Federal Tax Policy and Charitable Giving: Revisiting the 1985 Study by Charles T. Clotfelter

|

|

|

- Ilene Fowler

- 6 years ago

- Views:

Transcription

1 University of Kentucky UKnowledge MPA/MPP Capstone Projects Martin School of Public Policy and Administration 2012 Federal Tax Policy and Charitable Giving: Revisiting the 1985 Study by Charles T. Clotfelter Mary Catherine Tinnon University of Kentucky Click here to let us know how access to this document benefits you. Recommended Citation Tinnon, Mary Catherine, "Federal Tax Policy and Charitable Giving: Revisiting the 1985 Study by Charles T. Clotfelter" (2012). MPA/MPP Capstone Projects This Graduate Capstone Project is brought to you for free and open access by the Martin School of Public Policy and Administration at UKnowledge. It has been accepted for inclusion in MPA/MPP Capstone Projects by an authorized administrator of UKnowledge. For more information, please contact

2 Federal Tax Policy and Charitable Giving: Revisiting the 1985 Study by Charles T. Clotfelter Mary Catherine Tinnon Graduate Capstone Martin School of Public Policy and Administration Dr. Joshua Cowen, Faculty Advisor Dr. Dwight Denison, Faculty Advisor

3 TABLE OF CONTENTS Executive Summary...3 Introduction...4 Literature Review...5 Research Design..9 Analysis & Findings...16 Discussion...22 References 26 2

4 EXECUTIVE SUMMARY This study was inspired and given its basic research design by a study conducted in 1985 by Charles T. Clotfelter, which sought to explain charitable giving by both individuals and corporations in relation to federal tax policy. Clotfelter determined that federal tax policy did influence charitable giving by corporations. The issue to be addressed here is, do the Clotfelter findings still hold true today? The focus of this current study is on charitable giving by corporations only and the dataset was built from the same IRS Statistics of Income that Clotfelter used. Additional data were added from the Bureau of Labor Statistics. There were a total of nineteen industries included and the years focused on were The data were analyzed using two pooled time- series models. The first model used ln charitable contributions as the dependent variable and unemployment rate, number returns, ln total assets, ln cash, ln total income tax after credits, and ln noncash expenses as the independent variables. The second model was identical to the first but added four dummy variables, INDUSTRY_7, INDUSTRY_11, INDUSTRY_15, and INDUSTRY_18, to control for industry. The initial findings from the first model indicate that total income tax after credits and noncash expenses are statistically significant with positive effects. However, in the second model that accounts for specific industry, those monetary variables (total income tax after credits and noncash expenses) are no longer significant. INDUSTRY_11 is statistically significant with positive effects and INDUSTRY_15 is also statistically significant but with negative effects. Overall, it is industry that matters the most. Further analysis of the industry effects on charitable contributions among corporations is recommended in order to provide a better understanding of why some industries are more generous than others. It is also recommended that the dataset be expanded to cover a broader range of years and to catch the affects of marginal tax rate in conjunction with industry. 3

5 INTRODUCTION The National Bureau of Economic Research reported that December 2007 through June 2009 marked the longest recession in the United States since World War II. During and since the eighteen- month recession, nonprofit organizations and charities alike have struggled financially to keep afloat. These organizations are seeing portions of their state and federal funding decline as well as the charitable contributions from outside individuals and businesses that they must be able to depend on each year. This economic environment is making it very difficult for not only the existing nonprofits but also those seeking to start- up new not- for- profit organizations. According to the National Center for Charitable Statistics, there are currently over one and a half million tax- exempt organizations in the United States and, as of the year 2009, there were well over three million tax returns filed with the Internal Revenue Service by corporations. 1 Corporations outnumber nonprofits by a ratio of nearly two to one and they are also the source for a significant portion of charitable contributions to the nonprofit sector. It is important to note, however, that unlike nonprofits, corporations are taxed at both the federal and state level. There is much debate on whether or not federal tax policy affects charitable giving among individuals and corporations. For example, when the marginal tax rates are higher, are individuals and corporations more or less likely to partake in charitable giving? Is there any difference when the marginal tax rates are lower? 1 In 2009, the Internal Revenue Service Corporation Source Book: Statistics of Income reported that there were 3,148,768 tax returns filed for active corporations with Net Income. 4

6 These are both common questions considered when analyzing the issue. Some even argue that the tax deductions given for charitable donations should be eliminated entirely. It is not only an interesting concept to study, but it is also relevant in addressing how our federal tax structure affects our entire tax- exempt sector. These nonprofit organizations consist of many of our schools, hospitals, churches, symphonies, and other recreational facilities, just to name a few. Whether or not the federal tax structure affects charitable gifts is important to not only the taxpayers but also these organizations, which rely on the donations. In this paper, I will focus my research on charitable giving by corporations in relation to the financial background of and industry to which the corporation belongs. The purpose for conducting research in this area is to determine whether there was in fact any effect on the charitable giving of corporations during the years across all industries. The basic design will be similar that of a previous study from 1985 that has since become outdated. LITERATURE REVIEW Published in 1985, Charles T. Clotfelter s book Federal Tax Policy and Charitable Giving outlines many different concepts, analyses, and findings on this issue. He focuses his research on (1) the effect of a federal personal income tax on individual charitable giving, (2) implications of tax policy for volunteering, (3) corporate contributions and the effect of the charitable deduction in the corporate income tax, (4) the estate tax and the importance of bequests for various nonprofit 5

7 activities, and (5) the role of private foundations within the larger charitable sector and the tax legislation affecting them. The extent of this book and his studies is rather large and widespread so, for the purpose of this paper, I will only be focusing on charitable contributions by corporations. To be more specific, I will be looking at this same topic and using the same data sources as Clotfelter, but with the most recent publications instead. With this, I can compare how or if the effects have changed regarding corporate contributions and charitable giving in the years versus It is for this reason that most of the literature I will use comes from Clotfelter s aforementioned book. Chapter 5 of Federal Tax Policy and Charitable Giving is devoted entirely to the effects of corporate income tax on corporate contributions. Clotfelter indicates that most data collected and used on this issue come from the Internal Revenue Service in both the Statistics of Income series and Source Book of Statistics of Income. He goes on to include a chart titled Table 5.9 Summary of Empirical Studies of Corporate Contributions, which lists eight different studies ranging from the years These studies mostly looked at total or average contributions from corporations as the dependent variable and net income as the income measure in the independent variables. Clotfelter s study included an econometric analysis of aggregate data on corporate contributions from 1936 to The focus was on the variation in corporate income and in the price of gifts over time and across asset classes. Major findings from the study can be summed up as, federal taxes, especially tax 6

8 provisions affecting charitable giving, have important effects on the size and distribution of giving. The deductions in the individual, corporate, and estate taxes are of course most important, in the sense that no other tax changes with comparable revenue effects would influence charitable giving as much as the elimination of these deductions. (Clotfelter, p. 276) A conflicting study conducted by Peter Navarro in 1988, Why do Corporations Give to Charity? found no relation between contributions and the federal tax rate. Navarro presents both a theoretical model and empirical model; he then estimates the empirical model to reach this conclusion. Variables included in the model were categorized under demand side motives, cost side motives, managerial discretion, and other factors. (Navarro, pp ) Other less significant findings from his study were that contributions are negatively related to amount of debt as opposed to equity in the firm s capital structure and contributions are positively related to increases in dividends. While this article presents some very interesting findings in regard to corporate contributions and tax policy, I will limit my review of it because it mostly examines variables unrelated to my research. A third perspective can be found in John L. Campbell s article, Why Would Corporations Behave in Socially Responsible Ways? An Institutional Theory of Corporate Responsibility. In this study, Campbell cites both conflicting studies (Clotfelter, 1985 and Navarro, 1988) but instead of agreeing with one or the other, he names a third factor: property rights. That is, he does not seek to explain whether or not tax law affects charitable giving by firms. From a different approach, Campbell says tax law in general is an important property rights institution, which 7

9 may affect corporate behavior regarding philanthropic giving. This third angle can be best presented as, this stream of research suggests that property rights and, by implication, other forms of state regulation may affect the degree to which corporations behave in socially responsible ways. (Campbell, p. 949) In addition to these three studies, there have been a number of different approaches by other authors attempting to explain why and to what extent corporations donate to charities. Similar to the findings in Clotfelter, Carroll and Joulfaian (2005), Lin (2006) and Bakija and Heim (2011) all determined that tax policy strongly influenced philanthropy. The results indicated a negative correlation between corporate philanthropy and tax prices as well as a positive correlation between corporate philanthropy and income and advertising. (Carroll & Joulfaian, 2005) There was also found to be a negative relationship between donations and the capital gains tax rates. (Lin, 2006) Brown, Helland, and Smith (2006) also found that corporate philanthropy had a positive relationship with firm advertising. Their empirical study further indicated that firms with larger boards of directors give more to charity and firms with higher debt- to- value ratios give less in donations. (Brown, Helland, & Smith, 2006) It is clear that the past research on this topic has been very broad and rather inconclusive. Some research suggests that tax policy does affect corporate charitable giving while others do not. In a different manner, some research completely avoids tax policy and focuses on other determinants. For the purposes of this study, I will not be able to advocate a single viewpoint. Instead, I will simply revisit the 1985 study conducted by Clotfelter and attempt to generate similar 8

10 analyses with the most current data available. The focus on charitable contributions by corporations shifts from tax rate effects to the financial background of and industry in which the corporation belongs. RESEARCH DESIGN The research design used is similar to that of Clotfelter s in his book, Federal Tax Policy and Charitable Giving. My primary source is the same as Clotfelter s; however, the data is nearly thirty years more recent. The purpose of my research is to find out whether Clotfelter s findings in 1985 can be replicated today and whether they remain accurate. The structure of Clotfelter s study was an econometric analysis of aggregate data on corporate contributions from the years The data sources used came from the Internal Revenue Service in the Statistics of Income series and the Source Book of Statistics of Income. The variables used were Income and Price. Income can be defined as net income before tax. Price can be defined as the net cost to a firm of making another dollar of corporate contributions. The Statistics of Income series has data as recent as 2009 and includes annual numbers for income, assets, contributions, and other items for corporation income tax returns. The Source Book of Statistics of Income also has data as recent as 2008 and has information by industry and asset size. For my study, I will use only the Statistics of Income. The units of analysis in my research are industries. Corporate income tax return data and unemployment rates for the years 2005, 2006, 2007, 2008, and 9

11 2009 were collected by industry to form the dataset. One of the two estimation equations used by Clotfelter was an aggregate time- series analysis. The second of these equations was a pooled time- series/cross- section analysis. I will be using the data from the Statistics of Income and Bureau of Labor Statistics to estimate a pooled time- series model. In Clotfelter s pooled time- series model, the dependent variable is logarithm of average contributions. The explanatory variables are as follows: In(1- Rm), In(1- Ra), In ACFN, In NIN, and U. Defined: In (Income); Rm (marginal tax rate); Ra (average tax rate: normal tax rate plus excess- profits taxes as percent of net income); ACFN (average cash flow after taxes); NIN (average net income after taxes); and U (unemployment rate). The units of analysis were corporations by asset size and this yielded a sample of 506 observations. According to Clotfelter, the most important limitations of the Internal Revenue Services data have to do with the possibility of mismeasurement of contributions and economic profits. The IRS data on contributions only counts those that are tax deductible. Further, the IRS does not provide a concise definition of corporate income. These are two concerns that must be regarded when interpreting the results. He goes on to say, specifically with regard to the second pooled time- series equation, Two econometric problems often arise in estimation using pooled data such as this: autocorrelation and heteroskedasticity. (Clotfelter, p. 214) I will need to keep these same possibilities in mind when evaluating the results of my estimation. 10

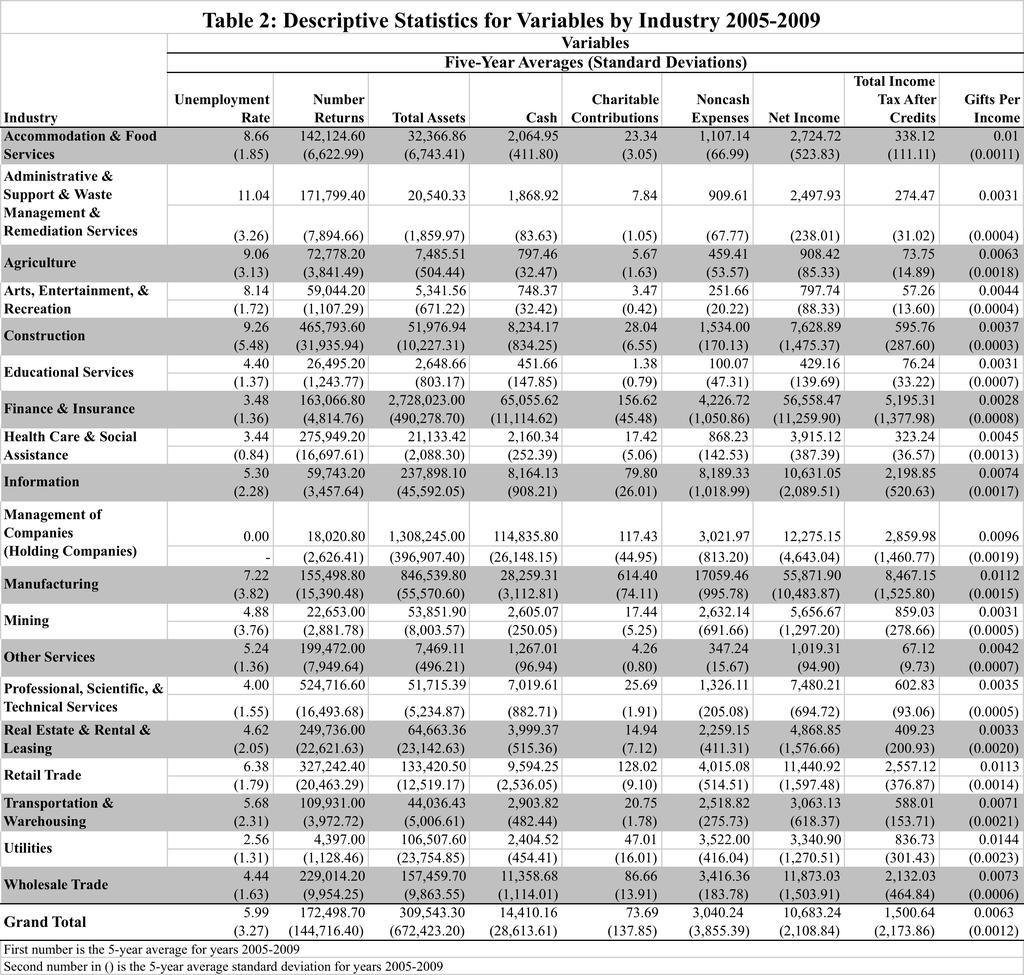

12 DATA DESCRIPTION The data used in this study from the Statistics of Income include nine variables: number of returns, total assets, cash, charitable contributions, amortization, depreciation, depletion, net income, and total income tax after credits. Data obtained from the Bureau of Labor Statistics includes only one variable, unemployment rate. Once uploaded into STATA, two new variables were created, gifts per income and noncash expenses. Gifts per income expresses charitable contributions as a percentage of net income and was necessary to include as a control variable for changes in the economy by industry. Noncash expenses is amortization, depreciation, and depletion added together into one variable for the sole purpose of simplicity. Observations were collected for the nine variables listed above across nineteen different industries over a five- year period ( ). As mentioned prior, industry is the unit of analysis. The industries are as follows: Accommodation & Food Services, Administrative & Support & Waste Management & Remediation Services, Agriculture, Arts, Entertainment, & Recreation, Construction, Educational Services, Finance & Insurance, Health Care & Social Assistance, Information, Management of Companies (Holding Companies), Manufacturing, Mining, Other Services, Professional, Scientific, & Technical Services, Real Estate & Rental & Leasing, Retail Trade, Transportation & Warehousing, Utilities, and Wholesale Trade. 11

and focused much of his analyses on the effects of the marginal tax rate on corporate charitable contributions.")

13 RESEARCH MODEL The purpose of this paper is to look beyond Clotfelter s findings in 1985 and present a similar, yet new, perspective on the study of charitable giving. Clotfelter used data over a much longer timeframe ( ) and focused much of his analyses on the effects of the marginal tax rate on corporate charitable contributions. This was not included in my model because the marginal tax rate during the years did not change and was therefore irrelevant. In 12

14 addition to this difference, I chose to look at industry effects in relation to charitable contributions. As noted previously, there are a total of nineteen industries included in the data as well as eleven variables of interest. Two of the variables, unemployment rate and number of returns, are not monetary values. The eight monetary variables (total assets, cash, charitable contributions, amortization, depreciation, depletion, net income, and total income tax after credits) were then re- scaled into units of ten thousand to simplify the results. For the purpose of simplifying the data and being able to more easily identify patterns, five- year averages and standard deviations were also calculated for each variable across all nineteen industries. The results can be seen in Table 2. It should be noted that Management of Companies (Holding Companies) does not have a value for unemployment rate because the Bureau of Labor Statistics did not recognize this industry. In the Clotfelter models, variables were converted into logarithms. For the purpose of keeping my model similar to his, all eight monetary variables were log transformed. As mentioned above, in order to see the effects of all the noncash expense variables (amortization, depreciation, and depletion), a new variable was created, NC (noncash expenses). It was then necessary to log transform this new variable. The purpose in converting these variables into logarithms was because of the apparent skewed nature among some of the independent variables. Some were very small while others were very large and some were monetary while others were not. In order to account for these differences and provide a more normal distribution for the skewed data, logarithmic values were the most practical. 13

15 14

16 Once these variables were log transformed, two regression models were used. Both models were comprised of variables over a five- year period of time across nineteen industries; therefore, a pooled time- series regression was used. The first model did not control for industry while the second did. Research Question 1: Do the selected independent variables (unemployment rate, number returns, total assets, cash, total income tax after credits, and noncash expenses) affect corporate charitable contributions? This first regression was estimated using a pooled time- series model. The dependent variable was charitable contributions and the independent variables were unemployment rate, number of returns, total assets, total cash, total income tax after credits, and total noncash expenses. The latter four were in logarithm values. This regression model can be written as: Y= β0 + β1x1 + β2x βnxn + ε Y is the logarithm of total charitable contributions by industry, X represents the variables of interest, and ε accounts for the random error in the model. The standard errors of each estimate are also clustered by industry. 15

17 Research Question 2: Does industry matter when analyzing the affect of the selected independent variables on corporate charitable contributions? This second regression was also estimated using a pooled time- series model. Four industries (Finance & Insurance, Manufacturing, Real Estate, and Utilities) were included as dummy variables to control for any differences resulting from the first model. These industries were chosen because of patterns indicated in the descriptive statistics as outlined in Table 2. The equation is identical to the first except for the four dummy variables added to the end. This regression model can be written as: Y= β0 + β1x1 + β2x βnxn + β7d1 + β8d2 + β9d3 + β10d4 + ε Y is once again the logarithm of charitable contributions, X represents the variables of interest, D represents controlling for the dummy variables for industry, and ε accounts for the random error in the model. The standard errors of each estimate are again clustered by industry. ANALYSIS & FINDINGS The results from both models were different than those from the previous empirical analysis by Clotfelter. Clotfelter was able to attribute the differences in charitable contributions over the years studied to changes in the marginal tax rate on corporate income. Because the marginal tax rate did not change during the years analyzed in this study, the variables of interest were not identical. The first model looked at the relationship between unemployment rate, number of returns, total 16

18 assets, total cash, total income tax after credits, and noncash expenses and the dependent variable, charitable contributions. The findings indicate that both total income tax after credits and noncash expenses are statistically significant with positive effects. Total income tax after credits has a fairly large, positive effect with a coefficient of 0.596, while noncash expenses has a smaller, positive effect with a coefficient of These results can be seen in Table 3. When dummy variables are added to control for industry in the second model, the findings no longer indicate that the monetary variables matter. Industry 11 (Manufacturing) and industry 15 (Real Estate) are both statistically significant in the regression. The manufacturing industry had a very large, positive effect with a coefficient of The real estate industry, on the other hand, had a fairly large, negative effect with a coefficient of These results can be seen in Table 4. The first model revealed that both total income tax after credits and noncash expenses were statistically significant. What this means is that the amount of total income tax a corporation must pay after credits positively affects their amount of charitable contributions. Furthermore, the amount of noncash expenses a corporation is responsible for also affects their amount of charitable contributions. In theory this makes sense. If a corporation has a large amount of taxes they must pay, even after all credits are deducted, it is probably going to alter the way they choose to give in charitable donations. In regard to noncash expenses, made up of amortization, depreciation, and depletion, it also makes logical sense that if a corporation has a large amount of their expenses in areas other than cash it will affect how they choose to give in charitable contributions. 17

19 TABLE 3: REGRESSION MODEL 1 RESULTS COEFFICIENT (ROBUST STD. ERROR) INDEPENDENT VARIABLES (1) ln Charitable Contributions Unemployment Rate (0.0293) Number Returns 7.29e-07 (9.49e-07) ln Total Assets (0.298) ln Cash (0.372) ln Total Income Tax After Credits 0.596** (0.208) ln Noncash Expenses 0.348* (0.169) Constant *** (0.697) Observations 90 R-squared Robust standard errors in parentheses *** p<0.01, ** p<0.05, * p<0.1 Both of these variables have a positive correlation with charitable contributions meaning that as they increase, charitable contributions also increase. This might be explained as corporations with more total income tax after credits had more income tax to begin with. A corporation that is paying more in income tax likely has more money in general to give away in the form of donations. Thus, this variable is significant in predicting whether a corporation gives more or less to charities. This same concept can be applied to noncash expenses. 18

20 The second model reveals much more compelling evidence and indicates that industry is what really matters when determining a corporation s influences on charitable giving. When controlling for four of the nineteen industries (Industry 7- Finance & Insurance, Industry 11- Manufacturing, Industry 15- Real Estate, and Industry 18- Utilities), total income tax after credits and noncash expenses are no longer statistically significant. Instead, industries 11 (manufacturing) and 15 (real estate) are significant at p<0.01. This was an unexpected finding so in order to better understand what this meant I took the analysis one step further. To see the dollar value difference by industry, five equations were used based on the equations from research questions one and two. The results can be seen in Table 5. First, the dollar value of charitable contributions without industries was calculated by multiplying each variable average by each variable coefficient then adding them together and adding the constant. Next, it was necessary to take the inverse log of that number because those numbers had been previously log transformed. Once that number was found, the total was multiplied by ten thousand because the numbers had been scaled down into units of 10,000 when uploaded into STATA. This number was $251,

21 TABLE 4: REGRESSION MODEL 2 RESULTS COEFFICIENT (ROBUST STD. ERROR) INDEPENDENT VARIABLES (1) ln Charitable Contributions Unemployment Rate (0.0251) Number Returns 1.18e-06 (9.01e-07) ln Total Assets (0.475) ln Cash (0.377) ln Total Income Tax After Credits (0.223) ln Noncash Expenses (0.290) INDUSTRY_ (0.946) INDUSTRY_ *** (0.225) INDUSTRY_ *** (0.188) INDUSTRY_ (0.302) Constant *** (1.211) Observations 90 R-squared Robust standard errors in parentheses *** p<0.01, ** p<0.05, * p<0.1 Once this number was calculated, the dollar values could be found for each of the four industries included. To do this, the amount found in the first equation, $251,259 was added to the coefficient of each industry. Then the inverse log was found and that number was multiplied by ten thousand. This meant that the process 20

22 would need to be repeated four times for the four different industries. The results indicate that for finance and insurance, charitable contributions were less than the average across all industries at $156,966. Manufacturing was much higher at $535,810, real estate was $135,119, and utilities came in at $334,738. In other words, this is the dollar value of charitable contributions, on average in each industry, which corporations gave during the years There are a number of reasons to explain why these were the results. It is difficult to identify any exact reason why corporations from some industries might donate more than others, but here are a few examples. The American economy was 21

23 well on its way to the recession that hit in 2007 and the years analyzed in this study would capture those effects. Some industries were hit harder than others and it is possible that those that were hurt the most do not have as much money or willingness to donate as those that remained fairly untouched. On the other hand, with no regard to the current economic conditions, some industries simply have a larger amount of money and available cash to donate than others. In this study, the manufacturing industry is a good example of that. Of the four industries controlled for in the model, manufacturing had the third highest five- year average in cash and by far the largest amount spent on charitable contributions. It is also conceivable that those industries with less available cash, which still have a large amount of assets, will donate less than others. While this is complete speculation, it is an area where more research could be done. DISCUSSION RECOMMENDATIONS This is an interesting topic for both nonprofit organizations and policy makers to examine. If monetary variables do not matter but industry does, then the nonprofit organizations should analyze this further to determine which of these industries to target for charitable gifts. While this is likely to already be occurring, it would be helpful as a nonprofit manager to know which types of corporations, by industry, on average, are the most generous when it comes to donations. 22

24 From a policy maker standpoint, it would be interesting to know what types of deductions and tax credits, by industry, result in the most charitable giving. Are some industries eligible for more deductions and credits than others? In other words, what types of policies are responsible for this difference by industry? If it is accurate that industry matters more than anything, this could also provide evidence for policy makers wishing to eliminate the charitable tax breaks without adversely affecting the nonprofit sector. These are all ideas what would require much time, data, and analysis to research, which brings me to the particular constraints that were present in this study. LIMITATIONS There were several limitations to this study, particularly in regard to the dataset. There were issues of both time and available data. First, the study was originally intended to be nearly identical to that of Clotfelter s 1985 research, which looked at marginal tax rates and charitable giving among corporations. This was immediately a problem because the timeframe used in this study was much smaller. He was able to look at data from the years and this study was only Over the forty- five years in the Clotfelter study, the marginal tax rate changed many times which he was able to use and say affected charitable giving. Over the five years in this study, the marginal tax rate did not change, therefore, other variables had to be utilized. Next, there was the issue of time. Given that I did not have unlimited time to conduct the study, the number of years included in the dataset was limited to five. 23

25 While the data were available for many years prior to 2005, I believed that five years would be sufficient to try to provide some answers to the basic research questions. If provided more time, it would be an interesting next step to see what differences there might be in running the same regression models with data from earlier years. With the very strong economy of the 1990 s, I would like to see whether this would change the results that were found in this study. Finally, there was the issue of omitted variables. As previously mentioned, the Bureau of Labor Statistics did not have unemployment data available for all nineteen industries. There were no numbers for the Management of Companies (Holding Companies) industry for any of the five years. This meant that the industry had to be excluded from the regression models, which included unemployment rate as an independent variable. It is unlikely that this one industry would have skewed the results too much but regardless it must be stated that there was one industry completely left out of the models. FUTURE RESEARCH Given the limitations of this study, there is an extensive amount of research that could be conducted to further examine this topic. In order to get a better understanding of marginal tax rates, and in accordance with the Clotfelter study, one could use my models and widen the dataset to include every year since 1990 and the marginal tax rates. This would be more in line with his analysis and also catch any affects of tax rates on charitable contributions since his study. 24

26 The idea that industry is what matters is also an area that could be studied further. This could be done by taking a select few industries and looking more in- depth at their various financial situations and market conditions. It could also mean looking more at the types of charities that particular industries give money to and what implications that has for policy makers and nonprofit managers. Overall, the findings of this study were unexpected but promising for those seeking to further understand what drives corporations by industry to give a portion of their profits to charitable organizations across America. 25

27 REFERENCES Bakija, Jon and Bradley T. Heim. How Does Charitable Giving Respond to Incentives and Income? New Estimates From Panel Data, National Tax Journal, Vol. 64, No. 2 (2011) Brown, William O., Eric Helland, and Janet Kiholm Smith. Corporate Philanthropic Practices, Journal of Corporate Finance, Vol. 12, No. 5 (2006) Bureau of Labor Statistics. Labor Force Statistics From the Current Population Survey. Last Revised March 2, Campbell, John L. Why Would Corporations Behave in Socially Responsible Ways? An Institutional Theory of Corporate Responsibility, Academy of Management Review, Vol. 32, No. 3 (2007) Carroll, Robert and David Joulfaian. Taxes and Corporate Giving to Charity, Public Finance Review, Vol. 33, No. 3 (2005) Clotfelter, Charles T, Federal Tax Policy and Charitable Giving, (Chicago: University of Chicago Press, 1985) Internal Revenue Service. Statistics of Income. Last Revised March 6, Lin, Sandy. The Effect of the Capital Gains Tax on Donations of Cash and Appreciated Assets, WRLC Digital Depository, (2006) National Bureau of Economic Research. Business Cycle Dating Committee, Last Revised September 20, National Center for Charitable Statistics. Quick Facts About Nonprofits. Last Revised August, Navarro, Peter. Why do Corporations Give to Charity?, The Journal of Business, Vol. 61, No. 1 (Jan., 1988)

An Analysis of the Effect of State Aid Transfers on Local Government Expenditures

An Analysis of the Effect of State Aid Transfers on Local Government Expenditures John Perrin Advisor: Dr. Dwight Denison Martin School of Public Policy and Administration Spring 2017 Table of Contents

An Analysis of the Effect of State Aid Transfers on Local Government Expenditures John Perrin Advisor: Dr. Dwight Denison Martin School of Public Policy and Administration Spring 2017 Table of Contents

Julio Videras Department of Economics Hamilton College

LUCK AND GIVING Julio Videras Department of Economics Hamilton College Abstract: This paper finds that individuals who consider themselves lucky in finances donate more than individuals who do not consider

LUCK AND GIVING Julio Videras Department of Economics Hamilton College Abstract: This paper finds that individuals who consider themselves lucky in finances donate more than individuals who do not consider

Employment Effects of Reducing Capital Gains Tax Rates in Ohio. William Melick Kenyon College. Eric Andersen American Action Forum

Employment Effects of Reducing Capital Gains Tax Rates in Ohio William Melick Kenyon College Eric Andersen American Action Forum June 2011 Executive Summary Entrepreneurial activity is a key driver of

Employment Effects of Reducing Capital Gains Tax Rates in Ohio William Melick Kenyon College Eric Andersen American Action Forum June 2011 Executive Summary Entrepreneurial activity is a key driver of

THE EFFECT OF THE CAPITAL GAINS TAX ON DONATIONS OF CASH AND APPRECIATED ASSETS

THE EFFECT OF THE CAPITAL GAINS TAX ON DONATIONS OF CASH AND APPRECIATED ASSETS A Thesis submitted to the Faculty of the Graduate School of Arts & Sciences of Georgetown University in partial fulfillment

THE EFFECT OF THE CAPITAL GAINS TAX ON DONATIONS OF CASH AND APPRECIATED ASSETS A Thesis submitted to the Faculty of the Graduate School of Arts & Sciences of Georgetown University in partial fulfillment

Labor Market Protections and Unemployment: Does the IMF Have a Case? Dean Baker and John Schmitt 1. November 3, 2003

cepr Center for Economic and Policy Research Briefing Paper Labor Market Protections and Unemployment: Does the IMF Have a Case? Dean Baker and John Schmitt 1 November 3, 2003 CENTER FOR ECONOMIC AND POLICY

cepr Center for Economic and Policy Research Briefing Paper Labor Market Protections and Unemployment: Does the IMF Have a Case? Dean Baker and John Schmitt 1 November 3, 2003 CENTER FOR ECONOMIC AND POLICY

THE DESIGN OF THE INDIVIDUAL ALTERNATIVE

00 TH ANNUAL CONFERENCE ON TAXATION CHARITABLE CONTRIBUTIONS UNDER THE ALTERNATIVE MINIMUM TAX* Shih-Ying Wu, National Tsing Hua University INTRODUCTION THE DESIGN OF THE INDIVIDUAL ALTERNATIVE minimum

00 TH ANNUAL CONFERENCE ON TAXATION CHARITABLE CONTRIBUTIONS UNDER THE ALTERNATIVE MINIMUM TAX* Shih-Ying Wu, National Tsing Hua University INTRODUCTION THE DESIGN OF THE INDIVIDUAL ALTERNATIVE minimum

CAPITAL STRUCTURE AND THE 2003 TAX CUTS Richard H. Fosberg

CAPITAL STRUCTURE AND THE 2003 TAX CUTS Richard H. Fosberg William Paterson University, Deptartment of Economics, USA. KEYWORDS Capital structure, tax rates, cost of capital. ABSTRACT The main purpose

CAPITAL STRUCTURE AND THE 2003 TAX CUTS Richard H. Fosberg William Paterson University, Deptartment of Economics, USA. KEYWORDS Capital structure, tax rates, cost of capital. ABSTRACT The main purpose

Online Appendix for. Explaining Corporate Capital Structure: Product Markets, Leases, and Asset Similarity. Joshua D.

Online Appendix for Explaining Corporate Capital Structure: Product Markets, Leases, and Asset Similarity Section 1: Data A. Overview of Capital IQ Joshua D. Rauh Amir Sufi Capital IQ (CIQ) is a Standard

Online Appendix for Explaining Corporate Capital Structure: Product Markets, Leases, and Asset Similarity Section 1: Data A. Overview of Capital IQ Joshua D. Rauh Amir Sufi Capital IQ (CIQ) is a Standard

Deal Stats Transaction Survey

July 2012 December 2012 Summary Report Prepared by Jason M. Bolt, CFA, ASA Columbia Financial Advisors, Inc. K. Perry Campbell, Ph.D., CM&AA ACT Capital Advisors, LLC April 2013 A Publication of the AM&AA

July 2012 December 2012 Summary Report Prepared by Jason M. Bolt, CFA, ASA Columbia Financial Advisors, Inc. K. Perry Campbell, Ph.D., CM&AA ACT Capital Advisors, LLC April 2013 A Publication of the AM&AA

THE BEHAVIOUR OF GOVERNMENT OF CANADA REAL RETURN BOND RETURNS: AN EMPIRICAL STUDY

ASAC 2005 Toronto, Ontario David W. Peters Faculty of Social Sciences University of Western Ontario THE BEHAVIOUR OF GOVERNMENT OF CANADA REAL RETURN BOND RETURNS: AN EMPIRICAL STUDY The Government of

ASAC 2005 Toronto, Ontario David W. Peters Faculty of Social Sciences University of Western Ontario THE BEHAVIOUR OF GOVERNMENT OF CANADA REAL RETURN BOND RETURNS: AN EMPIRICAL STUDY The Government of

Factors in the returns on stock : inspiration from Fama and French asset pricing model

Lingnan Journal of Banking, Finance and Economics Volume 5 2014/2015 Academic Year Issue Article 1 January 2015 Factors in the returns on stock : inspiration from Fama and French asset pricing model Yuanzhen

Lingnan Journal of Banking, Finance and Economics Volume 5 2014/2015 Academic Year Issue Article 1 January 2015 Factors in the returns on stock : inspiration from Fama and French asset pricing model Yuanzhen

NBER WORKING PAPER SERIES CHARITABLE BEQUESTS AND TAXES ON INHERITANCES AND ESTATES: AGGREGATE EVIDENCE FROM ACROSS STATES AND TIME

NBER WORKING PAPER SERIES CHARITABLE BEQUESTS AND TAXES ON INHERITANCES AND ESTATES: AGGREGATE EVIDENCE FROM ACROSS STATES AND TIME Jon Bakija William Gale Joel Slemrod Working Paper 9661 http://www.nber.org/papers/w9661

NBER WORKING PAPER SERIES CHARITABLE BEQUESTS AND TAXES ON INHERITANCES AND ESTATES: AGGREGATE EVIDENCE FROM ACROSS STATES AND TIME Jon Bakija William Gale Joel Slemrod Working Paper 9661 http://www.nber.org/papers/w9661

How Are Interest Rates Affecting Household Consumption and Savings?

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 2012 How Are Interest Rates Affecting Household Consumption and Savings? Lacy Christensen Utah State University

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 2012 How Are Interest Rates Affecting Household Consumption and Savings? Lacy Christensen Utah State University

Wage Scars and Human Capital Theory: Appendix

Wage Scars and Human Capital Theory: Appendix Justin Barnette and Amanda Michaud Kent State University and Indiana University October 2, 2017 Abstract A large literature shows workers who are involuntarily

Wage Scars and Human Capital Theory: Appendix Justin Barnette and Amanda Michaud Kent State University and Indiana University October 2, 2017 Abstract A large literature shows workers who are involuntarily

Green Giving and Demand for Environmental Quality: Evidence from the Giving and Volunteering Surveys. Debra K. Israel* Indiana State University

Green Giving and Demand for Environmental Quality: Evidence from the Giving and Volunteering Surveys Debra K. Israel* Indiana State University Working Paper * The author would like to thank Indiana State

Green Giving and Demand for Environmental Quality: Evidence from the Giving and Volunteering Surveys Debra K. Israel* Indiana State University Working Paper * The author would like to thank Indiana State

VERIFYING OF BETA CONVERGENCE FOR SOUTH EAST COUNTRIES OF ASIA

Journal of Indonesian Applied Economics, Vol.7 No.1, 2017: 59-70 VERIFYING OF BETA CONVERGENCE FOR SOUTH EAST COUNTRIES OF ASIA Michaela Blasko* Department of Operation Research and Econometrics University

Journal of Indonesian Applied Economics, Vol.7 No.1, 2017: 59-70 VERIFYING OF BETA CONVERGENCE FOR SOUTH EAST COUNTRIES OF ASIA Michaela Blasko* Department of Operation Research and Econometrics University

Macroeconomic Impact of S ESOPs on the U.S. Economy

Macroeconomic Impact of S ESOPs on the U.S. Economy By Alex Brill April 17, 2013 1350 Connecticut Ave. NW Suite 610 Washington, DC 20036 www.matrixglobaladvisors.com Executive Summary S corporations that

Macroeconomic Impact of S ESOPs on the U.S. Economy By Alex Brill April 17, 2013 1350 Connecticut Ave. NW Suite 610 Washington, DC 20036 www.matrixglobaladvisors.com Executive Summary S corporations that

How Changes in Tax Rates Might Affect Itemized Charitable Deductions. The Center on Philanthropy at Indiana University March 2009

Executive Summary How Changes in Tax Rates Might Affect Itemized Charitable Deductions The Center on Philanthropy at Indiana University March 2009 President Obama s budget proposal for 2010 and beyond

Executive Summary How Changes in Tax Rates Might Affect Itemized Charitable Deductions The Center on Philanthropy at Indiana University March 2009 President Obama s budget proposal for 2010 and beyond

Volume 29, Issue 4. A Nominal Theory of the Nominal Rate of Interest and the Price Level: Some Empirical Evidence

Volume 29, Issue 4 A Nominal Theory of the Nominal Rate of Interest and the Price Level: Some Empirical Evidence Tito B.S. Moreira Catholic University of Brasilia Geraldo Silva Souza University of Brasilia

Volume 29, Issue 4 A Nominal Theory of the Nominal Rate of Interest and the Price Level: Some Empirical Evidence Tito B.S. Moreira Catholic University of Brasilia Geraldo Silva Souza University of Brasilia

Nonprofit organizations are becoming a large and important

Nonprofit Taxable Activities, Production Complementarities, and Joint Cost Allocations Nonprofit Taxable Activities, Production Complementarities, and Joint Cost Allocations Abstract - Nonprofit organizations

Nonprofit Taxable Activities, Production Complementarities, and Joint Cost Allocations Nonprofit Taxable Activities, Production Complementarities, and Joint Cost Allocations Abstract - Nonprofit organizations

Taxing Inventory: An Analysis of its Effects in Indiana

Taxing Inventory: An Analysis of its Effects in Indiana Larry DeBoer Professor of Agricultural Economics, Purdue University TFC ewer than ten states tax the assessed value of business inventories as part

Taxing Inventory: An Analysis of its Effects in Indiana Larry DeBoer Professor of Agricultural Economics, Purdue University TFC ewer than ten states tax the assessed value of business inventories as part

2018 outlook and analysis letter

2018 outlook and analysis letter The vital statistics of America s state park systems Jordan W. Smith, Ph.D. Yu-Fai Leung, Ph.D. December 2018 2018 outlook and analysis letter Jordan W. Smith, Ph.D. Yu-Fai

2018 outlook and analysis letter The vital statistics of America s state park systems Jordan W. Smith, Ph.D. Yu-Fai Leung, Ph.D. December 2018 2018 outlook and analysis letter Jordan W. Smith, Ph.D. Yu-Fai

Do Domestic Chinese Firms Benefit from Foreign Direct Investment?

Do Domestic Chinese Firms Benefit from Foreign Direct Investment? Chang-Tai Hsieh, University of California Working Paper Series Vol. 2006-30 December 2006 The views expressed in this publication are those

Do Domestic Chinese Firms Benefit from Foreign Direct Investment? Chang-Tai Hsieh, University of California Working Paper Series Vol. 2006-30 December 2006 The views expressed in this publication are those

EXECUTIVE COMPENSATION AND FIRM PERFORMANCE: BIG CARROT, SMALL STICK

EXECUTIVE COMPENSATION AND FIRM PERFORMANCE: BIG CARROT, SMALL STICK Scott J. Wallsten * Stanford Institute for Economic Policy Research 579 Serra Mall at Galvez St. Stanford, CA 94305 650-724-4371 wallsten@stanford.edu

EXECUTIVE COMPENSATION AND FIRM PERFORMANCE: BIG CARROT, SMALL STICK Scott J. Wallsten * Stanford Institute for Economic Policy Research 579 Serra Mall at Galvez St. Stanford, CA 94305 650-724-4371 wallsten@stanford.edu

Dividend Policy: Determining the Relevancy in Three U.S. Sectors

Dividend Policy: Determining the Relevancy in Three U.S. Sectors Corey Cole Eastern New Mexico University Ying Yan Eastern New Mexico University David Hemley Eastern New Mexico University The purpose of

Dividend Policy: Determining the Relevancy in Three U.S. Sectors Corey Cole Eastern New Mexico University Ying Yan Eastern New Mexico University David Hemley Eastern New Mexico University The purpose of

Government Consumption Spending Inhibits Economic Growth in the OECD Countries

Government Consumption Spending Inhibits Economic Growth in the OECD Countries Michael Connolly,* University of Miami Cheng Li, University of Miami July 2014 Abstract Robert Mundell is the widely acknowledged

Government Consumption Spending Inhibits Economic Growth in the OECD Countries Michael Connolly,* University of Miami Cheng Li, University of Miami July 2014 Abstract Robert Mundell is the widely acknowledged

1 Introduction. Domonkos F Vamossy. Whitworth University, United States

Proceedings of FIKUSZ 14 Symposium for Young Researchers, 2014, 285-292 pp The Author(s). Conference Proceedings compilation Obuda University Keleti Faculty of Business and Management 2014. Published by

Proceedings of FIKUSZ 14 Symposium for Young Researchers, 2014, 285-292 pp The Author(s). Conference Proceedings compilation Obuda University Keleti Faculty of Business and Management 2014. Published by

Does Minimum Wage Lower Employment for Teen Workers? Kevin Edwards. Abstract

Does Minimum Wage Lower Employment for Teen Workers? Kevin Edwards Abstract This paper will look at the effect that the state and federal minimum wage increases between 2006 and 2010 had on the employment

Does Minimum Wage Lower Employment for Teen Workers? Kevin Edwards Abstract This paper will look at the effect that the state and federal minimum wage increases between 2006 and 2010 had on the employment

Risk-Adjusted Futures and Intermeeting Moves

issn 1936-5330 Risk-Adjusted Futures and Intermeeting Moves Brent Bundick Federal Reserve Bank of Kansas City First Version: October 2007 This Version: June 2008 RWP 07-08 Abstract Piazzesi and Swanson

issn 1936-5330 Risk-Adjusted Futures and Intermeeting Moves Brent Bundick Federal Reserve Bank of Kansas City First Version: October 2007 This Version: June 2008 RWP 07-08 Abstract Piazzesi and Swanson

Working Paper Series May David S. Allen* Associate Professor of Finance. Allen B. Atkins Associate Professor of Finance.

CBA NAU College of Business Administration Northern Arizona University Box 15066 Flagstaff AZ 86011 How Well Do Conventional Stock Market Indicators Predict Stock Market Movements? Working Paper Series

CBA NAU College of Business Administration Northern Arizona University Box 15066 Flagstaff AZ 86011 How Well Do Conventional Stock Market Indicators Predict Stock Market Movements? Working Paper Series

An Evaluation of the Relationship Between Private and Public R&D Funds with Consideration of Level of Government

1 An Evaluation of the Relationship Between Private and Public R&D Funds with Consideration of Level of Government Sebastian Hamirani Fall 2017 Advisor: Professor Stephen Hamilton Submitted 7 December

1 An Evaluation of the Relationship Between Private and Public R&D Funds with Consideration of Level of Government Sebastian Hamirani Fall 2017 Advisor: Professor Stephen Hamilton Submitted 7 December

THE EFFECTS OF THE EU BUDGET ON ECONOMIC CONVERGENCE

THE EFFECTS OF THE EU BUDGET ON ECONOMIC CONVERGENCE Eva Výrostová Abstract The paper estimates the impact of the EU budget on the economic convergence process of EU member states. Although the primary

THE EFFECTS OF THE EU BUDGET ON ECONOMIC CONVERGENCE Eva Výrostová Abstract The paper estimates the impact of the EU budget on the economic convergence process of EU member states. Although the primary

Economic Growth and Convergence across the OIC Countries 1

Economic Growth and Convergence across the OIC Countries 1 Abstract: The main purpose of this study 2 is to analyze whether the Organization of Islamic Cooperation (OIC) countries show a regional economic

Economic Growth and Convergence across the OIC Countries 1 Abstract: The main purpose of this study 2 is to analyze whether the Organization of Islamic Cooperation (OIC) countries show a regional economic

The Effect of Macroeconomic Conditions on Applications to Supplemental Security Income

Syracuse University SURFACE Syracuse University Honors Program Capstone Projects Syracuse University Honors Program Capstone Projects Spring 5-1-2014 The Effect of Macroeconomic Conditions on Applications

Syracuse University SURFACE Syracuse University Honors Program Capstone Projects Syracuse University Honors Program Capstone Projects Spring 5-1-2014 The Effect of Macroeconomic Conditions on Applications

Financial Constraints and the Risk-Return Relation. Abstract

Financial Constraints and the Risk-Return Relation Tao Wang Queens College and the Graduate Center of the City University of New York Abstract Stock return volatilities are related to firms' financial

Financial Constraints and the Risk-Return Relation Tao Wang Queens College and the Graduate Center of the City University of New York Abstract Stock return volatilities are related to firms' financial

Long-run Consumption Risks in Assets Returns: Evidence from Economic Divisions

Long-run Consumption Risks in Assets Returns: Evidence from Economic Divisions Abdulrahman Alharbi 1 Abdullah Noman 2 Abstract: Bansal et al (2009) paper focus on measuring risk in consumption especially

Long-run Consumption Risks in Assets Returns: Evidence from Economic Divisions Abdulrahman Alharbi 1 Abdullah Noman 2 Abstract: Bansal et al (2009) paper focus on measuring risk in consumption especially

Stock price synchronicity and the role of analyst: Do analysts generate firm-specific vs. market-wide information?

Stock price synchronicity and the role of analyst: Do analysts generate firm-specific vs. market-wide information? Yongsik Kim * Abstract This paper provides empirical evidence that analysts generate firm-specific

Stock price synchronicity and the role of analyst: Do analysts generate firm-specific vs. market-wide information? Yongsik Kim * Abstract This paper provides empirical evidence that analysts generate firm-specific

High Frequency Autocorrelation in the Returns of the SPY and the QQQ. Scott Davis* January 21, Abstract

High Frequency Autocorrelation in the Returns of the SPY and the QQQ Scott Davis* January 21, 2004 Abstract In this paper I test the random walk hypothesis for high frequency stock market returns of two

High Frequency Autocorrelation in the Returns of the SPY and the QQQ Scott Davis* January 21, 2004 Abstract In this paper I test the random walk hypothesis for high frequency stock market returns of two

starting on 5/1/1953 up until 2/1/2017.

An Actuary s Guide to Financial Applications: Examples with EViews By William Bourgeois An actuary is a business professional who uses statistics to determine and analyze risks for companies. In this guide,

An Actuary s Guide to Financial Applications: Examples with EViews By William Bourgeois An actuary is a business professional who uses statistics to determine and analyze risks for companies. In this guide,

AN ANALYSIS OF THE DEGREE OF DIVERSIFICATION AND FIRM PERFORMANCE Zheng-Feng Guo, Vanderbilt University Lingyan Cao, University of Maryland

The International Journal of Business and Finance Research Volume 6 Number 2 2012 AN ANALYSIS OF THE DEGREE OF DIVERSIFICATION AND FIRM PERFORMANCE Zheng-Feng Guo, Vanderbilt University Lingyan Cao, University

The International Journal of Business and Finance Research Volume 6 Number 2 2012 AN ANALYSIS OF THE DEGREE OF DIVERSIFICATION AND FIRM PERFORMANCE Zheng-Feng Guo, Vanderbilt University Lingyan Cao, University

Labor Economics Field Exam Spring 2014

Labor Economics Field Exam Spring 2014 Instructions You have 4 hours to complete this exam. This is a closed book examination. No written materials are allowed. You can use a calculator. THE EXAM IS COMPOSED

Labor Economics Field Exam Spring 2014 Instructions You have 4 hours to complete this exam. This is a closed book examination. No written materials are allowed. You can use a calculator. THE EXAM IS COMPOSED

Hedging inflation by selecting stock industries

Hedging inflation by selecting stock industries Author: D. van Antwerpen Student number: 288660 Supervisor: Dr. L.A.P. Swinkels Finish date: May 2010 I. Introduction With the recession at it s end last

Hedging inflation by selecting stock industries Author: D. van Antwerpen Student number: 288660 Supervisor: Dr. L.A.P. Swinkels Finish date: May 2010 I. Introduction With the recession at it s end last

HOW DOES CHARITABLE GIVING RESPOND TO INCENTIVES AND INCOME? NEW ESTIMATES FROM PANEL DATA. Jon Bakija and Bradley T. Heim

National Tax Journal, June 2011, 64 (2, Part 2), 615 650 HOW DOES CHARITABLE GIVING RESPOND TO INCENTIVES AND INCOME? NEW ESTIMATES FROM PANEL DATA Jon Bakija and Bradley T. Heim We estimate the elasticity

National Tax Journal, June 2011, 64 (2, Part 2), 615 650 HOW DOES CHARITABLE GIVING RESPOND TO INCENTIVES AND INCOME? NEW ESTIMATES FROM PANEL DATA Jon Bakija and Bradley T. Heim We estimate the elasticity

The Fisher Equation and Output Growth

The Fisher Equation and Output Growth A B S T R A C T Although the Fisher equation applies for the case of no output growth, I show that it requires an adjustment to account for non-zero output growth.

The Fisher Equation and Output Growth A B S T R A C T Although the Fisher equation applies for the case of no output growth, I show that it requires an adjustment to account for non-zero output growth.

Estimating Personal Consumption With and Without Savings in Wrongful Death Cases

Journal of Forensic Economics 13(1), 2000, pp. 1 10 2000 by the National Association of Forensic Economics Estimating Personal Consumption With and Without Savings in Wrongful Death Cases Martine T. Ajwa,

Journal of Forensic Economics 13(1), 2000, pp. 1 10 2000 by the National Association of Forensic Economics Estimating Personal Consumption With and Without Savings in Wrongful Death Cases Martine T. Ajwa,

MODELING VOLATILITY OF US CONSUMER CREDIT SERIES

MODELING VOLATILITY OF US CONSUMER CREDIT SERIES Ellis Heath Harley Langdale, Jr. College of Business Administration Valdosta State University 1500 N. Patterson Street Valdosta, GA 31698 ABSTRACT Consumer

MODELING VOLATILITY OF US CONSUMER CREDIT SERIES Ellis Heath Harley Langdale, Jr. College of Business Administration Valdosta State University 1500 N. Patterson Street Valdosta, GA 31698 ABSTRACT Consumer

Global Impact Funding Trust

Global Impact Funding Trust 1 Welcome to GIFT. One of the great dividends of financial success is the pleasure of giving back to your community, in support of a social cause, to benefit those in need or

Global Impact Funding Trust 1 Welcome to GIFT. One of the great dividends of financial success is the pleasure of giving back to your community, in support of a social cause, to benefit those in need or

1) The Effect of Recent Tax Changes on Taxable Income

The Effect of Recent Tax Changes on Taxable Income") 1) The Effect of Recent Tax Changes on Taxable Income In the most recent issue of the Journal of Policy Analysis and Management, Bradley Heim published a paper called The Effect of Recent Tax Changes on

1) The Effect of Recent Tax Changes on Taxable Income In the most recent issue of the Journal of Policy Analysis and Management, Bradley Heim published a paper called The Effect of Recent Tax Changes on

Volume 29, Issue 2. A note on finance, inflation, and economic growth

Volume 29, Issue 2 A note on finance, inflation, and economic growth Daniel Giedeman Grand Valley State University Ryan Compton University of Manitoba Abstract This paper examines the impact of inflation

Volume 29, Issue 2 A note on finance, inflation, and economic growth Daniel Giedeman Grand Valley State University Ryan Compton University of Manitoba Abstract This paper examines the impact of inflation

Public Expenditure on Capital Formation and Private Sector Productivity Growth: Evidence

ISSN 2029-4581. ORGANIZATIONS AND MARKETS IN EMERGING ECONOMIES, 2012, VOL. 3, No. 1(5) Public Expenditure on Capital Formation and Private Sector Productivity Growth: Evidence from and the Euro Area Jolanta

ISSN 2029-4581. ORGANIZATIONS AND MARKETS IN EMERGING ECONOMIES, 2012, VOL. 3, No. 1(5) Public Expenditure on Capital Formation and Private Sector Productivity Growth: Evidence from and the Euro Area Jolanta

Budgetary Trade-offs Between Social Services, Development Services and Defense* in Jordan

Journal of Administrative Sciences And Economics Vol. 8-1997 Budgetary Trade-offs Between Social Services, Development Services and Defense* in Jordan Dr. Qasem Hamouri Dr. Basem Hamouri Mr. Mohamad Al-Bitar

Journal of Administrative Sciences And Economics Vol. 8-1997 Budgetary Trade-offs Between Social Services, Development Services and Defense* in Jordan Dr. Qasem Hamouri Dr. Basem Hamouri Mr. Mohamad Al-Bitar

Do School District Bond Guarantee Programs Matter?

Providence College DigitalCommons@Providence Economics Student Papers Economics 12-2013 Do School District Bond Guarantee Programs Matter? Michael Cirrotti Providence College Follow this and additional

Providence College DigitalCommons@Providence Economics Student Papers Economics 12-2013 Do School District Bond Guarantee Programs Matter? Michael Cirrotti Providence College Follow this and additional

THE IMPACT OF MINIMUM WAGE INCREASES BETWEEN 2007 AND 2009 ON TEEN EMPLOYMENT

THE IMPACT OF MINIMUM WAGE INCREASES BETWEEN 2007 AND 2009 ON TEEN EMPLOYMENT A Thesis submitted to the Faculty of the Graduate School of Arts and Sciences of Georgetown University in partial fulfillment

THE IMPACT OF MINIMUM WAGE INCREASES BETWEEN 2007 AND 2009 ON TEEN EMPLOYMENT A Thesis submitted to the Faculty of the Graduate School of Arts and Sciences of Georgetown University in partial fulfillment

Average Earnings and Long-Term Mortality: Evidence from Administrative Data

American Economic Review: Papers & Proceedings 2009, 99:2, 133 138 http://www.aeaweb.org/articles.php?doi=10.1257/aer.99.2.133 Average Earnings and Long-Term Mortality: Evidence from Administrative Data

American Economic Review: Papers & Proceedings 2009, 99:2, 133 138 http://www.aeaweb.org/articles.php?doi=10.1257/aer.99.2.133 Average Earnings and Long-Term Mortality: Evidence from Administrative Data

An Analysis of Spain s Sovereign Debt Risk Premium

The Park Place Economist Volume 22 Issue 1 Article 15 2014 An Analysis of Spain s Sovereign Debt Risk Premium Tim Mackey '14 Illinois Wesleyan University, tmackey@iwu.edu Recommended Citation Mackey, Tim

The Park Place Economist Volume 22 Issue 1 Article 15 2014 An Analysis of Spain s Sovereign Debt Risk Premium Tim Mackey '14 Illinois Wesleyan University, tmackey@iwu.edu Recommended Citation Mackey, Tim

Exchange Rate Exposure and Firm-Specific Factors: Evidence from Turkey

Journal of Economic and Social Research 7(2), 35-46 Exchange Rate Exposure and Firm-Specific Factors: Evidence from Turkey Mehmet Nihat Solakoglu * Abstract: This study examines the relationship between

Journal of Economic and Social Research 7(2), 35-46 Exchange Rate Exposure and Firm-Specific Factors: Evidence from Turkey Mehmet Nihat Solakoglu * Abstract: This study examines the relationship between

Relationship between Consumer Price Index (CPI) and Government Bonds

and Government Bonds") MPRA Munich Personal RePEc Archive Relationship between Consumer Price Index (CPI) and Government Bonds Muhammad Imtiaz Subhani Iqra University Research Centre (IURC), Iqra university Main Campus Karachi,

MPRA Munich Personal RePEc Archive Relationship between Consumer Price Index (CPI) and Government Bonds Muhammad Imtiaz Subhani Iqra University Research Centre (IURC), Iqra university Main Campus Karachi,

Geoffrey M.B. Tootell

Geoffrey M.B. Tootell Economist, Federal Reserve Bank of Boston. The author thanks Fed colleagues Lynn Broune, Eric Rosengren, and Joe Peek for helpful comments. T he results of the study of discrimination

Geoffrey M.B. Tootell Economist, Federal Reserve Bank of Boston. The author thanks Fed colleagues Lynn Broune, Eric Rosengren, and Joe Peek for helpful comments. T he results of the study of discrimination

Any Willing Provider Legislation: A Cost Driver?

Any Willing Provider Legislation: A Cost Driver? Michael Allgrunn, Ph.D. Assistant Professor of Economics University of South Dakota Brandon Haiar, M.B.A. June 2012 Prepared for the South Dakota Association

Any Willing Provider Legislation: A Cost Driver? Michael Allgrunn, Ph.D. Assistant Professor of Economics University of South Dakota Brandon Haiar, M.B.A. June 2012 Prepared for the South Dakota Association

Augmenting Okun s Law with Earnings and the Unemployment Puzzle of 2011

Augmenting Okun s Law with Earnings and the Unemployment Puzzle of 2011 Kurt G. Lunsford University of Wisconsin Madison January 2013 Abstract I propose an augmented version of Okun s law that regresses

Augmenting Okun s Law with Earnings and the Unemployment Puzzle of 2011 Kurt G. Lunsford University of Wisconsin Madison January 2013 Abstract I propose an augmented version of Okun s law that regresses

The Impact of State and Local Government Spending on Charitable Giving in the United States. Lynn Vandendriessche

The Impact of State and Local Government Spending on Charitable Giving in the United States Lynn Vandendriessche Professor Peter Arcidiacono, Faculty Advisor Professor Michelle Connolly, Faculty Advisor

The Impact of State and Local Government Spending on Charitable Giving in the United States Lynn Vandendriessche Professor Peter Arcidiacono, Faculty Advisor Professor Michelle Connolly, Faculty Advisor

Empirical evaluation of the 2001 and 2003 tax cut policies on personal consumption: Long Run impact

Georgia State University From the SelectedWorks of Fatoumata Diarrassouba Spring March 29, 2013 Empirical evaluation of the 2001 and 2003 tax cut policies on personal consumption: Long Run impact Fatoumata

Georgia State University From the SelectedWorks of Fatoumata Diarrassouba Spring March 29, 2013 Empirical evaluation of the 2001 and 2003 tax cut policies on personal consumption: Long Run impact Fatoumata

A Study of the Effects of Budget-Balancing Practices and Fiscal Policies on State Fiscal Health

University of Kentucky UKnowledge MPA/MPP Capstone Projects Martin School of Public Policy and Administration 2010 A Study of the Effects of Budget-Balancing Practices and Fiscal Policies on State Fiscal

University of Kentucky UKnowledge MPA/MPP Capstone Projects Martin School of Public Policy and Administration 2010 A Study of the Effects of Budget-Balancing Practices and Fiscal Policies on State Fiscal

Advanced Topic 7: Exchange Rate Determination IV

Advanced Topic 7: Exchange Rate Determination IV John E. Floyd University of Toronto May 10, 2013 Our major task here is to look at the evidence regarding the effects of unanticipated money shocks on real

Advanced Topic 7: Exchange Rate Determination IV John E. Floyd University of Toronto May 10, 2013 Our major task here is to look at the evidence regarding the effects of unanticipated money shocks on real

INTRODUCTION: ECONOMIC ANALYSIS OF TAX EXPENDITURES

National Tax Journal, June 2011, 64 (2, Part 2), 451 458 Introduction INTRODUCTION: ECONOMIC ANALYSIS OF TAX EXPENDITURES James M. Poterba Many economists and policy analysts argue that broadening the

National Tax Journal, June 2011, 64 (2, Part 2), 451 458 Introduction INTRODUCTION: ECONOMIC ANALYSIS OF TAX EXPENDITURES James M. Poterba Many economists and policy analysts argue that broadening the

NBER WORKING PAPER SERIES TAX EVASION AND CAPITAL GAINS TAXATION. James M. Poterba. Working Paper No. 2119

NBER WORKING PAPER SERIES TAX EVASION AND CAPITAL GAINS TAXATION James M. Poterba Working Paper No. 2119 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 January 1987

NBER WORKING PAPER SERIES TAX EVASION AND CAPITAL GAINS TAXATION James M. Poterba Working Paper No. 2119 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 January 1987

Further Test on Stock Liquidity Risk With a Relative Measure

International Journal of Education and Research Vol. 1 No. 3 March 2013 Further Test on Stock Liquidity Risk With a Relative Measure David Oima* David Sande** Benjamin Ombok*** Abstract Negative relationship

International Journal of Education and Research Vol. 1 No. 3 March 2013 Further Test on Stock Liquidity Risk With a Relative Measure David Oima* David Sande** Benjamin Ombok*** Abstract Negative relationship

The End of State Income Convergence

Chapter 2 The End of State Income Convergence The convergence thesis offers a broad and plausible explanation for the widely different rates of state economic development that chapter 1 describes. The

Chapter 2 The End of State Income Convergence The convergence thesis offers a broad and plausible explanation for the widely different rates of state economic development that chapter 1 describes. The

Credit Risk: Contract Characteristics for Success

Credit Risk: Characteristics for Success By James P. Murtagh, PhD Equipment leasing companies need reliable information to assess the default risk on lease contracts. Lenders have historically built independent

Credit Risk: Characteristics for Success By James P. Murtagh, PhD Equipment leasing companies need reliable information to assess the default risk on lease contracts. Lenders have historically built independent

Description of the Sample and Limitations of the Data

Section 3 Description of the Sample and Limitations of the Data T his section describes the 2008 Corporate sample design, sample selection, data capture, data cleaning, and data completion. The techniques

Section 3 Description of the Sample and Limitations of the Data T his section describes the 2008 Corporate sample design, sample selection, data capture, data cleaning, and data completion. The techniques

Appendix B for Acemoglu-Guerrieri Capital Deepening and Non-Balanced Economic Growth (Not for Publication)

") Appendix B for Acemoglu-Guerrieri Capital Deepening and Non-Balanced Economic Growth (Not for Publication) National Income Product Accounts Data All the data used in the paper refer to US data and are

Appendix B for Acemoglu-Guerrieri Capital Deepening and Non-Balanced Economic Growth (Not for Publication) National Income Product Accounts Data All the data used in the paper refer to US data and are

A Reply to Roberto Perotti s "Expectations and Fiscal Policy: An Empirical Investigation"

A Reply to Roberto Perotti s "Expectations and Fiscal Policy: An Empirical Investigation" Valerie A. Ramey University of California, San Diego and NBER June 30, 2011 Abstract This brief note challenges

A Reply to Roberto Perotti s "Expectations and Fiscal Policy: An Empirical Investigation" Valerie A. Ramey University of California, San Diego and NBER June 30, 2011 Abstract This brief note challenges

Business Cycles II: Theories

Macroeconomic Policy Class Notes Business Cycles II: Theories Revised: December 5, 2011 Latest version available at www.fperri.net/teaching/macropolicy.f11htm In class we have explored at length the main

Macroeconomic Policy Class Notes Business Cycles II: Theories Revised: December 5, 2011 Latest version available at www.fperri.net/teaching/macropolicy.f11htm In class we have explored at length the main

Online Appendix for Liquidity Constraints and Consumer Bankruptcy: Evidence from Tax Rebates

Online Appendix for Liquidity Constraints and Consumer Bankruptcy: Evidence from Tax Rebates Tal Gross Matthew J. Notowidigdo Jialan Wang January 2013 1 Alternative Standard Errors In this section we discuss

Online Appendix for Liquidity Constraints and Consumer Bankruptcy: Evidence from Tax Rebates Tal Gross Matthew J. Notowidigdo Jialan Wang January 2013 1 Alternative Standard Errors In this section we discuss

Guide to The Philanthropy Outlook Model 2019 & Marts & Lundy. Indiana University Lilly Family School of Philanthropy RESEARCHED AND

Guide to The Philanthropy Outlook Model 2019 & 2020 P R E S E N T E D BY Marts & Lundy RESEARCHED AND W R I T T E N BY Indiana University Lilly Family School of Philanthropy JA N UA RY 2019 Variable Definitions

Guide to The Philanthropy Outlook Model 2019 & 2020 P R E S E N T E D BY Marts & Lundy RESEARCHED AND W R I T T E N BY Indiana University Lilly Family School of Philanthropy JA N UA RY 2019 Variable Definitions

An Empirical Examination of Traditional Equity Valuation Models: The case of the Athens Stock Exchange

European Research Studies, Volume 7, Issue (1-) 004 An Empirical Examination of Traditional Equity Valuation Models: The case of the Athens Stock Exchange By G. A. Karathanassis*, S. N. Spilioti** Abstract

European Research Studies, Volume 7, Issue (1-) 004 An Empirical Examination of Traditional Equity Valuation Models: The case of the Athens Stock Exchange By G. A. Karathanassis*, S. N. Spilioti** Abstract

Deal Stats Transaction Survey

January 2016 - June 2016 Summary Report Prepared by Brady Cary and Robert Regis, ASA of Columbia Financial Advisors, Inc. 12/31/16 A Publication of the AM&AA Market Research Committee Market Research Committee

January 2016 - June 2016 Summary Report Prepared by Brady Cary and Robert Regis, ASA of Columbia Financial Advisors, Inc. 12/31/16 A Publication of the AM&AA Market Research Committee Market Research Committee

Effects of Estate Tax Reform on Charitable Giving

Tax Policy Issues and Options URBAN BROOKINGS TAX POLICY CENTER No. 6, July 2003 Effects of Estate Tax Reform on Charitable Giving Jon M. Bakija and William G. Gale Estate tax repeal would reduce annual

Tax Policy Issues and Options URBAN BROOKINGS TAX POLICY CENTER No. 6, July 2003 Effects of Estate Tax Reform on Charitable Giving Jon M. Bakija and William G. Gale Estate tax repeal would reduce annual

Jaime Frade Dr. Niu Interest rate modeling

Interest rate modeling Abstract In this paper, three models were used to forecast short term interest rates for the 3 month LIBOR. Each of the models, regression time series, GARCH, and Cox, Ingersoll,

Interest rate modeling Abstract In this paper, three models were used to forecast short term interest rates for the 3 month LIBOR. Each of the models, regression time series, GARCH, and Cox, Ingersoll,

R-Star Wars: The Phantom Menace

R-Star Wars: The Phantom Menace James Bullard President and CEO 34th Annual National Association for Business Economics (NABE) Economic Policy Conference Feb. 26, 2018 Washington, D.C. Any opinions expressed

R-Star Wars: The Phantom Menace James Bullard President and CEO 34th Annual National Association for Business Economics (NABE) Economic Policy Conference Feb. 26, 2018 Washington, D.C. Any opinions expressed

MERCATUS ON POLICY. The Charitable Contributions Deduction. Jeremy Horpedahl. January 2016

MERCATUS ON POLICY The Charitable Contributions Deduction Jeremy Horpedahl January 2016 Jeremy Horpedahl is an assistant professor of economics at the University of Central Arkansas, where he teaches principles

MERCATUS ON POLICY The Charitable Contributions Deduction Jeremy Horpedahl January 2016 Jeremy Horpedahl is an assistant professor of economics at the University of Central Arkansas, where he teaches principles

Tentative Lessons from the Recent Disinflationary Effort

PHILLIP CAGAN Columbia University WILLIAM FELLNER American Enterprise Institute Tentative Lessons from the Recent Disinflationary Effort DISINFLATION, after an extended period of inflationary demand policy

PHILLIP CAGAN Columbia University WILLIAM FELLNER American Enterprise Institute Tentative Lessons from the Recent Disinflationary Effort DISINFLATION, after an extended period of inflationary demand policy

Pension fund investment: Impact of the liability structure on equity allocation

Pension fund investment: Impact of the liability structure on equity allocation Author: Tim Bücker University of Twente P.O. Box 217, 7500AE Enschede The Netherlands t.bucker@student.utwente.nl In this

Pension fund investment: Impact of the liability structure on equity allocation Author: Tim Bücker University of Twente P.O. Box 217, 7500AE Enschede The Netherlands t.bucker@student.utwente.nl In this

Access to Retirement Savings and its Effects on Labor Supply Decisions

Access to Retirement Savings and its Effects on Labor Supply Decisions Yan Lau Reed College May 2015 IZA / RIETI Workshop Motivation My Question: How are labor supply decisions affected by access of Retirement

Access to Retirement Savings and its Effects on Labor Supply Decisions Yan Lau Reed College May 2015 IZA / RIETI Workshop Motivation My Question: How are labor supply decisions affected by access of Retirement

Elasticity of the Lexington-Fayette Urban County Government Tax Structure

University of Kentucky UKnowledge MPA/MPP Capstone Projects Martin School of Public Policy and Administration 2006 Elasticity of the Lexington-Fayette Urban County Government Tax Structure Bradly Settle

University of Kentucky UKnowledge MPA/MPP Capstone Projects Martin School of Public Policy and Administration 2006 Elasticity of the Lexington-Fayette Urban County Government Tax Structure Bradly Settle

Impact of Weekdays on the Return Rate of Stock Price Index: Evidence from the Stock Exchange of Thailand

Journal of Finance and Accounting 2018; 6(1): 35-41 http://www.sciencepublishinggroup.com/j/jfa doi: 10.11648/j.jfa.20180601.15 ISSN: 2330-7331 (Print); ISSN: 2330-7323 (Online) Impact of Weekdays on the

Journal of Finance and Accounting 2018; 6(1): 35-41 http://www.sciencepublishinggroup.com/j/jfa doi: 10.11648/j.jfa.20180601.15 ISSN: 2330-7331 (Print); ISSN: 2330-7323 (Online) Impact of Weekdays on the

THE DETERMINANTS OF BANK DEPOSIT VARIABILITY: A DEVELOPING COUNTRY CASE

Economics and Sociology Occasional Paper No. 1692 THE DETERMINANTS OF BANK DEPOSIT VARIABILITY: A DEVELOPING COUNTRY CASE by Richard L. Meyer Shirin N azma and Carlos E. Cuevas February, 1990 Agricultural

Economics and Sociology Occasional Paper No. 1692 THE DETERMINANTS OF BANK DEPOSIT VARIABILITY: A DEVELOPING COUNTRY CASE by Richard L. Meyer Shirin N azma and Carlos E. Cuevas February, 1990 Agricultural

Contents TWELFTH ANNUAL REPORT CARD ON CHARITABLE GIVING FOR METRO MILWAUKEE

TWELFTH ANNUAL REPORT CARD ON CHARITABLE GIVING FOR METRO MILWAUKEE November 2008 PUBLISHED BY GREATER MILWAUKEE FOUNDATION SPONSORS Donors Forum of Wisconsin The Faye McBeath Foundation United Way of

TWELFTH ANNUAL REPORT CARD ON CHARITABLE GIVING FOR METRO MILWAUKEE November 2008 PUBLISHED BY GREATER MILWAUKEE FOUNDATION SPONSORS Donors Forum of Wisconsin The Faye McBeath Foundation United Way of

Chapter 5 Mean Reversion in Indian Commodities Market

Chapter 5 Mean Reversion in Indian Commodities Market 5.1 Introduction Mean reversion is defined as the tendency for a stochastic process to remain near, or tend to return over time to a long-run average

Chapter 5 Mean Reversion in Indian Commodities Market 5.1 Introduction Mean reversion is defined as the tendency for a stochastic process to remain near, or tend to return over time to a long-run average

An Analysis of Potential Tax Incentives to Increase Charitable Giving in Puerto Rico

THE URBAN INSTITUTE An Analysis of Potential Tax Incentives to Increase Charitable Giving in Puerto Rico January 2010 Elizabeth T. Boris, Joseph J. Cordes, Mauricio Soto, and Eric J. Toder Improved incentives

THE URBAN INSTITUTE An Analysis of Potential Tax Incentives to Increase Charitable Giving in Puerto Rico January 2010 Elizabeth T. Boris, Joseph J. Cordes, Mauricio Soto, and Eric J. Toder Improved incentives

Credit Risk: Contract Characteristics for Success

Credit Risk: Contract Characteristics for Success About The Equipment Leasing and Finance Foundation The Equipment Leasing and Finance Foundation is a 501c3 non-profit organization that provides vision

Credit Risk: Contract Characteristics for Success About The Equipment Leasing and Finance Foundation The Equipment Leasing and Finance Foundation is a 501c3 non-profit organization that provides vision

Mortality of Beneficiaries of Charitable Gift Annuities 1 Donald F. Behan and Bryan K. Clontz