VALUE AND MOMENTUM EVERYWHERE

|

|

|

- Melinda Fields

- 6 years ago

- Views:

Transcription

1 AQR Capital Management, LLC Two Greenwich Plaza, Third Floor Greenwich, CT T: F: VALUE AND MOMENTUM EVERYWHERE Clifford S. Asness AQR Capital Management, LLC Tobias J. Moskowitz University of Chicago, Booth School and NBER Lasse H. Pedersen NYU, CEPR, and NBER The information set forth herein has been obtained or derived from sources believed by the author to be reliable. However, the author does not make any representation or warranty, express or implied, as to the information s accuracy or completeness, nor does the author recommend that the attached information serve as the basis of any investment decision. This document has been provided to you solely for information purposes and does not constitute an offer or solicitation of an offer, or any advice or recommendation, to purchase any securities or other financial instruments, and may not be construed as such. This document is intended exclusively for the use of the person to whom it has been delivered by the author, and it is not to be reproduced or redistributed to any other person.

2 Motivation Some of the most studied capital market phenomena are Value effect: assets with high book value -to-market value outperform low ones Momentum effect: recent relative winners outperform recent relative losers Value and momentum are often studied only separately only in certain asset classes only one asset class at a time 2

3 Literature Literature US stock selection (Statman (1980), Fama-French (1992), Jegadeesh and Titman (1993), Asness (1994)) Stocks in other countries (Fama and French (1998), Rouwenhorst (1998), Liew and Vassalou (2000), Griffin and Martin (2003), Chui, Titman, Wei (2002)) Country equity indices (Asness, Liew, and Stevens (1997), Bhojraj and Swaminathan (2006)) Currency momentum (Shleifer and Summers (1990), Kho (1996), LeBaron (1999)) Commodity momentum (Gorton, Hayashi and Rouwenhorst (2007)) Value effects in currencies and commodities (?) Value and momentum in government bonds (?) 3

4 What We Do Extend and unify analysis of value and momentum (almost) everywhere Breadth of asset classes and markets studied in a unified setting simultaneously Combining asset classes and combining value with momentum large economic and statistical gains Gain insight by looking across asset classes and globally at once Identify connections between value and momentum across markets Providing evidence for common global phenomena/ factors Consider common explanations: macro and liquidity risks New evidence consistent with or against existing theories for these phenomena Rational explanations---common factor structure, production-based theories? Behavioral explanations---misreaction to idiosyncratic information? 4

5 Main Results Value and momentum effects appear in all of the major asset classes Value and momentum strategies both have positive Sharpe ratios despite being negatively correlated Therefore, a 50/50 combination has higher Sharpe than either stand alone Large diversification benefits from combining asset classes globally: 1. Economic power of the combined asset class portfolios 2. Statistical power of the combined portfolio reduces noise Striking co-movement patterns across asset classes: Value here correlates with value there Momentum here correlates with momentum there Value and momentum negatively correlated everywhere 5

6 Main Results Macro risk doesn t explain much Liquidity risk: Value loads positively and momentum loads negatively on our measure of funding liquidity risk Liquidity risk is priced and may explain part of value premium, but makes momentum more puzzling Partly explains global comovement patterns and negative correlation between value and momentum Interesting dynamic effects: Importance of liquidity risk increases significantly over time, rising sharply after the summer of 1998 Over time, value and momentum both become less profitable, more correlated across markets and asset classes, and more correlated with each other 6

7 Main Results These risks and patterns are statistically present when looking everywhere Not easy to detect these in any single strategy or asset class Liquidity risk and dynamics may point to the importance of trading costs and limited arbitrage in explaining these phenomena But, there is a lot left to be explained We re planning to make our data available for other researchers and to maintain it going forward at: 7

8 Overview of Talk Data and methodology New facts on performance of value and momentum everywhere Co-movement patterns Exposures to macroeconomic and liquidity risks The power of looking everywhere at once Some interesting dynamics 8

9 Data Sources Stock selection U.S.: Universe: CRSP common equity with a recent book value, at least 12 months of returns, excluding ADR s, foreign shares REITS, financials, closed-end funds, stocks with share prices less than $1, and stocks in bottom quartile of market cap. Focus on top half of remaining universe based on market cap (top 37.5% of total universe). Prices and returns: CRSP Book values: Compustat U.K., Japan, Continental Europe: Universe: BARRA with recent book value from Worldscope, at least 12 months of returns and same filters as US. Prices and returns: Barra Book values: Worldscope Equity country selection Stock index returns and book values: MSCI Bond country selection Returns: Datastream MSCI 10-year government bond index in excess of local short rate Short rate and 10-year government bond yield: Bloomberg Inflation forecasts for next 12 months: analysts estimates compiled by Consensus Economics Currency selection Spot exchange rates: Datastream LIBOR short rates: Bloomberg 9

10 Data Sources Commodity selection Aluminum, Copper, Nickel, Zinc, Lead, Tin: London Metal Exchange (LME) Brent Crude, Gas Oil: Intercontinental Exchange (ICE) Live Cattle, Feeder Cattle, Lean Hogs: Chicago Mercantile Exchange (CME) Corn, Soybeans, Soy Meal, Soy Oil, Wheat: Chicago Board of Trade (CBOT) WTI Crude, RBOB Gasoline, Heating Oil, Natural Gas: New York Mercantile Exchange (NYMEX) Gold, Silver: New York Commodities Exchange (COMEX) Cotton, Coffee, Cocoa, Sugar: New York Board of Trade (NYBOT) Platinum: Tokyo Commodity Exchange (TOCOM) Macro indicators Recession = linear interpolation between peak (=0) and trough dates (=1) US dates from NBER, Non-US dates from Economic Cycle Research Institute Long-run consumption growth = 3-year future growth in per capita consumption (sum of 3-year changes in above) Funding liquidity indicators TED spread (3 month LIBOR minus 3 month T-bill rate), U.S., U.K., Japan, Germany (Bloomberg and International Fund Services (IFS)) 3-month LIBOR minus term repo rate (IFS, various brokers) Supplement with quantity and market liquidity indicators: VIX, Pastor-Stambaugh, Acharya-Pedersen, Sadka, Adrian-Shin. 10

11 Measures of Value and Momentum We use simple and, to the extent possible, standard and uniform measures Momentum: Return from t-12 to t-2 months Value: Stocks: book-to-price Country equity indices: aggregate book-to-price Commodities: book is the average commodity spot price 4.5 to 5.5 years ago Currencies: book is the average exchange rate 4.5 to 5.5 years ago adjusted for interest-rate differentials, i.e. excess return from t-60 to t-1 deviation from UIP, or change in PPP if real rates are constant across countries Bonds: real bond yield, i.e. yield minus expected inflation book is discounted cash-flows using expected inflation 11

12 Lagging Price in the Value Measure We use most recently available price in our value measure Induces some negative correlation between value and momentum within (but not across) asset classes Easy to create highly negatively correlated portfolios, harder to have them both deliver positive expected returns/alphas Replicate using lagged value measures for robustness (appendix in the paper) Using most recent price is a natural value measure (hard to imagine more recent price does not provide useful information) Efficient frontier will look the same 12

13 Methodology Portfolios sorted on value and momentum within each asset class: Three equal groups (high, middle, low) Value-weight for stocks, equal-weight for other asset classes Portfolios based on 50/50 combination of value/momentum: Also examine High Lowspreadreturns Allows us to also examine long vs. short side of trade *Robustness: when combine across asset classes, do both equal-weighting and equalvolatility weighting (e.g., commodities have 5 times the volatility as bonds) 13

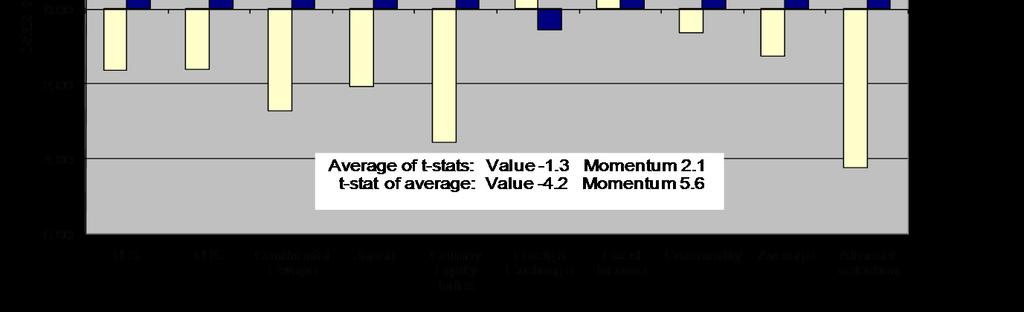

14 Table I: Performance of Value and Momentum Sorted Portfolios Across Markets and Asset Classes 14

15 Table I (cont.) 15

16 Table II: Correlation of Value and Momentum Across Markets and Asset Classes 16

17 Table II (cont.) 17

18 Table IV: Macroeconomic and Liquidity Risk Exposures 18

19 Power of Looking Everywhere: Liquidity Risk 19

20 Economic Magnitudes Statistical correlations we uncover are significant and interesting, but only a starting point Economic magnitudes of premia and correlation structure explained is small Liquidity risk may explain part of value premium and negative correlation between value and momentum, but only makes momentum premium more puzzling A lot left to be explained! 20

21 Dynamics of Value and Liquidity Risk Illiquidity Beta for value over time 21

22 Dynamics of Momentum and Liquidity Risk Illiquidity Beta for momentum over time 22

23 Value in Liquid vs. Illiquid Times 23

24 Momentum in Liquid vs. Illiquid Times 24

25 Conclusions Value and momentum work in a variety of markets and asset classes Their combination works better than either stand alone Large economic and statistical benefits to our unified approach of looking across markets and asset classes Identify interesting global co-movement structure Data hint toward a link between these phenomena and liquidity risk Interesting dynamics related to liquidity risk and extreme events Still far from a full explanation 25

26 Conclusions Theory must accommodate the patterns we uncover: 1. Large Sharpe ratios from combining strategies across asset classes 2. Why value and momentum load oppositely on liquidity risk 3. What causes the link between similar strategies in seemingly different asset classes? 4. What is driving the dynamics we observe? 26

27 Appendix 27

28 Over-Optimistic or Pessimistic for Real-World Implementation? Over-optimistic No transactions or financing costs makes performance closer for stock vs. non-stock and val vs. mom Backtests never hit a funding-liquidity (or confidence) problem Going forward returns may be lower data-mining (though having looked everywhere reduces this risk) because some people trade on these strategies or, not, e.g. because returns are compensation for risk? Over-pessimistic We used only the simplest value and momentum measures; weighting each strategy the same There are many possible improvements (that must be balanced vs. the dangers of data-mining); e.g., improved value/momentum measures, variable strategy weighting (statically and dynamically) 28

29 Current versus Lagged Measures of Value Comparison to Fama-French Portfolios (02/ /2008) 29

30 First principal component for value and momentum strategies 30

31 Comovement Everywhere *Significant at the 5% level. 31

32 Table 5: Asset Pricing Tests 32

33 Table 5: Asset Pricing Tests (cont.) 33

34 Other Liquidity Measures: Correlations 34

35 Table 7: Dynamics of Value and Momentum 35

36 Not Everything Works Everywhere The power of looking everywhere at once can also highlight patterns specific to an asset class or market. Provides a more general test of patterns found in U.S. equities Example: January effect in value and momentum (Table 8) 36

37 Seasonal patterns to correlation structure? Are seasonal effects in value and momentum driving the strong correlation structure? 37

Value and Momentum Everywhere

Value and Momentum Everywhere Clifford S. Asness, Tobias J. Moskowitz, and Lasse H. Pedersen! First Version: March 2008 This Version: February, 2009 Abstract Value and momentum ubiquitously generate abnormal

Value and Momentum Everywhere Clifford S. Asness, Tobias J. Moskowitz, and Lasse H. Pedersen! First Version: March 2008 This Version: February, 2009 Abstract Value and momentum ubiquitously generate abnormal

Value and Momentum Everywhere

Value and Momentum Everywhere Clifford S. Asness, Tobias J. Moskowitz, and Lasse H. Pedersen First Version: March 2008 This Version: June, 2009 Abstract We study jointly the ubiquitous returns to value

Value and Momentum Everywhere Clifford S. Asness, Tobias J. Moskowitz, and Lasse H. Pedersen First Version: March 2008 This Version: June, 2009 Abstract We study jointly the ubiquitous returns to value

Value and Momentum Everywhere

Value and Momentum Everywhere Clifford S. Asness, Tobias J. Moskowitz, and Lasse H. Pedersen 1 Preliminary and Incomplete June, 2008 Abstract We study jointly the returns to value and momentum strategies

Value and Momentum Everywhere Clifford S. Asness, Tobias J. Moskowitz, and Lasse H. Pedersen 1 Preliminary and Incomplete June, 2008 Abstract We study jointly the returns to value and momentum strategies

Carry. Ralph S.J. Koijen, London Business School and NBER

Carry Ralph S.J. Koijen, London Business School and NBER Tobias J. Moskowitz, Chicago Booth and NBER Lasse H. Pedersen, NYU, CBS, AQR Capital Management, CEPR, NBER Evert B. Vrugt, VU University, PGO IM

Carry Ralph S.J. Koijen, London Business School and NBER Tobias J. Moskowitz, Chicago Booth and NBER Lasse H. Pedersen, NYU, CBS, AQR Capital Management, CEPR, NBER Evert B. Vrugt, VU University, PGO IM

Value and Momentum Everywhere

Value and Momentum Everywhere Clifford S. Asness, Tobias J. Moskowitz, and Lasse H. Pedersen Current Version: November, 2011 Abstract The ubiquitous returns to value and momentum strategies have become

Value and Momentum Everywhere Clifford S. Asness, Tobias J. Moskowitz, and Lasse H. Pedersen Current Version: November, 2011 Abstract The ubiquitous returns to value and momentum strategies have become

Are there common factors in individual commodity futures returns?

Are there common factors in individual commodity futures returns? Recent Advances in Commodity Markets (QMUL) Charoula Daskalaki (Piraeus), Alex Kostakis (MBS) and George Skiadopoulos (Piraeus & QMUL)

Are there common factors in individual commodity futures returns? Recent Advances in Commodity Markets (QMUL) Charoula Daskalaki (Piraeus), Alex Kostakis (MBS) and George Skiadopoulos (Piraeus & QMUL)

Commitments of Traders: Commodities

Commitments of Traders: Commodities Leveraged funds positioning covering the week ending March 6, 218 Ole S. Hansen Head of Commodity Strategy 6-Mar-18 Change Change Change Change Pct 1 yr high 1 yr low

Commitments of Traders: Commodities Leveraged funds positioning covering the week ending March 6, 218 Ole S. Hansen Head of Commodity Strategy 6-Mar-18 Change Change Change Change Pct 1 yr high 1 yr low

OVERVIEW OF THE BACHE COMMODITY INDEX SM

OVERVIEW OF THE BACHE COMMODITY INDEX SM March 2010 PFDS Holdings, LLC One New York Plaza, 13th Fl NY, NY 10292-2013 212-778-4000 Disclaimer Copyright 2010 PFDS Holdings, LLC. All rights reserved. The

OVERVIEW OF THE BACHE COMMODITY INDEX SM March 2010 PFDS Holdings, LLC One New York Plaza, 13th Fl NY, NY 10292-2013 212-778-4000 Disclaimer Copyright 2010 PFDS Holdings, LLC. All rights reserved. The

Value and Momentum Everywhere

THE JOURNAL OF FINANCE VOL. LXVIII, NO. 3 JUNE 2013 Value and Momentum Everywhere CLIFFORD S. ASNESS, TOBIAS J. MOSKOWITZ, and LASSE HEJE PEDERSEN ABSTRACT We find consistent value and momentum return

THE JOURNAL OF FINANCE VOL. LXVIII, NO. 3 JUNE 2013 Value and Momentum Everywhere CLIFFORD S. ASNESS, TOBIAS J. MOSKOWITZ, and LASSE HEJE PEDERSEN ABSTRACT We find consistent value and momentum return

Value and Momentum Everywhere

Value and Momentum Everywhere Clifford S. Asness, Tobias J. Moskowitz, and Lasse Heje Pedersen Current Version: June 2012 Abstract We study the returns to value and momentum strategies jointly across eight

Value and Momentum Everywhere Clifford S. Asness, Tobias J. Moskowitz, and Lasse Heje Pedersen Current Version: June 2012 Abstract We study the returns to value and momentum strategies jointly across eight

FNCE4040 Derivatives Chapter 2

FNCE4040 Derivatives Chapter 2 Mechanics of Futures Markets Futures Contracts Available on a wide range of assets Exchange traded Specifications need to be defined: What can be delivered, Where it can

FNCE4040 Derivatives Chapter 2 Mechanics of Futures Markets Futures Contracts Available on a wide range of assets Exchange traded Specifications need to be defined: What can be delivered, Where it can

Morgan Stanley Wealth Management Due Diligence Meeting

Morgan Stanley Wealth Management Due Diligence Meeting Commodities: Taking Advantage of Supply and Demand Fiona English, Client Portfolio Manager 24 26 April 2013, Milan Page 1 I For broker/dealer use

Morgan Stanley Wealth Management Due Diligence Meeting Commodities: Taking Advantage of Supply and Demand Fiona English, Client Portfolio Manager 24 26 April 2013, Milan Page 1 I For broker/dealer use

Macquarie Diversified Commodity Capped Building Block Indices. Index Manual May 2016

Macquarie Diversified Commodity Capped Building Block Indices Manual May 2016 NOTICES AND DISCLAIMERS BASIS OF PROVISION This Manual sets out the rules for the Macquarie Building Block Indices (each, an

Macquarie Diversified Commodity Capped Building Block Indices Manual May 2016 NOTICES AND DISCLAIMERS BASIS OF PROVISION This Manual sets out the rules for the Macquarie Building Block Indices (each, an

ETF.com Presents INSIDE COMMODITIES WEEK

ETF.com Presents INSIDE COMMODITIES WEEK A Practical Guide to Commodity Investing: 5 Things Every Investor Needs to Know November 17, 2014 swaps John T. Hyland, CFA Chief Investment Office United States

ETF.com Presents INSIDE COMMODITIES WEEK A Practical Guide to Commodity Investing: 5 Things Every Investor Needs to Know November 17, 2014 swaps John T. Hyland, CFA Chief Investment Office United States

USCF Mutual Funds TRUST USCF Commodity Strategy Fund

Filed pursuant to Rule 497(e) Securities Act File No. 333-214468 Investment Company Act File No. 811-23213 USCF Mutual Funds TRUST USCF Commodity Strategy Fund Class A Shares (USCFX) and Class I Shares

Filed pursuant to Rule 497(e) Securities Act File No. 333-214468 Investment Company Act File No. 811-23213 USCF Mutual Funds TRUST USCF Commodity Strategy Fund Class A Shares (USCFX) and Class I Shares

Commitments of Traders: Commodities

Commitments of Traders: Commodities Leveraged funds positioning covering the week ending May 8, 218 Ole S. Hansen Head of Commodity Strategy 8-May-18 Change Change Change Change Pct 1 yr high 1 yr low

Commitments of Traders: Commodities Leveraged funds positioning covering the week ending May 8, 218 Ole S. Hansen Head of Commodity Strategy 8-May-18 Change Change Change Change Pct 1 yr high 1 yr low

Commitments of Traders: Commodities

Commitments of Traders: Commodities Leveraged funds positioning covering the week ending June 19, 218 Ole S. Hansen Head of Commodity Strategy 19-Jun-18 Change Change Change Change Pct 1 yr high 1 yr low

Commitments of Traders: Commodities Leveraged funds positioning covering the week ending June 19, 218 Ole S. Hansen Head of Commodity Strategy 19-Jun-18 Change Change Change Change Pct 1 yr high 1 yr low

Commitments of Traders: Commodities

Commitments of Traders: Commodities Leveraged funds positioning covering the week ending June 26, 218 Ole S. Hansen Head of Commodity Strategy 26-Jun-18 Change Change Change Change Pct 1 yr high 1 yr low

Commitments of Traders: Commodities Leveraged funds positioning covering the week ending June 26, 218 Ole S. Hansen Head of Commodity Strategy 26-Jun-18 Change Change Change Change Pct 1 yr high 1 yr low

Principles of Portfolio Construction

Principles of Portfolio Construction Salient Quantitative Research, February 2013 Today s Topics 1. Viewing portfolios in terms of risk 1. The language of risk 2. Calculating an allocation s risk profile

Principles of Portfolio Construction Salient Quantitative Research, February 2013 Today s Topics 1. Viewing portfolios in terms of risk 1. The language of risk 2. Calculating an allocation s risk profile

Commitments of Traders: Commodities

Commitments of Traders: Commodities Leveraged funds positioning covering the week ending July 3, 218 Ole S. Hansen Head of Commodity Strategy 3-Jul-18 Change Change Change Change Pct 1 yr high 1 yr low

Commitments of Traders: Commodities Leveraged funds positioning covering the week ending July 3, 218 Ole S. Hansen Head of Commodity Strategy 3-Jul-18 Change Change Change Change Pct 1 yr high 1 yr low

Commitments of Traders: Commodities

Commitments of Traders: Commodities Leveraged funds positioning covering the week ending July 1, 218 Ole S. Hansen Head of Commodity Strategy 1-Jul-18 Change Change Change Change Pct 1 yr high 1 yr low

Commitments of Traders: Commodities Leveraged funds positioning covering the week ending July 1, 218 Ole S. Hansen Head of Commodity Strategy 1-Jul-18 Change Change Change Change Pct 1 yr high 1 yr low

Description of the. RBC Commodity Excess Return Index and RBC Commodity Total Return Index

Description of the RBC Commodity Excess Return Index and RBC Commodity Total Return Index This document contains information about the RBC Commodity Excess Return Index and RBC Commodity Total Return Index,

Description of the RBC Commodity Excess Return Index and RBC Commodity Total Return Index This document contains information about the RBC Commodity Excess Return Index and RBC Commodity Total Return Index,

Thinking. Alternative. Third Quarter The Role of Alternative Beta Premia

Alternative Thinking The Role of Alternative Beta Premia While risk parity strategies are our highest-capacity answer for investing in long-only, core asset classes, alternative beta premia dynamic long-short

Alternative Thinking The Role of Alternative Beta Premia While risk parity strategies are our highest-capacity answer for investing in long-only, core asset classes, alternative beta premia dynamic long-short

/ CRB Index May 2005

May 2005 / CRB Index Overview: Past, Present and Future Founded in 1957, the Reuters CRB Index has a long history as the most widely followed Index of commodities futures. Since 1961, there have been 9

May 2005 / CRB Index Overview: Past, Present and Future Founded in 1957, the Reuters CRB Index has a long history as the most widely followed Index of commodities futures. Since 1961, there have been 9

Building a Better Commodities Portfolio

Bradley Kay Summer 2012 Portfolio Solutions Group Ari Levine Vice President Yao Hua Ooi Principal Lasse H. Pedersen, Ph.D. Principal Building a Better Commodities Portfolio Executive Summary Institutional

Bradley Kay Summer 2012 Portfolio Solutions Group Ari Levine Vice President Yao Hua Ooi Principal Lasse H. Pedersen, Ph.D. Principal Building a Better Commodities Portfolio Executive Summary Institutional

Bache Commodity Index SM. Q Review

SM Bache Commodity Index SM Q3 2009 Review The Bache Commodity Index SM Built for Commodity Investors The Bache Commodity Index SM (BCI SM ) is a transparent, fully investable commodity index. Its unique

SM Bache Commodity Index SM Q3 2009 Review The Bache Commodity Index SM Built for Commodity Investors The Bache Commodity Index SM (BCI SM ) is a transparent, fully investable commodity index. Its unique

BLOOMBERG COMMODITY INDEX 2018 TARGET WEIGHTS

BLOOMBERG COMMODITY INDEX 2018 TARGET WEIGHTS 2018 SUMMARY 26 commodity contracts tested for inclusion No constituent changes (22 commodities constituents / 20 commodities) Energy reaches lowest weight

BLOOMBERG COMMODITY INDEX 2018 TARGET WEIGHTS 2018 SUMMARY 26 commodity contracts tested for inclusion No constituent changes (22 commodities constituents / 20 commodities) Energy reaches lowest weight

Comovement and the. London School of Economics Grantham Research Institute. Commodity Markets and their Financialization IPAM May 6, 2015

London School of Economics Grantham Research Institute Commodity Markets and ir Financialization IPAM May 6, 2015 1 / 35 generated uncorrelated returns Commodity markets were partly segmented from outside

London School of Economics Grantham Research Institute Commodity Markets and ir Financialization IPAM May 6, 2015 1 / 35 generated uncorrelated returns Commodity markets were partly segmented from outside

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited) June 30, 2017

June 30, 2017") CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited) June 30, 2017 SHARES VALUE EXCHANGE-TRADED FUNDS - 10.2% Guggenheim Ultra Short Duration ETF 1 108,400 $ 5,452,520 Total Exchange-Traded Funds (Cost $5,429,550)

CONSOLIDATED SCHEDULE OF INVESTMENTS (Unaudited) June 30, 2017 SHARES VALUE EXCHANGE-TRADED FUNDS - 10.2% Guggenheim Ultra Short Duration ETF 1 108,400 $ 5,452,520 Total Exchange-Traded Funds (Cost $5,429,550)

Ferreting out the Naïve One: Positive Feedback Trading and Commodity Equilibrium Prices. Jaap W. B. Bos Paulo Rodrigues Háng Sūn

Ferreting out the Naïve One: Positive Feedback Trading and Commodity Equilibrium Prices Jaap W. B. Bos Paulo Rodrigues Háng Sūn Extra large volatilities of commodity prices. Coincidence with Commodity

Ferreting out the Naïve One: Positive Feedback Trading and Commodity Equilibrium Prices Jaap W. B. Bos Paulo Rodrigues Háng Sūn Extra large volatilities of commodity prices. Coincidence with Commodity

KEY CONCEPTS. Understanding Commodities

KEY CONCEPTS Understanding Commodities TABLE OF CONTENTS WHAT ARE COMMODITIES?... 3 HOW COMMODITIES ARE TRADED... 3 THE BENEFITS OF COMMODITY TRADING...5 WHO TRADES COMMODITIES?...6 TERMINOLOGY... 7 UNDERSTANDING

KEY CONCEPTS Understanding Commodities TABLE OF CONTENTS WHAT ARE COMMODITIES?... 3 HOW COMMODITIES ARE TRADED... 3 THE BENEFITS OF COMMODITY TRADING...5 WHO TRADES COMMODITIES?...6 TERMINOLOGY... 7 UNDERSTANDING

Hedge Funds, Hedge Fund Beta, and the Future for Both. Clifford Asness. Managing and Founding Principal AQR Capital Management, LLC

Hedge Funds, Hedge Fund Beta, and the Future for Both Clifford Asness Managing and Founding Principal AQR Capital Management, LLC An Alternative Future Seven years ago, I wrote a paper about hedge funds

Hedge Funds, Hedge Fund Beta, and the Future for Both Clifford Asness Managing and Founding Principal AQR Capital Management, LLC An Alternative Future Seven years ago, I wrote a paper about hedge funds

Betting Against Beta

Betting Against Beta Andrea Frazzini AQR Capital Management LLC Lasse H. Pedersen NYU, CEPR, and NBER Copyright 2010 by Andrea Frazzini and Lasse H. Pedersen The views and opinions expressed herein are

Betting Against Beta Andrea Frazzini AQR Capital Management LLC Lasse H. Pedersen NYU, CEPR, and NBER Copyright 2010 by Andrea Frazzini and Lasse H. Pedersen The views and opinions expressed herein are

First Trust Global Tactical Commodity Strategy Fund (FTGC) Consolidated Portfolio of Investments March 31, 2018 (Unaudited) Stated.

Consolidated Portfolio of Investments March 31, 2018 (Unaudited) Stated.") Consolidated Portfolio of Investments Principal Description Stated Coupon Stated Maturity TREASURY BILLS 80.1% $ 48,000,000 U.S. Treasury Bill (a)... (b) 04/12/18 $ 47,978,254 10,000,000 U.S. Treasury

Consolidated Portfolio of Investments Principal Description Stated Coupon Stated Maturity TREASURY BILLS 80.1% $ 48,000,000 U.S. Treasury Bill (a)... (b) 04/12/18 $ 47,978,254 10,000,000 U.S. Treasury

Futures Perfect? Pension Investment in Futures Markets

Futures Perfect? Pension Investment in Futures Markets Mark Greenwood F.I.A. 28 September 2017 FUTURES PERFECT? applications to pensions futures vs OTC derivatives tour of futures markets 1 The futures

Futures Perfect? Pension Investment in Futures Markets Mark Greenwood F.I.A. 28 September 2017 FUTURES PERFECT? applications to pensions futures vs OTC derivatives tour of futures markets 1 The futures

Weekly Flows by Sector (US$mn) Top 5 Inflows/Outflows (US$mn) Top 5 / Bottom 5 Performers. Diversified Energy Industrial

Top 5 Inflows/Outflows (US$mn) Top 5 / Bottom 5 Performers. Diversified Energy Industrial") Weekly Flows by Sector (US$mn) TOTAL -22 Diversified Energy Industrial Precious -165 Agriculture Livestock Equities FX -4-2 -39-1 8 1-3 -2-1 1 Top 5 Inflows/Outflows (US$mn) Coffee Soybeans Cotton USD

Weekly Flows by Sector (US$mn) TOTAL -22 Diversified Energy Industrial Precious -165 Agriculture Livestock Equities FX -4-2 -39-1 8 1-3 -2-1 1 Top 5 Inflows/Outflows (US$mn) Coffee Soybeans Cotton USD

Pricing Supplement Dated November 16, 2012

Pricing Supplement Dated November 16, 2012 To the Product Prospectus Supplement ERN-COMM-1 Dated February 24, 2011, Prospectus Supplement Dated January 28, 2011, and Prospectus Dated January 28, 2011 $4,834,000

Pricing Supplement Dated November 16, 2012 To the Product Prospectus Supplement ERN-COMM-1 Dated February 24, 2011, Prospectus Supplement Dated January 28, 2011, and Prospectus Dated January 28, 2011 $4,834,000

NASDAQ Commodity Index Family

Index Overview NASDAQ Commodity Index Family The NASDAQ Commodity Index Family provides a broad way to track U.S. dollar denominated commodities traded on U.S. and U.K. exchanges. NASDAQ s transparent

Index Overview NASDAQ Commodity Index Family The NASDAQ Commodity Index Family provides a broad way to track U.S. dollar denominated commodities traded on U.S. and U.K. exchanges. NASDAQ s transparent

First Trust Global Tactical Commodity Strategy Fund (FTGC) Consolidated Portfolio of Investments September 30, 2017 (Unaudited) Stated.

Consolidated Portfolio of Investments September 30, 2017 (Unaudited) Stated.") Consolidated Portfolio of Investments Principal Description Stated Coupon Stated Maturity TREASURY BILLS 61.0% $ 30,000,000 U.S. Treasury Bill (a)... (b) 10/19/17 $ 29,987,055 15,000,000 U.S. Treasury

Consolidated Portfolio of Investments Principal Description Stated Coupon Stated Maturity TREASURY BILLS 61.0% $ 30,000,000 U.S. Treasury Bill (a)... (b) 10/19/17 $ 29,987,055 15,000,000 U.S. Treasury

ETF Securities Weekly Flows Analysis ETP investors bargain-hunt as commodities capitulate

Nitesh Shah Director - Commodity Strategist research@etfsecurities.com 8 May 217 ETF Securities Weekly Flows Analysis ETP investors bargain-hunt as commodities capitulate Oil ETPs continue to see inflows

Nitesh Shah Director - Commodity Strategist research@etfsecurities.com 8 May 217 ETF Securities Weekly Flows Analysis ETP investors bargain-hunt as commodities capitulate Oil ETPs continue to see inflows

UBS Bloomberg CMCI. a b. A new perspective on commodity investments.

a b Structured investment products for investors in Switzerland and Liechtenstein. For marketing purposes only. UBS Bloomberg CMCI A new perspective on commodity investments. UBS Bloomberg CMCI Index Universe

a b Structured investment products for investors in Switzerland and Liechtenstein. For marketing purposes only. UBS Bloomberg CMCI A new perspective on commodity investments. UBS Bloomberg CMCI Index Universe

Handelsbanken Index Update Log. Version as of 1 June 2016

Handelsbanken Index Update Log Version as of 1 June 2016 Handelsbanken Nordic Low Volatility 40 Index (SEK) Announcement Date 2016-06-01 Implementation Date 2016-06-01 Changed Definition(s) Corporate Action

Handelsbanken Index Update Log Version as of 1 June 2016 Handelsbanken Nordic Low Volatility 40 Index (SEK) Announcement Date 2016-06-01 Implementation Date 2016-06-01 Changed Definition(s) Corporate Action

Weekly Flows by Sector (US$mn) Top 5 Inflows/Outflows (US$mn) Top 5 / Bottom 5 Performers. Diversified Energy Industrial

Top 5 Inflows/Outflows (US$mn) Top 5 / Bottom 5 Performers. Diversified Energy Industrial") Weekly Flows by Sector (US$mn) TOTAL -153 Diversified Energy Industrial Precious -195 Agriculture Livestock Equities FX -2-3 -1 3 2 26-3 -2-1 1 Top 5 Inflows/Outflows (US$mn) EUR JPY Cotton Agriculture

Weekly Flows by Sector (US$mn) TOTAL -153 Diversified Energy Industrial Precious -195 Agriculture Livestock Equities FX -2-3 -1 3 2 26-3 -2-1 1 Top 5 Inflows/Outflows (US$mn) EUR JPY Cotton Agriculture

BZX Information Circular EDGA Information Circular BYX Information Circular EDGX Information Circular

BZX Information Circular 17-064 EDGA Information Circular 17-064 BYX Information Circular 17-064 EDGX Information Circular 17-064 Date: May 23, 2017 Re: GraniteShares ETF Trust Pursuant to the Rules of

BZX Information Circular 17-064 EDGA Information Circular 17-064 BYX Information Circular 17-064 EDGX Information Circular 17-064 Date: May 23, 2017 Re: GraniteShares ETF Trust Pursuant to the Rules of

Weekly Flows by Sector (US$mn) Top 5 Inflows/Outflows (US$mn) Top 5 / Bottom 5 Performers TOTAL. Diversified Energy Industrial Precious

Top 5 Inflows/Outflows (US$mn) Top 5 / Bottom 5 Performers TOTAL. Diversified Energy Industrial Precious") Weekly Flows by Sector (US$mn) TOTAL Diversified Energy Industrial Precious Agriculture Livestock Equities FX -5-4 9 1 7 12 48 69-5 5 1 Top 5 Inflows/Outflows (US$mn) Industrial metals Energy Copper USD

Weekly Flows by Sector (US$mn) TOTAL Diversified Energy Industrial Precious Agriculture Livestock Equities FX -5-4 9 1 7 12 48 69-5 5 1 Top 5 Inflows/Outflows (US$mn) Industrial metals Energy Copper USD

Opal Financial Group FX & Commodity Summit for Institutional Investors Chicago. Term Structure Properties of Commodity Investments

Opal Financial Group FX & Commodity Summit for Institutional Investors Chicago Term Structure Properties of Commodity Investments March 20, 2007 Ms. Hilary Till Co-editor, Intelligent Commodity Investing,

Opal Financial Group FX & Commodity Summit for Institutional Investors Chicago Term Structure Properties of Commodity Investments March 20, 2007 Ms. Hilary Till Co-editor, Intelligent Commodity Investing,

Bache Commodity Long/Short Index Annual Review

Bache Commodity Long/Short Index 2010 Annual Review Table of Contents Performance Summary 1 Sector Analysis 2 Contribution of BCLSI Return Factors 3 Changes to the Long/Short Index Methodology 3 Commodity

Bache Commodity Long/Short Index 2010 Annual Review Table of Contents Performance Summary 1 Sector Analysis 2 Contribution of BCLSI Return Factors 3 Changes to the Long/Short Index Methodology 3 Commodity

Weekly Flows by Sector (US$mn) Top 5 Inflows/Outflows (US$mn) Top 5 / Bottom 5 Performers. TOTAL Diversified Energy Industrial

Top 5 Inflows/Outflows (US$mn) Top 5 / Bottom 5 Performers. TOTAL Diversified Energy Industrial") Weekly Flows by Sector (US$mn) TOTAL Diversified Energy Industrial Precious -81 Agriculture Livestock Equities FX -3-38 -1 2 8 5 75-1 -5 5 1 Top 5 Inflows/Outflows (US$mn) Agriculture Copper USD Coffee

Weekly Flows by Sector (US$mn) TOTAL Diversified Energy Industrial Precious -81 Agriculture Livestock Equities FX -3-38 -1 2 8 5 75-1 -5 5 1 Top 5 Inflows/Outflows (US$mn) Agriculture Copper USD Coffee

INTRODUCING RISK PARITY ON MOMENTUM AND CARRY PORTFOLIOS. Teresa Botelho Neves 1029

A Work Project, presented as part of the requirements for the Award of a Masters Degree in Finance from the NOVA School of Business and Economics INTRODUCING RISK PARITY ON MOMENTUM AND CARRY PORTFOLIOS

A Work Project, presented as part of the requirements for the Award of a Masters Degree in Finance from the NOVA School of Business and Economics INTRODUCING RISK PARITY ON MOMENTUM AND CARRY PORTFOLIOS

CMCI Active (January 2011) Flexibility & Performance

Flexibility & Performance") CMCI Active (January 0) Flexibility & Performance Executive Summary CMCI Active index gives you the benefit of innovative UBS Bloomberg CMCI methodology and the flexibility to change the Index exposure

CMCI Active (January 0) Flexibility & Performance Executive Summary CMCI Active index gives you the benefit of innovative UBS Bloomberg CMCI methodology and the flexibility to change the Index exposure

Discussion of: Carry. by: Ralph Koijen, Toby Moskowitz, Lasse Pedersen, and Evert Vrugt. Kent Daniel. Columbia University, Graduate School of Business

Discussion of: Carry by: Ralph Koijen, Toby Moskowitz, Lasse Pedersen, and Evert Vrugt Kent Daniel Columbia University, Graduate School of Business LSE Paul Woolley Center Annual Conference 8 June, 2012

Discussion of: Carry by: Ralph Koijen, Toby Moskowitz, Lasse Pedersen, and Evert Vrugt Kent Daniel Columbia University, Graduate School of Business LSE Paul Woolley Center Annual Conference 8 June, 2012

Consolidated Schedule of Investments January 31, 2018 (Unaudited)

") Consolidated Schedule of Investments January 31, 2018 (Unaudited) Interest Rate Maturity Date Principal Amount Value U.S. Treasury Securities 29.81% U.S. Treasury Bills 13.56% (a) U.S. Treasury Bills (b)

Consolidated Schedule of Investments January 31, 2018 (Unaudited) Interest Rate Maturity Date Principal Amount Value U.S. Treasury Securities 29.81% U.S. Treasury Bills 13.56% (a) U.S. Treasury Bills (b)

Extending Benchmarks For Commodity Investments

University of Pennsylvania ScholarlyCommons Summer Program for Undergraduate Research (SPUR) Wharton Undergraduate Research 2017 Extending Benchmarks For Commodity Investments Vinayak Kumar University

University of Pennsylvania ScholarlyCommons Summer Program for Undergraduate Research (SPUR) Wharton Undergraduate Research 2017 Extending Benchmarks For Commodity Investments Vinayak Kumar University

USCF Dynamic Commodity Insight Monthly Insight September 2018

Key Takeaways The US Commodity Index Fund (USCI) and the USCF SummerHaven Dynamic Commodity Strategy No K-1 Fund (SDCI) gained 1.94% and 1.84%, respectively, last month as September was the best month

Key Takeaways The US Commodity Index Fund (USCI) and the USCF SummerHaven Dynamic Commodity Strategy No K-1 Fund (SDCI) gained 1.94% and 1.84%, respectively, last month as September was the best month

THE ALTERNATIVE BENCHMARK COMMODITY INDEX: A FACTOR-BASED APPROACH TO COMMODITY INVESTMENT

THE ALTERNATIVE BENCHMARK COMMODITY INDEX: A FACTOR-BASED APPROACH TO COMMODITY INVESTMENT AIA RESEARCH REPORT Revised Oct 2015 Contact: Richard Spurgin ALTERNATIVE INVESTMENT ANALYTICS LLC 400 AMITY STREET,

THE ALTERNATIVE BENCHMARK COMMODITY INDEX: A FACTOR-BASED APPROACH TO COMMODITY INVESTMENT AIA RESEARCH REPORT Revised Oct 2015 Contact: Richard Spurgin ALTERNATIVE INVESTMENT ANALYTICS LLC 400 AMITY STREET,

26th International Copper Conference Madrid. Christoph Eibl Chief Executive March 2013

26th International Copper Conference Madrid Christoph Eibl Chief Executive March 2013 Preferences Copper form a Fund Manager s point of view As a strategic investor (i.e. long only) fundamentals rule Deficit

26th International Copper Conference Madrid Christoph Eibl Chief Executive March 2013 Preferences Copper form a Fund Manager s point of view As a strategic investor (i.e. long only) fundamentals rule Deficit

Web Resources. Acknowledgements

GUY BOWER Web Resources Daniels Trading offer comprehensive, reliable and customer-focused commodity futures brokerage services to address all trading preferences. Their website is also a great place for

GUY BOWER Web Resources Daniels Trading offer comprehensive, reliable and customer-focused commodity futures brokerage services to address all trading preferences. Their website is also a great place for

Global economy on track for solid recovery

Global economy on track for solid recovery World real GDP grew by 5 percent in 20 Real GDP growth, percent 8 6 4 2 0-2 -4 Emerging and developing economies Advanced economies World -6 1980 1985 1990 1995

Global economy on track for solid recovery World real GDP grew by 5 percent in 20 Real GDP growth, percent 8 6 4 2 0-2 -4 Emerging and developing economies Advanced economies World -6 1980 1985 1990 1995

6,479,864 (Cost $6,480,320) (c) Net Other Assets and Liabilities 26.1%... 2,286,259 Net Assets 100.0%... $ 8,766,123

(c) Net Other Assets and Liabilities 26.1%... 2,286,259 Net Assets 100.0%... $ 8,766,123") Consolidated Portfolio of Investments Principal TREASURY BILLS 73.9% Description Stated Coupon Stated Maturity $ 1,000,000 U.S. Treasury Bill (a) (b) 4/12/18 $ 999,547 1,500,000 U.S. Treasury Bill (a)

Consolidated Portfolio of Investments Principal TREASURY BILLS 73.9% Description Stated Coupon Stated Maturity $ 1,000,000 U.S. Treasury Bill (a) (b) 4/12/18 $ 999,547 1,500,000 U.S. Treasury Bill (a)

BETASHARES AGRICULTURE ETF CURRENCY HEDGED (SYNTHETIC) ASX CODE: QAG BETASHARES CRUDE OIL INDEX ETF CURRENCY HEDGED (SYNTHETIC) ASX CODE: OOO

ASX CODE: QAG BETASHARES CRUDE OIL INDEX ETF CURRENCY HEDGED (SYNTHETIC) ASX CODE: OOO") BETASHARES FUNDS PRODUCT DISCLOSURE STATEMENT BETASHARES AGRICULTURE ETF CURRENCY HEDGED (SYNTHETIC) ASX CODE: QAG BETASHARES CRUDE OIL INDEX ETF CURRENCY HEDGED (SYNTHETIC) ASX CODE: OOO BETASHARES COMMODITIES

BETASHARES FUNDS PRODUCT DISCLOSURE STATEMENT BETASHARES AGRICULTURE ETF CURRENCY HEDGED (SYNTHETIC) ASX CODE: QAG BETASHARES CRUDE OIL INDEX ETF CURRENCY HEDGED (SYNTHETIC) ASX CODE: OOO BETASHARES COMMODITIES

Commodities: Hedging, Regulation, and Documentation

Commodities: Hedging, Regulation, and Documentation Kathryn F. Murphy Husch Blackwell What is a Commodity? Black s Law Dictionary definition of Commodities: Goods, wares, and merchandise of any kind; movables;

Commodities: Hedging, Regulation, and Documentation Kathryn F. Murphy Husch Blackwell What is a Commodity? Black s Law Dictionary definition of Commodities: Goods, wares, and merchandise of any kind; movables;

Trading Costs of Asset Pricing Anomalies

Trading Costs of Asset Pricing Anomalies Andrea Frazzini AQR Capital Management Ronen Israel AQR Capital Management Tobias J. Moskowitz University of Chicago, NBER, and AQR Copyright 2014 by Andrea Frazzini,

Trading Costs of Asset Pricing Anomalies Andrea Frazzini AQR Capital Management Ronen Israel AQR Capital Management Tobias J. Moskowitz University of Chicago, NBER, and AQR Copyright 2014 by Andrea Frazzini,

CAX Commodity Arbitrage Index. Objectives and Guidelines. Copyright 2009 Alternative-Index Ltd 1

CAX Commodity Arbitrage Index Objectives and Guidelines Copyright 2009 Alternative-Index Ltd www.alternative-index.com 1 Index Objectives Provide an investable benchmark with daily liquidity that covers

CAX Commodity Arbitrage Index Objectives and Guidelines Copyright 2009 Alternative-Index Ltd www.alternative-index.com 1 Index Objectives Provide an investable benchmark with daily liquidity that covers

TRADING THE CATTLE AND HOG CRUSH SPREADS

TRADING THE CATTLE AND HOG CRUSH SPREADS Chicago Mercantile Exchange Inc. (CME) and the Chicago Board of Trade (CBOT) have signed a definitive agreement for CME to provide clearing and related services

TRADING THE CATTLE AND HOG CRUSH SPREADS Chicago Mercantile Exchange Inc. (CME) and the Chicago Board of Trade (CBOT) have signed a definitive agreement for CME to provide clearing and related services

2019 Holiday Trading Schedule Martin Luther King, Jr. Day

2019 Holiday Trading Schedule Martin Luther King, Jr. Day The following schedule is taken from sources that Station believes are accurate and are subject to change. The schedule has been assembled for

2019 Holiday Trading Schedule Martin Luther King, Jr. Day The following schedule is taken from sources that Station believes are accurate and are subject to change. The schedule has been assembled for

Goldman Sachs Commodity Index

600 450 300 29 Jul 1992 188.3 150 0 Goldman Sachs Commodity Index 31 Oct 2007 598 06 Feb 2002 170.25 Average yearly return = 23.8% Jul-94 Jul-95 Jul-96 Jul-97 Jul-98 Jul-99 Jul-00 Jul-01 Jul-02 Jul-03

600 450 300 29 Jul 1992 188.3 150 0 Goldman Sachs Commodity Index 31 Oct 2007 598 06 Feb 2002 170.25 Average yearly return = 23.8% Jul-94 Jul-95 Jul-96 Jul-97 Jul-98 Jul-99 Jul-00 Jul-01 Jul-02 Jul-03

Tue Extended Close Trade Date 1/12/2018 1/12/2018 1/12/2018 1/15/2018 1/15/2018 1/15/2018 1/16/2018 1/16/2018 1/16/2018. Mon Open Trade Date

2018 Holiday Trading Schedule Martin Luther King Day The following schedule is taken from sources that TradeStation believes are accurate and are subject to change. The schedule has been assembled for

2018 Holiday Trading Schedule Martin Luther King Day The following schedule is taken from sources that TradeStation believes are accurate and are subject to change. The schedule has been assembled for

UBS ETC on UBS Bloomberg S&P GSCI Constant Maturity Index

About UBS ETCs UBS Exchange Traded Commodities (ETCs) are simple and efficient products for investors in commodity markets. Through a single stock exchange transaction, they provide instant exposure to

About UBS ETCs UBS Exchange Traded Commodities (ETCs) are simple and efficient products for investors in commodity markets. Through a single stock exchange transaction, they provide instant exposure to

Commodities How to Leverage Opportunity

Commodities How to Leverage Opportunity Investment Conference, Boston, March 2010 Peter Königbauer Senior Portfolio Manager For Broker/Dealer Use Only and Not to be Distributed to the Public Agenda Commodity

Commodities How to Leverage Opportunity Investment Conference, Boston, March 2010 Peter Königbauer Senior Portfolio Manager For Broker/Dealer Use Only and Not to be Distributed to the Public Agenda Commodity

Dynamic Trading with Predictable Returns and Transaction Costs. Dynamic Portfolio Choice with Frictions. Nicolae Gârleanu

Dynamic Trading with Predictable Returns and Transaction Costs Dynamic Portfolio Choice with Frictions Nicolae Gârleanu UC Berkeley, CEPR, and NBER Lasse H. Pedersen New York University, Copenhagen Business

Dynamic Trading with Predictable Returns and Transaction Costs Dynamic Portfolio Choice with Frictions Nicolae Gârleanu UC Berkeley, CEPR, and NBER Lasse H. Pedersen New York University, Copenhagen Business

Bache Commodity Index SM Annual Review

SM Bache Commodity Index SM 2007 Annual Review The Bache Commodity Index SM Built for Commodity Investors The Bache Commodity Index SM (BCI SM ) is a transparent, fully investable commodity index. Our

SM Bache Commodity Index SM 2007 Annual Review The Bache Commodity Index SM Built for Commodity Investors The Bache Commodity Index SM (BCI SM ) is a transparent, fully investable commodity index. Our

Managed futures: An alternative investment strategy in which futures contracts are used as part of the investment strategy. 2

WisdomTree Managed Futures Strategy Funds WTMF MANAGED FUTURES CAN PROVIDE MULTI-LEVEL DIVERSIFICATION Institutional investors have long utilized managed futures strategies as a way to achieve diversification

WisdomTree Managed Futures Strategy Funds WTMF MANAGED FUTURES CAN PROVIDE MULTI-LEVEL DIVERSIFICATION Institutional investors have long utilized managed futures strategies as a way to achieve diversification

THE BLOOMBERG COMMODITY INDEX METHODOLOGY

The data and information (the Information ) presented in this methodology (this Methodology ) reflect the methodology for determining the composition and calculation of the Bloomberg Commodity Index (

The data and information (the Information ) presented in this methodology (this Methodology ) reflect the methodology for determining the composition and calculation of the Bloomberg Commodity Index (

Thanks also to Daniels Trading who provided some of the data and technical assistance.

GUY BOWER Contents 1. Introduction 3 2. Mini Glossary 4 3. Strategy #1: The Bull Spread 6 4. Strategy #2: The Bear Spread 8 5. Strategy #3: The Inter Commodity Spread 10 6. Summation 12 7. About the Author

GUY BOWER Contents 1. Introduction 3 2. Mini Glossary 4 3. Strategy #1: The Bull Spread 6 4. Strategy #2: The Bear Spread 8 5. Strategy #3: The Inter Commodity Spread 10 6. Summation 12 7. About the Author

Known to financial academics

Momentum Investing Finally Accessible for Individual Investors By Tobias J. Moskowitz, PhD Known to financial academics for many years, momentum investing is a powerful tool for building portfolio efficiency,

Momentum Investing Finally Accessible for Individual Investors By Tobias J. Moskowitz, PhD Known to financial academics for many years, momentum investing is a powerful tool for building portfolio efficiency,

ETF Securities Weekly Flows Analysis Safe havens gain traction as trade war escalates

Nitesh Shah Director, Research research@etfsecurities.com 9 April 218 ETF Securities Weekly Flows Analysis Safe havens gain traction as trade war escalates Safe haven demand drives US$23.9mn into long

Nitesh Shah Director, Research research@etfsecurities.com 9 April 218 ETF Securities Weekly Flows Analysis Safe havens gain traction as trade war escalates Safe haven demand drives US$23.9mn into long

December 6, To Our Clients and Friends:

FINAL CFTC RULE ON POSITION LIMITS December 6, 2011 To Our Clients and Friends: On October 18, the U.S. Commodity Futures Trading Commission (the CFTC ) adopted new Part 151 (the Final Rule ) of its regulations

FINAL CFTC RULE ON POSITION LIMITS December 6, 2011 To Our Clients and Friends: On October 18, the U.S. Commodity Futures Trading Commission (the CFTC ) adopted new Part 151 (the Final Rule ) of its regulations

2018 Holiday Trading Schedule Good Friday

2018 Holiday Trading Schedule Good day The following schedule is taken from sources that Station believes are accurate and are subject to change. The schedule has been assembled for information purposes

2018 Holiday Trading Schedule Good day The following schedule is taken from sources that Station believes are accurate and are subject to change. The schedule has been assembled for information purposes

BEMO MONTHLY BULLETIN I EQUITY MARKETS

BEMO MONTHLY BULLETIN I EQUITY MARKETS GLOBAL EQUITY BENCHMARK INDICES Last Price MTD % YTD % 30D Vol World 1270.28 2.90% 1.29% -0.26% Developed 2153.1 3.05% 2.36% -0.40% Emerging 1087.46 1.68% -6.13%

BEMO MONTHLY BULLETIN I EQUITY MARKETS GLOBAL EQUITY BENCHMARK INDICES Last Price MTD % YTD % 30D Vol World 1270.28 2.90% 1.29% -0.26% Developed 2153.1 3.05% 2.36% -0.40% Emerging 1087.46 1.68% -6.13%

BROAD COMMODITY INDEX

BROAD COMMODITY INDEX COMMENTARY + STRATEGY FACTS APRIL 2017 80.00% CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) 60.00% 40.00% 20.00% 0.00% -20.00% -40.00% -60.00% -80.00% ABCERI S&P GSCI ER BCOMM ER

BROAD COMMODITY INDEX COMMENTARY + STRATEGY FACTS APRIL 2017 80.00% CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) 60.00% 40.00% 20.00% 0.00% -20.00% -40.00% -60.00% -80.00% ABCERI S&P GSCI ER BCOMM ER

WISDOMTREE RULES-BASED METHODOLOGY

WISDOMTREE RULES-BASED METHODOLOGY WisdomTree Managed Futures Index Last Updated June 206 Page of 8 WISDOMTREE RULES-BASED METHODOLOGY The WisdomTree Managed Futures Index tracks a diversified portfolio

WISDOMTREE RULES-BASED METHODOLOGY WisdomTree Managed Futures Index Last Updated June 206 Page of 8 WISDOMTREE RULES-BASED METHODOLOGY The WisdomTree Managed Futures Index tracks a diversified portfolio

2018 Holiday Trading Schedule Memorial Day

2018 Holiday Trading Schedule Memorial Day The following schedule is taken from sources that TradeStation believes are accurate and are subject to change. The schedule has been assembled for information

2018 Holiday Trading Schedule Memorial Day The following schedule is taken from sources that TradeStation believes are accurate and are subject to change. The schedule has been assembled for information

ETF Securities Weekly Flows Analysis Gold ETPs took the lion s share of outflows

Aneeka Gupta Associate Director, Equity & Commodities Research europeresearch@wisdomtree.com 23 July 218 ETF Securities Weekly Flows Analysis Gold ETPs took the lion s share of outflows Gold fails to catch

Aneeka Gupta Associate Director, Equity & Commodities Research europeresearch@wisdomtree.com 23 July 218 ETF Securities Weekly Flows Analysis Gold ETPs took the lion s share of outflows Gold fails to catch

Finding a better momentum strategy from the stock and commodity futures markets

Finding a better momentum strategy from the stock and commodity futures markets Kyung Yoon Kwon Abstract This paper proposes an improved momentum strategy that efficiently combines the stock momentum and

Finding a better momentum strategy from the stock and commodity futures markets Kyung Yoon Kwon Abstract This paper proposes an improved momentum strategy that efficiently combines the stock momentum and

The Trend is Your Friend: Time-series Momentum Strategies across Equity and Commodity Markets

The Trend is Your Friend: Time-series Momentum Strategies across Equity and Commodity Markets Athina Georgopoulou *, George Jiaguo Wang This version, June 2015 Abstract Using a dataset of 67 equity and

The Trend is Your Friend: Time-series Momentum Strategies across Equity and Commodity Markets Athina Georgopoulou *, George Jiaguo Wang This version, June 2015 Abstract Using a dataset of 67 equity and

2017 Holiday Trading Schedule Thanksgiving Day

2017 Holiday Trading Schedule Thanksgiving Day The following schedule is taken from sources that Station believes are accurate and are subject to change. The schedule has been assembled for information

2017 Holiday Trading Schedule Thanksgiving Day The following schedule is taken from sources that Station believes are accurate and are subject to change. The schedule has been assembled for information

USCF ETF Trust (Exact Name of Registrant as Specified in Charter)

") As filed with the Securities and Exchange Commission on April 24, 2018 Securities Act Registration No. 333-196273 Investment Company Act Registration No. 811-22930 SECURITIES AND EXCHANGE COMMISSION Washington,

As filed with the Securities and Exchange Commission on April 24, 2018 Securities Act Registration No. 333-196273 Investment Company Act Registration No. 811-22930 SECURITIES AND EXCHANGE COMMISSION Washington,

Semi-Annual Report. December 31, 201 SILVERPEPPER COMMODITY STRATEGIES GLOBAL MACRO FUND SILVERPEPPER MERGER ARBITRAGE FUND

Semi-Annual Report SILVERPEPPER COMMODITY STRATEGIES GLOBAL MACRO FUND Institutional Class - SPCIX Advisor Class - SPCAX SILVERPEPPER MERGER ARBITRAGE FUND Institutional Class - SPAIX Advisor Class - SPABX

Semi-Annual Report SILVERPEPPER COMMODITY STRATEGIES GLOBAL MACRO FUND Institutional Class - SPCIX Advisor Class - SPCAX SILVERPEPPER MERGER ARBITRAGE FUND Institutional Class - SPAIX Advisor Class - SPABX

The Copper Journal Weekly Report Index Of Charts

Weekly Report Index Of Charts 1 Price & Inventory Report 2 Base Metals Barometer 3 Year To Date % Price Change 4 LME Nonferrous Metals YTD % Change 5 Precious Metals YTD % Price Change 6 Energy YTD % Price

Weekly Report Index Of Charts 1 Price & Inventory Report 2 Base Metals Barometer 3 Year To Date % Price Change 4 LME Nonferrous Metals YTD % Change 5 Precious Metals YTD % Price Change 6 Energy YTD % Price

Invesco Balanced-Risk Commodity Strategy Annual Update

Invesco Balanced-Risk Commodity Strategy Annual Update 2017-2018 Water and Power Employees Retirement Plan August 8, 2018 For one-on-one U.S. institutional investor use only. All material presented is

Invesco Balanced-Risk Commodity Strategy Annual Update 2017-2018 Water and Power Employees Retirement Plan August 8, 2018 For one-on-one U.S. institutional investor use only. All material presented is

WELCOME TO THE WONDERFUL WORLD OF NUMBEROLOGY. Thursday June 29, 2017

WELCOME TO THE WONDERFUL WORLD OF NUMBEROLOGY Thursday June 29, 2017 BELOW YOU WILL FIND TABLES CONTAINING BOTH SHORT TERM AND LONGER TERM BUY/SELL VALUES BASED ON LAWG 647 MODEL BE MINDFUL I AM NOT RECOMMENDING

WELCOME TO THE WONDERFUL WORLD OF NUMBEROLOGY Thursday June 29, 2017 BELOW YOU WILL FIND TABLES CONTAINING BOTH SHORT TERM AND LONGER TERM BUY/SELL VALUES BASED ON LAWG 647 MODEL BE MINDFUL I AM NOT RECOMMENDING

Commodities: Diversification Returns

Commodities: Diversification Returns FQ Perspective May 214 Investment Team Historically, commodities have been good diversifiers to both equities and bonds. During the past several years, however, questions

Commodities: Diversification Returns FQ Perspective May 214 Investment Team Historically, commodities have been good diversifiers to both equities and bonds. During the past several years, however, questions

Mon Core Close Trade Date. Mon. Open Trade Date 12/22/ /22/ /22/ /25/ /25/ /25/ /26/ /26/ /26/2017

2017 Holiday Trading Schedule Christmas The following schedule is taken from sources that Station believes are accurate and are subject to change. The schedule has been assembled for information purposes

2017 Holiday Trading Schedule Christmas The following schedule is taken from sources that Station believes are accurate and are subject to change. The schedule has been assembled for information purposes

CFTC Adopts Final Rules on Speculative Position Limits

To Our Clients and Friends Memorandum friedfrank.com CFTC Adopts Final Rules on Speculative Position Limits During a public meeting held on October 18, 2011 (the Open Meeting ), the Commodity Futures Trading

To Our Clients and Friends Memorandum friedfrank.com CFTC Adopts Final Rules on Speculative Position Limits During a public meeting held on October 18, 2011 (the Open Meeting ), the Commodity Futures Trading

Index Description MS HDX RADAR 2 MSDY Index

Dated as of August 3, 2017 Index Description MS HDX RADAR 2 MSDY Index This document (the Index Description ) sets out the current methodology and rules used to construct, calculate and maintain the MS

Dated as of August 3, 2017 Index Description MS HDX RADAR 2 MSDY Index This document (the Index Description ) sets out the current methodology and rules used to construct, calculate and maintain the MS

Merrill Lynch Due Diligence Meeting October 2012, Boston. Commodities: Taking Advantage of Supply and Demand

Merrill Lynch Due Diligence Meeting 22-24 October 2012, Boston Commodities: Taking Advantage of Supply and Demand Peter Königbauer, Head of Aggressive Balanced and Real Assets, Senior Portfolio Manager

Merrill Lynch Due Diligence Meeting 22-24 October 2012, Boston Commodities: Taking Advantage of Supply and Demand Peter Königbauer, Head of Aggressive Balanced and Real Assets, Senior Portfolio Manager

Royal Bank of Canada

Pricing Supplement No. 3 to the Prospectus Dated October 14, 2003 and the Prospectus Supplement dated January 26, 2005 US$6,189,000 Royal Bank of Canada Senior Global Medium-Term Notes, Series A Principal

Pricing Supplement No. 3 to the Prospectus Dated October 14, 2003 and the Prospectus Supplement dated January 26, 2005 US$6,189,000 Royal Bank of Canada Senior Global Medium-Term Notes, Series A Principal

Commodity Monthly Monitor Commodity Rebound Gains Momentum

Commodity Monthly Monitor Commodity Rebound Gains Momentum May/June 2 Summary Despite a lacklustre performance in Q1 of this year, it increasingly looks like commodities are at a turning point, with most

Commodity Monthly Monitor Commodity Rebound Gains Momentum May/June 2 Summary Despite a lacklustre performance in Q1 of this year, it increasingly looks like commodities are at a turning point, with most

MONTHLY MARKET MONITOR (M 3 ) December 2014

December 2014") MONTHLY MARKET MONITOR (M 3 ) December 2014 January 5, 2014 THE LATEST MONTHLY MARKET RETURNS FROM THE RICHARDSON GMP TEAM GLOBAL MARKETS AT A GLANCE Americas Level 1mo 3mo 6mo 12mo YTD BRIC Level 1mo

MONTHLY MARKET MONITOR (M 3 ) December 2014 January 5, 2014 THE LATEST MONTHLY MARKET RETURNS FROM THE RICHARDSON GMP TEAM GLOBAL MARKETS AT A GLANCE Americas Level 1mo 3mo 6mo 12mo YTD BRIC Level 1mo

Risk Factor Indices Selection and Rebalance Dates

db Index Quant 3 October 2017 dbiq Index Guide Risk Factor Indices Selection and s The report is designed to provide the details of future selection and rebalance dates of various risk factor Indices handled

db Index Quant 3 October 2017 dbiq Index Guide Risk Factor Indices Selection and s The report is designed to provide the details of future selection and rebalance dates of various risk factor Indices handled