Resolving Tax Controversies: An Overview For Counsel Association of Corporate Counsel, 2017 Back to School Symposium August 15, 2017

|

|

|

- Sherman Fisher

- 6 years ago

- Views:

Transcription

1 Resolving Tax Controversies: An Overview For Counsel Association of Corporate Counsel, 2017 Back to School Symposium August 15, 2017 Brent C. Gardner, Senior Tax Counsel, Director of Tax Controversy, Hewlett-Packard Company Robert C. Morris, Partner, Norton Rose Fulbright

2 An Overview of the U.S. Tax Controversy Process IRS Examination Conducted by Revenue Agents IRS Examination function divided into four operating divisions responsible for different groups of taxpayers Wage & Investment, Small Business & Self-Employed, Large Business and International (LB&I), and Tax Exempt and Government Entities Statute of Limitations Generally the statute of limitations for the IRS to assess tax expires three years from the due date of the return or the date on which it was filed, whichever is later 2

3 An Overview of the U.S. Tax Controversy Process (cont d) Revenue Agent Report / 30-Day Letter Prepared and issued at the conclusion of the examination Details whether tax return will be accepted as filed or proposes adjustments Taxpayer may protest proposed adjustments to IRS Office of Appeals IRS Office of Appeals Independent organization within the IRS whose mission is to resolve tax disagreements Considers protests, holds conferences, and negotiates settlements Litigation United States Tax Court, United States District Court, United States Court of Federal Claims 3

4 IRS Examination: What is the IRS Asking for? 1. Board meeting minutes, W-2s for all officers and directors, audit committee minutes, and compensation committee meetings 2. Interview notes, internal communications, and requests to third parties 3. Draft opinions, final opinions, transfer pricing reports, and invoices from advisors 4. Intercompany agreements and customer agreements 5. Organizational charts and employee compensation/performance information 6. Site visits and court-reporter recorded interviews 7. Taxpayer to create documents 8. Written acknowledgement of Exam Team facts 9. Response to penalty IDR 4

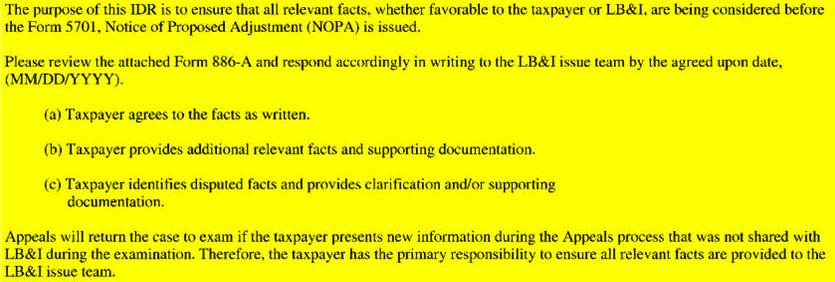

5 Written Acknowledgement of Facts (Publication 5125) LB&I issue team members are responsible for documenting all the facts that they have secured so that they can accurately apply the law. For potentially unagreed issues, the issue team members are For expected potentially to seek unagreed the taxpayer s issues, acknowledgment the issue on the team facts, resolve members any factual are differences expected and/or to document factual disputes. The issue manager should ensure that all relevant facts, including seek additional the taxpayer s and/or disputed acknowledgment facts, are appropriately on considered the facts, before resolve a Notice of any Proposed factual Adjustment differences is issued. If a and/or case is closed document to Appeals factual and the disputes. taxpayer provides relevant new information that requires investigation or additional analysis, the case will be returned to exam s jurisdiction for consideration. Before an unagreed issue is sent to Appeals, the issue team will solicit a ( ) Written Acknowledgment of the Facts (AOF) written acknowledgment of the facts to ensure all relevant facts 1. LB&I requires that all information, including all relevant facts and supporting documentation, be submitted to LB&I for consideration in the development of an issue. The taxpayer has primary responsibility for ensuring the facts have been fully provided to LB&I, so that the law is applied to the full set of facts. The taxpayer must be reminded that the case will be returned to exam's jurisdiction for consideration or examination if new information is provided by the taxpayer after a case is closed to Appeals. 3. Before an unagreed issue is sent to Appeals, the issue team will solicit a written acknowledgment of the facts to ensure all relevant facts, including those favorable to the taxpayer, are fully developed. This process will allow the issue team to address any additional or disputed facts identified by the taxpayer before the case is sent to Appeals. 5. The taxpayer must be reminded that the case will be returned to exam's jurisdiction for consideration or examination if new information is provided by the taxpayer after a case is closed to Appeals. 5

6 Sample Acknowledgement of Facts IDR from IRM 6

7 Missions IRS The IRS mission is to "provide America's taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all." APPEALS Resolve tax controversies, without litigation, on a basis which is fair and impartial to both the government and the taxpayer and in a manner that will enhance voluntary compliance and public confidence in the integrity and efficiency of the Internal Revenue Service. 7

8 IRS Appeals Statistical Snapshot FY 2012 FY 2013 FY 2014* FY 2015 Total Staffing 1,981 1,829 1,708 1,569 Total Receipts 135, , , ,870 Receipts Mix % Collection 55% 54% 53% 55% % Exam 45% 46% 47% 45% Total Closures 144, , , ,673 8

9 Early Referral to IRS Appeals Rev. Proc Developed, unagreed issues are transferred to IRS Appeals while the audit continues on other issues Benefits include consideration of issues without hot interest Appropriate when: The issue is not expected to be resolved at exam level The issue has been fully developed at exam level Resolution of the issue at appeals would result in resolution of the entire case The remaining issues under exam are not expected to be completed before IRS Appeals can resolve the early referral issue 9

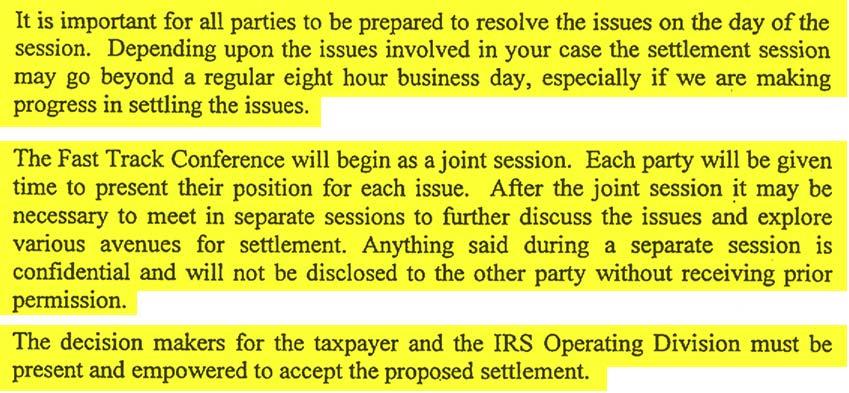

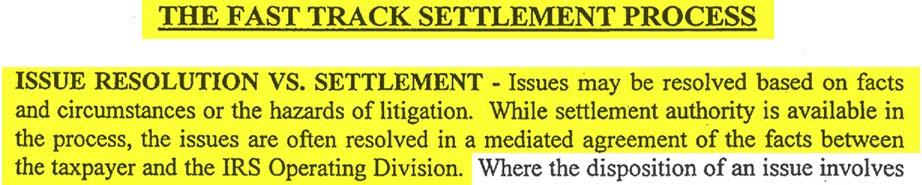

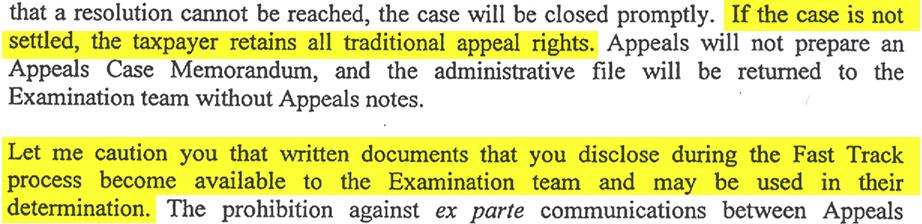

10 Fast Track Settlement Program Must now be considered by exam team Post issuance of notice of proposed adjustment, but before revenue agent report / 30-Day Letter Increase issue resolution at lowest level Case remains in exam s jurisdiction, but use IRS Appeals tools Goal is to complete within 120 days Taxpayer retains option to go to IRS Appeals Taxpayer, exam team, and IRS Appeals must agree to participate and agree to a mutual resolution Decision makers must be present at conference No prohibition on ex parte communications 10

11 Fast Track Settlement Opening Letter 11

12 Fast Track Settlement Attachment 12

13 Traditional IRS Appeals Protest is due 30 days after Revenue Agent Report is issued Exam team has discretion to grant extensions under reasonable circumstances Exam team s stingy practice on granting extensions Partial and skeletal protests may be rejected IRM Critical to prepare protest in advance of receiving Revenue Agent Report Exam team rebuttal 13

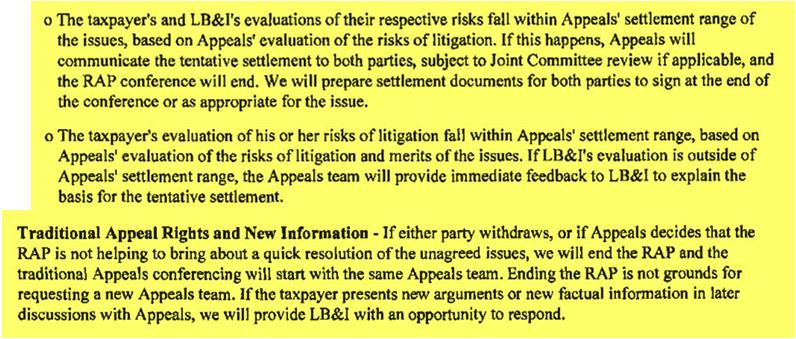

14 Rapid Appeals Process (RAP) (IRM ) Purpose Expedite the case in IRS Appeals Overview Uses mediation techniques to convert appeals preconference into working meeting for IRS Appeals, exam team, and taxpayer. IRS Appeals is responsible for independently evaluating the hazards of litigation. IRS Appeals is the sole decision maker for all disputed issues for IRS. Participation is voluntary. Traditional IRS Appeals process used if either party objects. Either party may withdraw at any time. Goals One conference to settle. Use best practices from Fast Track to resolve issues more quickly. Improve customer satisfaction. 14

15 Rapid Appeals Process Attachment 15

16 Rapid Appeals Process Attachment (cont d) 16

17 Post-Appeals Mediation (PAM) Rev. Proc , and Non-binding process used after settlement negotiations are unsuccessful An IRS Appeals Officer trained as a mediator (and if the taxpayer elects, a non-irs mediator) facilitates communications between the IRS and the taxpayer in order for the parties to reach their own negotiated settlement 17

18 Post-Appeals Mediation (PAM) PAM available at Taxpayer s request if settlement negotiations fail to resolve issue Current IRS Appeals practice is to acquiesce to Taxpayer s PAM request Selection of Mediators Current Selection Practice Taxpayer proposes 2-3 Appeals Officer mediators Taxpayer proposes 1-2 Independent Mediators IRS Appeals concurs or vetoes proposed candidates 18

19 Post-Appeals Mediation (PAM) Requires short written position paper (e.g., 20 pages) by each party Party s discretion to submit RAR, Protest Brief, etc. Mediators generally request parties last settlement offers 1-2 day mediation conference consisting of joint and separate sessions with mediators No prohibition on ex parte communications 19

20 Post-Appeals Mediation (PAM) Why undertake PAM? Mediators may bridge gap between parties last offers Means of correcting hazards assessment by inexperienced Appeals Officer Quick procedure: last chance to settle before litigation As next stop is courthouse, why not? 20

21 Duty to Preserve Documents The duty arises when the party has notice that the evidence is relevant to the litigation or when a The party duty should arises have when known the that party the evidence has notice may that be relevant the evidence to future is litigation. relevant Zubulake to litigation v. UBS or when Warburg a party LLC, should 220 F.R.D. have 212 known (S.D.N.Y. that 2003) the evidence (citing Fujitsu may Ltd. be v. relevant Fed. Exp. to Corp., future 247 F.3d litigation. 423, 436 (2d Cir. 2001) Failure to preserve may result in sanctions 21

22 Duty to Preserve Documents? Document production during the IRS's appeals process may be conducted in anticipation of litigation considering the size of the company and the business significance of the transaction. Deseret Management Corp. v. United States, 76 Fed. Cl. 88 (2007). For purposes of work product protection, litigation has been understood to include proceedings before administrative tribunals. Evergreen Trading, LLC. v. United States, 80 Fed. Cl. 122 (Fed. Cl. 2007). 22

23 Duty to Preserve Documents? [N]ot all audits by the IRS, or even extensive, IRS administrative proceedings to challenge results of those audits necessarily will lead to litigation. Although there is a point in time during interaction with the IRS that it is reasonable to conclude that litigation is likely or should be anticipated, that determination will differ in every case the courts are split among several circuits regarding when a party involved in the IRS administrative process should be deemed to anticipate litigation Consolidated Edison Co. v. United States, 90 Fed. Cl. 228 (2009). 23

24 Option B Choice of Forum United States Tax Court United States District Court United States Court of Federal Claims 24

25 2014 Tax Litigation Statistics 31,244 of 31,459 of tax litigation cases received by IRS Chief Counsel Attorneys were filed in Tax Court Approximately 2.5% to 5% of cases filed have resulted in a trial History shows that only 781-1,573 of the 31,459 cases filed in 2014 will result in a trial 25

26 Tax Court Docketed Cases, Rev. Proc Taxpayer files a petition in Tax Court in response to a statutory notice of deficiency After case is docketed, referred to IRS Appeals for settlement consideration. Certain exceptions apply: If IRS Appeals issued the notice or taxpayer foregoes settlement consideration by IRS Appeals generally not returned Cases designated for litigation or Division Counsel (or higher) determines referral not in interest of sound tax administration Appeals has sole authority to resolve 26

27 Designating a Case for Litigation 1. Certain cases present recurring, significant legal issues affecting large numbers of taxpayers. When there is a Certain cases present recurring, significant legal critical need for enforcement activity with respect to such issues issues, affecting cases are large designated numbers for litigation of taxpayers. in the interest of sound tax administration to establish judicial precedent, conserve resources, or reduce litigation costs for the For Service example, and taxpayers. judicial precedent For example, may judicial provide precedent guidance may provide for the guidance resolution for the of resolution industry-wide, of industry-wide, tax shelter tax shelter or other or other issues issues, thereby serving early issue resolution and conserving Service and taxpayer resources. IRM ( ) 27

28 Designating a Case for Litigation (cont d) the designated issue in a case will not be resolved 2. When under the jurisdiction of the Service, the designated issue in a case will not be resolved without a full concession by the taxpayer. without a full concession by the taxpayer. 3. In general, an issue will be designated when the case is under the jurisdiction of an Operating Division. If an issue in a case is designated, the taxpayer will not receive a 30-day letter with respect to remaining unresolved issues in the case. Rather, the taxpayer will be issued a If an statutory issue notice in of a deficiency. case is In designated, general, the designation the taxpayer of an issue will in a case will not preclude the settlement of the remaining issues after the not case receive is docketed. a 30-day Nor, in general, letter will with designation respect preclude to remaining Appeals from settling the same issue in other cases within its jurisdiction. As part of the unresolved designation process, issues Counsel in the will case. consider Rather, whether the the issue taxpayer is one of first impression or otherwise involves unique or unusual circumstances. If the will Chief be Counsel issued believes a statutory circumstances notice surrounding of deficiency. the designated In issue are such that settlement of the issue in other cases would be detrimental general, to the principles the designation of sound tax administration, of an issue the Chief in a Counsel case will confer with the Chief, Appeals. The Chief Counsel and the Chief, Appeals, will not also preclude confer as to the impact settlement of the settlement of the of remaining an issue on future issues settlements and a course of action with respect to the settlement of the issue that reflects the best interests of tax administration. after the case is docketed. 28

29

30 Disclaimer Norton Rose Fulbright US LLP, Norton Rose Fulbright LLP, Norton Rose Fulbright Australia, Norton Rose Fulbright Canada LLP and Norton Rose Fulbright South Africa Inc are separate legal entities and all of them are members of Norton Rose Fulbright Verein, a Swiss verein. Norton Rose Fulbright Verein helps coordinate the activities of the members but does not itself provide legal services to clients. References to Norton Rose Fulbright, the law firm and legal practice are to one or more of the Norton Rose Fulbright members or to one of their respective affiliates (together Norton Rose Fulbright entity/entities ). No individual who is a member, partner, shareholder, director, employee or consultant of, in or to any Norton Rose Fulbright entity (whether or not such individual is described as a partner ) accepts or assumes responsibility, or has any liability, to any person in respect of this communication. Any reference to a partner or director is to a member, employee or consultant with equivalent standing and qualifications of the relevant Norton Rose Fulbright entity. The purpose of this communication is to provide general information of a legal nature. It does not contain a full analysis of the law nor does it constitute an opinion of any Norton Rose Fulbright entity on the points of law discussed. You must take specific legal advice on any particular matter which concerns you. If you require any advice or further information, please speak to your usual contact at Norton Rose Fulbright.

Working with the IRS Office of Appeals What to Expect in Examination Appeals

Working with the IRS Office of Appeals What to Expect in Examination Appeals Glenn Gizzi Fall 2017 The Office of Appeals Established in 1927 Informal administrative forum Settle tax disputes without trial

Working with the IRS Office of Appeals What to Expect in Examination Appeals Glenn Gizzi Fall 2017 The Office of Appeals Established in 1927 Informal administrative forum Settle tax disputes without trial

McGladrey Tax Controversy Series Hot Topics in Tax Controversy Resolving Issues. January 26, 2012

McGladrey Tax Controversy Series Hot Topics in Tax Controversy Resolving Issues January 26, 2012 Agenda Topic Mins Introduction 5 Pre-Return Opportunities 15 Examination Opportunities 15 Appeals Opportunities

McGladrey Tax Controversy Series Hot Topics in Tax Controversy Resolving Issues January 26, 2012 Agenda Topic Mins Introduction 5 Pre-Return Opportunities 15 Examination Opportunities 15 Appeals Opportunities

Working with the IRS Office of Appeals

Working with the IRS Office of Appeals Tom Vangen, Appeals Team Manager, Joe Haynes, Appeals Team Manager Patrick McGuire, Area Director January 2018 TOPICS FOR TODAY: Overview of Examination Appeals The

Working with the IRS Office of Appeals Tom Vangen, Appeals Team Manager, Joe Haynes, Appeals Team Manager Patrick McGuire, Area Director January 2018 TOPICS FOR TODAY: Overview of Examination Appeals The

The Audit is Over Now What?

Where Do We Go From Here: A Comparison of Alternatives When You and the IRS Agree to Disagree JENNY LOUISE JOHNSON, Holland & Knight LLP Co-Chair of Tax Controversy Practice CHARLES E. HODGES, Kilpatrick

Where Do We Go From Here: A Comparison of Alternatives When You and the IRS Agree to Disagree JENNY LOUISE JOHNSON, Holland & Knight LLP Co-Chair of Tax Controversy Practice CHARLES E. HODGES, Kilpatrick

IRS Appeals New Faces, New Challenges

TEI s 68 th Midyear Conference IRS Appeals New Faces, New Challenges Brian Kaufman, Capital One Financial Corporation (moderator) Patti Burquest, RSM US LLP Alex Sadler, Morgan, Lewis & Bockius LLP Susan

TEI s 68 th Midyear Conference IRS Appeals New Faces, New Challenges Brian Kaufman, Capital One Financial Corporation (moderator) Patti Burquest, RSM US LLP Alex Sadler, Morgan, Lewis & Bockius LLP Susan

Fast Track and Appeals. David B. Blair David J. Fischer

Fast Track and Appeals David B. Blair David J. Fischer Appeals Judicial Approach and Culture (AJAC) Appeals will not engage in fact-finding Appeals will not consider new facts not presented to Exam Factual

Fast Track and Appeals David B. Blair David J. Fischer Appeals Judicial Approach and Culture (AJAC) Appeals will not engage in fact-finding Appeals will not consider new facts not presented to Exam Factual

What s News in Tax Analysis That Matters from Washington National Tax

What s News in Tax Analysis That Matters from Washington National Tax LB&I Updates Publication 5125 and the Internal Revenue Manual In February 2016, the IRS revised Publication 5125, which provides guidance

What s News in Tax Analysis That Matters from Washington National Tax LB&I Updates Publication 5125 and the Internal Revenue Manual In February 2016, the IRS revised Publication 5125, which provides guidance

Sheldon M. Kay Troy L. Olsen February 20, Current Update on IRS Appeals Division and Other Acronyms, Including AJAC, RAP, ADR and NII

Sheldon M. Kay Troy L. Olsen February 20, 2014 Current Update on IRS Appeals Division and Other Acronyms, Including AJAC, RAP, ADR and NII Polling Question How many times have you been before Appeals?

Sheldon M. Kay Troy L. Olsen February 20, 2014 Current Update on IRS Appeals Division and Other Acronyms, Including AJAC, RAP, ADR and NII Polling Question How many times have you been before Appeals?

Part 4. Examining Process. Chapter 46. LB&I Examination Process. Section 5. Resolving the Examination Resolving the Examination

Part 4. Examining Process Chapter 46. LB&I Examination Process Section 5. Resolving the Examination 4.46.5 Resolving the Examination 4.46.5.1 Overview 4.46.5.2 Issue Resolution 4.46.5.3 Resolution vs.

Part 4. Examining Process Chapter 46. LB&I Examination Process Section 5. Resolving the Examination 4.46.5 Resolving the Examination 4.46.5.1 Overview 4.46.5.2 Issue Resolution 4.46.5.3 Resolution vs.

14 Tips To Help Deal With (Or Avoid) The IRS In 2014

The IRS In 2014") Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com 14 Tips To Help Deal With (Or Avoid) The IRS In 2014

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com 14 Tips To Help Deal With (Or Avoid) The IRS In 2014

Managing the LB&I Examination Process: Using the Quality Examination Process and other Examination processes to your best advantage

Managing the LB&I Examination Process: Using the Quality Examination Process and other Examination processes to your best advantage Tax Controversy Web Series Second of Four sessions to be held through

Managing the LB&I Examination Process: Using the Quality Examination Process and other Examination processes to your best advantage Tax Controversy Web Series Second of Four sessions to be held through

HOW THE 1998 TAX ACT AFFECTS YOUR DEALINGS WITH THE IRS APPEALS OFFICE. The IRS Restructuring and Reform Act of 1998.

HOW THE 1998 TAX ACT AFFECTS YOUR DEALINGS WITH THE IRS APPEALS OFFICE The IRS Restructuring and Reform Act of 1998 January 22, 1999 Robert M. Kane, Jr. LeSourd & Patten, P.S. 600 University Street, Ste

HOW THE 1998 TAX ACT AFFECTS YOUR DEALINGS WITH THE IRS APPEALS OFFICE The IRS Restructuring and Reform Act of 1998 January 22, 1999 Robert M. Kane, Jr. LeSourd & Patten, P.S. 600 University Street, Ste

NAVIGATING AN IRS EXAM

NAVIGATING AN IRS EXAM Feb. 7, 2018 Today s presenters Patti Burquest Principal Washington National Tax practice lead Specializes in IRS examination and appeals matters, including alternative dispute resolutions

NAVIGATING AN IRS EXAM Feb. 7, 2018 Today s presenters Patti Burquest Principal Washington National Tax practice lead Specializes in IRS examination and appeals matters, including alternative dispute resolutions

Choosing Wisely: When to Use (or Not Use) Mediation to Obtain Cost Effective Closure in Exam & Collection Cases

Mediation to Obtain Cost Effective Closure in Exam & Collection Cases") Choosing Wisely: When to Use (or Not Use) Mediation to Obtain Cost Effective Closure in Exam & Collection Cases Maxine Aaronson Law Office of Maxine Aaronson 600 N. Pearl St. Suite 2170 Dallas, Texas 75201

Choosing Wisely: When to Use (or Not Use) Mediation to Obtain Cost Effective Closure in Exam & Collection Cases Maxine Aaronson Law Office of Maxine Aaronson 600 N. Pearl St. Suite 2170 Dallas, Texas 75201

Managing Tax Audits and Appeals September 29-30, 2016 Washington, DC

Managing Tax Audits and Appeals 2016 September 29-30, 2016 Washington, DC Tax Accounting Controversies & Developments Dwight Mersereau Resolving Accounting Method Issues General Background A taxpayer adopts

Managing Tax Audits and Appeals 2016 September 29-30, 2016 Washington, DC Tax Accounting Controversies & Developments Dwight Mersereau Resolving Accounting Method Issues General Background A taxpayer adopts

Overview of Today s Discussion

International Fiscal Association USA Branch New York Region Fall Seminar Thursday, December 18, 2014 What s Happening in LB&I Audits of International Issues Moderator: Diana Wollman Panelists: Nancy Chassman

International Fiscal Association USA Branch New York Region Fall Seminar Thursday, December 18, 2014 What s Happening in LB&I Audits of International Issues Moderator: Diana Wollman Panelists: Nancy Chassman

Tax Executives Institute Detroit Chapter Meeting

Tax Executives Institute Detroit Chapter Meeting David Blair dblair@crowell.com 202. 624.2765 Jennifer Ray jray@crowell.com 202. 624.2589 February 16, 2017 Navigating LB&I s New Issue Focused Audit Process

Tax Executives Institute Detroit Chapter Meeting David Blair dblair@crowell.com 202. 624.2765 Jennifer Ray jray@crowell.com 202. 624.2589 February 16, 2017 Navigating LB&I s New Issue Focused Audit Process

SECTION 5. SMALL CASE PROCEDURE FOR REQUESTING COMPETENT AUTHORITY ASSISTANCE.01 General.02 Small Case Standards.03 Small Case Filing Procedure

Rev. Proc. 2002 52 SECTION 1. PURPOSE OF THE REVENUE PROCEDURE SECTION 2. SCOPE.01 In General.02 Requests for Assistance.03 Authority of the U.S. Competent Authority.04 General Process.05 Failure to Request

Rev. Proc. 2002 52 SECTION 1. PURPOSE OF THE REVENUE PROCEDURE SECTION 2. SCOPE.01 In General.02 Requests for Assistance.03 Authority of the U.S. Competent Authority.04 General Process.05 Failure to Request

Compliance Assurance Process (CAP) Internal Revenue Manual (IRM) Sections

Internal Revenue Manual (IRM) Sections") Compliance Assurance Process (CAP) Internal Revenue Manual (IRM) Sections 4._.1.1 Introduction 4._.1.2 Overview of the Program (1) The Internal Revenue Service (IRS) initiated the Compliance Assurance

Compliance Assurance Process (CAP) Internal Revenue Manual (IRM) Sections 4._.1.1 Introduction 4._.1.2 Overview of the Program (1) The Internal Revenue Service (IRS) initiated the Compliance Assurance

Appeals NOTICE. ALI CLE - Handling a Tax Controversy: Audit, Appeals, Litigation and Collections October 8-9, 2015

205 Appeals ALI CLE - Handling a Tax Controversy: Audit, Appeals, Litigation and Collections October 8-9, 2015 NOTICE The following information is not intended to be written advice concerning one or more

205 Appeals ALI CLE - Handling a Tax Controversy: Audit, Appeals, Litigation and Collections October 8-9, 2015 NOTICE The following information is not intended to be written advice concerning one or more

IRS Controversies at Audit and Beyond

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1990 IRS Controversies at Audit and Beyond Charles

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1990 IRS Controversies at Audit and Beyond Charles

WRITTEN STATEMENT OF CHASTITY K. WILSON ON BEHALF OF THE THE AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS BEFORE

WRITTEN STATEMENT OF CHASTITY K. WILSON ON BEHALF OF THE THE AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS BEFORE THE UNITED STATES HOUSE OF REPRESENTATIVES COMMITTEE ON WAYS AND MEANS SUBCOMMITTEE

WRITTEN STATEMENT OF CHASTITY K. WILSON ON BEHALF OF THE THE AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS BEFORE THE UNITED STATES HOUSE OF REPRESENTATIVES COMMITTEE ON WAYS AND MEANS SUBCOMMITTEE

IRS Update: What s Happening Now

2 nd Annual CFMA Southwest Regional Conference San Diego, CA September 25-27, 2016 IRS Update: What s Happening Now Presented by: Kathy Petronchak KATHY PETRONCHAK Former IRS Commissioner of Small Business/Self

2 nd Annual CFMA Southwest Regional Conference San Diego, CA September 25-27, 2016 IRS Update: What s Happening Now Presented by: Kathy Petronchak KATHY PETRONCHAK Former IRS Commissioner of Small Business/Self

JOSEPH ALI Director, Technical Guidance Internal Revenue Service- Appeals Joe Ali is the Director for Appeals Technical Guidance.

JOSEPH ALI Director, Technical Guidance Internal Revenue Service- Appeals Joe Ali is the Director for Appeals Technical Guidance. In this position, he is responsible for managing, and directing the Area

JOSEPH ALI Director, Technical Guidance Internal Revenue Service- Appeals Joe Ali is the Director for Appeals Technical Guidance. In this position, he is responsible for managing, and directing the Area

SEC. 5. SMALL CASE PROCEDURE FOR REQUESTING COMPETENT AUTHORITY ASSISTANCE.01 General.02 Small Case Standards.03 Small Case Filing Procedure

26 CFR 601.201: Rulings and determination letters. Rev. Proc. 96 13 OUTLINE SECTION 1. PURPOSE OF MUTUAL AGREEMENT PROCESS SEC. 2. SCOPE Suspension.02 Requests for Assistance.03 U.S. Competent Authority.04

26 CFR 601.201: Rulings and determination letters. Rev. Proc. 96 13 OUTLINE SECTION 1. PURPOSE OF MUTUAL AGREEMENT PROCESS SEC. 2. SCOPE Suspension.02 Requests for Assistance.03 U.S. Competent Authority.04

Introduction to Appeals. October 2009

Introduction to Appeals October 2009 Appeals Founded In 1927, the IRS established an administrative appeal process to resolve tax disputes without litigation. Restructuring and Reform Act of 1998 Specifies

Introduction to Appeals October 2009 Appeals Founded In 1927, the IRS established an administrative appeal process to resolve tax disputes without litigation. Restructuring and Reform Act of 1998 Specifies

DID YOU GET YOUR BADGE SCANNED? UPDATE ON LB&I ENFORCEMENT CAMPAIGNS

DID YOU GET YOUR BADGE SCANNED? UPDATE ON LB&I ENFORCEMENT CAMPAIGNS #TaxLaw #FBA Username: taxlaw Password: taxlaw18 Presenters Moderator: Matthew Cooper, Senior Manager, Ernst & Young LLP Panelists:

DID YOU GET YOUR BADGE SCANNED? UPDATE ON LB&I ENFORCEMENT CAMPAIGNS #TaxLaw #FBA Username: taxlaw Password: taxlaw18 Presenters Moderator: Matthew Cooper, Senior Manager, Ernst & Young LLP Panelists:

Procedures for Protest to New York State and City Tribunals

September 25, 1997 Procedures for Protest to New York State and City Tribunals By: Glenn Newman This new feature of the New York Law Journal will highlight cases involving New York State and City tax controversies

September 25, 1997 Procedures for Protest to New York State and City Tribunals By: Glenn Newman This new feature of the New York Law Journal will highlight cases involving New York State and City tax controversies

Changes in IRS Exam and Appeals Procedures (and their impact on R&D Tax Credits)

") Changes in IRS Exam and Appeals Procedures (and their impact on R&D Tax Credits) Hosted by Bryan Auernig, Director Presented by Peter Mehta, Managing Director Tax Credit Co. September 22, 2015 Introductions

Changes in IRS Exam and Appeals Procedures (and their impact on R&D Tax Credits) Hosted by Bryan Auernig, Director Presented by Peter Mehta, Managing Director Tax Credit Co. September 22, 2015 Introductions

Federal Income Tax Examinations of Pass-Through Entities

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 2006 Federal Income Tax Examinations of Pass-Through

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 2006 Federal Income Tax Examinations of Pass-Through

25th Annual Health Sciences Tax Conference

25th Annual Health Sciences Tax Conference Current topics in IRS risk management and tax controversy December 7, 2015 Disclaimer EY refers to the global organization, and may refer to one or more, of the

25th Annual Health Sciences Tax Conference Current topics in IRS risk management and tax controversy December 7, 2015 Disclaimer EY refers to the global organization, and may refer to one or more, of the

Demystifying the IRS Appeals Process

Demystifying the IRS Appeals Process Houston TEI Tax School Shawn O Brien Houston, Texas (713) 238-2848 sobrien@mayerbrown.com IRS Audits and Global Controversy Issues May 4, 2017 Mayer Brown is a global

Demystifying the IRS Appeals Process Houston TEI Tax School Shawn O Brien Houston, Texas (713) 238-2848 sobrien@mayerbrown.com IRS Audits and Global Controversy Issues May 4, 2017 Mayer Brown is a global

New and Notable in IRS Controversy. Brian Paperny AT&T (Moderator) Mario Manniello Verizon Heather Maloy EY Kevin Brown PwC

Mario Manniello Verizon Heather Maloy EY Kevin Brown PwC") New and Notable in IRS Controversy Brian Paperny AT&T (Moderator) Mario Manniello Verizon Heather Maloy EY Kevin Brown PwC Disclaimer Views expressed in this presentation are those of the speakers and

New and Notable in IRS Controversy Brian Paperny AT&T (Moderator) Mario Manniello Verizon Heather Maloy EY Kevin Brown PwC Disclaimer Views expressed in this presentation are those of the speakers and

Federal Circuit Affirms FPAA Tolled Statute for Partnership when Losses were Attributable To Another Partnership

IRS Insights A closer look. In this issue: Federal Circuit Affirms FPAA Tolled Statute for Partnership when Losses were Attributable To Another Partnership... 1 IRS Grants Relief for Partnerships Filing

IRS Insights A closer look. In this issue: Federal Circuit Affirms FPAA Tolled Statute for Partnership when Losses were Attributable To Another Partnership... 1 IRS Grants Relief for Partnerships Filing

District court concludes that taxpayer s refund suit, relating to the carryback of a deduction for foreign taxes, was untimely

IRS Insights A closer look. In this issue: District court concludes that taxpayer s refund suit, relating to the carryback of a deduction for foreign taxes, was untimely... 1 IRS issues Chief Counsel Advice

IRS Insights A closer look. In this issue: District court concludes that taxpayer s refund suit, relating to the carryback of a deduction for foreign taxes, was untimely... 1 IRS issues Chief Counsel Advice

Tax Procedure Outline: Audit, Appeals, and Litigation

Tax Procedure Outline: Audit, Appeals, and Litigation Topic Page Before the Audit When the Business Engages in a Tax Sensitive Transaction What Document Creation and Retention Issues Should I Consider?................

Tax Procedure Outline: Audit, Appeals, and Litigation Topic Page Before the Audit When the Business Engages in a Tax Sensitive Transaction What Document Creation and Retention Issues Should I Consider?................

New and notable in IRS tax controversy

New and notable in IRS tax controversy Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal

New and notable in IRS tax controversy Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal

IRS Examination Developments for High Tech Firms

31 st Annual High Technology Tax Institute Sponsored by Tax Executives Institute, Inc. & San Jose State University College of Business November 9 & 10, 2015 IRS Examination Developments for High Tech Firms

31 st Annual High Technology Tax Institute Sponsored by Tax Executives Institute, Inc. & San Jose State University College of Business November 9 & 10, 2015 IRS Examination Developments for High Tech Firms

Internal Revenue Service Alternative Dispute Resolution Techniques

Internal Revenue Service Alternative Dispute Resolution Techniques May 2016 Boston Brussels Chicago Dallas Düsseldorf Frankfurt Houston London Los Angeles Miami Milan Munich New York Orange County Paris

Internal Revenue Service Alternative Dispute Resolution Techniques May 2016 Boston Brussels Chicago Dallas Düsseldorf Frankfurt Houston London Los Angeles Miami Milan Munich New York Orange County Paris

Corporate Whistleblower Developments Mark Oakes Partner Fulbright & Jaworski LLP June 10, 2014

Corporate Whistleblower Developments Mark Oakes Partner Fulbright & Jaworski LLP June 10, 2014 Mark Oakes Partner Securities Litigation, Investigations, and SEC Enforcement Norton Rose Fulbright T: +1

Corporate Whistleblower Developments Mark Oakes Partner Fulbright & Jaworski LLP June 10, 2014 Mark Oakes Partner Securities Litigation, Investigations, and SEC Enforcement Norton Rose Fulbright T: +1

Effective Management of IRS Information Document Requests (IDRs)

") Effective Management of IRS Information Document Requests (IDRs) George Hani, is the Chair of the Tax Department of Miller and Chevalier, Chartered. He concentrates his practice on the resolution of tax

Effective Management of IRS Information Document Requests (IDRs) George Hani, is the Chair of the Tax Department of Miller and Chevalier, Chartered. He concentrates his practice on the resolution of tax

Hot Audit Issues: 1. Parallel Audits 2. Reopening Audits 3. IDR Enforcement and Summons

Hot Audit Issues: 1. Parallel Audits 2. Reopening Audits 3. IDR Enforcement and Summons Shelley Leonard Parallel Audits 2 Parallel Audits IRS may conduct multiple types of audits concurrently Corporate

Hot Audit Issues: 1. Parallel Audits 2. Reopening Audits 3. IDR Enforcement and Summons Shelley Leonard Parallel Audits 2 Parallel Audits IRS may conduct multiple types of audits concurrently Corporate

DEPARTMENT OF THE TREASURY. July 18, Susan L. Latham /s/ Susan L. Latham Director, Policy, Quality and Case Support

DEPARTMENT OF THE TREASURY I N T E R N A L R E V E N U E S E R V I C E W A S H I N G T O N, D. C. 2 0 2 2 4 July 18, 2013 MEMORANDUM FOR APPEALS EMPLOYEES Control No. AP-08-0713-03 Expiration Date: 07/18/2014

DEPARTMENT OF THE TREASURY I N T E R N A L R E V E N U E S E R V I C E W A S H I N G T O N, D. C. 2 0 2 2 4 July 18, 2013 MEMORANDUM FOR APPEALS EMPLOYEES Control No. AP-08-0713-03 Expiration Date: 07/18/2014

IRS Audits and Appeals

ALGIERS AUSTIN DALLAS FORT WORTH HOUSTON LONDON MEXICO CITY MONTERREY NEW YORK PARIS RIO DE JANEIRO VITÓRIA IRS Audits and Appeals Tax Executives Institute March 21, 2006 Presented by Emily Parker emily.parker@tklaw.com

ALGIERS AUSTIN DALLAS FORT WORTH HOUSTON LONDON MEXICO CITY MONTERREY NEW YORK PARIS RIO DE JANEIRO VITÓRIA IRS Audits and Appeals Tax Executives Institute March 21, 2006 Presented by Emily Parker emily.parker@tklaw.com

TABLE OF CONTENTS. .03 Farmers cooperatives. .01 A request made during the course of an examination

Rev. Proc. 2000 2 TABLE OF CONTENTS SECTION 1. WHAT IS THE p. 77 PURPOSE OF THIS REVENUE PROCEDURE? SECTION 2. WHAT IS p. 78 TECHNICAL ADVICE? SECTION 3. ON WHAT ISSUES p. 78 MAY TECHNICAL ADVICE BE REQUESTED

Rev. Proc. 2000 2 TABLE OF CONTENTS SECTION 1. WHAT IS THE p. 77 PURPOSE OF THIS REVENUE PROCEDURE? SECTION 2. WHAT IS p. 78 TECHNICAL ADVICE? SECTION 3. ON WHAT ISSUES p. 78 MAY TECHNICAL ADVICE BE REQUESTED

Case 4:11-cv KGB Document 186 Filed 01/12/17 Page 1 of 5 IN THE UNITED STATES DISTRICT COURT EASTERN DISTRICT OF ARKANSAS WESTERN DIVISION

Case 4:11-cv-00749-KGB Document 186 Filed 01/12/17 Page 1 of 5 IN THE UNITED STATES DISTRICT COURT EASTERN DISTRICT OF ARKANSAS WESTERN DIVISION KENNETH WILLIAMS, MARY WILLIAMS, and KENNETH L. WILLIAMS

Case 4:11-cv-00749-KGB Document 186 Filed 01/12/17 Page 1 of 5 IN THE UNITED STATES DISTRICT COURT EASTERN DISTRICT OF ARKANSAS WESTERN DIVISION KENNETH WILLIAMS, MARY WILLIAMS, and KENNETH L. WILLIAMS

STATEMENT OF JENNIFER E. BREEN ON BEHALF OF THE AMERICAN BAR ASSOCIATION SECTION OF TAXATION BEFORE THE COMMITTEE ON SMALL BUSINESS OF THE

STATEMENT OF JENNIFER E. BREEN ON BEHALF OF THE AMERICAN BAR ASSOCIATION SECTION OF TAXATION BEFORE THE COMMITTEE ON SMALL BUSINESS OF THE UNITED STATES HOUSE OF REPRESENTATIVES FOR THE HEARING ON IRS

STATEMENT OF JENNIFER E. BREEN ON BEHALF OF THE AMERICAN BAR ASSOCIATION SECTION OF TAXATION BEFORE THE COMMITTEE ON SMALL BUSINESS OF THE UNITED STATES HOUSE OF REPRESENTATIVES FOR THE HEARING ON IRS

IRS Large Business & International Division Issues Transfer Pricing Guidance

IRS Insights A closer look. In this issue: IRS Large Business & International Division Issues Transfer Pricing Guidance... 1 Organisation for Economic Co-operation and Development Launces ICAP... 3 The

IRS Insights A closer look. In this issue: IRS Large Business & International Division Issues Transfer Pricing Guidance... 1 Organisation for Economic Co-operation and Development Launces ICAP... 3 The

RETIREMENT PLAN INVESTMENT MANAGEMENT AGREEMENT TRINITY PORTFOLIO ADVISORS LLC

vs.4 RETIREMENT PLAN INVESTMENT MANAGEMENT AGREEMENT TRINITY PORTFOLIO ADVISORS LLC Name of Plan: Name of Employer: Effective Date: This Retirement Plan Investment Management Agreement ( Agreement ) is

vs.4 RETIREMENT PLAN INVESTMENT MANAGEMENT AGREEMENT TRINITY PORTFOLIO ADVISORS LLC Name of Plan: Name of Employer: Effective Date: This Retirement Plan Investment Management Agreement ( Agreement ) is

Pre-Judgment Remedies Jordan Deering and Emily McCartney Norton Rose Fulbright Canada LLP March 6, 2018

Pre-Judgment Remedies Jordan Deering and Emily McCartney Norton Rose Fulbright Canada LLP March 6, 2018 Agenda 1. What are pre-judgment remedies? 2. Types of pre-judgment remedies 3. Ex-Parte Applications

Pre-Judgment Remedies Jordan Deering and Emily McCartney Norton Rose Fulbright Canada LLP March 6, 2018 Agenda 1. What are pre-judgment remedies? 2. Types of pre-judgment remedies 3. Ex-Parte Applications

Various publications, including FTB Publication 7277, "Personal Personal Income Tax Notice of Action

M0RRISON I FOERS 'ER Legal Updates & News Legal Updates California State Board of Equalization Adopts New Rules for Franchise Tax Board Tax Appeals May 2008 by Eric J. Cofill Coffill Related Practices:

M0RRISON I FOERS 'ER Legal Updates & News Legal Updates California State Board of Equalization Adopts New Rules for Franchise Tax Board Tax Appeals May 2008 by Eric J. Cofill Coffill Related Practices:

Strategies for Settling Tax Disputes

Strategies for Settling Tax Disputes Scott M. Stewart Partner, Chicago +1 312 701 7821 sstewart@mayerbrown.com John T. Hildy Partner, Chicago +1 312 701 7769 jhildy@mayerbrown.com Agenda Discuss our recent

Strategies for Settling Tax Disputes Scott M. Stewart Partner, Chicago +1 312 701 7821 sstewart@mayerbrown.com John T. Hildy Partner, Chicago +1 312 701 7769 jhildy@mayerbrown.com Agenda Discuss our recent

Bond Voyage: Navigating the waters of post-issuance compliance. Kristen Savant and Drew Slone Norton Rose Fulbright US LLP June 18, 2015

Bond Voyage: Navigating the waters of post-issuance compliance Kristen Savant and Drew Slone Norton Rose Fulbright US LLP June 18, 2015 2 Why can t I just set it and forget it? Possible IRS or SEC enforcement

Bond Voyage: Navigating the waters of post-issuance compliance Kristen Savant and Drew Slone Norton Rose Fulbright US LLP June 18, 2015 2 Why can t I just set it and forget it? Possible IRS or SEC enforcement

Memorandum. Office of Chief Counsel Internal Revenue Service. Number: Release Date: 7/7/2006 CC:PA:APJP:B2:AMIELKE POSTN

Office of Chief Counsel Internal Revenue Service Memorandum Number: 200627023 Release Date: 7/7/2006 CC:PA:APJP:B2:AMIELKE POSTN-112965-06 UILC: 6166.00-00, 6501.00-00, 6213.02-00, 7479.00-00, 7479.01-02

Office of Chief Counsel Internal Revenue Service Memorandum Number: 200627023 Release Date: 7/7/2006 CC:PA:APJP:B2:AMIELKE POSTN-112965-06 UILC: 6166.00-00, 6501.00-00, 6213.02-00, 7479.00-00, 7479.01-02

IRS Issue Price Regulations

IRS Issue Price Regulations National Association of Municipal Advisors WEBINAR March 2, 2017 National Association of Municipal Advisors Speakers l John Cross, Associate Tax Legislative Counsel, Office

IRS Issue Price Regulations National Association of Municipal Advisors WEBINAR March 2, 2017 National Association of Municipal Advisors Speakers l John Cross, Associate Tax Legislative Counsel, Office

Table of Contents. About This Book How To Use This Book Foreword Acknowledgments Preface

Table of Contents About This Book How To Use This Book Foreword Acknowledgments Preface vii ix xi xiii xv Chapter 1 Initial Client Engagement 1 Topical Index 1 1.01 Nature of Federal Tax Law 5 1.02 Role

Table of Contents About This Book How To Use This Book Foreword Acknowledgments Preface vii ix xi xiii xv Chapter 1 Initial Client Engagement 1 Topical Index 1 1.01 Nature of Federal Tax Law 5 1.02 Role

Like-Kind Exchange and Fixed Asset Conference

www.pwc.com Like-Kind Exchange and Fixed Asset Conference IRS Audit Readiness and Exam Experience The views expressed in this presentation should not be relied on as accounting, auditing or tax advice.

www.pwc.com Like-Kind Exchange and Fixed Asset Conference IRS Audit Readiness and Exam Experience The views expressed in this presentation should not be relied on as accounting, auditing or tax advice.

Valuation in Tax: What Non- Attorneys Should Know About Litigating Valuation Cases

Valuation in Tax: What Non- Attorneys Should Know About Litigating Valuation Cases Lawrence A. Sannicandro, Esq. Agostino & Associates, P.C. 14 Washington Place Hackensack, NJ 07601 (201) 488-5400, x.

Valuation in Tax: What Non- Attorneys Should Know About Litigating Valuation Cases Lawrence A. Sannicandro, Esq. Agostino & Associates, P.C. 14 Washington Place Hackensack, NJ 07601 (201) 488-5400, x.

Managing Tax Audits and Appeals September 22, 2016 Marina del Rey

Managing Tax Audits and Appeals 2016 September 22, 2016 Marina del Rey Privilege and Work Product Developments David J. Fischer - 3 - Privilege 101 Attorney-client privilege: Communications between an

Managing Tax Audits and Appeals 2016 September 22, 2016 Marina del Rey Privilege and Work Product Developments David J. Fischer - 3 - Privilege 101 Attorney-client privilege: Communications between an

Busy Season. all year long. TRI Tax Resolution Institute. where your tax debt is your power!

1 TRI Tax Resolution Institute where your tax debt is your power! Busy Season all year long www.taxresolutioninstitute.org info@taxresolutioninstitute.org (877) 829-8370 2 Appeals www.taxresolutioninstitute.org

1 TRI Tax Resolution Institute where your tax debt is your power! Busy Season all year long www.taxresolutioninstitute.org info@taxresolutioninstitute.org (877) 829-8370 2 Appeals www.taxresolutioninstitute.org

Rev. Proc CONTENTS SECTION 1. PURPOSE

26 CFR 601.204: Changes in accounting periods and in methods of accounting. (Also Part I, 441, 442, 444, 706, 1378; 1.441 1, 1.441 3, 1.442 1, 1.706 1, 1.1378 1.) Rev. Proc. 2002 38 CONTENTS SECTION 1.

26 CFR 601.204: Changes in accounting periods and in methods of accounting. (Also Part I, 441, 442, 444, 706, 1378; 1.441 1, 1.441 3, 1.442 1, 1.706 1, 1.1378 1.) Rev. Proc. 2002 38 CONTENTS SECTION 1.

Compliance Assurance Process (CAP) - Frequently Asked Questions (FAQs)

- Frequently Asked Questions (FAQs)") Compliance Assurance Process (CAP) - Frequently Asked Questions (FAQs) The Compliance Assurance Process (CAP) is a method of identifying and resolving tax issues through open, cooperative, and transparent

Compliance Assurance Process (CAP) - Frequently Asked Questions (FAQs) The Compliance Assurance Process (CAP) is a method of identifying and resolving tax issues through open, cooperative, and transparent

Non-Standard Accounting Measures: The Media, Regulators and Shareholders Zero In

Non-Standard Accounting Measures: The Media, Regulators and Shareholders Zero In Walied Soliman, Co-Chair, special situations team Orestes Pasparakis, Co-Chair, special situations team October 18, 2016

Non-Standard Accounting Measures: The Media, Regulators and Shareholders Zero In Walied Soliman, Co-Chair, special situations team Orestes Pasparakis, Co-Chair, special situations team October 18, 2016

Case: Document: 27 Page: 1 Filed: 06/05/

Case: 18-1586 Document: 27 Page: 1 Filed: 06/05/2018 2018-1586 UNITED STATES COURT OF APPEALS FOR THE FEDERAL CIRCUIT IN RE INTELLIGENT MEDICAL OBJECTS, INC., Appellant. Appeal from the United States Patent

Case: 18-1586 Document: 27 Page: 1 Filed: 06/05/2018 2018-1586 UNITED STATES COURT OF APPEALS FOR THE FEDERAL CIRCUIT IN RE INTELLIGENT MEDICAL OBJECTS, INC., Appellant. Appeal from the United States Patent

GIFT TAX RETURNS: FINDING AND FIXING PROBLEMS. Celeste C. Lawton Norton Rose Fulbright US LLP January 15, 2016

GIFT TAX RETURNS: FINDING AND FIXING PROBLEMS Celeste C. Lawton Norton Rose Fulbright US LLP January 15, 2016 Introduction Circumstances in which gift tax returns must be filed Common errors found in gift

GIFT TAX RETURNS: FINDING AND FIXING PROBLEMS Celeste C. Lawton Norton Rose Fulbright US LLP January 15, 2016 Introduction Circumstances in which gift tax returns must be filed Common errors found in gift

Rev. Proc I.R.B. 678 April 1, 2002

26 CFR 601.105: Examination of returns and claims for refund, credit, or abatement; determination of correct tax liability. (Also Part 1, 446, 481; 1.446 1, 1.481 1) Rev. Proc. 2002 18 SECTION 1. PURPOSE...680.01

26 CFR 601.105: Examination of returns and claims for refund, credit, or abatement; determination of correct tax liability. (Also Part 1, 446, 481; 1.446 1, 1.481 1) Rev. Proc. 2002 18 SECTION 1. PURPOSE...680.01

AD Tax Credits, Section 1603 Grant

Promoting the Anaerobic Digestion and Biogas Industries AD Tax Credits, Section 1603 Grant Updates and Audit Activity Our Partners: Organized by the American Biogas Council December 11, 2012 12 12:45 p.m.

Promoting the Anaerobic Digestion and Biogas Industries AD Tax Credits, Section 1603 Grant Updates and Audit Activity Our Partners: Organized by the American Biogas Council December 11, 2012 12 12:45 p.m.

ALI-ABA Course of Study Tax Controversy Practice: From Administrative Audit Through Litigation

59 ALI-ABA Course of Study Tax Controversy Practice: From Administrative Audit Through Litigation Sponsored with the cooperation of the ABA Section of Taxation June 12-13, 2008 Chicago, Illinois Internal

59 ALI-ABA Course of Study Tax Controversy Practice: From Administrative Audit Through Litigation Sponsored with the cooperation of the ABA Section of Taxation June 12-13, 2008 Chicago, Illinois Internal

Referral Agency and Packaging Agency Agreement

Referral Agency and Packaging Agency Agreement Please read this Referral Agency and Packaging Agency Agreement (the Agreement ) carefully. In signing this Agreement, you acknowledge that you have read,

Referral Agency and Packaging Agency Agreement Please read this Referral Agency and Packaging Agency Agreement (the Agreement ) carefully. In signing this Agreement, you acknowledge that you have read,

IRS Wasn't Wrong to Reject Taxpayer Payment Plan that Didn't Pay Off Liability in Ten Years

IRS Wasn't Wrong to Reject Taxpayer Payment Plan that Didn't Pay Off Liability in Ten Years Brown, TC Memo 2016-82 The Tax Court has held that IRS was not wrong to reject, based on several failings by

IRS Wasn't Wrong to Reject Taxpayer Payment Plan that Didn't Pay Off Liability in Ten Years Brown, TC Memo 2016-82 The Tax Court has held that IRS was not wrong to reject, based on several failings by

Internal Revenue Service. PURPOSE (1) This transmits revised IRM , Report of Foreign Bank and Financial Accounts (FBAR) Procedures.

This transmits revised IRM , Report of Foreign Bank and Financial Accounts (FBAR) Procedures.") MANUAL TRANSMITTAL Department of the Treasury Internal Revenue Service 4.26.17 MAY 5, 2008 PURPOSE (1) This transmits revised IRM 4.26.17, Report of Foreign Bank and Financial Accounts (FBAR) Procedures.

MANUAL TRANSMITTAL Department of the Treasury Internal Revenue Service 4.26.17 MAY 5, 2008 PURPOSE (1) This transmits revised IRM 4.26.17, Report of Foreign Bank and Financial Accounts (FBAR) Procedures.

FEDERAL TAX UPDATE Taxation Section Program Hot Topics and Updates

FEDERAL TAX UPDATE Taxation Section Program Hot Topics and Updates Robert D. Probasco Thompson & Knight LLP One Arts Plaza 1722 Routh Street, Suite 1500 Dallas, Texas 75201 (214) 969-1503 (214) 999-9113

FEDERAL TAX UPDATE Taxation Section Program Hot Topics and Updates Robert D. Probasco Thompson & Knight LLP One Arts Plaza 1722 Routh Street, Suite 1500 Dallas, Texas 75201 (214) 969-1503 (214) 999-9113

Tax Matters Partner: Power & Responsibility Partnership Committee American Bar Association, Tax Section January 21, 2011

Tax Matters Partner: Power & Responsibility Partnership Committee American Bar Association, Tax Section January 21, 2011 1. Scope a. The term Tax Matters Partner carries meaning only within TEFRA unified

Tax Matters Partner: Power & Responsibility Partnership Committee American Bar Association, Tax Section January 21, 2011 1. Scope a. The term Tax Matters Partner carries meaning only within TEFRA unified

APPEAL AND INDEPENDENT DISPUTE RESOLUTION PROCESSES

APPEAL AND INDEPENDENT DISPUTE RESOLUTION PROCESSES 2016 Fannie Mae. Trademarks of Fannie Mae. 8.17.2016 1 of 20 Contents INTRODUCTION... 4 PART A. APPEAL, IMPASSE, AND MANAGEMENT ESCALATION PROCESSES...

APPEAL AND INDEPENDENT DISPUTE RESOLUTION PROCESSES 2016 Fannie Mae. Trademarks of Fannie Mae. 8.17.2016 1 of 20 Contents INTRODUCTION... 4 PART A. APPEAL, IMPASSE, AND MANAGEMENT ESCALATION PROCESSES...

Puerto Rico Federal Bar Association Seminar

Puerto Rico Federal Bar Association Seminar Modification or Discharge of Debt In a Chapter 9 Case and How This Could Be Relevant To Puerto Rico ZACK A. CLEMENT Partner Fulbright & Jaworski LLP Norton Rose

Puerto Rico Federal Bar Association Seminar Modification or Discharge of Debt In a Chapter 9 Case and How This Could Be Relevant To Puerto Rico ZACK A. CLEMENT Partner Fulbright & Jaworski LLP Norton Rose

Audits of Estate Tax Returns and Protecting the Fiduciary Client. Presented to the Estate and Financial Planning Council of Central New Jersey

Audits of Estate Tax Returns and Protecting the Fiduciary Client Presented to the Estate and Financial Planning Council of Central New Jersey Frank Agostino, Esq. Lawrence A. Sannicandro, Esq. April 20,

Audits of Estate Tax Returns and Protecting the Fiduciary Client Presented to the Estate and Financial Planning Council of Central New Jersey Frank Agostino, Esq. Lawrence A. Sannicandro, Esq. April 20,

Legal update. Iran: new petroleum sector opportunities. March 2016 Energy Oil and gas. Background. Canadian sanctions

Legal update Iran: new petroleum sector opportunities March 2016 Energy Oil and gas The announcement last month by Foreign Affairs Minister Stéphane Dion lifting most of the sanctions restricting Canadian

Legal update Iran: new petroleum sector opportunities March 2016 Energy Oil and gas The announcement last month by Foreign Affairs Minister Stéphane Dion lifting most of the sanctions restricting Canadian

Uncertain tax positions and FIN 48: practical recommendations

OCTOBER 31, 2006 Uncertain tax positions and FIN 48: practical recommendations The time for adoption of FASB Interpretation No. 48, Accounting for Uncertainty in Income Taxes (FIN 48) is fast approaching

OCTOBER 31, 2006 Uncertain tax positions and FIN 48: practical recommendations The time for adoption of FASB Interpretation No. 48, Accounting for Uncertainty in Income Taxes (FIN 48) is fast approaching

Revenue Procedure 97-27

CLICK HERE to return to the home page Revenue Procedure 97-27 TABLE OF CONTENTS SECTION 1. PURPOSE.01 In general.02 Voluntary compliance.03 Significant changes SECTION 2. BACKGROUND.01 Change in method

CLICK HERE to return to the home page Revenue Procedure 97-27 TABLE OF CONTENTS SECTION 1. PURPOSE.01 In general.02 Voluntary compliance.03 Significant changes SECTION 2. BACKGROUND.01 Change in method

The Minnesota Workers Compensation Assigned Risk Plan (MWCARP) Legal Defense Services Request For Proposals

Legal Defense Services Request For Proposals") The Minnesota Workers Compensation Assigned Risk Plan (MWCARP) Legal Defense Services Request For Proposals ( RFP) Issued by Affinity Insurance Services, Inc. Plan Administrator - MWCARP This RFP is a

The Minnesota Workers Compensation Assigned Risk Plan (MWCARP) Legal Defense Services Request For Proposals ( RFP) Issued by Affinity Insurance Services, Inc. Plan Administrator - MWCARP This RFP is a

Recent Developments in Estate & Gift Tax

Recent Developments in Estate & Gift Tax Disclaimer The information presented in this handout from the Internal Revenue Service is for educational purposes only and shall not be cited or relied upon as

Recent Developments in Estate & Gift Tax Disclaimer The information presented in this handout from the Internal Revenue Service is for educational purposes only and shall not be cited or relied upon as

Uniform Rules of Practice Circuit Court of Illinois Nineteenth Judicial Circuit

If a l ~ DEC 1 4 2015 Uniform Rules of Practice Circuit Court of Illinois Nineteenth Judicial Circuit ~~ CIRCUIT CLERK Amendment to Rule 19.00, LAKE COUNTY RESIDENTIAL REAL ESTATE MORTGAGE FORECLOSURE

If a l ~ DEC 1 4 2015 Uniform Rules of Practice Circuit Court of Illinois Nineteenth Judicial Circuit ~~ CIRCUIT CLERK Amendment to Rule 19.00, LAKE COUNTY RESIDENTIAL REAL ESTATE MORTGAGE FORECLOSURE

Protest Procedure: A Primer

Protest Procedure: A Primer Marjorie Welch Interim General Counsel Oklahoma Tax Commission Agency s Mission Statement: To serve the people of Oklahoma by promoting tax compliance through quality service

Protest Procedure: A Primer Marjorie Welch Interim General Counsel Oklahoma Tax Commission Agency s Mission Statement: To serve the people of Oklahoma by promoting tax compliance through quality service

IRS Policy Changes Impact R&D Credit IRS changes magnify the importance of methodology and documentation

IRS changes magnify the importance of methodology and documentation The new IDR enforcement policy and the Appeals Judicial Approach and Culture project have been in effect for over a year. Both policies

IRS changes magnify the importance of methodology and documentation The new IDR enforcement policy and the Appeals Judicial Approach and Culture project have been in effect for over a year. Both policies

Court Special Services

BUDGET & FULL-TIME EQUIVALENTS SUMMARY & BUDGET PROGRAMS CHART Operating $ 15,248,900 Capital - FTEs - Darrel E. Parker Superior Court Executive Officer Grand Jury Court Special Services Conflict Defense

BUDGET & FULL-TIME EQUIVALENTS SUMMARY & BUDGET PROGRAMS CHART Operating $ 15,248,900 Capital - FTEs - Darrel E. Parker Superior Court Executive Officer Grand Jury Court Special Services Conflict Defense

Busy Season. all year long. TRI Tax Resolution Institute. where your tax debt is your power!

1 TRI Tax Resolution Institute where your tax debt is your power! Busy Season all year long www.taxresolutioninstitute.org info@taxresolutioninstitute.org (877) 829-8370 2 Appeals www.taxresolutioninstitute.org

1 TRI Tax Resolution Institute where your tax debt is your power! Busy Season all year long www.taxresolutioninstitute.org info@taxresolutioninstitute.org (877) 829-8370 2 Appeals www.taxresolutioninstitute.org

(4) Before afederal court. 14

Before afederal court. 14") 26 CFR 601.204: Changes in accounting periods and in methods of accounting. (Also Part I, 446, 481; 1.446 1, 1.481 1, 1.481 4.) Rev. Proc. 97 27 TABLE OF CONTENTS PAGE SECTION 1. PURPOSE... 11.01 In general...

26 CFR 601.204: Changes in accounting periods and in methods of accounting. (Also Part I, 446, 481; 1.446 1, 1.481 1, 1.481 4.) Rev. Proc. 97 27 TABLE OF CONTENTS PAGE SECTION 1. PURPOSE... 11.01 In general...

Effectively Representing the Taxpayer in a Substantiation and Penalty Case. US Tax Court Judicial Conference Tuesday March 27, 2018

Effectively Representing the Taxpayer in a Substantiation and Penalty Case US Tax Court Judicial Conference Tuesday March 27, 2018 Substantiation of Income/gross receipts and Expenses- generally Self-employed

Effectively Representing the Taxpayer in a Substantiation and Penalty Case US Tax Court Judicial Conference Tuesday March 27, 2018 Substantiation of Income/gross receipts and Expenses- generally Self-employed

IRS Insights A closer look. January In this issue:

IRS Insights A closer look. In this issue: US Court of Appeals for the Federal Circuit rules that a taxpayer and its subsidiary foreign sales corporation are not the same taxpayer for purposes of the interest

IRS Insights A closer look. In this issue: US Court of Appeals for the Federal Circuit rules that a taxpayer and its subsidiary foreign sales corporation are not the same taxpayer for purposes of the interest

Page 1 of 8 Part 7. Rulings and Agreements Chapter 2. TE/GE Closing Agreements Section 3. Tax Exempt Bonds Voluntary Closing Agreement Program 7.2.3 Tax Exempt Bonds

Page 1 of 8 Part 7. Rulings and Agreements Chapter 2. TE/GE Closing Agreements Section 3. Tax Exempt Bonds Voluntary Closing Agreement Program 7.2.3 Tax Exempt Bonds

sus PETITIONERS' SUPPLEMENTAL BRIEF MAY * MAY US TAX COURT gges t US TAX COURT 7:32 PM LAWRENCE G. GRAEV & LORNA GRAEV, Petitioners,

US TAX COURT gges t US TAX COURT RECEIVED y % sus efiled MAY 31 2017 * MAY 31 2017 7:32 PM LAWRENCE G. GRAEV & LORNA GRAEV, Petitioners, ELECTRONICALLY FILED v. Docket No. 30638-08 COMMISSIONER OF INTERNAL

US TAX COURT gges t US TAX COURT RECEIVED y % sus efiled MAY 31 2017 * MAY 31 2017 7:32 PM LAWRENCE G. GRAEV & LORNA GRAEV, Petitioners, ELECTRONICALLY FILED v. Docket No. 30638-08 COMMISSIONER OF INTERNAL

Smart Contracts Presentation to ACC 18 th October Sean Murphy

Smart Contracts Presentation to ACC 18 th October 2016 Sean Murphy What is a blockchain? How do blockchains operate? What are the benefits of blockchains? What are smart contracts? How do smart contracts

Smart Contracts Presentation to ACC 18 th October 2016 Sean Murphy What is a blockchain? How do blockchains operate? What are the benefits of blockchains? What are smart contracts? How do smart contracts

Comptroller Tax Process Improvements

Comptroller Tax Process Improvements Introduction Comptroller Susan Combs announces improvements to all phases of the Comptroller s tax process. After transferring the Administrative Law Judges (ALJs)

Comptroller Tax Process Improvements Introduction Comptroller Susan Combs announces improvements to all phases of the Comptroller s tax process. After transferring the Administrative Law Judges (ALJs)

WASHINGTON STATE LLC MEMBER-MANAGED OPERATING AGREEMENT

WASHINGTON STATE LLC MEMBER-MANAGED OPERATING AGREEMENT I. PRELIMINARY PROVISIONS (1) Effective Date: This operating agreement of effective, is adopted by the members whose signatures appear at the end

WASHINGTON STATE LLC MEMBER-MANAGED OPERATING AGREEMENT I. PRELIMINARY PROVISIONS (1) Effective Date: This operating agreement of effective, is adopted by the members whose signatures appear at the end

2016 IRS Collections Representation Boot Camp

2016 IRS Collections Representation Boot Camp Presented by: Dan Henn, CPA & Jassen Bowman, EA Sponsors: IRS Program Number: SDQJW-T-00040-16-I Sponsor ID #137128. Before We Get Started For proper CPE tracking,

2016 IRS Collections Representation Boot Camp Presented by: Dan Henn, CPA & Jassen Bowman, EA Sponsors: IRS Program Number: SDQJW-T-00040-16-I Sponsor ID #137128. Before We Get Started For proper CPE tracking,

WHAT EVERY PLANNER NEEDS TO KNOW ABOUT THE COURT SYSTEM

Diversity of opinion helps us be more successful! Your Success Matters! Therefore Prudential is pleased to provide you with material that offers different views and opinions on various subjects. Please

Diversity of opinion helps us be more successful! Your Success Matters! Therefore Prudential is pleased to provide you with material that offers different views and opinions on various subjects. Please

California's "Tax Amnesty": What Every California Taxpayer Should Know

California's "Tax Amnesty": What Every California Taxpayer Should Know 2/17/2005 State + Local Tax Client Alert On August 16, 2004, California enacted a tax amnesty ("Amnesty Program") covering both sales

California's "Tax Amnesty": What Every California Taxpayer Should Know 2/17/2005 State + Local Tax Client Alert On August 16, 2004, California enacted a tax amnesty ("Amnesty Program") covering both sales

Click to edit Master title style

Second level Third level Click No Fighting: to edit Master an title style Overview of Claims, Equitable Adjustments, and Click Disputes to edit Master text styles Second level Breakout Third Session level

Second level Third level Click No Fighting: to edit Master an title style Overview of Claims, Equitable Adjustments, and Click Disputes to edit Master text styles Second level Breakout Third Session level

Responding to Adverse IRS Audit Assessments: Audit Reconsideration Requests, IRS Appeals, and Settlement Strategies

Responding to Adverse IRS Audit Assessments: Audit Reconsideration Requests, IRS Appeals, and Settlement Strategies TUESDAY, MARCH 1, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved

Responding to Adverse IRS Audit Assessments: Audit Reconsideration Requests, IRS Appeals, and Settlement Strategies TUESDAY, MARCH 1, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved

IRS COLLECTION PROCEDURES AND TAXPAYER REMEDIES

IRS COLLECTION PROCEDURES AND TAXPAYER REMEDIES By: Daniel J. Cramer Cramer, Minock & Sweeney, PLC The IRS has broad powers to enforce tax laws and collect outstanding taxes. The most common IRS collection

IRS COLLECTION PROCEDURES AND TAXPAYER REMEDIES By: Daniel J. Cramer Cramer, Minock & Sweeney, PLC The IRS has broad powers to enforce tax laws and collect outstanding taxes. The most common IRS collection