2018 Income Tax Update - Commercial Real Estate

|

|

|

- Mark Clark

- 5 years ago

- Views:

Transcription

1 2018 Income Tax Update - Commercial Real Estate Stephen M. Lukinovich, CPA, PFS, CVA Andrew J. Ackermann, CPA, CVA Kentucky Commercial Real Estate Conference Louisville, KY October 30, 2018

2 Tax Cuts and Jobs Act A Member of PrimeGlobal An Association of Independent Accounting Firms 2

3 Commercial Real Estate Taxation 2018 Agenda 1. Expired income tax provisions 2. New tax reform 3. Depreciation updates 4. Updates on tax incentives 5. Opportunity zones 3

4 4

5 Energy Efficient Incentives Expired Effective 1/1/2018: Section 179D Deduction o Up to $1.80/square foot deduction Section 45L - Energy Efficient Home Tax Credit - $2,000 5

full year deduction - Federal, AMT and")

6 179D Lookback Rules Announced by IRS in December 2010 Applies for prior year missed 179D Now available for more than 3 previous tax years Do not amend prior-year tax returns Reflect prior year 179D deductions missed on current year tax return - Form 3115, 481(a) full year deduction - Federal, AMT and State 6

7 7

8 Federal Income Tax Reform Legislation Commercial Real Estate Substantially unchanged are: The rules regarding depreciation tax lives of commercial real property (39 years) Residential real property (27 1/2 years) Long-term capital gain tax rates, generally 20% The application of the 3.8% Medicare Surtax Section 1250 unrecapture rules/tax rate of 25% The tax rules regarding Low Income Housing Tax Credits 8

9 Qualified Business Income Deduction Effective for tax years beginning after Dec. 31, 2017, and before Jan. 1, 2026, an individual taxpayer generally may deduct 20% of domestic qualified business income from a partnership, LLC, S corporation or sole proprietorship Deduction amount for a tax year is the sum of: 1) the lesser of: a) the combined qualified business income amount ; or b) 20% of the excess of taxable income over the sum of i) net capital gain and ii) qualified cooperative dividends; plus 2) the lesser of: 20% of qualified cooperative dividends; or taxable income minus the taxpayer s net capital gain 9

10 QBI Deduction - continued In the case of a partnership or S corporation, the provision applies at the partner/shareholder level Partnership. Each partner takes into account the partner s allocable share of each qualified item of income, gain, deduction, and loss, and is credited with W- 2 wages for the tax year equal to the partner s allocable share of W-2 wages of the partnership Partner s allocable share of W-2 wages is required to be determined in the same manner as the partner s share of wage expenses S corporation Each shareholder of an S corporation takes into account the shareholder s pro rata share of each qualified item of income, gain, deduction, and loss, and is credited with W-2 wages for the year equal to the shareholder s pro rata share of W-2 wages of the corporation. 10

11 QBI Deduction - continued The deduction is generally limited based on greater of a) 50% of W-2 wages paid, or b) the sum of 25% of W-2 wages plus 2.5% of the unadjusted basis of qualified property held by the business (Note: this limitation is phased in above a threshold amount of taxable income) Qualified property must 1) be depreciable tangible property, 2) held at the close of the tax year, 3) used to produce qualified business income, and 4) the property s depreciation period cannot end before the close of the tax year (later of 10 years or last day of MACRS recovery period). The deduction is generally not allowed for certain specified service trades or businesses (Note: this disallowance is also phased in above the threshold amount of taxable income) Threshold amount is $315k MFJ ($157,500 for other taxpayers) Phase-in range is $100k MFJ ($50k for other taxpayers) Fully phased in at $415k MFJ ($207,500 for other taxpayers) 11

12 QBI Deduction - continued Qualified trade or business any trade or business other than a specified service trade or business (phase-in threshold) and other than the trade or business of being an employee Specified service business is any trade or business: involving the performance of services in the fields of accounting, actuarial science, athletics, brokerage services, consulting, financial services, health, law, or the performing arts; or involves the performance of services that consist of investing and investment management, trading or dealing in securities, partnership interests or commodities; or where the principal asset of such trade or business is the reputation or skill of one or more employees or owners. Note: engineering and architecture are not specified service businesses 12

13 QBI Deduction - continued Commercial and residential rental real estate activities (for this purpose only) will generally be considered a trade or business unless in the form of a triple net lease arrangement Self-rental arrangements will need to be carefully reviewed for eligibility of the 20%/2.5% deduction Economic unit self-rental arrangements will require further guidance Owners who are passive, with passive income, will be entitled to this new 20%/2.5% deduction 13

14 14

15 Beginning 1/1/2018 New EBIDTA Interest Expense Limitations 30% EBIDTA Interest Expense limitation applies The 30% of EBITDA interest expense limitation applies to commercial rental real estate activities The 30% interest expense limit is determined at the entity level Entities with less than $25 million in annual sales are exempt Real estate development activities with sales in excess of $25 million can elect ADS depreciation deductions instead o 40-year tax life for commercial rental real estate o 30-year tax life for apartments/single rental residences o 20-year tax life for QIP o Real estate developers that elect ADS depreciation will not be able to take bonus depreciation 15

16 Beginning 1/1/2018 New Like-Kind Exchange Rules Only commercial/investment real estate activities are eligible for tax-free exchange treatment Personal property is no longer eligible If real property (building) has Section 1245 property (personal property) embedded, especially pursuant to a cost segregation study, that portion of the property is ineligible for Section 1031 tax-fee treatment Important to determine the value of Section 1245 property embedded in real property upon pursuing a Section 1031 exchange Cost segregation studies on the replacement property, identifying Section 1245 personal property, with 100% bonus depreciation expense (especially on used property) should assist in minimizing the impact to this tax-free treatment limitation 16

17 Effective 1/1/2018 through 12/31/2025 New Loss Limitation $500,000 Trade or business loss new annual loss limitation Losses incurred by trade or business activities will continue to have basis limitations and the historical passive loss limitations apply $500,000 (MFJ)/$250,000 (MFS/Single) loss limitation Excess loss amounts will be carried forward Watch Cost Segregation Studies 17

18 Cash Basis Method of Accounting Reminder for Commercial Real Estate Activities The new 1/1/2018 $25 million revenue threshold does not apply to commercial rental real estate ventures Since rental real estate ventures do not have inventory, the cash basis method of accounting is generally available to pass-through commercial rental real estate ventures regardless of the level of sales revenue Syndicates are generally required to use the accrual basis method of accounting If 35% or more of the commercial rental real estate venture is owned by passive investors, and losses exist, generally, the activity must be accrual basis method of accounting 18

19 1/1/ Reduced C-Corporate Tax Reduced Tax Rate: Rate Tax years beginning after December 31, 2017, all C- Corporations, including personal service corporations, will be taxed at a 21% flat corporate tax Graduated rate structure is eliminated Corporate AMT repealed Any unused AMT credit carryforward is refundable beginning in 2018 refundable credit is equal to 50% of excess of the credit over amount allowable against the regular tax liability (100% beginning in 2021) 19

20 1/1/2018 Other New Tax Reform Rules Watch for new built in loss rule - applies if $250,000 loss is allocated to an incoming member Most individual income tax rates are lowered, and the top marginal rate is reduced from 39.6% to 37% Expires 12/31/2025 The Tax Reform Bill still permits individuals to itemize and deduct state and local taxes (including property taxes), but only up to $10k 20

21 Kentucky State Tax Update House Bills 366 & 487 broaden tax base Effective 1/1/18 Flat 5 % on business & individuals Effective 7/1/18 Sales tax on services Landscaping & lawn services Janitorial services Labor charges on installation of tangible personal property Others 21

22 22

23 Rental Real Estate Depreciation Effective 1/1/2018: 39 year and 27 ½ year tax lives maintained Special real property depreciation categories eliminated, except for Qualified Improvement Property (QIP) Section 179: $1 Million per year, beginning 1/1/2018 $500k per year through 12/31/

24 New Bonus Depreciation % s - through 12/31/2027 Bonus Depreciation Rates 09/11/01 05/05/03 30% 05/06/03 12/31/04 50% 01/01/05 12/31/07 0% 01/01/08 09/08/10 50% 09/09/10 12/31/11 100% 01/01/12 9/27/17 50% 9/28/17 12/31/22 100% 01/01/23 12/31/27 80% - 20% Watch property with construction contract prior to 9/28/2017 Property no longer needs to be new, beginning 9/28/

25 100% Bonus Depreciation 9/28/2017 through 12/31/2017: Normal qualified real estate categories remain through 12/31/2017, along with their historical tax lives Qualified Leasehold Improvement Property ( QLHI ) Qualified Improvement Property ( QIP ) Qualified Restaurant Property and Qualified Retail Property Used commercial property is now eligible for bonus depreciation, beginning 9/28/2017 QLHI and QIP property that is acquired during the abovereferenced period of time is now eligible for 100% bonus depreciation 25

26 100% Bonus Depreciation 9/28/ /31/2027: Embedded personal property/section 1245 property acquired during this period of time, pursuant to a cost segregation study, qualifies for 100% bonus depreciation, new and used You can elect a lower 50% or 0% bonus depreciation rate, per class effective 9/28/

27 Bonus Depreciation Phase Out 100% Bonus depreciation 1/1/ /31/2022 Bonus depreciation is scheduled to phase-out beginning 1/1/2023 The only qualified real estate property provision that survived, beginning 1/1/2018, is QIP QIP s tax life is now understood to be 15 years Note: There is an anticipated Technical Correction to be issued to permit the tax life of QIP at 15 years and make it eligible for bonus depreciation 27

28 Section 179 Beginning 1/1/2018 is $1 million/year Certain non-residential real property items qualify (QIP, HVAC, roof, security systems, and fire protection systems) NOTE: Normal Section 179 limitations apply. You need formal trade or business income; commercial rental real estate income typically does not qualify for Section 179 unless rising to the level of a formal trade or business activity 28

29 Rev. Proc New Retail & Restaurant Remodel Refresh Safe Harbor Taxpayers engaged in the trade or business of operating a retail establishment or restaurant with safe harbor method of accounting - audited financial statements Includes owners of shopping centers or corporate office with retail shopping Not included: 1245 property, automotive dealers, other motor vehicle dealers, gas stations, manufactured home dealers, nonstore retailers, hotel and motel business operators, civic or social organizations, amusement parks, theaters, casinos, country clubs, caterers 29

30 Rev. Proc New Retail & Restaurant Remodel Refresh Safe Harbor 75% deduction of qualified costs, remaining 25% capitalized and depreciated No disposition of prior costs capitalized 30

31 Qualified Leasehold Improvement Property Any improvement to an interior portion of a building that is nonresidential real property; excludes enlargements, elevators/escalators, common area work and internal structural framework Recovery period: 15 years Straight line method; half-year convention Can be included in Section 179 deduction if trade or business 31

32 Qualified Leasehold Improvement Property Eligible for 50% bonus depreciation 3 year rule applies - placed in service more than three years after the date the building was first placed in service Landlord or lessee can make interior improvement but must be made pursuant to a lease Landlord and tenant cannot be related parties Expires 12/31/

33 Qualified Restaurant Property Any section 1250 property that is a building - new building or existing structure - or an improvement to a building, If more than 50% of the building s square footage is devoted to the preparation of, and seating for onpremises consumption of, prepared meals Recovery period: 15 years Straight line method; half-year convention 33

34 Qualified Restaurant Property Can be included in Section 179 deduction trade or business normally tenant Not eligible for bonus depreciation unless qualified leasehold improvement property 2015 or Q.I.P. in year rule does not apply - placed in service more than three years after the date the building was first placed in service Encompasses the entire building structure as well as interior costs. Can be an acquired building Landlord and tenant can be related parties Expires 12/31/

35 Qualified Retail Improvement Property Effective 1/1/2016 Any improvement to an interior portion of a building which is nonresidential real property. Retail establishments that qualify include those open to the public and primarily in the business of the sale of goods (tangible personal property) to the general public and not services (grocery stores, clothing stores, hardware stores, and convenience stores) Recovery period: 15 years Straight line method; half-year convention Can be included in Section 179 deduction trade or business 35

36 Qualified Retail Improvement Property Effective 1/1/2016 Now eligible for 50% bonus depreciation 3 year rule applies - placed in service more than three years after the date the building was first placed in service Excludes enlargements, elevators/escalators, common area work, and internal structural framework Landlord and tenant can be related parties Building can be owner occupied Expires 12/31/

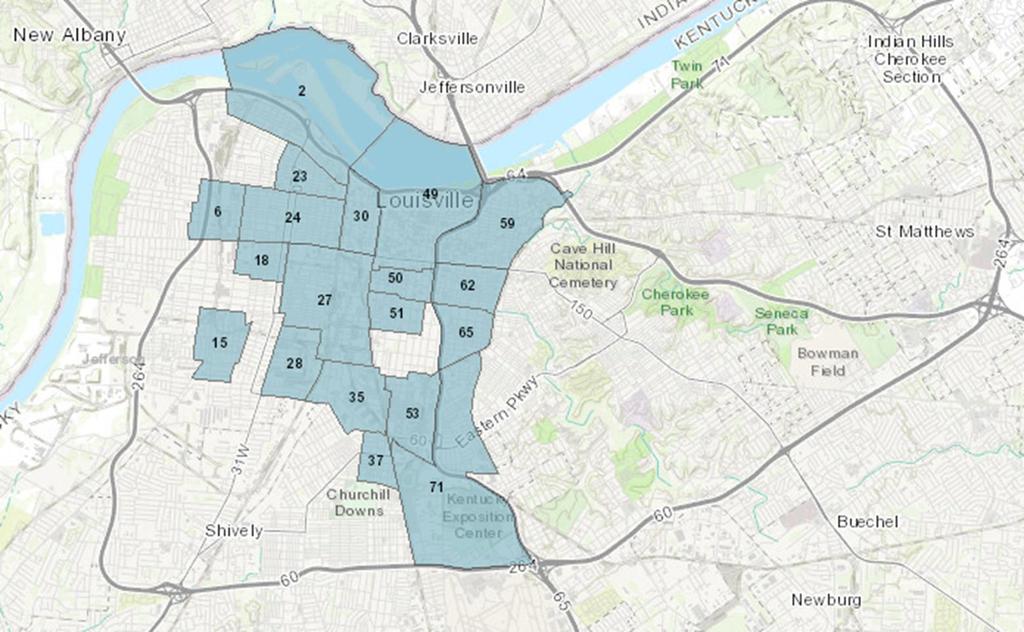

37 Qualified Improvement Property New category 1/1/2016 Effective 1/1/2016 Qualified improvement property is any improvement to an interior portion of a building that is nonresidential real property if the improvement is placed in service after the date the building was first placed in service, excluding: enlargements, elevators/escalators, and internal structural framework The improvements do not need to be made pursuant to a lease, and the building can be owner occupied 39 year tax life, through 12/31/ year tax life, beginning 1/1/2018 Technical Corrections 37

38 Qualified Improvement Property Straight line method; mid-month convention Can be included in Section 179 deduction trade or business Eligible for 50% bonus depreciation 3 year rule does not apply - placed in service more than three years after the date the building was first placed in service Excludes enlargements, elevators/escalators, common area work, and internal structural framework Landlord and tenant can be related parties Building can be owner occupied 38

39 Section 179 Commercial Rental Through 12/31/2017: Real Estate Section 179 deductions of $510,000 with a phase out starting at $2,030,000 Trade or Business only A deduction of $510,000 of Qualified Real Property (Qualified Leasehold Improvement Property, Qualified Restaurant Property, and Qualified Retail Improvement Property) is retroactive for 2017 Max $510,000 39

40 40

41 Historic Tax Credit Historic Tax Credit (HTC): The 10% credit was repealed for pre-1936 buildings The 20% credit for Qualified Rehabilitation Expenses (QRE) was retained with a modification. The credit allowable over a 5-year period Making the credit 4% per year of the QREs 41

42 1/1/2018 New HTC Rules, continued Transition rule to determine if the HTC is claimed under the old law: Was the full 20% in the year placed in service or under the new law, 4% per year over 5 years The taxpayer has a 24- or 60-month window to claim expenditures during rehabilitation If the taxpayer selects to start the window outside of 180 days after December 22, 2017, then the new law applies, otherwise the old law is still in effect 42

43 43

44 Qualified Opportunity Zones Enacted as part of sweeping federal tax legislation commonly referred to as the Tax Cuts and Jobs Act of Significant tax incentives for taxpayers to reinvest capital gains in certain property and businesses located or operating in specially designated tracts. ( QO Zone ). Encourage economic development in low income areas by providing various tax incentives for private investments in qualifying areas Estimated $6.1 trillion in unrealized capital gain at the end of This significant amount of capital available for reinvestment makes the QO Zones program potentially the largest economic development initiative in the country. Designed to channel more equity capital into distressed markets 44

45 Opportunity Zone Designation Treasury has designated QO Zones in all 50 states, the District of Columbia, and five U.S. possessions. In Kentucky, Treasury designated 144 low-income census tracts in 84 counties across the state as QO Zones. 19 designated QO Zones in Jefferson County. 2 designated QO Zones in Bullitt County. In Indiana, Treasury designated 156 tracts in 58 counties covering all or portions of 83 cities and towns throughout the state as QO Zones. 5 designated QO Zones in Clark and Floyd counties. The zones will effectively not change IRS has a listing by state States have websites for confirming QOZ locations 45

46 Designated O Zones in Kentucky Source: 46

47 Designated O Zones in Louisville Source:

48 Designated O Zones in Southern IN Source: 48

49 Designated O Zones in Southern IN Source: 49

50 QO Zone Benefits Qualified Opportunity Zone Funds (QOFs) Defer taxes by making timely investments when invested in Taxpayers Qualified Opportunity Zone Property 50

51 QO Zone Benefits There are three separate investment incentives that a taxpayer can elect to take advantage of with respect to their investment. 1. Initial gain deferral 2. Partial forgiveness 3. Permanent exclusion of gain on appreciation 51

52 Gain Recognition Gain deferral is temporary because the taxpayer must recognize the income in the tax year the investment is sold or the tax year that includes December 31, 2026, whichever is earlier. Gain is calculated as the lessor of: 1. Amount of gain deferred OR 2. The fair market value of investment in QOF interest less the basis in the QOF interest * * Basis is QOF is initially deemed to be zero 52

53 Deferral Period The period of capital gain tax deferral ends upon the earlier of: 53

54 Partial Forgiveness and Permanent Exclusion of Additional Gains Within 180 Days Basis increased by 10% of the deferred gain Up to 90% taxed Basis increased by Additional 5% of the deferred gain Up to 85% taxed Basis is equal to Fair Market Value Exclusion of gains on appreciation of investment 54

55 Example Before April 28, 2019 Taxpayer contributes the $1M of capital gain to a QOF QOF makes a timely investment of the $1M in Qualified Opportunity Zone Property April 28, 2026 (7 years) Taxpayer s basis in investment in QOF increases another 5% from $100k to $150k April 28, 2029 (10 years) Taxpayer sells its investment for $3M. The basis is equal to the FMV. No additional tax is owed on the appreciation. Oct. 30, 2018 Taxpayer enters into a sale that generate $1M of capital gain April 28, 2024 (5 years) Taxpayer s basis in investment in QOF increases 10% from $0 to $100k December 31, 2026 $850k of the $1M of initial capital gains are taxed and the basis in QOF investment increases to $1M Notes: The Taxpayer s initial basis is deemed to be $0 in the QOF investment 55

56 Investment Types in Opportunity Zones Real Estate Development and Rehab Project in Opportunity Zones New Businesses created in Opportunity Zones Expansion of Businesses already in Opportunity Zones Businesses expanding into Opportunity Zones 56

57 Qualified Opportunity Fund - Purpose A QO Fund is any investment vehicle organized as either a partnership (including an LLC treated as a partnership for tax purposes) or corporation that was formed for the purpose of investing in qualified opportunity zone property ( QOZ Property ). At least 90 percent of the QO Fund s assets must consist of QOZ Property. Fund can self certify 57

58 Qualified O Zone Property There are three categories of QOZ Property permitted: 1. Qualified Opportunity Zone Stock (Qualified Opportunity Zone Business) 2. Qualified Opportunity Zone Partnership Interest (Qualified Opportunity Zone Business) 3. Qualified Opportunity Zone Business Property 58

59 Qualified O Zone Stock and Partnership Interests The investment must be acquired after December 31, 2017 solely in exchange for cash; Must be a qualified opportunity zone business, or is being organized for the purpose of being a qualified opportunity zone business; Must remain a qualified opportunity zone business for substantially all of the qualified opportunity fund s holding period 59

60 Qualified O Zone Businesses A trade or business in which substantially all of the tangible property owned or leased by the taxpayer is qualified o zone business property At least 50% of income derived from active conduct Less than 5% of unadjusted basis of property is nonqualified financial property 60

61 Ineligible Businesses Sin Business Golf courses Race tracks Gambling facilities Liquor stores Country clubs Massage parlors Hot tub facilities Tanning facilities 61

62 Qualified O Zone Business Property Tangible property used in a trade or business Acquired by purchase from an unrelated party (20% threshold) after December 31, 2017 During substantially all of holding period, substantially all the use is in a QOZ Substantially all is defined as 70% Original use in the QOZ commences with the taxpayer OR Taxpayer substantially improves the property during any 30-month period after acquisition, additions to basis exceed an amount equal to the adjusted basis of such property at the beginning of such period Guidance allows for reasonable working capital 62

63 Basic Model for Rental Real Estate or direct ownership of QOZ Business Property within 180 days Investors QOF QOZ Partnership QOZ Business Property Rental Real Estate New construction Substantial improvement of adjusted basis excluding land 63

64 Civil Penalties for Noncompliance Failure to meet investment standard results in per month penalty % of shortfall multiplied by underpayment rate No penalty if failure is due to reasonable cause 64

65 Questions? 65

66 IRS Circular 230 Disclosure As a result of perceived abuses, the Treasury has recently promulgated Regulations for practice before the IRS. These Circular 230 regulations require all accountants to provide extensive disclosure when providing certain written tax communications to clients. In order to comply with our obligations under these Regulations, we would like to inform you that any advice given in this presentation, including any attachments, cannot be used to avoid penalties which the IRS might impose, because we have not included all of the information required by Circular 230, nor have we performed services that rise to this level of assurance. 66

67 Thank You! Stephen M. Lukinovich, CPA, PFS, CVA Andrew J. Ackermann, CPA, CVA

IRC 199A Deduction for Qualified Business Income

IRC 199A Deduction for Qualified Business Income What is it? 20% deduction against qualified business income Designed to provide a tax break to owners of pass through entities, in light of substantial

IRC 199A Deduction for Qualified Business Income What is it? 20% deduction against qualified business income Designed to provide a tax break to owners of pass through entities, in light of substantial

Business Changes in the Tax Cuts and Jobs Act. Alan D. Sobel, CPA December 27,

Business Changes in the Tax Cuts and Jobs Act Alan D. Sobel, CPA December 27, 2017 Alan.sobel@sobelcollc.com 973-994-9494 Background Most significant tax legislation since 1986 503 pages of legislation

Business Changes in the Tax Cuts and Jobs Act Alan D. Sobel, CPA December 27, 2017 Alan.sobel@sobelcollc.com 973-994-9494 Background Most significant tax legislation since 1986 503 pages of legislation

WHAT IT MEANS FOR CONTRACTORS AND REAL ESTATE EXECUTIVES

Tax Reform: WHAT IT MEANS FOR CONTRACTORS AND REAL ESTATE EXECUTIVES Presented By: JOHN HELLER, CPA Manager Tax Services Group Agenda We will cover: Review Corporate Tax Changes Business Deduction Changes

Tax Reform: WHAT IT MEANS FOR CONTRACTORS AND REAL ESTATE EXECUTIVES Presented By: JOHN HELLER, CPA Manager Tax Services Group Agenda We will cover: Review Corporate Tax Changes Business Deduction Changes

Taking Advantage of Opportunity Zones: A Panel Discussion. Presented by Buchanan Ingersoll & Rooney Tampa October 2018

Taking Advantage of Opportunity Zones: A Panel Discussion Presented by Buchanan Ingersoll & Rooney Tampa October 2018 Florida Opportunity Zones Potential to eliminate poverty Areas with business activity

Taking Advantage of Opportunity Zones: A Panel Discussion Presented by Buchanan Ingersoll & Rooney Tampa October 2018 Florida Opportunity Zones Potential to eliminate poverty Areas with business activity

GAINING MOMENTUM IN OUR NEW TAX ENVIRONMENT: Moving Forward with Confidence

CLICK TO EDIT MASTER TEXT STYLES GAINING MOMENTUM IN OUR NEW TAX ENVIRONMENT: Moving Forward with Confidence Sno L. Barry, CPA, MST Cathy Jackson, CPA, MST CLICK TO EDIT MASTER AREAS TEXT OF INTEREST STYLES

CLICK TO EDIT MASTER TEXT STYLES GAINING MOMENTUM IN OUR NEW TAX ENVIRONMENT: Moving Forward with Confidence Sno L. Barry, CPA, MST Cathy Jackson, CPA, MST CLICK TO EDIT MASTER AREAS TEXT OF INTEREST STYLES

Tax Cuts and Jobs Act. Issues Impacting the Real Estate Industry

Tax Cuts and Jobs Act Issues Impacting the Real Estate Industry Tax Cuts and Jobs Act Issues Impacting the Real Estate Industry On December 22, 2017, President Trump signed the Tax Cuts and Jobs Act (the

Tax Cuts and Jobs Act Issues Impacting the Real Estate Industry Tax Cuts and Jobs Act Issues Impacting the Real Estate Industry On December 22, 2017, President Trump signed the Tax Cuts and Jobs Act (the

New Tax Rules. For You and Your Business Owners

New Tax Rules For You and Your Business Owners 199A-The 20% Deduction for Pass Throughs The New Rules for Meals & Entertainment QSBS-Qualified Small Business Stock And the New Depreciation Rules Presented

New Tax Rules For You and Your Business Owners 199A-The 20% Deduction for Pass Throughs The New Rules for Meals & Entertainment QSBS-Qualified Small Business Stock And the New Depreciation Rules Presented

The Good, The Bad and the Ugly: Tax Reform in 2018 and Beyond

The Good, The Bad and the Ugly: Tax Reform in 2018 and Beyond Presenters: Timothy M. Tikalsky, CPA Date: May 18, 2018 1 RINA accountancy corporation www.rina.com Tax Cuts and Jobs Act Tax Cuts and Jobs

The Good, The Bad and the Ugly: Tax Reform in 2018 and Beyond Presenters: Timothy M. Tikalsky, CPA Date: May 18, 2018 1 RINA accountancy corporation www.rina.com Tax Cuts and Jobs Act Tax Cuts and Jobs

Tax Benefits of Investing in Opportunity Zones

Tax Benefits of Investing in Opportunity Zones Bradley J. Sklar ASCPA Montgomery, Alabama Opportunity Zones Created as part of the Tax Cut and Jobs Act of 2017 Purpose of Opportunity Zones To generate

Tax Benefits of Investing in Opportunity Zones Bradley J. Sklar ASCPA Montgomery, Alabama Opportunity Zones Created as part of the Tax Cut and Jobs Act of 2017 Purpose of Opportunity Zones To generate

How Does Tax Reform Affect Real Estate Developers & Investors?

How Does Tax Reform Affect Real Estate Developers & Investors? FEBRUARY 20, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar

How Does Tax Reform Affect Real Estate Developers & Investors? FEBRUARY 20, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar

Tax Planning for Real Estate Under the TCJA

By now, you have been bombarded with summaries and articles on the 507-page tax bill, formerly known as the Tax Cuts and Jobs Act of 2017, and signed into law by President Trump on Dec. 22, 2017 (the Act).

By now, you have been bombarded with summaries and articles on the 507-page tax bill, formerly known as the Tax Cuts and Jobs Act of 2017, and signed into law by President Trump on Dec. 22, 2017 (the Act).

How Tax Reforms Impacts Your Vineyard February 8, Presented by: Kathy Freshwater, CPA Craig Anderson, CPA

How Tax Reforms Impacts Your Vineyard February 8, 2018 Presented by: Kathy Freshwater, CPA Craig Anderson, CPA Presenters Kathy Freshwater Tax Senior Manager Yakima Craig Anderson Tax Partner Yakima High

How Tax Reforms Impacts Your Vineyard February 8, 2018 Presented by: Kathy Freshwater, CPA Craig Anderson, CPA Presenters Kathy Freshwater Tax Senior Manager Yakima Craig Anderson Tax Partner Yakima High

Tax Reform Highlights

etax Alert Tax Reform Highlights Final Business/Corporate/Partnership Provisions in Tax Cuts and Jobs Act of 2017 Here is a chart that briefly summarizes the major provisions affecting our business clients,

etax Alert Tax Reform Highlights Final Business/Corporate/Partnership Provisions in Tax Cuts and Jobs Act of 2017 Here is a chart that briefly summarizes the major provisions affecting our business clients,

Investing in Opportunity Zones

Investing in Opportunity Zones for the 2018 Defense Communities National Summit Gregory Clements Partner, Dover Novogradac & Company LLP gregory.clements@novoco.com Taxpayers can get capital gains tax

Investing in Opportunity Zones for the 2018 Defense Communities National Summit Gregory Clements Partner, Dover Novogradac & Company LLP gregory.clements@novoco.com Taxpayers can get capital gains tax

The Eagerly Awaited Opportunity Zone Regulations: What Do They Tell Us and What Do We Still Need to Figure Out?

The Eagerly Awaited Opportunity Zone Regulations: What Do They Tell Us and What Do We Still Need to Figure Out? Lisa M. Starczewski, Esq. Co-Chair, Tax Section & Opportunity Zones Team Buchanan Ingersoll

The Eagerly Awaited Opportunity Zone Regulations: What Do They Tell Us and What Do We Still Need to Figure Out? Lisa M. Starczewski, Esq. Co-Chair, Tax Section & Opportunity Zones Team Buchanan Ingersoll

What the Tax Cuts and Jobs Act Means for the Real Estate Industry

What the Tax Cuts and Jobs Act Means for the Real Estate Industry PRESENTED BY: ADAM HILL, CPA, PARTNER JON WILLIAMSON, CPA, MT, TAX MANAGER KIM PALMER, CPA, MT, PARTNER February 1, 2018 Welcome & Introductions

What the Tax Cuts and Jobs Act Means for the Real Estate Industry PRESENTED BY: ADAM HILL, CPA, PARTNER JON WILLIAMSON, CPA, MT, TAX MANAGER KIM PALMER, CPA, MT, PARTNER February 1, 2018 Welcome & Introductions

The Tax Cuts and Jobs Act1 (TCJA) made

made") Significant Provisions of the Tax Cuts and Jobs Act Affecting Closely Held Businesses and Their Owners by Gerald A. Shanker The Tax Cuts and Jobs Act1 (TCJA) made significant changes to the Internal Revenue

Significant Provisions of the Tax Cuts and Jobs Act Affecting Closely Held Businesses and Their Owners by Gerald A. Shanker The Tax Cuts and Jobs Act1 (TCJA) made significant changes to the Internal Revenue

Tax Cuts and Jobs Act

Tax Cuts and Jobs Act Presenters: Timothy M. Tikalsky, CPA Date: February 6, 2018 1 RINA accountancy corporation www.rina.com Tax Cuts and Jobs Act Tax Cuts and Jobs Act (TCJA) Name given by House in H.R.

Tax Cuts and Jobs Act Presenters: Timothy M. Tikalsky, CPA Date: February 6, 2018 1 RINA accountancy corporation www.rina.com Tax Cuts and Jobs Act Tax Cuts and Jobs Act (TCJA) Name given by House in H.R.

Real Estate Journal TM

Real Estate Journal TM Reproduced with permission from, V. 34, 11, p. 214, 11/07/2018. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com The Eagerly Awaited Opportunity

Real Estate Journal TM Reproduced with permission from, V. 34, 11, p. 214, 11/07/2018. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com The Eagerly Awaited Opportunity

Tax Cuts and Jobs Act Real Estate Industry Impact. April 30, 2018 Mary Beth Saylor, CPA Brent A. Wilkinson, CPA, JD

Tax Cuts and Jobs Act Real Estate Industry Impact April 30, 2018 Mary Beth Saylor, CPA Brent A. Wilkinson, CPA, JD Topics for Today Rate Changes Business Interest Limitation Net Operating Losses Excess

Tax Cuts and Jobs Act Real Estate Industry Impact April 30, 2018 Mary Beth Saylor, CPA Brent A. Wilkinson, CPA, JD Topics for Today Rate Changes Business Interest Limitation Net Operating Losses Excess

2017 Tax Cuts and Jobs Act: Impact on U.S. Real Estate Businesses

CLIENT MEMORANDUM 2017 Tax Cuts and Jobs Act: Impact on U.S. Real Estate Businesses January 30, 2018 The new tax act signed into law on December 22, 2017, popularly known as the Tax Cuts and Jobs Act (

CLIENT MEMORANDUM 2017 Tax Cuts and Jobs Act: Impact on U.S. Real Estate Businesses January 30, 2018 The new tax act signed into law on December 22, 2017, popularly known as the Tax Cuts and Jobs Act (

INSIGHT: The Eagerly Awaited Opportunity Zone Regulations: What Do They Tell Us and What Do We Still Need to Figure Out?

bloombergbna.com Reproduced with permission. Published October 23, 2018. Copyright 2018 The Bureau of National Affairs, Inc. 800-372-1033. For further use, please visit http://www.bna.com/copyright-permission-request/

bloombergbna.com Reproduced with permission. Published October 23, 2018. Copyright 2018 The Bureau of National Affairs, Inc. 800-372-1033. For further use, please visit http://www.bna.com/copyright-permission-request/

Overview Snell & Wilmer

Overview History of Opportunity Zone Program Opportunity Zones Qualification and Designation Tax Benefits of the Opportunity Zone Program Opportunity Funds What are the rules, how do you qualify? Opportunity

Overview History of Opportunity Zone Program Opportunity Zones Qualification and Designation Tax Benefits of the Opportunity Zone Program Opportunity Funds What are the rules, how do you qualify? Opportunity

National Housing & Rehabilitation Association Spring Developers Forum

National Housing & Rehabilitation Association Spring Developers Forum May 7-8, 2018 Marina del Rey, CA Sponsors: Leveraging Qualified Opportunity Zones: Development & Finance Strategies Laura Burns Eagle

National Housing & Rehabilitation Association Spring Developers Forum May 7-8, 2018 Marina del Rey, CA Sponsors: Leveraging Qualified Opportunity Zones: Development & Finance Strategies Laura Burns Eagle

Investing in Opportunity Act

Investing in Opportunity Act MODERATOR John Sciarretti Novogradac & Company LLP PANELISTS Joseph Bredehoft Husch Blackwell Jonathan Goldstein Advantage Capital Neil Faden Manatt, Phelps & Phillips LLP

Investing in Opportunity Act MODERATOR John Sciarretti Novogradac & Company LLP PANELISTS Joseph Bredehoft Husch Blackwell Jonathan Goldstein Advantage Capital Neil Faden Manatt, Phelps & Phillips LLP

5/29/ TAX CUTS AND JOBS ACT OVERVIEW. Individual Tax. Introduction-Individual Provisions. Dauphin County Bar Association May 30, 2018

2017 TAX CUTS AND JOBS ACT OVERVIEW Dauphin County Bar Association May 30, 2018 Individual Tax 2 Introduction-Individual Provisions In general, the individual provisions go into effect starting on January

2017 TAX CUTS AND JOBS ACT OVERVIEW Dauphin County Bar Association May 30, 2018 Individual Tax 2 Introduction-Individual Provisions In general, the individual provisions go into effect starting on January

Tax Cuts and Jobs Act Changes Impacting Real Estate. Presented by: Sefi Silverstein, CPA Len Nitti, CPA, MST

Tax Cuts and Jobs Act Changes Impacting Real Estate Presented by: Sefi Silverstein, CPA Len Nitti, CPA, MST Our Speakers Sefi Silverstein, CPA Len Nitti, CPA, MST 2 Housekeeping To submit questions use

Tax Cuts and Jobs Act Changes Impacting Real Estate Presented by: Sefi Silverstein, CPA Len Nitti, CPA, MST Our Speakers Sefi Silverstein, CPA Len Nitti, CPA, MST 2 Housekeeping To submit questions use

Tax Cuts and Jobs Act Construction Industry Impact

Tax Cuts and Jobs Act Construction Industry Impact Presented By: Sean M. Auger, Partner 1 Introduction Most but not all provisions effective for tax periods beginning after December 31, 2017 2 General

Tax Cuts and Jobs Act Construction Industry Impact Presented By: Sean M. Auger, Partner 1 Introduction Most but not all provisions effective for tax periods beginning after December 31, 2017 2 General

Overview of TCJA Changes Affecting Businesses. Reduction in Corporate Tax Rate and Dividends Received Deduction

We have compiled the following summary of the Tax Cuts & Jobs Act. These changes are very extensive and we are still waiting on regulations to be written to explain some things in more detail. We will

We have compiled the following summary of the Tax Cuts & Jobs Act. These changes are very extensive and we are still waiting on regulations to be written to explain some things in more detail. We will

K E Y N O T E S P E A K E R S

K E Y N O T E S P E A K E R S R o b e r t W i e b e, C P A Ro b e r t W @ w h h c p a s. c o m B e n H u b b e ll, C P A Be n H @ w h h c p a s. c o m 2 P R E S E N T A T I O N O U T L I N E 1. History

K E Y N O T E S P E A K E R S R o b e r t W i e b e, C P A Ro b e r t W @ w h h c p a s. c o m B e n H u b b e ll, C P A Be n H @ w h h c p a s. c o m 2 P R E S E N T A T I O N O U T L I N E 1. History

TAX REFORM CORPORATE & BUSINESS

The following chart sets forth some of the provisions affecting businesses in H.R. 1, originally called the Tax Cuts and Jobs Act (the Act), as signed by President Donald Trump on December 22, 2017. This

The following chart sets forth some of the provisions affecting businesses in H.R. 1, originally called the Tax Cuts and Jobs Act (the Act), as signed by President Donald Trump on December 22, 2017. This

TAX REFORM CORPORATE & BUSINESS

The following chart sets forth some of the provisions affecting businesses in the Tax Reform Act of 2017 (the Act). This chart highlights only some of the key issues and is not intended to address all

The following chart sets forth some of the provisions affecting businesses in the Tax Reform Act of 2017 (the Act). This chart highlights only some of the key issues and is not intended to address all

OPPORTUNITY ZONES GAIN DEFERRAL AND ELIMINATION ADAM M. COHEN

OPPORTUNITY ZONES GAIN DEFERRAL AND ELIMINATION ADAM M. COHEN COLORADO OPPORTUNITY ZONES 2 OPPORTUNITY ZONE BENEFITS 1. Initial Gain Deferral 2. Initial Gain Reduction 3. O-Zone Gain Elimination 3 GAIN

OPPORTUNITY ZONES GAIN DEFERRAL AND ELIMINATION ADAM M. COHEN COLORADO OPPORTUNITY ZONES 2 OPPORTUNITY ZONE BENEFITS 1. Initial Gain Deferral 2. Initial Gain Reduction 3. O-Zone Gain Elimination 3 GAIN

Business Tax. Pass-Through Entities. New 20% Deduction

Business Tax Pass-Through Entities New 20% Deduction For tax years beginning after Dec. 31, 2017, and before Jan. 1, 2026, taxpayers who have domestic qualified business income (QBI) from a partnership,

Business Tax Pass-Through Entities New 20% Deduction For tax years beginning after Dec. 31, 2017, and before Jan. 1, 2026, taxpayers who have domestic qualified business income (QBI) from a partnership,

Investing in Opportunity Act IIOA 2017 Tax Cuts & Jobs Act

Investing in Opportunity Act IIOA 2017 Tax Cuts & Jobs Act Tara Sherbert, CEO of The Sherbert Group The Sherbert Group is a unique integration of companies that provide valuable tax, accounting, investment

Investing in Opportunity Act IIOA 2017 Tax Cuts & Jobs Act Tara Sherbert, CEO of The Sherbert Group The Sherbert Group is a unique integration of companies that provide valuable tax, accounting, investment

Opportunity Zone Program Tax Cuts and Jobs Act

Opportunity Zone Program Tax Cuts and Jobs Act Marc L. Schultz (602) 382-6358 mschultz@swlaw.com Jason Brinkley (303) 634-2066 jbrinkley@swlaw.com Nicole Ament (303) 223-1174 nament@bhfs.com 1 Overview

Opportunity Zone Program Tax Cuts and Jobs Act Marc L. Schultz (602) 382-6358 mschultz@swlaw.com Jason Brinkley (303) 634-2066 jbrinkley@swlaw.com Nicole Ament (303) 223-1174 nament@bhfs.com 1 Overview

Client Letter: Year-End Tax Planning for 2018 (Business)

") Client Letter: Year-End Tax Planning for 2018 (Business) As I'm sure you're aware, the Tax Cuts and Jobs Act of 2017 (TCJA) was enacted at the end of last year. It's the largest tax overhaul since the

Client Letter: Year-End Tax Planning for 2018 (Business) As I'm sure you're aware, the Tax Cuts and Jobs Act of 2017 (TCJA) was enacted at the end of last year. It's the largest tax overhaul since the

2017 Year-End Tax Planning for Businesses BSB LLC

2017 Year-End Tax Planning for Businesses BSB LLC 2017 Year-End Tax Planning for Businesses The time to consider tax-saving opportunities for your business is before its tax year-end. Some of these opportunities

2017 Year-End Tax Planning for Businesses BSB LLC 2017 Year-End Tax Planning for Businesses The time to consider tax-saving opportunities for your business is before its tax year-end. Some of these opportunities

Let s Talk Taxes. Jim Forbes, CPA. February 12, 2013

Let s Talk Taxes Jim Forbes, CPA February 12, 2013 The income tax had made more liars out of the American people than golf. Will Rogers AGENDA The hardest thing in the world to understand is the income

Let s Talk Taxes Jim Forbes, CPA February 12, 2013 The income tax had made more liars out of the American people than golf. Will Rogers AGENDA The hardest thing in the world to understand is the income

Renewal of Bonus Depreciation & Enhanced Expensing Offers Tax-saving Opportunities

Renewal of Bonus Depreciation & Enhanced Expensing Offers Tax-saving Opportunities The recently enacted "Protecting Americans from Tax Hikes (PATH) Act of 2015" (P.L. 114-113, 12/18/2015) made a number

Renewal of Bonus Depreciation & Enhanced Expensing Offers Tax-saving Opportunities The recently enacted "Protecting Americans from Tax Hikes (PATH) Act of 2015" (P.L. 114-113, 12/18/2015) made a number

Comparison of Current Tax Law, House and Senate Tax Reform Bills, and Conference Report. December 15, 2017 INSURANCE PROVISIONS...

Comparison of Current Tax Law, House and Senate Tax Reform Bills, and Conference Report December 15, 2017 INSURANCE PROVISIONS...2 COMPENSATION AND RETIREMENT SAVINGS PROVISIONS...5 GENERAL BUSINESS PROVISIONS...7

Comparison of Current Tax Law, House and Senate Tax Reform Bills, and Conference Report December 15, 2017 INSURANCE PROVISIONS...2 COMPENSATION AND RETIREMENT SAVINGS PROVISIONS...5 GENERAL BUSINESS PROVISIONS...7

Tax Reform: What Dealers Need to Know

Tax Reform: What Dealers Need to Know 1 Disclosure To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication is not intended or written

Tax Reform: What Dealers Need to Know 1 Disclosure To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication is not intended or written

Business Tax Provisions

On December 22, 2017, President Trump signed the Tax Jobs and Cuts Act of 2017 (the Act). This will be the biggest tax overhaul in 30 years. The provisions below affect all entities from individuals to

On December 22, 2017, President Trump signed the Tax Jobs and Cuts Act of 2017 (the Act). This will be the biggest tax overhaul in 30 years. The provisions below affect all entities from individuals to

A PRIMER ON THE NEW FEDERAL QUALIFIED OPPORTUNITY ZONE PROVISIONS*

A PRIMER ON THE NEW FEDERAL QUALIFIED OPPORTUNITY ZONE PROVISIONS* By: Alveno N. Castilla and Ashley N. Wicks** Background For many years, the Internal Revenue Code has provided various incentives aimed

A PRIMER ON THE NEW FEDERAL QUALIFIED OPPORTUNITY ZONE PROVISIONS* By: Alveno N. Castilla and Ashley N. Wicks** Background For many years, the Internal Revenue Code has provided various incentives aimed

Guidance on Opportunity Zone Structuring & Capital Gain Deferral DECEMBER 12, 2018

Guidance on Opportunity Zone Structuring & Capital Gain Deferral DECEMBER 12, 2018 New IRC 1400Z-1 & 2 The new IRC 1400Z-1 & -2 establish an entirely novel & completely different regimen for deferring

Guidance on Opportunity Zone Structuring & Capital Gain Deferral DECEMBER 12, 2018 New IRC 1400Z-1 & 2 The new IRC 1400Z-1 & -2 establish an entirely novel & completely different regimen for deferring

Tax Credits for Small Wineries. Winery and Wine Distribution Law

Tax Credits for Small Wineries Winery and Wine Distribution Law Marc R. Greenough Foster Pepper PLLC Quincy, Washington August 5, 2008 Tax Credits for Small Wineries Under the Internal Revenue Code of

Tax Credits for Small Wineries Winery and Wine Distribution Law Marc R. Greenough Foster Pepper PLLC Quincy, Washington August 5, 2008 Tax Credits for Small Wineries Under the Internal Revenue Code of

Puerto Rico designated as an Opportunity Zone

Puerto Rico designated as an Opportunity Zone Francisco Luis, CPA, JD Tax Partner February 2019 DISCLAIMER: This presentation and its content do not constitute advice. Attendants should not act solely

Puerto Rico designated as an Opportunity Zone Francisco Luis, CPA, JD Tax Partner February 2019 DISCLAIMER: This presentation and its content do not constitute advice. Attendants should not act solely

A DEEPER LOOK Tax Reform: Corporations. the date on which a written binding contract is entered into for such acquisition.

A DEEPER LOOK 2017 Tax Reform: Corporations Corporate Tax Rates Reduced corporate tax rate is a flat 21% rate. Dividends-Received Deduction Percentages Reduced 80% dividends received deduction is reduced

A DEEPER LOOK 2017 Tax Reform: Corporations Corporate Tax Rates Reduced corporate tax rate is a flat 21% rate. Dividends-Received Deduction Percentages Reduced 80% dividends received deduction is reduced

Opportunity Zones Overview: Basics and Concepts

Opportunity Zones Overview: Basics and Concepts Ryan Brunton Husch Blackwell LLP ryan.brunton@huschblackwell.com RJ McArthur Plante Moran RJ.McArthur@plantemoran.com Benefits of the Opportunity Zone Incentive

Opportunity Zones Overview: Basics and Concepts Ryan Brunton Husch Blackwell LLP ryan.brunton@huschblackwell.com RJ McArthur Plante Moran RJ.McArthur@plantemoran.com Benefits of the Opportunity Zone Incentive

Opportunity Zones: The Latest

Opportunity Zones: The Latest November 15, 2018 National Development Council 2 Agenda Why invest in an Opportunity Zone fund? How did Opportunity Zones come to be? Steps in the Opportunity Zone Process

Opportunity Zones: The Latest November 15, 2018 National Development Council 2 Agenda Why invest in an Opportunity Zone fund? How did Opportunity Zones come to be? Steps in the Opportunity Zone Process

TAX CUTS AND JOB ACT OF 2017 Highlights

2017 TAX CUTS AND JOB ACT OF 2017 Highlights UPDATED January 9, 2018 www.cordascocpa.com TAX CUTS AND JOBS ACT OF 2017 INTRODUCTION After months of intense negotiations, the President signed the Tax Cuts

2017 TAX CUTS AND JOB ACT OF 2017 Highlights UPDATED January 9, 2018 www.cordascocpa.com TAX CUTS AND JOBS ACT OF 2017 INTRODUCTION After months of intense negotiations, the President signed the Tax Cuts

The Top 6 New Tax Bill Provisions Impacting the Real Estate Industry

The Top 6 New Tax Bill Provisions Impacting the Real Estate Industry The 2018 Tax Bill contains many major changes to the tax landscape for both businesses and individuals. Below are some key highlights

The Top 6 New Tax Bill Provisions Impacting the Real Estate Industry The 2018 Tax Bill contains many major changes to the tax landscape for both businesses and individuals. Below are some key highlights

Investment in Federal Opportunity Zones

Investment in Federal Opportunity Zones Opportunity Zones Overview What is the basic concept behind the legislation? A new community development program established by Congress that encourages long-term

Investment in Federal Opportunity Zones Opportunity Zones Overview What is the basic concept behind the legislation? A new community development program established by Congress that encourages long-term

Business tax highlights

Legislative Update Tax Cuts and Jobs Act Business tax highlights Table of contents Overview...1 C corporation changes... 2 Pass-through entity deduction... 3 Executive compensation... 7 Planning opportunities..

Legislative Update Tax Cuts and Jobs Act Business tax highlights Table of contents Overview...1 C corporation changes... 2 Pass-through entity deduction... 3 Executive compensation... 7 Planning opportunities..

New Tax Law: Issues for Partnerships, S corporations, and Their Owners

New Tax Law: Issues for Partnerships, S corporations, and Their Owners January 18, 2018 1 Introduction H.R. 1, originally known as the Tax Cuts and Jobs Act, was signed into law on December 22, 2017. The

New Tax Law: Issues for Partnerships, S corporations, and Their Owners January 18, 2018 1 Introduction H.R. 1, originally known as the Tax Cuts and Jobs Act, was signed into law on December 22, 2017. The

Lowell and Lawrence, Massachusetts Renewal Communities Incentives

Lowell and Lawrence, Massachusetts Renewal Communities Incentives An Initiative of the U. S. Department of Housing and Urban Development based on tax incentives authorized by the Community Renewal Tax

Lowell and Lawrence, Massachusetts Renewal Communities Incentives An Initiative of the U. S. Department of Housing and Urban Development based on tax incentives authorized by the Community Renewal Tax

HFMA Annual AccounTing and AudiTing UpdaTe. Tax UpdaTe

HFMA Annual AccounTing and AudiTing UpdaTe Tax UpdaTe Presented by: Jeffrey J. Petrell, JD, CPA, CGMA Partner Health Care Tax Services Kelly A. Brocious, CPA Senior Manager Health Care Tax Services 97

HFMA Annual AccounTing and AudiTing UpdaTe Tax UpdaTe Presented by: Jeffrey J. Petrell, JD, CPA, CGMA Partner Health Care Tax Services Kelly A. Brocious, CPA Senior Manager Health Care Tax Services 97

Tax Cuts and Jobs Act Questions and Answers for Small Businesses

Tax Cuts and Jobs Act Questions and Answers for Small Businesses February, 2018 This is a summary of items that are subject to variations and exceptions. It is not to be relied upon as tax advice. For

Tax Cuts and Jobs Act Questions and Answers for Small Businesses February, 2018 This is a summary of items that are subject to variations and exceptions. It is not to be relied upon as tax advice. For

SENATE TAX REFORM PROPOSAL CORPORATE & BUSINESS

The following chart sets forth some of the provisions affecting businesses in the Senate Finance Committee s version of the Tax Cuts and Jobs Act bill, as approved by the Senate Finance Committee on November

The following chart sets forth some of the provisions affecting businesses in the Senate Finance Committee s version of the Tax Cuts and Jobs Act bill, as approved by the Senate Finance Committee on November

ANALYSIS OF QUALIFIED OPPORTUNITY ZONES

March 15, 2018 Updated May 10, 2018 ANALYSIS OF QUALIFIED OPPORTUNITY ZONES This document provides a detailed analysis of the newly created tax incentives for investments in Qualified Opportunity Zones

March 15, 2018 Updated May 10, 2018 ANALYSIS OF QUALIFIED OPPORTUNITY ZONES This document provides a detailed analysis of the newly created tax incentives for investments in Qualified Opportunity Zones

12/19/2018 THOUGHTWARE. Financial Services THOUGHTWARE. Tax Reform Update. Income Tax Update for Financial Institutions

THOUGHTWARE Financial Services THOUGHTWARE Financial Services Tax Reform Update Income Tax Update for Financial Institutions December 20, 2018 1 To Receive CPE Credit Individuals Participate in entire

THOUGHTWARE Financial Services THOUGHTWARE Financial Services Tax Reform Update Income Tax Update for Financial Institutions December 20, 2018 1 To Receive CPE Credit Individuals Participate in entire

SELECTED BUSINESS TAX BREAKS MADE PERMANENT

breaks for 2015 and 2016: 1) Deduction (up to $4,000) for Qualified Higher Education Expenses; and 2) Deduction for Mortgage Insurance Premiums as Qualified Residence Interest. In addition, the following

breaks for 2015 and 2016: 1) Deduction (up to $4,000) for Qualified Higher Education Expenses; and 2) Deduction for Mortgage Insurance Premiums as Qualified Residence Interest. In addition, the following

Tax reform and the choice of business entity

The Adviser s Guide to Financial and Estate Planning: Tax reform and the choice of business entity Presented by: Steven G. Siegel, JD, LLM About the PFP Section & PFS Credential The AICPA Personal Financial

The Adviser s Guide to Financial and Estate Planning: Tax reform and the choice of business entity Presented by: Steven G. Siegel, JD, LLM About the PFP Section & PFS Credential The AICPA Personal Financial

Tax Incentives for Investments in Opportunity Zones: New Regulations Provide Clarity and More Questions

Tax Incentives for Investments in Opportunity Zones: New Regulations Provide Clarity and More Questions October 30, 2018 The 2017 Federal Tax Reform bill enacted a new set of tax incentives for investments

Tax Incentives for Investments in Opportunity Zones: New Regulations Provide Clarity and More Questions October 30, 2018 The 2017 Federal Tax Reform bill enacted a new set of tax incentives for investments

Tax Cuts and Jobs Act of 2017

Tax Cuts and Jobs Act of 2017 Introduction After months of intense negotiations, the President signed the Tax Cuts And Jobs Act Of 2017 (the New Law ) on December 22, 2017 - the most significant tax reform

Tax Cuts and Jobs Act of 2017 Introduction After months of intense negotiations, the President signed the Tax Cuts And Jobs Act Of 2017 (the New Law ) on December 22, 2017 - the most significant tax reform

Taxpayers may recharacterize contributions to one type of IRA (traditional or Roth) as a contribution to the other type of IRA.

as a contribution to the other type of IRA.") BENEFITS Affordable Care Act Individual Mandate Under the Affordable Care Act, individuals must have minimum essential The individual responsibility payment is reduced to $0 effective for months beginning

BENEFITS Affordable Care Act Individual Mandate Under the Affordable Care Act, individuals must have minimum essential The individual responsibility payment is reduced to $0 effective for months beginning

Tax Update: Legislative Developments and Tax Planning for Law Firms and Attorneys

Tax Update: Legislative Developments and Tax Planning for Law Firms and Attorneys Presented by Kristin Bettorf, CPA FM24 5/4/2018 4:15 PM The handout(s) and presentation(s) attached are copyright and trademark

Tax Update: Legislative Developments and Tax Planning for Law Firms and Attorneys Presented by Kristin Bettorf, CPA FM24 5/4/2018 4:15 PM The handout(s) and presentation(s) attached are copyright and trademark

TAX CUTS & JOBS ACT DEVELOPMENTS

TAX CUTS & JOBS ACT DEVELOPMENTS P L A N N I N G F O R B U S I N E S S E S A N D I N D I V I D U A L S D E C E M B E R 1 2, 2 0 1 8 THE TAX CUTS & JOBS ACT AT A GLANCE BUSINESS PROVISIONS Reduced Tax Rates

TAX CUTS & JOBS ACT DEVELOPMENTS P L A N N I N G F O R B U S I N E S S E S A N D I N D I V I D U A L S D E C E M B E R 1 2, 2 0 1 8 THE TAX CUTS & JOBS ACT AT A GLANCE BUSINESS PROVISIONS Reduced Tax Rates

Big Changes for Health Care Entities TA X C U T S & J O B S A C T O F

Big Changes for Health Care Entities TA X C U T S & J O B S A C T O F 2 0 1 7 OUR GOAL FOR TODAY Develop an awareness of the recent law changes that will affect healthcare organizations OUR GOAL FOR TODAY

Big Changes for Health Care Entities TA X C U T S & J O B S A C T O F 2 0 1 7 OUR GOAL FOR TODAY Develop an awareness of the recent law changes that will affect healthcare organizations OUR GOAL FOR TODAY

Limit on business interest deduction. Under the new law, every business, regardless of its form, is limited to a deduction for business interest equal

Dear Client, The recently enacted Tax Cuts and Jobs Act ("TCJA") is a sweeping tax package. Here's an overview of some of the more important business tax changes in the new law. Unless otherwise noted,

Dear Client, The recently enacted Tax Cuts and Jobs Act ("TCJA") is a sweeping tax package. Here's an overview of some of the more important business tax changes in the new law. Unless otherwise noted,

Depreciation In General

Accelerating Tax Deductions for Real Estate Review of Accelerated Depreciation and Repair Rules 2017 Schenck Real Estate Forum Ryan Sonnenberg, CPA Manager Depreciation In General Recover cost of asset

Accelerating Tax Deductions for Real Estate Review of Accelerated Depreciation and Repair Rules 2017 Schenck Real Estate Forum Ryan Sonnenberg, CPA Manager Depreciation In General Recover cost of asset

2018 Year-End Tax Planning for Businesses

2018 Year-End Tax Planning for Businesses Guilmartin, DiPiro & Sokolowski, LLC is an independent member of BDO Alliance USA. We are proud to share important information about financial matters with clients.

2018 Year-End Tax Planning for Businesses Guilmartin, DiPiro & Sokolowski, LLC is an independent member of BDO Alliance USA. We are proud to share important information about financial matters with clients.

To help organizations navigate the key provisions affecting businesses, we have summarized top provisions below.

HOW TAX REFORM IMPACTS BUSINESSES Summary On December 22, 2017, the President signed the Tax Cuts and Jobs Act (the "Act"). Signing the Act marked the largest change to U.S. tax policy in decades. Most

HOW TAX REFORM IMPACTS BUSINESSES Summary On December 22, 2017, the President signed the Tax Cuts and Jobs Act (the "Act"). Signing the Act marked the largest change to U.S. tax policy in decades. Most

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE New Individual Tax Rates New rate structure with seven tax brackets 10% (same as 2017)

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE New Individual Tax Rates New rate structure with seven tax brackets 10% (same as 2017)

Tax Cuts and Jobs Act. Durham Chamber of Commerce Public Policy Meeting January 9, 2018

Tax Cuts and Jobs Act Durham Chamber of Commerce Public Policy Meeting January 9, 2018 Tax Cuts in Billions Corporate/Business ($653) S-Corps/Partnership/Sole Proprietor ($414) International Tax Changes

Tax Cuts and Jobs Act Durham Chamber of Commerce Public Policy Meeting January 9, 2018 Tax Cuts in Billions Corporate/Business ($653) S-Corps/Partnership/Sole Proprietor ($414) International Tax Changes

Tax Cuts and Jobs Act

Tax Cuts and Jobs Act 1. Deduction For Qualified Business Income IRC 199A a. The Tax Cuts and Jobs Act permits pass-through business owners, including partners of partnerships, S corporation shareholders

Tax Cuts and Jobs Act 1. Deduction For Qualified Business Income IRC 199A a. The Tax Cuts and Jobs Act permits pass-through business owners, including partners of partnerships, S corporation shareholders

Adam Williams. Anthony Licavoli. Principal Tax Manager

1 2 Adam Williams Principal 734.302.4179 adam.williams@rehmann.com Anthony Licavoli Tax Manager 248.463.4598 anthony.licavoli@rehmann.com 3 4 5 What is your impression about the speed at which Congress

1 2 Adam Williams Principal 734.302.4179 adam.williams@rehmann.com Anthony Licavoli Tax Manager 248.463.4598 anthony.licavoli@rehmann.com 3 4 5 What is your impression about the speed at which Congress

2018 Year-End Tax Planning for Businesses

2018 Year-End Tax Planning for Businesses Businesses of all sizes, across all industries, have been impacted by the monumental changes to the federal tax code. To maximize tax savings and ensure compliance

2018 Year-End Tax Planning for Businesses Businesses of all sizes, across all industries, have been impacted by the monumental changes to the federal tax code. To maximize tax savings and ensure compliance

Depreciation and Expensing Opportunities Under Tax Reform

Depreciation and Expensing Opportunities Under Tax Reform CliftonLarsonAllen (CLA) Disclaimers The information contained herein is general in nature and is not intended, and should not be construed, as

Depreciation and Expensing Opportunities Under Tax Reform CliftonLarsonAllen (CLA) Disclaimers The information contained herein is general in nature and is not intended, and should not be construed, as

The 2017 Tax Reform Act: What Lawyers Should Know

The 2017 Tax Reform Act: What Lawyers Should Know Mark E. Gingrich, CPA, J.D. Tax Member Chris J. Harris, CPA, J.D. Tax Senior I Agenda I. 20% deduction under Sec. 199A II. Depreciation / like-kind exchange

The 2017 Tax Reform Act: What Lawyers Should Know Mark E. Gingrich, CPA, J.D. Tax Member Chris J. Harris, CPA, J.D. Tax Senior I Agenda I. 20% deduction under Sec. 199A II. Depreciation / like-kind exchange

Business Provisions Under the Tax Cuts and Jobs Act Compared to Previous Tax Law

Tax Rates Corporate tax rate Top rate of 35 percent Flat rate of 21 percent (effective 1/1/2018) Alternative minimum tax (AMT) 20 percent Repealed; AMT credits refundable from 2018 through 2021 (1) Personal

Tax Rates Corporate tax rate Top rate of 35 percent Flat rate of 21 percent (effective 1/1/2018) Alternative minimum tax (AMT) 20 percent Repealed; AMT credits refundable from 2018 through 2021 (1) Personal

Business Items from Tax Reform

Business Items from Tax Reform SCACPA Spring Splash Greenville, South Carolina May 18, 2018 Presented By: W. Verne McGough, Jr. Rogers, Townsend, & Thomas, P.C. 1221 Main Street, 14 th Floor Columbia,

Business Items from Tax Reform SCACPA Spring Splash Greenville, South Carolina May 18, 2018 Presented By: W. Verne McGough, Jr. Rogers, Townsend, & Thomas, P.C. 1221 Main Street, 14 th Floor Columbia,

Tax Cuts and Jobs Act of 2017

Tax Cuts and Jobs Act of 2017 Important Highlights for Individuals and Small Businesses On December 15, 2017, Congress released the 2017 Tax Cut and Jobs Act ( the Act ) that has now passed both the House

Tax Cuts and Jobs Act of 2017 Important Highlights for Individuals and Small Businesses On December 15, 2017, Congress released the 2017 Tax Cut and Jobs Act ( the Act ) that has now passed both the House

Tax cuts and jobs act

1 Tax cuts and jobs act BUSINESS & INDIVIDUAL TAX PROVISIONS PRESENTED BY: MIKE AMERIO & MIKE SOVIK (2017): MFJ Bracket $0 - $18,500 10% $18,501 - $75,900 15% $75,901 - $153,100 25% $153,101 - $233,350

1 Tax cuts and jobs act BUSINESS & INDIVIDUAL TAX PROVISIONS PRESENTED BY: MIKE AMERIO & MIKE SOVIK (2017): MFJ Bracket $0 - $18,500 10% $18,501 - $75,900 15% $75,901 - $153,100 25% $153,101 - $233,350

Tax Cut and Jobs Act. (updated 12/17/17) assurance - consulting - tax - technology - pncpa.com

assurance - consulting - tax - technology - pncpa.com") Tax Cut and Jobs Act (updated 12/17/17) assurance - consulting - tax - technology - pncpa.com Postlethwaite & Netterville, A Professional Accounting Corporation Overview Individual Tax Tax Reform Individual

Tax Cut and Jobs Act (updated 12/17/17) assurance - consulting - tax - technology - pncpa.com Postlethwaite & Netterville, A Professional Accounting Corporation Overview Individual Tax Tax Reform Individual

IMPACT OF TAX REFORM ON COMMERCIAL REAL ESTATE. Mary Burke Baker, Government Affairs Counselor K&L Gates, LLP

IMPACT OF TAX REFORM ON COMMERCIAL REAL ESTATE Mary Burke Baker, Government Affairs Counselor K&L Gates, LLP MOST SWEEPING TAX REFORM SINCE 1986 Tax Cuts and Jobs Act signed December 22, 2017 Generally

IMPACT OF TAX REFORM ON COMMERCIAL REAL ESTATE Mary Burke Baker, Government Affairs Counselor K&L Gates, LLP MOST SWEEPING TAX REFORM SINCE 1986 Tax Cuts and Jobs Act signed December 22, 2017 Generally

TAX PLANNING LETTER 2017 YEAR-END TAX PLANNING FOR BUSINESSES CONTENTS

2017 www.bdo.com TAX PLANNING LETTER CONTENTS Proposed Tax Reform (as of November 17, 2017)... 2 Tax Saving Opportunities for All Businesses... 5 Tax Saving Opportunities for Partnerships, Limited Liability

2017 www.bdo.com TAX PLANNING LETTER CONTENTS Proposed Tax Reform (as of November 17, 2017)... 2 Tax Saving Opportunities for All Businesses... 5 Tax Saving Opportunities for Partnerships, Limited Liability

Don t Let 2018 Be Taxing:

Don t Let 2018 Be Taxing: How Changes to the Tax Laws Change How We Counsel Businesses March 15, 2018 Agenda Introduction C corporation overview Pass-through overview Comparison 2 Introduction Types of

Don t Let 2018 Be Taxing: How Changes to the Tax Laws Change How We Counsel Businesses March 15, 2018 Agenda Introduction C corporation overview Pass-through overview Comparison 2 Introduction Types of

2016 BUSINESS YEAR-END PLANNING UPDATE

November 2016 AN ALERT FROM SMITH LEONARD PLLC: 2016 BUSINESS YEAR-END PLANNING UPDATE www.smith-leonard.com November 2016 2016 BUSINESS YEAR-END PLANNING UPDATE Year-end planning for businesses is particularly

November 2016 AN ALERT FROM SMITH LEONARD PLLC: 2016 BUSINESS YEAR-END PLANNING UPDATE www.smith-leonard.com November 2016 2016 BUSINESS YEAR-END PLANNING UPDATE Year-end planning for businesses is particularly

October 31, Summary of Opportunity Zone Proposed Regulations. Table of Contents

Schuyler M. Moore D: 310.201.7559 F: 310.201.4444 SMoore@ggfirm.com October 31, 2018 To Colleagues, Friends, and Clients: Re: Summary of Opportunity Zone Proposed Regulations This letter provides a summary

Schuyler M. Moore D: 310.201.7559 F: 310.201.4444 SMoore@ggfirm.com October 31, 2018 To Colleagues, Friends, and Clients: Re: Summary of Opportunity Zone Proposed Regulations This letter provides a summary

TAX CUTS AND JOBS ACT

TAX CUTS AND JOBS ACT Businesses Corporate tax rate will now be a flat 21% beginning January 1, 2018. Corporate alternative minimum tax has been repealed. Effective for tax years beginning after December

TAX CUTS AND JOBS ACT Businesses Corporate tax rate will now be a flat 21% beginning January 1, 2018. Corporate alternative minimum tax has been repealed. Effective for tax years beginning after December

Tax Reform Update and Q&A Session October 18, 2018

Tax Reform Update and Q&A Session October 18, 2018 Moderated By: Brian Ray, MS, CPA This presentation has been prepared for informational purposes only, and is not intended to or should be relied upon

Tax Reform Update and Q&A Session October 18, 2018 Moderated By: Brian Ray, MS, CPA This presentation has been prepared for informational purposes only, and is not intended to or should be relied upon

What Now? Implications of the Tax Cut and Jobs Act of 2017 on Families and Business

What Now? Implications of the Tax Cut and Jobs Act of 2017 on Families and Business August 10, 2018 Sarah Armstrong, Esq. Marjorie A. Rogers, Esq. Ed Street, CPA/ABV/CFF, CVA, ASA The information provided

What Now? Implications of the Tax Cut and Jobs Act of 2017 on Families and Business August 10, 2018 Sarah Armstrong, Esq. Marjorie A. Rogers, Esq. Ed Street, CPA/ABV/CFF, CVA, ASA The information provided

TAX & TRANSACTIONS BULLETIN

Volume 7 On October 22, 2004, President Bush signed the American Jobs Creation Act of 2004 ( Act ). The Act s main purpose is to repeal the extraterritorial income exclusion (ETI). To compensate U.S. manufacturers

Volume 7 On October 22, 2004, President Bush signed the American Jobs Creation Act of 2004 ( Act ). The Act s main purpose is to repeal the extraterritorial income exclusion (ETI). To compensate U.S. manufacturers

Tax Planning for Real Estate

Tax Planning for Real Estate Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP Pass-thru Deduction Deduction equal to 20% of domestic qualified business income (QBI) from a passthrough entity

Tax Planning for Real Estate Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP Pass-thru Deduction Deduction equal to 20% of domestic qualified business income (QBI) from a passthrough entity

TAX CUTS AND JOBS ACT

TAX CUTS AND JOBS ACT Public Law 115-97 December 22, 2017 TABLE OF CONTENTS BUSINESS PROVISIONS... 1-5 C CORPORATION TAX RATES REDUCED... 1 DIVIDENDS-RECEIVED DEDUCTION... 1 ALTERNATIVE MINIMUM TAX REPEALED

TAX CUTS AND JOBS ACT Public Law 115-97 December 22, 2017 TABLE OF CONTENTS BUSINESS PROVISIONS... 1-5 C CORPORATION TAX RATES REDUCED... 1 DIVIDENDS-RECEIVED DEDUCTION... 1 ALTERNATIVE MINIMUM TAX REPEALED

TCJA Top Ten Tax Law Changes for Small Businesses DARBY RICH, CPA - TAX MANAGER MYRA BAKKE, CPA - TAX SHAREHOLDER

TCJA Top Ten Tax Law Changes for Small Businesses DARBY RICH, CPA - TAX MANAGER MYRA BAKKE, CPA - TAX SHAREHOLDER #1 Corporate Tax Rates New Corporate Flat Tax Rate of 21% replaces old graduated brackets

TCJA Top Ten Tax Law Changes for Small Businesses DARBY RICH, CPA - TAX MANAGER MYRA BAKKE, CPA - TAX SHAREHOLDER #1 Corporate Tax Rates New Corporate Flat Tax Rate of 21% replaces old graduated brackets

2017 Tax Reform What you need to Know

Oil & Natural Gas Accounting & Tax 2018 2017 Tax Reform What you need to Know November 8, 2018 J. Marlin Witt, CPA, CFP, CGMA What Makes Us Different, Makes You Better Overview of Reform Product of budget

Oil & Natural Gas Accounting & Tax 2018 2017 Tax Reform What you need to Know November 8, 2018 J. Marlin Witt, CPA, CFP, CGMA What Makes Us Different, Makes You Better Overview of Reform Product of budget

May 8, 2018 Watkins Glen, New York

May 8, 2018 Watkins Glen, New York This presentation is intended for general educational and/or informational purposes only and does not replace specific, independent professional advice. This presentation

May 8, 2018 Watkins Glen, New York This presentation is intended for general educational and/or informational purposes only and does not replace specific, independent professional advice. This presentation

Tax Cuts and Jobs Act: A comparison for businesses

Tax Cuts and Jobs Act: A comparison for businesses The Tax Cuts and Jobs Act ("") changed deductions, depreciation, expensing, tax credits and other tax items that affect businesses. This side-by-side

Tax Cuts and Jobs Act: A comparison for businesses The Tax Cuts and Jobs Act ("") changed deductions, depreciation, expensing, tax credits and other tax items that affect businesses. This side-by-side