The Features of Investment Decision-Making

|

|

|

- Carol Mercy Wells

- 6 years ago

- Views:

Transcription

1 The Features of Investment Decision-Making Industrial management Controlling and Audit Olga Zhukovskaya

2 Main Issues 1. The Concept of Investing 2. The Tools for Investment Decision-Making 3. Mergers and Acquisitions 4. Strategic Plan Formation

3 1. The Concept of Investing

4 Investment Controlling is the fulfillment of Controlling targets regarding the different phases of the planning, realisation, and control of investments Investment Controlling has to ensure the target-orientated course of the entire planning and realisation process by firstly providing decision-orientated information, secondly by coordinating parts of the planning and finally by adequately controlling the course of planning.

5 Investing is the act of committing money or capital with the expectation of obtaining an additional income or profit.

6 Main distinctive features: Investing is not gambling. Gambling is putting money at risk by betting on an uncertain outcome with the hope that you might win money. A real investor does not simply throw his or her money at any random investment; he or she performs thorough analysis and commits capital only when there is a reasonable expectation of profit. There are still risks, and there are no guarantees, but investing is more than simply hoping.

not all")

7 Motives for investing the prospect of making a profit risks for the few remarkable successes which might come their way (eg. venture capital) not all investors want to make huge profits (eg. social enterprises)

8 Capital investment A capital investment involves a current cash outlay in anticipation of realizing benefits in the future, generally (well) beyond one year. These benefits may be either in the form of increased revenues or reductions in costs: the expenditures are called accordingly as income-expansion, or cost-reduction, expenditures. The cash outlay (as capital expenditure CapEx) go towards addition, disposition, modification, creation and replacement of fixed assets.

9 Types of capital investment The main type of capital investment is in fixed assets to allow increased operational capacity, capture a larger share of the market and in the process, generate more revenue. Companies may also make capital investment in the form of equity stakes in other companies operations, which indirectly benefits the investor companies by building business partnerships or expanding into new markets. Sources of capital The first funding option is always a company s own operating cash flow, which sometimes may not be enough to satisfy the amount of capital expenditures required. outside financing

10 The basic features of capital investment decisions are: a series of large anticipated benefits; a relatively high degree of risk; a relatively long period over which the returns are likely to be realised.

11 There are three broad motives for capital investment: renewal of worn out assets; acquisition of additional assets to expand the business and increase output; innovation to reduce costs and/or to create new value.

12

13

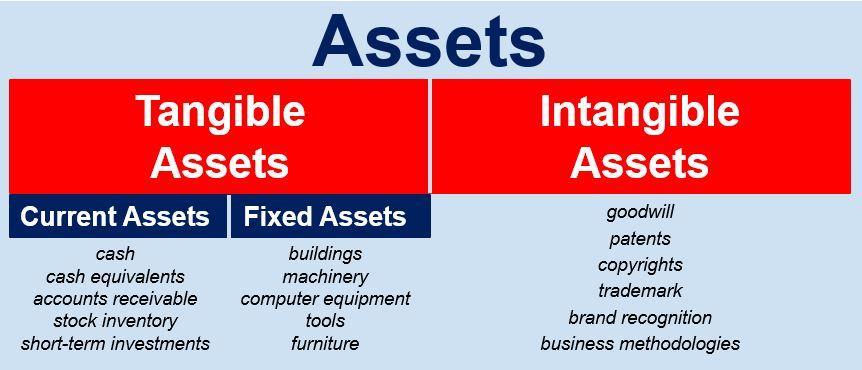

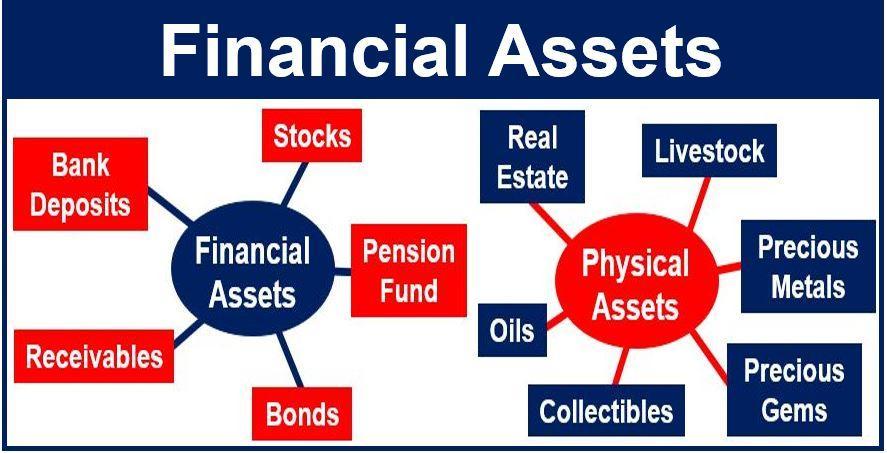

14 Objects of investment activity: assets (tangible, intangible, financial); immovable property, including enterprise as property complex; securities; intellectual property.

15 Capital investment aims to secure a competitive advantage of the organisation; might arise from better technology, access to new markets or an exclusive innovation.

16 Investment Strategy Systematic plan to allocate investable assets among investment choices such as bonds, certificates of deposit, commodities, real estate, stocks (shares), etc.

17 Investment Strategies Aggressive Investment Strategy attempts to maximize returns by taking a relatively higher degree of risk; emphasizes capital appreciation as a primary investment objective, rather than income or safety of principal. Passive investing aims to maximize returns over the long run by keeping the amount of buying and selling to a minimum; by avoiding the fees and the drag on performance that potentially occur from frequent trading; is not aimed at making quick gains or at getting rich with one great bet, but rather on building slow, steady wealth over time.

18 Capital budgeting techniques Now, the question is how to make sure that the decision is correct and rational. In a profit-oriented organization, it is simple to decide on to the objective of investing. The decision would be considered appropriate if it is a profitable investment and enhances the wealth of the shareholders. Capital budgeting techniques are utilized to do investment appraisal for such investments.

19 Capital budgeting Capital budgeting is a process used by companies for evaluating and ranking potential expenditures or investments that are significant in amount. Capital budgeting is a tool for maximizing a company s future profits since most companies are able to manage only a limited number of large projects at any one time.

20 Capital budgeting usually involves: the calculation of each project s future accounting profit by period, the cash flow by period, the present value of the cash flows after considering the time value of money, the number of years it takes for a project s cash flow to pay back the initial cash investment, an assessment of risk, and other factors.

21 2.The Tools for Investment Decision-Making

22 Time-value-of-money concepts In modern finance, time-value-of-money concepts play a central role in decision support and planning. When investment projections or business case results extend more than a year into the future, professionals usually want to see cash flows presented in two forms: in discounted terms and in non-discounted terms. Financial specialists want to see the timevalue-of-money impact on long-term projections.

23 Time Value of Money (TVM) is an important concept in financial management used to compare investment alternatives. A key feature of TVM is that a single sum of money or a series of equal, evenly-spaced payments or receipts promised in the future can be converted to an equivalent value today. Conversely, you can determine the value to which a single sum or a series of future payments will grow to at some future date.

24 The 5 components of TVM problems Periods (n). The total number of compounding or discounting periods in the holding period. Rate (i). The periodic interest rate or discount rate used in the analysis, usually expressed as an annual percentage. Present Value (PV). Represents a single sum of money today. Payment (PMT). Represents equal periodic payments received or paid each period. When payments are received they are positive, when payments are made they are negative. Future Value (FV). A one-time single sum of money to be received or paid in the future.

25 Discounted cash flow (DCF) is an application of the TVM concept the idea that money to be received or paid at some time in the future has less value, today, than an equal amount actually received or paid today. The DCF calculation finds the value appropriate today the present value for the future cash flow. The term discounting applies because the DCF present value is always lower than the cash flow future value.

26 The reasons for using DCF the PV of future funds is discounted below FV of the funds for at least three reasons: Opportunity. Money you have now could (in principle) be invested now, and gain return or interest between now and the future time. Money you will not have until a future time cannot be used now. Risk. Money you have now is not at risk. Money expected in the future is less certain. A well known proverb states this principle more colorfully: A bird in hand is worth two in the bush. Inflation: A sum you have today will very likely buy more than an equal sum you will not have until years in future. Inflation over time reduces the buying power of money.

27 Capital budgeting methods Discounting Cash Flow Criteria: Non-Discounting Cash Flow Criteria: Net Present Value (NPV) Benefit to Cost Ratio (BCR) Internal Rate of Return (IRR) Payback Period (PP) Accounting Rate of Return (ARR)

28 Payback period (PP) is the length of time required to recover the cost of an investment. The payback period of a given investment or project is an important determinant of whether to undertake the position or project, as longer payback periods are typically not desirable for investment positions. PP = Initial Investment / Annual Cash Inflow The discounted payback period discounts each of the estimated cash flows and then determines the payback period from those discounted flows.

29 Accounting Rate of Return (ARR) Accounting Rate of Return / Average rate of return / Simple Rate of Return (ARR) is the amount of profit, or return, an individual can expect based on an investment made. Accounting rate of return divides the average profit by the initial investment to get the ratio or return that can be expected. ARR does not consider the time value of money, which means that returns taken in during later years may be worth less than those taken in now. ARR = Average Accounting Profit / Average investment

30 In discounted cash flow analysis, two value terms are central: Present value (PV) describes how much a future sum of money is worth today. PV = CF/(1+r) n Where: CF = cash flow in future period r = the periodic rate of return or interest (also called the discount rate or the required rate of return) n = number of periods Futue value (FV) refers to a method of calculating how much the PV of an asset or cash will be worth at a specific time in the future.

31 The key idea of DCF Money loses its value over time which makes it more desirable to have it now rather than later. The longer the time period before an actual cash flow event occurs, the more the present value of future money is discounted below its future value.

32 Benefit Cost Ratio (BCR) A Benefit cost ratio (BCR) attempts to identify the relationship between the cost and benefits of a proposed project. The total discounted benefits are divided by the total discounted costs. Projects with a BCR greater than 1 have greater benefits than costs; hence they have positive net benefits. The higher the ratio, the greater the benefits relative to the costs.

33 Net present value (NPV) The total discounted value (present value) for a series of cash flow events across a time period extending into the future is the net present value (NPV) of a cash flow stream. The net present value (NPV) is an investment measure that tells an investor whether the investment is achieving a target yield at a given initial investment.

34 NPV theory According to NPV theory the future cash flows of an investment project are estimated. The expected cash flows are discounted at the cost of capital for the corporation and the results summed. If the NPV is positive the project is worthwhile and should be pursued. If it is negative the project should be turned down. If the NPV is zero it does not matter to the corporation whether the project is accepted or rejected.

35 NPV NPV also quantifies the adjustment to the initial investment needed to achieve the target yield assuming everything else remains the same. Formally, the NPV is simply the summation of cash flows (C) for each period (n) in the holding period (N), discounted at the investor s required rate of return (r):

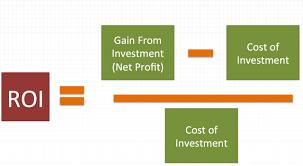

36 IRR Internal Rate of Return of an investment is the discount rate at which the net present value of costs (negative cash flows) of the investment equals the net present value of the benefits (positive cash flows) of the investment. 0 = P 0 + P 1 /(1+IRR) + P 2 /(1+IRR) 2 + P 3 /(1+IRR) P n /(1+IRR) n

37 IRR: main characteristics IRR allows managers to rank projects by their overall rates of return rather than their net present values, and the investment with the highest IRR is usually preferred IRR does not measure the absolute size of the investment or the return: this means that IRR can favor investments with high rates of return IRR is used to evaluate the attractiveness of a project or investment: if the IRR of a new project exceeds a company s required rate of return, that project is desirable

38 IRR: main characteristics Internal rate of return (IRR) is the interest rate at which the net present value of all the cash flows (both positive and negative) from a project or investment equal zero. Internal rate of return (IRR) for an investment is the percentage rate earned on each dollar invested for each period it is invested. IRR is also another term people use for interest.

39 NPV and IRR the NPV formula solves for the present value of a stream of cash flows, given a discount rate. The IRR on the other hand, solves for a rate of return when setting the NPV equal to zero (0). the IRR answers the question what rate of return will I achieve, given the following stream of cash flows? the NPV answers the question what is the following stream of cash flows worth at a particular discount rate, in today s money?

40 Weighted average cost of capital (WACC) Weighted average cost of capital (WACC) is a calculation of a firm s cost of capital in which each category of capital is proportionately weighted. All after-tax sources of capital are included in a WACC calculation. To calculate WACC, multiply the cost of each capital component by its proportional weight and take the sum of the results. Investors may often use WACC as an indicator of whether or not an investment is worth pursuing. WACC is the minimum acceptable rate of return at which a company yields returns for its investors.

41 Cash Flow Return on Investment (CFROI) CFROI is a term that refers to the operational performance of the enterprise, that the enterprise would achieve in case that it would generate operating cash flow in the same volume, which it reached in the reference period without additional investments over the life of current assets. Its calculation is based on the concept of IRR. CFROI = Cash Flow / Market Value of Capital Employed (Capital employed = Total Assets Current Liabilities)

42 Economic Value Added (EVA) is a measure of surplus value created on an investment can also be referred to as economic profit, and it attempts to capture the true economic profit of a company Elaborated by Stern Stewart & Co EVA = (Return on Capital - Cost of Capital) (Capital Invested in Project) EVA = NOPAT - WACC х CE, where NOPAT (Net Operating Profit Adjusted Taxes); WACC (Weighted Average Cost of Capital); CE (Capital Employed). *Operating Profit = Revenue - cost of goods sold, labor, and other day-to-day expenses incurred in the normal course of business

43 Real Options Theory Real Options Theory is an important new framework in the theory of investment decision. The standard theory it modifies is the NPV theory of investment decision. Where NPV theory is deficient and where Real Options theory fills the gap is where subsequent decisions can modify the project once it is undertaken. NPV makes no provision for this flexibility of the project and consequently undervalues its benefits.

44 Return on investment (ROI) Return on investment (ROI) measures the gain or loss generated on an investment relative to the amount of money invested. ROI is usually expressed as a percentage and is typically used for personal financial decisions, to compare a company s profitability or to compare the efficiency of different investments. ROI = (Net Profit / Cost of Investment) x 100%

45 Return on Investment (ROI)

46 3. Mergers and Acquisitions

47 Mergers and acquisitions (M&A) are tools of a long-term business strategy Mergers and acquisitions (M&A) is a general term that refers to the consolidation of companies or assets. We will refer to mergers and acquisitions (M & A) as a business transaction where one company acquires another company.

48 M & A When one company takes over another and clearly established itself as the new owner, the purchase is called an acquisition. From a legal point of view, the target company (the acquired company) ceases to exist, the buyer (the acquiring company) swallows the business and the buyer s stock continues to be traded. A merger happens when firms agree to go forward as a single new company rather than remain separately owned and operated. Both companies stocks are surrendered and new company stock is issued in its place.

49 Horizontal Mergers when a company merges or takes over another company that offers the same or similar product lines and services to the final consumers eliminates competition, which helps the company to increase its market share, revenues and profits, it also offers economies of scale A merger between Coca-Cola and the Pepsi beverage division, for example, would be horizontal in nature

50 Vertical Mergers combine two companies that are in the same value chain of producing the same good and service, but the only difference is the stage of production at which they are operating to secure supply of essential goods, and avoid disruption in supply For example, if a clothing store takes over a textile factory, this would be termed as vertical merger, since the industry is same, i.e. clothing, but the stage of production is different.

51 Concentric Mergers take place between firms that serve the same customers in a particular industry, but they don t offer the same products and services to facilitate consumers, since it would be easier to sell these products together; this would help the company diversify, hence higher profit; selling one of the products will also encourage the sale of the other, hence more revenues for the company if it manages to increase the sale of one of its product; to offer one-stop shopping, and therefore, convenience for consumers. For example, if a company that produces DVDs mergers with a company that produces DVD players, this would be termed as concentric merger, since DVD players and DVDs are complements products, which are usually purchased together.

52 Conglomerate Mergers When two companies that operates in completely different industry, regardless of the stage of production, a merger between both companies is known as conglomerate merger. This is usually done to diversify into other industries, which helps reduce risks. Example of a conglomerate merger was the merger between the Walt Disney Company and the American Broadcasting Company.

53 Asset Acquisitions individually identified assets and liabilities of the seller are sold to the acquirer The acquirer can choose which specific assets and liabilities it wants to purchase, avoiding unwanted assets and liabilities for which it does not want to assume responsibility

54 Stock Acquisitions all of the assets and liabilities of the seller are sold upon transfer of the seller s stock to the acquirer As such, no tedious valuation of the seller s individual assets and liabilities is required and the transaction is mechanically simple

55 The M&A Process can be broken down into five phases: Phase 4 Acquire through Negotiation Phase 3 Investigate & Value the Target Phase 5 Post-Merger Integration Phase 2 Search & Screen Targets Phase 1 Pre-Acquisition Review

56 Pre-Acquisition Review to assess your own situation and determine if a merger and acquisition strategy should be implemented Pre-merger integration activities (timing, communications and shared vision) are most critical, but often ignored. In general, companies focus purely on the financial side of the transaction. It is precisely because of this that 60 to 80 percent of mergers fail.

57 Search & Screen Targets is to search for possible takeover candidates. Target companies must fulfill a set of criteria so that the target company is a good strategic fit with the acquiring company. Compatibility and fit should be assessed across a range of criteria relative size, type of business, capital structure, organizational strengths, core competencies, market channels, etc. The search and screening process is performed inhouse by the acquiring company.

58 Investigate & Value the Target a more detail analysis of the target company. One wants to confirm that the target company is truly a good fit with the acquiring company. This will require a more thorough review of operations, strategies, financials, and other aspects of the target company. This detail review is called due diligence. Phase due diligence is initiated once a target company has been selected. A key part of due diligence is the valuation of the target company. In the preliminary phases of M & A, one will calculate a total value for the combined company. One has already calculated a value for our company (acquiring company) and now wants to calculate a value for the target as well as all other costs associated with the M & A.

59 Acquire through Negotiation Now that one has selected our target company, it s time to start the process of negotiating a M & A. One needs to develop a negotiation plan The most common approach to acquiring another company is for both companies to reach agreement concerning the M & A; i.e. a negotiated merger will take place. This negotiated arrangement is sometimes called a bear hug

60 Post-Merger Integration If all goes well, the two companies will announce an agreement to merge the two companies. The deal is finalized in a formal merger and acquisition agreement. Every company is different differences in culture, differences in information systems, differences in strategies, etc. As a result, the Post Merger Integration Phase is the most difficult phase within the M & A Process. This requires extensive planning and design throughout the entire organization.

61 Risks Even in situations where the acquired company is in the same line of business as the acquirer and is small enough to allow for easy post-merger integration, the likelihood of success is only about 50% Poor or inadequate communications A lack of transparency and inadequately preparing for the inclusion and retention of core competencies and staffing Not incorporating and building upon the branding, marketing and sales efforts Having two distinct cultures and service standards and not taking time to balance and merge the two (keep the best of both and lose the worst of both)

62 4.Strategic Plan Formation

63 A strategic plan is a document used to communicate with the organization the organizations goals, the actions needed to achieve those goals and all of the other critical elements developed during the planning exercise.

64 Balanced Scorecard (BSC) is a strategic planning and management system that is used extensively in business and industry, government, and nonprofit organizations worldwide to align business activities to the vision and strategy of the organization, improve internal and external communications, and monitor organization performance against strategic goals. There are over a hundred balanced scorecard and/or performance management automation development companies.

65 The balanced scorecard suggests that we view the organization from four perspectives, and to develop metrics, collect data and analyze it relative to each of these perspectives: Each of the four perspectives is interdependent - improvement in just one area is not necessarily a recipe for success in the other areas.

66 Factors in BSC (examples) Finance (Return On Investment, Cash Flow, Return on Capital Employed, Financial Results (Quarterly/Yearly)) Internal Business Processes (Number of activities per function, Duplicate activities across functions, Process alignment (is the right process in the right department?), Process bottlenecks, Process automation)

Customer (Delivery performance to customer, Quality performance for customer, Customer")

67 Factors in BSC (examples) Learning & Growth (Is there the correct level of expertise for the job? Employee turnover, Job satisfaction, Training/Learning opportunities) Customer (Delivery performance to customer, Quality performance for customer, Customer satisfaction rate, Customer percentage of market, Customer retention rate)

68 SMART The metrics set up must be SMART (commonly, Specific, Measurable, Achievable, Realistic and Timely) you cannot improve on what you can t measure! Metrics must also be aligned with the company s strategic plan.

69 To embark on the Balanced Scorecard path an organization first must know (and understand) the following: the company s mission statement; the company s strategic plan/vision; then the financial status of the organization; how the organization is currently structured and operating; the level of expertise of their employees; customer satisfaction level.

70

71 Thanks for Your Attention!

CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com.

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 3& 4 INVESTMENT APPRAISAL METHODS June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com. WESTFORD 2008 Thomson SCHOOL South-Western

MANAGEMENT OF FINANCIAL RESOURCES AND PERFORMANCE SESSIONS 3& 4 INVESTMENT APPRAISAL METHODS June 10 to 24, 2013 CA. Sonali Jagath Prasad ACA, ACMA, CGMA, B.Com. WESTFORD 2008 Thomson SCHOOL South-Western

The nature of investment decision

The nature of investment decision Investment decisions must be consistent with the objectives of the particular organization. In private-sector business, maximizing the wealth of the owners is normally

The nature of investment decision Investment decisions must be consistent with the objectives of the particular organization. In private-sector business, maximizing the wealth of the owners is normally

Commercestudyguide.com Capital Budgeting. Definition of Capital Budgeting. Nature of Capital Budgeting. The process of Capital Budgeting

Commercestudyguide.com Capital Budgeting Capital Budgeting decision is considered the most important and most critical decision for a finance manager. It involves decisions related to long-term investments

Commercestudyguide.com Capital Budgeting Capital Budgeting decision is considered the most important and most critical decision for a finance manager. It involves decisions related to long-term investments

The Capital Expenditure Decision

1 2 October 1989 The Capital Expenditure Decision CONTENTS 2 Paragraphs INTRODUCTION... 1-4 SECTION 1 QUANTITATIVE ESTIMATES... 5-44 Fixed Investment Estimates... 8-11 Working Capital Estimates... 12 The

1 2 October 1989 The Capital Expenditure Decision CONTENTS 2 Paragraphs INTRODUCTION... 1-4 SECTION 1 QUANTITATIVE ESTIMATES... 5-44 Fixed Investment Estimates... 8-11 Working Capital Estimates... 12 The

Chapter 11: Capital Budgeting: Decision Criteria

11-1 Chapter 11: Capital Budgeting: Decision Criteria Overview and vocabulary Methods Payback, discounted payback NPV IRR, MIRR Profitability Index Unequal lives Economic life 11-2 What is capital budgeting?

11-1 Chapter 11: Capital Budgeting: Decision Criteria Overview and vocabulary Methods Payback, discounted payback NPV IRR, MIRR Profitability Index Unequal lives Economic life 11-2 What is capital budgeting?

Session 02. Investment Decisions

Session 02 Investment Decisions Programme : Executive Diploma in Accounting, Business & Strategy (EDABS 2017) Course : Corporate Financial Management (EDABS 202) Lecturer : Mr. Asanka Ranasinghe MBA (Colombo),

Session 02 Investment Decisions Programme : Executive Diploma in Accounting, Business & Strategy (EDABS 2017) Course : Corporate Financial Management (EDABS 202) Lecturer : Mr. Asanka Ranasinghe MBA (Colombo),

INTRODUCTION TO FINANCIAL MANAGEMENT

INTRODUCTION TO FINANCIAL MANAGEMENT Meaning of Financial Management As we know finance is the lifeblood of every business, its management requires special attention. Financial management is that activity

INTRODUCTION TO FINANCIAL MANAGEMENT Meaning of Financial Management As we know finance is the lifeblood of every business, its management requires special attention. Financial management is that activity

Topics in Corporate Finance. Chapter 2: Valuing Real Assets. Albert Banal-Estanol

Topics in Corporate Finance Chapter 2: Valuing Real Assets Investment decisions Valuing risk-free and risky real assets: Factories, machines, but also intangibles: patents, What to value? cash flows! Methods

Topics in Corporate Finance Chapter 2: Valuing Real Assets Investment decisions Valuing risk-free and risky real assets: Factories, machines, but also intangibles: patents, What to value? cash flows! Methods

Unit-2. Capital Budgeting

Unit-2 Capital Budgeting Unit Structure 2.0. Objectives. 2.1. Introduction. 2.2. Presentation of subject matter. 2.2.1 Meaning of capital budgeting. 2.2.2 Capital expenditure. 2.2.3 Definitions. 2.2.4

Unit-2 Capital Budgeting Unit Structure 2.0. Objectives. 2.1. Introduction. 2.2. Presentation of subject matter. 2.2.1 Meaning of capital budgeting. 2.2.2 Capital expenditure. 2.2.3 Definitions. 2.2.4

CHAPTER 2 LITERATURE REVIEW

CHAPTER 2 LITERATURE REVIEW Capital budgeting is the process of analyzing investment opportunities and deciding which ones to accept. (Pearson Education, 2007, 178). 2.1. INTRODUCTION OF CAPITAL BUDGETING

CHAPTER 2 LITERATURE REVIEW Capital budgeting is the process of analyzing investment opportunities and deciding which ones to accept. (Pearson Education, 2007, 178). 2.1. INTRODUCTION OF CAPITAL BUDGETING

Global Financial Management

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

Session 2, Monday, April 3 rd (11:30-12:30)

") Session 2, Monday, April 3 rd (11:30-12:30) Capital Budgeting Continued and the Cost of Capital v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Internal

Session 2, Monday, April 3 rd (11:30-12:30) Capital Budgeting Continued and the Cost of Capital v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Internal

6.1 CAPITAL PROJECTS 6.2 CAPITAL BUDGETING PROCESS 6.3 CAPITAL PROJECT ANALYSIS 6.4 BUSINESS EXPANSION STRATEGIES

Chapter 6 Long-Term Financial Activities 6.1 CAPITAL PROJECTS 6.2 CAPITAL BUDGETING PROCESS 6.3 CAPITAL PROJECT ANALYSIS 6.4 BUSINESS EXPANSION STRATEGIES Lesson 6.1 Capital Projects Goals Describe types

Chapter 6 Long-Term Financial Activities 6.1 CAPITAL PROJECTS 6.2 CAPITAL BUDGETING PROCESS 6.3 CAPITAL PROJECT ANALYSIS 6.4 BUSINESS EXPANSION STRATEGIES Lesson 6.1 Capital Projects Goals Describe types

Corporate Finance: Introduction to Capital Budgeting

Corporate Finance: Introduction to Capital Budgeting João Carvalho das Neves Professor of Finance, ISEG jcneves@iseg.ulisboa.pt 2018-2019 1 WHAT IS CAPITAL BUDGETING? Capital budgeting is a formal process

Corporate Finance: Introduction to Capital Budgeting João Carvalho das Neves Professor of Finance, ISEG jcneves@iseg.ulisboa.pt 2018-2019 1 WHAT IS CAPITAL BUDGETING? Capital budgeting is a formal process

International Project Management. prof.dr MILOŠ D. MILOVANČEVIĆ

International Project Management prof.dr MILOŠ D. MILOVANČEVIĆ Project Evaluation and Analysis Project Financial Analysis Project Evaluation and Analysis The important aspects of project analysis are:

International Project Management prof.dr MILOŠ D. MILOVANČEVIĆ Project Evaluation and Analysis Project Financial Analysis Project Evaluation and Analysis The important aspects of project analysis are:

UNIT IV CAPITAL BUDGETING

UNIT IV CAPITAL BUDGETING Capital Budgeting: Capital budgeting is the process of making investment decision in long-term assets or courses of action. Capital expenditure incurred today is expected to bring

UNIT IV CAPITAL BUDGETING Capital Budgeting: Capital budgeting is the process of making investment decision in long-term assets or courses of action. Capital expenditure incurred today is expected to bring

A Manager's Guide to Financial Analysis

A Manager's Guide to Financial Analysis A Manager's Guide to Financial Analysis Fifth Edition Steven D. Grossman Contents About This Course How to Take This Course Introduction ix xi xiii 1 Financial

A Manager's Guide to Financial Analysis A Manager's Guide to Financial Analysis Fifth Edition Steven D. Grossman Contents About This Course How to Take This Course Introduction ix xi xiii 1 Financial

INVESTMENT APPRAISAL TECHNIQUES FOR SMALL AND MEDIUM SCALE ENTERPRISES

SAMUEL ADEGBOYEGA UNIVERSITY COLLEGE OF MANAGEMENT AND SOCIAL SCIENCES DEPARTMENT OF BUSINESS ADMINISTRATION COURSE CODE: BUS 413 COURSE TITLE: SMALL AND MEDIUM SCALE ENTERPRISE MANAGEMENT SESSION: 2017/2018,

SAMUEL ADEGBOYEGA UNIVERSITY COLLEGE OF MANAGEMENT AND SOCIAL SCIENCES DEPARTMENT OF BUSINESS ADMINISTRATION COURSE CODE: BUS 413 COURSE TITLE: SMALL AND MEDIUM SCALE ENTERPRISE MANAGEMENT SESSION: 2017/2018,

INTERNATIONAL JOURNAL OF MANAGEMENT RESEARCH AND REVIEW

INTERNATIONAL JOURNAL OF MANAGEMENT RESEARCH AND REVIEW A FUNDAMENTAL STUDY ON LONG- TERM INVESTMENT DECISION P. Selvam* 1, N. Punitavati 2 1 Assistant Professor, Department of Management studies, Alpha

INTERNATIONAL JOURNAL OF MANAGEMENT RESEARCH AND REVIEW A FUNDAMENTAL STUDY ON LONG- TERM INVESTMENT DECISION P. Selvam* 1, N. Punitavati 2 1 Assistant Professor, Department of Management studies, Alpha

Transactional Valuation - M&A / Private Equity August 2011

www.pwc.com Transactional Valuation - M&A / Private Equity Agenda Valuation for Mergers and Acquisition Valuation for PE Valuation for Demergers Slide 2 Valuation for Mergers and Acquisitions Understanding

www.pwc.com Transactional Valuation - M&A / Private Equity Agenda Valuation for Mergers and Acquisition Valuation for PE Valuation for Demergers Slide 2 Valuation for Mergers and Acquisitions Understanding

BFC2140: Corporate Finance 1

BFC2140: Corporate Finance 1 Table of Contents Topic 1: Introduction to Financial Mathematics... 2 Topic 2: Financial Mathematics II... 5 Topic 3: Valuation of Bonds & Equities... 9 Topic 4: Project Evaluation

BFC2140: Corporate Finance 1 Table of Contents Topic 1: Introduction to Financial Mathematics... 2 Topic 2: Financial Mathematics II... 5 Topic 3: Valuation of Bonds & Equities... 9 Topic 4: Project Evaluation

Session 1, Monday, April 8 th (9:45-10:45)

") Session 1, Monday, April 8 th (9:45-10:45) Time Value of Money and Capital Budgeting v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Time Value of Money:

Session 1, Monday, April 8 th (9:45-10:45) Time Value of Money and Capital Budgeting v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Time Value of Money:

Software Economics. Metrics of Business Case Analysis Part 1

Software Economics Metrics of Business Case Analysis Part 1 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements to compare

Software Economics Metrics of Business Case Analysis Part 1 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements to compare

Investment Decision Criteria. Principles Applied in This Chapter. Learning Objectives

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

M.V.S.R Engineering College. Department of Business Managment

M.V.S.R Engineering College Department of Business Managment CONCEPTS IN FINANCIAL MANAGEMENT 1. Finance. a.finance is a simple task of providing the necessary funds (money) required by the business of

M.V.S.R Engineering College Department of Business Managment CONCEPTS IN FINANCIAL MANAGEMENT 1. Finance. a.finance is a simple task of providing the necessary funds (money) required by the business of

Chapter 9. Capital Budgeting Decision Models

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

F3 Financial Strategy. Examiner s Answers

Strategic Level Paper F3 Financial Strategy May 2012 examination Examiner s Answers Question One Rationale This question begins by evaluating the recent financial performance and dividend policy of B.

Strategic Level Paper F3 Financial Strategy May 2012 examination Examiner s Answers Question One Rationale This question begins by evaluating the recent financial performance and dividend policy of B.

Investment Decision Criteria. Principles Applied in This Chapter. Disney s Capital Budgeting Decision

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting

Time Value of Money and Capital Budgeting") AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting Chapters Covered Time Value of Money: Part I, Domain B Chapter 6 Net

AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting Chapters Covered Time Value of Money: Part I, Domain B Chapter 6 Net

The following learning and growth perspective measures could enhance the implementation and management of Wellgas strategy:

SECTION A CASE QUESTIONS (Total: 50 marks) Answer 1(a) Wellgas strategy is to transform a fill-the-petrol tank routine into a delightful shopping experience for service-oriented customers who are ready

SECTION A CASE QUESTIONS (Total: 50 marks) Answer 1(a) Wellgas strategy is to transform a fill-the-petrol tank routine into a delightful shopping experience for service-oriented customers who are ready

Stock valuation. A reading prepared by Pamela Peterson-Drake, Florida Atlantic University

Stock valuation A reading prepared by Pamela Peterson-Drake, Florida Atlantic University O U T L I N E. Valuation of common stock. Returns on stock. Summary. Valuation of common stock "[A] stock is worth

Stock valuation A reading prepared by Pamela Peterson-Drake, Florida Atlantic University O U T L I N E. Valuation of common stock. Returns on stock. Summary. Valuation of common stock "[A] stock is worth

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Learning Objectives LO1 How to compute the net present value and why it is the best decision criterion. LO2 The payback rule and some of its shortcomings.

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Learning Objectives LO1 How to compute the net present value and why it is the best decision criterion. LO2 The payback rule and some of its shortcomings.

Engineering Economics and Financial Accounting

Engineering Economics and Financial Accounting Unit 5: Accounting Major Topics are: Balance Sheet - Profit & Loss Statement - Evaluation of Investment decisions Average Rate of Return - Payback Period

Engineering Economics and Financial Accounting Unit 5: Accounting Major Topics are: Balance Sheet - Profit & Loss Statement - Evaluation of Investment decisions Average Rate of Return - Payback Period

Distractor B: Candidate gets it wrong way round. Distractors C & D: Candidate only compares admin fee to cost without factor.

Answers ACCA Certified Accounting Technician Examination, Paper T10 Managing Finances June 2010 Answers Section A 1 D 2 A 365/ 23 100 1 173 % 100 1 = 365/ 23 1 1+ 1 173 99 = % Candidates should answer

Answers ACCA Certified Accounting Technician Examination, Paper T10 Managing Finances June 2010 Answers Section A 1 D 2 A 365/ 23 100 1 173 % 100 1 = 365/ 23 1 1+ 1 173 99 = % Candidates should answer

Lecture 6 Capital Budgeting Decision

Lecture 6 Capital Budgeting Decision The term capital refers to long-term assets used in production, while a budget is a plan that details projected inflows and outflows during some future period. Thus,

Lecture 6 Capital Budgeting Decision The term capital refers to long-term assets used in production, while a budget is a plan that details projected inflows and outflows during some future period. Thus,

2/9/2010. Investment Appraisal. Investment Appraisal. Investment Appraisal. Investment Appraisal. Investment Appraisal. Investment Appraisal

A means of assessing whether an investment project is worthwhile or not Investment project could be the purchase of a new PC for a small firm, a new piece of equipment in a manufacturing plant, a whole

A means of assessing whether an investment project is worthwhile or not Investment project could be the purchase of a new PC for a small firm, a new piece of equipment in a manufacturing plant, a whole

WEEK 7 Investment Appraisal -1

WEEK 7 Investment Appraisal -1 Learning Objectives Understand the nature and importance of investment decisions. Distinguish between discounted cash flow (DCF) and nondiscounted cash flow (non-dcf) techniques

WEEK 7 Investment Appraisal -1 Learning Objectives Understand the nature and importance of investment decisions. Distinguish between discounted cash flow (DCF) and nondiscounted cash flow (non-dcf) techniques

Project Integration Management

Project Integration Management The Key to Overall Project Success: Good Project Integration Management Project managers must coordinate all of the other knowledge areas throughout a project s life cycle.

Project Integration Management The Key to Overall Project Success: Good Project Integration Management Project managers must coordinate all of the other knowledge areas throughout a project s life cycle.

Mini MBA: Accounting & Finance

Introduction Mini MBA: Accounting & Finance This course is designed to cover and includes a comprehensive illustration of how accounting information is collected, recorded, analyzed and presented both

Introduction Mini MBA: Accounting & Finance This course is designed to cover and includes a comprehensive illustration of how accounting information is collected, recorded, analyzed and presented both

WHAT IS CAPITAL BUDGETING?

WHAT IS CAPITAL BUDGETING? Capital budgeting is a required managerial tool. One duty of a financial manager is to choose investments with satisfactory cash flows and rates of return. Therefore, a financial

WHAT IS CAPITAL BUDGETING? Capital budgeting is a required managerial tool. One duty of a financial manager is to choose investments with satisfactory cash flows and rates of return. Therefore, a financial

Chapter 7: Investment Decision Rules

Chapter 7: Investment Decision Rules-1 Chapter 7: Investment Decision Rules I. Introduction and Review of NPV A. Introduction Q: How decide which long-term investment opportunities to undertake? Key =>

Chapter 7: Investment Decision Rules-1 Chapter 7: Investment Decision Rules I. Introduction and Review of NPV A. Introduction Q: How decide which long-term investment opportunities to undertake? Key =>

Review of Financial Analysis Terms

Review of Financial Analysis Terms Financial Analysis Requirements Economic Evaluation of Potential TUR Techniques (310 CMR 50.46A) The TUR plan must include the discount rate, cost of capital, depreciation

Review of Financial Analysis Terms Financial Analysis Requirements Economic Evaluation of Potential TUR Techniques (310 CMR 50.46A) The TUR plan must include the discount rate, cost of capital, depreciation

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Introduction A long term view of benefits and costs must be taken when reviewing a capital expenditure project.

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Introduction A long term view of benefits and costs must be taken when reviewing a capital expenditure project.

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether

Chapter 10 The Basics of Capital Budgeting: Evaluating Cash Flows ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether

Describe the importance of capital investments and the capital budgeting process

Chapter 20 Making capital investment decisions Affects operations for many years Requires large sums of money Describe the importance of capital investments and the capital budgeting process 3 4 5 6 Operating

Chapter 20 Making capital investment decisions Affects operations for many years Requires large sums of money Describe the importance of capital investments and the capital budgeting process 3 4 5 6 Operating

MULTIPLE-CHOICE QUESTIONS Circle the correct answer on this test paper and record it on the computer answer sheet.

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 23 March, 2006 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 23 March, 2006 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

PAPER No. 4: Accounting Theory and Practice. 34: Shareholder Value Added and Market Value Added

Subject Paper No and Title Module No and Title Module Tag 4: Accounting Theory and Practice 34: Shareholder and Market COM_P4_M34 MODULE No. 34: Shareholder and Market TABLE OF CONTENTS 1. Learning Outcomes

Subject Paper No and Title Module No and Title Module Tag 4: Accounting Theory and Practice 34: Shareholder and Market COM_P4_M34 MODULE No. 34: Shareholder and Market TABLE OF CONTENTS 1. Learning Outcomes

Web Extension: The ARR Method, the EAA Approach, and the Marginal WACC

19878_12W_p001-010.qxd 3/13/06 3:03 PM Page 1 C H A P T E R 12 Web Extension: The ARR Method, the EAA Approach, and the Marginal WACC This extension describes the accounting rate of return as a method

19878_12W_p001-010.qxd 3/13/06 3:03 PM Page 1 C H A P T E R 12 Web Extension: The ARR Method, the EAA Approach, and the Marginal WACC This extension describes the accounting rate of return as a method

Chapter 6 Making Capital Investment Decisions

Making Capital Investment Decisions Solutions to Even-Numbered Problems and Cases 6.2 Manitoba Railroad Limited (MRL) (a) Discount Rate 7% Cash Cash Net Cash Cumulative Year Outflows Inflows Flows Cash

Making Capital Investment Decisions Solutions to Even-Numbered Problems and Cases 6.2 Manitoba Railroad Limited (MRL) (a) Discount Rate 7% Cash Cash Net Cash Cumulative Year Outflows Inflows Flows Cash

Topic 12 capital investment

Topic 12 capital investment Aldi press- release - There is a strong appetite among South Australians for an alternative place to shop and we are eager to show them the significant benefits that can come

Topic 12 capital investment Aldi press- release - There is a strong appetite among South Australians for an alternative place to shop and we are eager to show them the significant benefits that can come

FINANCE FOR STRATEGIC MANAGERS

FINANCE FOR STRATEGIC MANAGERS 1 P age FINANCE FOR STRATEGIC MANAGERS S. No Description Page No I UNDERSTAND THE ROLE OF FINANCIAL INFORMATION IN BUSINESS STRATEGY 1. Need for Financial Information 1.1

FINANCE FOR STRATEGIC MANAGERS 1 P age FINANCE FOR STRATEGIC MANAGERS S. No Description Page No I UNDERSTAND THE ROLE OF FINANCIAL INFORMATION IN BUSINESS STRATEGY 1. Need for Financial Information 1.1

Capital Budgeting CFA Exam Level-I Corporate Finance Module Dr. Bulent Aybar

Capital Budgeting CFA Exam Level-I Corporate Finance Module Dr. Bulent Aybar Professor of International Finance Capital Budgeting Agenda Define the capital budgeting process, explain the administrative

Capital Budgeting CFA Exam Level-I Corporate Finance Module Dr. Bulent Aybar Professor of International Finance Capital Budgeting Agenda Define the capital budgeting process, explain the administrative

Chapter 14 Solutions Solution 14.1

Chapter 14 Solutions Solution 14.1 a) Compare and contrast the various methods of investment appraisal. To what extent would it be true to say there is a place for each of them As capital investment decisions

Chapter 14 Solutions Solution 14.1 a) Compare and contrast the various methods of investment appraisal. To what extent would it be true to say there is a place for each of them As capital investment decisions

Introduction. The Assessment consists of: Evaluation questions that assess best practices. A rating system to rank your board s current practices.

ESG / Sustainability Governance Assessment: A Roadmap to Build a Sustainable Board By Coro Strandberg President, Strandberg Consulting www.corostrandberg.com November 2017 Introduction This is a tool for

ESG / Sustainability Governance Assessment: A Roadmap to Build a Sustainable Board By Coro Strandberg President, Strandberg Consulting www.corostrandberg.com November 2017 Introduction This is a tool for

The formula for the net present value is: 1. NPV. 2. NPV = CF 0 + CF 1 (1+ r) n + CF 2 (1+ r) n

n + CF 2 (1+ r) n") Lecture 6: Capital Budgeting 1 Capital budgeting refers to an investment into a long term asset. It must be noted that all investments have a cost and that investments should always have benefits such

Lecture 6: Capital Budgeting 1 Capital budgeting refers to an investment into a long term asset. It must be noted that all investments have a cost and that investments should always have benefits such

FINANCE REVIEW. Page 1 of 5

Correlation: A perfect positive correlation means as X increases, Y increases at the same rate Y Corr =.0 X A perfect negative correlation means as X increases, Y decreases at the same rate Y Corr = -.0

Correlation: A perfect positive correlation means as X increases, Y increases at the same rate Y Corr =.0 X A perfect negative correlation means as X increases, Y decreases at the same rate Y Corr = -.0

Essential Learning for CTP Candidates TEXPO Conference 2017 Session #03

TEXPO Conference 2017: Essential Learning for CTP Candidates Session #3 (Mon.1:45 3:00 pm) Overview of Basic CTP Math from ETM5 Chap 07: Earnings Credits Chap 11: Working Capital Chap 08: Fin. Statements

TEXPO Conference 2017: Essential Learning for CTP Candidates Session #3 (Mon.1:45 3:00 pm) Overview of Basic CTP Math from ETM5 Chap 07: Earnings Credits Chap 11: Working Capital Chap 08: Fin. Statements

Index. Business unit, 311, 350 Business-unit level strategies, 309, 311 Business-unit strategies, 311, 350

387 Index A Absenteeism rate, 239 Accounting, 26, 93 Definition, 3 Accounting system, 14 Accrual accounting, 176, 182, 194 Activity-based budgeting, 141 142, 150 Activity-based costing, 67 69, 71, 93,

387 Index A Absenteeism rate, 239 Accounting, 26, 93 Definition, 3 Accounting system, 14 Accrual accounting, 176, 182, 194 Activity-based budgeting, 141 142, 150 Activity-based costing, 67 69, 71, 93,

Mathematics of Finance

CHAPTER 55 Mathematics of Finance PAMELA P. DRAKE, PhD, CFA J. Gray Ferguson Professor of Finance and Department Head of Finance and Business Law, James Madison University FRANK J. FABOZZI, PhD, CFA, CPA

CHAPTER 55 Mathematics of Finance PAMELA P. DRAKE, PhD, CFA J. Gray Ferguson Professor of Finance and Department Head of Finance and Business Law, James Madison University FRANK J. FABOZZI, PhD, CFA, CPA

Organization Strategy and Project Selection The McGraw-Hill Companies, All Rights Reserved

Chapter 2 Organization Strategy and Project Selection McGraw-Hill/Irwin 2008 The McGraw-Hill Companies, All Rights Reserved 2-2 Why Project Managers Need to Understand the Strategic Management Process

Chapter 2 Organization Strategy and Project Selection McGraw-Hill/Irwin 2008 The McGraw-Hill Companies, All Rights Reserved 2-2 Why Project Managers Need to Understand the Strategic Management Process

Investment Education Series

Investment Education Series The Art of Investing Introduction Investing is an art and science that requires creativity, experience and good judgement on the art side and quantitative skills, precision

Investment Education Series The Art of Investing Introduction Investing is an art and science that requires creativity, experience and good judgement on the art side and quantitative skills, precision

2, , , , ,220.21

11-7 a. Project A: CF 0-6000; CF 1-5 2000; I/YR 14. Solve for NPV A $866.16. IRR A 19.86%. MIRR calculation: 0 14% 1 2 3 4 5-6,000 2,000 (1.14) 4 2,000 (1.14) 3 2,000 (1.14) 2 2,000 1.14 2,000 2,280.00

11-7 a. Project A: CF 0-6000; CF 1-5 2000; I/YR 14. Solve for NPV A $866.16. IRR A 19.86%. MIRR calculation: 0 14% 1 2 3 4 5-6,000 2,000 (1.14) 4 2,000 (1.14) 3 2,000 (1.14) 2 2,000 1.14 2,000 2,280.00

Software Economics. Introduction to Business Case Analysis. Session 2

Software Economics Introduction to Business Case Analysis Session 2 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements

Software Economics Introduction to Business Case Analysis Session 2 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements

Today I am. A. Ready for some serious learning. B. Enjoying being away from work. C. Hungry, skipped breakfast. D. Loving Tartu

Welcome Today I am A. Ready for some serious learning B. Enjoying being away from work C. Hungry, skipped breakfast D. Loving Tartu E. Tired, I just want to go home How many hours did you spend on this

Welcome Today I am A. Ready for some serious learning B. Enjoying being away from work C. Hungry, skipped breakfast D. Loving Tartu E. Tired, I just want to go home How many hours did you spend on this

MULTIPLE-CHOICE QUESTIONS Circle the correct answer on this test paper and record it on the computer answer sheet.

M I M E 310 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 15 November, 2007 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

M I M E 310 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 15 November, 2007 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

Introduction to Capital

Introduction to Capital What is Capital? Money invested in business to generate income The money, property, and other valuables which collectively represent the wealth of an individual or business The

Introduction to Capital What is Capital? Money invested in business to generate income The money, property, and other valuables which collectively represent the wealth of an individual or business The

Project Management CTC-ITC 310 Spring 2018 Howard Rosenthal

Project Management CTC-ITC 310 Spring 2018 Howard Rosenthal 1 Notice This course is based on and includes material from the text: A User s Manual To the PMBOK Guide Authors: Cynthia Stackpole Snyder Publisher:

Project Management CTC-ITC 310 Spring 2018 Howard Rosenthal 1 Notice This course is based on and includes material from the text: A User s Manual To the PMBOK Guide Authors: Cynthia Stackpole Snyder Publisher:

CPET 581 Smart Grid and Energy Management Nov. 20, 2013 Lecture

CPET 581 Smart Grid and Energy Management Nov. 20, 2013 Lecture References [ 1] Mechanical and Electrical Systems in Building, 5 th Edition, by Richard R. Janis and William K.Y. Tao, Publisher Pearson

CPET 581 Smart Grid and Energy Management Nov. 20, 2013 Lecture References [ 1] Mechanical and Electrical Systems in Building, 5 th Edition, by Richard R. Janis and William K.Y. Tao, Publisher Pearson

Introduction. The Assessment consists of: A checklist of best, good and leading practices A rating system to rank your company s current practices.

ESG / CSR / Sustainability Governance and Management Assessment By Coro Strandberg President, Strandberg Consulting www.corostrandberg.com September 2017 Introduction This ESG / CSR / Sustainability Governance

ESG / CSR / Sustainability Governance and Management Assessment By Coro Strandberg President, Strandberg Consulting www.corostrandberg.com September 2017 Introduction This ESG / CSR / Sustainability Governance

Investment decisions. Guidance and teaching advice. Basic principles

88 Investment decisions 09 Guidance and teaching advice We wrote this chapter with the premise that non-accounting students need to develop skills in using investment appraisal information to support good

88 Investment decisions 09 Guidance and teaching advice We wrote this chapter with the premise that non-accounting students need to develop skills in using investment appraisal information to support good

MGT201 Financial Management All Subjective and Objective Solved Midterm Papers for preparation of Midterm Exam2012 Question No: 1 ( Marks: 1 ) - Please choose one companies invest in projects with negative

MGT201 Financial Management All Subjective and Objective Solved Midterm Papers for preparation of Midterm Exam2012 Question No: 1 ( Marks: 1 ) - Please choose one companies invest in projects with negative

F3 Financial Strategy

Strategic Level Paper F3 Financial Strategy Senior Examiner s Answers SECTION A Answer to Question One (a)(i) Valuation of Company NN (excluding potential synergistic benefits and integration costs) NN:

Strategic Level Paper F3 Financial Strategy Senior Examiner s Answers SECTION A Answer to Question One (a)(i) Valuation of Company NN (excluding potential synergistic benefits and integration costs) NN:

MAXIMISE SHAREHOLDERS WEALTH.

TOPIC 4: Project Evaluation 4.1 Capital Budgeting Theory: Another term for investing, capital budgeting involves weighing up which assets to purchase with the funds that a company raises from its debt

TOPIC 4: Project Evaluation 4.1 Capital Budgeting Theory: Another term for investing, capital budgeting involves weighing up which assets to purchase with the funds that a company raises from its debt

Capital Budgeting Decisions

May 1-4, 2014 Capital Budgeting Decisions Today s Agenda n Capital Budgeting n Time Value of Money n Decision Making Example n Simple Return and Payback Methods Typical Capital Budgeting Decisions n Capital

May 1-4, 2014 Capital Budgeting Decisions Today s Agenda n Capital Budgeting n Time Value of Money n Decision Making Example n Simple Return and Payback Methods Typical Capital Budgeting Decisions n Capital

Software Economics. Introduction to Business Case Analysis. Session 2

Software Economics Introduction to Business Case Analysis Session 2 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements

Software Economics Introduction to Business Case Analysis Session 2 Today Last Session we covered FV, PV and NPV We started with setting up the financials of a Business Case We talked about measurements

Understanding Financial Management: A Practical Guide Problems and Answers

Understanding Financial Management: A Practical Guide Problems and Answers Chapter 1 Raising Funds and Cost of Capital 1.1 Financial Markets 1. What is the difference between a financial market and a financial

Understanding Financial Management: A Practical Guide Problems and Answers Chapter 1 Raising Funds and Cost of Capital 1.1 Financial Markets 1. What is the difference between a financial market and a financial

MGT201 Current Online Solved 100 Quizzes By

MGT201 Current Online Solved 100 Quizzes By http://vustudents.ning.com Question # 1 Which if the following refers to capital budgeting? Investment in long-term liabilities Investment in fixed assets Investment

MGT201 Current Online Solved 100 Quizzes By http://vustudents.ning.com Question # 1 Which if the following refers to capital budgeting? Investment in long-term liabilities Investment in fixed assets Investment

Lecture 3. Chapter 4: Allocating Resources Over Time

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Capital Budgeting Theory and Capital Budgeting Practice. University of Texas at El Paso. Pierre C. Ehe MBA

Capital Budgeting Theory and Capital Budgeting Practice University of Texas at El Paso Pierre C. Ehe MBA The three articles by Mukherjee posit the idea that inconsistencies exist between capital budgeting

Capital Budgeting Theory and Capital Budgeting Practice University of Texas at El Paso Pierre C. Ehe MBA The three articles by Mukherjee posit the idea that inconsistencies exist between capital budgeting

HKICPA Qualification Programme

HKICPA Qualification Programme Module B Corporate Financing KPMG Mock Exam Answers http://www.kaplanfinancial.com.hk Copyright Kaplan Financial (HK) Limited All rights reserved. No part of this examination

HKICPA Qualification Programme Module B Corporate Financing KPMG Mock Exam Answers http://www.kaplanfinancial.com.hk Copyright Kaplan Financial (HK) Limited All rights reserved. No part of this examination

Merger GuidelinesMerger Guidelines

Merger Guidelines Merger GuidelinesMerger Guidelines Danish Competition and Consumer Authority Carl Jacobsens Vej 35 2500 Valby Tlf. +45 41 71 50 00 E-mail: kfst@kfst.dk Online ISBN: 978-87-7029-542-0

Merger Guidelines Merger GuidelinesMerger Guidelines Danish Competition and Consumer Authority Carl Jacobsens Vej 35 2500 Valby Tlf. +45 41 71 50 00 E-mail: kfst@kfst.dk Online ISBN: 978-87-7029-542-0

Investment Appraisal. Chapter 3 Investments: Spot and Derivative Markets

Investment Appraisal Chapter 3 Investments: Spot and Derivative Markets Compounding vs. Discounting Invest sum over years, how much will it be worth? Terminal Value after n years @ r : if r 1 = r 2 = =

Investment Appraisal Chapter 3 Investments: Spot and Derivative Markets Compounding vs. Discounting Invest sum over years, how much will it be worth? Terminal Value after n years @ r : if r 1 = r 2 = =

Net Present Value Q: Suppose we can invest $50 today & receive $60 later today. What is our increase in value? Net Present Value Suppose we can invest

Ch. 11 The Basics of Capital Budgeting Topics Net Present Value Other Investment Criteria IRR Payback What is capital budgeting? Analysis of potential additions to fixed assets. Long-term decisions; involve

Ch. 11 The Basics of Capital Budgeting Topics Net Present Value Other Investment Criteria IRR Payback What is capital budgeting? Analysis of potential additions to fixed assets. Long-term decisions; involve

(2) shareholders incur costs to monitor the managers and constrain their actions.

shareholders incur costs to monitor the managers and constrain their actions.") (2) shareholders incur costs to monitor the managers and constrain their actions. Agency problems are mitigated by good systems of corporate governance. Legal and Regulatory Requirements: Australian Securities

(2) shareholders incur costs to monitor the managers and constrain their actions. Agency problems are mitigated by good systems of corporate governance. Legal and Regulatory Requirements: Australian Securities

All In One MGT201 Mid Term Papers More Than (10) BY

BY") All In One MGT201 Mid Term Papers More Than (10) BY http://www.vustudents.net MIDTERM EXAMINATION MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Why companies

All In One MGT201 Mid Term Papers More Than (10) BY http://www.vustudents.net MIDTERM EXAMINATION MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Why companies

1. give a picture of a company's ability to generate cash flow and pay it financial obligations: 2. Balance sheet items expressed as percentage of:

1. give a picture of a company's ability to generate cash flow and pay it financial obligations: a. Management ratios b. Working capital ratios c. Net profit margin ratios d. Solvency Ratios 2. Balance

1. give a picture of a company's ability to generate cash flow and pay it financial obligations: a. Management ratios b. Working capital ratios c. Net profit margin ratios d. Solvency Ratios 2. Balance

Study Session 11 Corporate Finance

Study Session 11 Corporate Finance ANALYSTNOTES.COM 1 A. An Overview of Financial Management a. Agency problem. An agency relationship arises when: The principal hires an agent to perform some services.

Study Session 11 Corporate Finance ANALYSTNOTES.COM 1 A. An Overview of Financial Management a. Agency problem. An agency relationship arises when: The principal hires an agent to perform some services.

CAPITAL BUDGETING AND THE INVESTMENT DECISION

C H A P T E R 1 2 CAPITAL BUDGETING AND THE INVESTMENT DECISION I N T R O D U C T I O N This chapter begins by discussing some of the problems associated with capital asset decisions, such as the long

C H A P T E R 1 2 CAPITAL BUDGETING AND THE INVESTMENT DECISION I N T R O D U C T I O N This chapter begins by discussing some of the problems associated with capital asset decisions, such as the long

Capital Budgeting: Decision Criteria

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

Consider a firm with two projects, A and B, each with the following cash flows and a 10 percent cost of capital: Project A Project B Year Cash Flows Cash Flows 0 -$100 -$150 1 $70 $100 2 $70 $100 What

ACC 501 Solved MCQ'S For MID & Final Exam 1. Which of the following is an example of positive covenant? Maintaining firm s working capital at or above some specified minimum level Furnishing audited financial

ACC 501 Solved MCQ'S For MID & Final Exam 1. Which of the following is an example of positive covenant? Maintaining firm s working capital at or above some specified minimum level Furnishing audited financial

Created by Stefan Momic for UTEFA. UTEFA Learning Session #2 Valuation September 27, 2018

UTEFA Learning Session #2 Valuation September 27, 2018 Agenda Introduction to Valuation Relative Valuation Intrinsic Valuation Discounted Cash Flow Analysis Valuation Trade-Offs Introduction to Valuation

UTEFA Learning Session #2 Valuation September 27, 2018 Agenda Introduction to Valuation Relative Valuation Intrinsic Valuation Discounted Cash Flow Analysis Valuation Trade-Offs Introduction to Valuation

Valuation of Businesses

Convenience translation from German into English Professional Guidelines of the Expert Committee on Business Administration of the Institute for Business Economics, Tax Law and Organization of the Austrian

Convenience translation from German into English Professional Guidelines of the Expert Committee on Business Administration of the Institute for Business Economics, Tax Law and Organization of the Austrian

Mid Term Papers. Spring 2009 (Session 02) MGT201. (Group is not responsible for any solved content)

MGT201. (Group is not responsible for any solved content)") Spring 2009 (Session 02) MGT201 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program

Spring 2009 (Session 02) MGT201 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program

Mergers and Acquisitions

Mergers and Acquisitions 1 Classifying M&A Merger: the boards of directors of two firms agree to combine and seek shareholder approval for combination. The target ceases to exist. Consolidation: a new

Mergers and Acquisitions 1 Classifying M&A Merger: the boards of directors of two firms agree to combine and seek shareholder approval for combination. The target ceases to exist. Consolidation: a new

Running head: THE TIME VALUE OF MONEY 1. The Time Value of Money. Ma. Cesarlita G. Josol. MBA - Acquisition. Strayer University

Running head: THE TIME VALUE OF MONEY 1 The Time Value of Money Ma. Cesarlita G. Josol MBA - Acquisition Strayer University FIN 534 THE TIME VALUE OF MONEY 2 Abstract The paper presents computations about

Running head: THE TIME VALUE OF MONEY 1 The Time Value of Money Ma. Cesarlita G. Josol MBA - Acquisition Strayer University FIN 534 THE TIME VALUE OF MONEY 2 Abstract The paper presents computations about

Project Management CSC 310 Spring 2017 Howard Rosenthal

Project CSC 310 Spring 2017 Howard Rosenthal 1 No?ce This course is based on and includes material from the text: Effective Project - Traditional, Agile, Extreme 7TH Edition Authors: Robert K. Wysocki

Project CSC 310 Spring 2017 Howard Rosenthal 1 No?ce This course is based on and includes material from the text: Effective Project - Traditional, Agile, Extreme 7TH Edition Authors: Robert K. Wysocki

Many decisions in operations management involve large

SUPPLEMENT Financial Analysis J LEARNING GOALS After reading this supplement, you should be able to: 1. Explain the time value of money concept. 2. Demonstrate the use of the net present value, internal

SUPPLEMENT Financial Analysis J LEARNING GOALS After reading this supplement, you should be able to: 1. Explain the time value of money concept. 2. Demonstrate the use of the net present value, internal

A Financial Perspective on Commercial Litigation Finance. Lee Drucker 2015

A Financial Perspective on Commercial Litigation Finance Lee Drucker 2015 Introduction: In general terms, litigation finance describes the provision of capital to a claimholder in exchange for a portion

A Financial Perspective on Commercial Litigation Finance Lee Drucker 2015 Introduction: In general terms, litigation finance describes the provision of capital to a claimholder in exchange for a portion

ACC 501 Quizzes Lecture 1 to 22

ACC501 Business Finance Composed By Faheem Saqib A mega File of MiD Term Solved MCQ For more Help Rep At Faheem_saqib2003@yahoocom Faheemsaqib2003@gmailcom 0334-6034849 ACC 501 Quizzes Lecture 1 to 22

ACC501 Business Finance Composed By Faheem Saqib A mega File of MiD Term Solved MCQ For more Help Rep At Faheem_saqib2003@yahoocom Faheemsaqib2003@gmailcom 0334-6034849 ACC 501 Quizzes Lecture 1 to 22

Lecture 15. Thursday Mar 25 th. Advanced Topics in Capital Budgeting

Lecture 15. Thursday Mar 25 th Equal Length Projects If 2 Projects are of equal length, but unequal scale then: Positive NPV says do projects Profitability Index allows comparison ignoring scale If cashflows

Lecture 15. Thursday Mar 25 th Equal Length Projects If 2 Projects are of equal length, but unequal scale then: Positive NPV says do projects Profitability Index allows comparison ignoring scale If cashflows