Welcome to: FNSBKG404 Carry Out Business Activity and Instalment Activity Statement Tasks

|

|

|

- Silvester Blankenship

- 5 years ago

- Views:

Transcription

1 Welcome to: FNSBKG404 Carry Out Business Activity and Instalment Activity Statement Tasks Lisa Genna Monday Room H G.09-6:00 pm to 9:00 pm 1

2 Lesson 3 FNSBKG404 Carry Out Business Activity and Instalment Activity Statement Tasks 2

3 Overview 1. The Instalment Activity Statement (IAS) 2. What is PAYG? 3. The PAYG withholding system 4. The PAYG instalment system (next week) 3

4 1. The Instalment Ac0vity Statement (IAS) 4

5 Types of Ac/vity Statements There are two (2) types of activity statements: The Business Activity Statement (BAS), which must be completed by those taxpayers who are required to report GST in that activity statement period. The Instalment Activity Statement (IAS), which applies to those not registered for GST, taxpayers with investment income and GST-registered businesses that have to report GST on a quarterly basis and other obligations on a monthly basis. 5

6 Who should use an IAS? The IAS mainly applies to: Individual taxpayers with investment income (e.g. rental, interest or dividend income) and/or business income. Trustees with business income. Businesses (including companies) not registered for GST (i.e. they have an annual GST turnover below the minimum GST registration threshold of $75,000). Some GST-registered businesses on a monthly reporting cycle for PAYG (e.g. the business must complete a quarterly BAS to report GST and a monthly IAS to report other items for the months in between). 6

amounts withheld from payments to others (lesson 3) PAYG instalments (lesson 4) Fringe Benefits Tax (FBT) instalments")

7 The Instalment Ac/vity Statement (IAS) An Instalment Activity Statement (IAS) is a single form the taxpayer completes and returns to the ATO to report the following obligations and entitlements: Pay-As-You-Go (PAYG) amounts withheld from payments to others (lesson 3) PAYG instalments (lesson 4) Fringe Benefits Tax (FBT) instalments (lesson 7) 7

8 Preparing an IAS The ATO sends the IAS to taxpayers before they need to lodge it. The statement is personalised, with some parts already completed to save time and effort. Each activity statement has a unique document identification number, which is shown on the front of the IAS. The document ID is used by the ATO s systems to identify the activity statement during processing. 8

9 Types of Instalment Ac/vity Statements There are four (4) different types of Instalment Activity Statements which are used for different purposes. Types of IAS IAS N IAS I IAS B IAS J Used by Taxpayers who have elected to report and pay an annual PAYG income tax instalment Taxpayers with PAYG tax withheld only (quarterly or monthly) Taxpayers with a PAYG income tax instalment obligation only Taxpayers with PAYG income tax instalment, PAYG tax withheld and FBT obligations 9

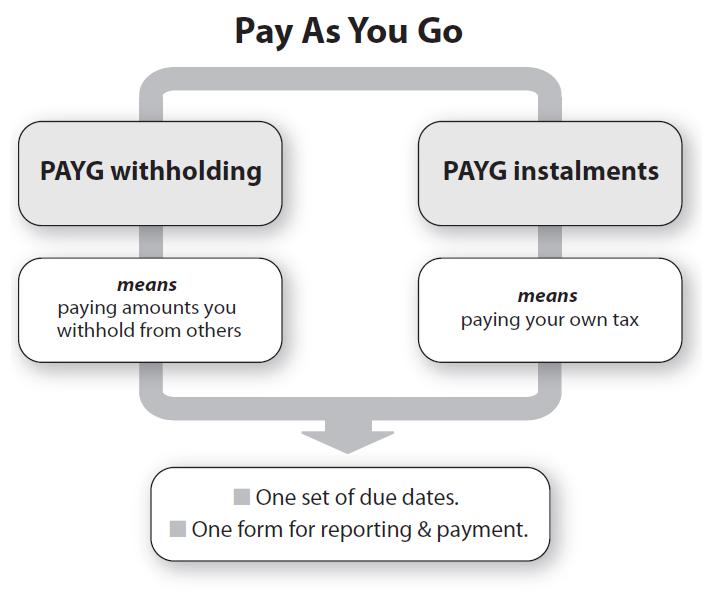

10 IAS Type N 10

11 IAS Type N 11

12 IAS Type I 12

13 IAS Type B 13

14 IAS Type J 14

15 2. What is PAYG? 15

16 What is PAYG? PAYG is an acronym for: Pay-As-You-Go 16

17 17

18 What is PAYG? PAYG is a single, integrated system for reporting and paying: à amounts withheld (PAYG withholding system) à tax on business and investment income (PAYG instalment system) The PAYG system brings withholding obligations and income tax instalments together into one system. The system was introduced in an attempt to simplify the overall tax collection system: One set of rules One set of payment dates One form to fill in 18

19 3. The PAYG Withholding System 19

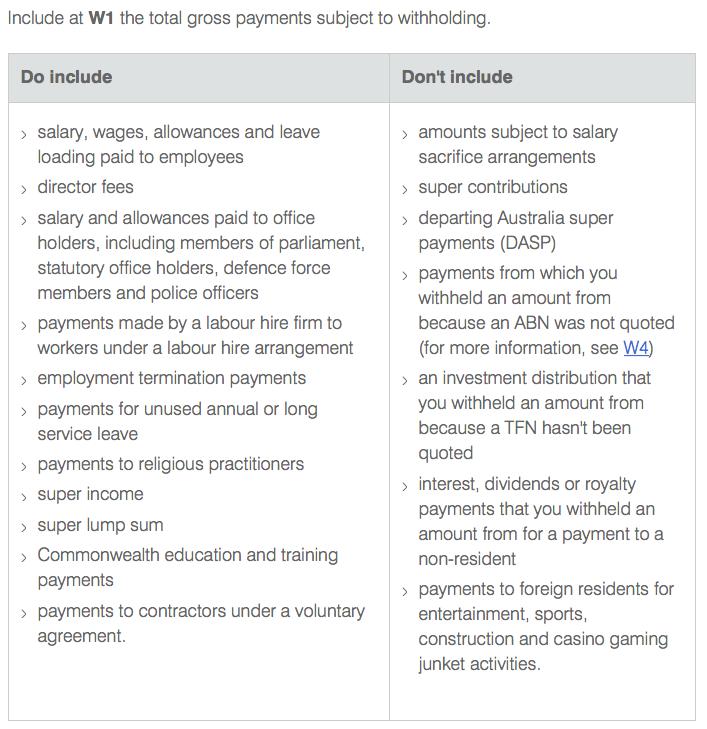

20 The PAYG withholding system The PAYG withholding system provides a single set of rules for businesses to collect income tax on behalf of the ATO. Withholding is the process by which amounts are deducted from income payments made to employees and others directly involved in the business. Amounts reported on Activity Statements include: W1 Total salary, wages and other payments. W2 Amount withheld from payments shown at W1. W4 Amount withheld where no ABN is quoted. W3 Other amounts withheld (excluding any amount shown at W2 or W4) 20

21 The PAYG withholding system Taxpayers must apply for registration for PAYG withholding before withholding any tax from payments to others. This can be done on the initial business registration with the ABR or, if you already have an ABN for your business: By phone By lodging a paper form Through your registered tax agent or BAS agent Online through the ATO s website 21

22 Taxpayers are required to complete the PAYG tax withheld section on each Activity Statement lodged to the ATO. Withheld amounts have to be sent to the ATO by the due date specified on the Activity Statement. Below is a sample of the PAYG tax withheld section of an Activity Statement. Note: all of the following items appear on both an IAS (Types I and J) and a BAS. 22

23 Withholding payment dates The dates on which withholding payments are remitted to the ATO depends on the annual amount of withholding. Note; Many non-business PAYG taxpayers (such as self-funded retirees) and some businesses will have the option of making an annual instalment. 23

24 Size of withholder Small withholders Have annual PAYG withholding amounts of up to $25,000 Frequency of payment and payment date Quarterly An amount deducted in any quarter is generally payable on the 28th of the month following the end of that quarter. The payment dates are: 28 October 28 February 28 April 28 July Medium withholders Have annual PAYG withholding amounts between $25,001 and $1 million Large withholders Have annual PAYG withholding amounts > $1 million (or is part of a group of companies that has withheld > $1 million in a previous income year) Monthly An amount deducted in any month is generally payable on the 21st day of the following month. Twice a week An amount deducted in any period commencing Saturday and ending Tuesday is payable on the following Monday. An amount deducted in any period commencing Wednesday and ending Friday is payable on the following Thursday. 24

25 Employer obliga/ons An employer s obligations regarding withholding tax include: 1.Registering for PAYG withholding 2. Notifying the ATO and paying amounts withheld using an activity statement (or electronically in the case of large withholders). 3. Providing a Payment Summary to payees at the end of each financial year. 4. Sending TFN declarations to the ATO. 5.Reporting (at least) annually to the ATO on all withholdings. 25

26 Payment Summaries At the end of each financial year, the employer who has withheld tax payments from its employees must prepare a Payment Summary for each payee (worker). The Payment Summary must be given to the payee (worker) by 14 July (or earlier if requested). The employer must keep a copy of each Payment Summary for their records. 26

27 Payment Summaries Amongst other things, the Payment Summary shows the total payments made to and the amount of tax withheld from each worker during the financial year ending 30 June. 27

28 28

29 What is the difference between GROSS wages and NET wages? 29

30 NET PAY (amount paid to employee) = GROSS WAGES - DEDUCTIONS 30

+ Incentives e.g. bonuses or commission 31")

31 Includes: Wages earned for period Gross wages (based on the hours worked and rate per hour) + Allowances e.g. overtime, sick or holiday pay (incl. annual leave loading at 17.5% of 4 weeks wages if applicable) + Incentives e.g. bonuses or commission 31

party e.g. ATO.")

32 Deduc/ons Includes: - Tax (i.e. PAYG withholding tax) - Other statutory and employee approved deductions Deductions are withheld in a liability account until paid to the relevant 3 rd (external) party e.g. ATO. 32

33 W1 Total salary, wages and other payments Include at W1 total gross payments that usually require PAYG tax to be withheld These mostly include: Payments to employees, company directors and office holders. Payments under a labour hire arrangement. Payments under voluntary agreements. Click on the following link to see a comprehensive list what you should and should not include at W1 on an activity statement: 33

34 34

35 35

36 W1 Total salary, wages and other payments > Payments made by a labour hire firm to workers under a labour hire arrangement 36

37 Carrying on a labour hire business If the taxpayer s business only (or partially) involves arranging for people to perform work or services for clients, the taxpayer is deemed under the PAYG legislation to be carrying on a labour-hire business. This rule does not apply if such an activity is incidental to other business activities. Key questions: What is a labour hire business? What are the implications of carrying on a labour hire business with regards to reporting PAYG amounts withheld? 37

38 Carrying on a labour hire business Labour hire arrangements typically involve at least two contracts: 1. One with a user of labour i.e. the client (e.g. Prime Constructions) and the labour hire firm (e.g. Workfast). 2. Another with the labour hire firm (e.g. Workfast) and the worker (e.g. Bob). 38

39 Carrying on a labour hire business 39

40 Carrying on a labour hire business The LHB contracts with the worker and pays the worker. Under the labour hire provisions, the LHB must deduct tax from any payments made to these workers for performing a service for its clients. There is no contract between the worker and the client. The client pays the LHB for the service provided. If the LHB is required to be registered for GST, GST will be payable on the LHB s supply to the end user i.e. the client. GST is not payable on the supply made by the worker to the LHB. Therefore, the worker cannot claim input tax credits for any GST paid for goods or services bought and used in performing the work or services provided to the client of the LHB. 40

41 What about payments to sub- contractors? Payments made by a contractor to a sub-contractor are not for the performance of work directly for a client and are therefore not subject to withholding under the labour hire provisions. 41

42 W1 Total salary, wages and other payments > Payments to contractors under a voluntary agreement 42

43 Employee or contractor? Use the ATO website decision tool htm&mnu=42711&mfp=001/003 43

44 Payments made under voluntary agreements A Voluntary Agreement is a written agreement between a business and a worker to bring work payments into the PAYG withholding system. To create a Voluntary Agreement the worker, as an individual, must: 1. Have an Australian Business Number (ABN). 2. Not be subject to any other PAYG withholding. 44

45 Payments made under voluntary agreements What does a Voluntary Agreement mean for the business? The business has to withhold tax from payments it makes to the contractor and send amounts withheld to the ATO. What does a Voluntary Agreement mean for the contractor? The contractor does not have to pay PAYG instalments for income they receive from the client their tax will be paid as they go. 45

46 Payments made under voluntary agreements The client has to withhold tax from payments it makes to the contractor and send amounts withheld to the ATO Contractor does work for client and invoices client for work done Contractor / Worker (payee) Business / Client (payer) Client pays contractor for work done 46

47 Voluntary agreements: How much to withhold? The payer has to withhold tax based on an agreed instalment amount. This is either a rate notified to the contractor by the ATO via the BAS or a flat rate of 20%. 47

48 Voluntary agreements : GST implica/ons 1. Voluntary Agreements usually fall outside the GST system, so when the contractor invoices the client, the amount will not include GST. 2. However, the contractor can still claim GST input tax credits on other business purchases. 48

49 Employment Termina/on Payments, workers compensa/on and leave payments Under the PAYG withholding system, an employer may have to withhold amounts from these payments. Separate calculation tables are available to calculate amounts withheld. The tax tables take into account personal income tax rates including, Medicare Levy, HELP and other rebates. Where the payee does not give the payer a TFN, tax must be withheld at 49% (resident employee) or 47% (foreign resident employee). 49

50 Large withholders Large withholder only need to complete field W1 on their Activity Statement. This type of taxpayer must NOT complete fields W2, W3, W4, W5 or 4 in the Summary Section of their Activity Statement because they would have electronically remitted a number of withholding amounts throughout the reporting period and therefore the ATO already has this information. 50

51 51

52 W2 Amounts withheld from payments shown at W1 Withholding for the purposes of W2 refers to amounts deducted from income payments made to workers and includes: 1. Payments made to employees, company directors and office holders. 2. Payments made under a labour hire agreement. 3. Payments made under voluntary agreement. 52

53 How much to withhold? Withholdings from payments made to employees and others directly involved in a business should be in accordance with tax tables published by the ATO. There are various tax tables published and take into account personal income tax rates, including the Medicare Levy, HELP debt and tax offsets. Tax tables are provided by the ATO for payments made on a weekly, fortnightly, monthly and quarterly basis. 53

54 How much to withhold? Tax offsets If an employee answered YES to Questions 9 and/or 10 on the TFN Declaration form, then reduce the amount withheld from the employee s wage (refer to applicable tax table). 54

55 How much to withhold? HELP debts If an employee has a HELP debt, additional tax may need to be withheld. HELP is designed to assist students by offering four (4) types of loans. The Commonwealth Government pays the debt on behalf of the student and is repaid through the taxation system when the student begins earning a specified level of income. 55

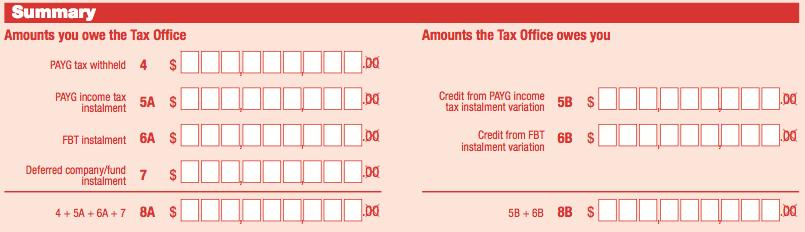

56 How much to withhold? HELP debts If an employee answered YES to Question 11 on the TFN Declaration form, then increase the amount withheld from the employee s wage (refer to applicable tax table). Refer to additional reading 56

57 57

58 W4 Amounts withheld where no ABN quoted If a business does not quote an ABN on their invoice, the business that receives the goods or services is required to withhold tax from the payment made to the supplier. Tax must be withheld if: You are a business making a payment for goods or services and the supplier of the goods or services has not quoted their ABN. You think the ABN quoted on an invoice may be false or you think it is not the real ABN of the supplier. The supplier has made a written, signed statement that the supply is of a private or domestic nature or that it relates to a hobby, but you have reasonable grounds to think the statement is false. 58

59 How much to withhold? The amount withheld from the payment should be at the top marginal rate plus the Medicare Levy and Temporary Budget Repair Levy (i.e. currently 49%). The supplier can claim this withheld amount as a credit on their next income tax return. 59

60 How much to withhold? Exceptions to the rule Tax does not have to withheld from a payment made to a supplier EVEN IF NO ABN HAS BEEN QUOTED if: 1. The recipient is an individual and the payment is wholly private or domestic in nature. 2. The payment is not > $75 (not including GST). 3. The entire payment is exempt income of the supplier (for example, if the supplier is a charity). 4. You are already withholding tax from the payment because you are an investment body paying an amount for which no TFN has been quoted. 60

61 61

62 W3 Other amounts withheld At W3, the taxpayer must include amounts (if any) withheld from any of the following payments: ü Interest, dividends, unit trust or other investment distributions made, where the person paid has not completed a TFN declaration form or otherwise provided the taxpayer with a TFN (includes a non-resident). ü Interest, dividends or royalty payments made to a non-resident. ü Any Departing Australia Superannuation Payments (DASP) made. ü Any payments made to foreign residents, for any of the following: Entertainment and sport activities Construction and related activities Arranging casino gaming junket activities 62

63 Non- resident withholding Tax must be withheld from interest, unfranked dividends and royalties paid to an individual, company, partnership, trust or superannuation fund that is not a resident of Australia. Payment type % to be withheld from the gross amount Interest 10% Unfranked dividends (or the unfranked component of a dividend) 30% Royalties 30% *Franked dividends have already had tax withheld from them when paid which is why they are not subject to further withholding 63

64 What is the difference between a franked dividend and an unfranked dividend? 64

65 65

66 W5 Total amounts withheld Include at W5 the total of W2 + W4 + W3 This amount needs to be copied to field 4 of the Summary Section of the activity statement* Do not include W1 in the W5 total *If the activity statement only asks you to report PAYG withholding, the activity statement won t have a summary section. The total withholding will be reported at field 9 of the Payment or Refund section of the activity statement. 66

67 67

68 Working out how much tax to withhold from an employee s gross pay Refer to CLASS ACTIVITY You can use the following ATO calculator to work out how much to withhold from an employee s gross pay: anchor=twc&anchor=twc#twc/questions Click here for a list of all the different types of tax tables: 68

Complete all assigned")

69 This week s homework Read the relevant chapter(s) (ref. DELIVERY & ASSESSMENT GUIDE) Complete all assigned activities.

70 You are now ready to start the next lesson on: PAYG Instalments 70

Welcome to: FNSBKG404 Carry Out Business Activity and Instalment Activity Statement Tasks

Welcome to: FNSBKG404 Carry Out Business Activity and Instalment Activity Statement Tasks Lisa Genna lisa.genna2@tafensw.edu.au Monday Room H G.09-6:00 pm to 9:00 pm Lesson 2 Part 1 TFN and ABN Requirements

Welcome to: FNSBKG404 Carry Out Business Activity and Instalment Activity Statement Tasks Lisa Genna lisa.genna2@tafensw.edu.au Monday Room H G.09-6:00 pm to 9:00 pm Lesson 2 Part 1 TFN and ABN Requirements

PAYG withholding. Guide for employers and businesses. What employers and businesses need to know to meet their PAYG withholding obligations

Guide for employers and businesses PAYG withholding What employers and businesses need to know to meet their PAYG withholding obligations For more information visit www.ato.gov.au NAT 8075-02.2009 Our

Guide for employers and businesses PAYG withholding What employers and businesses need to know to meet their PAYG withholding obligations For more information visit www.ato.gov.au NAT 8075-02.2009 Our

Welcome to: FNSBKG404 Carry Out Business Activity and Instalment Activity Statement Tasks

Welcome to: FNSBKG404 Carry Out Business Activity and Instalment Activity Statement Tasks Lisa Genna lisa.genna2@tafensw.edu.au Monday - 6:00 pm to 9:00 pm Class introductions J Class admin. Student Detail

Welcome to: FNSBKG404 Carry Out Business Activity and Instalment Activity Statement Tasks Lisa Genna lisa.genna2@tafensw.edu.au Monday - 6:00 pm to 9:00 pm Class introductions J Class admin. Student Detail

Withholding declaration upwards variation

Instructions and form for taxpayers Withholding declaration upwards variation WHO SHOULD COMPLETE THIS DECLARATION? You should complete this declaration if you want to: n increase the rate or amount withheld

Instructions and form for taxpayers Withholding declaration upwards variation WHO SHOULD COMPLETE THIS DECLARATION? You should complete this declaration if you want to: n increase the rate or amount withheld

INSTALMENT ACTIVITY STATEMENTS (IAS)

") Chapter 5: BAS & IAS INSTALMENT ACTIVITY STATEMENTS (IAS) What is an Instalment Activity Statement? Individual taxpayers, trustees with business income, and businesses not registered for use the Instalment

Chapter 5: BAS & IAS INSTALMENT ACTIVITY STATEMENTS (IAS) What is an Instalment Activity Statement? Individual taxpayers, trustees with business income, and businesses not registered for use the Instalment

Instructions for completing the PAYG withholding variation application 2013

Complete the application if you want to vary the rate or amount of pay as you go (PAYG) tax withheld from payments made to you for the year ending 30 June 2013. You must also complete the PAYG withholding

Complete the application if you want to vary the rate or amount of pay as you go (PAYG) tax withheld from payments made to you for the year ending 30 June 2013. You must also complete the PAYG withholding

What you need to report through Single Touch Payroll

Page 1 of 26 What you need to report through Single Touch Payroll Print entire document https://www.ato.gov.au/business/single-touch-payroll/in-detail/what-youneed-to-report-through-single-touch-payroll/

Page 1 of 26 What you need to report through Single Touch Payroll Print entire document https://www.ato.gov.au/business/single-touch-payroll/in-detail/what-youneed-to-report-through-single-touch-payroll/

Common BAS errors. General.

Page 1 of 8 Common BAS errors General Including wages and superannuation contributions as purchases at G11 Including wages and superannuation contributions as purchases at G11 Lodgment of blank forms Lodgment

Page 1 of 8 Common BAS errors General Including wages and superannuation contributions as purchases at G11 Including wages and superannuation contributions as purchases at G11 Lodgment of blank forms Lodgment

Tax file number declaration

Instructions and form for taxpayers Individuals Tax file number declaration The information you provide in this declaration will enable your payer to work out how much tax to withhold from payments made

Instructions and form for taxpayers Individuals Tax file number declaration The information you provide in this declaration will enable your payer to work out how much tax to withhold from payments made

Monthly withholding table

Pay as you go (PAYG) withholding NAT 1007 withholding table Includes withholding amounts calculated in accordance with the rules contained in Weekly tax table including instructions for calculating monthly

Pay as you go (PAYG) withholding NAT 1007 withholding table Includes withholding amounts calculated in accordance with the rules contained in Weekly tax table including instructions for calculating monthly

SA-HELP. Information for

SA-HELP Information for 2012 www.goingtouni.gov.au You must read this booklet before signing the commonwealth assistance form below SA-HELP form USING THIS BOOKLET As you read through, you will notice

SA-HELP Information for 2012 www.goingtouni.gov.au You must read this booklet before signing the commonwealth assistance form below SA-HELP form USING THIS BOOKLET As you read through, you will notice

Medicare levy variation declaration

Instructions and form for taxpayers Medicare levy variation declaration WHO SHOULD COMPLETE THIS DECLARATION? You should complete this declaration if you want to: n increase the amount withheld from payments

Instructions and form for taxpayers Medicare levy variation declaration WHO SHOULD COMPLETE THIS DECLARATION? You should complete this declaration if you want to: n increase the amount withheld from payments

Monthly tax table. Schedule 4 Pay as you go (PAYG) withholding NAT 1007

withholding NAT 1007") Schedule 4 Pay as you go (PAYG) withholding NAT 1007 tax table Incorporating Medicare levy and temporary flood and cyclone reconstruction levy (flood levy) FOR PAYMENTS MADE ON OR AFTER 1 JULY 2011 TO

Schedule 4 Pay as you go (PAYG) withholding NAT 1007 tax table Incorporating Medicare levy and temporary flood and cyclone reconstruction levy (flood levy) FOR PAYMENTS MADE ON OR AFTER 1 JULY 2011 TO

Income Tax Basics 2012 Day 2. Overview...1

Contents Overview...1 1. The self-assessment system...1 1.1 Periods of review...2 2. Preparing the business return...3 2.1 Accounting records vs. tax records...3 2.2 Process for completing the business

Contents Overview...1 1. The self-assessment system...1 1.1 Periods of review...2 2. Preparing the business return...3 2.1 Accounting records vs. tax records...3 2.2 Process for completing the business

Superannuation changes

This year s Federal Budget includes the most significant changes to Australia s superannuation system since 2007, plus tax initiatives to support low income earners and small businesses. On Tuesday 3 May,

This year s Federal Budget includes the most significant changes to Australia s superannuation system since 2007, plus tax initiatives to support low income earners and small businesses. On Tuesday 3 May,

Tax file number declaration

Instructions and form for taxpayers Tax file number declaration Information you provide in this declaration will allow your payer to This is not a TFN application form. ato.gov.au/tfn Terms we use When

Instructions and form for taxpayers Tax file number declaration Information you provide in this declaration will allow your payer to This is not a TFN application form. ato.gov.au/tfn Terms we use When

Superannuation changes

This year s Federal Budget includes the most significant changes to Australia s superannuation system since 2007, plus tax initiatives to support low income earners small businesses. On Tuesday 3 May,

This year s Federal Budget includes the most significant changes to Australia s superannuation system since 2007, plus tax initiatives to support low income earners small businesses. On Tuesday 3 May,

THINGS TO DO BEFORE 30 JUNE

16 June 2017, Volume 7, Page 1 Our Business Website Staff Update Fees Things to do before 30 June Taxation & Accounting Checklists Audit Checklists ATO My Deductions App Office Hours: 8:30am to 5:00pm

16 June 2017, Volume 7, Page 1 Our Business Website Staff Update Fees Things to do before 30 June Taxation & Accounting Checklists Audit Checklists ATO My Deductions App Office Hours: 8:30am to 5:00pm

Maximise year end opportunities and minimise risks

Maximise year end opportunities and minimise risks Key dates Pre 30 June 2014 Actions Review shareholder loan accounts and make minimum loan repayments (may need to declare dividends) Pay all superannuation

Maximise year end opportunities and minimise risks Key dates Pre 30 June 2014 Actions Review shareholder loan accounts and make minimum loan repayments (may need to declare dividends) Pay all superannuation

YOUR GUIDE TO PARTICIPATING IN THE FORTESCUE SALARY SACRIFICE SHARE PLAN

YOUR GUIDE TO PARTICIPATING IN THE FORTESCUE SALARY SACRIFICE SHARE PLAN Contents Your Deferred Salary Sacrifice Plan 03 Benefits and risks 04 Participation 05 Understanding the Plan 06 Tax guide 11 Definitions

YOUR GUIDE TO PARTICIPATING IN THE FORTESCUE SALARY SACRIFICE SHARE PLAN Contents Your Deferred Salary Sacrifice Plan 03 Benefits and risks 04 Participation 05 Understanding the Plan 06 Tax guide 11 Definitions

Weekly tax table. Schedule 2 Pay as you go (PAYG) withholding NAT Including instructions for calculating monthly and quarterly withholding

withholding NAT Including instructions for calculating monthly and quarterly withholding") Schedule 2 Pay as you go (PAYG) withholding NAT 1005 tax table Including instructions for calculating monthly and quarterly withholding FOR PAYMENTS MADE ON OR AFTER 1 JULY 2012 From 1 July 2012, the temporary

Schedule 2 Pay as you go (PAYG) withholding NAT 1005 tax table Including instructions for calculating monthly and quarterly withholding FOR PAYMENTS MADE ON OR AFTER 1 JULY 2012 From 1 July 2012, the temporary

Company Tax Return Preparation Checklist 2017

COMPANY TAX RETURN PREPARATION CHECKLIST 2017 This checklist should be completed in conjunction with the preparation of tax reconciliation return workpapers. The checklist provides a general list of major

COMPANY TAX RETURN PREPARATION CHECKLIST 2017 This checklist should be completed in conjunction with the preparation of tax reconciliation return workpapers. The checklist provides a general list of major

Important EOFY actions

Important EOFY actions Reducing your tax exposure, maximising the opportunities available to you, and reducing your risk of an audit by the regulators is in your best interests. With the end of the financial

Important EOFY actions Reducing your tax exposure, maximising the opportunities available to you, and reducing your risk of an audit by the regulators is in your best interests. With the end of the financial

TAX GUIDE You should use this guide if. You may wish to give this guide to your accountant or tax agent

TAX GUIDE 2016 17 2016 17 Tax Return Information Statement Guide This guide will help you to complete your 2016 17 tax return using your 2016 17 Tax Return Information Statement from Colonial First State

TAX GUIDE 2016 17 2016 17 Tax Return Information Statement Guide This guide will help you to complete your 2016 17 tax return using your 2016 17 Tax Return Information Statement from Colonial First State

GUIDE TO YOUR TAX STATEMENT FY2016/17. Daintree Capital Guide to your tax statement

GUIDE TO YOUR TAX STATEMENT FY2016/17 1 ABOUT THIS GUIDE If you have an investment in the Daintree Core Income Trust you can use this guide to help you complete your Individual tax return 2017 (tax return).

GUIDE TO YOUR TAX STATEMENT FY2016/17 1 ABOUT THIS GUIDE If you have an investment in the Daintree Core Income Trust you can use this guide to help you complete your Individual tax return 2017 (tax return).

ABN and ACNC Registration Policy and Procedures for Private Schools

ABN and ACNC Registration Policy and Procedures for Private Schools Title ABN and ACNC Registration Policy and Procedures for Private Schools Creation Date Version Last Revised Reformatted 31 March 2014

ABN and ACNC Registration Policy and Procedures for Private Schools Title ABN and ACNC Registration Policy and Procedures for Private Schools Creation Date Version Last Revised Reformatted 31 March 2014

2017 Take Home Quiz #1

Employee/Independent Contractor 1. To satisfy the Reasonable Basis test and treat a worker as an independent contractor, a company can rely on all of the following methods EXCEPT: A. a private letter ruling

Employee/Independent Contractor 1. To satisfy the Reasonable Basis test and treat a worker as an independent contractor, a company can rely on all of the following methods EXCEPT: A. a private letter ruling

Taxable payments annual report

Instructions and form for reporting of taxable payments Taxable payments annual report WHAT THIS FM IS F This form is the annual report to provide details of taxable payments made to businesses in specified

Instructions and form for reporting of taxable payments Taxable payments annual report WHAT THIS FM IS F This form is the annual report to provide details of taxable payments made to businesses in specified

Personal Income Tax Return Year End Questionnaire 2016

Personal Income Tax Return Year End Questionnaire 2016 Client: Date: To assist us in preparing your income tax return, please use this questionnaire as a checklist when you compile your information. With

Personal Income Tax Return Year End Questionnaire 2016 Client: Date: To assist us in preparing your income tax return, please use this questionnaire as a checklist when you compile your information. With

2016/17 Individual Income Tax Return Checklist

2016/17 Individual Income Tax Return Checklist To assist us in preparing your income tax return, please use this checklist when you compile your information. Completing the checklist can take some time

2016/17 Individual Income Tax Return Checklist To assist us in preparing your income tax return, please use this checklist when you compile your information. Completing the checklist can take some time

INDIVIDUAL TAX CHECKLIST 2013

FULL NAME: HOME ADDRESS: _ POSTAL ADDRESS: TELEPHONE: (H) (W) (M) EMAIL: FAX: OCCUPATION: BANK ACCOUNT DETAILS From 1 July 2013 the ATO won t be issuing cheque refunds. All refunds will need to be banked

FULL NAME: HOME ADDRESS: _ POSTAL ADDRESS: TELEPHONE: (H) (W) (M) EMAIL: FAX: OCCUPATION: BANK ACCOUNT DETAILS From 1 July 2013 the ATO won t be issuing cheque refunds. All refunds will need to be banked

Taxation of Australian nationals working overseas

nationals working overseas 2 Contents Introduction 1 1. Will I still have to pay tax in Australia while I work overseas? 2 1.1 The Australian tax system 2 1.2 Impact of overseas assignment 2 2. Will I

nationals working overseas 2 Contents Introduction 1 1. Will I still have to pay tax in Australia while I work overseas? 2 1.1 The Australian tax system 2 1.2 Impact of overseas assignment 2 2. Will I

Statement of formulas for calculating Higher Education Loan Program (HELP) component

component") Schedule 14 Pay as you go (PAYG) withholding NAT 2335 Statement of formulas for calculating Higher Education Loan Program (HELP) component Including coefficients for calculating weekly withholding amounts

Schedule 14 Pay as you go (PAYG) withholding NAT 2335 Statement of formulas for calculating Higher Education Loan Program (HELP) component Including coefficients for calculating weekly withholding amounts

GOODMAN CHARTERED ACCOUNTANTS INDIVIDUAL TAX CHECKLIST 2011 Income Tax Return

Name: Occupation: Residential Address: Postal Address: Telephone: (H) (W) (M) Email: Fax: INCOME 1 Salary or wage Include PAYG payment summaries. 2 Allowances, earnings, tips, director s fees, etc. Provide

Name: Occupation: Residential Address: Postal Address: Telephone: (H) (W) (M) Email: Fax: INCOME 1 Salary or wage Include PAYG payment summaries. 2 Allowances, earnings, tips, director s fees, etc. Provide

THE GOODS & SERVICES TAX (GST) SYSTEM

SYSTEM") AUSTRALIAN BUSINESS NUMBER (ABN) THE GOODS & SERVICES TAX (GST) SYSTEM The Australian Business Number (ABN) is the identifying number that businesses use when dealing with other businesses. The ABN is

AUSTRALIAN BUSINESS NUMBER (ABN) THE GOODS & SERVICES TAX (GST) SYSTEM The Australian Business Number (ABN) is the identifying number that businesses use when dealing with other businesses. The ABN is

GENERAL TAX ISSUES. represents. income and gains

GENERAL TAX ISSUES Income tax represents approximately 70 percent of the total tax revenue of the Australian Federal Government Income tax represents approximately 70% of the total tax revenue of the Australian

GENERAL TAX ISSUES Income tax represents approximately 70 percent of the total tax revenue of the Australian Federal Government Income tax represents approximately 70% of the total tax revenue of the Australian

PRACTICE UPDATE - JUNE 2017

PRACTICE UPDATE - JUNE 2017 Reduction in FBT Rate from 1st April 2017 Planned Changes to GST on Low Value Imported Goods Company tax cuts pass the senate with amendments Costs of Travelling in relation

PRACTICE UPDATE - JUNE 2017 Reduction in FBT Rate from 1st April 2017 Planned Changes to GST on Low Value Imported Goods Company tax cuts pass the senate with amendments Costs of Travelling in relation

Income Tax Basics 2008 Day 2

Introduction...1 1. What is the aim and structure of this seminar?...1 2. The self-assessment system...1 2.1 Complexity of returns has increased...2 3. Introduction to completing the business return...2

Introduction...1 1. What is the aim and structure of this seminar?...1 2. The self-assessment system...1 2.1 Complexity of returns has increased...2 3. Introduction to completing the business return...2

TaxWise Business News February 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TaxWise Business News February 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TaxWise Business News February 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

AMMA STATEMENT GUIDE A Guide to your Cromwell Property Group (ASX:CMW) 30 June 2018 AMMA Statement

30 June 2018 AMMA Statement") AMMA STATEMENT GUIDE A Guide to your Cromwell Property Group (ASX:CMW) 30 June 2018 AMMA Statement The information in this Guide has been prepared to assist Australian resident individual holders of Cromwell

AMMA STATEMENT GUIDE A Guide to your Cromwell Property Group (ASX:CMW) 30 June 2018 AMMA Statement The information in this Guide has been prepared to assist Australian resident individual holders of Cromwell

Guardian Investments - Budget 2016: What you need to know

Guardian Investments - Budget 2016: What you need to know This year s Federal Budget includes the most significant changes to Australia s superannuation system since 2007, plus tax initiatives to support

Guardian Investments - Budget 2016: What you need to know This year s Federal Budget includes the most significant changes to Australia s superannuation system since 2007, plus tax initiatives to support

Sample only. Change of registration details

Change of registration details Use this form to change the following registration details for the entity: entity name or trading name postal, email or business address authorised contact person associates

Change of registration details Use this form to change the following registration details for the entity: entity name or trading name postal, email or business address authorised contact person associates

TaxWise Business News February 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

Superannuation guarantee

Guide for employers Superannuation guarantee How to meet your super obligations The super guarantee system affects most employers in Australia so it is important you understand your obligations. Your tax

Guide for employers Superannuation guarantee How to meet your super obligations The super guarantee system affects most employers in Australia so it is important you understand your obligations. Your tax

ATO audits, yes. this year for real

ATO audits, yes. this year for real The financial year ends on THURSDAY 30 th June and so it s timely to reassess your financial position as we commence the 2016/2017 financial year. To assist you in preparing

ATO audits, yes. this year for real The financial year ends on THURSDAY 30 th June and so it s timely to reassess your financial position as we commence the 2016/2017 financial year. To assist you in preparing

Guide to Your Annual Tax Statement

July 2015 Guide to Your Annual Tax Statement To help you understand your annual tax statement and complete your tax return for the 2014/2015 financial year. How to use this guide This guide is designed

July 2015 Guide to Your Annual Tax Statement To help you understand your annual tax statement and complete your tax return for the 2014/2015 financial year. How to use this guide This guide is designed

ABN and ACNC Registration Policy and Procedures for Congregations, Presbyteries and Synod Boards

ABN and ACNC Registration Policy and Procedures for Congregations, Presbyteries and Synod Boards Title ABN and ACNC Registration Policy and Procedures for Congregations, Presbyteries and Synod Boards Creation

ABN and ACNC Registration Policy and Procedures for Congregations, Presbyteries and Synod Boards Title ABN and ACNC Registration Policy and Procedures for Congregations, Presbyteries and Synod Boards Creation

Only an entity that is carrying on an enterprise may register. Therefore, it is important that these terms are clearly understood.

2. MANAGING THE GST DO YOU NEED TO REGISTER Whether or not you are in the GST system depends upon whether you are registered or required to be registered. A registration system is necessary for the administration

2. MANAGING THE GST DO YOU NEED TO REGISTER Whether or not you are in the GST system depends upon whether you are registered or required to be registered. A registration system is necessary for the administration

Income Tax Basics 2007 Day 2. Introduction...1

Introduction...1 1. What is the aim and structure of this seminar?...1 2. The self-assessment system...1 2.1 Complexity of returns has increased...2 3. Introduction to completing the business return...2

Introduction...1 1. What is the aim and structure of this seminar?...1 2. The self-assessment system...1 2.1 Complexity of returns has increased...2 3. Introduction to completing the business return...2

INSTITUTE OF CERTIFIED BOOKKEEPERS

Level 27 Rialto South Tower 525 Collins Street MELBOURNE 3000 Tel: 1300 85 61 81 Fax: 1300 85 73 93 info@icb.org.au www.icb.org.au INSTITUTE OF CERTIFIED BOOKKEEPERS BOOKKEEPERS RESOURCE KIT Version August

Level 27 Rialto South Tower 525 Collins Street MELBOURNE 3000 Tel: 1300 85 61 81 Fax: 1300 85 73 93 info@icb.org.au www.icb.org.au INSTITUTE OF CERTIFIED BOOKKEEPERS BOOKKEEPERS RESOURCE KIT Version August

Independent Contractor or Employee?

Independent Contractor or Employee? Introduction It is not always clear whether a worker is an employee or a contractor. This Guide is designed to assist small, medium and large sized businesses operating

Independent Contractor or Employee? Introduction It is not always clear whether a worker is an employee or a contractor. This Guide is designed to assist small, medium and large sized businesses operating

Personal services income schedule 2012

Instructions for companies, partnerships and trusts Personal services income schedule 2012 Schedule and explanatory notes for 1 July 2011 30 June 2012 For more information visit www.ato.gov.au NAT 3421-06.2012

Instructions for companies, partnerships and trusts Personal services income schedule 2012 Schedule and explanatory notes for 1 July 2011 30 June 2012 For more information visit www.ato.gov.au NAT 3421-06.2012

Tax return for individuals July 2011 to 30 June 2012

Use Individual tax return instructions 2012 to fill in this tax return n Print clearly using a black pen only n Use BLOCK LETTERS and print one character per box S M I T H S T Tax return for individuals

Use Individual tax return instructions 2012 to fill in this tax return n Print clearly using a black pen only n Use BLOCK LETTERS and print one character per box S M I T H S T Tax return for individuals

ClearView Managed Investments

ClearView Managed Investments Individual Tax Return Instructions Help Guide 2018 This tax guide will help you to complete your tax return using your ClearView Managed Investments Annual Tax Statement for

ClearView Managed Investments Individual Tax Return Instructions Help Guide 2018 This tax guide will help you to complete your tax return using your ClearView Managed Investments Annual Tax Statement for

Tax basics. Tax basics for business operators. The basics:

Main topics - Tax basics - How tax works for different business structures - Summary of business taxes and payments - Claiming deductions for business expenses - Why keep good business records? - Contacts

Main topics - Tax basics - How tax works for different business structures - Summary of business taxes and payments - Claiming deductions for business expenses - Why keep good business records? - Contacts

Northern Beaches College Business Services Apprentice to Business Owner Program (A to B Program) Structure & Legal s;

Structure & Legal s;") Structure & Legal s; The four main types of business structures commonly used by small businesses are: Sole trader: an individual trading on their own Partnership: an association of people or entities

Structure & Legal s; The four main types of business structures commonly used by small businesses are: Sole trader: an individual trading on their own Partnership: an association of people or entities

A GUIDE TO YOUR STOCKLAND 30 JUNE 2007 ANNUAL TAX STATEMENT

A GUIDE TO YOUR STOCKLAND 30 JUNE 2007 ANNUAL TAX STATEMENT Stockland Corporation Limited ACN 000 181 733 Stockland Trust Management Limited ABN 86 001 900 741 AFSL No. 241190 As Responsible Entity for

A GUIDE TO YOUR STOCKLAND 30 JUNE 2007 ANNUAL TAX STATEMENT Stockland Corporation Limited ACN 000 181 733 Stockland Trust Management Limited ABN 86 001 900 741 AFSL No. 241190 As Responsible Entity for

TAXATION GUIDE INDEX. ! Statement by Supplier No ABN quoted. 13! PAYG payment summary No ABN quoted PAYG WITHHOLDING NO ABN QUOTED - SECTION 1

INDEX FORMS PAGE! Statement by Supplier No ABN quoted. 13! PAYG payment summary No ABN quoted... 14 PAYG WITHHOLDING NO ABN QUOTED - SECTION 1! Overview 2! Flowchart... 4! Procedures. 5! Guest Speakers.

INDEX FORMS PAGE! Statement by Supplier No ABN quoted. 13! PAYG payment summary No ABN quoted... 14 PAYG WITHHOLDING NO ABN QUOTED - SECTION 1! Overview 2! Flowchart... 4! Procedures. 5! Guest Speakers.

Taxable payments reporting for government entities

Taxable payments reporting for government entities Presented by Leassa Armstrong, Australian Taxation Office 22July 2016 Objective of today s presentation > The aim of today s session is to provide you

Taxable payments reporting for government entities Presented by Leassa Armstrong, Australian Taxation Office 22July 2016 Objective of today s presentation > The aim of today s session is to provide you

For BT Panorama Investments (SMSF account holders)

") Panorama Tax Policy Guide For the year ended 30 June 2017 Tax Guide For BT Panorama Investments (SMSF account holders) Part 1 General Information and Panorama Tax Policy Guide Part 2 Completing the Fund

Panorama Tax Policy Guide For the year ended 30 June 2017 Tax Guide For BT Panorama Investments (SMSF account holders) Part 1 General Information and Panorama Tax Policy Guide Part 2 Completing the Fund

April The small business $20,000 instant asset write-off. Time to go shopping! The $20,000 instant asset write-off explained

The small business $20,000 instant asset write-off. Time to go shopping! The small business write-off threshold of $20,000 was extended to 30 June 2018 and is available to all small businesses with an

The small business $20,000 instant asset write-off. Time to go shopping! The small business write-off threshold of $20,000 was extended to 30 June 2018 and is available to all small businesses with an

Guide to your Annual Tax Statement

Guide to your Annual Tax Statement Please Note This guide aims to assist individual taxpayers in completing their tax return for the 2010/11 income tax year It contains basic information about the treatment

Guide to your Annual Tax Statement Please Note This guide aims to assist individual taxpayers in completing their tax return for the 2010/11 income tax year It contains basic information about the treatment

2013/2014 BUDGET & ATO ITEMS

pics 21 June 2013, Volume 3, Page 1 INDIVIDUALS AND FAMILIES Taxable Income Threshold and Marginal Tax Rates The following rates for 2013/14 apply from 1 July 2013: Resident thresholds $ Marginal rates

pics 21 June 2013, Volume 3, Page 1 INDIVIDUALS AND FAMILIES Taxable Income Threshold and Marginal Tax Rates The following rates for 2013/14 apply from 1 July 2013: Resident thresholds $ Marginal rates

ABN and ACNC Registration Policy and Procedures for Parish Missions

ABN and ACNC Registration Policy and Procedures for Parish Missions Title ABN and ACNC Registration Policy and Procedures for Parish Missions Creation Date Version Last Revised Reformatted 31 March 2014

ABN and ACNC Registration Policy and Procedures for Parish Missions Title ABN and ACNC Registration Policy and Procedures for Parish Missions Creation Date Version Last Revised Reformatted 31 March 2014

Contact your VET provider or the VET FEE HELP enquiry line on , if you do not understand anything in this booklet.

VET FEE HELP Information Booklet 2010 Are you planning to undertake study in the Vocational Education and Training (VET) sector, in one or more of the following courses: a diploma; an advanced diploma;

VET FEE HELP Information Booklet 2010 Are you planning to undertake study in the Vocational Education and Training (VET) sector, in one or more of the following courses: a diploma; an advanced diploma;

Guide to Your Annual Tax Statement

July 2017 Guide to Your Annual Tax Statement A guide to completing your tax return for the 2016/2017 financial year (FY17) How to use this guide If you are an Australian resident individual taxpayer, this

July 2017 Guide to Your Annual Tax Statement A guide to completing your tax return for the 2016/2017 financial year (FY17) How to use this guide If you are an Australian resident individual taxpayer, this

2018 Company, Trust or Partnership Tax Return Checklist

Experienced Advice, from people who care 2018 Company, Trust or Partnership Tax Return Checklist Name of taxpayer/s: Address: Preferred contact no.: Preferred email: Financial institution details for tax

Experienced Advice, from people who care 2018 Company, Trust or Partnership Tax Return Checklist Name of taxpayer/s: Address: Preferred contact no.: Preferred email: Financial institution details for tax

CERTIFICATE IV. FNSTPB401 Complete business activity and instalment activity statements USER GUIDE. sample for review

CERTIFICATE IV FNSTPB401 Complete business activity and instalment activity statements USER GUIDE All Rights Reserved Copyright 2018 OfficeLink Learning Version 18.6 Xero No part of the contents of this

CERTIFICATE IV FNSTPB401 Complete business activity and instalment activity statements USER GUIDE All Rights Reserved Copyright 2018 OfficeLink Learning Version 18.6 Xero No part of the contents of this

n Print clearly, using a BLACK pen only. n Place X in ALL applicable boxes.

Self-managed superannuation fund annual return 2013 WHO SHOULD COMPLETE THIS ANNUAL RETURN? Only self-managed superannuation funds (SMSFs) can complete this annual return All other funds must complete

Self-managed superannuation fund annual return 2013 WHO SHOULD COMPLETE THIS ANNUAL RETURN? Only self-managed superannuation funds (SMSFs) can complete this annual return All other funds must complete

Small Business Entity Rules

End of Year Tax Planning Checklist 2012 Small Business Entity Rules Small Business Entities - the small business entity rules apply to a sole trader, partnership, company or trust which has a group turnover

End of Year Tax Planning Checklist 2012 Small Business Entity Rules Small Business Entities - the small business entity rules apply to a sole trader, partnership, company or trust which has a group turnover

IOOF tax guide. Guide to your tax statement

IOOF tax guide Guide to your tax statement July 2017 About this guide If you have an investment in any of our Trusts you can use this guide to help you complete your Tax return for Individuals 2017 (tax

IOOF tax guide Guide to your tax statement July 2017 About this guide If you have an investment in any of our Trusts you can use this guide to help you complete your Tax return for Individuals 2017 (tax

Superannuation Guarantee

Australian Taxation Office Superannuation Guarantee Instruction Guide and Statement Valid for all years up to and including 2002/2003 For those employers who have NOT paid the required amount of superannuation

Australian Taxation Office Superannuation Guarantee Instruction Guide and Statement Valid for all years up to and including 2002/2003 For those employers who have NOT paid the required amount of superannuation

Taxwise Individual News

Taxwise Individual News In this Issue... Medicare Levy Surcharge and Private Health Insurance Rebate Superannuation guarantee rate Super contributions caps Changes to superannuation excess concessional

Taxwise Individual News In this Issue... Medicare Levy Surcharge and Private Health Insurance Rebate Superannuation guarantee rate Super contributions caps Changes to superannuation excess concessional

Trust tax return 2014 (Summary)

") Trust tax return 2014 (Summary) Day Month Year to Day Month Year or specify period if part year or approved substitute period Trust information Tax file number (TFN) 31 777 459 Have you attached any 'other

Trust tax return 2014 (Summary) Day Month Year to Day Month Year or specify period if part year or approved substitute period Trust information Tax file number (TFN) 31 777 459 Have you attached any 'other

Tax Guide This guide is designed to help you understand your Fidante Partners tax statement and assist you with completing your 2018 Tax Return

Tax Guide 2018 This guide is designed to help you understand your Fidante Partners tax statement and assist you with completing your 2018 Tax Return Fidante Partners Limited (ABN 94 002 835 592) (AFSL

Tax Guide 2018 This guide is designed to help you understand your Fidante Partners tax statement and assist you with completing your 2018 Tax Return Fidante Partners Limited (ABN 94 002 835 592) (AFSL

January 2015 Newsletter

January 2015 Newsletter OUR SERVICES Did you know we can assist you in the following ways: Income Tax Income Tax Preparation Tax Planning Advice GST Business Activity Statements Superannuation Land Tax

January 2015 Newsletter OUR SERVICES Did you know we can assist you in the following ways: Income Tax Income Tax Preparation Tax Planning Advice GST Business Activity Statements Superannuation Land Tax

Record keeping for small business

Guide for small business operators Record keeping for small business Explains what business records you need to keep and outlines a basic record keeping system. For more information visit www.ato.gov.au

Guide for small business operators Record keeping for small business Explains what business records you need to keep and outlines a basic record keeping system. For more information visit www.ato.gov.au

Aspects of Financial Planning

Aspects of Financial Planning Taxation implications of overseas residency More and more of our clients are being given the opportunity to live and work overseas. Before you make the move, it is worthwhile

Aspects of Financial Planning Taxation implications of overseas residency More and more of our clients are being given the opportunity to live and work overseas. Before you make the move, it is worthwhile

Year end tax planning 2016 primary producers

Tax planning for primary producers Year end tax planning 2016 primary producers Important in 2015/16 Reduction to company tax rate for small business companies from 1 July 2015 From 1 July 2015, the income

Tax planning for primary producers Year end tax planning 2016 primary producers Important in 2015/16 Reduction to company tax rate for small business companies from 1 July 2015 From 1 July 2015, the income

JUNE 2017 NEWSLETTER. The 2017 financial year has seen the raft of changes, first introduced in the 2016 budget, legislated into law.

JUNE 2017 NEWSLETTER The 2017 financial year has seen the raft of changes, first introduced in the 2016 budget, legislated into law. Fortunately the 2017 budget did not announce any further large reform

JUNE 2017 NEWSLETTER The 2017 financial year has seen the raft of changes, first introduced in the 2016 budget, legislated into law. Fortunately the 2017 budget did not announce any further large reform

TaxWise. Business News February Focus on small business. What the ATO is seeing in the small business market. To do!

TaxWise Business News February 2019 Focus on small business What the ATO is seeing in the small business market On 2 November 2018, the Deputy Commissioner of Small Business, Deborah Jenkins, delivered

TaxWise Business News February 2019 Focus on small business What the ATO is seeing in the small business market On 2 November 2018, the Deputy Commissioner of Small Business, Deborah Jenkins, delivered

2018 Personal Tax Return Instructions

Page 1 of 6 2018 Personal Tax Return Instructions Your Last Name Your Given Names Postal Address Residential Address (if different to postal address) Your Occupation Work Phone No Mobile Phone No Home

Page 1 of 6 2018 Personal Tax Return Instructions Your Last Name Your Given Names Postal Address Residential Address (if different to postal address) Your Occupation Work Phone No Mobile Phone No Home

IMPORTANT REFERENCE CONTACT DETAILS

IMPORTANT REFERENCE CONTACT DETAILS Australian Taxation Office (ATO) Unless otherwise specified, all phone numbers listed here are available from 8.00am to 6.00pm, days, except public holidays. When you

IMPORTANT REFERENCE CONTACT DETAILS Australian Taxation Office (ATO) Unless otherwise specified, all phone numbers listed here are available from 8.00am to 6.00pm, days, except public holidays. When you

2018 INDIVIDUAL TAX RETURN - CHECKLIST

info@mwpartners.com.au 2018 INDIVIDUAL TAX RETURN - CHECKLIST Please use this document to collect all necessary information for the completion of your tax return for the financial year ended 30 June 2018.

info@mwpartners.com.au 2018 INDIVIDUAL TAX RETURN - CHECKLIST Please use this document to collect all necessary information for the completion of your tax return for the financial year ended 30 June 2018.

Guide to your tax statement FY2016/17

Guide to your tax statement FY2016/17 Important information This guide has been prepared by Perennial Investment Management Limited (PIML) ABN 13 108 747 637, AFS License No. 275101 as the responsible

Guide to your tax statement FY2016/17 Important information This guide has been prepared by Perennial Investment Management Limited (PIML) ABN 13 108 747 637, AFS License No. 275101 as the responsible

Tax on contributions. Non-concessional (after tax) contribution caps. Concessional (before tax) contributions

contribution caps. Concessional (before tax) contributions") This document summarises the main Federal Government taxes that apply to superannuation at the time of publication. For more information, contact Catholic Super on 1300 655 002 or the Australian Taxation

This document summarises the main Federal Government taxes that apply to superannuation at the time of publication. For more information, contact Catholic Super on 1300 655 002 or the Australian Taxation

Introduction 3. What is GST? 3. How GST works 3 What is the Tax fraction? 4. Types of supplies 4

1 P a g e CONTENTS Introduction 3 What is GST? 3 How GST works 3 What is the Tax fraction? 4 Types of supplies 4 supplies (SCREAM) 5 GST-free supplies 5 Input-taxed supplies 6 Implications for UCA congregations

1 P a g e CONTENTS Introduction 3 What is GST? 3 How GST works 3 What is the Tax fraction? 4 Types of supplies 4 supplies (SCREAM) 5 GST-free supplies 5 Input-taxed supplies 6 Implications for UCA congregations

How to complete the PAYG payment summary employment termination payment

Instructions for subject PAYG withholding payers How to complete the PAYG payment summary employment termination payment Instructions to help you complete PAYG payment summary employment termination payment

Instructions for subject PAYG withholding payers How to complete the PAYG payment summary employment termination payment Instructions to help you complete PAYG payment summary employment termination payment

Tax and Christmas party planning

Client Newsletter November 2017 Tax and Christmas party planning Christmas will be here before we know it, and the well-prepared business owner knows that a little tax planning can help make sure there

Client Newsletter November 2017 Tax and Christmas party planning Christmas will be here before we know it, and the well-prepared business owner knows that a little tax planning can help make sure there

Federal Budget

Federal Budget 2011-12 The bottom line The Federal Government handed down its budget for 2011-12 Tuesday night with an estimated cash deficit of $22.6 billion to be followed by an estimated cash surplus

Federal Budget 2011-12 The bottom line The Federal Government handed down its budget for 2011-12 Tuesday night with an estimated cash deficit of $22.6 billion to be followed by an estimated cash surplus

Single Touch Payroll

Single Touch Payroll Australian Taxation Office Payroll reporting Business implementation guide Date: 05/12/2017 This document and its attachments are Unclassified For further information or questions,

Single Touch Payroll Australian Taxation Office Payroll reporting Business implementation guide Date: 05/12/2017 This document and its attachments are Unclassified For further information or questions,

EOY Support Note # 5 Payment Summary Guide

EOY Support Note # 5 Payment Summary Guide The end of financial year deadline is fast approaching. This guide covers using MYOB to complete your PAYG payment summaries and other end of year payroll issues.

EOY Support Note # 5 Payment Summary Guide The end of financial year deadline is fast approaching. This guide covers using MYOB to complete your PAYG payment summaries and other end of year payroll issues.

Tax and the sharing economy

Information Newsletter - Tax & Super March 2017 Tax and the sharing economy The concept of a sharing economy has been around for long enough now to have had a very real impact on how we transact with each

Information Newsletter - Tax & Super March 2017 Tax and the sharing economy The concept of a sharing economy has been around for long enough now to have had a very real impact on how we transact with each

BUSINESS NEWS. Welcome to the June 2018 Edition Of our PBD Business Newsletter. I trust the following items are informative and interesting.

BUSINESS NEWS Welcome to the June 2018 Edition Of our PBD Business Newsletter I trust the following items are informative and interesting Regards, Pio De Corso ABN 26 645 374 624 15 Gorge Road, Paradise

BUSINESS NEWS Welcome to the June 2018 Edition Of our PBD Business Newsletter I trust the following items are informative and interesting Regards, Pio De Corso ABN 26 645 374 624 15 Gorge Road, Paradise

Microsoft Dynamics GP. GST and Australian Taxes

Microsoft Dynamics GP GST and Australian Taxes Copyright Copyright 2010 Microsoft. All rights reserved. Limitation of liability This document is provided as-is. Information and views expressed in this

Microsoft Dynamics GP GST and Australian Taxes Copyright Copyright 2010 Microsoft. All rights reserved. Limitation of liability This document is provided as-is. Information and views expressed in this

MEDICAL SERVICES GROUP 2017 Income Tax Information

MEDICAL SERVICES GROUP 2017 Income Tax Information Full Name Home Address Postal Address (if different from above) Occupation / Speciality Date of Birth Phone (W) Mobile Tax File Number Phone (H) Email

MEDICAL SERVICES GROUP 2017 Income Tax Information Full Name Home Address Postal Address (if different from above) Occupation / Speciality Date of Birth Phone (W) Mobile Tax File Number Phone (H) Email

Attribution Managed Investment Trust Member Annual (AMMA) Statement Guide 2018

Statement Guide 2018") Attribution Managed Investment Trust Member Annual (AMMA) Statement Guide 2018 This guide is designed to help you understand your Fidante Partners AMMA statement and assist you with completing your 2018

Attribution Managed Investment Trust Member Annual (AMMA) Statement Guide 2018 This guide is designed to help you understand your Fidante Partners AMMA statement and assist you with completing your 2018

THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA HOUSE OF REPRESENTATIVES

2016 THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA HOUSE OF REPRESENTATIVES INCOME TAX RATES AMENDMENT (WORKING HOLIDAY MAKER REFORM) BILL 2016 TREASURY LAWS AMENDMENT (WORKING HOLIDAY MAKER REFORM)

2016 THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA HOUSE OF REPRESENTATIVES INCOME TAX RATES AMENDMENT (WORKING HOLIDAY MAKER REFORM) BILL 2016 TREASURY LAWS AMENDMENT (WORKING HOLIDAY MAKER REFORM)