WHAT DOES THE HOUSE PRICE-TO-

|

|

|

- Janel Gaines

- 5 years ago

- Views:

Transcription

1 WHAT DOES THE HOUSE PRICE-TO- INCOME RATIO TELL US ABOUT THE HOUSING AFFORDABILITY: A THEORY AND INTERNATIONAL EVIDENCE (THIS VERSION: AUG 2016) Charles Ka Yui LEUNG City University of Hong Kong Edward TANG Hong Kong Shue Yan University

2 INTRODUCTION: BIG PICTURE QN: (especially after 2008 global financial crisis): 1. What is the normal asset price? What is the normal relationship between the asset price and economic fundamentals? 2. Do we have any implementable way to measure the deviations of the actual asset price from the normal counterpart? Can we establish an early warning system for the asset price? 2

3 FROM DEMOGRAPHIA (2016) 3

to detect")

4 IMF uses Price-to-income ratio (PIR) to detect possible housing bubble formation. Source: IMF Global Housing Watch 4

5 INTRODUCTION Even though PIR is widely accepted as a measure of housing affordability, formal modeling of PIR is relatively rare. We construct a simple DSGE model and derive the PIR out of that model. If agents are rational and foresee these movements, they would adjust their consumptionsaving decision, labor supply decision, as well as home purchase decision accordingly. Thus, we should expect the PIR to be somehow related to the movement of economic fundamentals, e.g. the output dynamics. 5

6 INTRODUCTION Oikainen (2009), Stadelmann (2010), Agnello and Schuknecht (2011), among others Aggregate output, labor wage and monetary policy are determinants of housing price Our paper attempts to relate PIR and the economic dynamics in a simple DSGE model when all these variables are determined endogenously. 6

7 A BENCHMARK MODEL Based on Greenwood and Hercowitz (1991), Benassy (1995) and Leung (2007, 2014). Time is discrete and the horizon is infinite. Population is assumed to be constant. Goods in the economy Non-durable consumption goods: C t Business (or physical) capital: K t Residential (or housing) capital: H t Representative agent Labor hours: L t Real cash balance: M t / P t Government prints nominal money: M t 7

8 MODEL (CONTINUED) Future stock of capital (business and housing) depends on current level of stock (after depreciation) and new investment. Firms employ labor and business capital from competitive input markets to produce output. Productivity shock is a AR(1) process. Government prints money at a rate / All agents in the model economy maximize their utility or profit. Goods market and housing market clear. 8

9 A BENCHMARK MODEL The representative household in the model maximizes the expected intertemporal utility: with a simple utility functional form 9

10 A BENCHMARK MODEL 10

11 A BENCHMARK MODEL 11

12 A BENCHMARK MODEL 12

13 A BENCHMARK MODEL 13

14 SOME BASIC RESULTS 14

15 A BENCHMARK MODEL 15

16 A BENCHMARK MODEL 16

17 MAIN RESULT (FLEXIBLE PRICE CASE) 17

18 CASE II: SHORT-TERM RIGID WAGES 18

19 SHORT-TERM RIGID WAGES (CONTIN.) 19

20 SHORT-TERM RIGID WAGES (CONTIN.) 20

21 MONETARY POLICY 21

22 A MODIFIED MONEY SUPPLY RULE 22

23 BASIC RESULT: MONETARY POLICY 23

24 MAIN RESULTS: SHORT-TERM RIGID WAGES 24

25 MAIN RESULTS: SHORT-TERM RIGID WAGES (II) 25

26 EMPIRICAL EVIDENCE Sampling period: 1997Q Q4 Countries: Australia, Canada, Denmark, Finland, France, Germany, Ireland, Italy, Japan, Netherlands, New Zealand, Norway, Spain, Sweden, UK, US. Data Real GDP and wage index: OECD Statistics Housing price index: Bank of International Settlements 26

27 EMPIRICAL EVIDENCE Equation (30): 27

28 EMPIRICAL EVIDENCE Equation (30): 28

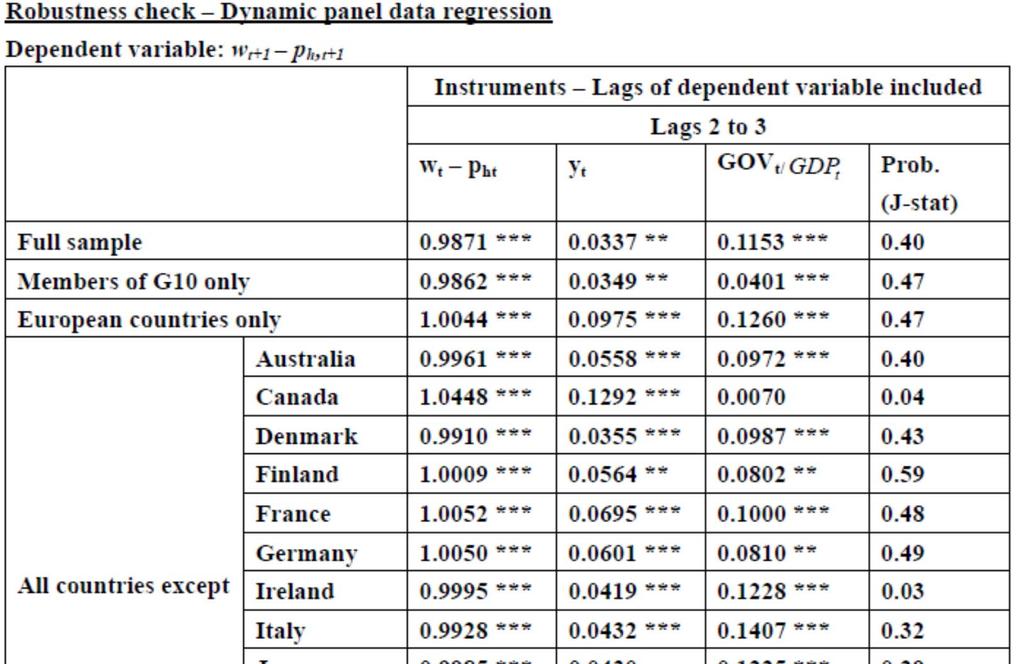

29 EMPIRICAL EVIDENCE Equation (29): Instruments Lags of dependent variable included Lags 2 to 3 Lags 2 to 4 Lags 2 to 5 w t p ht *** *** *** y t *** *** *** GMM weights AB-n-step AB-n-step AB-n-step J-statistics Prob.(J-statistics)

30 EMPIRICAL EVIDENCE One additional question: Are wage-to-house price ratio and real output having a long-run relationship? Yes, using panel cointegrating regressions. 30

31 EMPIRICAL EVIDENCE Panel unit root tests IPS W-statistic ADF-Fisher Chi-Square PP-Fisher Chi-square w t p h, t Δ(w t p h, t ) y t Δ(y t ) *** *** *** *** *** *** Notes: H 0 : Each country follows an individual unit root process. H 1 : At least one country s process is trend stationary. Exogenous variables: individual effects, individual linear trends. ***denotes 1% significance level. 31

32 EMPIRICAL EVIDENCE Panel cointegrating regressions Dependent variable: w t+1 p h, t+1 Fully-modified OLS Dynamic OLS y t *** *** ***denotes 1% significance level. 32

33 AN INTERPRETATION: Consider the economy is initially in the steady state (or, on a balanced growth path). Now a positive productivity shock. Output yt Typically, in the short run, the house price increases more than the wage, and hence wt pt Over time, however, 2 effects. Capital goods are accumulated wt Housing units are built as well pt Hence, wt pt Output and RIP can have a positive relationship in the long run. 33

34 34

35 Sep-97 Sep-98 Sep-99 Sep-00 Sep-01 Sep-02 Sep-03 Sep-04 Sep-05 Sep-06 Sep-07 Sep-08 Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 wt -pht Japan Actual Fitted Sep-97 Sep-98 Sep-99 Sep-00 Sep-01 Sep-02 Sep-03 Sep-04 Sep-05 Sep-06 Sep-07 Sep-08 Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 wt -pht Netherlands Actual Fitted Sep-97 Sep-98 Sep-99 Sep-00 Sep-01 Sep-02 Sep-03 Sep-04 Sep-05 Sep-06 Sep-07 Sep-08 Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 wt -pht New Zealand Actual Fitted Sep-97 Sep-98 Sep-99 Sep-00 Sep-01 Sep-02 Sep-03 Sep-04 Sep-05 Sep-06 Sep-07 Sep-08 Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 wt -pht Norway Actual Fitted

36 Sep-97 Sep-98 Sep-99 Sep-00 Sep-01 Sep-02 Sep-03 Sep-04 Sep-05 Sep-06 Sep-07 Sep-08 Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 wt -pht Spain Actual Fitted Sep-97 Sep-98 Sep-99 Sep-00 Sep-01 Sep-02 Sep-03 Sep-04 Sep-05 Sep-06 Sep-07 Sep-08 Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 wt -pht Sweden Actual Fitted Sep-97 Sep-98 Sep-99 Sep-00 Sep-01 Sep-02 Sep-03 Sep-04 Sep-05 Sep-06 Sep-07 Sep-08 Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 wt -pht UK Actual Fitted Sep-97 Sep-98 Sep-99 Sep-00 Sep-01 Sep-02 Sep-03 Sep-04 Sep-05 Sep-06 Sep-07 Sep-08 Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 wt -pht US Actual Fitted

37 CONCLUDING REMARKS Housing price-to-income ratio (PIR) is widely used in the media and policy discussion. This paper constructs a simple DSGE model, which studies the endogenous dynamics of the PIR. The volatility of PIR is positively and significantly correlated to the volatility of real GDP. PIR is positively correlated to its own lag and previous real GDP. PIR and real GDP has a long run relationship. 37

38 THANKS!! 38

What does the house price-to-income ratio tell. us about the housing market affordability: A. theory and international evidence

What does the house price-to-income ratio tell us about the housing market affordability: A theory and international evidence Charles Ka Yui Leung Edward Chi Ho Tang Wing Leong Teo August 14, 2015 Acknowledgement:

What does the house price-to-income ratio tell us about the housing market affordability: A theory and international evidence Charles Ka Yui Leung Edward Chi Ho Tang Wing Leong Teo August 14, 2015 Acknowledgement:

Optimal fiscal policy

Optimal fiscal policy Jasper Lukkezen Coen Teulings Overview Aim Optimal policy rule for fiscal policy How? Four building blocks: 1. Linear VAR model 2. Augmented by linearized equation for debt dynamics

Optimal fiscal policy Jasper Lukkezen Coen Teulings Overview Aim Optimal policy rule for fiscal policy How? Four building blocks: 1. Linear VAR model 2. Augmented by linearized equation for debt dynamics

International evidence of tax smoothing in a panel of industrial countries

Strazicich, M.C. (2002). International Evidence of Tax Smoothing in a Panel of Industrial Countries. Applied Economics, 34(18): 2325-2331 (Dec 2002). Published by Taylor & Francis (ISSN: 0003-6846). DOI:

Strazicich, M.C. (2002). International Evidence of Tax Smoothing in a Panel of Industrial Countries. Applied Economics, 34(18): 2325-2331 (Dec 2002). Published by Taylor & Francis (ISSN: 0003-6846). DOI:

Swedish Lessons: How Important are ICT and R&D to Economic Growth? Paper prepared for the 34 th IARIW General Conference, Dresden, Aug 21-27, 2016

Swedish Lessons: How Important are ICT and R&D to Economic Growth? Paper prepared for the 34 th IARIW General Conference, Dresden, Aug 21-27, 2016 Harald Edquist, Ericsson Research Magnus Henrekson, Research

Swedish Lessons: How Important are ICT and R&D to Economic Growth? Paper prepared for the 34 th IARIW General Conference, Dresden, Aug 21-27, 2016 Harald Edquist, Ericsson Research Magnus Henrekson, Research

Why so low for so long? A long-term view of real interest rates

Why so low for so long? A long-term view of real interest rates Claudio Borio, Piti Disyatat, and Phurichai Rungcharoenkitkul Bank of Finland/CEPR Conference, Demographics and the Macroeconomy, Helsinki,

Why so low for so long? A long-term view of real interest rates Claudio Borio, Piti Disyatat, and Phurichai Rungcharoenkitkul Bank of Finland/CEPR Conference, Demographics and the Macroeconomy, Helsinki,

Basic information. Tax-to-GDP ratio Date: 29 November 2010

Federal Department of Finance FDF Federal Finance Administration FFA Basic information Date: 29 November 2010 Tax-to-GDP ratio 2010 The tax-to-gdp ratio is the sum of all taxes and public levies in relation

Federal Department of Finance FDF Federal Finance Administration FFA Basic information Date: 29 November 2010 Tax-to-GDP ratio 2010 The tax-to-gdp ratio is the sum of all taxes and public levies in relation

EFFECT OF GENERAL UNCERTAINTY ON EARLY AND LATE VENTURE- CAPITAL INVESTMENTS: A CROSS-COUNTRY STUDY. Rajeev K. Goel* Illinois State University

DRAFT EFFECT OF GENERAL UNCERTAINTY ON EARLY AND LATE VENTURE- CAPITAL INVESTMENTS: A CROSS-COUNTRY STUDY Rajeev K. Goel* Illinois State University Iftekhar Hasan New Jersey Institute of Technology and

DRAFT EFFECT OF GENERAL UNCERTAINTY ON EARLY AND LATE VENTURE- CAPITAL INVESTMENTS: A CROSS-COUNTRY STUDY Rajeev K. Goel* Illinois State University Iftekhar Hasan New Jersey Institute of Technology and

When Credit Bites Back: Leverage, Business Cycles, and Crises

When Credit Bites Back: Leverage, Business Cycles, and Crises Òscar Jordà *, Moritz Schularick and Alan M. Taylor *Federal Reserve Bank of San Francisco and U.C. Davis, Free University of Berlin, and University

When Credit Bites Back: Leverage, Business Cycles, and Crises Òscar Jordà *, Moritz Schularick and Alan M. Taylor *Federal Reserve Bank of San Francisco and U.C. Davis, Free University of Berlin, and University

Internet Appendix: Government Debt and Corporate Leverage: International Evidence

Internet Appendix: Government Debt and Corporate Leverage: International Evidence Irem Demirci, Jennifer Huang, and Clemens Sialm September 3, 2018 1 Table A1: Variable Definitions This table details the

Internet Appendix: Government Debt and Corporate Leverage: International Evidence Irem Demirci, Jennifer Huang, and Clemens Sialm September 3, 2018 1 Table A1: Variable Definitions This table details the

Cyclical Convergence and Divergence in the Euro Area

Cyclical Convergence and Divergence in the Euro Area Presentation by Val Koromzay, Director for Country Studies, OECD to the Brussels Forum, April 2004 1 1 I. Introduction: Why is the issue important?

Cyclical Convergence and Divergence in the Euro Area Presentation by Val Koromzay, Director for Country Studies, OECD to the Brussels Forum, April 2004 1 1 I. Introduction: Why is the issue important?

Aggregate demand &long-run unemployment L. Ball 1999

Aggregate demand &long-run unemployment L. Ball 1999 Standard theory: equilibrium unemployment depends on labour market rigidities and institutional variables Monetary policy should focus on nominal stability,

Aggregate demand &long-run unemployment L. Ball 1999 Standard theory: equilibrium unemployment depends on labour market rigidities and institutional variables Monetary policy should focus on nominal stability,

Empirical appendix of Public Expenditure Distribution, Voting, and Growth

Empirical appendix of Public Expenditure Distribution, Voting, and Growth Lorenzo Burlon August 11, 2014 In this note we report the empirical exercises we conducted to motivate the theoretical insights

Empirical appendix of Public Expenditure Distribution, Voting, and Growth Lorenzo Burlon August 11, 2014 In this note we report the empirical exercises we conducted to motivate the theoretical insights

International Seminar on Strengthening Public Investment and Managing Fiscal Risks from Public-Private Partnerships

International Seminar on Strengthening Public Investment and Managing Fiscal Risks from Public-Private Partnerships Budapest, Hungary March 7 8, 2007 The views expressed in this paper are those of the

International Seminar on Strengthening Public Investment and Managing Fiscal Risks from Public-Private Partnerships Budapest, Hungary March 7 8, 2007 The views expressed in this paper are those of the

IMPLICATIONS OF LOW PRODUCTIVITY GROWTH FOR DEBT SUSTAINABILITY

IMPLICATIONS OF LOW PRODUCTIVITY GROWTH FOR DEBT SUSTAINABILITY Neil R. Mehrotra Brown University Peterson Institute for International Economics November 9th, 2017 1 / 13 PUBLIC DEBT AND PRODUCTIVITY GROWTH

IMPLICATIONS OF LOW PRODUCTIVITY GROWTH FOR DEBT SUSTAINABILITY Neil R. Mehrotra Brown University Peterson Institute for International Economics November 9th, 2017 1 / 13 PUBLIC DEBT AND PRODUCTIVITY GROWTH

Demographics and Secular Stagnation Hypothesis in Europe

Demographics and Secular Stagnation Hypothesis in Europe Carlo Favero (Bocconi University, IGIER) Vincenzo Galasso (Bocconi University, IGIER, CEPR & CESIfo) Growth in Europe?, Marseille, September 2015

Demographics and Secular Stagnation Hypothesis in Europe Carlo Favero (Bocconi University, IGIER) Vincenzo Galasso (Bocconi University, IGIER, CEPR & CESIfo) Growth in Europe?, Marseille, September 2015

on Inequality Monetary Policy, Macroprudential Regulation and Inequality Zurich, 3-4 October 2016

The Effects of Monetary Policy Shocks on Inequality Davide Furceri, Prakash Loungani and Aleksandra Zdzienicka International Monetary Fund Monetary Policy, Macroprudential Regulation and Inequality Zurich,

The Effects of Monetary Policy Shocks on Inequality Davide Furceri, Prakash Loungani and Aleksandra Zdzienicka International Monetary Fund Monetary Policy, Macroprudential Regulation and Inequality Zurich,

PORTUGAL E O CAMINHO PARA O FUTURO: A BANCA E O SEU PAPEL

XV CONFERÊNCIA A CRISE EUROPEIA E AS REFORMAS NECESSÁRIAS PORTUGAL E O CAMINHO PARA O FUTURO: A BANCA E O SEU PAPEL FERNANDO FARIA DE OLIVEIRA AGENDA European Context: From the Actual Crisis to Growth

XV CONFERÊNCIA A CRISE EUROPEIA E AS REFORMAS NECESSÁRIAS PORTUGAL E O CAMINHO PARA O FUTURO: A BANCA E O SEU PAPEL FERNANDO FARIA DE OLIVEIRA AGENDA European Context: From the Actual Crisis to Growth

The Velocity of Money and Nominal Interest Rates: Evidence from Developed and Latin-American Countries

The Velocity of Money and Nominal Interest Rates: Evidence from Developed and Latin-American Countries Petr Duczynski Abstract This study examines the behavior of the velocity of money in developed and

The Velocity of Money and Nominal Interest Rates: Evidence from Developed and Latin-American Countries Petr Duczynski Abstract This study examines the behavior of the velocity of money in developed and

Income smoothing and foreign asset holdings

J Econ Finan (2010) 34:23 29 DOI 10.1007/s12197-008-9070-2 Income smoothing and foreign asset holdings Faruk Balli Rosmy J. Louis Mohammad Osman Published online: 24 December 2008 Springer Science + Business

J Econ Finan (2010) 34:23 29 DOI 10.1007/s12197-008-9070-2 Income smoothing and foreign asset holdings Faruk Balli Rosmy J. Louis Mohammad Osman Published online: 24 December 2008 Springer Science + Business

University of Macedonia Department of Economics. Discussion Paper Series. Inflation, inflation uncertainty and growth: are they related?

ISSN 1791-3144 University of Macedonia Department of Economics Discussion Paper Series Inflation, inflation uncertainty and growth: are they related? Stilianos Fountas Discussion Paper No. 12/2010 Department

ISSN 1791-3144 University of Macedonia Department of Economics Discussion Paper Series Inflation, inflation uncertainty and growth: are they related? Stilianos Fountas Discussion Paper No. 12/2010 Department

Distribution Capital and the Short and Long Run Import Demand Elasticity M.J. Crucini and J.S. Davis

Distribution Capital and the Short and Long Run Import Demand Elasticity M.J. Crucini and J.S. Davis Discussant: Andrea Rao Board of Governors of the Federal Reserve System CD (2012): Motivation The trade

Distribution Capital and the Short and Long Run Import Demand Elasticity M.J. Crucini and J.S. Davis Discussant: Andrea Rao Board of Governors of the Federal Reserve System CD (2012): Motivation The trade

UK labour productivity since the onset of the crisis an international and historical perspective.

1 UK labour productivity since the onset of the crisis an international and historical perspective. OECD workshop on productivity Jumana Saleheen 5 November 2012 Bank of England Quarterly Bulletin article,

1 UK labour productivity since the onset of the crisis an international and historical perspective. OECD workshop on productivity Jumana Saleheen 5 November 2012 Bank of England Quarterly Bulletin article,

Sovereign Bond Yield Spreads: An International Analysis Giuseppe Corvasce

Sovereign Bond Yield Spreads: An International Analysis Giuseppe Corvasce Rutgers University Center for Financial Statistics and Risk Management Society for Financial Studies 8 th Financial Risks and INTERNATIONAL

Sovereign Bond Yield Spreads: An International Analysis Giuseppe Corvasce Rutgers University Center for Financial Statistics and Risk Management Society for Financial Studies 8 th Financial Risks and INTERNATIONAL

Monetary policy regimes and exchange rate fluctuations

Seðlabanki Íslands Monetary policy regimes and exchange rate fluctuations The views are of the author and do not necessarily reflect those of the Central Bank of Iceland Thórarinn G. Pétursson Central

Seðlabanki Íslands Monetary policy regimes and exchange rate fluctuations The views are of the author and do not necessarily reflect those of the Central Bank of Iceland Thórarinn G. Pétursson Central

Modelling and predicting labor force productivity

Modelling and predicting labor force productivity Ivan O. Kitov, Oleg I. Kitov Abstract Labor productivity in Turkey, Spain, Belgium, Austria, Switzerland, and New Zealand has been analyzed and modeled.

Modelling and predicting labor force productivity Ivan O. Kitov, Oleg I. Kitov Abstract Labor productivity in Turkey, Spain, Belgium, Austria, Switzerland, and New Zealand has been analyzed and modeled.

Economics Program Working Paper Series

Economics Program Working Paper Series Projecting Economic Growth with Growth Accounting Techniques: The Conference Board Global Economic Outlook 2012 Sources and Methods Vivian Chen Ben Cheng Gad Levanon

Economics Program Working Paper Series Projecting Economic Growth with Growth Accounting Techniques: The Conference Board Global Economic Outlook 2012 Sources and Methods Vivian Chen Ben Cheng Gad Levanon

Volume 31, Issue 1. Florence Huart University Lille 1

Volume 31, Issue 1 Has fiscal discretion during good times and bad times changed in the euro area countries? Florence Huart University Lille 1 Abstract We study the relationship between the change in the

Volume 31, Issue 1 Has fiscal discretion during good times and bad times changed in the euro area countries? Florence Huart University Lille 1 Abstract We study the relationship between the change in the

THE CONCEPT OF globalization has recently been the subject of considerable. International Evidence on the Determinants of Trade Dynamics

IMF Staff Papers Vol. 45, No. 3 (September 1998) 1998 International Monetary Fund International Evidence on the Determinants of Trade Dynamics ESWAR S. PRASAD and JEFFERY A. GABLE* This paper provides

IMF Staff Papers Vol. 45, No. 3 (September 1998) 1998 International Monetary Fund International Evidence on the Determinants of Trade Dynamics ESWAR S. PRASAD and JEFFERY A. GABLE* This paper provides

Growth has peaked amidst escalating risks

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

San Francisco Retiree Health Care Trust Fund Education Materials on Public Equity

M E K E T A I N V E S T M E N T G R O U P 5796 ARMADA DRIVE SUITE 110 CARLSBAD CA 92008 760 795 3450 fax 760 795 3445 www.meketagroup.com The Global Equity Opportunity Set MSCI All Country World 1 Index

M E K E T A I N V E S T M E N T G R O U P 5796 ARMADA DRIVE SUITE 110 CARLSBAD CA 92008 760 795 3450 fax 760 795 3445 www.meketagroup.com The Global Equity Opportunity Set MSCI All Country World 1 Index

The impact of global financial crisis on business cycles in Asian emerging economies by Jarko Fidrmuc and Iikka Korhonen

The impact of global financial crisis on business cycles in Asian emerging economies by Jarko Fidrmuc and Iikka Korhonen Discussion by Radhika Pandey National Institute of Public Finance and Policy, New

The impact of global financial crisis on business cycles in Asian emerging economies by Jarko Fidrmuc and Iikka Korhonen Discussion by Radhika Pandey National Institute of Public Finance and Policy, New

Basic information. Tax-to-GDP ratio Date: 24 October 2012

Federal Department of Finance FDF Federal Finance Administration FFA Basic information Date: 24 October 2012 Tax-to-GDP ratio 2011 The tax-to-gdp ratio is the sum of all taxes and social security levies

Federal Department of Finance FDF Federal Finance Administration FFA Basic information Date: 24 October 2012 Tax-to-GDP ratio 2011 The tax-to-gdp ratio is the sum of all taxes and social security levies

INFLATION TARGETING AND INDIA

INFLATION TARGETING AND INDIA CAN MONETARY POLICY IN INDIA FOLLOW INFLATION TARGETING AND ARE THE MONETARY POLICY REACTION FUNCTIONS ASYMMETRIC? Abstract Vineeth Mohandas Department of Economics, Pondicherry

INFLATION TARGETING AND INDIA CAN MONETARY POLICY IN INDIA FOLLOW INFLATION TARGETING AND ARE THE MONETARY POLICY REACTION FUNCTIONS ASYMMETRIC? Abstract Vineeth Mohandas Department of Economics, Pondicherry

Market Allocation Platform Guiding investment decisions to maximize ROI. Tourism Economics

Market Allocation Platform Guiding investment decisions to maximize ROI Tourism Economics core services Travel data and forecasts for 190 countries, 50 states, and 300 cities Policy analysis and recommendations

Market Allocation Platform Guiding investment decisions to maximize ROI Tourism Economics core services Travel data and forecasts for 190 countries, 50 states, and 300 cities Policy analysis and recommendations

Trust and Fertility Dynamics. Arnstein Aassve, Università Bocconi Francesco C. Billari, University of Oxford Léa Pessin, Universitat Pompeu Fabra

Trust and Fertility Dynamics Arnstein Aassve, Università Bocconi Francesco C. Billari, University of Oxford Léa Pessin, Universitat Pompeu Fabra 1 Background Fertility rates across OECD countries differ

Trust and Fertility Dynamics Arnstein Aassve, Università Bocconi Francesco C. Billari, University of Oxford Léa Pessin, Universitat Pompeu Fabra 1 Background Fertility rates across OECD countries differ

Algorithmic Order Guide

Algorithmic Order Guide STRATEGIES SUPPORTED MARKETS... 3 VWAP... 4 TWAP... 5 WITH VOLUME... 6 IMPLEMENTATION SHORTFALL... 7 PRE-MARKET LIMIT... 8 ICEBERG... 9 RELOAD...10 DARK....11 2 / 11 SUPPORTED MARKETS

Algorithmic Order Guide STRATEGIES SUPPORTED MARKETS... 3 VWAP... 4 TWAP... 5 WITH VOLUME... 6 IMPLEMENTATION SHORTFALL... 7 PRE-MARKET LIMIT... 8 ICEBERG... 9 RELOAD...10 DARK....11 2 / 11 SUPPORTED MARKETS

Table 1: Foreign exchange turnover: Summary of surveys Billions of U.S. dollars. Number of business days

Table 1: Foreign exchange turnover: Summary of surveys Billions of U.S. dollars Total turnover Number of business days Average daily turnover change 1983 103.2 20 5.2 1986 191.2 20 9.6 84.6 1989 299.9

Table 1: Foreign exchange turnover: Summary of surveys Billions of U.S. dollars Total turnover Number of business days Average daily turnover change 1983 103.2 20 5.2 1986 191.2 20 9.6 84.6 1989 299.9

Lecture 1: Traditional Open Macro Models and Monetary Policy

Lecture 1: Traditional Open Macro Models and Monetary Policy Isabelle Méjean isabelle.mejean@polytechnique.edu http://mejean.isabelle.googlepages.com/ Master Economics and Public Policy, International

Lecture 1: Traditional Open Macro Models and Monetary Policy Isabelle Méjean isabelle.mejean@polytechnique.edu http://mejean.isabelle.googlepages.com/ Master Economics and Public Policy, International

Trade in Services Between Enterprises of the Same Group

Trade in Services Between Enterprises of the Same Group Workshop on Statistics of International Trade in Services IBGE, Rio de Janeiro, Brazil December 1-4, 1 2009 Balance of Payments Division - Department

Trade in Services Between Enterprises of the Same Group Workshop on Statistics of International Trade in Services IBGE, Rio de Janeiro, Brazil December 1-4, 1 2009 Balance of Payments Division - Department

Fundamental and Non-Fundamental Explanations for House Price Fluctuations

Fundamental and Non-Fundamental Explanations for House Price Fluctuations Christian Hott Economic Advice 1 Unexplained Real Estate Crises Several countries were affected by a real estate crisis in recent

Fundamental and Non-Fundamental Explanations for House Price Fluctuations Christian Hott Economic Advice 1 Unexplained Real Estate Crises Several countries were affected by a real estate crisis in recent

Carry. Ralph S.J. Koijen, London Business School and NBER

Carry Ralph S.J. Koijen, London Business School and NBER Tobias J. Moskowitz, Chicago Booth and NBER Lasse H. Pedersen, NYU, CBS, AQR Capital Management, CEPR, NBER Evert B. Vrugt, VU University, PGO IM

Carry Ralph S.J. Koijen, London Business School and NBER Tobias J. Moskowitz, Chicago Booth and NBER Lasse H. Pedersen, NYU, CBS, AQR Capital Management, CEPR, NBER Evert B. Vrugt, VU University, PGO IM

What Happens During Recessions, Crunches and Busts?

What Happens During Recessions, Crunches and Busts? Stijn Claessens, M. Ayhan Kose and Marco E. Terrones Financial Studies Division, Research Department International Monetary Fund Presentation at the

What Happens During Recessions, Crunches and Busts? Stijn Claessens, M. Ayhan Kose and Marco E. Terrones Financial Studies Division, Research Department International Monetary Fund Presentation at the

The Balassa-Samuelson Effect and The MEVA G10 FX Model

The Balassa-Samuelson Effect and The MEVA G10 FX Model Abstract: In this study, we introduce Danske s Medium Term FX Evaluation model (MEVA G10 FX), a framework that falls within the class of the Behavioural

The Balassa-Samuelson Effect and The MEVA G10 FX Model Abstract: In this study, we introduce Danske s Medium Term FX Evaluation model (MEVA G10 FX), a framework that falls within the class of the Behavioural

ANNEX 3. The ins and outs of the Baltic unemployment rates

ANNEX 3. The ins and outs of the Baltic unemployment rates Introduction 3 The unemployment rate in the Baltic States is volatile. During the last recession the trough-to-peak increase in the unemployment

ANNEX 3. The ins and outs of the Baltic unemployment rates Introduction 3 The unemployment rate in the Baltic States is volatile. During the last recession the trough-to-peak increase in the unemployment

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York 1 Global macroeconomic trends Major headwinds Risks and uncertainties Policy questions and

Hamid Rashid, Ph.D. Chief Global Economic Monitoring Unit Development Policy Analysis Division UNDESA, New York 1 Global macroeconomic trends Major headwinds Risks and uncertainties Policy questions and

Heraklis Polemarchakis The Debt of Nations

Heraklis Polemarchakis The Debt of Nations The Crisis in the Euro Area Bank of Greece, Vouliagmeni, May 23 24, 2013 Outline An overview of numbers across the world Total for advanced economies Why Does

Heraklis Polemarchakis The Debt of Nations The Crisis in the Euro Area Bank of Greece, Vouliagmeni, May 23 24, 2013 Outline An overview of numbers across the world Total for advanced economies Why Does

Gernot Müller (University of Bonn, CEPR, and Ifo)

") Exchange rate regimes and fiscal multipliers Benjamin Born (Ifo Institute) Falko Jüßen (TU Dortmund and IZA) Gernot Müller (University of Bonn, CEPR, and Ifo) Fiscal Policy in the Aftermath of the Financial

Exchange rate regimes and fiscal multipliers Benjamin Born (Ifo Institute) Falko Jüßen (TU Dortmund and IZA) Gernot Müller (University of Bonn, CEPR, and Ifo) Fiscal Policy in the Aftermath of the Financial

Recognize the Relative Advantages of Natural Resource Equities vs. Commodities

Recognize the Relative Advantages of Natural Resource Equities vs. Commodities Investors look to the commodity market to provide three primary benefits: portfolio diversification, inflation protection,

Recognize the Relative Advantages of Natural Resource Equities vs. Commodities Investors look to the commodity market to provide three primary benefits: portfolio diversification, inflation protection,

PENSION FUND MANAGEMENT AND INTERNATIONAL INVESTMENT A GLOBAL PERSPECTIVE

PENSION FUND MANAGEMENT AND INTERNATIONAL INVESTMENT A GLOBAL PERSPECTIVE E Philip Davis Brunel University, West London e_philip_davis@msn.com www.geocities.com/e_philip_davis groups.yahoo.com/group/financial_stability

PENSION FUND MANAGEMENT AND INTERNATIONAL INVESTMENT A GLOBAL PERSPECTIVE E Philip Davis Brunel University, West London e_philip_davis@msn.com www.geocities.com/e_philip_davis groups.yahoo.com/group/financial_stability

Market Overview As of 1/31/2019

Asset Class Leadership Periodic Table Worst Best 78.51 58.21 41.45 37.21 34.47 27.45 26.46 20.58 19.69 29.09 27.58 2 18.88 16.71 15.51 15.12 15.06 11.15 7.84 7.28 4.98 2.64 2.11 0.39-2.91-5.50-13.71 20.14

Asset Class Leadership Periodic Table Worst Best 78.51 58.21 41.45 37.21 34.47 27.45 26.46 20.58 19.69 29.09 27.58 2 18.88 16.71 15.51 15.12 15.06 11.15 7.84 7.28 4.98 2.64 2.11 0.39-2.91-5.50-13.71 20.14

Household Balance Sheets and Debt an International Country Study

47 Household Balance Sheets and Debt an International Country Study Jacob Isaksen, Paul Lassenius Kramp, Louise Funch Sørensen and Søren Vester Sørensen, Economics INTRODUCTION AND SUMMARY What are the

47 Household Balance Sheets and Debt an International Country Study Jacob Isaksen, Paul Lassenius Kramp, Louise Funch Sørensen and Søren Vester Sørensen, Economics INTRODUCTION AND SUMMARY What are the

Market Overview As of 4/30/2018

Asset Class Leadership Periodic Table Worst Best 5.24-26.16-28.92-36.85-37.00-37.34-38.44-38.54-45.53 78.51 58.21 41.45 37.21 34.47 27.45 26.46 20.58 19.69 29.09 27.58 24.50 18.88 16.71 15.51 15.12 15.06

Asset Class Leadership Periodic Table Worst Best 5.24-26.16-28.92-36.85-37.00-37.34-38.44-38.54-45.53 78.51 58.21 41.45 37.21 34.47 27.45 26.46 20.58 19.69 29.09 27.58 24.50 18.88 16.71 15.51 15.12 15.06

Market Overview As of 11/30/2018

Asset Class Leadership Periodic Table Worst Best 5.24-26.16-28.92-36.85-37.00-37.34-38.44-38.54-45.53 78.51 58.21 41.45 37.21 34.47 27.45 26.46 20.58 19.69 29.09 27.58 24.50 18.88 16.71 15.51 15.12 15.06

Asset Class Leadership Periodic Table Worst Best 5.24-26.16-28.92-36.85-37.00-37.34-38.44-38.54-45.53 78.51 58.21 41.45 37.21 34.47 27.45 26.46 20.58 19.69 29.09 27.58 24.50 18.88 16.71 15.51 15.12 15.06

1000G 1000G HY

Asset Class Leadership Periodic Table Worst Best 5.24-26.16-28.92-36.85-37.00-37.34-38.44-38.54-45.53 78.51 58.21 41.45 37.21 34.47 27.45 26.46 20.58 19.69 29.09 27.58 24.50 18.88 16.71 15.51 15.12 15.06

Asset Class Leadership Periodic Table Worst Best 5.24-26.16-28.92-36.85-37.00-37.34-38.44-38.54-45.53 78.51 58.21 41.45 37.21 34.47 27.45 26.46 20.58 19.69 29.09 27.58 24.50 18.88 16.71 15.51 15.12 15.06

INSTITUTIONS AND GROWTH

Research Reports The institutional climate and economic growth INSTITUTIONS AND GROWTH IN OECD COUNTRIES The Ifo Institution Climate was created with the express intent of highlighting the key underlying

Research Reports The institutional climate and economic growth INSTITUTIONS AND GROWTH IN OECD COUNTRIES The Ifo Institution Climate was created with the express intent of highlighting the key underlying

CARRY TRADE: THE GAINS OF DIVERSIFICATION

CARRY TRADE: THE GAINS OF DIVERSIFICATION Craig Burnside Duke University Martin Eichenbaum Northwestern University Sergio Rebelo Northwestern University Abstract Market participants routinely take advantage

CARRY TRADE: THE GAINS OF DIVERSIFICATION Craig Burnside Duke University Martin Eichenbaum Northwestern University Sergio Rebelo Northwestern University Abstract Market participants routinely take advantage

Business Investment in the United States: Facts, Explana9ons, Puzzles, and Policies d Jason Furman Chairman, Council of Economic Advisers

Business Investment in the United States: Facts, Explana9ons, Puzzles, and Policies d Jason Furman Chairman, Council of Economic Advisers Progressive Policy Ins9tute September 3, 215 Note: Shading denotes

Business Investment in the United States: Facts, Explana9ons, Puzzles, and Policies d Jason Furman Chairman, Council of Economic Advisers Progressive Policy Ins9tute September 3, 215 Note: Shading denotes

Country Size Premiums and Global Equity Portfolio Structure

RESEARCH Country Size Premiums and Global Equity Portfolio Structure This paper examines the relation between aggregate country equity market capitalizations and country-level market index returns. Our

RESEARCH Country Size Premiums and Global Equity Portfolio Structure This paper examines the relation between aggregate country equity market capitalizations and country-level market index returns. Our

OUTLOOK FOR THE NEW ZEALAND GOVERNMENT DEBT MARKET. 1 The Treasury

OUTLOOK FOR THE NEW ZEALAND GOVERNMENT DEBT MARKET 1 The Treasury TODAY Economic outlook New Zealand Government: risk/reward Fiscal priorities NZDMO s strategy What to watch for 2 1. ECONOMIC OUTLOOK 3

OUTLOOK FOR THE NEW ZEALAND GOVERNMENT DEBT MARKET 1 The Treasury TODAY Economic outlook New Zealand Government: risk/reward Fiscal priorities NZDMO s strategy What to watch for 2 1. ECONOMIC OUTLOOK 3

Market Overview As of 8/31/2017

Asset Class Leadership Periodic Table Worst Best 39.42 16.65 11.81 7.05 6.97 5.49 1.87-0.17-9.78 5.24-26.16-28.92-36.85-37.00-37.34-38.44-38.54-45.53 78.51 58.21 41.45 37.21 34.47 27.45 26.46 20.58 19.69

Asset Class Leadership Periodic Table Worst Best 39.42 16.65 11.81 7.05 6.97 5.49 1.87-0.17-9.78 5.24-26.16-28.92-36.85-37.00-37.34-38.44-38.54-45.53 78.51 58.21 41.45 37.21 34.47 27.45 26.46 20.58 19.69

Saving, Investment, and the Financial System. Premium PowerPoint Slides by Ron Cronovich, Updated by Vance Ginn

C H A P T E R 26 Saving, Investment, and the Financial System Economics P R I N C I P L E S O F N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich, Updated by Vance Ginn 2009 South-Western, a

C H A P T E R 26 Saving, Investment, and the Financial System Economics P R I N C I P L E S O F N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich, Updated by Vance Ginn 2009 South-Western, a

Market Overview As of 10/31/2017

Asset Class Leadership Periodic Table Worst Best 39.42 16.65 11.81 7.05 6.97 5.49 1.87-0.17-9.78 5.24-26.16-28.92-36.85-37.00-37.34-38.44-38.54-45.53 78.51 58.21 41.45 37.21 34.47 27.45 26.46 20.58 19.69

Asset Class Leadership Periodic Table Worst Best 39.42 16.65 11.81 7.05 6.97 5.49 1.87-0.17-9.78 5.24-26.16-28.92-36.85-37.00-37.34-38.44-38.54-45.53 78.51 58.21 41.45 37.21 34.47 27.45 26.46 20.58 19.69

The Yield Curve as a Predictor of Economic Activity the Case of the EU- 15

The Yield Curve as a Predictor of Economic Activity the Case of the EU- 15 Jana Hvozdenska Masaryk University Faculty of Economics and Administration, Department of Finance Lipova 41a Brno, 602 00 Czech

The Yield Curve as a Predictor of Economic Activity the Case of the EU- 15 Jana Hvozdenska Masaryk University Faculty of Economics and Administration, Department of Finance Lipova 41a Brno, 602 00 Czech

Mortgage Lending, Banking Crises and Financial Stability in Asia

Mortgage Lending, Banking Crises and Financial Stability in Asia Peter J. Morgan Sr. Consultant for Research Yan Zhang Consultant Asian Development Bank Institute ABFER Conference on Financial Regulations:

Mortgage Lending, Banking Crises and Financial Stability in Asia Peter J. Morgan Sr. Consultant for Research Yan Zhang Consultant Asian Development Bank Institute ABFER Conference on Financial Regulations:

DANMARKS NATIONALBANK

DANMARKS NATIONALBANK WEALTH, DEBT AND MACROECONOMIC STABILITY Niels Lynggård Hansen, Head of Economics and Monetary Policy. IARIW, Copenhagen, 21 August 2018 Agenda Descriptive evidence on household debt

DANMARKS NATIONALBANK WEALTH, DEBT AND MACROECONOMIC STABILITY Niels Lynggård Hansen, Head of Economics and Monetary Policy. IARIW, Copenhagen, 21 August 2018 Agenda Descriptive evidence on household debt

Structural Cointegration Analysis of Private and Public Investment

International Journal of Business and Economics, 2002, Vol. 1, No. 1, 59-67 Structural Cointegration Analysis of Private and Public Investment Rosemary Rossiter * Department of Economics, Ohio University,

International Journal of Business and Economics, 2002, Vol. 1, No. 1, 59-67 Structural Cointegration Analysis of Private and Public Investment Rosemary Rossiter * Department of Economics, Ohio University,

Getting ready to prevent and tame another house price bubble

Macroprudential policy conference Should macroprudential policy target real estate prices? 11-12 May 2017, Vilnius Getting ready to prevent and tame another house price bubble Tomas Garbaravičius Board

Macroprudential policy conference Should macroprudential policy target real estate prices? 11-12 May 2017, Vilnius Getting ready to prevent and tame another house price bubble Tomas Garbaravičius Board

Transmission of Financial and Real Shocks in the Global Economy Using the GVAR

Transmission of Financial and Real Shocks in the Global Economy Using the GVAR Hashem Pesaran University of Cambridge For presentation at Conference on The Big Crunch and the Big Bang, Cambridge, November

Transmission of Financial and Real Shocks in the Global Economy Using the GVAR Hashem Pesaran University of Cambridge For presentation at Conference on The Big Crunch and the Big Bang, Cambridge, November

Lecture 9: Intermediate macroeconomics, autumn Lars Calmfors

Lecture 9: Intermediate macroeconomics, autumn 2008 Lars Calmfors 1 Theory of consumption Keynesian consumption function C = C(Y T) Consumption depends on current disposable income 0 < MPC < 1 But it is

Lecture 9: Intermediate macroeconomics, autumn 2008 Lars Calmfors 1 Theory of consumption Keynesian consumption function C = C(Y T) Consumption depends on current disposable income 0 < MPC < 1 But it is

Growth in OECD Unit Labour Costs slows to 0.4% in the third quarter of 2016

Growth in OECD Unit Labour Costs slows to.4% in the third quarter of 26 Growth in unit labour costs (ULCs) in the OECD area slowed to.4% in the third quarter of 26 (compared with.6% in the previous quarter)

Growth in OECD Unit Labour Costs slows to.4% in the third quarter of 26 Growth in unit labour costs (ULCs) in the OECD area slowed to.4% in the third quarter of 26 (compared with.6% in the previous quarter)

THE ROLE OF EXCHANGE RATES IN MONETARY POLICY RULE: THE CASE OF INFLATION TARGETING COUNTRIES

THE ROLE OF EXCHANGE RATES IN MONETARY POLICY RULE: THE CASE OF INFLATION TARGETING COUNTRIES Mahir Binici Central Bank of Turkey Istiklal Cad. No:10 Ulus, Ankara/Turkey E-mail: mahir.binici@tcmb.gov.tr

THE ROLE OF EXCHANGE RATES IN MONETARY POLICY RULE: THE CASE OF INFLATION TARGETING COUNTRIES Mahir Binici Central Bank of Turkey Istiklal Cad. No:10 Ulus, Ankara/Turkey E-mail: mahir.binici@tcmb.gov.tr

Some Basic Facts about Government Expenditures and Taxation in Canada. Econ 525

Some Basic Facts about Government Expenditures and Taxation in Canada Econ 525 Revenues and Expenditures in Canada Since we re studying the role of government in this course it is worth considering some

Some Basic Facts about Government Expenditures and Taxation in Canada Econ 525 Revenues and Expenditures in Canada Since we re studying the role of government in this course it is worth considering some

assumption. Use these two equations and your earlier result to derive an expression for consumption per worker in steady state.

Tutorial sheet 2 for UBC Macroeconomics Martin Ellison, 2018 Exercise on consumption in the Solow growth model The Solow growth model is in steady-state when investment ss YY tt is exactly offset by depreciation

Tutorial sheet 2 for UBC Macroeconomics Martin Ellison, 2018 Exercise on consumption in the Solow growth model The Solow growth model is in steady-state when investment ss YY tt is exactly offset by depreciation

Trade and Development Board Sixty-first session. Geneva, September 2014

UNITED NATIONS CONFERENCE ON TRADE AND DEVELOPMENT Trade and Development Board Sixty-first session Geneva, 15 26 September 2014 Item 3: High-level segment Tackling inequality through trade and development:

UNITED NATIONS CONFERENCE ON TRADE AND DEVELOPMENT Trade and Development Board Sixty-first session Geneva, 15 26 September 2014 Item 3: High-level segment Tackling inequality through trade and development:

Consumption, Income and Wealth

59 Consumption, Income and Wealth Jens Bang-Andersen, Tina Saaby Hvolbøl, Paul Lassenius Kramp and Casper Ristorp Thomsen, Economics INTRODUCTION AND SUMMARY In Denmark, private consumption accounts for

59 Consumption, Income and Wealth Jens Bang-Andersen, Tina Saaby Hvolbøl, Paul Lassenius Kramp and Casper Ristorp Thomsen, Economics INTRODUCTION AND SUMMARY In Denmark, private consumption accounts for

What Can Macroeconometric Models Say About Asia-Type Crises?

What Can Macroeconometric Models Say About Asia-Type Crises? Ray C. Fair May 1999 Abstract This paper uses a multicountry econometric model to examine Asia-type crises. Experiments are run for Thailand,

What Can Macroeconometric Models Say About Asia-Type Crises? Ray C. Fair May 1999 Abstract This paper uses a multicountry econometric model to examine Asia-type crises. Experiments are run for Thailand,

The macroeconomic effects of a carbon tax in the Netherlands Íde Kearney, 13 th September 2018.

The macroeconomic effects of a carbon tax in the Netherlands Íde Kearney, th September 08. This note reports estimates of the economic impact of introducing a carbon tax of 50 per ton of CO in the Netherlands.

The macroeconomic effects of a carbon tax in the Netherlands Íde Kearney, th September 08. This note reports estimates of the economic impact of introducing a carbon tax of 50 per ton of CO in the Netherlands.

Trade in Services Between Enterprises of the Same Group

Trade in Between Enterprises of the Same Group Workshop on Statistics of International Trade in IBGE, Rio de Janeiro, 1-4 December, 2009 (Balance of Payments Division / Department of Economics Banco Central

Trade in Between Enterprises of the Same Group Workshop on Statistics of International Trade in IBGE, Rio de Janeiro, 1-4 December, 2009 (Balance of Payments Division / Department of Economics Banco Central

Financial Integration, Financial Deepness and Global Imbalances

Financial Integration, Financial Deepness and Global Imbalances Enrique G. Mendoza University of Maryland, IMF & NBER Vincenzo Quadrini University of Southern California, CEPR & NBER José-Víctor Ríos-Rull

Financial Integration, Financial Deepness and Global Imbalances Enrique G. Mendoza University of Maryland, IMF & NBER Vincenzo Quadrini University of Southern California, CEPR & NBER José-Víctor Ríos-Rull

V Time Varying Covariance and Correlation. Covariances and Correlations

V Time Varying Covariance and Correlation DEFINITION OF CORRELATIONS ARE THEY TIME VARYING? WHY DO WE NEED THEM? ONE FACTOR ARCH MODEL DYNAMIC CONDITIONAL CORRELATIONS ASSET ALLOCATION THE VALUE OF CORRELATION

V Time Varying Covariance and Correlation DEFINITION OF CORRELATIONS ARE THEY TIME VARYING? WHY DO WE NEED THEM? ONE FACTOR ARCH MODEL DYNAMIC CONDITIONAL CORRELATIONS ASSET ALLOCATION THE VALUE OF CORRELATION

RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO OCTOBER 2003

OCTOBER 23 RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO 2 RECENT DEVELOPMENTS OUTLOOK MEDIUM-TERM CHALLENGES 3 RECENT DEVELOPMENTS In tandem with the global economic cycle, the Mexican

OCTOBER 23 RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO 2 RECENT DEVELOPMENTS OUTLOOK MEDIUM-TERM CHALLENGES 3 RECENT DEVELOPMENTS In tandem with the global economic cycle, the Mexican

When Credit Bites Back: Leverage, Business Cycles, and Crises

When Credit Bites Back: Leverage, Business Cycles, and Crises Òscar Jordà *, Moritz Schularick and Alan M. Taylor *Federal Reserve Bank of San Francisco and U.C. Davis, Free University of Berlin, and University

When Credit Bites Back: Leverage, Business Cycles, and Crises Òscar Jordà *, Moritz Schularick and Alan M. Taylor *Federal Reserve Bank of San Francisco and U.C. Davis, Free University of Berlin, and University

Fiscal and Monetary Policies: Background

Fiscal and Monetary Policies: Background Behzad Diba University of Bern April 2012 (Institute) Fiscal and Monetary Policies: Background April 2012 1 / 19 Research Areas Research on fiscal policy typically

Fiscal and Monetary Policies: Background Behzad Diba University of Bern April 2012 (Institute) Fiscal and Monetary Policies: Background April 2012 1 / 19 Research Areas Research on fiscal policy typically

Issue Brief for Congress

Order Code IB91078 Issue Brief for Congress Received through the CRS Web Value-Added Tax as a New Revenue Source Updated January 29, 2003 James M. Bickley Government and Finance Division Congressional

Order Code IB91078 Issue Brief for Congress Received through the CRS Web Value-Added Tax as a New Revenue Source Updated January 29, 2003 James M. Bickley Government and Finance Division Congressional

The Cyprus Economy: from Recovery to Sustainable Growth. Vincenzo Guzzo Resident Representative in Cyprus

The Economy: from Recovery to Sustainable Growth Vincenzo Guzzo Resident Representative in Growth momentum remains strong 18 : Real GDP ( billion) 1 Deviation from Pre-Crisis Level and Trend (Percent)

The Economy: from Recovery to Sustainable Growth Vincenzo Guzzo Resident Representative in Growth momentum remains strong 18 : Real GDP ( billion) 1 Deviation from Pre-Crisis Level and Trend (Percent)

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 24

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 24 I. OVERVIEW A. Framework B. Topics POLICY RESPONSES TO FINANCIAL CRISES APRIL 23, 2018 II.

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor Christina Romer LECTURE 24 I. OVERVIEW A. Framework B. Topics POLICY RESPONSES TO FINANCIAL CRISES APRIL 23, 2018 II.

Hong Kong s Experience

Cross Border Issues IMF Conference on Operationalizing Systemic Risk Monitoring Washington, D. C. 26 May 21 Hong Kong s Experience Dong He Executive Director (Research) Hong Kong Monetary Authority 1 Outline

Cross Border Issues IMF Conference on Operationalizing Systemic Risk Monitoring Washington, D. C. 26 May 21 Hong Kong s Experience Dong He Executive Director (Research) Hong Kong Monetary Authority 1 Outline

Overview. o Introduction. o Review of Literature. o Methodology and Data. o Findings and Discussion. o Conclusion

o Introduction Overview o Review of Literature o Methodology and Data o Findings and Discussion o Conclusion Introduction An economy has comparative advantage if it is more productive than another. Some

o Introduction Overview o Review of Literature o Methodology and Data o Findings and Discussion o Conclusion Introduction An economy has comparative advantage if it is more productive than another. Some

Constraints on Exchange Rate Flexibility in Transition Economies: a Meta-Regression Analysis of Exchange Rate Pass-Through

Constraints on Exchange Rate Flexibility in Transition Economies: a Meta-Regression Analysis of Exchange Rate Pass-Through Igor Velickovski & Geoffrey Pugh Applied Economics 43 (27), 2011 National Bank

Constraints on Exchange Rate Flexibility in Transition Economies: a Meta-Regression Analysis of Exchange Rate Pass-Through Igor Velickovski & Geoffrey Pugh Applied Economics 43 (27), 2011 National Bank

GDP, Share Prices, and Share Returns: Australian and New Zealand Evidence

Journal of Money, Investment and Banking ISSN 1450-288X Issue 5 (2008) EuroJournals Publishing, Inc. 2008 http://www.eurojournals.com/finance.htm GDP, Share Prices, and Share Returns: Australian and New

Journal of Money, Investment and Banking ISSN 1450-288X Issue 5 (2008) EuroJournals Publishing, Inc. 2008 http://www.eurojournals.com/finance.htm GDP, Share Prices, and Share Returns: Australian and New

A prolonged period of low real interest rates? 1

A prolonged period of low real interest rates? 1 Olivier J Blanchard, Davide Furceri and Andrea Pescatori International Monetary Fund From a peak of about 5% in 1986, the world real interest rate fell

A prolonged period of low real interest rates? 1 Olivier J Blanchard, Davide Furceri and Andrea Pescatori International Monetary Fund From a peak of about 5% in 1986, the world real interest rate fell

Regulatory Arbitrage in Action: Evidence from Banking Flows and Macroprudential Policy

Regulatory Arbitrage in Action: Evidence from Banking Flows and Macroprudential Policy Dennis Reinhardt and Rhiannon Sowerbutts Bank of England April 2016 Central Bank of Iceland, Systemic Risk Centre

Regulatory Arbitrage in Action: Evidence from Banking Flows and Macroprudential Policy Dennis Reinhardt and Rhiannon Sowerbutts Bank of England April 2016 Central Bank of Iceland, Systemic Risk Centre

The Bilateral J-Curve: Sweden versus her 17 Major Trading Partners

Bahmani-Oskooee and Ratha, International Journal of Applied Economics, 4(1), March 2007, 1-13 1 The Bilateral J-Curve: Sweden versus her 17 Major Trading Partners Mohsen Bahmani-Oskooee and Artatrana Ratha

Bahmani-Oskooee and Ratha, International Journal of Applied Economics, 4(1), March 2007, 1-13 1 The Bilateral J-Curve: Sweden versus her 17 Major Trading Partners Mohsen Bahmani-Oskooee and Artatrana Ratha

Developing Housing Finance Systems

Developing Housing Finance Systems Veronica Cacdac Warnock IIMB-IMF Conference on Housing Markets, Financial Stability and Growth December 11, 2014 Based on Warnock V and Warnock F (2012). Developing Housing

Developing Housing Finance Systems Veronica Cacdac Warnock IIMB-IMF Conference on Housing Markets, Financial Stability and Growth December 11, 2014 Based on Warnock V and Warnock F (2012). Developing Housing

Consumption Expenditure on Health and Education: Econometric Models and evolution of OECD countries in

University of Santiago de Compostela. Faculty of Economics. Econometrics * Working Paper Series Economic Development. nº 50 Consumption Expenditure on Health and Education: Econometric Models and evolution

University of Santiago de Compostela. Faculty of Economics. Econometrics * Working Paper Series Economic Development. nº 50 Consumption Expenditure on Health and Education: Econometric Models and evolution

Lecture 1b. The open economy. The international flows of capital and goods, balance of payments and exchange rates.

Lecture 1b. The open economy. The international flows of capital and goods, balance of payments and exchange rates. Carlos Llano (P) & Nuria Gallego (TA) References: these slides have been developed based

Lecture 1b. The open economy. The international flows of capital and goods, balance of payments and exchange rates. Carlos Llano (P) & Nuria Gallego (TA) References: these slides have been developed based

Fiscal Policy in Japan

Fiscal Policy in Japan - Issues and Future Directions- June 10th, 2015 Ministry of Finance General Government Gross Debt and Financial Balances (International Comparison) (%) 240 210 General Government

Fiscal Policy in Japan - Issues and Future Directions- June 10th, 2015 Ministry of Finance General Government Gross Debt and Financial Balances (International Comparison) (%) 240 210 General Government

OECD Report Shows Tax Burdens Falling in Many OECD Countries

OECD Centres Germany Berlin (49-30) 288 8353 Japan Tokyo (81-3) 5532-0021 Mexico Mexico (52-55) 5281 3810 United States Washington (1-202) 785 6323 AUSTRALIA AUSTRIA BELGIUM CANADA CZECH REPUBLIC DENMARK

OECD Centres Germany Berlin (49-30) 288 8353 Japan Tokyo (81-3) 5532-0021 Mexico Mexico (52-55) 5281 3810 United States Washington (1-202) 785 6323 AUSTRALIA AUSTRIA BELGIUM CANADA CZECH REPUBLIC DENMARK

Business cycle volatility and country zize :evidence for a sample of OECD countries. Abstract

Business cycle volatility and country zize :evidence for a sample of OECD countries Davide Furceri University of Palermo Georgios Karras Uniersity of Illinois at Chicago Abstract The main purpose of this

Business cycle volatility and country zize :evidence for a sample of OECD countries Davide Furceri University of Palermo Georgios Karras Uniersity of Illinois at Chicago Abstract The main purpose of this

Methodology Calculating the insurance gap

Methodology Calculating the insurance gap Insurance penetration Methodology 3 Insurance Insurance Penetration Rank Rank Rank penetration penetration difference 2018 2012 change 2018 report 2012 report

Methodology Calculating the insurance gap Insurance penetration Methodology 3 Insurance Insurance Penetration Rank Rank Rank penetration penetration difference 2018 2012 change 2018 report 2012 report