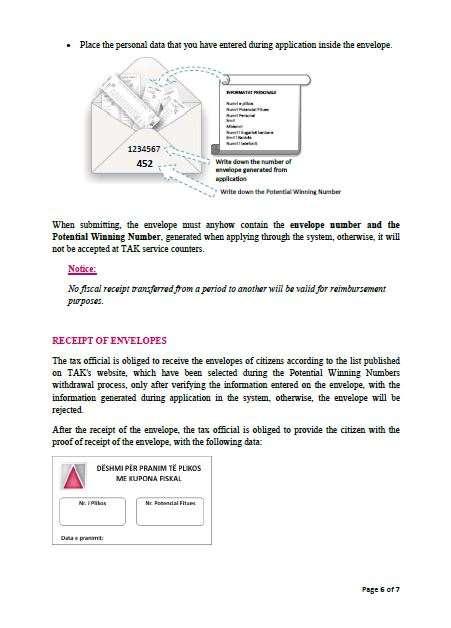

ANNUAL REPORT TAX ADMINISTRATION OF KOSOVO

|

|

|

- Earl Lambert

- 5 years ago

- Views:

Transcription

1

2 ANNUAL REPORT TAX ADMINISTRATION OF KOSOVO TAK`s Annual Report is elaborated pursuant to Article 8, paragraph 8.2 and 8.3 of the Law No. 03/L-222 on Tax Administration and Procedures. Article 8 - Reporting 1. The Director General shall furnish periodic reports of TAK s operations and performance to the Minister of Finance. 2. The Director General shall produce an annual report on the operations of TAK and deliver the report to the Minister of Finance and the Government of Kosovo, based in request within three (3) months after the end of each calendar year. 3. The annual report of TAK shall include: 3.1. details of the budget of TAK; 3.2. details of the number and level of staff of TAK; 3.3. details of the revenues collected by TAK showing details of the amount of revenue from each type of tax and each region and such other details as may be requested by the Minister of Finance; 3.4. estimates of the cost of collection for each type of tax revenue collected; 3.5. details of all tax liabilities cancelled under Article 43, including the names of the persons whose liability has been cancelled and the amount cancelled; 3.6. details of all initiations of proceedings for criminal tax offenses, where the investigation was commenced by the tax administration, including the name of each person who has been convicted, the sentence issued and the amounts of tax involved; and 3.7. information on the use of the powers authorized by Article 14 of this law, including the number and nature of any complaints about the use of those powers, but not including the names of the persons involved. page 2

3 TABLE OF CONTENT FOREWORD BY THE DIRECTOR GENERAL... 7 I. BACKGROUND BUDGET HUMAN RESOURCES TRAINING REVENUES STRUCTURE OF REVENUES REVENUES BY MONTH REVENUES BY TAX TYPES REVENUES BY MAIN TAX TYPES REVENUES IN LTD AND REGIONAL DIRECTORATES REVENUES GROUPED IN LTD AND REGIONAL DIRECTORATES TREATED VALUES COSTS PER 100 /UNIT ADDITIONAL TAX FROM AUDITS BY REGIONS NUMBER OF TAX AUDITS CARRIED OUT BY TAX INSPECTORS COMPLIANCE VISITS OUTCOMES FROM COMPLIANCE VISITS TAXPAYERS EDUCATION AND SERVICE REGISTRATION CALL CENTER FISCALIZED BUSINESSES IN LTD AND REGIONS REIMBURSEMENTS AND REFUNDS COMPARISON OF DEBT COLLECTION WITH LTD PLAN AND REGIONS GAMES OF CHANCE TAX INVESTIGATIONS AND INTELLIGENCE ACTIVITIES RELATED TO LEGAL INTERPRETATIONS AND REPRESENTATIONS COMPLAINTS OF TAXPAYERS INFORMATION TECHNOLOGY EXECUTIVE OFFICE INTERNATIONAL RELATIONS PARTICIPATION IN WORKING GROUPS PUBLIC RULINGS page 3

4 20.1. NO. 01/ TAXATION OF THE PENSIONS IN CASE OF WITHDRAWAL FROM THE KOSOVO PENSION SAVINGS TRUST (KPST) NO. 02/2017 INCENTIVES AND MOTIVATIONS FOR TAKING FISCAL RECEIPTS NO. 03/2017 APPLICATION OF THE REVERSE CHARGE FOR SERVICES PURCHASED OUTSIDE KOSOVO LIST OF BUSINESSES THAT HAVE BENEFITED VAT EXEMPTION ON IMPORT OF RAW MATERIALS AND IT EQUIPMENT page 4

5 TABLES Table 1: Budget spending in 2017, comparison with 2016 and Table 2: Number of employees by qualification, ethnicity and gender Table 3: Number of employees at TAK, Table 4: Training provided by local and international institutions, by number of training and participants: Table 5: Seminars and study visits/workshops Table 6: Taxpayers declaring turnover and payments, Table 7: Revenues collected by months Table 8: Revenues collected by tax type, compared with previous years Table 9: Revenues by year and main tax types Table 10: Revenues collected compared to the Plan for LTD and Regional Directorates Table 11: Revenues grouped in LTD and Regional Directorates Table 12: Values cost per 100 /Unit in revenue collection Table 13: Additional tax 2017 from tax audits, compare to years 2015 and Table 14: Number of audits carried out during , and comparison to the same period Table 15: Compliance visits by regional directorates and comparison to the 2017 Plan Table 16: Outcomes from compliance visits Table 17: Outcomes from fines for 2017 and comparison with the same period of Table 18: Results of OFAP activities for visits and audits Table 19: Activities performed by the Taxpayers Education and Service Department Table 20: Issuance of soft tax certificates by type of application Table 21: Activities performed by Taxpayers Education and Service Centres in LTD and Regional Directorates Table 22: State of businesses registered by regions Table 23: Electronic declarations by months and tax types Table 24: Activities performed by the Call Centre Table 25: Report on payments in LTD and Regional Directorates by Call Centre Table 26: The situation of businesses with fiscal cash registers by Regional Directorates Table 27: Reimbursements for fiscal receipts Table 28: Reimbursements and Refunds Table 29: Reimbursements and returns by months Table 30: Comparison of estimated and collected debts Table 31: Active debts by region Table 32: Debt forgiveness and payments Table 33: Performed activities of games of chance Table 34: Activities conducted by the Investigation and Intelligence Unit Table 35: Results in the Investigation and Intelligence Unit Table 36: Activities carried out by Division for Legislation and Legal Advice Table 37: Activities carried out by the Division for Inter-institutional Representation and Cooperation Table 38: Activities carried out by the Division for Inter-Institutional Representation and Cooperation page 5

6 FIGURES Chart 1: Budget spending Chart 2: Number and gender structure of employees Chart 3: Graphical presentation of collected revenues and pension contributions by the years Chart 4: Graphical representation of revenues by tax types Chart 5: Graphic representation of revenues by year and main tax types Chart 6: Graphical presentation of revenues by regional directorates Chart 7: Additional Tax amount Chart 8: Number of audits carried out by years, Chart 9: Conducted visits during Chart 10: Electronic declarations by months Chart 11: Electronic declaration by type of tax Chart 12: Graphic presentation of reimbursements for fiscal receipts Chart 13: Graphic presentation of debt collection page 6

7 FOREWORD BY THE DIRECTOR GENERAL It is my pleasure, as the Director General of the Tax Administration of Kosovo, to provide you with the Annual Work Report for 2017, in full format pursuant to the Law No. 03/L-222 on Tax Administration and Procedures. This report covers all TAK activities, together with the staff involved and that contributed to the positive results of the organization, enabling the budget of the Republic of Kosovo to fulfil its planned needs. In addition to its primary purpose that of revenue collection, TAK carries out numerous activities based on the Strategic Plan and other annual and periodic plans by providing better taxpayer services, increasing professionalism and transparency, improving the perception on integrity and honesty towards increased voluntary compliance in the payment of taxes. TAK has based all of the above towards enhancement of staff skills, improving key tax processes, both for taxpayers and TAK staff, providing an effective organizational structure, upgrading of Information Technology for more effective and efficient work, and great reduction in the level of informal economy. Undoubtedly, in addition to its in-house staff, TAK's achievements are also related to activities carried out with other local and international institutions that are providing expertise and professionalism to keep TAK in step with modern sister organizations. On this occasion, I would like to express my gratitude for the cooperation and coordination of activities, both to taxpayers and in-house staff. In addition, I would also like to express my high appreciation to the commitment and professional engagement of our organization's staff in achieving the objectives and improving the image of TAK by providing our society with a better prosperity for the future. Prishtina, March 2018 page 7

8 page 8

9 INTRODUCTION Elaboration of reports by the Tax Administration of Kosovo is a daily routine that covers numerous activities of TAK s staff ranging from field work to the numerous work activities to help people in the field. TAK also elaborates reports on the work of TAK with local institutions, as well as various international institutions. TAK s Annual Report 2017 is a legal requirement deriving from Paragraphs 2 and 3 of Article 8 of Law No. 03/L-222 on Tax Administration and Procedures, which defines reporting items. This Report provides details on TAK s budget, staff, collected revenues together with cost, cancelled liabilities, tax prosecutions as well as taxpayer complaints. All of the above are accompanied by numerous details and data reflecting the work in many specialized areas, both in the field of taxation and in other common and special areas of TAK staff, but also assisted by international institutions in the specialization and capacity building of our organization. This work has proven successful also in revenue collection, improving the image of TAK both domestically and abroad. TAK remains committed to fulfil and exceed its obligations defined by legislation, the Government, and local and international institutions, as well as to serve as an impetus for the development of the country and the society. page 9

10 I. BACKGROUND TAK was established on 17 January 2000 under the guidance and administration of UNMIK. In February 2003, UNMIK handed over the governance competences to the Ministry of Economy and Finance and since that time, TAK has been an autonomous organization, managed entirely by locals with assistance from international donor organizations, primarily USAID, EU and IMF. TAK, initially managed the Hotel and Restaurant Taxes, which was replaced with the Presumptive Tax, whereby all business income tax was charged. VAT was introduced on In April 2002, the salary and the profit tax were introduced for legal entities, which until then were only charged with the presumptive tax. In January 2005 a tax reform came into effect, replacing presumptive tax, salary tax and profit tax with two new types of taxes, i.e. Personal Income Tax, which is charged on natural persons and Corporate Income Tax, which is charged on legal entities. The tax system in Kosovo has evolved from the UNMIK regulation system in the system of tax laws issued by the Assembly of the Republic of Kosovo. These laws are considered to be understandable and easy to administer and enforce. page 10

11 Millions TAX ADMINISTRATION OF KOSOVO 1. BUDGET Estimated budget for all economic categories in 2017 was 8.9 million, of which 8.8 million were spent. The breakdown of expenditures by category is as follows: 6.8 million or 78.1% of total expenditures were spent on wages and salaries, 1.5 million 17.3% on goods and services, or 1.9% on utilities, and or 2.6% were capital expenditures. Compared to the previous year, spending was lower by 0.6%. Table of budget spending by economic category: Category of expenditure Budget 2017 Structure Comparison =4/ 7=4/5 8=4/3 Wages and salaries 6,585,102 6,889,254 6,881,449 6,881, % 100.0% 99.9% Goods and services 1,196,993 1,423,736 1,527,748 1,632, % 93.6% 107.4% Utilities 203, , , , % 94.9% 90.1% Capital expenditures 94, , , , % 88.0% 64.2% Total 8,079,543 8,858,125 8,806,720 8,951, % 98.4% 99.4% Table 1: Budget spending in 2017, comparison with 2016 and 2015 Source: Budget Division Budget spending , Chart 1: Budget spending Source: Budget Division page 11

12 2. HUMAN RESOURCES The objectives of Human Resources Division related to staff management were based on Law No. 03/L-149 on the Civil Service of the Republic of Kosovo, the regulations for the implementation of this law as well as the Work Plan of this Division for the coming year, in accordance with TAK Operational Plan for 2017 and Regulation No. 01/2015 on Rules and Procedures for Staff Recruitment, Development, Transfer and Suspension. The Human Resource Division was dedicated to the application of basic principles of civil service, legal procedures and the best staff management standards and practices in order to build a professional and efficient Tax Administration to the administration of taxes collected at the Kosovo level. The Human Resources Division also carried out the following activities: provided advice and guidance to the managers and other TAK staff, upon request, concerning performance appraisal; issuing certificates as proof of employment relationship in TAK; providing various professional advice related to the civil service in Kosovo; regular record keeping on the number of TAK employees who are on vacation (annual leave, maternity leave, unpaid leave, suspended, etc.). Total number of employees in the Tax Administration is 781, out of whom 535 men and 246 women. Six officials of TAK retired in On the other hand, in order to implement the Law on Public Debt Forgiveness, in 2017 TAK hired 60 officials under a special service contract, as foreseen by the Law No. 03/L-149 on the Civil Service. Based on the agreement signed by the Ministry of Finance with the University of Prishtina 2017 (MoF-UP-TAK), 52 students served internship at TAK. In addition, 56 other persons completed their internship at the Tax Administration. Number of employees by qualification, ethnicity and gender: Qualification Ethnicity Gender structure Superior Higher Secondary Primary Albanian Serbian Turkish Other Male Female Total % 1.2% 9.7% 0.3% 95.0% 4.0% 0.3% 0.8% 68.5% 31.5% 100.0% Table 2: Number of employees by qualification, ethnicity and gender Source: Human Resources Division page 12

13 Number and gender structure of employees Meshkuj Femra Gjithsej Chart 2: Number and gender structure of employees Geographic distribution of total employees at TAK, as of : Region Staff number % Gender Male % Female % LTD % % % Prishtina % % % Prishtina % % % Prishtina % % % Gjilan % % % Ferizaj % % % Prizren % % % Prizren % % % Gjakova % % % Peja % % % Mitrovica % % % Tax Investigations % % % Fiscal Devices % % % Call Center % % % ZGJoNA % % % Games of Chance % % % TSEC % % % HQ % % % Total % % % Table 3: Number of employees at TAK, 2017 Source: Human Resources Division page 13

14 2.1. TRAINING This year, this Division delivered and provided technical support for staff training. TAK, as well as local and international organizations, organized 58 trainings on different fields of tax legislation, involving 542 officials. In addition, 10 seminars and study visits/workshops were held with the participation of 57 officials. Two trainings were provided for external audiences (for other institutions), with 58 participants. Training provided by local and international institutions, by number of training and participants: Provider Number of delivered trainings Number of participants Number of days TAK MTI/TAK KIPA TK OECD CEF FLSA A.U.K/ USAID PHD/ ASHBK EU/EC UNDP/SCAAK Total Table 4: Training provided by local and international institutions, by number of training and participants: Source: Training Division report Seminars and study visits/workshops: Provider Number of delivered trainings Number of participants Number of days TAK/GIZ ACA /UNDP KLGI Çohu/KDI OEAK / KFOS OLC MIA Total Table 5: Seminars and study visits/workshops Source: Training Division page 14

15 3. REVENUES 3.1. STRUCTURE OF REVENUES During 2017, Tax Administration of Kosovo collected revenues amounting to million, compared to the same period of the previous year, revenues were increased by 7.2% or expressed in value for 27.9 million, while compared with the annual plan of million (excluding the inclusion of the revenue plan from PAK) for 2017 amounted to 98.37% or approximately 6.8 million less (excluding revenues collected by PAK through a request for credit in the amount of approximately 1.2 million). Revenues plan from PAK for 2017, are estimated 3.0 million revenues (from this position the value paid by the PAK through TAK's credit request for 2017 is 1.2 million and the rest of about 1.0 million has been revenues from regular activities collected by the PAK). Collected Pension Contributions for this period amounted to million euro. In total, Taxes and Pension Contributions collected this year amounted to million, which compared to the same period of last year the collection is higher for 6.7%. During 2017, TAK conducted very important activities that played a role in achieving its mission and vision as a modern administration. During this period changes have been made to the new Electronic Tax System - EDI, which is more advanced, more suitable for application, which includes new features that will facilitate the declaration and payment of taxes. Working groups were established for: Reporting the purchase/sales book for VAT through the EDI platform; Fiscal cash registers project; Health Insurance project, etc. In addition, TAK's management is engaged with a special commitment to provide TAK's support in the IT System replacement project as the key factor in the modernization of the Tax Administration, a project deriving from TAK's strategic objective for the time period TAK is based on the Strategic Plan , which through this strategy envisages professionalism, integrity, efficiency and excellency of services. Despite challenges, TAK is determined to continue with the utmost dedication towards achieving further success in its mission, collecting revenues by observing legal framework. TAK will consistently make efforts to increase voluntary compliance by providing professional, transparent and effective services for a fair and uniform implementation of tax laws. page 15

16 Millions TAX ADMINISTRATION OF KOSOVO Below is presented the table for taxpayers who have declared turnover and payments for the period : YEARS No. of declaring taxpayers 67,293 62,462 65,259 No. of declaring businesses 56,887 57,594 61,046 No. of businesses declaring turnover > 0 40,218 38,351 39,506 No. of taxpayers who have paid (by period) 46,256 44,153 45,320 No. of taxpayers who have paid (by date of payment) 57,946 49,140 50,057 Declared turnover amount 9,042,571,161 9,252,677,620 10,153,775,256 Table 6: Taxpayers declaring turnover and payments, Source: Risk Management Revenues from Taxes and Pension Contributions Pensionet Të Hyrat Total Chart 3: Graphical presentation of collected revenues and pension contributions by the years REVENUES BY MONTH Revenues trend by months, in January 2017 compared to 2016, revenues grew by 3.4%, in February by 11.1%, in March by 22.1%, in April more than 3.9%, in May for 4.0% higher, for June they are higher by 19.2%, for July higher by 6.1%, in August for 2.5%, in September are lower for 16.7% lower, in October grew by 6.4%, in November by 18% higher, whereas in December they grew for 34.7%. Compared to the annual projection of EUR million (excluding the inclusion of PAK's revenues plan), for 2017 revenues are collected reached 98.6%. page 16

17 Below are shown revenues collected by month, in comparison with the plan and previous years: Month Collection by years Plan 2017 Share in % (Review) Comparison collectionplan 2017 Comparison collection 2017/ =4/ 6 7=4/6 8=4/3 January 40,953,871 43,818,004 45,339, % 48,990, % % February 21,159,150 20,606,196 22,905, % 23,038, % % March 21,830,347 21,890,801 26,734, % 24,475, % % April 42,432,376 45,759,619 47,555, % 51,163, % % May 15,394,219 23,901,727 24,870, % 26,723, % % June 20,808,697 21,350,928 25,454, % 23,871, % % July 36,275,230 43,090,979 45,753, % 48,180, % % August 20,434,528 29,803,923 30,574, % 33,322, % % September 1 26,886,146 41,562,539 34,594, % 34,469, % 83.23% October 42,218,945 44,208,577 47,047, % 49,429, % % November 20,193,846 26,309,302 31,066, % 29,415, % % December 23,693,695 24,082,690 32,459, % 26,925, % % Total 332,281, ,385, ,355, % 420,000, % % Pension Con. 133,533, ,500, ,731, % Table 7: Revenues collected by months Source: MF-Treasury / TAK 3.3. REVENUES BY TAX TYPES In the revenues structure 2 by the tax types, the largest share marked VAT with 47.5%, followed by Withholding Tax at Source with 20.9%,Corporate Income Tax with 18.8%, Tax on Individual Business with 8.5% and Tax Withholding on Interest, Dividend, Royalty, Rent, Lottery and Game of Chance Winnings with 4.4%. Table of Revenues by tax types 2017: Tax Type Revenues by years % Plan 2017 Comparison =4/ 6 7=4/6 8=4/3 Value added tax 155,153, ,363, ,635, % 193,875, % 109.0% Withholding tax on wage 72,081,313 80,327,270 86,561, % 87,876, % 107.8% Tax on Individual Business 30,759,022 33,161,625 35,148, % 36,791, % 106.0% Withholding tax on interest, royalties and rent, etc. 6,393,399 11,254,117 18,073, % 12,201, % 160.6% Corporate Tax 67,893,662 81,278,873 77,936, % 89,257, % 95.9% Total 332,281, ,385, ,355, % 420,000, % 107.2% Table 8: Revenues collected by tax type, compared with previous years Source: Business report for January-December 2017, TAX 1 The collection of revenues is less in this reporting period (September 2017) compared with the same period of 2016 due to the fact that in September 2016, around EUR 11.0 million were collected only from a single taxpayer ("KEK ). 2 The amount of revenues reported by Treasury on is EUR million, while revenues generated by IT/SIGTAS on amounted to EUR million. The difference of EUR 2.0 million, between revenues reported by Treasury and those collected by SIGTAS is transferred to the account of Tax withheld at wage, in order to harmonize revenues between two sources. page 17

18 Chart 4: Graphical representation of revenues by tax types LEGEND: VAT Value Added Tax WHT Tax Withheld at Source PD - Tax on Individual Business WR - Tax Withholding on Interest, Dividend, Royalty, Rent, Lottery and Game of Chance Winnings CD Corporate Tax page 18

with 23.2%.")

19 3.4. REVENUES BY MAIN TAX TYPES Regarding revenues by main tax types, Value-Added Tax (VAT) had the highest share, respectively 47.5%, followed by Personal Income Tax (PIT) with 29.4% and Corporate Income Tax (CIT) with 23.2%. Revenues by three main tax types for : Type of tax Share in % Comparison across years =4/Ʃ 6=4/2 7=4/3 VAT 155,153, ,363, ,635, % 127.7% 109.0% CIT 74,287,060 92,532,989 96,010, % 129.1% 103.8% PIT 102,840, ,488, ,709, % 117.1% 107.2% Total 332,281, ,385, ,355, % 124.7% 107.2% Table 9: Revenues by year and main tax types Source: Business Report for January-December 2017, TAK Chart 5: Graphic representation of revenues by year and main tax types page 19

20 3.5. REVENUES IN LTD AND REGIONAL DIRECTORATES In the total amount of revenues collected during this period, amounting to EUR mil., the Large Taxpayer Department (LTD) participates with 49.3%, or expressed in the amount EUR mil., followed by Region Prishtina 1 with 17%, or expressed in amount over EUR 70.2 mil., while other regions participate with less than 10% of total revenues in this period, as follows: Table of revenues in LTD and Regional Directorates : Region Revenues by years 2017 Plan % (Revision) Comparison =4/ 6 7=4/6 8=4/3 LTD 3 190,479, ,525, ,125, % 210,468, % 97.9% Prishtina 1 54,748,524 63,831,208 70,263, % 68,960, % 110.1% Prishtina 2 15,272,878 20,963,317 28,369, % 28,579, % 135.3% Prishtina 3 24,773,133 29,500,734 33,624, % 33,322, % 114.0% Gjilan 6,809,857 10,028,258 12,218, % 12,663, % 121.8% Ferizaj 8,178,286 12,188,938 14,676, % 14,604, % 120.4% Prizren 1 7,516,194 9,447,998 11,820, % 12,866, % 125.1% Prizren 2 4 6,402,684 8,048,294 9,954, % 10,591, % 123.7% Gjakova 4,433,151 6,055,323 6,563, % 5,989, % 108.4% Peja 7,503,640 9,713,745 12,684, % 12,214, % 130.6% Mitrovica 6,163,044 8,081,778 10,055, % 9,738, % 124.4% Total 332,281, ,385, ,355, % 420,000, % 107.2% Table 10: Revenues collected compared to the Plan for LTD and Regional Directorates Source: Information Technology (SharePoint) 3 Less collection of LTD revenues in this reporting period compared to the same period of 2016 is as a result of the fact that based on the Decision for Restructuring of Taxpayers in LTD and Regions, the decision dated , in LTD out of 664 active taxpayers (506 businesses and 158 natural persons) in management in 2016 remained only 293 taxpayers (289 businesses and 4 natural persons) in 2017 (other taxpayers are distributed across other regions to MTU - Medium Taxpayer Unit). 4 Based on the Decision of the General Director of TAK, the decision dated ; the Regional Directorate of Prizren is divided into two new Directorates, namely: Prizren 1 and Prizren 2. Therefore, for the years 2015 and 2016, for these two new Directorates, the revenues are distributed according to their share in the revenues of 2017 (the revenues of the regions Prizren 1 and Prizren 2). page 20

21 Chart 6: Graphical presentation of revenues by regional directorates page 21

22 3.6. REVENUES GROUPED IN LTD AND REGIONAL DIRECTORATES From the revenues collected by LTD and two other groups of regions we have the following situation: In LTD compared to the same period of last year, collection share reached to 97.89% 5, in the Regional Directorates Prishtina 1, 2 and 3 grew for 20.27%, while in other Regional Directorates we marked an increase of 22.67%. Compared to the 2017 plan, in LTD collection share reached to 97.0%, in the regions of Pristina 1, 2 and 3 to 101.4%, while in other regions the collection share reached 99.1%. Table of revenues grouped into three regions: Region Revenues by years (Revision) % 2017 Plan Comparison =4/ 6 7=4/6 8=4/3 LTD 190,479, ,525, ,125, % 210,468, % 97.89% Prishtina 1,2,3 66,298,982 84,136, ,192, % 99,798, % % Other regions 47,006,856 63,564,334 77,973, % 78,667, % % CO - Budgetary wages 28,495,553 30,159,179 31,064, % 31,064, % % Total 332,281, ,385, ,355, % 420,000, % % Table 11: Revenues grouped in LTD and Regional Directorates Source: Information Technology (SharePoint) 4. TREATED VALUES COSTS PER 100 /UNIT Table of costs for every 100 units, for 2017: Year Treated values (Tax+ Pension contributions TAK s expenditures Table 12: Values cost per 100 /Unit in revenue collection Source: Annual Report of revenues Treated values of costs Per each 100 /Unit =3/2* ,698,963 8,079, ,128,164 8,858, ,086,818 8,807, Less collection of revenues from LTD in this reporting period compared to the same period of 2016 came as a result of the fact that based on the Decision for Restructuring of Taxpayers in LTD and Regions, the decision dated , in LTD out of 664 active taxpayers (506 businesses and 158 natural persons) in management in 2016 remained only 293 taxpayers (289 businesses and 4 natural persons) in 2017 (other taxpayers are distributed across other regions to MTU - Medium Taxpayer Unit). page 22

23 5. ADDITIONAL TAX FROM AUDITS BY REGIONS Additional tax, as a result of 1,444 tax audits and assessments from office is EUR 53.0 mil., compared with the same period of last year, the collection of additional tax is higher for EUR 3.9 mil., or expressed in percentage by 7.5%. Also in this period we have credit reduction of EUR 13.7 mil., and a loss reduction of EUR 40.2 mil. Table of additional tax from audits conducted during : Region Additional tax % Comparison Credit reduction 2017 Loss reduction =4/ 6=4/3 7 8 LTD 14,482,153 25,400,910 22,458, % 88.4% 5,232,517 14,453,921 Prishtina 1 7,301,640 3,828,663 4,917, % 128.4% 2,081,473 5,183,822 Prishtina 2 4,912,954 4,154,611 3,111, % 74.9% 912,918 2,870,319 Prishtina 3 3,307,895 4,146,875 5,350, % 129.0% 1,218,599 2,027,627 Gjilan 4,024,197 2,693,072 4,481, % 166.4% 707,725 2,741,618 Ferizaj 1,237,529 2,372,467 4,276, % 180.3% 693, ,814 Prizren 1 1,751,770 2,365,567 1,658, % - 676,353 1,366,154 Prizren ,669, % - 599,757 2,304,487 Gjakova 831, , , % 76.1% 146, ,555 Peja 2,814,757 1,660,282 1,705, % 102.7% 1,171,684 3,277,515 Mitrovica 1,924,565 1,837,190 2,950, % 160.6% 345,772 4,331,293 Total 42,589,073 49,133,295 53,092, % 108.1% 13,786,540 40,205,125 Table 13: Additional tax 2017 from tax audits, compare to years 2015 and 2017 Source: Information Technology VKME Module Chart 7: Additional Tax amount page 23

24 5.1. NUMBER OF TAX AUDITS CARRIED OUT BY TAX INSPECTORS Additional tax, as a result of 1,444 tax audits and assessments from office is EUR 53.0 mil. Compared with the previous year, the number of tax audits carried out was 96.2%. Table of the number of tax audits carried out during : Region Number of audits Audit Inspectors Comparison =4/3 LTD % Prishtina % Prishtina % Prishtina % Gjilan % Ferizaj % Prizren Prizren Gjakova % Peja % Mitrovica % Total 1,284 1,501 1, % Table 14: Number of audits carried out during , and comparison to the same period Source: Information Technology VKME Module Chart 8: Number of audits carried out by years, Based on the Decision of the General Director of TAK, the decision dated ; the Regional Directorate of Prizren is divided into two new Directorates, namely: Prizren 1 and Prizren 2. Therefore, for the years 2015 and 2016, for these two new Directorates, the revenues are distributed according to their share in the revenues of 2017 (the revenues of the regions Prizren 1 and Prizren 2. page 24

25 6. COMPLIANCE VISITS For this period, a total of 37,240 visits have been conducted, 6,434 mandatory fines were imposed and 368 fines for non-origin goods as a result of the observed irregularities. Table of compliance visits by regions: Region Number of conducted visits Comparison Mandatory fines Fines for nonorigin goods =4/3 6 7 LTD 2,663 1,862 1, % Prishtina 1 7,472 5,918 5, % Prishtina 2 5,339 4,568 3, % Prishtina 3 8,012 5,908 3, % 1, Gjilan 5,029 4,318 4, % Ferizaj 5,883 4,670 3, % Prizren 1 7,931 6,590 3, % Prizren , % Gjakova 1,879 1,583 1, % Peja 6,206 3,858 3, % Mitrovica 4,685 3,331 4, % Total 55,156 42,794 37, % 6, Table 15: Compliance visits by regional directorates and comparison to the 2017 Plan Source: Information Technology - VKME Chart 9: Conducted visits during page 25

26 6.1. OUTCOMES FROM COMPLIANCE VISITS During this period, as a result of the compliance visits were imposed mandatory fines totalling to EUR 1.6 mil. The value of the non-origin goods is EUR 869,569.00, as a result, the imposed fines amounted to EUR 153,178.00, the stock shortage amounted to EUR 24.9 mil., additional turnover amounted to EUR mil., and as a result, there was additional tax in the amount of EUR 19.8 mil., while the reduction of lending and losses amounted to EUR 19.5 mil. Table of outcomes from compliance visits: Region Value of Mandatory fines Value of Nonorigin goods Fines for non-origin goods 25 % Stock shortage Additional turnover Additional tax Credit reduction Loss reduction LTD 84,350 78,677 10,152 4,727,641 27,557,745 11,862,545 1,106, ,319 Prishtina 1 221,375 87,636 18,276 2,941,339 42,884,231 1,755,799 1,542,809 2,366,069 Prishtina 2 142,650 32,840 8,120 2,090,788 19,623, ,053 1,408,185 1,469,667 Prishtina 3 317, ,327 37,138 1,506,712 14,534, , ,428 1,667,817 Gjilan 155,675 54,674 13,503 1,015,851 7,789, , , ,486 Ferizaj 125,875 97,463 22,974 2,836,643 13,882, , , ,398 Prizren 1 197, ,649 6,270 3,276,307 9,524, , , ,101 Prizren 2 151,500 70,030 14,021 2,999,099 13,895, , , ,788 Gjakova 24,875 38,549 6, ,736 3,958, , , ,062 Peja 93,750 67,719 14,724 1,672,856 10,918, , , ,902 Mitrovica 160,775 65,005 1,598 1,486,562 17,276,170 1,255, ,065 2,143,814 Total 1,674, , ,178 24,994, ,844,933 19,875,782 8,432,948 11,122,423 Table 16: Outcomes from compliance visits Source: VKME Table of fines and comparison with the same period of the previous year: Region Number of mandatory fines 2017 Value of mandatory fines 2017 Number of mandatory fines 2016 Value of mandatory fines 2016 Index 2017/2016 Number of fines for non-origin goods 2017 Value of fines for non-origin goods 2017 Number of fines for non-origin goods 2016 Value of fines for non-origin goods 2016 Index 2017/ =2/ =7/9 LTD , , % 13 78, , % Prishtina , , % 33 87, , % Prishtina , , % 14 32, , % Prishtina 3 1, ,100 1, , % , , % Gjilan , , % 35 54, , % Ferizaj , , % 40 97, , % Prizren ,050 1, , , , Prizren , , Gjakova , , % 26 38, , % Peja , , % 18 67, , % Mitrovica , , % 32 65, , % Total 6,434 1,674,975 7,043 1,800, % , , % Table 17: Outcomes from fines for 2017 and comparison with the same period of 2016 Source: Information Technology VKME Module page 26

27 Now, as a separate function, the Office for Fines and Administrative Penalties deals only with case reviews when inspectors during the field visits and audits encounter irregularities or administrative violations. This function since May 2017 includes also the LTD and all taxpayers are covered by this function. Also in this month a joint Prishtina-based unit was established covering all three Pristina regions and LTD. Below are presented OFAP activities, both for visits and audits: Regjioni Vlera e mallit pa origjinë Ndëshkimi (25%) Derguar per ZGjoNA Nga vizitat Shqyrtuar nga ZGjoNA Aprovuar Pezulluar Në shqyrtim Nr. i gjobave Vlera e gjoba Kontrolle Ndeshkim Nga kontrollet Nr. i gjobave Vlera e gjobave DTM 77, , , ,614, ,700 Prishtinë 1 82, , , ,316, ,036 Prishtinë 2 32, , , , ,534 Prishtinë 3 140, , , ,292, ,125 Gjilan 54, , , ,249, ,375 Ferizaj 97, , , ,285, ,453 Prizren 1 134, , , , ,627 Prizren 2 70, , , , ,375 Gjakovë 38, , , , ,875 Pejë 58, , , , ,408 Mitrovicë 64, , , , ,375 Totali 852, , ,508 4,406 4, ,521 1,726,725 1,294 11,313,937 1, ,882 Table 18: Results of OFAP activities for visits and audits Source: Management of VKME projects page 27

28 7. TAXPAYERS EDUCATION AND SERVICE 7 The Scope of the Taxpayers Education and Service Department (TESD) is development and management of policies and strategies for the provision of services in the most qualitative, timely and accurately manner to taxpayers, including the direct provision of services to taxpayers through the Taxpayer Service Centre in Prishtina (TSC). Another important function is coordination and cooperation with Government Institutions: Kosovo Business Registration Agency (KBRA - MTI) in view of taxpayer registration, Kosovo Agency of Statistics (KAS) in order to coordinate activities for National Business Accounts, The Kosovo Pension Savings Trust (KPST) in compliance with the obligations on Pension Contributions, as well as cooperation with the media and institutions (Associations, Chambers of Commerce) representing taxpayers in view of better communication with taxpayers. Taxpayers Education and Service Department - TESD, considers that the Work Plan for 2017 has been successfully implemented, whereby taxpayers are provided education, information and facilitation of procedures through the provision of professional, transparent and efficient services in accordance with the Tax Legislation. Also, the objectives set for this period were accomplished at a satisfactory level, such as: delivering/holding of seminars and trainings, presentations, various events for certain tax issues, which in addition to being foreseen in the Annual Plan 2017, are also set forth in the Compliance Strategy In the framework of taxpayers' information, the following are foreseen: development of policies, programs and procedures related to taxpayer services at the general (central) and regional level, as well as coordination of joint activities. Requests submitted by the taxpayers, received in physical and electronic form, are treated with special commitment, thus responding to taxpayers in accordance with the Tax Legislation. In addition, greater security for taxpayers/public opinion has been created, they are provided with current information, in timely manner and through appropriate channels, and effective taxpayer services are developed in cooperation with stakeholders, such as the Chambers of Commerce, Business Community, Accounting Associations, etc. In order for taxpayers to be familiar with every step of the procedures required by tax legislation, novelties and other changes, are prepared/provided Taxpayers Notices, via TAK's web site, 7 Public Explanatory Decisions No. 01/2017, 02/2017 and 03/2017 page 28

29 Facebook, through taxpayers electronic addresses, Press Releases, Written and Electronic Media Interviews, Public Ruling/Documents, and the requests filed by the taxpayer within the legal timeline were reviewed, with a large number of Individual Rulings. The Taxpayer Education and Service Department, in cooperation with KFRC, has delivered Seminars for Taxpayers in all TAK regions, such as in Ferizaj, Gjilan, Prizren, Gjakova, Prishtina, Peja and Mitrovica. 12 seminars; 35 presentations for elementary school pupils and 23 presentations for high school students were delivered. The following topics were presented / addressed in these seminars: - Annual Declaration and Reporting of Financial Statements, - Applying the VAT reverse charge for the supply of services in the field of construction within the country, - Purchase Book and Sales Book Reporting - through EDI - Electronic System, - Tax on Wages and Pension Contributions, rents, VAT and VAT Refund, - Declaration of purchases over EUR 500, - Corporate Income Tax Annual Declaration CD, - Declaration through EDI Electronic System, - Law on Tax Administration and Procedures, - Law on Personal Income Tax, - Treatment of NGOs on Tax On Wages and Pension Contributions, - Treatment of NGOs on Rents Tax, - Treatment of NGOs on VAT VAT Refund, - Treatment of NGOs on Corporate Income Tax Annual Declaration CD, - Withholding Tax on Royalties, - Implementation of OECD Commentary on Royalties and ECJ regarding VAT, - Law on sponsorship compared with the Law on PIT/CIT, - Treatment of VAT on foreign donations to domestic contractors, - VAT Flat Rate for farmers, - Treatment of land renting, - Applying the VAT reverse charge for services purchased outside Kosovo. - Training/Meeting with SHUKOS, topic: Treatment of Debts, Donations, and VAT Declaration, - Treatment for private enforcement agents - their obligations in relation to tax legislation, - Trainings / workshops provided to TAK officials. During this period in working groups with the Control Department were prepared the following documents: page 29

30 - Explanatory Document on Recognition of Expenses - based on Accrual Principle; - Explanatory document on Exercise of the Right to VAT deduction; - Internal Regulation on VAT Refund in PIT and CIT; - Public Ruling No. 01/ Pension Tax on withdrawal from the Kosovo Pension Savings Trust (KPST) has been prepared by the Taxpayers Service and Education Department; - Public Ruling No.03 / Application of Reverse Charge for Services Purchased outside Kosovo; - Guideline for the procedures of equipment with tax certificate; - Draft manual: Questions - Answers; - Draft Brochure: Pay tax obligations in correct and timely manner, don't be subject to penalty; - Draft Brochure: General Information on Taxes in Kosovo; - Different Announcements / Releases through which taxpayers are notified during Activities performed by the Taxpayers Service and Education Department: Description of activities Number of activities Response in physical form 77 Response in electronic form 979 Response in electronic form to Regions 160 Responses for EDI 647 Responses through TAK web page 2,212 Responses to journalists 3 Total responses 4,078 Creation of Fiscal Numbers for Existing Businesses 42 Business Activation Cancellation of Fiscal Number Application for opening a tax account 48 Preparation of materials 36 Participation in working groups 41 Certificate Fiscal Number for tax representative 11 Conducted/delivered activities 278 Cooperation with other departments 155 Workshops/Trainings with taxpayers 26 Attendance of Trainings and Courses 7 Training for TAK s staff 5 Meetings with taxpayers 351 TAK activities with the Media 6 Table 19: Activities performed by the Taxpayers Education and Service Department Source: Taxpayers Education and Service Report Issuance of soft and hard copy certificates page 30

31 Tax certificates can be obtained in soft and hard copy. TAK during this period has issued 106,500 certificates, of which 51,198 soft copy certificates or 48.1% of all certificates and 55,302 certificates were issued from TAK (hard copy) counters or 51.9%. Table of issued tax certificates: No. Type of Tax Certificate TAK Online Persons Online EDI Total Structure by type =2+3+4 % 1 Visa Application 26,654 23,113 7,855 57, % 2 Other 16,512 6, , % 3 Tender Application 4,079-4,853 8, % 4 Release from Citizenship 2,509 2, , % 5 Business deregistration 2, , % 6 Loan Application 704-2,669 3, % 7 Citizenship acquisition % 8 License Application , % 9 Change of Business Ownership % 10 Maternity leave % 11 Change of business form % 12 Grant Application % 13 Subsidy Application % 14 Extension of residence permit in Kosovo % 15 Application for change of surname % 16 Application for customs warehouse % 17 License extension application % 18 Donation application % 19 Application for line extension % 20 Annual Turnover % 21 Deregistration of Fiscal Cash Registers % Total 55,302 33,444 17, , % Table 20: Issuance of soft tax certificates by type of application Source: Taxpayers Education and Service Report At Taxpayer Service Centre (TSC), takes place direct provision of services to taxpayers, regardless of the geographical scope. Such service is functional in Prishtina and in all other Regional Directorates. Services are provided through the queue management system that is installed in all regional offices. In this centre, services are provided uniquely, in open counters. Since , by the decision of TAK Management, started to provide services to LTD taxpayers, which means that the LTD service office is closed and from this date the LTD taxpayers will provide with services in the TSC. page 31

32 Activities performed by the LTD and Regional Taxpayers Service Centres: Type of Service LTD PR/ TSEC Gjilan Ferizaj Prizren Gjakova Peja Mitrovica TOTAL REQUESTS 3,550 45,202 16,168 9,186 20,037 10,459 12,405 7, ,224 ANNOUNCEMENTS 1,378 1, ,431 PROTOCOLS/SUBMISSIONS 111 7,268 4, ,691 5,400 5,970 1,219 26,769 PENSION CONTRIBUTIONS ,579 3,439 12,310 4,534 6,227 5,091 38,197 OTHER WORKS 686 8,593 9, ,684 2, ,083 27,772 LEGAL ADVICES 43 2, ,794 5,183 PRODUCED CERTIFICATES 21 1, ,852 VISITS APPROVAL OF CHANGE OF ADDRESSES ,302 ACCEPTING OF ENVELOPES 0 1, ,866 TOTAL 5,789 69,163 37,812 15,703 38,560 23,431 25,841 18, ,626 Table 21: Activities performed by Taxpayers Education and Service Centres in LTD and Regional Directorates Source: Information Technology - VKME Module / Taxpayers Education and Service 7.1. REGISTRATION The number of active businesses registered by the end of 2017 is 103,136 businesses, of which 68,049 are individual businesses whereas 35,087 are legal businesses, while 21,585 are fiscal numbers for natural persons. Table of businesses registered by regions: Region Individual Legal Total Natural persons Total = =4+5 LTD Prishtina 1 9,566 8,873 18,439 4,457 22,896 Prishtina 2 5,862 3,714 9,576 1,902 11,478 Prishtina 3 5,943 5,407 11,350 1,722 13,072 Gjilan 7,334 2,686 10,020 2,016 12,036 Ferizaj 8,526 3,344 11,870 2,024 13,894 Prizren 1 6,639 2,455 9,094 2,060 11,154 Prizren 2 5,642 1,677 7,319 1,427 8,746 Gjakova 4,138 1,461 5,599 1,427 7,026 Peja 8,053 3,178 11,231 2,526 13,757 Mitrovica 6,301 2,042 8,343 2,017 10,360 HQ Total 68,049 35, ,136 21, ,721 Table 22: State of businesses registered by regions Source: Information Technology (SharePoint) page 32

33 Thousands TAX ADMINISTRATION OF KOSOVO For the use of electronic declaration - EDI, until now 77,743 taxpayers have been registered, while 75,038 taxpayers have used this system. For this year, through the EDI system, 1,886,542 statements (including corrections) have been delivered/issued, whereby we have the following structure of declarations by tax types are: for VAT 16.0%, for Withholding Tax and For Pension Contributions (WM & CM) 27.6% each, for Tax on Interest, Dividends, Royalties, Rental, Lottery Winnings and Games of Chance (WR) 9.9% and for other taxes all together 9.7%. Table of electronic declarations by months: MONT E PT VAT WM CM IS QS PD CD WR IR DO HI DECLARATION 1 40, ,213 25,291 45,271 45,001 23,259 4, , , ,969 24,167 39,451 39,258 3,662 1,310 1, , , ,234 29,301 42,730 42,358 3,800 1,194 7,304 5,601 15, , ,622 25,624 44,145 43,921 22,921 3,754 1, , , ,480 23,749 42,522 42,161 3,925 1, , , ,809 22,592 41,605 41,349 3,341 1, , , ,255 24,562 44,954 44,766 23,440 4, , , ,704 23,873 42,518 42,368 4,991 1, , , ,737 24,579 42,304 42,207 4,128 1, , , ,779 26,540 48,058 48,091 24,201 4, , , ,004 25,633 43,876 43,726 5,341 1, , , ,736 26,261 44,909 44,762 4,355 1, , Total 1,886, , , , ,364 27,423 13,584 9, ,565 5, Table 23: Electronic declarations by months and tax types Source: SharePoint, TAK 250,000 Electronic declaration by months 200, , ,000 50,000 0 Janar Shkurt Mars Prill Maj Qershor Korrik Gusht Shtator Tetor Nëntor Dhjetor Series1 191, , , , , , , , , , , ,736 Chart 10: Electronic declarations by months page 33

34 Thousands TAX ADMINISTRATION OF KOSOVO 600, , ,000 Electronic declaration by type of tax 300, , ,000 0 VAT WM CM IS QS PD CD WR IR DO Series1 302, , , ,364 27,423 13,584 9, ,565 5, Chart 11: Electronic declaration by type of tax 8. CALL CENTER The Call Centre delivered the following activities: 51,331 successful calls; 19,523 taxpayers informed about the debt of , and missing statements in the system 15,721 taxpayers were informed about the missing VAT declarations for periods October/ October/2017; 1,257 taxpayers/partners have been informed about closing the IS tax account; 13,682 taxpayers have been informed of the possibility of benefiting from public debt forgiveness; 1,148 taxpayers on debt of ,99 missing declarations and fines; 443 taxpayers with debt of ,99 have been informed about 13,135 declarations missing in the system for different types of taxes; in 24,164 cases we were not able to accomplish the calls due to the wrong number and non-response by the taxpayer; verified payments received as a result of calls from the report payments received by CBK are 9,912 taxpayers; verified cases that have made declarations are 5,696 taxpayers, of which 646 taxpayers have declared without being contacted by the Call Centre. The number of incoming calls is 8,249, through which taxpayers have mainly contacted Call Centres to get additional information on VAT, PIT, CIT, business registration and deregistration, EDI Declaration, debt, declarations missing in the system, fiscal cash registers, debt forgiveness, reporting of purchases of over 500, about administrative issues, etc. page 34

35 Results of activities in the Call Centre: No Description of activities Increase/Decrease Index 1 Successful calls 45,076 51,331 6,255 14% 2 Unsuccessful calls 19,254 24,164 4,910 26% 3 Verification of payments 9,465 9, % 4 Verification of declarations 4,305 5,696 1,391 32% Total activities 78,100 91,103 13,003 76% Table 24: Activities performed by the Call Centre Source: Call Centre Report Total payments by region for the reporting period January - December 2017 is 2,861,005. The highest payment is marked in the Prishtina 1 region, in the amount of 534,447 or 19%, in the Prishtina 2 region in the amount of 426,281 or 15%, in the Prishtina 3 region in the amount of 384,436 or 13%, in Peja in the amount of 292,343 or 10%, while other regions have made payments below 10% of the total amount. Payments realized in LTD and Regional Directorates: Region January-December/2016 January- December/2017 Increase/Decrease LTD 136, , , % PRISHTINA 1 394, , , % PRISHTINA 2 217, , , % PRISHTINA 3 302, , , % GJILAN 163, , , % FERIZAJ 182, , , % PRIZREN 1 288, , PRIZREN 2-171, GJAKOVA 82, , , % PEJA 217, , , % MITROVICA 137, , , % Total 2,123,356 2,861, ,649 35% Table 25: Report on payments in LTD and Regional Directorates by Call Centre Source: Call Centre Report Index page 35

36 9. FISCALIZED BUSINESSES IN LTD AND REGIONS The total number of businesses equipped with fiscal cash registers by is 27,703. Only in 2017, 1,986 new businesses have been equipped with fiscal cash registers, and 646 fiscal cash registers have been installed in the businesses involved in the sale of oil derivatives. Table of businesses equipped with fiscal cash registers: Tipi i Pajisjes fiskale të instaluara deri Biznese të fiskalizuara PEF të instaluar PEF të Instaluar PAJISJE Çregjistrimi Janar - Janar - më shumë se FIZIKE TË I PEF deri Totali I PEF Pajisje per Regjioni Deri 2016 Dhjetor Totali Deri2016 Dhjetor Një herë INSTALUARA 2017 Arkë Printer të Instaluar derivate = = = , , , , PRISHTINË 1 3, ,097 4, , , ,649 1, PRISHTINË 2 2, ,955 3, , , ,748 1, PRISHTINË 3 2, ,144 3, , , ,777 1, GJILAN 2, ,665 2, , , , FERIZAJ 2, ,673 3, , , , PRIZREN 1 2, ,507 2, , , , PRIZREN 2 2, ,283 2, , , , GJAKOVË 1, ,383 1, , , , PEJË 3, ,535 4, , , , MITROVICË 2, ,257 2, , , , TOTALI 25,717 1,986 27,703 35,722 3,527 39,249 3,184 36,065 4,329 26,763 11, Table 26: The situation of businesses with fiscal cash registers by Regional Directorates Source: Information Technology, SharePoint With the entry into force of the Administrative Instruction (MF) No. 01/2015, Article 26 "Incentives and Motivations for Taking Fiscal Receipts" and AI 01/2017 obliges TAK to reimburse the financial means for citizens who submit fiscal receipts. The Division of Fiscal Cash Registers, in cooperation with other departments (Department of Taxpayers Service and Education, Department of Information Technology, Department for Program Support and Operations Department), Postal Service of Kosovo, Treasury and CBK have successfully managed this project during the period January - December During the period January-December 2017 (Q4 / 2016, Q1 / 2017, Q2 / 2017, Q3 / 2017), 682,414 envelops have been received, 680,224 envelops have been verified, 679,190 citizens have been followed-up for reimbursement in the amount of 13,046,619 and 10,336 citizens have been rejected in the amount of 196,786 for various reasons, such as: bank account errors, incorrect personal information, etc. Also, 250 citizens have been reimbursed in the amount of 4,795 (these citizens were of periods before the Q4 / 2016, where there were cases addressed after filing complaints and cases that have had other problems). page 36

37 Millions TAX ADMINISTRATION OF KOSOVO Table of reimbursement for fiscal receipts: No. Period Number of verified envelopes Reimbursement amount 1 Q2/ , ,105 2 Q3/ , ,770 Total ,873 1,252,875 3 Q4/ ,680 2,209,745 4 Q1/ ,391 2,994,370 5 Q2/ ,943 3,919,655 6 Q3/ ,972 5,170,375 Total ,986 14,294,145 7 Q4/ ,797 6,286,580 8 Q1/ ,569 6,496,445 9 Q2/2017 1, , Q3/2017 1, ,345 Total ,224 13,046,619 Table 27: Reimbursements for fiscal receipts Source: Report on fiscal cash registers Total 1,532,083 28,593, Reimbursements for fiscal coupons Chart 12: Graphic presentation of reimbursements for fiscal receipts page 37

38 10. REIMBURSEMENTS AND REFUNDS As regards reimbursements and refunds, 680,090 requests have been approved, of which 646 are for businesses and natural persons and the rest, 679,444 respectively, are for reimbursement of fiscal coupons. The total value of approved reimbursements is 52.4 million, of which 46.7 million is transferred to accounts for all types of taxes, whereas means in the amount of EUR 5.6 million are transferred for covering TAK/PS liabilities. According to Tax types, the highest approved values are for VAT reimbursement and refund, namely 31.2 million, million for fiscal receipts, 2.02 million for Corporate Tax, 372,000 for Personal Income Tax, and so on. Table of reimbursements by types of taxes: Type of tax Approved requests 2017 Obligations TAK/KP 2017 Structures Compariso n =4/ 8=6/4 Reimbursements 22,900,734 17,482,519 31,229, ,802, % 12.18% VAT Refund VAT 1,803, ,810 49, , % 0.02% Reimbursements - TAP 170,320 49, , , % 0.04% Refunds - TAP 23, ,190 14, , % 0.02% Reimbursements - TAK 611,310 8,047 1,776, , % 0.29% Refunds - TAK 534, , , , % 0.04% Refunds WR 250,751-35, % 0.00% Refunds TF % 0.00% Refunds TP 80, % 0.00% Refunds KP - 68, ,738, % 5.57% Deposit Refunds 2,112, % 0.00% Mandatory fine Refunds % 0.00% Reimbursement for fiscal receipts 1,252,875 14,289,350 13,051, , % 0.00% Total 29,740,034 33,255,614 46,770, ,090 5,668, % 12.12% Table 28: Reimbursements and Refunds Source: Division for Procedures and Fiscal Cash Registers The table below shows the reimbursements for 2017 by month whereby it is noted that most of the reimbursements were handled and processed in March, August, October and December page 38

39 Table of reimbursements by months for VAT, TAP, TAK and KP: Month Number of approved requests Amount required Amount approved Total obligations Amount transferred to the taxpayer account January 29 2,756,130 2,750,059 80,353 2,669,706 February 40 1,410,237 1,406,685 99,547 1,307,139 March 48 4,685,809 4,608, ,729 4,439,961 April 45 2,289,407 2,189, ,462 1,759,777 May 50 3,678,104 3,652, ,071 2,782,359 June 37 2,398,445 2,366, ,013 2,003,698 July 36 1,172,613 1,159, , ,575 August 45 5,281,768 5,214, ,920 4,815,313 September 46 1,362,824 1,349, ,709 1,050,479 October 94 4,906,203 4,649,633 1,260,554 3,389,080 November 87 3,404,889 3,208, ,383 2,435,190 December 100 7,082,799 6,832, ,854 6,172,139 Total ,429,228 39,388,022 5,668,606 33,719,416 Table 29: Reimbursements and returns by months Source: Report of the Division for Procedures 11. COMPARISON OF DEBT COLLECTION WITH LTD PLAN AND REGIONS Debt collection in 2017 amounted to EUR 66.8 million, whereas in 2016 amounted to EUR 68.3 million. This year, it was collected EUR 1.4 million or 2.0 % less. Table of debt collection and comparison with the plan/estimations: Region % Comparison =4/ 6=4/3 LTD 16,504,976 28,405,622 19,365, % 68.17% Prishtina 1 6,336,250 7,545,139 10,007, % % Prishtina 2 3,937,959 5,601,502 5,302, % 94.67% Prishtina 3 5,443,643 8,003,682 7,711, % 96.34% Gjilan 1,535,238 2,796,634 3,897, % % Ferizaj 2,232,240 3,788,649 5,013, % % Prizren1 4,229,197 5,446,333 4,544, % - Prizren ,296, % - Gjakova 912,461 1,372,142 1,400, % % Peja 1,913,315 2,977,421 3,518, % % Mitrovica 1,648,820 2,369,507 2,788, % % Total 44,694,098 68,306,630 66,845, % 97.86% Table 30: Comparison of estimated and collected debts Source: Information Technology VKME Module page 39

40 Millions TAX ADMINISTRATION OF KOSOVO Debt collection Chart 13: Graphic presentation of debt collection Table of active debts by regional directorates: No. Region Tax Penalties Interest Total = LTD 4,429,219 1,405, ,846 6,706,202 2 Prishtina 1 31,249,978 15,309,126 26,305,617 72,864,721 3 Prishtina 2 15,665,410 6,092,274 8,671,128 30,428,812 4 Prishtina 3 18,440,783 9,063,796 10,784,697 38,289,276 5 Gjilan 12,652,684 6,430,852 11,615,296 30,698,832 6 Ferizaj 13,666,997 6,012,887 11,973,821 31,653,704 7 Prizren 1 11,294,058 5,013,620 8,265,955 24,573,632 8 Prizren 2 11,166,300 5,443,557 13,039,332 29,649,189 9 Peja 9,551,738 4,754,587 9,271,990 23,578, Gjakova 5,697,947 1,769,702 3,773,548 11,241, Mitrovica 9,612,384 4,084,710 6,139,077 19,836,170 Total 143,427,498 65,380, ,712, ,520,052 8 Table 31: Active debts by region Source: TAK, SharePoint/Debt archive, state of the art The Division of Forced Collection has monitored the implementation of the Law No.05/L-043 on Public Debt Forgiveness. 8 The state of debts may vary depending on the date (but also within the same day) when these data were generated, since the IT system as such is always processing this data and, at any given moment and day, accepts and calculates both the taxpayer's declarations free of charge or those paid, not calculating the processing of penalties and interest for non-payment of the basic tax in time. page 40

41 The following table summarizes the debt forgiveness and collected payments of the two laws that have been in force, pension payments and payments of taxes and pensions from the agreements: Total report on the data of Law 05/L-043 and Law 05/L-119 for Cases Value of No. forgiveness 1 Forgiveness by Automation <100 21,789 4,583, Forgiveness by automation by the Coordinating Committee (entities to 8, ,473, which the debt was forgiven and which had obligations from ) 3 Debts (base + penalties + interest + fines) 3,379 76,463, Debts (penalties + interest + fines) 12,688 42,905, Total Debt Forgiven (5= ) 238,426, Total payments as an effect of Laws for Debt Forgiveness 33,440, Payments by Agreements (Taxes + Pensions) 1,306, Total payments-pensions as an effect of Laws for Debt Forgiveness 880, Table 32: Debt forgiveness and payments Source: Information Technology/SIGTAS page 41

42 12. GAMES OF CHANCE The Department of Games of Chance has successfully carried out the tasks foreseen by the Annual Work Plan, such as control activities, which were conducted through compliance and observation visits, visits coordinated with other institutions such as Kosovo Customs, Kosovo Police and municipal bodies, as well as reviewing different requests of taxpayers, starting from requests for continuation of licensing, requests for new licensing, requests for opening new units, requests for expansion of activity of slot machines, requests for organizing rewarding games, etc. Table of activities performed by games of chance: No. of No. of Type of visit visits employees Additional turnover Additional tax Credit reduction Decrease of loss Refunding visits Compliance- Educational Compliance- Collection of information Compliance - Reliability of documentation ,865,350 64,122 24, ,926 Compliance - Observing ,00 Compliance - Visits with police officers Compliance - Issuance of fiscal number Compliance - Contacts in the office 25-85, ,841 Other visits , Total 1, ,098,745 64,566 24, ,781 Table 33: Performed activities of games of chance Source: Division of Games of Chance During this period, DGC undertook the following actions as well: Number of premises closed for the reporting period Number of fines imposed for the reporting period Value of fines for the reporting period... 1,281,250 Number of reviewed requests for changing address Number of reviewed requests for expansion of activity Number of license extension requests Number of cases reviewed online Number of new licensing requests Number of requests for rewarding games page 42

43 13. TAX INVESTIGATIONS AND INTELLIGENCE The following activities were carried out during this period: 338 operational activities, 266 interviews, 5 raids, 13 criminal charges (reports of initial suspicion), 358 consultations with the Prosecutor's Office, Police, etc., 223 requests for information from third parties, 281 sets of information to third parties. During these activities, 2 fines of 500 were issued. We also have the following results: 32 open cases, 21 final investigative reports, 22 control reports, 79 subsequent cases, 48 subsequent controls. During this period, results from tax evasion were carried out in the amount of 667,014, without penalties and interests. Activities conducted by the Investigation and Intelligence Unit: Operating activities Interviews Raids Criminal charges Cooperation- Consultation (meetings) with Prosecutors/Police, etc. Information from third parties Information to third parties Fines issued Table 34: Activities conducted by the Investigation and Intelligence Unit Source: Tax Investigation Unit Value of fines Results from the operational activities of the Tax Investigation and Intelligence Unit: Open cases Final investigative reports Closed cases Control report Subsequent cases Number of subsequent controls Results from tax evasion Basic tax Penalties and interest ,014 - Table 35: Results in the Investigation and Intelligence Unit Source: Tax Investigation Unit 14. ACTIVITIES RELATED TO LEGAL INTERPRETATIONS AND REPRESENTATIONS Legal Interpretations - within the scope of this Division, the following activities have been developed and implemented: Regional offices and units within TAK addressed 168 requests to this division during this reporting period, out of which 166 have been completed while 2 are under process, and the following: The number of requests received for legal interpretations was 55, with all 55 of them being addressed; The number of requests for legal advice and opinions was 19, out of which 19 were completed; The number of answers to requests for clarification and other information during this period was 94, where answers were provided to 92 requests, whereas 2 cases are in the process. page 43

44 The participation of officials of this division at various meetings of the working groups during the reporting period is as follows: Officials participated in 51 meetings of inter-ministerial working groups outside TAK, out of 51 meetings held in total, while Officials participated in 59 meetings of working groups within the Tax Administration, out of 59 meetings held in total. During the reporting period, officials of this division participated in 133 official meetings with different tax officials from regional offices or various departments within the Central Office in order to provide legal support for legal issues. During this reporting period, officials of this division also participated in 8 various commissions established by the General Director. In the meantime, during the same period, we have received 21 draft laws and draft- Administrative Instructions for comments, as well as 19 different official documents for giving comments and recommendations regarding such drafts. The activities conducted and delivered are presented in tabular form as follows: Activities of the Division Report of Division for Legislation and Legal Advice / 2017 Requests from regional offices and other units within the Tax Administration Requests for legal interpretation Requests for legal advice/opinions Answers to requests for clarifications and other information Participation in working groups outside TAK Participation of officials in different working groups Participation in working groups within TAK Participation of officials in official meetings and various commissions Provision of legal support in official meetings Different commissions Comments on laws, sub-legal acts and other official documents Comments on laws, other sublegal acts Comments on different documents Received Carried out In process TOTALI Table 36: Activities carried out by Division for Legislation and Legal Advice Source: Report from legal services Comments on memorandums and other official acts Legal Representations - Division for Inter-Institutional Representation and Cooperation (DIRC), in the framework of the authorizations, has developed and carried out the following activities: page 44

45 o The number of criminal charges filed against persons suspected of tax evasion, abuse of authorizations in the economy and organization of unlawful gambling is 43. o During this period DIRC, we represented TAK in 156 court sessions in Basic Courts and Court of Appeals, whereas we presented in 125 sessions at the Department of Appeals. o The number of responses to claims where TAK was a defendant in the procedure is 53. o The number of objections towards Financial Expertise we have presented regarding DA decisions is 10. o The number of claims filed against the IOBCSK decisions to initiate administrative conflict is 5. o The number of decisions received by the Prosecutor's Office is 31, to which we responded according to the legal requirements. o The number of decisions received by the Courts is 82, to which we responded according to the legal requirements. o The number of orders received by the Courts is 50, to which we responded according to the legal requirements. o The number of judgments received by the Basic Court is 82, to which we responded according to the legal requirements. o The number of judgments received by the Court of Appeal is 18, to which we responded according to the legal requirements. o The number of judgments received by the Supreme Court - Special Chamber is 4, to which we responded according to the legal requirements. o The number of complaints filed with the Special Chamber against PAK decisions is 4. o The number of responses to defence filed with the Special Chamber against PAK decisions is 15. o The number of responses to KPA's rejoinders to the Special Chamber is 13. o During this period, we have issued 35 legal opinions regarding judgments and decisions received and 93 different responses to the regions, Police, Prosecutor's Office, Courts, State Advocacy and other relevant institutions. o The number of legal property claims filed in court proceedings for compensation of damages is 33. o Participation in the Working Group for preparing a public explanatory decision on tax treatment of deposits and borrowing. o Participation in the Working Group on amending and supplementing the Administrative Instruction No. 01/2015. o Participation in the Commission for authorization of economic operators, laboratories for FEDs certification, according to AI No. 01/2015. o Participation in the Coordination Commission for public debt forgiveness, pursuant to the Law on Public Debt Forgiveness. o Participation in the Complaints Commission within the Tax Administration of Kosovo. page 45

46 Activities developed and carried out according to the number of files and their participation: Responses to Claims, TAK Objection of Expertise, Files received by Regional Offices and the representation in Appeals against Judgments actions of the Legal Office regarding files Judicial hearings of Basic Court - Fiscal and DA Division Regions and those carried forward from the Files reviewed Files not reviewed Criminal charges Assessment of regions Appeal Division Court of Appeals and Private Enforcement Response to Claim of Basic Court - Fiscal Objection of Division Financial Expertise regarding Judgments of Basic Courts and Court of Appeals - Fiscal Claims against IOBCSK Decisions Claims against IOBCSK Decisions, Appeals against Judgments and Responses to various Submissions LTD Prishtina Prishtina Prishtina Gjilan Ferizaj Prizren Gjakova 28 4 Peja Mitrovica CO 2 2 TOTALI Table 37: Activities carried out by the Division for Inter-institutional Representation and Cooperation Source: Report from Legal Services Appeals against Judgments Responses to the Court page 46

47 Judgments, decisions, appeals and legal advice: Judgments, decisions, orders received by courts, prosecutors and private enforcement agents and TAK actions Complaints to PAK, Judgments of SCSC, Response to Defence, Rejoinders to SCSC Legal advice, participation in working groups Regions Decisions of Prosecutor's Office Decisions of Courts Orders of Courts Judgments of Basic Courts Judgments of the Court of Appeals Judgments of the Supreme Court Complaints in SCSC against PAK Decisions Complaints to the Panel of the SCSC Response to Defence of the SCSC LTD Prishtina Prishtina Prishtina Gjilan Ferizaj Prizren Gjakove Peja Mitrovica TOTAL Table 38: Activities carried out by the Division for Inter-Institutional Representation and Cooperation Source: Report from Legal Services Rejoinders to SCSC Legal opinions and advice Responses to various case files Legal Property Requirements Participation in Committees and Groups. page 47

48 15. COMPLAINTS OF TAXPAYERS The Complaints Directorate has developed and implemented activities based on legal responsibilities. It has received a total of 537 complaints, whereas 40 complaints were transferred from the previous year, thus totalling to 577 complaints. The complaints are disaggregated by type. For audits: - 15 complaints transferred from complaints were received in complaints were reviewed in complaints transferred to 2018 Complaints in field activities and on fine imposing decisions: - 20 complaints transferred from complaints were received in complaints were reviewed in complaints transferred from to 2018 Complaints from the Court, Taxpayer Advocate and other matters: - 5 complaints transferred from complaints were received in complaints were reviewed in complaints transferred to 2018 From the total of complaints, we have the reports as follows: total complaints transferred and received - 19 complaints resulted positive complaints resulted negative - 29 complaints partially - 17 complaints have expired - 86 complaints re-audit - 5 complaints revision - 58 complaints in process page 48

49 16. INFORMATION TECHNOLOGY Alongside the routine work and development of current projects within the IT Department, dedicated teams and officials from the work processes have been engaged in the on-going activities in the development of processes and working systems for the needs of TAK and other relevant institutions. Particular emphasis was put on the project of fiscal receipts envelopes management with, the preparations for accepting the payments with health contributions. The project of FATCA reporting to U.S. IRS, basic preparations for the project of receiving books on sales/purchases of taxpayers on VAT, cooperation in the inter-institutional communication project with the rule of law institutions, where TAK is represented by a member of the Coordination Committee. In the framework of international cooperation, an agreement with the Korean Internet Security Agency (KISA) has been signed, where we initially received technical assistance from cyber security experts and it is expected a continued cooperation and support from this agency to TAK. Based on the work plans and the available budget, we are supplied with equipment for IT and user needs, such as storage, PC, printer, etc. The Fiscal Cash Register Management System (CRMS) project has been completed. Prepared and implemented/updated: Implementation of the PRTG Application; Implementation of the System Centre Virtual Machine Manager; Upgrade of the mail server from the current version of Exchange 2010 to a new Exchange 2016 (to be continued in 2018); Supporting advancement and management of SMA; Upgrade of SharePoint from 2010 to 2016; System Security (Blocking Access to Windows Registry, Cmd, PowerShell; GPO Configuration). Also, there are systems and services provided for all temporary admitted staff according to the needs of regional offices. Expand and improve the basic functions of the SIGTAS application as well as advanced functions. Various activities have been carried out such as the maintenance and support of SIGTAS, including problem identification, reviews, re-reviews, case completion, assistance, and number of reviewed, tested and re-tested, closed and open matters, etc. IT was assisted in maintenance and upgrading of SIGTAS special modules such as: collection module, evaluation module and reminders, registration, as well as maintenance of all SIGTAS forms and reports and necessary procedures. The VKME, SMRM, SMA application and the envelope management application have been updated and extended. The Salary calculator (from Gross to Net and vice versa, both for primary and secondary employers) has been designed and published. Electronic Archive, e-deklarimi- Electronic Declarations, efiling- EDI-Electronic Declaration has been updated. page 49

50 The Book Module: Purchase Book and Book of Sales is functionalized. Purchases over 500 euros. VAT registration through EDI. Web Services for E-Payments; Implementation of the Digital Tax Certificate, through which this system enables the provision of tax certificate for natural persons and businesses (with the approval of the tax officer) Advancing and maintaining of the web-service with KBRA for registration of One-Stop-Shop businesses by business type. DOSSIER for downloading forms; List of passive businesses; Support and maintenance of applications; Technical Support Application; Application for daily activity registration; Human Resource Management Application; Management of fiscal receipts; Application for managing reports for Visits, Checks, Meetings (VKME); Call centre; Management of case collection. 17. EXECUTIVE OFFICE During this period, TAK General Director held 24 meetings with the High-Level Management, whereby it was discussed about topics related to the implementation of the Strategic Plan and Operational Plans and other topics of interest in order to achieve the planned objectives for this period. 206 meetings were held with local and international institutions and 101 other meetings were held with foreign and domestic parties as per request. During this period, TAK General Director had 22 media appearances, where topics such as Kosovo's tax system, new fiscal system, reimbursement campaign, revenue performance, collection of debts as well as other topics of interest to the public, were addressed. The Executive Office through the Public Communication Office has been continuously engaged in implementing the objectives based on the Media Plan and Communication Plan foreseen in the Annual Work Plan for 2017, undertaking thus numerous activities. Even during this period, the Communications Office has arranged the section of presentations in the media, thus initiating interviews and announcements for electronic and written media. During 2017, TAK had 63 media appearances, where it discussed various topics related to current TAK activities, provision of new services, achievements and progress that TAK has recorded during this period. TAK developments and activities have always been present in the media, through press releases, where we have published 90 press releases. A total of 119 responses have been provided to journalists - Mainly on topics related to the progress of revenue for 2017, games of chance activities, the effects of the law on debt forgiveness, the fiscalization of oil companies, the tax obligations of the singers, the reimbursement campaign, etc. page 50

51 The Communications Office during this period has developed media campaigns through publication of announcements for taxpayers in daily newspapers, where 22 notices/public rulings for taxpayers have been published. We have organized 5 press conferences for the purpose of disclosing TAK activities, as well as organized regular meetings with stakeholders. The Public Communications Office is responsible for maintaining and updating information on the website: TAK Facebook and SharePoint. page 51

52 18. INTERNATIONAL RELATIONS Agreements on Elimination of Double Taxation The support team, established by the decision of the Minister of Finance, held four meetings for the drafting of the action plan for the initiation of international agreements. As a result, 15 initiating letters have been sent to 15 European Union countries and to Kuwait and Qatar. The support team also drafted 11 drafts of AEDT which were sent for approval as an initiative in the Government of Kosovo. AEDT between Kosovo and Croatia was signed in March It was also signed an Agreement on Elimination of Double Taxation between Kosovo and Switzerland. The AEDT between Kosovo and Luxembourg was signed in December Concerning the negotiations on the AEDT, the negotiation cycle with Austria is concluded, which is expected to be signed at ministerial level, whereas in November 2017 has started the re-negotiation of AEDT between Kosovo and Germany. During the reporting period, the AEDTs between the United Arab Emirates and Kosovo and between Kosovo and Croatia also entered into force. 30 questions regarding the implementation of the AEDT have been addressed. A total of 243 Residence Certificates were issued. In the field of exchange of tax information under the AEDT, a total of 7 requests for tax information were addressed. Technical Assistance from Donors GIZ - In this regard, 12 meetings with GIZ were held during 2017, where it was discussed for the assessment of the current development of joint activities as well as the planning of missions/expertise for OFAP, the development of the OFAP unit and the use of electronic audits at the Large Taxpayers Directorate and the Tax Investigation Unit. During 2017, GIZ supported two trainings that were organized in Slovenia, the Centre of Excellence in Finance. Support was also provided to the training TAK officials in the field of Information Technology, held in Germany. A study visit organized by the German Ministry of Finance for TAK was also supported. Seven expert missions were organized by experts from the Bavarian Tax Administration, which were focused on holding workshops for using the electronic audit tools by the Tax Investigation and Intelligence Unit and in organizing a workshop for completing the Audit Handbook and conducting a general case study. It is worth pointing out that the use of the electronic audit tools has been evaluated by licensed officials. With the support of the expert on specific issues, meetingsworkshops were held for support through the provision of advice on specific issues from the VAT area. page 52

53 Regarding the OFAP unit, several missions were organized by the expert from the Bavarian Tax Administration, which provides capacity building support to the OFAP unit. In the missions of 2017, it was discussed and provided advice on the necessary amendments to legal framework in order to expand this office in the field of tax investigations, and a workshop was held whereby made possible finalization of the manual for internal use related to OFAP. In June 2017, TAK held a consultative meeting organized by the Project for Legal and Administrative Reform from GIZ, a project aimed at strengthening the capacities of the Judiciary and Administrative Officers with emphasis on increasing the cooperation between TAK and Court officials during the process of handling cases related to tax issues. In this regard, a study visit was also conducted in Germany, where, in addition to officials from other institutions, there were also 1 official from TAK. As a continuation of the support from GIZ for conducting the second Taxpayers Survey, meetings were held for the compilation of the questionnaire whereby was made able its finalization with focus groups. IMF - During the reporting period, a meeting was held with the Head of the IMF missions at TAK, the purpose of which was to identify areas for cooperation for In this regard, TAK has proposed that cooperation be in the field of Information Technology, implementation of IMF recommendations from the Debt Management Mission, Risk Management, voluntary compliance and handling of cases in the banking and insurance sectors. In April 2017, technical assistance (TA) was implemented on the topic "Progress in improvements in declaration and payment compliance and reduction of tax debts". The next technical assistance from the IMF was carried out in June 2017 regarding the Compliance Risk Management. In May 2017, it was held the 2nd annual meeting on "Strengthening economic governance and public finance management in South Eastern Europe" for coordination of technical assistance to countries in the region, organized by the IMF and the European Commission in Ljubljana. At the meeting, TAK has presented the technical assistance implemented so far and areas identified as having priority to cooperate with the IMF and the EC. Also in 2017, there were organized two TAs in the field of Information Technology regarding the data quality analysis in the database and the updating of the requirements in the file for the new information technology system. In October 2017, the main mission was organized by the Fiscal Affairs Department within the IMF, which aimed to analyse the current state of implementation of TAK strategy for , and recommendations from previous missions by the IMF. page 53