BFFF Annual Conference

|

|

|

- Cody Norton

- 5 years ago

- Views:

Transcription

1 BFFF Annual Conference The Economic Outlook February Roger Martin-Fagg Behavioural Economist

50-90% produced by")

2 THE DEFINITION OF VALUE ADDED SALES REVENUE subtract ALL PAID INVOICES = PROFIT AFTER TAX AND INTEREST + WAGES AND SALARIES This is Nominal Gross Domestic Product (GDP) 50-90% produced by businesses employing fewer than 200 people in most countries. Circa 57% in UK.

and can destroy money when a")

3 SHORT RUN ECONOMIC ACTIVITY is driven by the flow of spending MONEY X = multiplied by VELOCITY NOMINAL GDP 95% manufactured by commercial banks Determined by interest rates, the media, the weather, house prices but above all CONFIDENCE Banks manufacture money when they make a loan(bank credit)and can destroy money when a loan is paid down.

4

5 FEEDBACK LOOPS The economy is driven by positive feedback all the time: A small change becomes magnified by the systemic response The media is a major cause of instability There is no such thing as a stable economy

6 The World is on a synchronised upswing This is the first time in living memory What are the drivers?

7 The massive monetary stimulus is finally working $13Trn created by central banks around the World since 2009 But estimated $9Trn destroyed by commercial banks $4Trn net has mostly financed inflated real estate, bond, and equity prices BUT NOW COMMERCIAL BANKS ARE LENDING AGAIN and apart from the Fed, central banks are maintaining their stimulus

8 Share price performance due to massive central bank stimulus Trump tax cuts support current valuations

9 The recent volatility in share prices is almost entirely due to AI algorithms 90% of US shares now traded by computers not humans The algorithm magnifies swings up and down Changes in bond yields (longer term interest rates) is a major driver

10 US Money Supply Growth currently just right but Trump tax cuts will raise velocity and money supply This is mostly QE Tax cuts will inject $1.3Trn over 5 years

11 USA growing at over 3% expect 3.8% end 2018 The Trump tax package will increase velocity and money supply due to a surge in capital spend this year

12 China China will grow by 7%: the closure of excess capacity in heavy industry has reduced electricity demand 16 17

13 The EU will grow at 2.9% in 2018 QE begins Jan 2015

14 GDP growth has risen in G7 advanced economies GDP in the G7 economies

15 Unemployment has continued to fall across advanced economies Euro-area, UK and US unemployment rates (a) The UK and the US are hitting the full employment ceiling

16 The Bank of England is assuming supply side growth now only 1.5% inflation excess demand Full employment Labour supply Education Attitude Equipment Infrastructure Entrepreneurship Money multiplied by velocity ie total spending SUPPLY SIDE DEMAND SIDE This means the UK can expect lower real growth and higher interest rates

17 UK Money Supply Interest rates increased in Nov 2017 because of surge in lending earlier in that year. NB lending took off after help to buy announced in April 2013

18 Household real income growth has slowed Consumption growth and contributions to four-quarter real post-tax income growth

19 Household spending is over 60% of total spending in the economy This forecast assumes a soft Brexit

20 The saving ratio has fallen further over the past year Household saving (a) Saving as a percentage of household post-tax income. Includes NPISH. The diamond shows Bank staff s projection for 2017 Q4. (b) Saving as a percentage of household post-tax income, excluding income not directly received by households such as flows into employment-related pension schemes and imputed rents. Excludes NPISH.

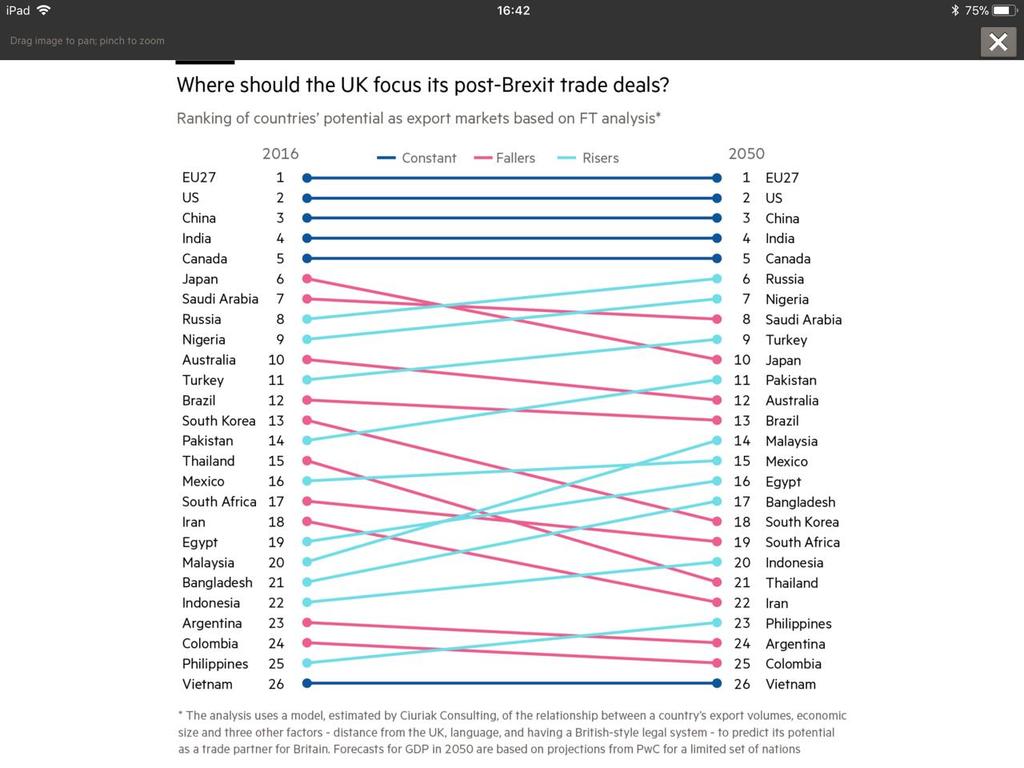

21 Retail Sales Trending Downwards

22 Indicators show UK exports are growing UK exports and survey indicators of export growth

23 (a) The diamond shows Bank staff s projection for 2017 Q4. The current account deficit on our balance of payments has narrowed slightly but it is still 80Bn a year

24 Manufacturing continued to support output growth in Q4 Contributions to average quarterly GVA growth (a) (a) (b) Chained-volume measures at basic prices. Figures in parentheses are weights in nominal GDP in Components may not sum to the total due to chain-linking. Other production includes utilities, extraction and agriculture.

25 Net migration of key young workers is falling

26 Oil and industrial metals prices have risen further in recent months US dollar oil and commodity prices

27 Sterling has remained 15% 20% below its late-2015 peak Sterling Exchange Rate Index

28 What determines the exchange rate of a large open economy? relative interest rates expectations geo-politics relative exchange rates relative inflation rates NB 96% of all currency trades through London are speculative The recent strength of sterling is due to weak dollar and expectations of higher UK

29 The Brexit issue is consuming all the UK Government s horsepower The likelihood of a back swan event (unpredictable) is probably greater than ever Such an event would disrupt an otherwise strongly performing global economy

30 The next slide gives estimates of export attractiveness for post Brexit UK for the next 35 years The UK is a major exporter of services Demographics, distance from the UK, language, and legal system were dependent variables in addition to GDP size and expected growth rate

31

32 Inflation will be rising everywhere Baltic dry index up 50% in the last two months Oil up at $7O Unemployment at 4.2% in the USA Wage inflation and interest rates will respond expect fed funds rate to be 3.2% year end Bank rate will rise in all major economies

33 A Hard Brexit On March if walk away with no deal we revert to WTO trading arrangements Sterling will drop to $1.20 and 1.05 Euro or lower Supply chains will be severely disrupted Confidence will crash Companies will immediately delay payments The recession begins

34 Soft Brexit The UK has agreed to fully align with EU regulations until 2021 Beyond 2021 UK courts will take into account ECJ case law A soft Brexit is the only way the UK Government can prevent a Corbyn victory in 2022 The UK will grow max rate 1.5% pa until business has invested in labour saving technology. It will be at least 5 years.

35 UK Real GDP Scenarios per 4% annum 3% 2.5% 2% TRANSITIONAL FREE TRADE DEAL 1% inflation and interest rates rise above expectations end % NO deal 20% chance

36 Currently the UK has 50 Free Trade Agreements, with another 40 in the pipeline. These are negotiated by the EU on our behalf. If they cannot be cut and pasted, we start from the beginning.

37 Key Points The global boom is driving up commodity prices and wages The USA will overheat end 2018 The UK will underperform due to Brexit The EU is now a growth story Interest rates will rise everywhere Exchange rates will be more volatile than usual due to unexpected changes in interest rates and geopolitics

38 UK Forecast for the next 12 months Real GDP growth 1.8% Real wages up 1% year end Retail: tough first half, better second half House prices up 1-3% Inflation + 2.3% Interest rates 1% year end -$: 1.34 but big swings Euro 1.15 Soft Brexit

39 The biggest challenge for UK Business How to keep customers happy whilst automating the business as the labour shortage bites

A PIVOTAL OCTOBER. Issue #14. October 2018

A PIVOTAL OCTOBER Issue #14 October 2018 Stock markets tend to post their best returns from October to April but October itself can be the most volatile month of the year. The tug of war between good news

A PIVOTAL OCTOBER Issue #14 October 2018 Stock markets tend to post their best returns from October to April but October itself can be the most volatile month of the year. The tug of war between good news

PMI and economic outlook

PMI and economic outlook Chris Williamson Chief Business Economist, IHS Markit 1 st November 2017 2 PMI coverage Current coverage Expansion pipeline 40+ Countries covered 27,000+ Companies surveyed every

PMI and economic outlook Chris Williamson Chief Business Economist, IHS Markit 1 st November 2017 2 PMI coverage Current coverage Expansion pipeline 40+ Countries covered 27,000+ Companies surveyed every

LIFTING THE LID ON PANDORA S BOX A CHANGE OF PACE FOR BRITISH CONSTRUCTION

LIFTING THE LID ON PANDORA S BOX A CHANGE OF PACE FOR BRITISH CONSTRUCTION EXECUTIVE SUMMARY The UK economy continues to perform robustly though significant threats remain. Potential risk of a slowdown

LIFTING THE LID ON PANDORA S BOX A CHANGE OF PACE FOR BRITISH CONSTRUCTION EXECUTIVE SUMMARY The UK economy continues to perform robustly though significant threats remain. Potential risk of a slowdown

The Outlook for the UK Consumer Sector A Note. Gavyn Davies. 9 May Overview

The Outlook for the UK Consumer Sector A Note Gavyn Davies 9 May 2018 Overview Consumers expenditure accounts for 66 per cent of GDP in the UK. There is therefore a huge variety of investment opportunities

The Outlook for the UK Consumer Sector A Note Gavyn Davies 9 May 2018 Overview Consumers expenditure accounts for 66 per cent of GDP in the UK. There is therefore a huge variety of investment opportunities

Monthly Economic Review

Monthly Economic Review FEBRUARY 2018 Based on January 2018 data releases Bedfordshire Chamber of Commerce Headlines UK GDP growth picked up in Q4, driven by stronger output from the services sector The

Monthly Economic Review FEBRUARY 2018 Based on January 2018 data releases Bedfordshire Chamber of Commerce Headlines UK GDP growth picked up in Q4, driven by stronger output from the services sector The

Government and Public Sector

Government and Public Sector Budget 2016 Digest Government and Public Sector Budget 2016 Digest 1 Economic story The background for the economic forecast is a slowing world economy. 2 The Chancellor talked

Government and Public Sector Budget 2016 Digest Government and Public Sector Budget 2016 Digest 1 Economic story The background for the economic forecast is a slowing world economy. 2 The Chancellor talked

Forecast evaluation report October 2012

Forecast evaluation report 2012 16 October 2012 The aim of the FER We publish 2 EFO forecasts a year We emphasise and quantify uncertainty But still publish detail of central forecast and evaluate ex post

Forecast evaluation report 2012 16 October 2012 The aim of the FER We publish 2 EFO forecasts a year We emphasise and quantify uncertainty But still publish detail of central forecast and evaluate ex post

Mark Scheme (Results) Summer 2007

Summer 2007") Mark Scheme (Results) Summer 2007 GCE GCE Economic (6353) Paper 1 Edexcel Limited. Registered in England and Wales No. 4496750 Registered Office: One90 High Holborn, London WC1V 7BH 6353 Mark Scheme Summer

Mark Scheme (Results) Summer 2007 GCE GCE Economic (6353) Paper 1 Edexcel Limited. Registered in England and Wales No. 4496750 Registered Office: One90 High Holborn, London WC1V 7BH 6353 Mark Scheme Summer

growth but still remains at approximately 1.5% of potential GDP.

THE UK ECONOMY IN FOCUS/APPLICATIONS Reminder of key objectives: Low and positive inflation (inflation rate target of 2%/- 1%) Sustainable growth of real GDP (no target) falling unemployment (no target)

THE UK ECONOMY IN FOCUS/APPLICATIONS Reminder of key objectives: Low and positive inflation (inflation rate target of 2%/- 1%) Sustainable growth of real GDP (no target) falling unemployment (no target)

Introduction. ECON204 Notes. Response to the GFC Crisis Monetary policy Cut interest rates Quantitative easing

Introduction ECON204 Notes Response to the GFC Crisis Monetary policy Cut interest rates Quantitative easing Fiscal policy Governments spent and borrowed a lot Fiscal deficits funded by debt Many have

Introduction ECON204 Notes Response to the GFC Crisis Monetary policy Cut interest rates Quantitative easing Fiscal policy Governments spent and borrowed a lot Fiscal deficits funded by debt Many have

The All-In-1 Investment Bond and Guaranteed Capital Bond. Investment Report 2016

The All-In-1 Investment Bond and Guaranteed Capital Bond Investment Report 2016 The All-In-1 Investment Bond and Guaranteed Capital Bond Investment Report 2016 This information does not constitute investment

The All-In-1 Investment Bond and Guaranteed Capital Bond Investment Report 2016 The All-In-1 Investment Bond and Guaranteed Capital Bond Investment Report 2016 This information does not constitute investment

Spring 2018 forecast. The economic forecast for Europe Main messages

Main messages "Expansion to continue amid new risks" Economic expansion set to continue in all Member States Labour market improvements continue Inflation expected to move up very gradually Public finances

Main messages "Expansion to continue amid new risks" Economic expansion set to continue in all Member States Labour market improvements continue Inflation expected to move up very gradually Public finances

UK Economic Outlook March 2017

www.pwc.co.uk/economics Contents 1 2 3 4 Global outlook UK economic trends and prospects Consumer spending prospects after Brexit Will robots steal our jobs? 2 Global growth in 2017 should be slightly

www.pwc.co.uk/economics Contents 1 2 3 4 Global outlook UK economic trends and prospects Consumer spending prospects after Brexit Will robots steal our jobs? 2 Global growth in 2017 should be slightly

Spain Economic Outlook Q FIRST QUARTER. Economic Outlook. Spain. Economic Outlook. Spain

Economic Outlook FIRST QUARTER 2016 Spain Economic Outlook Spain The world economy will continue to grow, but at a slower pace than in the past and with more risks Spain's economy has started 2016 with

Economic Outlook FIRST QUARTER 2016 Spain Economic Outlook Spain The world economy will continue to grow, but at a slower pace than in the past and with more risks Spain's economy has started 2016 with

The WTO Option and the Northern Ireland Economy. Dr Eoin Magennis, Senior Economist Ulster University Economic Policy Centre. ulster.ac.

The WTO Option and the Northern Ireland Economy Dr Eoin Magennis, Senior Economist Ulster University Economic Policy Centre ulster.ac.uk March 2017 Agenda What is the WTO Option? How equipped is the NI

The WTO Option and the Northern Ireland Economy Dr Eoin Magennis, Senior Economist Ulster University Economic Policy Centre ulster.ac.uk March 2017 Agenda What is the WTO Option? How equipped is the NI

What questions would you like answered?

What questions would you like answered? Define the following: Globalisation an expansion of world trade leading to increased international interdependence GDP The value of goods and services produced in

What questions would you like answered? Define the following: Globalisation an expansion of world trade leading to increased international interdependence GDP The value of goods and services produced in

Austria s economy will grow by 2¾% in 2017

Gerhard Fenz, Friedrich Fritzer, Martin Schneider 1 In the first half of 217, Austria s economy gathered further momentum. With growth rates by.8% in both the first and the second quarters, Austria recorded

Gerhard Fenz, Friedrich Fritzer, Martin Schneider 1 In the first half of 217, Austria s economy gathered further momentum. With growth rates by.8% in both the first and the second quarters, Austria recorded

2018 ECONOMIC OUTLOOK

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY December 4 207 208 ECONOMIC OUTLOOK EXPECT BETTER GROWTH WORLDWIDE John Lynch Chief Investment Strategist, LPL Financial Barry Gilbert, PhD, CFA Asset Allocation

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY December 4 207 208 ECONOMIC OUTLOOK EXPECT BETTER GROWTH WORLDWIDE John Lynch Chief Investment Strategist, LPL Financial Barry Gilbert, PhD, CFA Asset Allocation

The Economic Context for Budget 2019

The Economic Context for Budget 219 1 October 218 Oliver Mangan Chief Economist AIB Steady global growth forecast but GDP (Vol Change) 217 218(f) 219(f) 22(f) World 3.7 3.7 3.7 3.7 Advanced Economies 2.3

The Economic Context for Budget 219 1 October 218 Oliver Mangan Chief Economist AIB Steady global growth forecast but GDP (Vol Change) 217 218(f) 219(f) 22(f) World 3.7 3.7 3.7 3.7 Advanced Economies 2.3

Quarterly investment outlook. Five key issues shaping current investment strategy Third quarter 2016

Quarterly investment outlook Five key issues shaping current investment strategy Third quarter 2016 Five key issues shaping current investment strategy Third quarter 2016 Page 2 Five key issues shaping

Quarterly investment outlook Five key issues shaping current investment strategy Third quarter 2016 Five key issues shaping current investment strategy Third quarter 2016 Page 2 Five key issues shaping

Flexible Guarantee Bond, Flexible Guarantee Bond Series 2, Flexi Guarantee Plan and Flexible Guarantee Funds. Investment Report 2016

Flexible Guarantee Bond, Flexible Guarantee Bond Series 2, Flexi Guarantee Plan and Flexible Guarantee Funds Investment Report 2016 Flexible Guarantee Bond, Flexible Guarantee Bond Series 2, Flexi Guarantee

Flexible Guarantee Bond, Flexible Guarantee Bond Series 2, Flexi Guarantee Plan and Flexible Guarantee Funds Investment Report 2016 Flexible Guarantee Bond, Flexible Guarantee Bond Series 2, Flexi Guarantee

Commercial Cards & Payments Leo Abruzzese October 2015 New York

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

Monthly Bulletin of Economic Trends: Review of the Australian Economy

MELBOURNE INSTITUTE Applied Economic & Social Research Monthly Bulletin of Economic Trends: Review of the Australian Economy December 7 Released on December 7 Outlook for Australia Economic Activity Actual

MELBOURNE INSTITUTE Applied Economic & Social Research Monthly Bulletin of Economic Trends: Review of the Australian Economy December 7 Released on December 7 Outlook for Australia Economic Activity Actual

The Impact of Brexit on the UK Economy. Centre For Business Research, Judge Business School, University of Cambridge

The Impact of Brexit on the UK Economy Ken Coutts Graham Gudgin Centre For Business Research, Judge Business School, University of Cambridge Prof. Neil Gibson Ulster University March 2017 OUTLINE The Economic

The Impact of Brexit on the UK Economy Ken Coutts Graham Gudgin Centre For Business Research, Judge Business School, University of Cambridge Prof. Neil Gibson Ulster University March 2017 OUTLINE The Economic

What is Monetary Policy?

What is Monetary Policy? Monetary stability means stable prices and confidence in the currency. Stable prices are defined by the Government's inflation target, which the Bank seeks to meet through the

What is Monetary Policy? Monetary stability means stable prices and confidence in the currency. Stable prices are defined by the Government's inflation target, which the Bank seeks to meet through the

Irish Economic Update AIB Treasury Economic Research Unit

Irish Economic Update AIB Treasury Economic Research Unit 9th October 2018 Budget 2019 Public Finances in Balance The Irish economy has performed strongly in recent years, boosting tax revenues. Corporation

Irish Economic Update AIB Treasury Economic Research Unit 9th October 2018 Budget 2019 Public Finances in Balance The Irish economy has performed strongly in recent years, boosting tax revenues. Corporation

Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks John Praveen

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Stocks Bottoming On Track to Recovery. Near-term Risks John Praveen

CPA Australia Management accounting conference Australian economy Julie Toth Chief Economist Australian Industry Group. aigroup.com.

CPA Australia Management accounting conference 2016 Australian economy 2016-17 Julie Toth Chief Economist Australian Industry Group Events & opportunities for Australian business in 2016-17: Global and

CPA Australia Management accounting conference 2016 Australian economy 2016-17 Julie Toth Chief Economist Australian Industry Group Events & opportunities for Australian business in 2016-17: Global and

Finland falling further behind euro area growth

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

ECONOMIC RECOVERY AT CRUISE SPEED

EBF Economic Outlook Nr 43 May 2018 2018 SPRING OUTLOOK ON THE EURO AREA ECONOMIES IN 2018-2019 ECONOMIC RECOVERY AT CRUISE SPEED EDITORIAL TEAM: Francisco Saravia (author), Helge Pedersen - Chair of the

EBF Economic Outlook Nr 43 May 2018 2018 SPRING OUTLOOK ON THE EURO AREA ECONOMIES IN 2018-2019 ECONOMIC RECOVERY AT CRUISE SPEED EDITORIAL TEAM: Francisco Saravia (author), Helge Pedersen - Chair of the

Economic activity gathers pace

Produced by the Economic Research Unit October 2014 A quarterly analysis of trends in the Irish economy Economic activity gathers pace Positive data flow Recovery broadening out GDP growth revised up to

Produced by the Economic Research Unit October 2014 A quarterly analysis of trends in the Irish economy Economic activity gathers pace Positive data flow Recovery broadening out GDP growth revised up to

Andersons Professor of International Trade Department of Agricultural, Environmental & Development Economics Ohio State University

Macroeconomic Outlook Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Ohio State University Extension Global economic

Macroeconomic Outlook Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Ohio State University Extension Global economic

An economic update Craig Botham, Economist May 2017

An economic update Craig Botham, Economist May 2017 2016 image of the year Donald and Nigel at Trump towers Source: Splashnews.com. 1 Key issues UK: the election, Brexit and beyond Europe: out of the woods?

An economic update Craig Botham, Economist May 2017 2016 image of the year Donald and Nigel at Trump towers Source: Splashnews.com. 1 Key issues UK: the election, Brexit and beyond Europe: out of the woods?

Global economy in charts

Global economy in charts Ian Stewart, Debapratim De, Tom Simmons & Peter Ireson Economics & Markets Research, Deloitte, London Summary 1. Global activity easing 2. Slowdown most apparent in euro area 3.

Global economy in charts Ian Stewart, Debapratim De, Tom Simmons & Peter Ireson Economics & Markets Research, Deloitte, London Summary 1. Global activity easing 2. Slowdown most apparent in euro area 3.

Economic outlook Thoughts on what to expect in Dr. Ira Kalish Chief Global Economist, Deloitte

Economic outlook Thoughts on what to expect in 2018 Dr. Ira Kalish Chief Global Economist, Deloitte USA Strong job market Full employment Employment rising faster than needed to absorb new entrants into

Economic outlook Thoughts on what to expect in 2018 Dr. Ira Kalish Chief Global Economist, Deloitte USA Strong job market Full employment Employment rising faster than needed to absorb new entrants into

What s next? A macro view of 2018

What s next? A macro view of 2018 Hong Kong 12 January 2018 John Greenwood Chief Economist, Invesco Ltd This document is intended only for 2018 Invesco Roadshow in Hong Kong. This is not an invitation

What s next? A macro view of 2018 Hong Kong 12 January 2018 John Greenwood Chief Economist, Invesco Ltd This document is intended only for 2018 Invesco Roadshow in Hong Kong. This is not an invitation

Macroeconomic Challenges and Forecasts for Poland

Macroeconomic Challenges and Forecasts for Poland June EFC warns - the best is behind us and proposes actions Opinion of the European Financial Congress There is a general consensus among the European

Macroeconomic Challenges and Forecasts for Poland June EFC warns - the best is behind us and proposes actions Opinion of the European Financial Congress There is a general consensus among the European

Highlights and key messages for business and public policy

Highlights and key messages for business and public policy Key projections 2018 2019 Real GDP growth 1.5% 1.6% Consumer spending growth 1.1% 1.3% Inflation (CPI) 2.7% 2.3% Source: PwC main scenario projections

Highlights and key messages for business and public policy Key projections 2018 2019 Real GDP growth 1.5% 1.6% Consumer spending growth 1.1% 1.3% Inflation (CPI) 2.7% 2.3% Source: PwC main scenario projections

The Saturday Economist UK Economic Outlook Q1 2015

The Saturday Economist The Saturday Economist UK Economic Outlook Q1 2015 Leisure and Construction driving recovery UK Economic Outlook March 2015 Page 1 The UK recovery continues. We expect growth of

The Saturday Economist The Saturday Economist UK Economic Outlook Q1 2015 Leisure and Construction driving recovery UK Economic Outlook March 2015 Page 1 The UK recovery continues. We expect growth of

Economic Survey December 2006 English Summary

Economic Survey December English Summary. Short term outlook Reaching an annualized growth rate of.5 per cent in the first half of, GDP growth in Denmark has turned out considerably stronger than expected

Economic Survey December English Summary. Short term outlook Reaching an annualized growth rate of.5 per cent in the first half of, GDP growth in Denmark has turned out considerably stronger than expected

Preliminary Investment Trends Report

Preliminary Investment Trends Report QUEBEC: Construction investment in Quebec picks up over the medium term driven by infrastructure, mining and pipeline projects. Following a decline in, residential

Preliminary Investment Trends Report QUEBEC: Construction investment in Quebec picks up over the medium term driven by infrastructure, mining and pipeline projects. Following a decline in, residential

Interest Rate Forecast

Interest Rate Forecast Economics January Highlights Global growth firms Waiting for Trumponomics Bank of Canada on hold Recent growth momentum in the global economy continued in December and looks to extend

Interest Rate Forecast Economics January Highlights Global growth firms Waiting for Trumponomics Bank of Canada on hold Recent growth momentum in the global economy continued in December and looks to extend

Global MT outlook: Will the crisis in emerging markets derail the recovery?

Global MT outlook: Will the crisis in emerging markets derail the recovery? John Walker Chairman and Chief Economist jwalker@oxfordeconomics.com March 2014 Oxford Economics Oxford Economics is one of the

Global MT outlook: Will the crisis in emerging markets derail the recovery? John Walker Chairman and Chief Economist jwalker@oxfordeconomics.com March 2014 Oxford Economics Oxford Economics is one of the

Economics Standard level Paper 2

Economics Standard level Paper 2 Tuesday 5 May 2015 (morning) 1 hour 30 minutes Instructions to candidates Do not open this examination paper until instructed to do so. You are not permitted access to

Economics Standard level Paper 2 Tuesday 5 May 2015 (morning) 1 hour 30 minutes Instructions to candidates Do not open this examination paper until instructed to do so. You are not permitted access to

Weekly Market Commentary

LPL FINANCIAL RESEARCH Weekly Market Commentary November 18, 2014 Emerging Markets Opportunity Still Emerging Burt White Chief Investment Officer LPL Financial Jeffrey Buchbinder, CFA Market Strategist

LPL FINANCIAL RESEARCH Weekly Market Commentary November 18, 2014 Emerging Markets Opportunity Still Emerging Burt White Chief Investment Officer LPL Financial Jeffrey Buchbinder, CFA Market Strategist

Economic Outlook, January 2016 Jeffrey M. Lacker President, Federal Reserve Bank of Richmond

Economic Outlook, January 2016 Jeffrey M. Lacker President, Federal Reserve Bank of Richmond Annual Meeting of the South Carolina Business & Industry Political Education Committee Columbia, South Carolina

Economic Outlook, January 2016 Jeffrey M. Lacker President, Federal Reserve Bank of Richmond Annual Meeting of the South Carolina Business & Industry Political Education Committee Columbia, South Carolina

Irish Economic Update AIB Treasury Economic Research Unit

Irish Economic Update AIB Treasury Economic Research Unit 10th October 2017 Budget 2018 Deficit Close To Being Eliminated The Irish economy has performed strongly in recent years, which has helped to boost

Irish Economic Update AIB Treasury Economic Research Unit 10th October 2017 Budget 2018 Deficit Close To Being Eliminated The Irish economy has performed strongly in recent years, which has helped to boost

Structural changes in the Maltese economy

Structural changes in the Maltese economy Article published in the Annual Report 2014, pp. 72-76 BOX 4: STRUCTURAL CHANGES IN THE MALTESE ECONOMY 1 Since the global recession that took hold around the

Structural changes in the Maltese economy Article published in the Annual Report 2014, pp. 72-76 BOX 4: STRUCTURAL CHANGES IN THE MALTESE ECONOMY 1 Since the global recession that took hold around the

Preliminary Investment Trends Report

Preliminary Investment Trends Report ALBERTA: 215 224 Proposed and ongoing oil sands, pipeline, storage terminals, electric power facilities and transmission projects continue to push Alberta s construction

Preliminary Investment Trends Report ALBERTA: 215 224 Proposed and ongoing oil sands, pipeline, storage terminals, electric power facilities and transmission projects continue to push Alberta s construction

THE ECONOMIC OUTLOOK IN 2012 ILTA CONFERENCE. 9 May 2012 Vicky Pryce

THE ECONOMIC OUTLOOK IN 2012 ILTA CONFERENCE 9 May 2012 Vicky Pryce Contents Global and European economy UK economy Prospects for individuals and businesses Concluding remarks what next? Global and European

THE ECONOMIC OUTLOOK IN 2012 ILTA CONFERENCE 9 May 2012 Vicky Pryce Contents Global and European economy UK economy Prospects for individuals and businesses Concluding remarks what next? Global and European

AVIVA INVESTORS UK INDUSTRIAL PROPERTY A SAFE HAVEN? by Tom Goodwin

This document is for professional clients, financial advisers and institutional or qualified investors only. Not to be distributed, or relied on by retail clients. AVIVA INVESTORS UK INDUSTRIAL PROPERTY

This document is for professional clients, financial advisers and institutional or qualified investors only. Not to be distributed, or relied on by retail clients. AVIVA INVESTORS UK INDUSTRIAL PROPERTY

Housing market. Forecasts

Housing market Forecasts - 2018 Summer COUNTRYWIDE HOUSING MARKET FORECASTS 2018 COUNTRYWIDE HOUSING MARKET FORECASTS 2018 Forecasts Executive summary 2014 2015 2017 2018 It will be a bumpy time ahead,

Housing market Forecasts - 2018 Summer COUNTRYWIDE HOUSING MARKET FORECASTS 2018 COUNTRYWIDE HOUSING MARKET FORECASTS 2018 Forecasts Executive summary 2014 2015 2017 2018 It will be a bumpy time ahead,

LESS DYNAMIC GROWTH AMID HIGH UNCERTAINTY

OVERVIEW: The European economy has moved into lower gear amid still robust domestic fundamentals. GDP growth is set to continue at a slower pace. LESS DYNAMIC GROWTH AMID HIGH UNCERTAINTY Interrelated

OVERVIEW: The European economy has moved into lower gear amid still robust domestic fundamentals. GDP growth is set to continue at a slower pace. LESS DYNAMIC GROWTH AMID HIGH UNCERTAINTY Interrelated

2016 Economic Outlook for Ireland & Eurozone IFP Launch

2016 Economic Outlook for Ireland & Eurozone IFP Launch December 3 rd 2015 Jim Power Global Background US & UK growing at reasonable pace Euro Zone growing well below potential Emerging markets in some

2016 Economic Outlook for Ireland & Eurozone IFP Launch December 3 rd 2015 Jim Power Global Background US & UK growing at reasonable pace Euro Zone growing well below potential Emerging markets in some

Release date : 28 December Economic update - December Key data highlights:

Economic update - December Key data highlights:. ember saw inflation fall slightly to 2.3 per cent, reducing the likelihood of a Bank Rate rise from 0.75 per cent. Consumers remain wary of their day-to-day

Economic update - December Key data highlights:. ember saw inflation fall slightly to 2.3 per cent, reducing the likelihood of a Bank Rate rise from 0.75 per cent. Consumers remain wary of their day-to-day

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review October 16 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Please see disclaimer on the last page of this report 1 Key Issues Global

Global Macroeconomic Monthly Review October 16 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Please see disclaimer on the last page of this report 1 Key Issues Global

South Region Committee Brexit and the Associated Challenges

South Region Committee Brexit and the Associated Challenges event in Tralee with Jim Power Tralee, 17 October 2017 Brexit and the Associated Challenges The Institute of Banking, Tralee October 17 th 2017

South Region Committee Brexit and the Associated Challenges event in Tralee with Jim Power Tralee, 17 October 2017 Brexit and the Associated Challenges The Institute of Banking, Tralee October 17 th 2017

9 November 2018 AUSTRALIAN ECONOMIC DEVELOPMENTS

9 November 2018 AUSTRALIAN ECONOMIC DEVELOPMENTS This week the Reserve Bank of Australia (RBA) left the cash rate at a record low of 1.50%. The RBA expects inflation and wages to accelerate gradually from

9 November 2018 AUSTRALIAN ECONOMIC DEVELOPMENTS This week the Reserve Bank of Australia (RBA) left the cash rate at a record low of 1.50%. The RBA expects inflation and wages to accelerate gradually from

Advanced Market Analysis for Commercial Real Estate

Ward Center for Real Estate Studies www.ccim.com Advanced Market Analysis for Commercial Real Estate PPT Handout EXCELLENCE SUCCESS SKILL LEADERSHIP CHALLENGE STRENGTH Copyright 2012 by the CCIM Institute

Ward Center for Real Estate Studies www.ccim.com Advanced Market Analysis for Commercial Real Estate PPT Handout EXCELLENCE SUCCESS SKILL LEADERSHIP CHALLENGE STRENGTH Copyright 2012 by the CCIM Institute

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH Augustine Faucher Chief Economist November 13, 2017 Senior Economic Advisor Chief Economist BETTER GROWTH THIS YEAR, AND AN UPGRADE TO 2018 World output,

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH Augustine Faucher Chief Economist November 13, 2017 Senior Economic Advisor Chief Economist BETTER GROWTH THIS YEAR, AND AN UPGRADE TO 2018 World output,

conclusions Gavin Cameron University of Oxford OUBEP Topical Economics 2006

the BRIC economies: conclusions Gavin Cameron University of Oxford OUBEP Topical Economics 2006 introduction Global Monetary Easing in 2001 3 Fuels consumer boom in West (esp. USA) Fuels investment boom

the BRIC economies: conclusions Gavin Cameron University of Oxford OUBEP Topical Economics 2006 introduction Global Monetary Easing in 2001 3 Fuels consumer boom in West (esp. USA) Fuels investment boom

DO NOT WRITE ANY ANSWERS IN THIS SOURCE BOOKLET. YOU MUST ANSWER THE QUESTIONS IN THE PROVIDED ANSWER BOOKLET.

SPECIMEN MATERIAL AS ECONOMICS 7135/2 Paper 2 The national economy in a global context Source booklet DO NOT WRITE ANY ANSWERS IN THIS SOURCE BOOKLET. YOU MUST ANSWER THE QUESTIONS IN THE PROVIDED ANSWER

SPECIMEN MATERIAL AS ECONOMICS 7135/2 Paper 2 The national economy in a global context Source booklet DO NOT WRITE ANY ANSWERS IN THIS SOURCE BOOKLET. YOU MUST ANSWER THE QUESTIONS IN THE PROVIDED ANSWER

General Certificate of Education Advanced Level Examination June 2010

General Certificate of Education Advanced Level Examination June 2010 Economics ECON4 Unit 4 The National and International Economy For this paper you must have: a 12-page answer book. You may use a calculator.

General Certificate of Education Advanced Level Examination June 2010 Economics ECON4 Unit 4 The National and International Economy For this paper you must have: a 12-page answer book. You may use a calculator.

The Irish Economic Update

The Irish Economic Update Continuing Robust Growth February 218 Oliver Mangan Chief Economist AIB 1 Strong recovery by Irish economy since 213 Irish economy boomed from 1993 to 27 with GDP up by over 25%

The Irish Economic Update Continuing Robust Growth February 218 Oliver Mangan Chief Economist AIB 1 Strong recovery by Irish economy since 213 Irish economy boomed from 1993 to 27 with GDP up by over 25%

Economic Outlook. December Dan McLaughlin. Chief Economist

Economic Outlook December 211 Chief Economist Dan McLaughlin 11q3(e) 11q1 1q3 Global growth has slowed this year... Global Growth (%) 6 4 2-2 -4-6 1q1 9q3 9q1 8q3 8q1 7q3 7q1 World US Euro And OECD expects

Economic Outlook December 211 Chief Economist Dan McLaughlin 11q3(e) 11q1 1q3 Global growth has slowed this year... Global Growth (%) 6 4 2-2 -4-6 1q1 9q3 9q1 8q3 8q1 7q3 7q1 World US Euro And OECD expects

World Economy Geopolitics Investment Strategy. The Impact of EU s Sovereign Risks on Turkish Economy. Presentation given by

World Economy Geopolitics Investment Strategy OUTLOOK FOR WORLD S MAJOR FINANCIAL MARKETS The Impact of EU s Sovereign Risks on Turkish Economy Presentation given by Dr. Michael Ivanovitch, President MSI

World Economy Geopolitics Investment Strategy OUTLOOK FOR WORLD S MAJOR FINANCIAL MARKETS The Impact of EU s Sovereign Risks on Turkish Economy Presentation given by Dr. Michael Ivanovitch, President MSI

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Monday 23 May 2016 Morning Time allowed: 1 hour 15 minutes

S EONOMIS Unit 2 The National Economy Monday 23 May 2016 Morning Time allowed: 1 hour 15 minutes Materials For this paper you must have: an objective test answer sheet a black ball-point pen an Q 8-page

S EONOMIS Unit 2 The National Economy Monday 23 May 2016 Morning Time allowed: 1 hour 15 minutes Materials For this paper you must have: an objective test answer sheet a black ball-point pen an Q 8-page

AS Economics Essay Questions

TheRevisionGuide.com Accelerating your potential Revision Worksheet AS Economics Essay Questions Worksheet by: Apsara Sumanasiri Student Name : Date:. TheRevisionGuide (www.therevisionguide.com) is a free

TheRevisionGuide.com Accelerating your potential Revision Worksheet AS Economics Essay Questions Worksheet by: Apsara Sumanasiri Student Name : Date:. TheRevisionGuide (www.therevisionguide.com) is a free

Economy Check-In: Post 2008 Crisis Market Update Special Report

Insight. Education. Analysis. Economy Check-In: Post 2008 Crisis Market Update Special Report By Kevin Chambers The 2008 crisis was one of the worst downturns in American economic history. News reports

Insight. Education. Analysis. Economy Check-In: Post 2008 Crisis Market Update Special Report By Kevin Chambers The 2008 crisis was one of the worst downturns in American economic history. News reports

Japan Chart Book. 5 February 2014

Japan Chart Book 5 February Japan: Economic Forecast Dashboard Forecast highlights Real GDP growth forecast at. in and. in 5 Slower consumption in -5 but offset by improved exports and investment Gradual

Japan Chart Book 5 February Japan: Economic Forecast Dashboard Forecast highlights Real GDP growth forecast at. in and. in 5 Slower consumption in -5 but offset by improved exports and investment Gradual

Eurozone Economic Watch. July 2018

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

... Eye on the Economy August

............................................................................................. Eye on the Economy August 2015.............................................................................................

............................................................................................. Eye on the Economy August 2015.............................................................................................

The Irish Economic Update

The Irish Economic Update Growth Remains Strong April 218 Oliver Mangan Chief Economist AIB 1 Strong recovery by Irish economy since 213 Irish economy boomed from 1993 to 27 with GDP up by over 25% Celtic

The Irish Economic Update Growth Remains Strong April 218 Oliver Mangan Chief Economist AIB 1 Strong recovery by Irish economy since 213 Irish economy boomed from 1993 to 27 with GDP up by over 25% Celtic

The Irish Economic Update

The Irish Economic Update Continuing Robust Growth January 218 Oliver Mangan Chief Economist AIB 1 Strong recovery by Irish economy since 213 Irish economy boomed from 1993 to 27 with GDP up by over 25%

The Irish Economic Update Continuing Robust Growth January 218 Oliver Mangan Chief Economist AIB 1 Strong recovery by Irish economy since 213 Irish economy boomed from 1993 to 27 with GDP up by over 25%

Monthly Economic Review

Monthly Economic Review DECEMBER 2017 Based on November 2017 data releases Bedfordshire Chamber of Commerce Headlines UK GDP growth in Q3 unrevised as business investment and the UK s trade position weakens

Monthly Economic Review DECEMBER 2017 Based on November 2017 data releases Bedfordshire Chamber of Commerce Headlines UK GDP growth in Q3 unrevised as business investment and the UK s trade position weakens

The real change in private inventories added 0.22 percentage points to the second quarter GDP growth, after subtracting 0.65% in the first quarter.

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy bounced back in the second quarter of 2007, growing at the fastest pace in more than a year. According the final estimates released

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy bounced back in the second quarter of 2007, growing at the fastest pace in more than a year. According the final estimates released

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. July 12, Capital Markets Division, Economics Department. leumiusa.

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

THE UCLA ANDERSON FORECAST FOR THE NATION

THE UCLA ANDERSON FORECAST FOR THE NATION DECEMBER REPORT Sunny 2018, Cloudy SUNNY 2018, CLOUDY Sunny 2018, Cloudy David Shulman Senior Economist, UCLA Anderson Forecast December Of a sudden, propelled

THE UCLA ANDERSON FORECAST FOR THE NATION DECEMBER REPORT Sunny 2018, Cloudy SUNNY 2018, CLOUDY Sunny 2018, Cloudy David Shulman Senior Economist, UCLA Anderson Forecast December Of a sudden, propelled

The international environment

The international environment This article (1) discusses developments in the global economy since the August 1999 Quarterly Bulletin. Domestic demand growth remained strong in the United States, and with

The international environment This article (1) discusses developments in the global economy since the August 1999 Quarterly Bulletin. Domestic demand growth remained strong in the United States, and with

Global Economic Outlook - July 2017

Global Economic Outlook - July 2017 June 28, 2017 by Carl Tannenbaum, Asha Bangalore, Ankit Mital, Brian Liebovich of Northern Trust Global economic activity has generally been good during the first six

Global Economic Outlook - July 2017 June 28, 2017 by Carl Tannenbaum, Asha Bangalore, Ankit Mital, Brian Liebovich of Northern Trust Global economic activity has generally been good during the first six

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Mayura Hooper Phone: 973-367-7930 Email:

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Mayura Hooper Phone: 973-367-7930 Email:

Advanced Market Analysis for Commercial Real Estate

Ward Center for Real Estate Studies www.ccim.com Advanced Market Analysis for Commercial Real Estate PPT Handout EXCELLENCE SUCCESS SKILL LEADERSHIP CHALLENGE STRENGTH Copyright 2012 by the CCIM Institute

Ward Center for Real Estate Studies www.ccim.com Advanced Market Analysis for Commercial Real Estate PPT Handout EXCELLENCE SUCCESS SKILL LEADERSHIP CHALLENGE STRENGTH Copyright 2012 by the CCIM Institute

Explore the themes and thinking behind our decisions.

ASSET ALLOCATION COMMITTEE VIEWPOINTS First Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

ASSET ALLOCATION COMMITTEE VIEWPOINTS First Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

Structural Changes in the Maltese Economy

Structural Changes in the Maltese Economy Dr. Aaron George Grech Modelling and Research Department, Central Bank of Malta, Castille Place, Valletta, Malta Email: grechga@centralbankmalta.org Doi:10.5901/mjss.2015.v6n5p423

Structural Changes in the Maltese Economy Dr. Aaron George Grech Modelling and Research Department, Central Bank of Malta, Castille Place, Valletta, Malta Email: grechga@centralbankmalta.org Doi:10.5901/mjss.2015.v6n5p423

BCC UK Economic Forecast Q4 2015

BCC UK Economic Forecast Q4 2015 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and

BCC UK Economic Forecast Q4 2015 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and

October th edition. Global Capital Confidence Barometer Chile

October 2016 15th edition Capital Confidence Barometer Chile About the Barometer EY s Capital Confidence Barometer is a regular survey of senior executives from large companies around the world, conducted

October 2016 15th edition Capital Confidence Barometer Chile About the Barometer EY s Capital Confidence Barometer is a regular survey of senior executives from large companies around the world, conducted

SUMMARY OF MACROECONOMIC DEVELOPMENTS

SUMMARY OF MACROECONOMIC DEVELOPMENTS NOVEMBER 2018 2 Summary of macroeconomic developments, November 2018 Indicators of global economic activity suggest a continuation of solid growth in the final quarter

SUMMARY OF MACROECONOMIC DEVELOPMENTS NOVEMBER 2018 2 Summary of macroeconomic developments, November 2018 Indicators of global economic activity suggest a continuation of solid growth in the final quarter

EU steel market situation and outlook. Key challenges

70th Session of the OECD Steel Committee Paris, 12 13 May 2011 EU steel market situation and outlook http://www.eurofer.org/index.php/eng/issues-positions/economic-development-steel-market Key challenges

70th Session of the OECD Steel Committee Paris, 12 13 May 2011 EU steel market situation and outlook http://www.eurofer.org/index.php/eng/issues-positions/economic-development-steel-market Key challenges

Economics Update. Andrew Smith. February

Economics Update Andrew Smith February 2017 Twitter: @AndrewSmithEcon World economy reflating? Annual growth forecasts (%) 2013 2014 2015 2016 (e) 2017 (f) 2018 (f) US 2.2 2.4 2.6 1.6 2.3 2.5 Japan 1.6

Economics Update Andrew Smith February 2017 Twitter: @AndrewSmithEcon World economy reflating? Annual growth forecasts (%) 2013 2014 2015 2016 (e) 2017 (f) 2018 (f) US 2.2 2.4 2.6 1.6 2.3 2.5 Japan 1.6

SME Monitor Q aldermore.co.uk

SME Monitor Q1 2014 aldermore.co.uk aldermore.co.uk Contents Executive summary UK economic overview SME inflation index one year review SME cost inflation trends SME business confidence SME credit conditions

SME Monitor Q1 2014 aldermore.co.uk aldermore.co.uk Contents Executive summary UK economic overview SME inflation index one year review SME cost inflation trends SME business confidence SME credit conditions

Main Economic & Financial Indicators Poland

Main Economic & Financial Indicators Poland. 6 OCTOBER 2015 NAOKO ISHIHARA ECONOMIST ECONOMIC RESEARCH OFFICE (LONDON) T +44-(0)20-7577-2179 E naoko.ishihara@uk.mufg.jp The Bank of Tokyo-Mitsubishi UFJ,

Main Economic & Financial Indicators Poland. 6 OCTOBER 2015 NAOKO ISHIHARA ECONOMIST ECONOMIC RESEARCH OFFICE (LONDON) T +44-(0)20-7577-2179 E naoko.ishihara@uk.mufg.jp The Bank of Tokyo-Mitsubishi UFJ,

Emerging Markets Equities VALUE COULD EXTEND THE EMERGING MARKETS RALLY

PRICE POINT December 2017 Timely intelligence and analysis for our clients. Emerging Markets Equities VALUE COULD EXTEND THE EMERGING MARKETS RALLY KEY POINTS Emerging markets (EM) equities have extended

PRICE POINT December 2017 Timely intelligence and analysis for our clients. Emerging Markets Equities VALUE COULD EXTEND THE EMERGING MARKETS RALLY KEY POINTS Emerging markets (EM) equities have extended

Strengths (+) and weaknesses ( )

and weaknesses ( )") Country Report Australia Country Report Marcel Weernink Economic growth in Australia decelerates due to lower mining investments. The outlook depends heavily on demand from China for its commodities and

Country Report Australia Country Report Marcel Weernink Economic growth in Australia decelerates due to lower mining investments. The outlook depends heavily on demand from China for its commodities and

Economic Indicators. Roland Berger Institute

Economic Indicators Roland Berger Institute October 2017 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Economic Indicators Roland Berger Institute October 2017 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

ECONOMY REPORT - CHINESE TAIPEI

ECONOMY REPORT - CHINESE TAIPEI (Extracted from 2001 Economic Outlook) REAL GROSS DOMESTIC PRODUCT The Chinese Taipei economy grew strongly during the first three quarters of 2000, thanks largely to robust

ECONOMY REPORT - CHINESE TAIPEI (Extracted from 2001 Economic Outlook) REAL GROSS DOMESTIC PRODUCT The Chinese Taipei economy grew strongly during the first three quarters of 2000, thanks largely to robust

BASE METALS - MONTHLY

June 6, 2011 BASE METALS - MONTHLY Base metal prices ended largely lower on the back of re-emergence of concerns from the Euro-zone, weak economic data and expectation of decline in demand. European debt

June 6, 2011 BASE METALS - MONTHLY Base metal prices ended largely lower on the back of re-emergence of concerns from the Euro-zone, weak economic data and expectation of decline in demand. European debt

Baseline U.S. Economic Outlook, Summary Table*

March 19 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Weak February Job Growth, and

March 19 Gus Faucher Stuart Hoffman William Adams Kurt Rankin Abbey Omodunbi Chief Economist Senior Economic Advisor Senior Economist Economist Economist Executive Summary Weak February Job Growth, and

9 March 2018 AUSTRALIAN ECONOMIC DEVELOPMENTS. Services and construction stay on track in February

AUSTRALIAN ECONOMIC DEVELOPMENTS 9 March 2018 This week the Reserve Bank of Australia (RBA) left the cash rate on hold at a record low of 1.50%, where it has been since August 2016. The accompanying statement

AUSTRALIAN ECONOMIC DEVELOPMENTS 9 March 2018 This week the Reserve Bank of Australia (RBA) left the cash rate on hold at a record low of 1.50%, where it has been since August 2016. The accompanying statement

Teetering on the brink: is the world heading for another financial crisis?

Teetering on the brink: is the world heading for another financial crisis? Adrian Cooper CEO & Chief Economist acooper@oxfordeconomics.com Peter Suomi Director petersuomi@oxfordeconomics.com October 2011

Teetering on the brink: is the world heading for another financial crisis? Adrian Cooper CEO & Chief Economist acooper@oxfordeconomics.com Peter Suomi Director petersuomi@oxfordeconomics.com October 2011