2016 IRS Collections Representation Boot Camp

|

|

|

- Clyde Manning

- 5 years ago

- Views:

Transcription

1 2016 IRS Collections Representation Boot Camp Presented by: Dan Henn, CPA & Jassen Bowman, EA Sponsors: IRS Program Number: SDQJW-T I Sponsor ID # Before We Get Started For proper CPE tracking, please sign in and out each day. No need to sign in/out for breaks and lunch. Please sign out if you are going to miss a particular session, also. Twitter hashtag: #TaxResolutionTraining Acronyms: Don t hesitate to ask what they mean. Questions: Feel free to ask questions during the presentations. This makes for better learning for everybody. 1

2 Collections Due Process Appeals Presented by Jassen Bowman, EA Course Objectives Purpose of CDP Appeals Eligibility for CDP Forms Appeals outcomes 2

3 Why file a CDP? Stay of enforcement but for tax periods covered only Time CDPs are Appeal s lowest priority despite being ¾ of their case inventory Appeals is your friend Their job is to prevent litigation Why file a CDP? continued Approximately half of all my IA s have been granted in Appeals as a result of a CDP. Do be aware that CDP tolls CSED. Look for CDP rights in transcript review. 3

4 Statutory Authority IRC 6320: Right to appeal NFTL (668-Y) IRC 6330: Right to appeal proposed levies and actual levies, including: Jeopardy levies State tax refund levies Bank levies A/R levies Wage levies Appeals Limits By statute (26 USC 6320(b)(2)) Taxpayers are only entitled to ONE appeals hearing per tax type and tax period! but applies to liens and levies separately. 4

5 Appeals Limits By statute (26 USC 6330) They re only required to tell you once that they re going to levy. Letter 3174 is merely a courtesy under the IRM, not required by law. Appeals Limits Per 26 USC 6330(f) IRS must offer you the right to a hearing, but can still proceed with levy action in cases of: Disqualified Employment Tax Levy 2-year lookback rule Federal contractor levies State tax refund levies Jeopardy levies 5

6 Forms Form 12153, Request For Collection Due Process or Equivalent Hearing. 6

7 7

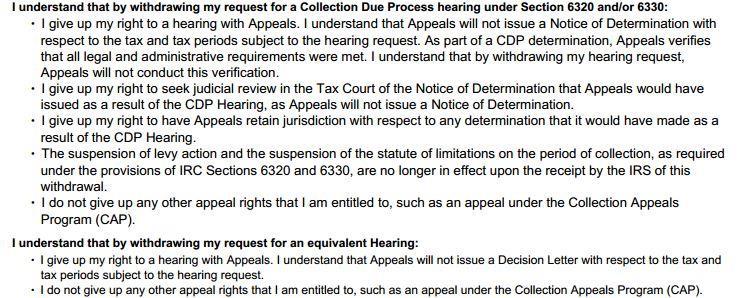

8 Forms Form 12256, Withdrawal of Request for Collection Due Process or Equivalent Hearing Why would you ever want to withdraw a CDP? 8

9 9

10 Appeals Process Hurry up and wait Use this time wisely! Expect a request for information 433 with full documentation (even if under $50k) Make note of who is calling who. Don t miss it! If the scheduled date/time doesn t work, request rescheduling well in advance. Appeals Personnel Settlement Officers Primarily deal with collection alternatives Appeals Officers Primarily deal with liability issues Appeals Team Managers Review & approve collection alternatives Account Resolution Specialists Support staff 10

11 Appeals Hearings Hearings are purposefully informal Verify administrative procedures have been met Frivolous appeals Appeals Hearings Duty to ensure that collection action balances the need for the efficient collection of taxes with the legitimate concern of the person that any collection action be no more intrusive than necessary. This helps prevent lawsuits May not raise issues considered in previous appeals or litigation Important to know your client case history 11

12 Equivalent Hearings If you missed the 30-day window, can still request EH within one year No suspension of collections action No CSED toll No retained jurisdiction No judicial review rights Appeals Outcomes If agreement is reached Appeals sends Form 12257, Waiver of Appeals Notice of Determination in a Collection Due Process Hearing Waives judicial review rights Not required to sign If no agreement is reached Notice of Determination issued Comes with additional rights (Tax Court) 12

13 Appeals Judicial Approach & Culture (AJAC) Appeals improvement project started in 2012 Goal is to increase the independence and distance between Appeals and other IRS functions Appeals owns the process of dispute resolution they do NOT assess tax, investigate, examine, etc. Appeals Policy Changes FY 13: Clarify that Appeals Officers cannot take an investigatory approach to OIC appeals Takes collections and taxpayers word on most matters Will not seek to change asset valuations in OIC, but can consider taxpayer or collections provided documentation for changes 13

14 Appeals Policy Changes FY 14: Appeals will no longer raise NEW issues in hearings Will retain and resolve underdeveloped cases New OICs submitted within Appeals are reviewed by OIC centers, but case remains in Appeals jurisdiction 433-A(OIC) sent for review to avoid Appeals taking an investigatory stance Outside of CDP, OIC rejections in Appeals will no longer incur collection alternatives IA/CNC cases: NFTL determinations will not be made by Appeals Appeals Policy Changes Big Picture: Appeals does not want to be first finder of fact. Bigger Picture: Message to CFF to deliver only fully developed cases. E.g., do your job. 14

15 Quick Bonus Info OIC filed while CDP pending is retained by Appeals, but processed by OIC center. TIGTA : 2012 internal audit of CDP effectiveness Found no improvement in Appeals deficiencies CSED computation errors Appeals failed to properly document impartiality Improper classification of requests Honorable Mention Collection Appeals Program Streamlined, fast track Appeals process GM conference required within 2 business days Typically filed on levy action 15

16 Collection Appeals Program 941 levy releases 1. Third-party harm. 2. Jeopardize collection due to disruption of business operations. IRM Fun Times IRM 5.1.9, Collection Appeal Rights IRM , Pre-Levy Actions, Restrictions on Levy, Post-Levy Actions IRM , Collection Due Process Appeals Program For Tax Court related matters, also see CC , Tax Court jurisdiction in CDP cases to consider NON-CDP matters CC , Guidance for certain employment tax cases (including in CDP cases) 16

17 The CDP is one of the most powerful tools in your tax debt resolution arsenal USE IT! 17

18 2016 IRS Collections Representation Boot Camp Presented by: Dan Henn, CPA & Jassen Bowman, EA Sponsors: IRS Program Number: SDQJW-T I Sponsor ID # Trust Fund Recovery Penalty Assessment: Who s On The Hook? Presented by Jassen Bowman, EA 18

19 Course Objectives Provide an overview of personal assessment criteria for the Trust Fund Recovery Penalty. Understand the conditions necessary for an individual to be declared a responsible party. Understand the conditions necessary for an individual to be declared a willful party. Review the completion of IRS Form Discuss defenses against personal assessment. Personal Assessment Overview 19

20 What is the Trust Fund Recovery Penalty? IRC 3505, Third Party Responsibility IRC 6672, Personal Assessment Only assessable against responsible person. Responsible person must willfully fail to pay over trust fund taxes. Penalty is the full amount of trust fund portion of payroll tax liability Withheld income taxes Withheld Social Security taxes Withheld Medicare taxes Establishing Responsibility 20

21 Who s responsible? IRM : Responsibility is a matter of status, duty, and authority. A determination of responsibility is dependent on the facts and circumstances of each case. Examples: Officers Bookkeeper PEO Shareholder What responsible does Hires Fires Makes FTD Signs payroll checks Has certain officer duties Directs the actions of employees in these same matters 21

22 Delegation Generally, authority can be delegated, but not responsibility. Was the delegator removed from authority by the delegation? Establishing Willfullness 22

23 Was it on purpose? Was the failure to pay deliberate? Was the responsible person aware of the failure to pay? Failure to correct the failure proves willfulness Question: Were other bills paid instead? IRS Form 4180 Interview 23

24 TFRP Interview Personal interview required by IRM Over the phone, with representative present, is preferred. For 4180 NOT available online, RO not permitted to provide blank copy. Schedule the interview, with pre-completed Form 4180 in hand. Know your willful and/or responsible defense going in. Advise clients not to answer ANY questions about roles and responsibilities without you present if RO calls or shows up. Summons authority Never sign Form 2751 accepting assessment without a good reason. 24

25 25

26 26

27 Form 4180 Page 3: PSP/PEO interview Page 4: Additional info, RO comments, signatures Defenses Against Personal Assessment 27

28 Core Defense Clearly separate responsible from willful. Silo everything. Fighting Responsibility Don t play CFO Don t prepare 941 s Don t prepare payroll Don t be on the bank account as authorized check signer Don t be the name on EFTPS Don t have access to online banking 28

29 Fighting Willfullness Don t be the person paying the bills. Don t be the person deciding which bills to pay. Don t be in the loop on financial matters. Don t interact with the IRS. Conclusion Best course of action is to set up business structure in the most advantageous way from the get go. For most single member LLC s or single shareholder S corps, there is no defense. For other situations, dig to find somebody else to throw under the bus for the other component. Use the 1153/2751 as leverage. 60 day rule Form 2750, ASED Extension 29

30 2016 IRS Collections Representation Boot Camp Presented by: Dan Henn, CPA & Jassen Bowman, EA Sponsors: IRS Program Number: SDQJW-T I Sponsor ID # Putting It All Together Presented by Jassen Bowman, EA 30

31 The IRS Notice Cycle Assessment Letter 1058 Bill 1 CP-504 Bill 2 NTFL 31

32 32

Tax Pro Sales Cycle: 1) Lead Generation 2) Lead Nurturing 3) Consultation 4) Prospect follow up and client conversion 5) Case work 6) Cross sell to other")

33 Six Steps To Six Figures (and beyond!) Tax Pro Sales Cycle: 1) Lead Generation 2) Lead Nurturing 3) Consultation 4) Prospect follow up and client conversion 5) Case work 6) Cross sell to other services for years to come Key concept: The goal of each step is to get them to the next step! Lifetime Customer Value 33

$12,000 to $20,000 in new annual tax prep fees 4) In four years, that s")

34 Lifetime Customer Value Tax resolution is either a vehicle to other work, or IS the additional service you offer. Build your recurring tax prep practice. Easy way to add 10 to 50 new 1040 s per year for a solo practitioner (plus collect 10k- 200k doing it). One attorney client uses tax resolution as a lead generator for their international tax litigation practice. 941 cases: Perfect lead generator for monthly bookkeeping & payroll servicing.. What does this look like in practice? Four tax resolution cases per month brings you 1) $132,000+ in annual representation fees 2) $25,000 to $50,000 in unfiled return prep 3) $12,000 to $20,000 in new annual tax prep fees 4) In four years, that s nearly 200 recurring tax returns from just representation clients 5) plus their referrals 6) plus insurance, wealth management, bookkeeping, etc. 34

Marketing Assistant 3) Case Work Management Platform CanopyTax.")

Processes/Systems It s been a")

35 Tools 1) Sales/Marketing CRM Platform Contactually Nutshell/Insightly Tax-specific ATOM 2) Marketing Assistant 3) Case Work Management Platform CanopyTax.com 4) E-services + TDS Access 5) Transcript Analysis Software Audit Detective from Tax Help Software Canopy now includes this feature 6) Processes/Systems It s been a whirlwind three days 35

36 Discussion What s YOUR next step? 36

2016 IRS Collections Representation Boot Camp

2016 IRS Collections Representation Boot Camp Presented by: Dan Henn, CPA & Jassen Bowman, EA Sponsors: IRS Program Number: SDQJW-T-00040-16-I Sponsor ID #137128. Before We Get Started For proper CPE tracking,

2016 IRS Collections Representation Boot Camp Presented by: Dan Henn, CPA & Jassen Bowman, EA Sponsors: IRS Program Number: SDQJW-T-00040-16-I Sponsor ID #137128. Before We Get Started For proper CPE tracking,

Advanced Tax Resolution Seminar

Advanced Tax Resolution Seminar Presented by: Dan Henn, CPA & Jassen Bowman, EA Sponsored By: IRS Program Number: SDQJW-T-00043-16-I Sponsor ID #137128. Before We Get Started For proper CPE tracking, please

Advanced Tax Resolution Seminar Presented by: Dan Henn, CPA & Jassen Bowman, EA Sponsored By: IRS Program Number: SDQJW-T-00043-16-I Sponsor ID #137128. Before We Get Started For proper CPE tracking, please

Introduction to Collections: 9/6/2012. The Basics of the IRS Collections Process

David F. Miles, E.A. is a consultant with 20/20 Tax Resolution, Inc. with 15 years of tax resolution experience. David works nationally as a taxpayer representative focusing on state and IRS collections.

David F. Miles, E.A. is a consultant with 20/20 Tax Resolution, Inc. with 15 years of tax resolution experience. David works nationally as a taxpayer representative focusing on state and IRS collections.

First Time Abatement (of Penalties) Made Easy Failure To File Failure To Pay Failure To Deposit

Made Easy Failure To File Failure To Pay Failure To Deposit") First Time Abatement (of Penalties) Made Easy Failure To File Failure To Pay Failure To Deposit Presenter Roger Nemeth, EA & NTPI Fellow President & Developer Audit Detective, LLC Working Undercover Narcotics

First Time Abatement (of Penalties) Made Easy Failure To File Failure To Pay Failure To Deposit Presenter Roger Nemeth, EA & NTPI Fellow President & Developer Audit Detective, LLC Working Undercover Narcotics

Part 5. Collecting Process. Chapter 14. Installment Agreements. Section 1. Securing Installment Agreements Securing Installment Agreements

Part 5. Collecting Process Chapter 14. Installment Agreements Section 1. Securing Installment Agreements 5.14.1 Securing Installment Agreements 5.14.1.1 Overview 5.14.1.2 Installment Agreements and Taxpayer

Part 5. Collecting Process Chapter 14. Installment Agreements Section 1. Securing Installment Agreements 5.14.1 Securing Installment Agreements 5.14.1.1 Overview 5.14.1.2 Installment Agreements and Taxpayer

IRS COLLECTION PROCEDURES AND TAXPAYER REMEDIES

IRS COLLECTION PROCEDURES AND TAXPAYER REMEDIES By: Daniel J. Cramer Cramer, Minock & Sweeney, PLC The IRS has broad powers to enforce tax laws and collect outstanding taxes. The most common IRS collection

IRS COLLECTION PROCEDURES AND TAXPAYER REMEDIES By: Daniel J. Cramer Cramer, Minock & Sweeney, PLC The IRS has broad powers to enforce tax laws and collect outstanding taxes. The most common IRS collection

TRI Tax Resolution Institute. where your tax debt is your power! Busy Season. all year long

TRI Tax Resolution Institute where your tax debt is your power! Busy Season all year long Low Hanging Fruit How to make real money in the next 12 months Meet our speaker Peter Y. Stephan, CPA (800) 658-7590

TRI Tax Resolution Institute where your tax debt is your power! Busy Season all year long Low Hanging Fruit How to make real money in the next 12 months Meet our speaker Peter Y. Stephan, CPA (800) 658-7590

Intro to Collections

Intro to Collections The Basics of the IRS Collection Process David F. Miles, E.A. August 6, 2013 Lecture Introduction This is an introductory course of IRS collections. The course will cover the fundamentals

Intro to Collections The Basics of the IRS Collection Process David F. Miles, E.A. August 6, 2013 Lecture Introduction This is an introductory course of IRS collections. The course will cover the fundamentals

Collection Due Process Hearing

263 Collection Due Process (CDP) Statutory Right A gift from the IRS Restructuring and Reform Act of 1998 1. Lien IRC 6320 2. Levy IRC 6330 263 264 Critical Issues of CDP Use it or lose it 30 days to REQUEST

263 Collection Due Process (CDP) Statutory Right A gift from the IRS Restructuring and Reform Act of 1998 1. Lien IRC 6320 2. Levy IRC 6330 263 264 Critical Issues of CDP Use it or lose it 30 days to REQUEST

President IRS Solutions Author Loves Taxes Loves Teaching Former Revenue Officer.

DAVID STONE, E.A. President IRS Solutions Author Loves Taxes Loves Teaching Former Revenue Officer 2 In this Session We Will Learn: 1. What tools the IRS has to use 2. What tools are available to the accountant

DAVID STONE, E.A. President IRS Solutions Author Loves Taxes Loves Teaching Former Revenue Officer 2 In this Session We Will Learn: 1. What tools the IRS has to use 2. What tools are available to the accountant

Busy Season. all year long. TRI Tax Resolution Institute. where your tax debt is your power!

1 TRI Tax Resolution Institute where your tax debt is your power! Busy Season all year long www.taxresolutioninstitute.org info@taxresolutioninstitute.org (877) 829-8370 2 Appeals www.taxresolutioninstitute.org

1 TRI Tax Resolution Institute where your tax debt is your power! Busy Season all year long www.taxresolutioninstitute.org info@taxresolutioninstitute.org (877) 829-8370 2 Appeals www.taxresolutioninstitute.org

INTERNAL MANUAL -- PASSPORT CERTIFICATION PROCEDURES

INTERNAL MANUAL -- PASSPORT CERTIFICATION PROCEDURES (Excerpted from IRS Internal Manual. https://www.irs.gov/irm. Both sections below are substantially the same. The first applies to field collection

INTERNAL MANUAL -- PASSPORT CERTIFICATION PROCEDURES (Excerpted from IRS Internal Manual. https://www.irs.gov/irm. Both sections below are substantially the same. The first applies to field collection

Federal and State Employment Tax Issues

Federal and State Employment Tax Issues Seminar prepared for the Virginia Society of Enrolled Agents (September 2014) by The three most common problems 1. Not filing; 2. Not making timely deposits; and

Federal and State Employment Tax Issues Seminar prepared for the Virginia Society of Enrolled Agents (September 2014) by The three most common problems 1. Not filing; 2. Not making timely deposits; and

TRI Tax Resolution Institute. where your tax debt is your power! Busy Season. all year long

TRI Tax Resolution Institute where your tax debt is your power! Busy Season all year long Low Hanging Fruit How to make real money in the next 12 months Meet our speaker Peter Y. Stephan, CPA (800) 658-7590

TRI Tax Resolution Institute where your tax debt is your power! Busy Season all year long Low Hanging Fruit How to make real money in the next 12 months Meet our speaker Peter Y. Stephan, CPA (800) 658-7590

Busy Season. all year long. TRI Tax Resolution Institute. where your tax debt is your power!

1 TRI Tax Resolution Institute where your tax debt is your power! Busy Season all year long www.taxresolutioninstitute.org info@taxresolutioninstitute.org (877) 829-8370 2 Appeals www.taxresolutioninstitute.org

1 TRI Tax Resolution Institute where your tax debt is your power! Busy Season all year long www.taxresolutioninstitute.org info@taxresolutioninstitute.org (877) 829-8370 2 Appeals www.taxresolutioninstitute.org

Kevin Murphy, Esq. Andreozzi Bluestein LLP 9145 Main Street Clarence, NY PH# (716) , Fax# (716)

, Fax# (716)") Kevin Murphy, Esq. Andreozzi Bluestein LLP 9145 Main Street Clarence, NY 14031 PH# (716) 633-3200, Fax# (716) 633-0301 kmm@andreozzibluestein.com PART 1 BASIC TAX ISSUES IN BANKRUPTCY Tax Collection Defense

Kevin Murphy, Esq. Andreozzi Bluestein LLP 9145 Main Street Clarence, NY 14031 PH# (716) 633-3200, Fax# (716) 633-0301 kmm@andreozzibluestein.com PART 1 BASIC TAX ISSUES IN BANKRUPTCY Tax Collection Defense

IRS Wasn't Wrong to Reject Taxpayer Payment Plan that Didn't Pay Off Liability in Ten Years

IRS Wasn't Wrong to Reject Taxpayer Payment Plan that Didn't Pay Off Liability in Ten Years Brown, TC Memo 2016-82 The Tax Court has held that IRS was not wrong to reject, based on several failings by

IRS Wasn't Wrong to Reject Taxpayer Payment Plan that Didn't Pay Off Liability in Ten Years Brown, TC Memo 2016-82 The Tax Court has held that IRS was not wrong to reject, based on several failings by

Responding to Adverse IRS Audit Assessments: Audit Reconsideration Requests, IRS Appeals, and Settlement Strategies

Responding to Adverse IRS Audit Assessments: Audit Reconsideration Requests, IRS Appeals, and Settlement Strategies TUESDAY, MARCH 1, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved

Responding to Adverse IRS Audit Assessments: Audit Reconsideration Requests, IRS Appeals, and Settlement Strategies TUESDAY, MARCH 1, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved

Your client calls frantic one

The IRS Disqualified Employment Tax Levy Just When the Client Thought It Was Safe to Owe Money Again By Lauren M. McNair, Esq. and Eric L. Green, Esq., Green & Sklarz LLC Your client calls frantic one

The IRS Disqualified Employment Tax Levy Just When the Client Thought It Was Safe to Owe Money Again By Lauren M. McNair, Esq. and Eric L. Green, Esq., Green & Sklarz LLC Your client calls frantic one

The Audit is Over Now What?

Where Do We Go From Here: A Comparison of Alternatives When You and the IRS Agree to Disagree JENNY LOUISE JOHNSON, Holland & Knight LLP Co-Chair of Tax Controversy Practice CHARLES E. HODGES, Kilpatrick

Where Do We Go From Here: A Comparison of Alternatives When You and the IRS Agree to Disagree JENNY LOUISE JOHNSON, Holland & Knight LLP Co-Chair of Tax Controversy Practice CHARLES E. HODGES, Kilpatrick

ALI-ABA Course of Study How To Handle a Tax Controversy at the IRS and in Court: From Administrative Audit Through Litigation

149 ALI-ABA Course of Study How To Handle a Tax Controversy at the IRS and in Court: From Administrative Audit Through Litigation Sponsored with the cooperation of the ABA Section of Taxation May 28-29,

149 ALI-ABA Course of Study How To Handle a Tax Controversy at the IRS and in Court: From Administrative Audit Through Litigation Sponsored with the cooperation of the ABA Section of Taxation May 28-29,

Do a Paycheck Checkup

Do a Paycheck Checkup Alan Gregerson October 25, 2018 Why a Paycheck Checkup? Some law changes in the Tax Cuts and Jobs Act may affect your withholding. Protect against having too little tax withheld and

Do a Paycheck Checkup Alan Gregerson October 25, 2018 Why a Paycheck Checkup? Some law changes in the Tax Cuts and Jobs Act may affect your withholding. Protect against having too little tax withheld and

The Federal Payroll Tax Case (Focus on Trust-Fund Recovery Penalty)

") The Federal Payroll Tax Case (Focus on Trust-Fund Recovery Penalty) STEPHEN P. KAUFFMAN ESQ. SKEEN & KAUFFMAN 911 N. CHARLES ST. BALTIMORE, MD 21201 SKAUFFMAN@SKAUFFLAW.COM 443.478.3720 Payroll Tax Compliance

The Federal Payroll Tax Case (Focus on Trust-Fund Recovery Penalty) STEPHEN P. KAUFFMAN ESQ. SKEEN & KAUFFMAN 911 N. CHARLES ST. BALTIMORE, MD 21201 SKAUFFMAN@SKAUFFLAW.COM 443.478.3720 Payroll Tax Compliance

THE TRUST FUND RECOVERY PENALTY. Cincinnati Bar Report. Published April, By Howard S. Levy

THE TRUST FUND RECOVERY PENALTY Cincinnati Bar Report Published April, 2006 By Howard S. Levy To the IRS, not all taxes are necessarily created equal. The failure to pay over employee withholding taxes

THE TRUST FUND RECOVERY PENALTY Cincinnati Bar Report Published April, 2006 By Howard S. Levy To the IRS, not all taxes are necessarily created equal. The failure to pay over employee withholding taxes

Field Collection Operations Employment Tax Compliance Efforts & Current Collection Hot Topics

Field Collection Operations Employment Tax Compliance Efforts & Current Collection Hot Topics Regina Malisham IRS Stakeholder Liaison FY 2016 Field Collection Operations 2 FY 2016 Field Collection Operations

Field Collection Operations Employment Tax Compliance Efforts & Current Collection Hot Topics Regina Malisham IRS Stakeholder Liaison FY 2016 Field Collection Operations 2 FY 2016 Field Collection Operations

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS Route To: Partners PPC's Guide to Dealing with the IRS Managers. Twenty second Edition (June 2014)

") LIST OF SUBSTANTIVE CHANGES AND ADDITIONS Route To: Partners PPC's Guide to Dealing with the IRS Managers Staff File Twenty second Edition (June 2014) The following are some of the features of this year

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS Route To: Partners PPC's Guide to Dealing with the IRS Managers Staff File Twenty second Edition (June 2014) The following are some of the features of this year

Table of Contents. About This Book How To Use This Book Foreword Acknowledgments Preface

Table of Contents About This Book How To Use This Book Foreword Acknowledgments Preface vii ix xi xiii xv Chapter 1 Initial Client Engagement 1 Topical Index 1 1.01 Nature of Federal Tax Law 5 1.02 Role

Table of Contents About This Book How To Use This Book Foreword Acknowledgments Preface vii ix xi xiii xv Chapter 1 Initial Client Engagement 1 Topical Index 1 1.01 Nature of Federal Tax Law 5 1.02 Role

Trust Fund Recovery. A Tax Resolution Institute Publication 2016

A Tax Resolution Institute Publication 2016 Trust Fund Recovery Facing possible retributions such as civil liability for unpaid employment taxes, including penalties and interest, and possible criminal

A Tax Resolution Institute Publication 2016 Trust Fund Recovery Facing possible retributions such as civil liability for unpaid employment taxes, including penalties and interest, and possible criminal

Offer-in-Compromise Why or Why Not

Why or Why Not The Capital of Texas Enrolled Agents November 2010 by: lg brooks, ea Why or Why Not Table of Contents Introduction 3 The Offer Process 4 The Offer in Compromise: Offers in General 4 Grounds

Why or Why Not The Capital of Texas Enrolled Agents November 2010 by: lg brooks, ea Why or Why Not Table of Contents Introduction 3 The Offer Process 4 The Offer in Compromise: Offers in General 4 Grounds

DEPARTMENT OF THE TREASURY. July 18, Susan L. Latham /s/ Susan L. Latham Director, Policy, Quality and Case Support

DEPARTMENT OF THE TREASURY I N T E R N A L R E V E N U E S E R V I C E W A S H I N G T O N, D. C. 2 0 2 2 4 July 18, 2013 MEMORANDUM FOR APPEALS EMPLOYEES Control No. AP-08-0713-03 Expiration Date: 07/18/2014

DEPARTMENT OF THE TREASURY I N T E R N A L R E V E N U E S E R V I C E W A S H I N G T O N, D. C. 2 0 2 2 4 July 18, 2013 MEMORANDUM FOR APPEALS EMPLOYEES Control No. AP-08-0713-03 Expiration Date: 07/18/2014

ACCOUNTAX SCHOOL OF BUSINESS, INCORPORATED A Profile in Continuing Professional Education. Representing Clients During the Collections Process

ACCOUNTAX SCHOOL OF BUSINESS, INCORPORATED A Profile in Continuing Professional Education Representing Clients During the Collections Process A. Extension of time to pay (e.g., Form 1127-A) If a taxpayer

ACCOUNTAX SCHOOL OF BUSINESS, INCORPORATED A Profile in Continuing Professional Education Representing Clients During the Collections Process A. Extension of time to pay (e.g., Form 1127-A) If a taxpayer

STATUTE OF LIMITATIONS Analyze This. By LG Brooks Enrolled Agent

The capital of Texas enrolled agents Austin, Texas November 2008 STATUTE OF LIMITATIONS Analyze This By LG Brooks Enrolled Agent I. BIOGRAPHY LG Brooks, BA, EA LG Brooks is an Enrolled Agent and is the

The capital of Texas enrolled agents Austin, Texas November 2008 STATUTE OF LIMITATIONS Analyze This By LG Brooks Enrolled Agent I. BIOGRAPHY LG Brooks, BA, EA LG Brooks is an Enrolled Agent and is the

Notice of Deficiency Proposed increase in tax and notice of your right to challenge

AUR Notice Department of the Treasury Internal Revenue Service Notice AUR control number To contact us Last date to petition Tax Court Page 1 of 9 Notice of Deficiency Proposed increase in tax and notice

AUR Notice Department of the Treasury Internal Revenue Service Notice AUR control number To contact us Last date to petition Tax Court Page 1 of 9 Notice of Deficiency Proposed increase in tax and notice

IRS Provides Guidance on FBAR Penalties

Page 1 of 5 The Tax Adviser IRS Provides Guidance on FBAR Penalties Updated procedures on penalties imposed for failing to file the Report of Foreign Bank and Financial Accounts provide consistency and

Page 1 of 5 The Tax Adviser IRS Provides Guidance on FBAR Penalties Updated procedures on penalties imposed for failing to file the Report of Foreign Bank and Financial Accounts provide consistency and

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS. PPC s Guide to Dealing with the IRS. Twenty-third Edition (June 2015)

") Route To: j Partners j Managers j Staff j File P.O. Box 115008 Carrollton, TX 75011-5008 Tel (972) 250-7750 (800) 431-9025 Fax (888) 216-1929 tax.thomsonreuters.com LIST OF SUBSTANTIVE CHANGES AND ADDITIONS

Route To: j Partners j Managers j Staff j File P.O. Box 115008 Carrollton, TX 75011-5008 Tel (972) 250-7750 (800) 431-9025 Fax (888) 216-1929 tax.thomsonreuters.com LIST OF SUBSTANTIVE CHANGES AND ADDITIONS

Review Questions and Final Exam

Review Questions and Final Exam Course name: Ethics for Enrolled Agents-2010 Course number: 9001.10 Number of questions: Prerequisite: Course level: Recommended CPE credit: Recommended study time: Review

Review Questions and Final Exam Course name: Ethics for Enrolled Agents-2010 Course number: 9001.10 Number of questions: Prerequisite: Course level: Recommended CPE credit: Recommended study time: Review

Offer in Compromise. What you need to know...1. Paying for your offer...2. How to apply...3. Completing the application package...

Form 656 Booklet Offer in Compromise CONTENTS What you need to know...1 Paying for your offer...2 How to apply...3 Completing the application package...3 Important information...4 Removable Forms - Form

Form 656 Booklet Offer in Compromise CONTENTS What you need to know...1 Paying for your offer...2 How to apply...3 Completing the application package...3 Important information...4 Removable Forms - Form

Offer In Compromise Line Instructions Irs Forms

Offer In Compromise Line Instructions Irs Forms 433 Form 433-A, Collection Information Statement for Wage Earners and Standards for completing the Expense section of Forms 433-A and 433-F Online Payment

Offer In Compromise Line Instructions Irs Forms 433 Form 433-A, Collection Information Statement for Wage Earners and Standards for completing the Expense section of Forms 433-A and 433-F Online Payment

Proposed 10.4(c) provides the requirements to be designated as a registered return preparer.

provides the requirements to be designated as a registered return preparer.") SECTION: CIRCULAR 230 PROPOSED REVISIONS TO CIRCULAR 230 TO ESTABLISH REGISTERED RETURN PREPARERS, MANDATE FOR OVERSIGHT BY CHIEF TAX PRACTITIONER IN FIRM AND PENALTY FOR FAILING TO ELECTRONIC FILE MANDATED

SECTION: CIRCULAR 230 PROPOSED REVISIONS TO CIRCULAR 230 TO ESTABLISH REGISTERED RETURN PREPARERS, MANDATE FOR OVERSIGHT BY CHIEF TAX PRACTITIONER IN FIRM AND PENALTY FOR FAILING TO ELECTRONIC FILE MANDATED

Choosing Wisely: When to Use (or Not Use) Mediation to Obtain Cost Effective Closure in Exam & Collection Cases

Mediation to Obtain Cost Effective Closure in Exam & Collection Cases") Choosing Wisely: When to Use (or Not Use) Mediation to Obtain Cost Effective Closure in Exam & Collection Cases Maxine Aaronson Law Office of Maxine Aaronson 600 N. Pearl St. Suite 2170 Dallas, Texas 75201

Choosing Wisely: When to Use (or Not Use) Mediation to Obtain Cost Effective Closure in Exam & Collection Cases Maxine Aaronson Law Office of Maxine Aaronson 600 N. Pearl St. Suite 2170 Dallas, Texas 75201

MODULE 1. IRS Personnel & Access to Information

MODULE 1 IRS Personnel & Access to Information Module 1: IRS Personnel & Access to Information Created Exclusively for ASTPS Sponsored Seminars Rescue Squad: Troubled Taxpayers Lawrence M. Lawler Certified

MODULE 1 IRS Personnel & Access to Information Module 1: IRS Personnel & Access to Information Created Exclusively for ASTPS Sponsored Seminars Rescue Squad: Troubled Taxpayers Lawrence M. Lawler Certified

Gleim EA Review Updates to Part Edition, 1st Printing April 2016

Page 1 of 6 Gleim EA Review Updates to Part 3 2016 Edition, 1st Printing April 2016 NOTE: Text that should be deleted is displayed with a line through it. New text is shown with a blue background. This

Page 1 of 6 Gleim EA Review Updates to Part 3 2016 Edition, 1st Printing April 2016 NOTE: Text that should be deleted is displayed with a line through it. New text is shown with a blue background. This

IRS Policy Changes Impact R&D Credit IRS changes magnify the importance of methodology and documentation

IRS changes magnify the importance of methodology and documentation The new IDR enforcement policy and the Appeals Judicial Approach and Culture project have been in effect for over a year. Both policies

IRS changes magnify the importance of methodology and documentation The new IDR enforcement policy and the Appeals Judicial Approach and Culture project have been in effect for over a year. Both policies

HOW THE 1998 TAX ACT AFFECTS YOUR DEALINGS WITH THE IRS APPEALS OFFICE. The IRS Restructuring and Reform Act of 1998.

HOW THE 1998 TAX ACT AFFECTS YOUR DEALINGS WITH THE IRS APPEALS OFFICE The IRS Restructuring and Reform Act of 1998 January 22, 1999 Robert M. Kane, Jr. LeSourd & Patten, P.S. 600 University Street, Ste

HOW THE 1998 TAX ACT AFFECTS YOUR DEALINGS WITH THE IRS APPEALS OFFICE The IRS Restructuring and Reform Act of 1998 January 22, 1999 Robert M. Kane, Jr. LeSourd & Patten, P.S. 600 University Street, Ste

Your Peace of Mind Audit Protection Plan Also Includes Tax Identity Fraud Recovery

Frequently Asked Questions What happens when I receive an audit notice or letter? As soon as you receive a notice or audit letter from the IRS, give us a call immediately so we can start resolving the

Frequently Asked Questions What happens when I receive an audit notice or letter? As soon as you receive a notice or audit letter from the IRS, give us a call immediately so we can start resolving the

Darren John Guillot Director, Field Collection Operations Internal Revenue Service

Darren John Guillot Director, Field Collection Operations Internal Revenue Service Darren Guillot has program responsibility for Field Collection nationwide including International and ATAT revenue officers.

Darren John Guillot Director, Field Collection Operations Internal Revenue Service Darren Guillot has program responsibility for Field Collection nationwide including International and ATAT revenue officers.

44th Annual Chesapeake Tax Conference September 16th, IRS Audit Update

44th Annual Chesapeake Tax Conference September 16th, 2013 IRS Audit Update Stuart M. Schabes, Esquire Ober, Kaler, Grimes & Shriver smschabes@ober.com 410-347-7696 Overview IRS FY 2012 STATS Individuals

44th Annual Chesapeake Tax Conference September 16th, 2013 IRS Audit Update Stuart M. Schabes, Esquire Ober, Kaler, Grimes & Shriver smschabes@ober.com 410-347-7696 Overview IRS FY 2012 STATS Individuals

Changes in IRS Exam and Appeals Procedures (and their impact on R&D Tax Credits)

") Changes in IRS Exam and Appeals Procedures (and their impact on R&D Tax Credits) Hosted by Bryan Auernig, Director Presented by Peter Mehta, Managing Director Tax Credit Co. September 22, 2015 Introductions

Changes in IRS Exam and Appeals Procedures (and their impact on R&D Tax Credits) Hosted by Bryan Auernig, Director Presented by Peter Mehta, Managing Director Tax Credit Co. September 22, 2015 Introductions

Tax Issues in Foreclosure Cases

Tax Issues in Foreclosure Cases September 19, 2017 Christopher Fasano Staff Attorney Mobilization for Justice, Inc. cfasano@mfjlegal.org Contents of Presentation I. Income from the discharge of indebtedness

Tax Issues in Foreclosure Cases September 19, 2017 Christopher Fasano Staff Attorney Mobilization for Justice, Inc. cfasano@mfjlegal.org Contents of Presentation I. Income from the discharge of indebtedness

2018 Paychex Reference Guide for Accountants

2018 Paychex Reference Guide for Accountants Paychex Promise There are too many what if moments that can disrupt your clients business. The Paychex Promise helps assure that covering payroll will never

2018 Paychex Reference Guide for Accountants Paychex Promise There are too many what if moments that can disrupt your clients business. The Paychex Promise helps assure that covering payroll will never

How To Represent A Taxpayer Before The IRS Office Of Appeals

How To Represent A Taxpayer Before The IRS Office Of Appeals October 3, 2017 6:00 PM 9:00 PM RSVP: http://conta.cc/2iwivlv Bergen Community College Ciarco Learning Center 355 Main Street Room, 102/103

How To Represent A Taxpayer Before The IRS Office Of Appeals October 3, 2017 6:00 PM 9:00 PM RSVP: http://conta.cc/2iwivlv Bergen Community College Ciarco Learning Center 355 Main Street Room, 102/103

IRS Practice and Procedure as to the Collection of Payroll Taxes. Penalties and Interest

IRS Practice and Procedure as to the Collection of Payroll Taxes By: Kenneth B. Schwartz, Esq., CPA 500 North Broadway, Ste 124 Jericho, N.Y. 11754 Tel: 516-333-7020 www.schwartzattorney.com December 2,

IRS Practice and Procedure as to the Collection of Payroll Taxes By: Kenneth B. Schwartz, Esq., CPA 500 North Broadway, Ste 124 Jericho, N.Y. 11754 Tel: 516-333-7020 www.schwartzattorney.com December 2,

Welcome to TaxMama s Place Home of the

1 Welcome to TaxMama s Place Home of the 10 Steps to Resolving Collection Issues Table of Contents 2 Meet Your Instructors 1. Determine the Statute of Limitations 2. Gather Information 3. Evaluate your

1 Welcome to TaxMama s Place Home of the 10 Steps to Resolving Collection Issues Table of Contents 2 Meet Your Instructors 1. Determine the Statute of Limitations 2. Gather Information 3. Evaluate your

DEALING WITH THE IRS

2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 DEALING WITH THE IRS More individuals deal with the IRS than any other federal government agency.

2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 DEALING WITH THE IRS More individuals deal with the IRS than any other federal government agency.

ALI-ABA Course of Study How To Handle a Tax Controversy at the IRS and in Court: From Administrative Audit Through Litigation

191 ALI-ABA Course of Study How To Handle a Tax Controversy at the IRS and in Court: From Administrative Audit Through Litigation Sponsored with the cooperation of the ABA Section of Taxation June 24-25,

191 ALI-ABA Course of Study How To Handle a Tax Controversy at the IRS and in Court: From Administrative Audit Through Litigation Sponsored with the cooperation of the ABA Section of Taxation June 24-25,

C A R A S & S H U L M A N, P C C e r t i f i e d P u b l i c A c c o u n t a n t s B u s i n e s s A d v i s o r s

C A R A S & S H U L M A N, P C C e r t i f i e d P u b l i c A c c o u n t a n t s B u s i n e s s A d v i s o r s Dear Client: Subject: 2016 Tax Engagement Letter This letter is to confirm and specify

C A R A S & S H U L M A N, P C C e r t i f i e d P u b l i c A c c o u n t a n t s B u s i n e s s A d v i s o r s Dear Client: Subject: 2016 Tax Engagement Letter This letter is to confirm and specify

Field Collection Emphasis

Field Collection Emphasis and how it impacts the tax practitioner community Timothy S. Sherrill North Atlantic Area Director Field Collection June 2018 A presentation for the South Jersey Working Together

Field Collection Emphasis and how it impacts the tax practitioner community Timothy S. Sherrill North Atlantic Area Director Field Collection June 2018 A presentation for the South Jersey Working Together

The IRS Collection Process

IRS Mission: Provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all. What You Should

IRS Mission: Provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all. What You Should

Tenth Circuit Finds IRS Followed Procedures and Could Proceed with Levy Action. Cropper v. Comm., (CA 10 6/22/2016) 117 AFTR 2d

117 AFTR 2d") Tenth Circuit Finds IRS Followed Procedures and Could Proceed with Levy Action Cropper v. Comm., (CA 10 6/22/2016) 117 AFTR 2d 2016-794 The Court of Appeals for the Tenth Circuit concluded that because

Tenth Circuit Finds IRS Followed Procedures and Could Proceed with Levy Action Cropper v. Comm., (CA 10 6/22/2016) 117 AFTR 2d 2016-794 The Court of Appeals for the Tenth Circuit concluded that because

An Overview of Offers in Compromise. Course #6800/QAS6800 Course Material

An Overview of Offers in Compromise Course #6800/QAS6800 Course Material An Overview of Offers in Compromise (Course #6800/QAS6800) Table of Contents Page Chapter 1: Introduction to Settling with the IRS

An Overview of Offers in Compromise Course #6800/QAS6800 Course Material An Overview of Offers in Compromise (Course #6800/QAS6800) Table of Contents Page Chapter 1: Introduction to Settling with the IRS

AIRA 28 th Annual Bankruptcy & Restructuring Conference. Wednesday, June 6, 2012 San Francisco, CA

AIRA 28 th Annual Bankruptcy & Restructuring Conference Wednesday, June 6, 2012 San Francisco, CA TAX DISCHARGE Dennis Bean, CPA, CIRA Bean Hunt Harris & Company Certified Public Accountants Fresno, Ca.

AIRA 28 th Annual Bankruptcy & Restructuring Conference Wednesday, June 6, 2012 San Francisco, CA TAX DISCHARGE Dennis Bean, CPA, CIRA Bean Hunt Harris & Company Certified Public Accountants Fresno, Ca.

IRS Notices. September 24, Whitepaper on IRS Notices, with an emphasis on a CP2000. By Erin Koplitz, CPA

IRS Notices September 24, 2015 Whitepaper on IRS Notices, with an emphasis on a CP2000 By Erin Koplitz, CPA Table of Contents FAQs for a CP2000... 1 Responding to a Notice... 3 Read the Notice... 4 Identify

IRS Notices September 24, 2015 Whitepaper on IRS Notices, with an emphasis on a CP2000 By Erin Koplitz, CPA Table of Contents FAQs for a CP2000... 1 Responding to a Notice... 3 Read the Notice... 4 Identify

Message about your. If we don t hear from you. What you need to do immediately. Department of Treasury Internal Revenue Service

Department of Treasury Internal Revenue Service 2D BARCODE Social Security number To contact us Phone 1- Your Caller ID: Page 1 of 4 ADR barcode Message about your Form You didn t file a Form tax return

Department of Treasury Internal Revenue Service 2D BARCODE Social Security number To contact us Phone 1- Your Caller ID: Page 1 of 4 ADR barcode Message about your Form You didn t file a Form tax return

Representing the Innocent Spouse in Pre- and Post-Filing Tax Controversies

Representing the Innocent Spouse in Pre- and Post-Filing Tax Controversies Presented to CPA Academy Lawrence A. Sannicandro, Esq. 1 Overview I. Introduction II. Conflicts of Interest III. Overview of Innocent

Representing the Innocent Spouse in Pre- and Post-Filing Tax Controversies Presented to CPA Academy Lawrence A. Sannicandro, Esq. 1 Overview I. Introduction II. Conflicts of Interest III. Overview of Innocent

JOSEPH ALI Director, Technical Guidance Internal Revenue Service- Appeals Joe Ali is the Director for Appeals Technical Guidance.

JOSEPH ALI Director, Technical Guidance Internal Revenue Service- Appeals Joe Ali is the Director for Appeals Technical Guidance. In this position, he is responsible for managing, and directing the Area

JOSEPH ALI Director, Technical Guidance Internal Revenue Service- Appeals Joe Ali is the Director for Appeals Technical Guidance. In this position, he is responsible for managing, and directing the Area

Resolving Tax Controversies: An Overview For Counsel Association of Corporate Counsel, 2017 Back to School Symposium August 15, 2017

Resolving Tax Controversies: An Overview For Counsel Association of Corporate Counsel, 2017 Back to School Symposium August 15, 2017 Brent C. Gardner, Senior Tax Counsel, Director of Tax Controversy, Hewlett-Packard

Resolving Tax Controversies: An Overview For Counsel Association of Corporate Counsel, 2017 Back to School Symposium August 15, 2017 Brent C. Gardner, Senior Tax Counsel, Director of Tax Controversy, Hewlett-Packard

Understanding the IRS Notice Process

Understanding the IRS Notice Process 287 The current lame duck commissioner of the IRS has promised from the inception of his tenure to clean up the IRS notice process 1 Understanding the IRS Notice Process

Understanding the IRS Notice Process 287 The current lame duck commissioner of the IRS has promised from the inception of his tenure to clean up the IRS notice process 1 Understanding the IRS Notice Process

District Court Determines IRS Exceeded Regulatory Limit on FBAR Penalties

IRS Insights A closer look. In this issue: District Court Determines IRS Exceeded Regulatory Limit on FBAR Penalties... 1 Internal Revenue Service Issues Guidelines for IRS Chief Counsel on Supervisory

IRS Insights A closer look. In this issue: District Court Determines IRS Exceeded Regulatory Limit on FBAR Penalties... 1 Internal Revenue Service Issues Guidelines for IRS Chief Counsel on Supervisory

Fast Track and Appeals. David B. Blair David J. Fischer

Fast Track and Appeals David B. Blair David J. Fischer Appeals Judicial Approach and Culture (AJAC) Appeals will not engage in fact-finding Appeals will not consider new facts not presented to Exam Factual

Fast Track and Appeals David B. Blair David J. Fischer Appeals Judicial Approach and Culture (AJAC) Appeals will not engage in fact-finding Appeals will not consider new facts not presented to Exam Factual

TOP THINGS TO REMEMBER ABOUT THE TRUSTEE S OFFICE AND YOUR CHAPTER 13 CASE

TOP THINGS TO REMEMBER ABOUT THE TRUSTEE S OFFICE AND YOUR CHAPTER 13 CASE 1. Know your case number. 2. Make your payments. Send your payments in time for the payments to reach the Trustee s office by

TOP THINGS TO REMEMBER ABOUT THE TRUSTEE S OFFICE AND YOUR CHAPTER 13 CASE 1. Know your case number. 2. Make your payments. Send your payments in time for the payments to reach the Trustee s office by

1500 Pennsylvania Avenue, NW 1111 Constitution Avenue, NW Washington, DC Washington, DC 20224

The Honorable Steven T. Mnuchin Secretary of the Treasury Commissioner Department of the Treasury Internal Revenue Service 1500 Pennsylvania Avenue, NW 1111 Constitution Avenue, NW Washington, DC 20220

The Honorable Steven T. Mnuchin Secretary of the Treasury Commissioner Department of the Treasury Internal Revenue Service 1500 Pennsylvania Avenue, NW 1111 Constitution Avenue, NW Washington, DC 20220

Convention 2017 Session Descriptions

Convention 2017 Session Descriptions BONUS Session: IRS Statutes of Limitation Dates: ASED, RSED, & CSED - 2CE This class will cover the three primary IRS Statute of Limitation Dates including definitions,

Convention 2017 Session Descriptions BONUS Session: IRS Statutes of Limitation Dates: ASED, RSED, & CSED - 2CE This class will cover the three primary IRS Statute of Limitation Dates including definitions,

/ Maryland Volunteer Lawyers Visit for more info on upcoming training and clinics!

facebook.com/mvlsprobono / Maryland Volunteer Lawyers Service @MVLSProBono Visit www.mvlslaw.org/events for more info on upcoming training and clinics! Resources for MVLS Volunteers: Looking for Pro Bono

facebook.com/mvlsprobono / Maryland Volunteer Lawyers Service @MVLSProBono Visit www.mvlslaw.org/events for more info on upcoming training and clinics! Resources for MVLS Volunteers: Looking for Pro Bono

OPR Discipline What You Need To Know

OPR Discipline What You Need To Know Learning Objectives Rules Governing Authority to Practice OPR Referral and Complaint Process Common Circular 230 Violations and Considerations Statutory Authority 31

OPR Discipline What You Need To Know Learning Objectives Rules Governing Authority to Practice OPR Referral and Complaint Process Common Circular 230 Violations and Considerations Statutory Authority 31

TAX CONTROVERSY TOOLKIT

TAX CONTROVERSY TOOLKIT Toolkit for Handling a Pro Bono Tax Controversy Texas Young Lawyers Association 2014 Edition Disclaimer: This publication is intended to provide lawyers with current and accurate

TAX CONTROVERSY TOOLKIT Toolkit for Handling a Pro Bono Tax Controversy Texas Young Lawyers Association 2014 Edition Disclaimer: This publication is intended to provide lawyers with current and accurate

Tax Resolution Essentials

1 Tax Resolution Essentials Quality education and training materials created and presented by the Tax Resolution Institute for accounting and legal professionals 1 2 Tax Resolution Essentials Will work

1 Tax Resolution Essentials Quality education and training materials created and presented by the Tax Resolution Institute for accounting and legal professionals 1 2 Tax Resolution Essentials Will work

Defined Benefit Takeover Issues

Workshop 5 Defined Benefit Takeover Issues Lynn M. Young, MSPA, EA Pinnacle Plan Design, LLC Tucson, AZ Richard Kutikoff, MSPA, FSA, EA Pacific Benefit Services, Inc. Sherman Oaks, CA Defined Benefit Takeover

Workshop 5 Defined Benefit Takeover Issues Lynn M. Young, MSPA, EA Pinnacle Plan Design, LLC Tucson, AZ Richard Kutikoff, MSPA, FSA, EA Pacific Benefit Services, Inc. Sherman Oaks, CA Defined Benefit Takeover

Audits of Estate Tax Returns and Protecting the Fiduciary Client. Presented to the Estate and Financial Planning Council of Central New Jersey

Audits of Estate Tax Returns and Protecting the Fiduciary Client Presented to the Estate and Financial Planning Council of Central New Jersey Frank Agostino, Esq. Lawrence A. Sannicandro, Esq. April 20,

Audits of Estate Tax Returns and Protecting the Fiduciary Client Presented to the Estate and Financial Planning Council of Central New Jersey Frank Agostino, Esq. Lawrence A. Sannicandro, Esq. April 20,

DEALING WITH THE IRS

DEALING WITH THE IRS 2 3 DEALING WITH THE IRS More individuals deal with the IRS than any other federal government agency. The IRS processes more than 100 million individual income tax returns every year.

DEALING WITH THE IRS 2 3 DEALING WITH THE IRS More individuals deal with the IRS than any other federal government agency. The IRS processes more than 100 million individual income tax returns every year.

Notice of intent to levy Intent to terminate your installment agreement

Department of the Treasury Internal Revenue Service Austin, TX 73301-0030 JAMES & KAREN Q. HINDS 22 BOULDER STREET HANSON, CT 00000-7253 Tax period 2016 To contact us 800-xxx-xxxx Your caller ID NNNN Page

Department of the Treasury Internal Revenue Service Austin, TX 73301-0030 JAMES & KAREN Q. HINDS 22 BOULDER STREET HANSON, CT 00000-7253 Tax period 2016 To contact us 800-xxx-xxxx Your caller ID NNNN Page

Portney & Company Certified Public Accountants & Business Consultants Portney Consulting, LLC Portney Management Group, LLC

Portney & Company Certified Public Accountants & Business Consultants Portney Consulting, LLC Portney Management Group, LLC 70 Grand Avenue, River Edge, New Jersey 07661 www.portney.com ~ Info@portney.com

Portney & Company Certified Public Accountants & Business Consultants Portney Consulting, LLC Portney Management Group, LLC 70 Grand Avenue, River Edge, New Jersey 07661 www.portney.com ~ Info@portney.com

The Hidden Costs of Paper-Based Payments. How Electronic Payments Save You Time, Cut Your Costs and Improve Your Customer Relationships

The Hidden Costs of Paper-Based Payments How Electronic Payments Save You Time, Cut Your Costs and Improve Your Customer Relationships The Hidden Costs of a Simple Check B2B payment methods are slow and

The Hidden Costs of Paper-Based Payments How Electronic Payments Save You Time, Cut Your Costs and Improve Your Customer Relationships The Hidden Costs of a Simple Check B2B payment methods are slow and

Year-end Tax Planning Letter

December 2011 Year-end Tax Planning Letter To Our Clients and Friends: As we approach year end, it s again time to focus on last-minute tax planning changes that you might want to consider to benefit you

December 2011 Year-end Tax Planning Letter To Our Clients and Friends: As we approach year end, it s again time to focus on last-minute tax planning changes that you might want to consider to benefit you

IRS FORM (4180 interview form) This document is being presented by: The Tax Resolution Institute, Inc.

This document is being presented by: The Tax Resolution Institute, Inc.") (877) 829-8370 www.taxresolutioninstitute.org IRS FORM 4180 (4180 interview form) This document is being presented by: The Tax Resolution Institute, Inc. Form 4180 (August 2012) Section I - Person Interviewed

(877) 829-8370 www.taxresolutioninstitute.org IRS FORM 4180 (4180 interview form) This document is being presented by: The Tax Resolution Institute, Inc. Form 4180 (August 2012) Section I - Person Interviewed

WRITTEN STATEMENT OF CHASTITY K. WILSON ON BEHALF OF THE THE AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS BEFORE

WRITTEN STATEMENT OF CHASTITY K. WILSON ON BEHALF OF THE THE AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS BEFORE THE UNITED STATES HOUSE OF REPRESENTATIVES COMMITTEE ON WAYS AND MEANS SUBCOMMITTEE

WRITTEN STATEMENT OF CHASTITY K. WILSON ON BEHALF OF THE THE AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS BEFORE THE UNITED STATES HOUSE OF REPRESENTATIVES COMMITTEE ON WAYS AND MEANS SUBCOMMITTEE

What s News in Tax Analysis That Matters from Washington National Tax

What s News in Tax Analysis That Matters from Washington National Tax LB&I Updates Publication 5125 and the Internal Revenue Manual In February 2016, the IRS revised Publication 5125, which provides guidance

What s News in Tax Analysis That Matters from Washington National Tax LB&I Updates Publication 5125 and the Internal Revenue Manual In February 2016, the IRS revised Publication 5125, which provides guidance

Welcome to TaxMama s Place Home of the. After SUCCESSFUL Collections or Audits What Next? 08/15/11

1 Welcome to TaxMama s Place Home of the After SUCCESSFUL Collections or Audits What Next? 2 Table of Contents Meet Your Instructors The end of the audit Closing letters how to read them, and ensuring

1 Welcome to TaxMama s Place Home of the After SUCCESSFUL Collections or Audits What Next? 2 Table of Contents Meet Your Instructors The end of the audit Closing letters how to read them, and ensuring

Review Questions and Final Exam

Review Questions and Final Exam Course name: Course number: 920215 Number of questions: Prerequisite: Review Final exam None 10 10 Course level: Recommended CPE credit: Recommended study time: Course format:

Review Questions and Final Exam Course name: Course number: 920215 Number of questions: Prerequisite: Review Final exam None 10 10 Course level: Recommended CPE credit: Recommended study time: Course format:

A Guide to Tax Resolution: Solving IRS Problems

A Guide to Tax Resolution: Solving IRS Problems 0 A Guide to Tax Resolution: Solving IRS Problems Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form

A Guide to Tax Resolution: Solving IRS Problems 0 A Guide to Tax Resolution: Solving IRS Problems Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form

TAX PRACTICE FINAL COPYRIGHT 2017 LGUTEF. Learning Objectives. Introduction

TAX PRACTICE 14 Issue 1: Substitute for Returns and Superseding Returns.. 506 Issue 2: Nonfilers........... 509 Issue 3: Collection Statute of Limitations.............. 513 Issue 4: Transferees, Nominees,

TAX PRACTICE 14 Issue 1: Substitute for Returns and Superseding Returns.. 506 Issue 2: Nonfilers........... 509 Issue 3: Collection Statute of Limitations.............. 513 Issue 4: Transferees, Nominees,

IRS Errors Get Taxpayer Partial Abatement of Late Payment Interest

IRS Errors Get Taxpayer Partial Abatement of Late Payment Interest King, TC Memo 2015-36 Where a taxpayer was unable to pay his employment tax liabilities on time and asked for an installment payment agreement,

IRS Errors Get Taxpayer Partial Abatement of Late Payment Interest King, TC Memo 2015-36 Where a taxpayer was unable to pay his employment tax liabilities on time and asked for an installment payment agreement,

Before we get to specific suggestions, here are two important considerations to keep in mind.

November 1, 2017 To Our Clients and Friends: As we get closer to the end of yet another year, it s time to tie up the loose ends and implement tax saving strategies. This has been an interesting year in

November 1, 2017 To Our Clients and Friends: As we get closer to the end of yet another year, it s time to tie up the loose ends and implement tax saving strategies. This has been an interesting year in

Page 1 of 8 Part 7. Rulings and Agreements Chapter 2. TE/GE Closing Agreements Section 3. Tax Exempt Bonds Voluntary Closing Agreement Program 7.2.3 Tax Exempt Bonds

Page 1 of 8 Part 7. Rulings and Agreements Chapter 2. TE/GE Closing Agreements Section 3. Tax Exempt Bonds Voluntary Closing Agreement Program 7.2.3 Tax Exempt Bonds

You must file your 2012 tax return

ADR Department of the Treasury Internal Revenue Service PO BOX 149338 Austin TX 78714-9338 Notice 2566 Tax Year 2012 Social Security number 999-99-9999 To contact us Phone 1-866-681-4271 Hours of operation

ADR Department of the Treasury Internal Revenue Service PO BOX 149338 Austin TX 78714-9338 Notice 2566 Tax Year 2012 Social Security number 999-99-9999 To contact us Phone 1-866-681-4271 Hours of operation

Disputing an assessment

IR776 June 2018 Disputing an assessment What to do if you dispute an assessment 2 DISPUTING AN ASSESSMENT Introduction While we make every effort to apply the tax laws fairly and correctly, there may be

IR776 June 2018 Disputing an assessment What to do if you dispute an assessment 2 DISPUTING AN ASSESSMENT Introduction While we make every effort to apply the tax laws fairly and correctly, there may be

UNEMPLOYMENT COMPENSATION

UNEMPLOYMENT COMPENSATION Unemployment compensation is a state program to help workers who are unemployed through no fault of their own. It is run by the Virginia Employment Commission (VEC). How do I

UNEMPLOYMENT COMPENSATION Unemployment compensation is a state program to help workers who are unemployed through no fault of their own. It is run by the Virginia Employment Commission (VEC). How do I

Office of Chief Counsel

Department of the Treasury Internal Revenue Service 1 Office of Chief Counsel Notice CC-2005-009 May 19, 2005 Subject: Change in Pre-Review Requirements for Suit Letters Requesting Judicial Approval of

Department of the Treasury Internal Revenue Service 1 Office of Chief Counsel Notice CC-2005-009 May 19, 2005 Subject: Change in Pre-Review Requirements for Suit Letters Requesting Judicial Approval of

New Developments in How to Win Benefits. New Court Cases

New Developments in How to Win Benefits New Court Cases Savage v. Shinseki, Vet. App. No. 09-4406 Duty to seek clarification of a private medical report What happened? Veteran sought higher rating for

New Developments in How to Win Benefits New Court Cases Savage v. Shinseki, Vet. App. No. 09-4406 Duty to seek clarification of a private medical report What happened? Veteran sought higher rating for

IRS Update: What s Happening Now

2 nd Annual CFMA Southwest Regional Conference San Diego, CA September 25-27, 2016 IRS Update: What s Happening Now Presented by: Kathy Petronchak KATHY PETRONCHAK Former IRS Commissioner of Small Business/Self

2 nd Annual CFMA Southwest Regional Conference San Diego, CA September 25-27, 2016 IRS Update: What s Happening Now Presented by: Kathy Petronchak KATHY PETRONCHAK Former IRS Commissioner of Small Business/Self

Registration Disclosure

Registration Disclosure ONLINE BANKING ACCOUNT ACCESS AGREEMENT AND DISCLOSURE STATEMENT Vibrant Credit Union This Agreement establishes the rules that cover your electronic access to your account(s) at

Registration Disclosure ONLINE BANKING ACCOUNT ACCESS AGREEMENT AND DISCLOSURE STATEMENT Vibrant Credit Union This Agreement establishes the rules that cover your electronic access to your account(s) at