Mil.\\3\i^\ '. IL > 'M'L ; 3 TOflO ads7tddfl 1

|

|

|

- Camron Fisher

- 5 years ago

- Views:

Transcription

1 Mil.\\3\i^\ '. IL > 'M'L ; 3 TOflO ads7tddfl 1

2

3

4

5 WORKING PAPER ALFRED P. SLOAN SCHOOL OF MANAGEMENT AN OVERVIEW OF TAKEOVER DEFENSES by Richard S. Ruback Sloan School of Management Massachusetts Institute of Technology WP# September 1986 MASSACHUSETTS INSTITUTE OF TECHNOLOGY 50 MEMORIAL DRIVE CAMBRIDGE, MASSACHUSETTS 02139

6

7 AN OVERVIEW OF TAKEOVER DEFENSES by Richard S. Ruback Sloan School of Management Massachusetts Institute of Technology WP# September 1986

8 p-^--«i DEC

9 AN OVERVIEW OF TAKEOVER DEFENSES by Richard S. Ruback* Sloan School of Management Massachusetts Institute of Technology I. Introduction Takeover defenses include all actions by managers to resist having their firms acquired. Attempts by target managers to defeat outstanding takeover proposals are overt forms of takeover defenses. Resistance also includes actions that occur before a takeover offer is made which make the firm more difficult to acquire. The intensity of the defenses can range from mild to severe. Mild resistance forces bidders to restructure their offers, but does not prevent an acquisition or raise the takeover price substantially. Severe resistance can block takeover bids, thereby giving the incumbent managers of the target firm veto power over acquisition proposals. A natural place to begin the analysis of takeover defenses is with the wealth effects of takeovers. There is broad agreement that being a takeover target substantially increases the wealth of shareholders. Historical estimates of the stock price increases of target firms are about 20 percent in mergers and about 30 percent in tender offers. More recently, premiums have exceeded 50 percent. It does not require a lot of complicated analysis to determine that the right to sell a share of stock for 50 percent more than its previous market price benefits target shareholders.

10 At first glance, the large gains for target stockholders in takeovers seems to imply that all takeover resistance is bad. Resistance makes the firm more difficult to acquire. If the defense works, it lowers the probability of a takeover. This means that stockholders are less likely to receive takeover premiums. Even for an economist, it is hard to argue that shareholders benefit by reducing their chance to sell shares at a premium. But the issue is not that simple. Takeover resistance can benefit shareholders. Stockholders are concerned about the market value of the firm. The market value of any firm is the sum of two components: the value of the firm conditional on retaining the same management team; and the expected change in value of the firm from a corporate control change, which equals the probability of a takeover times the change in value from a takeover. Value of the Probability Change in Market value = firm with current + of a control x value from a of the firm managers change control change Stockholders are concerned about how takeover defenses affect all three components of value: the value of the firm under current managers, the probability of an acquisition, and the offer price if a takeover bid occurs. While takeover defenses may lower the probability of being acquired, they may also increase the offer price. Furthermore, takeover defenses can affect the value of the firm even if it isn't acquired, that is, the value with its incumbent management team. For example, consider a defense that allows incumbent managers to completely block all takeover bids. This would reduce the probability of a control change to zero and eliminate the

11 expected takeover premium. The market price of the firm would then consist entirely of the value with its incumbent managers. This value arguably could be affected in two opposite ways by the takeover defense. First, the value could decrease as managers enjoy the leisure that the isolation from being fired provides. Second, the value could increase as managers stop wasting time and corporate resources worrying about a hostile takeover. It is difficult to determine a priori whether takeover defenses are good or bad for stockholders. But one way to assess a takeover defenses is to examine the rationale for resistance. Managers resist takeovers for three broad reasons: (1) they believe the firm has hidden values; (2) they believe resistance will increase the offer price; and (3) they want to retain their positions. 1. Managers believe the firm as hidden values : The management of most corporations have private information about the future prospects of the firm. This information usually includes plans, strategies, ideas, patents, and similar items that cannot be made public. Even if they are efficient, market prices cannot include the value of information that the market doesn't have. When assessing a takeover bid, managers compare the offer price to their estimate of value of the firm. Their estimate, of course, includes the value of the private information that they possess. When the inside information is favorable, the managers' per share assessment of value will exceed the market price of the firm's stock. Offer prices above the market price of the stock could be below the managers' assessment of value. In such cases, managers would help stockholders by actively opposing the offer.

12 Opposition based on "hidden values" is in the shareholders' interests only when the private information is valuable. A problem is that the general optimism of managers about the future of their firms clouds their perception of values. Host top managers usually argue that their firms are under-valued by the market. Managers believe the market is systematically inefficient - it always underestimates the value of their firm. But this optimism, or distrust of market prices, is an insufficient basis to oppose takeover bids. To qualify as a potential stockholder wealth increasing reason to oppose takeovers, the inside information must be of the type that an investor would pay to obtain. 2. Managers believe resistance will increase the offer price : In most transactions in which there is disagreement about value, it pays to haggle about price. Corporate takeovers are no exception. In mergers, the managers of the target and bidding firms negotiate directly. In tender offers, however, the haggling generally occurs in the newspapers. The bidder circumvents the target's managers by making an offer directly to the shareholders. The target shareholders, therefore, lack a centralized bargaining agent. But takeover defenses can help: by making takeovers more difficult, resistance can slow down a bidder. This gives potential competing bidders the opportunity to enter the auction for the target firm. The most common form of this behavior is soliciting an offer from a "white knight" after a hostile takeover bid. This auction seems to increase the final offer prices for target shares. Ruback (1983) reports that the final offer price exceeded the

find that stockholder gains are substantially greater when there are multiple bids.")

13 initial offer by 23 percent in 48 competitive tender offers during More recently, Bradley, Desai, and Kim (1986) find that stockholder gains are substantially greater when there are multiple bids. They report gains of 24 percent for targets in single bidder tender offers and gains of 2 41 percent for targets in multiple bidder contests. Since takeover defenses can encourage competitive bidders to make an offer, these data provide some support for the view that resistance leads to higher offer prices. Some managers use this rationale to adopt extreme antitakeover defenses that virtually prevent hostile tender offers. They argue that without the board as a centralized bargaining agent, shareholders will sell out at too low a price. Such a view presumes that the market for corporate control is uncompetitive and inefficient. The weight of scientific evidence and the casual observation of control contests suggests that such a view is incorrect. Furthermore, extreme forms of takeover defenses can have some relatively severe side-effects because it prevents the removal of inefficient managers. 3. Managers want to retain their positions : If the bidding firm plans to replace the target's incumbent managers, the target's managers have little incentive to endorse the takeover proposal. Such an endorsement would guarantee that they would lose the power, prestige, and value of the organization-specific human capital associated with their positions. In addition to the desire to retain their positions, managers are likely to have the natural belief that they are the best managers of the firm. Loyalty to employees also encourages resistance. Finally, being

14 . taken over can be considered a sign of failure: the premium indicates that the bidder believes it can manage the firm better than the incumbent managers In summary, takeover resistance motivated by first rationale of hidden values and the second rationale of inducing an auction can benefit target shareholders. However, the managers' natural bias is likely to result in opposition to some takeovers that would benefit target shareholders. The third reason for takeover defenses, managerial self-interest, benefits the stockholders only if resistance happens by chance to be the appropriate action for one of the first two reasons. These three reasons for takeover defenses are not mutually exclusive; combinations of the three are often present in defense strategies. For example, managers may use takeover defenses because they prefer friendly, negotiated transactions. This combines elements of the three reasons for takeover defenses. Negotiated acquisitions enable the target managers to share ideas and information with the bidding firm. Consistent with the first and second reasons, this may increase the offer price. It also increases the chances of retaining the target's management team, which is consistent with the third reason. Finally, a negotiated transaction is generally more civilized: to the managers that is like an increase in compensation. There is very little general evidence to assess the overall impact of takeover resistance on stockholder values. However, Walkling and Long (1984) present some intriguing evidence: managers with large stockholdings in their firms are less likely to oppose takeovers than managers with small

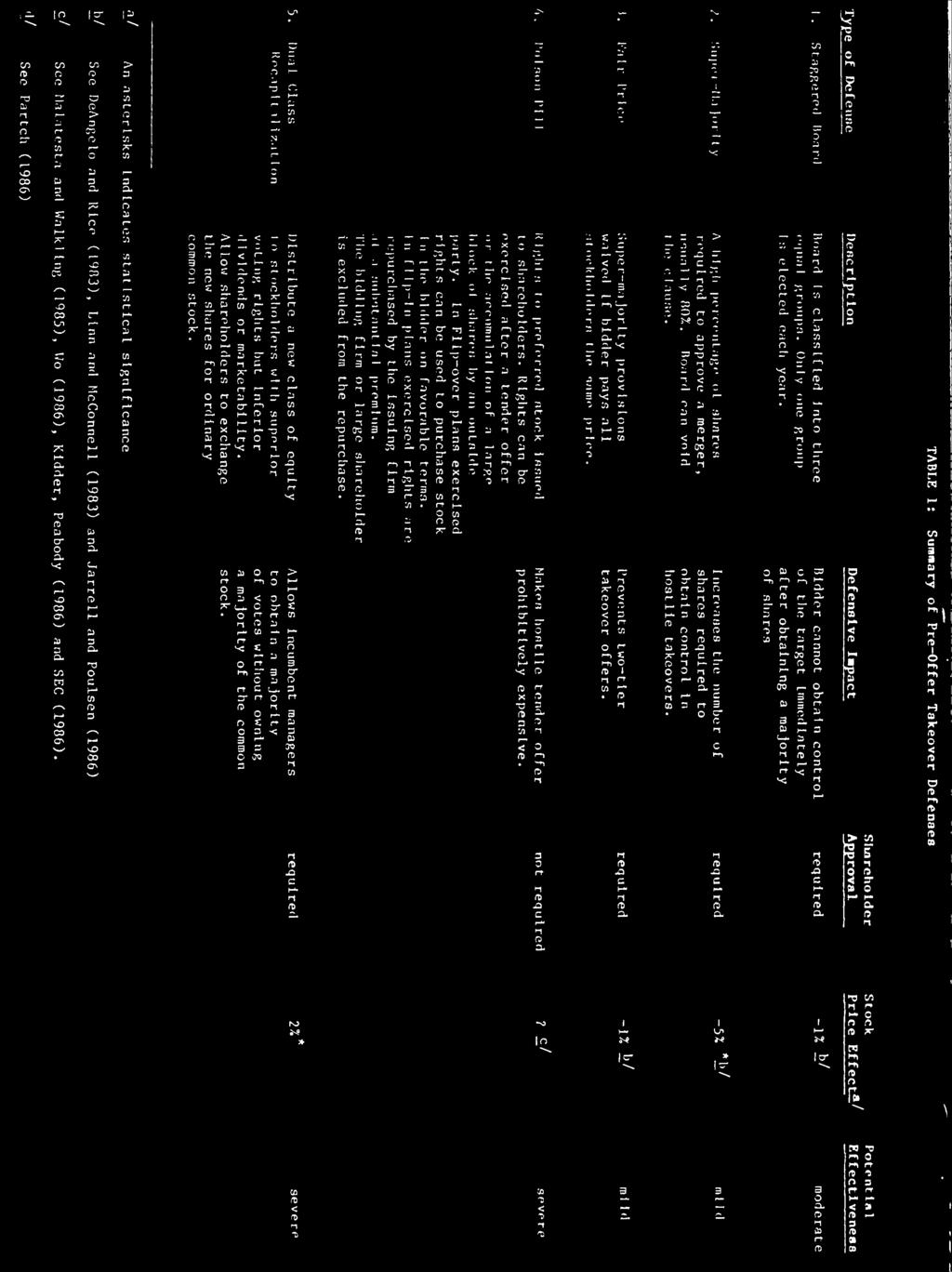

15 stockholdings. These data can be interpreted in two ways: either managers with large stockholdings oppose to little because of the risk of losing the big payoff from being acquired; or managers with small stockholdings oppose too much, because they care about their jobs and have no equity gains to offset the loss in compensation. While not resolving whether there is too much or too little opposition, the Walkling and Long study does suggest the importance of the effect of takeovers on managers in the decision process. The stock price evidence tends to focus on individual types of defensive actions. In the next section, I explain and evaluate pre-offer defenses. Section 3 does the same for post-offer defenses Pre-offer Takeover Defenses In this section I describe several types of takeover defenses that occur prior to an actual takeover bid. These defenses are summarized in Table 1. The table contains a brief description of the defense and its defensive impact, whether shareholder approval is required, the stock price effect, and its potential effectiveness. The stock price effects are my round number summary of the detailed empirical studies. An asterisks indicates statistical significance. The potential effectiveness measure in Table 1 is intended to capture the degree to which the defense would be effective, assuming that the incumbent management team uses it fully. I have described defenses as mild when they inconvenience bidders or force them to restructure their bids without raising the takeover price significantly. Severe defenses give the incumbent managers absolute veto power of corporate control changes.

16 The potential effectiveness rating will differ from the stock price effect in at least three of the circumstances. First, the market may believe that the courts will prevent the incumbent managers from using the device, so that a very effective device will be associated with a small stock price effect. Second, the stock price effect might be small for an effective device because the adoption was anticipated. Third, the stock price effect could be small because the change in the probability of being acquired, and thus the change in expected premium, is too small to be reliably measured for even a very effective device. This is most likely to occur when the firm is not the subject of takeover speculation. 1. Staggered board elections : In this corporate charter provision, the board of directors is classified into three groups. Each year only one of the groups, or one-third of the directors, is elected. This makes it difficult for a hostile bidder to gain immediate control of the target firm, even if the bidder owns a majority of the common stock. About one-half of Standard & Poors 500 firms have adopted this type of takeover defense. My estimate of the stock price effect of adopting a staggered board is -1 percent, which is not statistically significant. DeAngelo and Rice (1983) examine the stock returns for 100 firms that adopted antitakeover corporate charter amendments; 53 of these included staggered boards. They find no significant stock price response to the adoption of the amendments around the proxy mailing date. Similarly, Linn and McConnell (1983) find no stock price effects for a sample of 388 antitakeover amendments around the proxy mailing date. However, they find significantly positive returns over the interval from the proxy mailing date to the stockholder meeting date.

17 More recently, Jarrell and Poulsen (1986) report negative, but insignificant returns of about -1 percent for 28 firms that adopted classified boards since Staggered boards are a moderately effective takeover defense. By preventing a majority holder from obtaining control of the board for two years, this defense hinders the bidder's ability to make significant changes in the corporation immediately. This limitation may in turn reduce the bidder's willingness to bid, and may increase the bidder's difficulty in getting financing. 2. Super-maiority provisions : These corporate charter provisions require a very high percentage of shares to approve a merger, usually 80 percent. These provisions are also typically accompanied by lock-in provisions that require a super-majority to change the antitakeover provisions. Some supermajority provisions apply to all mergers. Others are only applied at the board's discretion to takeovers that they oppose or that involve a large stockholder. Hostile takeover bidders require a higher percentage of shares to obtain control of the target firm when the firm has a super-majority amendment. The samples of antitakeover amendments examined by DeAngelo and Rice (1983) and Linn and McConnell (1983) both included super-majority provisions. Both studies found no significant negative stock price effects. But Jarrell and Poulson (1986) argue that these earlier amendments did not generally include an escape clause for the board. They report that supermajority amendments with escape clauses are associated with a statistically significant return of -5 percent, whereas super-majority amendments without

18 10 escape clauses are associated with insignificant returns of -1 percent. In spite of the significant stock price response, I consider a supermajority amendment a mild takeover defense. Bidders can respond to this amendment by simply tendering for the whole firm. This need not increase the total cost of the acquisition. Without super-majority amendment, a partial offer could be used to obtain control. In this case, all stockholders would tender and receive a weighted average of the offer price and the post-expiration price. The bidder can respond to the super-majority amendment by simply offering this average price to all shareholders. 3. Fair Price Amendments : In these corporate charter changes, a fair price is defined as the same price. That is, a super-majority provision is waived if the bidder pays all stockholders the same price. About 35 percent of firms have these amendments. Fair price amendments are designed to prevent two-tier takeover offers. In such offers, the bidding firm makes a first-tier tender offer for a fraction of the target's common stock. The tender offer includes provisions for a second-tier merger. The merger price in the second-tier is substantially below the first-tier tender offer price. This provides an incentive for stockholders to tender to receive the highest price. Since most stockholders tender, and since the bidder accepts shares on a pro-rata basis, most shareholders get a weighted average of the first and second tier offer prices, or the blended price. Jarrell and Poulson (1986) report insignificant stock price changes of percent for 143 fair price amendments. Consistent with this insignificant stock price effect, fair price amendments are a mild takeover

19 11 defense. By requiring the same price for all shares, the bidder is forced to offer all shareholders the blended price. This restructures the offer, but does not raise the cost of acquiring the target. 4. Poison Pills : These are preferred stock rights plans adopted by the board of directors; shareholder approval is not generally required. However, the plans usually use "blank check preferred stock", which are securities authorized by stockholders whose terms are determined by the board prior to the issuance of the security. In a poison pill, rights to preferred stock are issued to stockholders. The rights are inactive until they are triggered. A triggering event occurs when a tender offer is made for a large fraction of the firm, usually 30 percent, or after a single shareholder accumulates a large block of the firm, usually 20 percent. The triggered rights can be redeemed by the board of directors for a short time after the triggering event occurs. If the rights are not redeemed, they can be exercised. There are two different plans for dealing their exercised rights: flip-over plans and flip-in plans. In flip-over plans the exercised rights are used to purchase preferred stock, for, say, $100. The preferred stock is then convertible into $200 of equity in the bidding firm in the event of a merger. The primary effect of this plan is to raise the minimum offer price that shareholders would accept in a tender offer. For example, suppose a target's stock price was $50. Shareholders would choose not to tender their shares for any offer price less than the $150 payoff they would get from exercising the right ($50 of stock plus $200 of equity in the bidder minus the $100 cost of exercising). The minimum premium, therefore, is 200 percent.

20 12 In flip-in plans, the rights are repurchased from the shareholders by the issuing firm at a substantial premium, usually 100 percent. That is, the $100 of preferred stock would be repurchased for $200. The triggering firm that made the offer, or the triggering large shareholder, is excluded from the repurchase. This repurchase price sets a lower bound on the minimum offer price that shareholders will accept. It also dilutes the value of the bidding firm's equity position in the target. Flip-in plans often contain flip-over provision that are effective for mergers. Poison pills are relatively recent phenomena. Prior to the Delaware Chancery Court decision in 1985 that upheld the legality of the plans, there were only three such plans. Currently, there are over 200 poison pill plans. Because these plans are so new, there is limited empirical evidence on them. In a study of 12 early plans, Malatesta and Walkling (1985) find negative abnormal returns associated with the adoption of poison pills. Ho (1986) finds no abnormal returns for a sample of 23 poison pills. The SEC's Study of 37 pills find returns of -1 percent for all pills and larger negative returns for firms that were subject to takeover speculation. A study of 167 poison pills by Kidder, Peabody, Inc. finds no stock price impact. But this study is methodologically flawed, so that it's conclusions are unreliable. The impact of these plans, therefore, is currently unknown. Both forms of poison pills are severe takeover defenses. These plans have the potential to insulate incumbent managers completely from hostile takeovers. The plans cannot be circumvented by restructuring bids. Flip-in plans are slightly more effective than flip-over plans because they prevent the creeping acquisitions of the type Sir James Goldsmith used in his attack

21 13 on Crown-Zellerbach. 5. Dual Class Recapitalizations : These plans restructure the equity of the firm into two classes with different voting rights. Usually, the class with inferior voting rights has one vote per share and the class with superior voting rights has 10 votes per share. The superior voting stock is typically distributed to shareholders. It can then be exchanged for ordinary common stock. The superior voting stock generally has lower dividend or reduced marketability; this induces stockholders to exchange their superior voting stock for inferior voting common stock. The managers of the firm do not participate in the exchange. This shifts the voting power of the corporation. Managers with relatively small equity holdings can control a majority of the votes after the recapitalization. This gives managers veto rights over control changes. Firms with dual class equity are relatively rare. Partch (1986) reports that 43 firms issued limited voting stock over the period of However, recently the New York Stock Exchange has requested permission from the SEC to change their one share, one vote rule to allow NYSE firms to adopt such dual class equity structures. These recapitalizations, therefore, could become much more common in the near future. The empirical evidence presented by Partch (1986) is mixed. She reports a significant positive return of about 2 percent for the 43 firms that adopted dual class plans. However, there are about as many increases as decreases in stock prices and the median is only about one-half of one percent. She concludes that the weight of the evidence suggests no

22 14 significant stock price changes. Furthermore, these historical estimates may not be relevant for assessing the impact of a dual class recapitalization for a typical firm. As Partch emphasizes, the firms in her sample are atypical. They generally have substantial inside or family ownership; on average the managerial ownership was 49 percent of the firm prior to the recapitalization. Thus, the plans may not have substantially changed the probability of being taken over for these firms. The managers' approval would be required with or without the dual class equity. Dual class recapitalizations can be very effective takeover devices. By concentrating voting power in the hands of incumbent managers, the device prevents bidders from obtaining control by tendering for the outside shares. Even if a bidder was successful in acquiring all of the outside equity, it would not have sufficient votes to replace the incumbent managers or merge with the target. Ill. Post-Offer Takeover Defenses After a bidder makes a hostile tender offer, the defensive actions include many of the pre-offer defenses, as well as several actions that can be directed at a specific bidder. Table 2 summarizes these post-offer defensive responses. 1. Targeted Repurchases; These transactions, popularly called greenmail, occur when a firm buys a block of its common stock held by a single shareholder or a group of shareholders. The repurchase is often at a premium, and the repurchase offer is not extended to other shareholders. Targeted repurchases can be used as a takeover defense by offering an inducement to a bidder to cease the offer and sell its shares back to the

, Bradley and Wakeman (1983), and Mikkelson and Ruback (1985a, 1986) report significant stock returns of about -3 percent at the announcement of the")

23 is issuing firm at a profit. However, evidence presented by Mikkelson and Ruback (1986) indicates that only about five percent of 111 repurchases occurred after the announcement of a takeover attempt. About one-third of the repurchases occurred after some less overt form of attempts to change control, such as preliminary plans for an acquisition attempt or proxy contests. Since twothirds of targeted repurchases do not involve' any indication of a brewing control contest, the classification of these transactions as takeover defenses is questionable. Empirical studies by Dann and DeAngelo (1983), Bradley and Wakeman (1983), and Mikkelson and Ruback (1985a, 1986) report significant stock returns of about -3 percent at the announcement of the targeted repurchase. But Mikkelson and Ruback (1986) report that this loss is more than offset by stock price increases associated with the initial purchase of the block and other intervening events. The negative stock price reaction to the targeted repurchase announcement, therefore, seems to be caused by the reversal of takeover expectations formed at the initial investment. Overall, the total return associated with these transactions, including the initial investment, intervening events and targeted repurchase is 7 percent, which is statistically significant. Consistent with this positive overall stock price effect, repurchasing firms seem to have a higher frequency of control changes subsequent to the targeted repurchase. 2. Standstill Agreements : These agreements limit the ownership by a given firm for a specified period of time. The agreement may involve allocating a number on seats on the board of directors to the large shareholder. Also,

24 16 the shareholder may agree to vote with management. These agreements serve as a takeover defense by eliminating, at least temporarily, a potential bidder. The shareholder may, however, gain some control over corporate assets through seats on the board. Thus, a standstill agreement is more like a treaty than a defense. Empirical results by Dann and DeAngelo (1983) show that the adoption of standstill agreements are associated with a significant fall in stock prices of about -4 percent. Furthermore, Mikkelson and Ruback (1986) find that the negative returns in response to targeted repurchases are much greater when they are accompanied by standstill agreements. These agreements, therefore, seem to reduce the wealth of target stockholders. But this stock price fall could just reflect the market's disappointment that an expected takeover will not occur. Like the targeted repurchase finding, the negative returns may just represent the reversal of favorable expectations. 3. Litigation : Perhaps the most common form of post-offer defense is to file some sort of suit against the bidding firm. Jarrell (1985) reports such litigation occurs in about one-third of all tender offers between 1962 and The suits charge the bidder firms with fraud, violation of anti-, trust or securities regulations, and so on. The litigation seems to serve two purposes. First, it delays the bidder, thereby encouraging the entry of competing bidders. Consistent with their view, Jarrell reports that the frequency of competing bids in 62 percent for tender offers involving litigation and 11 percent in tender offers without litigation. Second, the litigation encourages the bidder to raise the offer price to induce the target to drop the suit and thereby

le. 4. Acquisitions and Divestitures : These changes in the firm's asset structure can be used to defend against a takeover bid.")

25 17 avoid legal expenses. Jarrell reports that the stock price effect associated with the filing the suit is about zero, on average, for 71 such litigations. This suggests that the defense is roughly a fair gan±)le. 4. Acquisitions and Divestitures : These changes in the firm's asset structure can be used to defend against a takeover bid. Such tactics include divesting an asset that the bidder wants, buying assets that the bidder doesn't want, or buying assets that will create anti-trust or other regulatory problems. Each of these actions make the target less attractive to the bidding firm, and reduces the price the bidder is willing to pay for the target. Data provided by Dann and DeAnglelo (1986) for 20 such transactions indicate that they reduce stock prices by about 2 percent, which is statistically significant. 5. Liability Restructuring : Issuing voting securities can increase the number of shares required by a hostile bidder. Typically, the firm places these voting securities in friendly hands that agree to support the incumbent managers. Repurchase can also be used to reduce the number of public shares, making it more difficult to buy enough shares to obtain control. These repurchases are often financed by debt issues that may make the firm less attractive to potential bidders. These restructures seem to reduce stockholder wealth. Dann and DeAngelo (1986) report stock price declines of 2 percent on average for 31 such restructures. IV. Conclusions I wish I could conclude that takeover defenses are generally good or bad for stockholders. But the answer is not that simple. Furthermore, there isn't enough evidence of experience with takeover defenses for precise

26 18 conclusions. I do, however, think that the analysis and evidence support three propositions. First, defenses that give incumbent managers the power to veto hostile takeovers seem to be harmful. Of course, there are circumstances where such defenses can help stockholders, but I think those circumstances are relatively rare. Poison pills and dual class recapitalizations are cause for particular concern. There may be a way to circumvent the power that the incumbent managers have with these defenses, but no one has discovered it yet. Second, defenses that destroy assets are probably bad. This category includes asset sales below their values or asset purchases above their values that are executed simply to thwart a takeover. Similarly, liability restructuring to the extent it interferes with investment also destroys assets. Once again there are circumstances where such actions may help stockholders, but these cases are very rare. Third, defenses which do not give managers veto power and do not destroy assets, such as antitakeover corporate charter changes, are probably not harmful. These defenses may cause bidders to restructure offers. They may even result in slightly higher offer prices. Their major cost is that the defenses will reduce the benefit from being an acquiring firm and thereby reduce takeover activity. However, there is no evidence that the frequency of takeovers has been reduced by antitakeover corporate charter amendments. In summary, some takeover defenses seem to be harmful. Perhaps not surprisingly, the most harmful tactics seem to be the most recent

27 19 innovations, such as poison pills. This is disturbing because these defenses are not subject to shareholder vote and thus are especially difficult to control. Of course, they may just seem powerful because participants in the market have not yet had the opportunity to design tactics to circumvent the defenses.

for a review of the evidence on takeovers.")

for a more detailed discussion of management compensation and takeovers. See also Lewellen, Loderer, and Rosenfeld (1985).")

28 20 FOOTNOTES * I would like to thank Paul Healy, James Poterba, and Nancy Rose for comments on previous drafts. The support of the National Science Foundation Grant #SES is gratefully acknowledged. See Jensen and Ruback (1983) for a review of the evidence on takeovers. The stock returns are measured over the interval beginning five days before the first offer and ending 40 days after it. See Hikkelson and Ruback (1985b) for a more detailed discussion of management compensation and takeovers. See also Lewellen, Loderer, and Rosenfeld (1985). Frequency estimates are based on data published by the Investor Responsibility Research Center, Inc. See Easterbrook and Fishel (1981a 1981b), Gilson (1982), Bebchuk (1982a, b), and Ruback (1984).

: 275-300.")

29 : 2i REFERENCES Bebchuk, Lucian. 1982a. "The Case for Facilitating Competing Tender Offers; A Reply and Extension" Stanford Law Review. Bebchuk, Lucian. 1982b. "The Case for Facilitating Competing Tender Offers" Harvard Law Review. Bradley, Michael and L. Macdonald Wakeman "The Wealth Effects of Targeted Share Repurchases" Journal of Financial Economics (April): Dann, Larry Y., and Harry DeAngleo "Corporate Financial Policy and Corporate Control: A Study of Defensive Adjustments in Asset and Ownership Structure" Managerial Economics Research Center of the University of Rochester Working Paper (August). Dann, Larry Y. and Harry DeAngelo "Standstill Agreements, Privately Negotiated Stock Repurchases and the Market for Corporate Control" Journal of Financial Economics (April): DeAngelo, Harry and Edward M. Rice "Antitakeover Charter Amendments and Stockholder Wealth" Journal of Financial Economics (April)

: 1733-1750. Gilson, Ronald J. 1982.")

30 . 22 Easterbrook, Frank H. and Daniel R. Fischel. 1981a. "The Proper Role of a Target's Management in Responding to a Tender Offer" Harvard Law Review (April): Easterbrook, Frank H. and Daniel R. Fischel. 1981b. "Takeover Bids, Defensive Tactics, and Shareholders' Welfare" Business Lawyer (July): Gilson, Ronald J "Seeking Competitive Bids Versus Pure Passivity in Tender Offer Defense" Stanford Law Review. Ho, Michael J "Share Rights Plans: Poison Pill, Placebo, or Suicide Tablet?" Massachusetts Institute of Technology Sloan School of Management, Masters Thesis (February). Jarrell, Gregg A "The Wealth Effects of Litigating by Targets: Do Interests Diverge in a Merge?" Journal of Law and Economics (April): Jarrell, Gregg A. and Annette B. Poulsen "Shark Repellents and Stock Prices: The Effects of Antitakeover Amendments Since 1980" mimeo (August)

. Lambert, Richard A. and David F. Larker. 1985.")

.")

31 23 Jensen, Michael C., and Richard S. Ruback "The Market for Corporate Control: The Scientific Evidence" Journal of Financial Economics (April): Kidder, Peabody and Company "Impact of Adoption of Stockholder Rights Plans on Stock Price" (June). Lambert, Richard A. and David F. Larker "Golden Parachutes, Executive Decision-Making and Shareholder Wealth" Journal of Accounting and Economics 7: Lewellen, Wilbur, Claudio Loderer, and Ahron Rosenfeld "Merger Decisions and Executive Stock Ownership in Acquiring Firms" Journal of Accounting and Economics (April): Malatesta, Paul H, and Ralph A. Walkling "The Impact of 'Poison Pill' Securities on Stockholder Wealth" Working Paper, University of Washington (July). Mikkelson, Wayne and Richard S. Ruback. 1985a. "An Empirical Analysis of the Interfirm Equity Investment Process" Journal of Financial Economics (December):

. Partch, Megan. 1986.")

. Ruback, Richard S. 1983. \"Assessing Competition in the Market for Corporate Acquisitions\" Journal of Financial Economics, 11, (April): 141-153.")

32 24 Mikkelson, Wayne H. and Richard S. Ruback. 1985b. "Takeovers and Managerial Compensation: A Discussion" Journal of Financial Economics (December): Mikkelson, Wayne and Richard S. Ruback "Targeted Repurchases and Common Stock Returns" Working Paper, Massachusetts Institute of Technology, Sloan School of Management # , (June). Partch, Megan "The Creation of a Class of Limited Voting Common Stock and Shareholder Wealth" Working Paper, University of Oregon. (May). The Office of the Chief Economist Securities and Exchange Commission "The Economics of Poison Pills" (March). Ruback, Richard S "Assessing Competition in the Market for Corporate Acquisitions" Journal of Financial Economics, 11, (April): Ruback, Richard S "An Economic View of the Market for Corporate Control" Delaware Journal of Corporate Law 9, (May-August):

33 25 Walkling, R. A. and M. S. Long "Agency Theory, Managerial Welfare and Takeover Bid Resistance" Rand Journal of E conomics. 15, (Spring):

34 I- n I- en

35 ire (6 n 3 n > s ro re 0) re o, CO re ro a. > 3 CO re cr 00 ro re 3 3 re > 3 re > 3 rr re en TT 3 a. ro o en cr rr I- n I- C I O rr rr ^ C I CO CO?3 m CD rr c n 3 09 TO 0) O s

36 238^ 062

37

38

39

40 y ',^. tw^ ' St Date D ue a- 'i-'% Wki 5J9flJj.^0^^ Lib-26-67

41 Mil IIBRARIFS nilpi? 3 TOflD DD57TD0fl 1

42 :L,!i.l.l!,i!MliLiliJ!! ^j^ ^ iiftihiwyihmihiiiamiiii iiiilih.j.aa iiiwa fj-wihi luaiimdhiiililimtiiymia^

Chapter URL:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Mergers and Acquisitions Volume Author/Editor: Alan J. Auerbach, ed. Volume Publisher: University

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Mergers and Acquisitions Volume Author/Editor: Alan J. Auerbach, ed. Volume Publisher: University

WORKING PAPER MASSACHUSETTS

BASEMENT HD28.M414 no. Ibll- Dewey ALFRED P. WORKING PAPER SLOAN SCHOOL OF MANAGEMENT Corporate Investments In Common Stock by Wayne H. Mikkelson University of Oregon Richard S. Ruback Massachusetts

BASEMENT HD28.M414 no. Ibll- Dewey ALFRED P. WORKING PAPER SLOAN SCHOOL OF MANAGEMENT Corporate Investments In Common Stock by Wayne H. Mikkelson University of Oregon Richard S. Ruback Massachusetts

FIN 423/523 Takeover Defenses

FIN 423/523 Takeover Defenses Successful takeovers: target stockholders gain 20-35% or more Unsuccessful takeovers: target stockholders gain little if not eventually taken over Question: Why would target

FIN 423/523 Takeover Defenses Successful takeovers: target stockholders gain 20-35% or more Unsuccessful takeovers: target stockholders gain little if not eventually taken over Question: Why would target

Tobin's Q and the Gains from Takeovers

THE JOURNAL OF FINANCE VOL. LXVI, NO. 1 MARCH 1991 Tobin's Q and the Gains from Takeovers HENRI SERVAES* ABSTRACT This paper analyzes the relation between takeover gains and the q ratios of targets and

THE JOURNAL OF FINANCE VOL. LXVI, NO. 1 MARCH 1991 Tobin's Q and the Gains from Takeovers HENRI SERVAES* ABSTRACT This paper analyzes the relation between takeover gains and the q ratios of targets and

Mergers, Acquisitions and Divestures

Session 11 &12 Mergers, Acquisitions and Divestures Programme : Postgraduate Diploma in Business, Finance & Strategy (PGDBFS 2018) Course : Corporate Valuation (PGDBFS 203) Lecturer : Mr. Asanka Ranasinghe

Session 11 &12 Mergers, Acquisitions and Divestures Programme : Postgraduate Diploma in Business, Finance & Strategy (PGDBFS 2018) Course : Corporate Valuation (PGDBFS 203) Lecturer : Mr. Asanka Ranasinghe

Chapter 23 Mergers and Acquisitions

T23.1 Chapter Outline Chapter Organization Chapter 23 Mergers and Acquisitions! 23.1 The Legal Forms of Acquisitions! 23.2 Taxes and Acquisitions! 23.3 Accounting for Acquisitions! 23.4 Gains from Acquisition!

T23.1 Chapter Outline Chapter Organization Chapter 23 Mergers and Acquisitions! 23.1 The Legal Forms of Acquisitions! 23.2 Taxes and Acquisitions! 23.3 Accounting for Acquisitions! 23.4 Gains from Acquisition!

DODGE & COX FUNDS PROXY VOTING POLICIES AND PROCEDURES. Revised February 15, 2018

DODGE & COX FUNDS PROXY VOTING POLICIES AND PROCEDURES Revised February 15, 2018 The Dodge & Cox Funds have authorized Dodge & Cox to vote proxies on behalf of the Dodge & Cox Funds pursuant to the following

DODGE & COX FUNDS PROXY VOTING POLICIES AND PROCEDURES Revised February 15, 2018 The Dodge & Cox Funds have authorized Dodge & Cox to vote proxies on behalf of the Dodge & Cox Funds pursuant to the following

Volume Title: Corporate Takeovers: Causes and Consequences. Volume URL:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Corporate Takeovers: Causes and Consequences Volume Author/Editor: Alan J. Auerbach, ed.

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Corporate Takeovers: Causes and Consequences Volume Author/Editor: Alan J. Auerbach, ed.

Mergers, Acquisitions and Divestures

Session 11 &12 Mergers, Acquisitions and Divestures Programme : Postgraduate Diploma in Business, Finance & Strategy (PGDBFS 2017) Course : Corporate Valuation (PGDBFS 203) Lecturer : Mr. Asanka Ranasinghe

Session 11 &12 Mergers, Acquisitions and Divestures Programme : Postgraduate Diploma in Business, Finance & Strategy (PGDBFS 2017) Course : Corporate Valuation (PGDBFS 203) Lecturer : Mr. Asanka Ranasinghe

M&A with Golden Parachutes and Network Effects*

M&A with Golden Parachutes and Network Effects Jeong Hun Oh ABSTRACT In this paper, using game model, we show that the network effects from M&A in ICT sector can generate abnormal returns in the market.

M&A with Golden Parachutes and Network Effects Jeong Hun Oh ABSTRACT In this paper, using game model, we show that the network effects from M&A in ICT sector can generate abnormal returns in the market.

What Investment Managers Need to Know About Charters and Bylaws

Published in the June edition of ISSue Alert (Vol. 14, No. 6). Reprinted with the permission of Institutional Shareholder Services, a Thomson Financial company. What Investment Managers Need to Know About

Published in the June edition of ISSue Alert (Vol. 14, No. 6). Reprinted with the permission of Institutional Shareholder Services, a Thomson Financial company. What Investment Managers Need to Know About

MERGER & CONSOLIDATION: OVERVIEW

MERGER & CONSOLIDATION: OVERVIEW Merger: A contractual and statutory process by : (1) which one corporation (the surviving corporation) acquires all of the assets and liabilities of another corporation

MERGER & CONSOLIDATION: OVERVIEW Merger: A contractual and statutory process by : (1) which one corporation (the surviving corporation) acquires all of the assets and liabilities of another corporation

FIN 423 M&A Strategy. Dodd (JFE, 1980): Successful & Unsuccessful Mergers

: Successful & Unsuccessful Mergers") Successful & unsuccessful mergers & tender offers Sharks White Knights winners losers FIN 423 M&A Strategy Dodd (JFE, 1980): Successful & Unsuccessful Mergers 151 targets, 126 bidders NYSE, 1970-77 Announcement

Successful & unsuccessful mergers & tender offers Sharks White Knights winners losers FIN 423 M&A Strategy Dodd (JFE, 1980): Successful & Unsuccessful Mergers 151 targets, 126 bidders NYSE, 1970-77 Announcement

Market for Corporate Control: Takeovers. Nino Papiashvili Institute of Finance Ulm University

Market for Corporate Control: Takeovers Nino Papiashvili Institute of Finance Ulm University 1 Introduction Takeovers - the market for corporate control - where management teams compete with one another

Market for Corporate Control: Takeovers Nino Papiashvili Institute of Finance Ulm University 1 Introduction Takeovers - the market for corporate control - where management teams compete with one another

Antitakeover amendments and managerial entrenchment: New evidence from investment policy and CEO compensation

University of Massachusetts Boston From the SelectedWorks of Atreya Chakraborty January 1, 2010 Antitakeover amendments and managerial entrenchment: New evidence from investment policy and CEO compensation

University of Massachusetts Boston From the SelectedWorks of Atreya Chakraborty January 1, 2010 Antitakeover amendments and managerial entrenchment: New evidence from investment policy and CEO compensation

Some Puzzles. Stock Splits

Some Puzzles Stock Splits When stock splits are announced, stock prices go up by 2-3 percent. Some of this is explained by the fact that stock splits are often accompanied by an increase in dividends.

Some Puzzles Stock Splits When stock splits are announced, stock prices go up by 2-3 percent. Some of this is explained by the fact that stock splits are often accompanied by an increase in dividends.

WORKING PAPER MASSACHUSETTS

BASEMEN, HD28.M414 \o.inoi- WORKING PAPER ALFRED P. SLOAN SCHOOL OF MANAGEMENT Targeted Repurchases eind Common Stock Retxirns Wayne H. Mikkelson College of Business Administration Richard S. Ruback

BASEMEN, HD28.M414 \o.inoi- WORKING PAPER ALFRED P. SLOAN SCHOOL OF MANAGEMENT Targeted Repurchases eind Common Stock Retxirns Wayne H. Mikkelson College of Business Administration Richard S. Ruback

Privately Negotiated Repurchases and Monitoring by Block Shareholders

Privately Negotiated Repurchases and Monitoring by Block Shareholders Murali Jagannathan College of Management Binghamton University Binghamton, NY 607.777.4639 Muralij@binghamton.edu Clifford Stephens

Privately Negotiated Repurchases and Monitoring by Block Shareholders Murali Jagannathan College of Management Binghamton University Binghamton, NY 607.777.4639 Muralij@binghamton.edu Clifford Stephens

Good News for Buyers and Sellers: Acquisitions in the Lodging Industry

Cornell University School of Hotel Administration The Scholarly Commons Articles and Chapters School of Hotel Administration Collection 12-2001 Good News for Buyers and Sellers: Acquisitions in the Lodging

Cornell University School of Hotel Administration The Scholarly Commons Articles and Chapters School of Hotel Administration Collection 12-2001 Good News for Buyers and Sellers: Acquisitions in the Lodging

CHAPTER 29. Corporate Governance. Chapter Synopsis

CHAPTER 29 Corporate Governance Chapter Synopsis 29.1 Corporate Governance and Agency Costs Corporate governance is the system of controls, regulations, and incentives designed to maximize firm value and

CHAPTER 29 Corporate Governance Chapter Synopsis 29.1 Corporate Governance and Agency Costs Corporate governance is the system of controls, regulations, and incentives designed to maximize firm value and

Do Rejected Takeover Offers Maximize Shareholder Value? Jeff Masse. Supervised by Dr. James Parrino. Abstract

Do Rejected Takeover Offers Maximize Shareholder Value? Jeff Masse Supervised by Dr. James Parrino Abstract In the context of today s current environment of increased shareholder activism, how do shareholders

Do Rejected Takeover Offers Maximize Shareholder Value? Jeff Masse Supervised by Dr. James Parrino Abstract In the context of today s current environment of increased shareholder activism, how do shareholders

IN THE FACE OF AN UNSOLICITED BID

IN THE FACE OF AN UNSOLICITED BID Given the significant decline in share prices, hostile bids are on the rise. At the same time, many companies are under increased pressure from shareholder activists to

IN THE FACE OF AN UNSOLICITED BID Given the significant decline in share prices, hostile bids are on the rise. At the same time, many companies are under increased pressure from shareholder activists to

Managerial compensation and the threat of takeover

Journal of Financial Economics 47 (1998) 219 239 Managerial compensation and the threat of takeover Anup Agrawal*, Charles R. Knoeber College of Management, North Carolina State University, Raleigh, NC

Journal of Financial Economics 47 (1998) 219 239 Managerial compensation and the threat of takeover Anup Agrawal*, Charles R. Knoeber College of Management, North Carolina State University, Raleigh, NC

MBO Financing Risks And Managers' Use Of Anti- Takeover Measures

Marquette University e-publications@marquette Finance Faculty Research and Publications Finance, Department of 7-1-2004 MBO Financing Risks And Managers' Use Of Anti- Takeover Measures Sarah Peck Marquette

Marquette University e-publications@marquette Finance Faculty Research and Publications Finance, Department of 7-1-2004 MBO Financing Risks And Managers' Use Of Anti- Takeover Measures Sarah Peck Marquette

Appendix: The Disciplinary Motive for Takeovers A Review of the Empirical Evidence

Appendix: The Disciplinary Motive for Takeovers A Review of the Empirical Evidence Anup Agrawal Culverhouse College of Business University of Alabama Tuscaloosa, AL 35487-0224 Jeffrey F. Jaffe Department

Appendix: The Disciplinary Motive for Takeovers A Review of the Empirical Evidence Anup Agrawal Culverhouse College of Business University of Alabama Tuscaloosa, AL 35487-0224 Jeffrey F. Jaffe Department

Mergers and Acquisitions

Takeovers Takeover: transfers the control right of the firm from one group to another Merger Mergers and Acquisitions Acquisition Acquisition of Stock, 2018 Takeovers Proxy Contest Going Private Acquisition

Takeovers Takeover: transfers the control right of the firm from one group to another Merger Mergers and Acquisitions Acquisition Acquisition of Stock, 2018 Takeovers Proxy Contest Going Private Acquisition

WORKING PAPER SLOAN SCHOOL OF MANAGEMENT MASSACHUSETTS ALFRED P. CAMBRIDGE, MASSACHUSETTS Dewey INSTITUTE OF TECHNOLOGY 50 MEMORIAL DRIVE

HD28.M414 Dewey rvo.(6 7'^~ c. a ALFRED P. WORKING PAPER SLOAN SCHOOL OF MANAGEMENT An Empirical Analysis of the Interfirm Equity Investment Process by Wayne H. Mikkelson University of Oregon Richard S.

HD28.M414 Dewey rvo.(6 7'^~ c. a ALFRED P. WORKING PAPER SLOAN SCHOOL OF MANAGEMENT An Empirical Analysis of the Interfirm Equity Investment Process by Wayne H. Mikkelson University of Oregon Richard S.

Lecture 8 (Notes by Leora Schiff) The Law of Mergers and Acquisitions (Spring 2003) - Prof. John Akula

The Law of Mergers and Acquisitions (Spring 2003) - Prof. John Akula") Lecture 8 (Notes by Leora Schiff) 15.649 - The Law of Mergers and Acquisitions (Spring 2003) - Prof. John Akula Sarbanes-Oxley I. New Rules for Directors and Officers a. CEO/CFO certifications i. Section

Lecture 8 (Notes by Leora Schiff) 15.649 - The Law of Mergers and Acquisitions (Spring 2003) - Prof. John Akula Sarbanes-Oxley I. New Rules for Directors and Officers a. CEO/CFO certifications i. Section

FIN 423 Corp Fin'l Policy & Control Poison pills. Poison or Placebo? Evidence on the Deterrence and Wealth Effects of Modern Antitakeover Measures

Poison or Placebo? Evidence on the Deterrence and Wealth Effects of Modern Antitakeover Measures Robert Comment and G. William Schwert Takeover Rate (Left Scale) 2.5% 2.0% Death of the M&A Market 1.5%

Poison or Placebo? Evidence on the Deterrence and Wealth Effects of Modern Antitakeover Measures Robert Comment and G. William Schwert Takeover Rate (Left Scale) 2.5% 2.0% Death of the M&A Market 1.5%

Journal of Financial and Strategic Decisions Volume 11 Number 2 Fall 1998 THE INFORMATION CONTENT OF THE ADOPTION OF CLASSIFIED BOARD PROVISIONS

Journal of Financial and Strategic Decisions Volume 11 Number 2 Fall 1998 THE INFORMATION CONTENT OF THE ADOPTION OF CLASSIFIED BOARD PROVISIONS Philip H. Siegel * and Khondkar E. Karim * Abstract The

Journal of Financial and Strategic Decisions Volume 11 Number 2 Fall 1998 THE INFORMATION CONTENT OF THE ADOPTION OF CLASSIFIED BOARD PROVISIONS Philip H. Siegel * and Khondkar E. Karim * Abstract The

SHAREHOLDERS & CORPORATE CONTROL

SHAREHOLDERS & CORPORATE CONTROL DATA SPOTLIGHT David F. Larcker and Brian Tayan Corporate Governance Research Initiative Stanford Graduate School of Business SHAREHOLDER PROPOSALS Shareholders are active

SHAREHOLDERS & CORPORATE CONTROL DATA SPOTLIGHT David F. Larcker and Brian Tayan Corporate Governance Research Initiative Stanford Graduate School of Business SHAREHOLDER PROPOSALS Shareholders are active

FIN 514 Poison or Placebo? Evidence on the Deterrence and Wealth Effects of Modern Antitakeover Measures Robert Comment and G.

FIN 514 Poison or Placebo? Evidence on the Deterrence and Wealth Effects of Modern Antitakeover Measures Robert Comment and G. William Schwert 2.5% Death of the M&A Market 2.0% Takeover Rate (%) 1.5% 1.0%

FIN 514 Poison or Placebo? Evidence on the Deterrence and Wealth Effects of Modern Antitakeover Measures Robert Comment and G. William Schwert 2.5% Death of the M&A Market 2.0% Takeover Rate (%) 1.5% 1.0%

Are Walsh and Seward's (1990) Dimensions for

Dimensions for") Faculty Working Paper 93-0114 Are Walsh and Seward's (1990) Dimensions for Classifying Antitakeover Defenses Critical from a Stockholder Wealth Perspective? An Empirical Examination James M. Mahoney Wharton

Faculty Working Paper 93-0114 Are Walsh and Seward's (1990) Dimensions for Classifying Antitakeover Defenses Critical from a Stockholder Wealth Perspective? An Empirical Examination James M. Mahoney Wharton

Do Golden Parachutes Increase Shareholders Wealth in the M&A between ICT Companies?*

International Telecommunications Policy Review, Vol.19 No.1 (2012. 3) pp.1-14 Do Golden Parachutes Increase Shareholders Wealth in the M&A between ICT Companies? Jeong Hun Oh ABSTRACT In this paper, using

International Telecommunications Policy Review, Vol.19 No.1 (2012. 3) pp.1-14 Do Golden Parachutes Increase Shareholders Wealth in the M&A between ICT Companies? Jeong Hun Oh ABSTRACT In this paper, using

CORPORATE CONTROL EVENTS EB434 ENTERPRISE GOVERNANCE

CORPORATE CONTROL EVENTS 16 EB434 ENTERPRISE GOVERNANCE corporate control events Open market purchases on the stock market Tender offer offer made directly to shareholders (often by law, to all shareholders

CORPORATE CONTROL EVENTS 16 EB434 ENTERPRISE GOVERNANCE corporate control events Open market purchases on the stock market Tender offer offer made directly to shareholders (often by law, to all shareholders

Board Declassification and Bargaining Power *

Board Declassification and Bargaining Power * Miroslava Straska School of Business, Virginia Commonwealth University, 301 W. Main Street, Richmond, VA 23220 mstraska@vcu.edu (804) 828-1741 H. Gregory Waller

Board Declassification and Bargaining Power * Miroslava Straska School of Business, Virginia Commonwealth University, 301 W. Main Street, Richmond, VA 23220 mstraska@vcu.edu (804) 828-1741 H. Gregory Waller

Acquisitions, mergers, and takeovers terminology - Wikipedia, the free encyclopedia

Page 1 of 5 Acquisitions, mergers, and takeovers terminology From Wikipedia, the free encyclopedia The following are some concepts and terms used in acquisitions, mergers and takeovers of private and public

Page 1 of 5 Acquisitions, mergers, and takeovers terminology From Wikipedia, the free encyclopedia The following are some concepts and terms used in acquisitions, mergers and takeovers of private and public

FIN 514 Markup Pricing

FIN 514 Markup Pricing Questions: Why do target stock prices rise before public offers? Does this affect the final price of the acquisition? Why? Takeover Premiums Usually Include Some Period of Prebid

FIN 514 Markup Pricing Questions: Why do target stock prices rise before public offers? Does this affect the final price of the acquisition? Why? Takeover Premiums Usually Include Some Period of Prebid

FIN 540 Poison or Placebo?

FIN 540 Poison or Placebo? Evidence on the Deterrence and Wealth Effects of Modern Antitakeover Measures Robert Comment and G. William Schwert Death of the M&A Market Fig. 1. Monthly time-series plot of

FIN 540 Poison or Placebo? Evidence on the Deterrence and Wealth Effects of Modern Antitakeover Measures Robert Comment and G. William Schwert Death of the M&A Market Fig. 1. Monthly time-series plot of

Long Term Performance of Divesting Firms and the Effect of Managerial Ownership. Robert C. Hanson

Long Term Performance of Divesting Firms and the Effect of Managerial Ownership Robert C. Hanson Department of Finance and CIS College of Business Eastern Michigan University Ypsilanti, MI 48197 Moon H.

Long Term Performance of Divesting Firms and the Effect of Managerial Ownership Robert C. Hanson Department of Finance and CIS College of Business Eastern Michigan University Ypsilanti, MI 48197 Moon H.

The Rise of Nanny Corporations

March 3, 2011 The Rise of Nanny Corporations Author: David M. Grinberg This article was originally published in the February 25, 2011 issues of the Los Angeles Daily Journal and San Francisco Daily Journal

March 3, 2011 The Rise of Nanny Corporations Author: David M. Grinberg This article was originally published in the February 25, 2011 issues of the Los Angeles Daily Journal and San Francisco Daily Journal

Journal Of Financial And Strategic Decisions Volume 10 Number 3 Fall 1997

Journal Of Financial And Strategic Decisions Volume 0 Number 3 Fall 997 EVENT RISK BOND COVENANTS AND SHAREHOLDER WEALTH: EVIDENCE FROM CONVERTIBLE BONDS Terrill R. Keasler *, Delbert C. Goff * and Steven

Journal Of Financial And Strategic Decisions Volume 0 Number 3 Fall 997 EVENT RISK BOND COVENANTS AND SHAREHOLDER WEALTH: EVIDENCE FROM CONVERTIBLE BONDS Terrill R. Keasler *, Delbert C. Goff * and Steven

Golden Parachutes Research Spotlight

Golden Parachutes Research Spotlight David F. Larcker and Brian Tayan Corporate Governance Research Initiative Stanford Graduate School of Business Key Concepts Golden parachute: Compensation paid upon

Golden Parachutes Research Spotlight David F. Larcker and Brian Tayan Corporate Governance Research Initiative Stanford Graduate School of Business Key Concepts Golden parachute: Compensation paid upon

Background p. 1 Introduction p. 3 Definitions p. 7 Valuing a Transaction p. 7 Types of Mergers p. 7 Reasons for Mergers and Acquisitions p.

Preface p. xi Background p. 1 Introduction p. 3 Definitions p. 7 Valuing a Transaction p. 7 Types of Mergers p. 7 Reasons for Mergers and Acquisitions p. 8 Merger Financing p. 8 Merger Professionals p.

Preface p. xi Background p. 1 Introduction p. 3 Definitions p. 7 Valuing a Transaction p. 7 Types of Mergers p. 7 Reasons for Mergers and Acquisitions p. 8 Merger Financing p. 8 Merger Professionals p.

Chapter 025 Mergers and Acquisitions

Multiple Choice Questions 1. The complete absorption of one company by another, wherein the acquiring firm retains its identity and the acquired firm ceases to exist as a separate entity, is called a:

Multiple Choice Questions 1. The complete absorption of one company by another, wherein the acquiring firm retains its identity and the acquired firm ceases to exist as a separate entity, is called a:

Selectica v. Versata: Delaware Chancery Court Upholds Poison Pill Shareholder Rights Plan with 4.99% Triggering Threshold Designed to Protect NOLs

March 2010 Selectica v. Versata: Delaware Chancery Court Upholds Poison Pill Shareholder Rights Plan with 4.99% Triggering Threshold Designed to Protect NOLs COURT ACKNOWLEDGES RISK OF LOSING COMPANY S

March 2010 Selectica v. Versata: Delaware Chancery Court Upholds Poison Pill Shareholder Rights Plan with 4.99% Triggering Threshold Designed to Protect NOLs COURT ACKNOWLEDGES RISK OF LOSING COMPANY S

The Board s Role in Merger and Acquisition Transactions

The Board s Role in Merger and Acquisition Transactions American Bankers Association Annual Convention Director Boot Camp Nashville, Tennessee October 16, 2016 John J. Gorman, Esq. Lawrence M. F. Spaccasi,

The Board s Role in Merger and Acquisition Transactions American Bankers Association Annual Convention Director Boot Camp Nashville, Tennessee October 16, 2016 John J. Gorman, Esq. Lawrence M. F. Spaccasi,

MERGER ANNOUNCEMENTS AND MARKET EFFICIENCY: DO MARKETS PREDICT SYNERGETIC GAINS FROM MERGERS PROPERLY?

MERGER ANNOUNCEMENTS AND MARKET EFFICIENCY: DO MARKETS PREDICT SYNERGETIC GAINS FROM MERGERS PROPERLY? ALOVSAT MUSLUMOV Department of Management, Dogus University. Acıbadem 81010, Istanbul / TURKEY Tel:

MERGER ANNOUNCEMENTS AND MARKET EFFICIENCY: DO MARKETS PREDICT SYNERGETIC GAINS FROM MERGERS PROPERLY? ALOVSAT MUSLUMOV Department of Management, Dogus University. Acıbadem 81010, Istanbul / TURKEY Tel:

Avenue Investment Management Proxy Policy and Corporate Governance

Avenue Investment Management Inc. Avenue Investment Management Proxy Policy and Corporate Governance We know that shareholders rightfully look to Avenue Investment Management to be responsive to matters

Avenue Investment Management Inc. Avenue Investment Management Proxy Policy and Corporate Governance We know that shareholders rightfully look to Avenue Investment Management to be responsive to matters

Corporate Governance Data and Measures Revisited

Corporate Governance Data and Measures Revisited David F. Larcker Stanford Graduate School of Business Peter C. Reiss Stanford Graduate School of Business Youfei Xiao Duke University, Fuqua School of Business

Corporate Governance Data and Measures Revisited David F. Larcker Stanford Graduate School of Business Peter C. Reiss Stanford Graduate School of Business Youfei Xiao Duke University, Fuqua School of Business

Mergers & Acquisitions

Mergers & Acquisitions Topics Covered Sensible Motives for Mergers Some Dubious Reasons for Mergers Estimating Merger Gains and Costs The Mechanics of a Merger Proxy Fights, Takeovers, and the Market for

Mergers & Acquisitions Topics Covered Sensible Motives for Mergers Some Dubious Reasons for Mergers Estimating Merger Gains and Costs The Mechanics of a Merger Proxy Fights, Takeovers, and the Market for

FIN Corp Fin'l Policy & Control: Selling Seasoned Equity. Why Sell Seasoned Equity? Why Sell Seasoned Equity? (cont.)

") FIN 423 -- Corp Fin'l Policy & Control: Selling Seasoned Equity Underwritten Offerings Shelf Registration Rights Offerings Dividend Reinvestment Plans Private Placements Why Sell Seasoned Equity? 1. Raise

FIN 423 -- Corp Fin'l Policy & Control: Selling Seasoned Equity Underwritten Offerings Shelf Registration Rights Offerings Dividend Reinvestment Plans Private Placements Why Sell Seasoned Equity? 1. Raise

Debt, Debt Structure and Corporate Performance after Unsuccessful Takeovers: Evidence from Target Firms that Remain Independent.

Debt, Debt Structure and Corporate Performance after Unsuccessful Takeovers: Evidence from Target Firms that Remain Independent January 12, 2004 Abstract: Significant increases in the level of target leverage

Debt, Debt Structure and Corporate Performance after Unsuccessful Takeovers: Evidence from Target Firms that Remain Independent January 12, 2004 Abstract: Significant increases in the level of target leverage

Note that there is an overlap between the T/F and multiple-choice questions, as some of the T/F statements are used in multiple-choice questions.

Fundamentals of Financial Management 14th Edition Brigham Houston TEST BANK Complete download test bank for Fundamentals of Financial Management 14th Edition Brigham https://testbankarea.com/download/test-bank-fundamentals-financialmanagement-14th-edition-brigham-houston/

Fundamentals of Financial Management 14th Edition Brigham Houston TEST BANK Complete download test bank for Fundamentals of Financial Management 14th Edition Brigham https://testbankarea.com/download/test-bank-fundamentals-financialmanagement-14th-edition-brigham-houston/

Security Capital Research & Management Incorporated Proxy Voting Procedures and Guidelines. April 1, 2017

Security Capital Research & Management Incorporated Proxy Voting Procedures and Guidelines April 1, 2017 Table of Contents Part I: Security Capital Proxy-Voting Procedures A. Objective 3 B. Proxy Committee.

Security Capital Research & Management Incorporated Proxy Voting Procedures and Guidelines April 1, 2017 Table of Contents Part I: Security Capital Proxy-Voting Procedures A. Objective 3 B. Proxy Committee.

Stock Price Behavior of Acquirers and Targets Due to M&A Announcement in USA Banking

Iranian Economic Review, Vol.17, No. 1, 2013 Stock Price Behavior of Acquirers and Targets Due to M&A Announcement in USA Banking Clay Moffett Mohammad Naserbakht Abstract T Received: 2012/09/18 Accepted:

Iranian Economic Review, Vol.17, No. 1, 2013 Stock Price Behavior of Acquirers and Targets Due to M&A Announcement in USA Banking Clay Moffett Mohammad Naserbakht Abstract T Received: 2012/09/18 Accepted:

Topics in Corporate Finance. Chapter 9: Mergers and Acquisitions. Albert Banal-Estanol

Topics in Corporate Finance Chapter 9: Mergers and Acquisitions Merger activity in the US during the past century Mergers in Europe Mergers come in waves and are procyclical This chapter s Plan Evidence

Topics in Corporate Finance Chapter 9: Mergers and Acquisitions Merger activity in the US during the past century Mergers in Europe Mergers come in waves and are procyclical This chapter s Plan Evidence

Austria Treasury Shares Guide IBA Corporate and M&A Law Committee 2014

Austria Treasury Shares Guide IBA Corporate and M&A Law Committee 2014 Contact Christian Herbst Schönherr Attorneys at Law, Vienna ch.herbst@schoenherr.eu Contents Page INTRODUCTION 2 GENERAL OVERVIEW

Austria Treasury Shares Guide IBA Corporate and M&A Law Committee 2014 Contact Christian Herbst Schönherr Attorneys at Law, Vienna ch.herbst@schoenherr.eu Contents Page INTRODUCTION 2 GENERAL OVERVIEW

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Corporate Takeovers: Causes and Consequences Volume Author/Editor: Alan J. Auerbach, ed.

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Corporate Takeovers: Causes and Consequences Volume Author/Editor: Alan J. Auerbach, ed.

MGMT 165: Corporate Finance

MGMT 165: Corporate Finance Corporate Governance Fanis Tsoulouhas UC Merced Fanis Tsoulouhas (UCM) Lectures 1 and 2 1 / 20 Moral Hazard The fundamental problem in corporate governance is a principal-agent

MGMT 165: Corporate Finance Corporate Governance Fanis Tsoulouhas UC Merced Fanis Tsoulouhas (UCM) Lectures 1 and 2 1 / 20 Moral Hazard The fundamental problem in corporate governance is a principal-agent

Managerial Entrenchment and Valuation Effects of. Toehold Acquisitions

Managerial Entrenchment and Valuation Effects of Toehold Acquisitions Ki Beom Binh, Jeongsun Yun Abstract This paper examines the market reactions to toehold acquisitions to determine whether and under

Managerial Entrenchment and Valuation Effects of Toehold Acquisitions Ki Beom Binh, Jeongsun Yun Abstract This paper examines the market reactions to toehold acquisitions to determine whether and under

Marketability, Control, and the Pricing of Block Shares

Marketability, Control, and the Pricing of Block Shares Zhangkai Huang * and Xingzhong Xu Guanghua School of Management Peking University Abstract Unlike in other countries, negotiated block shares have

Marketability, Control, and the Pricing of Block Shares Zhangkai Huang * and Xingzhong Xu Guanghua School of Management Peking University Abstract Unlike in other countries, negotiated block shares have

Classified boards, firm value, and managerial entrenchment $

Journal of Financial Economics 83 (2007) 501 529 www.elsevier.com/locate/jfec Classified boards, firm value, and managerial entrenchment $ Olubunmi Faleye College of Business Administration, Northeastern

Journal of Financial Economics 83 (2007) 501 529 www.elsevier.com/locate/jfec Classified boards, firm value, and managerial entrenchment $ Olubunmi Faleye College of Business Administration, Northeastern

Takeover bids and target directors incentives: the impact of a bid on directors wealth and board seats

Takeover bids and target directors incentives: the impact of a bid on directors wealth and board seats Jarrad Harford * School of Business Administration University of Washington Seattle, WA 98195 206.543.4796

Takeover bids and target directors incentives: the impact of a bid on directors wealth and board seats Jarrad Harford * School of Business Administration University of Washington Seattle, WA 98195 206.543.4796

The Gains from Contracting with Equity. Myron B. Slovin Department of Finance Louisiana State University Baton Rouge, LA 70803

The Gains from Contracting with Equity by Myron B. Slovin Department of Finance Louisiana State University Baton Rouge, LA 70803 Marie E. Sushka Department of Finance Arizona State University Tempe, AZ

The Gains from Contracting with Equity by Myron B. Slovin Department of Finance Louisiana State University Baton Rouge, LA 70803 Marie E. Sushka Department of Finance Arizona State University Tempe, AZ

A Baker s Dozen 13 Defensive Takeover Measures Available to Closed-End Investment Companies Organized as Delaware Statutory Trusts

Vol. 17, No. 11 November 2010 A Baker s Dozen 13 Defensive Takeover Measures Available to Closed-End Investment Companies Organized as Delaware Statutory Trusts By: Eric A. Mazie, Michael D. Allen and

Vol. 17, No. 11 November 2010 A Baker s Dozen 13 Defensive Takeover Measures Available to Closed-End Investment Companies Organized as Delaware Statutory Trusts By: Eric A. Mazie, Michael D. Allen and

UK managed funds trading around M&A announcements

UK managed funds trading around M&A announcements By Raymond da Silva Rosa* Minh Huong To** & Terry Walter*** Abstract We test UK fund managers stock selection ability by investigating if they revise their

UK managed funds trading around M&A announcements By Raymond da Silva Rosa* Minh Huong To** & Terry Walter*** Abstract We test UK fund managers stock selection ability by investigating if they revise their

This can vary from 50.1% to 90%+ (some states don't want outsiders to control their companies)

") Execution and Legal There are 2 ways to gain control of a company: 1. Acquire enough shares to constitute control according to the laws of the state in which the target is incorporated This can vary from

Execution and Legal There are 2 ways to gain control of a company: 1. Acquire enough shares to constitute control according to the laws of the state in which the target is incorporated This can vary from

Vanguard's proxy voting guidelines

Vanguard's proxy voting guidelines The Board of Trustees (the Board) of each Vanguard fund has adopted proxy voting procedures and guidelines to govern proxy voting by the fund. The Board has delegated

Vanguard's proxy voting guidelines The Board of Trustees (the Board) of each Vanguard fund has adopted proxy voting procedures and guidelines to govern proxy voting by the fund. The Board has delegated

FIN 540 Interfirm Tender Offers & Mergers. Interfirm Mergers: Basic Facts

FIN 540 Interfirm Tender Offers & Mergers Payoffs to Stockholders of Target & Bidder Firms Sources of Gains/Motivations for Mergers Types of Mergers horizontal vertical conglomerate Interfirm Mergers:

FIN 540 Interfirm Tender Offers & Mergers Payoffs to Stockholders of Target & Bidder Firms Sources of Gains/Motivations for Mergers Types of Mergers horizontal vertical conglomerate Interfirm Mergers:

INVESTORS & ACTIVISM. David F. Larcker and Brian Tayan Corporate Governance Research Initiative Stanford Graduate School of Business

INVESTORS & ACTIVISM David F. Larcker and Brian Tayan Corporate Governance Research Initiative Stanford Graduate School of Business THE ROLE OF SHAREHOLDERS The shareholder-centric view holds that the

INVESTORS & ACTIVISM David F. Larcker and Brian Tayan Corporate Governance Research Initiative Stanford Graduate School of Business THE ROLE OF SHAREHOLDERS The shareholder-centric view holds that the

Board Classification and Managerial Entrenchment: Evidence from the Market for Corporate Control

Board Classification and Managerial Entrenchment: Evidence from the Market for Corporate Control Thomas W. Bates * Department of Finance Eller College of Management University of Arizona P.O. Box 210108

Board Classification and Managerial Entrenchment: Evidence from the Market for Corporate Control Thomas W. Bates * Department of Finance Eller College of Management University of Arizona P.O. Box 210108

ECON 4245 Economics of the Firm

ECON 4245 Economics of the Firm Lecturer: Tore Nilssen, office ES 1216, tore.nilssen@econ.uio.no Seminars: Diderik Lund, office ES 1130, diderik.lund@econ.uio.no 13 lectures; 6 seminars (in two groups)

ECON 4245 Economics of the Firm Lecturer: Tore Nilssen, office ES 1216, tore.nilssen@econ.uio.no Seminars: Diderik Lund, office ES 1130, diderik.lund@econ.uio.no 13 lectures; 6 seminars (in two groups)

Poison Pills, Optimal Contracting and the Market for Corporate Control: Evidence from Fortune 500 Firms

Poison Pills, Optimal Contracting and the Market for Corporate Control: Evidence from Fortune 500 Firms Atreya Chakraborty and Christopher F. Baum Graduate School of International Economics and Finance,

Poison Pills, Optimal Contracting and the Market for Corporate Control: Evidence from Fortune 500 Firms Atreya Chakraborty and Christopher F. Baum Graduate School of International Economics and Finance,

Chapter 1 Introduction to Business Combinations and the Conceptual Framework

Chapter 1 Introduction to Business Combinations and the Conceptual Framework Multiple Choice 1. Stock given as consideration for a business combination is valued at a. fair market value b. par value c.

Chapter 1 Introduction to Business Combinations and the Conceptual Framework Multiple Choice 1. Stock given as consideration for a business combination is valued at a. fair market value b. par value c.

2017 AGGREGATE PROXY VOTING SUMMARY

2017 AGGREGATE PROXY VOTING SUMMARY In this report, we summarize our proxy voting record for the 12-month period ended June 30, 2017 (the Reporting Period ). Our goal is to highlight some of the critical

2017 AGGREGATE PROXY VOTING SUMMARY In this report, we summarize our proxy voting record for the 12-month period ended June 30, 2017 (the Reporting Period ). Our goal is to highlight some of the critical

Delaware Supreme Court Upholds Validity of "NOL" Rights Plan

Delaware Supreme Court Upholds Validity of "NOL" Rights Plan But Cautions That, Under a Unocal Analysis, "Context Determines Reasonableness" By Robert Reder, Alison Fraser and Josh Weiss of Milbank, Tweed,

Delaware Supreme Court Upholds Validity of "NOL" Rights Plan But Cautions That, Under a Unocal Analysis, "Context Determines Reasonableness" By Robert Reder, Alison Fraser and Josh Weiss of Milbank, Tweed,

Introduction to Corporate Governance

Introduction to Corporate Governance Presented by the Corporate Governance Committee and the Young Lawyer Committee July 28, 2016 Bruce Dravis, Partner, Downey Brand LLP Ashley Gault, Associate, Roetzel

Introduction to Corporate Governance Presented by the Corporate Governance Committee and the Young Lawyer Committee July 28, 2016 Bruce Dravis, Partner, Downey Brand LLP Ashley Gault, Associate, Roetzel

The Implications of Takeovers The Applicability of Michael C. Jensen and Richard S. Ruback s theory of Hostile Corporate Takeovers on the U.K.

The Implications of Takeovers The Applicability of Michael C. Jensen and Richard S. Ruback s theory of Hostile Corporate Takeovers on the U.K. Market Master Thesis MSc. EBA Finance and Strategic Management

The Implications of Takeovers The Applicability of Michael C. Jensen and Richard S. Ruback s theory of Hostile Corporate Takeovers on the U.K. Market Master Thesis MSc. EBA Finance and Strategic Management

Stock Repurchase as a Defense against Hostile Takeovers

Journal of Korean Law Vol. 8, 349-363, June 2009 Stock Repurchase as a Defense against Hostile Takeovers Hee Jeu Kang* Abstract The board of directors has the authority to decide on the sale of the company

Journal of Korean Law Vol. 8, 349-363, June 2009 Stock Repurchase as a Defense against Hostile Takeovers Hee Jeu Kang* Abstract The board of directors has the authority to decide on the sale of the company

FMR Co. ( FMR ) Proxy Voting Guidelines

Proxy Voting Guidelines") January 2017 I. General Principles A. Voting of shares will be conducted in a manner consistent with the best interests of clients. In other words, securities of a portfolio company will generally be voted

January 2017 I. General Principles A. Voting of shares will be conducted in a manner consistent with the best interests of clients. In other words, securities of a portfolio company will generally be voted

PRE-DISCLOSURE ACCUMULATIONS BY ACTIVIST INVESTORS: EVIDENCE AND POLICY

Working Draft, May 2013 PRE-DISCLOSURE ACCUMULATIONS BY ACTIVIST INVESTORS: EVIDENCE AND POLICY Forthcoming, Journal of Corporation Law, Volume 39, Fall 2013 Lucian A. Bebchuk, Alon Brav, Robert J. Jackson,

Working Draft, May 2013 PRE-DISCLOSURE ACCUMULATIONS BY ACTIVIST INVESTORS: EVIDENCE AND POLICY Forthcoming, Journal of Corporation Law, Volume 39, Fall 2013 Lucian A. Bebchuk, Alon Brav, Robert J. Jackson,

THE PRESSURE TO TENDER: AN ANALYSIS AND A PROPOSED REMEDY

THE PRESSURE TO TENDER: AN ANALYSIS AND A PROPOSED REMEDY By LUciAN ARtv BEBCHUK* I. INTRODUCTION In the face of a takeover bid, shareholders' tender decisions are subject to substantial distortions. A

THE PRESSURE TO TENDER: AN ANALYSIS AND A PROPOSED REMEDY By LUciAN ARtv BEBCHUK* I. INTRODUCTION In the face of a takeover bid, shareholders' tender decisions are subject to substantial distortions. A

MERGERS, ACQUISITIONS, AND CORPORATE RESTRUCTURINGS

MERGERS, ACQUISITIONS, AND CORPORATE RESTRUCTURINGS FIFTH EDITION PATRICK A. GAUGHAN WILEY JOHN WILEY & SONS, INC. CONTENTS Case Study Preface xi xv Part 1 Background 1 1 Introduction 3 Recent M&A Trends

MERGERS, ACQUISITIONS, AND CORPORATE RESTRUCTURINGS FIFTH EDITION PATRICK A. GAUGHAN WILEY JOHN WILEY & SONS, INC. CONTENTS Case Study Preface xi xv Part 1 Background 1 1 Introduction 3 Recent M&A Trends

Shareholder Rights Plans Canadian Regulators Propose Modified US Style Of Regulation

Shareholder Rights Plans Canadian Regulators Propose Modified US Style Of Regulation Kevin Thomson kthomson@dwpv.com Lisa Damiani ldamiani@dwpv.com \\mtlapps02\marketing\systems\kv - Research, Interaction

Shareholder Rights Plans Canadian Regulators Propose Modified US Style Of Regulation Kevin Thomson kthomson@dwpv.com Lisa Damiani ldamiani@dwpv.com \\mtlapps02\marketing\systems\kv - Research, Interaction

Corporations Short Outline-Thompson Focused on Olde Learnin

AMH P. 1 Corporations Short Outline-Thompson Focused on Olde Learnin Voting Special Meetings Delaware- Only call by Bd of dir. Unless otherwise auth. by bylaws- 211 MBCA- Call by 10% Stakeholder- w/purpose