International evidence of tax smoothing in a panel of industrial countries

|

|

|

- Maria Flynn

- 5 years ago

- Views:

Transcription

1 Strazicich, M.C. (2002). International Evidence of Tax Smoothing in a Panel of Industrial Countries. Applied Economics, 34(18): (Dec 2002). Published by Taylor & Francis (ISSN: ). DOI: / International evidence of tax smoothing in a panel of industrial countries Mark C. Strazicich ABSTRACT A panel of industrial countries is examined for evidence of `tax smoothing. Tax smoothing results when governments minimize tax distortions over time. The model provides a positive theory of government debt and is due primarily to Barro. Unit root tests are performed in panel data to test the null hypothesis of nonstationary tax rates. Panel regressions are then undertaken to test the null hypothesis that tax rate changes are unpredictable and test for evidence of an alternative hypothesis. Political and economic variables are examined for their ability to predict tax rate changes. Overall, the results cannot reject the null hypotheses and support tax smoothing by national governments.

2 I. INTRODUCTION The goal of this paper is to contribute towards understanding the behaviour of government debt. Tax smoothing results when governments `smooth tax rates to minimize the costs of taxation over time. If the marginal costs of taxation are an increasing function of the amount of resources taxed, given a long-run balanced budget constraint, then minimization of the total costs of taxation implies that the planned tax rate will be constant over time. Changes in the tax rate will be unpredictable and the tax rate will behave as a random walk. Temporary deviations in government spending and output from their permanent levels will result in a deficit or surplus, but no change in the tax rate. The model provides a positive theory of government debt and is due primarily to Barro (1979). This study examines two implications of the tax smoothing model. First, the random walk implication predicts that the tax rate will be a nonstationary time series with a unit root. Second, tax smoothing implies that tax rate changes will be unpredictable. Therefore, lagged information should not be useful in predicting tax rate changes. These implications are examined by testing the null hypotheses that the tax rate has a unit root and that tax rate changes are orthogonal to lagged information. To address some recent criticisms that political factors might prevent tax smoothing, political variables are included in the lagged information set. Significant lagged information could also provide evidence of an alternative hypothesis. Testing is undertaken in panels created by pooling time series from 19 industrial countries. The use of panel data significantly increases the power of the tests to reject their null hypotheses. Annual central government data is examined for the period 1955±1988. Overall, the results cannot reject the null hypotheses and support tax smoothing by national governments. Section II discusses the theory of tax smoothing and reviews some of the literature. Section III describes the model. Section IV discusses the data. Section V presents the empirical results. Section VI summarizes and concludes. II. BACKGROUND Tax smoothing implies that governments set tax rates so as to minimize the cost of intertemporal tax distortions. Given the information available today, the tax rate would be considered

3 as permanent and would be changed only with new information about future government spending and output. No prediction could be made of tax rate changes and the tax rate would behave as a random walk. Empirical testing of the tax smoothing theory has focused on single country tests. See, for example, Barro (1981, 1986), Sahasakul (1986), Kochin et al. (1986), Trehan and Walsh (1988), Bizer and Durlauf (1990, 1991), Gupta (1992), Huang and Lin (1993) and Strazicich (1997). Results of these tests have been mixed. Barro, Kochin et al., Huang and Lin, and Strazicich find general support for tax smoothing when examining US federal tax rates. Gupta finds evidence of tax smoothing when examining Canadian federal tax rates. Contrary to this, Sahasakul and Bizer and Durlauf reject tax smoothing when examining US federal tax rates. Trehan and Walsh reject tax smoothing when examining US federal tax revenues. These tests examine either the time series properties of the data or test regression models derived from tax smoothing. One exception to performing single country tests is Roubini and Sachs (1989). Using a reduced form model of the deficit derived from tax smoothing; Roubini and Sachs test a panel of 14 OECD countries for evidence of tax smoothing. General government deficits are regressed on a number of variables suggested by tax smoothing. They include a measure of political influence that, if significant, may be unfavourable to tax smoothing. Roubini and Sachs find budget deficits to be significantly affected by political factors, especially since 1975, and reject tax smoothing. They suggest that political factors, in particular the cohesion of national governments, significantly affect the budget making process to the detriment of tax smoothing. For example, a weakly cohesive government might ignore such forward looking costs as intertemporal tax distortions. In separate single country tests they regress the first differenced tax rate on a constant term. They reject tax smoothing after finding a significant constant term, or `drift, for most countries. A number of issues can be raised regarding the testing methodology employed by Roubini and Sachs. One potential problem with their methodology is its reliance on correctly specifying a particular reduced-form model. If the model tested is not correctly specified, then biased estimates may result. The authors describe a model where the budget deficit is a function of last year s deficit, the change in unemployment, the change in output growth, the change in the rate of real interest minus the rate of

4 growth of output multiplied by the lagged debt-to-gdp ratio, and a political cohesion variable. Tax smoothing hypothesizes that temporary changes in government spending will be financed by changes in the government s budget balance but with no change in the tax rate. Roubini and Sachs use changes in unemployment and GDP growth to account for temporary changes in the ratio of government spending to GDP. While correct in principle, a more direct measure of temporary government spending to output is not included. As such, their results may be sensitive to their measure of temporary government spending to output. Bias regression coeficients will result if changes in unemployment and GDP growth do not accurately measure the ratio of temporary government spending to output. The model tested by Sahasakul is subject to this same potential criticism. Contrary to this, the methodology employed in this paper does not depend on accurately specifying a particular reduced-form model. A second potential problem with the approach in Roubini and Sachs relates to their use of general government data. Benjamin and Kochin (1978, 1982) suggest that resource mobility may constrain state and local governments from smoothing tax rates. As deficits and surpluses occur, mobile resources would be encouraged to seek out taxable jurisdictions where current government spending exceeds current taxes and vice versa. Therefore, the ability of state and local governments to smooth tax rates would be diminished. Resource mobility predicts that state and local governments will balance budgets and not smooth tax rates. Strazicich (1996, 1997) presents evidence from the USA and Canada in support of this argument. Thus, inclusion of revenue from all levels of government in the tax rate measure tested by Roubini and Sachs could bias results in favour of rejecting tax smoothing. The final issue deals with the assumption by Roubini and Sachs that a drift in tax rates rejects tax smoothing. If the marginal cost function of the tax rate was decreasing over time, tax smoothing would predict an upward drift in the tax rate. Therefore, finding a significant drift in tax rates is not sufficient to reject tax smoothing. 1 III. THE MODEL The tax smoothing model, in panel data, assumes a government budget identity for country i at period t as follows: (1)

5 where G it is real total government expenditures excluding interest on the national debt, B it is the real stock of national debt outstanding at the end of period t, T it is real tax revenue, and r it is the real rate of interest. Dividing terms in Equation 1 by Y it (real output of country i), an intertemporal budget constraint can be expressed as follows: According to Equation 3, only the ratio of permanent government spending to output and the ratio of previously outstanding debt to output determine the tax rate at time t. For example, a temporary increase in g it would be primarily financed by debt, since any increase in g it would be less than the current increase in g it. The tax rate

6 would rise by less than the current increase in g it, implying a `smoothing of tax rates over time. Thus, tax smoothing provides a theory of government debt: deficits arise when government spending is temporarily high or when output is temporarily low. IV. DATA Panel data on the average tax rate series (½it) will be examined for the period 1955± The average tax rate for each of 19 countries is calculated as annual central government revenue divided by annual Gross Domestic Product (GDP). The countries examined are the USA, Canada, Australia, Japan, New Zealand, Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, the Netherlands, Norway, Sweden, Switzerland, and the UK. Data comes from various editions of the International Financial Statistics Yearbook published by the International Monetary Fund.3 Tests for significant lagged information employ four lagged values each of the tax rate, the ratio of government expenditures to output, the growth of real GDP and a measure of the national government s political cohesion or unity denoted as pol it. An additional term representing pol it since 1975 is also examined and is denoted as poldit.4 As in Roubini and Sachs, pold it is used to test the null hypothesis that political cohesiveness of national governments gained importance in the budget making process after Annual data on government expenditure and real GDP is available since 1960 and comes from various

7 editions of the International Financial Statistics Yearbook. The political cohesion measure is taken from Roubini and Sachs and is available for 14 countries over the period 1960± The measure is a number from zero to three, determined by factors such as whether a parliamentary government has a majority or a presidential government has diff erent political parties controlling the executive and legislative branches. A value of zero indicates the most cohesive government and a value of three the least cohesive. See the Data Appendix for additional discussion of the data. V. EMPIRICAL TESTS Unit root tests

8 Therefore, under the null hypothesis of a unit root tax smoothing is supported in all countries, while under the

at the 5% level of significance.")

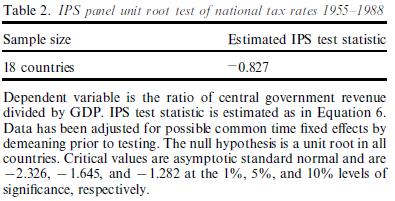

9 alternative hypothesis tax smoothing is rejected in one or more countries. Single equation unit root test results are reported in Table 1. The single equation tests reject the unit root null hypothesis only in one country (Finland) at the 5% level of significance. To determine if inability to reject the unit root null in more than one country is due to low power, the panel unit root test is undertaken using all countries except Finland. The results are reported in Table 2. The IPS panel test statistic of 0:827 cannot reject the unit root null at any of the usual significance levels. Overall, the findings in Table 1 and 2 support tax smoothing by national governments.

10 Regression tests of lagged information

11 VI. CONCLUSIONS National government tax rates were examined in 19 industrial countries for evidence of tax smoothing. If governments set tax rates to minimize distortions over time, the tax rate will be a nonstationary time series with a unit root and tax rate changes will be unpredictable. The null hypothesis was first examined by testing for a unit root in each country. The null of tax smoothing was rejected in only one country (i.e. Finland). To increase power, testing was undertaken in panel data utilizing time series from all countries except Finland. In spite of greater power, the panel test results could not reject the null hypothesis of a unit root in national tax rates. Panel regression tests were then undertaken to examine the null hypothesis that tax rate changes are unpredictable from past information and look for evidence of an alternative hypothesis. Results were unable to reject the null hypothesis that tax rate changes are unpredictable. Political variables were not significant in any case. Overall, the empirical findings presented in this paper provide support for tax smoothing as a theory of national government debt.

12 ACKNOWLEDGEMENTS The author thanks Levis Kochin and Paul Evans for helpful comments. REFERENCES Barro, R. J. (1979) On the determination of the public debt, Journal of Political Economy, 87, 940±71. Barro, R. J. (1981) On the predictability of tax-rate changes. Unpublished manuscript, University of Rochester, Rochester, New York. Barro, R. J. (1986) US deficits since World War I, Scandinavian Journal of Economics, 88, 195±222. Benjamin, D. K. and Kochin, L. A. (1978) A theory of state and local government debt. Unpublished manuscript, Department of Economics, University of Washington, Seattle, Washington. Benjamin, D. K. and Kochin, L. A. (1982) A proposition on windfalls and taxes when some but not all resources are mobile, Economic Inquiry, 20, 393±404. Bizer, D. S. and Durlauf, S. N. (1990) Testing the positive theory of government finance, Journal of Monetary Economics, 26, 123±41. Bizer, D. S. and Durlauf, S. N. (1991) Erratum, Journal of Monetary Economics, 27, 149. Evans, P. and Karras, G. (1991) Are government activities productive? Evidence from a panel of US states. Working paper, Department of Economics, The Ohio State University, Columbus, Ohio. Gupta, K. (1992) Optimal taxation policy: Evidence from Canada, Public Finance, 47, 193±200. de Haan, J. and Sturm, J. E. (1997) Political and economic determinants of OECD budget deficits and government expenditures: A reinvestigation, European Journal of Political Economy, 13, 739±50. Huang, C. and Lin, K. (1993) Deficits, government expenditures, and tax smoothing in the United States: 1929±1988, Journal of Monetary Economics, 31, 317±39.

13 Im, K., Pesaran, M. and Shin, Y. (1997) Testing for unit roots in heterogeneous panels. Working paper, University of Cambridge. Kochin, L. A., Benjamin, D. K. and Meador, M. (1986) The observational equivalence of rational and irrational consumers if taxation is efficient, in West Coast Federal Reserve/ Academic Conference 1985, San Francisco: Federal Reserve Bank of San Francisco. MacKinnon, J. G. (1991) Critical values for cointegration tests, in Long-run Economic Relationships: Readings in Cointegration, edited by R. F. Engle and C. W. J. Granger, Oxford University Press, Chapter 13. Ng, S. and Perron, P. (1995) Unit root tests in ARMA models with data-dependent methods for the selection of the truncation lag, Journal of the American Statistical Association, 90, 269±81. Perron, P. (1989) The great crash, the oil price shock, and the unit root hypothesis, Econometrica, 57, 1361±401. Roubini, N. and Sachs, J. D. (1989) Political and economic determinants of budget deficits in the industrial democracies, European Economic Review, 33, 903±38. Sahasakul, C. (1986) The US evidence on optimal taxation over time, Journal of Monetary Economics, 18, 251±75. Strazicich, M. C. (1996) Are state and provincial governments tax smoothing? Evidence from panel data, Southern Economic Journal, 62, 979±88. Strazicich, M. C. (1997) Does tax smoothing dffer by the level of government? Time series evidence from Canada and the United States, Journal of Macroeconomics, 19, 305±26. Trehan, B. and Walsh, C. (1988) Common trends, the government s budget constraint, and revenue smoothing, Journal of Economic Dynamics and Control, 12, 425±44.

14 APPENDIX Revenue of the Central Government, Expenditures of the Central Government, Gross Domestic Product, and Real Gross Domestic Product: International Financial Statistics Yearbook, International Monetary Fund, Washington, DC. 1955±59, 1981 edition; 1960±62, 1990 edition; 1963± 1988, 1993 edition. Political cohesion estimates come from Roubini and Sachs (1989). In some countries, government revenues and expenditures are measured for the fiscal year (FY), while GDP is measured for the calendar year (CY). Therefore, when revenues and expenditures for country i are originally shown for the fiscal year they are converted into the calendar year as follows: (1a) where 0 < λ < 1. New Zealand s GDP was also shown for the fiscal year and was, therefore, converted to the calendar year. Equation 1a is similar to (3.1) in Evans and Karras (1991).

Are State and Provincial Governments Tax Smoothing? Evidence from Panel Data*

Are State and Provincial Governments Tax Smoothing? Evidence from Panel Data* MARK C. STRAZICICH The Ohio State University Newark, Ohio I. Introduction The theory of debt examined here is known variously

Are State and Provincial Governments Tax Smoothing? Evidence from Panel Data* MARK C. STRAZICICH The Ohio State University Newark, Ohio I. Introduction The theory of debt examined here is known variously

University of Macedonia Department of Economics. Discussion Paper Series. Inflation, inflation uncertainty and growth: are they related?

ISSN 1791-3144 University of Macedonia Department of Economics Discussion Paper Series Inflation, inflation uncertainty and growth: are they related? Stilianos Fountas Discussion Paper No. 12/2010 Department

ISSN 1791-3144 University of Macedonia Department of Economics Discussion Paper Series Inflation, inflation uncertainty and growth: are they related? Stilianos Fountas Discussion Paper No. 12/2010 Department

WHAT DOES THE HOUSE PRICE-TO-

WHAT DOES THE HOUSE PRICE-TO- INCOME RATIO TELL US ABOUT THE HOUSING AFFORDABILITY: A THEORY AND INTERNATIONAL EVIDENCE (THIS VERSION: AUG 2016) Charles Ka Yui LEUNG City University of Hong Kong Edward

WHAT DOES THE HOUSE PRICE-TO- INCOME RATIO TELL US ABOUT THE HOUSING AFFORDABILITY: A THEORY AND INTERNATIONAL EVIDENCE (THIS VERSION: AUG 2016) Charles Ka Yui LEUNG City University of Hong Kong Edward

Government expenditure and Economic Growth in MENA Region

Available online at http://sijournals.com/ijae/ Government expenditure and Economic Growth in MENA Region Mohsen Mehrara Faculty of Economics, University of Tehran, Tehran, Iran Email: mmehrara@ut.ac.ir

Available online at http://sijournals.com/ijae/ Government expenditure and Economic Growth in MENA Region Mohsen Mehrara Faculty of Economics, University of Tehran, Tehran, Iran Email: mmehrara@ut.ac.ir

The Velocity of Money and Nominal Interest Rates: Evidence from Developed and Latin-American Countries

The Velocity of Money and Nominal Interest Rates: Evidence from Developed and Latin-American Countries Petr Duczynski Abstract This study examines the behavior of the velocity of money in developed and

The Velocity of Money and Nominal Interest Rates: Evidence from Developed and Latin-American Countries Petr Duczynski Abstract This study examines the behavior of the velocity of money in developed and

Monetary policy regimes and exchange rate fluctuations

Seðlabanki Íslands Monetary policy regimes and exchange rate fluctuations The views are of the author and do not necessarily reflect those of the Central Bank of Iceland Thórarinn G. Pétursson Central

Seðlabanki Íslands Monetary policy regimes and exchange rate fluctuations The views are of the author and do not necessarily reflect those of the Central Bank of Iceland Thórarinn G. Pétursson Central

Basic information. Tax-to-GDP ratio Date: 29 November 2010

Federal Department of Finance FDF Federal Finance Administration FFA Basic information Date: 29 November 2010 Tax-to-GDP ratio 2010 The tax-to-gdp ratio is the sum of all taxes and public levies in relation

Federal Department of Finance FDF Federal Finance Administration FFA Basic information Date: 29 November 2010 Tax-to-GDP ratio 2010 The tax-to-gdp ratio is the sum of all taxes and public levies in relation

Volume 29, Issue 2. Is volume index of gdp per capita stationary in oecd countries? panel stationary tests with structural breaks

Volume 29, Issue 2 Is volume index of gdp per capita stationary in oecd countries? panel stationary tests with structural breaks Tsangyao Chang Department of Finance, Feng Chia University, Taichung, Taiwan

Volume 29, Issue 2 Is volume index of gdp per capita stationary in oecd countries? panel stationary tests with structural breaks Tsangyao Chang Department of Finance, Feng Chia University, Taichung, Taiwan

Household Balance Sheets and Debt an International Country Study

47 Household Balance Sheets and Debt an International Country Study Jacob Isaksen, Paul Lassenius Kramp, Louise Funch Sørensen and Søren Vester Sørensen, Economics INTRODUCTION AND SUMMARY What are the

47 Household Balance Sheets and Debt an International Country Study Jacob Isaksen, Paul Lassenius Kramp, Louise Funch Sørensen and Søren Vester Sørensen, Economics INTRODUCTION AND SUMMARY What are the

COINTEGRATION AND MARKET EFFICIENCY: AN APPLICATION TO THE CANADIAN TREASURY BILL MARKET. Soo-Bin Park* Carleton University, Ottawa, Canada K1S 5B6

1 COINTEGRATION AND MARKET EFFICIENCY: AN APPLICATION TO THE CANADIAN TREASURY BILL MARKET Soo-Bin Park* Carleton University, Ottawa, Canada K1S 5B6 Abstract: In this study we examine if the spot and forward

1 COINTEGRATION AND MARKET EFFICIENCY: AN APPLICATION TO THE CANADIAN TREASURY BILL MARKET Soo-Bin Park* Carleton University, Ottawa, Canada K1S 5B6 Abstract: In this study we examine if the spot and forward

Issue Brief for Congress

Order Code IB91078 Issue Brief for Congress Received through the CRS Web Value-Added Tax as a New Revenue Source Updated January 29, 2003 James M. Bickley Government and Finance Division Congressional

Order Code IB91078 Issue Brief for Congress Received through the CRS Web Value-Added Tax as a New Revenue Source Updated January 29, 2003 James M. Bickley Government and Finance Division Congressional

The Bilateral J-Curve: Sweden versus her 17 Major Trading Partners

Bahmani-Oskooee and Ratha, International Journal of Applied Economics, 4(1), March 2007, 1-13 1 The Bilateral J-Curve: Sweden versus her 17 Major Trading Partners Mohsen Bahmani-Oskooee and Artatrana Ratha

Bahmani-Oskooee and Ratha, International Journal of Applied Economics, 4(1), March 2007, 1-13 1 The Bilateral J-Curve: Sweden versus her 17 Major Trading Partners Mohsen Bahmani-Oskooee and Artatrana Ratha

Investigating the Intertemporal Risk-Return Relation in International. Stock Markets with the Component GARCH Model

Investigating the Intertemporal Risk-Return Relation in International Stock Markets with the Component GARCH Model Hui Guo a, Christopher J. Neely b * a College of Business, University of Cincinnati, 48

Investigating the Intertemporal Risk-Return Relation in International Stock Markets with the Component GARCH Model Hui Guo a, Christopher J. Neely b * a College of Business, University of Cincinnati, 48

Basic information. Tax-to-GDP ratio Date: 24 October 2012

Federal Department of Finance FDF Federal Finance Administration FFA Basic information Date: 24 October 2012 Tax-to-GDP ratio 2011 The tax-to-gdp ratio is the sum of all taxes and social security levies

Federal Department of Finance FDF Federal Finance Administration FFA Basic information Date: 24 October 2012 Tax-to-GDP ratio 2011 The tax-to-gdp ratio is the sum of all taxes and social security levies

EFFECT OF GENERAL UNCERTAINTY ON EARLY AND LATE VENTURE- CAPITAL INVESTMENTS: A CROSS-COUNTRY STUDY. Rajeev K. Goel* Illinois State University

DRAFT EFFECT OF GENERAL UNCERTAINTY ON EARLY AND LATE VENTURE- CAPITAL INVESTMENTS: A CROSS-COUNTRY STUDY Rajeev K. Goel* Illinois State University Iftekhar Hasan New Jersey Institute of Technology and

DRAFT EFFECT OF GENERAL UNCERTAINTY ON EARLY AND LATE VENTURE- CAPITAL INVESTMENTS: A CROSS-COUNTRY STUDY Rajeev K. Goel* Illinois State University Iftekhar Hasan New Jersey Institute of Technology and

Business cycle volatility and country zize :evidence for a sample of OECD countries. Abstract

Business cycle volatility and country zize :evidence for a sample of OECD countries Davide Furceri University of Palermo Georgios Karras Uniersity of Illinois at Chicago Abstract The main purpose of this

Business cycle volatility and country zize :evidence for a sample of OECD countries Davide Furceri University of Palermo Georgios Karras Uniersity of Illinois at Chicago Abstract The main purpose of this

Long-run Stability of Demand for Money in China with Consideration of Bilateral Currency Substitution

Long-run Stability of Demand for Money in China with Consideration of Bilateral Currency Substitution Yongqing Wang The Department of Business and Economics The University of Wisconsin-Sheboygan Sheboygan,

Long-run Stability of Demand for Money in China with Consideration of Bilateral Currency Substitution Yongqing Wang The Department of Business and Economics The University of Wisconsin-Sheboygan Sheboygan,

Sources of Government Revenue in the OECD, 2016

FISCAL FACT No. 517 July, 2016 Sources of Government Revenue in the OECD, 2016 By Kyle Pomerleau Director of Federal Projects Kevin Adams Research Assistant Key Findings OECD countries rely heavily on

FISCAL FACT No. 517 July, 2016 Sources of Government Revenue in the OECD, 2016 By Kyle Pomerleau Director of Federal Projects Kevin Adams Research Assistant Key Findings OECD countries rely heavily on

Optimal fiscal policy

Optimal fiscal policy Jasper Lukkezen Coen Teulings Overview Aim Optimal policy rule for fiscal policy How? Four building blocks: 1. Linear VAR model 2. Augmented by linearized equation for debt dynamics

Optimal fiscal policy Jasper Lukkezen Coen Teulings Overview Aim Optimal policy rule for fiscal policy How? Four building blocks: 1. Linear VAR model 2. Augmented by linearized equation for debt dynamics

Income smoothing and foreign asset holdings

J Econ Finan (2010) 34:23 29 DOI 10.1007/s12197-008-9070-2 Income smoothing and foreign asset holdings Faruk Balli Rosmy J. Louis Mohammad Osman Published online: 24 December 2008 Springer Science + Business

J Econ Finan (2010) 34:23 29 DOI 10.1007/s12197-008-9070-2 Income smoothing and foreign asset holdings Faruk Balli Rosmy J. Louis Mohammad Osman Published online: 24 December 2008 Springer Science + Business

Volume 31, Issue 1. Florence Huart University Lille 1

Volume 31, Issue 1 Has fiscal discretion during good times and bad times changed in the euro area countries? Florence Huart University Lille 1 Abstract We study the relationship between the change in the

Volume 31, Issue 1 Has fiscal discretion during good times and bad times changed in the euro area countries? Florence Huart University Lille 1 Abstract We study the relationship between the change in the

Growth in OECD Unit Labour Costs slows to 0.4% in the third quarter of 2016

Growth in OECD Unit Labour Costs slows to.4% in the third quarter of 26 Growth in unit labour costs (ULCs) in the OECD area slowed to.4% in the third quarter of 26 (compared with.6% in the previous quarter)

Growth in OECD Unit Labour Costs slows to.4% in the third quarter of 26 Growth in unit labour costs (ULCs) in the OECD area slowed to.4% in the third quarter of 26 (compared with.6% in the previous quarter)

Ricardian Equivalence: Further Evidence

University of Massachusetts Boston From the SelectedWorks of Atreya Chakraborty 1996 Ricardian Equivalence: Further Evidence Atreya Chakraborty, University of Massachusetts, Boston Available at: https://works.bepress.com/atreya_chakraborty/25/

University of Massachusetts Boston From the SelectedWorks of Atreya Chakraborty 1996 Ricardian Equivalence: Further Evidence Atreya Chakraborty, University of Massachusetts, Boston Available at: https://works.bepress.com/atreya_chakraborty/25/

Bank Loan Officers Expectations for Credit Standards: evidence from the European Bank Lending Survey

Bank Loan Officers Expectations for Credit Standards: evidence from the European Bank Lending Survey Anastasiou Dimitrios and Drakos Konstantinos * Abstract We employ credit standards data from the Bank

Bank Loan Officers Expectations for Credit Standards: evidence from the European Bank Lending Survey Anastasiou Dimitrios and Drakos Konstantinos * Abstract We employ credit standards data from the Bank

Savings Investment Correlation in Developing Countries: A Challenge to the Coakley-Rocha Findings

Savings Investment Correlation in Developing Countries: A Challenge to the Coakley-Rocha Findings Abu N.M. Wahid Tennessee State University Abdullah M. Noman University of New Orleans Mohammad Salahuddin*

Savings Investment Correlation in Developing Countries: A Challenge to the Coakley-Rocha Findings Abu N.M. Wahid Tennessee State University Abdullah M. Noman University of New Orleans Mohammad Salahuddin*

PUBLIC DEBT AND DEFICIT IN MEXICO: COMMENT* JohnH. Welch. Federal Reserve Bank of Dallas

PUBLIC DEBT AND DEFICIT IN MEXICO: A COMMENT* JohnH. Welch Federal Reserve Bank of Dallas Resumen: Este comentario muestra que el balance presupuestario intertemporal de México fue mantenido durante el

PUBLIC DEBT AND DEFICIT IN MEXICO: A COMMENT* JohnH. Welch Federal Reserve Bank of Dallas Resumen: Este comentario muestra que el balance presupuestario intertemporal de México fue mantenido durante el

Tax Burden, Tax Mix and Economic Growth in OECD Countries

Tax Burden, Tax Mix and Economic Growth in OECD Countries PAOLA PROFETA RICCARDO PUGLISI SIMONA SCABROSETTI June 30, 2015 FIRST DRAFT, PLEASE DO NOT QUOTE WITHOUT THE AUTHORS PERMISSION Abstract Focusing

Tax Burden, Tax Mix and Economic Growth in OECD Countries PAOLA PROFETA RICCARDO PUGLISI SIMONA SCABROSETTI June 30, 2015 FIRST DRAFT, PLEASE DO NOT QUOTE WITHOUT THE AUTHORS PERMISSION Abstract Focusing

Conditional convergence: how long is the long-run? Paul Ormerod. Volterra Consulting. April Abstract

Conditional convergence: how long is the long-run? Paul Ormerod Volterra Consulting April 2003 pormerod@volterra.co.uk Abstract Mainstream theories of economic growth predict that countries across the

Conditional convergence: how long is the long-run? Paul Ormerod Volterra Consulting April 2003 pormerod@volterra.co.uk Abstract Mainstream theories of economic growth predict that countries across the

International Income Smoothing and Foreign Asset Holdings.

MPRA Munich Personal RePEc Archive International Income Smoothing and Foreign Asset Holdings. Faruk Balli and Rosmy J. Louis and Mohammad Osman Massey University, Vancouver Island University, University

MPRA Munich Personal RePEc Archive International Income Smoothing and Foreign Asset Holdings. Faruk Balli and Rosmy J. Louis and Mohammad Osman Massey University, Vancouver Island University, University

IMPLICATIONS OF LOW PRODUCTIVITY GROWTH FOR DEBT SUSTAINABILITY

IMPLICATIONS OF LOW PRODUCTIVITY GROWTH FOR DEBT SUSTAINABILITY Neil R. Mehrotra Brown University Peterson Institute for International Economics November 9th, 2017 1 / 13 PUBLIC DEBT AND PRODUCTIVITY GROWTH

IMPLICATIONS OF LOW PRODUCTIVITY GROWTH FOR DEBT SUSTAINABILITY Neil R. Mehrotra Brown University Peterson Institute for International Economics November 9th, 2017 1 / 13 PUBLIC DEBT AND PRODUCTIVITY GROWTH

8-Jun-06 Personal Income Top Marginal Tax Rate,

8-Jun-06 Personal Income Top Marginal Tax Rate, 1975-2005 2005 2000 1999 1998 1997 1996 1995 1994 1993 1992 1991 1990 1989 1988 Australia 47% 47% 47% 47% 47% 47% 47% 47% 47% 47% 47% 48% 49% 49% Austria

8-Jun-06 Personal Income Top Marginal Tax Rate, 1975-2005 2005 2000 1999 1998 1997 1996 1995 1994 1993 1992 1991 1990 1989 1988 Australia 47% 47% 47% 47% 47% 47% 47% 47% 47% 47% 47% 48% 49% 49% Austria

Macroeconomic Theory and Policy

ECO 209Y Macroeconomic Theory and Policy Lecture 3: Aggregate Expenditure and Equilibrium Income Gustavo Indart Slide 1 Assumptions We will assume that: There is no depreciation There are no indirect taxes

ECO 209Y Macroeconomic Theory and Policy Lecture 3: Aggregate Expenditure and Equilibrium Income Gustavo Indart Slide 1 Assumptions We will assume that: There is no depreciation There are no indirect taxes

Prices and Output in an Open Economy: Aggregate Demand and Aggregate Supply

Prices and Output in an Open conomy: Aggregate Demand and Aggregate Supply chapter LARNING GOALS: After reading this chapter, you should be able to: Understand how short- and long-run equilibrium is reached

Prices and Output in an Open conomy: Aggregate Demand and Aggregate Supply chapter LARNING GOALS: After reading this chapter, you should be able to: Understand how short- and long-run equilibrium is reached

Corrigendum. OECD Pensions Outlook 2012 DOI: ISBN (print) ISBN (PDF) OECD 2012

ISBN (PDF) OECD 2012") OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

Double-Taxing Capital Income: How Bad Is the Problem?

November 15, 2006 Double-Taxing Capital Income: How Bad Is the Problem? by Patrick Fleenor Fiscal Fact No. 71 Introduction Double taxation is a common and often misused expression in tax policy discussions.

November 15, 2006 Double-Taxing Capital Income: How Bad Is the Problem? by Patrick Fleenor Fiscal Fact No. 71 Introduction Double taxation is a common and often misused expression in tax policy discussions.

Sources of Government Revenue in the OECD, 2017

FISCAL FACT No. 558 Aug. 2017 Sources of Government Revenue in the OECD, 2017 Amir El-Sibaie Analyst Key Findings: OECD countries rely heavily on consumption taxes, such as the value-added tax, and social

FISCAL FACT No. 558 Aug. 2017 Sources of Government Revenue in the OECD, 2017 Amir El-Sibaie Analyst Key Findings: OECD countries rely heavily on consumption taxes, such as the value-added tax, and social

MONEY, PRICES AND THE EXCHANGE RATE: EVIDENCE FROM FOUR OECD COUNTRIES

money 15/10/98 MONEY, PRICES AND THE EXCHANGE RATE: EVIDENCE FROM FOUR OECD COUNTRIES Mehdi S. Monadjemi School of Economics University of New South Wales Sydney 2052 Australia m.monadjemi@unsw.edu.au

money 15/10/98 MONEY, PRICES AND THE EXCHANGE RATE: EVIDENCE FROM FOUR OECD COUNTRIES Mehdi S. Monadjemi School of Economics University of New South Wales Sydney 2052 Australia m.monadjemi@unsw.edu.au

Sources of Government Revenue in the OECD, 2018

FISCAL FACT No. 581 Mar. 2018 Sources of Government Revenue in the OECD, 2018 Amir El-Sibaie Analyst Key Findings In 2015, OECD countries relied heavily on consumption taxes, such as the value-added tax,

FISCAL FACT No. 581 Mar. 2018 Sources of Government Revenue in the OECD, 2018 Amir El-Sibaie Analyst Key Findings In 2015, OECD countries relied heavily on consumption taxes, such as the value-added tax,

The relationship between output and unemployment in France and United Kingdom

The relationship between output and unemployment in France and United Kingdom Gaétan Stephan 1 University of Rennes 1, CREM April 2012 (Preliminary draft) Abstract We model the relation between output

The relationship between output and unemployment in France and United Kingdom Gaétan Stephan 1 University of Rennes 1, CREM April 2012 (Preliminary draft) Abstract We model the relation between output

GOVERNMENT BORROWING AND THE LONG- TERM INTEREST RATE: APPLICATION OF AN EXTENDED LOANABLE FUNDS MODEL TO THE SLOVAK REPUBLIC

ECONOMIC ANNALS, Volume LV, No. 184 / January March 2010 UDC: 3.33 ISSN: 0013-3264 Scientific Papers Yu Hsing* DOI:10.2298/EKA1084058H GOVERNMENT BORROWING AND THE LONG- TERM INTEREST RATE: APPLICATION

ECONOMIC ANNALS, Volume LV, No. 184 / January March 2010 UDC: 3.33 ISSN: 0013-3264 Scientific Papers Yu Hsing* DOI:10.2298/EKA1084058H GOVERNMENT BORROWING AND THE LONG- TERM INTEREST RATE: APPLICATION

Understanding the World Economy. Fiscal policy. Nicolas Coeurdacier Lecture 9

Understanding the World Economy Fiscal policy Lecture 9 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 9 : Fiscal policy 1. Public spending 2. Taxation 3. Debt and deficits 4. Fiscal policy

Understanding the World Economy Fiscal policy Lecture 9 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 9 : Fiscal policy 1. Public spending 2. Taxation 3. Debt and deficits 4. Fiscal policy

School of Economics and Management

School of Economics and Management TECHNICAL UNIVERSITY OF LISBON Department of Economics Carlos Pestana Barros & Nicolas Peypoch António Afonso & Christophe Rault A Comparative Analysis of Productivity

School of Economics and Management TECHNICAL UNIVERSITY OF LISBON Department of Economics Carlos Pestana Barros & Nicolas Peypoch António Afonso & Christophe Rault A Comparative Analysis of Productivity

Household Financial Wealth By Selected Country

Household Financial Wealth By Selected Country US$ Trillions 60 50-37% Indicates Projected Shortfall 40 30 20 Extrapolation of Historical Growth 2003-24 Projection (Based on Demographic Trends) -47% -34%

Household Financial Wealth By Selected Country US$ Trillions 60 50-37% Indicates Projected Shortfall 40 30 20 Extrapolation of Historical Growth 2003-24 Projection (Based on Demographic Trends) -47% -34%

Taxes and the co-location of intangibles and tangibles

Taxes and the co-location of intangibles and tangibles Simon Loretz ETPF/CEPS Conference on Business Taxation Brussels, 27 April, 2012 Motivation Intangible assets are increasingly seen as important for

Taxes and the co-location of intangibles and tangibles Simon Loretz ETPF/CEPS Conference on Business Taxation Brussels, 27 April, 2012 Motivation Intangible assets are increasingly seen as important for

Dividend, investment and the direction of causality

Working Paper 2/2011 Dividend, investment and the direction of causality P S Sanju P S Nirmala M Ramachandran DEPARTMENT OF ECONOMICS PONDICHERRY UNIVERSITY March 2011 system28 [Type the company name]

Working Paper 2/2011 Dividend, investment and the direction of causality P S Sanju P S Nirmala M Ramachandran DEPARTMENT OF ECONOMICS PONDICHERRY UNIVERSITY March 2011 system28 [Type the company name]

CENTRAL BANK INDEPENDENCE: A SENSITIVITY ANALYSIS

CENTRAL BANK INDEPENDENCE: A SENSITIVITY ANALYSIS SYLVESTER EIJFFINGER, ERIC SCHALING and MARCO HOEBERICHTS College of Europe, Humboldt University of Berlin, and CentER for Economic Research, Tilburg University,

CENTRAL BANK INDEPENDENCE: A SENSITIVITY ANALYSIS SYLVESTER EIJFFINGER, ERIC SCHALING and MARCO HOEBERICHTS College of Europe, Humboldt University of Berlin, and CentER for Economic Research, Tilburg University,

The persistence of regional unemployment: evidence from China

Applied Economics, 200?,??, 1 5 The persistence of regional unemployment: evidence from China ZHONGMIN WU Canterbury Business School, University of Kent at Canterbury, Kent CT2 7PE UK E-mail: Z.Wu-3@ukc.ac.uk

Applied Economics, 200?,??, 1 5 The persistence of regional unemployment: evidence from China ZHONGMIN WU Canterbury Business School, University of Kent at Canterbury, Kent CT2 7PE UK E-mail: Z.Wu-3@ukc.ac.uk

Empirical appendix of Public Expenditure Distribution, Voting, and Growth

Empirical appendix of Public Expenditure Distribution, Voting, and Growth Lorenzo Burlon August 11, 2014 In this note we report the empirical exercises we conducted to motivate the theoretical insights

Empirical appendix of Public Expenditure Distribution, Voting, and Growth Lorenzo Burlon August 11, 2014 In this note we report the empirical exercises we conducted to motivate the theoretical insights

Aviation Economics & Finance

Aviation Economics & Finance Professor David Gillen (University of British Columbia )& Professor Tuba Toru-Delibasi (Bahcesehir University) Istanbul Technical University Air Transportation Management M.Sc.

Aviation Economics & Finance Professor David Gillen (University of British Columbia )& Professor Tuba Toru-Delibasi (Bahcesehir University) Istanbul Technical University Air Transportation Management M.Sc.

VARIABILITY OF THE INFLATION RATE AND THE FORWARD PREMIUM IN A MONEY DEMAND FUNCTION: THE CASE OF THE GERMAN HYPERINFLATION

VARIABILITY OF THE INFLATION RATE AND THE FORWARD PREMIUM IN A MONEY DEMAND FUNCTION: THE CASE OF THE GERMAN HYPERINFLATION By: Stuart D. Allen and Donald L. McCrickard Variability of the Inflation Rate

VARIABILITY OF THE INFLATION RATE AND THE FORWARD PREMIUM IN A MONEY DEMAND FUNCTION: THE CASE OF THE GERMAN HYPERINFLATION By: Stuart D. Allen and Donald L. McCrickard Variability of the Inflation Rate

ON THE LONG-TERM MACROECONOMIC EFFECTS OF SOCIAL SPENDING IN THE UNITED STATES (*) Alfredo Marvão Pereira The College of William and Mary

Alfredo Marvão Pereira The College of William and Mary") ON THE LONG-TERM MACROECONOMIC EFFECTS OF SOCIAL SPENDING IN THE UNITED STATES (*) Alfredo Marvão Pereira The College of William and Mary Jorge M. Andraz Faculdade de Economia, Universidade do Algarve,

ON THE LONG-TERM MACROECONOMIC EFFECTS OF SOCIAL SPENDING IN THE UNITED STATES (*) Alfredo Marvão Pereira The College of William and Mary Jorge M. Andraz Faculdade de Economia, Universidade do Algarve,

The Impact of Trade and Factor Flows on Domestic Taxation

International Journal of Business and Economics, 2007, Vol. 6, No. 1, 47-62 The Impact of Trade and Factor Flows on Domestic Taxation Ryo Takashima * Department of Economics, Washington & Jefferson College,

International Journal of Business and Economics, 2007, Vol. 6, No. 1, 47-62 The Impact of Trade and Factor Flows on Domestic Taxation Ryo Takashima * Department of Economics, Washington & Jefferson College,

Exchange Rate Market Efficiency: Across and Within Countries

Exchange Rate Market Efficiency: Across and Within Countries Tammy A. Rapp and Subhash C. Sharma This paper utilizes cointegration testing and common-feature testing to investigate market efficiency among

Exchange Rate Market Efficiency: Across and Within Countries Tammy A. Rapp and Subhash C. Sharma This paper utilizes cointegration testing and common-feature testing to investigate market efficiency among

A note on testing for tax-smoothing in general equilibrium

A note on testing for tax-smoothing in general equilibrium Jim Malley 1,*, Apostolis Philippopoulos 2 1 Department of Economics, University of Glasgow, Glasgow G12 8RT, UK 2 Department of International

A note on testing for tax-smoothing in general equilibrium Jim Malley 1,*, Apostolis Philippopoulos 2 1 Department of Economics, University of Glasgow, Glasgow G12 8RT, UK 2 Department of International

Fiscal Policy in Japan

Fiscal Policy in Japan - Issues and Future Directions- June 10th, 2015 Ministry of Finance General Government Gross Debt and Financial Balances (International Comparison) (%) 240 210 General Government

Fiscal Policy in Japan - Issues and Future Directions- June 10th, 2015 Ministry of Finance General Government Gross Debt and Financial Balances (International Comparison) (%) 240 210 General Government

Appraising fiscal reaction functions

School of Economics and Management TECHNICAL UNIVERSITY OF LISBON Department of Economics Carlos Pestana Barros & Nicolas Peypoch António Afonso & João Tovar Jalles Appraising fiscal reaction functions

School of Economics and Management TECHNICAL UNIVERSITY OF LISBON Department of Economics Carlos Pestana Barros & Nicolas Peypoch António Afonso & João Tovar Jalles Appraising fiscal reaction functions

INTERDEPENDENCE OF THE BANKING SECTOR AND THE REAL SECTOR: EVIDENCE FROM OECD COUNTRIES

INTERDEPENDENCE OF THE BANKING SECTOR AND THE REAL SECTOR: EVIDENCE FROM OECD COUNTRIES İlkay Şendeniz-Yüncü * Levent Akdeniz ** Kürşat Aydoğan *** March 2006 Abstract This paper investigates the validity

INTERDEPENDENCE OF THE BANKING SECTOR AND THE REAL SECTOR: EVIDENCE FROM OECD COUNTRIES İlkay Şendeniz-Yüncü * Levent Akdeniz ** Kürşat Aydoğan *** March 2006 Abstract This paper investigates the validity

Sources of Government Revenue in the OECD, 2014

FISCAL FACT Nov. 2014 No. 443 Sources of Government Revenue in the OECD, 2014 By Kyle Pomerleau Economist Key Findings OECD countries rely heavily on consumption taxes, such as the value added tax, and

FISCAL FACT Nov. 2014 No. 443 Sources of Government Revenue in the OECD, 2014 By Kyle Pomerleau Economist Key Findings OECD countries rely heavily on consumption taxes, such as the value added tax, and

Government Tax Revenue, Expenditure, and Debt in Sri Lanka : A Vector Autoregressive Model Analysis

Government Tax Revenue, Expenditure, and Debt in Sri Lanka : A Vector Autoregressive Model Analysis Introduction Uthajakumar S.S 1 and Selvamalai. T 2 1 Department of Economics, University of Jaffna. 2

Government Tax Revenue, Expenditure, and Debt in Sri Lanka : A Vector Autoregressive Model Analysis Introduction Uthajakumar S.S 1 and Selvamalai. T 2 1 Department of Economics, University of Jaffna. 2

TAX SMOOTHING HYPOTHESIS: A CASE OF PAKISTAN

TAX SMOOTHING HYPOTHESIS: A CASE OF PAKISTAN By Hananiah Beatrice Submitted to Department of Economics Central European University In partial fulfillment of the requirements for the degree of Master of

TAX SMOOTHING HYPOTHESIS: A CASE OF PAKISTAN By Hananiah Beatrice Submitted to Department of Economics Central European University In partial fulfillment of the requirements for the degree of Master of

Statistical annex. Sources and definitions

Statistical annex Sources and definitions Most of the statistics shown in these tables can be found as well in several other (paper or electronic) publications or references, as follows: the annual edition

Statistical annex Sources and definitions Most of the statistics shown in these tables can be found as well in several other (paper or electronic) publications or references, as follows: the annual edition

An Investigation into the Sensitivity of Money Demand to Interest Rates in the Philippines

An Investigation into the Sensitivity of Money Demand to Interest Rates in the Philippines Jason C. Patalinghug Southern Connecticut State University Studies into the effect of interest rates on money

An Investigation into the Sensitivity of Money Demand to Interest Rates in the Philippines Jason C. Patalinghug Southern Connecticut State University Studies into the effect of interest rates on money

INSTITUTE OF ECONOMIC STUDIES

ISSN 1011-8888 INSTITUTE OF ECONOMIC STUDIES WORKING PAPER SERIES W17:04 December 2017 The Modigliani Puzzle Revisited: A Note Margarita Katsimi and Gylfi Zoega, Address: Faculty of Economics University

ISSN 1011-8888 INSTITUTE OF ECONOMIC STUDIES WORKING PAPER SERIES W17:04 December 2017 The Modigliani Puzzle Revisited: A Note Margarita Katsimi and Gylfi Zoega, Address: Faculty of Economics University

7.3 The Household s Intertemporal Budget Constraint

Summary Chapter 7 Borrowing, Lending, and Budget Constraints 7.1 Overview - Borrowing and lending is a fundamental act of economic life - Expectations about future exert the greatest influence on firms

Summary Chapter 7 Borrowing, Lending, and Budget Constraints 7.1 Overview - Borrowing and lending is a fundamental act of economic life - Expectations about future exert the greatest influence on firms

Do Closer Economic Ties Imply Convergence in Income - The Case of the U.S., Canada, and Mexico

Law and Business Review of the Americas Volume 1 1995 Do Closer Economic Ties Imply Convergence in Income - The Case of the U.S., Canada, and Mexico Thomas Osang Follow this and additional works at: http://scholar.smu.edu/lbra

Law and Business Review of the Americas Volume 1 1995 Do Closer Economic Ties Imply Convergence in Income - The Case of the U.S., Canada, and Mexico Thomas Osang Follow this and additional works at: http://scholar.smu.edu/lbra

REDUCTION OF EMPLOYMENT PROTECTION IN OECD COUNTRIES: ITS DRIVING FORCES

Forum REDUCTION OF EMPLOYMENT PROTECTION IN OECD COUNTRIES: ITS DRIVING FORCES employment protection in OECD countries in the past. There are few studies which have analysed this relationship empirically.

Forum REDUCTION OF EMPLOYMENT PROTECTION IN OECD COUNTRIES: ITS DRIVING FORCES employment protection in OECD countries in the past. There are few studies which have analysed this relationship empirically.

The Balassa-Samuelson Effect and The MEVA G10 FX Model

The Balassa-Samuelson Effect and The MEVA G10 FX Model Abstract: In this study, we introduce Danske s Medium Term FX Evaluation model (MEVA G10 FX), a framework that falls within the class of the Behavioural

The Balassa-Samuelson Effect and The MEVA G10 FX Model Abstract: In this study, we introduce Danske s Medium Term FX Evaluation model (MEVA G10 FX), a framework that falls within the class of the Behavioural

National Income & Business Cycles

National Income & Business Cycles accounting identities for the open economy the small open economy model what makes it small how the trade balance and exchange rate are determined how policies affect

National Income & Business Cycles accounting identities for the open economy the small open economy model what makes it small how the trade balance and exchange rate are determined how policies affect

What Can Macroeconometric Models Say About Asia-Type Crises?

What Can Macroeconometric Models Say About Asia-Type Crises? Ray C. Fair May 1999 Abstract This paper uses a multicountry econometric model to examine Asia-type crises. Experiments are run for Thailand,

What Can Macroeconometric Models Say About Asia-Type Crises? Ray C. Fair May 1999 Abstract This paper uses a multicountry econometric model to examine Asia-type crises. Experiments are run for Thailand,

EQUITY RETURNS AND INFLATION: THE PUZZLINGLY LONG LAGS

EQUITY RETURNS AND INFLATION: THE PUZZLINGLY LONG LAGS James R. Lothian and Cornelia McCarthy ABSTRACT This paper examines data for stock prices and price levels of 14 developed countries during the post-wwii

EQUITY RETURNS AND INFLATION: THE PUZZLINGLY LONG LAGS James R. Lothian and Cornelia McCarthy ABSTRACT This paper examines data for stock prices and price levels of 14 developed countries during the post-wwii

Applied Econometrics and International Development. AEID.Vol. 5-3 (2005)

") PURCHASING POWER PARITY BASED ON CAPITAL ACCOUNT, EXCHANGE RATE VOLATILITY AND COINTEGRATION: EVIDENCE FROM SOME DEVELOPING COUNTRIES AHMED, Mudabber * Abstract One of the most important and recurrent

PURCHASING POWER PARITY BASED ON CAPITAL ACCOUNT, EXCHANGE RATE VOLATILITY AND COINTEGRATION: EVIDENCE FROM SOME DEVELOPING COUNTRIES AHMED, Mudabber * Abstract One of the most important and recurrent

The Distortionary Effects of Inflation: An Empirical Investigation

The Distortionary Effects of Inflation: An Empirical Investigation Vikas Kakkar* Department of Economics and Finance City University of Hong Kong Kowloon, Hong Kong E-Mail: efvikas@cityu.edu.hk Tel: (852)

The Distortionary Effects of Inflation: An Empirical Investigation Vikas Kakkar* Department of Economics and Finance City University of Hong Kong Kowloon, Hong Kong E-Mail: efvikas@cityu.edu.hk Tel: (852)

The Global Financial Crisis and the Return of the Nordic Model?

The Global Financial Crisis and the Return of the Nordic Model? Lars Calmfors Embassy of Denmark and the Swedish Institute of International Affairs 18 November Topics 1. The global economic crisis 2. Globalisation

The Global Financial Crisis and the Return of the Nordic Model? Lars Calmfors Embassy of Denmark and the Swedish Institute of International Affairs 18 November Topics 1. The global economic crisis 2. Globalisation

Understanding the World Economy Master in Economics and Business. Fiscal policy. Nicolas Coeurdacier

Understanding the World Economy Master in Economics and Business Fiscal policy Lecture 9 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 9 : Fiscal policy 1. Public spending 2. Taxation 3.

Understanding the World Economy Master in Economics and Business Fiscal policy Lecture 9 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 9 : Fiscal policy 1. Public spending 2. Taxation 3.

The government spending and private consumption: a panel cointegration analysis

International Review of Economics and Finance 10 (2001) 95±108 The government spending and private consumption: a panel cointegration analysis Tsung-wu Ho* Department of Economics, Shih Hsin University,

International Review of Economics and Finance 10 (2001) 95±108 The government spending and private consumption: a panel cointegration analysis Tsung-wu Ho* Department of Economics, Shih Hsin University,

Cointegration Tests and the Long-Run Purchasing Power Parity: Examination of Six Currencies in Asia

Volume 23, Number 1, June 1998 Cointegration Tests and the Long-Run Purchasing Power Parity: Examination of Six Currencies in Asia Ananda Weliwita ** 2 The validity of the long-run purchasing power parity

Volume 23, Number 1, June 1998 Cointegration Tests and the Long-Run Purchasing Power Parity: Examination of Six Currencies in Asia Ananda Weliwita ** 2 The validity of the long-run purchasing power parity

CURRENT ACCOUNT DEFICITS IN THE TRANSITION ECO- NOMIES

CURRENT ACCOUNT DEFICITS IN THE TRANSITION ECO- NOMIES Mark J. HOLMES * Abstract: This study tests for the stationarity and sustainability of current account deficits for ten transition economies. For

CURRENT ACCOUNT DEFICITS IN THE TRANSITION ECO- NOMIES Mark J. HOLMES * Abstract: This study tests for the stationarity and sustainability of current account deficits for ten transition economies. For

The Implications for Fiscal Policy Considering Rule-of-Thumb Consumers in the New Keynesian Model for Romania

Vol. 3, No.3, July 2013, pp. 365 371 ISSN: 2225-8329 2013 HRMARS www.hrmars.com The Implications for Fiscal Policy Considering Rule-of-Thumb Consumers in the New Keynesian Model for Romania Ana-Maria SANDICA

Vol. 3, No.3, July 2013, pp. 365 371 ISSN: 2225-8329 2013 HRMARS www.hrmars.com The Implications for Fiscal Policy Considering Rule-of-Thumb Consumers in the New Keynesian Model for Romania Ana-Maria SANDICA

Burden of Taxation: International Comparisons

Burden of Taxation: International Comparisons Standard Note: SN/EP/3235 Last updated: 15 October 2008 Author: Bryn Morgan Economic Policy & Statistics Section This note presents data comparing the national

Burden of Taxation: International Comparisons Standard Note: SN/EP/3235 Last updated: 15 October 2008 Author: Bryn Morgan Economic Policy & Statistics Section This note presents data comparing the national

Some Basic Facts about Government Expenditures and Taxation in Canada. Econ 525

Some Basic Facts about Government Expenditures and Taxation in Canada Econ 525 Revenues and Expenditures in Canada Since we re studying the role of government in this course it is worth considering some

Some Basic Facts about Government Expenditures and Taxation in Canada Econ 525 Revenues and Expenditures in Canada Since we re studying the role of government in this course it is worth considering some

DANMARKS NATIONALBANK

DANMARKS NATIONALBANK WEALTH, DEBT AND MACROECONOMIC STABILITY Niels Lynggård Hansen, Head of Economics and Monetary Policy. IARIW, Copenhagen, 21 August 2018 Agenda Descriptive evidence on household debt

DANMARKS NATIONALBANK WEALTH, DEBT AND MACROECONOMIC STABILITY Niels Lynggård Hansen, Head of Economics and Monetary Policy. IARIW, Copenhagen, 21 August 2018 Agenda Descriptive evidence on household debt

On the sustainability of the EU's current account deficits

Loughborough University Institutional Repository On the sustainability of the EU's current account deficits This item was submitted to Loughborough University's Institutional Repository by the/an author.

Loughborough University Institutional Repository On the sustainability of the EU's current account deficits This item was submitted to Loughborough University's Institutional Repository by the/an author.

The Impact of Tax Policies on Economic Growth: Evidence from Asian Economies

The Impact of Tax Policies on Economic Growth: Evidence from Asian Economies Ihtsham ul Haq Padda and Naeem Akram Abstract Tax based fiscal policies have been regarded as less policy tool to overcome the

The Impact of Tax Policies on Economic Growth: Evidence from Asian Economies Ihtsham ul Haq Padda and Naeem Akram Abstract Tax based fiscal policies have been regarded as less policy tool to overcome the

Are Greek budget deficits 'too large'? National University of Ireland, Galway

Provided by the author(s) and NUI Galway in accordance with publisher policies. Please cite the published version when available. Title Are Greek budget deficits 'too large'? Author(s) Fountas, Stilianos

Provided by the author(s) and NUI Galway in accordance with publisher policies. Please cite the published version when available. Title Are Greek budget deficits 'too large'? Author(s) Fountas, Stilianos

Trust and Fertility Dynamics. Arnstein Aassve, Università Bocconi Francesco C. Billari, University of Oxford Léa Pessin, Universitat Pompeu Fabra

Trust and Fertility Dynamics Arnstein Aassve, Università Bocconi Francesco C. Billari, University of Oxford Léa Pessin, Universitat Pompeu Fabra 1 Background Fertility rates across OECD countries differ

Trust and Fertility Dynamics Arnstein Aassve, Università Bocconi Francesco C. Billari, University of Oxford Léa Pessin, Universitat Pompeu Fabra 1 Background Fertility rates across OECD countries differ

OECD Report Shows Tax Burdens Falling in Many OECD Countries

OECD Centres Germany Berlin (49-30) 288 8353 Japan Tokyo (81-3) 5532-0021 Mexico Mexico (52-55) 5281 3810 United States Washington (1-202) 785 6323 AUSTRALIA AUSTRIA BELGIUM CANADA CZECH REPUBLIC DENMARK

OECD Centres Germany Berlin (49-30) 288 8353 Japan Tokyo (81-3) 5532-0021 Mexico Mexico (52-55) 5281 3810 United States Washington (1-202) 785 6323 AUSTRALIA AUSTRIA BELGIUM CANADA CZECH REPUBLIC DENMARK

Demographics and Secular Stagnation Hypothesis in Europe

Demographics and Secular Stagnation Hypothesis in Europe Carlo Favero (Bocconi University, IGIER) Vincenzo Galasso (Bocconi University, IGIER, CEPR & CESIfo) Growth in Europe?, Marseille, September 2015

Demographics and Secular Stagnation Hypothesis in Europe Carlo Favero (Bocconi University, IGIER) Vincenzo Galasso (Bocconi University, IGIER, CEPR & CESIfo) Growth in Europe?, Marseille, September 2015

Structural Cointegration Analysis of Private and Public Investment

International Journal of Business and Economics, 2002, Vol. 1, No. 1, 59-67 Structural Cointegration Analysis of Private and Public Investment Rosemary Rossiter * Department of Economics, Ohio University,

International Journal of Business and Economics, 2002, Vol. 1, No. 1, 59-67 Structural Cointegration Analysis of Private and Public Investment Rosemary Rossiter * Department of Economics, Ohio University,

), is described there by a function of the following form: U (c t. )= c t. where c t

, is described there by a function of the following form: U (c t. )= c t. where c t") 4.0 3.5 3.0 2.5 2.0 1.5 1.0 0.5 Figure B15. Graphic illustration of the utility function when s = 0.3 or 0.6. 0.0 0.0 0.0 0.5 1.0 1.5 2.0 s = 0.6 s = 0.3 Note. The level of consumption, c t, is plotted

4.0 3.5 3.0 2.5 2.0 1.5 1.0 0.5 Figure B15. Graphic illustration of the utility function when s = 0.3 or 0.6. 0.0 0.0 0.0 0.5 1.0 1.5 2.0 s = 0.6 s = 0.3 Note. The level of consumption, c t, is plotted

Aggregate demand &long-run unemployment L. Ball 1999

Aggregate demand &long-run unemployment L. Ball 1999 Standard theory: equilibrium unemployment depends on labour market rigidities and institutional variables Monetary policy should focus on nominal stability,

Aggregate demand &long-run unemployment L. Ball 1999 Standard theory: equilibrium unemployment depends on labour market rigidities and institutional variables Monetary policy should focus on nominal stability,

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 24

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 24 I. OVERVIEW A. Framework B. Topics POLICY RESPONSES TO FINANCIAL CRISES APRIL 23, 2018 II.

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 24 I. OVERVIEW A. Framework B. Topics POLICY RESPONSES TO FINANCIAL CRISES APRIL 23, 2018 II.

Why the saving rate has been falling in Japan

October 2007 Why the saving rate has been falling in Japan Yoshiaki Azuma and Takeo Nakao Doshisha University Faculty of Economics Imadegawa Karasuma Kamigyo Kyoto 602-8580 Japan Doshisha University Working

October 2007 Why the saving rate has been falling in Japan Yoshiaki Azuma and Takeo Nakao Doshisha University Faculty of Economics Imadegawa Karasuma Kamigyo Kyoto 602-8580 Japan Doshisha University Working

The Dynamics between Government Debt and Economic Growth in South Asia: A Time Series Approach

The Empirical Economics Letters, 15(9): (September 16) ISSN 1681 8997 The Dynamics between Government Debt and Economic Growth in South Asia: A Time Series Approach Nimantha Manamperi * Department of Economics,

The Empirical Economics Letters, 15(9): (September 16) ISSN 1681 8997 The Dynamics between Government Debt and Economic Growth in South Asia: A Time Series Approach Nimantha Manamperi * Department of Economics,

A NOTE ON PUBLIC SPENDING EFFICIENCY

A NOTE ON PUBLIC SPENDING EFFICIENCY try to implement better institutions and should reassign many non-core public sector activities to the private sector. ANTÓNIO AFONSO * Public sector performance Introduction

A NOTE ON PUBLIC SPENDING EFFICIENCY try to implement better institutions and should reassign many non-core public sector activities to the private sector. ANTÓNIO AFONSO * Public sector performance Introduction

education (captured by the school leaving age), household income (measured on a ten-point

, household income (measured on a ten-point") A Web-Appendix A.1 Information on data sources Individual level responses on benefit morale, tax morale, age, sex, marital status, children, education (captured by the school leaving age), household income

A Web-Appendix A.1 Information on data sources Individual level responses on benefit morale, tax morale, age, sex, marital status, children, education (captured by the school leaving age), household income

Understanding the World Economy Master in Economics and Business. Fiscal policy. Nicolas Coeurdacier

Understanding the World Economy Master in Economics and Business Fiscal policy Lecture 9 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 9 : Fiscal policy 1. Public spending 2. Taxation 3.

Understanding the World Economy Master in Economics and Business Fiscal policy Lecture 9 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 9 : Fiscal policy 1. Public spending 2. Taxation 3.

Debt and the managerial Entrenchment in U.S

Debt and the managerial Entrenchment in U.S Kammoun Chafik Faculty of Economics and Management of Sfax University of Sfax, Tunisia, Route de Gremda km 2, Aein cheikhrouhou, Sfax 3032, Tunisie. Boujelbène

Debt and the managerial Entrenchment in U.S Kammoun Chafik Faculty of Economics and Management of Sfax University of Sfax, Tunisia, Route de Gremda km 2, Aein cheikhrouhou, Sfax 3032, Tunisie. Boujelbène

ECON 3010 Intermediate Macroeconomics Chapter 6

ECON 3010 Intermediate Macroeconomics Chapter 6 The Open Economy Imports and exports of selected countries, 2010 60 50 Exports Imports Percent of GDP 40 30 20 10 0 Australia China Germany Greece S. Korea

ECON 3010 Intermediate Macroeconomics Chapter 6 The Open Economy Imports and exports of selected countries, 2010 60 50 Exports Imports Percent of GDP 40 30 20 10 0 Australia China Germany Greece S. Korea

Cyclical Convergence and Divergence in the Euro Area

Cyclical Convergence and Divergence in the Euro Area Presentation by Val Koromzay, Director for Country Studies, OECD to the Brussels Forum, April 2004 1 1 I. Introduction: Why is the issue important?

Cyclical Convergence and Divergence in the Euro Area Presentation by Val Koromzay, Director for Country Studies, OECD to the Brussels Forum, April 2004 1 1 I. Introduction: Why is the issue important?

Public Financial Management (PFMx) Module

Module") Public Financial Management (PFMx) Module 4 The Annual Budget Preparation and Approval This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Fiscal

Public Financial Management (PFMx) Module 4 The Annual Budget Preparation and Approval This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Fiscal