Foreign Tax Issues. By Merrill Fromer Pages

|

|

|

- Osborne Day

- 5 years ago

- Views:

Transcription

1 Foreign Tax Issues By Merrill Fromer Pages

2 Foreign Tax Issues pg. 435 Issue 1: Reporting by US Citizens Living Abroad Issue 2: Foreign Earned Income Exclusion Issue 3: Nonresident Alien Reporting Issue 4: Withholding on Payments to Nonresident Aliens Issue 5: Nonresident Spouse Treated as US Resident Issue 6: 2017 Rules for Foreign Owned US LLCs

3 Issue 1 Reporting by US Citizens/Residents Living Abroad pg. 436 Generally subject to same filing and paying rules on US source income: Some differences Filing deadlines & deductions Treatment of Income from US possessions, US govt. employees and scholarship exclusion Foreign income exclusions, exclusion or deduction for foreign housing may be available

4 Terms US Source Income NIB Fixed, determinable, annual, or periodic income Income effectively connected with a trade or business

5 Reporting by US Citizens Living Abroad pg. 436 Taxpayer worldwide income is generally taxable regardless of where the taxpayer resides in US dollars All gross income is used to determine a filing requirement Automatic 2 month extension allowed (June 15 th ) Extension to October 15 th must be requested (Form 4868) Taxpayer may request in writing for an additional 2 months

6 Sample Letter October 1, 2017 Department of the Treasury Internal Revenue Service Center Austin, Texas, Re: Izzy R. Late, SSN Dear Sir or Madam, We hereby request an extension of time until December 15, 2017, to file the 2017 US individual income tax return for the above-named taxpayer. The facts in support of this application are as follows: 1. The taxpayer is currently living outside of the United States. 2. The taxpayer filed Form 4868 on or before June 15, 2017, thus obtaining an extension of time until October 15, 2016, to file her tax return. 3. The taxpayer now requests an additional extension until December 15, 2017, because of the difficulty in gathering the information necessary to file a complete and accurate tax return.

7 Moving Expenses To or From The United States pg. 438 Same as moving to Ohio from New Jersey Move is directly related to a new full time job location Closely related to the start of work Meets distance test (50 miles further) Time test (39 weeks in first year) Directly related to foreign earned income If income is partially excluded (foreign income housing exclusion) moving expenses are allocated

8 Retirees Moving Back to The US pg. 438 Retirees no time tests Must be permanently retired (from former employment) Main job and residence must have been outside US What is considered permanently retired? Age and health Customary retirement age (similar work) Retirement payments started & Time between returning to fulltime work

9 Survivors Who Move to the US pg. 438 Spouse or dependent Death was outside the US While employed/working outside the US Must meet all 5 requirements: 1. Moves to a residence in the US 2. Within 6 months of death 3. The move is from the decedents former home 4. Decedents former home was outside the US 5. Former home was also spouse s or dependent s home

10 Allocation of Moving Expenses pg. 438 Moving expenses must be directly related to foreign earned income If any part of that foreign income is excludable under the foreign earned income exclusion or housing exclusion.. The portion related to the exclusion is not deductible

11 Reimbursements of Moving Expenses pg. 439 Nonaccountable plans included in gross income (deductible & non deductible amounts) Accountable plans include in gross income only nondeductible amounts: Meals Housing Trips Real estate expenses

12 Report of Foreign Bank and Financial Accounts pg. 439 FBAR Filing Requirements Financial interest Signature authority Any other authority or control Aggregate value exceeding $10,000 at any time during the year Deadline April 15 th / extendable to October 15 th For 2016 there was an automatic extension to October 15 th, 2017

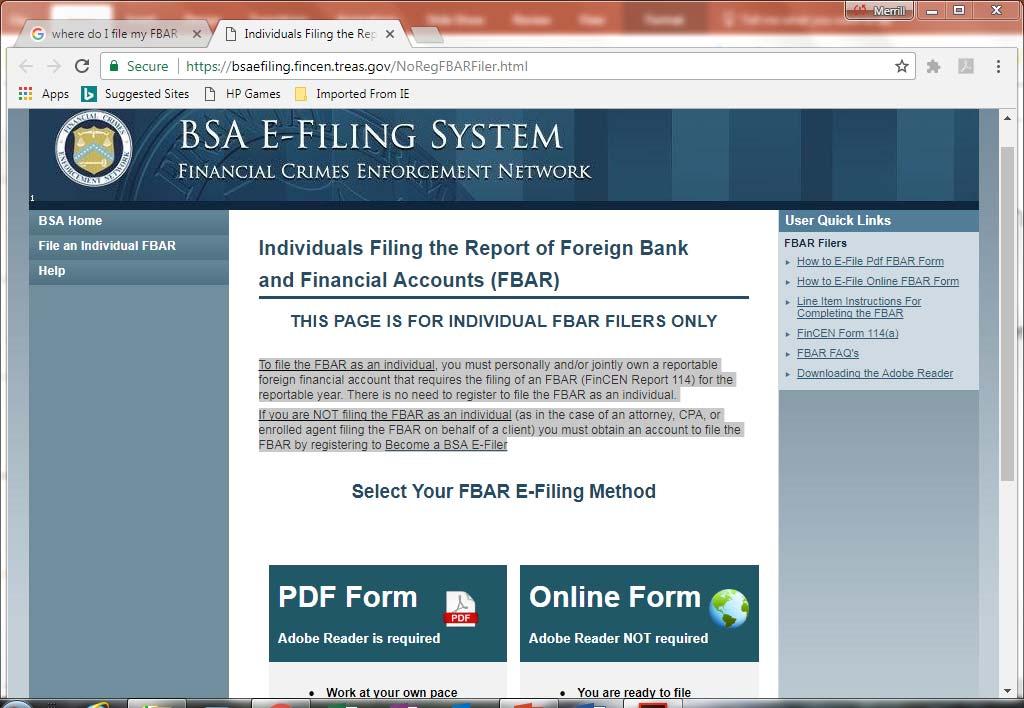

13 Filing an FBAR FinCEN Report 114 NIB To file the FBAR as an individual, you must personally and/or jointly own a reportable foreign financial account that requires the filing of an FBAR (FinCEN Report 114) for the reportable year. There is no need to register to file the FBAR as an individual. If you are NOT filing the FBAR as an individual (as in the case of an attorney, CPA, or enrolled agent filing the FBAR on behalf of a client) you must obtain an account to file the FBAR by registering to Become a BSA E-Filer

14

15 If You Failed to File an FBAR pg. 440 For taxpayers living abroad SFCP Streamlined Filing Compliance Procedure Non-residents Dual citizens OVDI Offshore Voluntary Compliance Program Chose only one For potential willful and or civil or criminal Situations - OVDI

16 FACTA - Foreign Account Tax Compliance Act pg. 440 Other filing requirements Form 8938 Statement of Specific Foreign Financial Assets Form 5741 Information Return of US person with Respect to Certain Foreign Corporations Form 3520 & or Form 3520-A Foreign Trusts and Foreign Gifts Form 8865 Return of US Persons with Respect to Certain Foreign Partnerships Form 926 Return by a US Transferor of Property to a Foreign Partnership

17 Specified Individuals NIB A U.S. citizen A resident alien of the United States for any part of the tax year (see Pub. 519 for more information) A nonresident alien who makes an election to be treated as resident alien for purposes of filing a joint income tax return A nonresident alien who is a bona fide resident of American Samoa or Puerto Rico (See Pub. 570 for definition of a bona fide resident

18 Form 8938 Filing Requirements The aggregate value of your specified foreign financial assets is more than the reporting thresholds that applies to you: Unmarried taxpayers living in the US: The total value of your specified foreign financial assets is more than $50,000 on the last day of the tax year or more than $75,000 at any time during the tax year Married taxpayers filing a joint income tax return and living in the US: The total value of your specified foreign financial assets is more than $100,000 on the last day of the tax year or more than $150,000 at any time during the tax year Married taxpayers filing separate income tax returns and living in the US: The total value of your specified foreign financial assets is more than $50,000 on the last day of the tax year or more than $75,000 at any time during the tax year.

19 A specified foreign financial asset NIB Any financial account maintained by a foreign financial institution, except as indicated on the instructions Other foreign financial assets held for investment that are not in an account maintained by a US or foreign financial institution, namely: Stock or securities issued by someone other than a U.S. person Any interest in a foreign entity, and Any financial instrument or contract that has as an issuer or counterparty that is other than a U.S. person.

20 Form Taxpayer Living Abroad NIB You are filing a return other than a joint return and the total value of your specified foreign assets is more than $200,000 on the last day of the tax year or more than $300,000 at any time during the year; or You are filing a joint return and the value of your specified foreign asset is more than $400,000 on the last day of the tax year or more than $600,000 at any time during the year

21 Income from US Territories or Possessions pg. 440 Guam Commonwealth of the Northern Mariana Islands American Samoa US Virgin Islands Puerto Rico

22 Determining Residency Status in US Territories pg Physically present in the territory for 183 days during the tax year Does not have a tax home outside the territory during the tax year, and Does not have a closer connection to the US or to another foreign country

23 Self-Employment US Territory pg. 441 Self-employed in a US Territory pay self-employment tax Regardless if the income is excludable Regardless if you otherwise have no US filing requirement File 1040-SS or Form 1040-PR (Puerto Rico)

24 Issue #2 Foreign Earned Income/Housing Exclusion Page

25 Income Exclusion pg. 444 Income Exclusion $102,100 Housing 16,336 Exclusion/Deduction Total exclusion/deduction $118,436

26 Foreign County pg. 445 A foreign country is any territory (including the air space and territorial waters) Under the sovereignty of a government other than that of the US. It includes the seabed and subsoil of those submarine areas adjacent to the territorial waters of a foreign country and over which the foreign country has exclusive rights under international law to explore and exploit the natural resources

27 Foreign Country pg.445 Foreign country does not include US possessions such as Puerto Rico, Guam, the Commonwealth of the Northern Mariana Islands, the U.S. Virgin Islands, or American Samoa. For purposes of these foreign exclusions or deduction, the terms foreign, abroad, and overseas, refer to areas outside the US, American Samoa, Guam, the Commonwealth of the Northern Mariana Islands, Puerto Rico, the U.S. Virgin Islands, and the Antarctic region. Foreign country does not include ships and aircraft traveling in or above international waters, and it does not include offshore installations that are located outside the territorial waters of any individual nation.

28 What is Foreign Earned Income? Pg. 445 Income you earn in a foreign country (performing services) Construction Playing ball Working in the mall Selling/serving coffee Self-employment

29 Foreign Earned Income Does Not Include pg Pay received as a military or civilian employee of the US government or any of its agencies 2. Pay for services conducted in international waters (not a foreign country) 3. Pay in combat zones, as designated by an executive order of the president 4. Payments received after the end of the tax year following the year in which the services that earned the income were performed 5. The value of meals and lodging furnished for the convenience of the employer 6. Pension or annuity payments, including social security benefits

30 Tax Home pg. 445 A tax home is the general area of a taxpayer s main place of business, employment, or post of duty, regardless of where he or she maintains a family home. Tax home is the place where the taxpayer is permanently or indefinitely engaged to work as an employee or self-employed individual. Having a tax home in a specific location does not necessarily mean that the location is the taxpayer s place of residence or domicile for tax purposes.

31 Tax Home and Abode pg. 446 Abode is defined as one's home, habitation, residence, domicile, or place of dwelling. It does not mean a principal place of business. Abode is not the same as tax home. The location of a person s abode often will depend on where he or she maintains economic, family, and personal ties

32 Example 12.2 pg. 446 Taxpayer works on an offshore oil rig in territorial waters of Spain Works 28-day on and than 28-days off Returns to U.S. residence during his 28-days off Adobe is in the US Tax home is not in a foreign country No exclusion for income

33 Example 12.3 Tax Home and Abode is in a Foreign Country pg. 446 Taxpayer has been living/working in Massachusetts for several years November 2016 transferred to London, England She expects to be there for at least 15 months Placed her car and belongings in storage Rented her home to another family Moved her husband and children to employer provided rental in London Rented a car, British driving license, library cards, opened bank accounts enrolled children in school.

34 Bona Fide Residence Test pg Taxpayer intention Purpose of the trip Nature and length of stay Form 2555 must be filed with the IRS IRS makes the determination if the taxpayer is a bona fide resident of a foreign country Temporary job (even longer than 1 year) does not qualify Foreign country has a treaty with the US

35 Example 12.5 Domicile vs. Residence pg. 447 GG went to Paris to for an extended period of time Set up permanent quarters for herself and family She always intended to return to her home in Ohio She could have her domicile in Ohio and bona fide residence in Paris

36 Uninterrupted Period (Entire Year) pg. 447 The Test Must reside in a foreign country Uninterrupted period of time that includes an entire year January 1 December 31 Taxpayer can have periods of absence (vacations, business, health) Must intend to return to foreign residence in a reasonable time

37 Example 12.6 pg. 447 Katsu Lin is the Tokyo representative of a US employer He arrived with his family in Tokyo on 11/1/2016 His assignment is indefinite, and he intends to live there with his family until his company sends him to a new post He immediately established residence in Tokyo On 4/2/2017 he traveled to the United States to meet with his employer, leaving his family in Tokyo He returned to Tokyo on 5/1 and continued living there On 1/1/2018, he will have completed an uninterrupted period of residence for a full tax year, and he may qualify as a bona fide resident of Japan.

38 Bona Fide Residence Allocation pg. 448 Once a taxpayer meets the bona fide residence test for 1 year, other years come into play If I arrive in Spain for employment on 3/1/2016 Remain in Spain the entire 2017 year Return to Ohio 6/30/2018 I now have a partial year for 2016 and 2018 If I have not yet filed my 2016 return I could claim a partial year income exclusion If I did file my 2016, I would need to file an amended 2016 return

39 Physical Presence Test pg. 448 Another option to qualifying for the income and housing exclusions Physically present for 330 full days Nature and purpose still count (tax home) Type of residence and intentions of returning are not considered Generally much easier to meet this test Still requires a US Treaty with the foreign country(s)

40 Counting The Months pg. 449 Can begin any day Ends the day before the same calendar day (12 months later) Must be 12 consecutive months Does not have to start when you enter or leave the foreign country The taxpayer can choose the 12 month period The 12 month periods can overlap

41 Example pg. 449 Larry worked in New Zealand for a 20 month period (1/1/16 8/31/17) February 2016 spent 29 days & February days in the U.S. In New Zealand 330 full days each of the following 2, 12 month periods 1/1/ /31/2016 & 9/1/2016 8/31/2017 By overlapping, he meets the physical presence test for the entire 20 months

42 Exception to Both Tests pg. 449 War Civil unrest Similar adverse conditions Must have established tax home Met the bona fide residence or physical presence test IRS publishes list of countries and minimum time requirements Taxpayer must still allocate income or housing exclusion based on actual days present in the foreign country

43 Claiming The Exclusion or Deduction pg Form 2552 or Form 2555EZ (If no SE income, total foreign did not exceed $101,300, and you had no business or moving expenses) Filed with your Form 1040 or 1040X The Form is actually an eligibility application Claiming the credit is an optional election The Form is used to claim the income exclusion or the allowance/deduction

44 Effect on Other Deductions pg. 453 No Foreign Tax Credit (against excluded income) No additional child tax credit or EITC (income exclusion or housing exclusion) IRA contribution add back either/both exclusion(s) to determine compensation for IRA contribution limits

45 Foreign Housing Exclusion or Deduction pg. 453 Same test for income exclusion Housing exemption - Employer provided funds directly or indirectly Housing deduction Paid from self-employed income

46 Foreign Housing Exclusion pg. 450 Qualified expenses is limited to 30% of foreign earned income exclusion 2017 limit is $102,100 X 30% = $30,630 This is further reduced and limited to a 16% of maximum income exclusion (later slide) The limit varies by country (city) like per diem there is a list

47 Part Year Exclusion pg. 451 A qualifying taxpayer must adjust the maximum exclusion based on the number of qualifying days Multiply $102,100 X qualifying days / 365 Assume you meet all of the qualifying test and you were present for 330 full days in $102,100 X 330 days = 33,693,000 / 365 = $92,310 exclusion (90%)

48 What s in Housing Expenses pg. 453 Reasonable expenses paid or incurred For qualifying period of time Do in include costs that increase the value or life of the property

49 Calculation The Exclusion/Deduction pg % X $102,100 = $16,336 / 365 day = $44.76 per day (max) Less this base housing amount from his/her total housing expense to arrive at the housing amount for the year Up to the 30% of the maximum foreign earned income exclusion Dependent on location Claimed on Form 2555 Limited to net foreign earned income Excess can be carried over 1 year

50 Issue 3 Nonresident Alien Reporting pg. 454 Generally subject to US tax on US source income Table 2-1 IRS Pub 519 Income is divided into two categories 1. Fixed, Determinable, Annual or Periodic income or 2. Effectively connected income

51 Issue 3: Nonresident Alien Reporting p. 454

52 Two Categories of US Sourced Income FDAP pg. 455 Category 1 Fixed paid in amounts known ahead of time Determinable specific basis for computing the amount Annual until a specific event occurs (death) Periodic paid from time to time (can increase or decrease in $ or length)

53 US Source Income Does Not Include pg. 455 Gains derived from the sale of real or personal property (including market discount Option Premiums (not including original issue discount) Items of income excluded from gross income, without regard to the US or foreign status of Tax-exempt municipal bond interest Certain scholarship income (depends on residence of payer)

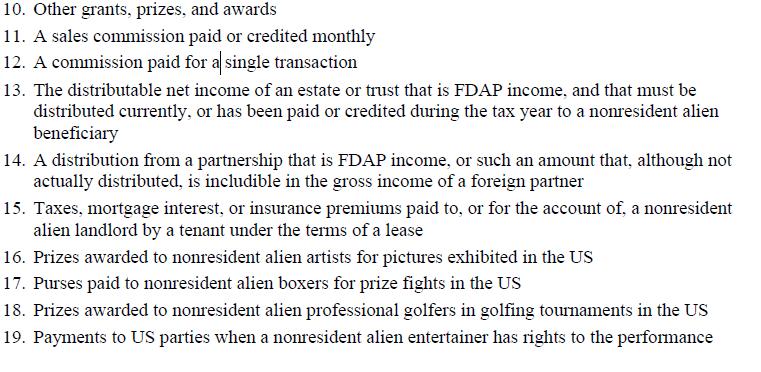

54 US Source Income Does Include pg Compensation for personal services (such as commissions and gross proceeds from performances) 2. Dividends 3. Interest (but see the later discussion of nontaxable interest) 4. Original issue discount 5. Pensions and annuities 6. Alimony 7. Real property income, such as rents, other than gains from the sale of real property 8. Royalties 9. Scholarships and fellowship grants (depends on residence of payer)

55

56 US Source FDAP pg. 456 Social Security Benefits 85% in includable (unless treaty rate) Net Capital Gains- 30% rate (183 day rule )(unless treaty rate) 183 day rule - If individual/nonresident alien is present in US for 183 or more days during the tax year Less than 183 days no tax on listed capital gain transaction Many tax treaties eliminate most capital gains (encourage investment in US) Generally does not apply to residential Real Estate

57 Tax Treaties pg. 458 Compensation for personal services (independent contractor) treaty may exempt you from withholding (provide withholding agent Form 8233) Alien students, trainees, teachers & researchers (employees) exempt, use Form 8233 (most treaties) Other treaties exempting US sourced income require Form 8233 Form 8233 need to be filed each tax year Form W-4 should be provided to employer (see Pub 15)

58 Tax Treaties Disclosure pg. 458 File Form 8233 with tax return any time claiming a treaty benefit Taxpayer must file a US return and Form 8233 for any listed benefit 1. A reduction or modification in the taxation of gain or loss from the disposition of a US real property interest based on a treaty 2. A change to the source of an item of income or a deduction based on a treaty 3. A credit for a specific foreign tax for which a foreign tax credit would not usually be allowed under the Internal Revenue Code

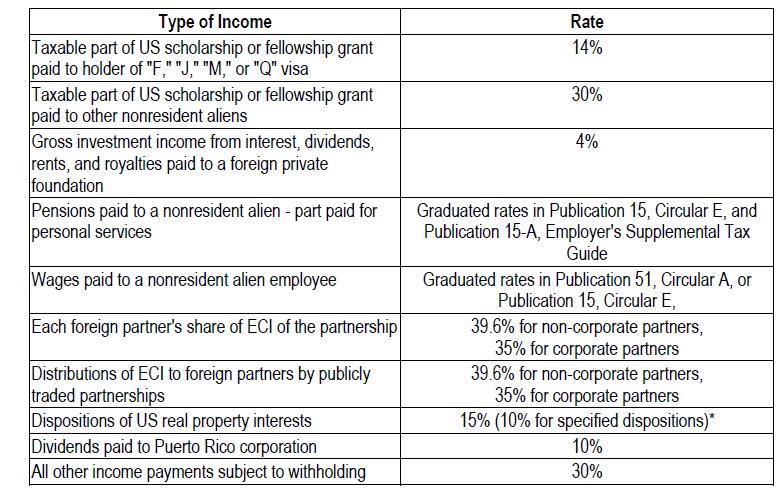

59 Other Excluded Income (non-treaty) pg. 459 Interest income not connected to a US trade or business Generally include CD s Deposit/withdrawable accounts savings, checking Amounts held by an insurance company under an agreement to pay interest

60 Income #2 Effectively Connected Income (ECI) pg. 459 Associated with a US trade or business under the principles of US tax law Generally associated with Visa designation F, J, M, Q Deductions can be claimed against EIC to arrive at net EIC Net EIC is taxed at same rates as US citizens & residents (unless treaty rate) Reported on 1040-NR List of other trade or business income considered ECI in book and (Pub 519)

61 ECI pg. 459 Wages & any other compensation performed in the US Location of where the service is determines if income is ECI Exceptions personal services provided by an independent resident alien contractor may be specially exempted by a treaty Specific treaty provisions IRS Publication 915 Income should be allocated between US/outside the US by days of service

62 Example pg. 461 Jean Garneau, a citizen and resident of Canada, is employed as a professional hockey player by a US hockey club. Under Jean's contract, he received $150,000 for 242 days of play during the year This includes days spent at pre-season training camp, days during the regular season, and playoff game days. Of the 242 days, 194 days were spent performing services in the US and 48 days were spent performing services in Canada. The amount of US source income is $120,248 ( ) $150,000

63 Allocation of Fringe Benefits pg. 461 Allocated based on geographic basis Housing benefits Education benefits Local transportation benefits Tax benefits/reimbursements allocated to taxing jurisdictions Hazard pay allocated to pay zone Moving expenses allocated to new employment location

64 Sources of Income pg. 462 Vessel of Aircrafts Airline or cruse ship employees Does use begin and end in the US? Yes considered derived entirely from sources in the US and subject to withholding if not effectively connected to a US trade or business Crew members of a foreign vessel(nonresident aliens) temporary presence not income from a US source

65 Sources of Income pg. 462 Scholarships, Fellowships and Grants US sourced = income from US Pension Payments Source of pension determines if income work is performed in the US = US source income Pension Earnings Pension trust is a US trust = US source income Treaties always override general rules/law there are several for pensions and Social Security (Mexico and Canada)

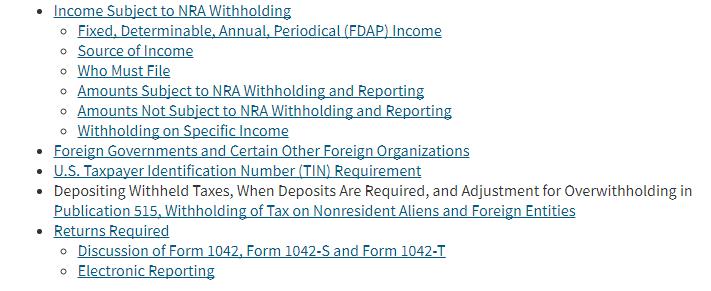

66 Issue #4: Withholding on Payments pg. 463 Withholding help ensure the filing of a tax return that might otherwise never been filed The term NRP Withholdings refers to withholding on payments under: IRC 1441, 1442 & FDAP is subject to a flat 30% (or a reduced rate) Tax is generally withheld from the payment

67 NRA refers to IRC 1441, 1442 & 1443 withholding requirements pg. 463 Generally, a foreign person is subject to U.S. tax on its U.S. source income. Most types of U.S. source income received by a foreign person are subject to U.S. tax of 30%. A reduced rate, including exemption, may apply if an Internal Revenue Code Section provides for a lower rate, or there is a tax treaty between the foreign person's country of residence and the United States. The tax is generally withheld (NRA withholding) from the payment made to the foreign person.

68 NRA Withholdings NIB The term NRA withholding is used in this area descriptively to refer to withholding required under sections 1441, 1442, and 1443 of the Internal Revenue Code. Generally, NRA withholding describes the withholding regime that requires 30% withholding on a payment of U.S. source income and the filing of Form 1042 and related Form 1042-S. Payments to all foreign persons, including nonresident alien individuals, foreign entities and governments, may be subject to NRA withholding

69

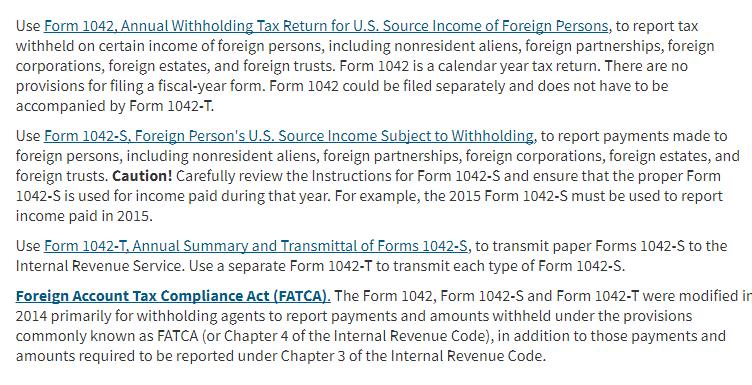

70 Use Form 1042, Annual Withholding Tax Return for U.S. Source Income of Foreign Persons, Use Form 1042-S, Foreign Person's U.S. Source Income Subject to Withholding,. Use Form 1042-T, Annual Summary and Transmittal of Forms 1042-S. Foreign Account Tax Compliance Act (FATCA). The Form 1042, Form 1042-S and Form 1042-T were modified in 2014 primarily for withholding agents to report payments and amounts withheld under the provisions commonly known as FATCA (or Chapter 4 of the Internal Revenue Code), in addition to those payments and amounts required to be reported under Chapter 3 of the Internal Revenue Code.

71

72 Amounts not subject to withholding pg. 464 Portfolio interest paid on obligations that meet certain requirements Bank deposit interest that is not effectively connected with the conduct of a US trade or business Original issue discount (OID) on certain short-term obligations Nonbusiness gambling income of a nonresident alien playing blackjack, baccarat, craps, roulette, or big-6 wheel in the US Amounts paid as part of the purchase price of an obligation sold between interest payment dates OID paid on the sale of an obligation other than a redemption Insurance premiums paid on a contract issued by a foreign insurer

73 When, Who & How Much to Withhold pg. 465 Withholding agent Statutory rates generally 30 % - there are also reduced rates Many treaties have either reduced or eliminate withholdings Often rates are based on Visa designation Withholdings are withheld at time of payment

74

75 Who is the Withholding Agent pg. 466 Could be a US or Foreign person, partnership, trust, association or corporation just about anyone or any entity foreign or domestic Could be more than one withholding agent for the same payment Has control, receipt, control, disposal or payment to a foreign person

76 Domestic & Foreign Trust Funds Rules/Same Withholding agent is personally liable for any tax liability required to be withheld Independent of the foreign persons tax liability If the agent fails to withheld & foreign payee fails to pay both are liable for the tax Tax only will be collected once

77 Issue #5 - Nonresident Spouse Treated as US Resident pg. 471 One Taxpayer must be a US citizen or resident alien or One spouse is not a resident until the end of the year If spouses elect to treat the nonresident alien spouse as a US resident, the following three rules apply: 1. Both spouses are treated, for income tax purposes, as residents for all tax years for which the election is in effect. 2. They must file a joint income tax return for the year in which they make the election. 3. Neither spouse can claim under any tax treaty that they are not a US resident for a tax year for which the election is in effect

78 Example pg. 472 Pat Smith, a US citizen, is married to Norman, a nonresident alien. Pat and Norman make the election to treat Norman as a resident alien by attaching a statement to their joint return. Pat and Norman must report their worldwide income for the year for which they make the election and for all later years unless the election is suspended or terminated. Although Pat and Norman must file a joint return for the year for which they make the election, they can file either joint or separate returns for later years.

79 Making the Election pg. 472 No specific Form exists Spouse must have a valid Social Security number or ITIN Statement attached to current return signed by both spouses Declaration that one spouse that one spouse is either a US citizen or resident alien and the other neither Include both names, address(s) and signatures (SSN and or ITIN) Attach to the joint return or amended joint return Sample election is in the book

80 Suspending the Election pg. 473 Automatic suspension if neither spouse is a US citizen or resident alien (election applies to partial year) Election is unsuspended if status reverts to prior year (citizen, resident status re-instated) Revocation election for any year by the original due date of the return (statement attach to return with community property information)

81 Termination Of Election pg. 473 Termination upon death of either spouse (following year) Divorce or Legal Separation January 1 in the year the divorce or separation occurs Inadequate records IRC can terminate (tax or status records)

82 Resident Alien NIB A resident alien is a foreign person who is a permanent resident of the country in which he or she resides, but does not have citizenship. To fall under this classification in the United States, a person needs to either have a current green card or have had one in the previous calendar year. People can also fall under the U.S. classification of resident alien if they have been in the United States for more than 31 days during the current year, along with having been in the United States for at least 183 days over a three-year period, including the current year.

83 Issue #6 Foreign Owned U.S. LLC s pg. 474 For tax years beginning on or after January 1, 2017 New Regs. treat foreign owned (directedly or indirectly) subject to reporting requirements under IRC 6038 For a 25% or more foreign owned LLC, Corporation or foreign corporation engaged in a U.S. trade or business Form 5472

84 The End Questions

85 What s in Housing Expenses pg. 453 Reasonable expenses paid or incurred For qualifying period of time Do in include costs that increase the value or life of the property

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014 Federal Income Tax Withholding 14.1-1 U.S. citizens & resident aliens are subject to income tax withholding

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014 Federal Income Tax Withholding 14.1-1 U.S. citizens & resident aliens are subject to income tax withholding

Taxation of: U.S. Foreign Nationals

Taxation of: U.S. Foreign Nationals 2017 Edition ZanderSterling.com 1 The information contained in this publication is provided for general informational purposes only and is based on U.S. income tax law

Taxation of: U.S. Foreign Nationals 2017 Edition ZanderSterling.com 1 The information contained in this publication is provided for general informational purposes only and is based on U.S. income tax law

Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding

Form W-8BEN Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding (Rev. February 2006) OMB No. 1545-1621 Department of the Treasury Section references are to the Internal

Form W-8BEN Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding (Rev. February 2006) OMB No. 1545-1621 Department of the Treasury Section references are to the Internal

The United States Government defines an alien as any individual who is not

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

Americans Living Abroad. 61 Tax Questions you should know.

Americans Living Abroad 61 Tax Questions you should know 1 General FAQs 1. I m a U.S. citizen living and working outside of the United States for many years. Do I still need to file a U.S. tax return?

Americans Living Abroad 61 Tax Questions you should know 1 General FAQs 1. I m a U.S. citizen living and working outside of the United States for many years. Do I still need to file a U.S. tax return?

Form 1040NR Filing Challenges and Effective Approaches

Form 1040NR Filing Challenges and Effective Approaches Determining Taxpayer Classifications and Elections, Computing Income and Deductions, and Understanding Spouse/Dependent Treatment TUESDAY, SEPTEMBER

Form 1040NR Filing Challenges and Effective Approaches Determining Taxpayer Classifications and Elections, Computing Income and Deductions, and Understanding Spouse/Dependent Treatment TUESDAY, SEPTEMBER

If you have foreign accounts, entities, or assets, chances are that you

International Tax Form Filing Guide If you have foreign accounts, entities, or assets, chances are that you will be required to file various forms disclosing them. Some of these forms are filed with your

International Tax Form Filing Guide If you have foreign accounts, entities, or assets, chances are that you will be required to file various forms disclosing them. Some of these forms are filed with your

U.S. Tax Guide for Aliens

Department of the Treasury Internal Revenue Service Publication 519 Cat. No. 15023T U.S. Tax Guide for Aliens For use in preparing 2000 Returns Contents Introduction... 1 Important Changes... 2 Important

Department of the Treasury Internal Revenue Service Publication 519 Cat. No. 15023T U.S. Tax Guide for Aliens For use in preparing 2000 Returns Contents Introduction... 1 Important Changes... 2 Important

MANAGING INTERNATIONAL TAX ISSUES

MANAGING INTERNATIONAL TAX ISSUES Starting A Business Retirement Strategies Operating A Business Marriage Investing Tax Smart Estate Planning Ending A Business Off to School Divorce And Separation Travel

MANAGING INTERNATIONAL TAX ISSUES Starting A Business Retirement Strategies Operating A Business Marriage Investing Tax Smart Estate Planning Ending A Business Off to School Divorce And Separation Travel

Domestic Tax Issues for Non-resident Aliens

Domestic Tax Issues for Non-resident Aliens Presented by Monica Haven, EA, JD, LLM mhaven@pobox.com www.mhaven.net What we ll cover Are Non-resident Aliens from Mars? Where is home for Dual Status Aliens?

Domestic Tax Issues for Non-resident Aliens Presented by Monica Haven, EA, JD, LLM mhaven@pobox.com www.mhaven.net What we ll cover Are Non-resident Aliens from Mars? Where is home for Dual Status Aliens?

The HIRE Act contains several provisions of interest to clients with foreign accounts and foreign trusts including the FATCA provisions.

On March 18, 2010 President Obama signed into law the Hiring Incentives to Restore Employment (HIRE) Act which provided tax incentives to employers who hire and retain workers. To pay for these benefits,

On March 18, 2010 President Obama signed into law the Hiring Incentives to Restore Employment (HIRE) Act which provided tax incentives to employers who hire and retain workers. To pay for these benefits,

Aliens & Citizens: Foreign and Domestic Tax Issues

Aliens & Citizens: Foreign and Domestic Tax Issues What we ll cover Are Non-resident Aliens from Mars? Where is home for Dual Status Aliens? How do we tax extraterrestrial income? Do Space Treaties give

Aliens & Citizens: Foreign and Domestic Tax Issues What we ll cover Are Non-resident Aliens from Mars? Where is home for Dual Status Aliens? How do we tax extraterrestrial income? Do Space Treaties give

International Tax and Asset- Reporting for the Everyday Client

International Tax and Asset- Reporting for the Everyday Client Jason B. Freeman, J.D., CPA Freeman Law, PLLC 2595 Dallas Pkwy., Suite 420 Frisco, Texas 75034 www.freemanlaw-pllc.com Copyright Freeman Law,

International Tax and Asset- Reporting for the Everyday Client Jason B. Freeman, J.D., CPA Freeman Law, PLLC 2595 Dallas Pkwy., Suite 420 Frisco, Texas 75034 www.freemanlaw-pllc.com Copyright Freeman Law,

U.S. Income Tax for Foreign Students, Scholars and Teachers. Arthur R. Kerr II Vacovec Mayotte & Singer LLP

U.S. Income Tax for Foreign Students, Scholars and Teachers Arthur R. Kerr II Vacovec Mayotte & Singer LLP 617-964-0500 akerr@vacovec.com Are You Resident or Nonresident? Residence for tax purposes not

U.S. Income Tax for Foreign Students, Scholars and Teachers Arthur R. Kerr II Vacovec Mayotte & Singer LLP 617-964-0500 akerr@vacovec.com Are You Resident or Nonresident? Residence for tax purposes not

, ending. child tax credit (1) First name Last name

First name Last name") Department of the Treasury Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return 2016 OMB No. 1545-0074 For the year Jan. 1-Dec. 31, 2016, or other tax year beginning, ending Form Your first

Department of the Treasury Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return 2016 OMB No. 1545-0074 For the year Jan. 1-Dec. 31, 2016, or other tax year beginning, ending Form Your first

EXPAT TAX HANDBOOK. Non-Citizens and U.S. Tax Residency. Tax Year Ephraim Moss, Esq Ext 101

EXPAT TAX HANDBOOK Non-Citizens and U.S. Tax Residency Tax Year 2018 Ephraim Moss, Esq. 718-887-9933 Ext 101 emoss@expattaxprofessionals.com Joshua Ashman, CPA 718-887-9933 Ext 102 jashman@expattaxprofessionals.com

EXPAT TAX HANDBOOK Non-Citizens and U.S. Tax Residency Tax Year 2018 Ephraim Moss, Esq. 718-887-9933 Ext 101 emoss@expattaxprofessionals.com Joshua Ashman, CPA 718-887-9933 Ext 102 jashman@expattaxprofessionals.com

Taxation of: U.S. Citizens & Residents Living Abroad

Taxation of: U.S. Citizens & Residents Living Abroad 2017 Edition ZanderSterling.com 1 The information contained in this publication is provided for general informational purposes only and is based on

Taxation of: U.S. Citizens & Residents Living Abroad 2017 Edition ZanderSterling.com 1 The information contained in this publication is provided for general informational purposes only and is based on

U.S. taxation of foreign citizens

U.S. taxation of foreign citizens Global Mobility Services 2019 kpmg.com U.S. taxation of foreign citizens The following information is not intended to be written advice concerning one or more Federal

U.S. taxation of foreign citizens Global Mobility Services 2019 kpmg.com U.S. taxation of foreign citizens The following information is not intended to be written advice concerning one or more Federal

Alien Tax Home Representation Form

Alien Tax Home Representation Form I have reviewed the attached tax home information for aliens and/or have consulted with my tax advisor and make the following good faith representation (please check

Alien Tax Home Representation Form I have reviewed the attached tax home information for aliens and/or have consulted with my tax advisor and make the following good faith representation (please check

American Citizens Abroad. Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION

American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation 5 December 2016; 1 November 2017; 1 December 2017; 18 January 2018; 19 April 2018 INTRODUCTION This side-by-side analysis

American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation 5 December 2016; 1 November 2017; 1 December 2017; 18 January 2018; 19 April 2018 INTRODUCTION This side-by-side analysis

Aliens & Citizens Foreign and Domestic Tax Issues

Aliens & Citizens Foreign and Domestic Tax Issues Monica Haven 051711 Summary Whether from Venus or Venice, resident or nonresident, illegal worker or student, here or overseas, US taxpayers face a myriad

Aliens & Citizens Foreign and Domestic Tax Issues Monica Haven 051711 Summary Whether from Venus or Venice, resident or nonresident, illegal worker or student, here or overseas, US taxpayers face a myriad

Tax Issues for U.S. Citizens Living Abroad

LifeMark Partners, Inc. 1306 Concourse Drive Suite 350 Linthicum, MD 21090 410-837-3022 marketing@lifemarkpartners.com www.lifemarkpartners.com Tax Issues for U.S. Citizens Living Abroad Page 1 of 5, see

LifeMark Partners, Inc. 1306 Concourse Drive Suite 350 Linthicum, MD 21090 410-837-3022 marketing@lifemarkpartners.com www.lifemarkpartners.com Tax Issues for U.S. Citizens Living Abroad Page 1 of 5, see

THE F-1 VISA PRIVILEGED U.S. TAX STATUS AND HOW TO KEEP IT

THE F-1 VISA PRIVILEGED U.S. TAX STATUS AND HOW TO KEEP IT Authors Neha Rastogi Beate Erwin Tags Exempt Individual F-1 Visa Foreign Students Nonresident Alien Foreign students leaving their home country

THE F-1 VISA PRIVILEGED U.S. TAX STATUS AND HOW TO KEEP IT Authors Neha Rastogi Beate Erwin Tags Exempt Individual F-1 Visa Foreign Students Nonresident Alien Foreign students leaving their home country

~E~ E-3 visa, 103 Earnings statement, 100, 131, 135, 136,

Index ~A~ ACA Affordable Care Act 14, 173 A, G visa holders, 5, 6, 7, 37, 103 A-2 visa, PRI 6, 126, 132, 133 A-3 visa, 138, 141 Abuse, abusive employment situation, 141,142 Actual days, Z, 7, 8 Adjusted

Index ~A~ ACA Affordable Care Act 14, 173 A, G visa holders, 5, 6, 7, 37, 103 A-2 visa, PRI 6, 126, 132, 133 A-3 visa, 138, 141 Abuse, abusive employment situation, 141,142 Actual days, Z, 7, 8 Adjusted

THE TAXATION OF INDIVIDUALS AND FAMILIES

THE TAXATION OF INDIVIDUALS AND FAMILIES Scheduled for a Public Hearing Before the TAX POLICY SUBCOMMITTEE of the HOUSE COMMITTEE ON WAYS AND MEANS on July 19, 2017 Prepared by the Staff of the JOINT COMMITTEE

THE TAXATION OF INDIVIDUALS AND FAMILIES Scheduled for a Public Hearing Before the TAX POLICY SUBCOMMITTEE of the HOUSE COMMITTEE ON WAYS AND MEANS on July 19, 2017 Prepared by the Staff of the JOINT COMMITTEE

Instructions for Form 1042-S Foreign Person s U.S. Source Income Subject to Withholding

2009 Instructions for Form 1042-S Foreign Person s U.S. Source Income Subject to Withholding Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

2009 Instructions for Form 1042-S Foreign Person s U.S. Source Income Subject to Withholding Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

Foreign Tax Issues REBECCA DONEHEW

Foreign Tax Issues REBECCA DONEHEW Form 5471 Information Returns of U.S. Persons with Respect to Certain Foreign Corporations Used to satisfy the reported requirements of transactions between foreign corporations

Foreign Tax Issues REBECCA DONEHEW Form 5471 Information Returns of U.S. Persons with Respect to Certain Foreign Corporations Used to satisfy the reported requirements of transactions between foreign corporations

U.S. TAX ISSUES FOR CANADIANS

U.S. TAX ISSUES FOR CANADIANS If you own rental property in the United States or spend extended periods of time there, you could be subject to various U.S. filing requirements, even though you may have

U.S. TAX ISSUES FOR CANADIANS If you own rental property in the United States or spend extended periods of time there, you could be subject to various U.S. filing requirements, even though you may have

Canadian Residents Going Down South

Canadian Residents Going Down South P151(E) Rev. 10 Is this pamphlet for you? T his pamphlet is for you if you spent part of the year in the United States (U.S.), for example, for health reasons or on

Canadian Residents Going Down South P151(E) Rev. 10 Is this pamphlet for you? T his pamphlet is for you if you spent part of the year in the United States (U.S.), for example, for health reasons or on

TAX TIPS FOR FOREIGN MISSIONARIES OF THE SEVENTH-DAY ADVENTIST CHURCH

TAX TIPS FOR FOREIGN MISSIONARIES OF THE SEVENTH-DAY ADVENTIST CHURCH RICHARD E. GREEN, CPA 5010 Centennial Commons Dr NW Acworth, GA 30102-2181 Phone (770) 529-4394 EMAIL taxman@regreencpa.com Web Page

TAX TIPS FOR FOREIGN MISSIONARIES OF THE SEVENTH-DAY ADVENTIST CHURCH RICHARD E. GREEN, CPA 5010 Centennial Commons Dr NW Acworth, GA 30102-2181 Phone (770) 529-4394 EMAIL taxman@regreencpa.com Web Page

American Citizens Abroad. Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION

1 November 2017; 1 December 2017; 19 January 2018 American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION This side-by-side analysis compares Current Law (i.e.,

1 November 2017; 1 December 2017; 19 January 2018 American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION This side-by-side analysis compares Current Law (i.e.,

2017 Instructions for Schedule 8812

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule 8812 Child Tax Credit Part I of Schedule 8812 documents that any qualifying child whom you identify with an ITIN is a

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule 8812 Child Tax Credit Part I of Schedule 8812 documents that any qualifying child whom you identify with an ITIN is a

Instructions for Form W-7

Instructions for Form W-7 (January 2010) Application for IRS Individual Taxpayer Identification Number Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

Instructions for Form W-7 (January 2010) Application for IRS Individual Taxpayer Identification Number Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

U.S. Tax Guide for Aliens

Department of the Treasury Internal Revenue Service Publication 519 Cat. No. 15023T U.S. Tax Guide for Aliens For use in preparing 2013 Returns Contents Introduction... 1 What's New... 2 Reminders... 3

Department of the Treasury Internal Revenue Service Publication 519 Cat. No. 15023T U.S. Tax Guide for Aliens For use in preparing 2013 Returns Contents Introduction... 1 What's New... 2 Reminders... 3

EXPAT TAX.A TO Z. ASSETS Anything you own that has value is considered an asset. Bank accounts,

EXPAT TAX.A TO Z US tax law is difficult enough to understand without the added burden of trying to understand the overseas side of things. Here is an explanation of expat key words and phrases that will

EXPAT TAX.A TO Z US tax law is difficult enough to understand without the added burden of trying to understand the overseas side of things. Here is an explanation of expat key words and phrases that will

Earned Income Credit i

Earned Income Credit i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

Earned Income Credit i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

U.S. Taxation of Americans Abroad

GLOBAL MOBILITY SERVICES U.S. Taxation of Americans Abroad kpmg.com U.S. taxation of Americans abroad The following information is not intended to be written advice concerning one or more federal tax matters

GLOBAL MOBILITY SERVICES U.S. Taxation of Americans Abroad kpmg.com U.S. taxation of Americans abroad The following information is not intended to be written advice concerning one or more federal tax matters

EXPAT TAX HANDBOOK. Tax Considerations For Remote Workers Living Abroad

EXPAT TAX HANDBOOK Tax Considerations For Remote Workers Living Abroad Tax Year 2017 Expat Tax Handbook Tax Considerations for Remote Workers Living Abroad Table of Contents: Introduction / 3 U.S. Federal

EXPAT TAX HANDBOOK Tax Considerations For Remote Workers Living Abroad Tax Year 2017 Expat Tax Handbook Tax Considerations for Remote Workers Living Abroad Table of Contents: Introduction / 3 U.S. Federal

Instructions for Form 1040NR-EZ

2011 Instructions for Form 1040NR-EZ U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Department of the Treasury Internal Revenue Service Section references are to the Internal

2011 Instructions for Form 1040NR-EZ U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Department of the Treasury Internal Revenue Service Section references are to the Internal

Foreign Student and Scholar Volunteer Tax Return Preparation. VITA Training 1

Foreign Student and Scholar Volunteer Tax Return Preparation VITA Training 1 e-learning Options & Understanding Taxes Website http://www.irs.gov/app/understandingtaxes/index.jsp VITA Training 2 Foreign

Foreign Student and Scholar Volunteer Tax Return Preparation VITA Training 1 e-learning Options & Understanding Taxes Website http://www.irs.gov/app/understandingtaxes/index.jsp VITA Training 2 Foreign

EXPATRIATE TAX QUESTIONNAIRE FOR U.S. CITIZENS LIVING ABROAD. Acosta Tax & Advisory, PA

EXPATRIATE TAX QUESTIONNAIRE FOR U.S. CITIZENS LIVING ABROAD Acosta Tax & Advisory, PA This questionnaire can be filled out by hand or in MS Word Indicate year this form is completed for: Primary Taxpayer

EXPATRIATE TAX QUESTIONNAIRE FOR U.S. CITIZENS LIVING ABROAD Acosta Tax & Advisory, PA This questionnaire can be filled out by hand or in MS Word Indicate year this form is completed for: Primary Taxpayer

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

Your Federal Income Tax Responsibilities as an Au Pair

S. Landau Services Steven Landau, E.A.* 2610 NW 56th Street #103 Seattle, WA 98107-4118 PHONE: (206) 784-1070 TOLL FREE: (877) 220-3241 TOLL FREE FAX: (877) 220-3889 E-MAIL: Steven@SLandauServices.com

S. Landau Services Steven Landau, E.A.* 2610 NW 56th Street #103 Seattle, WA 98107-4118 PHONE: (206) 784-1070 TOLL FREE: (877) 220-3241 TOLL FREE FAX: (877) 220-3889 E-MAIL: Steven@SLandauServices.com

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

Looking Beyond Our Borders:

Looking Beyond Our Borders: U.S. Income, Estate, and Gift Tax Implications 2017 Advanced Estate Planning Conference MGM Grand Las Vegas June 13, 2017 Peggy A. Ugent, CPA 100 CONGRESS AVENUE, SUITE 1440

Looking Beyond Our Borders: U.S. Income, Estate, and Gift Tax Implications 2017 Advanced Estate Planning Conference MGM Grand Las Vegas June 13, 2017 Peggy A. Ugent, CPA 100 CONGRESS AVENUE, SUITE 1440

US Tax and Reporting Compliances affecting Indian Americans

US Tax and Reporting Compliances affecting Indian Americans May 12 th 2014 Lloyd Pinto Director Grant Thornton India LLP Contents Basic Framework of Taxation for Individuals Taxation of Certain Categories

US Tax and Reporting Compliances affecting Indian Americans May 12 th 2014 Lloyd Pinto Director Grant Thornton India LLP Contents Basic Framework of Taxation for Individuals Taxation of Certain Categories

WHAT MAKES YOU A BONA FIDE RESIDENT OF PUERTO RICO FOR US INCOME TAX PURPOSES, AND ACT 20 AND 22 IMPLICATIONS

WHAT MAKES YOU A BONA FIDE RESIDENT OF PUERTO RICO FOR US INCOME TAX PURPOSES, AND ACT 20 AND 22 IMPLICATIONS By: Ricardo Muñiz W hether you are planning to move to Puerto Rico ( PR ) to enjoy the benefits

WHAT MAKES YOU A BONA FIDE RESIDENT OF PUERTO RICO FOR US INCOME TAX PURPOSES, AND ACT 20 AND 22 IMPLICATIONS By: Ricardo Muñiz W hether you are planning to move to Puerto Rico ( PR ) to enjoy the benefits

Expat Client Questionnaire

Expat Client Questionnaire The tax professionals at Williams and Parsons, PC are dedicated to serving the American expatriate community. Filling out this organizer will help with gathering the information

Expat Client Questionnaire The tax professionals at Williams and Parsons, PC are dedicated to serving the American expatriate community. Filling out this organizer will help with gathering the information

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS. Document created and modified by Financial Services Revised February 8, 2018

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS Document created and modified by Financial Services Revised February 8, 2018 Table of Contents Pages Introduction 1 Definition of Terms 2-5 Frequently

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS Document created and modified by Financial Services Revised February 8, 2018 Table of Contents Pages Introduction 1 Definition of Terms 2-5 Frequently

Form1040-ES/V (OCR) Department of the Treasury Internal Revenue Service

Department of the Treasury Internal Revenue Service") Form1040-ES/V (OCR) Department Treasury Internal Revenue Service Purpose of This Package Use this package to figure and pay your estimated tax. If you are not required to make estimated tax payments for

Form1040-ES/V (OCR) Department Treasury Internal Revenue Service Purpose of This Package Use this package to figure and pay your estimated tax. If you are not required to make estimated tax payments for

Tax Information for US Citizen Employees of the World Bank

Tax Information for US Citizen Employees of the World Bank Rick Ward LLC February 12, 2018 Disclosure This presentation has been prepared for employees of the World Bank by LLC. The information in this

Tax Information for US Citizen Employees of the World Bank Rick Ward LLC February 12, 2018 Disclosure This presentation has been prepared for employees of the World Bank by LLC. The information in this

Form Specified Individual. The Instructions to Form 8938 define a Specified Individual as: A U.S. Citizen.

Form 8938 On March 18, 2010, the Foreign Account Tax Compliance Act ( FATCA ) was enacted as part of the Hiring Incentives to Restore Employment ( HIRE ) Act. Section 511 of FATCA creates new Internal

Form 8938 On March 18, 2010, the Foreign Account Tax Compliance Act ( FATCA ) was enacted as part of the Hiring Incentives to Restore Employment ( HIRE ) Act. Section 511 of FATCA creates new Internal

Instructions for Form 1042-S

2014 Instructions for Form 1042-S Foreign Person's U.S. Source Income Subject to Withholding Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

2014 Instructions for Form 1042-S Foreign Person's U.S. Source Income Subject to Withholding Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

Tax Seminar for Americans Living Abroad

Tax Seminar for Americans Living Abroad Hosted by the U.S. Embassy Athens & American-Hellenic Chamber of Commerce Wednesday, 12 February 2014 The American School of Classical Studies Athens, Greece 2014

Tax Seminar for Americans Living Abroad Hosted by the U.S. Embassy Athens & American-Hellenic Chamber of Commerce Wednesday, 12 February 2014 The American School of Classical Studies Athens, Greece 2014

DUAL-STATUS RETURN U.S. Nonresident Alien Income Tax Return LEE F DUT X. MN Foreign province/county

DUAL-STATUS RETURN U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1-December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning,

DUAL-STATUS RETURN U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1-December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning,

Red Light: Dealing with the IRS Enforcement Action

SESSION 4.3 Red Light: Dealing with the IRS Enforcement Action Michael Guerra, EASi Lori Nichols, Internal Revenue Service Carol Rutlen, Partner, GTN/Rutlen Associates LLC B SESSION 4.3 Red Light: Dealing

SESSION 4.3 Red Light: Dealing with the IRS Enforcement Action Michael Guerra, EASi Lori Nichols, Internal Revenue Service Carol Rutlen, Partner, GTN/Rutlen Associates LLC B SESSION 4.3 Red Light: Dealing

Top 10 Tax Issues facing U.S. Citizens living in Canada

Top 10 Tax Issues facing U.S. Citizens living in Canada An individual may be considered a U.S. citizen if he or she: was born in the U.S.; successfully applied to become a naturalized citizen of the U.S.;

Top 10 Tax Issues facing U.S. Citizens living in Canada An individual may be considered a U.S. citizen if he or she: was born in the U.S.; successfully applied to become a naturalized citizen of the U.S.;

TAX GUIDE FOR FOREIGN VISITORS. Anne E. Davenport, CPA October 2012

TAX GUIDE FOR FOREIGN VISITORS FOR USE BY: All Employees and Students Anne E. Davenport, CPA October 2012 Updated June 24, 2016 Table of Contents Introduction...1 Section 1: Definition of Terms...2 1.1

TAX GUIDE FOR FOREIGN VISITORS FOR USE BY: All Employees and Students Anne E. Davenport, CPA October 2012 Updated June 24, 2016 Table of Contents Introduction...1 Section 1: Definition of Terms...2 1.1

Expats/Inpats: Working Across Borders

Expats/Inpats: Working Across Borders Annick Nguessan 23 October 2015 International Tax Series Agenda & Objectives Introduction Types of assignments Impact of Expatriates/Inpatriates on employer U.S. taxation

Expats/Inpats: Working Across Borders Annick Nguessan 23 October 2015 International Tax Series Agenda & Objectives Introduction Types of assignments Impact of Expatriates/Inpatriates on employer U.S. taxation

2016 FOREIGN NATIONAL QUESTIONNAIRE

PLEASE COMPLETE EACH ITEM INCLUDED IN THE FOREIGN NATIONAL QUESTIONNAIRE FOR EACH MEMBER OF YOUR HOUSEHOLD. TAXPAYER SPOUSE NAME: NAME: 100) PERSONAL INFORMATION 101) Country (countries) of citizenship:

PLEASE COMPLETE EACH ITEM INCLUDED IN THE FOREIGN NATIONAL QUESTIONNAIRE FOR EACH MEMBER OF YOUR HOUSEHOLD. TAXPAYER SPOUSE NAME: NAME: 100) PERSONAL INFORMATION 101) Country (countries) of citizenship:

Certification: Certified by (taxpayer) 2017 Foreign national organizer Form 1040NR and dual status and resident returns 1

2017 Foreign national organizer Form 1040NR and dual status and resident returns 1") This organizer is designed to assist you in gathering the information required for preparation of your nonresident alien/dual status tax returns and is intended to supplement your individual income tax

This organizer is designed to assist you in gathering the information required for preparation of your nonresident alien/dual status tax returns and is intended to supplement your individual income tax

Economic Stimulus Payment Guide for Benefit Recipients

Economic Stimulus Payment Guide for Benefit Recipients Even if you are not otherwise required to file a tax return, you may still be eligible for an economic stimulus payment from the federal government.?

Economic Stimulus Payment Guide for Benefit Recipients Even if you are not otherwise required to file a tax return, you may still be eligible for an economic stimulus payment from the federal government.?

Information Reporting and Civil Penalties (in a Nutshell)

") I. In General Information Reporting and Civil Penalties (in a Nutshell) By Lucy S. Lee, Esq. Caplin & Drysdale, Chartered Washington, D.C. 2008 Lucy S. Lee The Internal Revenue Code (the Code ) 1 generally

I. In General Information Reporting and Civil Penalties (in a Nutshell) By Lucy S. Lee, Esq. Caplin & Drysdale, Chartered Washington, D.C. 2008 Lucy S. Lee The Internal Revenue Code (the Code ) 1 generally

Earned Income Table. Earned Income for EIC, Additional Child Tax Credit and Dependent Care Credit. Common EIC Filing Errors

Earned Income Table Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from selfemployment Gross

Earned Income Table Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from selfemployment Gross

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA

`` TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

`` TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien for

Information for Foreign National Students, Scholars and Staff I. Introduction For federal tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien for

U.S. / ISRAELI INCOME TAX UPDATE FOR YEAR 2016 (2015 Tax Year)

") 02-999-2104, 03-527-3254, 09-746-0623 Cellular: 052-274-9999 Fax: 02-991-0195 Email: alan@ardcpa.com Website: www.ardcpa.com U.S. / ISRAELI INCOME TAX UPDATE FOR YEAR 2016 (2015 Tax Year) The 2015 U.S.

02-999-2104, 03-527-3254, 09-746-0623 Cellular: 052-274-9999 Fax: 02-991-0195 Email: alan@ardcpa.com Website: www.ardcpa.com U.S. / ISRAELI INCOME TAX UPDATE FOR YEAR 2016 (2015 Tax Year) The 2015 U.S.

TAXABLE AND NONTAXABLE COMPENSATON. CHAPTER 3, Part I (2016)

") TAXABLE AND NONTAXABLE COMPENSATON CHAPTER 3, Part I (2016) 1 GROSS INCOME The IRC uses the term gross income to determine a taxpayer s federal tax bill and defines it as compensation for services, including

TAXABLE AND NONTAXABLE COMPENSATON CHAPTER 3, Part I (2016) 1 GROSS INCOME The IRC uses the term gross income to determine a taxpayer s federal tax bill and defines it as compensation for services, including

Non-Resident Alien Frequently Asked Questions

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

NONRESIDENT ALIEN TAX COMPLIANCE. A Policy and Procedure Manual. University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann

Nonresident Alien Tax Specialist Kellie Grahmann") NONRESIDENT ALIEN TAX COMPLIANCE A Policy and Procedure Manual University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann CONTENTS Nonresident Alien Tax Compliance Summary Taxation

NONRESIDENT ALIEN TAX COMPLIANCE A Policy and Procedure Manual University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann CONTENTS Nonresident Alien Tax Compliance Summary Taxation

Nonrefundable Credits

Nonrefundable Credits TaxSlayer Navigation: Federal Section>Deductions>Credits Menu Select for Form 1116, Foreign Tax Credit Select for Form 2441 Child Tax Credit. See Child Tax Credit Tip & Interview

Nonrefundable Credits TaxSlayer Navigation: Federal Section>Deductions>Credits Menu Select for Form 1116, Foreign Tax Credit Select for Form 2441 Child Tax Credit. See Child Tax Credit Tip & Interview

Instructions for Form 1116

Department of the Treasury Internal Revenue Service Instructions for Form 1116 Foreign Tax Credit (Individual, Estate, Trust, or Nonresident Alien Individual) Section references are to the Internal Revenue

Department of the Treasury Internal Revenue Service Instructions for Form 1116 Foreign Tax Credit (Individual, Estate, Trust, or Nonresident Alien Individual) Section references are to the Internal Revenue

Did You Say You Have a U.S. Passport?

Did You Say You Have a U.S. Passport? STEP Bahamas 7 June 2012 Jack Brister, Principal International Tax Services jbrister@mbafcpa.com Introduction So you have a U.S. Passport. Welcome to the club! Your

Did You Say You Have a U.S. Passport? STEP Bahamas 7 June 2012 Jack Brister, Principal International Tax Services jbrister@mbafcpa.com Introduction So you have a U.S. Passport. Welcome to the club! Your

DIVISION OF REVENUE AND TAXATION COMMONWEALTH OF THE NORTHERN MARIANA ISLANDS CNMI Nonresident Alien Income Tax Return

Form 040NR-CM DIVISION OF REVENUE AND TAXATION COMMONWEALTH OF THE NORTHERN MARIANA ISLANDS CNMI Nonresident Alien Income Tax Return For the year January December 3, 03, or other tax year beginning, 03,

Form 040NR-CM DIVISION OF REVENUE AND TAXATION COMMONWEALTH OF THE NORTHERN MARIANA ISLANDS CNMI Nonresident Alien Income Tax Return For the year January December 3, 03, or other tax year beginning, 03,

9/20/2017. USA the dream destination. EB5 visa allows dream to be a reality. Tax regulations in USA affecting NRIs Resident Indians

Tax regulations in USA affecting NRIs Resident Indians By SANKET SHAH CO-FOUNDER AND MANAGING DIRECTOR USA the dream destination USA has always been and will be a dream destination Getting a job Sending

Tax regulations in USA affecting NRIs Resident Indians By SANKET SHAH CO-FOUNDER AND MANAGING DIRECTOR USA the dream destination USA has always been and will be a dream destination Getting a job Sending

PUERTO RICO BUSINESS LAW NOTES

Are You a Bona Fide Resident of Puerto Rico for US Income Tax Purposes? IRS Issues Final Regulations This Article updates and supersedes our November 9, 2004 (No. 2004-12) and May 26, 2005 (No. 2005-01)

Are You a Bona Fide Resident of Puerto Rico for US Income Tax Purposes? IRS Issues Final Regulations This Article updates and supersedes our November 9, 2004 (No. 2004-12) and May 26, 2005 (No. 2005-01)

TAX FILING FOR STUDENTS AND SCHOLARS 101. Columbus Community Legal Services

TAX FILING FOR STUDENTS AND SCHOLARS 101 Columbus Community Legal Services INTRODUCTION Who are we? Part of the Catholic University of America s Columbus School of Law Columbus Community Legal Services

TAX FILING FOR STUDENTS AND SCHOLARS 101 Columbus Community Legal Services INTRODUCTION Who are we? Part of the Catholic University of America s Columbus School of Law Columbus Community Legal Services

Addendum: An addition to an existing document, such as additional terms or a modification of terms.

Research Corporation of the University of Hawai i 2.002 Definitions Accountable Plan: A business reimbursement expense plan for the payment of business expenses incurred by a service provider (such as

Research Corporation of the University of Hawai i 2.002 Definitions Accountable Plan: A business reimbursement expense plan for the payment of business expenses incurred by a service provider (such as

(US Thailand Double Taxation Treaty) The Government of the Kingdom of Thailand and the Government of the United States of America,

The Government of the Kingdom of Thailand and the Government of the United States of America,") CONVENTION BETWEEN THE GOVERNMENT OF THE KINGDOM OF THAILAND AND THE GOVERNMENT OF THE UNITED STATES OF AMERICA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO

CONVENTION BETWEEN THE GOVERNMENT OF THE KINGDOM OF THAILAND AND THE GOVERNMENT OF THE UNITED STATES OF AMERICA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO

Internal Revenue Service. Enrolled Agent Exam Part ONE. Exam Year May 1, 2017 February 28, Table of Contents

Internal Revenue Service Enrolled Agent Exam Part ONE Exam Year May 1, 2017 February 28, 2018 Table of Contents Lesson 1. Taxpayer Identification and Data Gathering Expansion of the Tax Code Internal Taxes

Internal Revenue Service Enrolled Agent Exam Part ONE Exam Year May 1, 2017 February 28, 2018 Table of Contents Lesson 1. Taxpayer Identification and Data Gathering Expansion of the Tax Code Internal Taxes

OFFICIAL POLICY. Policy Statement

OFFICIAL POLICY 9.1.7 Resident Alien vs Nonresident Alien Status 2/8/16 Policy Statement. This handout is intended as a general guide on residence status for tax purposes. Please note that there are significant

OFFICIAL POLICY 9.1.7 Resident Alien vs Nonresident Alien Status 2/8/16 Policy Statement. This handout is intended as a general guide on residence status for tax purposes. Please note that there are significant

Nonresident Alien State of Hawaii Tax Workshop

Nonresident Alien State of Hawaii Tax Workshop University of Hawaii J-1 State of Hawaii Tax Workshop March 23, 2017 Major Differences: Federal & Hawaii Federal Tax treaties Green card test Substantial

Nonresident Alien State of Hawaii Tax Workshop University of Hawaii J-1 State of Hawaii Tax Workshop March 23, 2017 Major Differences: Federal & Hawaii Federal Tax treaties Green card test Substantial

Estate & Gift Tax Treatment for Non-Citizens

ADVANCED MARKETS Estate & Gift Tax Treatment for Non-Citizens BECAUSE YOU ASKED It goes without saying that the laws governing the U.S. estate and gift tax system are complex. When you then consider the

ADVANCED MARKETS Estate & Gift Tax Treatment for Non-Citizens BECAUSE YOU ASKED It goes without saying that the laws governing the U.S. estate and gift tax system are complex. When you then consider the

NEW VENDOR REQUEST NEW VENDOR INFORMATION INTERNATIONAL VENDOR REQUEST INDIVIDUAL

INTERNATIONAL VENDOR REQUEST INDIVIDUAL NEW VENDOR REQUEST This form, in conjunction with the attached taxpayer identification document, must be completed to add a new vendor to our accounting software

INTERNATIONAL VENDOR REQUEST INDIVIDUAL NEW VENDOR REQUEST This form, in conjunction with the attached taxpayer identification document, must be completed to add a new vendor to our accounting software

Supplier Information Form Instructions

Purpose of Form. An organization that is required to file an information return with the IRS must obtain your correct Federal Taxpayer Identification Number in order to report income paid to you. The Tax

Purpose of Form. An organization that is required to file an information return with the IRS must obtain your correct Federal Taxpayer Identification Number in order to report income paid to you. The Tax

TECHNICAL EXPLANATION OF THE UNITED STATES-JAPAN INCOME TAX CONVENTION GENERAL EFFECTIVE DATE UNDER ARTICLE 28: 1 JANUARY 1973 TABLE OF ARTICLES

TECHNICAL EXPLANATION OF THE UNITED STATES-JAPAN INCOME TAX CONVENTION GENERAL EFFECTIVE DATE UNDER ARTICLE 28: 1 JANUARY 1973 It is the practice of the Treasury Department to prepare for the use of the

TECHNICAL EXPLANATION OF THE UNITED STATES-JAPAN INCOME TAX CONVENTION GENERAL EFFECTIVE DATE UNDER ARTICLE 28: 1 JANUARY 1973 It is the practice of the Treasury Department to prepare for the use of the

Economic Stimulus Payment Guide for Benefit Recipients

Economic Stimulus Payment Guide for Benefit Recipients Even if you are not otherwise required to file a tax return, you may still be eligible for an economic stimulus payment from the federal government.?

Economic Stimulus Payment Guide for Benefit Recipients Even if you are not otherwise required to file a tax return, you may still be eligible for an economic stimulus payment from the federal government.?

IRS Federal Income Tax Publications provided by efile.com

IRS Federal Income Tax Publications provided by efile.com This publication should serve as a relevant source for up to date tax answers to your tax questions. Unlike most tax forms, many tax publications

IRS Federal Income Tax Publications provided by efile.com This publication should serve as a relevant source for up to date tax answers to your tax questions. Unlike most tax forms, many tax publications

U.S. Nonresident Alien Income Tax Return

Form 1040NR U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1 December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning, 2011, and

Form 1040NR U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1 December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning, 2011, and

Nonresident Aliens. Resident Alien. Are you a resident alien? Filing Your 2017 Minnesota Income Tax and Property Tax Refund Returns

Nonresident Aliens Filing Your 2017 Minnesota Income Tax and Property Tax Refund Returns Resident Alien Are you a resident alien? A resident alien is generally taxed in the same way as U.S. citizens You

Nonresident Aliens Filing Your 2017 Minnesota Income Tax and Property Tax Refund Returns Resident Alien Are you a resident alien? A resident alien is generally taxed in the same way as U.S. citizens You

FBAR Citizenship Lead Sheet

Tax Period Per Return Per Exam Adjustment Reference 12/31/2006 U.S. Person U.S. Person 401-1.1, 401-3.2 12/31/2007 U.S. Person U.S. Person 401-1.1, 401-3.2 12/31/2008 U.S. Person U.S. Person 401-1.1, 401-3.2

Tax Period Per Return Per Exam Adjustment Reference 12/31/2006 U.S. Person U.S. Person 401-1.1, 401-3.2 12/31/2007 U.S. Person U.S. Person 401-1.1, 401-3.2 12/31/2008 U.S. Person U.S. Person 401-1.1, 401-3.2

Tax & Estate Planning for Snowbirds

Tax & Estate Planning for Snowbirds Amin Mawani Schulich School of Business York University amawani@schulich.yorku.ca Taxes do influence behaviour Windowless Castles Narrow frontages SIN & gasoline taxes

Tax & Estate Planning for Snowbirds Amin Mawani Schulich School of Business York University amawani@schulich.yorku.ca Taxes do influence behaviour Windowless Castles Narrow frontages SIN & gasoline taxes

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A VANILLA APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A VANILLA APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION October 15, 2017 Congress and the Administration are expected to consider changes in US tax

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A VANILLA APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION October 15, 2017 Congress and the Administration are expected to consider changes in US tax

Earned Income Table. Earned Income

Earned Income Table Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from self-employment Gross

Earned Income Table Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from self-employment Gross

Tax Workshop for MIT Students and Scholars. Residents for Tax Purposes. Download Slides here: https://goo.gl/q1tigg

Tax Workshop for MIT Students and Scholars Residents for Tax Purposes Download Slides here: https://goo.gl/q1tigg Monday, February 26, 2018 1 Presenters Present Information: Chris Durham HR/Payroll Manager,

Tax Workshop for MIT Students and Scholars Residents for Tax Purposes Download Slides here: https://goo.gl/q1tigg Monday, February 26, 2018 1 Presenters Present Information: Chris Durham HR/Payroll Manager,

Panex 1040 Individual - Spouse Home address (number and street). If you have a P.O. box, see instructions.

. If you have a P.O. box, see instructions.") Form 4 Department of the Treasury ' Internal Revenue Service (99) U.S. Individual Income Tax Return For the year Jan. - Dec.,, or other tax year beginning,, ending Your first name and initial OMB No. 545-74

Form 4 Department of the Treasury ' Internal Revenue Service (99) U.S. Individual Income Tax Return For the year Jan. - Dec.,, or other tax year beginning,, ending Your first name and initial OMB No. 545-74

CHAPTER 2 GROSS INCOME AND EXCLUSIONS

Solutions for Questions and Problems Chapter 2 39 CHAPTER 2 GROSS INCOME AND ECLUSIONS Group 1 - Multiple Choice Questions 1. C (Section 2.1) 8. C (Section 2.6) 2. C (Section 2.1) 9. B (Section 2.7) 3.

Solutions for Questions and Problems Chapter 2 39 CHAPTER 2 GROSS INCOME AND ECLUSIONS Group 1 - Multiple Choice Questions 1. C (Section 2.1) 8. C (Section 2.6) 2. C (Section 2.1) 9. B (Section 2.7) 3.

2016 Publication 4011

016 Publication 4011 Foreign Student and Scholar Volunteer Resource Guide For Use in Preparing Tax Year 016 Returns»» Volunteer Income Tax Assistance (VITA)»» Tax Counseling for the Elderly (TCE) For the

016 Publication 4011 Foreign Student and Scholar Volunteer Resource Guide For Use in Preparing Tax Year 016 Returns»» Volunteer Income Tax Assistance (VITA)»» Tax Counseling for the Elderly (TCE) For the

5 Qualifying widow(er) with dependent child 6a Yourself. If someone can claim you as a dependent, do not check box 6a...

with dependent child 6a Yourself. If someone can claim you as a dependent, do not check box 6a...") Form 040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 204 OMB No. 545-0074 IRS Use Only Do not write or staple in this space. 0/0 0/0 4 For the year Jan. Dec.

Form 040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 204 OMB No. 545-0074 IRS Use Only Do not write or staple in this space. 0/0 0/0 4 For the year Jan. Dec.

Tax Professionals. 2. Do your clients want to know the status of their refund? Go to and click on Where s My Refund?

www.irs.gov/efile Questions and Answers for Tax Professionals 1. What s new for the IRS e-file Program? 1 IRS e-file has implemented State Only e-file returns with Foreign Addresses including the U.S.

www.irs.gov/efile Questions and Answers for Tax Professionals 1. What s new for the IRS e-file Program? 1 IRS e-file has implemented State Only e-file returns with Foreign Addresses including the U.S.