Module 5: Special Financing and Investment Decisions

|

|

|

- Lionel Craig

- 6 years ago

- Views:

Transcription

1 Module 5: Special Financing and Investment Decisions

2 Reading 5.1: Introduction to Project Financing

3 Some projects are so large that it may be best to finance them as they are standalone operations. Projects are typically large, complex, and capital intensive; but generate steady cash flows. Contractual arrangements: Completion & quality assurance Raw material supply Output/service purchase Completion, quality assurance, & purchase Cash flow guarantee One or more sponsoring companies will provide the equity investment, with the rest coming from outside debt financing.

4

5 Advantages of project financing Can share the benefits of the project while being able to spread the risk around (sponsors, suppliers, customers, & creditors). Expand debt capacity (special purpose vehicles, off balance sheet) Disadvantages of project financing Significant legal and advisory fees. If financial institution requires guarantees another fee. Can t always pass on the risk lenders may demand premium.

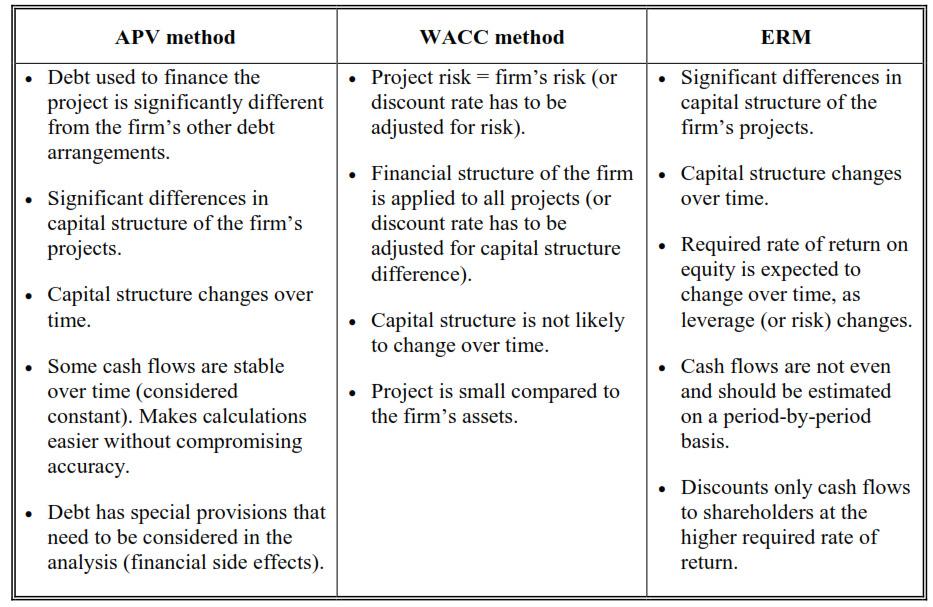

6 Reading : Investment Analysis Using Adjusted Present Value

7 Adjusted present value Separate a project s cash flows into two groups: 1. NPV of unlevered project (assume 100% equity financed) 2. NPV of cash flows associated with financing

8 Base-case NPV Calculated the same way as in Module 2 (equations 2-16 &2-16a) Discount rate is unlevered cost of equity (CAPM). Typically, a company s cost of equity will incorporate the company s leverage. To adjust for leverage: Use equation 2-22 to calculate the unlevered beta:

9 Base-case NPV Use equation 2-20 using unlevered beta to determine the unlevered firm s cost of equity. Unlevered Beta

10 Discount rates used in financing related cash flows: Interest tax shield after-tax interest payment discounted using after-tax cost of debt After-tax PV of Flotation costs - Total flotation costs PV of tax shield (discounted using after-tax cost of debt) similar to Bond/Pfd share refi in Module 3 Financing-related investment credits and subsidies If firm receives credits/subsidies due to using debt pv of credits/subsidies treated as financing related item and added to base case NPV. If firm receives credits/subsidies regardless of financing amounts included in base case NPV reduction of initial investment outlay. If a company receives investment tax credit related to purchase of specific asset reduces net investment outlay Operating subsidy is after tax benefit discounted by after tax cost of debt

11 **Both the value of low interest loan & value of subsidies are added to NPV**

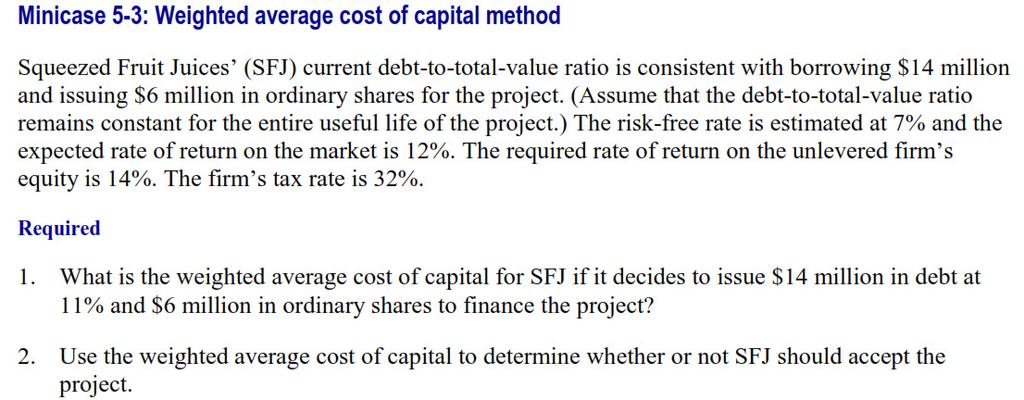

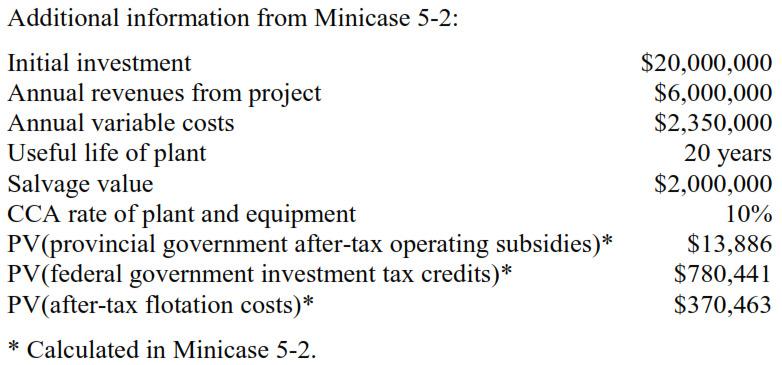

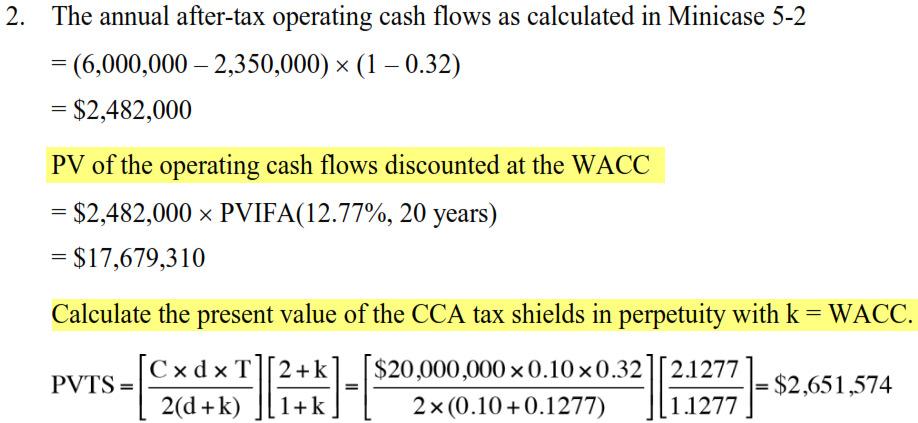

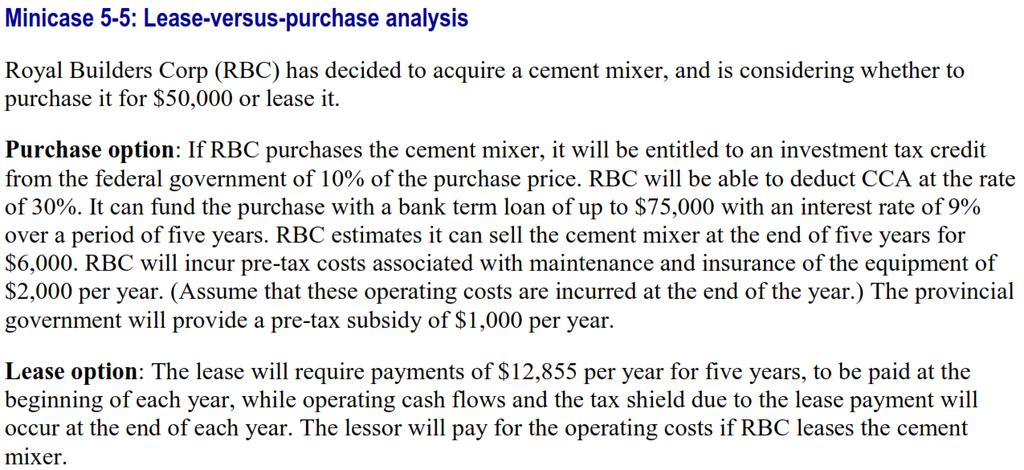

12 Minicase 5-2

13 Questions 1-6 deal with calculating base case NPV, questions 7-9 deal with the financing related benefits.

14

15

16

17

18

19

20

21

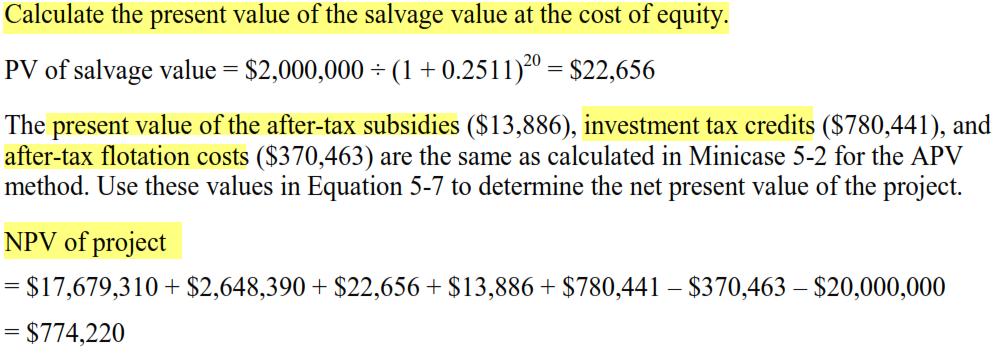

22 Reading 5.2: Investment Analysis Using Weighted Average Cost of Capital (WACC) Applying firm s WACC to a project assumes project s risks & characteristics are the same as the company s.

23 Adjusting discount rate for project s financial leverage Or, when beta is not given:

24 WACC WACC is used to discount cash flows to determine NPV: 1. Estimate after-tax cash flows assuming all equity financing (same as APV) 2. Calculate WACC 3. Discount cash flows at WACC 4. For calculating tax shields lost to salvage, discount salvage value at cost of equity. 5. Estimate cash flows that are low risk side effects/related to financing and discount at after tax cost of debt. 6. NPV = PV a/tax cash flows from operations + PV salvage price WACC + PV investment tax credits/subsidies - PV a/tax flotation costs initial outlays Equation 5-7

25 Other cash flows All cash flows are discounted at WACC except: Salvage price & salvage value term in calculating tax shields lost to salvage discounted at levered cost of equity Tax shield on flotation costs discounted at a/tax cost of debt A/tax tax credits/subsidies discounted at a/tax cost of debt

26 Differences between APV & WACC APV discounts operating cash flows for base case NPV at unlevered cost of equity. APV adjusts for debt by adding present value of interest tax shield to base case NPV; WACC method adjusts discount rate (lower) which leads to higher present value of operating cash flows

27

28

29

30

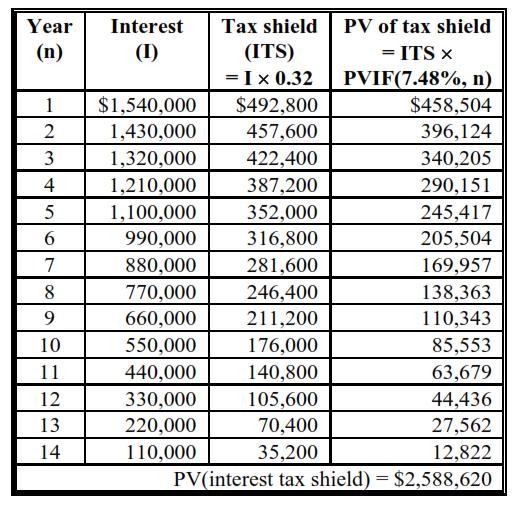

31 NPV using APV method = $ 2,080,138 NPV using WACC = $744,220 WACC method assumes constant capital structure, while APV can allow for the capital structure to change. Using the APV method, the bulk of the value came from discounting the interest tax shield by a a/tax cost of debt (7.48%). Remember, when computing a present value calculation the lower the discount rate (all other things being equal), the higher the present value number.

32 Reading 5.3: Investment Analysis Using Equity Residual (Flow to Equity)

33 Equity residual method (ERM) Determine cash flows that accrue to shareholders (i.e after paying operating & financing costs and debt repayments.

34 Cash flows get discounted at levered cost of equity. Do you use company s cost of equity or projects? Use company s if: 1. Project has same risk as firm s assets 2. Firm is expected to use debt level for project that is similar to firm s capital structure. 3. Capital structure is expected to stay stable during project s life span. If you need to adjust for financial leverage use same procedure as in APV.

35 If project s capital structure is going to change over time

36 If project s capital structure is going to change over time

37

38

39 Reading 5.5: Leases

40 Reading 5.6: Analysis of the Lease/Purchase Financing Decision

41 Equivalent loan Lease financing is a substitute for debt financing. To compare leasing with borrowing to purchase, we need to determine the equivalent loan that would commit the firm to exactly the same cash outflows under the lease. Discount cash flows by a/tax cost of debt (except salvage value and tax shield related to salvage WACC)

42 PV CCA tax shields 5-14 C = initial undepreciated capital cost of the asset d = CCA rate of the class to which the asset belongs T = corporate tax rate S = salvage value of the asset at the end of year n r = after-tax interest rate on debt WACCn = weighted average cost of capital

43 PV operating cost savings 5-15 Operating costs under a lease can be cheaper than from ownership.

44 Net present value to leasing (NVL) NVL = initial investment outlay equivalent loan Equation 5-16 NVL measures net cost savings realized by firm if it leases rather than borrows to purchase. Same decision rules apply.

45

46 Solution Step 1: Calculate the initial investment outlay. = purchase price federal government investment tax credit = $50,000 (0.10 $50,000) = $45,000 Step 2: Calculate the leasing costs. Present value of lease payments: If RBC purchases the cement mixer through a bank loan, the interest rate will be 9%. The after-tax cost of debt = 9% (1 0.40) = 5.40% The lease payment per year is $12,855, to be paid at the beginning of each year. PV of the annuity due = $12,855 PVIFA(5.4%, 5) ( ) = $58,018

47 Solution The lease payments are deductible for tax purposes, and the tax shield due to the lease payment is received at the end of each year. PV of the tax shield due to lease payments = $12, PVIFA(5.4%, 5) = $22,018 PV of the lease payments on an after-tax basis = $58,018 $22,018 = $36,000

48 Present value of operating costs RBC will incur no operating costs if it leases the cement mixer. Under the borrowing alternative, it would incur these costs. PV of the after-tax operating costs = $2,000 (1 0.40) PVIFA(5.4%, 5) = $5,138 Present value of tax shields lost by leasing over buying (Equation 5-14): The initial capital cost of the asset is $45,000 CCA rate is 30% after-tax interest rate is 5.40% WACC is 15% tax rate is 40%, salvage value of the cement mixer at the end of five years is $6,000.

49 CCA tax shield available on purchase of the asset, if the asset is held indefinitely. CCA tax shield lost to the purchaser of the asset due to sale of the asset for its salvage value. PV of CCA lost tax shields if RBC leases = 14,863 1,011 = 13,852 PV of the salvage value lost by leasing (discounted at the WACC) = $6,000 (1.15) 5 = 2,983 PV of the provincial government subsidies lost under the lease option = $1,000 (1 0.40) PVIFA(5.4%, 5) = 2,569

50 Step 3: Calculate the equivalent loan. Equation 5-13 Borrowing to purchase is preferable the amount that RBC could borrow under the equivalent loan is more than initial investment outlay.

51 Step 4: Calculate the net value to leasing. Equation 5-16 The net value to leasing (NVL) = initial investment outlay equivalent loan = $45,000 $50,266 = $5,266 RBC should not lease the asset.

Ron Muller MODULE 6: SPECIAL FINANCING AND INVESTMENT DECISIONS QUESTION 1

MODULE 6: SPECIAL FINANCING AND INVESTMENT DECISIONS QUESTION 1 Barney s Ltd. is trying to decide whether or not to lease or borrow to buy a new computer facility from the manufacturer. Annual maintenance

MODULE 6: SPECIAL FINANCING AND INVESTMENT DECISIONS QUESTION 1 Barney s Ltd. is trying to decide whether or not to lease or borrow to buy a new computer facility from the manufacturer. Annual maintenance

Chapter 15. Required Returns and the Cost of Capital. Required Returns and the Cost of Capital. Key Sources of Value Creation

15-1 Chapter 15 Required Returns and the Cost of Capital Fundamentals of Financial Management, 12/e Created by: Gregory A. Kuhlemeyer, Ph.D. 15-2 After studying Chapter 15, you should be able to: Explain

15-1 Chapter 15 Required Returns and the Cost of Capital Fundamentals of Financial Management, 12/e Created by: Gregory A. Kuhlemeyer, Ph.D. 15-2 After studying Chapter 15, you should be able to: Explain

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

Chapter 18 Valuation and Capital Budgeting for the Levered Firm Dec. 2012

University of Science and Technology Beijing Dongling School of Economics and management Chapter 18 Valuation and Capital Budgeting for the Levered Firm Dec. 2012 Dr. Xiao Ming USTB 1 Key Concepts and

University of Science and Technology Beijing Dongling School of Economics and management Chapter 18 Valuation and Capital Budgeting for the Levered Firm Dec. 2012 Dr. Xiao Ming USTB 1 Key Concepts and

CA - FINAL INTERNATIONAL FINANCIAL MANAGEMENT. FCA, CFA L3 Candidate

CA - FINAL INTERNATIONAL FINANCIAL MANAGEMENT FCA, CFA L3 Candidate 12.1 International Financial Management Study Session 12 LOS 1 : International Capital Budgeting Capital Budgeting is the process

CA - FINAL INTERNATIONAL FINANCIAL MANAGEMENT FCA, CFA L3 Candidate 12.1 International Financial Management Study Session 12 LOS 1 : International Capital Budgeting Capital Budgeting is the process

Debt. Firm s assets. Common Equity

Debt/Equity Definition The mix of securities that a firm uses to finance its investments is called its capital structure. The two most important such securities are debt and equity Debt Firm s assets Common

Debt/Equity Definition The mix of securities that a firm uses to finance its investments is called its capital structure. The two most important such securities are debt and equity Debt Firm s assets Common

Given the following information, what is the WACC for the following firm?

Chapter 1 Cost of Capital The required return for an asset is a function of the risk of the asset and the return to the investor is the same as the cost to the company. The firms cost of capital provides

Chapter 1 Cost of Capital The required return for an asset is a function of the risk of the asset and the return to the investor is the same as the cost to the company. The firms cost of capital provides

2013, Study Session #11, Reading # 37 COST OF CAPITAL 1. INTRODUCTION

COST OF CAPITAL 1 WACC = Weighted Avg. Cost of Capital MCC = Marginal Cost of Capital TCS = Target Capital Structure IOS = Investment Opportunity Schedule YTM = Yield-to-Maturity ERP = Equity Risk Premium

COST OF CAPITAL 1 WACC = Weighted Avg. Cost of Capital MCC = Marginal Cost of Capital TCS = Target Capital Structure IOS = Investment Opportunity Schedule YTM = Yield-to-Maturity ERP = Equity Risk Premium

MGT Financial Management Mega Quiz file solved by Muhammad Afaaq

MGT 201 - Financial Management Mega Quiz file solved by Muhammad Afaaq Afaaq_tariq@yahoo.com Afaaqtariq233@gmail.com Asslam O Alikum MGT 201 Mega Quiz file solved by Muhammad Afaaq Remember Me in Your

MGT 201 - Financial Management Mega Quiz file solved by Muhammad Afaaq Afaaq_tariq@yahoo.com Afaaqtariq233@gmail.com Asslam O Alikum MGT 201 Mega Quiz file solved by Muhammad Afaaq Remember Me in Your

PAPER No.: 8 Financial Management MODULE No. : 25 Capital Structure Theories IV: MM Hypothesis with Taxes, Merton Miller Argument

Subject Financial Management Paper No. and Title Module No. and Title Module Tag Paper No.8: Financial Management Module No. 25: Capital Structure Theories IV: MM Hypothesis with Taxes and Merton Miller

Subject Financial Management Paper No. and Title Module No. and Title Module Tag Paper No.8: Financial Management Module No. 25: Capital Structure Theories IV: MM Hypothesis with Taxes and Merton Miller

Advanced Corporate Finance

Introduction Advanced Corporate Finance Introduction Instructor: Nikunj Kapadia Office: Room 310 C Tel: 545 5643 Email: nkapadia@som.umass.edu Class Room: 108 Course Requirement Prerequisite: FINOPMGT

Introduction Advanced Corporate Finance Introduction Instructor: Nikunj Kapadia Office: Room 310 C Tel: 545 5643 Email: nkapadia@som.umass.edu Class Room: 108 Course Requirement Prerequisite: FINOPMGT

Question # 1 of 15 ( Start time: 01:53:35 PM ) Total Marks: 1

Total Marks: 1") MGT 201 - Financial Management (Quiz # 5) 380+ Quizzes solved by Muhammad Afaaq Afaaq_tariq@yahoo.com Date Monday 31st January and Tuesday 1st February 2011 Question # 1 of 15 ( Start time: 01:53:35 PM

MGT 201 - Financial Management (Quiz # 5) 380+ Quizzes solved by Muhammad Afaaq Afaaq_tariq@yahoo.com Date Monday 31st January and Tuesday 1st February 2011 Question # 1 of 15 ( Start time: 01:53:35 PM

Capital Structure Decisions

GSU, Department of Finance, AFM - Capital Structure / page 1 - Corporate Finance Capital Structure Decisions - Relevant textbook pages - none - Relevant eoc-problems - none - Other relevant material -

GSU, Department of Finance, AFM - Capital Structure / page 1 - Corporate Finance Capital Structure Decisions - Relevant textbook pages - none - Relevant eoc-problems - none - Other relevant material -

OFFICE OF CAREER SERVICES INTERVIEWS FINANCIAL MODELING

OFFICE OF CAREER SERVICES INTERVIEWS FINANCIAL MODELING Basic valuation concepts are among the most popular technical tasks you will be asked to discuss in investment banking and other finance interviews.

OFFICE OF CAREER SERVICES INTERVIEWS FINANCIAL MODELING Basic valuation concepts are among the most popular technical tasks you will be asked to discuss in investment banking and other finance interviews.

Valuing Levered Projects

Valuing Levered Projects Interactions between financing and investing Nico van der Wijst 1 D. van der Wijst Finance for science and technology students 1 First analyses 2 3 4 2 D. van der Wijst Finance

Valuing Levered Projects Interactions between financing and investing Nico van der Wijst 1 D. van der Wijst Finance for science and technology students 1 First analyses 2 3 4 2 D. van der Wijst Finance

600 Solved MCQs of MGT201 BY

600 Solved MCQs of MGT201 BY http://vustudents.ning.com Why companies invest in projects with negative NPV? Because there is hidden value in each project Because there may be chance of rapid growth Because

600 Solved MCQs of MGT201 BY http://vustudents.ning.com Why companies invest in projects with negative NPV? Because there is hidden value in each project Because there may be chance of rapid growth Because

MGT201 Financial Management Solved MCQs A Lot of Solved MCQS in on file

MGT201 Financial Management Solved MCQs A Lot of Solved MCQS in on file Which group of ratios measures a firm's ability to meet short-term obligations? Liquidity ratios Debt ratios Coverage ratios Profitability

MGT201 Financial Management Solved MCQs A Lot of Solved MCQS in on file Which group of ratios measures a firm's ability to meet short-term obligations? Liquidity ratios Debt ratios Coverage ratios Profitability

Leverage. Capital Budgeting and Corporate Objectives

Leverage Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Overview Capital Structure does not matter!» Modigliani & Miller propositions

Leverage Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Overview Capital Structure does not matter!» Modigliani & Miller propositions

Module 6: Introduction to Valuation of Corporations

Module 6: Introduction to Valuation of Corporations Reading 6.2: Stages of Growth and Financing Reading 6.3-1 : Mergers and Acquisitions Mergers & acquisitions (M&A) Merger Shareholders of two companies

Module 6: Introduction to Valuation of Corporations Reading 6.2: Stages of Growth and Financing Reading 6.3-1 : Mergers and Acquisitions Mergers & acquisitions (M&A) Merger Shareholders of two companies

Homework Solutions - Lecture 2 Part 2

Homework Solutions - Lecture 2 Part 2 1. In 1995, Time Warner Inc. had a Beta of 1.61. Part of the reason for this high Beta was the debt left over from the leveraged buyout of Time by Warner in 1989,

Homework Solutions - Lecture 2 Part 2 1. In 1995, Time Warner Inc. had a Beta of 1.61. Part of the reason for this high Beta was the debt left over from the leveraged buyout of Time by Warner in 1989,

AFM 371 Practice Problem Set #2 Winter Suggested Solutions

AFM 371 Practice Problem Set #2 Winter 2008 Suggested Solutions 1. Text Problems: 16.2 (a) The debt-equity ratio is the market value of debt divided by the market value of equity. In this case we have

AFM 371 Practice Problem Set #2 Winter 2008 Suggested Solutions 1. Text Problems: 16.2 (a) The debt-equity ratio is the market value of debt divided by the market value of equity. In this case we have

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

MBA Corporate Finance CUMULATIVE FINAL EXAM - Summer 2009

MBA 8135 - Corporate Finance CUMULATIVE FINAL EXAM - Summer 2009 Georgia State University Department of Finance August 1, 2009 Name (please print) Instructor: PART I: MULTIPLE CHOICE Choose the letter

MBA 8135 - Corporate Finance CUMULATIVE FINAL EXAM - Summer 2009 Georgia State University Department of Finance August 1, 2009 Name (please print) Instructor: PART I: MULTIPLE CHOICE Choose the letter

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

CHAPTER 6 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concepts Review and Critical Thinking Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will

CHAPTER 8 INTEREST RATES AND BOND VALUATION

CHAPTER 8 INTEREST RATES AND BOND VALUATION Answers to Concept Questions 1. No. As interest rates fluctuate, the value of a Treasury security will fluctuate. Long-term Treasury securities have substantial

CHAPTER 8 INTEREST RATES AND BOND VALUATION Answers to Concept Questions 1. No. As interest rates fluctuate, the value of a Treasury security will fluctuate. Long-term Treasury securities have substantial

CA - FINAL 1.1 Capital Budgeting LOS No. 1: Introduction Capital Budgeting is the process of Identifying & Evaluating capital projects i.e. projects where the cash flows to the firm will be received

CA - FINAL 1.1 Capital Budgeting LOS No. 1: Introduction Capital Budgeting is the process of Identifying & Evaluating capital projects i.e. projects where the cash flows to the firm will be received

Economic Value Added (EVA)

") Economic Value Added (EVA), 2018 Definition Features and problems Computation Economic Value Added (EVA) EVA is promoted by a consulting firm Stern Steward & Co., which was established in 1982 and pioneered

Economic Value Added (EVA), 2018 Definition Features and problems Computation Economic Value Added (EVA) EVA is promoted by a consulting firm Stern Steward & Co., which was established in 1982 and pioneered

MGT201 Financial Management Solved MCQs

MGT201 Financial Management Solved MCQs Why companies invest in projects with negative NPV? Because there is hidden value in each project Because there may be chance of rapid growth Because they have invested

MGT201 Financial Management Solved MCQs Why companies invest in projects with negative NPV? Because there is hidden value in each project Because there may be chance of rapid growth Because they have invested

Sample Final Exam Part I

Sample Final Exam Part I (20 marks) There are 20 multiple choice questions in this part. Choose the one answer that best answers each question. Each question counts one mark. 1. The interest rate at which

Sample Final Exam Part I (20 marks) There are 20 multiple choice questions in this part. Choose the one answer that best answers each question. Each question counts one mark. 1. The interest rate at which

Solved MCQs MGT201. (Group is not responsible for any solved content)

") Solved MCQs 2010 MGT201 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program (MBA,

Solved MCQs 2010 MGT201 (Group is not responsible for any solved content) Subscribe to VU SMS Alert Service To Join Simply send following detail to bilal.zaheem@gmail.com Full Name Master Program (MBA,

Cost of Capital. Chapter 15. Key Concepts and Skills. Cost of Capital

Chapter 5 Key Concepts and Skills Know how to determine a firm s cost of equity capital Know how to determine a firm s cost of debt Know how to determine a firm s overall cost of capital Cost of Capital

Chapter 5 Key Concepts and Skills Know how to determine a firm s cost of equity capital Know how to determine a firm s cost of debt Know how to determine a firm s overall cost of capital Cost of Capital

Corporate Finance Solutions to In Session Detail Review Material

Corporate Finance Solutions to In Session Detail Review Material COPYRIGHT 2013 4 POINT LEARNING SYSTEMS INC. ALL RIGHTS RESERVED. 1 Disclaimer: These questions are designed to provide the student with

Corporate Finance Solutions to In Session Detail Review Material COPYRIGHT 2013 4 POINT LEARNING SYSTEMS INC. ALL RIGHTS RESERVED. 1 Disclaimer: These questions are designed to provide the student with

Valuation Techniques BANSI S. MEHTA & CO.

Valuation Techniques USHMA SHAH BANSI S. MEHTA & CO. PRICE is what you pay. VALUE is what you get. They are not the I can make a whole lot more money skilfully managing intangible assets than managing

Valuation Techniques USHMA SHAH BANSI S. MEHTA & CO. PRICE is what you pay. VALUE is what you get. They are not the I can make a whole lot more money skilfully managing intangible assets than managing

CHAPTER 19. Valuation and Financial Modeling: A Case Study. Chapter Synopsis

CHAPTER 19 Valuation and Financial Modeling: A Case Study Chapter Synopsis 19.1 Valuation Using Comparables A valuation using comparable publicly traded firm valuation multiples may be used as a preliminary

CHAPTER 19 Valuation and Financial Modeling: A Case Study Chapter Synopsis 19.1 Valuation Using Comparables A valuation using comparable publicly traded firm valuation multiples may be used as a preliminary

COST OF CAPITAL

COST OF CAPITAL 2017 1 Introduction Cost of Capital (CoC) are the cost of funds used for financing a business CoC depends on the mode of financing used In most cases a combination of debt and equity is

COST OF CAPITAL 2017 1 Introduction Cost of Capital (CoC) are the cost of funds used for financing a business CoC depends on the mode of financing used In most cases a combination of debt and equity is

Financing decisions (2) Class 16 Financial Management,

Class 16 Financial Management,") Financing decisions (2) Class 16 Financial Management, 15.414 Today Capital structure M&M theorem Leverage, risk, and WACC Reading Brealey and Myers, Chapter 17 Key goal Financing decisions Ensure that

Financing decisions (2) Class 16 Financial Management, 15.414 Today Capital structure M&M theorem Leverage, risk, and WACC Reading Brealey and Myers, Chapter 17 Key goal Financing decisions Ensure that

Financial Analysis Refresher

Financial Analysis Refresher Spring 2017 CE Conference Mark Myles - TURI Financial Analysis Requirements Economic Evaluation of Potential TUR Techniques (310 CMR 50.46A) The TUR plan must include the discount

Financial Analysis Refresher Spring 2017 CE Conference Mark Myles - TURI Financial Analysis Requirements Economic Evaluation of Potential TUR Techniques (310 CMR 50.46A) The TUR plan must include the discount

CHAPTER 15 COST OF CAPITAL

CHAPTER 15 COST OF CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. It is the minimum rate of return the firm must earn overall on its existing assets. If it earns more than this,

CHAPTER 15 COST OF CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. It is the minimum rate of return the firm must earn overall on its existing assets. If it earns more than this,

FIN Chapter 14. Cost of Capital. Liuren Wu

FIN 3000 Chapter 14 Cost of Capital Liuren Wu Overview 1. Understand the concepts underlying the firm s overall cost of capital and the purpose of its calculation. 2. Evaluate a firm s capital structure,

FIN 3000 Chapter 14 Cost of Capital Liuren Wu Overview 1. Understand the concepts underlying the firm s overall cost of capital and the purpose of its calculation. 2. Evaluate a firm s capital structure,

PAPER No. 8: Financial Management MODULE No. 27: Capital Structure in practice

Subject Financial Management Paper No. and Title Module No. and Title Module Tag Paper No.8: Financial Management Module No. 27: Capital Structure in Practice COM_P8_M27 TABLE OF CONTENTS 1. Learning outcomes

Subject Financial Management Paper No. and Title Module No. and Title Module Tag Paper No.8: Financial Management Module No. 27: Capital Structure in Practice COM_P8_M27 TABLE OF CONTENTS 1. Learning outcomes

Maximizing the value of the firm is the goal of managing capital structure.

Key Concepts and Skills Understand the effect of financial leverage on cash flows and the cost of equity Understand the impact of taxes and bankruptcy on capital structure choice Understand the basic components

Key Concepts and Skills Understand the effect of financial leverage on cash flows and the cost of equity Understand the impact of taxes and bankruptcy on capital structure choice Understand the basic components

FREDERICK OWUSU PREMPEH

EXCEL PROFESSIONAL INSTITUTE 3.3 ADVANCED FINANCIAL MANAGEMENT LECTURES SLIDES FREDERICK OWUSU PREMPEH EXCEL PROFESSIONAL INSTITUTE Lecture 8 Theories of capital structure traditional and Modigliani and

EXCEL PROFESSIONAL INSTITUTE 3.3 ADVANCED FINANCIAL MANAGEMENT LECTURES SLIDES FREDERICK OWUSU PREMPEH EXCEL PROFESSIONAL INSTITUTE Lecture 8 Theories of capital structure traditional and Modigliani and

Corporate Finance & Risk Management 06 Financial Valuation

Corporate Finance & Risk Management 06 Financial Valuation Christoph Schneider University of Mannheim http://cf.bwl.uni-mannheim.de schneider@uni-mannheim.de Tel: +49 (621) 181-1949 Topics covered After-tax

Corporate Finance & Risk Management 06 Financial Valuation Christoph Schneider University of Mannheim http://cf.bwl.uni-mannheim.de schneider@uni-mannheim.de Tel: +49 (621) 181-1949 Topics covered After-tax

The Cost of Capital. Principles Applied in This Chapter. The Cost of Capital: An Overview

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital. Chapter 14

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

Copyright 2009 Pearson Education Canada

CHAPTER FIVE Qualitative Questions Question 1 Shareholders prefer to have cash dividends paid to them now rather than waiting for potential payments in the future. Future cash flows from retained earnings

CHAPTER FIVE Qualitative Questions Question 1 Shareholders prefer to have cash dividends paid to them now rather than waiting for potential payments in the future. Future cash flows from retained earnings

OPTIMAL CAPITAL STRUCTURE & CAPITAL BUDGETING WITH TAXES

OPTIMAL CAPITAL STRUCTURE & CAPITAL BUDGETING WITH TAXES Topics: Consider Modigliani & Miller s insights into optimal capital structure Without corporate taxes è Financing policy is irrelevant With corporate

OPTIMAL CAPITAL STRUCTURE & CAPITAL BUDGETING WITH TAXES Topics: Consider Modigliani & Miller s insights into optimal capital structure Without corporate taxes è Financing policy is irrelevant With corporate

5. Risk in capital budgeting implies that the decision maker knows of the cash flows. A. Probability B. Variability C. Certainity D.

1. The assets of a business can be classified as A. Only fixed assets B. Only current assets C. Fixed and current assets D. None of the above 2. What is customer value? A. Post purchase dissonance B. Excess

1. The assets of a business can be classified as A. Only fixed assets B. Only current assets C. Fixed and current assets D. None of the above 2. What is customer value? A. Post purchase dissonance B. Excess

More Tutorial at Corporate Finance

[Type text] More Tutorial at Corporate Finance Question 1. Hardwood Factories, Inc. Hardwood Factories (HF) expects earnings this year of $6/share, and it plans to pay a $4 dividend to shareholders this

[Type text] More Tutorial at Corporate Finance Question 1. Hardwood Factories, Inc. Hardwood Factories (HF) expects earnings this year of $6/share, and it plans to pay a $4 dividend to shareholders this

CHAPTER 8 MAKING CAPITAL INVESTMENT DECISIONS

CHAPTER 8 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concept Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will be used in a project. The relevant

CHAPTER 8 MAKING CAPITAL INVESTMENT DECISIONS Answers to Concept Questions 1. In this context, an opportunity cost refers to the value of an asset or other input that will be used in a project. The relevant

Describe the importance of capital investments and the capital budgeting process

Chapter 20 Making capital investment decisions Affects operations for many years Requires large sums of money Describe the importance of capital investments and the capital budgeting process 3 4 5 6 Operating

Chapter 20 Making capital investment decisions Affects operations for many years Requires large sums of money Describe the importance of capital investments and the capital budgeting process 3 4 5 6 Operating

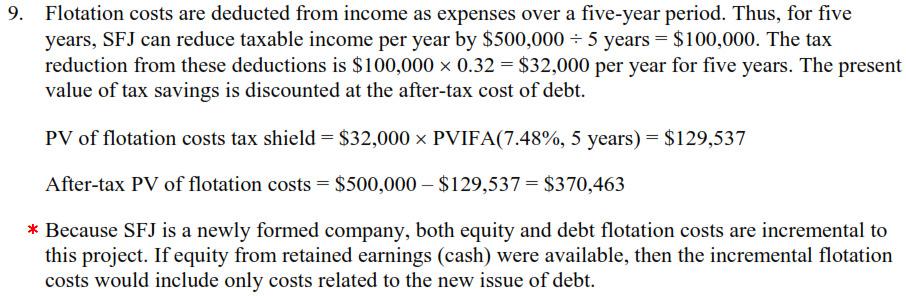

Flotation costs are deductible for tax purposes over a 5-year period. Assume a 40% corporate tax rate.

MODULE 3: LONG-TERM SOURCES OF FUNDS QUESTION 1 TM Corp. has $10,000,000 bond issue outstanding, with annual interest payments at 12%. The issue has 15 years remaining until maturity, but it is callable

MODULE 3: LONG-TERM SOURCES OF FUNDS QUESTION 1 TM Corp. has $10,000,000 bond issue outstanding, with annual interest payments at 12%. The issue has 15 years remaining until maturity, but it is callable

Capital Structure Questions

Capital Structure Questions What do you think? Will the following firm characteristics result in the use of more or less debt? Large firms More tangible assets More lower risk; better access to capital

Capital Structure Questions What do you think? Will the following firm characteristics result in the use of more or less debt? Large firms More tangible assets More lower risk; better access to capital

FEEDBACK TUTORIAL LETTER

FEEDBACK TUTORIAL LETTER 2 nd SEMESTER 2017 ASSIGNMENT 1 MANAGERIAL FINANCE 4B MAF412S 1 Assignment 1 QUESTION 1 COMPANY A & B a) Co. A Co. B Net Operating Income 5,000,000 5,000,000 Less: interest -1,500,000

FEEDBACK TUTORIAL LETTER 2 nd SEMESTER 2017 ASSIGNMENT 1 MANAGERIAL FINANCE 4B MAF412S 1 Assignment 1 QUESTION 1 COMPANY A & B a) Co. A Co. B Net Operating Income 5,000,000 5,000,000 Less: interest -1,500,000

Corporate Finance. Dr Cesario MATEUS Session

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 4 26.03.2014 The Capital Structure Decision 2 Maximizing Firm value vs. Maximizing Shareholder Interests If the

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 4 26.03.2014 The Capital Structure Decision 2 Maximizing Firm value vs. Maximizing Shareholder Interests If the

Web Extension: Comparison of Alternative Valuation Models

19878_26W_p001-009.qxd 3/14/06 3:08 PM Page 1 C H A P T E R 26 Web Extension: Comparison of Alternative Valuation Models We described the APV model in Chapter 26 because it is easier to implement when

19878_26W_p001-009.qxd 3/14/06 3:08 PM Page 1 C H A P T E R 26 Web Extension: Comparison of Alternative Valuation Models We described the APV model in Chapter 26 because it is easier to implement when

Homework Solutions - Lecture 2

Homework Solutions - Lecture 2 1. The value of the S&P 500 index is 1312.41 and the treasury rate is 1.83%. In a typical year, stock repurchases increase the average payout ratio on S&P 500 stocks to over

Homework Solutions - Lecture 2 1. The value of the S&P 500 index is 1312.41 and the treasury rate is 1.83%. In a typical year, stock repurchases increase the average payout ratio on S&P 500 stocks to over

Module 4: Capital Structure and Dividend Policy

Module 4: Capital Structure and Dividend Policy Reading 4.1 Capital structure theory Reading 4.2 Capital structure theory in perfect markets Reading 4.3 Impact of corporate taxes on capital structure Reading

Module 4: Capital Structure and Dividend Policy Reading 4.1 Capital structure theory Reading 4.2 Capital structure theory in perfect markets Reading 4.3 Impact of corporate taxes on capital structure Reading

Financial, Treasury and : Forex 1 : Management

Financial, Treasury and : Forex 1 : Management RollNo... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 7 Total number of printed pages : 7 NOTE : 1. Answer FIVE questions including

Financial, Treasury and : Forex 1 : Management RollNo... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 7 Total number of printed pages : 7 NOTE : 1. Answer FIVE questions including

AFM 271. Midterm Examination #2. Friday June 17, K. Vetzal. Answer Key

AFM 21 Midterm Examination #2 Friday June 1, 2005 K. Vetzal Name: Answer Key Student Number: Section Number: Duration: 1 hour and 30 minutes Instructions: 1. Answer all questions in the space provided.

AFM 21 Midterm Examination #2 Friday June 1, 2005 K. Vetzal Name: Answer Key Student Number: Section Number: Duration: 1 hour and 30 minutes Instructions: 1. Answer all questions in the space provided.

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions 1. Text Problems: 6.2 (a) Consider the following table: time cash flow cumulative cash flow 0 -$1,000,000 -$1,000,000 1 $150,000 -$850,000

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions 1. Text Problems: 6.2 (a) Consider the following table: time cash flow cumulative cash flow 0 -$1,000,000 -$1,000,000 1 $150,000 -$850,000

REVIEW FOR SECOND QUIZ. Show me the money

REVIEW FOR SECOND QUIZ Show me the money The skill set for this test Can you compute the cost of capital for a project (rather than a firm)? How do you estimate the cost of equity for a project? What debt

REVIEW FOR SECOND QUIZ Show me the money The skill set for this test Can you compute the cost of capital for a project (rather than a firm)? How do you estimate the cost of equity for a project? What debt

Handout for Unit 4 for Applied Corporate Finance

Handout for Unit 4 for Applied Corporate Finance Unit 4 Capital Structure Contents 1. Types of Financing 2. Financing Choices 3. How much debt is good? 4. Debt Benefits vs Costs 5. Approaches to arriving

Handout for Unit 4 for Applied Corporate Finance Unit 4 Capital Structure Contents 1. Types of Financing 2. Financing Choices 3. How much debt is good? 4. Debt Benefits vs Costs 5. Approaches to arriving

Chapter 8. Fundamentals of Capital Budgeting

Chapter 8 Fundamentals of Capital Budgeting Chapter Outline 8.1 Forecasting Earnings 8.2 Determining Free Cash Flow and NPV 8.3 Choosing Among Alternatives 8.4 Further Adjustments to Free Cash Flow 8.5

Chapter 8 Fundamentals of Capital Budgeting Chapter Outline 8.1 Forecasting Earnings 8.2 Determining Free Cash Flow and NPV 8.3 Choosing Among Alternatives 8.4 Further Adjustments to Free Cash Flow 8.5

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination CORPORATE FINANCIAL MAMANGMENT JUNE 2011 Suggested

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination CORPORATE FINANCIAL MAMANGMENT JUNE 2011 Suggested

FINALTERM EXAMINATION Spring 2009 MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

FINALTERM EXAMINATION Spring 2009 MGT201- Financial Management (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one What is the long-run objective of financial management? Maximize earnings per

Risk, Return and Capital Budgeting

Risk, Return and Capital Budgeting For 9.220, Term 1, 2002/03 02_Lecture15.ppt Student Version Outline 1. Introduction 2. Project Beta and Firm Beta 3. Cost of Capital No tax case 4. What influences Beta?

Risk, Return and Capital Budgeting For 9.220, Term 1, 2002/03 02_Lecture15.ppt Student Version Outline 1. Introduction 2. Project Beta and Firm Beta 3. Cost of Capital No tax case 4. What influences Beta?

Postal Test Paper_P14_Final_Syllabus 2016_Set 1 Paper 14: Strategic Financial Management

Paper 14: Strategic Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 14 - Strategic Financial Management Full

Paper 14: Strategic Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 14 - Strategic Financial Management Full

I. Multiple choice questions: Circle one answer that is the best. (2.5 points each)

") I. Multiple choice questions: Circle one answer that is the best. (2.5 points each) 1. An investor discovers that for a certain group of stocks, large positive price changes are always followed by large

I. Multiple choice questions: Circle one answer that is the best. (2.5 points each) 1. An investor discovers that for a certain group of stocks, large positive price changes are always followed by large

FN428 : Investment Banking. Lecture 23 : Revision class

FN428 : Investment Banking Lecture 23 : Revision class Recap : Theory of Financial Intermediary An overview of Investment Banking Investment Bank vs. Commercial Bank Which are the various divisions of

FN428 : Investment Banking Lecture 23 : Revision class Recap : Theory of Financial Intermediary An overview of Investment Banking Investment Bank vs. Commercial Bank Which are the various divisions of

Financial Planning and Control. Semester: 1/2559

Financial Planning and Control Semester: 1/2559 Krisada Khruachalee Master of Science in Applied Statistics, Master of Science in Finance, Bachelor of Business Administration (Cum Laude), Finance and Banking

Financial Planning and Control Semester: 1/2559 Krisada Khruachalee Master of Science in Applied Statistics, Master of Science in Finance, Bachelor of Business Administration (Cum Laude), Finance and Banking

Corporate Finance Primer

Chartered Professional Accountants of Canada, CPA Canada, CPA are trademarks and/or certification marks of the Chartered Professional Accountants of Canada. 2018, Chartered Professional Accountants of

Chartered Professional Accountants of Canada, CPA Canada, CPA are trademarks and/or certification marks of the Chartered Professional Accountants of Canada. 2018, Chartered Professional Accountants of

Chapter 18 Interest rates / Transaction Costs Corporate Income Taxes (Cash Flow Effects) Example - Summary for Firm U Summary for Firm L

Example - Summary for Firm U Summary for Firm L") Chapter 18 In Chapter 17, we learned that with a certain set of (unrealistic) assumptions, a firm's value and investors' opportunities are determined by the asset side of the firm's balance sheet (i.e.,

Chapter 18 In Chapter 17, we learned that with a certain set of (unrealistic) assumptions, a firm's value and investors' opportunities are determined by the asset side of the firm's balance sheet (i.e.,

QUESTION ONE Briefly explain three practical uses of the capital asset pricing model. ( 6 marks) Beta equity coefficient

Beta equity coefficient") QUESTIONS QUESTION ONE Briefly explain three practical uses of the capital asset pricing model. ( 6 marks) (b) Mr. P K is currently holding a portfolio consisting of shares of four companies quoted on

QUESTIONS QUESTION ONE Briefly explain three practical uses of the capital asset pricing model. ( 6 marks) (b) Mr. P K is currently holding a portfolio consisting of shares of four companies quoted on

Disclaimer: This resource package is for studying purposes only EDUCATION

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 6: Valuing stocks Bond Cash Flows, Prices, and Yields - Maturity date: Final payment date - Term: Time remaining until

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 6: Valuing stocks Bond Cash Flows, Prices, and Yields - Maturity date: Final payment date - Term: Time remaining until

Session 1, Monday, April 8 th (9:45-10:45)

") Session 1, Monday, April 8 th (9:45-10:45) Time Value of Money and Capital Budgeting v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Time Value of Money:

Session 1, Monday, April 8 th (9:45-10:45) Time Value of Money and Capital Budgeting v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Time Value of Money:

DISCOUNTED CASH-FLOW ANALYSIS

DISCOUNTED CASH-FLOW ANALYSIS Objectives: Study determinants of incremental cash flows Estimate incremental after-tax cash flows from accounting data and use them to estimate NPV Introduce salvage value

DISCOUNTED CASH-FLOW ANALYSIS Objectives: Study determinants of incremental cash flows Estimate incremental after-tax cash flows from accounting data and use them to estimate NPV Introduce salvage value

risk free rate 7% market risk premium 4% pre-merger beta 1.3 pre-merger % debt 20% pre-merger debt r d 9% Tax rate 40%

Hager s Home Repair Company, a regional hardware chain, which specializes in do-ityourself materials and equipment rentals, is cash rich because of several consecutive good years. One of the alternative

Hager s Home Repair Company, a regional hardware chain, which specializes in do-ityourself materials and equipment rentals, is cash rich because of several consecutive good years. One of the alternative

Homework and Suggested Example Problems Investment Valuation Damodaran. Lecture 2 Estimating the Cost of Capital

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 2 Estimating the Cost of Capital Lecture 2 begins with a discussion of alternative discounted cash flow models, including

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 2 Estimating the Cost of Capital Lecture 2 begins with a discussion of alternative discounted cash flow models, including

MTP_Final_Syllabus 2016_Jun2017_Set 2 Paper 14 Strategic Financial Management

Paper 14 Strategic Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory body under an Act of Parliament) Page 1 Paper 14 Strategic Financial Management Full

Paper 14 Strategic Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory body under an Act of Parliament) Page 1 Paper 14 Strategic Financial Management Full

CHAPTER 9 STOCK VALUATION

CHAPTER 9 STOCK VALUATION Answers to Concept Questions 1. The value of any investment depends on the present value of its cash flows; i.e., what investors will actually receive. The cash flows from a share

CHAPTER 9 STOCK VALUATION Answers to Concept Questions 1. The value of any investment depends on the present value of its cash flows; i.e., what investors will actually receive. The cash flows from a share

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination CORPORATE FINANCIAL MANAGEMENT PILOT PAPER Marking

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination CORPORATE FINANCIAL MANAGEMENT PILOT PAPER Marking

Advanced Corporate Finance. 3. Capital structure

Advanced Corporate Finance 3. Capital structure Practical Information Change of groups! A => : Group 3 Friday 10-12 am F => N : Group 2 Monday 4-6 pm O => Z : Group 1 Friday 4-6 pm 2 Objectives of the

Advanced Corporate Finance 3. Capital structure Practical Information Change of groups! A => : Group 3 Friday 10-12 am F => N : Group 2 Monday 4-6 pm O => Z : Group 1 Friday 4-6 pm 2 Objectives of the

CHAPTER 14. Capital Structure in a Perfect Market. Chapter Synopsis

CHAPTR 14 Capital Structure in a Perfect Market Chapter Synopsis 14.1 quity Versus Debt Financing A firm s capital structure refers to the debt, equity, and other securities used to finance its fixed assets.

CHAPTR 14 Capital Structure in a Perfect Market Chapter Synopsis 14.1 quity Versus Debt Financing A firm s capital structure refers to the debt, equity, and other securities used to finance its fixed assets.

Estimating Cash Flows

Estimating Cash Flows From accounts to cashflow Assets Liabilities Existing investments Generate cash flows today include long-lived (fixed) and short-lived (wc) assets Assets in Place Debt Fixed claim

Estimating Cash Flows From accounts to cashflow Assets Liabilities Existing investments Generate cash flows today include long-lived (fixed) and short-lived (wc) assets Assets in Place Debt Fixed claim

FCF t. V = t=1. Topics in Chapter. Chapter 16. How can capital structure affect value? Basic Definitions. (1 + WACC) t

t") Topics in Chapter Chapter 16 Capital Structure Decisions Overview and preview of capital structure effects Business versus financial risk The impact of debt on returns Capital structure theory, evidence,

Topics in Chapter Chapter 16 Capital Structure Decisions Overview and preview of capital structure effects Business versus financial risk The impact of debt on returns Capital structure theory, evidence,

CHAPTER 16 CAPITAL STRUCTURE: BASIC CONCEPTS

CHAPTER 16 CAPITAL STRUCTURE: BASIC CONCEPTS Answers to Concepts Review and Critical Thinking Questions 2. False. A reduction in leverage will decrease both the risk of the stock and its expected return.

CHAPTER 16 CAPITAL STRUCTURE: BASIC CONCEPTS Answers to Concepts Review and Critical Thinking Questions 2. False. A reduction in leverage will decrease both the risk of the stock and its expected return.

Advanced Corporate Finance. 3. Capital structure

Advanced Corporate Finance 3. Capital structure Objectives of the session So far, NPV concept and possibility to move from accounting data to cash flows => But necessity to go further regarding the discount

Advanced Corporate Finance 3. Capital structure Objectives of the session So far, NPV concept and possibility to move from accounting data to cash flows => But necessity to go further regarding the discount

Financial Modeling Fundamentals Module 08 Discounted Cash Flow (DCF) Analysis Quiz Questions

Analysis Quiz Questions") Financial Modeling Fundamentals Module 08 Discounted Cash Flow (DCF) Analysis Quiz Questions 1. How much would you be willing to pay for a company that generates exactly $100 in Free Cash Flow into eternity?

Financial Modeling Fundamentals Module 08 Discounted Cash Flow (DCF) Analysis Quiz Questions 1. How much would you be willing to pay for a company that generates exactly $100 in Free Cash Flow into eternity?

THE UNIVERSITY OF NEW SOUTH WALES JUNE / JULY 2006 FINS1613. Business Finance Final Exam

Student Name: Student ID Number: THE UNIVERSITY OF NEW SOUTH WALES JUNE / JULY 2006 FINS1613 Business Finance Final Exam (1) TIME ALLOWED - 2 hours (2) TOTAL NUMBER OF QUESTIONS - 50 (3) ANSWER ALL QUESTIONS

Student Name: Student ID Number: THE UNIVERSITY OF NEW SOUTH WALES JUNE / JULY 2006 FINS1613 Business Finance Final Exam (1) TIME ALLOWED - 2 hours (2) TOTAL NUMBER OF QUESTIONS - 50 (3) ANSWER ALL QUESTIONS

Understanding Financial Management: A Practical Guide Problems and Answers

Understanding Financial Management: A Practical Guide Problems and Answers Chapter 1 Raising Funds and Cost of Capital 1.1 Financial Markets 1. What is the difference between a financial market and a financial

Understanding Financial Management: A Practical Guide Problems and Answers Chapter 1 Raising Funds and Cost of Capital 1.1 Financial Markets 1. What is the difference between a financial market and a financial

Investment Appraisal

Investment Appraisal Introduction to Investment Appraisal Whatever level of management authorises a capital expenditure, the proposed investment should be properly evaluated, and found to be worthwhile

Investment Appraisal Introduction to Investment Appraisal Whatever level of management authorises a capital expenditure, the proposed investment should be properly evaluated, and found to be worthwhile

AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting

Time Value of Money and Capital Budgeting") AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting Chapters Covered Time Value of Money: Part I, Domain B Chapter 6 Net

AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting Chapters Covered Time Value of Money: Part I, Domain B Chapter 6 Net

Review of Financial Analysis Terms

Review of Financial Analysis Terms Financial Analysis Requirements Economic Evaluation of Potential TUR Techniques (310 CMR 50.46A) The TUR plan must include the discount rate, cost of capital, depreciation

Review of Financial Analysis Terms Financial Analysis Requirements Economic Evaluation of Potential TUR Techniques (310 CMR 50.46A) The TUR plan must include the discount rate, cost of capital, depreciation

Chapter 8: Prospective Analysis: Valuation Implementation

Chapter 8: Prospective Analysis: Valuation Implementation Key Concepts in Chapter 8 Two key issues must be addressed to implement valuation theory: 1. Determining the appropriate discount rate to use in

Chapter 8: Prospective Analysis: Valuation Implementation Key Concepts in Chapter 8 Two key issues must be addressed to implement valuation theory: 1. Determining the appropriate discount rate to use in

MIDTERM EXAM SOLUTIONS

MIDTERM EXAM SOLUTIONS Finance 40610 Security Analysis Mendoza College of Business Professor Shane A. Corwin Fall Semester 2005 Monday, October 10, 2005 Multiple Choice (28 points) Choose the best answer

MIDTERM EXAM SOLUTIONS Finance 40610 Security Analysis Mendoza College of Business Professor Shane A. Corwin Fall Semester 2005 Monday, October 10, 2005 Multiple Choice (28 points) Choose the best answer

Finance 303 Financial Management Review Notes for Final. Chapters 11&12

Finance 303 Financial Management Review Notes for Final Chapters 11&12 Capital budgeting Project classifications Capital budgeting techniques (5 approaches, concepts and calculations) Cash flow estimation

Finance 303 Financial Management Review Notes for Final Chapters 11&12 Capital budgeting Project classifications Capital budgeting techniques (5 approaches, concepts and calculations) Cash flow estimation

Chapter 14 The Cost of Capital

Topics Covered Chapter 14 The Cost of Capital Konan Chan Financial Management, Fall 2018 Cost of capital Weighted average cost of capital (WACC) Capital structure Required rates of return Divisional costs

Topics Covered Chapter 14 The Cost of Capital Konan Chan Financial Management, Fall 2018 Cost of capital Weighted average cost of capital (WACC) Capital structure Required rates of return Divisional costs

Financial Statements, Taxes and Cash Flow

Financial Statements, Taxes and Cash Flow Faculty of Business Administration Lakehead University Spring 2003 May 5, 2003 2.1 The Balance Sheet 2.2 The Income Statement 2.3 Cash Flow 2.4 Taxes 2.5 Capital

Financial Statements, Taxes and Cash Flow Faculty of Business Administration Lakehead University Spring 2003 May 5, 2003 2.1 The Balance Sheet 2.2 The Income Statement 2.3 Cash Flow 2.4 Taxes 2.5 Capital

3 Leasing Decisions. The Institute of Chartered Accountants of India

3 Leasing Decisions BASIC CONCEPTS AND FORMULAE 1. Introduction Lease can be defined as a right to use an equipment or capital goods on payment of periodical amount. Two principal parties to any lease

3 Leasing Decisions BASIC CONCEPTS AND FORMULAE 1. Introduction Lease can be defined as a right to use an equipment or capital goods on payment of periodical amount. Two principal parties to any lease