Form 1040NR Filing Challenges and Effective Approaches

|

|

|

- Linette Hopkins

- 5 years ago

- Views:

Transcription

1 Form 1040NR Filing Challenges and Effective Approaches Determining Taxpayer Classifications and Elections, Computing Income and Deductions, and Understanding Spouse/Dependent Treatment TUESDAY, SEPTEMBER 17, 2013, 1:00-3:00 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit you must: Respond to verification codes presented throughout the seminar. If you have not printed out the Official Record of Attendance, please print it now. (see Handouts tab in Conference Materials box on left-hand side of your computer screen). To earn Continuing Education credits, you must write down the verification codes in the corresponding spaces found on the Official Record of Attendance form. Complete and submit the Official Record of Attendance for Continuing Education Credits, which is available on the program page along with the presentation materials. Instructions on how to return it are included on the form. To earn full credit, you must remain on the line for the entire program. For this program, attendees must listen to the audio over the telephone. WHOM TO CONTACT For Additional Registrations: -Call Strafford Customer Service x10 (or x10) For Assistance During the Program: - On the web, use the chat box at the bottom left of the screen - On the phone, press *0 ( star zero)

2 Sound Quality Call in on the telephone by dialing and enter your PIN when prompted, and view the presentation slides online. If you have any difficulties during the call, press *0 for assistance. You may also send us a chat or sound@straffordpub.com so we can address the problem. Viewing Quality To maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

3 If you have not printed or downloaded the conference materials for this program, please complete the following steps: Click on the + sign next to Conference Materials in the middle of the left-hand column on your screen. Click on the tab labeled Handouts that appears, and there you will see a PDF of the slides and the Official Record of Attendance for today's program. Double-click on the PDF and a separate page will open. Print the slides by clicking on the printer icon.

4 Form 1040NR Filing Challenges and Effective Approaches Sept. 17, 2013 Carolyn Turnbull

5 Introduction Determine the taxpayer s U.S. resident or nonresident alien status at the end of the tax year What form to file? Form 1040? Form 1040NR? Form 1040NR-EZ? When to file? Where to file? File Form 1040X to amend Form 1040NR or Form 1040NR-EZ 5

6 Introduction (cont.) Potential penalties Civil penalties Failure to file Late payment of tax Accuracy-related penalties Fraud Filing erroneous claim for refund or credit Frivolous tax submission Failure to supply taxpayer identification number 6

7 Introduction (cont.) Potential penalties Criminal penalties Tax evasion Will failure to file a return, supply information, or pay any tax due Fraud and false statements Preparing and filing a fraudulent return Identity theft Penalty for failure to disclose a treaty position by filing Form

8 IRS Publications Publication 15 (Circular E), Employer s Tax Guide Publication 17, Your Federal Income Tax Publication 54, Tax Guide for U.S. Citizens and Resident Aliens Abroad Publication 515, Withholding of Tax on Nonresident Aliens and Foreign Entities Publication 519, U.S. Tax Guide for Aliens Publication 597, Information on the United States-Canada Income Tax Treaty Publication 901, U.S. Tax Treaties 8

9 WHO MUST FILE FORM 1040NR

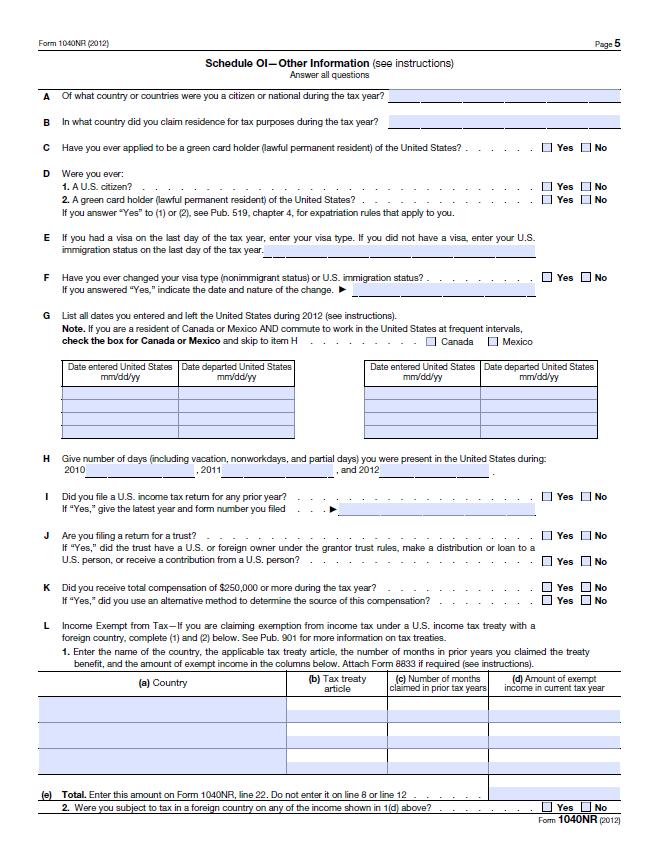

10 Who Must File Form 1040NR? Any of the following apply: Filer is an NRA engaged or considered to be engaged in a U.S. trade or business during the year; Filer is an NRA not engaged in a U.S. trade or business and 1. Received income from U.S. sources reportable on Schedule NEC, and 2. Not all U.S. tax owed was withheld. Filer represents a decedent who would have been required to file Form 1040NR. Filer is a fiduciary for an estate or trust required to file Form 1040NR. 10

11 Who Must File Form 1040NR? (cont.) NRA owes any special taxes (e.g., AMT or recapture of first-time homebuyer credit) NRA receives HSA, Archer MSA, or Medicare Advantage MSA distributions NRA has at least $400 of self-employment earnings and is a resident of a country with whom U.S. has an international social security agreement. NRA wants to claim a refund of overwithheld or overpaid tax NRA wants to claim the benefit of any deductions or credits (e.g., deductions against income from real property that he/she is choosing to treat as ECI) 11

12 Exceptions for Filing Form 1040NR NRA s only U.S. trade or business was performance of personal services, and - Wages are less than the personal exemption ($3,800 for 2012), and - NRA has no need to file a return To claim refund of overwithheld taxes, Satisfy additional withholding at source, or Claim full or partial exemption for income under an income tax treaty. NRA was a student, teacher, or trainee temporarily present in the U.S. under an F, J, M, or Q visa, and NRA has no income subject to tax under 871. NRA is a partner in a U.S. partnership not engaged in a U.S. trade or business during the year and NRA s Schedule K-1 (Form 1065) includes only income from U.S. sources reported on Schedule NEC - NRA must file Form 1040NR if U.S. taxes are over or under withheld.. 12

13 Can the NRA file Form 1040NR-EZ? Individual must meet all of the following conditions: - Not claiming any dependents; - Cannot be claimed as a dependent on another person s U.S. return; - If married, is not claiming an exemption for his/her spouse; - The only U.S. source income is from wages, salaries, tips, taxable refunds of state and local income taxes, and scholarship or fellowship grants; - Taxable income < $100,000; - Only exclusion that may be claimed is the exclusion for scholarship and fellowship grants; - Only adjustment to income that may be claimed is the student loan interest deduction; - Is not claiming any tax credits; 13

14 Can the NRA file Form 1040NR-EZ? Individual must meet all of the following conditions: - If married, is not claiming an exemption for his/her spouse; - Has no itemized deductions other than state and local income taxes; - The return is not an expatriate return ; - Only taxes owed are: The tax from the Tax Table included in the Form 1040NR-EZ instructions, or Unreported social security and Medicare tax from Forms 4137 or 8918; and Is not claiming a credit for excess social security other tier 1 RRTA tax withheld. 14

15 Other Forms NRA May Have to File Form 8833, Treaty-Based Return Position Disclosure Under Section 6114 or 7701(b) Form 8840, Closer Connection Exception Statement for Aliens Form 8843, Statement for Exempt Individuals and Individuals With a Medical Condition Form 8938, Statement of Specified Foreign Financial Assets Form 8854, Initial and Annual Expatriation Statement 15

16 NONRESIDENT ALIEN

17 Definition of Resident Alien and Nonresident Alien (NRA) Alien - person who is not a U.S. citizen NRA - individual who is neither a U.S citizen or U.S. resident Resident alien - Alien is considered an NRA unless he/she meets one of the following two tests for the calendar year: Green card test Substantial presence test 17

18 Green Card Test Satisfies the green card test if a lawful permanent resident of the U.S. at any time during the calendar year Lawful permanent resident of the U.S. at any time if the individual has been given the privilege, according to immigration laws, of residing permanently in the U.S. as an immigrant. Generally treated as a lawful permanent resident of the U.S. if USCIS has issued the individual an alien registration card ( green card ) 18

19 Green Card Test Once an individual satisfies the green card test, the individual will continue to have resident alien status under this test unless the status is taken away or is administratively or judicially determined to have been abandoned. Resident status taken away U.S. government issues a final administrative or judicial order of exclusion or deportation Resident status abandoned Timing depends upon whether the administrative or judicial determination of abandonment of resident status is initiated by the taxpayer or by USCIS or U.S. consular officer A lawful permanent resident who fails to file a tax return when required to do so may be regarded as having abandoned resident status and may lose permanent resident status. 19

20 Substantial Presence Test Alien meets this test if physically present in the U.S. on at least: 31 days during the current year; and 183 days during the 3-year period that includes the current year and the 2 years immediately preceding years, counting 100% of the days present during the current year, 1/3 of days present during 1 st preceding year, and 1/6 of day present during 2 nd preceding year. 20

21 Substantial Presence Test Example Individual A is physically present in the U.S. on 120 days in each of the years 2011, 2012 and To determine if A meets the physical presence test for 2013, count the days as follows: 2013: 120 days x 100% = 120 days 2012: 120 days x 1/3 = 40 days 2011: 120 days x 1/6 = 20 days Total number of days for 2011, 2012, and 2013 = 180 days Conclusion: A is not considered a resident alien under the physical presence test. 21

22 Days of Presence in the United States General Rule - Days of presence includes any day the alien is physically present in the U.S. at any time during the day. Exceptions - Regular commuters from Canada or Mexico - Days in transit between U.S. and foreign destination - Crewe members of a foreign vessel - Days that forced the alien to remain in the U.S. because of a medical condition that developed with the alien was in the U.S. - Days the alien was an exempt individual File Form

23 Days of Presence in the United States General Rule - Days of presence includes any day the alien is physically present in the U.S. at any time during the day. Exceptions - Regular commuters from Canada or Mexico - Days in transit between U.S. and foreign destination - Crewe members of a foreign vessel - Days that forced the alien to remain in the U.S. because of a medical condition that developed with the alien was in the U.S. - Days the alien was an exempt individual File Form

24 Exempt Individuals Foreign government-related individual temporarily present in the U.S. under an A or G visa Teacher or trainee temporarily present in the U.S. under a J or Q visa who substantially complies with the terms of the visa Student temporarily present in the U.S. under an F, J, M, or Q visa who substantially complies with the terms of the visa Professional athlete temporarily present in the U.S. to compete in a charitable sports event 24

25 Closer Connection to a Foreign Country General Rule Alien who meets the substantial presence test can be treated as an NRA if the individual: - Is present in the U.S. < 183 days during the tax year; - Maintains a tax home in a foreign country during the tax year; and - Has a closer connection during the tax year to one foreign country in which the individual has a tax home than to the U.S. Exception: Individual has a closer connection to two (but not more than two) foreign countries. File Form Certain foreign students can use closer connection exception even if present in the U.S. 183 days during the tax year. - Foreign student files Form 8843 to claim closer connection exception. 25

26 26 Slide Intentionally Left Blank

27 Establishing a Closer Connection to a Foreign Country Individual has closer connection to foreign country if individual or Commissioner establishes that the individual has maintained more significant contacts with the foreign country than the U.S. Fact and circumstances to be considered: - Country individual designates as his/her residence on forms and documents - Types of official documents the individual files (e.g., Form W-9, Form W-8BEN, or Form W-8ECI) - Location of individual s permanent home - Location of individual s family - Location of personal belongings - Individual s current social, political, cultural, professional, or religious affiliations - Individual s business activities (other than those that constitute the individual s tax home) - Where the individual holds a driver s license - Where the individual is registered to vote - Charitable organization to which the individual contributes 27

28 Establishing a Closer Connection to a Foreign Country (cont.) Closer connection is unavailable if: - Individual has personally applied or taken steps during the year to change his/her status to U.S. permanent resident; or - Individual has an application pending during the year for adjustment of status. 28

29 DUAL-RESIDENT TAXPAYERS

30 Dual-Resident Taxpayers and Coordination with Income Tax Treaties Dual-resident taxpayer is a person who is a resident of the U.S. and another country under the laws of each country. Dual-resident claiming treaty benefits files Form 1040NR or Form 1040NR-EZ as an NRA. - Income tax treaty must contain tie-breaker rules Taxpayer must file Form 8833 if he/she determines residency under an income tax treaty and receives income or payments > $100,000. Dual-resident may be required to file Form

31 DUAL-STATUS TAXPAYERS

32 Dual-Status Taxpayers Taxpayer is dual-status taxpayer if taxpayer is both an NRA and a resident alien during the same year. - Most common in the year the taxpayer arrives in or departs from the U.S. U.S. tax return filing requirements - Dual-status taxpayer separates income between income while a U.S. resident and income while an NRA. Files Form 1040 with Form 1040NR statement if a resident alien on last day of the tax year. Files Form 1040NR with Form 1040 statement if an NRA on last day of the tax year. - Dual-status taxpayer is subject to U.S. tax on worldwide income while a U.S. resident alien. - Dual-status taxpayer is subject to U.S. tax on U.S.-source or U.S. ECI received during part of the year while an NRA. 32

33 Special Rules for Dual-Status Taxpayers May not claim the standard deduction, even for the part of the year the individual is a U.S. resident. May not claim Head of Household or use Schedule D of the Tax Computation Worksheet. May not file a joint return unless individual elects to be taxed as a resident alien rather than a dual-status taxpayer. Tax rates - Dual-status taxpayer who is married at the end of the year and does not elect to file a joint return must use married filing separate rates. - May be able to use single rates if: Taxpayer lived apart from his/her spouse during the last 6 months of the tax year, and Taxpayer is a married resident of Canada, Mexico, or South Korea, or a married U.S. national. 33

34 Special Rules for Dual-Status Taxpayers (cont.) Exemptions May claim personal exemption for him- or herself. May only claim personal exemptions for spouse and dependents for part of the year taxpayer is a U.S. resident. Special rules apply for part of the year a dual-status taxpayer is a nonresident if taxpayer is: - A resident of Canada, Mexico, or South Korea; - A U.S. national; or - A student or business apprentice from India. 34

35 Special Rules for Dual-Status Taxpayers (cont.) Tax Credits Dual-status taxpayer may not claim the following tax credits: - Earned income tax credit; - Credit for elderly or disabled; or - Education tax credits. 35

36 First Year of Residency for Dual-Status Taxpayers If an individual is a U.S. resident alien during the current calendar year but was not a U.S. resident alien at any time during the preceding calendar year, the individual is a U.S. resident for only the part of the year that begins on the residency starting date. - The individual is a nonresident alien for the part of the year before that date. 36

37 First Year of Residency for Dual-Status Taxpayers Residency Starting Date for Substantial Presence Test General rule: Residency starting date is first day individual is present in the U.S. during the calendar year. Up to 10 days of actual presence in U.S. may be disregarded. - Individuals must have closer connection to and tax home in same foreign country on those days. - Individual who is a U.S. resident because of the substantial presence test and who qualifies to use an early termination date may exclude up to 10 days of physical presence in the U.S. in determining the individual s residency termination. - Days are included in calculating the substantial presence test. - Must file statement with the IRS to apply 10-day exclusion. 37

38 First Year of Residency for Dual-Status Taxpayers Residency Starting Date for Green Card Test If individual meets green card test but not substantial presence test during the calendar year, residency starting date is first day individual is present in the U.S. as lawful permanent resident. If individual meets both green card test and substantial presence test during the calendar year, residency starting date is earlier of first day during the calendar year the individual is present in the U.S. under the substantial presence test or as a lawful permanent resident. 38

39 First Year of Residency for Dual-Status Taxpayers Residency During Preceding Year ( No Lapse Rule) An individual who was a U.S. resident during any part of the preceding calendar year and who is a U.S. resident for any part of the current year will be considered a U.S. resident at the beginning of the current year. - Rule applies regardless of whether an individual is a U.S. resident under the substantial presence test or green card test. 39

40 First-Year Election ( 7701(b)(4) An individual who does not meet the either the green card or the substantial presence test for either the current calendar year (2012) (the election year ) or the immediately preceding calendar year (2011), but who meets the substantial presence test for the following calendar year (2013), may elect to be treated as a resident of the U.S. for part of the current calendar year (2012) if the individual satisfies both of the following conditions: - Individual was present in the U.S. 31 days during the election year; and - Individual was present in the U.S. 75% of number of days beginning with first day of the 31-day period and ending last day of election year. Individual may treat up to 5 days of absence from the U.S. as days of presence in the U.S. for purposes of this 75% requirement Certain days may not be counted for purposes of the 31 days and 75% requirements, above. 40

41 First-Year Election ( 7701(b)(4) Residency Starting Date Residency starting date during the election year is the first day of the earliest 31-day period that the individual uses to qualify under 31-day test, above. If individual is present in the U.S. for more than one 31-day period and the individual satisfies the 75% requirement, above, for each one of those periods, the individual s residency starting period is the first day of the first 31-day period. If an individual is present in the U.S. for more than one 31-day period, but the individual satisfies the 75% requirement for only a later 31-day period, the individual s residency starting date is the first day of the later 31-day period. 41

42 First-Year Election ( 7701(b)(4) Procedures for Making First-Year Election See Appendix 42

43 43 Slide Intentionally Left Blank

44 Last Year of Residency for Dual-Status Taxpayers U.S. resident who is not a U.S. resident during any part of the following year ceases to be a U.S. resident on the residency termination date. No lapse rule - Individual will be treated as a U.S. resident for the entire calendar year if the individual is a resident during any part of the following calendar year. 44

45 Last Year of Residency for Dual-Status Taxpayers Early Residency Termination Date Individual may qualify for earlier residency termination date than December 31 under following circumstances: - May use last day individual was physically present in the U.S. if individual met substantial presence test. - May use first day no longer a lawful permanent resident of U.S. if individual met the green card test. - May use later of two dates, above, if individual met both the substantial presence and green card tests. Individual qualifies to use an early residency termination date if the individual had a tax home in a foreign country and a closer connection to that foreign country for the remainder of the last year of the individual s U.S. residency. 45

46 Last Year of Residency for Dual-Status Taxpayers De Minimis Presence for Early Residency Termination Date Individual who is a U.S. resident because of the substantial presence test and who qualifies to use an early termination date may exclude up to 10 days of physical presence in the U.S. in determining the individual s residency termination date. Individual can exclude days from more than one period, but total number of days in all periods may not exceed 10 days. Individual cannot exclude any days in a period of consecutive days unless the individual can exclude all of the days in the period. Individual must include any days the individual excludes in determining the residency termination date in determining whether the individual meets the substantial presence test. Individual must file a statement with the IRS to establish his/her U.S. residency termination date. 46

47 Election to Treat Nonresident Spouse as U.S. Resident ( 6013(g)) Qualifications for 6013(g) election - Taxpayers are married at the end of the tax year. - One of the spouses is a U.S. citizen or U.S. resident at the end of the tax year. Consequence of 6013(g) election - Both spouses are treated as U.S. residents for entire year of election and all subsequent years unless the election is suspended or terminated. - Both spouses are taxed on worldwide income. - Neither spouse can claim they are not U.S. residents under a tax treaty. - Spouses must file a joint return for the year of the election. - Neither spouse may make a 6013(g) election for any later year, even if they separate, divorce, or remarry. See Appendix for procedures for making a 6013(g) election. - Election can be made on an amended return. 47

48 Election to Treat Nonresident Spouse as U.S. Resident ( 6013(g)) Suspension of 6013(g) Election Election is suspended for taxable year if neither spouse is a U.S. spouse (e.g., both spouses are NRAs) during the year. - Effect is that neither spouse may file a joint return during the suspension. Death of a spouse - If either spouse dies during any taxable year for which an election under 6013(g) is in effect, other than the first taxable year for which the election is to be in effect, the taxable year shall include, solely for purposes of determining whether an election is in effect only those days during the taxable year during which both spouses are alive. If U.S. spouse dies, election is not suspended for that taxable year. If NRA spouse dies, election is not suspended for that taxable year. If neither spouse was a U.S. citizen or resident during the period of the taxable year when both spouses were alive, the election is suspended for that year even if the surviving spouse subsequently acquires U.S. citizenship or residency 48

49 Electing U.S. Resident Alien Status ( 6013(h)) Termination of 6013(g) Election Sec. 6013(g) election terminates upon earliest of the following events: - Either spouse revokes the election; - The death of either spouse; - Spouses legally separate under a decree of divorce or separate maintenance; or - Termination of the election by the IRS. See Appendix for effective date of termination. 49

50 Electing U.S. Resident Alien Status ( 6013(h)) Dual-status taxpayer can elect to be treated as U.S. resident alien for entire taxable year if all of the following are met: - Individual is an NRA at the beginning of the year; - Individual is a resident alien or U.S. citizen at the year of the year; - Individual is married to a U.S. citizen or U.S. resident at the end of the year; and - Spouse joins the taxpayer in making the election. Spouses who were both NRAs at the beginning of the year and U.S. residents at the end of the year may make the election. Individual who is single at the end of the year may not make the election. 50

51 Electing U.S. Resident Alien Status ( 6013(h)) Effect of 6013(h) Election - Taxpayer and spouse are both treated as U.S. residents for the entire tax year. Note: Sec. 6013(h) has no effect on the couple s U.S. status in any year subsequent to the year of the election. - Both spouses are taxed on their worldwide income. - Spouses must file a joint return for the year of the election. - Neither spouse may make the election for any later year, even if they separate, divorce, or remarry. - Special instructions and restrictions for dual-status taxpayers do not apply to the taxpayer. See Appendix for procedures for making a 6013(h) election. - Election can be made on an amended return. 51

52 COMPLETING THE FORM 1040NR

53 Two Types of Federal Taxation Patterns Foreign Taxpayer NRAs pay U.S. tax on U.S. income in two entirely different ways depending upon whether the income the individual earns is from "passive" sources or whether the income results from the foreign taxpayer s conduct of an active trade or business in the U.S. Source of Income Rules - U.S. source income - Foreign source income - Deductions Taxation of Passive (Non-Business) Income: - 30% flat tax rate on gross income - Withholding obligations and contingency Taxation of Active Trade or Business Income - Graduated income tax rates - ECI Treaties 53

54 Unlike a Foreign Taxpayer that is taxed on passive U.S. source income only Income of a Foreign Taxpayer that conducts a trade or business in the U.S. will pay tax on all of its United States source income and in limited circumstances, U.S. tax must be paid on income that is earned from foreign sources and not U.S. sources. Foreign source income that is attributable to a Foreign Taxpayer's U.S. trade or business activity may be taxed by the U.S. and is called "Effectively Connected Income". 54

55 Source of Income Rules U.S. Source Income Foreign Source Income Deductions There is a strict set of rules that governs the determination of whether income finds its source in the United States or a foreign place for U.S. tax purposes. 55

56 Source of Income Compensation for personal services. The source of income from the personal services is located at the place where the services are performed. Rents and Royalties: Rent or royalty income has its source at the location, or place of use, of the leased or licensed property. Real Properly Income and Gain: Income and gain from the rental or sale of real estate has its source at the place where the property is situated. Sale of Personal Property: Historically, gain from the sale of personal property has been sourced at the place of sale which is generally held to be the place where title to the goods passes; however, the rules have become more complex taking other factors in place. 56

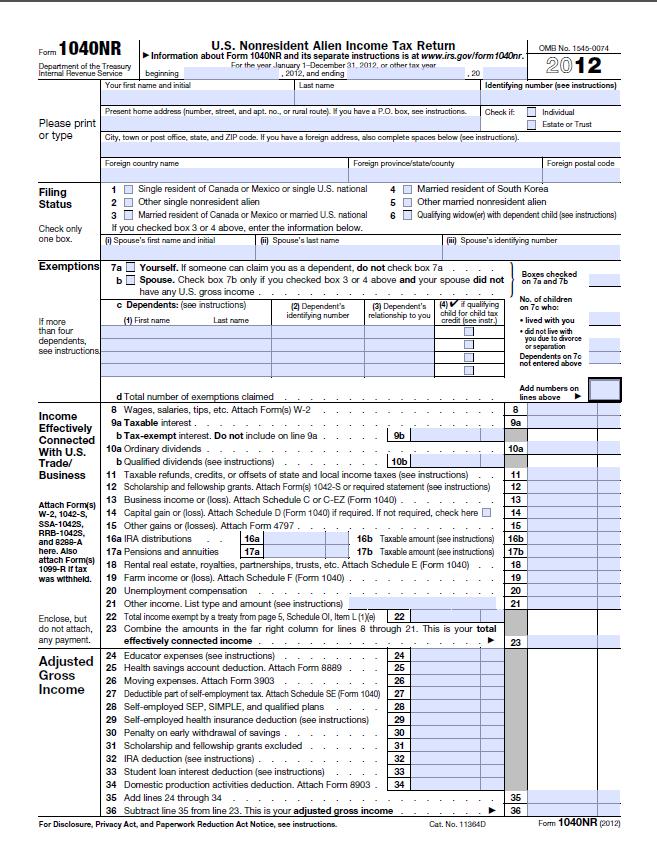

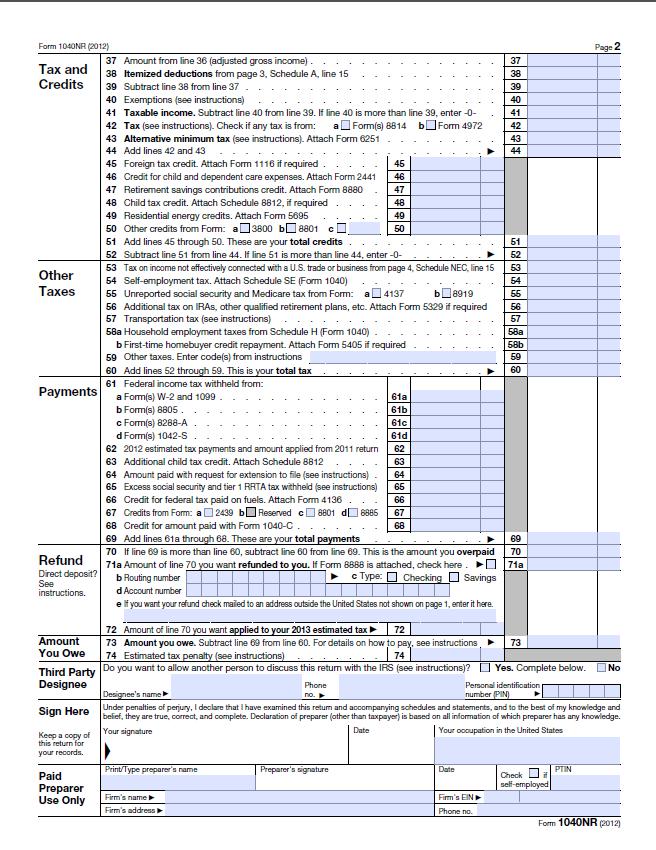

57 Source of Income Interest. The source of interest income is generally determined by reference to the residence of the debtor; interest paid by a resident of the United States constitutes U.S. source income, while interest paid by foreign residents is generally foreignsource income. Dividends. The source of dividend income generally depends on the nationality or place of incorporation of the corporate payer; that is, distributions by U.S. corporations constitute domesticsource income, while dividends of foreign corporations are foreign-source income. There are, however, several important exceptions to these rules. 57

58 The Effect of Bilateral Treaties Extremely Important Benefits Tax treaties between the U.S. and other countries can operate to: 1. reduce (or even eliminate) the rate of U.S. tax on certain types of U.S. income derived by Foreign Taxpayers situated in the treaty-partner country; 2. override various statutory source of income rules 3. exempt certain types of income or activities from taxation, by one or both treaty-partner countries; and 4. extend credit for taxes levied by one country to situations where the domestic law would not so provide. 58

59 59

60 60

61 61

62 62

63 63

64 Overall Structure of Form 1040NR Form 1040NR is designed for NRA to report ECI and FDAP on which insufficient tax was withheld. - ECI is reported on pages 1 and 2. - FDAP taxable under 871(a)(1) and U.S. source capital gains taxable under 871(a)(2), and the tax calculated thereon, are reported on Schedule NEC on page 4. The tax is then carried to line 52 on page 2 Itemized deductions are reported on Schedule A and carried to line 37 on page 2 of Form 1040NR. Tax on ECI, net of itemized deductions, is computed on page 2 of Form 1040NR. Credits against tax, including credits for taxes withheld at source and estimated taxes, are shown on page 2. Any net tax due or tax overpayment is shown at the bottom of page 2. Page 5 asks a number of questions. 64

65 Community Income Community income is treated in accordance with the applicable community property laws with the following exceptions: - For earned income other than income from a trade or business or partnership distributive share income, the income is reported by the spouse whose services earned the income on his/her separate return - For trade or business income other than partnership distributive share income, income is reported by the spouse carrying on the trade or business on that spouse s return. - For partnership distributive share income (loss), income or loss is reported on the return of the spouse who is the partner. - For income derived from the separate property of one spouse that is not earned income, trade or business income, or partnership distributive share income, the income is reported on the return of the spouse with the separate property. 65

66 Tax Year Alien s tax year is the calendar year unless the alien has previously established a fiscal year. Alien s fiscal year must end on the last day of a month. Alien who has established a fiscal year in a foreign country prior to becoming subject to U.S. income tax may adopt the calendar year as his/her taxable year for U.S. tax purposes without requesting a change in accounting period. If an alien who has previously established a fiscal year becomes a U.S. resident during a calendar year, the alien will be considered a U.S. resident during any part of the alien s fiscal year that falls within that calendar year. See Reg (b)-6(b) for examples. 66

67 Identifying Number Alien is required to enter either SSN or ITIN on page 1 of Form 1040NR. Fiduciary enters estate or trust s EIN on page 1 of Form 1040NR. 67

68 Filing Status Married NRAs are generally taxed at the married filing separate tax rates. - Special rules exist for residents of Canada, Mexico. South Korea, or married U.S. nationals. Taxpayer who is married at the end of the year is considered married for the entire tax year. Taxpayer who is single, divorced, or legally separated is considered single for the entire tax year. If the taxpayer s spouse died during the tax year, the taxpayer is considered married to that spouse for the entire tax year unless the spouse remarried before the end of the tax year. 68

69 Filing Status (cont.) Married taxpayer who lives apart from his/her spouse, and who is a resident of Canada, Mexico, or South Korea, or is a U.S. national, may file as single if they meet the following requirements: - Taxpayer files a return separate from his/her spouse; - Taxpayer paid more than half the cost to maintain his/her home during the year; - Taxpayer lived apart from his/her spouse during the last 6 months of the year; - Taxpayer s home was the main home for a child, stepchild, or foster child for more than half of the year; and - Taxpayer can claim a dependency exemption for the child, or the child s other parent claims the dependency exemption under the rules for children of divorced or separated par Canada, Mexico. South Korea, or married U.S. nationals. 69

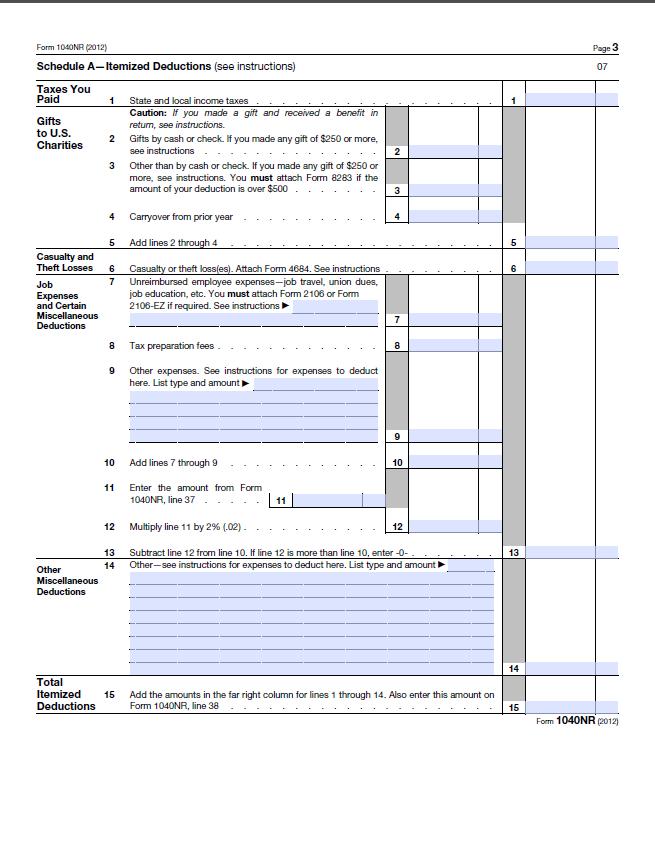

70 Filing Status (cont.) Married residents of Canada or Mexico or married U.S. nationals who meet the five requirements should check box 1 on page 1 of Form 1040NR. Married residents of South Korea who meet the five requirements should check box 2 on page 1 of Form 1040NR. 70

71 Filing Status (cont.) Qualifying widow(er) with qualifying child - Taxpayer may check box 4 on page 1 if he/she meets all of the following requirements: Taxpayer was a resident of Canada, Mexico, South Korea, or a U.S. national; Taxpayer had not remarried by the end of the current tax year and taxpayer s spouse died in one of the two preceding years; Taxpayer has a child or stepchild (not including a foster child) whom taxpayer can claim as a dependent; Child lived in the taxpayer s home for the entire year; Taxpayer paid > one-half cost of maintaining the home; Taxpayer was U.S. citizen or resident in year spouse died; and Taxpayer could have filed a joint return in year spouse died, even if taxpayer did not do so. 71

72 Exemptions NRA may generally claim personal exemption for him- or herself. Residents of India who were students or business apprentices may be able to claim exemptions for their spouse and dependents. Married residents of Canada, Mexico, or South Korea, or married U.S. nationals may claim an exemption for their spouse only if spouse had no gross income and cannot be claimed as a dependent on another U.S. taxpayer s return. Married resident of South Korea may not claim exemption for his/her spouse if spouse did not live with taxpayer in the U.S. at any time during the year. Resident of Canada or Mexico or a U.S. national may claim an exemption for a child or other dependent on the same terms as a U.S. citizen. Resident of South Korea may only claim an exemption for child who lived with taxpayer in the U.S. at some time during the year. 72

73 Income Effectively Connected With a U.S. Trade or Business ( ECI ) ECI, after allowable deductions, is taxed at graduated rates. Types of ECI 73 - Personal services See Appendix for the following exemptions: - Certain compensation for services provided in the U.S. for a foreign employer; - Certain compensation for services performed as a regular crew member of a foreign vessel engaged in transportation between the U.S. and a foreign country or U.S. possession; - Certain compensation received from a foreign employer by nonresident students or exchange visitors present in the U.S. under an F, J, M, or Q visa; - Certain income received under a qualified trust or from a qualified trust exempt from U.S. tax; Taxable scholarship or fellowship grants received by a student or trainee temporarily present in the U.S. under an F, J, M, or Q visa. Distributive share of partnership income attributable to U.S. trade or business Distributions of DNI from an estate or trust engaged in a U.S. trade or business

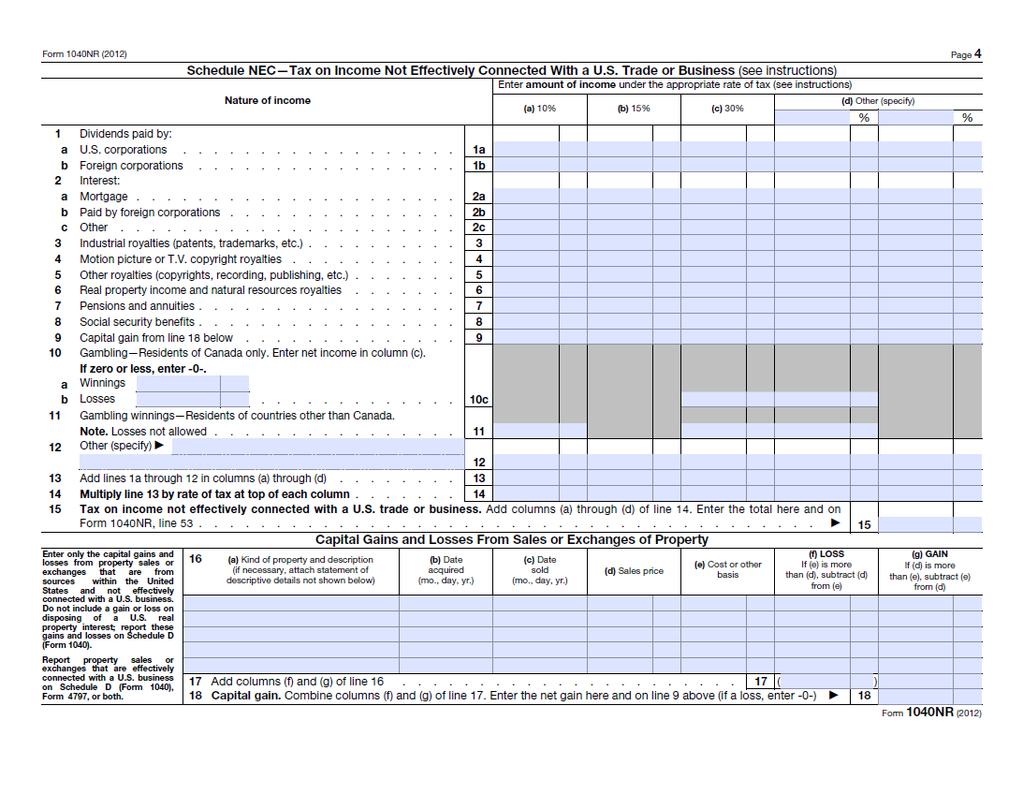

74 Income Effectively Connected With a U.S. Trade or Business ( ECI ) Types of ECI cont A taxpayer who trades in stocks, securities, and commodities may or may not be engaged in a trade or business. - Investment income may or may not be effectively connected with a U.S. trade or business. FDAP Gains (some of which are considered capital gains) from the sale or exchange of: - Timber, coal, or domestic iron ore with a retained economic interest; - Patents, copyrights, and similar property on which taxpayer receives contingent payments after October 4, 1966; - Patents transferred before October 5, 1966; and - OID obligations. Capital gains (and losses)

75 Income Effectively Connected With a U.S. Trade or Business ( ECI ) Tests to determine ECI - Asset-use test - Business activities test Transportation income Special rules exist for interests in U.S. real property 75

76 76 Slide Intentionally Left Blank

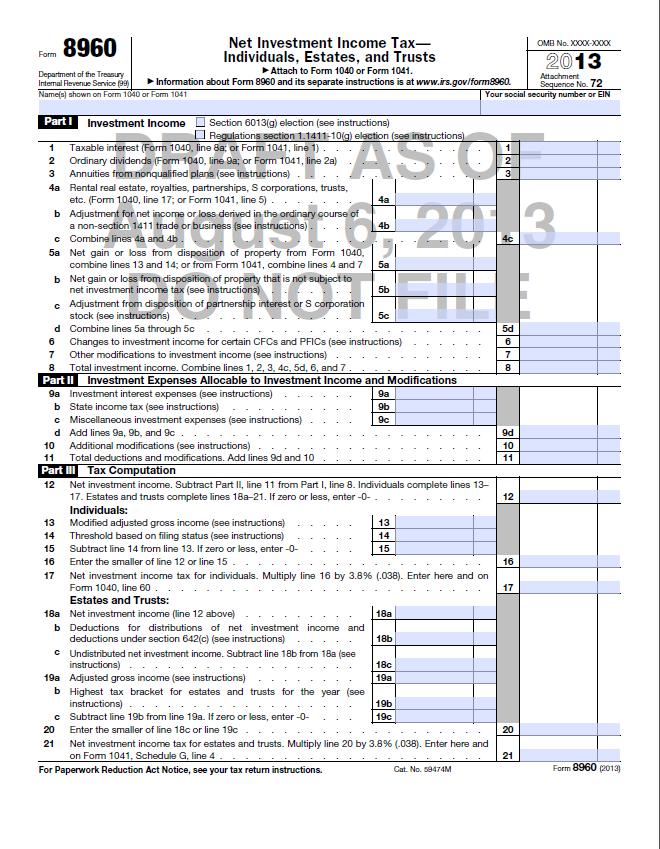

77 Itemized Deductions Schedule A NRAs may generally not claim the standard deduction. - Exception: Students and business apprentices who are eligible for the benefits of Article 21(2) of the U.S.-India Income Tax Treaty can claim the standard deduction if they do not itemize. Most deductions are allowed only to the extent they are allocated and apportioned to ECI, including: 77 - State and local income taxes; - Job expenses and certain other miscellaneous itemized deductions subject to the 2% of AGI limitation; - Other miscellaneous deductions, such as: Casualty and theft losses of income-producing property; Losses from other activities from Schedule K-1 (Form 1065-B), box 2; Deduction for repayment of amounts under claim of right > $,3,000; Certain unrecovered investment in a pension; and Impairment-related work expenses of a disabled person.

78 Itemized Deductions Schedule A Expenses that are allowed even if they do not relate to ECI - Charitable donations - Casualty and theft losses Property must be located in the U.S. at the time of casualty or theft. 78

79 Tax Liability (Before Credits and Payments) Income tax computed on ECI - Regular tax - Additional taxes, if applicable Form 8814, Parent s Election to Report Child s Interest and Dividends Form 4972, Tax on Lump-Sum Distributions - Alternative minimum tax, Form 6251 Other taxes - Tax on income not effectively connected with a U.S. trade or business from Schedule NEC - Unreported social security and Medicare taxes from Form 4137 and Form Additional tax on IRAs, other retirement plans, etc. - Transportation tax - Household employment taxes from Schedule H (Form 1040) 79.

80 Credits are only allowed against ECI. Tax Credits Some of the credits the NRA may be able to claim include: - Foreign tax credit - Credit for child and dependent care expenses - Retirement savings contribution credit - Child tax credit - Mortgage interest credit (Form 8936) - Qualified adoption expenses (Form 8939) - Residential energy credits (Form 5695) - General business credits (Form 3800) - Credit for prior year minimum tax (Form 8801) NRA may not claim: - Earned income tax credit - Credit for the elderly or disabled - Education credits 80

81 Noneffectively Connected Income (NEC) Fixed or determinable annual periodic income ( FDAP ) - Dividends - Interest (other than OID) - Rents - Premiums - Annuities - Salaries - Wages - Other compensation - Royalties - OID from the sale, exchange, or payment on a bond or other debt instrument issued at a discount after March 31, Certain gross proceeds from gambling winnings in the U.S. - Eighty-five percent of U.S. social security and tier 1 railroad retirement benefits, unless exempted by treaty 81

82 Noneffectively Connected Income (NEC) (cont.) Capital gains and losses from the sale of property not effectively connected with a U.S. trade or business - Note: Gains and losses from the sale of a U.S. real property interest are treated as ECI and should be reported on Schedule D, Form 4797, or both. Taxed at flat 30-percent rate, unless reduced by treaty or statute. 82

83 NEW IRC 1411, MEDICARE SURTAX ON NET INVESTMENT INCOME

84 New IRC 1411, Medicare Surtax on Net Investment Income Background Sec. 1411(a) imposes a 3.8% tax on the lesser of an individual s: - Net investment income, or - The excess (if any) of Modified adjusted gross income (MAGI) over A threshold amount. Threshold amount - $250,000 for taxpayers filing a joint return or surviving spouses - $125,000 for married taxpayers filing separately - $200,000 for other taxpayers 84

85 New IRC 1411, Medicare Surtax on Net Investment Income Background cont. For estates and trusts, 1411(a)(2) imposes a 3.8% tax on the lesser of: - Undistributed net investment income, or - The excess (if any) of Adjusted gross income, over The dollar amount at which the highest tax bracket in which 1(e) begins for the year. 85

86 New IRC 1411, Medicare Surtax on Net Investment Income Background cont. Sec. 1411(c) defines net investment income as the excess (if any) of: - The sum of Gross income from interest, dividends, annuities, royalties, and rents, other than such income which is derived in the ordinary course of a trade or business described in 1411(c)(2), Other gross income derived from a trade or business described in 1411(c)(2), and Net gain (to the extent taken into account in computing taxable income) attributable to the disposition of property other than property held in a trade or business not described in 1411(c)(2), over - The deductions allowed by Subtitle A of the Internal Revenue Code that are properly allocable to such gross income or net gain. A trade or business is described in 1411(c)(2) if the trade or business is: - A passive activity with respect to the taxpayer, or - A trade or business of trading in financial instruments or commodities. Sec. 1411(e) provides that 1411 does not apply to a nonresident alien. 86

87 Proposed 1411 Regulations (REG , December 5, 2012) Prop. Reg (a)(2)(i) provides that in the case of a U.S. citizen or resident who is married (as defined in 7703) to an NRA, the spouses will be treated as married filing separately for purposes of For purposes of calculating the 1411 tax, the citizen or resident spouse will be subject to the $125,000 threshold for married filing separately, and the NRA will be exempt from Each spouse must separately calculate his/her own net investment income. 87

88 Proposed 1411 Regulations (REG , December 5, 2012) Prop. Reg (a)(2)(i)(B) provides that married taxpayers who file a Federal joint income tax return pursuant to a 6013(g) election can also elect to be treated as making a 6013(g) election for purposes of The effect of such election is to include combined income of the two spouses in the 1411(a)(1) calculation and subject the income to the $250,000 threshold for married taxpayers filing a joint return. 88

89 Proposed 1411 Regulations (REG , December 5, 2012) Residents of U.S. Territories An individual who is a citizen, resident, or nonresident alien of the U.S. may qualify as a bona fide resident of a U.S. territory. Application of 1411 to a bona fide resident of a U.S. territory depends on whether the territory has a mirror code system of taxation Bona fide residents of a territory that has a mirror code system have no obligation to file a U.S. income tax return provided they report and pay tax to their respective U.S. territory. - Result is that 1411 does not apply to bona fide residents of the U.S. territories that have a mirror code system. - Three (out of five) territories that have a mirror code of taxation include: Guam Northern Mariana Islands United States Virgin Islands - U.S. territories that do not have a mirror code system are: Puerto Rico American Samoa

90 Proposed 1411 Regulations (REG , December 5, 2012) Residents of U.S. Territories Tax under 1411(a) is applicable to bona fide residents of Puerto Rico and American Samoa if they have U.S. reportable income that gives rise to both net investment income and MAGI exceeds the reporting threshold. Sec. 1411(a) does not apply, however, to bona fide residents of Puerto Rico and American Samoa if they are U.S. nonresident aliens. - Individuals who are bona fide residents of nonmirror code jurisdictions remain subject to Chapter 1 of Subtitle A pursuant to

91 91

Taxation of: U.S. Foreign Nationals

Taxation of: U.S. Foreign Nationals 2017 Edition ZanderSterling.com 1 The information contained in this publication is provided for general informational purposes only and is based on U.S. income tax law

Taxation of: U.S. Foreign Nationals 2017 Edition ZanderSterling.com 1 The information contained in this publication is provided for general informational purposes only and is based on U.S. income tax law

Instructions for Form 1040NR-EZ

2011 Instructions for Form 1040NR-EZ U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Department of the Treasury Internal Revenue Service Section references are to the Internal

2011 Instructions for Form 1040NR-EZ U.S. Income Tax Return for Certain Nonresident Aliens With No Dependents Department of the Treasury Internal Revenue Service Section references are to the Internal

Your Federal Income Tax Responsibilities as an Au Pair

S. Landau Services Steven Landau, E.A.* 2610 NW 56th Street #103 Seattle, WA 98107-4118 PHONE: (206) 784-1070 TOLL FREE: (877) 220-3241 TOLL FREE FAX: (877) 220-3889 E-MAIL: Steven@SLandauServices.com

S. Landau Services Steven Landau, E.A.* 2610 NW 56th Street #103 Seattle, WA 98107-4118 PHONE: (206) 784-1070 TOLL FREE: (877) 220-3241 TOLL FREE FAX: (877) 220-3889 E-MAIL: Steven@SLandauServices.com

U.S. Nonresident Alien Income Tax Return

Form 1040NR Department of the Treasury Internal Revenue Service U.S. Nonresident Alien Income Tax Return Information about Form 1040NR and its separate instructions is at www.irs.gov/form1040nr. For the

Form 1040NR Department of the Treasury Internal Revenue Service U.S. Nonresident Alien Income Tax Return Information about Form 1040NR and its separate instructions is at www.irs.gov/form1040nr. For the

U.S. Nonresident Alien Income Tax Return

Form 1040NR U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1 December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning, 2011, and

Form 1040NR U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1 December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning, 2011, and

U.S. Nonresident Alien Income Tax Return

Form 14NR Department of the Treasury Internal Revenue Service Please print or type U.S. Nonresident Alien Income Tax Return Information about Form 14NR and its separate instructions is at www.irs.gov/form14nr.

Form 14NR Department of the Treasury Internal Revenue Service Please print or type U.S. Nonresident Alien Income Tax Return Information about Form 14NR and its separate instructions is at www.irs.gov/form14nr.

The United States Government defines an alien as any individual who is not

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

U.S. Tax Guide for Aliens

Department of the Treasury Internal Revenue Service Publication 519 Cat. No. 15023T U.S. Tax Guide for Aliens For use in preparing 2000 Returns Contents Introduction... 1 Important Changes... 2 Important

Department of the Treasury Internal Revenue Service Publication 519 Cat. No. 15023T U.S. Tax Guide for Aliens For use in preparing 2000 Returns Contents Introduction... 1 Important Changes... 2 Important

THE TAXATION OF INDIVIDUALS AND FAMILIES

THE TAXATION OF INDIVIDUALS AND FAMILIES Scheduled for a Public Hearing Before the TAX POLICY SUBCOMMITTEE of the HOUSE COMMITTEE ON WAYS AND MEANS on July 19, 2017 Prepared by the Staff of the JOINT COMMITTEE

THE TAXATION OF INDIVIDUALS AND FAMILIES Scheduled for a Public Hearing Before the TAX POLICY SUBCOMMITTEE of the HOUSE COMMITTEE ON WAYS AND MEANS on July 19, 2017 Prepared by the Staff of the JOINT COMMITTEE

U.S. Nonresident Alien Income Tax Return. Of what country were you a citizen or national during the tax year?

1040NR U.S. nresident Alien Income Tax Return OMB. 1545-0089 2002 Form For the year January 1 December 31, 2002, or other tax year Department of the Treasury Internal Revenue Service beginning, 2002, and

1040NR U.S. nresident Alien Income Tax Return OMB. 1545-0089 2002 Form For the year January 1 December 31, 2002, or other tax year Department of the Treasury Internal Revenue Service beginning, 2002, and

Certain Cash Contributions for Typhoon Haiyan Relief Efforts in the Philippines Can Be Deducted on Your 2013 Tax Return

Certain Cash Contributions for Typhoon Haiyan Relief Efforts in the Philippines Can Be Deducted on Your 2013 Tax Return A new law allows you to choose to deduct certain charitable contributions of money

Certain Cash Contributions for Typhoon Haiyan Relief Efforts in the Philippines Can Be Deducted on Your 2013 Tax Return A new law allows you to choose to deduct certain charitable contributions of money

U.S. Tax Guide for Aliens

Department of the Treasury Internal Revenue Service Publication 519 Cat. No. 15023T U.S. Tax Guide for Aliens For use in preparing 2013 Returns Contents Introduction... 1 What's New... 2 Reminders... 3

Department of the Treasury Internal Revenue Service Publication 519 Cat. No. 15023T U.S. Tax Guide for Aliens For use in preparing 2013 Returns Contents Introduction... 1 What's New... 2 Reminders... 3

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014 Federal Income Tax Withholding 14.1-1 U.S. citizens & resident aliens are subject to income tax withholding

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014 Federal Income Tax Withholding 14.1-1 U.S. citizens & resident aliens are subject to income tax withholding

DO NOT FILE THIS FORM IN 2019 WITH YOUR TAX RETURN

THIS FORM IN 2019 WITH YOUR TAX RETURN This IRS Tax Form is ONLY A DRAFT for 2019. This form will most likely be changed before its final version is ready to be used in 2019 with your 2018 Tax Return.

THIS FORM IN 2019 WITH YOUR TAX RETURN This IRS Tax Form is ONLY A DRAFT for 2019. This form will most likely be changed before its final version is ready to be used in 2019 with your 2018 Tax Return.

~E~ E-3 visa, 103 Earnings statement, 100, 131, 135, 136,

Index ~A~ ACA Affordable Care Act 14, 173 A, G visa holders, 5, 6, 7, 37, 103 A-2 visa, PRI 6, 126, 132, 133 A-3 visa, 138, 141 Abuse, abusive employment situation, 141,142 Actual days, Z, 7, 8 Adjusted

Index ~A~ ACA Affordable Care Act 14, 173 A, G visa holders, 5, 6, 7, 37, 103 A-2 visa, PRI 6, 126, 132, 133 A-3 visa, 138, 141 Abuse, abusive employment situation, 141,142 Actual days, Z, 7, 8 Adjusted

DUAL-STATUS RETURN U.S. Nonresident Alien Income Tax Return LEE F DUT X. MN Foreign province/county

DUAL-STATUS RETURN U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1-December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning,

DUAL-STATUS RETURN U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1-December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning,

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A Nonresident Alien Tax Compliance: Challenges and Planning Techniques for Tax Professionals Recent IRS Compliance Campaign, ECI vs. FDAP Income,

Presenting a live 90-minute webinar with interactive Q&A Nonresident Alien Tax Compliance: Challenges and Planning Techniques for Tax Professionals Recent IRS Compliance Campaign, ECI vs. FDAP Income,

DIVISION OF REVENUE AND TAXATION COMMONWEALTH OF THE NORTHERN MARIANA ISLANDS CNMI Nonresident Alien Income Tax Return

Form 040NR-CM DIVISION OF REVENUE AND TAXATION COMMONWEALTH OF THE NORTHERN MARIANA ISLANDS CNMI Nonresident Alien Income Tax Return For the year January December 3, 03, or other tax year beginning, 03,

Form 040NR-CM DIVISION OF REVENUE AND TAXATION COMMONWEALTH OF THE NORTHERN MARIANA ISLANDS CNMI Nonresident Alien Income Tax Return For the year January December 3, 03, or other tax year beginning, 03,

U.S. taxation of foreign citizens

U.S. taxation of foreign citizens Global Mobility Services 2019 kpmg.com U.S. taxation of foreign citizens The following information is not intended to be written advice concerning one or more Federal

U.S. taxation of foreign citizens Global Mobility Services 2019 kpmg.com U.S. taxation of foreign citizens The following information is not intended to be written advice concerning one or more Federal

Americans Living Abroad. 61 Tax Questions you should know.

Americans Living Abroad 61 Tax Questions you should know 1 General FAQs 1. I m a U.S. citizen living and working outside of the United States for many years. Do I still need to file a U.S. tax return?

Americans Living Abroad 61 Tax Questions you should know 1 General FAQs 1. I m a U.S. citizen living and working outside of the United States for many years. Do I still need to file a U.S. tax return?

Foreign Earned Income: Exclusion and Other Tax Issues for Expat Workers

Foreign Earned Income: Exclusion and Other Tax Issues for Expat Workers Navigating Tax Treaties, Social Security Totalization Agreements, and Other Complexities TUESDAY, JULY 16, 2013, 1:00-2:50 pm Eastern

Foreign Earned Income: Exclusion and Other Tax Issues for Expat Workers Navigating Tax Treaties, Social Security Totalization Agreements, and Other Complexities TUESDAY, JULY 16, 2013, 1:00-2:50 pm Eastern

Table of Contents. Preliminary Work and General Filing Requirements... 1

Table of Contents Preliminary Work and General Filing Requirements.... 1 General Requirement to File...3 Signatures....4 Marital Status...6 Married....6 Unmarried....7 Filing Status...7 Single....7 Married

Table of Contents Preliminary Work and General Filing Requirements.... 1 General Requirement to File...3 Signatures....4 Marital Status...6 Married....6 Unmarried....7 Filing Status...7 Single....7 Married

Attendees seeking CPE credit must listen to the audio over the telephone.

Presenting a live 110 minute teleconference with interactive Q&A New 3.8% Net Investment Income Tax: Planning for Closely Held Companies Navigating New Medicare Tax, Self Employment l Tax, and Capital

Presenting a live 110 minute teleconference with interactive Q&A New 3.8% Net Investment Income Tax: Planning for Closely Held Companies Navigating New Medicare Tax, Self Employment l Tax, and Capital

Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding

Form W-8BEN Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding (Rev. February 2006) OMB No. 1545-1621 Department of the Treasury Section references are to the Internal

Form W-8BEN Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding (Rev. February 2006) OMB No. 1545-1621 Department of the Treasury Section references are to the Internal

Non-Resident Alien Frequently Asked Questions

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

Final IRS Sect. 67(e) Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor

Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor") Final IRS Sect. 67(e) Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor WEDNESDAY, OCTOBER 15, 2014, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Final IRS Sect. 67(e) Regs for Estate and Trust Taxpayers: Applying the Required 2% Deduction Floor WEDNESDAY, OCTOBER 15, 2014, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Form1040-ES/V (OCR) Department of the Treasury Internal Revenue Service

Department of the Treasury Internal Revenue Service") Form1040-ES/V (OCR) Department Treasury Internal Revenue Service Purpose of This Package Use this package to figure and pay your estimated tax. If you are not required to make estimated tax payments for

Form1040-ES/V (OCR) Department Treasury Internal Revenue Service Purpose of This Package Use this package to figure and pay your estimated tax. If you are not required to make estimated tax payments for

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features: W. Aaron Hawthorne, Managing Director, Andersen Tax, Dallas

Presenting a live 90-minute webinar with interactive Q&A U.S.-Mexican Tax and Estate Planning for Cross-Border Clients Reconciling U.S. and Mexican Law on Trusts, Ownership of Real Property, Situs and

Presenting a live 90-minute webinar with interactive Q&A U.S.-Mexican Tax and Estate Planning for Cross-Border Clients Reconciling U.S. and Mexican Law on Trusts, Ownership of Real Property, Situs and

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2013

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2013 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION January 8, 2013 JCX-2-13R I. SUMMARY OF PRESENT-LAW FEDERAL TAX SYSTEM A. Individual Income

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2013 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION January 8, 2013 JCX-2-13R I. SUMMARY OF PRESENT-LAW FEDERAL TAX SYSTEM A. Individual Income

Mastering FATCA Compliance and Implementation for NFFEs: Are You Ready for the July 1 Deadline?

Mastering FATCA Compliance and Implementation for NFFEs: Are You Ready for the July 1 Deadline? TUESDAY, JUNE 24, 2014, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit

Mastering FATCA Compliance and Implementation for NFFEs: Are You Ready for the July 1 Deadline? TUESDAY, JUNE 24, 2014, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit

Mastering Form 1040NR U.S. Nonresident Alien Income Tax Returns Identifying ECI and FDAP, Determining Taxpayer Classifications and Elections

FOR LIVE PROGRAM ONLY Mastering Form 1040NR U.S. Nonresident Alien Income Tax Returns Identifying ECI and FDAP, Determining Taxpayer Classifications and Elections WEDNESDAY, SEPTEMBER 20, 2017, 1:00-2:50

FOR LIVE PROGRAM ONLY Mastering Form 1040NR U.S. Nonresident Alien Income Tax Returns Identifying ECI and FDAP, Determining Taxpayer Classifications and Elections WEDNESDAY, SEPTEMBER 20, 2017, 1:00-2:50

THE F-1 VISA PRIVILEGED U.S. TAX STATUS AND HOW TO KEEP IT

THE F-1 VISA PRIVILEGED U.S. TAX STATUS AND HOW TO KEEP IT Authors Neha Rastogi Beate Erwin Tags Exempt Individual F-1 Visa Foreign Students Nonresident Alien Foreign students leaving their home country

THE F-1 VISA PRIVILEGED U.S. TAX STATUS AND HOW TO KEEP IT Authors Neha Rastogi Beate Erwin Tags Exempt Individual F-1 Visa Foreign Students Nonresident Alien Foreign students leaving their home country

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

Form W 8BEN and W 9 Compliance in

Presenting a live 110 minute teleconference with interactive Q&A Form W 8BEN and W 9 Compliance in Foreign and US U.S. Business Transactions Avoiding Traps With Unnecessary Back Up Withholding or Invalid

Presenting a live 110 minute teleconference with interactive Q&A Form W 8BEN and W 9 Compliance in Foreign and US U.S. Business Transactions Avoiding Traps With Unnecessary Back Up Withholding or Invalid

Section 1202 Qualified Small Business Stock: Maximizing Tax Advantages of Gain Exclusion and Deferral

Section 1202 Qualified Small Business Stock: Maximizing Tax Advantages of Gain Exclusion and Deferral THURSDAY, AUGUST 27, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Section 1202 Qualified Small Business Stock: Maximizing Tax Advantages of Gain Exclusion and Deferral THURSDAY, AUGUST 27, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Instructions for Form 1042-S Foreign Person s U.S. Source Income Subject to Withholding

2009 Instructions for Form 1042-S Foreign Person s U.S. Source Income Subject to Withholding Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

2009 Instructions for Form 1042-S Foreign Person s U.S. Source Income Subject to Withholding Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

Form 1120S Challenges for Enrolled Agents: Navigating Latest Regs, Rulings and Guidance

Form 1120S Challenges for Enrolled Agents: Navigating Latest Regs, Rulings and Guidance Anticipating Issues With Computations, Dividends, Distributions, Fringe Benefits, Etc. THURSDAY, JUNE 27, 2013, 1:00-2:50

Form 1120S Challenges for Enrolled Agents: Navigating Latest Regs, Rulings and Guidance Anticipating Issues With Computations, Dividends, Distributions, Fringe Benefits, Etc. THURSDAY, JUNE 27, 2013, 1:00-2:50

AARP FOUNDATION TAX-AIDE SCOPE MANUAL WHAT S IN WHAT S OUT

AARP Foundation Tax-Aide helps low and moderate income taxpayers, with special attention to those 60 and older. Volunteers are trained to assist in filing Form 1040 and certain other schedules and forms.

AARP Foundation Tax-Aide helps low and moderate income taxpayers, with special attention to those 60 and older. Volunteers are trained to assist in filing Form 1040 and certain other schedules and forms.

2016 Publication 4011

016 Publication 4011 Foreign Student and Scholar Volunteer Resource Guide For Use in Preparing Tax Year 016 Returns»» Volunteer Income Tax Assistance (VITA)»» Tax Counseling for the Elderly (TCE) For the

016 Publication 4011 Foreign Student and Scholar Volunteer Resource Guide For Use in Preparing Tax Year 016 Returns»» Volunteer Income Tax Assistance (VITA)»» Tax Counseling for the Elderly (TCE) For the

US Tax Information for Diplomatic Families at the Canadian Embassy

US Tax Information for Diplomatic Families at the Canadian Rick Ward LLC January 16, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of January

US Tax Information for Diplomatic Families at the Canadian Rick Ward LLC January 16, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of January

American Citizens Abroad. Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION

American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation 5 December 2016; 1 November 2017; 1 December 2017; 18 January 2018; 19 April 2018 INTRODUCTION This side-by-side analysis

American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation 5 December 2016; 1 November 2017; 1 December 2017; 18 January 2018; 19 April 2018 INTRODUCTION This side-by-side analysis

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien for

Information for Foreign National Students, Scholars and Staff I. Introduction For federal tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien for

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features: Dean C. Berry, Partner, Cadwalader Wickersham & Taft, New York

Presenting a live 90-minute webinar with interactive Q&A Estate Planning Involving Resident and Non-Resident Aliens Navigating Estate, Gift and GST Tax Rules; Leveraging Estate and Lifetime Gifting Opportunities

Presenting a live 90-minute webinar with interactive Q&A Estate Planning Involving Resident and Non-Resident Aliens Navigating Estate, Gift and GST Tax Rules; Leveraging Estate and Lifetime Gifting Opportunities

MANAGING INTERNATIONAL TAX ISSUES

MANAGING INTERNATIONAL TAX ISSUES Starting A Business Retirement Strategies Operating A Business Marriage Investing Tax Smart Estate Planning Ending A Business Off to School Divorce And Separation Travel

MANAGING INTERNATIONAL TAX ISSUES Starting A Business Retirement Strategies Operating A Business Marriage Investing Tax Smart Estate Planning Ending A Business Off to School Divorce And Separation Travel

, ending. child tax credit (1) First name Last name

First name Last name") Department of the Treasury Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return 2016 OMB No. 1545-0074 For the year Jan. 1-Dec. 31, 2016, or other tax year beginning, ending Form Your first

Department of the Treasury Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return 2016 OMB No. 1545-0074 For the year Jan. 1-Dec. 31, 2016, or other tax year beginning, ending Form Your first

Form 1042-S Compliance: Mastering Filing Challenges and Avoiding Steep Penalties

Form 1042-S Compliance: Mastering Filing Challenges and Avoiding Steep Penalties Navigating Rules on Reporting and Withholding on U.S.-Source Income for Foreign Persons TUESDAY, DECEMBER 17, 2013, 1:00-2:50

Form 1042-S Compliance: Mastering Filing Challenges and Avoiding Steep Penalties Navigating Rules on Reporting and Withholding on U.S.-Source Income for Foreign Persons TUESDAY, DECEMBER 17, 2013, 1:00-2:50

U.S. Income Tax for Foreign Students, Scholars and Teachers. Arthur R. Kerr II Vacovec Mayotte & Singer LLP

U.S. Income Tax for Foreign Students, Scholars and Teachers Arthur R. Kerr II Vacovec Mayotte & Singer LLP 617-964-0500 akerr@vacovec.com Are You Resident or Nonresident? Residence for tax purposes not

U.S. Income Tax for Foreign Students, Scholars and Teachers Arthur R. Kerr II Vacovec Mayotte & Singer LLP 617-964-0500 akerr@vacovec.com Are You Resident or Nonresident? Residence for tax purposes not

Foreign Tax Issues REBECCA DONEHEW

Foreign Tax Issues REBECCA DONEHEW Form 5471 Information Returns of U.S. Persons with Respect to Certain Foreign Corporations Used to satisfy the reported requirements of transactions between foreign corporations

Foreign Tax Issues REBECCA DONEHEW Form 5471 Information Returns of U.S. Persons with Respect to Certain Foreign Corporations Used to satisfy the reported requirements of transactions between foreign corporations

U.S. TAX ISSUES FOR CANADIANS

U.S. TAX ISSUES FOR CANADIANS If you own rental property in the United States or spend extended periods of time there, you could be subject to various U.S. filing requirements, even though you may have

U.S. TAX ISSUES FOR CANADIANS If you own rental property in the United States or spend extended periods of time there, you could be subject to various U.S. filing requirements, even though you may have

Panex 1040 Individual - Spouse Home address (number and street). If you have a P.O. box, see instructions.

. If you have a P.O. box, see instructions.") Form 4 Department of the Treasury ' Internal Revenue Service (99) U.S. Individual Income Tax Return For the year Jan. - Dec.,, or other tax year beginning,, ending Your first name and initial OMB No. 545-74

Form 4 Department of the Treasury ' Internal Revenue Service (99) U.S. Individual Income Tax Return For the year Jan. - Dec.,, or other tax year beginning,, ending Your first name and initial OMB No. 545-74

2017 Instructions for Schedule 8812

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule 8812 Child Tax Credit Part I of Schedule 8812 documents that any qualifying child whom you identify with an ITIN is a

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule 8812 Child Tax Credit Part I of Schedule 8812 documents that any qualifying child whom you identify with an ITIN is a

Foreign Tax Issues. By Merrill Fromer Pages

Foreign Tax Issues By Merrill Fromer Pages 435-475 Foreign Tax Issues pg. 435 Issue 1: Reporting by US Citizens Living Abroad Issue 2: Foreign Earned Income Exclusion Issue 3: Nonresident Alien Reporting

Foreign Tax Issues By Merrill Fromer Pages 435-475 Foreign Tax Issues pg. 435 Issue 1: Reporting by US Citizens Living Abroad Issue 2: Foreign Earned Income Exclusion Issue 3: Nonresident Alien Reporting

Domestic Tax Issues for Non-resident Aliens

Domestic Tax Issues for Non-resident Aliens Presented by Monica Haven, EA, JD, LLM mhaven@pobox.com www.mhaven.net What we ll cover Are Non-resident Aliens from Mars? Where is home for Dual Status Aliens?

Domestic Tax Issues for Non-resident Aliens Presented by Monica Haven, EA, JD, LLM mhaven@pobox.com www.mhaven.net What we ll cover Are Non-resident Aliens from Mars? Where is home for Dual Status Aliens?

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

Foreign Earned Income: Form 2555 Exclusion Reporting and Other Tax Issues for Expat Workers

Foreign Earned Income: Form 2555 Exclusion Reporting and Other Tax Issues for Expat Workers Navigating Tax Treaties, Social Security Totalization Agreements, and Other Complexities THURSDAY, MAY 8, 2014,

Foreign Earned Income: Form 2555 Exclusion Reporting and Other Tax Issues for Expat Workers Navigating Tax Treaties, Social Security Totalization Agreements, and Other Complexities THURSDAY, MAY 8, 2014,

IRS Federal Income Tax Publications provided by efile.com

IRS Federal Income Tax Publications provided by efile.com This publication should serve as a relevant source for up to date tax answers to your tax questions. Unlike most tax forms, many tax publications

IRS Federal Income Tax Publications provided by efile.com This publication should serve as a relevant source for up to date tax answers to your tax questions. Unlike most tax forms, many tax publications

US Tax Information for Diplomatic Families at the Australian Embassy

US Tax Information for Diplomatic Families at the Australian Rick Ward LLC January 25, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of

US Tax Information for Diplomatic Families at the Australian Rick Ward LLC January 25, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of

OUT OF SCOPE - VITA 2017 TAX YEAR The following are out of scope. While this list may not be all inclusive, it is provided for your awareness only.

The following are out of scope. While this list may not be all inclusive, it is provided for your awareness only. Legislative Extenders Residential energy-efficient property credit (Form 5695, Part I)

The following are out of scope. While this list may not be all inclusive, it is provided for your awareness only. Legislative Extenders Residential energy-efficient property credit (Form 5695, Part I)

Aliens & Citizens: Foreign and Domestic Tax Issues

Aliens & Citizens: Foreign and Domestic Tax Issues What we ll cover Are Non-resident Aliens from Mars? Where is home for Dual Status Aliens? How do we tax extraterrestrial income? Do Space Treaties give

Aliens & Citizens: Foreign and Domestic Tax Issues What we ll cover Are Non-resident Aliens from Mars? Where is home for Dual Status Aliens? How do we tax extraterrestrial income? Do Space Treaties give

Bob Smith Betty Smith Home address (number and street). If you have a P.O.box, see instructions. J Important!

. If you have a P.O.box, see instructions. J Important!") Presidential Lakeview WA 99999 Election Campaign Note: Checking Yes will not change your tax or reduce your refund. You Spouse (See instructions.) A Do you, or your spouse if filing a joint return, want

Presidential Lakeview WA 99999 Election Campaign Note: Checking Yes will not change your tax or reduce your refund. You Spouse (See instructions.) A Do you, or your spouse if filing a joint return, want

Overview of the Tax Structure

Overview of the Tax Structure 2007, CCH INCORPORATED 4025 West Peterson Ave. Chicago, IL 60646-6085 http://www.cch.com 1 of 35 3 of 35 Responsibilities of Taxpayers Prepare appropriate tax forms and schedules

Overview of the Tax Structure 2007, CCH INCORPORATED 4025 West Peterson Ave. Chicago, IL 60646-6085 http://www.cch.com 1 of 35 3 of 35 Responsibilities of Taxpayers Prepare appropriate tax forms and schedules

Figuring your Taxes and Credits

Figuring your Taxes and Credits This self-study explains how to figure your tax and how to figure the tax of certain children who have more than $2,100 of unearned income. Also discussed are various tax

Figuring your Taxes and Credits This self-study explains how to figure your tax and how to figure the tax of certain children who have more than $2,100 of unearned income. Also discussed are various tax

TAX GUIDE FOR FOREIGN VISITORS. Anne E. Davenport, CPA October 2012

TAX GUIDE FOR FOREIGN VISITORS FOR USE BY: All Employees and Students Anne E. Davenport, CPA October 2012 Updated June 24, 2016 Table of Contents Introduction...1 Section 1: Definition of Terms...2 1.1

TAX GUIDE FOR FOREIGN VISITORS FOR USE BY: All Employees and Students Anne E. Davenport, CPA October 2012 Updated June 24, 2016 Table of Contents Introduction...1 Section 1: Definition of Terms...2 1.1

US Tax Information for Diplomatic Families at the German Embassy

US Tax Information for Diplomatic Families at the German Rick Ward LLC February 26, 2018 Disclosure This presentation has been prepared for employees of the World Bank by LLC. The information in this presentation

US Tax Information for Diplomatic Families at the German Rick Ward LLC February 26, 2018 Disclosure This presentation has been prepared for employees of the World Bank by LLC. The information in this presentation

See separate instructions. Your social security number RIGHT ANGLE XXX-XX-XXXX If a joint return, spouse's first name and initial

Form Department of the Treasury - Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 216 OMB No. 1545-74 For the year Jan. 1-Dec. 31, 216, or other tax year beginning, 216, ending, 2 Your

Form Department of the Treasury - Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 216 OMB No. 1545-74 For the year Jan. 1-Dec. 31, 216, or other tax year beginning, 216, ending, 2 Your

NC-4 Employee s Withholding Allowance Certificate

Web 10-17 NC-4 Employee s Withholding Allowance Certificate PURPOSE - Complete Form NC-4 so that your employer can withhold the correct amount of State income tax from your pay. If you do not provide an

Web 10-17 NC-4 Employee s Withholding Allowance Certificate PURPOSE - Complete Form NC-4 so that your employer can withhold the correct amount of State income tax from your pay. If you do not provide an

CHAPTER 2 GROSS INCOME AND EXCLUSIONS

Solutions for Questions and Problems Chapter 2 39 CHAPTER 2 GROSS INCOME AND EXCLUSIONS Group 1 - Multiple Choice Questions 1. C (Section 2.1) 8. C (Section 2.6) 2. C (Section 2.1) 9. B (Section 2.7) 3.

Solutions for Questions and Problems Chapter 2 39 CHAPTER 2 GROSS INCOME AND EXCLUSIONS Group 1 - Multiple Choice Questions 1. C (Section 2.1) 8. C (Section 2.6) 2. C (Section 2.1) 9. B (Section 2.7) 3.

US Tax Information for Diplomatic Families at the Swiss Embassy

US Tax Information for Diplomatic Families at the Swiss Rick Ward LLC October 18, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of October

US Tax Information for Diplomatic Families at the Swiss Rick Ward LLC October 18, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of October

Volunteer Income Tax Assistance (VITA) Session 2017 Tax Year Georgia Form 500 with Form 1040NR

Session 2017 Tax Year Georgia Form 500 with Form 1040NR") Volunteer Income Tax Assistance (VITA) Session 2017 Tax Year Georgia Form 500 with Form 1040NR Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance

Volunteer Income Tax Assistance (VITA) Session 2017 Tax Year Georgia Form 500 with Form 1040NR Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance

Cut here and give this certificate to your employer. Keep the top portion for your records.

Web 12-18 NC-4 Employee s Withholding Allowance Certificate PURPOSE - Complete Form NC-4 so that your employer can withhold the correct amount of State income tax from your pay. If you do not provide an

Web 12-18 NC-4 Employee s Withholding Allowance Certificate PURPOSE - Complete Form NC-4 so that your employer can withhold the correct amount of State income tax from your pay. If you do not provide an

Equivalent Appendix How To Get Tax Help... 27

Department of the Treasury Internal Revenue Service Contents Reminder... 1 Introduction... 1 Publication 915 Are Any of Your Benefits Taxable?... 2 Cat. No. 15320P How To Report Your Benefits... 5 Social

Department of the Treasury Internal Revenue Service Contents Reminder... 1 Introduction... 1 Publication 915 Are Any of Your Benefits Taxable?... 2 Cat. No. 15320P How To Report Your Benefits... 5 Social