN countries? 16

17 Insurance having gone through phases of development in Asia Phase 1: monopolistic market structure, entry barriers, price/product regulations Phase 2: liberalisation, deregulation and globalisation Phase 3: economic/income growth, solvency reforms, personal lines Nonlife premiums (USD b) Life & health premiums (USD b) International insurers entering EM Asia markets India opened insurance sector to private and foreign companies Global financial crisis 240 ASEAN Framework Agreement on Services signed in 1995 China entered WTO in Dec Asia financial crisis 0 40% Nonlife premiums real growth Life & health premiums real growth 20% 0% -20% Source: Swiss Re Economic Research & Consulting 17

18 Many emerging Asian markets have low insurance penetration but are poised to achieve fast growth 4% Early movers Middle market Growers Slow growth Non-life insurance penetration (premiums as a % of GDP) South Korea 3% Penetration growth South Africa Japan Morocco Thailand 2% Kenya China Malaysia Singapore Hong Kong Mozambique 1% Cote d Ivoire Brunei India Angola Vietnam Indonesia Ethiopia Ghana Philippines Cambodia Bangladesh Nigeria 0% GDP per capita in 1000 USD Income growth log scale Asia Middle East Africa Taiwan Source: Swiss Re Economic Research & Consulting. 18

19 Fundamentals remain strong middle income class and urbanisation 100% 80% The number of middle-income households is expected to rapidly increase in Asia Pacific, especially in India and China USD trillion Urbanisation-led infrastructure spending is expected to be the highest in China during (USD trillion) Commercial floor space construction Water & waste-water management Energy sector Transportation 60% 9 40% 20% 5 0% North America Europe Central & South America Asia Pacific Sub-Saharan Africa Middle East & North Africa 0 China India Indonesia Middle East & Africa Latin America Other Emerging markets Source: OECD, McKinsey Institute

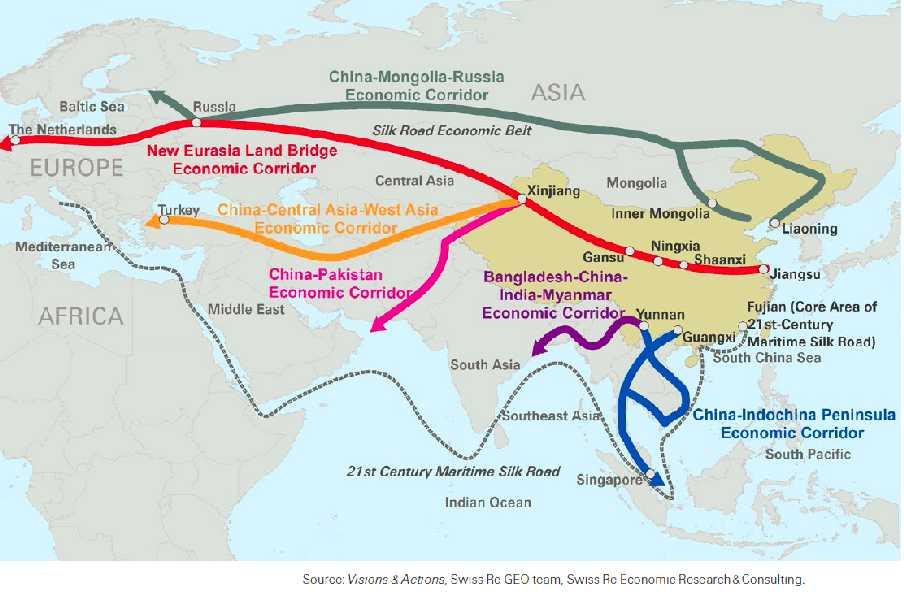

20 One-Belt-One-Road 20

21 Demographic changes and healthcare needs Old age support ratio (population aged over population aged 65+) Government funding and out-of-pocket expenditure are the main financing channels for healthcare expenditure % % % 6 40% % 0 Japan South Korea Singapore Hong Kong China Thailand Australia Vietnam Indonesia World Malaysia India Philippines 0% Government fund Social fund Private insurance out-of-pocket other private fund Source: WHO World Health Statistics, United Nations Population Division

22 Technologies will have an impact on the whole of society and thus shift risk pools and create new opportunities. World's largest transportation company owns no vehicles - Largest accommodation provider owns no real estate - Largest phone company owns no telco infra - World's most valuable retailer has no inventory - Most popular media owner creates no content - Fastest growing banks have no actual money - World's largest movie house owns no cinemas - Largest software vendors don't write the apps - What will be the insurance headline? Source: Tech Crunch, The Battle Is For The Customer Interface, Insurance and the Connected World, Strategy Meets Action

23 Digital Technology Adaption Curve Media Retail Telecom, Insurance and Banking Impact of digitalisation Energy Consumer Packaged Goods Automotive Logistics Health Care Data protection and privacy Are consumers comfortable with insurers access to information on usage/ behavior Non-traditional players are entering across the value chain Several major disruptions have occurred Point on digitalisation journey Disruptive moves (e.g. by pure online players) have affected these industries, but the final outcome is still to be determined Source: BCG, How to jump start a digital transformation, 2015 Effect of digitalisation is still unknown and disruptive changes remain to be seen; these industries are very similar in their overall level of digitalisation 23

24 In ASEAN, mortality protection gap increased by an annual average of 9% over the past decade to USD 3.5 trillion 350% 18% 250% 12% 150% 6% 50% 0% Vietnam Thailand Malaysia Singapore Philippines Indonesia ASEAN Mortality protection gap in 2014 (USD bn), LHS Avg annual increase in mortality protection gap ( ), RHS Note: mortality protection gap is defined as the difference between the protection needed (10x of average annual salary) and the protection in place (including net financial assets/savings and relevant life insurance) to maintain dependents in living standards following the death of the primary breadwinner. Source: Swiss Re Economic Research & Consulting 24

25 Uninsured Nat Cat losses have been particularly large in Thailand, Indonesia, Philippines and Myanmar Accumulative nat cat losses, USD bn ( ) Uninsured Nat Cat losses Insured Nat Cat losses Thailand Indonesia Philippines Myanmar Vietnam Malaysia Cambodia Laos Singapore (40) (30) (20) (10) Insured losses Uninsured losses Source: Swiss Re Economic Research & Consulting 25

26 ASEAN Economic Community ASEAN in 2030 AEC 1 could create USD280 bn to USD615 bn in annual economic value USD 7 trillion in infrastructure investment opportunities Consuming class 2 doubling to 163 mn households Urbanisation: More than 90 mn people are expected to move to cities 1. AEC stands for ASEAN Economic Community 2. Consuming class refers to those with income exceeding the level at which they can begin to make significant discretionary purchases. Source: Southeast Asia at the crossroads: Three path to prosperity, Nov 2014, Mckinsey&Company. 26

27 Concluding remarks Growth in ASEAN is increasingly constrained by 1) weak trade outlook; 2) limited room for further debt accumulation; and 3) already low interest rates Regional markets will nonetheless continue to pursue fiscal expansion to support growth Longer term, structural and economic reforms are key to success Regardless of when the Fed actually lifts off, the impact is already felt in ASEAN The next phase of growth deleveraging but not a financial crisis What these mean to the insurance industry? 27

28 28

29 Legal notice 2016 Swiss Re. All rights reserved. You are not permitted to create any modifications or derivative works of this presentation or to use it for commercial or other public purposes without the prior written permission of Swiss Re. The information and opinions contained in the presentation are provided as at the date of the presentation and are subject to change without notice. Although the information used was taken from reliable sources, Swiss Re does not accept any responsibility for the accuracy or comprehensiveness of the details given. All liability for the accuracy and completeness thereof or for any damage or loss resulting from the use of the information contained in this presentation is expressly excluded. Under no circumstances shall Swiss Re or its Group companies be liable for any financial or consequential loss relating to this presentation. 29

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund (percent YOY) 8 6 Real GDP Growth ASSUMPTIONS A more gradual monetary policy normalization 4 2 21 211 212

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund (percent YOY) 8 6 Real GDP Growth ASSUMPTIONS A more gradual monetary policy normalization 4 2 21 211 212

The Role of Insurance in Developing Markets. Frank O Neill CEO Africa & Middle East Swiss Re

The Role of Insurance in Developing Markets Frank O Neill CEO Africa & Middle East Swiss Re (Re)insurance enables entrepreneurial risk-taking Henry Ford, referring to New York City in the early 20th century:

The Role of Insurance in Developing Markets Frank O Neill CEO Africa & Middle East Swiss Re (Re)insurance enables entrepreneurial risk-taking Henry Ford, referring to New York City in the early 20th century:

Asia and the Pacific: Economic Outlook and Drivers

2018/FDM1/004 Session 2.1 Asia and the Pacific: Economic Outlook and Drivers Purpose: Information Submitted by: International Monetary Fund Finance and Central Bank Deputies Meeting Port Moresby, Papua

2018/FDM1/004 Session 2.1 Asia and the Pacific: Economic Outlook and Drivers Purpose: Information Submitted by: International Monetary Fund Finance and Central Bank Deputies Meeting Port Moresby, Papua

Global/Regional Economic and Financial Outlook. Odd Per Brekk Director IMF Regional Office for Asia and the Pacific APEC SFOM, June

Global/Regional Economic and Financial Outlook Odd Per Brekk Director IMF Regional Office for Asia and the Pacific APEC SFOM, June 11-12 2015 2015/SFOM13/002 Session: 1 Global/Regional Economic and Financial

Global/Regional Economic and Financial Outlook Odd Per Brekk Director IMF Regional Office for Asia and the Pacific APEC SFOM, June 11-12 2015 2015/SFOM13/002 Session: 1 Global/Regional Economic and Financial

2017 Asia and Pacific Regional Economic Outlook:

217 Asia and Pacific Regional Economic Outlook: Preparing for Choppy Seas Ranil Salgado International Monetary Fund Asia and Pacific Department May 12, 217 OAP Seminar Key messages and roadmap The near-term

217 Asia and Pacific Regional Economic Outlook: Preparing for Choppy Seas Ranil Salgado International Monetary Fund Asia and Pacific Department May 12, 217 OAP Seminar Key messages and roadmap The near-term

Indonesia Economic Outlook and Policy Challenges

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

Asia and the Pacific: Economic Outlook. PFTAC Steering Committee Meeting March 27, 2018 Suva, Fiji

Asia and the Pacific: Economic Outlook PFTAC Steering Committee Meeting March 27, 2018 Suva, Fiji 1 Growth in the region remains strong... Growth Projections: World and Selected Asia (Percent change from

Asia and the Pacific: Economic Outlook PFTAC Steering Committee Meeting March 27, 2018 Suva, Fiji 1 Growth in the region remains strong... Growth Projections: World and Selected Asia (Percent change from

WORLD ECONOMIC OUTLOOK October 2017

WORLD ECONOMIC OUTLOOK October 2017 Andreas Bauer Sr Resident Representative @imf_delhi World Economic Outlook The big picture Global activity picked up further in 2017H1 the outlook is now for higher

WORLD ECONOMIC OUTLOOK October 2017 Andreas Bauer Sr Resident Representative @imf_delhi World Economic Outlook The big picture Global activity picked up further in 2017H1 the outlook is now for higher

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 2009

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 29 Anoop Singh Asia and Pacific Department IMF 1 Five key questions

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 29 Anoop Singh Asia and Pacific Department IMF 1 Five key questions

Quarterly Economic Outlook: Quarter on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Economic Outlook and Risks in the APEC Region

2018/FMM/002 Agenda Item: 1.1 Economic Outlook and Risks in the APEC Region Purpose: Information Submitted by: ADB 25th Finance Ministers Meeting Port Moresby, Papua New Guinea 17 October 2018 Economic

2018/FMM/002 Agenda Item: 1.1 Economic Outlook and Risks in the APEC Region Purpose: Information Submitted by: ADB 25th Finance Ministers Meeting Port Moresby, Papua New Guinea 17 October 2018 Economic

Key Economic Challenges in Japan and Asia. Changyong Rhee IMF Asia and Pacific Department February

Key Economic Challenges in Japan and Asia Changyong Rhee IMF Asia and Pacific Department February 2017 1 Global and Asia Outlook 2 Global activity strengthening, with rising dispersion and uncertainty

Key Economic Challenges in Japan and Asia Changyong Rhee IMF Asia and Pacific Department February 2017 1 Global and Asia Outlook 2 Global activity strengthening, with rising dispersion and uncertainty

Asian Insights Third quarter 2016 Asia s commitment in policies and reforms

Asian Insights Third quarter 2016 Asia s commitment in policies and reforms One of the commonalities between most Asian governments is the dedicated commitment they have in using policies and initiatives

Asian Insights Third quarter 2016 Asia s commitment in policies and reforms One of the commonalities between most Asian governments is the dedicated commitment they have in using policies and initiatives

Global Equites declined from Concern over Trade War

Quarterly Market Outlook: Quarter 2 2018 on 3 April 2018 Global Equites declined from Concern over Trade War Investment Outlook for 2 nd Quarter 2018 Equity Thailand U.S. Europe Japan Asia Bond Thailand

Quarterly Market Outlook: Quarter 2 2018 on 3 April 2018 Global Equites declined from Concern over Trade War Investment Outlook for 2 nd Quarter 2018 Equity Thailand U.S. Europe Japan Asia Bond Thailand

B-GUIDE: Economic Outlook

Aug-12 Apr-13 Dec-13 Aug-14 Apr-15 Dec-15 Aug-16 Apr-17 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Quarterly Economic Outlook: Quarter 4 2017 4 January 2018 B-GUIDE: Economic Outlook The economy

Aug-12 Apr-13 Dec-13 Aug-14 Apr-15 Dec-15 Aug-16 Apr-17 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Quarterly Economic Outlook: Quarter 4 2017 4 January 2018 B-GUIDE: Economic Outlook The economy

ECONOMIC OUTLOOK FOR SOUTHEAST ASIA, CHINA AND INDIA 2018:

ECONOMIC OUTLOOK FOR SOUTHEAST ASIA, CHINA AND INDIA 2018: FOSTERING GROWTH THROUGH DIGITALISATION Kensuke Tanaka, Head of Asia Desk OECD Development Centre Asia-Pacific Business Forum, Hong Kong, China

ECONOMIC OUTLOOK FOR SOUTHEAST ASIA, CHINA AND INDIA 2018: FOSTERING GROWTH THROUGH DIGITALISATION Kensuke Tanaka, Head of Asia Desk OECD Development Centre Asia-Pacific Business Forum, Hong Kong, China

Indonesia Economic Quarterly: October 2012 Maintaining resilience

Indonesia Economic Quarterly: October 1 Maintaining resilience Ndiame Diop Lead Economist & Economic Advisor, Indonesia World Bank October 15, 1 Paramadina Public Policy Institute www.worldbank.org/id

Indonesia Economic Quarterly: October 1 Maintaining resilience Ndiame Diop Lead Economist & Economic Advisor, Indonesia World Bank October 15, 1 Paramadina Public Policy Institute www.worldbank.org/id

Asian Development Outlook 2017

1 Asian Development Outlook 2017 Transcending the Middle-Income Challenge Donghyun Park Principal Economist Asian Development Bank The views expressed in this document are those of the authors and do not

1 Asian Development Outlook 2017 Transcending the Middle-Income Challenge Donghyun Park Principal Economist Asian Development Bank The views expressed in this document are those of the authors and do not

Insurance data sources and data needs: Private-sector perspectives. Raymond Yeung, Swiss Re OECD-Asia Regional Seminar, September 23-24, Kuala Lumpur

Insurance data sources and data needs: Private-sector perspectives Raymond Yeung, Swiss Re OECD-Asia Regional Seminar, September 23-24, Kuala Lumpur Agenda About Swiss Re's sigma Applications of insurance

Insurance data sources and data needs: Private-sector perspectives Raymond Yeung, Swiss Re OECD-Asia Regional Seminar, September 23-24, Kuala Lumpur Agenda About Swiss Re's sigma Applications of insurance

Fed monetary policy amid a global backdrop of negative interest rates

Fed monetary policy amid a global backdrop of negative interest rates Kathy Bostjancic Head of US Macro Investor Services kathybostjancic@oxfordeconomics.com April 2016 Oxford Economics forecast highlights

Fed monetary policy amid a global backdrop of negative interest rates Kathy Bostjancic Head of US Macro Investor Services kathybostjancic@oxfordeconomics.com April 2016 Oxford Economics forecast highlights

Investment Theme 3Q18. Ageing Population. Source: AFP Photo

Investment Theme 3Q18 Ageing Population Source: AFP Photo 91 Investment Theme III: Ageing Population Jason Low, CFA Strategist The global population is growing older and people are living longer. Demographics

Investment Theme 3Q18 Ageing Population Source: AFP Photo 91 Investment Theme III: Ageing Population Jason Low, CFA Strategist The global population is growing older and people are living longer. Demographics

How Serious of a Threat Is Global Deflation?

How Serious of a Threat Is Global Deflation? Nariman Behravesh Farid Abolfathi John Mothersole Dan Ryan Todd Lee Howard Archer Global Insight Teleconference December 17, 22 199s: A Deflationary Wave The

How Serious of a Threat Is Global Deflation? Nariman Behravesh Farid Abolfathi John Mothersole Dan Ryan Todd Lee Howard Archer Global Insight Teleconference December 17, 22 199s: A Deflationary Wave The

AAPA Shifting Trade Patterns The Changing Asia Market

AAPA Shifting Trade Patterns The Changing Asia Market Today s objective Provide a 30,000 perspective on the Asian economy and its short-term outlook Focus on three topics 1. Economic growth 2. Trade growth

AAPA Shifting Trade Patterns The Changing Asia Market Today s objective Provide a 30,000 perspective on the Asian economy and its short-term outlook Focus on three topics 1. Economic growth 2. Trade growth

B-GUIDE: Market Outlook

Quarterly Market Outlook: Quarter 1 2018 on 5 th January 2018 Investment Outlook for 1 st Quarter 2018 Accelerating Global Economy Supports the Rising Earnings Equity Thailand US Europe Japan Asia Bond

Quarterly Market Outlook: Quarter 1 2018 on 5 th January 2018 Investment Outlook for 1 st Quarter 2018 Accelerating Global Economy Supports the Rising Earnings Equity Thailand US Europe Japan Asia Bond

Divergent Monetary Policy Implication for sub-saharan African Economies. By Sarah O. Alade Deputy Governor, Economic Policy Central Bank of Nigeria

Divergent Monetary Policy Implication for sub-saharan African Economies By Sarah O. Alade Deputy Governor, Economic Policy Central Bank of Nigeria Crisis background The recent financial crisis is one of

Divergent Monetary Policy Implication for sub-saharan African Economies By Sarah O. Alade Deputy Governor, Economic Policy Central Bank of Nigeria Crisis background The recent financial crisis is one of

Asian Development Outlook 2017 Update

Asian Development Outlook 217 Update Sustaining Development Through Public Private Partnership Yasuyuki Sawada Chief Economist Asian Development Bank EMBARGOED UNTIL 9:3 AM Manila/Hong Kong, China/Singapore

Asian Development Outlook 217 Update Sustaining Development Through Public Private Partnership Yasuyuki Sawada Chief Economist Asian Development Bank EMBARGOED UNTIL 9:3 AM Manila/Hong Kong, China/Singapore

The Medium to Long-Term Economic Outlook for Asia

The Medium to Long-Term Economic Outlook for Asia February 3, 2017 Yoko Takeda Mitsubishi Research Institute Copyright (C) Mitsubishi Research Institute, Inc. Issues for discussion for Asian Economy Copyright

The Medium to Long-Term Economic Outlook for Asia February 3, 2017 Yoko Takeda Mitsubishi Research Institute Copyright (C) Mitsubishi Research Institute, Inc. Issues for discussion for Asian Economy Copyright

ASIAN ECONOMIC INTEGRATION REPORT 2017

ASIAN ECONOMIC INTEGRATION REPORT 2017 THE ERA OF FINANCIAL INTERCONNECTEDNESS: HOW CAN ASIA STRENGTHEN FINANCIAL RESILIENCE? Cyn-Young Park Director of Regional Cooperation and Integration Economic Research

ASIAN ECONOMIC INTEGRATION REPORT 2017 THE ERA OF FINANCIAL INTERCONNECTEDNESS: HOW CAN ASIA STRENGTHEN FINANCIAL RESILIENCE? Cyn-Young Park Director of Regional Cooperation and Integration Economic Research

Asian Development Outlook 2016: Asia s Potential Growth

Asian Development Outlook 2016: Asia s Potential Growth Juzhong Zhuang Deputy Chief Economist Asian Development Bank Presentation at The views expressed in this document are those of the author and do

Asian Development Outlook 2016: Asia s Potential Growth Juzhong Zhuang Deputy Chief Economist Asian Development Bank Presentation at The views expressed in this document are those of the author and do

Emerging markets in the global crisis and beyond

Emerging markets in the global crisis and beyond May 5, 29 Maria Laura Lanzeni Head of Emerging Markets Think Tank of Deutsche Bank Group Agenda Emerging markets & BRICs as global players Impact of the

Emerging markets in the global crisis and beyond May 5, 29 Maria Laura Lanzeni Head of Emerging Markets Think Tank of Deutsche Bank Group Agenda Emerging markets & BRICs as global players Impact of the

FINANCE TO ENSURE ASIA S ECONOMIC GROWTH DR. RANEE JAYAMAHA CHAIRPERSON - HATTON NATIONAL BANK PLC

FINANCE TO ENSURE ASIA S ECONOMIC GROWTH DR. RANEE JAYAMAHA CHAIRPERSON - HATTON NATIONAL BANK PLC TABLE 1 : REAL GDP GROWTH OF SOUTHEAST ASIA, CHINA AND INDIA (ANNUAL PERCENTAGE CHANGE) PROJECTIONS ASEAN-6

FINANCE TO ENSURE ASIA S ECONOMIC GROWTH DR. RANEE JAYAMAHA CHAIRPERSON - HATTON NATIONAL BANK PLC TABLE 1 : REAL GDP GROWTH OF SOUTHEAST ASIA, CHINA AND INDIA (ANNUAL PERCENTAGE CHANGE) PROJECTIONS ASEAN-6

Asia and Europe require greater physical connectivity and the models for such

Why Do Asia and Europe Need More Connectivity? Some Ideas from the European and ASEAN Experience Alicia Garcia Herrero and Jianwei Xu, BRUEGEL Asia and Europe require greater physical connectivity and

Why Do Asia and Europe Need More Connectivity? Some Ideas from the European and ASEAN Experience Alicia Garcia Herrero and Jianwei Xu, BRUEGEL Asia and Europe require greater physical connectivity and

For More Efficient Tax Administration in Asia

For More Efficient Tax Administration in Asia Satoru Araki, Public Management Specialist (Taxation) Regional and Sustainable Development Department Asian Development Bank The 5th IMF-Japan High-Level Tax

For More Efficient Tax Administration in Asia Satoru Araki, Public Management Specialist (Taxation) Regional and Sustainable Development Department Asian Development Bank The 5th IMF-Japan High-Level Tax

Managing the capital of a re/insurance group today

Managing the capital of a re/insurance group today Michel M. Liès, Group CEO, Swiss Re ASTIN, AFIR/ ERM and IAALS Colloquia Mexico City, 1 October 2012 Trends 2 The world is getting richer and older (despite

Managing the capital of a re/insurance group today Michel M. Liès, Group CEO, Swiss Re ASTIN, AFIR/ ERM and IAALS Colloquia Mexico City, 1 October 2012 Trends 2 The world is getting richer and older (despite

A Global Economic and Market Outlook

A Global Economic and Market Outlook Presented by Dr Chris Caton December 2008 US Housing starts and Permits 2.3 (Millions) Permits Starts 2.1 1.9 1.7 1.5 1.3 1.1 0.9 0.7 96 97 98 99 00 01 02 03 04 05

A Global Economic and Market Outlook Presented by Dr Chris Caton December 2008 US Housing starts and Permits 2.3 (Millions) Permits Starts 2.1 1.9 1.7 1.5 1.3 1.1 0.9 0.7 96 97 98 99 00 01 02 03 04 05

Introduction to INDONESIA

Introduction to INDONESIA Indonesia is the fifth largest economy in Asia in nominal GDP terms and the third most populous nation behind China and India. It has recorded strong economic growth over the

Introduction to INDONESIA Indonesia is the fifth largest economy in Asia in nominal GDP terms and the third most populous nation behind China and India. It has recorded strong economic growth over the

Asia Key Economic and Financial Indicators 13-Jul-17

Asia Key Economic and Financial Indicators -Jul-7 ASEAN Brunei (BN) Cambodia (KH) Indonesia () Laos (LA) Malaysia () Myanmar (MM) Philippines () Singapore () Thailand () Vietnam () East Asia China (CN)

Asia Key Economic and Financial Indicators -Jul-7 ASEAN Brunei (BN) Cambodia (KH) Indonesia () Laos (LA) Malaysia () Myanmar (MM) Philippines () Singapore () Thailand () Vietnam () East Asia China (CN)

The effects of the financial crisis on developing countries mapping out the issues. By Julian Jessop

The effects of the financial crisis on developing countries mapping out the issues By Julian Jessop 1. Plan of My Talk The outlook for advanced economies. Impact on developing countries. Some losers and

The effects of the financial crisis on developing countries mapping out the issues By Julian Jessop 1. Plan of My Talk The outlook for advanced economies. Impact on developing countries. Some losers and

Introduction to PHILIPPINES

Introduction to PHILIPPINES With a population of about 100 million people, the Philippines, which comprises more than 7,000 islands, is the 12th most populous country in the world. An additional 12 million

Introduction to PHILIPPINES With a population of about 100 million people, the Philippines, which comprises more than 7,000 islands, is the 12th most populous country in the world. An additional 12 million

Economics. Market Insight Tuesday, 6 June, Malaysia Economy. Exports and Imports slowed down in April. Chart 1: Malaysia: External Trade

Market Insight Tuesday, 6 June, 2017 RM'bn Jan'10 Jan'11 Jan'12 Jan'13 Jan'14 Jan'15 Jan'16 Jan'17 % y-o-y Imran Nurginias Ibrahim imran@bimbsec.com.my PP16795/03/2013(031743) 03-26131733 www.bisonline.com

Market Insight Tuesday, 6 June, 2017 RM'bn Jan'10 Jan'11 Jan'12 Jan'13 Jan'14 Jan'15 Jan'16 Jan'17 % y-o-y Imran Nurginias Ibrahim imran@bimbsec.com.my PP16795/03/2013(031743) 03-26131733 www.bisonline.com

Developing Asia s Short-Run Economic Outlook and Main Risks

Developing Asia s Short-Run Economic Outlook and Main Risks Dr. Donghyun Park, Asian Development Bank Workshop on Bond Market Development in Emerging East Asia Raffles Hotel Le Royal Phnom Penh, Cambodia,

Developing Asia s Short-Run Economic Outlook and Main Risks Dr. Donghyun Park, Asian Development Bank Workshop on Bond Market Development in Emerging East Asia Raffles Hotel Le Royal Phnom Penh, Cambodia,

Sustaining Resilience, Expanding Opportunities for Inclusive Growth

1 Sustaining Resilience, Expanding Opportunities for Inclusive Growth Deputy Governor Diwa C. Guinigundo Bangko Sentral ng Pilipinas Source: Google images 2 PH emerges as growth leader in the ASEAN pack

1 Sustaining Resilience, Expanding Opportunities for Inclusive Growth Deputy Governor Diwa C. Guinigundo Bangko Sentral ng Pilipinas Source: Google images 2 PH emerges as growth leader in the ASEAN pack

Regional integration in Asia:

Regional integration in Asia: Trends and Issues Cyn-Young Park Director Economic Research and Regional Cooperation Department Asian Development Bank ADB-ASIAN THINK TANK DEVELOPMENT FORUM 2017: Financing

Regional integration in Asia: Trends and Issues Cyn-Young Park Director Economic Research and Regional Cooperation Department Asian Development Bank ADB-ASIAN THINK TANK DEVELOPMENT FORUM 2017: Financing

Asia Key Economic and Financial Indicators 20-Oct-16

Asia Key Economic and Financial Indicators -Oct- ASEAN Brunei (BN) Cambodia (KH) Indonesia () Laos (LA) Malaysia () Myanmar (MM) Philippines () Singapore () Thailand () Vietnam () East Asia China (CN)

Asia Key Economic and Financial Indicators -Oct- ASEAN Brunei (BN) Cambodia (KH) Indonesia () Laos (LA) Malaysia () Myanmar (MM) Philippines () Singapore () Thailand () Vietnam () East Asia China (CN)

Third Global Market Expansion Services Report Executive Summary

1 EMERGING MARKET PLAYERS ON THE RISE DISCOVER HOW MARKET EXPANSION SERVICES PROVIDERS HELP EMERGING MARKET PLAYERS DRIVE GROWTH, EXPANSION AND REGIONAL INTEGRATION Third Global Market Expansion Services

1 EMERGING MARKET PLAYERS ON THE RISE DISCOVER HOW MARKET EXPANSION SERVICES PROVIDERS HELP EMERGING MARKET PLAYERS DRIVE GROWTH, EXPANSION AND REGIONAL INTEGRATION Third Global Market Expansion Services

Asian Banking, Depositor Preference, and Deposit Insurance

Asian Banking, Depositor Preference, and Deposit Insurance Kevin Davis Professor of Finance, University of Melbourne Research Director, ACFS Professor, Monash University University of Melbourne 1 Summary

Asian Banking, Depositor Preference, and Deposit Insurance Kevin Davis Professor of Finance, University of Melbourne Research Director, ACFS Professor, Monash University University of Melbourne 1 Summary

SMSF Investment Seminar Sydney. 18 Oct 2010

SMSF Investment Seminar Sydney 18 Oct 2010 Important Notice This document has been prepared by Asian Masters Fund Limited (Asian Masters Fund). The material that follows is a presentation of general background

SMSF Investment Seminar Sydney 18 Oct 2010 Important Notice This document has been prepared by Asian Masters Fund Limited (Asian Masters Fund). The material that follows is a presentation of general background

Sovereign Risks and Financial Spillovers

Sovereign Risks and Financial Spillovers International Monetary Fund October 21 Roadmap What is the Outlook for Global Financial Stability? Sovereign Risks and Financial Fragilities Sovereign and Banking

Sovereign Risks and Financial Spillovers International Monetary Fund October 21 Roadmap What is the Outlook for Global Financial Stability? Sovereign Risks and Financial Fragilities Sovereign and Banking

Introduction to MALAYSIA

Introduction to MALAYSIA Malaysia is an upper-middle income, highly open economy with a record of strong economic performance and poverty reduction since independence from Great Britain in 1957. Malaysia

Introduction to MALAYSIA Malaysia is an upper-middle income, highly open economy with a record of strong economic performance and poverty reduction since independence from Great Britain in 1957. Malaysia

Global Economics Monthly Review

Global Economics Monthly Review January 8 th, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Please see important disclaimer on the last page of this report 1 Key Issues Global

Global Economics Monthly Review January 8 th, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Please see important disclaimer on the last page of this report 1 Key Issues Global

Understanding the Global ASEAN Consumer

Understanding the Global ASEAN Consumer The Philippines Millennials Roberto B. Tan Treasurer of the Philippines February 2015 ASEAN Offers a Future of Prosperity and Stability Combined GDP of nearly USD3tr

Understanding the Global ASEAN Consumer The Philippines Millennials Roberto B. Tan Treasurer of the Philippines February 2015 ASEAN Offers a Future of Prosperity and Stability Combined GDP of nearly USD3tr

Economic Indicators. Roland Berger Institute

Economic Indicators Roland Berger Institute October 2017 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Economic Indicators Roland Berger Institute October 2017 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Global growth weakening as some risks materialise

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

Global Risk Outlook May 2016

Global Risk Outlook May 2016 Scott Livermore Managing Director and COO slivermore@oxfordeconomics.com About Oxford Economics Oxford Economics is a world leader in global forecasting and quantitative analysis.

Global Risk Outlook May 2016 Scott Livermore Managing Director and COO slivermore@oxfordeconomics.com About Oxford Economics Oxford Economics is a world leader in global forecasting and quantitative analysis.

Taking ASEAN+1 FTAs towards the RCEP

Taking ASEAN+1 FTAs towards the RCEP Ikumo Isono Economist Economic Research Institute for ASEAN and East Asia (ERIA) October 30, 2013, S.C. Tsiang Memorial Hall, CIER, Taipei What is RCEP? New FTA negotiation

Taking ASEAN+1 FTAs towards the RCEP Ikumo Isono Economist Economic Research Institute for ASEAN and East Asia (ERIA) October 30, 2013, S.C. Tsiang Memorial Hall, CIER, Taipei What is RCEP? New FTA negotiation

East Asia-Pacific Economic Update Clearing skies

East Asia-Pacific Economic Update Clearing skies William E. Wallace Lead Economist World Bank 4 November 29 Jakarta Indonesia Indonesia through the global crisis Growth has been picking up After stalling

East Asia-Pacific Economic Update Clearing skies William E. Wallace Lead Economist World Bank 4 November 29 Jakarta Indonesia Indonesia through the global crisis Growth has been picking up After stalling

Global Economic Management and Asia s Responsibility Masahiro Kawai Asian Development Bank Institute

Global Economic Management and Asia s Responsibility Masahiro Kawai Asian Development Bank Institute PECC 18 th General Meeting Economic Crisis and Recovery: Roles for the Asia-Pacific Economies Washington,

Global Economic Management and Asia s Responsibility Masahiro Kawai Asian Development Bank Institute PECC 18 th General Meeting Economic Crisis and Recovery: Roles for the Asia-Pacific Economies Washington,

ASIAN ECONOMIES. Economics, interest rates and currencies chart pack

ASIAN ECONOMIES Economics, interest rates and currencies chart pack Amy Auster Senior Economist Melbourne 2 May 25 E-mail: austera@anz.com Internet: http://www.anz.com/go/economics 1 Major revisions to

ASIAN ECONOMIES Economics, interest rates and currencies chart pack Amy Auster Senior Economist Melbourne 2 May 25 E-mail: austera@anz.com Internet: http://www.anz.com/go/economics 1 Major revisions to

BTMU ASEAN TOPICS. YUMA TSUCHIYA ECONOMIC RESEARCH OFFICE SINGAPORE 23 JANUARY 2018

BTMU ASEAN TOPICS YUMA TSUCHIYA ECONOMIC RESEARCH OFFICE SINGAPORE yuma_tsuchiya@sg.mufg.jp 23 JANUARY 218 (ORIGINAL JAPANESE VERSION RELEASED ON 28 DECEMBER 217) The Bank of Tokyo-Mitsubishi UFJ, Ltd.

BTMU ASEAN TOPICS YUMA TSUCHIYA ECONOMIC RESEARCH OFFICE SINGAPORE yuma_tsuchiya@sg.mufg.jp 23 JANUARY 218 (ORIGINAL JAPANESE VERSION RELEASED ON 28 DECEMBER 217) The Bank of Tokyo-Mitsubishi UFJ, Ltd.

Near-term growth: moderating, but no imminent hard landing. Vulnerabilities are growing along the current growth path

1 Near-term growth: moderating, but no imminent hard landing Vulnerabilities are growing along the current growth path financial and structural reform must be accelerated to contain risks and transition

1 Near-term growth: moderating, but no imminent hard landing Vulnerabilities are growing along the current growth path financial and structural reform must be accelerated to contain risks and transition

ASEAN Snapshot. Special Coverage On Tourism May 2018 ASEAN ESTABLISHMENT ASEAN ECONOMIC PERFORMANCE ASEAN COUNTRIES DECLARED INDEPENDENCE

Snapshot Special Coverage On Tourism May 2018 The Association of Southeast Asian Nations () was established on 08 August 1967 in Bangkok,, with the signing of the Declaration. -10 was formed when the 10th

Snapshot Special Coverage On Tourism May 2018 The Association of Southeast Asian Nations () was established on 08 August 1967 in Bangkok,, with the signing of the Declaration. -10 was formed when the 10th

Emerging Markets Outlook

Mark Mobius, Ph.D. Executive Chairman Templeton Emerging Markets Group Emerging Markets Outlook Dealer Use Only / Not for Distribution to the Public Agenda Performance Emerging Markets Equities: Demand

Mark Mobius, Ph.D. Executive Chairman Templeton Emerging Markets Group Emerging Markets Outlook Dealer Use Only / Not for Distribution to the Public Agenda Performance Emerging Markets Equities: Demand

Japan-ASEAN Comprehensive Economic Partnership

Japan- Comprehensive Economic Partnership By Dr. Kitti Limskul 1. Introduction The economic cooperation between countries and Japan has been concentrated on trade, investment and official development assistance

Japan- Comprehensive Economic Partnership By Dr. Kitti Limskul 1. Introduction The economic cooperation between countries and Japan has been concentrated on trade, investment and official development assistance

Indonesia Economic Quarterly: December 2012 Policies in focus

Indonesia Economic Quarterly: December 212 Policies in focus Ndiame Diop Lead Economist & Economic Advisor, Indonesia World Bank December 18, 212 World Bank and The Habibie Center Joint Launch Event Intercontinental

Indonesia Economic Quarterly: December 212 Policies in focus Ndiame Diop Lead Economist & Economic Advisor, Indonesia World Bank December 18, 212 World Bank and The Habibie Center Joint Launch Event Intercontinental

How the emerging markets slowdown will impact listed Spanish companies

How the emerging markets slowdown will impact listed Spanish companies Nereida González, Pablo Guijarro and Diego Mendoza 1 Despite the favourable impact of recent international expansion by Spanish companies,

How the emerging markets slowdown will impact listed Spanish companies Nereida González, Pablo Guijarro and Diego Mendoza 1 Despite the favourable impact of recent international expansion by Spanish companies,

Indonesia Economic Quarterly, July 2014 Hard choices. Ndiamé Diop Lead Economist

Indonesia Economic Quarterly, July 214 Hard choices Ndiamé Diop Lead Economist The new administration will face major near-term challenges Fiscal pressures Economic growth Poverty and inequality reduction

Indonesia Economic Quarterly, July 214 Hard choices Ndiamé Diop Lead Economist The new administration will face major near-term challenges Fiscal pressures Economic growth Poverty and inequality reduction

Global Economic Indictors: CRB Raw Industrials & Global Economy

Global Economic Indictors: & Global Economy December 14, 2017 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box

Global Economic Indictors: & Global Economy December 14, 2017 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box

GLOBAL MARKET OUTLOOK

GLOBAL MARKET OUTLOOK Max Darnell, Managing Partner, Chief Investment Officer All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. performance is no

GLOBAL MARKET OUTLOOK Max Darnell, Managing Partner, Chief Investment Officer All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. performance is no

International Monetary Fund

International Monetary Fund World Economic Outlook Jörg Decressin Deputy Director Research Department, IMF April 212 Towards Lasting Stability Global Economy Pulled Back from the Brink Policies Stepped

International Monetary Fund World Economic Outlook Jörg Decressin Deputy Director Research Department, IMF April 212 Towards Lasting Stability Global Economy Pulled Back from the Brink Policies Stepped

The Global Landscape Focus on the U.S. and China

The Global Landscape Focus on the U.S. and China Ronald Temple, CFA Managing Director, Portfolio Manager/Analyst September 214 This presentation and all research and materials enclosed are property of

The Global Landscape Focus on the U.S. and China Ronald Temple, CFA Managing Director, Portfolio Manager/Analyst September 214 This presentation and all research and materials enclosed are property of

Strategies for Successful Business in Asia Fasico is proud to be a partner of

Strategies for Successful Business in Asia Fasico is proud to be a partner of Introduction to Fasico Established as a fully independent consulting firm, in position to support European companies in Asia.

Strategies for Successful Business in Asia Fasico is proud to be a partner of Introduction to Fasico Established as a fully independent consulting firm, in position to support European companies in Asia.

The Global Economy. RISI Asian Forest Products Summit 22 June, David Katsnelson Director, Macroeconomics

The Global Economy Heightened drisks RISI Asian Forest Products Summit 22 June, 2016 David Katsnelson Director, Macroeconomics Agenda 1. Global Snapshot A Two-Track World 2. China Slowing, Not Crashing

The Global Economy Heightened drisks RISI Asian Forest Products Summit 22 June, 2016 David Katsnelson Director, Macroeconomics Agenda 1. Global Snapshot A Two-Track World 2. China Slowing, Not Crashing

Korea and Australia in a globalised world

Korea and Australia in a globalised world November 7 Amy Auster Head of International Economics Economics@ANZ Globalisation is the structural change of our time 7,, 5,, 3,, 1, Global merchandise trade

Korea and Australia in a globalised world November 7 Amy Auster Head of International Economics Economics@ANZ Globalisation is the structural change of our time 7,, 5,, 3,, 1, Global merchandise trade

World Economic Trend, Spring 2006, No. 9

World Economic Trend, Spring, No. 9 Published on June 8 by the Cabinet Office Key Points of Chapter 1 (summary) 1. Global price stability: Global economy continues to show price stability and recovery

World Economic Trend, Spring, No. 9 Published on June 8 by the Cabinet Office Key Points of Chapter 1 (summary) 1. Global price stability: Global economy continues to show price stability and recovery

Standard Chartered Bank

Standard Chartered Bank Morgan Stanley Sixteenth Annual Asia Pacific Summit Anna Marrs Regional CEO, ASEAN & South Asia CEO, Commercial & Private Banking 0 Important Notice This document contains or incorporates

Standard Chartered Bank Morgan Stanley Sixteenth Annual Asia Pacific Summit Anna Marrs Regional CEO, ASEAN & South Asia CEO, Commercial & Private Banking 0 Important Notice This document contains or incorporates

Global Economic Prospects: Spillovers amid Weak Growth. Select Publications from DECPG

// Global Economic Prospects: Spillovers amid Weak Growth February M. Ayhan Kose Disclaimer! The views presented here are those of the authors and do NOT necessarily reflect the views and policies of the

// Global Economic Prospects: Spillovers amid Weak Growth February M. Ayhan Kose Disclaimer! The views presented here are those of the authors and do NOT necessarily reflect the views and policies of the

Key developments and outlook

1/17 Key developments and outlook Economic growths in 2016 and 2017 remain close to the previous assessment. Better-than-expected merchandise exports and private consumption compensate for weaker-than-expected

1/17 Key developments and outlook Economic growths in 2016 and 2017 remain close to the previous assessment. Better-than-expected merchandise exports and private consumption compensate for weaker-than-expected

Economic and Investment Review. Kelvin Blacklock and Nick Scott Prudential Corporation Asia November 2004

Economic and Investment Review Kelvin Blacklock and Nick Scott Prudential Corporation Asia November 24 24 Key messages Asia saves enormous amounts of capital and is fast becoming the world s provider of

Economic and Investment Review Kelvin Blacklock and Nick Scott Prudential Corporation Asia November 24 24 Key messages Asia saves enormous amounts of capital and is fast becoming the world s provider of

Presentation. Global Financial Crisis and the Asia-Pacific Economies: Lessons Learnt and Challenges Introduction of the Issues

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 211, Manila,

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 211, Manila,

The Evolving Role of Trade in Asia: Opening a New Chapter. Fall 2018 REO Background Paper

The Evolving Role of Trade in Asia: Opening a New Chapter Fall 2018 REO Background Paper Outline Trade Tensions and Spillovers: Spotlight on Asia Gains from Liberalization 2 Trade tensions have escalated.

The Evolving Role of Trade in Asia: Opening a New Chapter Fall 2018 REO Background Paper Outline Trade Tensions and Spillovers: Spotlight on Asia Gains from Liberalization 2 Trade tensions have escalated.

All the BRICs dampening world trade in 2015

Aug Weekly Economic Briefing Emerging Markets All the BRICs dampening world trade in World trade in has been hit by an unexpectedly sharp drag from the very largest emerging economies. The weakness in

Aug Weekly Economic Briefing Emerging Markets All the BRICs dampening world trade in World trade in has been hit by an unexpectedly sharp drag from the very largest emerging economies. The weakness in

Asian Insights What to watch closely in Asia in 2016

Asian Insights What to watch closely in Asia in 2016 Q1 2016 The past year turned out to be a year where one of the oldest investment adages came true: Sell in May and go away, don t come back until St.

Asian Insights What to watch closely in Asia in 2016 Q1 2016 The past year turned out to be a year where one of the oldest investment adages came true: Sell in May and go away, don t come back until St.

Restructuring of Malaysia s economy Post-GE14 International Factors and Perspectives Impacting Malaysia s 2019 Economic Outlook

Restructuring of Malaysia s economy Post-GE14 International Factors and Perspectives Impacting Malaysia s 2019 Economic Outlook Yeah Kim Leng Professor of Economics Sunway University Business School 24

Restructuring of Malaysia s economy Post-GE14 International Factors and Perspectives Impacting Malaysia s 2019 Economic Outlook Yeah Kim Leng Professor of Economics Sunway University Business School 24

Re: Consulting Canadians on a possible Canada-ASEAN Free Trade Agreement

October 16, 2018 Canada ASEAN trade consultations Global Affairs Canada Trade Policy and Negotiations Division (TCA) Lester B. Pearson Building 125 Sussex Drive Ottawa, Ontario K1A 0G2 Via email: CanadaASEAN-ANASE.Consultations@international.gc.ca

October 16, 2018 Canada ASEAN trade consultations Global Affairs Canada Trade Policy and Negotiations Division (TCA) Lester B. Pearson Building 125 Sussex Drive Ottawa, Ontario K1A 0G2 Via email: CanadaASEAN-ANASE.Consultations@international.gc.ca

Indonesia: Building on Resilience and Prospering Amid Global Economic Uncertainty

Indonesia: Building on Resilience and Prospering Amid Global Economic Uncertainty 2016 Article IV Consultation Report on Indonesia John G. Nelmes IMF Senior Resident Representative for Indonesia Academic

Indonesia: Building on Resilience and Prospering Amid Global Economic Uncertainty 2016 Article IV Consultation Report on Indonesia John G. Nelmes IMF Senior Resident Representative for Indonesia Academic

The Macro-Economic Outlook and the Challenges for the World

The Macro-Economic Outlook and the Challenges for the World Invest Save and Impact Seminar Singapore February 27, 2013 Brian Fabbri President Fabbri Global Economics Visiting Research Fellow, CAMRI, NUS

The Macro-Economic Outlook and the Challenges for the World Invest Save and Impact Seminar Singapore February 27, 2013 Brian Fabbri President Fabbri Global Economics Visiting Research Fellow, CAMRI, NUS

Market volatility to continue

How much more? Renewed speculation that financial institutions may report increased US subprime-related losses has sent equity markets tumbling. How much more bad news can investors expect going forward?

How much more? Renewed speculation that financial institutions may report increased US subprime-related losses has sent equity markets tumbling. How much more bad news can investors expect going forward?

TRADE FINANCE NEWSLETTER

JUNE 2013 TRADE FINANCE NEWSLETTER Dear Customer, Welcome to the first edition of our Trade Finance Newsletter. When we talk to our customers we understand that there is a need for a regular update on

JUNE 2013 TRADE FINANCE NEWSLETTER Dear Customer, Welcome to the first edition of our Trade Finance Newsletter. When we talk to our customers we understand that there is a need for a regular update on

2015 Market Review & Outlook. January 29, 2015

2015 Market Review & Outlook January 29, 2015 Economic Outlook Jason O. Jackman, CFA President & Chief Investment Officer Percentage Interest Rates Unexpectedly Decline 4.5 10-Year Government Yield 4 3.5

2015 Market Review & Outlook January 29, 2015 Economic Outlook Jason O. Jackman, CFA President & Chief Investment Officer Percentage Interest Rates Unexpectedly Decline 4.5 10-Year Government Yield 4 3.5

Growth has peaked amidst escalating risks

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

Charting Mexico s Economy

Charting Mexico s Economy Designed to help executives catch up with the economy and incorporate macro impacts into company s planning. Annual subscription includes 2 semiannual issues published in June

Charting Mexico s Economy Designed to help executives catch up with the economy and incorporate macro impacts into company s planning. Annual subscription includes 2 semiannual issues published in June

Southeast Asian Economic Outlook 2010

Southeast Asian Economic Outlook 2010 Kensuke Tanaka Project Manager and Economist OECD Development Centre Asia and Pacific Desk SAEO Presentation MPDD seminar series UNESCAP Januar 2011 Three regional

Southeast Asian Economic Outlook 2010 Kensuke Tanaka Project Manager and Economist OECD Development Centre Asia and Pacific Desk SAEO Presentation MPDD seminar series UNESCAP Januar 2011 Three regional

Global Economic Outlook John Hawksworth Chief Economist, PwC September 2012

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

www.pwc.co.uk/economics Global Economic Outlook John Hawksworth Chief Economist, September 2012 Agenda Global overview Short term prospects for Europe, US and BRICs Long term trends: demographics, growth

Emerging Markets Debt: Outlook for the Asset Class

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Global Economic Prospects: A Fragile Recovery. June M. Ayhan Kose Four Questions

//7 Global Economic Prospects: A Fragile Recovery June 7 M. Ayhan Kose akose@worldbank.org Four Questions How is the health of the global economy? Recovery underway, broadly as expected How important is

//7 Global Economic Prospects: A Fragile Recovery June 7 M. Ayhan Kose akose@worldbank.org Four Questions How is the health of the global economy? Recovery underway, broadly as expected How important is

Ravi Menon: The global economy in 2019

Ravi Menon: The global economy in 2019 Fireside chat remarks by Mr Ravi Menon, Managing Director of the Monetary Authority of Singapore, at Citibank's 16th Asia Pacific Investors Conference, Singapore,

Ravi Menon: The global economy in 2019 Fireside chat remarks by Mr Ravi Menon, Managing Director of the Monetary Authority of Singapore, at Citibank's 16th Asia Pacific Investors Conference, Singapore,

Asia Watch. The US giveth, the US taketh away. Group Economics Emerging Markets Research. Group Economics: Enabling smart decisions.

Asia Watch Group Economics Emerging Markets Research 1 June 18 Arjen van Dijkhuizen Senior Economist Tel: +31 68 85 arjen.van.dijkhuizen@nl.abnamro.com The US giveth, the US taketh away Growth momentum

Asia Watch Group Economics Emerging Markets Research 1 June 18 Arjen van Dijkhuizen Senior Economist Tel: +31 68 85 arjen.van.dijkhuizen@nl.abnamro.com The US giveth, the US taketh away Growth momentum

Global Economic Prospects

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO)

") Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO) Special Edition ASEAN+3 Macroeconomic Research Office (AMRO) Singapore January 2018 This Monthly Update of the AREO was prepared by the Regional

Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO) Special Edition ASEAN+3 Macroeconomic Research Office (AMRO) Singapore January 2018 This Monthly Update of the AREO was prepared by the Regional

Changing Economic Landscape and its impact on procurement and supply chains Jonathan Ravelas

Changing Economic Landscape and its impact on procurement and supply chains Jonathan Ravelas Presentation Outline I. World Economy II. Outlook on the Philippines III. Risks IV. Implications to Supply Chain/Procurement

Changing Economic Landscape and its impact on procurement and supply chains Jonathan Ravelas Presentation Outline I. World Economy II. Outlook on the Philippines III. Risks IV. Implications to Supply Chain/Procurement