Mergers & Acquisitions

|

|

|

- Robert Kelley

- 5 years ago

- Views:

Transcription

1 Mergers & Acquisitions

2 Topics Covered Sensible Motives for Mergers Some Dubious Reasons for Mergers Estimating Merger Gains and Costs The Mechanics of a Merger Proxy Fights, Takeovers, and the Market for Corporate Control Mergers and the Economy

3 Types of Mergers Horizontal mergers Combinations of two firms in the same industry (Bank of New York and Mellon Financial Corporation, 2007) Vertical mergers Involves companies at different stages of production Forward integration: Boise Cascade (paper manufacturer) acquire Office Max (office products distributor), 2003 Backward integration: TomTom (maker of car navigation devices) acquire Tele Atlas (digital map data), 2008 Conglomerate mergers Involves companies in unrelated line of businesses MIG (financial services) acquire Olympic Airlines (Travel & Leisure), 2009

4 M&A Around the World ( ) Deals Horizontal mergers 41.7% Vertical mergers 4% Conglomerate mergers 54.3% Cross border 21.7% Please see, Gugler, Mueller, Yurtoglu and Zulehner (2003)

5 Sensible Reasons for Mergers Economies of Scale A larger firm may be able to reduce its per unit cost by using excess capacity or spreading fixed costs across more units.

6 Sensible Reasons for Mergers Economies of Vertical Integration Control over suppliers may reduce costs. Over integration can cause the opposite effect. S Pre-integration (less efficient) S Company S S S S S Post-integration (more efficient) Company S

7 Sensible Reasons for Mergers Combining Complementary Resources The two firms have complementary resources - each has what the other needs. Merging may results in each firm filling in the missing pieces of their firm with pieces from the other firm. Firm A Firm B

8 Sensible Reasons for Mergers Mergers as a Use for Surplus Funds If your firm is in a mature industry with few, if any, positive NPV projects available, acquisition may be the best use of your funds. Firms with a surplus of cash and a shortage of good investment opportunities often turn to mergers financed by cash. Such firms often find themselves targeted for takeover by other firms that propose to redeploy the cash for them. Example: the early 1980s many cash-rich oil companies found themselves threatened by takeover.

9 Sensible Reasons for Mergers Eliminating Inefficiencies There are firms with unexploited opportunities to cut costs and increase sales and earnings (poor management). Such firms are natural candidates for acquisition by other firms with better management. A merger is not the only way to improve management, but sometimes it is the only simple and practical way.

10 Sensible Reasons for Mergers Industry Consolidation The biggest opportunities to improve efficiency seem to come in industries with too many firms and too much capacity. The banking industry is an example. The US entered the 1980s with far too many banks, largely as a result of outdated restrictions on interstate banking. As these restrictions eroded and communications and technology improved, hundreds of small banks were swept up into regional or super-regional banks.

11 Bank of America Family Tree

12 Dubious Reasons for Mergers Diversification Investors should not pay a premium for diversification since they can do it themselves. The trouble with this argument is that diversification is easier and cheaper for the stockholders than for the corporation.

13 Dubious Reasons for Mergers Increasing EPS: The Bootstrap Game Acquiring Firm has high P/E ratio Selling firm has low P/E ratio After merger, acquiring firm has short term EPS rise Long term, acquirer will have slower than normal EPS growth due to share dilution

14 Dubious Reasons for Mergers Increasing EPS: The Bootstrap Game World Enterprises (before merger) Muck and Slurry World Enterprises (after buying Muck and Slurry) EPS $ 2.00 $ 2.00 $ 2.67 Price per share $ $ $ P/E Ratio Number of shares 100, , ,000 Total earnings $ 200,000 $ 200,000 $ 400,000 Total market value $ 4,000,000 $ 2,000,000 $ 6,000,000 Current earnings per dollar invested in stock $ 0.05 $ 0.10 $ 0.067

15 Dubious Reasons for Mergers

16 Lower Financing Costs When two firms merge, the combined company (AB) can borrow at lower interest rates than either firm could separately. In part this is true! While the two firms are separate, they do not guarantee each other s debt. But after the merger each firm effectively does guarantee the other s debt. Because these mutual guarantees make the debt less risky, lenders demand a lower interest rate. Does the lower interest rate mean a net gain to the merger? Not necessarily! Although AB s shareholders do gain from the lower interest rate, they lose by having to guarantee each other s debt.

17 Estimating Merger Gains Questions Is there an overall economic gain to the merger? Do the terms of the merger make the company and its shareholders better off? PV(AB) > PV(A) + PV(B) There is an economic gain only if the two firms are worth more together than apart

18 Estimating Merger Gains and Costs Gain PV AB (PV A PV B ) PV AB Cost Cash paid PV B NPV gain cos t PV AB (cash PV B )

19 Example: Firm A has a value of 200M, and B has a value of 50M. Two firms merge creating 25M in synergies. Firm A buys B with cash for 65M. What is the merger cost to firm A s stockholders? PV PV PV A B Gain AB PV PV A AB PV B 25 Gain 275M Cost Cash paid PV M B

20 Example (cont d) What is the merger gain to firm A s stockholders? The NPV to firm A s stockholders will be the difference between the gain and the cost. NPV A Gain Cost M NPV A wealth with merger - (PV AB Cash) (275 65) M PV A wealth without merger

21 Merger is Financed by Stock Cost Cost NP AB target firm shareholde rs receive of the combined firms xpv AB PV B PV B target firm shareholde rs receive N shares the fraction x of the combined firms

22 Accounting for a Merger Accounting for the merger of A Corp and B Corp assuming that A Corp pays $18 million for B Corp. Initial Balance Sheets A Corporation B Corporation NWC D NWC 1 0 D FA E FA 9 10 E Balance Sheet of AB corporation NWC D FA E Goodwill

23 Takeover Methods Tools Used To Acquire Companies Proxy Contest Tender Offer Acquisition Merger Leveraged Buy-Out Manageme nt Buy-Out

24 Takeover Defenses

25 Anti-takeover Devices Greenmail (Management offer to buy him out, at a substantial bonus over the market price of the stock) Example: Bass brothers acquired 9.9% of Texaco (1984). Texaco s management paid the Bass brothers $137 million premium over the market price or $55 per share - $35 market price of the stock poison pills or shareholder rights plans (the plans usually take the form of rights issued to shareholders. Pills give shareholders the ability to purchase shares from, or sell shares back to, the target company (the flip-in pill) and/or the potential acquirer (the flip-over pill)

26 Other Anti-takeover Devices white knight (third party who agrees to buy a significant portion of stock to keep it out of the acquirer s hands) New class of shareholder with unequal voting rights Crown Jewel strategy (the target company would sell the most valuable assets) I will eat you before you eat me pacman defence (example: Bendix - Martin Marietta (1982))

27 Winners and Losers in the Merger Game Stock Market Reaction to Merger Announcements The average 3-day CAR for acquirer and target firms combined is 1.8% (AMS) The average 3-day CAR for target firms is 16% (AMS) The average 3-day CAR for acquirer firms is -0.7% (AMS) Target firm shareholders also do better when there is no equity financing (AMS) The losers were mainly the largest acquirers; the stockholders of the other acquirers appeared to gain (MSS) Mergers seem to create value for shareholders overall, but the target firm shareholders are clearly winners in merger transactions Please see, Andrade, Mitchell and Stafford (2001) JEP (AMS) and Moeller, Schlingemann and Stulz (2004) JFE (MSS)

28 Winners and Losers in the Merger Game (cont d) Long-Term Abnormal Returns Long-term event studies measuring negative abnormal returns over the three to five years following merger completion Serious methodological concerns with the long-term event studies (for example, crosssectional correlation of ARs)

29 Winners and Losers in the Merger Game (cont d) Pre- and Post-Merger Profitability Healy, Palepu and Ruback (1992) find that merged firms experience improvements in asset productivity, leading to higher operating cash flows relative to their industry median. Operating performance (cash flow to sales) is strong relative to industry benchmarks prior to the merger, and improves slightly subsequent to the merger transaction (AMS). On average, there is an improvement in operating performance following the merger (AMS).

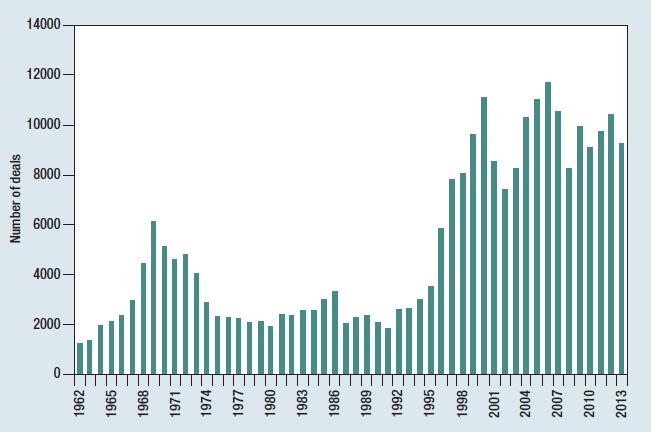

30 Empirical Features of Merger Activity Mergers occur in waves Within a wave, mergers strongly cluster by industry Often prompted by deregulation and by changes in technology (for example, deregulation of telecoms and banking in the 1990s led to a spate of mergers in both industries)

31 Recent Mergers

32 Mergers ( )

33 Web Resources

Topics in Corporate Finance. Chapter 9: Mergers and Acquisitions. Albert Banal-Estanol

Topics in Corporate Finance Chapter 9: Mergers and Acquisitions Merger activity in the US during the past century Mergers in Europe Mergers come in waves and are procyclical This chapter s Plan Evidence

Topics in Corporate Finance Chapter 9: Mergers and Acquisitions Merger activity in the US during the past century Mergers in Europe Mergers come in waves and are procyclical This chapter s Plan Evidence

Mergers, Acquisitions and Divestures

Session 11 &12 Mergers, Acquisitions and Divestures Programme : Postgraduate Diploma in Business, Finance & Strategy (PGDBFS 2018) Course : Corporate Valuation (PGDBFS 203) Lecturer : Mr. Asanka Ranasinghe

Session 11 &12 Mergers, Acquisitions and Divestures Programme : Postgraduate Diploma in Business, Finance & Strategy (PGDBFS 2018) Course : Corporate Valuation (PGDBFS 203) Lecturer : Mr. Asanka Ranasinghe

Chapter 23 Mergers and Acquisitions

T23.1 Chapter Outline Chapter Organization Chapter 23 Mergers and Acquisitions! 23.1 The Legal Forms of Acquisitions! 23.2 Taxes and Acquisitions! 23.3 Accounting for Acquisitions! 23.4 Gains from Acquisition!

T23.1 Chapter Outline Chapter Organization Chapter 23 Mergers and Acquisitions! 23.1 The Legal Forms of Acquisitions! 23.2 Taxes and Acquisitions! 23.3 Accounting for Acquisitions! 23.4 Gains from Acquisition!

Mergers, Acquisitions and Divestures

Session 11 &12 Mergers, Acquisitions and Divestures Programme : Postgraduate Diploma in Business, Finance & Strategy (PGDBFS 2017) Course : Corporate Valuation (PGDBFS 203) Lecturer : Mr. Asanka Ranasinghe

Session 11 &12 Mergers, Acquisitions and Divestures Programme : Postgraduate Diploma in Business, Finance & Strategy (PGDBFS 2017) Course : Corporate Valuation (PGDBFS 203) Lecturer : Mr. Asanka Ranasinghe

Mergers and Acquisitions

Takeovers Takeover: transfers the control right of the firm from one group to another Merger Mergers and Acquisitions Acquisition Acquisition of Stock, 2018 Takeovers Proxy Contest Going Private Acquisition

Takeovers Takeover: transfers the control right of the firm from one group to another Merger Mergers and Acquisitions Acquisition Acquisition of Stock, 2018 Takeovers Proxy Contest Going Private Acquisition

Corporate Finance. Lecture 12: Mergers and Acquisitions. Albert Banal-Estanol

Corporate Finance 12: Mergers and Acquisitions Merger activity in the US during the past century Mergers in Europe Mergers come in waves and are procyclical Recent Mergers Industry Acquiring Company Selling

Corporate Finance 12: Mergers and Acquisitions Merger activity in the US during the past century Mergers in Europe Mergers come in waves and are procyclical Recent Mergers Industry Acquiring Company Selling

Chapter 31: Mergers. Problem Sets (3, 12, 13, 15)

") Chapter 31: Mergers Problem Sets (3, 12, 13, 15) Problem 3: (See Ch31, p.839) Velcro Saddles is contemplating the acquisition of Pogo Ski Sticks, Inc. The values of the two companies as separate entities

Chapter 31: Mergers Problem Sets (3, 12, 13, 15) Problem 3: (See Ch31, p.839) Velcro Saddles is contemplating the acquisition of Pogo Ski Sticks, Inc. The values of the two companies as separate entities

Module 6: Introduction to Valuation of Corporations

Module 6: Introduction to Valuation of Corporations Reading 6.2: Stages of Growth and Financing Reading 6.3-1 : Mergers and Acquisitions Mergers & acquisitions (M&A) Merger Shareholders of two companies

Module 6: Introduction to Valuation of Corporations Reading 6.2: Stages of Growth and Financing Reading 6.3-1 : Mergers and Acquisitions Mergers & acquisitions (M&A) Merger Shareholders of two companies

Chapter 025 Mergers and Acquisitions

Multiple Choice Questions 1. The complete absorption of one company by another, wherein the acquiring firm retains its identity and the acquired firm ceases to exist as a separate entity, is called a:

Multiple Choice Questions 1. The complete absorption of one company by another, wherein the acquiring firm retains its identity and the acquired firm ceases to exist as a separate entity, is called a:

Chapter 1 Introduction to Business Combinations and the Conceptual Framework

Chapter 1 Introduction to Business Combinations and the Conceptual Framework Multiple Choice 1. Stock given as consideration for a business combination is valued at a. fair market value b. par value c.

Chapter 1 Introduction to Business Combinations and the Conceptual Framework Multiple Choice 1. Stock given as consideration for a business combination is valued at a. fair market value b. par value c.

MERGER & CONSOLIDATION: OVERVIEW

MERGER & CONSOLIDATION: OVERVIEW Merger: A contractual and statutory process by : (1) which one corporation (the surviving corporation) acquires all of the assets and liabilities of another corporation

MERGER & CONSOLIDATION: OVERVIEW Merger: A contractual and statutory process by : (1) which one corporation (the surviving corporation) acquires all of the assets and liabilities of another corporation

CORPORATE CONTROL EVENTS EB434 ENTERPRISE GOVERNANCE

CORPORATE CONTROL EVENTS 16 EB434 ENTERPRISE GOVERNANCE corporate control events Open market purchases on the stock market Tender offer offer made directly to shareholders (often by law, to all shareholders

CORPORATE CONTROL EVENTS 16 EB434 ENTERPRISE GOVERNANCE corporate control events Open market purchases on the stock market Tender offer offer made directly to shareholders (often by law, to all shareholders

Mergers and Acquisitions

Mergers and Acquisitions 1 Classifying M&A Merger: the boards of directors of two firms agree to combine and seek shareholder approval for combination. The target ceases to exist. Consolidation: a new

Mergers and Acquisitions 1 Classifying M&A Merger: the boards of directors of two firms agree to combine and seek shareholder approval for combination. The target ceases to exist. Consolidation: a new

Appendix: The Disciplinary Motive for Takeovers A Review of the Empirical Evidence

Appendix: The Disciplinary Motive for Takeovers A Review of the Empirical Evidence Anup Agrawal Culverhouse College of Business University of Alabama Tuscaloosa, AL 35487-0224 Jeffrey F. Jaffe Department

Appendix: The Disciplinary Motive for Takeovers A Review of the Empirical Evidence Anup Agrawal Culverhouse College of Business University of Alabama Tuscaloosa, AL 35487-0224 Jeffrey F. Jaffe Department

The impact of large acquisitions on the share price and operating financial performance of acquiring companies listed on the JSE

on CJB the Smit JSE and MJD Ward* The impact of large acquisitions on the share price and operating financial performance of acquiring companies listed 1. INTRODUCTION * A KPMG survey in London found that

on CJB the Smit JSE and MJD Ward* The impact of large acquisitions on the share price and operating financial performance of acquiring companies listed 1. INTRODUCTION * A KPMG survey in London found that

Long Term Performance of Divesting Firms and the Effect of Managerial Ownership. Robert C. Hanson

Long Term Performance of Divesting Firms and the Effect of Managerial Ownership Robert C. Hanson Department of Finance and CIS College of Business Eastern Michigan University Ypsilanti, MI 48197 Moon H.

Long Term Performance of Divesting Firms and the Effect of Managerial Ownership Robert C. Hanson Department of Finance and CIS College of Business Eastern Michigan University Ypsilanti, MI 48197 Moon H.

The Benefits of Market Timing: Evidence from Mergers and Acquisitions

The Benefits of Timing: Evidence from Mergers and Acquisitions Evangelos Vagenas-Nanos University of Glasgow, University Avenue, Glasgow, G12 8QQ, UK Email: evangelos.vagenas-nanos@glasgow.ac.uk Abstract

The Benefits of Timing: Evidence from Mergers and Acquisitions Evangelos Vagenas-Nanos University of Glasgow, University Avenue, Glasgow, G12 8QQ, UK Email: evangelos.vagenas-nanos@glasgow.ac.uk Abstract

Transactional Valuation - M&A / Private Equity August 2011

www.pwc.com Transactional Valuation - M&A / Private Equity Agenda Valuation for Mergers and Acquisition Valuation for PE Valuation for Demergers Slide 2 Valuation for Mergers and Acquisitions Understanding

www.pwc.com Transactional Valuation - M&A / Private Equity Agenda Valuation for Mergers and Acquisition Valuation for PE Valuation for Demergers Slide 2 Valuation for Mergers and Acquisitions Understanding

FIN 423 M&A Strategy. Dodd (JFE, 1980): Successful & Unsuccessful Mergers

: Successful & Unsuccessful Mergers") Successful & unsuccessful mergers & tender offers Sharks White Knights winners losers FIN 423 M&A Strategy Dodd (JFE, 1980): Successful & Unsuccessful Mergers 151 targets, 126 bidders NYSE, 1970-77 Announcement

Successful & unsuccessful mergers & tender offers Sharks White Knights winners losers FIN 423 M&A Strategy Dodd (JFE, 1980): Successful & Unsuccessful Mergers 151 targets, 126 bidders NYSE, 1970-77 Announcement

SCHOOL OF ECONOMICS AND FINANCE NOVEMBER EXAMINATION: 2007 SUBJECT, COURSE AND CODE: THE CORPORATE INVESTMENT DECISION (FINA321)

") 1 SCHOOL OF ECONOMICS AND FINANCE NOVEMBER EXAMINATION: 2007 SUBJECT, COURSE AND CODE: THE CORPORATE INVESTMENT DECISION (FINA321) EXAMINERS (INTERNAL): EXAMINER (EXTERNAL): MRS S DONNELLY MR J MASEKO,

1 SCHOOL OF ECONOMICS AND FINANCE NOVEMBER EXAMINATION: 2007 SUBJECT, COURSE AND CODE: THE CORPORATE INVESTMENT DECISION (FINA321) EXAMINERS (INTERNAL): EXAMINER (EXTERNAL): MRS S DONNELLY MR J MASEKO,

Final Examination Semester 2 / Year 2010

Southern College Kolej Selatan 南方学院 Final Examination Semester 2 / Year 2010 COURSE : COURSE CODE : FINE3003 TIME : 2 1/2 HOURS DEPARTMENT : ACCOUNTING & FINANCE, MANAGEMENT LECTURER : KAN YOKE YUE Students

Southern College Kolej Selatan 南方学院 Final Examination Semester 2 / Year 2010 COURSE : COURSE CODE : FINE3003 TIME : 2 1/2 HOURS DEPARTMENT : ACCOUNTING & FINANCE, MANAGEMENT LECTURER : KAN YOKE YUE Students

Do diversified or focused firms make better acquisitions?

Do diversified or focused firms make better acquisitions? on the 2015 American Finance Association (AFA) Meeting Program Mehmet Cihan Tulane University Sheri Tice Tulane University December 2014 ABSTRACT

Do diversified or focused firms make better acquisitions? on the 2015 American Finance Association (AFA) Meeting Program Mehmet Cihan Tulane University Sheri Tice Tulane University December 2014 ABSTRACT

Acquisitions, mergers, and takeovers terminology - Wikipedia, the free encyclopedia

Page 1 of 5 Acquisitions, mergers, and takeovers terminology From Wikipedia, the free encyclopedia The following are some concepts and terms used in acquisitions, mergers and takeovers of private and public

Page 1 of 5 Acquisitions, mergers, and takeovers terminology From Wikipedia, the free encyclopedia The following are some concepts and terms used in acquisitions, mergers and takeovers of private and public

Background p. 1 Introduction p. 3 Definitions p. 7 Valuing a Transaction p. 7 Types of Mergers p. 7 Reasons for Mergers and Acquisitions p.

Preface p. xi Background p. 1 Introduction p. 3 Definitions p. 7 Valuing a Transaction p. 7 Types of Mergers p. 7 Reasons for Mergers and Acquisitions p. 8 Merger Financing p. 8 Merger Professionals p.

Preface p. xi Background p. 1 Introduction p. 3 Definitions p. 7 Valuing a Transaction p. 7 Types of Mergers p. 7 Reasons for Mergers and Acquisitions p. 8 Merger Financing p. 8 Merger Professionals p.

Mergers & Acquisitions Juraj Sipko National Bank of Slovakia

Mergers & Acquisions Juraj Sipko National Bank of Slovakia Abstract This paper describes the past, present, and possible future development of mergers and acquisions (M&As). Based on historical data, mainly

Mergers & Acquisions Juraj Sipko National Bank of Slovakia Abstract This paper describes the past, present, and possible future development of mergers and acquisions (M&As). Based on historical data, mainly

Mergers and Acquisitions: A Strategic Valuation Approach

Mergers and Acquisitions: A Strategic Valuation Approach Mergers and Acquisitions: A Strategic Valuation Approach Emery A. Trahan Contents About This Course How to Take This Course xiii 1 An Overview

Mergers and Acquisitions: A Strategic Valuation Approach Mergers and Acquisitions: A Strategic Valuation Approach Emery A. Trahan Contents About This Course How to Take This Course xiii 1 An Overview

Characteristics of Mergers & Acquisitions A Survey on Value Creation, Synergies, and Market Cyclicality

University of Iowa Honors Theses University of Iowa Honors Program Fall 2017 Characteristics of Mergers & Acquisitions A Survey on Value Creation, Synergies, and Market Cyclicality Eric Hale Follow this

University of Iowa Honors Theses University of Iowa Honors Program Fall 2017 Characteristics of Mergers & Acquisitions A Survey on Value Creation, Synergies, and Market Cyclicality Eric Hale Follow this

OLD/PRACTICE Final Exam

OLD/PRACTICE Final Exam ADM 335 M&N Corporate Finance Professors: Kaouthar Lajili Devinder Ghandi Time: Three hours NAME: STUDENT NUMBER: SIGNATURE: GENERAL INSTRUCTIONS: Hand in everything at the end

OLD/PRACTICE Final Exam ADM 335 M&N Corporate Finance Professors: Kaouthar Lajili Devinder Ghandi Time: Three hours NAME: STUDENT NUMBER: SIGNATURE: GENERAL INSTRUCTIONS: Hand in everything at the end

The influence of the method of payment on the long-term firm performance in Dutch M&A

Bachelor s Thesis Finance The influence of the method of payment on the long-term firm performance in Dutch M&A Author: Koen de Natris ANR: s427776 Date: May 18, 2012 Supervisor: F. Urzúa Table of Contents

Bachelor s Thesis Finance The influence of the method of payment on the long-term firm performance in Dutch M&A Author: Koen de Natris ANR: s427776 Date: May 18, 2012 Supervisor: F. Urzúa Table of Contents

Market for Corporate Control: Takeovers. Nino Papiashvili Institute of Finance Ulm University

Market for Corporate Control: Takeovers Nino Papiashvili Institute of Finance Ulm University 1 Introduction Takeovers - the market for corporate control - where management teams compete with one another

Market for Corporate Control: Takeovers Nino Papiashvili Institute of Finance Ulm University 1 Introduction Takeovers - the market for corporate control - where management teams compete with one another

T.Y.B.F.M. Sem VI. Corporate Restructuring

T.Y.B.F.M Sem VI Corporate Restructuring Note- All Questions are compulsory. Marks in the bracket indicate full marks. Q. 1 (A) Fill in the blanks (Any 8) (8) 1. refers to the material consolidation of

T.Y.B.F.M Sem VI Corporate Restructuring Note- All Questions are compulsory. Marks in the bracket indicate full marks. Q. 1 (A) Fill in the blanks (Any 8) (8) 1. refers to the material consolidation of

MERGERS AND ACQUISITIONS IN U.S. AGRIBUSINESS

MERGERS AND ACQUISITIONS IN U.S. AGRIBUSINESS INTERNATIONAL FOOD AND AGRIBUSINESS MANAGEMENT ASSOCIATION ANNUAL MEETING 2015 MINNEAPOLIS SAINT PAUL, USA; JUNE 2015 Carlos O. Trejo-Pech (Universidad Panamericana

MERGERS AND ACQUISITIONS IN U.S. AGRIBUSINESS INTERNATIONAL FOOD AND AGRIBUSINESS MANAGEMENT ASSOCIATION ANNUAL MEETING 2015 MINNEAPOLIS SAINT PAUL, USA; JUNE 2015 Carlos O. Trejo-Pech (Universidad Panamericana

Mergers. Theory. Contribution

Mergers There has been research done in looking at Mergers from different perspectives. Overall the literature analyses the premium given, stock returns and goodwill. Majority of literature looks at mergers

Mergers There has been research done in looking at Mergers from different perspectives. Overall the literature analyses the premium given, stock returns and goodwill. Majority of literature looks at mergers

Financial Strategy and Valuation (FSV / SL 2) Strategic Level Pilot Paper - Suggested Answer Scheme

Strategic Level Pilot Paper - Suggested Answer Scheme") Financial Strategy and Valuation (FSV / SL 2) Strategic Level Pilot Paper - Suggested Answer Scheme PART I Question No. 01 (40 Marks) 1. Answer: Yes, I agree with the statement. Growth Business risk high

Financial Strategy and Valuation (FSV / SL 2) Strategic Level Pilot Paper - Suggested Answer Scheme PART I Question No. 01 (40 Marks) 1. Answer: Yes, I agree with the statement. Growth Business risk high

Mergers, acquisitions, and corporate restructuring: Conceptual issues 1

Mergers, acquisitions, and corporate restructuring: Conceptual issues 1 Class work: Each student attending the class, shall read this document and facilitate class discussion. He or She may further the

Mergers, acquisitions, and corporate restructuring: Conceptual issues 1 Class work: Each student attending the class, shall read this document and facilitate class discussion. He or She may further the

International Review of Law and Economics

International Review of Law and Economics 30 (2010) 186 192 Contents lists available at ScienceDirect International Review of Law and Economics Is the event study methodology useful for merger analysis?

International Review of Law and Economics 30 (2010) 186 192 Contents lists available at ScienceDirect International Review of Law and Economics Is the event study methodology useful for merger analysis?

epub WU Institutional Repository

epub WU Institutional Repository Tomaso Duso and Klaus Gugler and Burcin B. Yurtoglu Is the event study methodology useful for merger analysis? A comparison of stock market and accounting data Article

epub WU Institutional Repository Tomaso Duso and Klaus Gugler and Burcin B. Yurtoglu Is the event study methodology useful for merger analysis? A comparison of stock market and accounting data Article

Estimating Merger Synergies and the Impact on Corporate Performance An Empirical Approach. Copenhagen Business School 2014

Estimating Merger Synergies and the Impact on Corporate Performance An Empirical Approach Master s thesis Anders Elgemark MSc Applied Economics and Finance Copenhagen Business School 2014 Author: Anders

Estimating Merger Synergies and the Impact on Corporate Performance An Empirical Approach Master s thesis Anders Elgemark MSc Applied Economics and Finance Copenhagen Business School 2014 Author: Anders

Fundamentals of. Finance EDITION. Richard A. Brealey London Business School

Fundamentals of Finance EDITION Richard A. Brealey London Business School Stewart C. Myers Sloan School of Management, Massachusetts Institute of Technology Alan J. Marcus Carroll School of Management,

Fundamentals of Finance EDITION Richard A. Brealey London Business School Stewart C. Myers Sloan School of Management, Massachusetts Institute of Technology Alan J. Marcus Carroll School of Management,

How do business groups evolve? Evidence from new project announcements.

How do business groups evolve? Evidence from new project announcements. Meghana Ayyagari, Radhakrishnan Gopalan, and Vijay Yerramilli June, 2009 Abstract Using a unique data set of investment projects

How do business groups evolve? Evidence from new project announcements. Meghana Ayyagari, Radhakrishnan Gopalan, and Vijay Yerramilli June, 2009 Abstract Using a unique data set of investment projects

FIN 423/523 Takeover Defenses

FIN 423/523 Takeover Defenses Successful takeovers: target stockholders gain 20-35% or more Unsuccessful takeovers: target stockholders gain little if not eventually taken over Question: Why would target

FIN 423/523 Takeover Defenses Successful takeovers: target stockholders gain 20-35% or more Unsuccessful takeovers: target stockholders gain little if not eventually taken over Question: Why would target

MBO Financing Risks And Managers' Use Of Anti- Takeover Measures

Marquette University e-publications@marquette Finance Faculty Research and Publications Finance, Department of 7-1-2004 MBO Financing Risks And Managers' Use Of Anti- Takeover Measures Sarah Peck Marquette

Marquette University e-publications@marquette Finance Faculty Research and Publications Finance, Department of 7-1-2004 MBO Financing Risks And Managers' Use Of Anti- Takeover Measures Sarah Peck Marquette

Chapter 14 Mergers, Acquisitions, and the Valuation of Shares

Mergers, Acquisitions, and the Valuation of Shares Solutions to Even-Numbered Problems and Cases 14.2 Fashion Accessories Fashion Accessories must recently have been the subject of a rumoured hostile takeover

Mergers, Acquisitions, and the Valuation of Shares Solutions to Even-Numbered Problems and Cases 14.2 Fashion Accessories Fashion Accessories must recently have been the subject of a rumoured hostile takeover

Nike, Inc. Financial Statement Analysis CHAPTER 17

CHAPTER 17 AP Photo/Matt York Financial Statement Analysis Nike, Inc. J ust do it. These three words identify one of the most recognizable brands in the world, Nike. While this phrase inspires athletes

CHAPTER 17 AP Photo/Matt York Financial Statement Analysis Nike, Inc. J ust do it. These three words identify one of the most recognizable brands in the world, Nike. While this phrase inspires athletes

Market for corporate control and privatised utilities

Market for corporate control and privatised utilities Sanjukta Datta OU Business School Michael Young Building The Open University Walton Hall Milton Keynes MK7 6AA United Kingdom Email: s.datta@open.ac.uk

Market for corporate control and privatised utilities Sanjukta Datta OU Business School Michael Young Building The Open University Walton Hall Milton Keynes MK7 6AA United Kingdom Email: s.datta@open.ac.uk

risk free rate 7% market risk premium 4% pre-merger beta 1.3 pre-merger % debt 20% pre-merger debt r d 9% Tax rate 40%

Hager s Home Repair Company, a regional hardware chain, which specializes in do-ityourself materials and equipment rentals, is cash rich because of several consecutive good years. One of the alternative

Hager s Home Repair Company, a regional hardware chain, which specializes in do-ityourself materials and equipment rentals, is cash rich because of several consecutive good years. One of the alternative

MGT201 Financial Management Solved Subjective For Final Term Exam Preparation

MGT201 Financial Management Solved Subjective For Final Term Exam Preparation Operating lease Operating Lease offers Financing AND MAINTENANCE: often the Lessor is the Supplier / Vendor of the Asset i.e.

MGT201 Financial Management Solved Subjective For Final Term Exam Preparation Operating lease Operating Lease offers Financing AND MAINTENANCE: often the Lessor is the Supplier / Vendor of the Asset i.e.

AGGREGATE MERGER ACTIVITY AND THE BUSINESS CYCLE. A Thesis Submitted to the College of. Graduate Studies and Research

AGGREGATE MERGER ACTIVITY AND THE BUSINESS CYCLE A Thesis Submitted to the College of Graduate Studies and Research In Partial Fulfillment of the Requirements For the Degree of Master of Science In the

AGGREGATE MERGER ACTIVITY AND THE BUSINESS CYCLE A Thesis Submitted to the College of Graduate Studies and Research In Partial Fulfillment of the Requirements For the Degree of Master of Science In the

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES. Suggested Answers

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES Suggested Answers Level : Professional Subject : Corporate Financial Management Diet : December 2006 The suggested answers are published for the purpose

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES Suggested Answers Level : Professional Subject : Corporate Financial Management Diet : December 2006 The suggested answers are published for the purpose

Value Creation of Mergers and Acquisitions in IT industry before and during the Financial Crisis

Fang Chen, Suhong Li 175 Value Creation of Mergers and Acquisitions in IT industry before and during the Financial Crisis Fang Chen 1*, Suhong Li 2 1 Finance Department University of Rhode Island, Kingston,

Fang Chen, Suhong Li 175 Value Creation of Mergers and Acquisitions in IT industry before and during the Financial Crisis Fang Chen 1*, Suhong Li 2 1 Finance Department University of Rhode Island, Kingston,

Do M&As Create Value for US Financial Firms. Post the 2008 Crisis?

Do M&As Create Value for US Financial Firms Post the 2008 Crisis? By Mohammed Almutair A Research Project Submitted to Saint Mary s University, Halifax, Nova Scotia in Partial Fulfillment of the Requirements

Do M&As Create Value for US Financial Firms Post the 2008 Crisis? By Mohammed Almutair A Research Project Submitted to Saint Mary s University, Halifax, Nova Scotia in Partial Fulfillment of the Requirements

CIS March 2012 Exam Diet

CIS March 2012 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Level 2 Corporate Finance (1 13) 1. Which of the following statements

CIS March 2012 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Level 2 Corporate Finance (1 13) 1. Which of the following statements

FIRM SIZE AND THE GAINS FROM ACQUISITIONS. Sara B. Moeller, Frederik P. Schlingemann, Rene M. Stulz. Journal of Financial Economics 73 (2004)

") FIRM SIZE AND THE GAINS FROM ACQUISITIONS Sara B. Moeller, Frederik P. Schlingemann, Rene M. Stulz Journal of Financial Economics 73 (2004) 201 228 Presenter: Anh Tran 1. Introduction What is the size

FIRM SIZE AND THE GAINS FROM ACQUISITIONS Sara B. Moeller, Frederik P. Schlingemann, Rene M. Stulz Journal of Financial Economics 73 (2004) 201 228 Presenter: Anh Tran 1. Introduction What is the size

Chapter 8: Business Organizations Section 3

Chapter 8: Business Organizations Section 3 Objectives 1. Explain the characteristics of corporations. 2. Analyze the advantages of incorporation. 3. Analyze the disadvantages of incorporation. 4. Compare

Chapter 8: Business Organizations Section 3 Objectives 1. Explain the characteristics of corporations. 2. Analyze the advantages of incorporation. 3. Analyze the disadvantages of incorporation. 4. Compare

Tobin's Q and the Gains from Takeovers

THE JOURNAL OF FINANCE VOL. LXVI, NO. 1 MARCH 1991 Tobin's Q and the Gains from Takeovers HENRI SERVAES* ABSTRACT This paper analyzes the relation between takeover gains and the q ratios of targets and

THE JOURNAL OF FINANCE VOL. LXVI, NO. 1 MARCH 1991 Tobin's Q and the Gains from Takeovers HENRI SERVAES* ABSTRACT This paper analyzes the relation between takeover gains and the q ratios of targets and

A theory on merger timing and announcement returns

A theory on merger timing and announcement returns Paulo J. Pereira and Artur Rodrigues CEF.UP and Faculdade de Economia, Universidade do Porto. NIPE and School of Economics and Management, University

A theory on merger timing and announcement returns Paulo J. Pereira and Artur Rodrigues CEF.UP and Faculdade de Economia, Universidade do Porto. NIPE and School of Economics and Management, University

CHAPTER 19 RAISING CAPITAL

CHAPTER 19 RAISING CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. A company s internally generated cash flow provides a source of equity financing. For a profitable company, outside

CHAPTER 19 RAISING CAPITAL Answers to Concepts Review and Critical Thinking Questions 1. A company s internally generated cash flow provides a source of equity financing. For a profitable company, outside

Economics of Strategy Fifth Edition. Besanko, Dranove, Shanley, and Schaefer. Chapter 7. Diversification. Copyright 2010 John Wiley Sons, Inc.

Economics of Strategy Fifth Edition Besanko, Dranove, Shanley, and Schaefer Chapter 7 Diversification Slides by: Richard Ponarul, California State University, Chico Copyright 2010 John Wiley Sons, Inc.

Economics of Strategy Fifth Edition Besanko, Dranove, Shanley, and Schaefer Chapter 7 Diversification Slides by: Richard Ponarul, California State University, Chico Copyright 2010 John Wiley Sons, Inc.

Merger and acquisition wave from a macro-economic perspective

Merger and acquisition wave from a macro-economic perspective A research on explanations for the merger and acquisition wave 2004-2007 Master Thesis Finance Faculty of Economics and Business Administration

Merger and acquisition wave from a macro-economic perspective A research on explanations for the merger and acquisition wave 2004-2007 Master Thesis Finance Faculty of Economics and Business Administration

MERGERS, ACQUISITIONS, AND CORPORATE RESTRUCTURINGS

MERGERS, ACQUISITIONS, AND CORPORATE RESTRUCTURINGS FIFTH EDITION PATRICK A. GAUGHAN WILEY JOHN WILEY & SONS, INC. CONTENTS Case Study Preface xi xv Part 1 Background 1 1 Introduction 3 Recent M&A Trends

MERGERS, ACQUISITIONS, AND CORPORATE RESTRUCTURINGS FIFTH EDITION PATRICK A. GAUGHAN WILEY JOHN WILEY & SONS, INC. CONTENTS Case Study Preface xi xv Part 1 Background 1 1 Introduction 3 Recent M&A Trends

MERGER ANNOUNCEMENTS AND MARKET EFFICIENCY: DO MARKETS PREDICT SYNERGETIC GAINS FROM MERGERS PROPERLY?

MERGER ANNOUNCEMENTS AND MARKET EFFICIENCY: DO MARKETS PREDICT SYNERGETIC GAINS FROM MERGERS PROPERLY? ALOVSAT MUSLUMOV Department of Management, Dogus University. Acıbadem 81010, Istanbul / TURKEY Tel:

MERGER ANNOUNCEMENTS AND MARKET EFFICIENCY: DO MARKETS PREDICT SYNERGETIC GAINS FROM MERGERS PROPERLY? ALOVSAT MUSLUMOV Department of Management, Dogus University. Acıbadem 81010, Istanbul / TURKEY Tel:

Level 2: Study Session 09: Equity Investments: Industry and Company Analysis 160 questions.

Level 2: Study Session 09: Equity Investments: Industry and Company Analysis 160 questions. Introduction by the Author : Hi there, CFA fellows, here you are. You see, it doesn't need to be an expensive

Level 2: Study Session 09: Equity Investments: Industry and Company Analysis 160 questions. Introduction by the Author : Hi there, CFA fellows, here you are. You see, it doesn't need to be an expensive

D. Options in Capital Structure

D. Options in Capital Structure 55 The most direct applications of option pricing in capital structure decisions is in the design of securities. In fact, most complex financial instruments can be broken

D. Options in Capital Structure 55 The most direct applications of option pricing in capital structure decisions is in the design of securities. In fact, most complex financial instruments can be broken

Are Japanese Acquisitions Efficient Investments?

RIETI Discussion Paper Series 13-E-085 Are Japanese Acquisitions Efficient Investments? INOUE Kotaro Tokyo Institute of Technology NARA Saori Meiji University YAMASAKI Takashi Kobe University The Research

RIETI Discussion Paper Series 13-E-085 Are Japanese Acquisitions Efficient Investments? INOUE Kotaro Tokyo Institute of Technology NARA Saori Meiji University YAMASAKI Takashi Kobe University The Research

Online Appendix to R&D and the Incentives from Merger and Acquisition Activity *

Online Appendix to R&D and the Incentives from Merger and Acquisition Activity * Index Section 1: High bargaining power of the small firm Page 1 Section 2: Analysis of Multiple Small Firms and 1 Large

Online Appendix to R&D and the Incentives from Merger and Acquisition Activity * Index Section 1: High bargaining power of the small firm Page 1 Section 2: Analysis of Multiple Small Firms and 1 Large

M.V.S.R Engineering College. Department of Business Managment

M.V.S.R Engineering College Department of Business Managment CONCEPTS IN FINANCIAL MANAGEMENT 1. Finance. a.finance is a simple task of providing the necessary funds (money) required by the business of

M.V.S.R Engineering College Department of Business Managment CONCEPTS IN FINANCIAL MANAGEMENT 1. Finance. a.finance is a simple task of providing the necessary funds (money) required by the business of

The following learning and growth perspective measures could enhance the implementation and management of Wellgas strategy:

SECTION A CASE QUESTIONS (Total: 50 marks) Answer 1(a) Wellgas strategy is to transform a fill-the-petrol tank routine into a delightful shopping experience for service-oriented customers who are ready

SECTION A CASE QUESTIONS (Total: 50 marks) Answer 1(a) Wellgas strategy is to transform a fill-the-petrol tank routine into a delightful shopping experience for service-oriented customers who are ready

The Effect of Cross-Border Acquisitions on Shareholders Wealth in the Nordic Market

Stockholm School of Economics Department of Finance Thesis in Finance Fall 2012 The Effect of Cross-Border Acquisitions on Shareholders Wealth in the Nordic Market Abstract: This study examines the short-term

Stockholm School of Economics Department of Finance Thesis in Finance Fall 2012 The Effect of Cross-Border Acquisitions on Shareholders Wealth in the Nordic Market Abstract: This study examines the short-term

Good News for Buyers and Sellers: Acquisitions in the Lodging Industry

Cornell University School of Hotel Administration The Scholarly Commons Articles and Chapters School of Hotel Administration Collection 12-2001 Good News for Buyers and Sellers: Acquisitions in the Lodging

Cornell University School of Hotel Administration The Scholarly Commons Articles and Chapters School of Hotel Administration Collection 12-2001 Good News for Buyers and Sellers: Acquisitions in the Lodging

Taiwan. Proxy Voting Guidelines Benchmark Policy Recommendations. Effective for Meetings on or after February 1, 2016

Taiwan Proxy Voting Guidelines 2016 Benchmark Policy Recommendations Effective for Meetings on or after February 1, 2016 Published December 18, 2015 www.issgovernance.com 2015 ISS Institutional Shareholder

Taiwan Proxy Voting Guidelines 2016 Benchmark Policy Recommendations Effective for Meetings on or after February 1, 2016 Published December 18, 2015 www.issgovernance.com 2015 ISS Institutional Shareholder

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination CORPORATE FINANCIAL MANAGEMENT PILOT PAPER Marking

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination CORPORATE FINANCIAL MANAGEMENT PILOT PAPER Marking

For more information, please contact

Xiaoying, Pan (2013) The Effects of Mergers and Acquisitions on Company s Operating Performance. [Dissertation (University of Nottingham only)] (Unpublished) Access from the University of Nottingham repository:

Xiaoying, Pan (2013) The Effects of Mergers and Acquisitions on Company s Operating Performance. [Dissertation (University of Nottingham only)] (Unpublished) Access from the University of Nottingham repository:

Stock Price Behavior of Acquirers and Targets Due to M&A Announcement in USA Banking

Iranian Economic Review, Vol.17, No. 1, 2013 Stock Price Behavior of Acquirers and Targets Due to M&A Announcement in USA Banking Clay Moffett Mohammad Naserbakht Abstract T Received: 2012/09/18 Accepted:

Iranian Economic Review, Vol.17, No. 1, 2013 Stock Price Behavior of Acquirers and Targets Due to M&A Announcement in USA Banking Clay Moffett Mohammad Naserbakht Abstract T Received: 2012/09/18 Accepted:

Bribery and Corruption

Bribery and Corruption M&A Corruption Due Diligence 2018 Association of Certified Fraud Examiners, Inc. Introduction M&A transactions deal with the buying, selling, dividing, and combining of different

Bribery and Corruption M&A Corruption Due Diligence 2018 Association of Certified Fraud Examiners, Inc. Introduction M&A transactions deal with the buying, selling, dividing, and combining of different

TomTom/Tele Atlas: navigating DG COMP s decision

TomTom/Tele Atlas: navigating DG COMP s decision Prepared for the 2008 ACE annual conference Budapest Matthew Johnson, Senior Consultant Overview - Oxera s role in the case - issues - the position of Garmin

TomTom/Tele Atlas: navigating DG COMP s decision Prepared for the 2008 ACE annual conference Budapest Matthew Johnson, Senior Consultant Overview - Oxera s role in the case - issues - the position of Garmin

Mergers and acquisitions in Poland value creation in different types of transactions and the impact of culture on shareholders wealth

Mergers and acquisitions in Poland value creation in different types of transactions and the impact of culture on shareholders wealth Master Thesis MSc in Finance and International Business Authors: Sebastian

Mergers and acquisitions in Poland value creation in different types of transactions and the impact of culture on shareholders wealth Master Thesis MSc in Finance and International Business Authors: Sebastian

Final Examination Semester 1 / Year 2008

Southern College Kolej Selatan 南方学院 Final Examination Semester 1 / Year 2008 COURSE : COURSE CODE : FINE3003 TIME : 2 1/2 HOURS DEPARTMENT : MANAGEMENT LECTURER : KAN YOKE YUE Student s ID : Batch No.

Southern College Kolej Selatan 南方学院 Final Examination Semester 1 / Year 2008 COURSE : COURSE CODE : FINE3003 TIME : 2 1/2 HOURS DEPARTMENT : MANAGEMENT LECTURER : KAN YOKE YUE Student s ID : Batch No.

Sources of gains in horizontal mergers: Evidence from geographic expansion

Sources of gains in horizontal mergers: Evidence from geographic expansion Douglas Fairhurst Ryan Williams * September 2014 ABSTRACT: We use a novel measure to provide evidence on the debated source of

Sources of gains in horizontal mergers: Evidence from geographic expansion Douglas Fairhurst Ryan Williams * September 2014 ABSTRACT: We use a novel measure to provide evidence on the debated source of

An empirical examination of White Knight Corporate Takeovers: Performances and Motivations. Xing Chen. A Thesis. The John Molson School of Business

An empirical examination of White Knight Corporate Takeovers: Performances and Motivations Xing Chen A Thesis in The John Molson School of Business Presented in Partial Fulfillment of the Requirements

An empirical examination of White Knight Corporate Takeovers: Performances and Motivations Xing Chen A Thesis in The John Molson School of Business Presented in Partial Fulfillment of the Requirements

Mergers MERGERS, CORPORATE CONTROL, AND GOVERNANCE

1 CHAPTER PART 10 MERGERS, CORPORATE CONTROL, AND GOVERNANCE Mergers The scale and pace of merger activity in the United States have been remarkable. In 2006, a record year for mergers, U.S. companies

1 CHAPTER PART 10 MERGERS, CORPORATE CONTROL, AND GOVERNANCE Mergers The scale and pace of merger activity in the United States have been remarkable. In 2006, a record year for mergers, U.S. companies

Chapter 19. Financial Statement Analysis. Learning Objectives. The Annual Report Usually Contains...

PowerPoint to accompany Chapter 19 Financial Statement Analysis Learning Objectives 1. Perform a horizontal analysis of comparative financial statements 2. Perform a vertical analysis of financial statements

PowerPoint to accompany Chapter 19 Financial Statement Analysis Learning Objectives 1. Perform a horizontal analysis of comparative financial statements 2. Perform a vertical analysis of financial statements

D. Agus Harjito Faculty of Economics, Universitas Islam Indonesia

ISSN : 1410-9018 SINERGI KA JIAN BISNIS DAN MANAJEMEN Vol. 8 No. 1, Januari 2006 Hal. 1-12 THE EFFECT OF MERGER AND ACQUISITION ANNOUNCEMENTS ON STOCK PRICE BEHAVIOUR AND FINANCIAL PERFORMANCE CHANGES:

ISSN : 1410-9018 SINERGI KA JIAN BISNIS DAN MANAJEMEN Vol. 8 No. 1, Januari 2006 Hal. 1-12 THE EFFECT OF MERGER AND ACQUISITION ANNOUNCEMENTS ON STOCK PRICE BEHAVIOUR AND FINANCIAL PERFORMANCE CHANGES:

Suggested Answer_Syl2012_Dec2014_Paper_20 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2014 Paper- 20 : FINANCIAL ANALYSIS & BUSINESS VALUATION Time Allowed : 3 Hours Full Marks : 100 The figures in the margin

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2014 Paper- 20 : FINANCIAL ANALYSIS & BUSINESS VALUATION Time Allowed : 3 Hours Full Marks : 100 The figures in the margin

Restructuring Corporate America by John J. Clark, John T. Gerlach, and Gerald Oslo

Sacred Heart University Review Volume 16 Issue 1 Sacred Heart University Review, Volume XVI, Numbers 1 & 2, Fall 1995/ Spring 1996 Article 8 1996 Restructuring Corporate America by John J. Clark, John

Sacred Heart University Review Volume 16 Issue 1 Sacred Heart University Review, Volume XVI, Numbers 1 & 2, Fall 1995/ Spring 1996 Article 8 1996 Restructuring Corporate America by John J. Clark, John

A Manager's Guide to Financial Analysis

A Manager's Guide to Financial Analysis A Manager's Guide to Financial Analysis Fifth Edition Steven D. Grossman Contents About This Course How to Take This Course Introduction ix xi xiii 1 Financial

A Manager's Guide to Financial Analysis A Manager's Guide to Financial Analysis Fifth Edition Steven D. Grossman Contents About This Course How to Take This Course Introduction ix xi xiii 1 Financial

CHAPTER 25 ACQUISITIONS AND TAKEOVERS

1 CHAPTER 25 ACQUISITIONS AND TAKEOVERS Firms are acquired for a number of reasons. In the 1960s and 1970s, firms such as Gulf and Western and ITT built themselves into conglomerates by acquiring firms

1 CHAPTER 25 ACQUISITIONS AND TAKEOVERS Firms are acquired for a number of reasons. In the 1960s and 1970s, firms such as Gulf and Western and ITT built themselves into conglomerates by acquiring firms

Corporations, Mergers, and Multinationals 8.3 notes

Corporations, Mergers, and Multinationals 8.3 notes What types of corporations exist? What are the advantages of incorporation? What are the disadvantages of incorporation? How can corporations combine?

Corporations, Mergers, and Multinationals 8.3 notes What types of corporations exist? What are the advantages of incorporation? What are the disadvantages of incorporation? How can corporations combine?

The long-term operating performance of European mergers and acquisitions

The long-term operating performance of European mergers and acquisitions Finance Working Paper N. 137/2006 November 2006 Marina Martynova The University of Sheffield Management School Sjoerd Oosting Tilburg

The long-term operating performance of European mergers and acquisitions Finance Working Paper N. 137/2006 November 2006 Marina Martynova The University of Sheffield Management School Sjoerd Oosting Tilburg

Do Rejected Takeover Offers Maximize Shareholder Value? Jeff Masse. Supervised by Dr. James Parrino. Abstract

Do Rejected Takeover Offers Maximize Shareholder Value? Jeff Masse Supervised by Dr. James Parrino Abstract In the context of today s current environment of increased shareholder activism, how do shareholders

Do Rejected Takeover Offers Maximize Shareholder Value? Jeff Masse Supervised by Dr. James Parrino Abstract In the context of today s current environment of increased shareholder activism, how do shareholders

This can vary from 50.1% to 90%+ (some states don't want outsiders to control their companies)

") Execution and Legal There are 2 ways to gain control of a company: 1. Acquire enough shares to constitute control according to the laws of the state in which the target is incorporated This can vary from

Execution and Legal There are 2 ways to gain control of a company: 1. Acquire enough shares to constitute control according to the laws of the state in which the target is incorporated This can vary from

NBER WORKING PAPER SERIES DO SHAREHOLDERS OF ACQUIRING FIRMS GAIN FROM ACQUISITIONS? Sara B. Moeller Frederik P. Schlingemann René M.

NBER WORKING PAPER SERIES DO SHAREHOLDERS OF ACQUIRING FIRMS GAIN FROM ACQUISITIONS? Sara B. Moeller Frederik P. Schlingemann René M. Stulz Working Paper 9523 http://www.nber.org/papers/w9523 NATIONAL

NBER WORKING PAPER SERIES DO SHAREHOLDERS OF ACQUIRING FIRMS GAIN FROM ACQUISITIONS? Sara B. Moeller Frederik P. Schlingemann René M. Stulz Working Paper 9523 http://www.nber.org/papers/w9523 NATIONAL

TomTom Fourth Quarter and Full Year 2007 Financial Results

TomTom Fourth Quarter and Full Year 2007 Financial Results 21 February 2008 Harold Goddijn - CEO Marina Wyatt - CFO 2008 TomTom Fourth Quarter and Full Year 2007 Financial Results Disclaimer This Presentation

TomTom Fourth Quarter and Full Year 2007 Financial Results 21 February 2008 Harold Goddijn - CEO Marina Wyatt - CFO 2008 TomTom Fourth Quarter and Full Year 2007 Financial Results Disclaimer This Presentation

Do diversified or focused firms make better acquisitions?

Do diversified or focused firms make better acquisitions? March 15, 2014 Abstract This paper examines the stock market s reaction to merger and acquisition announcements to see if the market perceives

Do diversified or focused firms make better acquisitions? March 15, 2014 Abstract This paper examines the stock market s reaction to merger and acquisition announcements to see if the market perceives

Can the Source of Cash Accumulation Alter the Agency Problem of Excess Cash Holdings? Evidence from Mergers and Acquisitions ABSTRACT

Can the Source of Cash Accumulation Alter the Agency Problem of Excess Cash Holdings? Evidence from Mergers and Acquisitions ABSTRACT This study argues that the source of cash accumulation can distinguish

Can the Source of Cash Accumulation Alter the Agency Problem of Excess Cash Holdings? Evidence from Mergers and Acquisitions ABSTRACT This study argues that the source of cash accumulation can distinguish

Wealth Destruction on a Massive Scale? A Study of Acquiring-Firm Returns in the Recent Merger Wave

THE JOURNAL OF FINANCE VOL. LX, NO. 2 APRIL 2005 Wealth Destruction on a Massive Scale? A Study of Acquiring-Firm Returns in the Recent Merger Wave SARA B. MOELLER, FREDERIK P. SCHLINGEMANN, and RENÉ M.STULZ

THE JOURNAL OF FINANCE VOL. LX, NO. 2 APRIL 2005 Wealth Destruction on a Massive Scale? A Study of Acquiring-Firm Returns in the Recent Merger Wave SARA B. MOELLER, FREDERIK P. SCHLINGEMANN, and RENÉ M.STULZ

The Post-Merger Equity Value Performance of Acquiring Firms in the Hospitality Industry

Journal of Hospitality Financial Management The Professional Refereed Journal of the Association of Hospitality Financial Management Educators Volume 8 ssue 1 Article 2 2000 The Post-Merger Equity Value

Journal of Hospitality Financial Management The Professional Refereed Journal of the Association of Hospitality Financial Management Educators Volume 8 ssue 1 Article 2 2000 The Post-Merger Equity Value

TRENDS IN MERGERS AND ACQUISITIONS

TRENDS IN MERGERS AND ACQUISITIONS November 25th, 2015 Salvatore Borda 1036350 Andrea Colpani 1014473 Michael Santarossa 1036254 Nicolò Monno 1015629 Selina Nelli 1007213 2 Agenda INTRODUCTION DIFFERENCES

TRENDS IN MERGERS AND ACQUISITIONS November 25th, 2015 Salvatore Borda 1036350 Andrea Colpani 1014473 Michael Santarossa 1036254 Nicolò Monno 1015629 Selina Nelli 1007213 2 Agenda INTRODUCTION DIFFERENCES

Mil.\\3\i^\ '. IL > 'M'L ; 3 TOflO ads7tddfl 1

Mil.\\3\i^\ '. IL > 'M'L ; 3 TOflO ads7tddfl 1 WORKING PAPER ALFRED P. SLOAN SCHOOL OF MANAGEMENT AN OVERVIEW OF TAKEOVER DEFENSES by Richard S. Ruback Sloan School of Management Massachusetts Institute

Mil.\\3\i^\ '. IL > 'M'L ; 3 TOflO ads7tddfl 1 WORKING PAPER ALFRED P. SLOAN SCHOOL OF MANAGEMENT AN OVERVIEW OF TAKEOVER DEFENSES by Richard S. Ruback Sloan School of Management Massachusetts Institute

FIN 540 Interfirm Tender Offers & Mergers. Interfirm Mergers: Basic Facts

FIN 540 Interfirm Tender Offers & Mergers Payoffs to Stockholders of Target & Bidder Firms Sources of Gains/Motivations for Mergers Types of Mergers horizontal vertical conglomerate Interfirm Mergers:

FIN 540 Interfirm Tender Offers & Mergers Payoffs to Stockholders of Target & Bidder Firms Sources of Gains/Motivations for Mergers Types of Mergers horizontal vertical conglomerate Interfirm Mergers:

Link download Solutions Manual:

DOWNLOAD FULL TEST BANK FOR ADVANCED ACCOUNTING 12TH EDITION BY FISCHER TAYLOR CHENG Link download full: https://testbankservice.com/download/test-bank-for-advancedaccounting-12th-edition-by-fischer-taylor-cheng/

DOWNLOAD FULL TEST BANK FOR ADVANCED ACCOUNTING 12TH EDITION BY FISCHER TAYLOR CHENG Link download full: https://testbankservice.com/download/test-bank-for-advancedaccounting-12th-edition-by-fischer-taylor-cheng/