Background. MUNICIPALITIES AND DOWNTOWN REDEVELOPMENT IN SOUTH CAROLINA: Expanding The Tool Kit

|

|

|

- Rosaline Patterson

- 5 years ago

- Views:

Transcription

geared toward infrastructure and")

1 MUNICIPALITIES AND DOWNTOWN REDEVELOPMENT IN SOUTH CAROLINA: Expanding The Tool Kit Background Over past 30 years, shift focus from remediation to development Need for commercially vibrant, historically distinctive downtowns Emphasis on quality of life, tourism, livability Existing governmental mechanisms (TIF districts; GO bonds; utility revenue bonds) geared toward infrastructure and context. Good for setting the table but not putting anything on it Need to develop product 1

2 Direct Government Product Libraries, museums, performing arts centers, parks, recreation facilities, as well as government facilities Some new mechanisms to drive these in addition to traditional tools (like GO bonds) include installment purchase revenue bonds, hospitality and accommodations bonds, new market tax credit financing. Development of collaborative and mixed use facilities Examples: Greenwood Arts Center; Francis Marion Performing Arts Center in Florence; Florence County Museum Greenwood Cultural Facility 1911 Federal Building Jointly redeveloped by City, County, Self Foundation with federal, state, local governmental and private funds. Total Cost of $1,750,000 20,118 square feet housing museum galleries, conference and recreational facilities, visitor and tourism center, foundation and arts council offices 2

3 Greenwood Federal Building/Cultural Facility Francis Marion University Performing Arts Center 64,000 square foot facility built on site of abandoned motel in downtown Florence Contains 850 seat main theater, 150 seat black box theater, University classroom and office space, nonprofit offices $30M project, jointly developed by FMU, City, County, and Drs. Bruce and Lee Foundation First FMU presence in City of Florence in the University s 40 year history 3

4 Francis Marion University Performing Arts Center Florence County Museum $12M, 28,000 square foot facility Jointly financed by County, State, and Drs. Bruce and Lee Foundation Partnership with existing 501(c)(3) Florence Museum County portion funded with hospitality fee revenue bond 4

5 Florence County Museum Incentivizing Private Investment Expanding tax base, creating jobs Not much in standard municipal tool kit in this regard Most direct investment incentives at County level and geared toward manufacturers A couple of tools that are available and that are driving projects in South Carolina Special source revenue credits (direct subsidy resulting in tax abatement with possibility of leverage) Federal and state rehabilitation tax credits (largely coordination and facilitation role with some possibility of subsidy through participation) 5

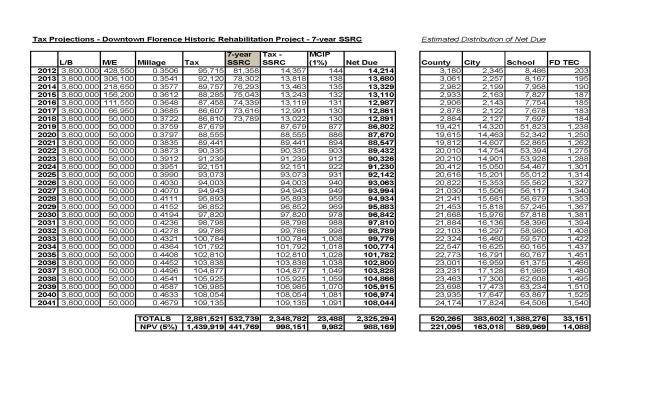

6 Special Source Revenue Credits South Carolina Code Sections and Properties given multi-county business park (MCBP) designation are eligible to receive credits against property taxes (which are fees generated by MCBP) to offset cost of infrastructure serving the project Level of credits and duration flexible Credit granted by County Council Unlike FILOT, available to any commercial activity Can t overlay on TIF District Potential for leveraging through special source bonds SSRC Project: Hotel Florence 53 room boutique hotel and 180 seat restaurant in 1905 building in downtown Florence $4.2M project Developer approached City and County for incentives Centerpiece was 7 year, 85% SSRC Would generate $533,000 in credits to developer/owner Existing TIF created problem Will generate approximately $1M in state and federal historic rehab tax credits 6

7 Hotel Florence Hotel Florence 7

State")

Abandoned building rehab tax credit (25%); authorizing bill died in General Assembly earlier this")

8 Rehabilitation Tax Credits Old Florence County Library (Before) Several Types Range from 10% to 25% of eligible project expenditures Federal historic rehab credit (10 or 20%, depending on National Register status) State rehab credit (10%), follows federal State retail rehab credit (10%), minimum 40,000 sf Textile facility rehab credit (25%) Abandoned building rehab tax credit (25%); authorizing bill died in General Assembly earlier this month 8

9 Old Florence County Library (After) Old Florence County Library 1925 County Library with 1970s addition Removed addition and returned building to original appearance 24,000 sf leased by Turner Padget law firm $5M project Over $1M in tax credits Largest commercial investment in Downtown Florence in 50 years 9

10 Key Federal Tax Incentives What is a Tax Credit? Rehabilitation Tax Credit (IRC Section 47). New Markets Tax Credit (IRC Section 45D). Credits vs. Deductions A Credit Offsets Tax Liability Dollar for Dollar Deduction Credit Income $100 $100 Less: Deductions (20) - Taxable Income Gross tax 35% Less: Credits - (20) Net Tax 35%

11 How Tax Credits Deliver Capital Example 1: Historic Tax Credits (HTCs) Sample Structure Federal tax credits not sold, but passed to investors General Partner 1% Owner Tax Credit Investor 99% Owner through partnerships Require structuring with partnerships and equity 99% Credits contributions Project Generally, partnership agreements contemplate exit of tax credit investor after compliance period Project Total, $97. Developer Equity, $19.5 Soft Debt, $10 Hard Debt, $53.3 Downtown office and retail Multiple phased project with additional HTC equity expected for future phases HTC represented key piece of financing to meet business requirements of developer 11

12 Example 2: Combining New Markets Tax Credit (NMTC) & HTC Halves Sponsor Equity Agenda Project Total, $19.7 NMTC Equity, $3.0 Fed. HTC Equity, $3.0 State HTC Equity, $2.2 Developer Equity, $4.0 Hard Debt, $7.5 Tax Credit Equity, $8.2 Renovation of historic hotel Federal HTCs, State HTCs, Federal NMTCs each with its own investor Multiple parties involved Low put price to exit tax credit equity at compliance period Market lender cooperated with structuring to increase money in first loss position and decrease exposure Types of Federal Historic Tax Credit Calculating the Credit Qualifying for the Credit Claiming the Credit Current Deal Structures Questions 12

13 The Rehabilitation Tax Credits Internal Revenue Code Section 47 There are Two Types of Federal HTC: 10% & 20% Credit 13

14 Important Dates in the History of the Rehabilitation Tax Credits 1976: First federal tax incentives for historic preservation (accelerated depreciation/ amortization). 1978: First federal tax credit for rehab of historic buildings (10%). 1981: Three tiered tax credit (25%, 20% and 15%), including first credit for rehab of older, non-historic buildings. 1986: Current two tiered structure; passive loss limitations imposed. The 20% Rehabilitation Tax Credit Fundamentals Tax Aspects Administered by the IRS. Preservation aspects jointly administered by NPS and State Historic Pres. Offices (SHPOs). Tax Credits = dollar for dollar reduction in tax liability (contrast with deduction). RTC is the most important (in dollar volume) federal preservation program. 14

15 The 20% Rehabilitation Tax Credit Statistics 937 projects approved by NPS in 2011* In 2011, roughly 69% of HTC projects were for multi-family housing, 16% for office space, 3% for commercial space* Of the 94.5% of Projects receiving Part 3 approvals that used other incentives or publicly supported financing, 48% used state historic tax credits* Federal Approval Process 3 Part Application Process Part 1 Historic Status Part 2 Design Approval Part 3 Project Completion State and National Park Service Review 60-Day Minimum Review Secretary of Interior s Standards for Rehabilitation *Source: Annual Report for Fiscal Year 2011: Federal Tax Incentives for Rehabilitating Historic Buildings National Park Service 15

16 What Types of Buildings Qualify? What Kinds of Buildings Qualify? The IRS Rules: Depreciable Building Requirement Must be a building. Building is defined as a structure or edifice enclosing a space within its wall and usually covered by a roof. Building must be depreciable. Depreciable buildings are generally those used for nonresidential (i.e. commercial) or residential rental purposes. (See Section 168(e)) Almost Anything But a Personal Residence Apartments Hotels Office Buildings Warehouses Distribution Facilities Back-Office Support/Computer/Call Centers Sports Facilities Mixed Use of Any of the Above 16

The NPS Rules: Certified Historic Structure Requirement Option #1 Building is listed in the")

17 What Types of Buildings Qualify? (cont d) What Types of Buildings Qualify? (cont d) The NPS Rules: Certified Historic Structure Requirement Option #1 Building is listed in the National Register of Historic Places. The NPS Rules: Certified Historic Structure Requirement Option #2 Building is located in a registered historic district and certified by the Sec. of the Interior as being of historic significance to the district. 17

18 Be Sure You Pass The Test Standard Rehabilitation Test Look back from placed in service date to basis in building 24 months prior or beginning of project, whichever is later QREs must exceed prior basis or $5,000, whichever is greater Substantial Rehabilitation Test Phased Rehabilitation Test Must be evidence that project will take longer than 24 months to complete prior to commencing rehab 60-month window Otherwise similar rules What Types of Rehabilitations Qualify? Definition of QREs Qualified Rehabilitation Expenditures (QREs) is the tax term given to those development costs on which rehabilitation tax credits can be claimed. QREs are any amounts chargeable to a capital account made in connection with the renovation, restoration or reconstruction of a qualified rehabilitated building (including its structural components), except as provided by law. Rolling 24-month window 18

19 What Types of Rehabilitations Qualify? Definition of QREs (cont d.) What Types of Rehabilitations Qualify? Definition of QREs (cont d.) QREs include costs related to: walls, partitions, floors, ceilings; permanent coverings such as paneling or tiling; windows and doors; air conditioning or heating systems, plumbing and plumbing fixtures; chimneys, stairs, elevators, sprinkling systems, fire escapes; QREs include costs related to: construction period interest and taxes; architect fees, engineering fees, construction management costs; reasonable developer fees 19

20 What is Not a QRE? Sample Development Budget Land & Interest Carry on Land Building Acquisition & Interest Carry on Acquisition Acquisition-Related Costs Site Improvements & Landscaping Enlargements & Demolition Personal Property Tax Exempt Use Property Qualified Depreciable Rehabilitation Non-Eligible Funded Total Expenditures Basis Expense Other Acquisition Costs-Land 40, ,000 Acquisition Cost- Building 120, , Construction Period Interest for Rehab 20,167 20, Permanent/Construction Loan Fee 6,000 1,000-5,000 - Achitectural, Engineering 28,000 28, Construction Contract 300, , Site Improvements 5,000-5, Contingency 35,000 35, Appliances 17,800-17, Historic Tax Credit Application Fee 2,500 2, Professional Fees 15,000 15, Marketing & Leasing Reserves 20, ,000 Insurance and RE Taxes During Construction 15,000 15, Development Fee 124,893 83,333 41, TOTAL APPLICATIONS: 749, , ,360 5,000 60,000 20

21 Calculating the Credit What Triggers the Credit? QREs $ 500,000 Credit Rate 20%* Credits $ 100,000 Placement in Service CO or TCO is Evidence of Placement in Service Calculate the equity amount: $1.15 per credit multiplied by $100,000 credits = $115,000 * Credit Rate is sometimes 10%. Is the building ready for occupancy? 21

22 When Can the Credit Be Claimed? Who Can Claim the Credit? Generally, the Year Placed In Service - 100% of the Credit Claimed Carry back One Year Carry forward 20 Years Historic credits are shared among owners based on the profits allocation Profits is considered to include the owner s share of: Taxable income Operating cash flow These allocations must remain the same during the recapture period 22

23 Limitations of the Use of the Credit How to Claim the Rehab Tax Credit Passive Loss Rules Alternative Minimum Tax At-Risk Rules Companies whose stock is publicly-traded generally aren t subject to these limitations 23

24 How to Claim the Rehab Tax Credit (cont d) Credits are claimed by filing IRS form 3468 along with the tax return for the year in which the taxpayer claims the credit. Part 3 Approval need not have already been obtained (but generally must be obtained within 30 months of tax return filing date) What is the Risk of Recapture? Triggering recapture Disposition of the property Disposition of at least 1/3 partnership interest Noncompliance with Secretary s Standards Property becomes tax exempt use property Total casualty loss Amount of recapture 100% of the credit in the first 12 months from placed in service Declines 20% every 12 months thereafter Possible recapture becomes zero after 60 months 24

25 Other Tax Credit Issues Single Entity Structure Development Fee Amount Payment Tax Exempt Use Property - Check The Tenants! Basis Adjustment-and impact on LIHTC.01% Credits, Profits & Losses, Fees and Cash Flow Managing Member (Developer Affiliate) Developer Equity Tax Credit, LLC (Property Owner) Tax Credit Investor LLC Historic Tax Credit Equity 99.99% Credits, Profits & Losses and Cash Flow Dev. Fee Tax Credit Investor Developer Loan Proceeds Debt Service Payments Rental Payments Construction/ Perm Lender Tenants 25

26 Historic Tax Credit Syndication The Credit Pass-Through Structure Landlord LLC owns fee simple, undertakes rehab, enters into Dev. Agreement, and earns the Historic Tax Credit. Master Tenant, LLC leases the entire project from the Landlord LLC for a fixed annual rental payment. Historic Tax Credit Syndication The Credit Pass-Through Structure (cont d.) Master Tenant, LLC operates the property, subleases to end users and enters into the Property Management Contract. Landlord makes special tax election to pass the Historic Tax Credit through to the Master Tenant LLC. 26

27 Master Lease/Credit Pass-Through Structure Investors Capitalize Project for Credit and Other Tax Benefits Managing Member (Developer Affiliate) Tax Credit Investor LLC Leveraged Lender (Bank) Tax Credit Investor Developer Equity 99.99% Credits, Profits & Losses, Fees and Cash Flow.01% Credits, Profits & Losses, Fees and Cash Flow Historic Tax Credit Equity 99.99% Credits, Profits & Losses, and Cash Flow $4,312,030 Investment Fund LLC $1,152,000 HTC Equity $2,007,720 NMTC Equity 7,150,000 QEI Load (4.5% of QEI) 321,750 Landlord, LLC (Property Owner/Lessor) Loan Proceeds Debt Service Payments Construction/ Perm Lender Pass-through of Historic Tax Credits & Share of Lease Payment & Equity Investment Master Tenant, LLC (Master Tenant) Rental Payments Sub-Tenants/ End Users CDE: QEI: QALICB: Loan A 4,312,030 Loan B 2,837,970 Sub-CDE LLC QALICB/Landlord LLC (Property Owner) Development Budget: $8M Community Development Entity Qualified Equity Investment Qualified Active Low Income Business 100% Ownership Lease Master Tenant, LLC 27

28 Thank you! More Information? Joseph Wallace Reznick Group J. Christopher Riddle, Esq. Haynsworth Sinkler Boyd, P.A Benjamin T. Zeigler, Esq. Haynsworth Sinkler Boyd, P.A

Tools of the Trade: Tax Credits 101

Tools of the Trade: Tax Credits 101 What is tax credit financing and how does it work? HOST: LAURA BURNS COMMUNITY IMPACT COMPLIANCE MANAGER Q&A: WILLIAM FIEDERLEIN PROJECT MANAGER INTRO: MERRILL HOOPENGARDNER

Tools of the Trade: Tax Credits 101 What is tax credit financing and how does it work? HOST: LAURA BURNS COMMUNITY IMPACT COMPLIANCE MANAGER Q&A: WILLIAM FIEDERLEIN PROJECT MANAGER INTRO: MERRILL HOOPENGARDNER

3 rd Annual NYS Redevelopment Summit Albany NY Keys to Successful Brownfield Redevelopment Tax Credits and Other Financial Incentives June 13, 2018

3 rd Annual NYS Redevelopment Summit Albany NY Keys to Successful Brownfield Redevelopment Tax Credits and Other Financial Incentives June 13, 2018 National Development Council Who We Are National non-profit

3 rd Annual NYS Redevelopment Summit Albany NY Keys to Successful Brownfield Redevelopment Tax Credits and Other Financial Incentives June 13, 2018 National Development Council Who We Are National non-profit

Government Programs. Credits and Incentives Continue to Fuel Development. November 5, 2012

Government Programs Credits and Incentives Continue to Fuel Development November 5, 2012 Speaker Bio Howard E. Gordon Partner 757.629.0607 hgordon@williamsmullen.com Howard Gordon s practice is focused

Government Programs Credits and Incentives Continue to Fuel Development November 5, 2012 Speaker Bio Howard E. Gordon Partner 757.629.0607 hgordon@williamsmullen.com Howard Gordon s practice is focused

Dallas Coffin Company Building (Constructed 1909) NYLO South Dallas (2012)

NYLO South Dallas (2012)") Dallas Coffin Company Building (Constructed 1909) NYLO South Dallas (2012) Panel Introductions Tax Credit Introduction Federal Non-refundable credit that can offset corporate federal income tax of non-closely

Dallas Coffin Company Building (Constructed 1909) NYLO South Dallas (2012) Panel Introductions Tax Credit Introduction Federal Non-refundable credit that can offset corporate federal income tax of non-closely

Regional Initiative Council Meetings Financing the Vision Lunch Discussion August 27, Carolinas. Durham Bulls Athletic Park.

Regional Initiative Council Meetings Financing the Vision Lunch Discussion August 27, 2015 Carolinas PNC Triangle Club Durham Bulls Athletic Park Panel Members TUCKER BARTLETT Executive Vice President,

Regional Initiative Council Meetings Financing the Vision Lunch Discussion August 27, 2015 Carolinas PNC Triangle Club Durham Bulls Athletic Park Panel Members TUCKER BARTLETT Executive Vice President,

New Markets Tax Credits

1 New Markets Tax Credits Lecture Notes City of San Antonio Community Development Summit 2009 927 Dudley Road Edgewood, KY 41017 Ph: 859-578-4850 Fax: 859-578-4860 2006 All rights reserved. Version: May

1 New Markets Tax Credits Lecture Notes City of San Antonio Community Development Summit 2009 927 Dudley Road Edgewood, KY 41017 Ph: 859-578-4850 Fax: 859-578-4860 2006 All rights reserved. Version: May

Understanding Tax Credit Programs for Historic Buildings Thursday, March 20 th, 2014

Understanding Tax Credit Programs for Historic Buildings Thursday, March 20 th, 2014 Jim Draeger Historic Preservation Officer Wisconsin Historical Society Neil White Business Development Planner City

Understanding Tax Credit Programs for Historic Buildings Thursday, March 20 th, 2014 Jim Draeger Historic Preservation Officer Wisconsin Historical Society Neil White Business Development Planner City

Combining Opportunity Zones with Tax Credits

Combining Opportunity Zones with Tax Credits MODERATOR Nicolo Pinoli Novogradac & Company LLP PANELISTS Fred Copeman Boston Financial Investment Management, LP Craig Nolte Federal Reserve Bank Of San Francisco

Combining Opportunity Zones with Tax Credits MODERATOR Nicolo Pinoli Novogradac & Company LLP PANELISTS Fred Copeman Boston Financial Investment Management, LP Craig Nolte Federal Reserve Bank Of San Francisco

FREQUENTLY ASKED QUESTIONS ABOUT TAX CREDITS FOR REHABILITATION

State Historic Preservation Office Oklahoma Historical Society 800 Nazih Zuhdi Drive Oklahoma City, OK 73105 405/521-6249 FAX 405/522-0816 http://www.okhistory.org/shpo/shpom.htm Fact Sheet #14 August

State Historic Preservation Office Oklahoma Historical Society 800 Nazih Zuhdi Drive Oklahoma City, OK 73105 405/521-6249 FAX 405/522-0816 http://www.okhistory.org/shpo/shpom.htm Fact Sheet #14 August

N A T I O N A L I N T E R A G E N C Y C O M M U N I T Y R E I N V E S T M E N T C O N F E R E N C E

2 0 1 0 N A T I O N A L I N T E R A G E N C Y C O M M U N I T Y R E I N V E S T M E N T C O N F E R E N C E Building and Managing an Investment Portfolio Dudley Benoit, SVP Community Development Banking

2 0 1 0 N A T I O N A L I N T E R A G E N C Y C O M M U N I T Y R E I N V E S T M E N T C O N F E R E N C E Building and Managing an Investment Portfolio Dudley Benoit, SVP Community Development Banking

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features: John R. Orrick, Jr., Partner, Linowes and Blocher, Bethesda, Md.

Presenting a live 90-minute webinar with interactive Q&A Mixed-Use and Economic Development Financing Structures and Options Leveraging Construction and Mezzanine Loans, Preferred Equity, Tax Increment

Presenting a live 90-minute webinar with interactive Q&A Mixed-Use and Economic Development Financing Structures and Options Leveraging Construction and Mezzanine Loans, Preferred Equity, Tax Increment

2018 Income Tax Update - Commercial Real Estate

2018 Income Tax Update - Commercial Real Estate Stephen M. Lukinovich, CPA, PFS, CVA Andrew J. Ackermann, CPA, CVA Kentucky Commercial Real Estate Conference Louisville, KY October 30, 2018 Tax Cuts and

2018 Income Tax Update - Commercial Real Estate Stephen M. Lukinovich, CPA, PFS, CVA Andrew J. Ackermann, CPA, CVA Kentucky Commercial Real Estate Conference Louisville, KY October 30, 2018 Tax Cuts and

Chapter 20. Federal Income Taxation. IRS Tax Classifications. IRS Tax Classifications. Taxation of Individuals & Corporations

Federal Income Taxation Chapter 20 Income Taxation and Value Whether you like it or not, you have a silent partner who shares in your enterprise If RE investors are successful, federal (& usually state)

Federal Income Taxation Chapter 20 Income Taxation and Value Whether you like it or not, you have a silent partner who shares in your enterprise If RE investors are successful, federal (& usually state)

State Historic Homes Rehabilitation Tax Credit CGS

State Historic Homes Rehabilitation Tax Credit CGS 10-416 Historic Homes Rehabilitation Tax Credit Basic Eligibility Requirements Listed on the State or National Register Located in a Program Targeted

State Historic Homes Rehabilitation Tax Credit CGS 10-416 Historic Homes Rehabilitation Tax Credit Basic Eligibility Requirements Listed on the State or National Register Located in a Program Targeted

Tax Credits for Small Wineries. Winery and Wine Distribution Law

Tax Credits for Small Wineries Winery and Wine Distribution Law Marc R. Greenough Foster Pepper PLLC Quincy, Washington August 5, 2008 Tax Credits for Small Wineries Under the Internal Revenue Code of

Tax Credits for Small Wineries Winery and Wine Distribution Law Marc R. Greenough Foster Pepper PLLC Quincy, Washington August 5, 2008 Tax Credits for Small Wineries Under the Internal Revenue Code of

Building the Capital Stack

Building the Capital Stack MODERATOR Thomas Boccia Novogradac & Company LLP PANELISTS John Cornell Nixon Peabody LLP Gary Elkins Elkins PLC Irvin Henderson Henderson & Company Scott DeMartino Dentons Phill

Building the Capital Stack MODERATOR Thomas Boccia Novogradac & Company LLP PANELISTS John Cornell Nixon Peabody LLP Gary Elkins Elkins PLC Irvin Henderson Henderson & Company Scott DeMartino Dentons Phill

Colorado Historic Preservation Income Tax Credit (Updated March 2010)

") Colorado Historic Preservation Income Tax Credit (Updated March 2010) ELIGIBLE PROPERTIES Over 50 years old and historically designated on the State Register of Historic Places or landmarked by a Certified

Colorado Historic Preservation Income Tax Credit (Updated March 2010) ELIGIBLE PROPERTIES Over 50 years old and historically designated on the State Register of Historic Places or landmarked by a Certified

LOW-INCOME HOUSING TAX CREDIT CLOSINGS FOR PHAs AND RAD TRANSACTIONS. June 2015

LOW-INCOME HOUSING TAX CREDIT CLOSINGS FOR PHAs AND RAD TRANSACTIONS June 2015 What Do Tax Credits Finance? New construction and rehab projects Acquisition in some cases Housing for families, special needs

LOW-INCOME HOUSING TAX CREDIT CLOSINGS FOR PHAs AND RAD TRANSACTIONS June 2015 What Do Tax Credits Finance? New construction and rehab projects Acquisition in some cases Housing for families, special needs

Funding Resources for Historic Properties

Funding Resources for Historic Properties Grants Two grant programs: Historic Preservation Fund (HPF) Educational programs and documentation projects Heritage Trust Fund (HTF) Bricks and Mortar, physical

Funding Resources for Historic Properties Grants Two grant programs: Historic Preservation Fund (HPF) Educational programs and documentation projects Heritage Trust Fund (HTF) Bricks and Mortar, physical

NMTC Legal, Tax & Structuring Issues Roundtable. Jerry Breed Bryan Cave LLP Washington, DC

NMTC Legal, Tax & Structuring Issues Roundtable Jerry Breed Bryan Cave LLP Washington, DC REVENUE PROCEDURE 2014-12 ISSUES UNDER COMBINED NMTC/HTC TRANSACTIONS Applicable Sections of Revenue Procedure

NMTC Legal, Tax & Structuring Issues Roundtable Jerry Breed Bryan Cave LLP Washington, DC REVENUE PROCEDURE 2014-12 ISSUES UNDER COMBINED NMTC/HTC TRANSACTIONS Applicable Sections of Revenue Procedure

AMERICAN BAR ASSOCIATION FORUM ON AFFORDABLE HOUSING AND COMMUNITY DEVELOPMENT 2017 ANNUAL MEETING TAX CREDIT DISCUSSIONS WITH IRS, TREASURY AND CDFI

AMERICAN BAR ASSOCIATION FORUM ON AFFORDABLE HOUSING AND COMMUNITY DEVELOPMENT 2017 ANNUAL MEETING TAX CREDIT DISCUSSIONS WITH IRS, TREASURY AND CDFI May 24, 2017 PANEL 1 LOW-INCOME HOUSING TAX CREDIT

AMERICAN BAR ASSOCIATION FORUM ON AFFORDABLE HOUSING AND COMMUNITY DEVELOPMENT 2017 ANNUAL MEETING TAX CREDIT DISCUSSIONS WITH IRS, TREASURY AND CDFI May 24, 2017 PANEL 1 LOW-INCOME HOUSING TAX CREDIT

OFFICE TENANCY ASSISTANCE PROGRAM

Planning and Economic Development Department Urban Renewal Section 71 Main Street West, 7th Floor Hamilton, Ontario L8P 4Y5 Phone: (905) 546-2424 Ext. 2755 Fax: (905) 546-2693 OFFICE TENANCY ASSISTANCE

Planning and Economic Development Department Urban Renewal Section 71 Main Street West, 7th Floor Hamilton, Ontario L8P 4Y5 Phone: (905) 546-2424 Ext. 2755 Fax: (905) 546-2693 OFFICE TENANCY ASSISTANCE

Historic Preservation Tax Exemption for Knights of Pythias/Union Bankers Building at 2557 Elm Street

Memorandum DATE May 7, 2018 CITY OF DALLAS TO Members of the Economic Development & Housing Committee: Tennell Atkins, Chair, Rickey D. Callahan, Vice-Chair, Lee M. Kleinman, Scott Griggs, Casey Thomas,

Memorandum DATE May 7, 2018 CITY OF DALLAS TO Members of the Economic Development & Housing Committee: Tennell Atkins, Chair, Rickey D. Callahan, Vice-Chair, Lee M. Kleinman, Scott Griggs, Casey Thomas,

PIDC/PHFA Affordable Housing Seminar March 6, 2013

PIDC/PHFA Affordable Housing Seminar March 6, 2013 PAID Background Overview: Managed by PIDC, PAID is a public authority created by the City of Philadelphia pursuant to the Economic Development Financing

PIDC/PHFA Affordable Housing Seminar March 6, 2013 PAID Background Overview: Managed by PIDC, PAID is a public authority created by the City of Philadelphia pursuant to the Economic Development Financing

Using Low Income Housing Tax Credits (LIHTC)

") FINANCING MULTI-FAMILY HOUSING: STRUCTURING THE LOW INCOME HOUSING TAX CREDIT AND TAX EXEMPT BONDS Documenting Transactions for Investors and Developers Using Low Income Housing Tax Credits (LIHTC) B Y

FINANCING MULTI-FAMILY HOUSING: STRUCTURING THE LOW INCOME HOUSING TAX CREDIT AND TAX EXEMPT BONDS Documenting Transactions for Investors and Developers Using Low Income Housing Tax Credits (LIHTC) B Y

BERGAMOT ADVISORY COMMITTEE MEETING 2/22/16: FLIP CHART NOTES

Hotel Use Discussion BERGAMOT ADVISORY COMMITTEE MEETING 2/22/16: FLIP CHART NOTES Proposed Size: 65 feet, 6 floors, 100 rooms Why a hotel is important to the project: It produces high paying jobs, estimated

Hotel Use Discussion BERGAMOT ADVISORY COMMITTEE MEETING 2/22/16: FLIP CHART NOTES Proposed Size: 65 feet, 6 floors, 100 rooms Why a hotel is important to the project: It produces high paying jobs, estimated

Historic Tax Credits New Money for Your Old Property

Historic Tax Credits New Money for Your Old Property Art Schuldt, Housing Solutions Alliance, LLC Micah Strange, Housing Solutions Alliance, LLC Cindy Hamilton, Heritage Consulting Group John Bowman, Foss

Historic Tax Credits New Money for Your Old Property Art Schuldt, Housing Solutions Alliance, LLC Micah Strange, Housing Solutions Alliance, LLC Cindy Hamilton, Heritage Consulting Group John Bowman, Foss

Public Economics, Inc. DWIGHT E. BERG, P.E. (888) Public Economics, Inc.

Public Economics, Inc.") New Markets Tax Credits for Non-profit Real Estate Financing DWIGHT E. BERG, P.E. dwight@dwightberg.com Introduction New Markets Tax Credit ( NMTC ) program created by Community Renewal Tax Relief Act

New Markets Tax Credits for Non-profit Real Estate Financing DWIGHT E. BERG, P.E. dwight@dwightberg.com Introduction New Markets Tax Credit ( NMTC ) program created by Community Renewal Tax Relief Act

GMHF Affordable Housing Loan Products

GMHF Affordable Housing Loan Products FOR RENTAL & SINGLE FAMILY AFFORDABLE HOUSING Predevelopment Loans Acquisition Loans Construction /Rehab Loans Tax Credit Bridge Loans Mini Perm & Permanent Loans

GMHF Affordable Housing Loan Products FOR RENTAL & SINGLE FAMILY AFFORDABLE HOUSING Predevelopment Loans Acquisition Loans Construction /Rehab Loans Tax Credit Bridge Loans Mini Perm & Permanent Loans

Introduction to New Markets Tax Credits

Introduction to New Markets Tax Credits Moderated by: Jonevan Hornsby, Empire State New Markets Presented by: Tim Favaro Cannon Heyman & Weiss, LLP Steve Kunin Rise Community Capital LLC Tom Oldenburg

Introduction to New Markets Tax Credits Moderated by: Jonevan Hornsby, Empire State New Markets Presented by: Tim Favaro Cannon Heyman & Weiss, LLP Steve Kunin Rise Community Capital LLC Tom Oldenburg

How to Prepare a Supportive Housing Operating Pro Forma

How to Prepare a Supportive Housing Operating Pro Forma The Operating Pro Forma is the tool used to estimate the expenses of a project during operations. It provides a summary of anticipated ongoing project

How to Prepare a Supportive Housing Operating Pro Forma The Operating Pro Forma is the tool used to estimate the expenses of a project during operations. It provides a summary of anticipated ongoing project

Town Square Redevelopment. Phase I Contract Discussion

Town Square Redevelopment Phase I Contract Discussion Date: June 8, 2017 Current Estimated Schedule Draft RFQ Review September 20, 2016 Final RFQ Publication October 10, 2016 Part I Team Shortlist January

Town Square Redevelopment Phase I Contract Discussion Date: June 8, 2017 Current Estimated Schedule Draft RFQ Review September 20, 2016 Final RFQ Publication October 10, 2016 Part I Team Shortlist January

Chapter 10B. Tax Aspects of Real Estate and Real Estate Sales *

0001 [ST: 10B-1] [ED: 10B-7] [REL: 162] (Beg Group) Composed: Wed Feb 28 15:17:37 EST 2018 Chapter 10B Tax Aspects of Real Estate and Real Estate Sales * SCOPE This chapter covers the fundamentals of the

0001 [ST: 10B-1] [ED: 10B-7] [REL: 162] (Beg Group) Composed: Wed Feb 28 15:17:37 EST 2018 Chapter 10B Tax Aspects of Real Estate and Real Estate Sales * SCOPE This chapter covers the fundamentals of the

Emmanuel Arellano Director Portfolio Management. Hanan Bowman Asset Strategy Manager Portfolio Management

Portfolio Management / FY 2017 (July 1, 2016 - June 30, 2017) Capital Expenditures Plan SDHC Board of Commissioners May 6, 2016 Emmanuel Arellano Director Portfolio Management Hanan Bowman Asset Strategy

Portfolio Management / FY 2017 (July 1, 2016 - June 30, 2017) Capital Expenditures Plan SDHC Board of Commissioners May 6, 2016 Emmanuel Arellano Director Portfolio Management Hanan Bowman Asset Strategy

Use of Municipal Hotel Occupancy Tax Revenue

Use of Municipal Hotel Occupancy Tax Revenue May be used only to promote tourism, conventions, and the hotel industry. Revenue may not be used for general revenue purposes or general governmental operations

Use of Municipal Hotel Occupancy Tax Revenue May be used only to promote tourism, conventions, and the hotel industry. Revenue may not be used for general revenue purposes or general governmental operations

7Z, - /'). L--[ - Memorandum

. L--[ - Memorandum") Memorandum DATE October 30, 2015 SU8Jt::c1 ro Members of the Economic Development Committee: Rickey D. Callahan (Chair), Casey Thomas, II (Vice Chair), Lee M. Kleinman, Adam Medrano, Carolyn King Arnold,

Memorandum DATE October 30, 2015 SU8Jt::c1 ro Members of the Economic Development Committee: Rickey D. Callahan (Chair), Casey Thomas, II (Vice Chair), Lee M. Kleinman, Adam Medrano, Carolyn King Arnold,

State Comparisons of. Assorted Tax Credits

EXHIBIT D1-a State Comparisons of Assorted Tax Credits Arkansas Tax Reform and Relief Legislative Task Force October 29, 2018 Arkansas Department of Finance and Administration Waste Reduction & Recycling

EXHIBIT D1-a State Comparisons of Assorted Tax Credits Arkansas Tax Reform and Relief Legislative Task Force October 29, 2018 Arkansas Department of Finance and Administration Waste Reduction & Recycling

Tax Cuts and Jobs Act

Tax Cuts and Jobs Act 1. Deduction For Qualified Business Income IRC 199A a. The Tax Cuts and Jobs Act permits pass-through business owners, including partners of partnerships, S corporation shareholders

Tax Cuts and Jobs Act 1. Deduction For Qualified Business Income IRC 199A a. The Tax Cuts and Jobs Act permits pass-through business owners, including partners of partnerships, S corporation shareholders

1 Integrated Planning & Public Works

1 Integrated Planning & Public Works STAFF REPORT Building Standards Title: Building Standards 2016 Fees and Charges Report Number: IPPW2015-111 Author: Lynn Balfour Meeting Type: Finance & Strategic Planning

1 Integrated Planning & Public Works STAFF REPORT Building Standards Title: Building Standards 2016 Fees and Charges Report Number: IPPW2015-111 Author: Lynn Balfour Meeting Type: Finance & Strategic Planning

Honorable Mayor and Members of the City Council Phil Kamlarz, City Manager

Office of the City Manager To: From: Honorable Mayor and Members of the City Council Phil Kamlarz, City Manager Submitted by: Jane Micallef, Director, Housing and Community Services Department Subject:

Office of the City Manager To: From: Honorable Mayor and Members of the City Council Phil Kamlarz, City Manager Submitted by: Jane Micallef, Director, Housing and Community Services Department Subject:

A Credit For Rehabilitation Of Historic Barns

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau A Credit For Rehabilitation Of Historic Barns General The investment tax credit under Article 9-A,

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau A Credit For Rehabilitation Of Historic Barns General The investment tax credit under Article 9-A,

San Francisco Multi-Purpose Venue Project. Fiscal Impact Analysis: Revenues. Draft Report. Prepared for: The City and County of San Francisco

Draft Report San Francisco Multi-Purpose Venue Project Fiscal Impact Analysis: Revenues Prepared for: The City and County of San Francisco Prepared by: Economic & Planning Systems, Inc. April 27, 2015

Draft Report San Francisco Multi-Purpose Venue Project Fiscal Impact Analysis: Revenues Prepared for: The City and County of San Francisco Prepared by: Economic & Planning Systems, Inc. April 27, 2015

Federal Tax Policies Affecting Commercial Real Estate Brokers

Federal Tax Policies Affecting Commercial Real Estate Brokers Updated October, 2006 CCIM Institute 430 N. Michigan Avenue Chicago, IL 60611 (312) 321-4460 Table of Contents Table of Contents... 1 Introduction...

Federal Tax Policies Affecting Commercial Real Estate Brokers Updated October, 2006 CCIM Institute 430 N. Michigan Avenue Chicago, IL 60611 (312) 321-4460 Table of Contents Table of Contents... 1 Introduction...

September 7, Estimated Total Economic Impact and Direct Tax Revenue Generation of Different Potential Waterfront Uses

1435 Walnut Street, 4 th Floor Philadelphia, PA 19102 215-717-2777 econsultsolutions.com September 7, 2017 Estimated Economic Impact and Direct Tax Revenue Generation of Different Potential Waterfront

1435 Walnut Street, 4 th Floor Philadelphia, PA 19102 215-717-2777 econsultsolutions.com September 7, 2017 Estimated Economic Impact and Direct Tax Revenue Generation of Different Potential Waterfront

AMENDMENT TO THE MONTCALM COUNTY BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE 107 S LAFAYETTE, LLC REDEVELOPMENT PROJECT

AMENDMENT TO THE MONTCALM COUNTY BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE 107 S LAFAYETTE, LLC REDEVELOPMENT PROJECT January 30, 2017 Introduction 107 S Lafayette, LLC ("107 S Lafayette")

AMENDMENT TO THE MONTCALM COUNTY BROWNFIELD REDEVELOPMENT AUTHORITY BROWNFIELD PLAN FOR THE 107 S LAFAYETTE, LLC REDEVELOPMENT PROJECT January 30, 2017 Introduction 107 S Lafayette, LLC ("107 S Lafayette")

Financing Developments with Tax Credits

Financing Developments with Tax Credits Presenter Background Sammy Ehtisham, Assistant Vice President of Acquisitions Work exclusively with developments that utilize the Federal Low Income Housing Tax

Financing Developments with Tax Credits Presenter Background Sammy Ehtisham, Assistant Vice President of Acquisitions Work exclusively with developments that utilize the Federal Low Income Housing Tax

Common Mistakes to Jeopardize Retirement Accounts

Common Mistakes to Jeopardize Retirement Accounts Presented by: Angela H. Wong, CPA 4966 El Camino Real, Suite 205 Los Altos, California, 94022 650-968-1518 angela@wongcpa.us Materials covered in this

Common Mistakes to Jeopardize Retirement Accounts Presented by: Angela H. Wong, CPA 4966 El Camino Real, Suite 205 Los Altos, California, 94022 650-968-1518 angela@wongcpa.us Materials covered in this

Springfield High School

5.1 Springfield High School Springfield School District Delaware County - Pennsylvania Master Plan Presentation Town Hall Meeting 5 Project Cost Estimates/ Project Financing Strategy / Tax Impact February

5.1 Springfield High School Springfield School District Delaware County - Pennsylvania Master Plan Presentation Town Hall Meeting 5 Project Cost Estimates/ Project Financing Strategy / Tax Impact February

TAX UPDATES YOU NEED TO KNOW NOW

OCTOBER 12, 2018 TAX UPDATES YOU NEED TO KNOW NOW Tyler Waldrupe, CPA, Senior Manager Jeffrey A. Ring, CPA, Principal AGENDA 1 2 HIGHLIGHTS OF TAX CUTS & JOBS ACT DISCUSS STATE COMPLIANCE WITH TAX CUTS

OCTOBER 12, 2018 TAX UPDATES YOU NEED TO KNOW NOW Tyler Waldrupe, CPA, Senior Manager Jeffrey A. Ring, CPA, Principal AGENDA 1 2 HIGHLIGHTS OF TAX CUTS & JOBS ACT DISCUSS STATE COMPLIANCE WITH TAX CUTS

Small Building Participation Loan Program

HCR s Small Building Participation Loan Program provides gap project financing assistance for qualified housing developers for acquisition, capital costs and related soft costs associated with the preservation

HCR s Small Building Participation Loan Program provides gap project financing assistance for qualified housing developers for acquisition, capital costs and related soft costs associated with the preservation

APPENDIX E ALLOWABLE CAPITAL EXPENDITURE GUIDELINES

APPENDIX E ALLOWABLE CAPITAL EXPENDITURE GUIDELINES Introduction State capital appropriations are funded primarily through the issuance of State bonds. State bonds must be authorized by Ohio voters via

APPENDIX E ALLOWABLE CAPITAL EXPENDITURE GUIDELINES Introduction State capital appropriations are funded primarily through the issuance of State bonds. State bonds must be authorized by Ohio voters via

Sec. 42. Low-income housing credit

Sec. 42. Low-income housing credit STATUTE TITLE 26, Subtitle A, CHAPTER 1, Subchapter A, PART IV, Subpart D, Sec. 42 (a) (b) For purposes of section 38, the amount of the low-income housing credit determined

Sec. 42. Low-income housing credit STATUTE TITLE 26, Subtitle A, CHAPTER 1, Subchapter A, PART IV, Subpart D, Sec. 42 (a) (b) For purposes of section 38, the amount of the low-income housing credit determined

Selling Your Home. Contents. Important Change for Important Reminders. Publication 523 Cat. No W. For use in preparing 1998 Returns

Department of the Treasury Internal Revenue Service Publication 523 Cat. No. 15044W Selling Your Home For use in preparing 1998 Returns Contents Introduction... 2 Chapter 1. Main Home... 2 Chapter 2. Rules

Department of the Treasury Internal Revenue Service Publication 523 Cat. No. 15044W Selling Your Home For use in preparing 1998 Returns Contents Introduction... 2 Chapter 1. Main Home... 2 Chapter 2. Rules

Tax Credit 101. Plan.Build.House. Presented By: Darrell Beavers and Sammy Ehtisham Date/Time: Tuesday, August 21 st at 3:00 PM

Tax Credit 101 Presented By: Darrell Beavers and Sammy Ehtisham Date/Time: Tuesday, August 21 st at 3:00 PM Presenting Sponsor Presenter Background Darrell Beavers Housing Development Director at OHFA

Tax Credit 101 Presented By: Darrell Beavers and Sammy Ehtisham Date/Time: Tuesday, August 21 st at 3:00 PM Presenting Sponsor Presenter Background Darrell Beavers Housing Development Director at OHFA

2019 Development Charges Study Technical Stakeholder Consultation. Wednesday, November 21, 2018 Burnhamthorpe Community Centre

2019 Development Charges Study Technical Stakeholder Consultation Wednesday, November 21, 2018 Burnhamthorpe Community Centre Today we will discuss... Introductions City DC Survey Results Overview of the

2019 Development Charges Study Technical Stakeholder Consultation Wednesday, November 21, 2018 Burnhamthorpe Community Centre Today we will discuss... Introductions City DC Survey Results Overview of the

GENERAL ASSEMBLY OF NORTH CAROLINA 1991 SESSION CHAPTER 594 HOUSE BILL 703

GENERAL ASSEMBLY OF NORTH CAROLINA 1991 SESSION CHAPTER 594 HOUSE BILL 703 AN ACT TO AUTHORIZE WAKE COUNTY TO LEVY A ROOM OCCUPANCY TAX AND A PREPARED FOOD AND BEVERAGE TAX. The General Assembly of North

GENERAL ASSEMBLY OF NORTH CAROLINA 1991 SESSION CHAPTER 594 HOUSE BILL 703 AN ACT TO AUTHORIZE WAKE COUNTY TO LEVY A ROOM OCCUPANCY TAX AND A PREPARED FOOD AND BEVERAGE TAX. The General Assembly of North

Loans in Areas Having Special Flood Hazards; Interagency Questions and Answers Regarding Flood Insurance

Loans in Areas Having Special Flood Hazards; Interagency Questions and Answers Regarding Flood Insurance Note: This document is extracted from the Federal Register publication at 74 FR 35914 (July 21,

Loans in Areas Having Special Flood Hazards; Interagency Questions and Answers Regarding Flood Insurance Note: This document is extracted from the Federal Register publication at 74 FR 35914 (July 21,

Make It Right Foundation and Subsidiaries. As of December 31, 2013 and 2012

Consolidated Financial Statements and Report of Independent Certified Public Accountants Make It Right Foundation and Subsidiaries As of December 31, 2013 and 2012 Make It Right Foundation and Subsidiaries

Consolidated Financial Statements and Report of Independent Certified Public Accountants Make It Right Foundation and Subsidiaries As of December 31, 2013 and 2012 Make It Right Foundation and Subsidiaries

Ohio Legislative Service Commission

Ohio Legislative Service Commission Fiscal Note & Local Impact Statement Tom Middleton and other LSC staff Bill: H.B. 233 of the 131st G.A. Date: April 8, 2016 Status: As Reported by Senate Ways & Means

Ohio Legislative Service Commission Fiscal Note & Local Impact Statement Tom Middleton and other LSC staff Bill: H.B. 233 of the 131st G.A. Date: April 8, 2016 Status: As Reported by Senate Ways & Means

IRC 199A Deduction for Qualified Business Income

IRC 199A Deduction for Qualified Business Income What is it? 20% deduction against qualified business income Designed to provide a tax break to owners of pass through entities, in light of substantial

IRC 199A Deduction for Qualified Business Income What is it? 20% deduction against qualified business income Designed to provide a tax break to owners of pass through entities, in light of substantial

HUD s Rental Assistance Demonstration Program

NALHFA 2014 Annual Educational Conference April 2-5, 2014 Omni Hotel at CNN Center HUD s Rental Assistance Demonstration Program Presented By: John B. Rucker, III Executive Vice President john.rucker@merchantcapital.com

NALHFA 2014 Annual Educational Conference April 2-5, 2014 Omni Hotel at CNN Center HUD s Rental Assistance Demonstration Program Presented By: John B. Rucker, III Executive Vice President john.rucker@merchantcapital.com

Racine Event Center & Hotel. RDA & Committee of the Whole Meeting Tuesday, June 27

Racine Event Center & Hotel RDA & Committee of the Whole Meeting Tuesday, June 27 Agenda o o o o o o Team introductions What the event center and hotel will do for our city? The schedule/process What will

Racine Event Center & Hotel RDA & Committee of the Whole Meeting Tuesday, June 27 Agenda o o o o o o Team introductions What the event center and hotel will do for our city? The schedule/process What will

Audit Funding Program - Application Form

Audit Funding Program - Application Form This Application is between Toronto Hydro-Electric System Limited (the LDC ) and the Participant named below. By submitting this Application, the Participant understands

Audit Funding Program - Application Form This Application is between Toronto Hydro-Electric System Limited (the LDC ) and the Participant named below. By submitting this Application, the Participant understands

TULSA DEVELOPMENT AUTHORITY BOARD MEETING. MEETING OF: April 6, 2017

TULSA DEVELOPMENT AUTHORITY BOARD MEETING MEETING OF: April 6, 2017 TO: FROM: SUBJECT: CHAIRMAN AND BOARD MEMBERS OFFICE OF TULSA DEVELOPMENT AUTHORITY 410 S BOSTON AVE (FIRST PLACE GARAGE) FIRST PLACE

TULSA DEVELOPMENT AUTHORITY BOARD MEETING MEETING OF: April 6, 2017 TO: FROM: SUBJECT: CHAIRMAN AND BOARD MEMBERS OFFICE OF TULSA DEVELOPMENT AUTHORITY 410 S BOSTON AVE (FIRST PLACE GARAGE) FIRST PLACE

NCAHMA Spring Underwriting Forum April 7-8, 2010 Physical Needs Assessments

NCAHMA Spring Underwriting Forum April 7-8, 2010 Physical Needs Assessments 1. What is a CNA? Presentation by: Thomas E. Fielder Phone: 859-276-0000 / tfielder@fieldergroup.com a) Comprehensive review

NCAHMA Spring Underwriting Forum April 7-8, 2010 Physical Needs Assessments 1. What is a CNA? Presentation by: Thomas E. Fielder Phone: 859-276-0000 / tfielder@fieldergroup.com a) Comprehensive review

As Introduced. 132nd General Assembly Regular Session S. B. No

132nd General Assembly Regular Session S. B. No. 72 2017-2018 Senator Huffman Cosponsors: Senators Terhar, Jordan A B I L L To amend sections 164.07, 307.022, 307.671, 307.673, 307.674, 307.696, 351.06,

132nd General Assembly Regular Session S. B. No. 72 2017-2018 Senator Huffman Cosponsors: Senators Terhar, Jordan A B I L L To amend sections 164.07, 307.022, 307.671, 307.673, 307.674, 307.696, 351.06,

Tax Cuts and Jobs Act Changes Impacting Real Estate. Presented by: Sefi Silverstein, CPA Len Nitti, CPA, MST

Tax Cuts and Jobs Act Changes Impacting Real Estate Presented by: Sefi Silverstein, CPA Len Nitti, CPA, MST Our Speakers Sefi Silverstein, CPA Len Nitti, CPA, MST 2 Housekeeping To submit questions use

Tax Cuts and Jobs Act Changes Impacting Real Estate Presented by: Sefi Silverstein, CPA Len Nitti, CPA, MST Our Speakers Sefi Silverstein, CPA Len Nitti, CPA, MST 2 Housekeeping To submit questions use

NORTHERN MARIANAS HOUSING CORPORATION LOW-INCOME HOUSING TAX CREDIT PROGRAM 2016 APPLICATION

NORTHERN MARIANAS HOUSING CORPORATION LOW-INCOME HOUSING TAX CREDIT PROGRAM 2016 APPLICATION I. APPLICANT INFORMATION 1 A. Partnership or Limited Liability Company Information 2 B. Identity of Interest

NORTHERN MARIANAS HOUSING CORPORATION LOW-INCOME HOUSING TAX CREDIT PROGRAM 2016 APPLICATION I. APPLICANT INFORMATION 1 A. Partnership or Limited Liability Company Information 2 B. Identity of Interest

The Economic Capture of the Downtown Phoenix Redevelopment Area. Prepared for:

The Economic Capture of the Downtown Phoenix Redevelopment Area Prepared for: June 2018 Table of Contents Section 1: Executive Summary... 2 Section 2: Introduction and Purpose... 4 2.1 Analytical Qualifiers...4

The Economic Capture of the Downtown Phoenix Redevelopment Area Prepared for: June 2018 Table of Contents Section 1: Executive Summary... 2 Section 2: Introduction and Purpose... 4 2.1 Analytical Qualifiers...4

Opportunity Zones. How to capitalize the funds and get OZ equity into a project

Opportunity Zones How to capitalize the funds and get OZ equity into a project CONNECT WITH US Presenter Michael Ross President, Principal +1 (512) 975 7290 michael.ross@bakertilly.com Michael Ross, president

Opportunity Zones How to capitalize the funds and get OZ equity into a project CONNECT WITH US Presenter Michael Ross President, Principal +1 (512) 975 7290 michael.ross@bakertilly.com Michael Ross, president

New Markets Tax Credits. How to close a gap in a project s financing and add a layer of tax credit equity to the capital stack

New Markets Tax Credits How to close a gap in a project s financing and add a layer of tax credit equity to the capital stack CONNECT WITH US Presenter Michael Ross President, Principal +1 (512) 975 7290

New Markets Tax Credits How to close a gap in a project s financing and add a layer of tax credit equity to the capital stack CONNECT WITH US Presenter Michael Ross President, Principal +1 (512) 975 7290

NYS Housing Finance Agency Affordable Rental Housing Term Sheet & Financing Guide

PROGRAM DESCRIPTION Goal: NYS Housing Finance Agency Affordable Rental Housing Term Sheet & Financing Guide The New York State Housing Finance Agency (HFA) Affordable Rental Housing Program provides tax-exempt

PROGRAM DESCRIPTION Goal: NYS Housing Finance Agency Affordable Rental Housing Term Sheet & Financing Guide The New York State Housing Finance Agency (HFA) Affordable Rental Housing Program provides tax-exempt

Capital Improvements: Planning and Budgeting in the District of Columbia. Susan M. Banta Former Senior Budget Officer

Capital Improvements: Planning and Budgeting in the District of Columbia Susan M. Banta Former Senior Budget Officer Capital Improvements Program The District of Columbia s Capital Improvements Program

Capital Improvements: Planning and Budgeting in the District of Columbia Susan M. Banta Former Senior Budget Officer Capital Improvements Program The District of Columbia s Capital Improvements Program

Federal tax credits and incentives that make an impact Engineering and Construction Conference

Federal tax credits and incentives that make an impact 2017 Engineering and Construction Conference Federal tax considerations + credits & incentives Agenda Topic Research & development tax credit Section

Federal tax credits and incentives that make an impact 2017 Engineering and Construction Conference Federal tax considerations + credits & incentives Agenda Topic Research & development tax credit Section

Tax Planning for Real Estate Under the TCJA

By now, you have been bombarded with summaries and articles on the 507-page tax bill, formerly known as the Tax Cuts and Jobs Act of 2017, and signed into law by President Trump on Dec. 22, 2017 (the Act).

By now, you have been bombarded with summaries and articles on the 507-page tax bill, formerly known as the Tax Cuts and Jobs Act of 2017, and signed into law by President Trump on Dec. 22, 2017 (the Act).

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION HOUSE BILL DRH40552-MCx-164 (04/05)

") H GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 0 HOUSE BILL DRH0-MCx- (0/0) H.B. 00 Apr, 0 HOUSE PRINCIPAL CLERK D Short Title: Safe Infrastructure & Low Property Tax Act. (Public) Sponsors: Referred to:

H GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 0 HOUSE BILL DRH0-MCx- (0/0) H.B. 00 Apr, 0 HOUSE PRINCIPAL CLERK D Short Title: Safe Infrastructure & Low Property Tax Act. (Public) Sponsors: Referred to:

Historic Tax Credit Introduction Federal Historic Tax Credit

Historic Tax Credit Introduction Federal Historic Tax Credit Federal Historic Primary objective - encourage redevelopment of historic buildings Secondary economic development, urban and rural community

Historic Tax Credit Introduction Federal Historic Tax Credit Federal Historic Primary objective - encourage redevelopment of historic buildings Secondary economic development, urban and rural community

Eldred Preserve Project

Application to County of Sullivan Industrial Development Agency for Financial Assistance for Eldred Preserve Project Prepared by: Planning & Research Consultants 100 Fourth Street Honesdale, PA 18431 (570)

Application to County of Sullivan Industrial Development Agency for Financial Assistance for Eldred Preserve Project Prepared by: Planning & Research Consultants 100 Fourth Street Honesdale, PA 18431 (570)

CHAPTER 2: GENERAL PROGRAM RULES

The HOME program has a number of basic rules that apply to all program activities. These rules concern: The definition of a project; The form and amount of subsidy; Eligible costs; The property; The applicant

The HOME program has a number of basic rules that apply to all program activities. These rules concern: The definition of a project; The form and amount of subsidy; Eligible costs; The property; The applicant

DEVELOPMENT CHARGES BACKGROUND STUDY

DEVELOPMENT CHARGES BACKGROUND STUDY Town of Innisfil C o n s u l t i n g L t d. July 19, 2018 TABLE OF CONTENTS EXECUTIVE SUMMARY... 1 I PURPOSE OF THE DEVELOPMENT CHARGES BACKGROUND STUDY... 6 A. INTRODUCTION

DEVELOPMENT CHARGES BACKGROUND STUDY Town of Innisfil C o n s u l t i n g L t d. July 19, 2018 TABLE OF CONTENTS EXECUTIVE SUMMARY... 1 I PURPOSE OF THE DEVELOPMENT CHARGES BACKGROUND STUDY... 6 A. INTRODUCTION

The Final Tangible Property Regulations West Virginia Tax Institute

The Final Tangible Property Regulations West Virginia Tax Institute October 20, 2014 Notice ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY KPMG or Teresa Castanias, CPA TO BE USED,

The Final Tangible Property Regulations West Virginia Tax Institute October 20, 2014 Notice ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY KPMG or Teresa Castanias, CPA TO BE USED,

Insights. Community Developments. Low-Income Housing Tax Credits: Affordable Housing Investment Opportunities for Banks. February 2008.

Comptroller of the Currency Administrator of National Banks US Department of the Treasury Community Developments February 2008 Community Affairs Department Insights Low-Income Housing Tax Credits: Affordable

Comptroller of the Currency Administrator of National Banks US Department of the Treasury Community Developments February 2008 Community Affairs Department Insights Low-Income Housing Tax Credits: Affordable

Public Revenue Department. Real Estate

Real Estate 0 What is a supply? VAT will be due where a taxable supply is being made by a Taxable Person In the UAE For consideration By any person In the course of conducting business A supply of goods

Real Estate 0 What is a supply? VAT will be due where a taxable supply is being made by a Taxable Person In the UAE For consideration By any person In the course of conducting business A supply of goods

Innovative Financing Strategies. Introduction by: Mark Cooter, Managing Partner, Cherry Bekaert, LLP

Innovative Financing Strategies Introduction by: Mark Cooter, Managing Partner, Cherry Bekaert, LLP Panelists: Harry Huntley, Executive Director, SC Jobs & Economic Development Authority Nancy Whitworth,

Innovative Financing Strategies Introduction by: Mark Cooter, Managing Partner, Cherry Bekaert, LLP Panelists: Harry Huntley, Executive Director, SC Jobs & Economic Development Authority Nancy Whitworth,

THE ABC S OF AFFORDABLE HOUSING DEVELOPMENT

Presentation Overview Page Tax Credit Program Fundamentals 3 Qualified Allocation Plan Review 22 What Makes a Successful Application 32 2 Tax Credit Program Fundamentals 3 Housing Priorities Increase the

Presentation Overview Page Tax Credit Program Fundamentals 3 Qualified Allocation Plan Review 22 What Makes a Successful Application 32 2 Tax Credit Program Fundamentals 3 Housing Priorities Increase the

Audit Technique Guide IRC 42, Low-Income Housing Credit. DRAFT FOR COMMENT ONLY January 2014

Audit Technique Guide IRC 42, Low-Income Housing Credit DRAFT FOR COMMENT ONLY January 2014 This Audit Technique Guide is a draft for comment and may not be citied as authority. Information in the document

Audit Technique Guide IRC 42, Low-Income Housing Credit DRAFT FOR COMMENT ONLY January 2014 This Audit Technique Guide is a draft for comment and may not be citied as authority. Information in the document

Business Changes in the Tax Cuts and Jobs Act. Alan D. Sobel, CPA December 27,

Business Changes in the Tax Cuts and Jobs Act Alan D. Sobel, CPA December 27, 2017 Alan.sobel@sobelcollc.com 973-994-9494 Background Most significant tax legislation since 1986 503 pages of legislation

Business Changes in the Tax Cuts and Jobs Act Alan D. Sobel, CPA December 27, 2017 Alan.sobel@sobelcollc.com 973-994-9494 Background Most significant tax legislation since 1986 503 pages of legislation

IN-SOURCING" CAPITAL EB-5 LOANS AND EQUITY NMTC TAX CREDIT EQUITY NON-RECOURSE PROJECT FINANCE BONDS

IN-SOURCING" CAPITAL EB-5 LOANS AND EQUITY NMTC TAX CREDIT EQUITY NON-RECOURSE PROJECT FINANCE BONDS Daniel M. McRae, Partner Seyfarth Shaw LLP 1075 Peachtree Street, N.E., Ste 2500 Atlanta, GA 30309 404.888.1883

IN-SOURCING" CAPITAL EB-5 LOANS AND EQUITY NMTC TAX CREDIT EQUITY NON-RECOURSE PROJECT FINANCE BONDS Daniel M. McRae, Partner Seyfarth Shaw LLP 1075 Peachtree Street, N.E., Ste 2500 Atlanta, GA 30309 404.888.1883

Depreciation In General

Accelerating Tax Deductions for Real Estate Review of Accelerated Depreciation and Repair Rules 2017 Schenck Real Estate Forum Ryan Sonnenberg, CPA Manager Depreciation In General Recover cost of asset

Accelerating Tax Deductions for Real Estate Review of Accelerated Depreciation and Repair Rules 2017 Schenck Real Estate Forum Ryan Sonnenberg, CPA Manager Depreciation In General Recover cost of asset

2465 Reynolds Ave, North Las Vegas, NV 89030

12,020' Reynolds Medical & Attorney Build-Out Elevator 89030 2465 Reynolds Ave, North Las Vegas, NV 89030 Listing ID: 29944111 Status: Active Property Type: Office For Sale (also listed as Special Purpose)

12,020' Reynolds Medical & Attorney Build-Out Elevator 89030 2465 Reynolds Ave, North Las Vegas, NV 89030 Listing ID: 29944111 Status: Active Property Type: Office For Sale (also listed as Special Purpose)

What the Tax Cuts and Jobs Act Means for the Real Estate Industry

What the Tax Cuts and Jobs Act Means for the Real Estate Industry PRESENTED BY: ADAM HILL, CPA, PARTNER JON WILLIAMSON, CPA, MT, TAX MANAGER KIM PALMER, CPA, MT, PARTNER February 1, 2018 Welcome & Introductions

What the Tax Cuts and Jobs Act Means for the Real Estate Industry PRESENTED BY: ADAM HILL, CPA, PARTNER JON WILLIAMSON, CPA, MT, TAX MANAGER KIM PALMER, CPA, MT, PARTNER February 1, 2018 Welcome & Introductions

ITEM 7 ESTIMATED INITIAL INVESTMENT. YOUR ESTIMATED INITIAL INVESTMENT FOR A SHOPPING MALL FOOD COURT LOCATION (Single Unit) Method of Payment

Method of Payment") ITEM 7 ESTIMATED INITIAL INVESTMENT SHOPPING MALL FOOD COURT LOCATION (Single Unit) Initial Franchise Fee 1 $30,000 Lump Sum At Signing of Franchise Agreement Travel and Living Expenses While Training

ITEM 7 ESTIMATED INITIAL INVESTMENT SHOPPING MALL FOOD COURT LOCATION (Single Unit) Initial Franchise Fee 1 $30,000 Lump Sum At Signing of Franchise Agreement Travel and Living Expenses While Training

2017 Tax Cuts and Jobs Act: Impact on U.S. Real Estate Businesses

CLIENT MEMORANDUM 2017 Tax Cuts and Jobs Act: Impact on U.S. Real Estate Businesses January 30, 2018 The new tax act signed into law on December 22, 2017, popularly known as the Tax Cuts and Jobs Act (

CLIENT MEMORANDUM 2017 Tax Cuts and Jobs Act: Impact on U.S. Real Estate Businesses January 30, 2018 The new tax act signed into law on December 22, 2017, popularly known as the Tax Cuts and Jobs Act (

Tax Cuts and Jobs Act Real Estate Industry Impact. April 30, 2018 Mary Beth Saylor, CPA Brent A. Wilkinson, CPA, JD

Tax Cuts and Jobs Act Real Estate Industry Impact April 30, 2018 Mary Beth Saylor, CPA Brent A. Wilkinson, CPA, JD Topics for Today Rate Changes Business Interest Limitation Net Operating Losses Excess

Tax Cuts and Jobs Act Real Estate Industry Impact April 30, 2018 Mary Beth Saylor, CPA Brent A. Wilkinson, CPA, JD Topics for Today Rate Changes Business Interest Limitation Net Operating Losses Excess

Lowell and Lawrence, Massachusetts Renewal Communities Incentives

Lowell and Lawrence, Massachusetts Renewal Communities Incentives An Initiative of the U. S. Department of Housing and Urban Development based on tax incentives authorized by the Community Renewal Tax

Lowell and Lawrence, Massachusetts Renewal Communities Incentives An Initiative of the U. S. Department of Housing and Urban Development based on tax incentives authorized by the Community Renewal Tax

THE MOUNTAIN CLUB ON LOON UNIT OWNERS' ASSOCIATION AND SUBSIDIARY FOR THE YEAR ENDED DECEMBER 31, 2013 AND INDEPENDENT AUDITORS REPORT

THE MOUNTAIN CLUB ON LOON UNIT OWNERS' ASSOCIATION AND SUBSIDIARY FOR THE YEAR ENDED DECEMBER 31, 2013 AND INDEPENDENT AUDITORS REPORT THE MOUNTAIN CLUB ON LOON UNIT OWNERS' ASSOCIATION AND SUBSIDIARY

THE MOUNTAIN CLUB ON LOON UNIT OWNERS' ASSOCIATION AND SUBSIDIARY FOR THE YEAR ENDED DECEMBER 31, 2013 AND INDEPENDENT AUDITORS REPORT THE MOUNTAIN CLUB ON LOON UNIT OWNERS' ASSOCIATION AND SUBSIDIARY

Federal Tax Code 2017 House and Senate Tax Reform Proposals

Current Law (Section) H.R. 1 Tax Cuts and Jobs Act (House version) House Comments and Recommendations H.R. 1 Tax Cuts and Jobs Act (Senate version) Senate Comments and Recommendations (26 U.S.C. 121) Exclusion

Current Law (Section) H.R. 1 Tax Cuts and Jobs Act (House version) House Comments and Recommendations H.R. 1 Tax Cuts and Jobs Act (Senate version) Senate Comments and Recommendations (26 U.S.C. 121) Exclusion

COMMERCIAL MORTGAGE FINANCING SOLUTIONS

COMMERCIAL MORTGAGE FINANCING SOLUTIONS Attached is an introduction to NORTHERN RANGE CAPITAL CORP describing some of our unique mortgage financing programs. At Northern Range Capital we assist our clients

COMMERCIAL MORTGAGE FINANCING SOLUTIONS Attached is an introduction to NORTHERN RANGE CAPITAL CORP describing some of our unique mortgage financing programs. At Northern Range Capital we assist our clients

SunTrust Community Capital, LLC New Markets Tax Credit Introduction

SunTrust Community Capital, LLC New Markets Tax Credit Introduction STCC Products & Services SunTrust Community Capital (STCC) provides debt and equity capital for projects that economically benefit and

SunTrust Community Capital, LLC New Markets Tax Credit Introduction STCC Products & Services SunTrust Community Capital (STCC) provides debt and equity capital for projects that economically benefit and

2365 Reynolds Ave, North Las Vegas, NV 89030

10% Down $77 psf 7,072' Medical Office Elevator & Gray Shell 2365 Reynolds Ave, North Las Vegas, NV 89030 Listing ID: 29944110 Status: Active Property Type: Office For Sale Office Type: Business Park,

10% Down $77 psf 7,072' Medical Office Elevator & Gray Shell 2365 Reynolds Ave, North Las Vegas, NV 89030 Listing ID: 29944110 Status: Active Property Type: Office For Sale Office Type: Business Park,