Module 6: Introduction to Valuation of Corporations

|

|

|

- Caren Edwards

- 5 years ago

- Views:

Transcription

1 Module 6: Introduction to Valuation of Corporations

2 Reading 6.2: Stages of Growth and Financing

3

4

5

6 Reading : Mergers and Acquisitions

7 Mergers & acquisitions (M&A) Merger Shareholders of two companies approve the combination of their companies into a single company under a statutory amalgamation. Existing shares are exchanged for new shares in the merged entity. Acquisition One company acquires voting control of another company by buying the company s common shares either for cash, shares, or a combination of the two.

8 Types of mergers Horizontal merger Companies are direct competitors in the same product lines & markets. The end goal is larger market share ( possibly expansion into different markets). Scrutinized the most from a regulatory perspective. Vertical merger When a company acquires a supplier secure reliable supply of materials and components, improve product development, etc. Congeneric merger Companies who sell different but related products. It has been a series of congeneric acquisitions that have shaped Canada s major banks. Conglomerate merger combination of companies that operate in entirely unrelated markets/industries.

9 Motives for mergers Operating economies of scale/scope Larger market share/production = lower unit production costs. Biggest benefit is usually stated in terms of cost synergies. Strategic motives Company may acquire a supplier (vertical merger) to secure a key component. Market power and control Company uses increase size and power in one part of business to its advantage in another part. Financial economies of scale Better and cheaper access to funds in the capital markets. Greater exposure to sell side analysts/institutional investors. Increase in management capabilities A company may acquire a smaller company whose best asset is a couple of key employees/executives.

10 Fast growth Often easier to buy growth/expansion in new geographic markets or different lines of business. Diversification Primary motive for a conglomerate to expand. Main belief is that the company s earnings will be more stable the more it diversifies, and thus reduce the company s risk. Investment opportunity A company may view another company as being cheap, and thus a worthwhile investment. This may be due to the state of the global economy, or company specific issues.

11 Vertical mergers Vertical mergers make sense if/when: The threat of production failures are serious enough to warrant bringing production in house. If firm s activities are complex and difficult to control. There are a few outside suppliers and they tend to behave in an opportunistic manner. If there is a realistic possibility of achieving economies of integration (more cost effective for one company doing what two companies can do).

12 Vertical mergers Vertical mergers don t make sense if/when: Can achieve economies of scale, but not worth it because of low production volume. There is the potential for unknown costs associated with entering new business. Friendly vs hostile takeover

13 Strategies designed to inhibit takeover attempts 1. Keep voting power in hand of current shareholders (or a small group of shareholders) Dual class shares certain group of shareholders have class of share with far greater voting privileges (10 votes for one class A share, v.s 1 vote for each class B share). Employee stock option plans (ESOPs) management may vote the shares allocated to ESOP. Gives management a little more voting power. Changing majority vote company s charter could be changed to require significant majority vote by shareholders to approve takeover. Staggered board of directors small number of directors are elected per year. This makes it hard for a company looking to takeover the company to elect its own directors.

14 Strategies designed to inhibit takeover attempts 2. Golden parachutes - Design executive compensation so key executives will receive large benefits if contracts terminated. 3. Poison pills Rights/warrants are issued that become valuable when an unfriendly bidder controls certain percentage of company s vote.

15 Fighting a declared takeover attempt Find a white knight a third company that will agree to a friendly acquisition. Negotiate with the bidder to stop the takeover process for a period of time so that the two companies can negotiate a friendly merger. Make sure shares owned by bidder will not exceed those of management or management friendly shareholders: Buyback shares of bidder at a premium (white mail) Use cash or borrow to buy back shares Sell shares to friendly third parties Management could take measures to make company less desirable: Buy assets that could create anti-trust issues or bidder may find undesirable Sell attractive assets Load up the company with debt Make your own takeover attempt for bidder

16 Reading &6.4: Leveraged Buyouts

.")

17 LBO is where an acquisition is financed with a significant amount of debt. If the investors include employees of the company, it is considered a management buyout (MBO). Most of the time, the company acquired is publicly traded, and is proceeded to be taken private (i.e no longer publicly traded). Once the company has improved its operations/profitability, the company is then usually taken public again at a huge profit for the owners. Generally not the case for a MBO: under a MBO the company may be run just as it always has been.

18 Good targets for an LBO Company is stable with a consistent history of profitability (i.e low business risk), and generates strong cash flows (it s the cash flows that will pay off the debt). Company operates in a stable industry and generally has an asset base that deteriorates slowly (i.e doesn t need a major reinvestment in assets anytime soon), and is quite tangible (offers good collateral value). Company currently has relatively low amount of debt.

19 Is leasing an option? Can the company use the tax shield that interest payments offer? With lease financing of assets, reduces initial cash outlays. Difficulty with lease financing: Leasing companies may prefer to wait until the LBO goes through, which may be too late from the perspective of the LBO sponsors. Lease financing may not be large enough for the needs of the LBO. LBO deal may be too complex and occurring too quickly for leasing companies.

20 Evaluating a merger/lbo The evaluation of a potential merger is very much a capital budgeting problem. The present value of the cash flows generated must be greater than the purchase price. The key is the premium being offered to acquire the company. Study after study has concluded that the majority of mergers fail this is normally due to the high premium that must be paid to acquire the company and/or anticipated synergies that never materialize.

21 Reading 6.5: Basic Valuation Using Discounted Cash Flows

22 Basics of discounted cash flow valuation Basic discounted valuation model: Equation 6-4 Forecasted cash flows Terminal value There are 3 key inputs: cash flows (C), discount rate (r), and growth rate (g). The different models are based on different methods of determining which cash flows to value. Remember, are you valuing the firm in its entirety, or just the equity of the firm?

23 Reading 6.6: Valuation Using Operating Cash Flows and the WACC

24 Operating cash flows (OCF) Equation 6-5 Forecasted cash flows Terminal value OCF = operating cash flows after tax, including cash flows from non-cash items. WACC = Weighted average cost of capital g = perpetual growth rate

25 Calculating operating cash flows

26 Determining NPV of acquisition Equation 6-6 Equation 6-7

27 Reading 6.7: Valuation Using Free Cash Flows to the Firm

28 Free cash flows to firm (FCFF) Equation 6-8 A/tax operating cash flows Net capital investments Terminal value

29 FCFF using APV Using APV at the unlevered cost of equity to the operating and investing cash flows. Adjust for financial side effects discounted at cost of debt. Equation 6-9

30 Reading 6.8: Valuation Using Free Cash Flows to Equity

31 Free cash flows to equity (FCFE) Value the equity portion of the company by considering cash flows that flow directly to shareholders.

32 Equation 6-10

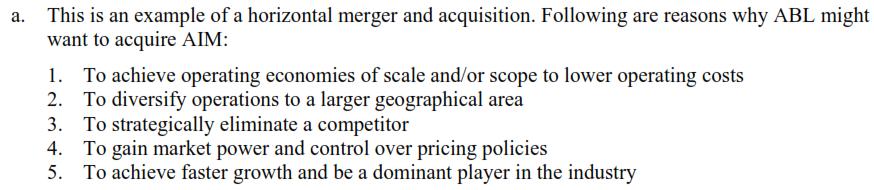

33 From June 2011 exam ABL Corp. is one of the industry leaders looking for target companies to acquire on the market. One such target, AIM Inc., is being pursued by ABL s main rival, LAB Inc. LAB has made a bid valuing AIM at $100,000. ABL is seeking your advice on whether they should also bid on AIM.

34 From June 2011 exam

35

36

37

38

39

40

41

42 From June 2012 exam Big Nickel Inc. (BN) has found a target company to take over: Small Nickel Corp. (SN), a smaller mining company.

43

44

45

46 Reading 6.9: Valuation Using Dividend Growth Models

47 Dividend growth models Variation of FCFE where we use dividends as a substitute for cash flows. If you dividends are specified for the forecast periods:

48 If the forecast period is characterized as a period of high growth, then the following model is used:

49

50

51

52 Reading 6.11: Valuation Using Price-Multiple Ratios

53 Using price-multiples Instead of discounting cash flows, using multiples is easier and based on the notion that the current transaction should be priced similar to previous transactions.

54 From June 2014:

55

56

57

58

59

60

61

62

63

64

65

Chapter 23 Mergers and Acquisitions

T23.1 Chapter Outline Chapter Organization Chapter 23 Mergers and Acquisitions! 23.1 The Legal Forms of Acquisitions! 23.2 Taxes and Acquisitions! 23.3 Accounting for Acquisitions! 23.4 Gains from Acquisition!

T23.1 Chapter Outline Chapter Organization Chapter 23 Mergers and Acquisitions! 23.1 The Legal Forms of Acquisitions! 23.2 Taxes and Acquisitions! 23.3 Accounting for Acquisitions! 23.4 Gains from Acquisition!

CORPORATE CONTROL EVENTS EB434 ENTERPRISE GOVERNANCE

CORPORATE CONTROL EVENTS 16 EB434 ENTERPRISE GOVERNANCE corporate control events Open market purchases on the stock market Tender offer offer made directly to shareholders (often by law, to all shareholders

CORPORATE CONTROL EVENTS 16 EB434 ENTERPRISE GOVERNANCE corporate control events Open market purchases on the stock market Tender offer offer made directly to shareholders (often by law, to all shareholders

Mergers, Acquisitions and Divestures

Session 11 &12 Mergers, Acquisitions and Divestures Programme : Postgraduate Diploma in Business, Finance & Strategy (PGDBFS 2018) Course : Corporate Valuation (PGDBFS 203) Lecturer : Mr. Asanka Ranasinghe

Session 11 &12 Mergers, Acquisitions and Divestures Programme : Postgraduate Diploma in Business, Finance & Strategy (PGDBFS 2018) Course : Corporate Valuation (PGDBFS 203) Lecturer : Mr. Asanka Ranasinghe

Mergers and Acquisitions

Takeovers Takeover: transfers the control right of the firm from one group to another Merger Mergers and Acquisitions Acquisition Acquisition of Stock, 2018 Takeovers Proxy Contest Going Private Acquisition

Takeovers Takeover: transfers the control right of the firm from one group to another Merger Mergers and Acquisitions Acquisition Acquisition of Stock, 2018 Takeovers Proxy Contest Going Private Acquisition

Corporate Finance. Lecture 12: Mergers and Acquisitions. Albert Banal-Estanol

Corporate Finance 12: Mergers and Acquisitions Merger activity in the US during the past century Mergers in Europe Mergers come in waves and are procyclical Recent Mergers Industry Acquiring Company Selling

Corporate Finance 12: Mergers and Acquisitions Merger activity in the US during the past century Mergers in Europe Mergers come in waves and are procyclical Recent Mergers Industry Acquiring Company Selling

Mergers, Acquisitions and Divestures

Session 11 &12 Mergers, Acquisitions and Divestures Programme : Postgraduate Diploma in Business, Finance & Strategy (PGDBFS 2017) Course : Corporate Valuation (PGDBFS 203) Lecturer : Mr. Asanka Ranasinghe

Session 11 &12 Mergers, Acquisitions and Divestures Programme : Postgraduate Diploma in Business, Finance & Strategy (PGDBFS 2017) Course : Corporate Valuation (PGDBFS 203) Lecturer : Mr. Asanka Ranasinghe

Topics in Corporate Finance. Chapter 9: Mergers and Acquisitions. Albert Banal-Estanol

Topics in Corporate Finance Chapter 9: Mergers and Acquisitions Merger activity in the US during the past century Mergers in Europe Mergers come in waves and are procyclical This chapter s Plan Evidence

Topics in Corporate Finance Chapter 9: Mergers and Acquisitions Merger activity in the US during the past century Mergers in Europe Mergers come in waves and are procyclical This chapter s Plan Evidence

Mergers and Acquisitions: A Strategic Valuation Approach

Mergers and Acquisitions: A Strategic Valuation Approach Mergers and Acquisitions: A Strategic Valuation Approach Emery A. Trahan Contents About This Course How to Take This Course xiii 1 An Overview

Mergers and Acquisitions: A Strategic Valuation Approach Mergers and Acquisitions: A Strategic Valuation Approach Emery A. Trahan Contents About This Course How to Take This Course xiii 1 An Overview

This can vary from 50.1% to 90%+ (some states don't want outsiders to control their companies)

") Execution and Legal There are 2 ways to gain control of a company: 1. Acquire enough shares to constitute control according to the laws of the state in which the target is incorporated This can vary from

Execution and Legal There are 2 ways to gain control of a company: 1. Acquire enough shares to constitute control according to the laws of the state in which the target is incorporated This can vary from

Mergers and Acquisitions

Mergers and Acquisitions 1 Classifying M&A Merger: the boards of directors of two firms agree to combine and seek shareholder approval for combination. The target ceases to exist. Consolidation: a new

Mergers and Acquisitions 1 Classifying M&A Merger: the boards of directors of two firms agree to combine and seek shareholder approval for combination. The target ceases to exist. Consolidation: a new

CIS March 2012 Exam Diet

CIS March 2012 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Level 2 Corporate Finance (1 13) 1. Which of the following statements

CIS March 2012 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Level 2 Corporate Finance (1 13) 1. Which of the following statements

Acquisitions, mergers, and takeovers terminology - Wikipedia, the free encyclopedia

Page 1 of 5 Acquisitions, mergers, and takeovers terminology From Wikipedia, the free encyclopedia The following are some concepts and terms used in acquisitions, mergers and takeovers of private and public

Page 1 of 5 Acquisitions, mergers, and takeovers terminology From Wikipedia, the free encyclopedia The following are some concepts and terms used in acquisitions, mergers and takeovers of private and public

Lesson 10 THE MERGERS AND ACQUISITION MARKET. AN OVERVIEW. INTRODUCTION TO COMPANY S VALUE AND VALUATION TECHNIQUES. DCF AND COMPARABLES

Lesson 10 THE MERGERS AND ACQUISITION MARKET. AN OVERVIEW. INTRODUCTION TO COMPANY S VALUE AND VALUATION TECHNIQUES. DCF AND COMPARABLES Internal growth vs. External growth Internal growth investments

Lesson 10 THE MERGERS AND ACQUISITION MARKET. AN OVERVIEW. INTRODUCTION TO COMPANY S VALUE AND VALUATION TECHNIQUES. DCF AND COMPARABLES Internal growth vs. External growth Internal growth investments

Chapter 1 Introduction to Business Combinations and the Conceptual Framework

Chapter 1 Introduction to Business Combinations and the Conceptual Framework Multiple Choice 1. Stock given as consideration for a business combination is valued at a. fair market value b. par value c.

Chapter 1 Introduction to Business Combinations and the Conceptual Framework Multiple Choice 1. Stock given as consideration for a business combination is valued at a. fair market value b. par value c.

Module 5: Special Financing and Investment Decisions

Module 5: Special Financing and Investment Decisions Reading 5.1: Introduction to Project Financing Some projects are so large that it may be best to finance them as they are standalone operations. Projects

Module 5: Special Financing and Investment Decisions Reading 5.1: Introduction to Project Financing Some projects are so large that it may be best to finance them as they are standalone operations. Projects

Mergers & Acquisitions

Mergers & Acquisitions Topics Covered Sensible Motives for Mergers Some Dubious Reasons for Mergers Estimating Merger Gains and Costs The Mechanics of a Merger Proxy Fights, Takeovers, and the Market for

Mergers & Acquisitions Topics Covered Sensible Motives for Mergers Some Dubious Reasons for Mergers Estimating Merger Gains and Costs The Mechanics of a Merger Proxy Fights, Takeovers, and the Market for

Market for Corporate Control: Takeovers. Nino Papiashvili Institute of Finance Ulm University

Market for Corporate Control: Takeovers Nino Papiashvili Institute of Finance Ulm University 1 Introduction Takeovers - the market for corporate control - where management teams compete with one another

Market for Corporate Control: Takeovers Nino Papiashvili Institute of Finance Ulm University 1 Introduction Takeovers - the market for corporate control - where management teams compete with one another

risk free rate 7% market risk premium 4% pre-merger beta 1.3 pre-merger % debt 20% pre-merger debt r d 9% Tax rate 40%

Hager s Home Repair Company, a regional hardware chain, which specializes in do-ityourself materials and equipment rentals, is cash rich because of several consecutive good years. One of the alternative

Hager s Home Repair Company, a regional hardware chain, which specializes in do-ityourself materials and equipment rentals, is cash rich because of several consecutive good years. One of the alternative

Level 2: Study Session 09: Equity Investments: Industry and Company Analysis 160 questions.

Level 2: Study Session 09: Equity Investments: Industry and Company Analysis 160 questions. Introduction by the Author : Hi there, CFA fellows, here you are. You see, it doesn't need to be an expensive

Level 2: Study Session 09: Equity Investments: Industry and Company Analysis 160 questions. Introduction by the Author : Hi there, CFA fellows, here you are. You see, it doesn't need to be an expensive

OLD/PRACTICE Final Exam

OLD/PRACTICE Final Exam ADM 335 M&N Corporate Finance Professors: Kaouthar Lajili Devinder Ghandi Time: Three hours NAME: STUDENT NUMBER: SIGNATURE: GENERAL INSTRUCTIONS: Hand in everything at the end

OLD/PRACTICE Final Exam ADM 335 M&N Corporate Finance Professors: Kaouthar Lajili Devinder Ghandi Time: Three hours NAME: STUDENT NUMBER: SIGNATURE: GENERAL INSTRUCTIONS: Hand in everything at the end

FINALTERM EXAMINATION Fall 2009 MGT201- Financial Management (Session - 3)

") FINALTERM EXAMINATION Fall 2009 MGT201- Financial Management (Session - 3) Time: 120 min Marks: 87 Question No: 1 ( Marks: 1 ) - Please choose one ABC s and XYZ s debt-to-total assets ratio is 0.4. What

FINALTERM EXAMINATION Fall 2009 MGT201- Financial Management (Session - 3) Time: 120 min Marks: 87 Question No: 1 ( Marks: 1 ) - Please choose one ABC s and XYZ s debt-to-total assets ratio is 0.4. What

KEY TERMS IN MERGERS AND ACQUISITIONS

Surviving M&A: Make the Most of Your Company Being Acquired By Scott Moeller Copyright 2009 John Wiley & Sons, Ltd. KEY TERMS IN MERGERS AND ACQUISITIONS Acquisition When one company (the buyer ) purchases

Surviving M&A: Make the Most of Your Company Being Acquired By Scott Moeller Copyright 2009 John Wiley & Sons, Ltd. KEY TERMS IN MERGERS AND ACQUISITIONS Acquisition When one company (the buyer ) purchases

Capital Structure. Capital Structure. Konan Chan. Corporate Finance, Leverage effect Capital structure stories. Capital structure patterns

Capital Structure, 2018 Konan Chan Capital Structure Leverage effect Capital structure stories MM theory Trade-off theory Free cash flow theory Pecking order theory Market timing Capital structure patterns

Capital Structure, 2018 Konan Chan Capital Structure Leverage effect Capital structure stories MM theory Trade-off theory Free cash flow theory Pecking order theory Market timing Capital structure patterns

Web Extension: Comparison of Alternative Valuation Models

19878_26W_p001-009.qxd 3/14/06 3:08 PM Page 1 C H A P T E R 26 Web Extension: Comparison of Alternative Valuation Models We described the APV model in Chapter 26 because it is easier to implement when

19878_26W_p001-009.qxd 3/14/06 3:08 PM Page 1 C H A P T E R 26 Web Extension: Comparison of Alternative Valuation Models We described the APV model in Chapter 26 because it is easier to implement when

FIN 423/523 Takeover Defenses

FIN 423/523 Takeover Defenses Successful takeovers: target stockholders gain 20-35% or more Unsuccessful takeovers: target stockholders gain little if not eventually taken over Question: Why would target

FIN 423/523 Takeover Defenses Successful takeovers: target stockholders gain 20-35% or more Unsuccessful takeovers: target stockholders gain little if not eventually taken over Question: Why would target

SCHOOL OF ECONOMICS AND FINANCE NOVEMBER EXAMINATION: 2007 SUBJECT, COURSE AND CODE: THE CORPORATE INVESTMENT DECISION (FINA321)

") 1 SCHOOL OF ECONOMICS AND FINANCE NOVEMBER EXAMINATION: 2007 SUBJECT, COURSE AND CODE: THE CORPORATE INVESTMENT DECISION (FINA321) EXAMINERS (INTERNAL): EXAMINER (EXTERNAL): MRS S DONNELLY MR J MASEKO,

1 SCHOOL OF ECONOMICS AND FINANCE NOVEMBER EXAMINATION: 2007 SUBJECT, COURSE AND CODE: THE CORPORATE INVESTMENT DECISION (FINA321) EXAMINERS (INTERNAL): EXAMINER (EXTERNAL): MRS S DONNELLY MR J MASEKO,

Financial Strategy and Valuation (FSV / SL 2) Strategic Level Pilot Paper - Suggested Answer Scheme

Strategic Level Pilot Paper - Suggested Answer Scheme") Financial Strategy and Valuation (FSV / SL 2) Strategic Level Pilot Paper - Suggested Answer Scheme PART I Question No. 01 (40 Marks) 1. Answer: Yes, I agree with the statement. Growth Business risk high

Financial Strategy and Valuation (FSV / SL 2) Strategic Level Pilot Paper - Suggested Answer Scheme PART I Question No. 01 (40 Marks) 1. Answer: Yes, I agree with the statement. Growth Business risk high

FIN 540 Interfirm Tender Offers & Mergers. Interfirm Mergers: Basic Facts

FIN 540 Interfirm Tender Offers & Mergers Payoffs to Stockholders of Target & Bidder Firms Sources of Gains/Motivations for Mergers Types of Mergers horizontal vertical conglomerate Interfirm Mergers:

FIN 540 Interfirm Tender Offers & Mergers Payoffs to Stockholders of Target & Bidder Firms Sources of Gains/Motivations for Mergers Types of Mergers horizontal vertical conglomerate Interfirm Mergers:

Bribery and Corruption

Bribery and Corruption M&A Corruption Due Diligence 2018 Association of Certified Fraud Examiners, Inc. Introduction M&A transactions deal with the buying, selling, dividing, and combining of different

Bribery and Corruption M&A Corruption Due Diligence 2018 Association of Certified Fraud Examiners, Inc. Introduction M&A transactions deal with the buying, selling, dividing, and combining of different

MGT201 Financial Management Solved Subjective For Final Term Exam Preparation

MGT201 Financial Management Solved Subjective For Final Term Exam Preparation Operating lease Operating Lease offers Financing AND MAINTENANCE: often the Lessor is the Supplier / Vendor of the Asset i.e.

MGT201 Financial Management Solved Subjective For Final Term Exam Preparation Operating lease Operating Lease offers Financing AND MAINTENANCE: often the Lessor is the Supplier / Vendor of the Asset i.e.

Transactional Valuation - M&A / Private Equity August 2011

www.pwc.com Transactional Valuation - M&A / Private Equity Agenda Valuation for Mergers and Acquisition Valuation for PE Valuation for Demergers Slide 2 Valuation for Mergers and Acquisitions Understanding

www.pwc.com Transactional Valuation - M&A / Private Equity Agenda Valuation for Mergers and Acquisition Valuation for PE Valuation for Demergers Slide 2 Valuation for Mergers and Acquisitions Understanding

Corporations, Mergers, and Multinationals 8.3 notes

Corporations, Mergers, and Multinationals 8.3 notes What types of corporations exist? What are the advantages of incorporation? What are the disadvantages of incorporation? How can corporations combine?

Corporations, Mergers, and Multinationals 8.3 notes What types of corporations exist? What are the advantages of incorporation? What are the disadvantages of incorporation? How can corporations combine?

Restructuring Corporate America by John J. Clark, John T. Gerlach, and Gerald Oslo

Sacred Heart University Review Volume 16 Issue 1 Sacred Heart University Review, Volume XVI, Numbers 1 & 2, Fall 1995/ Spring 1996 Article 8 1996 Restructuring Corporate America by John J. Clark, John

Sacred Heart University Review Volume 16 Issue 1 Sacred Heart University Review, Volume XVI, Numbers 1 & 2, Fall 1995/ Spring 1996 Article 8 1996 Restructuring Corporate America by John J. Clark, John

ECON 4245 Economics of the Firm

ECON 4245 Economics of the Firm Lecturer: Tore Nilssen, office ES 1216, tore.nilssen@econ.uio.no Seminars: Diderik Lund, office ES 1130, diderik.lund@econ.uio.no 13 lectures; 6 seminars (in two groups)

ECON 4245 Economics of the Firm Lecturer: Tore Nilssen, office ES 1216, tore.nilssen@econ.uio.no Seminars: Diderik Lund, office ES 1130, diderik.lund@econ.uio.no 13 lectures; 6 seminars (in two groups)

Debt. Firm s assets. Common Equity

Debt/Equity Definition The mix of securities that a firm uses to finance its investments is called its capital structure. The two most important such securities are debt and equity Debt Firm s assets Common

Debt/Equity Definition The mix of securities that a firm uses to finance its investments is called its capital structure. The two most important such securities are debt and equity Debt Firm s assets Common

Corporate Finance: Final Exam

Corporate Finance: Final Exam Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. Novellus Inc. is a publicly traded company that operates in three

Corporate Finance: Final Exam Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. Novellus Inc. is a publicly traded company that operates in three

MGT201 Subjective Material

MGT201 Subjective Material Question No: 50 ( Marks: 3 ) Management Buyouts is a form of buyouts. Explain this term in your own words. Management buyouts are similar in all major legal aspects to any other

MGT201 Subjective Material Question No: 50 ( Marks: 3 ) Management Buyouts is a form of buyouts. Explain this term in your own words. Management buyouts are similar in all major legal aspects to any other

Chapter 025 Mergers and Acquisitions

Multiple Choice Questions 1. The complete absorption of one company by another, wherein the acquiring firm retains its identity and the acquired firm ceases to exist as a separate entity, is called a:

Multiple Choice Questions 1. The complete absorption of one company by another, wherein the acquiring firm retains its identity and the acquired firm ceases to exist as a separate entity, is called a:

MGMT 165: Corporate Finance

MGMT 165: Corporate Finance Corporate Governance Fanis Tsoulouhas UC Merced Fanis Tsoulouhas (UCM) Lectures 1 and 2 1 / 20 Moral Hazard The fundamental problem in corporate governance is a principal-agent

MGMT 165: Corporate Finance Corporate Governance Fanis Tsoulouhas UC Merced Fanis Tsoulouhas (UCM) Lectures 1 and 2 1 / 20 Moral Hazard The fundamental problem in corporate governance is a principal-agent

Ron Muller MODULE 6: SPECIAL FINANCING AND INVESTMENT DECISIONS QUESTION 1

MODULE 6: SPECIAL FINANCING AND INVESTMENT DECISIONS QUESTION 1 Barney s Ltd. is trying to decide whether or not to lease or borrow to buy a new computer facility from the manufacturer. Annual maintenance

MODULE 6: SPECIAL FINANCING AND INVESTMENT DECISIONS QUESTION 1 Barney s Ltd. is trying to decide whether or not to lease or borrow to buy a new computer facility from the manufacturer. Annual maintenance

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Learning Objectives LO1 How to compute the net present value and why it is the best decision criterion. LO2 The payback rule and some of its shortcomings.

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Learning Objectives LO1 How to compute the net present value and why it is the best decision criterion. LO2 The payback rule and some of its shortcomings.

PAPER No. 8: Financial Management MODULE No. 27: Capital Structure in practice

Subject Financial Management Paper No. and Title Module No. and Title Module Tag Paper No.8: Financial Management Module No. 27: Capital Structure in Practice COM_P8_M27 TABLE OF CONTENTS 1. Learning outcomes

Subject Financial Management Paper No. and Title Module No. and Title Module Tag Paper No.8: Financial Management Module No. 27: Capital Structure in Practice COM_P8_M27 TABLE OF CONTENTS 1. Learning outcomes

Mergers and Acquisitions Report 2016 Taiwan

This article was published in the Mergers and Acquisitions Report 2016 on March 23, 2016. Mergers and Acquisitions Report 2016 Taiwan Ken-Ying Tseng, Robin Chang, Lihuei Mao and Patricia Lin, Lee and Li

This article was published in the Mergers and Acquisitions Report 2016 on March 23, 2016. Mergers and Acquisitions Report 2016 Taiwan Ken-Ying Tseng, Robin Chang, Lihuei Mao and Patricia Lin, Lee and Li

Chapter 14 Mergers, Acquisitions, and the Valuation of Shares

Mergers, Acquisitions, and the Valuation of Shares Solutions to Even-Numbered Problems and Cases 14.2 Fashion Accessories Fashion Accessories must recently have been the subject of a rumoured hostile takeover

Mergers, Acquisitions, and the Valuation of Shares Solutions to Even-Numbered Problems and Cases 14.2 Fashion Accessories Fashion Accessories must recently have been the subject of a rumoured hostile takeover

Capital Structure (General)

") Capital Structure (General) Question 1 What is the debt:equity ratio for the following UK company? Assets Fixed assets 120 Current assets Stock 50 Debtors 80 250 Liabilities Creditors due in less than

Capital Structure (General) Question 1 What is the debt:equity ratio for the following UK company? Assets Fixed assets 120 Current assets Stock 50 Debtors 80 250 Liabilities Creditors due in less than

One Of The Largest Undeveloped Gold Projects In Quebec

One Of The Largest Undeveloped Gold Projects In Quebec Apr. 11, 2016 2:44 PM ET About: Aurvista Gold Corp (ARVSF) Don Durrett Growth, contrarian, newsletter provider, research analyst Summary A step by

One Of The Largest Undeveloped Gold Projects In Quebec Apr. 11, 2016 2:44 PM ET About: Aurvista Gold Corp (ARVSF) Don Durrett Growth, contrarian, newsletter provider, research analyst Summary A step by

Economics of Strategy Fifth Edition. Besanko, Dranove, Shanley, and Schaefer. Chapter 7. Diversification. Copyright 2010 John Wiley Sons, Inc.

Economics of Strategy Fifth Edition Besanko, Dranove, Shanley, and Schaefer Chapter 7 Diversification Slides by: Richard Ponarul, California State University, Chico Copyright 2010 John Wiley Sons, Inc.

Economics of Strategy Fifth Edition Besanko, Dranove, Shanley, and Schaefer Chapter 7 Diversification Slides by: Richard Ponarul, California State University, Chico Copyright 2010 John Wiley Sons, Inc.

The Three Ts of Successful M&A

Volume XIX, Issue 63 The Three Ts of Successful M&A In mature industries, M&A is often seen as a route to accelerated growth, and there are many examples of businesses successfully pursuing this as a growth

Volume XIX, Issue 63 The Three Ts of Successful M&A In mature industries, M&A is often seen as a route to accelerated growth, and there are many examples of businesses successfully pursuing this as a growth

The Examiner's Answers F3 - Financial Strategy

The Examiner's Answers F3 - Financial Strategy Some of the answers that follow are fuller and more comprehensive than would be expected from a well-prepared candidate. They have been written in this way

The Examiner's Answers F3 - Financial Strategy Some of the answers that follow are fuller and more comprehensive than would be expected from a well-prepared candidate. They have been written in this way

CORPORATE VALUATION METHODOLOGIES

CORPORATE VALUATION METHODOLOGIES What is the business worth? Although a simple question, determining the value of any business in today s economy requires a sophisticated understanding of financial analysis

CORPORATE VALUATION METHODOLOGIES What is the business worth? Although a simple question, determining the value of any business in today s economy requires a sophisticated understanding of financial analysis

STATEGIC FIT IN MERGERS AND ACQUISITIONS AN IMPERATIVE

1 STATEGIC FIT IN MERGERS AND ACQUISITIONS AN IMPERATIVE 2 INTRODUCTION Mergers and acquisitions (M&A) and corporate restructuring are a big part of the corporate finance world. Every day, Wall Street

1 STATEGIC FIT IN MERGERS AND ACQUISITIONS AN IMPERATIVE 2 INTRODUCTION Mergers and acquisitions (M&A) and corporate restructuring are a big part of the corporate finance world. Every day, Wall Street

Do Management Buyouts of US Companies Demand Higher Premiums than UK Companies? Why?

Do Management Buyouts of US Companies Demand Higher Premiums than UK Companies? Why? Harsh Nanda The Leonard N. Stern School of Business Glucksman Institute for Research in Securities Markets Faculty Advisor:

Do Management Buyouts of US Companies Demand Higher Premiums than UK Companies? Why? Harsh Nanda The Leonard N. Stern School of Business Glucksman Institute for Research in Securities Markets Faculty Advisor:

Capital structure I: Basic Concepts

Capital structure I: Basic Concepts What is a capital structure? The big question: How should the firm finance its investments? The methods the firm uses to finance its investments is called its capital

Capital structure I: Basic Concepts What is a capital structure? The big question: How should the firm finance its investments? The methods the firm uses to finance its investments is called its capital

Week 6 Equity Valuation 1

Week 6 Equity Valuation 1 Overview of Valuation The basic assumption of all these valuation models is that the future value of all returns can be discounted back to today s present value. Where t = time

Week 6 Equity Valuation 1 Overview of Valuation The basic assumption of all these valuation models is that the future value of all returns can be discounted back to today s present value. Where t = time

2017 Exit Academy. Evaluating Alternatives and Valuation

2017 Exit Academy Evaluating Alternatives and Valuation Sales Critical Issue Where is Company in Its Lifecycle? Introduction Growth & Adoption Penetration and Maturation Consolidation and Decline Debt

2017 Exit Academy Evaluating Alternatives and Valuation Sales Critical Issue Where is Company in Its Lifecycle? Introduction Growth & Adoption Penetration and Maturation Consolidation and Decline Debt

Mergers, acquisitions, and corporate restructuring: Conceptual issues 1

Mergers, acquisitions, and corporate restructuring: Conceptual issues 1 Class work: Each student attending the class, shall read this document and facilitate class discussion. He or She may further the

Mergers, acquisitions, and corporate restructuring: Conceptual issues 1 Class work: Each student attending the class, shall read this document and facilitate class discussion. He or She may further the

Allstate Agency Value Index 2011 Year Review

Allstate Agency Value Index Year Review In there were many active topics of discussion in the Allstate Community. Agency Terminations, Mergers and Acquisitions, Esurance along with the hottest of all topics:

Allstate Agency Value Index Year Review In there were many active topics of discussion in the Allstate Community. Agency Terminations, Mergers and Acquisitions, Esurance along with the hottest of all topics:

M&A Rules in Japan. May 2005 Ministry of Economy, Trade and Industry

M&A Rules in Japan 1. Structural changes in corporate environment in Japan 2. Negative effects resulting from lack rules on hostile takeovers 3. Global M&A market rules regulations in U.S., EU Japan 4.

M&A Rules in Japan 1. Structural changes in corporate environment in Japan 2. Negative effects resulting from lack rules on hostile takeovers 3. Global M&A market rules regulations in U.S., EU Japan 4.

tax basis for the assets and can affect depreciation in subsequent periods.

42 Accounting Considerations There is one final decision that, in our view, seems to play a disproportionate role in the way in which acquisitions are structured and in setting their terms, and that is

42 Accounting Considerations There is one final decision that, in our view, seems to play a disproportionate role in the way in which acquisitions are structured and in setting their terms, and that is

Private Equity Strategies. By Ascanio Rossini

Private Equity Strategies By Ascanio Rossini Outline 1. What is Private Equity (PE) and what distinguishes it from other asset classes? i. Definition ii. Key Features iii. Fund Structure 2. Private Equity

Private Equity Strategies By Ascanio Rossini Outline 1. What is Private Equity (PE) and what distinguishes it from other asset classes? i. Definition ii. Key Features iii. Fund Structure 2. Private Equity

web extension 24A FCF t t 1 TS t (1 r su ) t t 1

t t 1") The Adjusted Present Value (APV) Approachl 24A-1 web extension 24A The Adjusted Present Value (APV) Approach The corporate valuation or residual equity methods described in the textbook chapter work well

The Adjusted Present Value (APV) Approachl 24A-1 web extension 24A The Adjusted Present Value (APV) Approach The corporate valuation or residual equity methods described in the textbook chapter work well

Chapter 8: Business Organizations Section 3

Chapter 8: Business Organizations Section 3 Objectives 1. Explain the characteristics of corporations. 2. Analyze the advantages of incorporation. 3. Analyze the disadvantages of incorporation. 4. Compare

Chapter 8: Business Organizations Section 3 Objectives 1. Explain the characteristics of corporations. 2. Analyze the advantages of incorporation. 3. Analyze the disadvantages of incorporation. 4. Compare

The Features of Investment Decision-Making

The Features of Investment Decision-Making Industrial management Controlling and Audit Olga Zhukovskaya Main Issues 1. The Concept of Investing 2. The Tools for Investment Decision-Making 3. Mergers and

The Features of Investment Decision-Making Industrial management Controlling and Audit Olga Zhukovskaya Main Issues 1. The Concept of Investing 2. The Tools for Investment Decision-Making 3. Mergers and

An Indian Journal FULL PAPER ABSTRACT KEYWORDS. Trade Science Inc. Analysis and prevention of risks of enterprise merger and acquisition

[Type text] [Type text] [Type text] 2014 ISSN : 0974-7435 Volume 10 Issue 10 BioTechnology An Indian Journal FULL PAPER BTAIJ, 10(10), 2014 [4344-4349] Analysis and prevention of risks of enterprise merger

[Type text] [Type text] [Type text] 2014 ISSN : 0974-7435 Volume 10 Issue 10 BioTechnology An Indian Journal FULL PAPER BTAIJ, 10(10), 2014 [4344-4349] Analysis and prevention of risks of enterprise merger

How Private Equities Create Value. LBOs, Expansion deals and the future of PEs - Trends

How Private Equities Create Value LBOs, Expansion deals and the future of PEs - Trends 1 Contents - Introduction to Value Creation in PEs - LBOs - Operating Leverage - Financial Leverage - Recent trends

How Private Equities Create Value LBOs, Expansion deals and the future of PEs - Trends 1 Contents - Introduction to Value Creation in PEs - LBOs - Operating Leverage - Financial Leverage - Recent trends

MERGER & CONSOLIDATION: OVERVIEW

MERGER & CONSOLIDATION: OVERVIEW Merger: A contractual and statutory process by : (1) which one corporation (the surviving corporation) acquires all of the assets and liabilities of another corporation

MERGER & CONSOLIDATION: OVERVIEW Merger: A contractual and statutory process by : (1) which one corporation (the surviving corporation) acquires all of the assets and liabilities of another corporation

Corporate Strategy - Mergers & Acquisitions Dr. Sebastian Spaeth Matthias

Corporate Strategy - Mergers & Acquisitions Dr. Sebastian Spaeth Matthias Stuermer 1 Where we left off Organizational Structure Definition Dimensions: Specialization,

Corporate Strategy - Mergers & Acquisitions Dr. Sebastian Spaeth Matthias Stuermer 1 Where we left off Organizational Structure Definition Dimensions: Specialization,

STRATEGY. Dr. Humam AL-Jazaeri Syrian Virtual University. MBAP Course. Winter Session Six

STRATEGY Dr. Humam AL-Jazaeri Syrian Virtual University MBAP Course Winter 2010 Session Six 1 Part One Strategy: Conceptual & Analytical Framework 2 Corporate Level Strategy 3 Samsung: Business Portfolio

STRATEGY Dr. Humam AL-Jazaeri Syrian Virtual University MBAP Course Winter 2010 Session Six 1 Part One Strategy: Conceptual & Analytical Framework 2 Corporate Level Strategy 3 Samsung: Business Portfolio

ANALYSIS OF MEASURES AND TACTICS OF DEFENSE AGAINST HOSTILE TAKEOVERS OF COMPANIES IN THE STRATEGIC FUNCTION OF MANAGING A COMPANY

I International Symposium Engineering Management And Competitiveness 2011 (EMC2011) June 24-25, 2011, Zrenjanin, Serbia ANALYSIS OF MEASURES AND TACTICS OF DEFENSE AGAINST HOSTILE TAKEOVERS OF COMPANIES

I International Symposium Engineering Management And Competitiveness 2011 (EMC2011) June 24-25, 2011, Zrenjanin, Serbia ANALYSIS OF MEASURES AND TACTICS OF DEFENSE AGAINST HOSTILE TAKEOVERS OF COMPANIES

Background p. 1 Introduction p. 3 Definitions p. 7 Valuing a Transaction p. 7 Types of Mergers p. 7 Reasons for Mergers and Acquisitions p.

Preface p. xi Background p. 1 Introduction p. 3 Definitions p. 7 Valuing a Transaction p. 7 Types of Mergers p. 7 Reasons for Mergers and Acquisitions p. 8 Merger Financing p. 8 Merger Professionals p.

Preface p. xi Background p. 1 Introduction p. 3 Definitions p. 7 Valuing a Transaction p. 7 Types of Mergers p. 7 Reasons for Mergers and Acquisitions p. 8 Merger Financing p. 8 Merger Professionals p.

Investment Knowledge Series. Valuation

Investment Knowledge Series Valuation INVESTMENT KNOWLEDGE SERIES Valuation capital city training & consulting www.capitalcitytraining.com i Published 2011 by Capital City Training Ltd ISBN: 978-0-9569238-1-3

Investment Knowledge Series Valuation INVESTMENT KNOWLEDGE SERIES Valuation capital city training & consulting www.capitalcitytraining.com i Published 2011 by Capital City Training Ltd ISBN: 978-0-9569238-1-3

Final Exam: Corporate Finance

Final Exam: Corporate Finance Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. Thexos Inc. is a company that has operated in two businesses, housewares

Final Exam: Corporate Finance Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. 1. Thexos Inc. is a company that has operated in two businesses, housewares

International Glossary of Business Valuation Terms

International Glossary of Business Valuation Terms To enhance and sustain the quality of business valuations for the benefit of the profession and its clientele, the below identified societies and organizations

International Glossary of Business Valuation Terms To enhance and sustain the quality of business valuations for the benefit of the profession and its clientele, the below identified societies and organizations

Capital Budgeting in Global Markets

Capital Budgeting in Global Markets Fall 2013 Stephen Sapp Yes, our chief analyst is recommending further investments in the new year. 1 Introduction Capital budgeting is the process of determining which

Capital Budgeting in Global Markets Fall 2013 Stephen Sapp Yes, our chief analyst is recommending further investments in the new year. 1 Introduction Capital budgeting is the process of determining which

Advanced Company Analysis Valuation & Financial Modelling. 5-9 March 2017 Manama, Bahrain. euromoneylearningsolutions.

Advanced Company Analysis Valuation & Financial Modelling 5-9 March 2017 Manama, Bahrain euromoneylearningsolutions.com/learnmore Advanced Company Analysis Valuation & Financial Modelling Accelerate your

Advanced Company Analysis Valuation & Financial Modelling 5-9 March 2017 Manama, Bahrain euromoneylearningsolutions.com/learnmore Advanced Company Analysis Valuation & Financial Modelling Accelerate your

Maximizing the value of the firm is the goal of managing capital structure.

Key Concepts and Skills Understand the effect of financial leverage on cash flows and the cost of equity Understand the impact of taxes and bankruptcy on capital structure choice Understand the basic components

Key Concepts and Skills Understand the effect of financial leverage on cash flows and the cost of equity Understand the impact of taxes and bankruptcy on capital structure choice Understand the basic components

Avenue Investment Management Proxy Policy and Corporate Governance

Avenue Investment Management Inc. Avenue Investment Management Proxy Policy and Corporate Governance We know that shareholders rightfully look to Avenue Investment Management to be responsive to matters

Avenue Investment Management Inc. Avenue Investment Management Proxy Policy and Corporate Governance We know that shareholders rightfully look to Avenue Investment Management to be responsive to matters

Link download Solutions Manual:

DOWNLOAD FULL TEST BANK FOR ADVANCED ACCOUNTING 12TH EDITION BY FISCHER TAYLOR CHENG Link download full: https://testbankservice.com/download/test-bank-for-advancedaccounting-12th-edition-by-fischer-taylor-cheng/

DOWNLOAD FULL TEST BANK FOR ADVANCED ACCOUNTING 12TH EDITION BY FISCHER TAYLOR CHENG Link download full: https://testbankservice.com/download/test-bank-for-advancedaccounting-12th-edition-by-fischer-taylor-cheng/

MERGERS, ACQUISITIONS, AND CORPORATE RESTRUCTURINGS

MERGERS, ACQUISITIONS, AND CORPORATE RESTRUCTURINGS FIFTH EDITION PATRICK A. GAUGHAN WILEY JOHN WILEY & SONS, INC. CONTENTS Case Study Preface xi xv Part 1 Background 1 1 Introduction 3 Recent M&A Trends

MERGERS, ACQUISITIONS, AND CORPORATE RESTRUCTURINGS FIFTH EDITION PATRICK A. GAUGHAN WILEY JOHN WILEY & SONS, INC. CONTENTS Case Study Preface xi xv Part 1 Background 1 1 Introduction 3 Recent M&A Trends

Corporate Finance. Dr Cesario MATEUS Session

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 4 26.03.2014 The Capital Structure Decision 2 Maximizing Firm value vs. Maximizing Shareholder Interests If the

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 4 26.03.2014 The Capital Structure Decision 2 Maximizing Firm value vs. Maximizing Shareholder Interests If the

ESOPs: Myths, Methods, and Mistakes

ESOPs: Myths, Methods, and Mistakes How it works The ins and outs of ESOPs Common misconceptions explained Tips and tricks Risks vs. rewards How to avoid common mistakes Contentsoduction 3 The Ins & Outs

ESOPs: Myths, Methods, and Mistakes How it works The ins and outs of ESOPs Common misconceptions explained Tips and tricks Risks vs. rewards How to avoid common mistakes Contentsoduction 3 The Ins & Outs

Final Examination Semester 2 / Year 2010

Southern College Kolej Selatan 南方学院 Final Examination Semester 2 / Year 2010 COURSE : COURSE CODE : FINE3003 TIME : 2 1/2 HOURS DEPARTMENT : ACCOUNTING & FINANCE, MANAGEMENT LECTURER : KAN YOKE YUE Students

Southern College Kolej Selatan 南方学院 Final Examination Semester 2 / Year 2010 COURSE : COURSE CODE : FINE3003 TIME : 2 1/2 HOURS DEPARTMENT : ACCOUNTING & FINANCE, MANAGEMENT LECTURER : KAN YOKE YUE Students

On Track. Focus on ETF Performance. For professional clients only

On Track Focus on ETF Performance For professional clients only Introduction ETFs have been designed to provide low-cost and transparent access to the world s markets, combining the simple tradability

On Track Focus on ETF Performance For professional clients only Introduction ETFs have been designed to provide low-cost and transparent access to the world s markets, combining the simple tradability

Third, achieve optimal tax-efficiency and avoid triggering an immediate taxable event, if possible.

MONETIZING PRIVATELY-HELD AND FAMILY-OWNED BUSINESSES Overview Financial and wealth advisors often serve private clients who are wealthy on paper, but the bulk of whose wealth is tied up in the ownership

MONETIZING PRIVATELY-HELD AND FAMILY-OWNED BUSINESSES Overview Financial and wealth advisors often serve private clients who are wealthy on paper, but the bulk of whose wealth is tied up in the ownership

Agency Costs of Free Cash Flow, CorporateFinance, and Takeovers. The Role of Debt in Motivating Organizational Efficiency

Agency Costs of Free Cash Flow, CorporateFinance, and Takeovers A++ Conflicts between Managers and Shareholders Pursue Growth: Agency theory Payouts to shareholders reduce the resources under manager s

Agency Costs of Free Cash Flow, CorporateFinance, and Takeovers A++ Conflicts between Managers and Shareholders Pursue Growth: Agency theory Payouts to shareholders reduce the resources under manager s

SOLUTION FINANCIAL MANAGEMENT MAY 2013

SOLUTION 1 a) A demerger results in the splitting up of a firm into smaller, legally separate firms. The financial benefits and disadvantages are largely dependent upon the individual situation. Among

SOLUTION 1 a) A demerger results in the splitting up of a firm into smaller, legally separate firms. The financial benefits and disadvantages are largely dependent upon the individual situation. Among

Merger, Acquisition & Restructuring

13 Merger, Acquisition & Restructuring Question 1 Explain synergy in the context of Mergers and Acquisitions. (4 Marks) (November 2012) Synergy May be defined as follows: V (AB) > V(A) + V (B). In other

13 Merger, Acquisition & Restructuring Question 1 Explain synergy in the context of Mergers and Acquisitions. (4 Marks) (November 2012) Synergy May be defined as follows: V (AB) > V(A) + V (B). In other

DIVERSIFICATION AND THE PRIVATELY HELD BUSINESS

DIVERSIFICATION AND THE PRIVATELY HELD BUSINESS STRATEGIC CONSIDERATIONS FOR A HIGHLY CONCENTRATED ASSET CLASS For many of the world s most successful entrepreneurs, the creation of significant wealth

DIVERSIFICATION AND THE PRIVATELY HELD BUSINESS STRATEGIC CONSIDERATIONS FOR A HIGHLY CONCENTRATED ASSET CLASS For many of the world s most successful entrepreneurs, the creation of significant wealth

T.Y.B.F.M. Sem VI. Corporate Restructuring

T.Y.B.F.M Sem VI Corporate Restructuring Note- All Questions are compulsory. Marks in the bracket indicate full marks. Q. 1 (A) Fill in the blanks (Any 8) (8) 1. refers to the material consolidation of

T.Y.B.F.M Sem VI Corporate Restructuring Note- All Questions are compulsory. Marks in the bracket indicate full marks. Q. 1 (A) Fill in the blanks (Any 8) (8) 1. refers to the material consolidation of

How Markets React to Different Types of Mergers

How Markets React to Different Types of Mergers By Pranit Chowhan Bachelor of Business Administration, University of Mumbai, 2014 And Vishal Bane Bachelor of Commerce, University of Mumbai, 2006 PROJECT

How Markets React to Different Types of Mergers By Pranit Chowhan Bachelor of Business Administration, University of Mumbai, 2014 And Vishal Bane Bachelor of Commerce, University of Mumbai, 2006 PROJECT

For purposes of this book the term private equity refers to the

CCC-Bierman 01 (1-34).qxp 11/18/02 9:40 AM Page 1 CHAPTER 1 The Many Virtues of Private Equity For purposes of this book the term private equity refers to the common stock of a corporation where that common

CCC-Bierman 01 (1-34).qxp 11/18/02 9:40 AM Page 1 CHAPTER 1 The Many Virtues of Private Equity For purposes of this book the term private equity refers to the common stock of a corporation where that common

INTERNATIONAL UNIVERSITY OF JAPAN MBA PROGRAM Syllabus Corporate Restructuring and M&A by Takato Hiraki Visiting Professor Spring 2014

INTERNATIONAL UNIVERSITY OF JAPAN MBA PROGRAM Syllabus Corporate Restructuring and M&A by Takato Hiraki Visiting Professor Spring 2014 Office Hours: 10:00 ~10:30 am and noon time on Monday (and by appointment)

INTERNATIONAL UNIVERSITY OF JAPAN MBA PROGRAM Syllabus Corporate Restructuring and M&A by Takato Hiraki Visiting Professor Spring 2014 Office Hours: 10:00 ~10:30 am and noon time on Monday (and by appointment)

CHAPTER 25 ACQUISITIONS AND TAKEOVERS

1 CHAPTER 25 ACQUISITIONS AND TAKEOVERS Firms are acquired for a number of reasons. In the 1960s and 1970s, firms such as Gulf and Western and ITT built themselves into conglomerates by acquiring firms

1 CHAPTER 25 ACQUISITIONS AND TAKEOVERS Firms are acquired for a number of reasons. In the 1960s and 1970s, firms such as Gulf and Western and ITT built themselves into conglomerates by acquiring firms

Industry Consolidations Financing Alternatives for Acquisition-Driven Companies

Financing Alternatives for Acquisition-Driven Companies Charles A Sheffield President, Sheffield Capital Advisors This article focuses on the trends and financing opportunities for clients who are pursuing

Financing Alternatives for Acquisition-Driven Companies Charles A Sheffield President, Sheffield Capital Advisors This article focuses on the trends and financing opportunities for clients who are pursuing

Advanced Leveraged Buyouts and LBO Models Quiz Questions

Advanced Leveraged Buyouts and LBO Models Quiz Questions Types of Debt Transaction and Operating Assumptions Sources & Uses Pro-Forma Balance Sheet Adjustments Debt Schedules Linking and Modifying the

Advanced Leveraged Buyouts and LBO Models Quiz Questions Types of Debt Transaction and Operating Assumptions Sources & Uses Pro-Forma Balance Sheet Adjustments Debt Schedules Linking and Modifying the

TRANSFERRING YOUR COMPANY TO KEY EMPLOYEES WHITE PAPER

Julia. M Carlson 1007 SW Bayley Street Newport, OR 97365 julia.carlson@lpl.com Phone: (541) 574-6464 www.financialfreedomwmg.com TRANSFERRING YOUR COMPANY TO KEY EMPLOYEES WHITE PAPER Owners wishing to

Julia. M Carlson 1007 SW Bayley Street Newport, OR 97365 julia.carlson@lpl.com Phone: (541) 574-6464 www.financialfreedomwmg.com TRANSFERRING YOUR COMPANY TO KEY EMPLOYEES WHITE PAPER Owners wishing to

Choosing the Right Valuation Approach

Choosing the Right Valuation Approach Robert Parrino, CFA Director Hicks, Muse, Tate & Furst Center for Private Equity Finance McCombs School of Business, University of Texas at Austin Austin, Texas Before

Choosing the Right Valuation Approach Robert Parrino, CFA Director Hicks, Muse, Tate & Furst Center for Private Equity Finance McCombs School of Business, University of Texas at Austin Austin, Texas Before

Advanced Structuring of LBOs & Private Equity Transactions Masterclass

Advanced Structuring of LBOs & Private Equity Transactions Masterclass A comprehensive examination of PE reviewing the 5 stages from PE, lender, advisors, management and investor s perspective This Course

Advanced Structuring of LBOs & Private Equity Transactions Masterclass A comprehensive examination of PE reviewing the 5 stages from PE, lender, advisors, management and investor s perspective This Course

Lecture 8 (Notes by Leora Schiff) The Law of Mergers and Acquisitions (Spring 2003) - Prof. John Akula

The Law of Mergers and Acquisitions (Spring 2003) - Prof. John Akula") Lecture 8 (Notes by Leora Schiff) 15.649 - The Law of Mergers and Acquisitions (Spring 2003) - Prof. John Akula Sarbanes-Oxley I. New Rules for Directors and Officers a. CEO/CFO certifications i. Section

Lecture 8 (Notes by Leora Schiff) 15.649 - The Law of Mergers and Acquisitions (Spring 2003) - Prof. John Akula Sarbanes-Oxley I. New Rules for Directors and Officers a. CEO/CFO certifications i. Section

M.V.S.R Engineering College. Department of Business Managment

M.V.S.R Engineering College Department of Business Managment CONCEPTS IN FINANCIAL MANAGEMENT 1. Finance. a.finance is a simple task of providing the necessary funds (money) required by the business of

M.V.S.R Engineering College Department of Business Managment CONCEPTS IN FINANCIAL MANAGEMENT 1. Finance. a.finance is a simple task of providing the necessary funds (money) required by the business of