LOW-INCOME HOUSING TAX CREDIT CLOSINGS FOR PHAs AND RAD TRANSACTIONS. June 2015

|

|

|

- Blake Pierce

- 5 years ago

- Views:

Transcription

1 LOW-INCOME HOUSING TAX CREDIT CLOSINGS FOR PHAs AND RAD TRANSACTIONS June 2015

2 What Do Tax Credits Finance? New construction and rehab projects Acquisition in some cases Housing for families, special needs tenants, single room occupancy and the elderly Urban, rural and suburban locations Additional tax incentives for projects in high-cost or difficult-todevelop areas

3 How Do Housing Tax Credits Work? Rental units with tenants earning no more than 60% of area median income Investors earn dollar-for-dollar credits against their federal tax liability Investors also get tax benefits from losses Generally, tax credits are received over the first 10 years of operation Some tax credits are recaptured by the IRS if the project does not comply for 15 years

4 Unit Restrictions Threshold Elections Who can live there? 40/60 election 20/50 election All tax credit units must be within election parameters Rent Restricted How much can tenants pay? Rents and utilities limited to 30% of threshold income Allowable rent based on size of unit

5 No Tax Credit/ No Deduction Deduction Tax Credit Net Income from Operations 1,000,000 1,000,000 1,000,000 Tax Deductions none (300,000) none Taxable Income 1,000, ,000 1,000,000 Tax Liability: Tax at 40% tax rate $ 400, , ,000 Low-Income Housing Tax Credits none none (300,000) Net Tax Liability $ 400,000 $ 280,000 $ 100,000

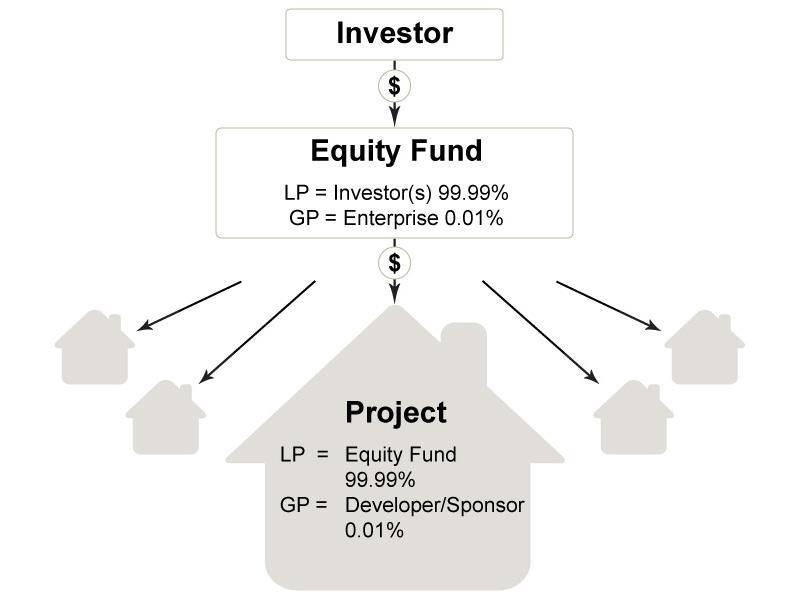

6 Structure Tax Credit Syndication Limited partnership structure General partner owns just 0.01%, but controls and operates the project Passive limited partner invests equity in return for 99.99% ownership

7 Structure Tax Credit Syndication Sale to Investor Limited Partner of most of the tax credits and tax losses maximizes investor equity More investor equity reduces other financing needs and helps project development L.P. is a passive investor, and gets its return almost exclusively from the tax credits and losses

8 12

9

10 The Parties in a Tax Credit Syndication Development Team Developer General contractor Architect Attorney Accountant Property manager Consultants Lenders Construction lender Permanent lenders Lender attorneys State Housing Finance Agency Syndicator Underwriter Fund manager Attorney

11 Computing Tax Credits: Basis Eligible Basis X Applicable Fraction X Basis Boost (if applicable) = Qualified Basis

12 Computing Tax Credits: Annual Tax Credits Qualified Basis X Tax Credit Rate = Annual Tax Credits

13 Computing Tax Credits: Total Tax Credits Annual Tax Credits X 10 (Years) = Total Tax Credits

14 Computing Tax Credit Equity Total Tax Credits X Pay Price (Cents per dollar) = Equity

15 Computing Basis to Calculate Credits Eligible Basis - Depreciable basis of residential rental housing eligible for tax credits Qualified Basis - Adjust Eligible Basis for non-income qualified tenants, using Applicable Fraction (the % of units qualifying for credits)

16 Applicable Fraction Lesser of: The number of qualifying rent-paying residential units over the total number of rent-paying residential units or The square footage of qualifying rent-paying residential units over the total square footage of rent-paying residential units

17 Computing Basis to Calculate Credits Basis Boost Increase tax credit basis by 30% if project is in a qualified census tract (QCT) a difficult to develop area (DDA) or A state designated difficult development area Does not apply to tax-exempt financed projects Applies if building or project is placed in service after 07/30/08

18 Eligible Basis Excludes the following: land and land-related costs building acquisition and related costs historic tax credits taken on residential part of project fees and costs related to permanent loan financing syndication-related costs tax credit fees reserves post-construction working capital federal grants non-residential costs

19 Eligible Basis Includes Impact Fees Onsite Roads, sidewalks and parking lots Offsite if adjacent, functionally related and owner maintained Cost of Utility Hookup Landscaping if adjacent to building Final grading of building site

20 Eligible Basis Excludes: Initial grading Landscaping not adjacent to building Includes: Common area Full time manager s unit Community space

21 Computing Annual Tax Credits Total Development Budget $9,632,000 Less ineligible costs 1,062,500 Eligible Basis $8,569,500 Applicable Fraction x100% QCT/DDA Basis Boost x 130% Qualified Basis $11,140,350

22 Computing Annual Tax Credits: 9% Credit Qualified Basis $11,140,350 Applicable Rate*** x 9.00% Annual Tax Credits $ 1,002,631 ***Published rate would apply if PIS before 07/31/08 or after 2013.

23 Computing Total Tax Credits and the Equity Raise: 9% Credits Annual Tax Credits $ 1,002, Years x 10 years Total Tax Credits $ 10,026,310 Price Paid x $0.80 Equity $ 8,021,048 Equity represents 83% of development costs

24 Computing Annual Tax Credits: 4% Credit Qualified Basis $11,140,350 Applicable Rate (Nov. 2011) 3.19% Annual Tax Credits $355,377

25 Computing Total Tax Credits and the Equity Raise: 4% Credits Annual Tax Credits $ 355, Years x 10 years Total Tax Credits $ 3,553,770 Price Paid x $0.80 Equity $ 2,843,016 Equity represents 30% of total development costs

26 Structuring the Project Step 1: Estimate tax credit basis Step 2: Estimate tax credits generated Step 3: Estimate investor equity Step 4: Estimate first mortgage amount Step 5: Estimate the funding gap Step 6: Fill the gap with a combination of other funds

27 Sources of Funding to Fill the Gap HOME, CDBG funds AHP Funds ARRA Funds TCAP and Exchange Other Local Funds Deferred Development Fee Cost Savings (development or acquisition) Modification of First Mortgage Terms Income or Expense Modifications

28 Tax Credit Timeline Apply for tax credits Get a tax credit reservation Receive carryover allocation Incur more than 10% by required date Complete project and place it in service Apply for 8609s for all buildings Record extended use agreement Rent tax credit units to qualified tenants Elect when to start tax credits Keep tax credit units in compliance

29 Placing a Project in Service Project must be placed in service by the end of the second year following the Allocation Year Example: Credits allocated in 2010 Carryover met in 2011 All buildings in project must be placed in service by December 31, 2012

30 Placing a Project in Service New Construction When first unit is ready Certificate of Occupancy Rehabilitation more flexibility No earlier than the date when the rehab equals the greater of: $6,000 per unit or 20% of acquisition price Lower amount of rehab required if placed in service prior to 07/31/08

31 Financial Structuring: Kinds of Debt and Grants Hard Debt: Must pay, conventional bank debt Generally amortizing Soft Debt: Generally from governmental agencies Cash flow contingent or accruing Repayable Grants: not repayable

32 Grants Grants funds that are not repayable or cannot be repayable under reasonable assumptions Outright grants Forgivable loans Cannot be repaid at maturity Tax treatment Income recognition Potential basis reduction if federal funds

33 Federal Grants Development Grants funds that are used directly or indirectly to fund development costs Basis must be reduced Could flow through GP as a loan At the AFR, if 9% deal PIS prior to 07/31/08 Lower rate allowed if after 07/31/08 Caution reallocation and residual test issues

34 Federal Grants Operating Grants funds that support the operations of the project Building PIS after 07/30/08: No basis reduction Income must be recognized Building PIS before 07/31/08: Reduction of eligible basis Income must be recognized Exceptions for Sec. 8, Sec. 9, Shelter plus care

35 Special Situations Historic Tax Credits Add value to a deal, but rigid procedures and approvals are involved. Eligible basis for LIHTC reduced by the amount of the historic credit Energy Credits and Green Subsidies Credits for energy efficient appliances, solar energy property and other environmentally beneficial enhancements to project Special needs deals have structuring issues related to the length and strength of subsidies

36 The Syndicator s Approach To Underwriting Quality of the Development Team Project Characteristics Evaluation of the Development Budget Rents/ Market/ Marketability Operating Costs Reserves Sponsor Guarantees

37 Concerns Being Evaluated Reputations of the developer, general contractor and other members of the team Design considerations of the project Quality of materials to be used Timelines for construction and lease-up Useful life analysis will it continue to attract tenants as it ages? Market analysis are rents supported by outside analysis?

38 Quality of the Development Team Sponsor/ general partner experience Architect/ engineer design, supervision General contractor size and type of construction, capacity to produce on time Attorney and Accountant experience with tax credit partnership structure and issues and Mixed Finance/RAD Property manager experience with low-income tenants and management capability Consultants to fill in holes in experience

39 Evaluation of Project Characteristics Need - does it answer a real need in the community? Finances - does it meet the syndicator s financial threshold? Quality - will it continue to attract tenants? Strategic Interest - does it meet the syndicator s programmatic needs? Geography - is it located where syndicator and its investors want to invest?

40 Evaluation of Development Budget Can the project be completed in the time and within budget What will it cost to build the project? How much is needed to place it in service? What are reasonable timelines? What are the key risk areas to lenders and equity investors and how can the risks be ameliorated?

41 Rents/Market/Marketability Are rents realistic for the market area? What is demand for proposed housing? neighborhood what demographics will project address Are tax credit rents sufficiently below area market rents less of a concern if there is operating subsidy? What if subsidy is eliminated? Are other funding requirements factored in?

42 Site Assessment Criteria Access to employment and transportation Proximity to downtown or employers Transit Ability to support parking Proximity to services and amenities Retail, parks, etc. School district quality and proximity to neighborhood schools Curb appeal of immediately surrounding uses

43 Evaluation of Operating Costs Examine assumptions for proposed costs Are insurance, etc. costs confirmed by bid? Are repair and maintenance costs consistent with housing type and family size? If there s an elevator, are its costs included? Are legal, accounting and administrative costs high enough? Are reserves funded in a plausible way? Do costs need to be restructured for cash flow?

44 Structuring Project Reserves Reserves are a way to structure for the project s risks Operating and lease-up reserves protect against inadequate cash flow Replacement reserves provide funds for capital replacement when needed Other reserves (for tenant services, etc.) are structured for specific needs or risks0

45 Sources of Funds for Reserves Operating reserves usually come from investor equity, but may come from cash flow Operating reserves are paid in over time to optimize the use of equity Replacement reserves usually are funded from cash flow, but may come from equity Some projects need replacements reserves earlier than cash flow permits, requiring equity Special-needs housing may not have cash flow for reserves, which may be funded from equity

46 Sponsor Guarantees Allocate costs related to specific risks to the developer and related parties Areas where guarantees apply may include: development cost overruns delays in construction completion and lease-up operating deficits until stable operations reduced or delayed tax benefits partnership management

47 Due Diligence/Closing Items Development Team, Guarantor and Contractor Financials Identification of Development Team Responsibilities and Development Agreement Draft Operating Agreement Draft Tax Credit Approval ALTA Survey Environmental Phase 1 and 2(if necessary) Lead, Asbestos and other building testing Geotech and Wetlands Title Property Management Plan P&P Bonds

48 Long Lead Time Items Identification of Guarantors Construction Operating Deficit Bidding Plan and Cost Review Phase 2 and DEQ Approval if Contamination is Present Zoning Subdivision Title Tax Credit Approval Bond Commission Approval if 4% HUD Evidentiary Submission and Approval

THE ABC S OF AFFORDABLE HOUSING DEVELOPMENT

Presentation Overview Page Tax Credit Program Fundamentals 3 Qualified Allocation Plan Review 22 What Makes a Successful Application 32 2 Tax Credit Program Fundamentals 3 Housing Priorities Increase the

Presentation Overview Page Tax Credit Program Fundamentals 3 Qualified Allocation Plan Review 22 What Makes a Successful Application 32 2 Tax Credit Program Fundamentals 3 Housing Priorities Increase the

Mark Shelburne Novogradac & Company LLP

Mark Shelburne Novogradac & Company LLP Mark.shelburne@novoco.com /events OUTLINE Affordable Housing Overview How Ta Credits Are Calculated Typical Ownership Structure Development Timeline Acq/Rehab Deals

Mark Shelburne Novogradac & Company LLP Mark.shelburne@novoco.com /events OUTLINE Affordable Housing Overview How Ta Credits Are Calculated Typical Ownership Structure Development Timeline Acq/Rehab Deals

NORTHERN MARIANAS HOUSING CORPORATION LOW-INCOME HOUSING TAX CREDIT PROGRAM 2016 APPLICATION

NORTHERN MARIANAS HOUSING CORPORATION LOW-INCOME HOUSING TAX CREDIT PROGRAM 2016 APPLICATION I. APPLICANT INFORMATION 1 A. Partnership or Limited Liability Company Information 2 B. Identity of Interest

NORTHERN MARIANAS HOUSING CORPORATION LOW-INCOME HOUSING TAX CREDIT PROGRAM 2016 APPLICATION I. APPLICANT INFORMATION 1 A. Partnership or Limited Liability Company Information 2 B. Identity of Interest

Part IV - Project Costs

Part IV - Project Costs (Click on any of the items below) Signature Page Rent Qualification Chart Eligible Basis Limits Breakdown of Costs and Basis Carryover Tie Breaker Percentage Limits Operating Income

Part IV - Project Costs (Click on any of the items below) Signature Page Rent Qualification Chart Eligible Basis Limits Breakdown of Costs and Basis Carryover Tie Breaker Percentage Limits Operating Income

Brad Elphick, CPA Novogradac & Company LLP Chris Key, CPA Novogradac & Company LLP

Brad Elphick, CPA Novogradac & Company LLP brad.elphick@novoco.com Chris Key, CPA Novogradac & Company LLP chris.key@novoco.com /events OUTLINE Affordable Housing Overview How Ta Credits Are Calculated

Brad Elphick, CPA Novogradac & Company LLP brad.elphick@novoco.com Chris Key, CPA Novogradac & Company LLP chris.key@novoco.com /events OUTLINE Affordable Housing Overview How Ta Credits Are Calculated

OKLAHOMA HOUSING FINANCE AGENCY Affordable Housing Tax Credits Program (AHTC) 2016 Application Form for Allocation

2016 Application Form for Allocation") OKLAHOMA HOUSING FINANCE AGENCY Affordable Housing Tax Credits Program (AHTC) 2016 Application Form for Allocation 100 N.W. 63 rd St., Suite 200 Oklahoma City, OK 73116 or P.O. Box 26720 Oklahoma City,

OKLAHOMA HOUSING FINANCE AGENCY Affordable Housing Tax Credits Program (AHTC) 2016 Application Form for Allocation 100 N.W. 63 rd St., Suite 200 Oklahoma City, OK 73116 or P.O. Box 26720 Oklahoma City,

CHAPTER 2: GENERAL PROGRAM RULES

The HOME program has a number of basic rules that apply to all program activities. These rules concern: The definition of a project; The form and amount of subsidy; Eligible costs; The property; The applicant

The HOME program has a number of basic rules that apply to all program activities. These rules concern: The definition of a project; The form and amount of subsidy; Eligible costs; The property; The applicant

OKLAHOMA HOUSING FINANCE AGENCY Affordable Housing Tax Credits Program (AHTC) Carryover Application Form

Carryover Application Form") OKLAHOMA HOUSING FINANCE AGENCY Affordable Housing Tax Credits Program (AHTC) Carryover Application Form 100 N.W. 63 rd St., Suite 200 Oklahoma City, OK 73116 or P.O. Box 26720 Oklahoma City, OK 73126-0720

OKLAHOMA HOUSING FINANCE AGENCY Affordable Housing Tax Credits Program (AHTC) Carryover Application Form 100 N.W. 63 rd St., Suite 200 Oklahoma City, OK 73116 or P.O. Box 26720 Oklahoma City, OK 73126-0720

NYS Housing Finance Agency Affordable Rental Housing Term Sheet & Financing Guide

PROGRAM DESCRIPTION Goal: NYS Housing Finance Agency Affordable Rental Housing Term Sheet & Financing Guide The New York State Housing Finance Agency (HFA) Affordable Rental Housing Program provides tax-exempt

PROGRAM DESCRIPTION Goal: NYS Housing Finance Agency Affordable Rental Housing Term Sheet & Financing Guide The New York State Housing Finance Agency (HFA) Affordable Rental Housing Program provides tax-exempt

Small Building Participation Loan Program

HCR s Small Building Participation Loan Program provides gap project financing assistance for qualified housing developers for acquisition, capital costs and related soft costs associated with the preservation

HCR s Small Building Participation Loan Program provides gap project financing assistance for qualified housing developers for acquisition, capital costs and related soft costs associated with the preservation

Low-Income Housing Tax Credit (LIHTC) Program. Guideline. This Guideline is Effective September 12, 2018

Program. Guideline. This Guideline is Effective September 12, 2018") Low-Income Housing Tax Credit (LIHTC) Program Guideline 2018 This Guideline is Effective September 12, 2018 Table of Contents PREFACE... 3 I. Background... 3 II. Pre-Application Meeting... 4 III. Submission

Low-Income Housing Tax Credit (LIHTC) Program Guideline 2018 This Guideline is Effective September 12, 2018 Table of Contents PREFACE... 3 I. Background... 3 II. Pre-Application Meeting... 4 III. Submission

NEW HAMPSHIRE HOUSING FINANCE AUTHORITY UNDERWRITING AND DEVELOPMENT POLICIES FOR MULTI-FAMILY FINANCE

Rev. 10/11/07 (Correction 5/16/08) NEW HAMPSHIRE HOUSING FINANCE AUTHORITY UNDERWRITING AND DEVELOPMENT POLICIES FOR MULTI-FAMILY FINANCE Purpose: These underwriting standards are intended to be an internal

Rev. 10/11/07 (Correction 5/16/08) NEW HAMPSHIRE HOUSING FINANCE AUTHORITY UNDERWRITING AND DEVELOPMENT POLICIES FOR MULTI-FAMILY FINANCE Purpose: These underwriting standards are intended to be an internal

Georgia Housing and Finance Authority Tax Credit Manual

Georgia Housing and Finance Authority Tax Credit Manual This Manual is intended to be used as a basic resource for issues that arise regarding DCA s administration of the Federal and State Tax Credit Program

Georgia Housing and Finance Authority Tax Credit Manual This Manual is intended to be used as a basic resource for issues that arise regarding DCA s administration of the Federal and State Tax Credit Program

CALIFORNIA TAX CREDIT ALLOCATION COMMITTEE FINAL RESERVATION STATUS REPORT

CALIFORNIA TAX CREDIT ALLOCATION COMMITTEE FINAL RESERVATION STATUS REPORT Application Number: Project Name: Applicant Name: Applicant Contact: Phone: ( ) FAX: ( ) PART I: THE DEVELOPMENT TEAM A. The Development

CALIFORNIA TAX CREDIT ALLOCATION COMMITTEE FINAL RESERVATION STATUS REPORT Application Number: Project Name: Applicant Name: Applicant Contact: Phone: ( ) FAX: ( ) PART I: THE DEVELOPMENT TEAM A. The Development

AHFA 2018 HOME/Housing Credit/HTF APPLICATION WORKSHOP Culmination of year round efforts to provide information via:

AHFA 2018 HOME/Housing Credit/HTF APPLICATION WORKSHOP Culmination of year round efforts to provide information via: www.ahfa.com: Plans (prior and current) Application Documents Q & A opportunity MF Notices

AHFA 2018 HOME/Housing Credit/HTF APPLICATION WORKSHOP Culmination of year round efforts to provide information via: www.ahfa.com: Plans (prior and current) Application Documents Q & A opportunity MF Notices

Tax Exempt Reservation Letter

STATE OF CALIFORNIA CALIFORNIA TAX CREDIT ALLOCATION COMMITTEE 915 CAPITOL MALL, ROOM 485 SACRAMENTO, CA 95814 TELEPHONE: (916)654-6340 FAX: (916)654-6033 William J. Pavao Executive Director MEMBERS: Bill

STATE OF CALIFORNIA CALIFORNIA TAX CREDIT ALLOCATION COMMITTEE 915 CAPITOL MALL, ROOM 485 SACRAMENTO, CA 95814 TELEPHONE: (916)654-6340 FAX: (916)654-6033 William J. Pavao Executive Director MEMBERS: Bill

NEW YORK CITY HOUSING DEVELOPMENT CORPORATION INSTRUCTIONS SUMMARY SPREADSHEET FOR DEEP RENT SKEW PROJECTS FYE 2017

NEW YORK CITY HOUSING DEVELOPMENT CORPORATION INSTRUCTIONS SUMMARY SPREADSHEET FOR DEEP RENT SKEW PROJECTS FYE 2017 Please follow the instructions below for completing the SUMMARY SPREADSHEET for Mixed

NEW YORK CITY HOUSING DEVELOPMENT CORPORATION INSTRUCTIONS SUMMARY SPREADSHEET FOR DEEP RENT SKEW PROJECTS FYE 2017 Please follow the instructions below for completing the SUMMARY SPREADSHEET for Mixed

NEW HAMPSHIRE HOUSING FINANCE AUTHORITY UNDERWRITING AND DEVELOPMENT POLICIES FOR MULTI-FAMILY FINANCE

Rev. 10/4/2010 NEW HAMPSHIRE HOUSING FINANCE AUTHORITY UNDERWRITING AND DEVELOPMENT POLICIES FOR MULTI-FAMILY FINANCE Purpose: These underwriting standards are intended to be an internal procedures document

Rev. 10/4/2010 NEW HAMPSHIRE HOUSING FINANCE AUTHORITY UNDERWRITING AND DEVELOPMENT POLICIES FOR MULTI-FAMILY FINANCE Purpose: These underwriting standards are intended to be an internal procedures document

Low-Income Housing Tax Credit. Qualified Allocation Plan

TENNESSEE HOUSING DEVELOPMENT AGENCY Low-Income Housing Tax Credit Qualified Allocation Plan 2001 January 19, 2001 TENNESSEE HOUSING DEVELOPMENT AGENCY LOW-INCOME HOUSING TAX CREDIT QUALIFIED ALLOCATION

TENNESSEE HOUSING DEVELOPMENT AGENCY Low-Income Housing Tax Credit Qualified Allocation Plan 2001 January 19, 2001 TENNESSEE HOUSING DEVELOPMENT AGENCY LOW-INCOME HOUSING TAX CREDIT QUALIFIED ALLOCATION

TENNESSEE HOUSING DEVELOPMENT AGENCY. Low-Income Housing Tax Credit 2016 Final Application. 4% and 9%

TENNESSEE HOUSING DEVELOPMENT AGENCY Low-Income Housing Tax Credit 2016 Final Application 4% and 9% FOR DEVELOPMENTS REQUESTING IRS FORMS 8609 IN 2016 TENNESSEE HOUSING DEVELOPMENT AGENCY LIHTC VERIFICATION

TENNESSEE HOUSING DEVELOPMENT AGENCY Low-Income Housing Tax Credit 2016 Final Application 4% and 9% FOR DEVELOPMENTS REQUESTING IRS FORMS 8609 IN 2016 TENNESSEE HOUSING DEVELOPMENT AGENCY LIHTC VERIFICATION

TENNESSEE HOUSING DEVELOPMENT AGENCY. Low-Income Housing Tax Credit 2018 Final Application for Noncompetitive LIHTC only

TENNESSEE HOUSING DEVELOPMENT AGENCY Low-Income Housing Tax Credit 2018 Final Application for Noncompetitive LIHTC only FOR DEVELOPMENTS REQUESTING IRS FORMS 8609 IN 2018 TENNESSEE HOUSING DEVELOPMENT

TENNESSEE HOUSING DEVELOPMENT AGENCY Low-Income Housing Tax Credit 2018 Final Application for Noncompetitive LIHTC only FOR DEVELOPMENTS REQUESTING IRS FORMS 8609 IN 2018 TENNESSEE HOUSING DEVELOPMENT

TENNESSEE HOUSING DEVELOPMENT AGENCY. Low-Income Housing Tax Credit 2017 Phase II Final Application for Competitive LIHTC only

TENNESSEE HOUSING DEVELOPMENT AGENCY Low-Income Housing Tax Credit 2017 Phase II Final Application for Competitive LIHTC only FOR DEVELOPMENTS REQUESTING IRS FORMS 8609 IN 2017 TENNESSEE HOUSING DEVELOPMENT

TENNESSEE HOUSING DEVELOPMENT AGENCY Low-Income Housing Tax Credit 2017 Phase II Final Application for Competitive LIHTC only FOR DEVELOPMENTS REQUESTING IRS FORMS 8609 IN 2017 TENNESSEE HOUSING DEVELOPMENT

Housing and Economic Recovery Act of 2008

Housing and Economic Recovery Act of 2008 Temporary increase in housing credit cap for 2008 and 2009 Credits increase from $2.00 to $2.20 per capita Small states increase by 10% Provides for $11 billion

Housing and Economic Recovery Act of 2008 Temporary increase in housing credit cap for 2008 and 2009 Credits increase from $2.00 to $2.20 per capita Small states increase by 10% Provides for $11 billion

Fundamentals of the Real Estate Development Process Affordable & Market Rate Perspectives

Real Estate Development 101 Fundamentals of the Real Estate Development Process Affordable & Market Rate Perspectives DEVELOPMENT LIFE CYCLE SITE IDENTIFICATION FINANCING PLAN ACQUISITION DUE-DILIGENCE

Real Estate Development 101 Fundamentals of the Real Estate Development Process Affordable & Market Rate Perspectives DEVELOPMENT LIFE CYCLE SITE IDENTIFICATION FINANCING PLAN ACQUISITION DUE-DILIGENCE

TAX CREDITS 101. (How to Know Just Enough to Get You In Trouble)

") TAX CREDITS 101 (How to Know Just Enough to Get You In Trouble) Naomi W. Byrne, Consultant, EJP Consulting Group LLC JoAnn Rodriguez, Regional Supervisor, Allied-Orion Group ! Resources http://www.txtha.org/index.php/resources/!

TAX CREDITS 101 (How to Know Just Enough to Get You In Trouble) Naomi W. Byrne, Consultant, EJP Consulting Group LLC JoAnn Rodriguez, Regional Supervisor, Allied-Orion Group ! Resources http://www.txtha.org/index.php/resources/!

ANNUAL REPORT. Contact information:

ANNUAL REPORT $14,500,000 TEXAS DEPARTMENT OF HOUSING AND COMMUNITY AFFAIRS MULTIFAMILY HOUSING REVENUE BONDS (The Waters at Willow Run Apartments), Series 2013 Name: The Waters at Willow Run, LP Address:

ANNUAL REPORT $14,500,000 TEXAS DEPARTMENT OF HOUSING AND COMMUNITY AFFAIRS MULTIFAMILY HOUSING REVENUE BONDS (The Waters at Willow Run Apartments), Series 2013 Name: The Waters at Willow Run, LP Address:

Developer Guidance for KHC Underwriting Model Review Revised November 2016

Developer Guidance for KHC Underwriting Model Review Revised November 2016 KHC has developed the criteria below, which is used by the underwriters in reviewing a project s financial strength and adherence

Developer Guidance for KHC Underwriting Model Review Revised November 2016 KHC has developed the criteria below, which is used by the underwriters in reviewing a project s financial strength and adherence

WNC HOUSING TAX CREDIT FUND VI, L.P., SERIES 13. Annual Report to Partners. For the fiscal year ended March 31, 2018

Annual Report to Partners For the fiscal year ended March 31, 2018 August 3, 2018 Re: WNC Housing Tax Credit Fund VI, L.P., Series 13 (the Partnership ) Dear Investor: We are pleased to provide you with

Annual Report to Partners For the fiscal year ended March 31, 2018 August 3, 2018 Re: WNC Housing Tax Credit Fund VI, L.P., Series 13 (the Partnership ) Dear Investor: We are pleased to provide you with

HOME + LIHTC. Topics. Max HOME $$ 4/27/2011. HOME Basics LIHTC Basics Combining HOME + LIHTC. Lesser of amount represented by

Anker Heegaard The Compass Group HOME + LIHTC effectively use HOME and LIHTC together given today s market conditions and provide insight on key regulatory issues when combining the two sources. HOME +

Anker Heegaard The Compass Group HOME + LIHTC effectively use HOME and LIHTC together given today s market conditions and provide insight on key regulatory issues when combining the two sources. HOME +

San Diego Housing Commission Workshop & Discussion: Low-Income Housing Tax Credits June 16, 2017

Workshop & Discussion: Low-Income Housing Tax Credits June 16, 2017 Deborah N. Ruane Executive Vice President & Chief Strategy Officer Michael Pavco Senior Vice President Real Estate Division Introduction

Workshop & Discussion: Low-Income Housing Tax Credits June 16, 2017 Deborah N. Ruane Executive Vice President & Chief Strategy Officer Michael Pavco Senior Vice President Real Estate Division Introduction

EQUITY REPLACEMENT PROGRAM OVERVIEW

Overview Illinois Housing Development Authority EQUITY REPLACEMENT PROGRAM OVERVIEW June 1, 2009 The Tax Credit Assistance Program ( TCAP ) and the Section 1602 Program ( Section 1602 ) contained in the

Overview Illinois Housing Development Authority EQUITY REPLACEMENT PROGRAM OVERVIEW June 1, 2009 The Tax Credit Assistance Program ( TCAP ) and the Section 1602 Program ( Section 1602 ) contained in the

Michigan State Housing Development Authority. Multifamily Direct Lending Parameters. Style Definition: TOC 1 Style Definition: TOC 2: Left

Style Definition: TOC 1 Style Definition: TOC 2: Left Formatted: Font: 12 pt Michigan State Housing Development Authority Multifamily Direct Lending Parameters Updated March 23, 2016 2017 Table of Contents

Style Definition: TOC 1 Style Definition: TOC 2: Left Formatted: Font: 12 pt Michigan State Housing Development Authority Multifamily Direct Lending Parameters Updated March 23, 2016 2017 Table of Contents

Combining FHA Insured Loans with LIHTC

Combining FHA Insured Loans with LIHTC Presented by: Scott Graber Vice President Multifamily & Senior Housing sgraber@gershman.com (720) 507-1422 Bryan C Keller, CPA Partner-in-Charge of Real Estate Service

Combining FHA Insured Loans with LIHTC Presented by: Scott Graber Vice President Multifamily & Senior Housing sgraber@gershman.com (720) 507-1422 Bryan C Keller, CPA Partner-in-Charge of Real Estate Service

American Recovery and Reinvestment Act of 2009 (ARRA) Tax Credit Program for Washington State

Tax Credit Program for Washington State") American Recovery and Reinvestment Act of 2009 (ARRA) Tax Credit Program for Washington State Revised September 1, 2009 I. INTRODUCTION... 2 A. PROGRAM DESCRIPTION... 2 B. COMMISSION GOALS FOR ALLOCATION

American Recovery and Reinvestment Act of 2009 (ARRA) Tax Credit Program for Washington State Revised September 1, 2009 I. INTRODUCTION... 2 A. PROGRAM DESCRIPTION... 2 B. COMMISSION GOALS FOR ALLOCATION

Year 15: Transition Strategies for Expiring LIHTC Properties

Year 15: Transition Strategies for Expiring LIHTC Properties November 1, 2017 Enterprise Live Online Event Presenters: Greg Griffin, Sr. Director, Asset Management Sean Barnes, Sr. Disposition Manager,

Year 15: Transition Strategies for Expiring LIHTC Properties November 1, 2017 Enterprise Live Online Event Presenters: Greg Griffin, Sr. Director, Asset Management Sean Barnes, Sr. Disposition Manager,

SMALL SITES PROGRAM PROGRAM GUIDELINES

SMALL SITES PROGRAM PROGRAM GUIDELINES Mayor s Office of Housing & Community Development The ( SSP or Program ) Program Guidelines were originally approved as Underwriting Guidelines by the San Francisco

SMALL SITES PROGRAM PROGRAM GUIDELINES Mayor s Office of Housing & Community Development The ( SSP or Program ) Program Guidelines were originally approved as Underwriting Guidelines by the San Francisco

HOME INVESTMENT PARTNERSHIP PROGRAM (HOME) 2017 PROGRAM DESCRIPTION

2017 PROGRAM DESCRIPTION") HOME INVESTMENT PARTNERSHIP PROGRAM (HOME) 2017 PROGRAM DESCRIPTION Use of Funds The City of Kenosha intends to use its 2017 HOME funds for Program Administration and for eligible HOME Program activities

HOME INVESTMENT PARTNERSHIP PROGRAM (HOME) 2017 PROGRAM DESCRIPTION Use of Funds The City of Kenosha intends to use its 2017 HOME funds for Program Administration and for eligible HOME Program activities

Town of Windsor Community Development Housing Rehabilitation Program

Town of Windsor Community Development Housing Rehabilitation Program For more information or questions contact the Office of Community Development at (860) 285-1984 REVISED: MAY, 2018 TOWN OF WINDSOR OFFICE

Town of Windsor Community Development Housing Rehabilitation Program For more information or questions contact the Office of Community Development at (860) 285-1984 REVISED: MAY, 2018 TOWN OF WINDSOR OFFICE

WNC HOUSING TAX CREDIT FUND VI, L.P., SERIES 13. Annual Report to Partners. For the fiscal year ended March 31, 2017

Annual Report to Partners For the fiscal year ended March 31, 2017 August 4, 2017 Re: WNC Housing Tax Credit Fund VI, L.P., Series 13 (the Partnership ) Dear Investor: We are pleased to provide you with

Annual Report to Partners For the fiscal year ended March 31, 2017 August 4, 2017 Re: WNC Housing Tax Credit Fund VI, L.P., Series 13 (the Partnership ) Dear Investor: We are pleased to provide you with

FHA HOUSING TAX CREDIT PILOT PROGRAM FREQUENTLY ASKED QUESTIONS May 23, 2012

FHA HOUSING TAX CREDIT PILOT PROGRAM FREQUENTLY ASKED QUESTIONS May 23, 2012 Eligible Projects Q. Can the Pilot Program be used to acquire and rehab an existing market-rate property that will be converted

FHA HOUSING TAX CREDIT PILOT PROGRAM FREQUENTLY ASKED QUESTIONS May 23, 2012 Eligible Projects Q. Can the Pilot Program be used to acquire and rehab an existing market-rate property that will be converted

Final Regulations adopted January 30, 2002 (redlined version)

") CALIFORNIA TAX CREDIT ALLOCATION COMMITTEE REGULATIONS IMPLEMENTING THE FEDERAL AND STATE LOW INCOME HOUSING TAX CREDIT LAWS CALIFORNIA CODE OF REGULATIONS, TITLE 4, DIVISION 17, CHAPTER 1 Final Regulations

CALIFORNIA TAX CREDIT ALLOCATION COMMITTEE REGULATIONS IMPLEMENTING THE FEDERAL AND STATE LOW INCOME HOUSING TAX CREDIT LAWS CALIFORNIA CODE OF REGULATIONS, TITLE 4, DIVISION 17, CHAPTER 1 Final Regulations

Chapter 20. Federal Income Taxation. IRS Tax Classifications. IRS Tax Classifications. Taxation of Individuals & Corporations

Federal Income Taxation Chapter 20 Income Taxation and Value Whether you like it or not, you have a silent partner who shares in your enterprise If RE investors are successful, federal (& usually state)

Federal Income Taxation Chapter 20 Income Taxation and Value Whether you like it or not, you have a silent partner who shares in your enterprise If RE investors are successful, federal (& usually state)

Family & Elderly Family Apartments

FHA INSURED LOANS ~ Multifamily Accelerated Processing (MAP) ACQUISITION or REFINANCE Of EXISTING OCCUPIED RENTAL APARTMENTS Section 223(f) Family & Elderly Family Apartments PROGRAM FEATURES Fixed-rate,

FHA INSURED LOANS ~ Multifamily Accelerated Processing (MAP) ACQUISITION or REFINANCE Of EXISTING OCCUPIED RENTAL APARTMENTS Section 223(f) Family & Elderly Family Apartments PROGRAM FEATURES Fixed-rate,

Section 1602 Program Program Description. July 2, 2009

TENNESSEE HOUSING DEVELOPMENT AGENCY Section 1602 Program 2009 Program Description July 2, 2009 as amended January 26, 2010 TENNESSEE HOUSING DEVELOPMENT AGENCY SECTION 1602 PROGRAM DESCRIPTION 2009 PART

TENNESSEE HOUSING DEVELOPMENT AGENCY Section 1602 Program 2009 Program Description July 2, 2009 as amended January 26, 2010 TENNESSEE HOUSING DEVELOPMENT AGENCY SECTION 1602 PROGRAM DESCRIPTION 2009 PART

Insights. Community Developments. Low-Income Housing Tax Credits: Affordable Housing Investment Opportunities for Banks. February 2008.

Comptroller of the Currency Administrator of National Banks US Department of the Treasury Community Developments February 2008 Community Affairs Department Insights Low-Income Housing Tax Credits: Affordable

Comptroller of the Currency Administrator of National Banks US Department of the Treasury Community Developments February 2008 Community Affairs Department Insights Low-Income Housing Tax Credits: Affordable

SONOMA COUNTY COMMUNITY DEVELOPMENT COMMISSION

SONOMA COUNTY COMMUNITY DEVELOPMENT COMMISSION LOAN POLICIES Affordable Housing Development Affordable Housing Acquisition & Preservation Multi-family Housing Rehabilitation Community Facilities Table

SONOMA COUNTY COMMUNITY DEVELOPMENT COMMISSION LOAN POLICIES Affordable Housing Development Affordable Housing Acquisition & Preservation Multi-family Housing Rehabilitation Community Facilities Table

Notice: CPD CPD Division Directors All HOME Coordinators Issued: December 22, 2015 All HOME Participating Jurisdictions

U.S. Department of Housing and Urban Development Community Planning and Development Special Attention of: Notice: CPD-15-11 CPD Division Directors All HOME Coordinators Issued: December 22, 2015 All HOME

U.S. Department of Housing and Urban Development Community Planning and Development Special Attention of: Notice: CPD-15-11 CPD Division Directors All HOME Coordinators Issued: December 22, 2015 All HOME

GMHF Affordable Housing Loan Products

GMHF Affordable Housing Loan Products FOR RENTAL & SINGLE FAMILY AFFORDABLE HOUSING Predevelopment Loans Acquisition Loans Construction /Rehab Loans Tax Credit Bridge Loans Mini Perm & Permanent Loans

GMHF Affordable Housing Loan Products FOR RENTAL & SINGLE FAMILY AFFORDABLE HOUSING Predevelopment Loans Acquisition Loans Construction /Rehab Loans Tax Credit Bridge Loans Mini Perm & Permanent Loans

3 rd Annual NYS Redevelopment Summit Albany NY Keys to Successful Brownfield Redevelopment Tax Credits and Other Financial Incentives June 13, 2018

3 rd Annual NYS Redevelopment Summit Albany NY Keys to Successful Brownfield Redevelopment Tax Credits and Other Financial Incentives June 13, 2018 National Development Council Who We Are National non-profit

3 rd Annual NYS Redevelopment Summit Albany NY Keys to Successful Brownfield Redevelopment Tax Credits and Other Financial Incentives June 13, 2018 National Development Council Who We Are National non-profit

Federal Tax Code 2017 House and Senate Tax Reform Proposals

Current Law (Section) H.R. 1 Tax Cuts and Jobs Act (House version) House Comments and Recommendations H.R. 1 Tax Cuts and Jobs Act (Senate version) Senate Comments and Recommendations (26 U.S.C. 121) Exclusion

Current Law (Section) H.R. 1 Tax Cuts and Jobs Act (House version) House Comments and Recommendations H.R. 1 Tax Cuts and Jobs Act (Senate version) Senate Comments and Recommendations (26 U.S.C. 121) Exclusion

Benefits and Overview of Nonprofits. Participating in LIHTC Partnerships

Benefits and Overview of Nonprofits Participating in LIHTC Partnerships for the Florida Housing Coalition Conference Christina Apostolidis Partner, Naples, FL Novogradac & Company LLP christina.apostolidis@novoco.com

Benefits and Overview of Nonprofits Participating in LIHTC Partnerships for the Florida Housing Coalition Conference Christina Apostolidis Partner, Naples, FL Novogradac & Company LLP christina.apostolidis@novoco.com

Affordable Housing Program 2018 Implementation Plan

Affordable Housing Program 2018 Implementation Plan I) Overview of the Affordable Housing Program A) Introduction Affordable Housing Program 2018 Implementation Plan The Affordable Housing Program ( AHP

Affordable Housing Program 2018 Implementation Plan I) Overview of the Affordable Housing Program A) Introduction Affordable Housing Program 2018 Implementation Plan The Affordable Housing Program ( AHP

FHA INSURED LOANS ~ Multifamily Accelerated Processing (MAP) NEW CONSTRUCTION or SUBSTANTIAL REHABILITATION Of RENTAL APARTMENTS

NEW CONSTRUCTION or SUBSTANTIAL REHABILITATION Of RENTAL APARTMENTS") FHA INSURED LOANS ~ Multifamily Accelerated Processing (MAP) NEW CONSTRUCTION or SUBSTANTIAL REHABILITATION Of RENTAL APARTMENTS Section 221(d) Family Apartments, all Areas Section 220 Family Apartments,

FHA INSURED LOANS ~ Multifamily Accelerated Processing (MAP) NEW CONSTRUCTION or SUBSTANTIAL REHABILITATION Of RENTAL APARTMENTS Section 221(d) Family Apartments, all Areas Section 220 Family Apartments,

Audit Technique Guide IRC 42, Low-Income Housing Credit. DRAFT FOR COMMENT ONLY January 2014

Audit Technique Guide IRC 42, Low-Income Housing Credit DRAFT FOR COMMENT ONLY January 2014 This Audit Technique Guide is a draft for comment and may not be citied as authority. Information in the document

Audit Technique Guide IRC 42, Low-Income Housing Credit DRAFT FOR COMMENT ONLY January 2014 This Audit Technique Guide is a draft for comment and may not be citied as authority. Information in the document

U.S. Department of Housing and Urban Development Community Planning and Development

U.S. Department of Housing and Urban Development Community Planning and Development Special Attention of: Notice: CPD 97-03 All Secretary's Representatives All State/Area Coordinators Issued: March 27,

U.S. Department of Housing and Urban Development Community Planning and Development Special Attention of: Notice: CPD 97-03 All Secretary's Representatives All State/Area Coordinators Issued: March 27,

GOVERNOR STATE OF WISCONSIN

JIM DOYLE GOVERNOR STATE OF WISCONSIN August 31, 2010 Dear Friend of Affordable Housing: It is my pleasure to announce that Wisconsin s ongoing commitment to affordable housing will be continued into 2011

JIM DOYLE GOVERNOR STATE OF WISCONSIN August 31, 2010 Dear Friend of Affordable Housing: It is my pleasure to announce that Wisconsin s ongoing commitment to affordable housing will be continued into 2011

HOUSING AUTHORITY OF WASHINGTON COUNTY, OREGON BOND ISSUANCE GUIDELINES

HOUSING AUTHORITY OF WASHINGTON COUNTY, OREGON BOND ISSUANCE GUIDELINES 2016 PAB GUIDE Page 1 TABLE OF CONTENTS I. INTRODUCTION.... 3 II. III. IV. POLICY STATEMENT...3 TENANT INCOME REQUIREMENTS.. 4 BOND

HOUSING AUTHORITY OF WASHINGTON COUNTY, OREGON BOND ISSUANCE GUIDELINES 2016 PAB GUIDE Page 1 TABLE OF CONTENTS I. INTRODUCTION.... 3 II. III. IV. POLICY STATEMENT...3 TENANT INCOME REQUIREMENTS.. 4 BOND

HUD s Rental Assistance Demonstration Program

NALHFA 2014 Annual Educational Conference April 2-5, 2014 Omni Hotel at CNN Center HUD s Rental Assistance Demonstration Program Presented By: John B. Rucker, III Executive Vice President john.rucker@merchantcapital.com

NALHFA 2014 Annual Educational Conference April 2-5, 2014 Omni Hotel at CNN Center HUD s Rental Assistance Demonstration Program Presented By: John B. Rucker, III Executive Vice President john.rucker@merchantcapital.com

NEW HAMPSHIRE HOUSING FINANCE AUTHORITY UNDERWRITING STANDARDS AND DEVELOPMENT POLICIES FOR MULTI- FAMILY FINANCE

NEW HAMPSHIRE HOUSING FINANCE AUTHORITY UNDERWRITING STANDARDS AND DEVELOPMENT POLICIES FOR MULTI- FAMILY FINANCE TABLE OF CONTENTS PAGE(S) Part 1 Purpose 1.01 Purpose 4 Part 2 Loan Terms and Conditions

NEW HAMPSHIRE HOUSING FINANCE AUTHORITY UNDERWRITING STANDARDS AND DEVELOPMENT POLICIES FOR MULTI- FAMILY FINANCE TABLE OF CONTENTS PAGE(S) Part 1 Purpose 1.01 Purpose 4 Part 2 Loan Terms and Conditions

DCA Summary of 2008 Qualified Allocation Plan Revisions Core Plan, Appendix I & II

The following is intended to assist potential Applicants at identifying important revisions in the Qualified Application for the 2008 Application round. This list represents most, but not all, QAP changes.

The following is intended to assist potential Applicants at identifying important revisions in the Qualified Application for the 2008 Application round. This list represents most, but not all, QAP changes.

WNC HOUSING TAX CREDIT FUND VI, L.P., SERIES 10. Quarterly Report to Partners. September 30, 2017

Quarterly Report to Partners September 30, 2017 November 30, 2017 Re: WNC Housing Tax Credit Fund VI, L.P., Series 10 (the Partnership ) Dear Investor: We are pleased to provide you with the Partnership

Quarterly Report to Partners September 30, 2017 November 30, 2017 Re: WNC Housing Tax Credit Fund VI, L.P., Series 10 (the Partnership ) Dear Investor: We are pleased to provide you with the Partnership

WISCONSIN HOUSING AND ECONOMIC DEVELOPMENT AUTHORITY Low Income Housing Tax Credit (LIHTC) Program COST CERTIFICATION AUDIT GUIDE

Program COST CERTIFICATION AUDIT GUIDE") WISCONSIN HOUSING AND ECONOMIC DEVELOPMENT AUTHORITY Low Income Housing Tax Credit (LIHTC) Program COST CERTIFICATION AUDIT GUIDE REVISED NOVEMBER 13, 2007 BACKGROUND Owners of Projects consisting of more

WISCONSIN HOUSING AND ECONOMIC DEVELOPMENT AUTHORITY Low Income Housing Tax Credit (LIHTC) Program COST CERTIFICATION AUDIT GUIDE REVISED NOVEMBER 13, 2007 BACKGROUND Owners of Projects consisting of more

WNC HOUSING TAX CREDIT FUND VI, L.P., SERIES 8. For the fiscal year ended March, 31, 2018 and 2017

WNC HOUSING TAX CREDIT FUND VI, L.P., SERIES 8 Financial Statements and Independent Auditors Report For the fiscal year ended March, 31, 2018 and 2017 August 3, 2018 re: WNC Housing Tax Credit Fund VI,

WNC HOUSING TAX CREDIT FUND VI, L.P., SERIES 8 Financial Statements and Independent Auditors Report For the fiscal year ended March, 31, 2018 and 2017 August 3, 2018 re: WNC Housing Tax Credit Fund VI,

Presented by: 2016 Zeffert & Associates All Rights Reserved

Presented by: 2016 Zeffert & Associates All Rights Reserved The Goal of this Training The purpose of this training is to provide information for all interested personnel to successfully provide housing

Presented by: 2016 Zeffert & Associates All Rights Reserved The Goal of this Training The purpose of this training is to provide information for all interested personnel to successfully provide housing

ARLINGTON COUNTY, VIRGINIA. County Board Agenda Item Meeting of November 18, 2017

ARLINGTON COUNTY, VIRGINIA County Board Agenda Item Meeting of November 18, 2017 DATE: November 9, 2017 SUBJECT: Allocation of up to $13,511,036 in Fiscal Year 2018 Affordable Housing Investment Fund (AHIF)

ARLINGTON COUNTY, VIRGINIA County Board Agenda Item Meeting of November 18, 2017 DATE: November 9, 2017 SUBJECT: Allocation of up to $13,511,036 in Fiscal Year 2018 Affordable Housing Investment Fund (AHIF)

Exhibit A DRAFT Measure A1 Implementation Policies Rental Housing Development Fund & Innovation and Opportunity Fund

Exhibit A DRAFT Measure A1 Implementation Policies Rental Housing Development Fund & Innovation and Opportunity Fund On June 28, 2016, the Alameda County Board of Supervisors placed Measure A1 on the November

Exhibit A DRAFT Measure A1 Implementation Policies Rental Housing Development Fund & Innovation and Opportunity Fund On June 28, 2016, the Alameda County Board of Supervisors placed Measure A1 on the November

WNC HOUSING TAX CREDIT FUND VI, L.P., SERIES 10. Annual Report to Partners. For the fiscal year ended March 31, 2017

WNC HOUSING TAX CREDIT FUND VI, L.P., SERIES 10 Annual Report to Partners For the fiscal year ended March 31, 2017 August 4, 2017 Re: WNC Housing Tax Credit Fund VI, L.P., Series 10 (the Partnership )

WNC HOUSING TAX CREDIT FUND VI, L.P., SERIES 10 Annual Report to Partners For the fiscal year ended March 31, 2017 August 4, 2017 Re: WNC Housing Tax Credit Fund VI, L.P., Series 10 (the Partnership )

TEXAS HOUSING IMPACT FUND POLICY AND GUIDELINES 1 TABLE OF CONTENTS

TEXAS HOUSING IMPACT FUND POLICY AND GUIDELINES TABLE OF CONTENTS 1. POLICY.... 2 2. SOURCE OF FUNDS.... 2 3. ELIGIBLE ACTIVITIES... 2 4. USE OF LOAN PROCEEDS... 2 5. APPLICATION PROCESS... 2 6. APPLICATION

TEXAS HOUSING IMPACT FUND POLICY AND GUIDELINES TABLE OF CONTENTS 1. POLICY.... 2 2. SOURCE OF FUNDS.... 2 3. ELIGIBLE ACTIVITIES... 2 4. USE OF LOAN PROCEEDS... 2 5. APPLICATION PROCESS... 2 6. APPLICATION

Measure A1 Implementation Policies Rental Housing Development Fund & Innovation and Opportunity Fund

Measure A1 Implementation Policies Rental Housing Development Fund & Innovation and Opportunity Fund On June 28, 2016, the Alameda County Board of Supervisors placed Measure A1 on the November ballot for

Measure A1 Implementation Policies Rental Housing Development Fund & Innovation and Opportunity Fund On June 28, 2016, the Alameda County Board of Supervisors placed Measure A1 on the November ballot for

Tennessee Housing Development Agency 404 James Robertson Parkway, Suite 1200 Nashville, Tennessee /

Ted Fellman Tennessee Housing Development Agency 404 James Robertson Parkway, Suite 1200 Nashville, Tennessee 37243-0900 615/815-2200 Writer s Phone Number: Executive Director 615-815-2200 Writer s Fax

Ted Fellman Tennessee Housing Development Agency 404 James Robertson Parkway, Suite 1200 Nashville, Tennessee 37243-0900 615/815-2200 Writer s Phone Number: Executive Director 615-815-2200 Writer s Fax

Agenda. Process Findings Directions Forward

Agenda Process Findings Directions Forward Process Findings Findings: Market Survey Findings: Market Survey Findings: Market Survey Findings: Workforce Survey Findings: Themes Regional Benefits Rental

Agenda Process Findings Directions Forward Process Findings Findings: Market Survey Findings: Market Survey Findings: Market Survey Findings: Workforce Survey Findings: Themes Regional Benefits Rental

THE CITY OF LOS ANGELES HOUSING AND COMMUNITY INVESTMENT DEPARTMENT (HCIDLA)

") Council File# 16-0085 THE CITY OF LOS ANGELES HOUSING AND COMMUNITY INVESTMENT DEPARTMENT (HCIDLA) POLICIES FOR EVALUATING THE RECAPITALIZATION OF CERTAIN AFFORDABLE HOUSING DEVELOPMENTS WITH PRE-EXISTING

Council File# 16-0085 THE CITY OF LOS ANGELES HOUSING AND COMMUNITY INVESTMENT DEPARTMENT (HCIDLA) POLICIES FOR EVALUATING THE RECAPITALIZATION OF CERTAIN AFFORDABLE HOUSING DEVELOPMENTS WITH PRE-EXISTING

PIDC/PHFA Affordable Housing Seminar March 6, 2013

PIDC/PHFA Affordable Housing Seminar March 6, 2013 PAID Background Overview: Managed by PIDC, PAID is a public authority created by the City of Philadelphia pursuant to the Economic Development Financing

PIDC/PHFA Affordable Housing Seminar March 6, 2013 PAID Background Overview: Managed by PIDC, PAID is a public authority created by the City of Philadelphia pursuant to the Economic Development Financing

2010 QUALIFIED ALLOCATION PLAN

2010 QUALIFIED ALLOCATION PLAN Revised 15 January 2010 and supercedes all previously issued copies Effective for allocations made after December 31, 2009, until December 31, 2010, unless amended. Table

2010 QUALIFIED ALLOCATION PLAN Revised 15 January 2010 and supercedes all previously issued copies Effective for allocations made after December 31, 2009, until December 31, 2010, unless amended. Table

REQUIREMENTS FOR YEAR-END AUDITED FINANCIAL STATEMENTS VHFA FINANCED PROJECTS

REQUIREMENTS FOR YEAR-END AUDITED FINANCIAL STATEMENTS VHFA FINANCED PROJECTS The financial statements of the owner must conform with the following requirements: 1. The financial statements must be audited.

REQUIREMENTS FOR YEAR-END AUDITED FINANCIAL STATEMENTS VHFA FINANCED PROJECTS The financial statements of the owner must conform with the following requirements: 1. The financial statements must be audited.

U.S. Department of Housing and Urban Development Community Planning and Development

U.S. Department of Housing and Urban Development Community Planning and Development Special Attention of: Notice CPD 96-9 All Secretary's Representatives All State/Area Coordinators Issued: December 20,

U.S. Department of Housing and Urban Development Community Planning and Development Special Attention of: Notice CPD 96-9 All Secretary's Representatives All State/Area Coordinators Issued: December 20,

TENNESSEE HOUSING DEVELOPMENT AGENCY. Low-Income Housing Tax Credit. Qualified Allocation Plan

TENNESSEE HOUSING DEVELOPMENT AGENCY Low-Income Housing Tax Credit Qualified Allocation Plan 2000 TENNESSEE HOUSING DEVELOPMENT AGENCY LOW-INCOME HOUSING TAX CREDIT QUALIFIED ALLOCATION PLAN 2000 Part

TENNESSEE HOUSING DEVELOPMENT AGENCY Low-Income Housing Tax Credit Qualified Allocation Plan 2000 TENNESSEE HOUSING DEVELOPMENT AGENCY LOW-INCOME HOUSING TAX CREDIT QUALIFIED ALLOCATION PLAN 2000 Part

UNIVERSITY PLACE SOUTHEAST, L.P. TN FINANCIAL STATEMENTS DECEMBER 31, 2011

FINANCIAL STATEMENTS DECEMBER 31, 2011 Contents Page Independent Auditors Report... 1-2 Balance Sheet... 3-4 Statement Of Operations... 5 Statement Of Partners Equity... 6 Statement Of Cash Flows... 7

FINANCIAL STATEMENTS DECEMBER 31, 2011 Contents Page Independent Auditors Report... 1-2 Balance Sheet... 3-4 Statement Of Operations... 5 Statement Of Partners Equity... 6 Statement Of Cash Flows... 7

NEW HAMPSHIRE 2006 QUALIFIED ALLOCATION PLAN FOR THE LOW INCOME HOUSING TAX CREDIT PROGRAM 10/27/05

NEW HAMPSHIRE 2006 QUALIFIED ALLOCATION PLAN FOR THE LOW INCOME HOUSING TAX CREDIT PROGRAM 10/27/05 i TABLE OF CONTENTS Page HFA:109.01 Introduction 1 HFA:109.02 LIHTC Program Summary 1 A. Program Administration

NEW HAMPSHIRE 2006 QUALIFIED ALLOCATION PLAN FOR THE LOW INCOME HOUSING TAX CREDIT PROGRAM 10/27/05 i TABLE OF CONTENTS Page HFA:109.01 Introduction 1 HFA:109.02 LIHTC Program Summary 1 A. Program Administration

PENNSYLVANIA HOUSING FINANCE AGENCY (2018 UNDERWRITING APPLICATION)

") TAX CREDIT PROGRAM GUIDELINES The Low-Income Housing Tax Credit Program ("Tax Credit Program") is a federal program created by the 1986 Tax Reform Act and amended pursuant to several subsequent federal

TAX CREDIT PROGRAM GUIDELINES The Low-Income Housing Tax Credit Program ("Tax Credit Program") is a federal program created by the 1986 Tax Reform Act and amended pursuant to several subsequent federal

Background. MUNICIPALITIES AND DOWNTOWN REDEVELOPMENT IN SOUTH CAROLINA: Expanding The Tool Kit

MUNICIPALITIES AND DOWNTOWN REDEVELOPMENT IN SOUTH CAROLINA: Expanding The Tool Kit Background Over past 30 years, shift focus from remediation to development Need for commercially vibrant, historically

MUNICIPALITIES AND DOWNTOWN REDEVELOPMENT IN SOUTH CAROLINA: Expanding The Tool Kit Background Over past 30 years, shift focus from remediation to development Need for commercially vibrant, historically

CHAPTER NON-COMPETITIVE AFFORDABLE MULTIFAMILY RENTAL HOUSING PROGRAMS (MMRB/HC)

") CHAPTER 67-21 NON-COMPETITIVE AFFORDABLE MULTIFAMILY RENTAL HOUSING PROGRAMS (MMRB/HC) PART I ADMINISTRATION 67-21.001 Purpose and Intent 67-21.002 Definitions 67-21.0025 Miscellaneous Criteria 67-21.003

CHAPTER 67-21 NON-COMPETITIVE AFFORDABLE MULTIFAMILY RENTAL HOUSING PROGRAMS (MMRB/HC) PART I ADMINISTRATION 67-21.001 Purpose and Intent 67-21.002 Definitions 67-21.0025 Miscellaneous Criteria 67-21.003

Experience & Integrity. NH&RA 2016 Spring Developers Forum Marina Del Ray Dan Duda May, 2016

Experience & Integrity NH&RA 2016 Spring Developers Forum Marina Del Ray Dan Duda May, 2016 About Churchill Stateside Group Churchill Stateside Group, LLC (CSG) is a private financial services company

Experience & Integrity NH&RA 2016 Spring Developers Forum Marina Del Ray Dan Duda May, 2016 About Churchill Stateside Group Churchill Stateside Group, LLC (CSG) is a private financial services company

DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT

DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT This chapter presents the budget and program estimates for the Department of Housing and Urban Development. In order to better address the needs of communities

DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT This chapter presents the budget and program estimates for the Department of Housing and Urban Development. In order to better address the needs of communities

Low-Income Housing Tax Credit Provisions in the Housing and Economic Recovery Act of 2008

August 2008 Low-Income Housing Tax Credit Provisions in the Housing and Economic Recovery Act of 2008 BY ALAN S. COHEN, MICHAEL D. HAUN AND MATT WALDING The Housing and Economic Recovery Act of 2008 1

August 2008 Low-Income Housing Tax Credit Provisions in the Housing and Economic Recovery Act of 2008 BY ALAN S. COHEN, MICHAEL D. HAUN AND MATT WALDING The Housing and Economic Recovery Act of 2008 1

WNC HOUSING TAX CREDIT FUND VI, L.P., SERIES 7. Annual Report to Partners. For the fiscal year ended March 31, 2018

Annual Report to Partners For the fiscal year ended March 31, 2018 August 3, 2018 Re: WNC Housing Tax Credit Fund VI, L.P., Series 7 (the Partnership ) Dear Investor: We are pleased to provide you with

Annual Report to Partners For the fiscal year ended March 31, 2018 August 3, 2018 Re: WNC Housing Tax Credit Fund VI, L.P., Series 7 (the Partnership ) Dear Investor: We are pleased to provide you with

TAX CREDIT APPLICATION PACKAGE 2015 SUPPLEMENT HOUSING DEVELOPMENT FUND

TAX CREDIT APPLICATION PACKAGE 2015 SUPPLEMENT HOUSING DEVELOPMENT FUND If applying for Low Income Housing Tax Credits and a Housing Development Fund Loan, please review the attached, which describes the

TAX CREDIT APPLICATION PACKAGE 2015 SUPPLEMENT HOUSING DEVELOPMENT FUND If applying for Low Income Housing Tax Credits and a Housing Development Fund Loan, please review the attached, which describes the

CALIFORNIA TAX CREDIT ALLOCATION COMMITTEE REGULATIONS IMPLEMENTING THE FEDERAL AND STATE LOW INCOME HOUSING TAX CREDIT LAWS

CALIFORNIA TAX CREDIT ALLOCATION COMMITTEE REGULATIONS IMPLEMENTING THE FEDERAL AND STATE LOW INCOME HOUSING TAX CREDIT LAWS CALIFORNIA CODE OF REGULATIONS TITLE 4, DIVISION 17, CHAPTER 1 February 16,

CALIFORNIA TAX CREDIT ALLOCATION COMMITTEE REGULATIONS IMPLEMENTING THE FEDERAL AND STATE LOW INCOME HOUSING TAX CREDIT LAWS CALIFORNIA CODE OF REGULATIONS TITLE 4, DIVISION 17, CHAPTER 1 February 16,

Public Law H.R Joint Committee on Taxation Technical Explanation of Division C of H.R. 3221

9/5/2008 Housing Assistance Tax Act of 2008 Public Law 110-289 H.R. 3221 Joint Committee on Taxation Technical Explanation of Division C of H.R. 3221 H.R. 3221, the Housing and Economic Recovery Act of

9/5/2008 Housing Assistance Tax Act of 2008 Public Law 110-289 H.R. 3221 Joint Committee on Taxation Technical Explanation of Division C of H.R. 3221 H.R. 3221, the Housing and Economic Recovery Act of

LEGISLATIVE PRIORITIES

HUD SECTION 108 The Section 108 Program allows grantees of the Community Development Block Grant (CDBG) Program to borrow Federally-guaranteed funds for community development purposes. Section 108 borrowers

HUD SECTION 108 The Section 108 Program allows grantees of the Community Development Block Grant (CDBG) Program to borrow Federally-guaranteed funds for community development purposes. Section 108 borrowers

Memorandum of Understanding Execution Copy MEMORANDUM OF UNDERSTANDING

5 6 7 8 9 0 5 6 7 8 9 0 5 6 7 8 9 0 5 6 7 8 MEMORANDUM OF UNDERSTANDING This Memorandum of Understanding ( MOU ) is executed on this day of, 0 by and between the City of Downtown Development Authority

5 6 7 8 9 0 5 6 7 8 9 0 5 6 7 8 9 0 5 6 7 8 MEMORANDUM OF UNDERSTANDING This Memorandum of Understanding ( MOU ) is executed on this day of, 0 by and between the City of Downtown Development Authority

TENNESSEE HOUSING DEVELOPMENT AGENCY. Low-Income Housing Tax Credit Initial Application

TENNESSEE HOUSING DEVELOPMENT AGENCY 2013 Low-Income Housing Tax Credit Initial Application 1 Initial Application Instructions Low Income Housing Tax Credit Program Year 2013 Development PLEASE READ THESE

TENNESSEE HOUSING DEVELOPMENT AGENCY 2013 Low-Income Housing Tax Credit Initial Application 1 Initial Application Instructions Low Income Housing Tax Credit Program Year 2013 Development PLEASE READ THESE

Affordable Housing Program (AHP) Implementation Plan

Implementation Plan") Affordable Housing Program (AHP) Implementation Plan Effective March 28December 12, 2014 Affordable Housing Program (AHP) Implementation Plan Table of Contents I. Introduction... 3 A. General...3 B. Funding

Affordable Housing Program (AHP) Implementation Plan Effective March 28December 12, 2014 Affordable Housing Program (AHP) Implementation Plan Table of Contents I. Introduction... 3 A. General...3 B. Funding

FUND FOR RESTORATION OF MULTI-FAMILY HOUSING THIRD ROUND MONMOUTH/OCEAN SET-ASIDE PROGRAM GUIDELINES Approved: May 21, 2015

FUND FOR RESTORATION OF MULTI-FAMILY HOUSING THIRD ROUND MONMOUTH/OCEAN SET-ASIDE PROGRAM GUIDELINES Approved: May 21, 2015 The Department of Community Affairs ( DCA ) Community Development Block Grant

FUND FOR RESTORATION OF MULTI-FAMILY HOUSING THIRD ROUND MONMOUTH/OCEAN SET-ASIDE PROGRAM GUIDELINES Approved: May 21, 2015 The Department of Community Affairs ( DCA ) Community Development Block Grant

What is a QAP? What is a QAP? Q ualified A llocation

What is a QAP? What is a QAP? Q ualified A llocation P lan 1 Explain three different ways: Overview Legally Practically Overview Set of policies determining distribution of LIHTCs Also include rules for

What is a QAP? What is a QAP? Q ualified A llocation P lan 1 Explain three different ways: Overview Legally Practically Overview Set of policies determining distribution of LIHTCs Also include rules for

RESOURCES RESOURCES...SECTION 1

RESOURCES RESOURCES......SECTION 1 Resources 1. First Mortgage Financing 2 2. Deferred Payment Loan Funds 2 3. Housing Tax Credits (9% and 4%) 2 4. Predevelopment Loan Program 3 5. HOME Investment Partnerships

RESOURCES RESOURCES......SECTION 1 Resources 1. First Mortgage Financing 2 2. Deferred Payment Loan Funds 2 3. Housing Tax Credits (9% and 4%) 2 4. Predevelopment Loan Program 3 5. HOME Investment Partnerships

HOMEBUYERS PURCHASE PROGRAM POLICIES & PROCEDURES MANUAL PY 2007 SUMMARY

CITY OF EAST ORANGE, NEW JERSEY NEIGHBORHOOD HOUSING & REVITALIZATION DIVISION HOMEBUYERS PURCHASE PROGRAM POLICIES & PROCEDURES MANUAL PY 2007 SUMMARY The City of East Orange HOMEBuyers Purchase Program

CITY OF EAST ORANGE, NEW JERSEY NEIGHBORHOOD HOUSING & REVITALIZATION DIVISION HOMEBUYERS PURCHASE PROGRAM POLICIES & PROCEDURES MANUAL PY 2007 SUMMARY The City of East Orange HOMEBuyers Purchase Program

Mississippi Development Authority. Katrina Supplemental CDBG Funds. For. Affordable Housing Tax Credit Gap Funding

Katrina Supplemental CDBG Funds For Affordable Housing Tax Credit Gap Funding Partial Action Plan (Public comment version) Partial Action Plan For Affordable Housing Tax Credit Gap Funding OVERVIEW This

Katrina Supplemental CDBG Funds For Affordable Housing Tax Credit Gap Funding Partial Action Plan (Public comment version) Partial Action Plan For Affordable Housing Tax Credit Gap Funding OVERVIEW This

DEVELOPER PROGRAMS. Reasonable, and fall within the underwriting standards; and Affordable and meet the City s definition of affordability.

DEVELOPER PROGRAMS New Construction and Substantial Rehabilitation Program The purpose of this program is to provide financial assistance to new developments or substantial rehabilitation developments,

DEVELOPER PROGRAMS New Construction and Substantial Rehabilitation Program The purpose of this program is to provide financial assistance to new developments or substantial rehabilitation developments,

Subsidy Layering Review Guidelines & Application

Subsidy Layering Review Guidelines & Application In 2010, HUD granted the Ohio Housing Finance Agency (OHFA) the authority to complete Subsidy Layering Reviews (SLR). Public Housing Authorities (PHA) SLR

Subsidy Layering Review Guidelines & Application In 2010, HUD granted the Ohio Housing Finance Agency (OHFA) the authority to complete Subsidy Layering Reviews (SLR). Public Housing Authorities (PHA) SLR