Rate Setting for Service Centers The Basics. Caroline Beeman August 14, 2018

|

|

|

- Rosamund Armstrong

- 5 years ago

- Views:

Transcription

1 Rate Setting for Service Centers The Basics Caroline Beeman August 14,

2 MAXIMUS Higher Education Practice Serves more than 150 colleges, universities and university hospitals in 49 states plus Puerto Rico and the U.S. Virgin Islands 90 of top 100 research institutions Ranging from <$1M to >$1B in research Headquartered in Northbrook, Illinois Satellite offices in: Denver and Colorado Springs, Colorado Lexington, Kentucky Columbus, Ohio Phoenix, Arizona Charlottesville, Virginia Bluffton, South Carolina MAXIMUS is a leading provider of government services worldwide with more than 20,000 employees and >$2.0 billion annual revenue Gives our practice unparalleled financial stability and the resources to invest in developing expertise in federal regulations and guidance, e.g. 2 CFR Part 200 A CPE credit certificate (for 1 hour CPE) is available for a small administrative fee of $20 2

and Direct Costing Policy Service Centers and/or Recharge Centers Rates and Policies F&A Software Comprehensive Rate Information System (CRIS ) 150+ universities use CRIS WebSpace")

3 F&A and Other Rate Consulting Services F&A Cost Rate Proposal Preparation (Long and Short Form) and Negotiation (DHHS CAS & ONR/DCAA) Space Surveys/Reviews Fringe Benefit Rates Federal Disclosure Statement (DS 2) and Direct Costing Policy Service Centers and/or Recharge Centers Rates and Policies F&A Software Comprehensive Rate Information System (CRIS ) 150+ universities use CRIS WebSpace Space Utilization Software 50+ universities use WebSpace 3

4 MAXIMUS Higher Education Products & Services Grant Management Compliance and Internal Controls Effort Reporting Consulting and Software Uniform Guidance Diagnostic High Level Review Federal Compliance/Risk Assessment (C/RA) In-depth Review Grant Management Help Desk Services Online Grant Management and Onsite Faculty Training Learning Management and Continuing Education Software Research Operational Reviews Business Process Review and Improvement Policy and Procedure Assistance Transition Staffing Audit Response Assistance Export Control Compliance And more 4

5 Agenda Terminology Basic Rate Setting Principles Rates for External Users Determine the Base (Usage) Subsidies Federal and Non-Federal Rates Calculate the Over (Under) Recovery Reserve Accounts Sample Rate Template with Over (Under) Recovery 5

6 Terminology Each University has its own terminology Service center means SSF in some schools Recharge center Core same as recharge center in some schools Internal service provider Auxiliary in Florida, includes recharge centers and SSF 6

7 Basic Rate Setting Principles Actual cost is the most the rate is allowed to recover Only allowable cost can be included in federal rate Retain documentation of the rate calculation Rates must be reviewed and approved on a regular basis Regular basis means no less than every other year, i.e. biennually Rates must be adjusted when incoming funds exceed expenses (surplus balance) or else refunds must be issued Guidance is different for external users 7

8 Rates for External Users Different rules than for Federal and Internal Users The use of market prices may be appropriate Charges may include F&A plus fee in excess of costs This additional income is not used in the calculation of surplus/deficit balance Caution Recoveries in excess of full cost might be Program Income 8

9 Rate Calculation Annual Rate = Annual Costs / Total Annual Usage 9

10 Define Good or Service to Sell Microscope Lab Use of Microscope Zebra Fish Facility Fish Super Computing Facility Excess CPU Technical Rate Rack Space; 24 Hour Service; Connectivity Charge; Technical Labor Stores Facility Chemicals, Lab Supplies & Purchasing Services 10

11 Goal in Determining the Proper Unit Use the measurement which allocates costs equitably among all users For example, a center that performs tests on samples has two possible units of measure; it could charge per test, or per hour. If some tests take twice as long as others, and labor is a large portion of the cost of performing a test it is not equitable to charge each user on a per test basis. In such circumstances, the user rate will be on a per hour basis. 11

12 Evaluate Customer Base Internal University Sponsored Program Areas University Departments External Those who do not have a University account number Industry Students, faculty or staff acting in a personal capacity Estimate How Many Customers (Rate is a function of the Operating Costs/Users (Use) of the Service) 12

13 Estimating Usage In order to estimate usage, prior year(s) numbers can be used as a starting point and adjusted for anticipated changes. Centers without sufficient usage history can use available units as a starting point and adjust for downtime and other intervening factors. 13

14 Subsidies: NIH + University Funds Support a Core Total Allowable Direct Cost $110,000 NIH Direct Funding to Core - $ 60,000 Institution's Funding to Core - $ 10,000 Net Recoverable Cost $ 40,000 Number of service units 1,000 Net cost/unit $40 (Federal Rate) 100 External User units $110,000 1,000 = $110 plus F&A at 50% $110 x 50% = $55 External User rate $165 14

15 Federal Rate 15

16 Non-Federal Rate 16

17 Calculate the Over (Under) Recovery Fund Balance - Over (Under) Recovery Fund Balance - Surplus - End of Year $ 77,700 Cash Expenditures, excludes depreciation 166, Day Working Capital Limit 60 Working Capital Allowance 27,667 Fund Balance - Over (Under) Recovery $ 50,033 17

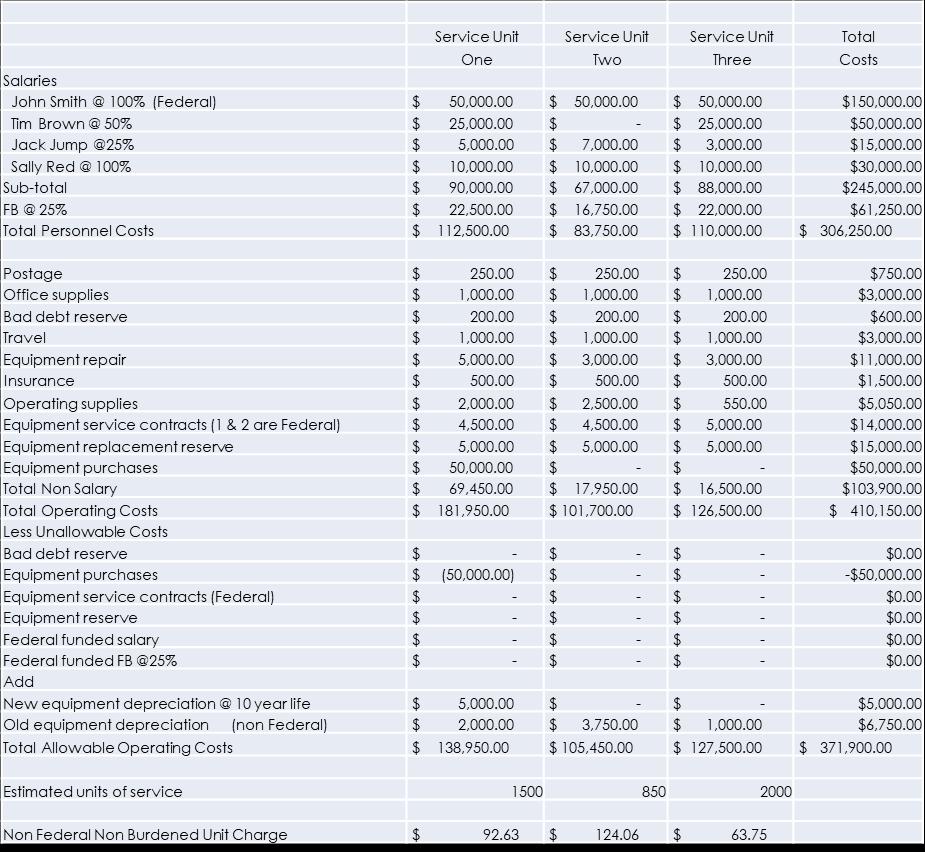

18 Example that includes adjustment for (Over) Under Recovery Service Center - Rate Calculation Personnel Expenses: Salaries/Wages: Base Salaries Projected Increase Projected Salaries % FTE on Service Center Total Center Expenses Staff Assist Rate Machine Rate Manager (at 100% of base salary) $ 60,000 3% $ 61, % $ 61,500 54,546 6,954 Technician (at 60% of base salary) $ 50,000 3% $ 51,500 60% $ 30,900 28,804 2,096 Total Salaries & Wages $ 110,000 $ 113,000 $ 92,400 83,350 9,050 Fringe benefits (S&W Center Expenses at 34.0% Rate) 34% 31,416 28,339 3,077 Non-Personnel Expenses: Materials and Supplies 1,500 1,500 Maintenance contract 2,000 2,000 Equipment (non-capitalized) 9,000 9,000 Security software - licensing and software (non-capitalized) 30,000 5,000 Equipment depreciation 40,000 15,000 (Over) Under Recovery (50,000) (41,000) (9,000) Total Operating Expenses $ 156,316 $ 70,689 $ 35,627 Base: Billable Staff Assist Hours 2,547 Billable Machine Hours 2,934 Internal Rates $ $

19 Rate Templates Can Be Very Complex 19

20 Reserve Account A reserve account is used to hold balances and record transactions that don t directly affect the rate charged to recharge center customers. If recharge or cost centers want to include equipment depreciation in the recharge rates, they should have a reserve budget. 20

")

21 Example: Depreciation, Reserve, Subsidy, Y/E Balance (page 1) 21

")

22 Example: Depreciation, Reserve, Subsidy, Y/E Balance (page 2) 22

23 Example: Depreciation, Reserve, Subsidy, Y/E Balance (page 3) 23

24 Summary of Key Compliance Issues Rates should recover no more than the cost of the good or service Rates must breakeven over time, reviewed and adjusted at least every two years Rates don t discriminate between users, especially those paying with federal funds Surpluses should not be used to fund unrelated activities Must maintain an official published price list after appropriate approvals have been obtained 24

25 Upcoming Webinars and Annual Meeting Tricks and Tips for Reporting in CRIS October 18 2:00 p.m. ET Pre-award Costs and Responsible Stewardship November 6 2:00 p.m. ET 31 st Annual MAXIMUS Higher Education Practice Meeting September Hilton Clearwater Beach, Florida 25

26 Slides should be available in link on survey when you exit webinar. If not, 26

MAXIMUS Higher Education Practice. Denver, CO; Charlotte, NC; Columbus, OH; Phoenix, AZ; Charlottesville, VA; Bluffton, SC; Colorado Springs, CO

Service Centers the Basics Caroline Beeman, MS, CRA Senior Manager April 26, 2016 1 MAXIMUS Higher Education Practice Headquartered in Northbrook, IL o Satellite Offices in: Denver, CO; Charlotte, NC;

Service Centers the Basics Caroline Beeman, MS, CRA Senior Manager April 26, 2016 1 MAXIMUS Higher Education Practice Headquartered in Northbrook, IL o Satellite Offices in: Denver, CO; Charlotte, NC;

Service Centers Questions and Answers

Service Centers Questions and Answers Caroline Beeman, MS, CRA Senior Manager May 16, 2017 1 MAXIMUS Higher Education Practice Headquartered in Northbrook, IL o Satellite Offices in: Denver, CO; Lexington,

Service Centers Questions and Answers Caroline Beeman, MS, CRA Senior Manager May 16, 2017 1 MAXIMUS Higher Education Practice Headquartered in Northbrook, IL o Satellite Offices in: Denver, CO; Lexington,

Service Centers: Financial Compliance

Service Centers: Financial Compliance What You Need to Know Jennifer (Wei) Mitchell Director of Cost Studies Northwestern University Wendy Meister Director, Education & Life Sciences Huron Consulting Group

Service Centers: Financial Compliance What You Need to Know Jennifer (Wei) Mitchell Director of Cost Studies Northwestern University Wendy Meister Director, Education & Life Sciences Huron Consulting Group

DIVISION OF RESEARCH RECHARGE FACILITIES OPERATING PROCEDURES. August SW 8th Street MARC 430 Miami, FL

DIVISION OF RESEARCH RECHARGE FACILITIES OPERATING PROCEDURES August 2013 11200 SW 8th Street MARC 430 Miami, FL 33199 http://research.fiu.edu Table of Contents Recharge Service Facility Operating Procedures

DIVISION OF RESEARCH RECHARGE FACILITIES OPERATING PROCEDURES August 2013 11200 SW 8th Street MARC 430 Miami, FL 33199 http://research.fiu.edu Table of Contents Recharge Service Facility Operating Procedures

Federal Compliance Webinar Series 2 CFR 200 Uniform Guidance Kris Rhodes, Director Jason Guilbeault, Senior Consultant

Federal Compliance Webinar Series 2 CFR 200 Uniform Guidance Kris Rhodes, Director Jason Guilbeault, Senior Consultant 1 MAXIMUS Higher Education Practice Headquartered in Northbrook, IL Satellite Offices

Federal Compliance Webinar Series 2 CFR 200 Uniform Guidance Kris Rhodes, Director Jason Guilbeault, Senior Consultant 1 MAXIMUS Higher Education Practice Headquartered in Northbrook, IL Satellite Offices

University of Delaware Service Center/Recharge Centers/Core Facilities. June 13, 2017

University of Delaware Service Center/Recharge Centers/Core Facilities June 13, 2017 Agenda 1. Purpose 2. Policy 3. Types 4. Federal Guidelines 5. Accounting for Service Centers 6. Capital Equipment and

University of Delaware Service Center/Recharge Centers/Core Facilities June 13, 2017 Agenda 1. Purpose 2. Policy 3. Types 4. Federal Guidelines 5. Accounting for Service Centers 6. Capital Equipment and

F&A Methodologies- Short Form Schools with Long Form Consideration. August 15, 2017

F&A Methodologies- Short Form Schools with Long Form Consideration August 15, 2017 1 Agenda Overview of F&A Short Form (SF) Methodology Long Form (LF) Methodology Differences between Short Form & Long

F&A Methodologies- Short Form Schools with Long Form Consideration August 15, 2017 1 Agenda Overview of F&A Short Form (SF) Methodology Long Form (LF) Methodology Differences between Short Form & Long

Determine and Develop Recharge Centers. January 16, 2015 University of Central Florida Steve Koogler, Compliance Manager

Determine and Develop Recharge Centers January 16, 2015 University of Central Florida Steve Koogler, Compliance Manager Goals for Today s Session Define a Service/Recharge Center and its characteristics

Determine and Develop Recharge Centers January 16, 2015 University of Central Florida Steve Koogler, Compliance Manager Goals for Today s Session Define a Service/Recharge Center and its characteristics

Deans, Directors, Department Heads, Business Administrators, Faculty, Finance Personnel, and Sponsored Project Personnel

Title: Applicable to: Recharge Center and Pass-Through Activity Guidelines Deans, Directors, Department Heads, Business Administrators, Faculty, Finance Personnel, and Sponsored Project Personnel Effective

Title: Applicable to: Recharge Center and Pass-Through Activity Guidelines Deans, Directors, Department Heads, Business Administrators, Faculty, Finance Personnel, and Sponsored Project Personnel Effective

SERVICE CENTERS. This policy has been established to ensure compliance with Federal regulations.

Issuing Authority: Office of Financial Services Effective Date: October 1, 2003 Policy: It is the policy of the California Institute of Technology (Caltech) to periodically review and adjust as appropriate

Issuing Authority: Office of Financial Services Effective Date: October 1, 2003 Policy: It is the policy of the California Institute of Technology (Caltech) to periodically review and adjust as appropriate

SERVICE CENTERS: The Not So Simple Basics

SERVICE CENTERS: The Not So Simple Basics Establishing FRA Conference New Orleans March 13-15, 2013 Sarah T Axelrod Director of Cost Analysis and Compliance Harvard University Jim Carter Senior Director

SERVICE CENTERS: The Not So Simple Basics Establishing FRA Conference New Orleans March 13-15, 2013 Sarah T Axelrod Director of Cost Analysis and Compliance Harvard University Jim Carter Senior Director

Procedures for Service Centers

OVERVIEW Procedures for Service Centers Guidelines of Service Centers Service Centers are entities within the University established for the specific purpose of providing product(s) or service(s) to other

OVERVIEW Procedures for Service Centers Guidelines of Service Centers Service Centers are entities within the University established for the specific purpose of providing product(s) or service(s) to other

SERVICE CENTER POLICY

SERVICE CENTER POLICY SCOPE This policy sets forth the California Institute of Technology's (Caltech) policy on service centers. This policy applies to all Caltech service centers. Auxiliary services are

SERVICE CENTER POLICY SCOPE This policy sets forth the California Institute of Technology's (Caltech) policy on service centers. This policy applies to all Caltech service centers. Auxiliary services are

University of Mississippi Medical Center Policy on Service Centers

I. Purpose University of Mississippi Medical Center Policy on Service Centers As a recipient of federal funding, UMMC is required to comply with the cost requirements of the Office of Management Budget

I. Purpose University of Mississippi Medical Center Policy on Service Centers As a recipient of federal funding, UMMC is required to comply with the cost requirements of the Office of Management Budget

Research & Sponsored Programs Accounting Policy Recharge Centers and Annual Approval of Rates POLICY STATEMENT

Research & Sponsored Programs Accounting Research & Sponsored Programs Accounting Policy Recharge Centers and Annual Approval of Rates Responsible Executive: Controller Responsible Department: RSPA Review

Research & Sponsored Programs Accounting Research & Sponsored Programs Accounting Policy Recharge Centers and Annual Approval of Rates Responsible Executive: Controller Responsible Department: RSPA Review

University of Nebraska at Omaha Service Center Procedure Appendix to Service Center Policy

University of Nebraska at Omaha Service Center Procedure Appendix to Service Center Policy I. Introduction These procedures provide a framework for the fiscal operations of the University of Nebraska at

University of Nebraska at Omaha Service Center Procedure Appendix to Service Center Policy I. Introduction These procedures provide a framework for the fiscal operations of the University of Nebraska at

VANDERBILT UNIVERSITY SERVICE CENTER POLICY

VANDERBILT UNIVERSITY SERVICE CENTER POLICY EFFECTIVE DATE: JULY 1, 2008 UPDATED: MAY 2017 I. POLICY STATEMENT Vanderbilt University operating units that charge internal users for goods and services are

VANDERBILT UNIVERSITY SERVICE CENTER POLICY EFFECTIVE DATE: JULY 1, 2008 UPDATED: MAY 2017 I. POLICY STATEMENT Vanderbilt University operating units that charge internal users for goods and services are

Service Center Training

Service Center Training January 23 & 24, 2013 Sarah T Axelrod, Director of Cost Analysis & Compliance, OSP sarah_axelrod@harvard.edu Patrick Fitzgerald, Assoc. Dean for Research Administration, FAS pwf@fas.harvard.edu

Service Center Training January 23 & 24, 2013 Sarah T Axelrod, Director of Cost Analysis & Compliance, OSP sarah_axelrod@harvard.edu Patrick Fitzgerald, Assoc. Dean for Research Administration, FAS pwf@fas.harvard.edu

Purdue University Recharge Center Policy INTRODUCTION

Purdue University Recharge Center Policy INTRODUCTION The authority for the establishment of rates, fees and charges for Purdue University is vested in the Board of Trustees and has been delegated in specific

Purdue University Recharge Center Policy INTRODUCTION The authority for the establishment of rates, fees and charges for Purdue University is vested in the Board of Trustees and has been delegated in specific

SERVICE CENTER GUIDELINES

SERVICE CENTER GUIDELINES I. Introduction Service Centers are units within University of Rochester Cost Centers that charge for goods or services in direct support of the research or academic missions

SERVICE CENTER GUIDELINES I. Introduction Service Centers are units within University of Rochester Cost Centers that charge for goods or services in direct support of the research or academic missions

Service Center Procedure Appendix to Service Center Policy

Service Center Procedure Appendix to Service Center Policy I. Introduction These procedures provide a framework for the fiscal operations of the University of Nebraska at Omaha (UNO) service centers that

Service Center Procedure Appendix to Service Center Policy I. Introduction These procedures provide a framework for the fiscal operations of the University of Nebraska at Omaha (UNO) service centers that

Core Research Facilities Guidelines Table of Contents

Core Research Facilities Guidelines Table of Contents 1. Purpose 2 2. Definitions 2 3. Criteria & Characteristics of Core Research Facility (CRF) and Department Core (DC) 3 4. Establishing a Core Facility

Core Research Facilities Guidelines Table of Contents 1. Purpose 2 2. Definitions 2 3. Criteria & Characteristics of Core Research Facility (CRF) and Department Core (DC) 3 4. Establishing a Core Facility

UCSF Sales and Service Center Policy Guidance and Procedures Manual

UCSF Sales and Service Center Policy Guidance and Procedures Manual Effective Date: 9/28/2016 Office of Origin: Finance Budget and Resource Management Table of Contents SECTION I: PURPOSE... 3 SECTION

UCSF Sales and Service Center Policy Guidance and Procedures Manual Effective Date: 9/28/2016 Office of Origin: Finance Budget and Resource Management Table of Contents SECTION I: PURPOSE... 3 SECTION

Dartmouth College. Service and Recharge Center Policies and Procedures. Dartmouth College Office of the Controller

Dartmouth College Service and Recharge Center Policies and Procedures Dartmouth College Office of the Controller June 2008 CONTENTS I. Introduction...1 II. General Policies...3 III. Service Center Practices

Dartmouth College Service and Recharge Center Policies and Procedures Dartmouth College Office of the Controller June 2008 CONTENTS I. Introduction...1 II. General Policies...3 III. Service Center Practices

Service Centers. University of Arkansas

Service Centers University of Arkansas What is a service center Why do I need a rate? What is our policy? What is our process? Topics to Cover What is a Service Center Org unit that charges for goods or

Service Centers University of Arkansas What is a service center Why do I need a rate? What is our policy? What is our process? Topics to Cover What is a Service Center Org unit that charges for goods or

University of Alaska Statewide Accounting Manual No.: P Date: 2/19/02 Page: 1 of 10. Service/Recharge Centers. Purpose and Scope:

Page: 1 of 10 Purpose and Scope: To provide guidelines for accounting and operation of service (recharge-type) centers and ensure compliance with federal requirements for recharge-type activity. These

Page: 1 of 10 Purpose and Scope: To provide guidelines for accounting and operation of service (recharge-type) centers and ensure compliance with federal requirements for recharge-type activity. These

Project Management of the F&A Process April 10, 2018

Project Management of the F&A Process April 10, 2018 1 Five Phases of Project Management Phase 1- Planning and Assessment Phase 2- Define Major Phases Phase 3- Execution of Tasks Phase 4- Monitoring and

Project Management of the F&A Process April 10, 2018 1 Five Phases of Project Management Phase 1- Planning and Assessment Phase 2- Define Major Phases Phase 3- Execution of Tasks Phase 4- Monitoring and

SECTION 109 HOST STATE LOAN-TO-DEPOSIT RATIOS. The Board of Governors of the Federal Reserve System, the Federal Deposit Insurance

SECTION 109 HOST STATE LOAN-TO-DEPOSIT RATIOS The Board of Governors of the Federal Reserve System, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency (the agencies)

SECTION 109 HOST STATE LOAN-TO-DEPOSIT RATIOS The Board of Governors of the Federal Reserve System, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency (the agencies)

COLORADO STATE UNIVERSITY-PUEBLO

COLORADO STATE UNIVERSITY-PUEBLO 1. Title: Self-Funded Activities 2. Purpose and Effect: This procedure provides guidelines for establishing, costing, pricing, and administering departmental self-funded

COLORADO STATE UNIVERSITY-PUEBLO 1. Title: Self-Funded Activities 2. Purpose and Effect: This procedure provides guidelines for establishing, costing, pricing, and administering departmental self-funded

Oklahoma State University Policy and Procedures

Oklahoma State University Policy and Procedures STORES 4-0140 BUSINESS & EXTERNAL RELATIONS Controller July 1996 INTRODUCTION AND SUMMARY 1.01 This policy provides a framework for the fiscal operations

Oklahoma State University Policy and Procedures STORES 4-0140 BUSINESS & EXTERNAL RELATIONS Controller July 1996 INTRODUCTION AND SUMMARY 1.01 This policy provides a framework for the fiscal operations

Understanding F&A Rates. OPTIONAL SUBHEAD HERE Sara Tarkington January 23 rd, 2018

OPTIONAL SUBHEAD HERE Sara Tarkington January 23 rd, 2018 Why an F&A Cost Rate? It is federal policy to provide for the reimbursement of F&A costs except when specific limitations and prohibitions exist

OPTIONAL SUBHEAD HERE Sara Tarkington January 23 rd, 2018 Why an F&A Cost Rate? It is federal policy to provide for the reimbursement of F&A costs except when specific limitations and prohibitions exist

Income from U.S. Government Obligations

Baird s ----------------------------------------------------------------------------------------------------------------------------- --------------- Enclosed is the 2017 Tax Form for your account with

Baird s ----------------------------------------------------------------------------------------------------------------------------- --------------- Enclosed is the 2017 Tax Form for your account with

Service Center Policy and Procedures University at Albany

Service Center Policy and Procedures University at Albany Prepared by: Office of the Controller University at Albany Review Date: March 24, 2017 Table of Contents 1. Regulations 2 2. Definitions.. 3 3.

Service Center Policy and Procedures University at Albany Prepared by: Office of the Controller University at Albany Review Date: March 24, 2017 Table of Contents 1. Regulations 2 2. Definitions.. 3 3.

Research Service Centers (RSC) and Core Facilities. July 31, 2014

and Core Facilities. July 31, 2014") Research Service Centers (RSC) and Core Facilities July 31, 2014 Today s Presenters Brian Bertlshofer Director, Cost Analysis bertlsbj@email.unc.edu (919) 843-4891 Trent Riley Cost Analyst trent_riley@unc.edu

Research Service Centers (RSC) and Core Facilities July 31, 2014 Today s Presenters Brian Bertlshofer Director, Cost Analysis bertlsbj@email.unc.edu (919) 843-4891 Trent Riley Cost Analyst trent_riley@unc.edu

Research Foundation of the City University of New York Service/Recharge Center Accounting & Operating Procedures

Research Foundation of the City University of New York Service/Recharge Center Accounting & Operating Procedures The establishment of a new Service or Recharge Center requires the permission of the Head

Research Foundation of the City University of New York Service/Recharge Center Accounting & Operating Procedures The establishment of a new Service or Recharge Center requires the permission of the Head

Section 22 Self-Supporting/Revenue Generating - Service and Storeroom Activities

Section 22 Self-Supporting/Revenue Generating - Service and Storeroom Activities Welcome to the Office of Business and Financial Services Open Comment Blog! The University of Illinois System, Office of

Section 22 Self-Supporting/Revenue Generating - Service and Storeroom Activities Welcome to the Office of Business and Financial Services Open Comment Blog! The University of Illinois System, Office of

Appendix. 1.0 Nondiscriminatory Rates. 2.0 Users. 3.0 Rate Components. 2.1 Internal Users. 2.2 External Users. 2.

Appendix 1.0 Nondiscriminatory Rates A Center must charge all internal users at the same rate for the same level of services or products purchased in the same circumstances. Rates should not differentiate

Appendix 1.0 Nondiscriminatory Rates A Center must charge all internal users at the same rate for the same level of services or products purchased in the same circumstances. Rates should not differentiate

Creating a Decision Tree: Exemptions and Deductions

Creating a Decision Tree: Exemptions and Deductions Marilyn Henry UnitedHealth Group Loredana Pfannenbecker PwC 1 UPPO Presentation Disclaimer Use of the Unclaimed Property Professionals Organization,

Creating a Decision Tree: Exemptions and Deductions Marilyn Henry UnitedHealth Group Loredana Pfannenbecker PwC 1 UPPO Presentation Disclaimer Use of the Unclaimed Property Professionals Organization,

GENERAL INSTRUCTIONS--Continuation Sheet... COVER SHEET AND CERTIFICATION... C-1. PART I General Information... I-1. Indirect Costs...

Revision Number 1 Effective Date June 30, 2006 INDEX GENERAL INSTRUCTIONS--Continuation Sheet.............. (i) COVER SHEET AND CERTIFICATION................... C-1 PART I General Information..................

Revision Number 1 Effective Date June 30, 2006 INDEX GENERAL INSTRUCTIONS--Continuation Sheet.............. (i) COVER SHEET AND CERTIFICATION................... C-1 PART I General Information..................

TA X FACTS NORTHERN FUNDS 2O17

TA X FACTS 2O17 Northern Funds Tax Facts provides specific information about your Northern Funds investment income and capital gain distributions for 2017. If you have any questions about how to apply

TA X FACTS 2O17 Northern Funds Tax Facts provides specific information about your Northern Funds investment income and capital gain distributions for 2017. If you have any questions about how to apply

Form 1410 FR.14 Instructions Internal Service Providers: Rate Calculation (Manual) Revision Date: 05/31/2018

Revision Date: 05/31/2018") Form 1410 FR.14 Instructions Internal Service Providers: Rate Calculation (Manual) Revision Date: 05/31/2018 Overview All Specialized Service Facilities (SSFs) and Recharge Centers (as defined in Yale

Form 1410 FR.14 Instructions Internal Service Providers: Rate Calculation (Manual) Revision Date: 05/31/2018 Overview All Specialized Service Facilities (SSFs) and Recharge Centers (as defined in Yale

PAY STATEMENT REQUIREMENTS

PAY MENT 2017 PAY MENT Alabama Alaska Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia No generally applicable wage payment law for private employers. Rate

PAY MENT 2017 PAY MENT Alabama Alaska Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia No generally applicable wage payment law for private employers. Rate

University of Massachusetts Amherst SERVICE CENTER GUIDELINES Definition of a Service Center

University of Massachusetts Amherst SERVICE CENTER GUIDELINES Definition of a Service Center Service centers are operating units established for the primary purpose of providing goods or services to the

University of Massachusetts Amherst SERVICE CENTER GUIDELINES Definition of a Service Center Service centers are operating units established for the primary purpose of providing goods or services to the

STATE FRANCHISE DISCLOSURE AND REGISTRATION LAWS

STATE FRANCHISE DISCLOSURE AND REGISTRATION LAWS 2015 Keith J. Kanouse Kanouse & Walker, P.A. One Boca Place, Suite 324 Atrium 2255 Glades Road Boca Raton, Florida 33431 Telephone: (561) 451-8090 Fax:

STATE FRANCHISE DISCLOSURE AND REGISTRATION LAWS 2015 Keith J. Kanouse Kanouse & Walker, P.A. One Boca Place, Suite 324 Atrium 2255 Glades Road Boca Raton, Florida 33431 Telephone: (561) 451-8090 Fax:

Motor Vehicle Sales/Use, Tax Reciprocity and Rate Chart-2005

The following is a Motor Vehicle Sales/Use Tax Reciprocity and Rate Chart which you may find helpful in determining the Sales/Use Tax liability of your customers who either purchase vehicles outside of

The following is a Motor Vehicle Sales/Use Tax Reciprocity and Rate Chart which you may find helpful in determining the Sales/Use Tax liability of your customers who either purchase vehicles outside of

Business Process Management for Government Helping Government Serve the People. MAXIMUS Federal Services RAC Summit December 5, 2013

Helping Government Serve the People MAXIMUS Federal Services RAC Summit December 5, 2013 MAXIMUS Federal Services RAC Summit QIC Program MAXIMUS Federal Services QIC Part A Appellant Tips/Best Practices

Helping Government Serve the People MAXIMUS Federal Services RAC Summit December 5, 2013 MAXIMUS Federal Services RAC Summit QIC Program MAXIMUS Federal Services QIC Part A Appellant Tips/Best Practices

Implementation Guidelines for Establishing Service Centers and Recharge Centers Charging Sponsored Projects

Responsible University Official: AVP & Comptroller Responsible Office: Financial Reporting Services Implementation Guidelines for Establishing Service Centers and Recharge Centers Charging Sponsored Projects

Responsible University Official: AVP & Comptroller Responsible Office: Financial Reporting Services Implementation Guidelines for Establishing Service Centers and Recharge Centers Charging Sponsored Projects

The table below reflects state minimum wages in effect for 2014, as well as future increases. State Wage Tied to Federal Minimum Wage *

State Minimum Wages The table below reflects state minimum wages in effect for 2014, as well as future increases. Summary: As of Jan. 1, 2014, 21 states and D.C. have minimum wages above the federal minimum

State Minimum Wages The table below reflects state minimum wages in effect for 2014, as well as future increases. Summary: As of Jan. 1, 2014, 21 states and D.C. have minimum wages above the federal minimum

Overview of the Investing in Manufacturing Communities Partnership Initiative. Special Webinar Briefing May 23, 2013

Overview of the Investing in Manufacturing Communities Partnership Initiative Special Webinar Briefing May 23, 2013 Mission Statement EDA s mission is to lead the federal economic development agenda by

Overview of the Investing in Manufacturing Communities Partnership Initiative Special Webinar Briefing May 23, 2013 Mission Statement EDA s mission is to lead the federal economic development agenda by

HARVARD UNIVERSITY. Academic Service Center Procedures Manual

HARVARD UNIVERSITY Academic Service Center Procedures Manual Updated 12/18/2014 Table of Contents Introduction 4 Definition of an Academic Service Center 4 Compliance - why we care 4 Purpose and Audience

HARVARD UNIVERSITY Academic Service Center Procedures Manual Updated 12/18/2014 Table of Contents Introduction 4 Definition of an Academic Service Center 4 Compliance - why we care 4 Purpose and Audience

Motor Vehicle Sales Tax Rates by State as of December 31, 2013 And Tax Credit Application

Florida Department of Revenue Tax Information Publication TIP No: 14A01-01 Date Issued: February 25, 2014 Motor Vehicle Rates by State as of December 31, 2013 And Tax Credit Application Motor Vehicles

Florida Department of Revenue Tax Information Publication TIP No: 14A01-01 Date Issued: February 25, 2014 Motor Vehicle Rates by State as of December 31, 2013 And Tax Credit Application Motor Vehicles

Interest Table 01/04/2010

The following table provides information on the interest charged by each of the 50 states and its territories: FOR THE UNITED S AND TERRITORIES Alabama Alaska Arizona Arkansas California Colorado Connecticut

The following table provides information on the interest charged by each of the 50 states and its territories: FOR THE UNITED S AND TERRITORIES Alabama Alaska Arizona Arkansas California Colorado Connecticut

Accounting Overview Training

Accounting Services Accounting Overview Training Revised April 24, 2014 Purpose To provide University Business Managers and Financial Administrators with: 1. A basic understanding of the authoritative

Accounting Services Accounting Overview Training Revised April 24, 2014 Purpose To provide University Business Managers and Financial Administrators with: 1. A basic understanding of the authoritative

Federal Reserve Bank of Dallas. July 15, 2005 SUBJECT. Banking Agencies Issue Host State Loan-to-Deposit Ratios DETAILS

Federal Reserve Bank of Dallas 2200 N. PEARL ST. DALLAS, TX 75201-2272 July 15, 2005 Notice 05-37 TO: The Chief Executive Officer of each financial institution and others concerned in the Eleventh Federal

Federal Reserve Bank of Dallas 2200 N. PEARL ST. DALLAS, TX 75201-2272 July 15, 2005 Notice 05-37 TO: The Chief Executive Officer of each financial institution and others concerned in the Eleventh Federal

504 Loan Program Rural Initiative - Waiver of Limitation on Lending Authority

This document is scheduled to be published in the Federal Register on 07/19/2018 and available online at https://federalregister.gov/d/2018-15312, and on govinfo.gov Billing Code: 8025-01 SMALL BUSINESS

This document is scheduled to be published in the Federal Register on 07/19/2018 and available online at https://federalregister.gov/d/2018-15312, and on govinfo.gov Billing Code: 8025-01 SMALL BUSINESS

INTERNAL REVENUE SERVICE. Tax Exempt and Government Entities (TE/GE) Operating Division. Federal, State and Local Governments

Operating Division. Federal, State and Local Governments") INTERNAL REVENUE SERVICE Tax Exempt and Government Entities (TE/GE) Operating Division Federal, State and Local Governments Federal, State and Local Governments The office of Federal State and Local Governments

INTERNAL REVENUE SERVICE Tax Exempt and Government Entities (TE/GE) Operating Division Federal, State and Local Governments Federal, State and Local Governments The office of Federal State and Local Governments

Notice Number: NOT-OD Key Dates. Related Announcements. Issued by. FAQs for Costing of NIH-Funded Core Facilities. Purpose

FAQs for Costing of NIH-Funded Core Facilities Notice Number: NOT-OD-13-053 Key Dates Release Date: April 8, 2013 Related Announcements NOT-OD-10-138 Issued by National Institutes of Health (NIH) Purpose

FAQs for Costing of NIH-Funded Core Facilities Notice Number: NOT-OD-13-053 Key Dates Release Date: April 8, 2013 Related Announcements NOT-OD-10-138 Issued by National Institutes of Health (NIH) Purpose

2017 NMLS Money Services Businesses Industry Report

2017 NMLS Money Services Businesses Industry Report Released September 26, 2018 Conference of State Bank Supervisors 1129 20 th Street, NW, 9 th Floor Washington, D.C. 20036-4307 2017 NMLS Money Services

2017 NMLS Money Services Businesses Industry Report Released September 26, 2018 Conference of State Bank Supervisors 1129 20 th Street, NW, 9 th Floor Washington, D.C. 20036-4307 2017 NMLS Money Services

Campus Administrative Policy

Campus Administrative Policy Policy Title: Internal Service Centers and Core Laboratories Policy Number: 2001 Functional Area: Finance Effective: January 1, 2016 Date Last Amended/Reviewed: January 1,

Campus Administrative Policy Policy Title: Internal Service Centers and Core Laboratories Policy Number: 2001 Functional Area: Finance Effective: January 1, 2016 Date Last Amended/Reviewed: January 1,

Dependent Verif ication Form

Dependent Verif ication Form Financial Aid Services 2017-2018 PART I: STUDENT INFORMATION Name: Last First Middle SPIRE ID: Date of Birth: / / Phone Number: ( ) - Email Address: INSTRUCTIONS: 1. This form

Dependent Verif ication Form Financial Aid Services 2017-2018 PART I: STUDENT INFORMATION Name: Last First Middle SPIRE ID: Date of Birth: / / Phone Number: ( ) - Email Address: INSTRUCTIONS: 1. This form

Welcome! Understanding Facilities and Administration (F&A) Costs. Matt Michener

Costs. Matt Michener") Understanding Facilities and Administration (F&A) Costs Also known as Overhead Costs, or Indirect Costs. Revised April 2017 1 Welcome! Presenters: Matt Michener matthew.michener@wsu.edu Grant and Contract

Understanding Facilities and Administration (F&A) Costs Also known as Overhead Costs, or Indirect Costs. Revised April 2017 1 Welcome! Presenters: Matt Michener matthew.michener@wsu.edu Grant and Contract

HEALTH CARE WAIVERS 101 THURSDAY, JULY 28, :00 PM ET/ 3:00 PM CT/2:00 PM MT/ 1:00 PM PT

HEALTH CARE WAIVERS 101 THURSDAY, JULY 28, 2016 4:00 PM ET/ 3:00 PM CT/2:00 PM MT/ 1:00 PM PT Special Thanks This webinar is supported by the Health Resources and Services Administration (HRSA) of the

HEALTH CARE WAIVERS 101 THURSDAY, JULY 28, 2016 4:00 PM ET/ 3:00 PM CT/2:00 PM MT/ 1:00 PM PT Special Thanks This webinar is supported by the Health Resources and Services Administration (HRSA) of the

GENERAL INSTRUCTIONS COVER SHEET AND CERTIFICATION C-1

INDEX GENERAL INSTRUCTIONS (i) COVER SHEET AND CERTIFICATION C-1 Part I General Information I-1 Part II Direct Costs II-1 Part III Indirect Costs III-1 Part IV Depreciation and Use Allowances IV-1 Part

INDEX GENERAL INSTRUCTIONS (i) COVER SHEET AND CERTIFICATION C-1 Part I General Information I-1 Part II Direct Costs II-1 Part III Indirect Costs III-1 Part IV Depreciation and Use Allowances IV-1 Part

RECHARGE Frequently Asked Questions

RECHARGE Frequently Asked Questions This is a living document and is continually edited and updated. We welcome your feedback and contributions. General Information: Q: What is a 21 account? A: A 21 account,

RECHARGE Frequently Asked Questions This is a living document and is continually edited and updated. We welcome your feedback and contributions. General Information: Q: What is a 21 account? A: A 21 account,

Tax Recommendations and Actions in Other States. Joel Michael House Research Department June 9, 2011

Tax Recommendations and Actions in Other States Joel Michael House Research Department June 9, 2011 Governors FY 2012 Recommendations 12 governors recommend net revenue (tax and fee) increases 12 governors

Tax Recommendations and Actions in Other States Joel Michael House Research Department June 9, 2011 Governors FY 2012 Recommendations 12 governors recommend net revenue (tax and fee) increases 12 governors

Equity and Fixed Income

Equity and Fixed Income ALLIANCEBERNSTEIN TAX BULLETIN 2005 This booklet is a summary of useful tax information for various AllianceBernstein funds. It will assist you, as an investor, in the preparation

Equity and Fixed Income ALLIANCEBERNSTEIN TAX BULLETIN 2005 This booklet is a summary of useful tax information for various AllianceBernstein funds. It will assist you, as an investor, in the preparation

Chapter D State and Local Governments

Chapter D State and Local Governments State and Local Governments contains detailed information on the taxes, revenues, and expenditures of states and localities. The public finances of these two levels

Chapter D State and Local Governments State and Local Governments contains detailed information on the taxes, revenues, and expenditures of states and localities. The public finances of these two levels

Medical Benefits Claim Instructions

Medical Benefits Claim Instructions Any person who knowingly and with intent to injure, defraud or deceive any insurance company or other person files an application for insurance or statement of claim

Medical Benefits Claim Instructions Any person who knowingly and with intent to injure, defraud or deceive any insurance company or other person files an application for insurance or statement of claim

CRS Report for Congress

Order Code RS21071 Updated February 15, 2005 CRS Report for Congress Received through the CRS Web Medicaid Expenditures, FY2002 and FY2003 Summary Karen L. Tritz Analyst in Social Legislation Domestic

Order Code RS21071 Updated February 15, 2005 CRS Report for Congress Received through the CRS Web Medicaid Expenditures, FY2002 and FY2003 Summary Karen L. Tritz Analyst in Social Legislation Domestic

Instructions for Form 5330

Department of the Treasury Internal Revenue Service Instructions for Form 5330 (Revised May 1993) Return of Excise Taxes Related to Employee Benefit Plans Section references are to the Internal Revenue

Department of the Treasury Internal Revenue Service Instructions for Form 5330 (Revised May 1993) Return of Excise Taxes Related to Employee Benefit Plans Section references are to the Internal Revenue

Proposal Budgeting 101 Why budgets are more than just a bunch of numbers

Why budgets are more than just a bunch of numbers September 26, 2016 MORE THAN NUMBERS Topics to be covered include: Being responsive to budget requirements by sponsor Describing the use of AY salary vs

Why budgets are more than just a bunch of numbers September 26, 2016 MORE THAN NUMBERS Topics to be covered include: Being responsive to budget requirements by sponsor Describing the use of AY salary vs

HARVARD UNIVERSITY. Academic Service Center Procedures Manual

HARVARD UNIVERSITY Academic Service Center Procedures Manual Table of Contents Introduction 4 Definition of an Academic Service Center 4 Compliance-why we care 4 Purpose and Audience 4 School/tub Level

HARVARD UNIVERSITY Academic Service Center Procedures Manual Table of Contents Introduction 4 Definition of an Academic Service Center 4 Compliance-why we care 4 Purpose and Audience 4 School/tub Level

BEFORE WE GET STARTED

SOLUTIONS FOR TAX PROFESSIONALS AND BUSINESSES TAX CREDITS INCENTIVES COST RECOVERY BEFORE WE GET STARTED Welcome and thank you for joining KBKG s live webinar We will start the live webinar at 12pm PT

SOLUTIONS FOR TAX PROFESSIONALS AND BUSINESSES TAX CREDITS INCENTIVES COST RECOVERY BEFORE WE GET STARTED Welcome and thank you for joining KBKG s live webinar We will start the live webinar at 12pm PT

COST ACCOUNTING STANDARDS BOARD DISCLOSURE STATEMENT FOR EDUCATIONAL INSTITUTIONS CASB DS-2

FOR CASB DS-2 UNIVERSITY OF COLORADO AT BOULDER JUNE 30 1997 REVISION 1 DATED MARCH 31, 2008 Resubmission April 30, 2009 REQUIRED BY PUBLIC LAW 100-679 UNIVERSITY OF COLORADO AT BOULDER INDEX GENERAL INSTRUCTIONS

FOR CASB DS-2 UNIVERSITY OF COLORADO AT BOULDER JUNE 30 1997 REVISION 1 DATED MARCH 31, 2008 Resubmission April 30, 2009 REQUIRED BY PUBLIC LAW 100-679 UNIVERSITY OF COLORADO AT BOULDER INDEX GENERAL INSTRUCTIONS

TABLE OF CONTENTS - CHAPTER 13

TABLE OF CONTENTS - CHAPTER 13 I. CHAPTER 13... 2 II. EXTERNAL REGULATIONS... 2 III. APPLICABILITY... 2 IV. KEY FEATURES OF... 3 V. ACCOUNTING, BUDGETING, AND COSTING... 4 A. Accounting... 4 B. Budgeting...

TABLE OF CONTENTS - CHAPTER 13 I. CHAPTER 13... 2 II. EXTERNAL REGULATIONS... 2 III. APPLICABILITY... 2 IV. KEY FEATURES OF... 3 V. ACCOUNTING, BUDGETING, AND COSTING... 4 A. Accounting... 4 B. Budgeting...

WikiLeaks Document Release

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS21071 Medicaid Expenditures, FY2003 and FY2004 Karen Tritz, Domestic Social Policy Division January 17, 2006 Abstract.

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS21071 Medicaid Expenditures, FY2003 and FY2004 Karen Tritz, Domestic Social Policy Division January 17, 2006 Abstract.

Payroll for Small Businesses: How Legislative Changes Will Affect Your Business in 2011

Payroll for Small Businesses: How Legislative Changes Will Affect Your Business in 2011 Nadine Hughes, CPP VP Tax Services CompuPay Inc. EFTPS Many small employers will have to start using EFTPS for payroll

Payroll for Small Businesses: How Legislative Changes Will Affect Your Business in 2011 Nadine Hughes, CPP VP Tax Services CompuPay Inc. EFTPS Many small employers will have to start using EFTPS for payroll

Preparation for a Successful Payroll Year end. Presented by: Jean Domaingue, CPP

Preparation for a Successful Payroll Year end Presented by: Jean Domaingue, CPP November 15, 2012 CompuPay is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor

Preparation for a Successful Payroll Year end Presented by: Jean Domaingue, CPP November 15, 2012 CompuPay is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor

What Every Transportation Manager Should Know About GARVEEs

May 2007 What Every Transportation Manager Should Know About GARVEEs Frederick J. Werner Federal Highway Administration Resource Center Frederick.werner@fhwa.dot.gov 0 Outline Background on Debt and Infrastructure

May 2007 What Every Transportation Manager Should Know About GARVEEs Frederick J. Werner Federal Highway Administration Resource Center Frederick.werner@fhwa.dot.gov 0 Outline Background on Debt and Infrastructure

Federal Registry. NMLS Federal Registry Quarterly Report Quarter I

Federal Registry NMLS Federal Registry Quarterly Report 2012 Quarter I Updated June 6, 2012 Conference of State Bank Supervisors 1129 20 th Street, NW, 9 th Floor Washington, D.C. 20036-4307 NMLS Federal

Federal Registry NMLS Federal Registry Quarterly Report 2012 Quarter I Updated June 6, 2012 Conference of State Bank Supervisors 1129 20 th Street, NW, 9 th Floor Washington, D.C. 20036-4307 NMLS Federal

Eaton Vance Open-End Funds

Eaton Vance Eaton Vance Open-End Funds 2016 Additional Tax Information Our Investment Affiliates Eaton Vance Management Contents Income by State 2 Tax-Exempt Income and AMT by Fund 9 Dividends-Received

Eaton Vance Eaton Vance Open-End Funds 2016 Additional Tax Information Our Investment Affiliates Eaton Vance Management Contents Income by State 2 Tax-Exempt Income and AMT by Fund 9 Dividends-Received

Dependent Veri ication Form

Financial Aid Services 20182019 Dependent Veriication Form PART I: Student Information Name: Last First Middle SPIRE ID: Date of Birth: / / Email Address: Phone Number: ( ) PART II: Your Parents Household

Financial Aid Services 20182019 Dependent Veriication Form PART I: Student Information Name: Last First Middle SPIRE ID: Date of Birth: / / Email Address: Phone Number: ( ) PART II: Your Parents Household

NAUPA Holder Workshop Legislative Trends and Highlights

2012-2013 NAUPA Holder Workshop Legislative Trends and Highlights May 17, 2013 Cherish Simmons Vice President Audits, Xerox The Foremost Authority on Unclaimed Property Unclaimed Property Legislative Update

2012-2013 NAUPA Holder Workshop Legislative Trends and Highlights May 17, 2013 Cherish Simmons Vice President Audits, Xerox The Foremost Authority on Unclaimed Property Unclaimed Property Legislative Update

Do you charge an expedite fee for online filings?

Topic: Expedite Fees and Online Filings Question by: Allison A. DeSantis : Ohio Date: March 14, 2012 Manitoba Corporations Canada Alabama Alaska Arizona Yes. The expedite fee is $35. We currently offer

Topic: Expedite Fees and Online Filings Question by: Allison A. DeSantis : Ohio Date: March 14, 2012 Manitoba Corporations Canada Alabama Alaska Arizona Yes. The expedite fee is $35. We currently offer

Required Training Completion Date. Asset Protection Reciprocity

Completion Alabama Alaska Arizona Arkansas California State Certification: must complete initial 16 hours (8 hrs of general LTC CE and 8 hrs of classroom-only CE specifically on the CA for LTC prior to

Completion Alabama Alaska Arizona Arkansas California State Certification: must complete initial 16 hours (8 hrs of general LTC CE and 8 hrs of classroom-only CE specifically on the CA for LTC prior to

Information for Non-Tax Filers

NONFIL 2018-2019 Information for Non-Tax Filers Dear Student, If you (and your parent, if dependent) worked in 2016 but did not file a tax return with the IRS, please bring your (and your parent, if dependent)

NONFIL 2018-2019 Information for Non-Tax Filers Dear Student, If you (and your parent, if dependent) worked in 2016 but did not file a tax return with the IRS, please bring your (and your parent, if dependent)

Proposal Budgeting 101 Why budgets are more than just a bunch of numbers

Why budgets are more than just a bunch of numbers October 18, 2018 MORE THAN NUMBERS Topics to be covered include: Being responsive to budget requirements by sponsor Describing the use of AY salary vs

Why budgets are more than just a bunch of numbers October 18, 2018 MORE THAN NUMBERS Topics to be covered include: Being responsive to budget requirements by sponsor Describing the use of AY salary vs

Example 1. Individual with a Nine-Month Appointment

Example 1. Individual with a Nine-Month Appointment Dr. Minion is on a nine-month faculty appointment in the Department of Biology. He is submitting a NIH R01 grant proposal with 1.2 person months effort.

Example 1. Individual with a Nine-Month Appointment Dr. Minion is on a nine-month faculty appointment in the Department of Biology. He is submitting a NIH R01 grant proposal with 1.2 person months effort.

# of Credit Unions As of March 31, 2011

# of Credit Unions # of Credit Unins # of Credit Unions As of March 31, 2011 8,600 8,400 8,200 8,000 8,478 8,215 7,800 7,909 7,600 7,400 7,651 7,442 7,200 7,000 6,800 # of Credit Unions -Trend By Asset-Based

# of Credit Unions # of Credit Unins # of Credit Unions As of March 31, 2011 8,600 8,400 8,200 8,000 8,478 8,215 7,800 7,909 7,600 7,400 7,651 7,442 7,200 7,000 6,800 # of Credit Unions -Trend By Asset-Based

DFA INVESTMENT DIMENSIONS GROUP INC. DIMENSIONAL INVESTMENT GROUP INC. Institutional Class Shares January 2018

DFA INVESTMENT DIMENSIONS GROUP INC. DIMENSIONAL INVESTMENT GROUP INC. Institutional Class Shares January 2018 Supplementary Tax Information 2017 The following supplementary information may be useful in

DFA INVESTMENT DIMENSIONS GROUP INC. DIMENSIONAL INVESTMENT GROUP INC. Institutional Class Shares January 2018 Supplementary Tax Information 2017 The following supplementary information may be useful in

Proposal Budgeting 101 Why budgets are more than just a bunch of numbers

Why budgets are more than just a bunch of numbers October 12, 2017 MORE THAN NUMBERS Topics to be covered include: Being responsive to budget requirements by sponsor Describing the use of AY salary vs

Why budgets are more than just a bunch of numbers October 12, 2017 MORE THAN NUMBERS Topics to be covered include: Being responsive to budget requirements by sponsor Describing the use of AY salary vs

THE ANSWER TO 1099 TAX INFORMATION REPORTING

1099 REPORTING THE ANSWER TO 1099 TAX INFORMATION REPORTING Researching IRS and state regulations, updating applications, year-end processing, printing, stuffing and mailing forms to recipients, filing

1099 REPORTING THE ANSWER TO 1099 TAX INFORMATION REPORTING Researching IRS and state regulations, updating applications, year-end processing, printing, stuffing and mailing forms to recipients, filing

2014 U.S. Census (2015) Median African-American Household Income Rank, Memphis Included. Household Median Income Ranking, African American Population

Median African-American Household Income Rank, Memphis Included. Household Median Income Ranking, African American Population") 2015 2015 Rankings Report Prepared by Elena Delavega, PhD, MSW Department of Social Work Benjamin L. Hooks Institute for Social Change University of Memphis 2014 U.S. Census (2015) - Rank, Memphis Included

2015 2015 Rankings Report Prepared by Elena Delavega, PhD, MSW Department of Social Work Benjamin L. Hooks Institute for Social Change University of Memphis 2014 U.S. Census (2015) - Rank, Memphis Included

STANDARD MANUALS EXEMPTIONS

STANDARD MANUALS EXEMPTIONS The manual exemptions permits a security to be distributed in a particular state without being registered if the company issuing the security has a listing for that security

STANDARD MANUALS EXEMPTIONS The manual exemptions permits a security to be distributed in a particular state without being registered if the company issuing the security has a listing for that security

Salary & Wages Fringe Benefits Equipment Travel Participant Support. BUDGET CATEGORIES (click on image to go to page)

") Salary & Wages Fringe Benefits Equipment Travel Participant Support BUDGET CATEGORIES (click on image to go to page) Salaries & Wages (Direct Cost) 1 of 2 Faculty and Key Personnel Salaries and wages should

Salary & Wages Fringe Benefits Equipment Travel Participant Support BUDGET CATEGORIES (click on image to go to page) Salaries & Wages (Direct Cost) 1 of 2 Faculty and Key Personnel Salaries and wages should

Trade Association and Coalition Participation

Millions of times a day, we re helping people on their path to better health from advising on prescriptions to helping manage chronic and specialty conditions. Because we re present in so many moments,

Millions of times a day, we re helping people on their path to better health from advising on prescriptions to helping manage chronic and specialty conditions. Because we re present in so many moments,

10 yrs. The benefit is capped at 80% of FAS. An elected official may. 2% (first 10 yrs.); or 2.25% (second 10 yrs.); or 2.5% over 20 yrs.

; or 2.25% (second 10 yrs.); or 2.5% over 20 yrs.") Table 3.13 STATE LEGISLATIVE RETIREMENT BENEFITS Alabama... Alaska... Age 60 with 10 yrs. Employee 6.75% 2% (first 10 yrs.); or 2.25% (second 10 yrs.); or 2.5% over 20 yrs. x average salary over 5 highest

Table 3.13 STATE LEGISLATIVE RETIREMENT BENEFITS Alabama... Alaska... Age 60 with 10 yrs. Employee 6.75% 2% (first 10 yrs.); or 2.25% (second 10 yrs.); or 2.5% over 20 yrs. x average salary over 5 highest

Susan J. Merritt, Senior Vice President Senior Fiduciary Officer, Northern Trust, Newport Beach, Calif.

Presenting a live 90-minute webinar with interactive Q&A Structuring Trust Protector Provisions: Powers & Duties, Trustee Oversight, Tax and Fiduciary Risks Avoiding Unintentional Fiduciary Classification,

Presenting a live 90-minute webinar with interactive Q&A Structuring Trust Protector Provisions: Powers & Duties, Trustee Oversight, Tax and Fiduciary Risks Avoiding Unintentional Fiduciary Classification,

Federal Rates and Limits

Federal s and Limits FICA Social Security (OASDI) Base $118,500 Medicare (HI) Base No Limit Social Security (OASDI) Percentage 6.20% Medicare (HI) Percentage Maximum Employee Social Security (OASDI) Withholding

Federal s and Limits FICA Social Security (OASDI) Base $118,500 Medicare (HI) Base No Limit Social Security (OASDI) Percentage 6.20% Medicare (HI) Percentage Maximum Employee Social Security (OASDI) Withholding

Important 2008 Tax Information Regarding Your Mutual Funds

Important 2008 Tax Information Regarding Your Mutual Funds Managed by WESTERN ASSET CLEARBRIDGE ADVISORS LEGG MASON CAPITAL MANAGEMENT BRANDYWINE GLOBAL BATTERYMARCH This Booklet is a summary of useful

Important 2008 Tax Information Regarding Your Mutual Funds Managed by WESTERN ASSET CLEARBRIDGE ADVISORS LEGG MASON CAPITAL MANAGEMENT BRANDYWINE GLOBAL BATTERYMARCH This Booklet is a summary of useful