Domestic Tax Issues for Non-resident Aliens

|

|

|

- Albert Banks

- 6 years ago

- Views:

Transcription

1 Domestic Tax Issues for Non-resident Aliens Presented by Monica Haven, EA, JD, LLM

2 What we ll cover Are Non-resident Aliens from Mars? Where is home for Dual Status Aliens? How do we tax extraterrestrial income? Do Space Treaties give us room? How on earth do aliens file?! Count-down to blast-off There is light at the end of the black hole! Is my account at First Galaxy Bank really foreign?

3 Why does it matter? US Citizens & Resident Aliens taxed on worldwide income Non-resident Aliens taxed only on US-source income

4 Is immigration status the same as residency? No these are separate determinations Individual in US on temporary visa may be a: Resident Alien Non-resident Alien Dual-status Non-resident treated as a Resident

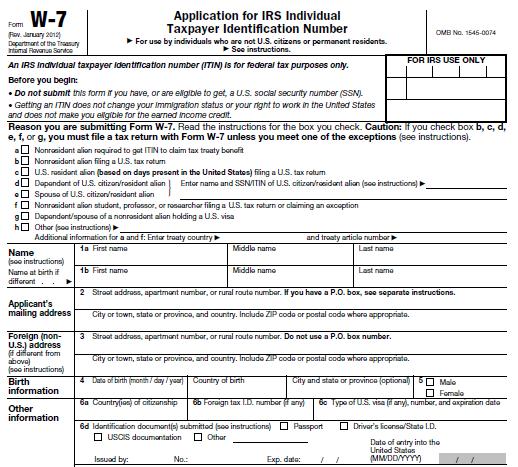

5 Must file US tax returns as though they were US citizens/residents Illegal Aliens Must use an Individual Taxpayer ID Number (use Form W-7)

6 Non-Resident Alien (NRA) Alien is not a US citizen by birth or naturalization Non-resident does not have Green Card and has not been present in the US for requisite time

7 Green Card Issued to permanent residents by US Citizenship & Immigration Services (USCIS) [formerly INS; renamed in 2003 when integrated into Dept. Homeland Security] Permanent unless administratively revoked or voluntarily (but procedurally) abandoned

8 Substantial Presence Test (SPT) Must be physically present in US (states & D.C. but not territories) for 31 days during current tax year AND 183 days in most recent 3-year period: All days in current year PLUS 1/3 of days in previous year PLUS 1/6 of days in year prior to previous EXCEPTION: If individual maintains a foreign tax home and a closer connection to one country

9 Example of Day Count Taxpayer was physically present in US for 120 days in each year 2008, 2009 & days in 2010 plus 40 days in 2009 (1/3 of 120) plus 20 days in 2008 (1/6 of 120) Total number of counted days = 180 Does not meet SPT

10 Days that are not counted If individual regularly commutes to work in US from Canada or Mexico is in the US for < 24 hours due to international transit is a crew member of a foreign vessel is unable to leave the US due to a medical condition is an exempt individual

11 Exempt individuals include Foreign government employees & diplomats if only temporary stay Teachers on J or Q visas unless > 2 years Students on F, J, M or Q visas unless > 5 years Professional athletes competing for charity Exempt individuals are subject to the SPT for all periods before and after they hold exempt status

12 Exempt Visas Academic F-1 Students F-2 Dependents of F-1 Type of Visa Exchange Visitors J-1 Visitors incl. exchange students & scholars J-2 Dependents of J-1 Work Restrictions Work authorized under very limited circumstances No work authorization Work authorized under certain circumstances Work authorized under certain circumstances Vocational and Language Students M-1 Vocational Student M-2 Dependents of M-1 Work authorized under certain circumstances No work authorization Cultural Exchange Visitors Q-1 International Cultural Exchange Work authorized for the sponsoring employer

13 Example of Exempt Status A foreign student with an F-1 Visa arrived in the US on January 1st, 2006 He is considered an NRA for 2006, 2007, 2008, 2009, and 2010 (His wife not a student came with him on an F-2 visa and is also an NRA through 2010) Both husband and wife will be considered residents in 2011, regardless of their academic status, since they have been in US > 5 years

leaves US after passing SPT in year of departure loses exempt status during the")

14 Dual Status Aliens (a.k.a. Part-year Residents) Individuals who are residents for one part of the year and nonresidents for another Occurs if individual enters US and passes SPT in year of arrival (must enter before July 1 st ) leaves US after passing SPT in year of departure loses exempt status during the year

15 Dual Status Elections (IRC 6013 ) 1. Back-date residency if: present in US 31 consecutive days in previous year AND meets SPT for current year 2. Treat as resident if: NRA at year-start and resident alien or citizen at year-end AND married at year-end to a US citizen or resident alien who agrees to file joint return Best used if US arrival on/after 7/2 & unable to qualify for SPT in prior year OR taxpayer is dual-status but wants to be treated as resident This is an once-in-a-lifetime election which cannot be made again if remarried

16 Examples of Residency Election Husband/Wife are NRAs at year-start but Husband becomes resident in June. Couple may elect to be treated as resident aliens. They may file jointly or separately in later years. Husband is a high-income earner US resident whose wife lives abroad and has no income. Husband can file separately or elect to file jointly. Wife and Son live permanently in the US. Husband joins them mid-year. They may elect to file jointly or Wife may file separately and claim Head of Household status (Wife is considered unmarried since Husband is an NRA). NRA Husband cannot file HOH

17

18 Tax Treatment of NRA s Income Taxed only on US-source (not worldwide) income Examples of income not considered US-source: Interest paid by US corp if 80% of gross income is derived from outside US Interest if funds are deposited in a foreign branch of US bank Personal service compensation received for work performed outside US Gain on sale of personal property if taxpayer s tax home is outside US

19 Calculating US-source Income NRA is a professional hockey player (goalie) with a US hockey club who received $98,500 for 242 days of play during the year Goalie played 194 days in US Goalie played 48 days in Canada US-source income = ( days) x $98,500 = $78,963 Use straight pro-ration

20 If US-source, is it effectively connected? Effectively connected if derived from US trade or business Can be reduced by personal exemptions & itemized deductions Taxed at graduated rates Not effectively connected Cannot be reduced by personal exemptions & itemized deductions Subject to 30% flat tax (unless lower treaty rate applies) NOTE: Capital Gains are not effectively connected.

Student is a degree candidate and (2) payment is received for tuition, books")

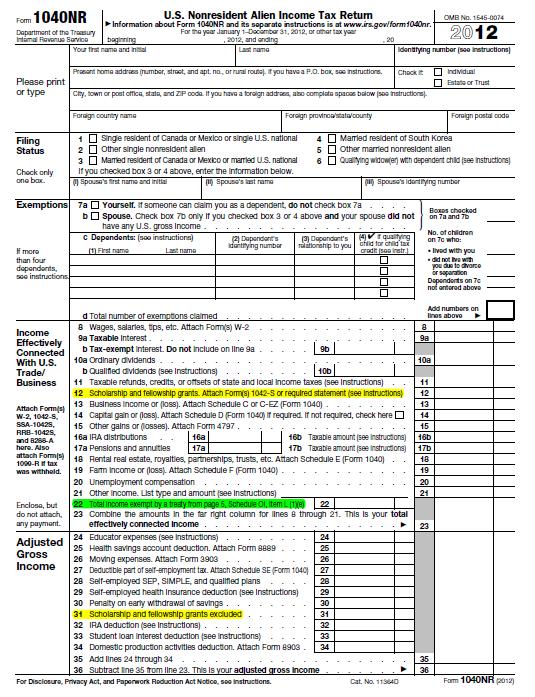

21 Effectively vs. Not Effectively * Qualified scholarship if (1) Student is a degree candidate and (2) payment is received for tuition, books or supplies [Excluded income must be reported on Form 1040NR, line31and statement must be attached to return

22 Scholarships Generally taxable is received from US payer Tax-exempt if qualified Degree candidate Eligible institution Received for tuition, books & supplies Report on Form 1040NR, Line 12 (exclude on Line 31) Some grants excluded by treaty US payer No payment for services Report on Form 1040NR, Line 22 & Schedule OI

23

24 Partnership Income Foreign partners in US partnership must file Form 1040NR on allocated share of effectively connected income Foreign partnerships with effectively connected income must file Form 1065 even operating from abroad, unless US source income $20K & < 1% of income allocable to US partners No US partners & all withholdings done at source

25 Gambling Winnings Considered not effectively connected Subject to 30% flat tax on gross income (cannot be reduced by gambling losses) EXCEPT: Canadian residents may file Form 1 Exempt gambling includes blackjack, baccarat, craps, roulette, big 6-Wheel, and certain horse- and dogracing winnings Gambling winnings may also be exempt under tax treaties

26 Treatment of Rental Income NRA is taxed on the gross rental revenue Considered not effectively connected Cannot be reduced by deductions for maintenance and management But, NRA may elect to treat the rental income as effectively connected under 871(d) Can offset income by allowable rental expenses Taxed at graduated rates on net income

27 Similar to US citizens Tax Treatment of NRA s Adjustments May contribute to IRAs & other qualified retirement plans May claim INcoming moving expenses but not OUTgoing May deduct student loan interest May deduct penalties on early withdrawal of savings if interest income is effectively connected

28 Unlike US citizens Tax Treatment of NRA s Deductions NRA may not claim Standard Deduction Itemized Deductions must be related to effectively connected income CAN deduct: State/local & property taxes, charitable contributions, casualty losses, and unreimbursed employee expenses CANNOT deduct: Medical expenses and mortgage interest Dual-status taxpayer also cannot use Standard Deduction but may use all itemized deductions

29 Tax Treatment of NRA s Tax Credits Name of Credit Same as US citizen Must file MFJ w/ US spouse Special Rules Adoption Child & Dep. Care Child Tax Dependent must be US citizen or resident Prior Year Min. Tax Earned Income Education Energy Foreign Tax Only on effectively connected income Retirement Savings

30 NRA Filing Status S, MFS or QW SPECIAL EXCEPTION: Married NRA may file S if resident of Canada, Mexico, South Korea or if married to US national (resident of American Samoa or Northern Mariana Islands ) AND has not lived with spouse for the last six months of the tax year MFJ if NRA is married to US citizen/resident & elects 6013(g) Cannot file HOH Resident spouse may file HOH if married to an NRA who is not treated as a spouse for tax purposes

31 NRA Personal Exemptions May claim PE for self (not spouse) SPECIAL EXCEPTION: Residents of Canada, Mexico, American Samoa & Northern Mariana Islands may claim PE for spouse without USsource income May claim PE for qualified dependents ITIN or SSN required for all exemptions claimed

32 Individual Taxpayer Identification Number Submit Form W-7 with: Proof of identity Tax return Mail to: Internal Revenue Service Austin Service Center ITIN Operation P.O. Box Austin, TX Wait 6 weeks, the call (800) for assistance

33

34 How many PE can NRA claim? Example 1: NRA exchange student from Russia lives in US with wife (no income) & 2 kids 1 PE Example 2: NRA exchange student from India lives in US with wife (no income) & 2 kids 2 PE due to special exception for India Example 3: NRA student from Canada lives in US - wife (no income) & 2 kids live in Canada 4 PE due to special rule for Canadians & Mexicans

35 Which form? NRA must use Form 1040NR Dual-status must use: 1040 if immigrant becomes resident by 12/ NR if taxpayer forfeits residency by 12/31 NRA without wage income can delay filing until June 15 th (can also defer ES # 1 payment until June 15 th but must then pay combined 1 st & 2 nd ES liability)

36 Effect of Tax Treaties (Refer to IRS Publication 901 AND legal counsel) Treaties generally reduce tax liability of NRA (not US citizen/resident) & are often reciprocal Treaty-based positions must be disclosed on Form $1,000 failure to file penalty File tax return even if treaty eliminates all tax liability Green Card holder who elects to be treated as non-resident under tax treaty is still subject to FBAR filing requirements! Not all states conform to federal tax treatment as per international treaties CA, for example, does not tax IRA distributions of non-resident Non-resident if temporary or transitory (e.g., vacation, passing through, completing a transaction)

37 Example of Tax Treatment under Treaty NRA is resident of foreign country that has tax treaty with US earnings from US sources include $24,100 compensation for personal services (on which tax is not limited by treaty) and $1,400 dividends (on which tax is limited to 15% by treaty) Personal service compensation $24,100 Less: Personal exemption - 3,650 Taxable income $20,450 Tax as per tax table for Single $2,653 Plus: Tax on gross dividends Total Tax Due $2,863

38 Special Rules for NRA Calendar year: If different tax year used abroad, NRA must allocate income/expenses Foreign Currency: If income received in foreign currency, NRA must convert to US dollars at prevailing rate on date received Depreciation: Use SL (over 40 years) for foreign real property; use 12-year life for personal property held abroad. Capital Gains: May be taxed on unrealized gains due to exchange rates in effect on dates of purchase & sale

39 Additional Disclosures Form 3520 for gifts & inheritances received from abroad > $100,000 Forms 5471, 8858, 8865 and for owners of foreign entities, if applicable Form 926 for certain transfers of property to foreign corporations

40 Surtax on Investment Income Does not apply to NRAs US citizens & residents married to NRA must file MFS MAGI threshold reduced from $200K to $125K Unless 6013 election made to file jointly

41 Tax Withholdings for NRA Pension Income Automatic 30% withholding (Form W-8BEN) Real Estate Transactions Automatic 10% withholding on gross proceeds Payroll Subject to income and FICA tax withholdings unless Totalization Agreement in effect (Form W-4) Self-employed NRA not subject to SE Tax Although NRA may be required to pay into system, he may not be able to collect from SSA

42 Totalization Agreements Employee pays Social Security tax to the country in which he is working EXCEPT: If he normally works abroad, but is sent to the US to work temporarily, he will pay Social Security taxes only to his home country Agreements with 24 countries currently in effect: Australia, Austria, Belgium, Canada, Chile, Czech Republic, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Japan, Luxembourg, the Netherlands, Norway, Poland, Portugal, South Korea, Spain, Sweden, Switzerland, United Kingdom

43 Example of Self-employment Tax Resident of Argentina published a book there and later became a US resident alien Foreign royalties must now be reported on US return as self-employment income in the year received, subject to SE Tax

44 State Rules for NRAs Different from state to state CA (as an example): Everyone present regardless of time is a resident Must file Form 540 if full year; 540NR if part-year Non-resident withholding (7%) on CA-source income, incl. compensation for services, rents/royalties, estate & trust distributions, lottery winnings, partnership income Mobile Workforce State Income Tax Fairness and Simplification Act of 2011 introduced (but not yet enacted) to allow all states to tax wages of non-residents working in state for > 30 days/year

45 Estate Tax for the NRA Domicile (intent) Residency (Green Card or SPT) US-domiciled NRA is subject to US estate tax (use Form 706-NA) Gross estate includes all tangible & intangible property in US Deduction for administrative expenses limited by ratio of US to worldwide gross estate Unlimited marital deduction only if the surviving spouse is US citizen, if assets are left to qualified domestic trust, or if treaty provisions stipulate $60,000 (not $5 million) estate exclusion Estates of US citizens permanently living abroad with assets located entirely abroad foreign estates subject to US tax only on US-source or effectively connected income

46 NRA Estate Tax Returns filed in 2010 [IRS, Statistics of Income Division, August 2011] Tax status, size of U.S. gross estate All returns, nontaxable and taxable Less than $100,000 [10] $100,000 under $500,000 $500,000 or more Nontaxable returns Taxable returns Total gross estate, U.S. tax purposes Number Amount ,785, ,389, ,464, ,931, ,329, ,455,507

47 Gift Tax for the NRA Subject to tax on gifts of US-situated real and tangible personal property Transfers of intangibles (stock & securities) are exempt from taxation

48 Leaving the US Resident and non-resident aliens must pay all tax due before departure & obtain tax clearance document File Forms 1040C if reporting taxable income File Form 2063 if no taxable income to report Must still file requisite income tax returns (Forms 1040 or 1040NR)

49 Aliens Exempt from Foreign government diplomats Departure Filing Employees of intl. organizations with tax-exempt wages & no other USsource income Students with no US-source income Vocational students with only interest income that is not effectively connected NRA only temporarily in US without taxable income Residents of Canada/Mexico who commute to US & earn US wages subject to withholding

50 Summary of Tax Treatment US Citizen & Resident Non-resident Alien (NRA) Dual-Status Alien Illegal Alien Lives in US? Yes No Part-Year Yes Which form? NR 1040 (resident 12/31) 1040NR (non-res 12/31 Taxable Inc? Worldwide US-source US-source while NRA Worldwide while Resident Tax Rules All familiar rules apply MFJ if 6013(g) elected No pers xmptns INcoming moving exp Cannot claim std ded Only some item ded MFJ if full year residence or 6013(g) elected Cannot file HOH Cannot claim std ded Can claim all item ded 1040 Worldwide All familiar rules apply

51 Monica Haven, E.A., J.D., L.L.M. (310) PHONE (310) FAX WEBSITE: The information contained herein is for educational use only and should not be construed as tax, financial, or legal advice. Each individual s situation is unique and may require specialized treatment. It is, therefore, imperative that you consult with tax and legal professionals prior to implementation of any strategies discussed.

Aliens & Citizens: Foreign and Domestic Tax Issues

Aliens & Citizens: Foreign and Domestic Tax Issues What we ll cover Are Non-resident Aliens from Mars? Where is home for Dual Status Aliens? How do we tax extraterrestrial income? Do Space Treaties give

Aliens & Citizens: Foreign and Domestic Tax Issues What we ll cover Are Non-resident Aliens from Mars? Where is home for Dual Status Aliens? How do we tax extraterrestrial income? Do Space Treaties give

Taxation of: U.S. Foreign Nationals

Taxation of: U.S. Foreign Nationals 2017 Edition ZanderSterling.com 1 The information contained in this publication is provided for general informational purposes only and is based on U.S. income tax law

Taxation of: U.S. Foreign Nationals 2017 Edition ZanderSterling.com 1 The information contained in this publication is provided for general informational purposes only and is based on U.S. income tax law

Federal Taxation of Aliens Working in the United States

Federal Taxation of Aliens Working in the United States Erika K. Lunder Legislative Attorney May 18, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research

Federal Taxation of Aliens Working in the United States Erika K. Lunder Legislative Attorney May 18, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University Before we begin Filing taxes means submitting tax forms (or

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University Before we begin Filing taxes means submitting tax forms (or

Estate & Gift Tax Treatment for Non-Citizens

ADVANCED MARKETS Estate & Gift Tax Treatment for Non-Citizens BECAUSE YOU ASKED It goes without saying that the laws governing the U.S. estate and gift tax system are complex. When you then consider the

ADVANCED MARKETS Estate & Gift Tax Treatment for Non-Citizens BECAUSE YOU ASKED It goes without saying that the laws governing the U.S. estate and gift tax system are complex. When you then consider the

Non-Resident Alien Frequently Asked Questions

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

U.S. Income Tax for Foreign Students, Scholars and Teachers. Arthur R. Kerr II Vacovec Mayotte & Singer LLP

U.S. Income Tax for Foreign Students, Scholars and Teachers Arthur R. Kerr II Vacovec Mayotte & Singer LLP 617-964-0500 akerr@vacovec.com Are You Resident or Nonresident? Residence for tax purposes not

U.S. Income Tax for Foreign Students, Scholars and Teachers Arthur R. Kerr II Vacovec Mayotte & Singer LLP 617-964-0500 akerr@vacovec.com Are You Resident or Nonresident? Residence for tax purposes not

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

U.S. taxation of foreign citizens

U.S. taxation of foreign citizens Global Mobility Services 2019 kpmg.com U.S. taxation of foreign citizens The following information is not intended to be written advice concerning one or more Federal

U.S. taxation of foreign citizens Global Mobility Services 2019 kpmg.com U.S. taxation of foreign citizens The following information is not intended to be written advice concerning one or more Federal

Aliens & Citizens Foreign and Domestic Tax Issues

Aliens & Citizens Foreign and Domestic Tax Issues Monica Haven 051711 Summary Whether from Venus or Venice, resident or nonresident, illegal worker or student, here or overseas, US taxpayers face a myriad

Aliens & Citizens Foreign and Domestic Tax Issues Monica Haven 051711 Summary Whether from Venus or Venice, resident or nonresident, illegal worker or student, here or overseas, US taxpayers face a myriad

U.S. Tax Guide for Aliens

Department of the Treasury Internal Revenue Service Publication 519 Cat. No. 15023T U.S. Tax Guide for Aliens For use in preparing 2000 Returns Contents Introduction... 1 Important Changes... 2 Important

Department of the Treasury Internal Revenue Service Publication 519 Cat. No. 15023T U.S. Tax Guide for Aliens For use in preparing 2000 Returns Contents Introduction... 1 Important Changes... 2 Important

TAX GUIDE FOR FOREIGN VISITORS. Anne E. Davenport, CPA October 2012

TAX GUIDE FOR FOREIGN VISITORS FOR USE BY: All Employees and Students Anne E. Davenport, CPA October 2012 Updated June 24, 2016 Table of Contents Introduction...1 Section 1: Definition of Terms...2 1.1

TAX GUIDE FOR FOREIGN VISITORS FOR USE BY: All Employees and Students Anne E. Davenport, CPA October 2012 Updated June 24, 2016 Table of Contents Introduction...1 Section 1: Definition of Terms...2 1.1

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014 Federal Income Tax Withholding 14.1-1 U.S. citizens & resident aliens are subject to income tax withholding

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014 Federal Income Tax Withholding 14.1-1 U.S. citizens & resident aliens are subject to income tax withholding

Instructions for Form 1040NR-EZ

2011 Instructions for Form 1040NR-EZ U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Department of the Treasury Internal Revenue Service Section references are to the Internal

2011 Instructions for Form 1040NR-EZ U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Department of the Treasury Internal Revenue Service Section references are to the Internal

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien for

Information for Foreign National Students, Scholars and Staff I. Introduction For federal tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien for

The United States Government defines an alien as any individual who is not

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

TAX POLICY AND PROCEDURE GUIDE FOR INCOME PAYMENTS TO ALIEN INDIVIDUALS

TAX POLICY AND PROCEDURE GUIDE FOR INCOME PAYMENTS TO ALIEN INDIVIDUALS Revised as of November 2007 University of Alabama at Birmingham Revision Date: November 2007 PREFACE The Tax Policy and Procedure

TAX POLICY AND PROCEDURE GUIDE FOR INCOME PAYMENTS TO ALIEN INDIVIDUALS Revised as of November 2007 University of Alabama at Birmingham Revision Date: November 2007 PREFACE The Tax Policy and Procedure

2016 Publication 4011

016 Publication 4011 Foreign Student and Scholar Volunteer Resource Guide For Use in Preparing Tax Year 016 Returns»» Volunteer Income Tax Assistance (VITA)»» Tax Counseling for the Elderly (TCE) For the

016 Publication 4011 Foreign Student and Scholar Volunteer Resource Guide For Use in Preparing Tax Year 016 Returns»» Volunteer Income Tax Assistance (VITA)»» Tax Counseling for the Elderly (TCE) For the

~E~ E-3 visa, 103 Earnings statement, 100, 131, 135, 136,

Index ~A~ ACA Affordable Care Act 14, 173 A, G visa holders, 5, 6, 7, 37, 103 A-2 visa, PRI 6, 126, 132, 133 A-3 visa, 138, 141 Abuse, abusive employment situation, 141,142 Actual days, Z, 7, 8 Adjusted

Index ~A~ ACA Affordable Care Act 14, 173 A, G visa holders, 5, 6, 7, 37, 103 A-2 visa, PRI 6, 126, 132, 133 A-3 visa, 138, 141 Abuse, abusive employment situation, 141,142 Actual days, Z, 7, 8 Adjusted

Your Federal Income Tax Responsibilities as an Au Pair

S. Landau Services Steven Landau, E.A.* 2610 NW 56th Street #103 Seattle, WA 98107-4118 PHONE: (206) 784-1070 TOLL FREE: (877) 220-3241 TOLL FREE FAX: (877) 220-3889 E-MAIL: Steven@SLandauServices.com

S. Landau Services Steven Landau, E.A.* 2610 NW 56th Street #103 Seattle, WA 98107-4118 PHONE: (206) 784-1070 TOLL FREE: (877) 220-3241 TOLL FREE FAX: (877) 220-3889 E-MAIL: Steven@SLandauServices.com

US Tax Information for Diplomatic Families at the Canadian Embassy

US Tax Information for Diplomatic Families at the Canadian Rick Ward LLC January 16, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of January

US Tax Information for Diplomatic Families at the Canadian Rick Ward LLC January 16, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of January

Frequently Asked Tax Questions 2018 Tax Returns

Frequently Asked Tax Questions 2018 Tax Returns Q. When is my tax return due? A. 2018 Federal (U.S. government) tax returns are due by April 15, 2019. State of Iowa tax returns are due by May 1, 2019.

Frequently Asked Tax Questions 2018 Tax Returns Q. When is my tax return due? A. 2018 Federal (U.S. government) tax returns are due by April 15, 2019. State of Iowa tax returns are due by May 1, 2019.

Instructions for Form W-7

Instructions for Form W-7 (January 2010) Application for IRS Individual Taxpayer Identification Number Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

Instructions for Form W-7 (January 2010) Application for IRS Individual Taxpayer Identification Number Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

Form 1040NR Filing Challenges and Effective Approaches

Form 1040NR Filing Challenges and Effective Approaches Determining Taxpayer Classifications and Elections, Computing Income and Deductions, and Understanding Spouse/Dependent Treatment TUESDAY, SEPTEMBER

Form 1040NR Filing Challenges and Effective Approaches Determining Taxpayer Classifications and Elections, Computing Income and Deductions, and Understanding Spouse/Dependent Treatment TUESDAY, SEPTEMBER

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

Payments Made to Nonresident Aliens

Payments Made to Nonresident Aliens A Policies and Procedures Manual This Procedures for Payments Made to Nonresident Aliens guide was prepared by Arctic International LLC in connection with Occidental

Payments Made to Nonresident Aliens A Policies and Procedures Manual This Procedures for Payments Made to Nonresident Aliens guide was prepared by Arctic International LLC in connection with Occidental

Estate Planning for Foreign Nationals

Estate Planning for Foreign Nationals What Financial Professionals Need to Know www.mcnulty-law.com Tel. (212) 431-7526 What We ll Be Covering Non-Tax Estate Planning Issues US Estate Taxation of US citizens

Estate Planning for Foreign Nationals What Financial Professionals Need to Know www.mcnulty-law.com Tel. (212) 431-7526 What We ll Be Covering Non-Tax Estate Planning Issues US Estate Taxation of US citizens

Tax Guide For Foreign Investors In U.S. Residential Real Estate

A T T O R N E Y S A T L A W Tax Guide For Foreign Investors In U.S. Residential Real Estate 2018 Edition In this guide I. Introduction 2 II. The U.S. Tax System 3 A. U.S. Persons 3 1. Basic Rules 3 2.

A T T O R N E Y S A T L A W Tax Guide For Foreign Investors In U.S. Residential Real Estate 2018 Edition In this guide I. Introduction 2 II. The U.S. Tax System 3 A. U.S. Persons 3 1. Basic Rules 3 2.

2012 Non-Resident Alien Tax Filings

2012 Non-Resident Alien Tax Filings Spring 2013 The Colorado College Business Office OMIS Overview of the U.S. Income Tax System Your employer withholds from your earnings an estimate of what your federal

2012 Non-Resident Alien Tax Filings Spring 2013 The Colorado College Business Office OMIS Overview of the U.S. Income Tax System Your employer withholds from your earnings an estimate of what your federal

ALI-ABA Course of Study International Trust and Estate Planning. August 16-17, 2007 Chicago, Illinois

35 ALI-ABA Course of Study International Trust and Estate Planning August 16-17, 2007 Chicago, Illinois Basic U.S. Transfer and Income Tax Rules Applicable to Non-Resident Aliens By Virginia F. Coleman

35 ALI-ABA Course of Study International Trust and Estate Planning August 16-17, 2007 Chicago, Illinois Basic U.S. Transfer and Income Tax Rules Applicable to Non-Resident Aliens By Virginia F. Coleman

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

American Citizens Abroad. Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION

American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation 5 December 2016; 1 November 2017; 1 December 2017; 18 January 2018; 19 April 2018 INTRODUCTION This side-by-side analysis

American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation 5 December 2016; 1 November 2017; 1 December 2017; 18 January 2018; 19 April 2018 INTRODUCTION This side-by-side analysis

Foreign Student and Scholar Volunteer Tax Return Preparation. VITA Training 1

Foreign Student and Scholar Volunteer Tax Return Preparation VITA Training 1 e-learning Options & Understanding Taxes Website http://www.irs.gov/app/understandingtaxes/index.jsp VITA Training 2 Foreign

Foreign Student and Scholar Volunteer Tax Return Preparation VITA Training 1 e-learning Options & Understanding Taxes Website http://www.irs.gov/app/understandingtaxes/index.jsp VITA Training 2 Foreign

UNIVERSITY OF DAYTON NONRESIDENT ALIEN TAX GUIDE CONTENTS COMMON VISA TYPES AND THEIR TREATMENTS

UNIVERSITY OF DAYTON NONRESIDENT ALIEN TAX GUIDE CONTENTS I. RESPONSIBILITIES II. III. IV. SOCIAL SECURITY NUMBER REQUIREMENT DEFINITIONS TAX TREATIES V. PAYMENTS TO NONRESIDENT ALIENS VI. COMMON VISA

UNIVERSITY OF DAYTON NONRESIDENT ALIEN TAX GUIDE CONTENTS I. RESPONSIBILITIES II. III. IV. SOCIAL SECURITY NUMBER REQUIREMENT DEFINITIONS TAX TREATIES V. PAYMENTS TO NONRESIDENT ALIENS VI. COMMON VISA

Alien Tax Home Representation Form

Alien Tax Home Representation Form I have reviewed the attached tax home information for aliens and/or have consulted with my tax advisor and make the following good faith representation (please check

Alien Tax Home Representation Form I have reviewed the attached tax home information for aliens and/or have consulted with my tax advisor and make the following good faith representation (please check

17/10/2017. Circular 230 disclaimer. Payroll for International Assignments. Agenda. Your presenters

Circular 230 disclaimer Payroll for International Assignments 17 th Annual Virginia Statewide Payroll Conference October 13, 2017 Any tax advice contained herein was not intended or written to be used,

Circular 230 disclaimer Payroll for International Assignments 17 th Annual Virginia Statewide Payroll Conference October 13, 2017 Any tax advice contained herein was not intended or written to be used,

US Tax Information for Diplomatic Families at the Australian Embassy

US Tax Information for Diplomatic Families at the Australian Rick Ward LLC January 25, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of

US Tax Information for Diplomatic Families at the Australian Rick Ward LLC January 25, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS. Document created and modified by Financial Services Revised February 8, 2018

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS Document created and modified by Financial Services Revised February 8, 2018 Table of Contents Pages Introduction 1 Definition of Terms 2-5 Frequently

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS Document created and modified by Financial Services Revised February 8, 2018 Table of Contents Pages Introduction 1 Definition of Terms 2-5 Frequently

International Students and Scholars Nonresident Tax Orientation. February 14, 2018

International Students and Scholars Nonresident Tax Orientation February 14, 2018 Nonresident Tax Orientation Agenda General Overview of U.S. Tax and Tax Forms Items subject to tax NRA Documentation Requirements

International Students and Scholars Nonresident Tax Orientation February 14, 2018 Nonresident Tax Orientation Agenda General Overview of U.S. Tax and Tax Forms Items subject to tax NRA Documentation Requirements

U.S. Nonresident Alien Income Tax Return

Form 14NR Department of the Treasury Internal Revenue Service Please print or type U.S. Nonresident Alien Income Tax Return Information about Form 14NR and its separate instructions is at www.irs.gov/form14nr.

Form 14NR Department of the Treasury Internal Revenue Service Please print or type U.S. Nonresident Alien Income Tax Return Information about Form 14NR and its separate instructions is at www.irs.gov/form14nr.

TAX POLICY AND PROCEDURE GUIDE FOR PAYMENTS TO ALIEN INDIVIDUALS

TAX POLICY AND PROCEDURE GUIDE FOR PAYMENTS TO ALIEN INDIVIDUALS Revised as of July 2017 University of Alabama at Birmingham PREFACE The Tax Policy and Procedure Guide for Income Payments to Alien Individuals

TAX POLICY AND PROCEDURE GUIDE FOR PAYMENTS TO ALIEN INDIVIDUALS Revised as of July 2017 University of Alabama at Birmingham PREFACE The Tax Policy and Procedure Guide for Income Payments to Alien Individuals

U.S. Tax Guide for Aliens

Department of the Treasury Internal Revenue Service Publication 519 Cat. No. 15023T U.S. Tax Guide for Aliens For use in preparing 2013 Returns Contents Introduction... 1 What's New... 2 Reminders... 3

Department of the Treasury Internal Revenue Service Publication 519 Cat. No. 15023T U.S. Tax Guide for Aliens For use in preparing 2013 Returns Contents Introduction... 1 What's New... 2 Reminders... 3

If you do not have all of the above forms, please call Junn De Guzman at (732)

") To: Non-Resident Aliens Requesting Special Tax Treatment From: Junn De Guzman, Sr. Accountant Payroll Department Date: December 31, 2011 Re: Requirements for Tax Benefits for Calendar Year 2012 Enclosed

To: Non-Resident Aliens Requesting Special Tax Treatment From: Junn De Guzman, Sr. Accountant Payroll Department Date: December 31, 2011 Re: Requirements for Tax Benefits for Calendar Year 2012 Enclosed

Foreign Earned Income: Exclusion and Other Tax Issues for Expat Workers

Foreign Earned Income: Exclusion and Other Tax Issues for Expat Workers Navigating Tax Treaties, Social Security Totalization Agreements, and Other Complexities TUESDAY, JULY 16, 2013, 1:00-2:50 pm Eastern

Foreign Earned Income: Exclusion and Other Tax Issues for Expat Workers Navigating Tax Treaties, Social Security Totalization Agreements, and Other Complexities TUESDAY, JULY 16, 2013, 1:00-2:50 pm Eastern

Canadian Residents Going Down South

Canadian Residents Going Down South P151(E) Rev. 10 Is this pamphlet for you? T his pamphlet is for you if you spent part of the year in the United States (U.S.), for example, for health reasons or on

Canadian Residents Going Down South P151(E) Rev. 10 Is this pamphlet for you? T his pamphlet is for you if you spent part of the year in the United States (U.S.), for example, for health reasons or on

2018 Instructions for Schedule SE (Form 1040)

") Department of the Treasury Internal Revenue Service 2018 Instructions for Schedule SE (Form 1040) Self-Employment Tax Use Schedule SE (Form 1040) to figure the tax due on net earnings from self-employment.

Department of the Treasury Internal Revenue Service 2018 Instructions for Schedule SE (Form 1040) Self-Employment Tax Use Schedule SE (Form 1040) to figure the tax due on net earnings from self-employment.

NONRESIDENT ALIEN TAX COMPLIANCE. A Policy and Procedure Manual. University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann

Nonresident Alien Tax Specialist Kellie Grahmann") NONRESIDENT ALIEN TAX COMPLIANCE A Policy and Procedure Manual University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann CONTENTS Nonresident Alien Tax Compliance Summary Taxation

NONRESIDENT ALIEN TAX COMPLIANCE A Policy and Procedure Manual University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann CONTENTS Nonresident Alien Tax Compliance Summary Taxation

TAX FILING FOR STUDENTS AND SCHOLARS 101. Columbus Community Legal Services

TAX FILING FOR STUDENTS AND SCHOLARS 101 Columbus Community Legal Services INTRODUCTION Who are we? Part of the Catholic University of America s Columbus School of Law Columbus Community Legal Services

TAX FILING FOR STUDENTS AND SCHOLARS 101 Columbus Community Legal Services INTRODUCTION Who are we? Part of the Catholic University of America s Columbus School of Law Columbus Community Legal Services

American Citizens Abroad. Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION

1 November 2017; 1 December 2017; 19 January 2018 American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION This side-by-side analysis compares Current Law (i.e.,

1 November 2017; 1 December 2017; 19 January 2018 American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION This side-by-side analysis compares Current Law (i.e.,

US Tax Information for Diplomatic Families at the German Embassy

US Tax Information for Diplomatic Families at the German Rick Ward LLC February 26, 2018 Disclosure This presentation has been prepared for employees of the World Bank by LLC. The information in this presentation

US Tax Information for Diplomatic Families at the German Rick Ward LLC February 26, 2018 Disclosure This presentation has been prepared for employees of the World Bank by LLC. The information in this presentation

US Tax Information for Diplomatic Families at the Swiss Embassy

US Tax Information for Diplomatic Families at the Swiss Rick Ward LLC October 18, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of October

US Tax Information for Diplomatic Families at the Swiss Rick Ward LLC October 18, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of October

8-Jun-06 Personal Income Top Marginal Tax Rate,

8-Jun-06 Personal Income Top Marginal Tax Rate, 1975-2005 2005 2000 1999 1998 1997 1996 1995 1994 1993 1992 1991 1990 1989 1988 Australia 47% 47% 47% 47% 47% 47% 47% 47% 47% 47% 47% 48% 49% 49% Austria

8-Jun-06 Personal Income Top Marginal Tax Rate, 1975-2005 2005 2000 1999 1998 1997 1996 1995 1994 1993 1992 1991 1990 1989 1988 Australia 47% 47% 47% 47% 47% 47% 47% 47% 47% 47% 47% 48% 49% 49% Austria

Americans Living Abroad. 61 Tax Questions you should know.

Americans Living Abroad 61 Tax Questions you should know 1 General FAQs 1. I m a U.S. citizen living and working outside of the United States for many years. Do I still need to file a U.S. tax return?

Americans Living Abroad 61 Tax Questions you should know 1 General FAQs 1. I m a U.S. citizen living and working outside of the United States for many years. Do I still need to file a U.S. tax return?

Overview of Tax Considerations for Canadians in the United States

Overview of Tax Considerations for Canadians in the United States Introduction Due to its proximity to the United States, Canada is the United States' largest trading partner. In addition, Canada is a

Overview of Tax Considerations for Canadians in the United States Introduction Due to its proximity to the United States, Canada is the United States' largest trading partner. In addition, Canada is a

Foreign Nationals Financial Professional Guide

Foreign Nationals Financial Professional Guide Policies issued by American General Life Insurance Company (AGL) except in New York, where issued by The United States Life Insurance Company in the City

Foreign Nationals Financial Professional Guide Policies issued by American General Life Insurance Company (AGL) except in New York, where issued by The United States Life Insurance Company in the City

Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding

Form W-8BEN Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding (Rev. February 2006) OMB No. 1545-1621 Department of the Treasury Section references are to the Internal

Form W-8BEN Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding (Rev. February 2006) OMB No. 1545-1621 Department of the Treasury Section references are to the Internal

Tax & Estate Planning for Snowbirds

Tax & Estate Planning for Snowbirds Amin Mawani Schulich School of Business York University amawani@schulich.yorku.ca Taxes do influence behaviour Windowless Castles Narrow frontages SIN & gasoline taxes

Tax & Estate Planning for Snowbirds Amin Mawani Schulich School of Business York University amawani@schulich.yorku.ca Taxes do influence behaviour Windowless Castles Narrow frontages SIN & gasoline taxes

Certain Cash Contributions for Typhoon Haiyan Relief Efforts in the Philippines Can Be Deducted on Your 2013 Tax Return

Certain Cash Contributions for Typhoon Haiyan Relief Efforts in the Philippines Can Be Deducted on Your 2013 Tax Return A new law allows you to choose to deduct certain charitable contributions of money

Certain Cash Contributions for Typhoon Haiyan Relief Efforts in the Philippines Can Be Deducted on Your 2013 Tax Return A new law allows you to choose to deduct certain charitable contributions of money

U.S. Nonresident Alien Income Tax Return

Form 1040NR Department of the Treasury Internal Revenue Service U.S. Nonresident Alien Income Tax Return Information about Form 1040NR and its separate instructions is at www.irs.gov/form1040nr. For the

Form 1040NR Department of the Treasury Internal Revenue Service U.S. Nonresident Alien Income Tax Return Information about Form 1040NR and its separate instructions is at www.irs.gov/form1040nr. For the

SPRING For Trusted Advisors

SPRING 2019 For Trusted Advisors Taxation - Income, Estate, and Gift The Roth IRA conversion decision. By Robert Keebler, CPA/PFS, MST, AEP (Distinguished) Traditional Individual Retirement Accounts (IRAs)

SPRING 2019 For Trusted Advisors Taxation - Income, Estate, and Gift The Roth IRA conversion decision. By Robert Keebler, CPA/PFS, MST, AEP (Distinguished) Traditional Individual Retirement Accounts (IRAs)

U.S. Nonresident Alien Income Tax Return

Form 1040NR U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1 December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning, 2011, and

Form 1040NR U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1 December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning, 2011, and

Instructions for Form 8802 (December 2003)

") Instructions for Form 8802 (December 2003) Application for United States Residency Certification Section references are to the Internal Revenue Code. Department of the Treasury Internal Revenue Service

Instructions for Form 8802 (December 2003) Application for United States Residency Certification Section references are to the Internal Revenue Code. Department of the Treasury Internal Revenue Service

TAX TIPS FOR FOREIGN MISSIONARIES OF THE SEVENTH-DAY ADVENTIST CHURCH

TAX TIPS FOR FOREIGN MISSIONARIES OF THE SEVENTH-DAY ADVENTIST CHURCH RICHARD E. GREEN, CPA 5010 Centennial Commons Dr NW Acworth, GA 30102-2181 Phone (770) 529-4394 EMAIL taxman@regreencpa.com Web Page

TAX TIPS FOR FOREIGN MISSIONARIES OF THE SEVENTH-DAY ADVENTIST CHURCH RICHARD E. GREEN, CPA 5010 Centennial Commons Dr NW Acworth, GA 30102-2181 Phone (770) 529-4394 EMAIL taxman@regreencpa.com Web Page

US Tax Information for Diplomatic Families at the British Embassy

US Tax Information for Diplomatic Families at the British Rick Ward LLC February 22, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of February

US Tax Information for Diplomatic Families at the British Rick Ward LLC February 22, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of February

Estate Planning for Non-U.S. Citizens

Estate Planning for Non-U.S. Citizens Andre Gucailo Financial Professional AXA Advisors, LLC 5337 Millenia Lakes Blvd., Suite 405 Orlando, FL 32839 407-926-2538 321-231-9879 Andre.gucailo@axa-advisors.com

Estate Planning for Non-U.S. Citizens Andre Gucailo Financial Professional AXA Advisors, LLC 5337 Millenia Lakes Blvd., Suite 405 Orlando, FL 32839 407-926-2538 321-231-9879 Andre.gucailo@axa-advisors.com

9/20/2017. USA the dream destination. EB5 visa allows dream to be a reality. Tax regulations in USA affecting NRIs Resident Indians

Tax regulations in USA affecting NRIs Resident Indians By SANKET SHAH CO-FOUNDER AND MANAGING DIRECTOR USA the dream destination USA has always been and will be a dream destination Getting a job Sending

Tax regulations in USA affecting NRIs Resident Indians By SANKET SHAH CO-FOUNDER AND MANAGING DIRECTOR USA the dream destination USA has always been and will be a dream destination Getting a job Sending

Federal Tax Information Session For International Scholars

Federal Tax Information Session For International Scholars Agenda Tax Basics Forms You RECEIVE Forms You COMPLETE Tax Residency Status Tax Filing Information for Non-residents Treaty Information Filling

Federal Tax Information Session For International Scholars Agenda Tax Basics Forms You RECEIVE Forms You COMPLETE Tax Residency Status Tax Filing Information for Non-residents Treaty Information Filling

DIVISION OF REVENUE AND TAXATION COMMONWEALTH OF THE NORTHERN MARIANA ISLANDS CNMI Nonresident Alien Income Tax Return

Form 040NR-CM DIVISION OF REVENUE AND TAXATION COMMONWEALTH OF THE NORTHERN MARIANA ISLANDS CNMI Nonresident Alien Income Tax Return For the year January December 3, 03, or other tax year beginning, 03,

Form 040NR-CM DIVISION OF REVENUE AND TAXATION COMMONWEALTH OF THE NORTHERN MARIANA ISLANDS CNMI Nonresident Alien Income Tax Return For the year January December 3, 03, or other tax year beginning, 03,

Nonresident Alien State of Hawaii Tax Workshop

Nonresident Alien State of Hawaii Tax Workshop University of Hawaii J-1 State of Hawaii Tax Workshop March 23, 2017 Major Differences: Federal & Hawaii Federal Tax treaties Green card test Substantial

Nonresident Alien State of Hawaii Tax Workshop University of Hawaii J-1 State of Hawaii Tax Workshop March 23, 2017 Major Differences: Federal & Hawaii Federal Tax treaties Green card test Substantial

Seminar NONRESIDENT EMPLOYEE TAX COMPLIANCE Revised October 31, 1996

Seminar NONRESIDENT EMPLOYEE TAX COMPLIANCE Revised October 31, 1996 Presented by Donna K. Torres and Patrice H. Gremillion Louisiana State University & A&M College Office of Accounting Services, Payroll

Seminar NONRESIDENT EMPLOYEE TAX COMPLIANCE Revised October 31, 1996 Presented by Donna K. Torres and Patrice H. Gremillion Louisiana State University & A&M College Office of Accounting Services, Payroll

EXPAT TAX HANDBOOK. Non-Citizens and U.S. Tax Residency. Tax Year Ephraim Moss, Esq Ext 101

EXPAT TAX HANDBOOK Non-Citizens and U.S. Tax Residency Tax Year 2018 Ephraim Moss, Esq. 718-887-9933 Ext 101 emoss@expattaxprofessionals.com Joshua Ashman, CPA 718-887-9933 Ext 102 jashman@expattaxprofessionals.com

EXPAT TAX HANDBOOK Non-Citizens and U.S. Tax Residency Tax Year 2018 Ephraim Moss, Esq. 718-887-9933 Ext 101 emoss@expattaxprofessionals.com Joshua Ashman, CPA 718-887-9933 Ext 102 jashman@expattaxprofessionals.com

DO NOT FILE THIS FORM IN 2019 WITH YOUR TAX RETURN

THIS FORM IN 2019 WITH YOUR TAX RETURN This IRS Tax Form is ONLY A DRAFT for 2019. This form will most likely be changed before its final version is ready to be used in 2019 with your 2018 Tax Return.

THIS FORM IN 2019 WITH YOUR TAX RETURN This IRS Tax Form is ONLY A DRAFT for 2019. This form will most likely be changed before its final version is ready to be used in 2019 with your 2018 Tax Return.

Nonresident Alien Federal Tax Workshop

Nonresident Alien Federal Tax Workshop Using GLACIER Tax Prep (GTP) as a tool for self-preparation of 2017 Federal Income Tax Return (Form 1040NR or Form 1040NR-EZ) and Form 8843, Payroll Tax Workshop

Nonresident Alien Federal Tax Workshop Using GLACIER Tax Prep (GTP) as a tool for self-preparation of 2017 Federal Income Tax Return (Form 1040NR or Form 1040NR-EZ) and Form 8843, Payroll Tax Workshop

EXPAT TAX.A TO Z. ASSETS Anything you own that has value is considered an asset. Bank accounts,

EXPAT TAX.A TO Z US tax law is difficult enough to understand without the added burden of trying to understand the overseas side of things. Here is an explanation of expat key words and phrases that will

EXPAT TAX.A TO Z US tax law is difficult enough to understand without the added burden of trying to understand the overseas side of things. Here is an explanation of expat key words and phrases that will

Expats/Inpats: Working Across Borders

Expats/Inpats: Working Across Borders Annick Nguessan 23 October 2015 International Tax Series Agenda & Objectives Introduction Types of assignments Impact of Expatriates/Inpatriates on employer U.S. taxation

Expats/Inpats: Working Across Borders Annick Nguessan 23 October 2015 International Tax Series Agenda & Objectives Introduction Types of assignments Impact of Expatriates/Inpatriates on employer U.S. taxation

IRS Reporting Rules. Reference Guide. serving the people who serve the world

IRS Reporting Rules Reference Guide serving the people who serve the world The United States has and continues to maintain a policy of not taxing the deposit interest earned by United States (US) nonresidents

IRS Reporting Rules Reference Guide serving the people who serve the world The United States has and continues to maintain a policy of not taxing the deposit interest earned by United States (US) nonresidents

Nonresident Alien Tax Issues: Why?

Taxation Issues: Nonresident Aliens Judy Todd & Tammy Childress Nonresident Alien Tax Issues: Why? Nonresident Alien s (NRA s) have higher tax liability Payor is liable for taxes, interest, and penalties

Taxation Issues: Nonresident Aliens Judy Todd & Tammy Childress Nonresident Alien Tax Issues: Why? Nonresident Alien s (NRA s) have higher tax liability Payor is liable for taxes, interest, and penalties

MEXICO - INTERNATIONAL TAX UPDATE -

TTN Conference May 2017 MEXICO - INTERNATIONAL TAX UPDATE - Arturo G. Brook Main Taxes Income Tax Value Added Tax Others Agenda DTTs and TIEAs FATCA (IGA) and CRS Choice of Vehicles Income Tax - General

TTN Conference May 2017 MEXICO - INTERNATIONAL TAX UPDATE - Arturo G. Brook Main Taxes Income Tax Value Added Tax Others Agenda DTTs and TIEAs FATCA (IGA) and CRS Choice of Vehicles Income Tax - General

DUAL-STATUS RETURN U.S. Nonresident Alien Income Tax Return LEE F DUT X. MN Foreign province/county

DUAL-STATUS RETURN U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1-December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning,

DUAL-STATUS RETURN U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1-December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning,

Foreign Earned Income: Form 2555 Exclusion Reporting and Other Tax Issues for Expat Workers

Foreign Earned Income: Form 2555 Exclusion Reporting and Other Tax Issues for Expat Workers Navigating Tax Treaties, Social Security Totalization Agreements, and Other Complexities THURSDAY, MAY 8, 2014,

Foreign Earned Income: Form 2555 Exclusion Reporting and Other Tax Issues for Expat Workers Navigating Tax Treaties, Social Security Totalization Agreements, and Other Complexities THURSDAY, MAY 8, 2014,

THE F-1 VISA PRIVILEGED U.S. TAX STATUS AND HOW TO KEEP IT

THE F-1 VISA PRIVILEGED U.S. TAX STATUS AND HOW TO KEEP IT Authors Neha Rastogi Beate Erwin Tags Exempt Individual F-1 Visa Foreign Students Nonresident Alien Foreign students leaving their home country

THE F-1 VISA PRIVILEGED U.S. TAX STATUS AND HOW TO KEEP IT Authors Neha Rastogi Beate Erwin Tags Exempt Individual F-1 Visa Foreign Students Nonresident Alien Foreign students leaving their home country

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A VANILLA APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A VANILLA APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION October 15, 2017 Congress and the Administration are expected to consider changes in US tax

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A VANILLA APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION October 15, 2017 Congress and the Administration are expected to consider changes in US tax

NRIs Resident Indians. By SANKET SHAH CO-FOUNDER AND MANAGING DIRECTOR

Tax regulations in USAaffecting NRIs Resident Indians By SANKET SHAH CO-FOUNDER AND MANAGING DIRECTOR USA thedream destination USA has always been and will be a dream destination Getting a job Sending

Tax regulations in USAaffecting NRIs Resident Indians By SANKET SHAH CO-FOUNDER AND MANAGING DIRECTOR USA thedream destination USA has always been and will be a dream destination Getting a job Sending

Setting up in Denmark

Setting up in Denmark 6. Taxation The Danish tax system for individuals rests on the global taxation principle. The principle holds that the income of individuals and companies with full tax liability

Setting up in Denmark 6. Taxation The Danish tax system for individuals rests on the global taxation principle. The principle holds that the income of individuals and companies with full tax liability

An Introduction to the US Estate and Gift Tax Regime

An Introduction to the US Estate and Gift Tax Regime DAVID G. ROBERTS www.crossborder.com CTF Edmonton Young Practitioners Group September 2012 Issues Who is a US person? US transfer taxes Common estate

An Introduction to the US Estate and Gift Tax Regime DAVID G. ROBERTS www.crossborder.com CTF Edmonton Young Practitioners Group September 2012 Issues Who is a US person? US transfer taxes Common estate

TAX PLANNING FOR FOREIGN INVESTORS Table of Contents

TAX PLANNING FOR FOREIGN INVESTORS Table of Contents 1. Introduction...1 1.1. Tax Planning vs. Tax Cheating...1 1.2. Legitimate Tax Planning...2 1.3. Economic Substance Doctrine...2 2. Income Tax Consequences...3

TAX PLANNING FOR FOREIGN INVESTORS Table of Contents 1. Introduction...1 1.1. Tax Planning vs. Tax Cheating...1 1.2. Legitimate Tax Planning...2 1.3. Economic Substance Doctrine...2 2. Income Tax Consequences...3

Private Company Services. U.S. Estate and Gift taxation of resident aliens and nonresident aliens

Private Company Services U.S. Estate and Gift taxation of resident aliens and nonresident aliens 2010 2012 Non-U.S. citizens, both resident and nonresident aliens, may be subject to U.S. estate and gift

Private Company Services U.S. Estate and Gift taxation of resident aliens and nonresident aliens 2010 2012 Non-U.S. citizens, both resident and nonresident aliens, may be subject to U.S. estate and gift

Looking Beyond Our Borders:

Looking Beyond Our Borders: U.S. Income, Estate, and Gift Tax Implications 2017 Advanced Estate Planning Conference MGM Grand Las Vegas June 13, 2017 Peggy A. Ugent, CPA 100 CONGRESS AVENUE, SUITE 1440

Looking Beyond Our Borders: U.S. Income, Estate, and Gift Tax Implications 2017 Advanced Estate Planning Conference MGM Grand Las Vegas June 13, 2017 Peggy A. Ugent, CPA 100 CONGRESS AVENUE, SUITE 1440

Foreign Tax Issues. By Merrill Fromer Pages

Foreign Tax Issues By Merrill Fromer Pages 435-475 Foreign Tax Issues pg. 435 Issue 1: Reporting by US Citizens Living Abroad Issue 2: Foreign Earned Income Exclusion Issue 3: Nonresident Alien Reporting

Foreign Tax Issues By Merrill Fromer Pages 435-475 Foreign Tax Issues pg. 435 Issue 1: Reporting by US Citizens Living Abroad Issue 2: Foreign Earned Income Exclusion Issue 3: Nonresident Alien Reporting

U.S. Nonresident Alien Income Tax Return. Of what country were you a citizen or national during the tax year?

1040NR U.S. nresident Alien Income Tax Return OMB. 1545-0089 2002 Form For the year January 1 December 31, 2002, or other tax year Department of the Treasury Internal Revenue Service beginning, 2002, and

1040NR U.S. nresident Alien Income Tax Return OMB. 1545-0089 2002 Form For the year January 1 December 31, 2002, or other tax year Department of the Treasury Internal Revenue Service beginning, 2002, and

Corrigendum. OECD Pensions Outlook 2012 DOI: ISBN (print) ISBN (PDF) OECD 2012

ISBN (PDF) OECD 2012") OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

RULES GOVERNING PAYMENT PROCESSING FOR FOREIGN NATIONALS

RULES GOVERNING PAYMENT PROCESSING FOR FOREIGN NATIONALS PAYMENT ELIGIBILITY Eligibility to receive specific types of payments is determined by the foreign national s visa status https://www.obfs.uillinois.edu/obfshome.cfm?path=foreignsecure

RULES GOVERNING PAYMENT PROCESSING FOR FOREIGN NATIONALS PAYMENT ELIGIBILITY Eligibility to receive specific types of payments is determined by the foreign national s visa status https://www.obfs.uillinois.edu/obfshome.cfm?path=foreignsecure

Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services

University of Washington Student Fiscal Services") Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services 1 Agenda U. S. Source of Income Scholarships Fellowships Tuition Waivers Prizes Stipends Social Security Number Tax Related

Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services 1 Agenda U. S. Source of Income Scholarships Fellowships Tuition Waivers Prizes Stipends Social Security Number Tax Related

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A BASELINE APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A BASELINE APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION September 27, 2017 Congress and the Administration are expected to consider changes in US

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A BASELINE APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION September 27, 2017 Congress and the Administration are expected to consider changes in US

NEW VENDOR REQUEST NEW VENDOR INFORMATION INTERNATIONAL VENDOR REQUEST INDIVIDUAL

INTERNATIONAL VENDOR REQUEST INDIVIDUAL NEW VENDOR REQUEST This form, in conjunction with the attached taxpayer identification document, must be completed to add a new vendor to our accounting software

INTERNATIONAL VENDOR REQUEST INDIVIDUAL NEW VENDOR REQUEST This form, in conjunction with the attached taxpayer identification document, must be completed to add a new vendor to our accounting software

Expat Client Questionnaire

Expat Client Questionnaire The tax professionals at Williams and Parsons, PC are dedicated to serving the American expatriate community. Filling out this organizer will help with gathering the information

Expat Client Questionnaire The tax professionals at Williams and Parsons, PC are dedicated to serving the American expatriate community. Filling out this organizer will help with gathering the information

Non-Resident Tax Workshop February 28, 2013 UTSA, Business Building Room Presented by:

Non-Resident Tax Workshop February 28, 2013 UTSA, Business Building Room 2.06.04 Presented by: Christine Bodily, Payroll Department, 458-4283 Christine.Bodily@utsa.edu Cherilyn Patteson, Office of International

Non-Resident Tax Workshop February 28, 2013 UTSA, Business Building Room 2.06.04 Presented by: Christine Bodily, Payroll Department, 458-4283 Christine.Bodily@utsa.edu Cherilyn Patteson, Office of International

DO NOT FILE THIS SCHEDULE IN 2019 WITH YOUR TAX RETURN. This IRS 1040 Schedule is ONLY A DRAFT for 2019.

DO NOT FILE THIS SCHEDULE IN 2019 WITH YOUR TAX RETURN This IRS 1040 Schedule is ONLY A DRAFT for 2019. This schedule will most likely be changed before its final version is ready to be used in 2019 with

DO NOT FILE THIS SCHEDULE IN 2019 WITH YOUR TAX RETURN This IRS 1040 Schedule is ONLY A DRAFT for 2019. This schedule will most likely be changed before its final version is ready to be used in 2019 with

2018 INTERNATIONAL CONFERENCE ON MUNICIPAL FISCAL HEALTH U.S. Tax Reform and Its Impact on State and Local Government Finance Presented by Jane L.

2018 INTERNATIONAL CONFERENCE ON MUNICIPAL FISCAL HEALTH U.S. Tax Reform and Its Impact on State and Local Government Finance Presented by Jane L. Campbell ; Director NDC Washington Office National Development

2018 INTERNATIONAL CONFERENCE ON MUNICIPAL FISCAL HEALTH U.S. Tax Reform and Its Impact on State and Local Government Finance Presented by Jane L. Campbell ; Director NDC Washington Office National Development

EXPATRIATE TAX GUIDE. Taxation of income from employment in the EU & EEA

EXPATRIATE TAX GUIDE Taxation of income from employment in the EU & EEA Poland 2016 CONTENTS* 2 Austria 4 Belgium 6 Bulgaria 8 Croatia 10 Cyprus 12 Czech Republic 14 Denmark 16 Estonia 18 Finland 20 France

EXPATRIATE TAX GUIDE Taxation of income from employment in the EU & EEA Poland 2016 CONTENTS* 2 Austria 4 Belgium 6 Bulgaria 8 Croatia 10 Cyprus 12 Czech Republic 14 Denmark 16 Estonia 18 Finland 20 France