IRS Appeals New Faces, New Challenges

|

|

|

- August Robbins

- 5 years ago

- Views:

Transcription

1 TEI s 68 th Midyear Conference IRS Appeals New Faces, New Challenges Brian Kaufman, Capital One Financial Corporation (moderator) Patti Burquest, RSM US LLP Alex Sadler, Morgan, Lewis & Bockius LLP Susan Seabrook, Eversheds Sutherland LLP

2 Resolving Disputes in Appeals Begins with Exam s submission of the taxpayer s protest of the RAR and Exam s rebuttal to the protest Consideration independent of Exam o The mission of Appeals is to resolve tax controversies, without litigation, on a basis which is fair and impartial to both the Government and the taxpayer and in a manner that will enhance voluntary compliance and public confidence in the integrity and efficiency of the Service. o Ex parte communications between Appeals officers and other IRS employees prohibited to the extent that such communications appear to compromise the independence of the Appeals officers Unlike Exam, Appeals is authorized to consider litigating hazards Has historically demonstrated willingness to materially reduce Exam adjustments on certain issues 2

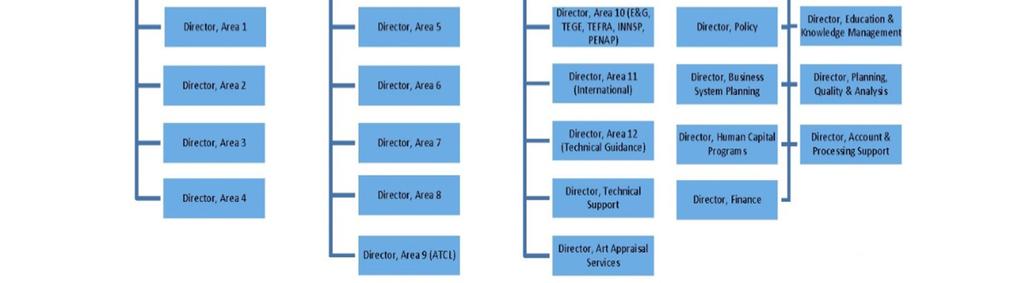

3 Appeals Organizational Chart 3

4 Appeals Judicial Approach and Culture Project (AJAC) Aimed to return Appeals to a more quasi-judicial approach in handling cases o See IRM and Appeals Policy Statements 8-2 & 8-3 Appeals will not raise new issues not considered by Exam or reopen previously agreed issues o Taxpayer-friendly principle; negates risk that taxpayer could end up worse off in Appeals than with Exam o But principle does not prevent Appeals from considering new legal theories or alternative arguments in support of an existing position 4

5 Appeals Judicial Approach and Culture Project (AJAC) (Cont d) Appeals will no longer return underdeveloped cases to Exam but will instead attempt to settle them based on factual hazards But Appeals will return a case to Exam if the taxpayer raises a new issue or provides new information o A new issue is a matter not raised during Compliance's consideration Effectively laid the groundwork for the Acknowledgement of Facts IDR 5

6 Recent Realignment of Appeals Recently, Appeals has undergone numerous practice changes that, in the opinion of some, frustrate Appeals historic purpose of settling tax controversies administratively. The changes include changes to: Appeals team cases conferencing initiative; Conference practices; Compliance and Counsel participation in settlement conferences; Informal issue coordination in Appeals; Appeals Team Case Leader (ATCL) settlement authority; and Appeals jurisdiction in docketed cases. 6

7 Recent Realignment of Appeals (Cont d) Numerous organizations have weighed on the recent changes. The Taxpayer Advocate Service s 2016 Annual Report to Congress stated that changes were impacting taxpayer rights to: o Challenge the IRS s position and be heard; o Appeal an IRS decision in an independent forum; o Privacy; and o A fair and just tax system. The ABA Section of Taxation provided comments and similarly expressed concern that several changes may decrease taxpayer access to settlement conferences and case resolution. 7

8 Appeals Team Cases Conferencing Initiative Expectations call with taxpayer and representatives, Exam, and Appeals o Sets vision for conference, addresses administrative matters, and expectations for conduct of conference o Conveyed that resolution expected at first conference Followed by expectations letter o New arguments and facts to be provided to Appeals and shared with other side at least 45 days in advance o Responses to any questions by Appeals must be answered within 2 weeks of the conference Exam is invited and expected to stay through the taxpayer s presentation up to the point when settlement discussions end o If the taxpayer agrees, Exam may stay longer and Appeals will use mediation techniques 8

9 Participation in Appeals Conferences by IRS Employees Appeals has the discretion to invite Counsel and/or Compliance to the conference. The prohibition against ex parte communications must not be violated. See Rev. Proc Appeals may also request that other experts attend conferences. IRM ( ) Perceived benefits o Ensures that Appeals understands Exam s position o Allows Appeals to test Exam s credibility o Everyone in the same room Perceived downsides o Potential for disruption and interference o Hinders settlement process o Slows down the conference o Increases cost 9

10 Face-to-Face Conferences IRM updated in October 2016 to default to telephone conferences and offer virtual delivery services (VDS) conference if available o IRM ( ) ( Except as set forth below, hold conferences by telephone. ) IRS rationale: resources, costs, faster resolution, consistency Significant objections: impeded right to fair and impartial hearing 10

11 Face-to-Face Conferences Recent developments o In September 2017, the IRS announced moving back to in-person Appeals conferences o In October 2017, the IRS issued a memo for Appeals employees stating that for field cases, if a taxpayer requests an in-person conference, Appeals will use its best efforts to schedule an in-person conference on a date and at a location that is reasonably convenient for the taxpayer and Appeals. Can still be limited by resource constraints Campus cases can t currently accommodate in-person conferences more expected soon on this issue o Appeals currently piloting virtual conferences 11

12 Informal Issue Coordination Taxpayers and practitioners have encountered Appeals officers and ATCLs attempting to be consistent on certain issues o Not done pursuant to any formal guidance o Rather appears coordination occurring at management level Consequences o Increased consistency among similarly situated taxpayers o But removes discretion from Appeals officers and ATCLs o Material differences between taxpayers may be disregarded o No transparency concerning the coordination 12

13 ATCL Settlement Authority There was concern that ATCL settlement authority provided the ATCL job description in IRM ( ) would be limited or removed However, these concerns did not bear out; settlement authority remains with the ATCLs o However, Appeals has revised its procedures to make clear that a manager must review a case and approve the settlement prior to finalizing the settlement. Interim Guidance Control No.: AP (Jan. 12, 2017) o Creates potential for consistency but also delays and frustrated settlements Other required coordination Appeals settlements, including by an ATCL, are subject to review and concurrence by the Technical Specialist if the settlement includes Appeals Coordinated Issues. Informally, there are Subject Matter Experts, and it appears to be the policy that they be consulted. 13

14 Appeals Jurisdiction in Docketed Cases Rev. Proc updates Appeals procedures for cases docketed in Tax Court o Generally, there is an automatic referral to Appeals if case not previously considered and taxpayer agrees When a docketed case is forwarded to Appeals, Appeals has sole authority to resolve the case until it is returned to Counsel o However, IRS Counsel has discretion to retain case Appeals may be denied for cases designated for litigation there are procedures to avoid such designation New provision: Appeals may be denied in cases where not in interest of sound tax administration some concern this may be applied to deny access to Appeals more frequently 14

15 Taxpayer-Adverse Guidance in Appeals Generally, if an IRS position (i.e., revenue ruling, TAM, etc.) is adverse to the taxpayer, Appeals may nevertheless concede the issue based on litigating hazards. IRM (2). o However, Appeals will not settle cases contrary to a National Office ruling on an issue that a court reviews under an abuse-of-discretion standard (e.g., a taxpayer s application for an advance (non-automatic) consent change in accounting method). IRM (2) and o Appeals also will not settle cases contrary to a National Office adverse ruling in response to a taxpayer s request for extension of time to request section 9100 relief. IRM Appeals must coordinate with the National Office when a full concession of an issue is recommended and contrary to the IRS position. Taxpayers perspectives: potential for expansive scope, contrary to Appeals purpose, and undercuts Appeals independence 15

16 What About Penalty Appeals? Delinquency penalties First Time Abate or Reasonable Cause? FTA phone Reasonable Cause respond to penalty notice in writing with request for abatement If denied, appeal to the Penalty Appeals Coordinator (PAC) and add a request for a transfer to Appeals if the PAC does not abate Request face-to-face Appeals conference For assessed penalties other than under section 6651, 6654 or 6655, request documentation of manager approval of the assessment. Chai v. Comm r, 851 F.3d 190 (2d Cir 2017) aff g in part, rev g in part T.C. Memo and Graev v. Comm r, 149 T.C. No. 23 (2017). Accuracy-related penalties Include in written protest highlighting authority supporting return position Consider ADR approaches 16

17 Alternatives to Traditional Appeals Early referral (Rev. Proc ) o Appeals takes jurisdiction; other issues remain in Exam o Available once an issue is fully developed (i.e., NOPA issued) Fast-Track Settlement (Rev. Proc ) o Exam retains jurisdiction o Occurs between issuance of NOPA and 30-day letter o Appeals role is to facilitate discussion and negotiations o Litigating hazards may be taken into account Rapid Appeals Process (IRM ) o Appeals jurisdiction o Uses Fast-Track Settlement techniques for matters already in Appeals Post-Appeals Mediation (Rev. Proc ) o Appeals mediator + private mediator at taxpayer s expense o Appeals officer defends position; steps into shoes of Exam o Last gasp before litigation 17

18 Thank You! We would be happy to answer any questions. 18

Sheldon M. Kay Troy L. Olsen February 20, Current Update on IRS Appeals Division and Other Acronyms, Including AJAC, RAP, ADR and NII

Sheldon M. Kay Troy L. Olsen February 20, 2014 Current Update on IRS Appeals Division and Other Acronyms, Including AJAC, RAP, ADR and NII Polling Question How many times have you been before Appeals?

Sheldon M. Kay Troy L. Olsen February 20, 2014 Current Update on IRS Appeals Division and Other Acronyms, Including AJAC, RAP, ADR and NII Polling Question How many times have you been before Appeals?

Working with the IRS Office of Appeals

Working with the IRS Office of Appeals Tom Vangen, Appeals Team Manager, Joe Haynes, Appeals Team Manager Patrick McGuire, Area Director January 2018 TOPICS FOR TODAY: Overview of Examination Appeals The

Working with the IRS Office of Appeals Tom Vangen, Appeals Team Manager, Joe Haynes, Appeals Team Manager Patrick McGuire, Area Director January 2018 TOPICS FOR TODAY: Overview of Examination Appeals The

Working with the IRS Office of Appeals What to Expect in Examination Appeals

Working with the IRS Office of Appeals What to Expect in Examination Appeals Glenn Gizzi Fall 2017 The Office of Appeals Established in 1927 Informal administrative forum Settle tax disputes without trial

Working with the IRS Office of Appeals What to Expect in Examination Appeals Glenn Gizzi Fall 2017 The Office of Appeals Established in 1927 Informal administrative forum Settle tax disputes without trial

The Audit is Over Now What?

Where Do We Go From Here: A Comparison of Alternatives When You and the IRS Agree to Disagree JENNY LOUISE JOHNSON, Holland & Knight LLP Co-Chair of Tax Controversy Practice CHARLES E. HODGES, Kilpatrick

Where Do We Go From Here: A Comparison of Alternatives When You and the IRS Agree to Disagree JENNY LOUISE JOHNSON, Holland & Knight LLP Co-Chair of Tax Controversy Practice CHARLES E. HODGES, Kilpatrick

Resolving Tax Controversies: An Overview For Counsel Association of Corporate Counsel, 2017 Back to School Symposium August 15, 2017

Resolving Tax Controversies: An Overview For Counsel Association of Corporate Counsel, 2017 Back to School Symposium August 15, 2017 Brent C. Gardner, Senior Tax Counsel, Director of Tax Controversy, Hewlett-Packard

Resolving Tax Controversies: An Overview For Counsel Association of Corporate Counsel, 2017 Back to School Symposium August 15, 2017 Brent C. Gardner, Senior Tax Counsel, Director of Tax Controversy, Hewlett-Packard

McGladrey Tax Controversy Series Hot Topics in Tax Controversy Resolving Issues. January 26, 2012

McGladrey Tax Controversy Series Hot Topics in Tax Controversy Resolving Issues January 26, 2012 Agenda Topic Mins Introduction 5 Pre-Return Opportunities 15 Examination Opportunities 15 Appeals Opportunities

McGladrey Tax Controversy Series Hot Topics in Tax Controversy Resolving Issues January 26, 2012 Agenda Topic Mins Introduction 5 Pre-Return Opportunities 15 Examination Opportunities 15 Appeals Opportunities

Part 4. Examining Process. Chapter 46. LB&I Examination Process. Section 5. Resolving the Examination Resolving the Examination

Part 4. Examining Process Chapter 46. LB&I Examination Process Section 5. Resolving the Examination 4.46.5 Resolving the Examination 4.46.5.1 Overview 4.46.5.2 Issue Resolution 4.46.5.3 Resolution vs.

Part 4. Examining Process Chapter 46. LB&I Examination Process Section 5. Resolving the Examination 4.46.5 Resolving the Examination 4.46.5.1 Overview 4.46.5.2 Issue Resolution 4.46.5.3 Resolution vs.

WRITTEN STATEMENT OF CHASTITY K. WILSON ON BEHALF OF THE THE AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS BEFORE

WRITTEN STATEMENT OF CHASTITY K. WILSON ON BEHALF OF THE THE AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS BEFORE THE UNITED STATES HOUSE OF REPRESENTATIVES COMMITTEE ON WAYS AND MEANS SUBCOMMITTEE

WRITTEN STATEMENT OF CHASTITY K. WILSON ON BEHALF OF THE THE AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS BEFORE THE UNITED STATES HOUSE OF REPRESENTATIVES COMMITTEE ON WAYS AND MEANS SUBCOMMITTEE

Federal Circuit Affirms FPAA Tolled Statute for Partnership when Losses were Attributable To Another Partnership

IRS Insights A closer look. In this issue: Federal Circuit Affirms FPAA Tolled Statute for Partnership when Losses were Attributable To Another Partnership... 1 IRS Grants Relief for Partnerships Filing

IRS Insights A closer look. In this issue: Federal Circuit Affirms FPAA Tolled Statute for Partnership when Losses were Attributable To Another Partnership... 1 IRS Grants Relief for Partnerships Filing

DID YOU GET YOUR BADGE SCANNED? UPDATE ON LB&I ENFORCEMENT CAMPAIGNS

DID YOU GET YOUR BADGE SCANNED? UPDATE ON LB&I ENFORCEMENT CAMPAIGNS #TaxLaw #FBA Username: taxlaw Password: taxlaw18 Presenters Moderator: Matthew Cooper, Senior Manager, Ernst & Young LLP Panelists:

DID YOU GET YOUR BADGE SCANNED? UPDATE ON LB&I ENFORCEMENT CAMPAIGNS #TaxLaw #FBA Username: taxlaw Password: taxlaw18 Presenters Moderator: Matthew Cooper, Senior Manager, Ernst & Young LLP Panelists:

Managing the LB&I Examination Process: Using the Quality Examination Process and other Examination processes to your best advantage

Managing the LB&I Examination Process: Using the Quality Examination Process and other Examination processes to your best advantage Tax Controversy Web Series Second of Four sessions to be held through

Managing the LB&I Examination Process: Using the Quality Examination Process and other Examination processes to your best advantage Tax Controversy Web Series Second of Four sessions to be held through

Introduction to Appeals. October 2009

Introduction to Appeals October 2009 Appeals Founded In 1927, the IRS established an administrative appeal process to resolve tax disputes without litigation. Restructuring and Reform Act of 1998 Specifies

Introduction to Appeals October 2009 Appeals Founded In 1927, the IRS established an administrative appeal process to resolve tax disputes without litigation. Restructuring and Reform Act of 1998 Specifies

NAVIGATING AN IRS EXAM

NAVIGATING AN IRS EXAM Feb. 7, 2018 Today s presenters Patti Burquest Principal Washington National Tax practice lead Specializes in IRS examination and appeals matters, including alternative dispute resolutions

NAVIGATING AN IRS EXAM Feb. 7, 2018 Today s presenters Patti Burquest Principal Washington National Tax practice lead Specializes in IRS examination and appeals matters, including alternative dispute resolutions

Fast Track and Appeals. David B. Blair David J. Fischer

Fast Track and Appeals David B. Blair David J. Fischer Appeals Judicial Approach and Culture (AJAC) Appeals will not engage in fact-finding Appeals will not consider new facts not presented to Exam Factual

Fast Track and Appeals David B. Blair David J. Fischer Appeals Judicial Approach and Culture (AJAC) Appeals will not engage in fact-finding Appeals will not consider new facts not presented to Exam Factual

Appeals NOTICE. ALI CLE - Handling a Tax Controversy: Audit, Appeals, Litigation and Collections October 8-9, 2015

205 Appeals ALI CLE - Handling a Tax Controversy: Audit, Appeals, Litigation and Collections October 8-9, 2015 NOTICE The following information is not intended to be written advice concerning one or more

205 Appeals ALI CLE - Handling a Tax Controversy: Audit, Appeals, Litigation and Collections October 8-9, 2015 NOTICE The following information is not intended to be written advice concerning one or more

Overview of Today s Discussion

International Fiscal Association USA Branch New York Region Fall Seminar Thursday, December 18, 2014 What s Happening in LB&I Audits of International Issues Moderator: Diana Wollman Panelists: Nancy Chassman

International Fiscal Association USA Branch New York Region Fall Seminar Thursday, December 18, 2014 What s Happening in LB&I Audits of International Issues Moderator: Diana Wollman Panelists: Nancy Chassman

Demystifying the IRS Appeals Process

Demystifying the IRS Appeals Process Houston TEI Tax School Shawn O Brien Houston, Texas (713) 238-2848 sobrien@mayerbrown.com IRS Audits and Global Controversy Issues May 4, 2017 Mayer Brown is a global

Demystifying the IRS Appeals Process Houston TEI Tax School Shawn O Brien Houston, Texas (713) 238-2848 sobrien@mayerbrown.com IRS Audits and Global Controversy Issues May 4, 2017 Mayer Brown is a global

Managing Tax Audits and Appeals September 29-30, 2016 Washington, DC

Managing Tax Audits and Appeals 2016 September 29-30, 2016 Washington, DC Tax Accounting Controversies & Developments Dwight Mersereau Resolving Accounting Method Issues General Background A taxpayer adopts

Managing Tax Audits and Appeals 2016 September 29-30, 2016 Washington, DC Tax Accounting Controversies & Developments Dwight Mersereau Resolving Accounting Method Issues General Background A taxpayer adopts

HOW THE 1998 TAX ACT AFFECTS YOUR DEALINGS WITH THE IRS APPEALS OFFICE. The IRS Restructuring and Reform Act of 1998.

HOW THE 1998 TAX ACT AFFECTS YOUR DEALINGS WITH THE IRS APPEALS OFFICE The IRS Restructuring and Reform Act of 1998 January 22, 1999 Robert M. Kane, Jr. LeSourd & Patten, P.S. 600 University Street, Ste

HOW THE 1998 TAX ACT AFFECTS YOUR DEALINGS WITH THE IRS APPEALS OFFICE The IRS Restructuring and Reform Act of 1998 January 22, 1999 Robert M. Kane, Jr. LeSourd & Patten, P.S. 600 University Street, Ste

What s News in Tax Analysis That Matters from Washington National Tax

What s News in Tax Analysis That Matters from Washington National Tax LB&I Updates Publication 5125 and the Internal Revenue Manual In February 2016, the IRS revised Publication 5125, which provides guidance

What s News in Tax Analysis That Matters from Washington National Tax LB&I Updates Publication 5125 and the Internal Revenue Manual In February 2016, the IRS revised Publication 5125, which provides guidance

Choosing Wisely: When to Use (or Not Use) Mediation to Obtain Cost Effective Closure in Exam & Collection Cases

Mediation to Obtain Cost Effective Closure in Exam & Collection Cases") Choosing Wisely: When to Use (or Not Use) Mediation to Obtain Cost Effective Closure in Exam & Collection Cases Maxine Aaronson Law Office of Maxine Aaronson 600 N. Pearl St. Suite 2170 Dallas, Texas 75201

Choosing Wisely: When to Use (or Not Use) Mediation to Obtain Cost Effective Closure in Exam & Collection Cases Maxine Aaronson Law Office of Maxine Aaronson 600 N. Pearl St. Suite 2170 Dallas, Texas 75201

IRS Audits and Appeals

ALGIERS AUSTIN DALLAS FORT WORTH HOUSTON LONDON MEXICO CITY MONTERREY NEW YORK PARIS RIO DE JANEIRO VITÓRIA IRS Audits and Appeals Tax Executives Institute March 21, 2006 Presented by Emily Parker emily.parker@tklaw.com

ALGIERS AUSTIN DALLAS FORT WORTH HOUSTON LONDON MEXICO CITY MONTERREY NEW YORK PARIS RIO DE JANEIRO VITÓRIA IRS Audits and Appeals Tax Executives Institute March 21, 2006 Presented by Emily Parker emily.parker@tklaw.com

Tax Executives Institute Detroit Chapter Meeting

Tax Executives Institute Detroit Chapter Meeting David Blair dblair@crowell.com 202. 624.2765 Jennifer Ray jray@crowell.com 202. 624.2589 February 16, 2017 Navigating LB&I s New Issue Focused Audit Process

Tax Executives Institute Detroit Chapter Meeting David Blair dblair@crowell.com 202. 624.2765 Jennifer Ray jray@crowell.com 202. 624.2589 February 16, 2017 Navigating LB&I s New Issue Focused Audit Process

JOSEPH ALI Director, Technical Guidance Internal Revenue Service- Appeals Joe Ali is the Director for Appeals Technical Guidance.

JOSEPH ALI Director, Technical Guidance Internal Revenue Service- Appeals Joe Ali is the Director for Appeals Technical Guidance. In this position, he is responsible for managing, and directing the Area

JOSEPH ALI Director, Technical Guidance Internal Revenue Service- Appeals Joe Ali is the Director for Appeals Technical Guidance. In this position, he is responsible for managing, and directing the Area

IRS Examination Developments for High Tech Firms

31 st Annual High Technology Tax Institute Sponsored by Tax Executives Institute, Inc. & San Jose State University College of Business November 9 & 10, 2015 IRS Examination Developments for High Tech Firms

31 st Annual High Technology Tax Institute Sponsored by Tax Executives Institute, Inc. & San Jose State University College of Business November 9 & 10, 2015 IRS Examination Developments for High Tech Firms

SECTION 5. SMALL CASE PROCEDURE FOR REQUESTING COMPETENT AUTHORITY ASSISTANCE.01 General.02 Small Case Standards.03 Small Case Filing Procedure

Rev. Proc. 2002 52 SECTION 1. PURPOSE OF THE REVENUE PROCEDURE SECTION 2. SCOPE.01 In General.02 Requests for Assistance.03 Authority of the U.S. Competent Authority.04 General Process.05 Failure to Request

Rev. Proc. 2002 52 SECTION 1. PURPOSE OF THE REVENUE PROCEDURE SECTION 2. SCOPE.01 In General.02 Requests for Assistance.03 Authority of the U.S. Competent Authority.04 General Process.05 Failure to Request

Compliance Assurance Process (CAP) Internal Revenue Manual (IRM) Sections

Internal Revenue Manual (IRM) Sections") Compliance Assurance Process (CAP) Internal Revenue Manual (IRM) Sections 4._.1.1 Introduction 4._.1.2 Overview of the Program (1) The Internal Revenue Service (IRS) initiated the Compliance Assurance

Compliance Assurance Process (CAP) Internal Revenue Manual (IRM) Sections 4._.1.1 Introduction 4._.1.2 Overview of the Program (1) The Internal Revenue Service (IRS) initiated the Compliance Assurance

11 - Court Rejects Taxpayer's Objections to IRS Collection Actions

11 - Court Rejects Taxpayer's Objections to IRS Collection Actions McAvey, TC Memo 2018-142 The Tax Court has held that IRS did not abuse its discretion with respect to various of its collection actions

11 - Court Rejects Taxpayer's Objections to IRS Collection Actions McAvey, TC Memo 2018-142 The Tax Court has held that IRS did not abuse its discretion with respect to various of its collection actions

Changes in IRS Exam and Appeals Procedures (and their impact on R&D Tax Credits)

") Changes in IRS Exam and Appeals Procedures (and their impact on R&D Tax Credits) Hosted by Bryan Auernig, Director Presented by Peter Mehta, Managing Director Tax Credit Co. September 22, 2015 Introductions

Changes in IRS Exam and Appeals Procedures (and their impact on R&D Tax Credits) Hosted by Bryan Auernig, Director Presented by Peter Mehta, Managing Director Tax Credit Co. September 22, 2015 Introductions

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS. PPC s Guide to Dealing with the IRS. Twenty-third Edition (June 2015)

") Route To: j Partners j Managers j Staff j File P.O. Box 115008 Carrollton, TX 75011-5008 Tel (972) 250-7750 (800) 431-9025 Fax (888) 216-1929 tax.thomsonreuters.com LIST OF SUBSTANTIVE CHANGES AND ADDITIONS

Route To: j Partners j Managers j Staff j File P.O. Box 115008 Carrollton, TX 75011-5008 Tel (972) 250-7750 (800) 431-9025 Fax (888) 216-1929 tax.thomsonreuters.com LIST OF SUBSTANTIVE CHANGES AND ADDITIONS

Strategies for Settling Tax Disputes

Strategies for Settling Tax Disputes Scott M. Stewart Partner, Chicago +1 312 701 7821 sstewart@mayerbrown.com John T. Hildy Partner, Chicago +1 312 701 7769 jhildy@mayerbrown.com Agenda Discuss our recent

Strategies for Settling Tax Disputes Scott M. Stewart Partner, Chicago +1 312 701 7821 sstewart@mayerbrown.com John T. Hildy Partner, Chicago +1 312 701 7769 jhildy@mayerbrown.com Agenda Discuss our recent

14 Tips To Help Deal With (Or Avoid) The IRS In 2014

The IRS In 2014") Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com 14 Tips To Help Deal With (Or Avoid) The IRS In 2014

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com 14 Tips To Help Deal With (Or Avoid) The IRS In 2014

25th Annual Health Sciences Tax Conference

25th Annual Health Sciences Tax Conference Current topics in IRS risk management and tax controversy December 7, 2015 Disclaimer EY refers to the global organization, and may refer to one or more, of the

25th Annual Health Sciences Tax Conference Current topics in IRS risk management and tax controversy December 7, 2015 Disclaimer EY refers to the global organization, and may refer to one or more, of the

Procedures for Protest to New York State and City Tribunals

September 25, 1997 Procedures for Protest to New York State and City Tribunals By: Glenn Newman This new feature of the New York Law Journal will highlight cases involving New York State and City tax controversies

September 25, 1997 Procedures for Protest to New York State and City Tribunals By: Glenn Newman This new feature of the New York Law Journal will highlight cases involving New York State and City tax controversies

New and Notable in IRS Controversy. Brian Paperny AT&T (Moderator) Mario Manniello Verizon Heather Maloy EY Kevin Brown PwC

Mario Manniello Verizon Heather Maloy EY Kevin Brown PwC") New and Notable in IRS Controversy Brian Paperny AT&T (Moderator) Mario Manniello Verizon Heather Maloy EY Kevin Brown PwC Disclaimer Views expressed in this presentation are those of the speakers and

New and Notable in IRS Controversy Brian Paperny AT&T (Moderator) Mario Manniello Verizon Heather Maloy EY Kevin Brown PwC Disclaimer Views expressed in this presentation are those of the speakers and

STATEMENT OF JENNIFER E. BREEN ON BEHALF OF THE AMERICAN BAR ASSOCIATION SECTION OF TAXATION BEFORE THE COMMITTEE ON SMALL BUSINESS OF THE

STATEMENT OF JENNIFER E. BREEN ON BEHALF OF THE AMERICAN BAR ASSOCIATION SECTION OF TAXATION BEFORE THE COMMITTEE ON SMALL BUSINESS OF THE UNITED STATES HOUSE OF REPRESENTATIVES FOR THE HEARING ON IRS

STATEMENT OF JENNIFER E. BREEN ON BEHALF OF THE AMERICAN BAR ASSOCIATION SECTION OF TAXATION BEFORE THE COMMITTEE ON SMALL BUSINESS OF THE UNITED STATES HOUSE OF REPRESENTATIVES FOR THE HEARING ON IRS

IRS Practice and Procedure as to the Collection of Payroll Taxes. Penalties and Interest

IRS Practice and Procedure as to the Collection of Payroll Taxes By: Kenneth B. Schwartz, Esq., CPA 500 North Broadway, Ste 124 Jericho, N.Y. 11754 Tel: 516-333-7020 www.schwartzattorney.com December 2,

IRS Practice and Procedure as to the Collection of Payroll Taxes By: Kenneth B. Schwartz, Esq., CPA 500 North Broadway, Ste 124 Jericho, N.Y. 11754 Tel: 516-333-7020 www.schwartzattorney.com December 2,

A Guide to Tax Resolution: Solving IRS Problems

A Guide to Tax Resolution: Solving IRS Problems 0 A Guide to Tax Resolution: Solving IRS Problems Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form

A Guide to Tax Resolution: Solving IRS Problems 0 A Guide to Tax Resolution: Solving IRS Problems Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form

Effective Management of IRS Information Document Requests (IDRs)

") Effective Management of IRS Information Document Requests (IDRs) George Hani, is the Chair of the Tax Department of Miller and Chevalier, Chartered. He concentrates his practice on the resolution of tax

Effective Management of IRS Information Document Requests (IDRs) George Hani, is the Chair of the Tax Department of Miller and Chevalier, Chartered. He concentrates his practice on the resolution of tax

SEC. 5. SMALL CASE PROCEDURE FOR REQUESTING COMPETENT AUTHORITY ASSISTANCE.01 General.02 Small Case Standards.03 Small Case Filing Procedure

26 CFR 601.201: Rulings and determination letters. Rev. Proc. 96 13 OUTLINE SECTION 1. PURPOSE OF MUTUAL AGREEMENT PROCESS SEC. 2. SCOPE Suspension.02 Requests for Assistance.03 U.S. Competent Authority.04

26 CFR 601.201: Rulings and determination letters. Rev. Proc. 96 13 OUTLINE SECTION 1. PURPOSE OF MUTUAL AGREEMENT PROCESS SEC. 2. SCOPE Suspension.02 Requests for Assistance.03 U.S. Competent Authority.04

IRS Wasn't Wrong to Reject Taxpayer Payment Plan that Didn't Pay Off Liability in Ten Years

IRS Wasn't Wrong to Reject Taxpayer Payment Plan that Didn't Pay Off Liability in Ten Years Brown, TC Memo 2016-82 The Tax Court has held that IRS was not wrong to reject, based on several failings by

IRS Wasn't Wrong to Reject Taxpayer Payment Plan that Didn't Pay Off Liability in Ten Years Brown, TC Memo 2016-82 The Tax Court has held that IRS was not wrong to reject, based on several failings by

ABA: Safe Harbor Parking Like-Kind Exchanges

ABA: Safe Harbor Parking Like-Kind Exchanges Robert D. Schachat and Glenn Johnson Ernst & Young LLP January 22, 2011 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst

ABA: Safe Harbor Parking Like-Kind Exchanges Robert D. Schachat and Glenn Johnson Ernst & Young LLP January 22, 2011 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst

Compliance Assurance Process (CAP) - Frequently Asked Questions (FAQs)

- Frequently Asked Questions (FAQs)") Compliance Assurance Process (CAP) - Frequently Asked Questions (FAQs) The Compliance Assurance Process (CAP) is a method of identifying and resolving tax issues through open, cooperative, and transparent

Compliance Assurance Process (CAP) - Frequently Asked Questions (FAQs) The Compliance Assurance Process (CAP) is a method of identifying and resolving tax issues through open, cooperative, and transparent

DEPARTMENT OF THE TREASURY. July 18, Susan L. Latham /s/ Susan L. Latham Director, Policy, Quality and Case Support

DEPARTMENT OF THE TREASURY I N T E R N A L R E V E N U E S E R V I C E W A S H I N G T O N, D. C. 2 0 2 2 4 July 18, 2013 MEMORANDUM FOR APPEALS EMPLOYEES Control No. AP-08-0713-03 Expiration Date: 07/18/2014

DEPARTMENT OF THE TREASURY I N T E R N A L R E V E N U E S E R V I C E W A S H I N G T O N, D. C. 2 0 2 2 4 July 18, 2013 MEMORANDUM FOR APPEALS EMPLOYEES Control No. AP-08-0713-03 Expiration Date: 07/18/2014

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS Route To: Partners PPC's Guide to Dealing with the IRS Managers. Twenty second Edition (June 2014)

") LIST OF SUBSTANTIVE CHANGES AND ADDITIONS Route To: Partners PPC's Guide to Dealing with the IRS Managers Staff File Twenty second Edition (June 2014) The following are some of the features of this year

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS Route To: Partners PPC's Guide to Dealing with the IRS Managers Staff File Twenty second Edition (June 2014) The following are some of the features of this year

IRS Large Business & International Division Issues Transfer Pricing Guidance

IRS Insights A closer look. In this issue: IRS Large Business & International Division Issues Transfer Pricing Guidance... 1 Organisation for Economic Co-operation and Development Launces ICAP... 3 The

IRS Insights A closer look. In this issue: IRS Large Business & International Division Issues Transfer Pricing Guidance... 1 Organisation for Economic Co-operation and Development Launces ICAP... 3 The

District Court Determines IRS Exceeded Regulatory Limit on FBAR Penalties

IRS Insights A closer look. In this issue: District Court Determines IRS Exceeded Regulatory Limit on FBAR Penalties... 1 Internal Revenue Service Issues Guidelines for IRS Chief Counsel on Supervisory

IRS Insights A closer look. In this issue: District Court Determines IRS Exceeded Regulatory Limit on FBAR Penalties... 1 Internal Revenue Service Issues Guidelines for IRS Chief Counsel on Supervisory

Table of Contents. About This Book How To Use This Book Foreword Acknowledgments Preface

Table of Contents About This Book How To Use This Book Foreword Acknowledgments Preface vii ix xi xiii xv Chapter 1 Initial Client Engagement 1 Topical Index 1 1.01 Nature of Federal Tax Law 5 1.02 Role

Table of Contents About This Book How To Use This Book Foreword Acknowledgments Preface vii ix xi xiii xv Chapter 1 Initial Client Engagement 1 Topical Index 1 1.01 Nature of Federal Tax Law 5 1.02 Role

IRS Policy Changes Impact R&D Credit IRS changes magnify the importance of methodology and documentation

IRS changes magnify the importance of methodology and documentation The new IDR enforcement policy and the Appeals Judicial Approach and Culture project have been in effect for over a year. Both policies

IRS changes magnify the importance of methodology and documentation The new IDR enforcement policy and the Appeals Judicial Approach and Culture project have been in effect for over a year. Both policies

Valuation in Tax: What Non- Attorneys Should Know About Litigating Valuation Cases

Valuation in Tax: What Non- Attorneys Should Know About Litigating Valuation Cases Lawrence A. Sannicandro, Esq. Agostino & Associates, P.C. 14 Washington Place Hackensack, NJ 07601 (201) 488-5400, x.

Valuation in Tax: What Non- Attorneys Should Know About Litigating Valuation Cases Lawrence A. Sannicandro, Esq. Agostino & Associates, P.C. 14 Washington Place Hackensack, NJ 07601 (201) 488-5400, x.

IRS Update: What s Happening Now

2 nd Annual CFMA Southwest Regional Conference San Diego, CA September 25-27, 2016 IRS Update: What s Happening Now Presented by: Kathy Petronchak KATHY PETRONCHAK Former IRS Commissioner of Small Business/Self

2 nd Annual CFMA Southwest Regional Conference San Diego, CA September 25-27, 2016 IRS Update: What s Happening Now Presented by: Kathy Petronchak KATHY PETRONCHAK Former IRS Commissioner of Small Business/Self

IRS PENALTIES. Avoidance and abatement. June 2017

IRS PENALTIES Avoidance and abatement June 2017 Today s presenters Patti Burquest Principal Washington National Tax Patti leads the firm s tax controversy team, with a focus on IRS examination and appeals.

IRS PENALTIES Avoidance and abatement June 2017 Today s presenters Patti Burquest Principal Washington National Tax Patti leads the firm s tax controversy team, with a focus on IRS examination and appeals.

Parliamentary Committee recommends fairer ATO processes and an independent Appeals area

TaxTalk Insights Tax Controversy & Dispute Resolution Parliamentary Committee recommends fairer ATO processes and an independent Appeals area 1 April 2015 In brief On 26 March 2015, the House of Representatives

TaxTalk Insights Tax Controversy & Dispute Resolution Parliamentary Committee recommends fairer ATO processes and an independent Appeals area 1 April 2015 In brief On 26 March 2015, the House of Representatives

Responding to Adverse IRS Audit Assessments: Audit Reconsideration Requests, IRS Appeals, and Settlement Strategies

Responding to Adverse IRS Audit Assessments: Audit Reconsideration Requests, IRS Appeals, and Settlement Strategies TUESDAY, MARCH 1, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved

Responding to Adverse IRS Audit Assessments: Audit Reconsideration Requests, IRS Appeals, and Settlement Strategies TUESDAY, MARCH 1, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS. PPC s Guide to Dealing with the IRS. Twenty-fourth Edition (June 2016)

") LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s Guide to Dealing with the IRS Twenty-fourth Edition (June 2016) The following are some of the features of this year s update of PPC s Guide to dealing with

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s Guide to Dealing with the IRS Twenty-fourth Edition (June 2016) The following are some of the features of this year s update of PPC s Guide to dealing with

The Code of Ethics for Arbitrators in Commercial Disputes Effective March 1, 2004

The Code of Ethics for Arbitrators in Commercial Disputes Effective March 1, 2004 The Code of Ethics for Arbitrators in Commercial Disputes was originally prepared in 1977 by a joint committee consisting

The Code of Ethics for Arbitrators in Commercial Disputes Effective March 1, 2004 The Code of Ethics for Arbitrators in Commercial Disputes was originally prepared in 1977 by a joint committee consisting

TABLE OF CONTENTS. .03 Farmers cooperatives. .01 A request made during the course of an examination

Rev. Proc. 2000 2 TABLE OF CONTENTS SECTION 1. WHAT IS THE p. 77 PURPOSE OF THIS REVENUE PROCEDURE? SECTION 2. WHAT IS p. 78 TECHNICAL ADVICE? SECTION 3. ON WHAT ISSUES p. 78 MAY TECHNICAL ADVICE BE REQUESTED

Rev. Proc. 2000 2 TABLE OF CONTENTS SECTION 1. WHAT IS THE p. 77 PURPOSE OF THIS REVENUE PROCEDURE? SECTION 2. WHAT IS p. 78 TECHNICAL ADVICE? SECTION 3. ON WHAT ISSUES p. 78 MAY TECHNICAL ADVICE BE REQUESTED

Hot Audit Issues: 1. Parallel Audits 2. Reopening Audits 3. IDR Enforcement and Summons

Hot Audit Issues: 1. Parallel Audits 2. Reopening Audits 3. IDR Enforcement and Summons Shelley Leonard Parallel Audits 2 Parallel Audits IRS may conduct multiple types of audits concurrently Corporate

Hot Audit Issues: 1. Parallel Audits 2. Reopening Audits 3. IDR Enforcement and Summons Shelley Leonard Parallel Audits 2 Parallel Audits IRS may conduct multiple types of audits concurrently Corporate

OSHA to Offer Alternative Dispute Resolution for Whistleblower Complaints

November 12, 2012 OSHA to Offer Alternative Dispute Resolution for Whistleblower Complaints Employers should evaluate whether new whistleblower complaints are eligible for the initiative, which provides

November 12, 2012 OSHA to Offer Alternative Dispute Resolution for Whistleblower Complaints Employers should evaluate whether new whistleblower complaints are eligible for the initiative, which provides

ALI-ABA Course of Study Sophisticated Estate Planning Techniques

397 ALI-ABA Course of Study Sophisticated Estate Planning Techniques Cosponsored by Massachusetts Continuing Legal Education, Inc. September 4-5, 2008 Boston, Massachusetts Planning for Private Equity

397 ALI-ABA Course of Study Sophisticated Estate Planning Techniques Cosponsored by Massachusetts Continuing Legal Education, Inc. September 4-5, 2008 Boston, Massachusetts Planning for Private Equity

Collection Due Process Hearing

263 Collection Due Process (CDP) Statutory Right A gift from the IRS Restructuring and Reform Act of 1998 1. Lien IRC 6320 2. Levy IRC 6330 263 264 Critical Issues of CDP Use it or lose it 30 days to REQUEST

263 Collection Due Process (CDP) Statutory Right A gift from the IRS Restructuring and Reform Act of 1998 1. Lien IRC 6320 2. Levy IRC 6330 263 264 Critical Issues of CDP Use it or lose it 30 days to REQUEST

AMERICAN BAR ASSOCIATION ADOPTED BY THE HOUSE OF DELEGATES August 11-12, 2003

AMERICAN BAR ASSOCIATION ADOPTED BY THE HOUSE OF DELEGATES August 11-12, 2003 RESOLVED, That the American Bar Association recommends the following reforms in the Medicare claims adjudication process to

AMERICAN BAR ASSOCIATION ADOPTED BY THE HOUSE OF DELEGATES August 11-12, 2003 RESOLVED, That the American Bar Association recommends the following reforms in the Medicare claims adjudication process to

Topical Index to Chapter 11 Penalties and Interest

Topical Index to Chapter 11 Penalties and Interest 11.01 Accuracy-related penalty 6662 Penalties grouped Negligence Substantial understatement of income tax Substantial valuation misstatement Substantial

Topical Index to Chapter 11 Penalties and Interest 11.01 Accuracy-related penalty 6662 Penalties grouped Negligence Substantial understatement of income tax Substantial valuation misstatement Substantial

IRS COLLECTION PROCEDURES AND TAXPAYER REMEDIES

IRS COLLECTION PROCEDURES AND TAXPAYER REMEDIES By: Daniel J. Cramer Cramer, Minock & Sweeney, PLC The IRS has broad powers to enforce tax laws and collect outstanding taxes. The most common IRS collection

IRS COLLECTION PROCEDURES AND TAXPAYER REMEDIES By: Daniel J. Cramer Cramer, Minock & Sweeney, PLC The IRS has broad powers to enforce tax laws and collect outstanding taxes. The most common IRS collection

Effectively Representing the Taxpayer in a Substantiation and Penalty Case. US Tax Court Judicial Conference Tuesday March 27, 2018

Effectively Representing the Taxpayer in a Substantiation and Penalty Case US Tax Court Judicial Conference Tuesday March 27, 2018 Substantiation of Income/gross receipts and Expenses- generally Self-employed

Effectively Representing the Taxpayer in a Substantiation and Penalty Case US Tax Court Judicial Conference Tuesday March 27, 2018 Substantiation of Income/gross receipts and Expenses- generally Self-employed

Intermediate Sanctions (IRC 4958) Update. By Lawrence M. Brauer and Leonard J. Henzke

Update. By Lawrence M. Brauer and Leonard J. Henzke") Intermediate Sanctions (IRC 4958) Update By Lawrence M. Brauer and Leonard J. Henzke Intermediate Sanctions (IRC 4958) Update By Lawrence M. Brauer and Leonard J. Henzke Overview Purpose This article

Intermediate Sanctions (IRC 4958) Update By Lawrence M. Brauer and Leonard J. Henzke Intermediate Sanctions (IRC 4958) Update By Lawrence M. Brauer and Leonard J. Henzke Overview Purpose This article

ROCKY MOUNTAIN TAX SEMINAR FOR PRIVATE FOUNDATIONS WHAT SHOULD WE EXPECT NOW FROM THE IRS?

ROCKY MOUNTAIN TAX SEMINAR FOR PRIVATE FOUNDATIONS September 16-18, 2015 Colorado Springs, Colorado WHAT SHOULD WE EXPECT NOW FROM THE IRS? by Celia Roady Morgan, Lewis & Bockius LLP 1111 Pennsylvania

ROCKY MOUNTAIN TAX SEMINAR FOR PRIVATE FOUNDATIONS September 16-18, 2015 Colorado Springs, Colorado WHAT SHOULD WE EXPECT NOW FROM THE IRS? by Celia Roady Morgan, Lewis & Bockius LLP 1111 Pennsylvania

ALI-ABA Course of Study How To Handle a Tax Controversy at the IRS and in Court: From Administrative Audit Through Litigation

157 ALI-ABA Course of Study How To Handle a Tax Controversy at the IRS and in Court: From Administrative Audit Through Litigation Sponsored with the cooperation of the ABA Section of Taxation June 24-25,

157 ALI-ABA Course of Study How To Handle a Tax Controversy at the IRS and in Court: From Administrative Audit Through Litigation Sponsored with the cooperation of the ABA Section of Taxation June 24-25,

The Family Limited Partnership:

The Family Limited Partnership: Forming, Funding, and Defending John F. Ramsbacher John W. Prokey Erin M. Wilms FLPs refuse to die. You can increase their longevity with careful planning. THE FAMILY LIMITED

The Family Limited Partnership: Forming, Funding, and Defending John F. Ramsbacher John W. Prokey Erin M. Wilms FLPs refuse to die. You can increase their longevity with careful planning. THE FAMILY LIMITED

24 th Annual Health Sciences Tax Conference

24 th Annual Health Sciences Tax Conference December 8, 2014 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of

24 th Annual Health Sciences Tax Conference December 8, 2014 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of

IRS REFUNDS DOES YOUR COMPANY HAVE ONE COMING?

IRS REFUNDS DOES YOUR COMPANY HAVE ONE COMING? Feb. 24, 2016 0 1 2016 RSM US LLP. All Rights Reserved. Today s speakers Patti Burquest Principal Leads the IRS Controversy practice within RSM s Washington

IRS REFUNDS DOES YOUR COMPANY HAVE ONE COMING? Feb. 24, 2016 0 1 2016 RSM US LLP. All Rights Reserved. Today s speakers Patti Burquest Principal Leads the IRS Controversy practice within RSM s Washington

Article from: Taxing Times. February 2010 Volume 6, Issue 1

Article from: Taxing Times February 2010 Volume 6, Issue 1 CHANGE IN BASIS OF COMPUTING RESERVES IS IT OR ISN T IT? By Peter H. Winslow and Lori J. Jones High on the list of the most frequently asked questions

Article from: Taxing Times February 2010 Volume 6, Issue 1 CHANGE IN BASIS OF COMPUTING RESERVES IS IT OR ISN T IT? By Peter H. Winslow and Lori J. Jones High on the list of the most frequently asked questions

Taxpayer Testimony as Credible Evidence

Author: Raby, Burgess J.W.; Raby, William L., Tax Analysts Taxpayer Testimony as Credible Evidence When section 7491, which shifts the burden of proof to the IRS for some taxpayers, was added to the tax

Author: Raby, Burgess J.W.; Raby, William L., Tax Analysts Taxpayer Testimony as Credible Evidence When section 7491, which shifts the burden of proof to the IRS for some taxpayers, was added to the tax

Law Office of W. Mark Scott, PLLC

The Resurgence of Whistleblowers in IRS Bond Enforcement By: W. Mark Scott I. THERE AND BACK AGAIN The IRS Office of Tax Exempt Bonds received a significant number of whistleblower tips during my tenure

The Resurgence of Whistleblowers in IRS Bond Enforcement By: W. Mark Scott I. THERE AND BACK AGAIN The IRS Office of Tax Exempt Bonds received a significant number of whistleblower tips during my tenure

Rev. Proc I.R.B. 678 April 1, 2002

26 CFR 601.105: Examination of returns and claims for refund, credit, or abatement; determination of correct tax liability. (Also Part 1, 446, 481; 1.446 1, 1.481 1) Rev. Proc. 2002 18 SECTION 1. PURPOSE...680.01

26 CFR 601.105: Examination of returns and claims for refund, credit, or abatement; determination of correct tax liability. (Also Part 1, 446, 481; 1.446 1, 1.481 1) Rev. Proc. 2002 18 SECTION 1. PURPOSE...680.01

Federal Income Tax Examinations of Pass-Through Entities

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 2006 Federal Income Tax Examinations of Pass-Through

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 2006 Federal Income Tax Examinations of Pass-Through

135 T.C. No. 4 UNITED STATES TAX COURT. WILLIAM PRENTICE COOPER, III, Petitioner v. COMMISSIONER OF INTERNAL REVENUE, Respondent

135 T.C. No. 4 UNITED STATES TAX COURT WILLIAM PRENTICE COOPER, III, Petitioner v. COMMISSIONER OF INTERNAL REVENUE, Respondent Docket Nos. 24178-09W, 24179-09W. Filed July 8, 2010. P filed two claims

135 T.C. No. 4 UNITED STATES TAX COURT WILLIAM PRENTICE COOPER, III, Petitioner v. COMMISSIONER OF INTERNAL REVENUE, Respondent Docket Nos. 24178-09W, 24179-09W. Filed July 8, 2010. P filed two claims

UILC: , , , , , ,

Office of Chief Counsel Internal Revenue Service Memorandum Number: 200503031 Release Date: 01/21/2005 CC:PA:APJP:B02 ------------ SCAF-119247-04 UILC: 6702.00-00, 6702.01-00, 6611.09-00, 6501.05-00, 6501.05-07,

Office of Chief Counsel Internal Revenue Service Memorandum Number: 200503031 Release Date: 01/21/2005 CC:PA:APJP:B02 ------------ SCAF-119247-04 UILC: 6702.00-00, 6702.01-00, 6611.09-00, 6501.05-00, 6501.05-07,

How To Represent A Taxpayer Before The IRS Office Of Appeals

How To Represent A Taxpayer Before The IRS Office Of Appeals October 3, 2017 6:00 PM 9:00 PM RSVP: http://conta.cc/2iwivlv Bergen Community College Ciarco Learning Center 355 Main Street Room, 102/103

How To Represent A Taxpayer Before The IRS Office Of Appeals October 3, 2017 6:00 PM 9:00 PM RSVP: http://conta.cc/2iwivlv Bergen Community College Ciarco Learning Center 355 Main Street Room, 102/103

Revenue Procedure 97-27

CLICK HERE to return to the home page Revenue Procedure 97-27 TABLE OF CONTENTS SECTION 1. PURPOSE.01 In general.02 Voluntary compliance.03 Significant changes SECTION 2. BACKGROUND.01 Change in method

CLICK HERE to return to the home page Revenue Procedure 97-27 TABLE OF CONTENTS SECTION 1. PURPOSE.01 In general.02 Voluntary compliance.03 Significant changes SECTION 2. BACKGROUND.01 Change in method

(4) Before afederal court. 14

Before afederal court. 14") 26 CFR 601.204: Changes in accounting periods and in methods of accounting. (Also Part I, 446, 481; 1.446 1, 1.481 1, 1.481 4.) Rev. Proc. 97 27 TABLE OF CONTENTS PAGE SECTION 1. PURPOSE... 11.01 In general...

26 CFR 601.204: Changes in accounting periods and in methods of accounting. (Also Part I, 446, 481; 1.446 1, 1.481 1, 1.481 4.) Rev. Proc. 97 27 TABLE OF CONTENTS PAGE SECTION 1. PURPOSE... 11.01 In general...

IRS Provides Guidance on FBAR Penalties

Page 1 of 5 The Tax Adviser IRS Provides Guidance on FBAR Penalties Updated procedures on penalties imposed for failing to file the Report of Foreign Bank and Financial Accounts provide consistency and

Page 1 of 5 The Tax Adviser IRS Provides Guidance on FBAR Penalties Updated procedures on penalties imposed for failing to file the Report of Foreign Bank and Financial Accounts provide consistency and

Inside the Compliance Assurance Process (CAP) Program: Is it Right for Your Clients?

Program: Is it Right for Your Clients?") Inside the Compliance Assurance Process (CAP) Program: Is it Right for Your Clients? Administrative Practice Committee ABA Tax Section October 21, 2011 Denver, Colorado Panel Participants Corina Trainer,

Inside the Compliance Assurance Process (CAP) Program: Is it Right for Your Clients? Administrative Practice Committee ABA Tax Section October 21, 2011 Denver, Colorado Panel Participants Corina Trainer,

Misclassification of Employees And Section 530 Relief

taxnotes Misclassification of Employees And Section 530 Relief By Phyllis Horn Epstein Reprinted from Tax Notes, March 13, 2017, p. 1411 Volume 154, Number 11 March 13, 2017 (C) Tax Analysts 2016. All

taxnotes Misclassification of Employees And Section 530 Relief By Phyllis Horn Epstein Reprinted from Tax Notes, March 13, 2017, p. 1411 Volume 154, Number 11 March 13, 2017 (C) Tax Analysts 2016. All

THE IRS NEW 2014 OFFSHORE VOLUNTARY DISCLOSURE PROCEDURES ANALYZED IN THE NEW OFFSHORE ENFORCEMENT ENVIRONMENT

THE IRS NEW 2014 OFFSHORE VOLUNTARY DISCLOSURE PROCEDURES ANALYZED IN THE NEW OFFSHORE ENFORCEMENT ENVIRONMENT Part II: THE STREAMLINED FILLING COMPLIANCE PROCEDURES On June 18, 2014, the Internal Revenue

THE IRS NEW 2014 OFFSHORE VOLUNTARY DISCLOSURE PROCEDURES ANALYZED IN THE NEW OFFSHORE ENFORCEMENT ENVIRONMENT Part II: THE STREAMLINED FILLING COMPLIANCE PROCEDURES On June 18, 2014, the Internal Revenue

The Internal Revenue Service is aware that certain promoters are advising

Part I Income Taxes Meritless Filing Position Based on Sections 932(c) and 934(b) Notice 2004-45 The Internal Revenue Service is aware that certain promoters are advising taxpayers to take highly questionable,

Part I Income Taxes Meritless Filing Position Based on Sections 932(c) and 934(b) Notice 2004-45 The Internal Revenue Service is aware that certain promoters are advising taxpayers to take highly questionable,

Prepared Remarks of William J. Wilkins, IRS Chief Counsel Federal Bar Association Tax Section March 5, 2010

Prepared Remarks of William J. Wilkins, IRS Chief Counsel Federal Bar Association Tax Section March 5, 2010 It s a pleasure to address this group. I think most of us count ourselves as fortunate to have

Prepared Remarks of William J. Wilkins, IRS Chief Counsel Federal Bar Association Tax Section March 5, 2010 It s a pleasure to address this group. I think most of us count ourselves as fortunate to have

IRS PUBLICATION 5091 BOND COMPLIANCE PRIMER 2016

IRS PUBLICATION 5091 BOND COMPLIANCE PRIMER 2016 Primer Objective: On behalf of ACS, thank you for your interest in obtaining additional information surrounding the post-issuance bond compliance requirements

IRS PUBLICATION 5091 BOND COMPLIANCE PRIMER 2016 Primer Objective: On behalf of ACS, thank you for your interest in obtaining additional information surrounding the post-issuance bond compliance requirements

APPEAL AND INDEPENDENT DISPUTE RESOLUTION PROCESSES

APPEAL AND INDEPENDENT DISPUTE RESOLUTION PROCESSES 2016 Fannie Mae. Trademarks of Fannie Mae. 8.17.2016 1 of 20 Contents INTRODUCTION... 4 PART A. APPEAL, IMPASSE, AND MANAGEMENT ESCALATION PROCESSES...

APPEAL AND INDEPENDENT DISPUTE RESOLUTION PROCESSES 2016 Fannie Mae. Trademarks of Fannie Mae. 8.17.2016 1 of 20 Contents INTRODUCTION... 4 PART A. APPEAL, IMPASSE, AND MANAGEMENT ESCALATION PROCESSES...

Updates on U.S. Transfer Pricing

Updates on U.S. Transfer Pricing John Hinman, Assistant to Director, Transfer Pricing Operations John Hughes, Senior International Advisor, Transfer Pricing Operations Crowell & Moring LLP Tax Seminar

Updates on U.S. Transfer Pricing John Hinman, Assistant to Director, Transfer Pricing Operations John Hughes, Senior International Advisor, Transfer Pricing Operations Crowell & Moring LLP Tax Seminar

UNITED STATES TAX COURT WASHINGTON, DC ORDER AND ORDER OF DISMISSAL FOR LACK OF JURISDICTION

24 RS UNITED STATES TAX COURT WASHINGTON, DC 20217 JOHN M. CRIM, Petitioner(s, v. Docket No. 1638-15 COMMISSIONER OF INTERNAL REVENUE, Respondent. ORDER AND ORDER OF DISMISSAL FOR LACK OF JURISDICTION

24 RS UNITED STATES TAX COURT WASHINGTON, DC 20217 JOHN M. CRIM, Petitioner(s, v. Docket No. 1638-15 COMMISSIONER OF INTERNAL REVENUE, Respondent. ORDER AND ORDER OF DISMISSAL FOR LACK OF JURISDICTION

IRS Controversies at Audit and Beyond

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1990 IRS Controversies at Audit and Beyond Charles

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1990 IRS Controversies at Audit and Beyond Charles

RETURN PREPARER PENALTIES UNDER TITLE 26

RETURN PREPARER PENALTIES UNDER TITLE 26 Bio Garrett Gregory Received JD from South Texas College of Law in 1999 Member of the Texas State Bar as of 1999 Received Master of Laws (Taxation) from Boston

RETURN PREPARER PENALTIES UNDER TITLE 26 Bio Garrett Gregory Received JD from South Texas College of Law in 1999 Member of the Texas State Bar as of 1999 Received Master of Laws (Taxation) from Boston

RE: Agency Fee For Fiscal Year Beginning July 1, 2008

TO: FROM: All Pilots Employed By American Airlines, Inc. Captain Bill Haug Secretary Treasurer, Allied Pilots Association RE: Agency Fee For Fiscal Year Beginning July 1, 2008 DATE: May 27, 2008 Pilots

TO: FROM: All Pilots Employed By American Airlines, Inc. Captain Bill Haug Secretary Treasurer, Allied Pilots Association RE: Agency Fee For Fiscal Year Beginning July 1, 2008 DATE: May 27, 2008 Pilots

BEST PRACTICES IN INTERNATIONAL ARBITRATION. Summary of Contents

BEST PRACTICES IN INTERNATIONAL ARBITRATION Summary of Contents The NAFTA 2022 Committee... 2 ADR in the NAFTA Region... 2 Guide to Private Sector Dispute Resolution in the NAFTA Region... 2 I. Methods/Forms

BEST PRACTICES IN INTERNATIONAL ARBITRATION Summary of Contents The NAFTA 2022 Committee... 2 ADR in the NAFTA Region... 2 Guide to Private Sector Dispute Resolution in the NAFTA Region... 2 I. Methods/Forms

CHAPTER 2: WORKING WITH THE TAX LAW

DOWNLOAD FULL TEST BANK FOR SOUTH WESTERN FEDERAL TAXATION 2015 INDIVIDUAL INCOME TAXES 38TH EDITION BY HOFFMAN AND SMITH Link download full: https://testbankservice.com/download/test-bank-for-south-western-federaltaxation-2015-individual-income-taxes-38th-edition-by-hoffman-and-smith/

DOWNLOAD FULL TEST BANK FOR SOUTH WESTERN FEDERAL TAXATION 2015 INDIVIDUAL INCOME TAXES 38TH EDITION BY HOFFMAN AND SMITH Link download full: https://testbankservice.com/download/test-bank-for-south-western-federaltaxation-2015-individual-income-taxes-38th-edition-by-hoffman-and-smith/

Internal Revenue Service Alternative Dispute Resolution Techniques

Internal Revenue Service Alternative Dispute Resolution Techniques May 2016 Boston Brussels Chicago Dallas Düsseldorf Frankfurt Houston London Los Angeles Miami Milan Munich New York Orange County Paris

Internal Revenue Service Alternative Dispute Resolution Techniques May 2016 Boston Brussels Chicago Dallas Düsseldorf Frankfurt Houston London Los Angeles Miami Milan Munich New York Orange County Paris

US Taxpayer Bill of Rights. Presentation of Nina E. Olson National Taxpayer Advocate 08 May 2017

US Taxpayer Bill of Rights Presentation of Nina E. Olson National Taxpayer Advocate 08 May 2017 Internal Revenue Code 7803(a) In discharging his duties, the Commissioner shall ensure that employees of

US Taxpayer Bill of Rights Presentation of Nina E. Olson National Taxpayer Advocate 08 May 2017 Internal Revenue Code 7803(a) In discharging his duties, the Commissioner shall ensure that employees of

Accounting Method Changes Current and Future State. American Bar Association Section of Taxation Tax Accounting Committee January 21, 2011

Accounting Method Changes Current and Future State American Bar Association Section of Taxation Tax Accounting Committee January 21, 2011 George Blaine Associate Chief Counsel (Income Tax & Accounting)

Accounting Method Changes Current and Future State American Bar Association Section of Taxation Tax Accounting Committee January 21, 2011 George Blaine Associate Chief Counsel (Income Tax & Accounting)

Is a Horse not a Horse When Entities Incur Investment Advisory Fees?

Is a Horse not a Horse When Entities Incur Investment Advisory Fees? Lou Harrison John Janiga Deductions under Section 67 for Investment Expeneses A colleague of mine, John Janiga, of the School of Business

Is a Horse not a Horse When Entities Incur Investment Advisory Fees? Lou Harrison John Janiga Deductions under Section 67 for Investment Expeneses A colleague of mine, John Janiga, of the School of Business